Efficacy of Large Language Models in Systematic Reviews

Abstract.

This study investigates the effectiveness of Large Language Models (LLMs) in interpreting existing literature through a systematic review of the relationship between Environmental, Social, and Governance (ESG) factors and financial performance. The primary objective is to assess how LLMs can replicate a systematic review on a corpus of ESG-focused papers. We compiled and hand-coded a database of 88 relevant papers published from March 2020 to May 2024. Additionally, we used a set of 238 papers from a previous systematic review of ESG literature from January 2015 to February 2020. We evaluated two current state-of-the-art LLMs, Meta AI’s Llama 3 8B and OpenAI’s GPT-4o, on the accuracy of their interpretations relative to human-made classifications on both sets of papers. We then compared these results to a ”Custom GPT” and a fine-tuned GPT-4o Mini model using the corpus of 238 papers as training data. The fine-tuned GPT-4o Mini model outperformed the base LLMs by 28.3% on average in overall accuracy on prompt 1. At the same time, the ”Custom GPT” showed a 3.0% and 15.7% improvement on average in overall accuracy on prompts 2 and 3, respectively. Our findings reveal promising results for investors and agencies to leverage LLMs to summarize complex evidence related to ESG investing, thereby enabling quicker decision-making and a more efficient market.

1. Introduction

1.1. Background and Motivation

Environmental, Social, and Governance (ESG) investing has continued to grow, with nearly a 60% increase in the use of ESG as investment criteria within the last two decades (Umar et al., 2020). Increasing awareness of sustainability issues has made ESG considerations a mainstream component for asset managers and institutional investors. The United Nations Principles for Responsible Investment now has over 609 asset owners holding USD 121.3 trillion combined assets under management in 2021 (Kräussl et al., 2024). Additionally, the percentage of corporations releasing ESG reports has increased from 35% in 2010 to 86% in 2020 (Rouen et al., 2024).

However, there is no consensus on whether ”ESG pays.” Ľuboš Pástor, Robert F. Stambaugh, and Lucian A. Taylor [(2022)], for example, find that U.S. green stocks outperform brown stocks. In contrast, Juddoo et al. [(2023)] conclude impact investing strategies do not provide greater returns than traditional strategies. Many others have concluded that ESG does pay (Huynh and Xia, 2021; Hekman et al., 2022), that ESG doesn’t pay (Raghunandan and Rajgopal, 2022; Bolton and Kacperczyk, 2021), or that ESG has no impact on financial returns (Laplume et al., 2022; Amiraslani et al., 2023).

In addition to this dispute in the industry, there are concerns regarding the volume, transparency, and usefulness of ESG reports released by corporations (Burnaev et al., 2023). These inconsistencies complicate accurate measurement of a firm’s ESG performance and its impact on financial outcomes. Large Language Models (LLMs) offer a promising solution in this context. LLMs can rapidly interpret and analyze vast amounts of text and numerical information, enabling them to improve the efficiency and accuracy of ESG data analysis and serve as a tool to help companies familiarize themselves with ESG standards (Chopra et al., 2024). Thus, LLMs offer the potential to reduce the complexity of the ESG investing landscape (Kumar et al., 2022).

1.2. Problem Statement

With the rapidly changing nature of ESG investing and the large volume of available information, staying informed and rapidly summarizing new information is imperative. However, this requires extensive expertise and time, which not all industry players have access to. Therefore, it is essential to evaluate LLM tools in the context of ESG to determine if they can expedite the review process without compromising accuracy.

1.3. Objectives

The primary objective of this research is to evaluate the effectiveness of LLM tools (Llama 3 8B from Meta AI, GPT-4o from OpenAI, a ”Custom GPT” chatbot from OpenAI, and a fine-tuned GPT-4o Mini Model from OpenAI) in conducting systematic reviews of the literature on the relationship between ESG performance and financial returns. By comparing the performance of LLMs to traditional manual systematic reviews, we evaluate the effectiveness of LLMs as a tool to help researchers and industry leaders efficiently interpret ESG information without compromising accuracy.

1.4. Outcome and Significance

We aim to contribute to two main strands of research: 1) the effectiveness of LLMs in summarizing and interpreting data and 2) the promise and pitfalls of systematic review.

Our development of a ”Custom GPT” and fine-tuned GPT-4o Mini model as well as the evaluation of two base model LLMs (Llama 3 and GPT-4o) highlighted the potential for LLMs to become a useful tool for interpreting ESG-related data. There were numerous occasions where all models excelled, such as with prompt 2 for papers classified as ”accounting-based” or ”both,” with accuracies ranging from 87.1% to 100%. Additionally, the fine-tuned GPT-4o Mini model outperformed the base LLMs by 28.3% on average in overall accuracy on prompt 1. The ”Custom GPT” also outperformed the base LLMs but by 3.0% and 15.7% on average in overall accuracy on prompts 2 and 3, respectively. Ultimately, this signifies that LLMs can serve as a helpful resource in interpreting ESG literature, especially after fine-tuning with relevant data.

Secondly, our study evaluated the use of LLMs in the context of systematic reviews to see if they can remove humans from the process. Systematic reviews are a key resource for advancing research, policy, and industry. However, the current best practices for systematic reviews are slow and labor-intensive, so much so that some reviews are no longer relevant by the time they are completed. Our study provides valuable insights into which models excel in specific contexts by assessing various LLMs in replicating systematic reviews. We highlight the potential for LLMs to transform systematic review best practices, given that the right prompt, model, and context have been selected.

2. Previous Works

In recent years, LLMs have made significant progress in their Natural Language Processing (NLP) abilities, marking an important milestone in real-world applications of Artificial Intelligence (AI). They can understand complex scenarios, analyze vast amounts of data, and generate relevant content, highlighting the immense potential present within their use in the sustainable financial industry (Chang et al., 2023; Wu et al., 2023). However, their development began with hand-coded models that relied on humans to determine sentiment.

Dev Shah et al. [(2018)] developed a manual sentiment analysis algorithm to predict the market movement of stocks within the pharmaceutical industry. They first gathered news articles on their stocks of interest and extracted the main text from those articles into n-grams (sets of words). Then, they created a data dictionary of 100 words covering a comprehensive list of topics specific to the pharmaceutical sector, classifying each word into a positive, negative, or neutral class of sentiment. Finally, the coded dictionary was used to classify the n-grams from the news text as ”positive,” ”neutral,” or ”negative,” corresponding to market predictions of stock price increase, remain steady, and decline, respectively. This method obtained a substantial prediction accuracy of 70.59%, highlighting the potential for sentiment analysis to play a significant role in increasing market efficiency (Shah et al., 2018). The researchers mention that a vital contributor to their high accuracy was the comprehensive data dictionary they made relying on domain expertise.

While Shah et al.’s [(2018)] model did not use machine learning techniques, Sandro Gössi et al. [(2023)] developed a more modern approach to the issue of sentiment analysis by fine-tuning the FinBERT model previously developed by Doug Araci [(2019)]. The FinBERT model is a fine-tuned version of the BERT language model (Devlin et al., 2019) for analyzing the sentiment of the financial text. Gössi et al. [(2023)] created a custom training set of 3535 complex sentences extracted from a dataset of Federal Open Market Committee (FOMC) financial texts, a significant increase in context from Shah et al. [(2018)]. Using this set to fine-tune the model, they saw significant increases in accuracy over the previous FinBert model and Shah et al.’s [(2018)] manual model, displaying the abilities of LLMs to extract meaning from nuanced language and financial jargon (Gössi et al., 2023). The performance benefits of continuous fine-tuning allude to the potential for future applications within niche areas such as ESG.

ESG scores are highly relevant to key players in the financial industry: asset owners determining investment risk, companies showcasing their environmental and social impacts, and regulators ensuring ethical standards are followed. ESG scoring is a meticulous process performed by key agencies, MSCI, Sustainalytics, ISS, Refinitiv, and FTSE Russell (Lykkesfeldt and Kjaergaard, 2022). To determine an overall ESG rating for a company, these agencies employ analysts to review historical data to understand drivers of ESG or hypothesize theoretical relationships that have not been tested. Each company determines its key metrics and corresponding weights to determine its own ESG score, leading to differences between the ratings of multiple agencies (Del Vitto et al., 2023). While this process has traditionally been performed by hand and statistical algorithms, LLMs can be a powerful tool to redefine ESG ratings (Zhao et al., 2024). Their capabilities of rapidly interpreting unstructured data, such as company reports, financial statements, and news articles, can significantly increase the efficiency of evaluating companies’ ESG performance. Furthermore, given unbiased training data, LLMs can remove human subjectivity and bias from all ratings, helping to reduce discrepancies across agencies (Zhao et al., 2024).

Del Vitto et al. [(2023)] tested the efficacy of white-box algorithms such as Ridge and Lasso linear regression and black-box algorithms such as Random Forests and Artificial Neural Networks (ANN). The algorithms were tested on their ability to predict ESG scores given a data set comprising 13,052 firms that are stratified by industry sector and geographical region. The algorithms were designed to evaluate firms on 180 environmental, 218 social, and 152 governance attributes. Overall, the Ridge and Lasso algorithms performed the best with root mean squared errors (RMSE) as low as 0.071. Additionally, ANN algorithms outperformed the Ridge and Lasso algorithms within the Social pillar, with the lowest RMSE of 0.090 (Del Vitto et al., 2023).

3. Methods

In this study, we assessed the performance of two base large language models (LLMs): Meta AI’s Llama 3 8B111Accessed using the Groq API and OpenAI’s GPT-4 Omni (GPT-4o). Our evaluation was conducted on two sets of papers: 88 papers published between March 2020 and May 2024 and a previously compiled set of 238 papers from January 2015 to February 2020 by Atz et al.[(2021)]. Each LLM was tested using nine specific prompts in a 3x3 experimental design (Figure 5). Due to API token input limitations, Llama 3 8B was only provided with the abstracts of the papers, while GPT-4o was given the full PDF.

We also developed a custom version of ChatGPT, named ”Custom GPT,” using the ”GPTs” feature on OpenAI’s ChatGPT platform. This custom model was given comprehensive context plus chain-of-thought prompts for all three categories. Additionally, the 238-paper set with hand-coded labels was provided as reference data. The custom model, titled ”ESG Returns Insights,” was subsequently published on the ChatGPT platform. Additionally, we fine-tuned the GPT-4o Mini model on the 238-paper set and evaluated its performance on the new 88-paper set, benchmarking it against the standard GPT-4o Mini model. The fine-tuning process focused on Prompt 1, using the context prompt as the system instruction.

3.1. Data Collection

We queried ProQuest, Science Direct, JSTOR, Google Scholar, and Social Science Research Network (SSRN) to find literature on ESG and financial performance published between March 2020 and May 2024. To ensure unbiased and high-quality papers were sourced, we filtered the results to include only papers from journals rated 3, 4, or 4* and classified as either ACCOUNT, FINANCE, ECON, ETHICS-CSR-MAN, or STRAT from the Chartered Association of Business 2021 Academic Journal Guide (Chartered Association of Business Schools, 2021). We compiled a corpus of 98 papers and hand-coded each in a typical systematic review format. However, we removed 10 papers, all from the Journal of Business Ethics, as they were deemed not salient enough (Atz et al., 2021). Of the remaining 88 papers, 14 manuscripts are not peer-reviewed. In addition to the new papers, we downloaded an older set from January 2015 to February 2020 comprising 238 papers from Atz et al. [(2021)].

3.2. Data Classification on New Set

The new data set labels followed the same structure as Atz et al.’s [(2023)] paper, as detailed in the online appendix (Atz et al., 2021). Three main questions were answered, and their responses were coded into the respective categories:

-

(1)

Does the study conclude a relationship between sustainability and financial performance? (positive, negative, or mixed/neutral)

-

(2)

How is financial success implemented? (market-based,

accounting-based, both, or other) -

(3)

How is sustainability implemented? (ESG, E, S, G, CSR, or other)

Two researchers independently coded the papers, achieving a rater agreement of 90%, with a third researcher resolving the discrepancy.

3.3. Prompt Categories and Definitions

We split up three questions into three categories (1-3), which were structured incrementally with increasing context (A-C). The A-level prompts were basic and simply asked the questions and listed the possible classifications. The B-level prompts provided increased context from the Atz et al. [(2023)] codebook behind the meaning of the classifications, along with one or two examples. The C-level prompts included all of the information from the B-level and A-level but were designed to follow a chain-of-thought approach. They asked the model to take specific steps in determining its response. In addition, the model was asked to return a reasoning and confidence score for its prediction. This confidence score was derived within the prediction of the LLM and, therefore, should not be interpreted as a technical measure of confidence. These prompts were used for Llama 3 and base GPT-4o.

3.4. Custom GPT Development and Model Fine-tuning

The ”Custom GPT” model was developed using the ChatGPT interface’s ”GPTs” tool, where we provided a set of instructions and relevant attachments for the default model context. The three chain-of-through prompts (1C, 2C, and 3C) were combined into one large set of instructions for the ”Custom GPT.” This way, following the input of a paper, all three prompts would be answered within a single response and without additional prompting. Each paper was tested in a new chat session to ensure that previous interactions did not influence the model’s responses. In addition to a specialized prompt, the model was provided the old corpus 238 papers as a labeled training sample.222Due to the design of OpenAI’s GPT builder, the old corpus served primarily as a reference rather than technical training data.

Then, using the 238 papers in the old corpus of studies, we fine-tuned the smaller GPT-4o Mini model using the OpenAI API. We used a batch size of 1, 3 epochs, and a learning rate multiplier of 1.8. This model was only fine-tuned on Category 1 and instructed to return a prediction only for the answer to question 1.

3.5. Data Processing and Analysis

After obtaining the outputs from each LLM for the new and old datasets, we ensured that all results were standardized. We then compiled the results for further analysis. The primary focus was comparing the models’ performance in correctly classifying the study findings and implementation methods across different prompts. We calculated the following metrics:

-

(1)

Overall Accuracy

-

(2)

Sub-accuracy for Each Prompt Class

-

(3)

F1 Score

Given the disproportionate number of classes across prompts and the varying number of instances per class, we calculated the Weighted Power Mean (Equation 1) with p = 2 for the F1 scores for each predicted class. This approach provides a nuanced evaluation of our model’s performance, addressing the challenges of imbalanced data and varying class frequencies.

| (1) |

4. Results

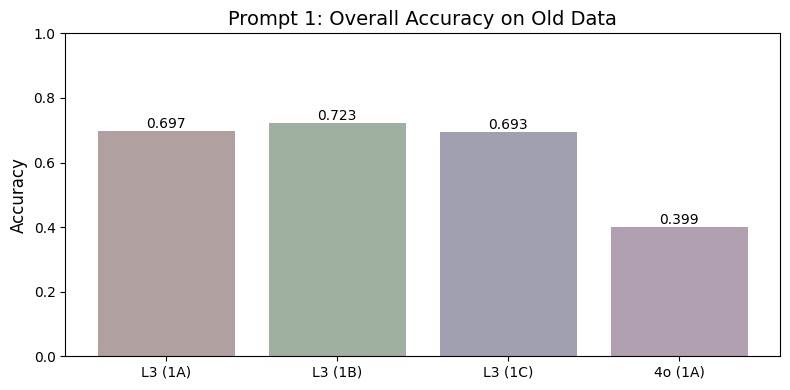

4.1. Old Data Set

Results of LLMs on new data set prompt 1A through C

We observed relatively no change in accuracy between the prompt variations for Llama 3 and noted a poor performance from base GPT-4o, nearly equivalent to guessing.

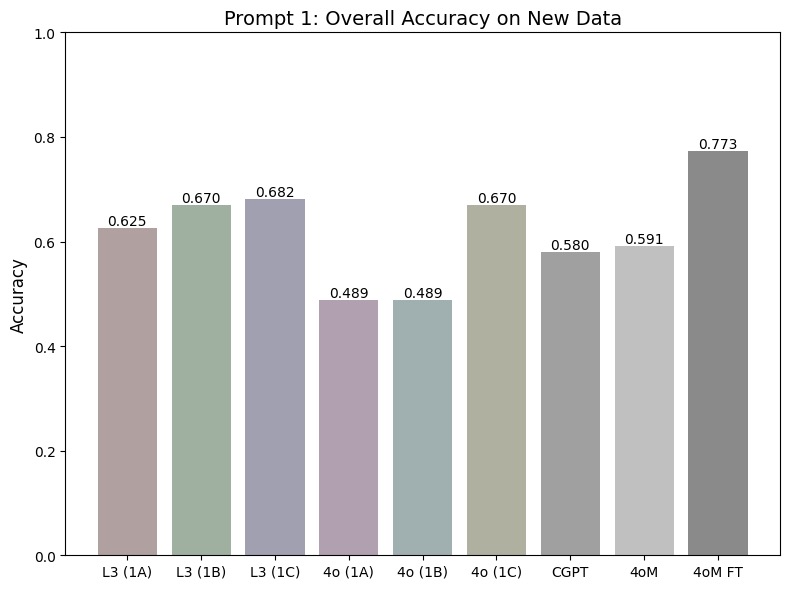

4.2. New Data Set

Results of LLMs on new data set prompt 1A through C

| Model | Overall | Positive | Negative | Mixed |

|---|---|---|---|---|

| L3 (1A) | 0.625 | 0.695 | 0.565 | 0.438 |

| L3 (1B) | 0.670 | 0.712 | 0.696 | 0.500 |

| L3 (1C) | 0.682 | 0.729 | 0.696 | 0.500 |

| 4o (1A) | 0.489 | 0.373 | 0.870 | 0.250 |

| 4o (1B) | 0.489 | 0.390 | 0.870 | 0.250 |

| 4o (1C) | 0.670 | 0.644 | 0.826 | 0.500 |

| CGPT | 0.580 | 0.576 | 0.696 | 0.375 |

| 4oM | 0.591 | 0.560 | 0.533 | 0.696 |

| 4oM FT | 0.773 | 0.780 | 0.733 | 0.783 |

The results show a substantial improvement in the GPT-4o base for prompt 1C, while Llama’s accuracy remained steady across all prompts. Both base LLMs showed poor performance on papers classified as ”Mixed.” GPT-4o performed its best in the negative category with a high accuracy of 87.0%. The custom GPT-4o only outperformed GPT-4o in prompts 1A and 1B but not 1C and underperformed Llama 3 across all prompts. However, the custom GPT-4o Mini outperformed both base LLMs across all prompts.

| Model | Overall | Market | Accounting | Both | Other |

|---|---|---|---|---|---|

| L3 (2A) | 0.841 | 0.769 | 0.903 | 1.000 | 0.286 |

| L3 (2B) | 0.852 | 0.385 | 1.000 | 1.000 | 0.286 |

| L3 (2C) | 0.818 | 0.154 | 0.968 | 1.000 | 0.571 |

| 4o (2A) | 0.761 | 0.538 | 0.871 | 1.000 | 0.000 |

| 4o (2B) | 0.795 | 0.308 | 0.968 | 1.000 | 0.000 |

| 4o (2C) | 0.830 | 0.692 | 0.935 | 1.000 | 0.000 |

| CGPT | 0.841 | 0.692 | 0.903 | 1.000 | 0.429 |

Base GPT-4o saw an increase in overall accuracy with the chain-of-thought prompt, whereas Llama 3 saw a decrease. Custom GPT-4o outperformed base GPT-4o across all three prompts, outperformed Llama 3 in 2C, and matched in 2B. All LLMs performed strongly on papers labeled as ”Accounting-Based” or ”Both” and poorly on papers labeled ”Other.”

| Model | Overall | ESG | E | S | G | CSR |

|---|---|---|---|---|---|---|

| L3 (3A) | 0.773 | 0.828 | 1.000 | 0.200 | 0.933 | 0.786 |

| L3 (3B) | 0.807 | 0.931 | 1.000 | 0.200 | 0.900 | 0.857 |

| L3 (3C) | 0.818 | 0.931 | 1.000 | 0.400 | 0.900 | 0.786 |

| 4o (3A) | 0.602 | 0.414 | 0.333 | 0.200 | 0.800 | 1.000 |

| 4o (3B) | 0.727 | 0.621 | 0.667 | 0.400 | 0.900 | 0.929 |

| 4o (3C) | 0.693 | 0.793 | 0.000 | 0.200 | 0.800 | 0.857 |

| CGPT | 0.852 | 0.966 | 0.333 | 0.500 | 0.967 | 0.786 |

There was no notable difference when switching between prompts A-C for either Llama 3 or base GPT-4o. Custom GPT outperformed both base LLMs across all prompts. Llama 3 classified papers in the ”ESG”, ”E”, and ”G” categories well. Base GPT-4o performed better with papers in the ”G” and ”CSR” categories. All three LLMs struggled with papers in the ”S” and ”Other” categories.

| Prompt | Correct | Incorrect |

|---|---|---|

| L3 (1C) | 0.866 | 0.832 |

| L3 (2c) | 0.858 | 0.833 |

| L3 (3C) | 0.880 | 0.872 |

| 4o (1C) | 0.937 | 0.924 |

| 4o (2C) | 0.969 | 0.924 |

| 4o (3C) | 0.966 | 0.926 |

There was no significant difference between the confidence scores when comparing both LLMs against each other and when comparing the scores for correct and incorrect classifications.

Result: Positive

Confidence: 0.9

Reason: The study concludes a significant and positive relationship between higher carbon emissions and higher stock returns across various sectors and countries.

GPT-4o overlooked the implication that higher carbon emissions equate to lower ESG, implying a negative correlation between ESG and financial performance. Misclassifications for similar reasons were prevalent across all three LLMs, occurring 9 times for base GPT-4o, 7 times for CustomGPT, and 5 times for Llama 3.333The fine-tuned GPT-4o Mini model only returned one-word classifications, therefore we were not able to determine the reason for misclassification.

| Model | Overall | 1A-C | 2A-C | 3A-C |

|---|---|---|---|---|

| L3 | 0.808 | 0.807 | 0.750 | 0.864 |

| 4o | 0.633 | 0.568 | 0.750 | 0.580 |

Both LLMs had a low agreement between predictions from prompts A-C, with Llama being consistent across all three prompts 80.8% of the time, compared to 63.3% for GPT-4o.

| Model | 1 | 2 | 3 |

|---|---|---|---|

| L3 (A) | 0.639 | 0.852 | 0.796 |

| L3 (B) | 0.683 | 0.848 | 0.835 |

| L3 (C) | 0.689 | 0.811 | 0.844 |

| 4o (A) | 0.488 | 0.784 | 0.632 |

| 4o (B) | 0.492 | 0.797 | 0.749 |

| 4o (C) | 0.679 | 0.842 | 0.757 |

| CGPT | 0.594 | 0.852 | 0.880 |

Table 6 shows the weighted power mean (with ) of the F1 scores for different LLM and prompt combinations across three scenarios.

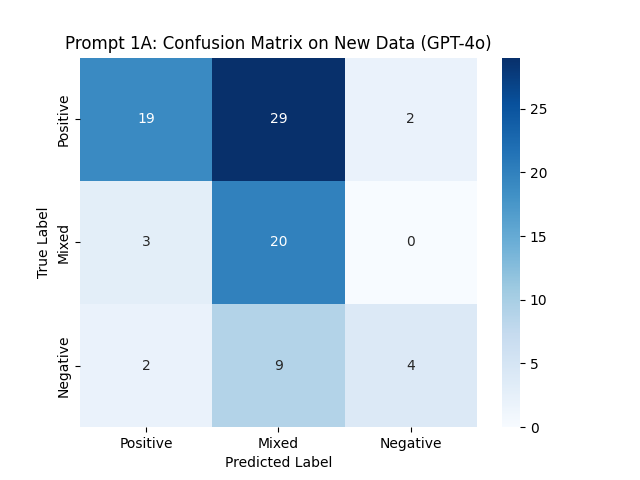

Figure 4 presents the confusion matrix for GPT-4o’s performance on the new data set with prompt 1A. ”Positive” samples were incorrectly classified as ”Mixed” 58% of the time. Overall, the model’s responses were skewed to the ”Mixed” category, incorrectly classifying true ”Positive” or ”Negative” studies as ”Mixed” frequently.

5. Discussion

5.1. Base Llama 3

Even though Llama only provided the abstracts of the papers, it outperformed GPT-4o on eight out of nine of the prompts. Furthermore, within Category 1, Llama 3 achieved the highest mean F1 score on Prompt C. Llama’s overall accuracy ranged from 62.5% to 85.2%, with the model struggling on category 1, a phenomenon witnessed across all models. Additionally, Llama had an average prompt agreement of 80.8%, making it reliant on needing a better prompt.

Despite many papers in our corpus of 88 mentioning both metrics within the text, they typically used only one for their conclusions and thus were not classified as ”Both.” Llama 3 excelled in category 2 for ”accounting-based” research papers, achieving accuracies between 90.3% and 100% and weighted power mean of F1 scores between 0.811 and 0.852, suggesting the model’s ability to efficiently scan text for key details while filtering out irrelevant information.

Furthermore, Llama 3 classified papers coded as ”ESG”, ”E”, and ”G” within category 3 well with accuracies ranging from 90.0% to 100% with one outlier of 82.8% for prompt 3A under ”ESG” classified papers. While many papers mention keywords such as ”climate” and ”environment,” a broader analysis was necessary to comprehend the overarching theme and differentiate between ”ESG” and the other individual categories. This highlights Llama 3’s remarkable ability to understand overall themes within the literature.

Overall, Llama 3’s performance within certain subcategories and consistent outperformance over base GPT-4o exemplify its viability as an LLM to assist during systematic review, but not entirely replace humans.

5.2. Base GPT-4o

Although base GPT-4o performed worse than Llama 3, it displayed highlights within certain prompts. For papers classified as ”Negative” in category 1, the model displayed relatively strong accuracies ranging from 82.6% to 87.0%. Because papers classified as ”Negative” are more likely to contain stronger language (need to find a source for this statement), the increase in accuracy may indicate that GPT-4o focuses more on searching for sentiment keywords throughout the paper. However, the model struggled with the ”Positive” class and misclassified 58% of ”Positive” papers as ”Mixed.” Furthermore, similar to Llama’s increase in performance for category 2, GPT-4o performed better on the ”Accounting-Based” paper, again highlighting the model’s ability to identify key information while ignoring the noise. Finally, GPT-4o was strong at classifying papers labeled as ”CSR” within category 3, which further supports the idea that GPT-4o can scan for keywords and sentiment well because often when CSR was used as a metric by the paper, it was explicitly stated as ”CSR” multiple times. The accuracy differences between GPT-4o and Llama 3 suggest a potential difference in training data between both LLMs. Additionally, the weighted power mean of the F1 score was the highest when using the chain-of-thought prompt, signifying that prompt design and structure play a significant role in the model outcome.

5.3. Fine-Tuned Models

The ”Custom GPT” outperformed the base GPT-4o model for eight out of the nine prompts, only performing worse on prompt 1C. Compared to Llama 3, the ”Custom GPT” outperformed on prompts 2C, 3A, 3B, and 3C, matched on prompts 2A, and underperformed on all category 1 prompts and 2C. Additionally, the Custom GPT achieved a higher mean F1 score than all other models in categories 2 and 3. Due to the ”Custom GPT’s” poor performance, in prompt 1, we fine-tuned a GPT-4o Mini model to excel within that category specifically. This new model outperformed all of the other models in category 1 and beat the standard GPT-4o Mini model by 30.8%. This indicates that with fine-tuning and proper prompting/context, LLMs can effectively interpret ESG literature.

5.4. Evaluation of LLMs as a Whole

Ultimately, the application of LLMs within ESG shows potential. However, the base model LLMs are not completely reliable, with a maximum accuracy of 68.2% in the overall relationship between financial performance and ESG, 77.6% in the financial metrics category, and 81.6% in the sustainability metrics category. The base Llama 3 model consistently outperformed GPT-4o, yet it did not reach accuracy levels safe enough to replace human reviewers. To improve performance and accuracy, fine-tuning methods allow LLMs to serve as a tool to expedite traditional systematic reviews and transition to new best practices.

5.5. Future Works

Our research highlights the importance of selecting the appropriate prompt, model, and context to maximize the utility of LLMs. The chain-of-thought prompting style improved accuracy and provided insights into the model’s “thought process,” making it an area worth further exploration. Future research should focus on fine-tuning LLMs with larger and more diverse datasets to enhance their ability to interpret nuanced and complex information. With these better-equipped models, researchers can develop frameworks that integrate LLMs into existing systematic review workflows to assist in data extraction, synthesis, and reporting, ultimately streamlining the review process and maintaining the relevance of systematic reviews over time.

Acknowledgements.

We thank Ulrich Atz for the guidance and review and for providing the OpenAI API computing credits. We also thank the seminar participants at the NYU Stern Center for Sustainable Business for valuable feedback.References

- (1)

- Amiraslani et al. (2023) Hami Amiraslani, Karl V. Lins, Henri Servaes, and Ane Tamayo. 2023. Trust, social capital, and the bond market benefits of ESG performance. Review of Accounting Studies 28, 2 (01 Jun 2023), 421–462. https://doi.org/10.1007/s11142-021-09646-0

- Araci (2019) Dogu Araci. 2019. FinBERT: Financial Sentiment Analysis with Pre-trained Language Models. ArXiv abs/1908.10063 (2019). https://api.semanticscholar.org/CorpusID:201646244

- Atz et al. (2021) Ulrich Atz, Tracy Van Holt, Zongyuan Zoe Liu, and Christopher Bruno. 2021. Online appendix: Does Sustainability Generate Better Financial Performance? Review, meta-analysis, and propositions. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3919652

- Bolton and Kacperczyk (2021) Patrick Bolton and Marcin Kacperczyk. 2021. Do investors care about carbon risk? Journal of Financial Economics 142, 2 (2021), 517–549. https://doi.org/10.1016/j.jfineco.2021.05.008

- Burnaev et al. (2023) Evgeny Burnaev, Evgeny Mironov, Aleksei Shpilman, Maxim Mironenko, and Dmitry Katalevsky. 2023. Practical AI Cases for Solving ESG Challenges. Sustainability 15, 17 (2023). https://doi.org/10.3390/su151712731

- Chang et al. (2023) Yupeng Chang, Xu Wang, Jindong Wang, Yuan Wu, Linyi Yang, Kaijie Zhu, Hao Chen, Xiaoyuan Yi, Cunxiang Wang, Yidong Wang, Wei Ye, Yue Zhang, Yi Chang, Philip S. Yu, Qiang Yang, and Xing Xie. 2023. A Survey on Evaluation of Large Language Models. arXiv:2307.03109 [cs.CL] https://arxiv.org/abs/2307.03109

- Chartered Association of Business Schools (2021) Chartered Association of Business Schools. 2021. Academic Journal Guide 2021. Technical Report. Chartered Association of Business Schools, London. https://charteredabs.org/academic-journal-guide Methodology, June 2021.

- Chopra et al. (2024) Shauhrat S. Chopra, Sachini Supunsala Senadheera, Pavani Dulanja Dissanayake, Piumi Amasha Withana, Rajeev Chib, Jay Hyuk Rhee, and Yong Sik Ok. 2024. Navigating the Challenges of Environmental, Social, and Governance (ESG) Reporting: The Path to Broader Sustainable Development. Sustainability 16, 2 (2024). https://doi.org/10.3390/su16020606

- Del Vitto et al. (2023) Alessandro Del Vitto, Daniele Marazzina, and Davide Stocco. 2023. ESG ratings explainability through machine learning techniques. Annals of Operations Research (19 Jul 2023). https://doi.org/10.1007/s10479-023-05514-z

- Devlin et al. (2019) Jacob Devlin, Ming-Wei Chang, Kenton Lee, and Kristina Toutanova. 2019. BERT: Pre-training of Deep Bidirectional Transformers for Language Understanding. arXiv:1810.04805 [cs.CL] https://arxiv.org/abs/1810.04805

- Gössi et al. (2023) Sandro Gössi, Ziwei Chen, Wonseong Kim, Bernhard Bermeitinger, and Siegfried Handschuh. 2023. FinBERT-FOMC: Fine-Tuned FinBERT Model with Sentiment Focus Method for Enhancing Sentiment Analysis of FOMC Minutes. In Proceedings of the Fourth ACM International Conference on AI in Finance (Brooklyn, NY, USA) (ICAIF ’23). Association for Computing Machinery, New York, NY, USA, 357–364. https://doi.org/10.1145/3604237.3626843

- Hekman et al. (2022) David R. Hekman, H. Phoenix VanWagoner, Bradley P. Owens, Terence R. Mitchell, Brooks C. Holtom, Thomas M. Lee, and Jennifer Dinger. 2022. An Examination of Whether and How Prevention Climate Alters the Influence of Turnover on Performance. Journal of Management 48, 3 (2022), 542–570. https://doi.org/10.1177/0149206320978451 arXiv:https://doi.org/10.1177/0149206320978451

- Huynh and Xia (2021) Thanh D. Huynh and Ying Xia. 2021. Climate Change News Risk and Corporate Bond Returns. Journal of Financial and Quantitative Analysis 56, 6 (2021), 1985–2009. https://doi.org/10.1017/S0022109020000757

- Juddoo et al. (2023) Kumari Juddoo, Issam Malki, Sudha Mathew, and Sheeja Sivaprasad. 2023. An impact investment strategy. Review of Quantitative Finance and Accounting 61, 1 (01 Jul 2023), 177–211. https://doi.org/10.1007/s11156-023-01149-0

- Kräussl et al. (2024) Roman Kräussl, Tobi Oladiran, and Denitsa Stefanova. 2024. A review on ESG investing: Investors’ expectations, beliefs and perceptions. Journal of Economic Surveys 38, 2 (2024), 476–502. https://doi.org/10.1111/joes.12599 arXiv:https://onlinelibrary.wiley.com/doi/pdf/10.1111/joes.12599

- Kumar et al. (2022) Satish Kumar, Dipasha Sharma, Sandeep Rao, Weng Marc Lim, and Sachin Kumar Mangla. 2022. Past, present, and future of sustainable finance: insights from big data analytics through machine learning of scholarly research. Annals of Operations Research (2022).

- Laplume et al. (2022) André O. Laplume, Jeffrey S. Harrison, Zhou Zhang, Xin Yu, and Kent Walker. 2022. Evidence of an Inverted U–Shaped Relationship between Stakeholder Management Performance Variation and Firm Performance. Business Ethics Quarterly 32, 2 (2022), 272–298. https://doi.org/10.1017/beq.2021.19

- Lykkesfeldt and Kjaergaard (2022) Poul Lykkesfeldt and Laurits Louis Kjaergaard. 2022. Encompassing ESG Rating Agencies. Springer International Publishing, Cham, 305–311. https://doi.org/10.1007/978-3-031-05800-4_39

- Raghunandan and Rajgopal (2022) Aneesh Raghunandan and Shiva Rajgopal. 2022. Do ESG funds make stakeholder-friendly investments? Review of Accounting Studies 27, 3 (01 Sep 2022), 822–863. https://doi.org/10.1007/s11142-022-09693-1

- Rouen et al. (2024) Ethan Rouen, Kunal Sachdeva, and Aaron Yoon. 2024. Sustainability Meets Substance: Evaluating ESG Reports in the Context of 10-Ks and Firm Performance. (Mar 2024). https://ssrn.com/abstract=4227934orhttp://dx.doi.org/10.2139/ssrn.4227934

- Shah et al. (2018) Dev Shah, Haruna Isah, and Farhana Zulkernine. 2018. Predicting the Effects of News Sentiments on the Stock Market. In 2018 IEEE International Conference on Big Data (Big Data). 4705–4708. https://doi.org/10.1109/BigData.2018.8621884

- Ulrich Atz and Bruno (2023) Zongyuan Zoe Liu Ulrich Atz, Tracy Van Holt and Christopher C. Bruno. 2023. Does sustainability generate better financial performance? review, meta-analysis, and propositions. Journal of Sustainable Finance & Investment 13, 1 (2023), 802–825. https://doi.org/10.1080/20430795.2022.2106934 arXiv:https://doi.org/10.1080/20430795.2022.2106934

- Umar et al. (2020) Zaghum Umar, Dimitris Kenourgios, and Sypros Papathanasiou. 2020. The static and dynamic connectedness of environmental, social, and governance investments: International evidence. Economic Modelling 93 (2020), 112–124. https://doi.org/10.1016/j.econmod.2020.08.007

- Wu et al. (2023) Shijie Wu, Ozan Irsoy, Steven Lu, Vadim Dabravolski, Mark Dredze, Sebastian Gehrmann, Prabhanjan Kambadur, David Rosenberg, and Gideon Mann. 2023. BloombergGPT: A Large Language Model for Finance. arXiv:2303.17564 [cs.LG] https://arxiv.org/abs/2303.17564

- Zhao et al. (2024) Huaqin Zhao, Zhengliang Liu, Zihao Wu, Yiwei Li, Tianze Yang, Peng Shu, Shaochen Xu, Haixing Dai, Lin Zhao, Gengchen Mai, Ninghao Liu, and Tianming Liu. 2024. Revolutionizing Finance with LLMs: An Overview of Applications and Insights. arXiv:2401.11641 [cs.CL] https://arxiv.org/abs/2401.11641

- Ľuboš Pástor et al. (2022) Ľuboš Pástor, Robert F. Stambaugh, and Lucian A. Taylor. 2022. Dissecting green returns. Journal of Financial Economics 146, 2 (2022), 403–424. https://doi.org/10.1016/j.jfineco.2022.07.007

Appendix A Table and Figure Abbreviations

-

•

L3: Meta AI’s Llama 3 Model with 8B Parameters

-

•

4o: OpenAI’s GPT4o Model

-

•

4oM: OpenAI’s GPT4o Mini Model

-

•

4oM F: OpenAI’s GPT4o Mini Model Finetuned on Corpus of Papers from 2015 to 2022 (Atz et al., 2021)

-

•

CGPT: Custom GPT using ChatGPT GPT-builder feature

-

•

Mixed: Mixed/Neutral

-

•

Accounting: Accounting-based metric of financial performance (ROA, ROE, etc.)

-

•

Market: Market-based metric of financial performance (Tobin’s Q, Jensen’s Alpha, etc.)

-

•

ESG: A holistic ESG score provided by third-party data providers

-

•

E: Environmental factors exclusively

-

•

G: Governance factors exclusively

-

•

S: Social factors exclusively

-

•

CSR: Corporate Social Responsibility

-

•

Prompt Category + Type (ex. 1C)

Figure 5: Prompt 1 Incremental Design

Prompt 1C

Prompt 1B

Prompt 1A

Take on the role of a business school academic whose task is to synthesize the main finding of a research paper.

The provided research paper investigates the relationship between financial returns and sustainability or ESG. Interpret the paper and answer this question: Does the study conclude there’s a relationship between sustainability and financial performance?

You must respond in one word classifying the relationship as ‘positive’, ‘negative’, or ‘mixed’. Also use ”mixed” if the paper is unclear or finds neutral/insignificant results.

Use the following guidance for answering:

Positive: A positive code indicates the authors found a general supportive/positive finding or that sustainability/ESG is associated with higher financial performance. Also consider the overall conclusion that the authors drew when there is no formal research hypothesis. Usually this is apparent in the abstract or the last section of a paper. Note that if a study finds a negative correlation between say carbon emissions (low is good) and financial performance (high is good), this would be an overall positive finding.

[…]

Use the following steps to determine your answer.

Information retrieval:

Step 1. Read the abstract and determine whether there is an unambiguous answer to the question.

Step 2. Read the Introduction (first section) and Conclusion (last section) to determine whether there is an unambiguous answer to the question.

[…]

Response:

Structure your answer in the following format:

- Result: Provide the one-word answer of ‘positive’, ‘negative’, or ‘mixed’.

- Confidence: Provide the number indicating your confidence.

- Reason: Provide the reasoning for your result. Illustrate it with an example from the paper.