Adaptive Multilevel Stochastic Approximation of the Value-at-Risk

Abstract

[13] (\citeyearCFL23) introduced a multilevel stochastic approximation scheme to compute the value-at-risk of a financial loss that is only simulatable by Monte Carlo. The optimal complexity of the scheme is in , being a prescribed accuracy, which is suboptimal when compared to the canonical multilevel Monte Carlo performance. This suboptimality stems from the discontinuity of the Heaviside function involved in the biased stochastic gradient that is recursively evaluated to derive the value-at-risk. To mitigate this issue, this paper proposes and analyzes a multilevel stochastic approximation algorithm that adaptively selects the number of inner samples at each level, and proves that its optimal complexity is in . Our theoretical analysis is exemplified through numerical experiments.

Keywords. stochastic approximation, value-at-risk, nested Monte Carlo, multilevel Monte Carlo, adaptive Monte Carlo.

MSC. 65C05, 62L20, 62G32, 91Gxx.

Introduction

The value-at-risk (VaR) is the predominant regulatory risk metric in finance [6]. It stands for the quantile, at some confidence level, of the loss on a portfolio. The probability that a loss exceeds the VaR expresses the chances of occurrence of large portfolio losses. Evaluating a portfolio’s VaR is thus paramount to assess its risk. However, a large class of financial portfolios can only be valued by Monte Carlo. This introduces a bias in the loss estimation, thereby increasing the complexity of VaR calculation. Determining a portfolio’s future VaR is thus regarded as a challenging task.

Following the celebrated works on VaR convexification [32, 8, 4], a nascent line of research has adopted a stochastic approximation (SA) viewpoint to estimate the VaR [4, 2, 3, 12, 9].

Recent developments [5, 13, 14] have focused on the nested nature of the problem.

Notably, [5] proposes a nested SA (NSA) method that couples an outer SA scheme with an inner nested Monte Carlo scheme to compute the VaR. It is shown in [13] that such a scheme runs optimally in time, being a prescribed accuracy.

Meanwhile, subsequently to the wide success of multilevel Monte Carlo (MLMC) methods [29, 30, 23, 15, 11], multilevel stochastic approximation (MLSA) algorithms [20, 16] have emerged as a means to accelerate biased SA schemes such as NSA.

While the latter injects biased nested simulations directly into an iterative SA scheme, MLSA telescopes a sequence of correlated estimate pairs of lower and lower biases, reducing the complexity by an order of magnitude.

[13] leverages this multilevel acceleration [20] to reduce the complexity of the VaR NSA scheme of [5] to , being a small number governed by the integrability degree of the loss.

They also identify a parametrization for their MLSA algorithm that achieves a complexity for the estimation of the expected shortfall (ES), a risk measure closely linked to the VaR, in .

[14] further obtains central limit theorems for VaR and ES NSA and MLSA schemes, as well as their Polyak-Ruppert versions that enjoy stronger numerical stability properties.

Albeit significant, the performance gain achieved by MLSA over NSA in estimating the VaR [13] is to be nuanced. The canonical optimal complexity for multilevel techniques is of order [23, 20]. The suboptimality of the VaR MLSA scheme arises from its inner recursions relying on the evaluation of a discontinuous gradient that is similar to a Heaviside (). When a biased simulation of the loss falls on the opposite side of the discontinuity relative to the exact target loss, the multilevel recursion incurs an update error. The accumulation of these errors propagates to the final estimator, leading to the suboptimality.

Motivated by valuing a digital option with Heaviside payoff in a local volatility model, [22] surveys multiple approaches to the above discontinuity issue in a multilevel Monte Carlo (MLMC) context. Most techniques described therein emanate from the derivative sensitivity computation literature and their common goal is to lower the variance of the paired estimators at each level of the multilevel simulation. We retain three ideas that may apply to our nested SA setting. Firstly, a natural idea is to smoothen the Heaviside payoff, but this only attains a complexity in due to a large smoothing Lipschitz constant. Secondly, Malliavin calculus could be used in conjunction with a cubic spline interpolation, which however propagates regression noises to the final estimator. Finally, levelwise adaptive refinement of inner Monte Carlo samplings seems to be a versatile technique that achieves the desired performance gain. It advocates to dynamically refine the biased simulations in order to deal with the discontinuity issue [24, 28, 25]. We quickly overview this technique below.

An early example of adaptive nested Monte Carlo simulation can be traced back to [10], who endeavor to accelerate the nested Monte Carlo root-finding algorithm of [27] for approximating the VaR. The latter algorithm combines an outer bisection method with an inner Monte Carlo sampling of the probability that the loss exceed the VaR, and involves the evaluation of a Heaviside centered at the VaR itself. Such a method proves however to be computationally more demanding than the aforementioned SA approaches. The adaptive strategy of [10] involves refining simulations for risk scenarios that are too close to the VaR, thereby reducing their probability of falling on the wrong side of the VaR threshold. Evaluating the Heaviside function at the biased loss becomes almost equivalent to evaluating it at the true loss. [24] revisits the same concept as [10], extending their method to the nested MLMC paradigm by adapting the number of inner simulations at each level. [28] generalizes this methodology to a broader class of MLMC problems.

[17] has led to similar adaptive ideas in a partial differential equation Monte Carlo approximation setting, where the Monte Carlo estimation error is assumed to be almost surely bounded.

Note that the terminology “adaptive MLMC” has also been employed in different meanings, for adaptive path simulation [31] and importance sampling [7].

In this article, we develop an adaptive refinement strategy to efficiently estimate the VaR using the MLSA algorithm derived in [13]. As in MLMC, our adaptive strategy prioritizes aligning the innovations with their target samplings relative to the discontinuities of the update functions at the SA iterates. However, the strategy that was developed for Monte Carlo in [24, 28] does not directly apply to our SA setting, since refining the innovations that drive an SA scheme shifts their distributions relatively to the SA iterates, which themselves evolve from one recursion to the next. On the one hand, this increases the risk of steering the iterates away from the target VaR. On the other hand, it affects the original SA problem formulation, rendering it possibly non-convex and possessing multiple stationary points. To address this issue, we carefully incorporate a saturation factor, varying throughout the iterations, to prevent the potential deviation of the iterates from the target VaR.

We apply our strategy to both NSA and MLSA paradigms and provide sharp -controls.

For a prescribed accuracy , their optimal complexities are shown to be and respectively, resulting in an order of magnitude speed-up on their non-adaptive counterparts, up to a logarithmic factor.

The adaptive MLSA algorithm largely attains a comparable complexity order to the standard unbiased Robbins-Monro algorithm, thus demonstrating the narrowing of the performance gap between nested MLSA schemes and Robbins-Monro schemes in the context of Heaviside-type update functions.

Our numerical analyses, conducted on a toy model as well as a more concrete financial setup, strongly support our theoretical findings.

The paper is structured as follows. Section 1 recalls the problem and main results in [13] regarding the estimation of the VaR using MLSA. Section 2 develops an adaptive refinement strategy to enhance the efficiency of the Monte Carlo sampling that is nested within the MLSA approach. Sections 3 and 4 exploit this strategy to reduce the complexities of NSA and MLSA and provide subsequent -controls and complexity rates. Section 5 presents numerical studies to demonstrate the performance improvement resulting from the adaptive strategy.

1 Stochastic Approximation Approach

This section recalls the setting and main results in [13] on the stochastic approximation of the VaR. They will serve as a baseline for the adaptive strategy that we develop in Section 2.

1.1 Unbiased Stochastic Approximation Algorithm

Let be a probability space accommodating all of the subsequent random variables. Let be an -valued random loss of a portfolio, defined at some time horizon . Following [1, 19], the VaR of at some confidence level , denoted , is defined as

| (1.1) |

As stated in [32, 8, 4], if the cdf of is continuous, then is the left-end solution to

| (1.2) |

Moreover, is convex and continuously differentiable on , with , , where

| (1.3) |

If is additionally increasing, then is strictly convex and is the unique minimizer of :

| (1.4) |

Besides, if admits a continuous pdf , then is twice continuously differentiable on , with , .

When iid samples of are available, [4] proposes to estimate using the unbiased SA scheme of dynamics

| (SA) |

where , is a real-valued random initialization independent of the innovations , and is a positive non-increasing sequence such that and .

We are interested in the setting where writes as a conditional expectation:

| (1.5) |

Here, and are two independent random variables taking values in and respectively, and is a measurable function such that . From a financial standpoint, typically models the dynamics of the portfolio’s risk factors up to the time horizon of the loss, their dynamics beyond and the subsequent future cash flows. Generally, the risk factors and can be sampled from a model and the cash flow structure is known.

In the case that cannot be sampled exactly, one must leverage its nested formulation to produce suitable simulations for the SA approach.

1.2 Nested Stochastic Approximation Algorithm

Let . A natural idea is to approximate by the nested Monte Carlo estimator

| (1.6) |

and and are independent. is termed the bias parameter since it helps control the VaR estimation bias as we clarify next. We swap by , , in the original problem (1.2) and obtain the approximate problem

| (1.7) |

Again, assuming that , if the cdf of is continuous, then is convex and continuously differentiable on , with , , recalling the definition (1.3). If is additionally increasing, then is strictly convex and

| (1.8) |

is well defined and constitutes a biased estimator of . Finally, If admits a continuous pdf , then is twice continuously differentiable on , with , .

Assuming continuous and increasing, can be estimated with a bias using the NSA scheme of dynamics

| (NSA) |

where , is a real-valued random initialization independent of the innovations and is a positive non-increasing sequence such that and .

Convergence Analysis.

Let . The global error of (NSA) writes as a sum of a statistical and a bias errors:

| (1.9) |

Assumption 1.1 ([13, Assumptions 2.2 & 2.5]).

-

(i)

For any , admits the first order Taylor expansion

for some functions satisfying, for any ,

-

(ii)

For any , the law of admits a continuous pdf with respect to the Lebesgue measure. Moreover, the pdfs converge locally uniformly to .

-

(iii)

For any ,

-

(iv)

The pdfs are uniformly bounded and uniformly Lipschitz, namely,

where denotes the Lipschitz constant of , .

Remark 1.1 ([14, Remark 1.1]).

Lemma 1.2 ([13, Proposition 2.4 & Theorem 2.7(i)]).

Complexity Analysis.

The controls of Lemma 1.2 on the bias and statistical errors in (1.9) result in the following complexities.

Proposition 1.3 ([13, Theorem 2.8]).

Let be a prescribed accuracy. Within the framework of Lemma 1.2(ii), setting

yields a global error for (NSA) of order as . The corresponding computational cost satisfies

for some positive constant independent of . The minimal computational cost satisfies

and is attained for , i.e. for under the constraint .

1.3 Multilevel Stochastic Approximation Algorithm

With a complexity ceiling for nested VaR estimation at as achieved by (NSA), a multilevel approach is proposed in [13] to accelerate the latter scheme. We recall below the MLSA scheme and the associated -control and complexity.

Take , an integer and a number of levels, and let

| (1.12) |

To each bias parameter , , corresponds an approximate problem to (1.2) of unique solution . These solutions can be telescoped into

| (1.13) |

By denoting a sequence of iterations amounts, the multilevel SA scheme [13, 20] consists in approximating with

| (MLSA) |

where each level is simulated independently. More precisely, once is simulated using iterations of (NSA) with bias , at each level , for , is obtained by iterating

| (1.14) |

where and and are real-valued random initializations independent of the innovations . Crucially, at each level , and are perfectly correlated, in the sense that

| (1.15) |

where are independent of .

At each level , and are referred to as the fine and coarse approximations. is referred to as the initial (or level ) approximation. We can infer from (1.14) that (MLSA) correlates multiple (NSA) pairs, each pair being set with consecutive bias parameters on the geometric scale . The produced effect is an incremental bias correction of the level approximation of bias . Conversely, (NSA) can be viewed as an (MLSA) instance with (higher) levels.

Convergence Analysis.

The following lemma delimits three frameworks under which we later derive -controls and complexities for (MLSA).

Lemma 1.4 ([13, Proposition 3.2]).

-

(i)

Assume that the real-valued random variables admit pdfs that are bounded uniformly in .

-

a.

If

(1.16) then, for any such that and any ,

where , with a positive constant that depends only upon .

-

b.

Assume that there exists a non-negative constant such that, for all ,

(1.17) Then, for any such that and any ,

-

a.

-

(ii)

Let , define , , , and consider the sequence of random variables given by , where

Assume that satisfies

(1.18) Then,

Remark 1.2 ([13, Remark 3.3]).

Lemma 1.4’s frameworks are ordered by strength. The Gaussian concentration framework (1.17) holds if is bounded for some [21, 18]. It entails (1.16) for any via an exponential series expansion. The framework (1.18) relaxes [27, Assumption 1] and is computationally optimal (c.f. Proposition 1.7(iii)). It holds for instance if is uniformly Lipschitz in and .

Assumption 1.5 ([13, Assumption 3.4]).

There exist positive constants such that, for any and any compact set ,

Remark 1.3 ([13, Remark 3.5]).

Complexity Analysis.

The global error of (MLSA) can be decomposed into a statistical and a bias errors:

| (1.21) |

Proposition 1.7 ([13, Proposition 3.7, Lemma 3.8 & Theorem 3.9]).

- (i)

- (ii)

- (iii)

Remark 1.4.

2 Adaptive Refinement Strategy

The suboptimality of (MLSA) is linked to the discontinuity of the gradient (1.3) intervening in the VaR recursion (1.14). Indeed, for , if the simulated loss

is too close to the estimate but falls on the opposite side of the discontinuity of with respect to its sampling target

| (2.1) |

an error is registered, lowering the overall performance of the multilevel algorithm.

To address this issue, we investigate the incorporation an adaptive refinement layer into (MLSA).

The following steps elucidate the intuition underlying the development of our adaptive refinement strategy. For simplicity, we consider a nested simulation , targeting an unbiased simulation , that we want to adaptively refine given a current iterate at the recursion rank . Assuming that and were used to simulate according to (1.6), refining the latter to consists in simulating additional independently from and and setting

| (2.2) |

A confidence based heuristic strategy.

We loosely adapt the reasonings employed in [24, Section 2.3.1] and [28, Section 3] to derive a preliminary strategy. Roughly speaking, considering a refinement amount and an iterate , we want to ensure that with high probability by aligning with on the same side of the discontinuity of at .

Using a conditional CLT,

To achieve the desired alignment, we consider a critical value corresponding to a confidence level and choose minimal such that with confidence , which can be expressed as

| (2.3) |

up to a modification of conditionally on . However, this approach is impractical as is inaccessible.

We thus switch perspective and require instead that with confidence , to ensure that and are on the same side relative to . We then select minimal such that

| (2.4) |

allowing for a modification of conditional on .

In effect, we augment the number of inner simulations of by refinements until the threshold around is crossed.

[24] views this process as estimating by in the original strategy (2.3). [25] interprets the evaluation of the criterion (2.4) as performing a Student t-test on the null hypothesis “”.

For more flexibility, we introduce two parameters and that respectively control the strictness and budgeting of the refinement strategy.

Refinement strictness.

We set and redefine the refinement strategy as choosing minimal such that

| (2.5) |

The parameter allows to adjust the tendency of the strategy to refine. Larger values impose more strictness. Setting retrieves the previous baseline strategy.

Refinement budgeting.

The strategy outlined above may be risky, as the refinement amount required to satisfy (2.5) could be excessively large, hence increasing the associated complexity. To address this, we impose an upper limit on at :

| (2.6) |

Note importantly the dependency of on . For the strategy to be computationally efficient, the entailed number of inner simulations should, on average, be comparable to the number of inner simulations absent the strategy. To ensure this, we relax the constant to a normalization factor that is calibrated such that . We have

From (2.6) and Assumption 1.1(iv),

Extending the definition of to with for , we obtain

for some positive constant . To balance the terms on the right-hand side, we normalize with , yielding the refinement strategy

This approach is essentially the same as that in [28]. The amount of inner simulations is increased until the varying threshold around is crossed.

Refinement saturation.

To illustrate the strategy so far, we test it along a single dynamic (NSA) of bias :

Unlike the Monte Carlo setting [28] where the iterate remains constant across the recursions, the iterates above change from one step to the next. This causes the innovations to refine to , de facto solving the root finding program , or equivalently, . Since evolves with , is no longer given by a cdf as it may not be monotone and could have several roots.

To address this issue, we saturate the refinement amount for large recursion ranks (corresponding to terminal SA phases) to the maximum allowed , allowing to veer into the convex program for large. This is achieved by incorporating an increasing dependency upon into the strategy’s threshold.

We refer to the definitive strategy described below and additional comments in Remark 3.1.

The following lemma revisits the framework (1.18) to grant a flexible basis for our adaptive refinement strategy.

Lemma 2.1.

Let . Define and the function , . Assume that the sequence of random variables , defined by , where

satisfies

| (2.7) |

Then

Remark 2.1.

The framework (1.18) can be viewed as a special case of (2.7) for consecutive bias pairs on the geometric scale . In (MLSA), the fine and coarse approximations at each level are controlled by consecutive bias parameters in . If one is to refine either approximation separately, the refined fine and coarse approximations are no longer controlled by consecutive bias parameters in , hence the need for the generalized framework above.

Following the roadmap of [24, 28, 25], we define

| (2.8) |

with the convention , where , , ,

| (2.9) |

and

| (2.10) |

Note the property , for some positive constant .

The constant is referred to as the confidence constant [24, 28], the refinement strictness parameter [28, 25], the budgeting parameter, the -dependent factor in (2.9) the saturation factor, and the quantity , that our adaptive strategy seeks greedily to make large enough, the error margin [10].

We refer to [28, Algorithm 3.1] for an analogous refinement strategy in a MLMC setting, that is independent of the recursion rank .

Remark 2.2.

-

(i)

At each level and recursion rank , the adaptive strategy refines the simulation used in (1.14) to , with the aim of escaping the region around the discontinuity of at .

-

(ii)

No refinement is applied at the level , as for all .

-

(iii)

The threshold depends on the hyperparameters and . The parameter controls the refinement strictness and its budgeting on the allowed refinement amount. The threshold decreases for and large. It also depends on the level and the recursion rank . Larger values lead to smaller thresholds while larger values lead to larger thresholds.

-

(iv)

Recalling the definition (2.1), by virtue of the almost sure convergence of to as (by the conditional law of large numbers, under suitable assumptions), the refined simulation is in theory closer to the actual simulation target than . It is therefore expected that with high probability.

-

(v)

In our derivation of the adaptive refinement strategy, the confidence constant took in fact the form of , where is a critical value of the law at some confidence level and is the sampling standard deviation. For a -confidence level, a natural choice for is three standard deviations, i.e. . The standard deviation can be estimated empirically. However, the ensuing convergence and complexity analyses show that our choice of constant for the adaptive strategy (2.8) accomplishes the desired performance gain. In practice, should be fine-tuned to avoid over- or under-adapting.

3 Adaptive Nested Stochastic Approximation Algorithm

Before delving into the adaptive refinement of (MLSA), let us first investigate the influence of our refinement strategy on (NSA), which we recall can be considered an instance of level (MLSA).

Consider a bias parameter , , on the geometric scale , which allows resorting to single-echelon refinements (2.2). The adaptively refined nested SA algorithm for estimating the VaR writes

| (adNSA) |

where

| (3.1) |

and is a random real-valued initialization that is independent of the innovations .

Remark 3.1.

Unlike [24, 28, 25], the adaptive refinement (2.8) depends on the recursion rank . As previously discussed, using an adaptive refinement independent of can be viewed as seeking a root of , which is not guaranteed to retrieve a problem like (1.7), as it could have multiple roots. The introduced dependency upon saturates the refinement amount to for large , aligning with with high probability and practically solving the strictly convex nested SA problem of bias parameter .

This behavior can be verified by calculation. Assuming that , by Markov’s inequality,

Since is a discrete random variable taking values in , there exists such that, for , . Thus the desired saturation effect for large.

Of course, the iterate depends on the recursion rank . The boundedness of the iterates in some space, , is hence essential to retrieve the asymptotic behavior described above. Such boundedness is established in Proposition 3.2.

3.1 Convergence Analysis

In the following, designates a positive constant that may change from line to line but does not depend on or . The proofs of the ensuing results are postponed to Appendix B.

Lemma 3.1.

Let , .

- (i)

- (ii)

Remark 3.2.

Recalling the definition of in (1.10), the next lemma provides an adaptive counterpart to Lemma 1.2(ii).

Proposition 3.2.

3.2 Complexity Analysis

Proposition 3.2(i) provides insight into the behavior of (adNSA). Fixing and running (adNSA) times results in a global error

where the first term represents the statistical error and the second the bias error.

Proposition 3.3.

Proof.

Remark 3.4.

According to the decomposition (1.9), if using (NSA) with a bias on the geometric scale , one must set

to achieve a bias error of order . (adNSA) requires by comparison a smaller , which in turn translates into a less expensive, albeit biased, simulation that is subsequently refined. This adjustment contributes to a reduction in the complexity of (adNSA).

The next lemma quantifies the average simulation amounts performed per iteration under the adaptive strategy.

Remark 3.5.

Note the analogous [28, Proposition 3.1] for adaptive Monte Carlo, independent nonetheless of the recursion rank . The average amount of inner simulations therein is in the order of . The saturation of our adaptive strategy for large is responsible for expanding these amounts by a small order depending on . We refer to Remark 3.1 for further comments on this dependence on .

Proposition 3.5.

Proof.

Remark 3.6.

The (adNSA) framework (3.2) scores a speed-up on (NSA) when . By comparison to Proposition 1.3, the complexities outlined above are an order of magnitude of lower than those of (NSA) for large under the framework (3.2) and up to a logarithmic factor under the frameworks (3.3) and (3.4). As we will see in the next section, (adNSA) serves as a fundamental component of the adaptive MLSA scheme. Consequently, the performance improvements noted on the former scheme should result in an acceleration of the latter.

4 Adaptive Multilevel Stochastic Approximation Algorithm

Recalling that (MLSA) telescopes multiple paired (NSA) schemes, the previous development on (adNSA) provides a framework for the extension of the adaptive refinement strategy to the multilevel paradigm. We define the adaptive multilevel SA (adMLSA) estimator for the VaR as

| (adMLSA) |

where represents the number of iterations at each level. Each level is simulated independently. As detailed in Remark 2.2(ii), the level estimator is not refined, resulting in iterations of (NSA). Each of the remaining levels is obtained as follows: after initializing , for each , once the components of have been simulated according to (1.15), and are separately refined as in (3.1), relative to the fine and coarse iterates and , into and respectively. These refined innovations are then injected into separate single updates of (adNSA) to obtain the next iterates .

4.1 Convergence Analysis

Below, designates a positive constant that may change from line to line but does not depend on . The proofs of the following results are postponed to Appendix B.

The next result guarantees stronger error controls for (adMLSA) comparatively with its non-adaptive counterpart, Lemma 1.4, for (MLSA).

Lemma 4.1.

Remark 4.1.

The main convergence result follows. Its proof is deferred to Appendix C.

Theorem 4.2.

Remark 4.2.

Similarly to Theorem 1.6, the upper estimate for the statistical error of (adMLSA) contains four terms: the first term governs the level simulation and the remaining three control the drifts and martingales arising in the multilevel linearization (C.7). The first difference with (MLSA) lies in the inclusion of , which stems from the controls of Proposition 3.2. Additionally, the final term exhibits an extra exponentiation in , resulting in an accelerated convergence rate compared to (MLSA).

The convergence rate speed-up, shown in the previous theorem, translates a significant performance gain that should reflect in the complexity of (adMLSA), as we clarify next.

4.2 Complexity Analysis

Throughout, denotes a positive constant that may change from line to line but remains independent of . We consider a prescribed accuracy for (adMLSA).

Approximating by results in a global error that decomposes into a statistical and a bias errors:

| (4.6) |

Proposition 4.3.

Remark 4.3.

In view of Propositions 4.3 and 1.7(i), to achieve an identical bias error order, (adMLSA) requires significantly less levels than (MLSA). In fact, for , (adMLSA) requires half as many levels as (MLSA) to achieve a bias error of order . This property alone makes (adMLSA) much faster than (MLSA). It is linked to the fact that, for a given number of levels , (adMLSA) achieves a bias error of order , an order of magnitude lower than (MLSA) that scores an order of .

Proposition 4.4.

Proof.

The average complexity of the adaptive multilevel SA algorithm satisfies

Invoking Lemma 3.4 concludes the proof. ∎

Remark 4.4.

Without the saturation factor in the refinement strategy, the computational cost would be lowered to , similar to both (MLSA) and the adaptive MLMC algorithm [28]. However, omitting the saturation factor would adversely affect the convergence of the statistical error (4.4). See Remark 3.1 for further comments on the necessity to saturate the refinements.

Theorem 4.5.

Proof.

Define

Following [24, 13], a heuristic proxy for the upper estimate in (4.4) is . To determine the optimal number of iterations , we optimize the complexity while constraining the aforementioned term to :

We can check easily that, with the obtained solutions, the remaining terms in the upper estimate (4.4) are of order .

∎

Remark 4.5.

- (i)

- (ii)

| Algorithm | MLSA | adMLSA |

| -control | ||

| (Decomposition (1.21), | (Decomposition (4.6), | |

| Lemma 1.2(i) and Theorem 1.6) | Lemma 1.2(i) and Theorem 4.2) | |

| Number of levels | ||

| (Proposition 1.7(i)) | (Proposition 4.3) | |

| Optimal complexity | ||

| (Proposition 1.7(iii)) | (Theorem 4.5) |

4.3 Heuristics

5 Financial Case Studies

In the ensuing numerical studies, we illustrate the performance gap closure between (MLSA) and (SA) that is made possible by adopting our adaptive refinement strategy. To this end, we revisit the VaR use cases already handled by (SA), (NSA) and (MLSA) in [13, Sections 4 & 5]. The implementations for the below case studies can be found at github.com/azarlouzi/ada_mlsa.

Confidence Constant Estimation.

In the following applications, we tune the confidence constant appearing in (2.9) on a grid. Remark 2.2(v) however suggests a different treatment for this constant.

Denote the sampling standard deviation and , , its empirical approximation given by

| (5.1) |

An alternative refinement strategy would incorporate an estimation of in (2.9) by at the refinement step , where is set to to retrieve a -confidence level on the closeness between and .

5.1 European Option

We succinctly recall here the setting of [13, Section 4]. We refer to the developments therein for rigorous derivation of the ensuing statements.

Consider a European option of maturity and payoff , on an underlying asset following a standard Brownian motion dynamic . The risk-free rate is null and pricing is performed under . The option’s value at time is

and its associated loss at a horizon is

We are interested in retrieving the VaR of this loss at some confidence level .

Analytical and Simulation Formulas.

Let ,

On the one hand,

where and are independent and of law . can thus be simulated exactly, hence the benchmarking unbiased SA scheme [4] is applicable to estimate the VaR.

On the other hand, for a bias parameter , can be approximated by

where . We can then apply (NSA), (MLSA), (adNSA), -(adNSA), (adMLSA) and -(adMLSA) on this basis to approximate the VaR.

Finally, the VaR at level has an analytical form:

| (5.2) |

where is the standard Gaussian cdf. Its evaluation will help assess the estimation errors of the aforementioned SA schemes.

Numerical Results.

We conduct below a performance comparison of the different SA schemes discussed in this paper. We set the confidence level to and the time horizon to , which yields via (5.2).

To minimize complexity, all algorithms are run with and their respective theoretical optimal iterations amounts. (SA), (NSA), (adNSA) and -(adNSA) are run with . (MLSA), (adMLSA) and -(adMLSA) are run with under the framework (3.2) with and . We set and for the adaptive schemes, as recommended in Section 4.3. Identical parametrization was applied to (adNSA), -(adNSA), (MLSA), (adMLSA) and -(adMLSA), and identical parametrization was applied to (MLSA), (adMLSA) and -(adMLSA). Further parametrizations of the adaptive and multilevel schemes, obtained via a grid search, are described in Table 5.1. The subsequent level amounts computed via (1.22), (3.6) and (4.7) are reported in columns , and . For (adNSA) and (adMLSA), the iterations amounts scaling factor (e.g. for (adMLSA) as per (4.8)) and the confidence constant were jointly optimized by grid search, which led to the choices and for (adNSA) and and for (adMLSA). As for -(adNSA) and -(adMLSA), we use the critical value with scaling factors and respectively.

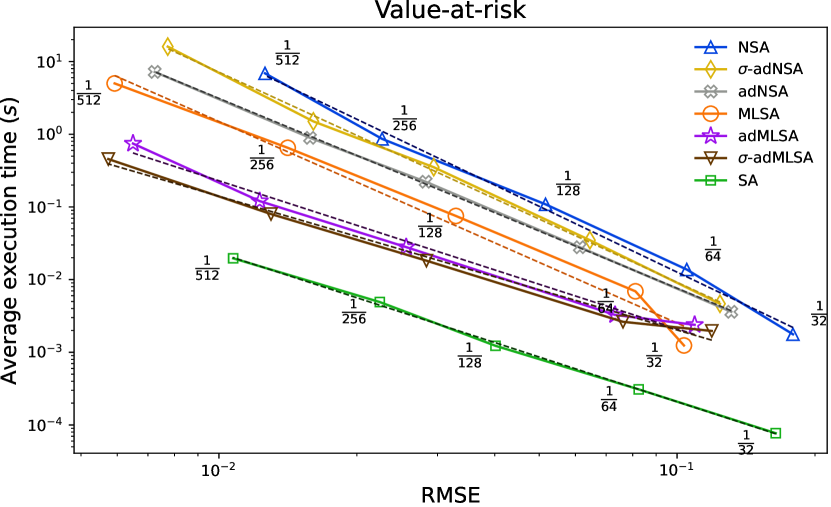

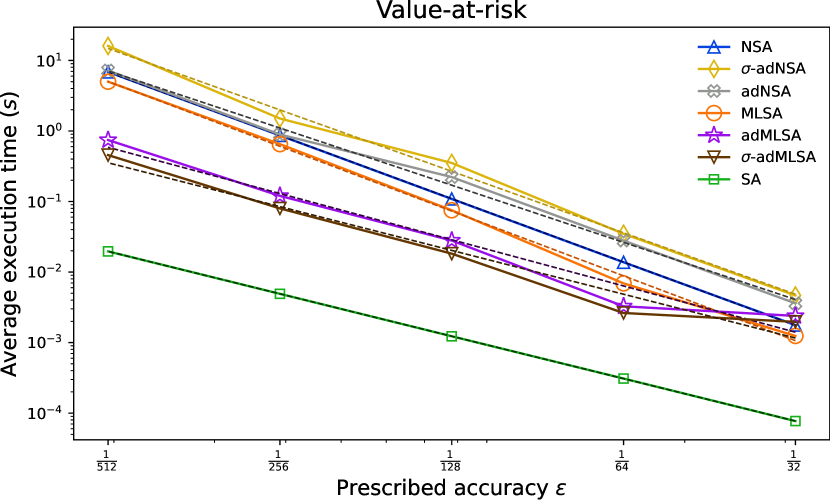

Root-mean-square errors (RMSEs) relative to the true and corresponding average execution times over runs, for a prescribed accuracy ranging in , are graphed for each algorithm on a logarithmic scale in Figure 5.1. Figure 5.2 plots the average execution times against the prescribed accuracies themselves to illustrate the achieved complexities. The slopes fitted on these curves, shown in dashed lines in Figures 5.1 and 5.2, are reported in Table 5.2.

SA scheme NSA -adNSA adNSA MLSA adMLSA -adMLSA SA RMSE Accuracy

[13, Section 4.3] already provides a thorough discussion on (SA), (NSA) and (MLSA). We retain here that (MLSA) scores a partial gain on the performance gap between (SA) and (NSA).

The novelties here are the adaptive schemes. On Figure 5.1, (adNSA) and -(adNSA) achieve comparable performances, outperforming (NSA) by a margin that seems to widen for smaller accuracies. (adNSA) seems to be slightly outperforming -(adNSA), which can be attributed to the overhead computation performed by -(adNSA) to recompute the confidence constant . (adMLSA) and -(adMLSA) show to be significantly outperforming (MLSA): for a target RMSE of order , (adMLSA) and -(adMLSA) run on average in while (MLSA) runs in , achieving a fold speed-up over their non-adaptive counterpart. -(adMLSA) seems to slightly outperform (adMLSA), which can be explained by the precision brought by the recomputation of the standard deviation , in spite of the entailed overhead computational time. However, this overperformance remains slim, recalling that the calibrated confidence constant for (adMLSA) needs not be readjusted on the whole accuracy range once it has been optimized on a couple of accuracies, thus eliminating any additional upstream fine-tuning.

Eventually, an examination of the fitted slopes highlights that (adNSA) and -(adNSA) achieve the theoretical complexity exponents predicted by Proposition 3.5. It also demonstrates that (adMLSA) and -(adMLSA) achieve the quadratic complexity anticipated by Theorem 4.5(i) for large. The performances of these schemes match that of (SA) that assumes the exact simulatability of the true loss .

5.2 Interest Rate Swap

The following setting is recapitulated from [13, Section 5].

We consider a swap, of strike , maturity and nominal , each leg being worth at inception, issued at par on some underlying interest (or FX) rate following a Black-Scholes model with risk neutral drift and constant volatility . At the coupon dates , the swap remunerates the cash flows , where , . The risk-free rate is and the risk neutral probability measure is .

For , let be the integer such that if , and otherwise. The fair value of the swap at time is

The loss on a short position on the swap at a time horizon is

We are interested in computing the VaR of this loss at some confidence level .

Analytical and Simulation Formulas.

On the one hand,

and . This allows simulating exactly, hence the availability of (SA) to approximate the VaR.

On the other hand, satisfies

| (5.3) |

where is independent of , with

and . The nested Monte Carlo averaging (1.6) is thus available to approximate (5.3), hence the applicability of (NSA), (adNSA), -(adNSA), (MLSA), (adMLSA) and -(adMLSA) to approximate the VaR.

Finally, the VaR at level is available analytically:

| (5.4) |

where is the standard Gaussian cdf. The output of this formula will serve as a benchmark for the outcomes of the aforementioned algorithms.

Numerical Results.

For the case study, we set , , , , , , and . We use the day count fraction convention. (5.4) yields .

We run all algorithms at their theoretical optimums, with and the corresponding optimal iterations amounts. The learning rate is employed for (SA) and for (NSA), (adNSA) and -(adNSA). For (adNSA), -(adNSA), (MLSA), (adMLSA) and -(adMLSA), we adopt the framework (3.2) with the exponent , the geometric step and the exponent for . As suggested in Section 4.3, we set and . For every prescribed accuracy , we tune (governing the number of levels for (MLSA), for (adNSA) and -(adNSA), and for (adMLSA) and -(adMLSA)) and the learning rate for (MLSA), (adMLSA) and -(adMLSA) on suitable grids. Table 5.3 lists these parametrizations by prescribed accuracy. The iterations amounts scaling factor and adaptive refinement confidence constant are tuned on grids. We retain for (adMLSA) and -(adMLSA), for (adMLSA), for (adNSA) and -(adNSA) and for (adNSA). We eventually set the critical value for -(adNSA) and -(adMLSA).

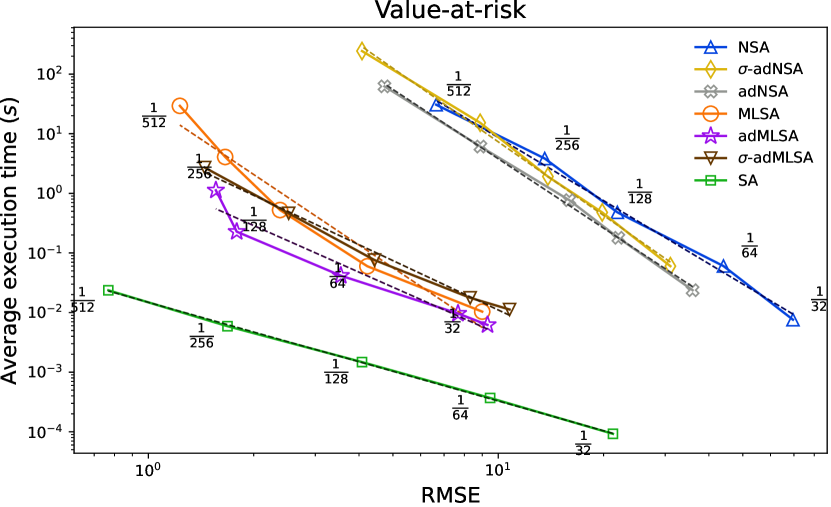

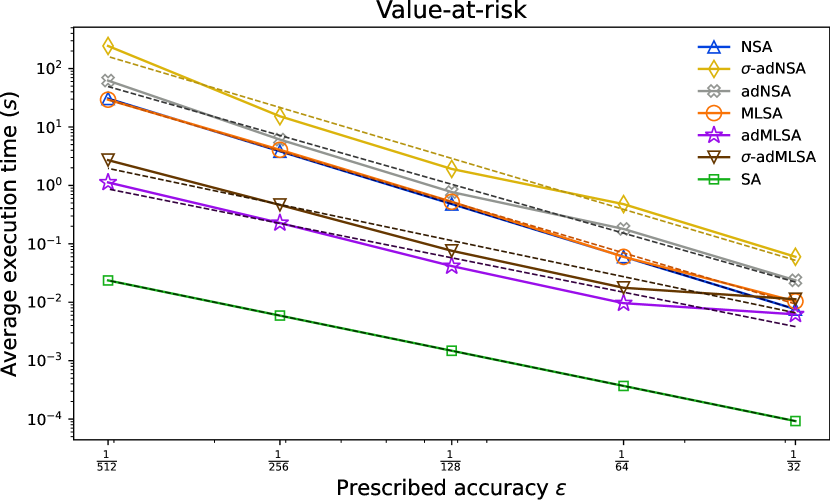

The joint evolution of the RMSE and average execution time over runs of each SA scheme, for an accuracy looping through , are plotted on a logarithmic scale on Figure 5.3. Figure 5.4 showcases the average execution times against the prescribed accuracies. Table 5.4 reports the regressed slopes on these curves as depicted in dashed lines on Figures 5.3 and 5.4.

SA scheme NSA -adNSA adNSA MLSA adMLSA -adMLSA SA RMSE Accuracy

Similar comments to the previous case study are applicable here. For smaller accuracies, (adNSA) and -(adNSA) score a speed-up with respect to (NSA) as do (adMLSA) and -(adMLSA) with respect to (MLSA). The performance margins between (adNSA) and -(adNSA) on the one hand and (adMLSA) and -(adMLSA) on the other hand are rather slim. (adNSA) and (adMLSA) remain preferable as they do not require recomputing once it has been fine-tuned on a couple of prescribed accuracies.

Although further fine-tuning may be required, the fitted slopes already indicate that the adaptive multilevel schemes are approaching the desired quadratic complexity.

Conclusion

For a prescribed accuracy , the canonical multilevel complexity order is retrieved, up to a logarithmic factor, for an MLSA scheme with a Heaviside-type update function. This is made possible by adopting an adaptive refinement strategy on the innovations driving the multilevel algorithm’s inner nested schemes. Our strategy allows to fulfill the closure of the performance gap that resides between nested MLSA and unbiased Robbins-Monro schemes for Heaviside-type update functions. The performance gain achieved by adaptive MLSA on its regular counterpart is significant in practice, attaining a ten fold speed-up in certain cases and expected to increase exponentially with smaller prescribed accuracies.

Appendix A Auxiliary Results

The proof of the following result is included in the preliminary steps of [13, Proposition 3.2] and is therefore omitted.

Lemma A.1.

-

(i)

Assume that there exists such that . Then, for any ,

-

(ii)

Assume that there exists such that for all . Then, for any and any ,

Similarly to [13], we define, for , and a positive integer , the Lyapunov function by

| (A.1) |

The following lemma states some important properties of .

Appendix B Proofs of the Auxiliary Convergence Results

Throughout, denotes a positive constant that may change from line to line but is independent of and .

Proof of Lemma 3.1.

By (2.8) and the law of total probability,

| (B.1) | ||||

| (B.2) |

and that, by (2.8) under the condition (1.16),

| (B.3) |

by Markov’s inequality and Lemma A.1(i),

Using the previous inequality, (B.1) and the condition (3.2) on then on ,

| (B.4) | ||||

(i) b. Let and . By (B.2), (B.3), the definition (2.8) in the case of (1.17), Markov’s exponential inequality and Lemma A.1(i),

Minimizing the above upper bound with respect to yields

In view of the condition (3.3) on , and , one gets

Therefore, recalling (B.1),

| (B.5) |

(ii) For , via the definition (2.8) in the case of (2.7), Markov’s exponential inequality and the condition (3.4) on , and ,

Thus, by (B.1),

| (B.6) |

∎

Proof of Proposition 3.2.

In this proof, we omit the superscript from the Lyapunov function and denote instead .

For any , let be the filtration defined by and

, .

Let . In the spirit of [13, Theorem 3.3], we test the Lyapunov along the dynamics (B.8). Using a second order Taylor expansion,

| (B.13) | ||||

It follows from Lemmas A.2(iii,iv), (A.2) and (B.11) that

| (B.14) | ||||

The mean value theorem guarantees that, for any , there exists such that

| (B.15) |

Besides, from (1.3),

| (B.16) |

with . Applying the triangle inequality to (B.15) and using (B.16),

| (B.17) |

Using the inequality , , and the very definition of ,

| (B.18) |

| (B.19) | ||||

with

Plugging the upper bounds (B.16) and (B.19) into (B.14),

| (B.20) | ||||

where

| (B.21) |

Via the tower law property,

and

so that is a -martingale increment sequence.

Hence, by taking the expectation on both sides of the inequality (B.20),

| (B.22) | ||||

(i) In the following steps, we provide sharper upper estimates for and .

Observe now that

where, using Lemma A.2(v) and (B.21),

Therefore, recalling that by Lemma A.2(iv), for any integer ,

Hence, iterating times the inequality (B.23),

| (B.24) | ||||

where

| (B.25) |

with the convention .

We employ similar lines of reasoning to those in the proof of [13, Theorem 3.1]. Omitting some technical details,

| (B.26) |

under the constraint if , for some constants satisfying .

Step 2. Inequality on .

We now take and in (B.22) and use (B.26) to obtain

where

Iterating times the previous inequality yields

| (B.27) | ||||

where

| (B.28) |

Similar computations to those in the proof of [13, Theorem 3.1] yield

| (B.29) |

with .

Step 3. Conclusion.

Combining (B.26) and (B.29) with the conclusion of Lemma A.2(v) completes the proof.

(ii) Using similar arguments to the previous point, we obtain the sharp upper estimate

| (B.30) |

with . Considering Lemma A.2(v), the inequalities (B.29) and (B.30) yield the sought upper estimate.

∎

Proof of Lemma 4.1.

We calculate

where

| (B.31) |

We analyze and separately.

Step 2. Study of .

Letting , one has, via the definition (2.8), Markov’s inequality and Lemma A.1(i),

Thus, by (B.31),

where we used the condition (4.1) on then on .

Appendix C Proof of Theorem 4.2

For any , let be the filtration defined by and

, .

Following (B.8), the dynamics (adNSA) can be decomposed into

| (C.1) |

where and are defined in (B.9)--(B.10) and

| (C.2) | ||||

| (C.3) |

Iterating (C.1),

| (C.4) | ||||

where

| (C.5) |

with the convention .

Given that as , there exists such that for , . Hence, using the inequality , , for large enough,

| (C.6) | ||||

where , with the convention .

According to (adMLSA) and the decomposition (C.4),

| (C.7) | ||||

We study each term in the above decomposition separately.

Step 1. Study of .

Following Remark 2.2(ii), no refinement is applied at level , so that by Lemma 1.2(ii),

Step 2. Study of .

By assumption, , and according to Lemma 1.2(i), is bounded. Hence .

Besides, by (C.6) and [14, Lemma A.1(ii)], under the condition .

Hence,

Step 3. Study of .

Recalling that, by Lemma 1.2(i), is bounded, there exists a compact set such that for any . From Lemma 1.2(i) and Assumptions 1.1(iv) and 1.5,

Consequently from (C.2), Proposition 3.2(ii) and the above inequality,

| (C.8) |

Recalling (C.6), under the condition if , by [14, Lemma A.1(i)],

Using that , the Cauchy-Schwarz inequality and the definition (4.5),

| (C.9) | ||||

Step 4. Study of .

Taking into account the fact that and Assumption 1.1(iv), a first order Taylor expansion yields

Hence, by the definition (C.3) and Proposition 3.2(ii) (which applies since if ),

Recalling (C.6) and that if by assumption, via [14, Lemma A.1(i)]

Step 5. Study of .

Using the inequalities (B.11) and (C.6) and recalling that if , by [14, Lemma A.1(i)],

Step 6. Study of .

Note that the random variables are independent with zero mean and that, at each level , are -martingale increments.

Therefore

References

- [1] C. Acerbi and D. Tasche ‘‘On the coherence of expected shortfall’’ In Journal of Banking & Finance 26.7, 2002, pp. 1487–1503

- [2] O. Bardou, N. Frikha and G. Pagès ‘‘Computing VaR and CVaR using stochastic approximation and adaptive unconstrained importance sampling’’ In Monte Carlo Methods and Applications 15.3, 2009, pp. 173–210 DOI: doi:10.1515/MCMA.2009.011

- [3] O. Bardou, N. Frikha and G. Pagès ‘‘CVaR hedging using quantization-based stochastic approximation algorithm’’ In Mathematical Finance 26.1, 2016, pp. 184–229

- [4] O. Bardou, N. Frikha and G. Pagès ‘‘Recursive computation of value-at-risk and conditional value-at-risk using MC and QMC’’ In Monte Carlo and Quasi-Monte Carlo Methods 2008 Springer, 2009, pp. 193–208

- [5] D. Barrera, S. Crépey, B. Diallo, G. Fort, E. Gobet and U. Stazhynski ‘‘Stochastic approximation schemes for economic capital and risk margin computations’’ In ESAIM: Proceedings and Surveys 65, 2019, pp. 182–218

- [6] Basel Committee on Banking Supervision ‘‘Consultative document: Fundamental Review of the Trading Book: A revised market risk framework’’, 2013 URL: bis.org/publ/bcbs265.pdf

- [7] M. Ben Alaya, K. Hajji and A. Kebaier ‘‘Adaptive importance sampling for multilevel Monte Carlo Euler method’’ In Stochastics 95.2 Taylor & Francis, 2023, pp. 303–327 DOI: 10.1080/17442508.2022.2084338

- [8] A. Ben-Tal and M. Teboulle ‘‘An old-new concept of convex risk measures: the optimized certainty equivalent’’ In Mathematical Finance 17.3, 2007, pp. 449–476 DOI: https://doi.org/10.1111/j.1467-9965.2007.00311.x

- [9] B. Bercu, M. Costa and S. Gadat ‘‘Stochastic approximation algorithms for superquantiles estimation’’ In Electronic Journal of Probability 26 Institute of Mathematical StatisticsBernoulli Society, 2021, pp. 1–29 DOI: 10.1214/21-EJP648

- [10] M. Broadie, Y. Du and C.. Moallemi ‘‘Efficient risk estimation via nested sequential simulation’’ In Management Science 57.6, 2011, pp. 1172–1194 DOI: 10.1287/mnsc.1110.1330

- [11] K. Bujok, B.. Hambly and C. Reisinger ‘‘Multilevel simulation of functionals of Bernoulli random variables with application to basket credit derivatives’’ In Methodology and Computing in Applied Probability 17.3, 2015, pp. 579–604 DOI: 10.1007/s11009-013-9380-5

- [12] M. Costa and S. Gadat ‘‘Non asymptotic controls on a recursive superquantile approximation’’ In Electronic Journal of Statistics 15.2 Institute of Mathematical StatisticsBernoulli Society, 2021, pp. 4718–4769 DOI: 10.1214/21-EJS1908

- [13] S. Crépey, N. Frikha and A. Louzi ‘‘A multilevel stochastic approximation algorithm for value-at-risk and expected shortfall estimation’’, 2023 arXiv:2304.01207

- [14] S. Crépey, N. Frikha, A. Louzi and G. Pagès ‘‘Asymptotic error analysis of multilevel stochastic approximations for the value-at-risk and expected shortfall’’, 2023 arXiv:2311.15333

- [15] S. Dereich ‘‘Multilevel Monte Carlo algorithms for Lévy-driven SDEs with Gaussian correction’’ In The Annals of Applied Probability 21.1 Institute of Mathematical Statistics, 2011, pp. 283–311

- [16] S. Dereich and T. Müller-Gronbach ‘‘General multilevel adaptations for stochastic approximation algorithms of Robbins--Monro and Polyak--Ruppert type’’ In Numerische Mathematik 142.2, 2019, pp. 279–328 DOI: 10.1007/s00211-019-01024-y

- [17] D. Elfverson, F. Hellman and A. Mälqvist ‘‘A multilevel Monte Carlo method for computing failure probabilities’’ In SIAM/ASA Journal on Uncertainty Quantification 4.1, 2016, pp. 312–330 DOI: 10.1137/140984294

- [18] M. Fathi and N. Frikha ‘‘Transport-entropy inequalities and deviation estimates for stochastic approximation schemes’’ In Electronic Journal of Probability 18 Institute of Mathematical StatisticsBernoulli Society, 2013, pp. 1–36 DOI: 10.1214/EJP.v18-2586

- [19] H. Föllmer and A. Schied ‘‘Convex risk measures’’ In Encyclopedia of Quantitative Finance John Wiley & Sons, Ltd, 2010 DOI: 10.1002/9780470061602.eqf15003

- [20] N. Frikha ‘‘Multi-level stochastic approximation algorithms’’ In The Annals of Applied Probability 26.2 Institute of Mathematical Statistics, 2016, pp. 933–985 DOI: 10.1214/15-AAP1109

- [21] N. Frikha and S. Menozzi ‘‘Concentration bounds for stochastic approximations’’ In Electronic Communications in Probability 17 Institute of Mathematical StatisticsBernoulli Society, 2012, pp. 1–15 DOI: 10.1214/ECP.v17-1952

- [22] M.. Giles ‘‘MLMC techniques for discontinuous functions’’, 2023 arXiv: https://arxiv.org/abs/2301.02882

- [23] M.. Giles ‘‘Multilevel Monte Carlo path simulation’’ In Operations Research 56.3, 2008, pp. 607–617 DOI: 10.1287/opre.1070.0496

- [24] M.. Giles and A.-L. Haji-Ali ‘‘Multilevel nested simulation for efficient risk estimation’’ In SIAM/ASA Journal on Uncertainty Quantification 7.2, 2019, pp. 497–525 DOI: 10.1137/18M1173186

- [25] M.. Giles, A.-L. Haji-Ali and J. Spence ‘‘Efficient risk estimation for the credit valuation adjustment’’, 2023 arXiv:2301.05886

- [26] D. Giorgi, V. Lemaire and G. Pagès ‘‘Weak error for nested multilevel Monte Carlo’’ In Methodology and Computing in Applied Probability 22, 2020, pp. 1325–1348 DOI: 10.1007/s11009-019-09751-3

- [27] M.. Gordy and S. Juneja ‘‘Nested simulation in portfolio risk measurement’’ In Management Science 56.10, 2010, pp. 1833–1848

- [28] A.-L. Haji-Ali, J. Spence and A.. Teckentrup ‘‘Adaptive multilevel Monte Carlo for probabilities’’ In SIAM Journal on Numerical Analysis 60.4, 2022, pp. 2125–2149 DOI: 10.1137/21M1447064

- [29] S. Heinrich ‘‘Monte Carlo complexity of global solution of integral equations’’ In Journal of Complexity 14.2, 1998, pp. 151–175 DOI: https://doi.org/10.1006/jcom.1998.0471

- [30] S. Heinrich ‘‘Multilevel Monte Carlo methods’’ In Large-Scale Scientific Computing Springer, 2001, pp. 58–67

- [31] H. Hoel, E. Schwerin, A. Szepessy and R. Tempone ‘‘Implementation and analysis of an adaptive multilevel Monte Carlo algorithm’’ In Monte Carlo Methods and Applications 20.1, 2014, pp. 1–41 DOI: doi:10.1515/mcma-2013-0014

- [32] R.. Rockafellar and S. Uryasev ‘‘Optimization of conditional value-at-risk’’ In Journal of Risk 2.3, 2000, pp. 21–41 DOI: 10.21314/JOR.2000.038