[Set of all natural numbers excluding zero]naN \newsym[Set of all natural numbers including zero]nawzNew A_0 \newsym[Set of all real numbers]reR \newsym[Set of all nonnegative real numbers]replus\re_+ \newsym[Base -field]FcalF \newsym[Base filtration]FFF \newsym[Base probability measure]PPP \newsym[Alternative probability measure]QQQ \newsym[Borel -field]BB \newsym[Topology]TT \newsym[Space of all real valued semimartingales]SMS \newsym[Space of all real valued caglad processes]LDL \newsym[Space of all real valued cadlag processes]DDD \newsym[Set of controls]MMM \newsym[Set of controlled processes]CPNN(Θ, ψ) \newsym[Process that generates the (augmented) base filtration]YY \newsym[Integrands, trading strategies]XX \newsym[Semimartingale integrators]SIS \closesymdef \setkomafontdisposition

Reinsurance with Neural Networks

Zusammenfassung

We consider an insurance company which faces financial risk in the form of insurance claims and market-dependent surplus fluctuations. The company aims to simultaneously control its terminal wealth (e.g. at the end of an accounting period) and the ruin probability in a finite time interval by purchasing reinsurance. The target functional is given by the expected utility of terminal wealth perturbed by a modified Gerber–Shiu penalty function. We solve the problem of finding the optimal reinsurance strategy and the corresponding maximal target functional via neural networks. The procedure is illustrated by a numerical example, where the surplus process is given by a Cramér–Lundberg model perturbed by a mean-reverting Ornstein–Uhlenbeck process.

Keywords: Optimal control Reinsurance Deep learning Cramér–Lundberg model Perturbed risk process Gerber–Shiu penalty function Ruin probability Multi-objective optimization Binary classification Pareto front

MSC2020: 68T07 91G05 91G60

1 Introduction

In 1903 Filip Lundberg suggested to model the surplus of an insurance company by a constant drift minus a compound Poisson process with iid almost positive jumps (Lundberg, 1903). The drift is interpreted as the premium rate, the jumps represent the claim sizes, whereas the Poisson process counts the claims. This setting, widely known as the classical risk model or Cramér–Lundberg model, gives a clear but simplified picture of the insurer’s balance.

For an insurance company, claims are not the only source of uncertainty. For example, the increase or decrease in the number of customers (see Braunsteins and Mandjes (2023)) or a random interest rate (see Eisenberg (2015)) will impact the risk process. Also, reputational considerations, investments in positively correlated financial markets, and correlations between different business branches and collectives of insured will play a considerable role. Recently, one started to consider models involving a dependence between the actuarial business and financial markets offering investment possibilities, see, for instance, Ceci et al. (2022), Leimcke (2020) and references therein.

An important modification of the classical risk model is due to Gerber (1970), who suggested to include an additional source of uncertainty — a Brownian motion. This new, perturbed classical risk model can better account for reality while still being a one-dimensional Markov process. The latter property makes the perturbed process a popular model for the surplus of an insurance company, see, for instance, Dufresne and Gerber (1991), Tsai (2001), Cheung and Liu (2023) and references therein.

However, by adding an additional source of uncertainty, in many optimisation settings, the calculations and proofs become much more complicated, resulting in the use of the viscosity approach, see for instance Eisenberg (2015). The viscosity approach allows to find the optimal strategy numerically, since the corresponding Hamilton–Jacobi–Bellman equation can be tackled using the finite difference method. To avoid this approach, one may discretize the surplus process, thereby allowing controls only at discrete time points. In particular, for a finite time horizon, this method has the advantage that all control strategies can be written in feedback form, i.e. depending on the finite number of the observed state values.

In actuarial control theory, after the model for the surplus has been chosen, the question arises which risk measure will be considered as a target to optimize. The most famous and extensively studied risk measure, suggested by Lundberg (1903), is the ruin probability, i.e. the probability that the surplus becomes negative in finite time. A vast number of results have appeared over the last century concerning the minimisation of the ruin probability in different settings. We refer the interested reader to Schmidli (2008), Asmussen and Albrecher (2010) and references therein. Alternative risk measures that have been considered over the last decades include in particular expected dividends, expected utility of terminal wealth, and expected capital injections, see, for instance, Albrecher et al. (2017), Avanzi (2009), Albrecher and Thonhauser (2009) and references therein.

Measuring the utility of the terminal wealth was first suggested by Borch (1961) and had since become one of the most important risk indicators in insurance mathematics. The wealth at some finite time — for instance, the time of a regulatory check, can provide useful clues about the company’s wellbeing. Including the ruin probability into the target functional has been considered for instance in Hipp (2018), where the main target is to maximize dividends, or in Thonhauser and Albrecher (2007), where the time value of ruin is taken into account. However, the multi-objective goal of simultaneously optimizing a risk measure (such as, in our case, the expected utility of terminal wealth) along with the ruin probability remains largely unexplored.

In the present manuscript, we look at a very general extension of the perturbed risk model that has not been considered before. The surplus of an insurance company is modelled by a jump process perturbed by a general diffusion (not necessarily a Brownian motion) on an interval with a deterministic time horizon . This implies that the problem we consider is 3-dimensional and depends on the time to maturity, on the state of the jump process and on the state of the diffusion. The functional to maximize is given by the expected utility of terminal wealth perturbed by a modified Gerber–Shiu (Gerber and Shiu, 1998) penalty function. It is optimized over the class of reinsurance policies, which are arguably the most popular type of controls in the literature (with investments, dividends and capital injections being common alternatives). A substantial body of literature exists on utility maximization and ruin minimization with reinsurance strategies, with notable contributions including Schmidli (2002), Promislow and Young (2005), Bai and Guo (2008), Schmidli (2001) and Taksar and Markussen (2003).

The role of the penalty function in this paper is twofold. It rewards the insurer if the surplus remains positive at all times (i.e. in the case of no ruin), while a negative surplus is penalised. In addition, one can opt for different weights for the expected utility and for the penalty function, depending on the individual preferences of the insurer. It means, we allow the insurer to prioritize their immediate needs: higher utility of the terminal surplus with higher risk or a more safer play.

As it seems unlikely that this problem can be solved explicitly, we seek for the optimal strategy in the class of feedback controls using machine learning techniques. More specifically, we use neural networks. Neural networks have become a popular tool in actuarial risk management, having been applied to mortality modelling, claims reserving, non-life insurance pricing and telematics. For a survey on recent advances of artificial intelligence in actuarial science, see Richman (2021) and references therein.

The task of finding optimal reinsurance (and dividend) strategies with neural networks has been studied in Cheng et al. (2020) and Jin et al. (2021). There, the authors develop a hybrid Markov chain approximation-based iterative deep learning algorithm to maximize expected dividends under consideration of the time value of ruin. In contrast to Cheng et al. (2020) and Jin et al. (2021), we include the ruin probability explicitly as a risk measure (besides the expected utility of terminal wealth) that is optimized. Moreover, we formulate our optimization problem as an empirical risk minimization problem, which can be solved efficiently by stochastic gradient descent methods, even in highly complex model settings.

The primary contributions of this paper are as follows:

-

1.

We introduce a novel framework for optimizing reinsurance strategies using deep learning techniques in order to maximize a target functional comprising a utility function penalized by an extended Gerber–Shiu function. The proposed method allows the insurer to balance between maximizing the expected utility of terminal wealth, and minimizing the probability of ruin.

-

2.

By drawing connections to binary classification problems and surrogate loss functions, we demonstrate how the optimization problem can be solved by empirical risk minimization, a method that, when combined with stochastic gradient descent, is particularly useful for optimizing neural networks.

-

3.

We illustrate our proposed methodology by a numerical example, where the surplus process is given by a Cramér–Lundberg model perturbed by a mean-reverting Ornstein–Uhlenbeck process. Our findings demonstrate the effectiveness of our method in finding optimal reinsurance strategies, and highlight the large scope of the approach.

2 Model description

We consider an insurer with a deterministic finite planning horizon . The insurer manages a portfolio of risks that generate premium payments. To mitigate potential large financial losses from unexpectedly high claim frequencies or sizes, the insurer can enter into reinsurance agreements. For a given number of time steps , these agreements are re-negotiated at time points , for the coverage period , where we set .

Our study is based on a probability space . The flow of information is modeled by an -valued stochastic process , where is a fixed dimension. The process induces a filtration of , allowing for the possibility that . That is, there might be some information that does not reveal itself even at maturity . We assume that is endowed with the Borel--field . All stochastic processes are indexed via the discrete time points .

Let denote the -adapted premium process. The payment ensures insurance coverage over the period . As in our numerical illustrations in Section 4, might be computed according to the expected value principle with a positive safety loading. Alternatively, can be calculated using any other known premium calculation principle such as, for instance, the standard deviation or zero-utility principle. The premium may also depend on the number and size of the previously occurred claims. However, for the sake of clarity, we concentrate on the expected value principle in order to better explain the features of our model, and leave further extensions to future research. Since the time horizon is assumed to be finite, we may assume, without loss of generality, that .

Inspired by the Cramér–Lundberg model, let be an -adapted, -valued and increasing process with , and represents the number of claims up to time . The -valued insurance claims are denoted by . We also consider a real-valued, -adapted process which represents random fluctuations, such as small claims and variations in premium income.

Remark 2.1.

A distinguishing feature is that , , and are not assumed to be independent.

The reinsurance agreement is characterized by a reinsurance strategy . For illustrative purposes, we assume the agreement to be proportional, that is, is an -adapted process with values in . Here, represents the retention level, and is the proportion of claims covered by the reinsurer during the period . For notational convenience, we set . The reinsurance premium is given by the process . We assume that for some continuous cost function .

For each reinsurance strategy , the surplus process is defined by , and

| (1) |

where is the initial capital. The surplus process without reinsurance is denoted .

The insurer’s preference is described by a continuous utility function . Here, we assume that the utility function is chosen such that is finite. For example, in Section 4 we will choose an exponential utility function in conjunction with exponentially distributed claims. If one were to choose Pareto-distributed claims – a popular choice in the literature – then another utility function is required due to the heavy tails of the Pareto distribution.

Definition 2.2.

A reinsurance strategy is called admissible, if is finite. The set of all admissible reinsurance strategies is denoted by .

In our model, the insurer aims to optimize the expected utility of terminal wealth while considering the probability of ruin across all admissible reinsurance strategies. This is done by incorporating a penalty term whose strength is expressed by a parameter . That way, the target is to solve the following optimization problem

| (2) |

Remark 2.3.

In (2), the two boundary cases and correspond to the pure expected utility maximization and ruin probability minimization problems, respectively. More generally, the convex combination in (2), is a linear scalarization of a multi-objective optimization problem, i.e. the original problem with two objectives – the expected utility of terminal wealth and the ruin probability – is transformed into a single-objective optimization problem. Our approach can also accommodate other objectives alongside those discussed in this paper, we leave the investigation of other objectives to future research. We also refer to Feinstein and Rudloff (2022), where the efficient frontier, i.e. the set of all optimal solutions for a multi-objective optimization problem, is approximated via neural networks.

Our problem formulation is kept very general, so that various notable models can be considered as special cases. For example, might be a self-exciting process observed at discrete time points. As in Section 4, could be (the discretization of) an Ornstein–Uhlenbeck process. Additionally, let us note that the formulation of this section extends naturally to the multi-dimensional case with, for instance, multiple correlated business lines.

We aim to solve the optimization problem (2) using empirical risk minimization and stochastic approximation, a classical concept in statistical learning theory which can be outlined as follows. Given a set of training data points that are independent and identically distributed, and a parametrized family of predictor functions , the goal is to minimize the empirical loss,

where denotes a loss function. If is differentiable with respect to , the gradient descent method can be used to minimize the empirical loss starting from an initial guess and iteratively updating

until a pre-determined termination criterion is reached. Here, denotes a learning rate, and denotes the gradient of with respect to .

For very large sample sizes, where computing the average gradient is numerically expensive, stochastic gradient descent (SGD) is a more efficient alternative, updating parameters based on individual gradients . However, due to the noisy nature of single-gradient updates, mini-batch stochastic gradient descent is often preferred. This method updates parameters based on the average gradient over a subset of the training points, balancing computational efficiency and stability.

Note that the loss is assumed to be differentiable with respect to . However, in our optimization problem, the ruin probability imposes numerical challenges due to the non-smooth nature of the indicator function. To address this issue, Subsection 2.1 explores connections to binary classification by replacing the indicator function with a surrogate loss function. This substitution makes the problem tractable via empirical risk minimization. Our surrogate loss model can be interpreted as a generalized (and to the best of our knowledge, never used before) version of a Gerber–Shiu penalty function.

2.1 Ruin probability and binary classification problems

Ruin probabilities can be expressed in terms of expectations. To this end, given , consider the map defined by . Then, one writes:

| (3) |

where denotes the indicator function over the set , i.e. for and otherwise.

Minimizing the ruin probability in (3) then amounts to finding the optimal , such that the mapping classifies as many data points as possible not as ruin. In other words, finding the optimal reinsurance strategy can be identified with the equivalent task of finding the optimal classifier for the binary classification problem where one seeks to map all data points to a non-ruin event. Using as an argument to is justified by the Doob–Dynkin representation theorem, which states that all -adapted processes can be written as functions of .

The main issue with the indicator function is that it is neither convex nor smooth. Therefore, optimizing (3) by using deep learning tools and empirical risk minimization, particularly minibatch stochastic gradient descent, becomes quite challenging. A remedy to this issue is to employ a surrogate loss function instead of the indicator function:

| (4) |

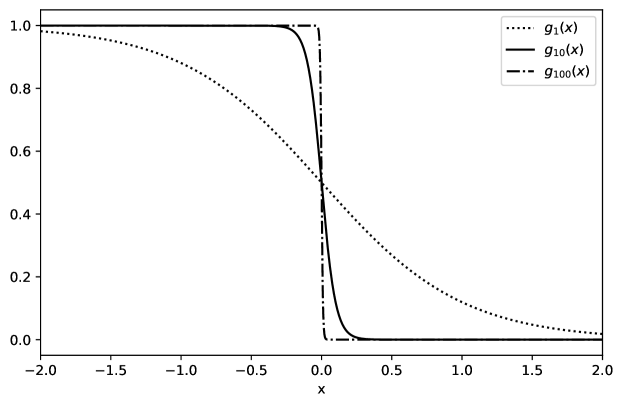

The surrogate loss function for is presented in Figure 1. This function will be also used (with ) in the numerical study in Section 4. For theory on surrogate loss functions for binary classification problems, see Bartlett et al. (2006); Nguyen et al. (2009); Reid and Williamson (2010).

Replacing the ruin probability in (2) by the expected surrogate loss of with respect to imposes a penalty on the expected utility, which can be seen as a generalized Gerber–Shiu function (Gerber and Shiu, 1998). Indeed, our surrogate loss function allows for an approximation of the ruin probability under mild assumptions.

Proposition 2.4.

Given , let be a uniformly bounded sequence of functions such that, -almost surely, . Then,

Beweis.

An application of Lebesgue’s dominated convergence theorem yields the assertion. ∎

3 Algorithmic reinsurance policies

We propose to solve (2) numerically via algorithmic reinsurance policies. These policies determine retention levels using neural networks that observe information to generate decisions. This approach is inspired by recent successful applications in quantitative finance and actuarial science. Popular use-cases are hedging, optimal stopping, model calibration, and scenario generation (Buehler et al., 2019; Becker et al., 2019; Horvath et al., 2021; Wiese et al., 2020).

Theorems that establish approximations in function space via neural networks are usually referred to as universal approximation theorems (UAT); notable contributions include Cybenko (1989) and Hornik (1991). These theorems establish the topological density of sets of neural networks in various topological spaces. One speaks of the universal approximation property (Kratsios, 2021) of a class of neural networks. Unfortunately, these theorems are usually non-constructive. To numerically find optimal neural networks, one typically combines backpropagation (see for example Rumelhart et al. (1986)) with ideas from stochastic approximation (Robbins and Monro, 1951; Kiefer and Wolfowitz, 1952; Dvoretzky, 1956).

Definition 3.1 (Deep feedforward neural network).

Let be a bounded, measurable and non-constant map. Given , we denote by the set of neural networks with an -dimensional input layer, one neuron with identity activation function in the output layer, hidden layers, and at most nodes with as activation function in each hidden layer (cf. Kidger and Lyons (2020, Definition 3.1)). We call elements from deep feedforward neural networks, or simply deep neural networks.

Definition 3.2 (Algorithmic reinsurance policy).

We denote by the set of all proportional reinsurance strategies that satisfy for some with , for each . Here, denotes the logistic function given by .

Definition 3.1 provides one example of a class of neural networks we can use, but other choices are possible. In light of Definition 3.2, one could consider for example recurrent neural networks or long short-term memory (LSTM) networks (see for example Hochreiter and Schmidhuber (1997)). We also refer to UATs for deep, narrow networks (Kidger and Lyons, 2020) and for randomized neural networks (Huang et al., 2006). Note that feedforward neural networks are usually defined with a linear readout map (as in Definition 3.1). In order to ensure that algorithmic reinsurance policies are valid proportional reinsurance policies assuming values in , we opt for the composition with the logistic function in Definition 3.2.

In this paper, we restrict ourselves to proportional reinsurance strategies. However, the same techniques can be applied to other types of reinsurance strategies. For example, excess-of-loss (XL) policies could be written as for some deep neural network . We leave the investigation and comparison of results for various algorithmic reinsurance treaties to future research.

For the sake of notational simplicity, given , and a smooth surrogate loss function , let

| (5) |

From a numerical perspective, solving the optimization problem (2) via algorithmic reinsurance policies motivates the use of Monte Carlo methods. Here, we first generate a finite amount of data points and replace, for each , the expectation and probability appearing in (2) by the empirical average

| (6) |

The summation over a finite number of data points allows us to re-interpret Equation (6) as the expectation of over a measure which assigns equal probability to every outcome. This motivates the assumption that the underlying probability space is finite, in which case all reinsurance strategies, including all algorithmic reinsurance policies, are admissible, i.e. in particular . Moreover, since in this case every singleton set for each is measurable (for otherwise we could not assign the probability to it), it is also natural to assume that is endowed with the power set to form a measurable space.

Theorem 3.3.

Assume that is a finite set, and that . Then, for every and , there exists an algorithmic reinsurance policy such that

| (7) |

Beweis.

The proof partially relies on some ideas from the proof of Buehler et al. (2019, Proposition 4.3). Let be an -optimal strategy, i.e. . Fix one time point . Since is -adapted, we have that is -measurable. Recall that is the smallest -algebra that makes measurable. An application of Doob–Dynkin’s lemma implies the existence of a Borel-measurable map such that .

Let be the Borel probability measure that is induced by on . Since is bounded (as it assumes values in ), we have for every and thus, in particular, .

Consider the sequence of functions given by if , if , and otherwise. Clearly, pointwise and thus, pointwise. We repeat the same construction for all time points, and construct a sequence of reinsurance policies, where for each . Since is finite,

We may therefore assume, without loss of generality, that takes values in a closed subset of that does neither contain nor , for a sufficiently large .

The sigmoid function , being a continuous bijection with continuous inverse , establishes a homeomorphism between and . Since , it follows that is bounded, and thus .

The universal approximation theorem (Hornik, 1991) ensures the existence of a sequence of shallow feedforward neural networks (i.e. feedforward neural networks with one hidden layer), such that in , as . But this implies, denoting , that in , as , and thus also in probability. Upon passing to a subsequence, which we also denote , we may assume that convergence holds outside of a -null set, in which case , -almost surely.

If we repeat the above arguments for every , we obtain a sequence of processes given by , such that for every , where convergence holds outside a -null set.

This implies that for every , where convergence holds outside a -null set, and consequently , -almost surely, which implies that and , -almost surely as . Since is finite,

We can thus find large enough, such that , and set . ∎

Remark 3.4.

Theorem 3.3 provides theoretical justification for solving the optimization problem (2) via algorithmic reinsurance policies. However, it is non-constructive in the sense that it does not shed any light on the way how the policy can be found. In order to solve the problem via empirical risk minimization in the next section, we will proceed in two steps:

-

1.

Approximate the indicator function used to form the ruin probability by a surrogate loss function. This step is justified by Proposition 2.4.

-

2.

Solve the surrogate problem by stochastic approximation over the set of algorithmic policies.

The final result is subject to two sources of numerical error: (1) the approximation of the indicator function, and (2) the approximation of the solution to the surrogate problem with algorithmic policies. However, both of these two errors can be made arbitrarily small.

Remark 3.5.

Classical universal approximation theorems which are formulated for feedforward neural networks usually assume a linear readout, which is not bounded. In order to obtain a valid proportional reinsurance policy, we need to guarantee that our algorithmic strategies assume values in . In Theorem 3.3 we were able to do this with some simple tricks for our specific model setting. For a more general treatment of non-Euclidean universal approximation, see Kratsios and Bilokopytov (2020).

4 Numerical experiments

In this section, we present a numerical example where the surplus is modeled by a Cramér–Lundberg process perturbed by an Ornstein–Uhlenbeck (OU) process. Including the OU process adds complexity, making the problem more challenging and realistic. The OU process may, for instance, represent the fluctuations in the number of clients or in premium payments.

We assume that the claims are iid, exponentially distributed with mean , represents a discretized Poisson process with intensity , and and are independent. The insurer charges premia according to the expected value principle with safety loading , i.e. . Similarly, the reinsurer charges premia according to the expected value principle with safety loading , i.e. . The process follows the dynamics

| (8) |

where are iid shocks with . We assume that the initial capital is positive to avoid starting in ruin. For our simulations, we take an arbitrarily chosen initial value of 1.

The utility function is of exponential type, , with risk-aversion coefficient . Table 1 summarizes the parameters for our base model. The values for , , and are taken from Schmidli (2001). For the neural network, we chose a two-hidden-layer topology with hyperbolic tangent (tanh) as activation function in the hidden layers and logistic activation in the output layer. The hidden layers contain 32 nodes each. The neural network takes the surplus as input; additional inputs were tested but provided negligible improvements. All computations were performed using Python, using the Keras deep learning API for constructing and training the neural networks.

| Model parameter | Value | |

|---|---|---|

| Initial wealth | ||

| Time horizon | ||

| Number of time steps | ||

| Claim arrival intensity | ||

| Expected claim size | ||

| Safety loading of insurer | ||

| Safety loading of reinsurer | ||

| Risk aversion coefficient | ||

| Tuning parameter | ||

| Surrogate loss parameter | ||

| OU mean-reversion level | ||

| OU mean-reversion speed | ||

| OU volatility coefficient |

Neural network training was performed on 2000 batches, each with a batch size of , using the Adam optimizer (Kingma and Ba, 2017) with an initial learning rate of . The learning rate was decreased by a factor of 10 after 10 epochs without improvement, with a minimum learning rate of . Early stopping was employed after 20 epochs without improvement. Distributions, expected utilities, and ruin probabilities were computed on a test set of size .

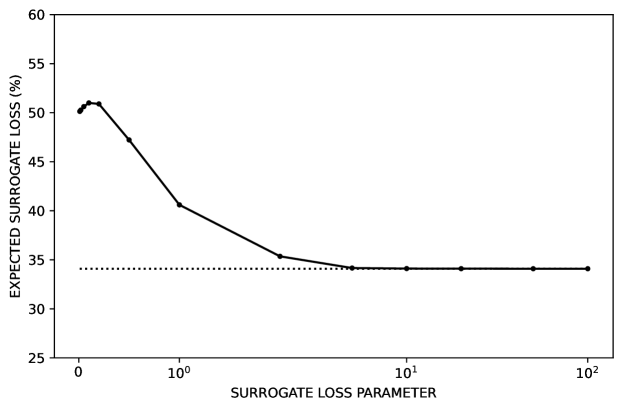

First, we want to numerically verify that the expected surrogate loss indeed approximates the ruin probability. To achieve this, we compute the ruin probability for our model without reinsurance (i.e. setting ) and compare the obtained value () with the expected surrogate loss for various values of . As shown in Figure 2, the expected surrogate loss approximates the ruin probability well when is sufficiently large. Based on these results, we fix for the subsequent analysis.

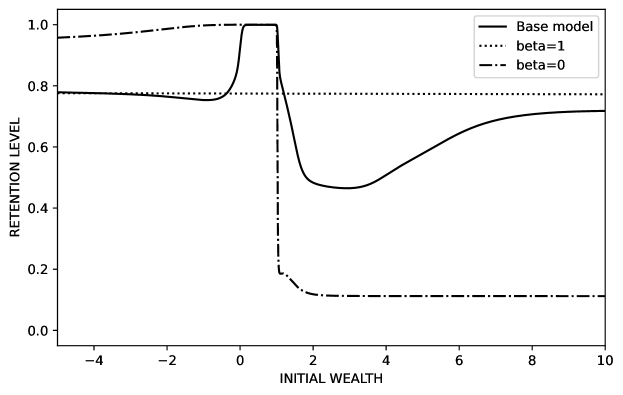

The parameter , given in (2), significantly influences the optimal retention level as a function of the surplus. For instance, in Schmidli (2001), where the ruin probability is minimized in a continuous-time setting, the optimal reinsurance strategy turns out to be constantly 1 until a certain surplus level is reached. After that, the retention level drops to a much lower value and converges to a constant as the surplus goes to infinity. In our model, by incorporating the ruin probability as an additional objective, the reinsurance policy must penalize scenarios where the insurer’s wealth becomes negative at any point in time up to maturity .

In our simulations, we noticed that it sufficed to optimize over those feedback strategies that do not depend on time, i.e. for (with ) and for some function , as using time-independent strategies did not improve the solution. Therefore, we can interpret our obtained strategies as functions depending on the initial capital. Figure 3 shows the optimal retention levels depending on the initial capital for the base case and the boundary cases (no penalisation through ruin probability, only ulility maximization) and (pure ruin probability minimization, no utility in the target functional).

One can check that the strategy corresponding to the case of pure ruin probability minimization has the same form (on the positive real line) as the strategy in the continuous time setting for the classical risk model, see Schmidli (2008, p. 53). In the base model, the presence of the utility function in the target functional enforces an increase in the optimal retention level starting from approximately . In the tradeoff between more safety (a smaller retention level) and more utility, the utility wins in the long run. Obviously, by maximizing exponential utility with no consideration of the ruin probability, the optimal strategy does not depend on the surplus (dotted line in Figure 3).

Recall that our objective contains two components: the expected utility of terminal wealth, and the expected surrogate loss approximating the ruin probability. By varying , we can generate optimal reinsurance strategies that approximately achieve Pareto-efficient solutions, where any improvement in one objective requires a compromise in the other. It is important to note that our results are subject to numerical errors due to:

-

1.

The surrogate loss function for the ruin probability,

-

2.

The finite size of training and test datasets, and

-

3.

The fact that neural networks can in general only approximate optimal policies up to some .

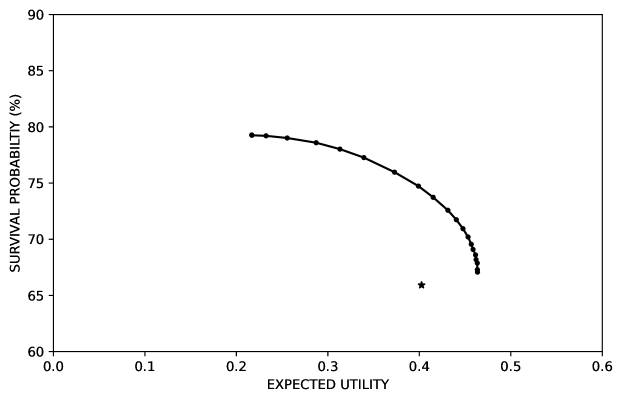

Figure 4 demonstrates the trade-off between expected utility of terminal wealth and ruin probability. Each individual point represents an approximate Pareto-efficient solution for different choices of , where improving one objective comes at the expense of the other. The star indicates the values obtained without reinsurance (i.e. ), highlighting the benefits of optimal reinsurance strategies. In particular, the figure highlights that, for our choice of parameters, reinsurance is always more favourable than non-reinsurance.

5 Conclusions

We introduce a novel framework for optimizing reinsurance strategies using a deep learning approach. The target functional consists of the expected utility of terminal wealth perturbed by a modified Gerber–Shiu penalty function. It allows to balance between maximizing the expected utility of terminal wealth, and minimizing the probability of ruin, depending on the individual preferences of the insurer.

We draw connections to concepts from binary classification and surrogate loss functions. This enables the problem to be addressed using empirical risk minimization methods. Combined with stochastic gradient descent, it allows for efficient optimization of algorithmic reinsurance policies, even in complex model settings.

Our numerical findings highlight the ability of our method to interpolate between the problems of maximizing expected utility of terminal wealth, and minimizing the probability of ruin. Future research could explore other optimization targets and reinsurance forms as well as more complex, higher-dimensional models with correlated business lines. Moreover, it would be interesting to explore optimal algorithmic reinsurance strategies that are robust with respect to parameter uncertainties, such as the intensity of the Poisson process, or the expected claim size. Finally, another interesting topic would be to optimize algorithmic reinsurance polices under distributional constraints on the wealth process.

Acknowledgements

Aleksandar Arandjelović acknowledges support from the International Cotutelle Macquarie University Research Excellence Scholarship. A significant part of work on this project was carried out while Aleksandar Arandjelović was affiliated with the research unit Financial and Actuarial Mathematics (FAM) at TU Wien in Vienna, Austria as well as the Department of Actuarial Studies and Business Analytics at Macquarie University in Sydney, Australia.

Literatur

- Albrecher and Thonhauser (2009) H. Albrecher and S. Thonhauser. Optimality results for dividend problems in insurance. RACSAM-Revista de la Real Academia de Ciencias Exactas, Fisicas y Naturales. Serie A. Matematicas, 103(2):295–320, 2009.

- Albrecher et al. (2017) H. Albrecher, J. Beirlant, and J.L. Teugels. Reinsurance: Actuarial and statistical aspects. John Wiley & Sons, 2017.

- Asmussen and Albrecher (2010) S. Asmussen and H. Albrecher. Ruin probabilities, volume 14. World scientific, 2010.

- Avanzi (2009) B. Avanzi. Strategies for dividend distribution: A review. North American Actuarial Journal, 13(2):217–251, 2009.

- Bai and Guo (2008) L. Bai and J. Guo. Optimal proportional reinsurance and investment with multiple risky assets and no-shorting constraint. Insurance: Mathematics and Economics, 42:968–975, 2008.

- Bartlett et al. (2006) P. L. Bartlett, M. I. Jordan, and Jon. D. McAuliffe. Convexity, classification, and risk bounds. Journal of the American Statistical Association, 101(473):138–156, 2006.

- Becker et al. (2019) S. Becker, P. Cheridito, and A. Jentzen. Deep optimal stopping. JMLR, 20(74):1–25, 2019.

- Borch (1961) K. Borch. The utility concept applied to the theory of insurance. ASTIN Bulletin, 1(5):245–255, 1961.

- Braunsteins and Mandjes (2023) P. Braunsteins and M. Mandjes. The Cramér–Lundberg model with a fluctuating number of clients. Insurance: Mathematics and Economics, 2023.

- Buehler et al. (2019) H. Buehler, L. Gonon, J. Teichmann, and B. Wood. Deep hedging. Quantitative Finance, 19(8):1271–1291, 2019.

- Ceci et al. (2022) C. Ceci, K. Colaneri, and A. Cretarola. Optimal reinsurance and investment under common shock dependence between financial and actuarial markets. Insurance: Mathematics and Economics, 105:252–278, 2022.

- Cheng et al. (2020) X. Cheng, Z. Jin, and H. Yang. Optimal insurance strategies: A hybrid deep learning Markov chain approximation approach. ASTIN Bulletin, 50(2):449–477, 2020.

- Cheung and Liu (2023) E.C.K. Cheung and H. Liu. Joint moments of discounted claims and discounted perturbation until ruin in the compound poisson risk model with diffusion. Probability in the Engineering and Informational Sciences, 37(2):387–417, 2023.

- Cybenko (1989) G. Cybenko. Approximation by superpositions of a sigmoidal function. Math. Control Signals Systems, 2(4):303–314, 1989.

- Dufresne and Gerber (1991) F. Dufresne and H.U. Gerber. Risk theory for the compound Poisson process that is perturbed by diffusion. Insurance: Mathematics and Economics, 10(1):51–59, 1991.

- Dvoretzky (1956) A. Dvoretzky. On stochastic approximation. In Proceedings of the Third Berkeley Symposium on Mathematical Statistics and Probability, 1954–1955, vol. I, pages 39–55. University of California Press, Berkeley and Los Angeles, Calif., 1956.

- Eisenberg (2015) J. Eisenberg. Optimal dividends under a stochastic interest rate. Insurance: Mathematics and Economics, 65:259–266, 2015.

- Feinstein and Rudloff (2022) Z. Feinstein and B. Rudloff. Deep learning the efficient frontier of convex vector optimization problems, 2022. arXiv preprint, https://arxiv.org/abs/2205.07077, math.OC.

- Gerber (1970) H.U. Gerber. An extension of the renewal equation and its application in the collective theory of risk. Scandinavian Actuarial Journal, 1970(3-4):205–210, 1970.

- Gerber and Shiu (1998) H.U. Gerber and E.S.W. Shiu. On the time value of ruin. North American Actuarial Journal, 2(1):48–72, 1998.

- Hipp (2018) C. Hipp. Company value with ruin constraint in Lundberg models. Risks, 6(3):73, 2018.

- Hochreiter and Schmidhuber (1997) S. Hochreiter and J. Schmidhuber. Long short-term memory. Neural Computation, 9(8):1735–1780, 1997.

- Hornik (1991) K. Hornik. Approximation capabilities of multilayer feedforward networks. Neural Networks, 4(2):251–257, 1991.

- Horvath et al. (2021) B. Horvath, A. Muguruza, and M. Tomas. Deep learning volatility: A deep neural network perspective on pricing and calibration in (rough) volatility models. Quantitative Finance, 21(1):11–27, 2021.

- Huang et al. (2006) G.-B. Huang, L. Chen, and C.-K. Siew. Universal approximation using incremental constructive feedforward networks with random hidden nodes. IEEE Transactions on Neural Networks, 17:879–892, 2006.

- Jin et al. (2021) Z. Jin, H. Yang, and G. Yin. A hybrid deep learning method for optimal insurance strategies: Algorithms and convergence analysis. Insurance: Mathematics and Economics, 96:262–275, 2021.

- Kidger and Lyons (2020) P. Kidger and T. Lyons. Universal approximation with deep narrow networks. In Proceedings of Thirty Third Conference on Learning Theory, volume 125 of Proceedings of Machine Learning Research, pages 2306–2327, 2020.

- Kiefer and Wolfowitz (1952) J. Kiefer and J. Wolfowitz. Stochastic estimation of the maximum of a regression function. Ann. Math. Statistics, 23:462–466, 1952.

- Kingma and Ba (2017) D.P. Kingma and J. Ba. Adam: A method for stochastic optimization, 2017. arXiv preprint, https://arxiv.org/abs/1412.6980, cs.LG.

- Kratsios (2021) A. Kratsios. The universal approximation property: characterization, construction, representation, and existence. Ann. Math. Artif. Intell., 89(5-6):435–469, 2021.

- Kratsios and Bilokopytov (2020) A. Kratsios and I. Bilokopytov. Non-Euclidean universal approximation. In H. Larochelle, M. Ranzato, R. Hadsell, M.F. Balcan, and H. Lin, editors, Advances in Neural Information Processing Systems, volume 33, pages 10635–10646. Curran Associates, Inc., 2020.

- Leimcke (2020) G. Leimcke. Bayesian Optimal Investment and Reinsurance to Maximize Exponential Utility of Terminal Wealth. PhD thesis, Karlsruher Institut für Technologie (KIT), 2020.

- Lundberg (1903) F. Lundberg. 1. Approximerad framställning af sannolikhetsfunktionen: 2. Återförsäkring af kollektivrisker. Akademisk afhandling. Almqvist & Wiksells, 1903.

- Nguyen et al. (2009) X. Nguyen, M. J. Wainwright, and M. I. Jordan. On surrogate loss functions and -divergences. The Annals of Statistics, 37(2):876–904, 2009.

- Promislow and Young (2005) S.D. Promislow and V.R. Young. Minimizing the probability of ruin when claims follow Brownian motion with drift. North American Actuarial Journal, 9(3):110–128, 2005.

- Reid and Williamson (2010) M. D. Reid and R. C. Williamson. Composite binary losses. Journal of Machine Learning Research, 11:2387–2422, 2010.

- Richman (2021) R. Richman. AI in actuarial science - A review of recent advances - Part 2. Annals of Actuarial Science, 15(2):230–258, 2021.

- Robbins and Monro (1951) H. Robbins and S. Monro. A stochastic approximation method. Ann. Math. Statistics, 22:400–407, 1951.

- Rumelhart et al. (1986) D. E. Rumelhart, G. E. Hinton, and R. J. Williams. Learning representations by back-propagating errors. Nature, 323(6088):533–536, 1986.

- Schmidli (2001) H. Schmidli. Optimal proportional reinsurance policies in a dynamic setting. Scandinavian Actuarial Journal, 2001(1):55–68, 2001.

- Schmidli (2002) H. Schmidli. On minimizing the ruin probability by investment and reinsurance. The Annals of Applied Probability, 12(3):890–907, 2002.

- Schmidli (2008) H. Schmidli. Stochastic Control in Insurance. Springer, London, 2008.

- Taksar and Markussen (2003) M.I. Taksar and C. Markussen. Optimal dynamic reinsurance policies for large insurance portfolios. Finance and Stochastics, 7:97–121, 2003.

- Thonhauser and Albrecher (2007) S. Thonhauser and H. Albrecher. Dividend maximization under consideration of the time value of ruin. Insurance: Mathematics and Economics, 41(1):163–184, 2007.

- Tsai (2001) C.C.-L. Tsai. On the discounted distribution functions of the surplus process perturbed by diffusion. Insurance: Mathematics and Economics, 28(3):401–419, 2001.

- Wiese et al. (2020) M. Wiese, R. Knobloch, R. Korn, and P. Kretschmer. Quant GANs: Deep generation of financial time series. Quantitative Finance, 20(9):1419–1440, 2020.