LEARN: An Invex Loss for Outlier Oblivious Robust Online Optimization

Abstract

We study a robust online convex optimization framework, where an adversary can introduce outliers by corrupting loss functions in an arbitrary number of rounds , unknown to the learner. Our focus is on a novel setting allowing unbounded domains and large gradients for the losses without relying on a Lipschitz assumption. We introduce the Log Exponential Adjusted Robust and iNvex (Learn) loss, a non-convex (invex) robust loss function to mitigate the effects of outliers and develop a robust variant of the online gradient descent algorithm by leveraging the Learn loss. We establish tight regret guarantees (up to constants), in a dynamic setting, with respect to the uncorrupted rounds and conduct experiments to validate our theory. Furthermore, we present a unified analysis framework for developing online optimization algorithms for non-convex (invex) losses, utilizing it to provide regret bounds with respect to the Learn loss, which may be of independent interest.

1 Introduction

In the mercurial era of digital information, the proliferation of online data streams has become ubiquitous, with applications spanning from financial markets and healthcare to e-commerce and social media (D. Hendricks and Wilcox,, 2016; Zhang et al.,, 2015; Fedoryszak et al.,, 2019; Kejariwal et al.,, 2015). The surge in real-time data generation across these diverse fields has underscored the pressing need for adaptive optimization strategies. These strategies need to navigate dynamic and uncertain environments, especially as organizations rely more on online decision-making processes. In this context, the demand for efficient and robust optimization techniques in the presence of outliers has become more pronounced.

Outlier robustness

Pioneering works in robust statistics (Huber,, 1964; Beaton and Tukey,, 1974) emphasized mitigating outliers’ impact on algorithm performance. In online optimization originally designed for uncorrupted streams, outliers pose challenges leading to suboptimal solutions (Feng et al.,, 2017). This motivates developing outlier-robust online methodologies, an area of recent focus (Diakonikolas et al.,, 2022; van Erven et al.,, 2021; Bhaskara and Ruwanpathirana,, 2020; Feng et al.,, 2017).

Online convex optimization (OCO)

The OCO framework (Hazan,, 2023; Orabona,, 2023) offers a useful mathematical framework for studying sequential predictions, especially in the presence of adversarial interventions. The adversary chooses a deterministic sequence of convex losses for each , where denotes the time horizon. In every round, the learner picks an action in a convex set for which she suffers the loss for the round and additionally gets to observe . The learner’s goal is to minimize the cumulative loss, i.e., , and her performance is evaluated using the notion of regret.

OCO with robustness

The OCO framework serves as a valuable starting point for studying algorithms that dynamically adapt to incoming data points while considering potential outliers’ influence. Drawing inspiration from the model proposed by van Erven et al., (2021), this work considers the OCO framework where the adversary is allowed to choose any of rounds to be ‘clean’ and inject outliers into the remaining rounds. This adversarial influence is exerted by tampering with the side information integral to constructing the loss function . Considering the example of the online ridge regression problem, where represents the incoming data point for round , and the loss is defined as , the adversary can corrupt either , or both to corrupt the round . The corrupted round is considered an outlier. We use to denote the uncorrupted side information and for the corrupted side information. The learner’s performance is measured using regret with respect to only the clean rounds, and we refer to this as clean regret. In this paper, we explore the notion of dynamic regret – a performance measure suitable for dynamic environments characterized by evolving data and shifting optimal decision parameters. Dynamic regret entails adapting strategies to compete effectively with evolving comparators, thereby mitigating the impact of changing environments on decision-making processes. Let be a sequence of learner’s actions and be a sequence of benchmark points such that . We also define . Clearly, for clean rounds. Then, the clean dynamic regret is defined to be

| (1) |

Our goal is to develop robust online algorithms to achieve sublinear regret with respect to and achieve optimal dependency on the number of outliers , which is unknown.

This work focuses on -strongly convex losses. Diverging from van Erven et al., (2021)’s static model, we introduce novel OCO techniques for outlier scenarios when the number of outliers is unknown. Unlike their work assuming known , and in contrast to common bounded domain/Lipschitz loss assumptions (Hazan,, 2023; Orabona,, 2023), our approach allows unbounded domains and non-Lipschitz losses. Following Jacobsen and Cutkosky, (2023), we permit arbitrarily large gradients away from ’s minimizer, extending applicability to outlier scenarios.

| Setting | Best-known upper bound | Our upper bound |

|---|---|---|

| Bounded domain | ||

| Unbounded domain | Not Available |

1.1 Main contributions

In this paper, we study a crucial question within the robust OCO framework:

Can we achieve sublinear clean dynamic regret in with optimal dependency on the outlier count , without its prior knowledge, when the adversary can corrupt an arbitrary subset of rounds?

We answer the aforementioned question in the affirmative with a linear dependence on the number of outliers, which is known to be unavoidable in the robust OCO setting (van Erven et al.,, 2021). Our main contributions in this work are summarized below:

-

1.

Introduction of Robust Invex Loss: At the core of our work lies the introduction of a robust, invex loss function, which we refer to as the Learn loss (refer to Equation (4)). The limitations of convex loss functions in handling outliers are well studied in the literature (Chen et al.,, 2022). As alternative solutions, researchers have investigated non-convex robust losses (Barron,, 2019). However, given the evolving landscape of mathematical studies in non-convex optimization, this transition poses challenges in the analysis. Striking a judicious balance, our Learn loss addresses the outlier-handling requirements and lends itself to rigorous theoretical analysis.

-

2.

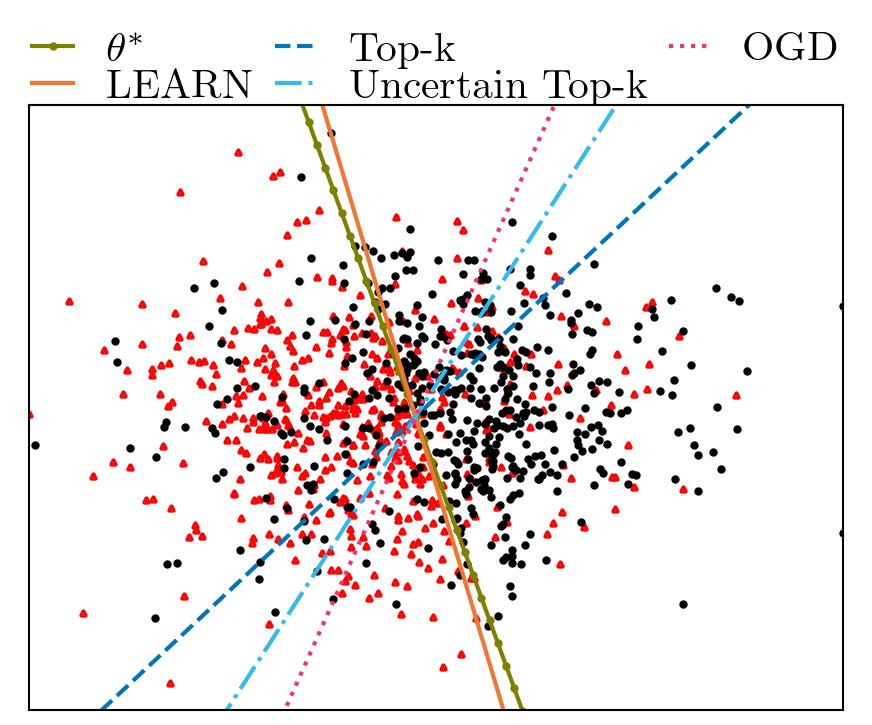

Unified analysis framework for robust online gradient descent algorithm: We introduce Learn, a robust variant of online gradient descent leveraging the outlier-handling Learn loss (Algorithm 1). We provide a unifying analytical framework for analyzing Algorithm 1’s regret, instrumental in establishing guarantees for our invex loss (Section 3.1). This framework extends to geodesically convex (Wang et al.,, 2023) and pseudo-convex (Zhang et al.,, 2018) losses, enhancing the applicability of our approach. We substantiate Learn’s robustness via online SVM experiments (Fig. 1, Appendix I.2), where it consistently predicts boundaries closely matching ground truth despite outliers, aligning with the theoretical guarantees (details are provided in Appendix I.2).

-

3.

Sublinear clean dynamic regret in bounded domain: In addition to analyzing regret for invex losses, we study the clean regret for strongly convex loss functions within the robust OCO framework (Section 3.2). Our algorithm can handle potentially unbounded gradients while remaining agnostic to the number of outliers. Our upper bound exhibits sublinear growth, specifically as , where optimal path variation is defined as . The bound is optimal with respect to both and and matches the lower bound presented in van Erven et al., (2021) for the static case (Also see Appendix B).

-

4.

An expert framework with outliers and sublinear clean dynamic regret: Extending dynamic regret bounds to unbounded domains is non-trivial, as shown by Jacobsen and Cutkosky, (2023) who used an expert framework. Introducing outliers poses new challenges hindering a straightforward extension to our setup. We address this by constructing a novel expert framework with experts to handle outliers, incurring expert regret (Lemma 3.4). This expert framework construction/analysis could be of independent interest. Utilizing it, we derive clean dynamic regret bounds. Our bound is . This matches existing bounds without outliers in dependence. Ours is the first work providing dynamic regret bounds for unbounded domains with outliers, to our knowledge.

Table 1 presents a concise summary of our results and contrasts them with the best existing results. In the bounded domain, the best-known upper bound presented in the table follows from the analysis of van Erven et al., (2021). We note that van Erven et al., (2021)’s results pertain to the static setting. In Appendix B, we present a straightforward extension of their result to the dynamic setting. However, unlike van Erven et al., (2021)’s approach, our algorithm does not require prior knowledge of and is capable of handling unbounded gradients. In the unbounded domain, to the best of our knowledge, our work presents the first-known results. We further validate our theoretical results through comprehensive numerical experiments conducted in Section 4.

Related works:

Our starting point is the robust OCO framework with outliers proposed by van Erven et al., (2021), though their analysis is limited to static regret with known outlier counts. The foundational works of Huber, (1964) and Beaton and Tukey, (1974) motivate the importance of handling outliers from a robust statistics perspective. Incorporating robust loss functions like Huber, Tukey’s biweight, etc., has been explored by Barron, (2019); Belagiannis et al., (2015) to enhance algorithm resilience against outliers. We build upon the expert framework approach of Jacobsen and Cutkosky, (2023) for unconstrained domains, extending it to handle outliers. Our robust approach aligns with the broader literature on robust optimization in theoretical computer science and machine learning problems, as comprehensively surveyed by Diakonikolas and Kane, (2023). A detailed section on the related works appears in the Appendix A.

2 Preliminaries and notation

We consider an online learning protocol delineated by the subsequent framework. At each iteration , the learner picks an action where is a convex set. Note that we provide results for both bounded and unbounded . Subsequently, the adversary reveals an -strongly convex, non-negative loss function where denotes the side information for round , resulting in the learner incurring a loss of . Note that the side information is also revealed along with the function to the learner in every round . For fixed , denotes the gradient of with respect to at . While we assume throughout that the gradient exists, our analysis still holds when is not smooth. We allow for the potential existence of large gradients by following the relaxed gradient assumption of Jacobsen and Cutkosky, (2023) with unknown non-negative constants and , i.e.,

| (2) |

where acts as the reference point. The round is said to be an outlier round if is corrupted and the corruption can be arbitrary. We use to denote the clean rounds. The maximum loss incurred by the learner is assumed to be smaller than in the clean rounds, i.e., , and the loss incurred by the learner may be unbounded in outlier rounds. Next, we provide a formal definition of invex functions, which generalize the concept of convex functions:

Definition 2.1 (Invex functions).

A differentiable function is called a -invex function on set if for any and a vector-valued function ,

| (3) |

where is the gradient of at .

Learn loss

In this work, we introduce a non-convex robust loss function, Log Exponential Adjusted Robust and iNvex (Learn) loss that transforms the output of a convex function as follows

| (4) |

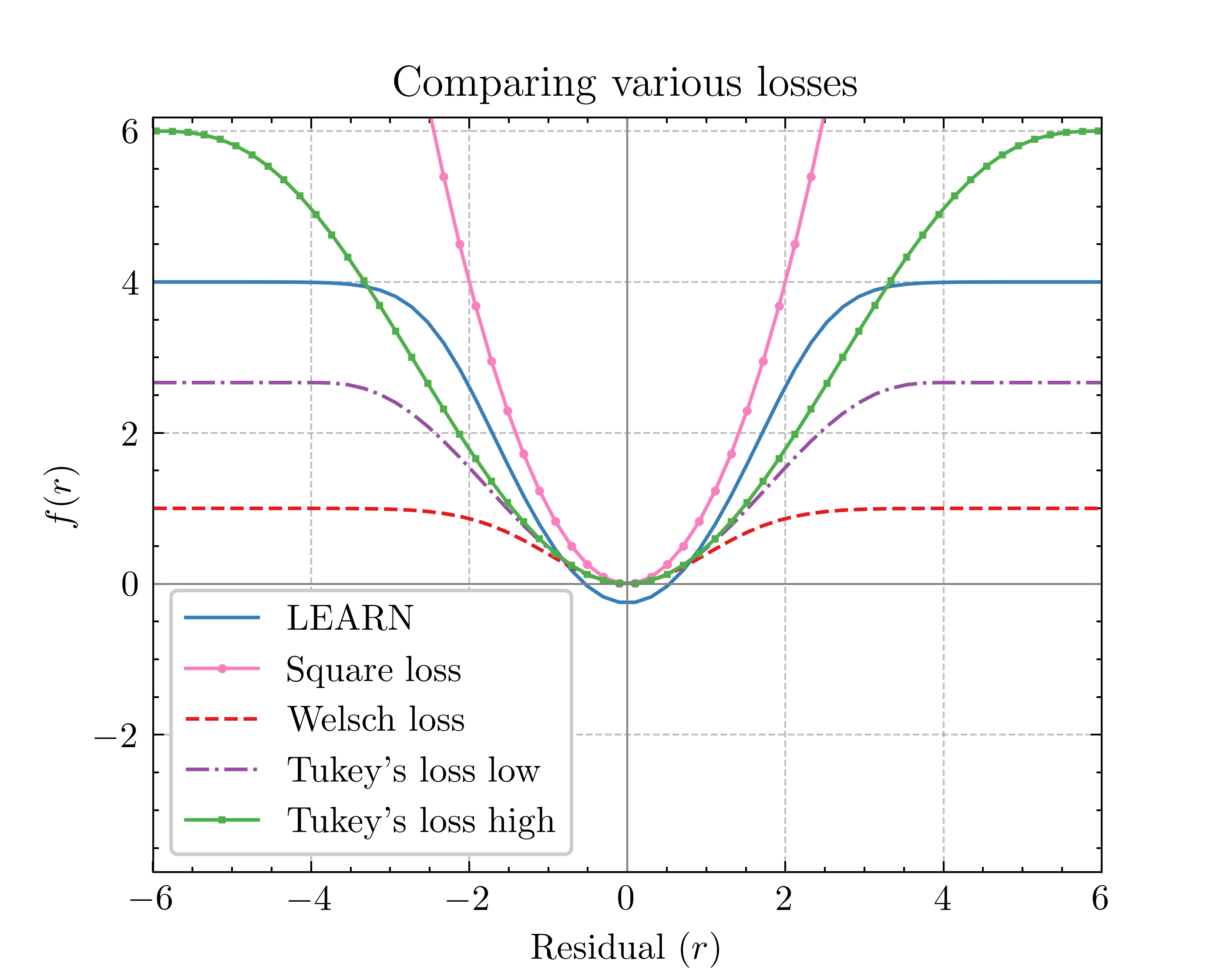

where are constants that can be tuned. Robust losses have been widely used in various real-world problems to reduce the sensitivity of algorithms to outliers (Barron,, 2019). The structure of Learn shares similarities with the log-sum-exp function, used previously for robustness (Lozano and Meinshausen,, 2013). To understand how Learn loss works to mitigate its susceptibility to outliers, we examine its behavior by comparing how resembles the square loss where denotes the residual, and the minimum is attained at . The Learn loss closely follows the behavior of the function in the vicinity of the origin and gradually levels off as we move away from it (Figure 3 in Appendix C). Importantly, the minimizers for both and are the same. Observe that for Learn loss, the norm of the gradient monotonically decreases with the distance from the minimum. This reduces the adverse influence of outliers during a gradient descent style update. This property, known as the redescending property (Hampel et al.,, 2011) in the M-estimation literature, enhances the robustness of the model. Additionally, it is worth noting that empirical studies have shown that non-convex losses offer better robustness when compared to the convex alternatives (Maronna et al.,, 2006).

3 Robust online convex optimization

In this section, we develop Learn, a robust variant of the online gradient descent algorithm aimed at minimizing regret within the robust (OCO) framework. We will consistently refer to this algorithm simply as Learn. This algorithm leverages the previously introduced Learn loss.

Given a convex set , the algorithm starts by picking an arbitrary action . For each round , the learner is revealed a convex loss function in conjunction with the side-information . Note that the adversary is capable of corrupting the side information for any out of the rounds and the learner does not see whether is corrupted. To mitigate the challenge presented by the corruption introduced by the adversary, our algorithm leverages Learn loss. The algorithm proceeds to construct based on the original loss function (Step 5) and executes the subsequent action through a projected gradient descent update on the robust loss .

In the context of encountering outliers, it is relevant to analyze the clean dynamic regret as defined in Equations (1), a task that we undertake in Section 3.2. However, we go beyond the confines of this initial exploration and examine the regret guarantees that pertain to the Learn loss itself. This exploration holds intrinsic interest, as it unveils our ability to extend the regret analysis to encompass a broader spectrum of invex losses beyond our originally introduced Learn loss denoted by .

To streamline the presentation of the results in this paper, we introduce the following notations:

| (5) | ||||||||

| (6) | ||||||||

The learner has the flexibility to fine-tune these constants by carefully selecting parameters and . For corrupted rounds, we introduce an additional quantity . This quantity measures the adversary’s capability to influence the optimal action of round , denoted by . Recall that for uncorrupted rounds, .

3.1 Regret analysis of the Learn loss

Here, as an independent analysis, we derive regret bounds associated with invex losses in isolation, agnostic to the presence of outliers.111We omit the effect of the side information for this analysis by defining for a fixed . In particular, we study the dynamic regret associated with the invex losses defined as

| (7) |

Note that by construction .

We introduce a versatile framework designed to bound the dynamic regret in the context of online invex optimization. Notably, this framework is not confined to Learn loss; it extends seamlessly to encompass other invex losses, including but not limited to geodesically convex loss, weakly pseudo-convex loss, and similar cases. In this setup, we will assume that is a closed and bounded convex set. We further assume that all the convex losses are bounded, i.e., for all (even when is corrupted). We use the invexity of the Learn loss and combine it with the results of our unified analysis framework (See Appendix E) to prove an upper bound on the robust dynamic regret. To this end, we state and prove the invexity of constructed at each step by Learn (Step 5). We denote

| (8) |

Lemma 3.1.

The following theorem establishes an upper bound on the robust dynamic regret when the learner employs Algorithm 1 and executes the actions by constructing -invex robust losses for each .

Theorem 3.2.

Notice that by optimally tuning the stepsize, experiences sublinear growth with respect to . The accompanying constants, which are independent of , can be fine-tuned by judiciously choosing parameters and . It is possible to ease the constraints associated with the bounded domain and the prior knowledge of by adopting an expert framework while preserving a sublinear regret. However, a detailed exploration of regret bounds in this context is postponed to subsequent sections.

3.2 Clean dynamic regret analysis

In this section, we study how Learn performs within the robust OCO framework when evaluated using the clean regret. We consider both bounded and unbounded domains and provide upper bounds tight up to constant factors.

3.2.1 Bounded domain

In the following theorem, we establish upper bounds on the clean dynamic regret for -strongly convex functions bounded in for rounds that are uncorrupted by the adversary. We take . The learner determines the actions to be taken by following Algorithm 1. With no prior knowledge on , we provide an regret bound matching the lower bound presented in van Erven et al., (2021) (extended to a dynamic environment in Appendix B).

Theorem 3.3.

For each , consider a sequence of -strongly convex loss functions . The losses during uncorrupted rounds are bounded in , while the losses during corrupted rounds may be unbounded. Let be the sequence of actions chosen by the learner using Algorithm 1. If the learner chooses , then

| (11) |

The behavior of grows sublinearly with respect to the total number of rounds and linear concerning the count of outlier rounds . It is crucial to underscore the dependence of the regret bound on , a measure quantifying the adversary’s capability to perturb the optimal action during corrupted rounds. This dependence highlights the sensitivity of the regret to the adversary’s influence in the presence of outliers. Lastly, the constants independent of within the regret expression can be fine-tuned through careful parameter choices for and . This provides an avenue for further optimization, allowing the learner to perform better with meticulous parameter tuning.

3.2.2 Unbounded domain via an expert framework

The scenario becomes notably more intricate when dealing with an unbounded domain, introducing an additional layer of complexity exacerbated by the presence of corrupted rounds initiated by the adversary. Recent work by Jacobsen and Cutkosky, (2023) have addressed the challenges associated with unbounded domains through the development of an expert framework. In alignment with this approach, we propose an expert framework tailored to handle outlier rounds. Our framework encompasses experts, each executing an instance of Algorithm 1 with a fixed stepsize and operating within a bounded domain where refers to a given expert. The learner strategically selects their action by means of a carefully constructed weighted average of the actions taken by the individual experts. As the domain is unbounded, we define for this section. We present the experts’ version of the Learn algorithm in Algorithm 2.

Next, we provide a proof sketch for bounding the clean dynamic regret that matches the lower bound in terms of and presented in Jacobsen and Cutkosky, (2023) for the setting without outliers. Consider parameters for sufficiently large and . The selection of parameters ( and ) for an expert is drawn from a set , defined as:

| (12) |

where and . Clearly, . Let be a sequence of actions chosen by the expert . Observe that for any expert ,

| (13) |

Taking , we bound in four major steps. First, if for any specific expert , then we establish that is bounded (Lemma G.2). Second, we demonstrate that remains bounded when . To that end, we prove the following bound on expert regret under the presence of outliers.

Lemma 3.4.

By choosing , the following regret guarantee holds with respect to any expert following Algorithm 2:

| (14) |

Third, we establish the bound on when (Lemma G.3). Finally, we show that is bounded when (Lemma G.4). Combining all these together, we state the following result:

Theorem 3.5 (Informal).

For each , let be a sequence of -strongly convex loss functions with possible of them corrupted by outliers. We assume that the loss for uncorrupted rounds falls within the range , whereas the loss for corrupted rounds can be unbounded. Let be a sequence of actions chosen by the learner using Algorithm 2 with parameters for the experts chosen from as defined in equation (12). Let . Then,

| (15) |

An overview of proof techniques

We now provide a high-level overview of our proof strategies, deferring the detailed proofs to the Appendix. Using standard methods (such as online gradient descent) in OCO, a typical bound on dynamic regret takes the following form:

| (16) |

for some positive . Notice that depends on the gradient norm for uncorrupted rounds, depends on and domain size for corrupted rounds, while depends on the domain size across all rounds. When gradients and domain sizes are bounded, choosing appropriately ensures growth for and , limiting to growth. Typically, in bounded domains, is controlled by assuming bounded gradient norms for uncorrupted rounds, and by filtering rounds with large gradient norms, ensuring small gradient norms for corrupted rounds (e.g., van Erven et al., (2021)). However, this requires bounded gradients for uncorrupted rounds and prior knowledge of , often unavailable, leading to uncontrollable growth of and . We circumvent this issue by carefully constructing the Learn loss function, working with instead of , and controlling its growth (Lemmas H.1,H.2). In the unbounded domain, can grow arbitrarily large and we develop an expert framework to control its growth (Lemma 3.4 and Appendix G). Experts operate in chosen bounded domains with fixed step sizes, and the learner strategically combines their actions to achieve a dynamic regret bound of .

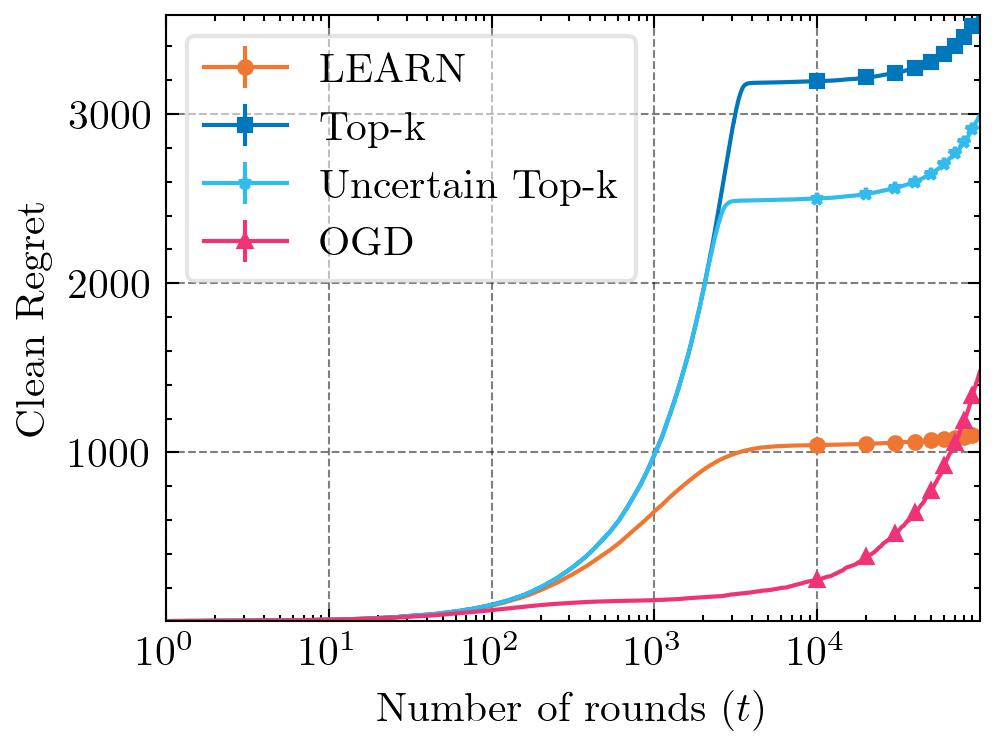

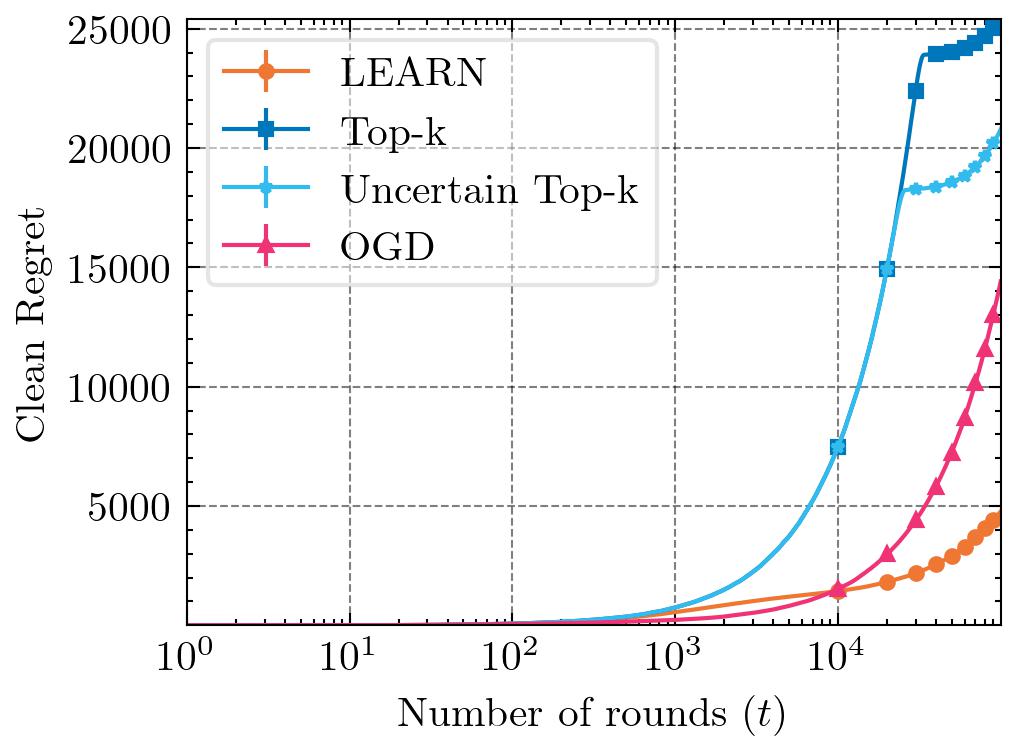

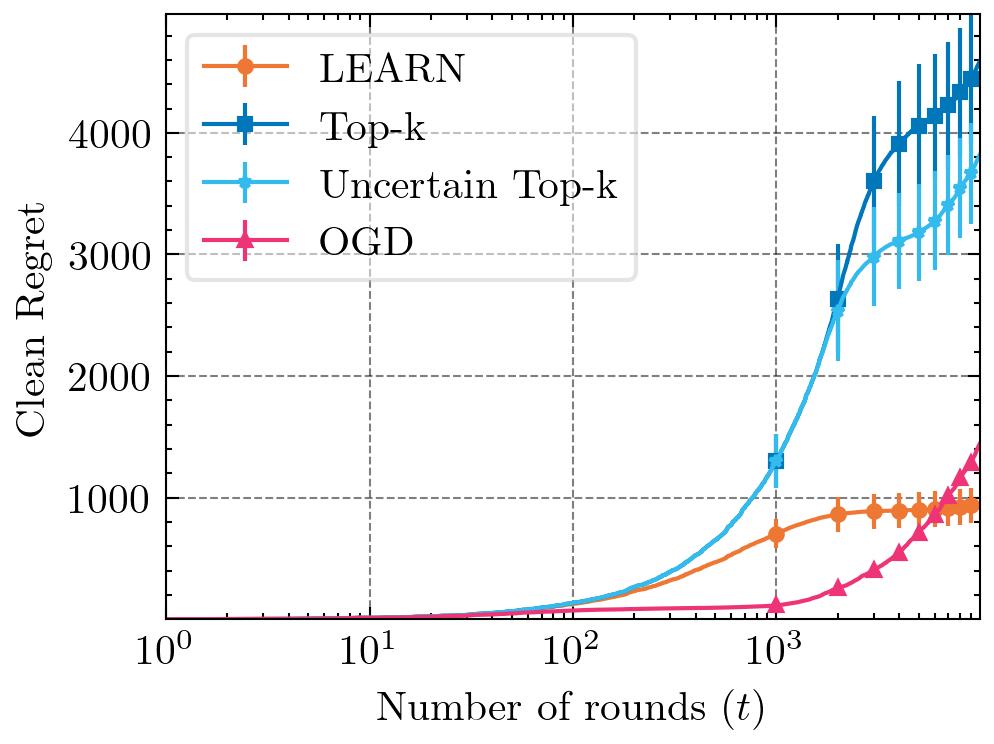

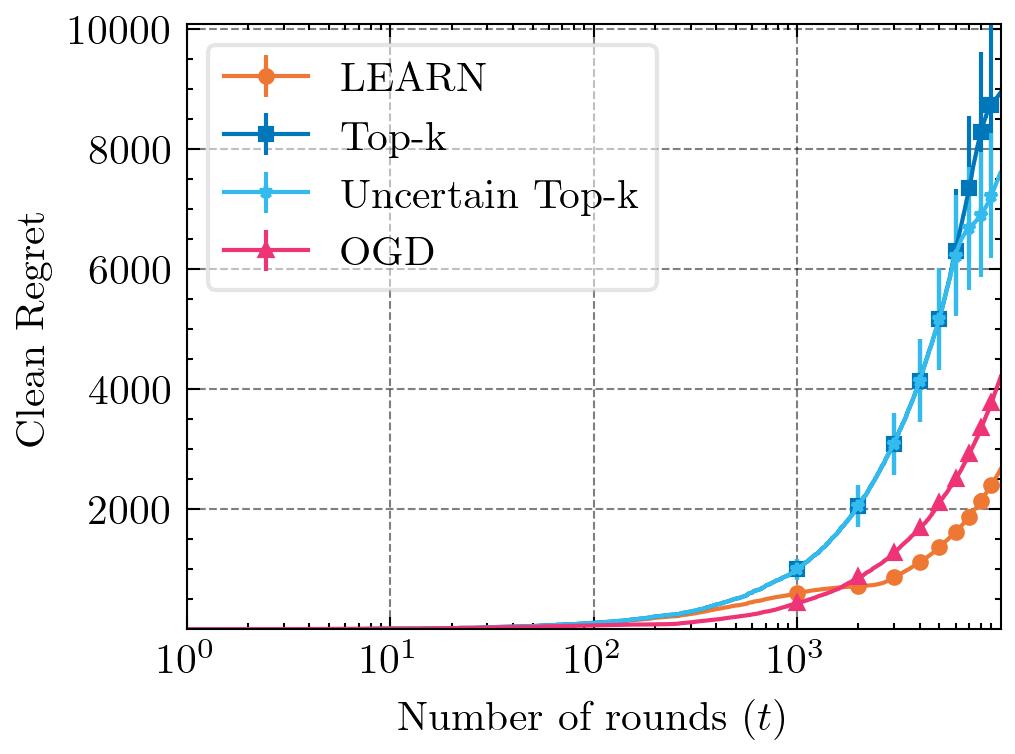

4 Experimental validation

This section presents numerical experiments conducted to substantiate our theoretical findings. We focus on two quintessential machine learning problems, online linear regression, and classification to validate our theory. In particular, we focus on online ridge regression and online support vector machine (SVM). We compare Learn with the Top-k filter algorithm (Top-k) of van Erven et al., (2021) and vanilla online gradient descent (OGD). Note that Top-k has access to the number of outliers , but Learn does not know . We also implemented an uncertain version of Top-k, labeled “Uncertain Top-k”, which only has access to an estimate of fixed at . We conduct experiments in an unbounded domain with potentially large gradients of -strongly convex loss functions. Note that none of the baselines provide theoretical guarantees for unbounded domains with outliers. All methods employ the same stepsize . We would like to clarify our choice of step size in the experiments. Given that the losses are -strongly convex, it is possible to set for the baselines. However, in our experiments, the value of was very small (), which results in a large step size. Consequently, the expected regret bound of becomes quite large. A numerical comparison revealed that using yields smaller regret for the baselines. Therefore, we opted for this more favorable step size in our experimental setup. We report the results for the clean dynamic regrets in Figure 2, averaged across independent runs with the standard errors. We provide additional experimental details in Appendix I.2 and Appendix I.3.

Online linear regression

In this experiment, the learner encounters the following loss function at each round for a fixed :

| (17) |

The response for uncorrupted rounds is generated using the linear model with a unit norm . The entries of are drawn independently from the normal distribution . Additionally, the additive noise is independently chosen from . For corrupted rounds, is chosen uniformly at random from the interval . Figures 2(a)-2(d) show the results from our experiments with varying numbers of outliers over rounds.

Online SVM

Following Shalev-Shwartz et al., (2007), we address the primal version of the online SVM problem. With set at , consistent with Shalev-Shwartz et al., (2007), the learner faces the following loss in each round :

| (18) |

The labels for the uncorrupted rounds are generated according to , where . Mislabeling occurs with probability when . The entries of are drawn independently from . For corrupted rounds, the adversary flips the sign of . Figures 2(e)-2(h) show the experimental results with varying numbers of outliers over rounds.

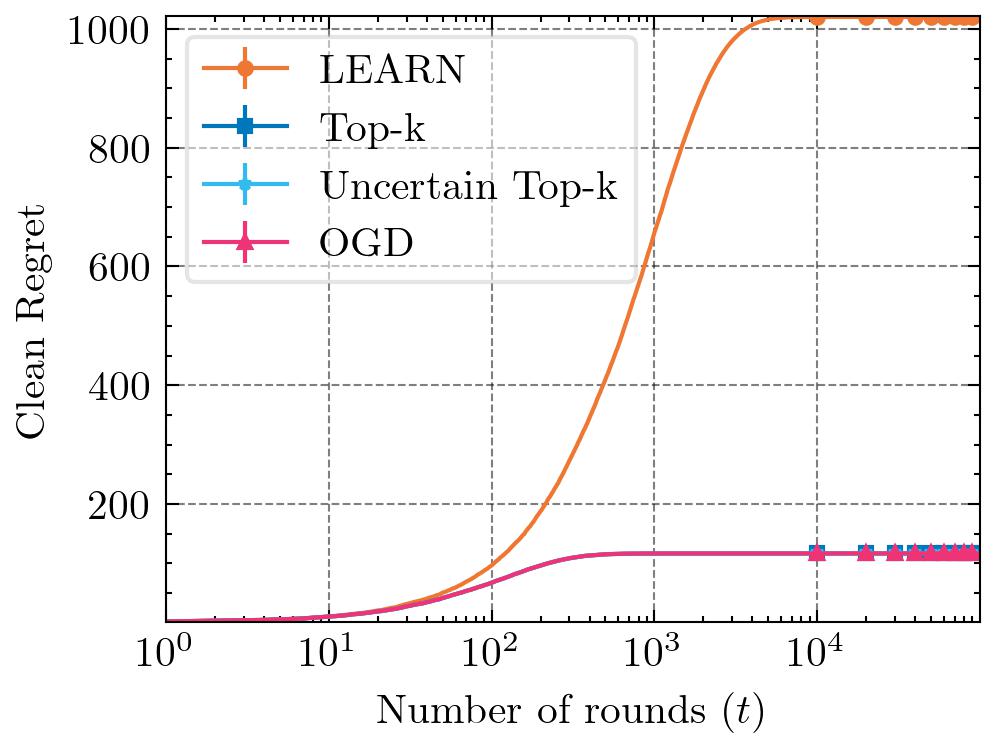

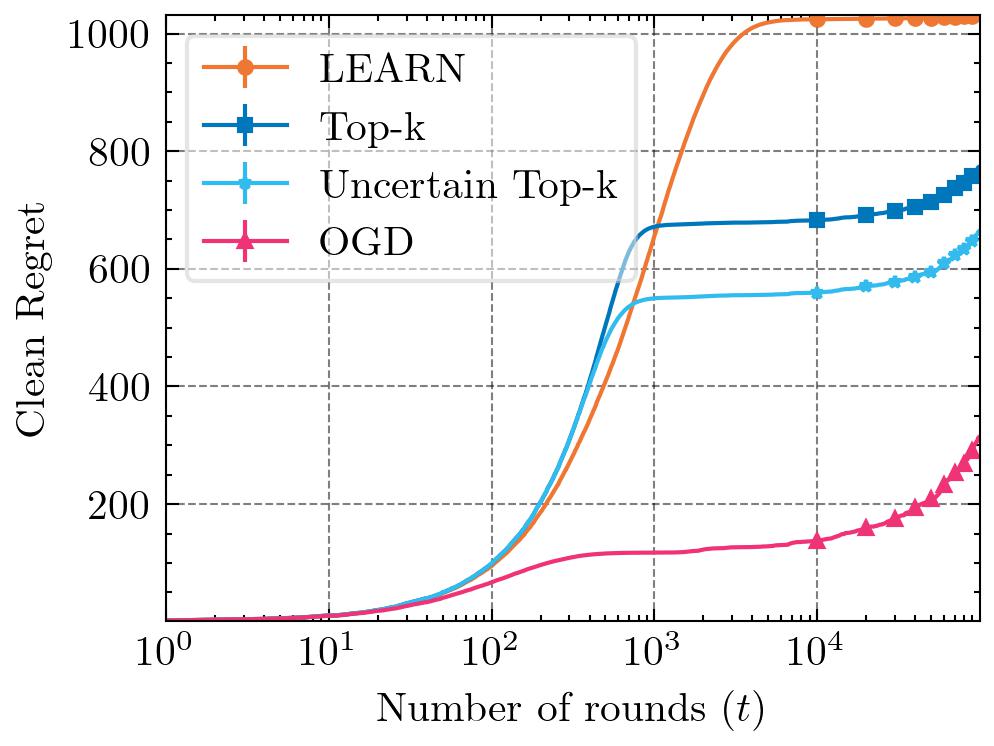

In the absence of outliers (), the results for both online linear regression (Figure 2(a)) and Online SVM (Figure 2(e)) illustrate a significant gap in the cumulative clean regret of Learn compared to other baselines. Learn is intentionally designed to anticipate outliers in the data, leading to cautious and slow updates initially, resulting in a substantial accumulation of regret in the beginning. However, the regret plot for Learn levels off after the initial few rounds. As the number of outliers increase (Figures 2(b) and 2(c) for online linear regression and Figures 2(f) and 2(g) for online SVM), the performance of all methods, except Learn, deteriorates significantly. Although OGD initially incurs small regret, its growth rate is the largest, implying that it will eventually surpass other methods. Learn, on the other hand, maintains roughly the same regret until . This demonstrates Learn’s robustness to outliers, even with higher outlier proportions. These observations corroborate our result in equation (70) of Theorem 3.3, which predicts sublinear behavior for sublinear . Lastly, recall that with , equation (70) in Theorem 3.3 does not assure sublinear regret. Correspondingly, Learn and other methods exhibit increasing regrets in this regime.

5 Conclusion and future work

In this work, we established tight dynamic regret guarantees within the robust OCO framework. Introducing the Learn algorithm, we showcased its effectiveness in handling outliers even when the outlier count remained unknown, particularly when the loss functions are -strongly convex. Moreover, our algorithm worked with unbounded domains and accommodated large gradients. Central to our algorithm, we employ Learn loss , an invex robust loss designed to diminish the influence of outliers during gradient descent style updates. Additionally, we formulated a unified analysis framework to develop online optimization algorithms tailored for a class of non-convex losses referred to as invex losses. This framework serves as the basis for obtaining regret bounds associated with the Learn loss. To substantiate our theoretical findings, we also conducted numerical experiments. A few natural extensions of our work include studying the robust loss with dynamic parameters and and leveraging the unified analysis framework to develop novel algorithms for various invex losses. In future, exploring the application of invex losses in online learning beyond the context of handling outliers would be interesting.

References

- Barron, (2019) Barron, J. T. (2019). A general and adaptive robust loss function. In Proceedings of the IEEE/CVF Conference on Computer Vision and Pattern Recognition, pages 4331–4339.

- Beaton and Tukey, (1974) Beaton, A. E. and Tukey, J. W. (1974). The fitting of power series, meaning polynomials, illustrated on band-spectroscopic data. Technometrics, 16(2):147–185.

- Belagiannis et al., (2015) Belagiannis, V., Rupprecht, C., Carneiro, G., and Navab, N. (2015). Robust optimization for deep regression. In 2015 IEEE International Conference on Computer Vision (ICCV). IEEE.

- Bhaskara and Ruwanpathirana, (2020) Bhaskara, A. and Ruwanpathirana, A. K. (2020). Robust algorithms for online -means clustering. In Proceedings of the 31st International Conference on Algorithmic Learning Theory, volume 117 of Proceedings of Machine Learning Research, pages 148–173. PMLR.

- Black and Anandan, (1996) Black, M. J. and Anandan, P. (1996). The robust estimation of multiple motions: Parametric and piecewise-smooth flow fields. Computer Vision and Image Understanding, 63(1):75–104.

- Chang et al., (2018) Chang, L., Roberts, S., and Welsh, A. (2018). Robust lasso regression using tukey’s biweight criterion. Technometrics, 60(1):36–47.

- Chen et al., (2022) Chen, S., Koehler, F., Moitra, A., and Yau, M. (2022). Online and distribution-free robustness: Regression and contextual bandits with huber contamination. In 2021 IEEE 62nd Annual Symposium on Foundations of Computer Science (FOCS), pages 684–695. IEEE.

- D. Hendricks and Wilcox, (2016) D. Hendricks, T. G. and Wilcox, D. (2016). Detecting intraday financial market states using temporal clustering. Quantitative Finance, 16(11):1657–1678.

- Dennis and Welsch, (1978) Dennis, J. E. and Welsch, R. E. (1978). Techniques for nonlinear least squares and robust regression. Communications in Statistics - Simulation and Computation, 7:345–359.

- Diakonikolas and Kane, (2023) Diakonikolas, I. and Kane, D. M. (2023). Algorithmic high-dimensional robust statistics. Cambridge university press.

- Diakonikolas et al., (2022) Diakonikolas, I., Kane, D. M., Pensia, A., and Pittas, T. (2022). Streaming algorithms for high-dimensional robust statistics. In International Conference on Machine Learning, pages 5061–5117. PMLR.

- Fedoryszak et al., (2019) Fedoryszak, M., Frederick, B., Rajaram, V., and Zhong, C. (2019). Real-time event detection on social data streams. In Proceedings of the 25th ACM SIGKDD International Conference on Knowledge Discovery & Data Mining, KDD ’19, page 2774–2782, New York, NY, USA. Association for Computing Machinery.

- Feng et al., (2017) Feng, J., Xu, H., and Mannor, S. (2017). Outlier robust online learning. arXiv preprint arXiv:1701.00251.

- Gokcesu and Gokcesu, (2021) Gokcesu, K. and Gokcesu, H. (2021). Generalized huber loss for robust learning and its efficient minimization for a robust statistics. arXiv preprint arXiv:2108.12627.

- Hampel et al., (2011) Hampel, F., Ronchetti, E., Rousseeuw, P., and Stahel, W. (2011). Robust Statistics: The Approach Based on Influence Functions. Wiley Series in Probability and Statistics. Wiley.

- Hazan, (2023) Hazan, E. (2023). Introduction to online convex optimization.

- Huber, (1964) Huber, P. J. (1964). Robust Estimation of a Location Parameter. The Annals of Mathematical Statistics, 35(1):73 – 101.

- Huber, (1973) Huber, P. J. (1973). Robust regression: asymptotics, conjectures and monte carlo. The annals of statistics, pages 799–821.

- Jacobsen and Cutkosky, (2023) Jacobsen, A. and Cutkosky, A. (2023). Unconstrained online learning with unbounded losses. In Proceedings of the 40th International Conference on Machine Learning, volume 202 of Proceedings of Machine Learning Research, pages 14590–14630. PMLR.

- Kejariwal et al., (2015) Kejariwal, A., Kulkarni, S., and Ramasamy, K. (2015). Real time analytics: algorithms and systems. Proceedings of the VLDB Endowment, 8(12):2040–2041.

- Lozano and Meinshausen, (2013) Lozano, A. C. and Meinshausen, N. (2013). Minimum distance estimation for robust high-dimensional regression. arXiv preprint arXiv:1307.3227.

- Maronna et al., (2006) Maronna, R., Martin, D., and Yohai, V. (2006). Robust Statistics: Theory and Methods. Wiley Series in Probability and Statistics. Wiley.

- Orabona, (2023) Orabona, F. (2023). A modern introduction to online learning.

- Shalev-Shwartz et al., (2007) Shalev-Shwartz, S., Singer, Y., and Srebro, N. (2007). Pegasos: Primal estimated sub-gradient solver for svm. In Proceedings of the 24th International Conference on Machine learning, pages 807–814.

- van Erven et al., (2021) van Erven, T., Sachs, S., Koolen, W. M., and Kotlowski, W. (2021). Robust online convex optimization in the presence of outliers. In Conference on Learning Theory, pages 4174–4194. PMLR.

- Wang et al., (2023) Wang, X., Tu, Z., Hong, Y., Wu, Y., and Shi, G. (2023). Online optimization over riemannian manifolds. Journal of Machine Learning Research, 24(84):1–67.

- Zhang et al., (2015) Zhang, F., Cao, J., Khan, S. U., Li, K., and Hwang, K. (2015). A task-level adaptive mapreduce framework for real-time streaming data in healthcare applications. Future Generation Computer Systems, 43-44:149–160.

- Zhang et al., (2018) Zhang, L., Lu, S., and Zhou, Z.-H. (2018). Adaptive online learning in dynamic environments. In Proceedings of the 32nd International Conference on Neural Information Processing Systems, NIPS’18, page 1330–1340, Red Hook, NY, USA. Curran Associates Inc.

- Zhang et al., (2017) Zhang, L., Yang, T., Yi, J., Jin, R., and Zhou, Z.-H. (2017). Improved dynamic regret for non-degenerate functions. Advances in Neural Information Processing Systems, 30.

Appendix A Related Work

This section provides a detailed overview of closely related lines of research that inform our work.

Outlier Robust Online Learning

Our work builds on the work of van Erven et al., (2021) where they consider the OCO framework when outliers are present. They specifically address the scenario where , the number of outliers, is known in advance, and the adversary can arbitrarily corrupt any of the rounds. The model assumes that inliers have a bounded range (not known), while outliers can extend to an unbounded range. Notably, learner performance is quantified through clean static regret. The core of their algorithm involves the maintaining of top- gradients, triggering updates to the online learning algorithm only when the norm of the gradient is less than 2 times the minimum norm within the top- gradients. They establish robust regret guarantees, offering for convex functions and for strongly convex functions, where represents the norm of the largest gradient considering only clean rounds. Their work, while providing valuable insights, assumes known values for , a bounded domain, and the existence of a Lipschitz bound for clean rounds. In contrast, our work extends beyond these assumptions, particularly focusing on dynamic environments where the number of outliers is unknown, the domain is unbounded, and the losses may not be Lipschitz.

Robust Losses

A pivotal element of our investigation lies in formulating and examining a non-convex robust loss function. To contextualize our work, we highlight pertinent robust losses featured in the existing literature. Notable examples include Huber loss (Huber,, 1964), Tukey’s biweight loss (Beaton and Tukey,, 1974), Welsch loss (Dennis and Welsch,, 1978) and Cauchy loss (Black and Anandan,, 1996) among others, each tailored to address different applications. Huber loss, for instance, strikes a balance between mean squared error and mean absolute error, rendering it suitable for robust regression (Huber,, 1973). Similarly, Tukey’s biweight loss, known for its efficacy in robust regression, provides resistance against outliers through a truncated quadratic penalty (Chang et al.,, 2018). It is worth noting that Tukey’s biweight loss, along with Cauchy and Welsch losses, are non-convex and satisfy the redescending property (Hampel et al.,, 2011). Learn loss also shares this attribute. For a detailed comparison of Learn loss with different robust losses see Appendix C. Various generalizations and extensions of these losses have been studied (Barron,, 2019; Gokcesu and Gokcesu,, 2021), reflecting the extensive exploration and adaptation of robust loss functions within the broader literature.

OCO with unbounded domains and gradients

It was only in the recent work of Jacobsen and Cutkosky, (2023) that a sublinear regret guarantee was achieved by avoiding the assumption that there exists for all rounds . They obtain sublinear regret guarantees in the standard OCO framework when the domain is unbounded, and the gradients grow large with the norm of actions (). They provide the first algorithm for dynamic regret minimization in the unbounded domain and gradient setup. In this work, we adopt an expert scheme akin to theirs to handle unbounded domains and gradients that can grow large in the robust outlier framework.

Related Applications

The work of Chen et al., (2022) studies online linear regression within a realizable context, accounting for small noise using the Huber contamination model (Huber,, 1964). However, our model (similarly the model of van Erven et al., (2021)) differs from theirs significantly. Notably, we do not impose any assumptions of realizability or control the corruption mechanism through probabilistic assumptions. Although distinct in the techniques employed, it is important to acknowledge a substantial body of related work addressing robust optimization in various theoretical computer science and machine learning problems. For a comprehensive overview, the textbook authored by Diakonikolas and Kane, (2023) stands out as an excellent reference.

Appendix B Dynamic Regret in a Bounded Domain Using Top-k Filter Algorithm

van Erven et al., (2021) established a tight bound on static regret within a bounded domain, assuming prior knowledge of . For convex losses, they achieved an optimal static regret upper bound of . In the case of strongly convex losses, this bound is further improved to , which remains optimal. In this section, we extend their results to the dynamic setting and establish a clean dynamic regret bound of within a bounded domain. Notably, this bound remains tight even for strongly convex functions (Zhang et al.,, 2017).

We make the following assumptions for our extension:

-

1.

The Lipschitz-adaptive algorithm ALG used by van Erven et al., (2021) is online gradient descent (OGD).

-

2.

The domain is bounded.

Let be the set of uncorrupted rounds. Then, we are interested in bounding the clean dynamic regret defined as:

| (19) |

Let denote the rounds flitered out by Algorithm 1 in van Erven et al., (2021), and let denote the rounds that are passed on to ALG. Then,

| (20) |

First, we bound .

| (21) |

The bound for the term follows directly from van Erven et al., (2021)’s proof of their Theorem 1:

| (22) |

where and .

Similarly, we take the bound for directly from van Erven et al., (2021)’s proof of Theorem 1:

| (23) |

At this point, it only remains to bound . Recall that OGD (instantiation of ALG) only sees the rounds in , and by reindexing them as , we can write for all :

| (24) |

Expanding RHS and by definition of , we have:

| (25) |

Now, substituting and using the contractive property of the projection on a convex set, we can write:

| (26) |

Simplifying,

| (27) |

Taking and using the convexity of , we get:

| (28) |

Summing it across all :

| (29) |

We make two observations:

-

1.

- due to van Erven et al., (2021)

-

2.

We choose to get:

| (30) |

Combining all the above results together, we get

| (31) |

Appendix C Comparison of Robust Losses

To understand how the robust loss works to mitigate its susceptibility to outliers, we examine the behavior of different non-convex losses, including our robust loss. We compare how these losses resemble the square loss near the origin and observe their behavior as we deviate from it.

Let us consider the square loss function where denotes the residual, and the minimum is attained at . Our robust loss, denoted by , instantiated with with constants and , is represented in the Figure 3. Note that closely follows the behavior of the function in the vicinity of the origin and gradually levels off as we move away from it. Importantly, the minimizers for both and are the same.

In Figure 3, we plot two other non-convex losses that are similar in appearance to our robust loss. First, we examine Tukey’s biweight loss, defined as

| (34) |

where denotes the residual and is a tunable parameter. We observe that, even when tuning the parameter to both high and low values, the curve fails to closely follow the curvature of the square loss, contrasting with the behavior of our robust loss. Moving away from the origin, Tukey’s loss flattens out at a slower when compared to .

Next, we consider the Welsch loss defined as

| (35) |

Here, the tunable parameter is set to in Figure 3. However, its limitation of being capped at one impedes its ability to track the underlying square loss precisely. This causes it to flatten out early, making it less suitable for online learning. These observations shed light on the distinctive characteristics of these losses and underscore the efficacy of our proposed robust loss in capturing the desired behavior.

Appendix D Invexity of the Robust Loss

D.1 Proof of Lemma 3.1

Proof.

To prove that is a -invex function, it suffices to show that all its stationary points are the global minima. Using the monocity of and functions, it follows that

| (36) |

Due to the convexity of , either or does not have any stationary point. Now,

| (37) |

It is obvious that if and only if . This immediately implies that is invex. Equivalently, there exists a function such that

| (38) |

Again, employing the monocity of and functions,

| (39) |

Let

Observe that as a consequence of . Next, we analyze the following quantity:

| (40) | ||||

| (41) | ||||

| (42) | ||||

| (43) | ||||

| (44) | ||||

| (45) | ||||

| (46) |

A note on the nondifferentiability of

In the scenario of a nondifferentiable yet convex function , the first-order optimality condition implies , where denotes the subdifferential set. It’s worth noting that the assertion immediately following equation (37) remains valid, taking into account the condition . ∎

D.2 Proof of Theorem 3.2

Proof.

We establish that our problem’s setting satisfies the necessary conditions to apply the unified analysis framework detailed in Appendix E. Using the Euclidean distance as our distance function , it is straightforward to verify that Assumption E.8 holds, with and . The assumption of a bounded domain, Assumption E.9, remains valid when substituting with .

Next, we verify Assumption E.10.

| (47) | ||||

| (48) | ||||

| (49) | ||||

| (50) |

where inequality (48) follows from the contraction of the projection on a convex set and is defined in the proof of Lemma 3.1. Using the results from Lemma 3.1, we can verify that the Assumption E.10 holds with and . Now, observe that . By choosing a constant step size for all and using the results from Theorem E.11, we obtain the following regret bound:

| (51) |

We observe that and then apply Lemma H.2 to write:

| (52) |

where is defined in Lemma H.2 and optimal path variation . By choosing,

| (53) |

we get

| (54) |

∎

Appendix E A Unified Framework to Bound Dynamic Regret for Online Invex Optimization

In this section, we develop a unified framework to bound dynamic regret for invex losses using a first-order algorithm. First, we present some definitions and assumptions which will be used later to construct our framework.

Definition E.1 (Invex functions).

A differentiable function is called a -invex function on set if for any and a vector-valued function ,

| (55) |

where is the gradient of at .

Remark E.2.

Conventionally, the notation is employed instead of within the definition of an invex function. The preference for in our work arises from the prior use of for a distinct purpose elsewhere in our paper.

Remark E.3.

When working in a non-Euclidean Riemannian manifold the inner product will be defined in the tangent space of induced by the Riemannian metric.

Remark E.4.

The choice of may not be unique.

Definition E.5 (First-order Algorithm).

We denote an algorithm as , where, at round , it accepts the current iterate , gradient , stepsize , and the function as inputs, and produces the next iterate as its output.

Definition E.6 (Distance function).

The function is called a distance function.222This concept can be extended to encompass non-Euclidean manifolds. Specifically, one can engage with Hadamard manifolds, taking into account geodesically convex functions.

Remark E.7.

Although can represent a metric associated with a metric space, we do not explicitly impose this requirement.

We consider an online invex optimization (OIO) framework akin to OCO where the learner engages in a sequential decision-making process. Specifically, in each round , the learner selects an action and observes a -invex loss denoted as . Subsequently, the learner employs a first-order optimization algorithm, denoted as , to perform the next action . All the procedural details of this algorithm are presented in the following section.

The learner aims to minimize the dynamic regret as defined below:

| (56) |

where and .

In this section, we use the variable with subscripts and superscripts to signify positive and finite () parameters. With this notational clarification, we are prepared to enumerate the assumptions essential for our setup.

Assumption E.8 (Generalized Law of Cosines).

For all , the distance function satisfies the following inequality:

| (57) |

Assumption E.9 (Bounded domain).

For all ,

| (58) |

Assumption E.10 (First-order update property).

Let be the chosen action at round and , then

| (59) |

Now, we are ready to state our theoretical result.

Theorem E.11.

Proof.

By substituting, and in Assumption E.8, we get:

| (61) | ||||

| (62) |

where inequality (62) follows from Assumption E.9. Next, we bound using Assumption E.10 and get:

| (63) | ||||

| (64) |

We get the following after rearranging the terms:

| (65) |

Recall that due to -invexity of , we have

| (66) |

The corollary below shows an explicit bound on by appropriately choosing .

Corollary E.12.

Let , and for all in Theorem E.11. Furthermore, define . If the learner chooses such that

| (68) |

then the following regret guarantee holds:

| (69) |

Observe that if , then .

Appendix F Bounds on the Clean Dynamic Regret in a Bounded Domain

F.1 Proof of Theorem 3.3

Proof.

Consider . We start our proof by analyzing the following quantity:

| (70) | ||||

| (71) | ||||

| (72) |

Observe that Q1 can be further decomposed as below.

| (73) | ||||

| (74) | ||||

| (75) | ||||

| (76) |

The first inequality (74) follows due to the contraction of the projection on the convex sets. We substitute inequality (76) in inequality (70) while keeping track of corrupted and uncorrupted rounds.

First, using convexity of for uncorrupted samples, i.e, , we get

| (77) |

and using Cauchy–Schwarz inequality for corrupted samples, i.e., for , we get

| (78) |

Using the results from Lemma H.2, we can bound:

| (79) |

To bound the last term of inequality (F.1) consider the term for some .

| (80) | ||||

| (81) | ||||

| (82) | ||||

| (83) |

Next, we will bound the term .

Using the results from lemma H.1 with and ,

| (84) | ||||

| (85) |

Thus,

| (86) |

Now we are ready to establish the sublinear bound on the clean dynamic regret.

We consider . Observe that, and for uncorrupted rounds. Summing up and telescoping inequalities (F.1) and (F.1) from , we get

| (87) | ||||

Furthermore, observe that . Thus,

| (88) | ||||

By choosing,

| (89) |

we get

∎

Appendix G Bounds on the Clean Dynamic Regret in Unbounded Domain

G.1 Formal Statement for Theorem 3.5

Theorem G.1.

For each , let be a sequence of -strongly convex loss functions with possible of them corrupted by outliers. We assume that the loss for uncorrupted rounds falls within the range , whereas the loss for corrupted rounds can be unbounded. Let be a sequence of actions chosen by the learner using Algorithm 2 with parameters for the experts chosen from as defined in equation (12). Let . The following regret guarantees hold:

-

•

If and , then

(90) -

•

If and , then

-

•

If and , then

-

•

If , then

(91) -

•

If , then

(92)

G.2 Proof of Theorem 3.5

Proof.

Let be a sequence of actions chosen by the expert . Observe that for any expert ,

| (93) | ||||

| (94) |

The proof unfolds in four major steps:

-

1.

Define . If for any specific expert , we establish that is bounded.

-

2.

Demonstrate that remains bounded when .

-

3.

Establish the bound on when .

-

4.

Conclude the proof by deriving a bound on when .

First, we bound the meta regret in a bounded domain using the following lemma.

Lemma G.2.

Let for some expert . Then,

| (95) |

We use the result from Lemma 3.4 to bound the expert regret. In the next lemma, we will bound the clean dynamic regret when is too large.

Lemma G.3.

Let and are a sequence of functions satisfying inequality (2), then

| (96) |

Finally, we will show that clean dynamic regret is bounded even when is too small.

Lemma G.4.

Let , then the following regret guarantee holds:

| (97) |

The final step is to bound the dynamic regret when , then it must be that for some expert ,

The optimal would be

| (98) |

If , we choose , which results in the dynamic regret:

Similarly, if , we choose , which results in the dynamic regret:

If falls between , then there exists an such that . We pick this and bound the dynamic regret as:

∎

G.3 Proof of Lemma G.2

Proof.

We proceed with the proof by analyzing the following quantity.

| (99) | ||||

| (100) | ||||

| (101) | ||||

| (102) | ||||

| (103) | ||||

| (104) | ||||

| (105) |

Using convexity of for uncorrupted samples, i.e, for ,

| (106) |

Similarly, for corrupted samples, i.e., ,

| (107) |

Now, we follow the same argument as the dynamic regret bound in Theorem 3.3 and end up with the following bound:

| (108) |

where . The above expression can be further simplified to:

| (109) |

∎

G.4 Proof of Lemma 3.4

Proof.

Recall from Algorithm 2 that,

| (110) | ||||

| (111) | ||||

| (112) |

Furthermore, using the definition of :

| (113) | ||||

| (114) | ||||

| (115) | ||||

| (116) |

Now, consider

| (117) | ||||

| (118) |

Note that the following inequality holds for any random variable and :

| (119) |

Consider . Also, observe that . Thus,

| (120) |

Using the convexity of ,

| (121) |

If round is corrupted, then

| (122) |

Summing through to , we get

| (123) |

It follows that,

| (125) |

By picking , we get

| (126) |

∎

G.5 Proof of Lemma G.3

Proof.

In this setting, we provide a trivial bound on dynamic regret (similar to Jacobsen and Cutkosky, (2023)).

| (127) | ||||

| (128) | ||||

| (129) |

Note that due to our construction of set , . Clearly, . Thus,

| (130) |

∎

G.6 Proof of Lemma G.4

Appendix H Useful bounds

Within this section, we derive some critical bounds integral to our analytical framework.

Lemma H.1.

For all and , .

Proof.

We will show that for , holds. Below, we assume and find a range of that satisfies this assumption.

Take . As long as , the above inequality is valid. ∎

Lemma H.2.

Proof.

We begin our proof by analyzing the following quantity.

| (136) |

Note that due to -strong convexity of , we have

| (137) |

where . Observe that . Thus,

| (138) |

This leads to the following inequality:

| (139) | ||||

It follows that,

| (142) |

∎

Lemma H.3.

Appendix I Experimental Validation

In this section, we perform numerical experiments to substantiate our theoretical findings. The experiments were conducted on a MacBook Pro running macOS 14.4.1, equipped with 32 GB of memory and an Apple M2 Max chip.

I.1 Baseline Algorithms

We conduct a comparative analysis, pitting Learn against several baseline algorithms, each serving as a benchmark in our experiments.

-

•

Top-k Filter Algorithm: Developed by van Erven et al., (2021), this algorithm operates under the assumption that the domain of the Online Convex Optimization (OCO) problem and the gradients of the uncorrupted loss functions are bounded. The core concept involves filtering out rounds with the largest gradients, assuming they might be outliers. If any outlier round is not filtered, it does not influence the update too much due to the bounded gradient assumption on the uncorrupted loss. The algorithm requires precise knowledge of and provides an bound on clean static regret under the bounded domain and Lipschitz gradient assumption. While this algorithm is analyzed for static regret, it can be extended easily to the setting of dynamic regret.

-

•

Uncertain Top-k Filter Algorithm: We devise a variant of the Top-k filter algorithm equipped with an estimate of the number of outliers. This estimate was fixed at . It is important to emphasize that this manufactured algorithm does not come with any accompanying theoretical guarantees.

-

•

Online Gradient Descent (OGD) Algorithm: As our third baseline, we select OGD, a workhorse for many machine learning problems. OGD operates without explicit consideration of the presence of outliers.

In the absence of outliers, all baselines converge to Online Gradient Descent (OGD). It is imperative to note that none of these methods provide theoretical guarantees in an unbounded domain with outliers. Despite the absence of theoretical guarantees, we selected these algorithms as baselines due to a shortage of alternatives that effectively address both unbounded domains and robustness to outliers.

I.2 Online Support Vector Machine

In our initial experimental configuration, we conducted a comparative analysis of Learn against other baseline methods for a classification problem, employing soft-margin Support Vector Machines (SVM) in an online setting. The specifics of the experimental setup are detailed below:

Uncorrupted Data Generation

In our experiments, the data for uncorrupted rounds () was generated following a specific data generation process:

| (149) |

Here, the entries of were uniformly drawn at random from the interval . Note that is the side information in this case. The entries of for uncorrupted rounds were independently drawn from a normal distribution . To allow for some mislabeling, the label of a round was flipped with a probability of if .

Corrupted Data Generation

In the experimental setup, we executed a total of rounds, allowing the adversary the flexibility to corrupt any out of the rounds, with the choice made uniformly at random. The experiments encompassed scenarios where took on values from the set .

For the corrupted rounds, the labeling process involved flipping the label, specifically by setting .

Strongly Convex Loss Function

Drawing inspiration from Shalev-Shwartz et al., (2007), we adopted a fixed loss function for each round, defined as:

| (150) |

Similar to Shalev-Shwartz et al., (2007), we set the parameter to . To maintain an unbounded domain for , we considered it as belonging to 2. It should be noted that in a noiseless setting with sufficiently small , dynamic optimal actions match the ground truth .

Choice of Parameters

In the case of Learn, the parameter was set to , while was maintained at . This selection was determined through a grid search across a small range of values. We did not undertake specific tuning efforts for optimality. Across all methods, including both baselines and Learn, a consistent step size of was employed.

Results

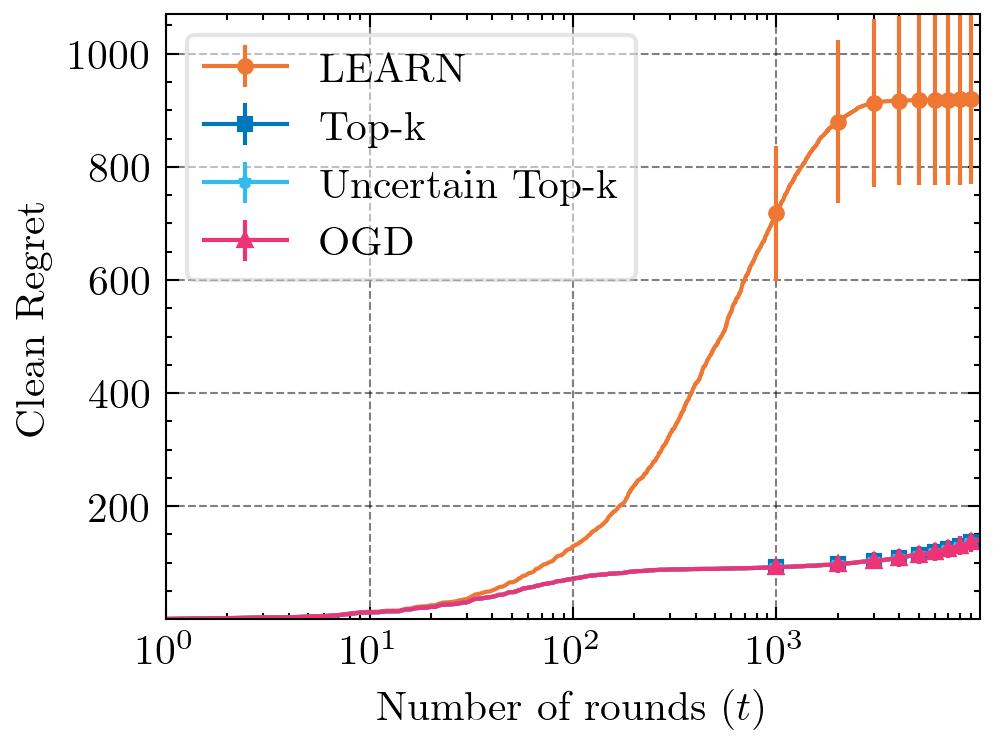

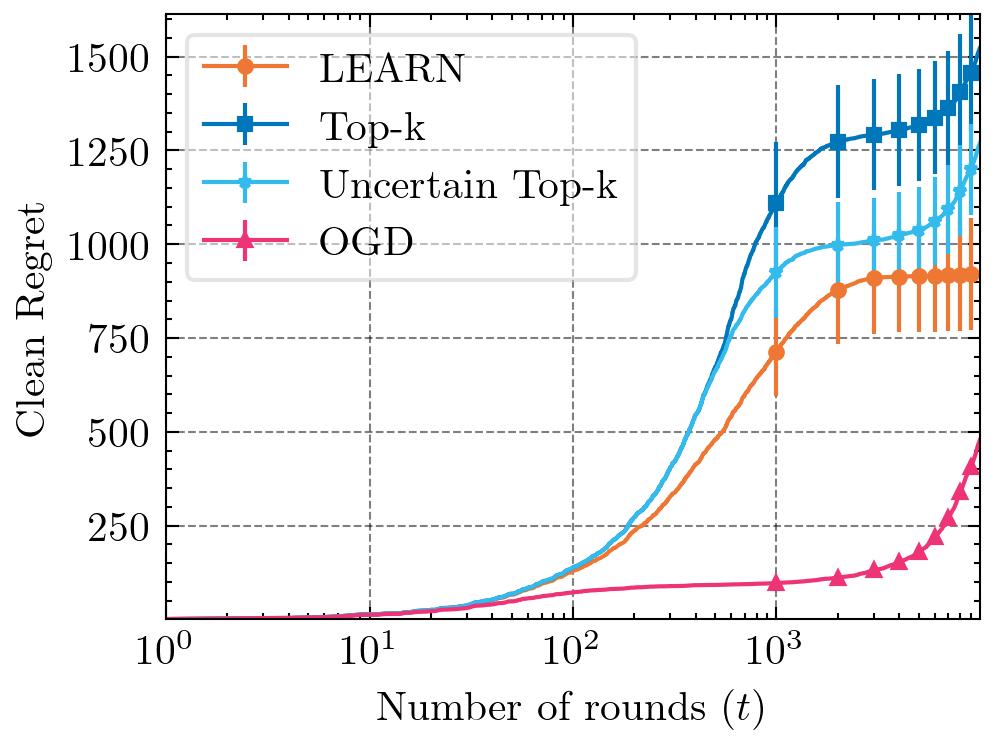

The experiments were executed across 30 independent runs, and the outcomes are presented in Figure 4. Referring back to Theorem 3.5, we anticipate the clean regret to vary in the order of . This implies sublinear regret for Learn until and constant regret when . The same behavior can be observed from the plots in Figure 4. The empirical observations derived from the experiment are outlined below:

-

•

Learn adopts a cautious updating strategy in the uncorrupted regime: This is illustrated by the observed gap in clean regret in Figure 4(a). In this context, the clean regret for other baselines flattens at a significantly lower value compared to Learn. This behavior stems from Learn’s inherent cautious update mechanism, specifically designed to anticipate the presence of corrupted rounds. Consequently, Learn experiences a substantial accumulation of regret initially, navigating a careful trajectory until it converges to the optimal action, leading to the eventual flattening of the regret curve.

-

•

Learn exhibits robustness to outliers: With an increasing value of , the performance of the baselines markedly deteriorates, while Learn remains relatively unaffected until Figure 4(d). This is evident when inspecting the maximum regret values across various curves. For Learn, the maximum regret hovers around until Figure 4(d), whereas other baselines experience a steep surge in regret in the presence of outliers.

-

•

Learn is good at capturing the underlying ground truth: In cases where the data adheres to a specific generating process, the presence of a flat curve indicates convergence to the optimal action (). Remarkably, Learn maintains a flat region in Figures 4(a) to 4(c) even in the presence of outliers, showcasing its ability to learn and adapt to the true underlying dynamics. In contrast, other methods falter in achieving this sustained flatness. Upon closer examination of the rate of growth, it becomes apparent that OGD is particularly susceptible to the disruptive influence of outliers.

- •

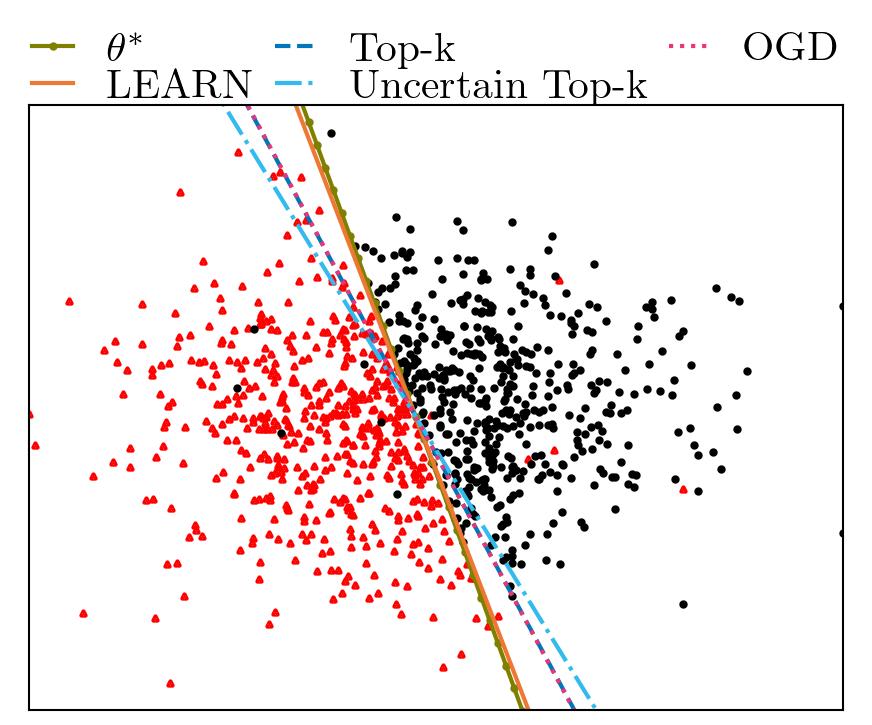

Visualizing the Decision Boundary

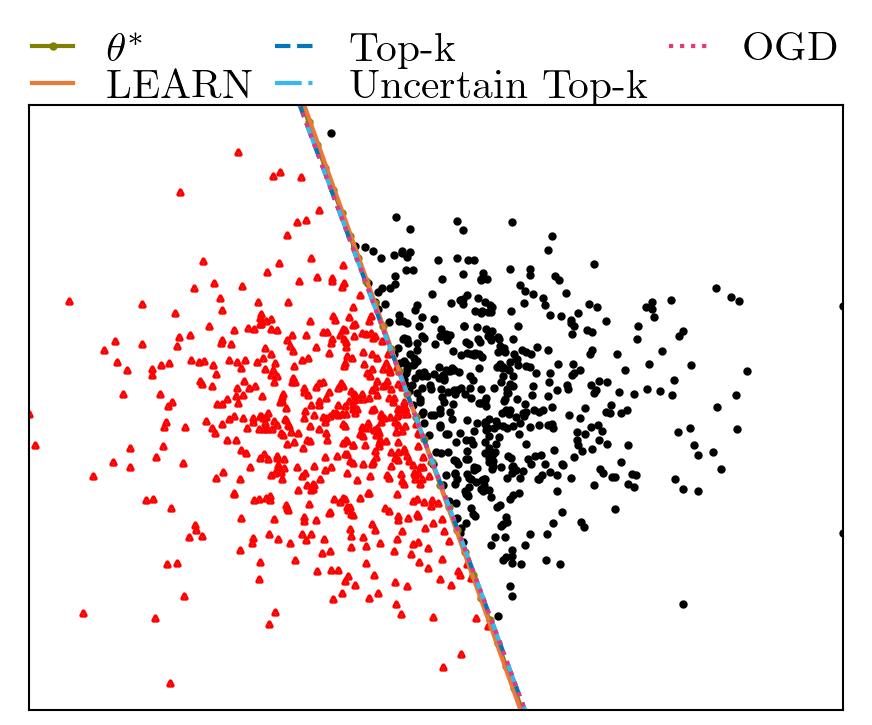

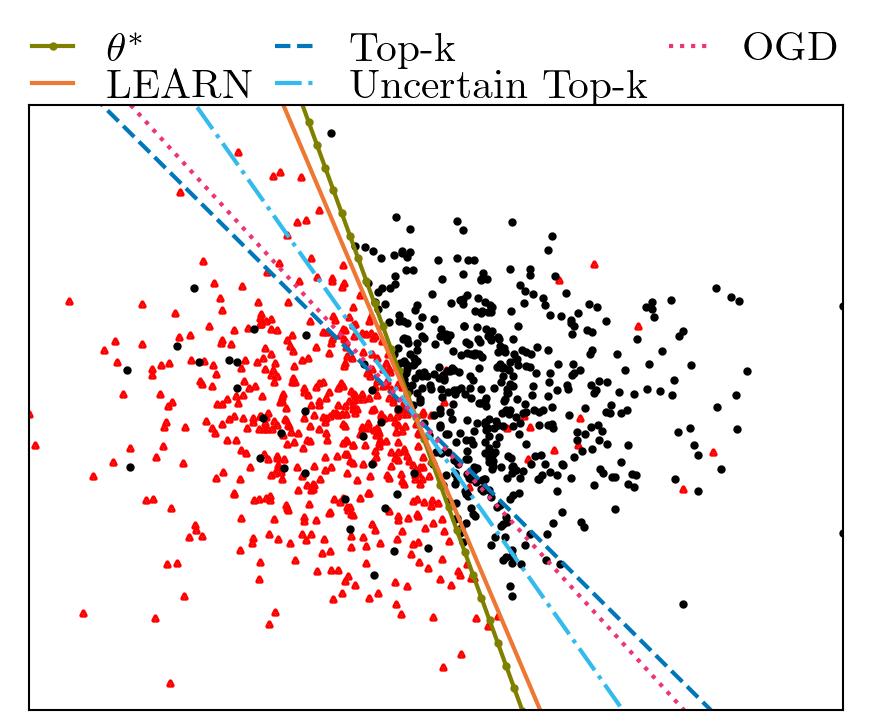

As the data (side information) adheres to a noiseless generative model, the online SVM problem can be thought of as a learning task where the objective is to learn the classification parameter . The decision boundaries learned by different methods with varying numbers of outliers are illustrated in Figure 5 for a single run. The decision boundary for (plotted as ) is also depicted. To enhance clarity, only rounds out of the total rounds are randomly selected for plotting.

In scenarios with uncorrupted data, all methods accurately learn . However, as the number of corrupted rounds increases, the decision boundaries for other baselines gradually deviate from the optimal boundary. In contrast, Learn exhibits robustness against outliers, maintaining a decision boundary close to the optimal configuration even in the presence of corrupted data.

I.3 Online Linear Regression

In our subsequent experimental setup, we undertook a comparative analysis, juxtaposing the performance of Learn against other baseline methods for a regression problem. Specifically, we explored the online ridge regression setting. The details of this experimental configuration are elaborated below:

Uncorrupted Data Generation

The data for uncorrupted rounds () adhered to a specific data generation process:

| (151) |

In this context, the entries of were uniformly drawn at random from the interval , followed by normalization to a unit norm. Note that is again the side information. The entries of for uncorrupted rounds were independently drawn from a normal distribution . Additionally, a small additive noise was independently chosen from .

Corrupted Data Generation

We conducted a total of rounds, providing the adversary with the flexibility to corrupt any out of the rounds, with the choice made uniformly at random. The experiments covered scenarios where assumed values from the set . In the context of corrupted rounds, was chosen uniformly at random from the interval .

Strongly Convex Loss Function

We employed the following fixed loss function for each round:

| (152) |

The parameter was set to . To enforce an unbounded domain for , we considered it to be an element of 100. In each round, the comparator was selected by minimizing the function as defined in Equation (152). Although it may not precisely match the ground truth due to the low influence of additive noise, our experimental results indicate its proximity to .

Choice of Parameters

In the context of Learn, the parameter was set to , and was held at . Once again, this choice resulted from a grid search across a limited range of values, with no dedicated tuning efforts for optimality. Consistently, across all methods, including both baselines and Learn, a uniform step size of was utilized.

Results

The experiments were executed across 30 independent runs, and the outcomes are presented in Figure 6. The results show the similar behavior as in the case of online SVM. We recall them here in the context of ridge regression:

-

•

Similar to Section I.2, Learn again employs a cautious update strategy, evident in the gap in clean regret in Figure 6(a). Unlike other baselines, Learn accumulates initial regret due to its cautious update mechanism designed for anticipating corrupted rounds, leading to slow flattening of the regret curve.

-

•

In the presence of outliers (until Figure 6(d)), Learn remains robust, maintaining a maximum regret around , while other baselines experience a sharp surge in regret.

- •

- •

Discussion on the choice of the step size for baselines

To clarify our choice of step size in the experiments: while it is theoretically possible to set given that the losses are -strongly convex, we encountered a situation where the value of was extremely small (). This led to an excessively large step size, causing the anticipated regret bound of to become quite substantial. Upon numerical evaluation, we found that using produced a significantly smaller regret for the baselines. As a result, we adopted this more favorable step size in our experimental framework.