Modeling the impact of Climate transition on real estate prices

Abstract

In this work, we propose a model to quantify the impact of the climate transition on a property in housing market. We begin by noting that property is an asset in an economy. That economy is organized in sectors, driven by its productivity which is a multidimensional Ornstein-Uhlenbeck process, while the climate transition is declined thanks to the carbon price, a continuous deterministic process. We then extend the sales comparison approach and the income approach to valuate an energy inefficient real estate asset. We obtain its value as the difference between the price of an equivalent efficient building following an exponential Ornstein-Uhlenbeck as well as the actualized renovation costs and the actualized sum of the future additional energy costs. These costs are due to the inefficiency of the building, before an optimal renovation date which depends on the carbon price process. Finally, we carry out simulations based on the French economy and the house price index of France. Our results allow to conclude that the order of magnitude of the depreciation obtained by our model is the same as the empirical observations.

keywords:

Stochastic modelling , Transition risk , Carbon price , Housing valuation , Real estate , Energy efficiencyThis research is part of the PhD thesis in Mathematical Finance of Lionel Sopgoui whose works are funded by a CIFRE grant from BPCE S.A. The opinions expressed in this research are those of the authors and are not meant to represent the opinions or official positions of BPCE S.A.

We would like to thank Jean-François Chassagneux, Antoine Jacquier, Smail Ibbou, and Géraldine Bouveret for helpful comments on an earlier version of this work.

Notations

-

1.

is the set of non-negative integers, , and is the set of integers.

-

2.

denotes the -dimensional Euclidean space, is the set of non-negative real numbers, .

-

3.

.

-

4.

is the set of real-valued matrices (), is the identity matrix.

-

5.

denotes the -th component of the vector . For all , we denote by the transpose matrix, and denotes the spectrum of .

-

6.

For all , we denote the scalar product , the Euclidean norm and for a matrix , we denote

-

7.

is a complete probability space.

-

8.

For , is a finite dimensional Euclidian vector space and for a -field , , denotes the set of -meassurable random variable with values in such that for and for , .

-

9.

For a filtration , and , is the set of continuous-time processes that are -adapted valued in and which satisfy

-

10.

If and are two random variables -valued, for , we note the conditional distribution of given , and the conditional distribution of given the filtration .

-

11.

If is a differentiable function, we note its first derivative.

Introduction

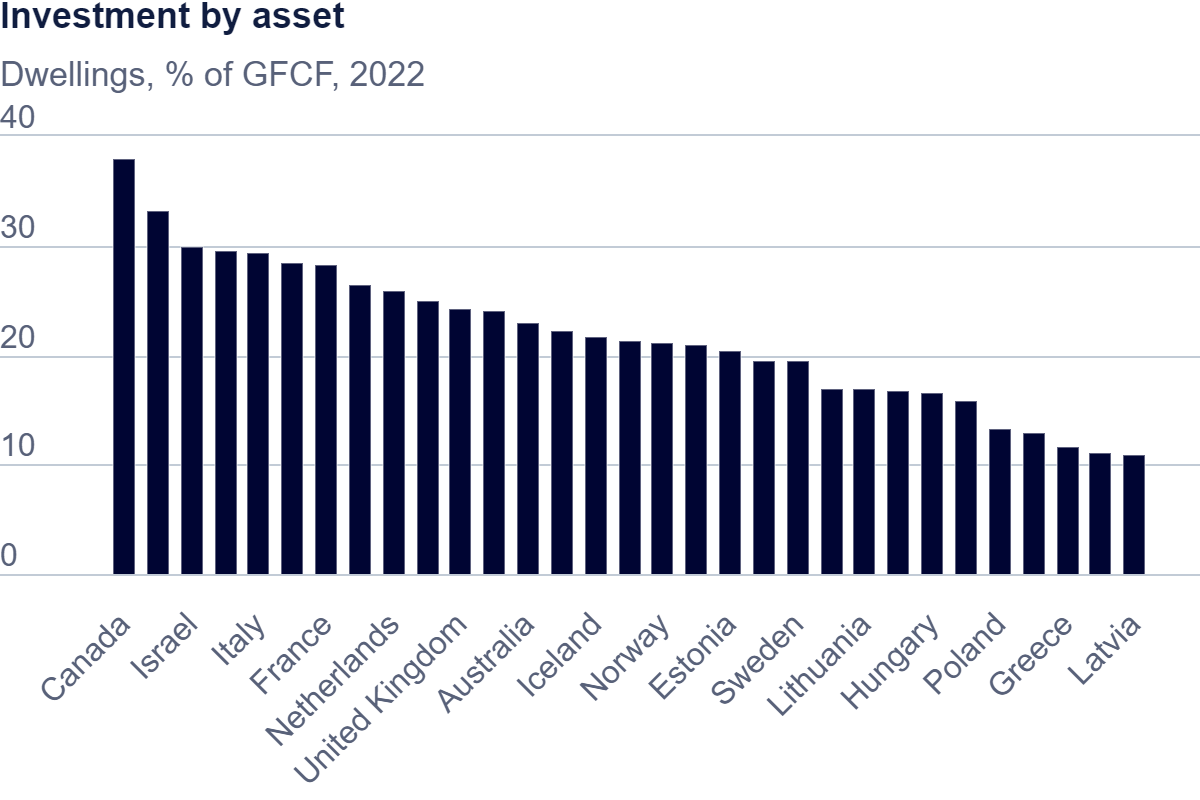

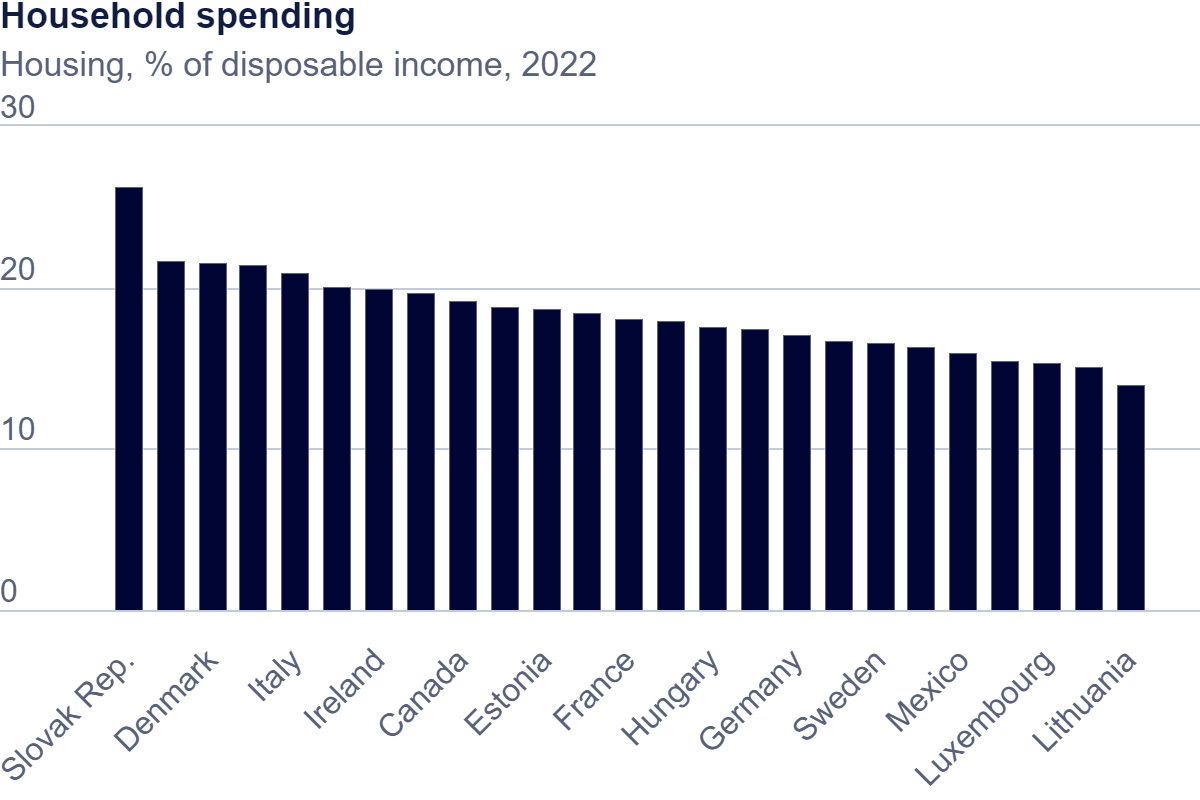

Real estate is a large part of capital stock and a large component of economic wealth. For example, Figure 5(a) from OECD, 2024b shows that dwellings represent between 10% and 40% of yearly investment and between 15% and 25% of yearly households’ disposable income. This explains the need to price real estate assets. Determining the market value of a building may be essential for accounting reasons (portfolio construction or management, asset price evolution, etc.), for making decisions (build, buy, or sell a property), or for applying for loans (collateral). In his dissertation, Schulz, (2003) presents three approaches for real estate valuation. The sales comparison approach which consists in using the transaction prices of highly comparable and recently sold properties to determine the market value of a given building. The income approach where the value of a property is the discounted sum of the (imputed) rent less all operating costs over its residual lifetime. The cost approach which consists in assuming that the value of a building is equals to the amount it would cost to buy the land (with identical characteristics) and to build a new building (with the same characteristics) on it.

The literature suggests several models for each approach. A real estate market model is proposed by Fabozzi et al., (2012) to price real estate derivatives, and then used for the calculation of the LGD by Frontczak and Rostek, (2015). These works model the price of a property as an exponential Ornstein-Uhlenbeck process while Moody’s, (2022) use a Geometric Brownian Motion. Laspeyres-Paasche housing index (see Gravelle and Rees, (2004)) is computed using the transactions price of buildings sold in the previous period, therefore value a property using the housing price index is an example sales comparison approach. For the income approach, the expected net (imputed) income is the tricky quantity to determine. Schulz, (2003) takes into account the relative maintenance and repair expenditures, the depreciating rate, the real estate tax rate, the real interest rate, the inflation of the rent (or imputed rent – the rental price an individual would pay for an asset they own –), etc. We will use these two approaches in this work.

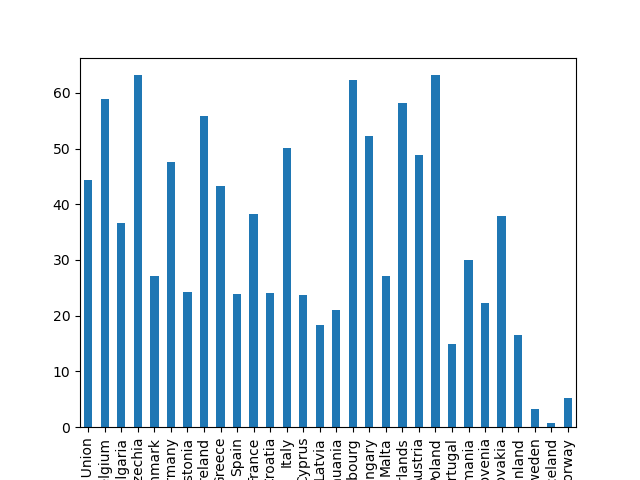

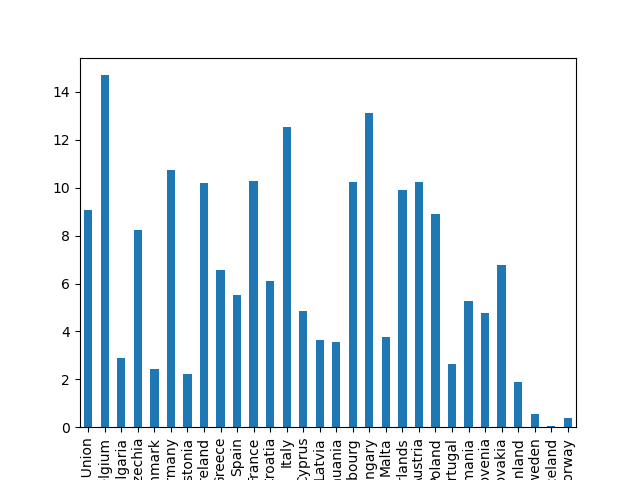

Climate change has a deep impact on human societies and their environments. One of the components of the climate risk is transition risk which relates to the potential economic and financial losses associated with the process of adjusting towards a low-carbon economy. Transition risk is becoming increasingly important in all parts of the economy and in particular in real estate. Residential or commercial buildings are one of the biggest greenhouse gases (GHG) emitters. Using Eurostat GHG emissions data (see Eurostat, (2022)), we find in Figure 6(a) that, between 2008 and 2021, around 45% of the total households emissions came from residential heating and cooling. And as shown in Figure 6(b), they represent around 9% of the total emissions, in the European Union (EU) zone. This is why renovation of buildings constitutes a central challenge in the climate policies. The Energy Performance of Buildings Directive (EPBD) from European Parliament, (2002) and European Union, (2022), introduced in 2002 by the European Commission and revised in 2010 and later, is a key instrument to increase the energy performance of buildings across the EU. Similarly to the carbon price, it is a way to implement climate transition. It consists in ranking buildings in terms of their energy efficiency (EE)111in ton of CO2 emissions per square meter per year or kilowatt hour per square meter per year by using letters from A to G (where A is the most efficient while G is the less). Aydin et al., (2020) found that EE is capitalized quite precisely into home prices in the Dutch housing market. de Ayala et al., (2016) found in a study on 1507 homes in Spain that dweelings labelled A, B or C are valued at between 5.4% and 9.8% higher price compared to D, E, F or G rated home. Franke and Nadler, (2019) also highlight that, in the rental decision-making, EE achieves a high importance score similar to that of rent, price and location respectively.

There is a great deal of statistical work on the effect of climate change on real estate, but very little modelling. It is this last point that interests us here. To introduce the climate transition, we draw inspiration from Ter Steege and Vogel, (2021) who write the price difference per square meter between two properties with different energy efficiency as the sum of the discounted value of (expected) energy cost differences. We will enhance their work by additionally considering the renovation costs to improve energy efficiency, and the optimal renovation date which will depend on the trajectory of energy prices (writing as a function of the carbon price). Initially, the building’s owner incurs additional energy costs due to the inefficiency of their property. Then, they may decide to spend money on renovations to make their building energy efficient. After the renovation, they no longer incur additional energy costs.

The rest of the present work is organized as follows. Because real estate industry is a sector of the economy, we start, in Section 1, by describing the economy concerned. We model, in Subsection 2, a building using both an exponential Ornstein-Uhlenbeck (O.U.) and a discounted sum of an income over its residual lifetime. Section 3 is dedicated to estimations and simulations while Section 4 focuses discussion.

1 Standing assumptions

We assume that the real estate assets are part of an economy divided in sectors, driven by dynamic and stochastic productivity, and subject to climate transition modeled by a dynamic and deterministic carbon price. Inspired by Bouveret et al., (2023)[Section 2] which models, in discrete time, a multisectoral closed economy subject to the carbon price. We introduce the following standing assumption which describes the productivity, which is considered to have stationary Ornstein-Uhlenbeck dynamics.

Standing Assumption 1.1.

We define the -valued process which evolves according to

| (1.1) |

where is a -dimensional Brownian Motion, and where the constants , the matrices , , and is an intensity of noise parameter that is fixed: it will be used later to obtain a tractable proxy of the firm value. Moreover, is a positive definite matrix and is a Hurwitz matrix i.e. its eigenvalues have strictly negative real parts.

We also introduce the following filtration with and for , .

Remark 1.2 (O.U. process).

We have the following results on O.U. that we will use later:

-

1.

According to Gobet and She, (2016)[Proposition 1], if one assumes that and are independent and is square integrable, then, there exists a unique square integrable solution to the -dimentional Ornstein-Uhlenbeck process satisfying , represented as

Additionally, for any , the distribution of conditional on is Gaussian , with the mean vector

(1.2) and the covariance matrix

(1.3) -

2.

Since is a Hurwitz matrix, then if we note , there exists so that for all . Therefore, according to Gobet and She, (2016)[Proposition 2], has a unique stationary distribution which is Gaussian with mean and covariance .

-

3.

We can show in A that for any , we have

and conditionally on , has an -dimensional normal distribution with the mean vector

(1.4) with

(1.5) and the covariance matrix

(1.6) -

4.

For later use, we define

(1.7) and observe that is a Markov process.

For the whole economy, we introduce a deterministic and exogenous carbon price in euro/dollar per ton. It allows us to model the impact of the transition pathways on the whole economy. We will note the complete carbon price process. We shall then assume the following setting.

Standing Assumption 1.3.

We introduce the carbon price process.

Let be given. The sequence satisfies

-

1.

for , , namely the carbon price is constant;

-

2.

for , , the carbon price may evolve;

-

3.

for , , namely the carbon price is constant.

We assume moreover that is .

An example of carbon price process

We assume the regulator fixes when the transition starts and the transition horizon time , the carbon price at the beginning of the transition , at the end of the transition , and the annual growth rate . Then, for all ,

| (1.8) |

In the example above that will be used in the rest of this work, we assume that the carbon price increases. However, there are several scenarios that could be considered, including a carbon price that would increase until a certain year before leveling off or even decreasing. We also assume an unique carbon price for the entire economy whereas we could proceed differently. For example, the carbon price could increase for production when stabilize or disappear on households in order to avoid social movements and so on. The framework can be adapted to various sectors as well as scenarios.

2 Valuation of a propertie under climate transition

The problem here is then to model the real estate market in the presence of the climate transition risk. Let us look at two of the three approaches mentioned in the introduction: the sales comparison approach and the income approach. For the efficient buildings, we use the first approach. Precisely, we will write the price of a property as the product of its surface area, its initial price, and the house price index (the latter described by an exponential Ornstein–Uhlenbeck dynamics). For the inefficient ones, we adopt the second approach. Explicitly, in addition to all the costs involved in owning the property, we will consider the energy costs due to energy inefficiency and the potential renovation costs.

According to Ter Steege and Vogel, (2021), in discrete time, the price difference per square meter between two properties, one of which with the highest EE label as the reference point (A+), should be solely explained by the sum of the discounted value of (expected) energy cost (noted ) differences:

| (2.1) |

This equation takes the perspective of a potential buyer who weighs the

options between buying the efficient property with score at a higher price and enjoying the lower energy costs, and buying the inefficient one with score at a discount that reflects the expected increased energy costs at time . Moreover, energy costs are the simple product of the expected energy price and a constant factor measuring the EE.

We extend the Ter Steege and Vogel, (2021) work here by assuming that:

-

1.

in the absence of climate transition, the housing price follows an Exponential Ornstein-Uhlenbeck process;

-

2.

each dwelling consumes a given quantity of energy per square meter, which is used to determine its energy efficiency, noted and expressed in kilowatts per square meter (KWh/m2);

-

3.

as a consequence, the dwelling price is depreciated (or appreciated) by the actualized sum of the future energy costs;

-

4.

once a certain level of energy efficiency is reached, the market is insensitive to this factor

-

5.

the energy price is a deterministic function of two variables, the first variable is the carbon price and the second is the source of energy,

-

6.

during the life of the property, the owner may undergo renovations which moves the energy efficiency from to , and whose cost per square meter is a function of its energy efficiency,

-

7.

the date of renovation of a dwelling is unknown, but is to be optimized.

-

8.

after renovations, the price of the building becomes insensitive to energy costs.

Assumption 2.1 (Housing price without climate transition).

We consider here two ways to model a housing price:

-

1.

The market value of the building indexed by at , is given by

(2.2) where

(2.3a) (2.3b) where is a standard Brownian motion independent to introduced in Standing Assumption 1.1 and driving the productivity of the economy. Moreover, , , , , and . We introduce the following filtration with for , .

-

2.

Owning a building allows to generate an ( the (imputed) income cash-flow process which is continuous and -adapted, therefore for all , an another way to write the price of the building is

(2.4) with .

We can do the following observations:

-

1.

in (2.2), is the value per square meter of the building at time (in euros/m2 for example) while is the log of housing price index whose dynamics is (2.3a) inspired by Frontczak and Rostek, (2015); Fabozzi et al., (2012). It characterizes the returns of the housing market which are correlated and fluctuates over time around a long-term average .

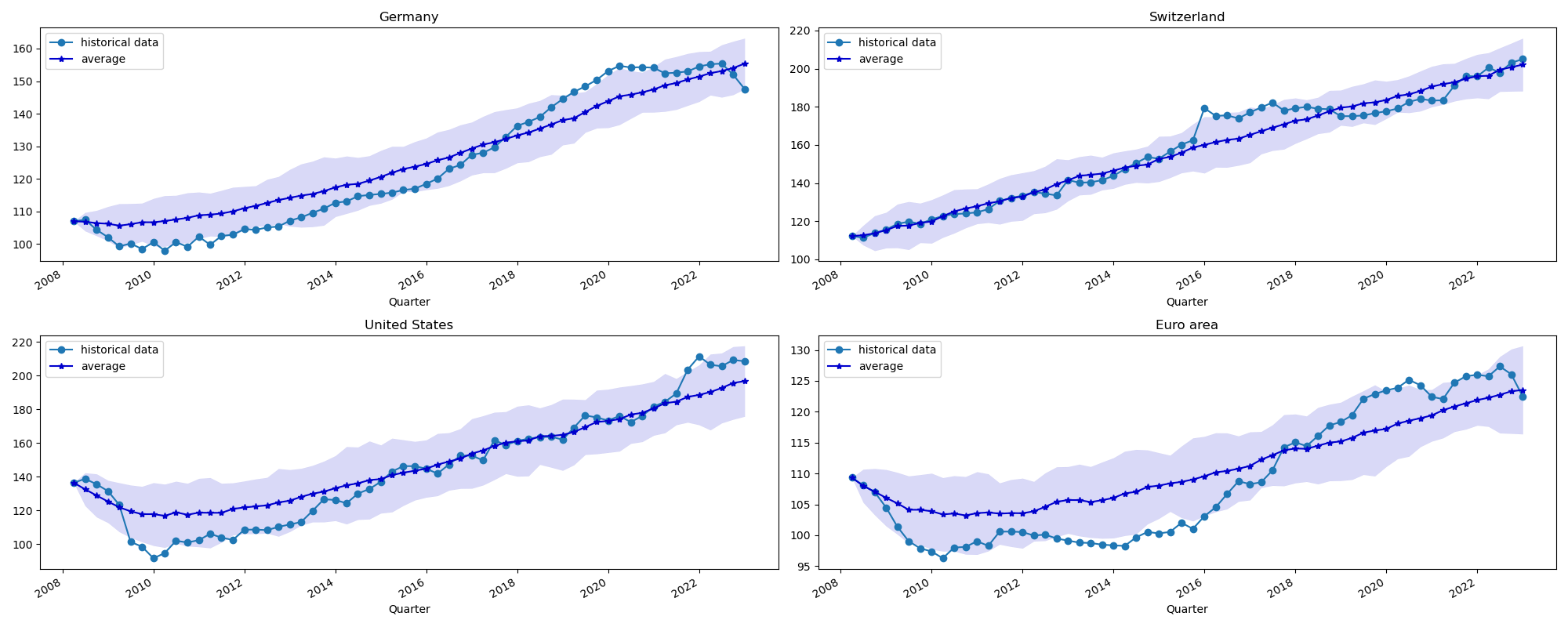

Figure 1: Mean and 95% confidence interval of the housing price index of four countries -

2.

Equation (2.4) refers to the fact that owning a building leads to additional income such as depreciation, maintenance costs, opportunity costs of capital (rent received or saved), or flow of various taxes (see Schulz, (2003)[Chapter 2]). Precisely, if we denote , for , we could write,

(2.5) where is related to maintenance and repair expenditures, is related to the depreciating rate, is related the real estate tax rate, is related the (imputed) rent rate.

-

3.

Moreover, recall that is the noise of the productivity process of the economy, the definition of in (2.3b) allows then to link the real estate market and the productivity (to verify this, one could look at the supply and use tables of INSEE, (2023)222The French National Institute of Statistics and Economic Studies to see the links between real estate activities and others economic sectors).

We are interested now by the law of the solution of (2.3a). We have for ,

| (2.6) |

We therefore get the distribution of conditional on (and not conditional on ) of is Gaussian

| (2.7) | ||||

| (2.8) |

We can rewrite (2.2) is for

The following corollary gives the conditional distribution of the collateral. Its proof is straightforward and directly comes from (2.7).

Corollary 2.2.

For , the law of conditional on is log-Normal with

| (2.9) |

and

| (2.10) |

We now turn our attention to the pricing of a building, taking into account its energy efficiency. We would like to compute the value of a dwelling at time time . We use the actualized sum of the cash flows before the renovation date (taking into account the additional energy costs due to inefficiency of the building), at the renovation date, and after the renovation date (when the building becomes efficient). Moreover, the agent chooses rationally the date of renovation which maximizes the value of his property. We have

Definition 2.3 (Housing price with climate transition).

The market value of the building serving as the collateral to firm at , given the carbon price sequence , is represented by

| (2.13) |

where

-

1.

is a continuous function from to ,

-

2.

for each source of energy , is a derivable function from to ,

-

3.

with .

Moreover, if the optimal renovation date noted exists in , we have

At time , represents the income at when the building is ”perfectly” efficient (i.e. whose the energy efficiency is ) while is the income of a non renovated building whose consequently undergoes the climate transition so that its income is the difference of the income of an equivalent efficient building minus the energy costs.

Therefore, the term is the actualized income at of the property before the optimal renovation date while the term is the actualized income at of the property after . Furthermore, the term is the actualized renovation costs which are performed at time . We note finally that for all , i.e. the agent can always renovate the home right away, but that might not be optimal.

An example of the energy price function

An example of the renovation costs function

We can consider that the costs of renovation of a dwelling , to move its energy efficiency from to , is

| (2.15) |

with and . This choice of allows us to model that when a building has a bad energy efficiency, its renovation is costly.

The expression (2.13) can be simplified in the following proposition.

Theorem 2.4.

Assume that the following conditions are satisfied:

-

1.

the carbon price function is non decreasing on and deterministic;

-

2.

the energy price is non decreasing on for all .

Then, the market value of the building serving as the collateral to firm at , given the carbon price sequence , is given by

| (2.16) |

where

| (2.17) |

and where the optimal date of renovations is given by

| if for all | (2.18) | ||||

| if for all | (2.19) | ||||

| the unique solution of on | (2.20) |

.

Proof.

Let and , the difference between a building with energy efficiency and an equivalent one with efficiency is

after a few calculations, we have

| (2.21) |

According to Standing Assumption 1.3, is deterministic. We can then write

| (2.22) |

The function under the ”inf” that we note

is twice differentiable on , its first order derivative is

and its second order derivative is

- 1.

-

2.

If (2.23) does not have a solution on , then

- (a)

- (b)

∎

The date of renovations (obtained by (2.18), (2.20), and(2.19)) shows that the optimal date chosen to renovate the building mainly depends on the carbon price policy . We also remark that the shock price due to the climate transition is deterministic. This is because the carbon price as well as renovation costs are deterministic. Note that is continuous. If, at date , we realize that the optimal renovation date is , the best thing we can do is to spend at date in order to renovate. We also have the following remarks.

Remark 2.5.

In our model, the usual price of housing is (partly) offset by the costs associated with the climate transition. The dwelling price could also be negative. However, we can imagine many others ways to decline the effects of transition on real estate, for example,

where is a jump diffusion process.

-

1.

We could for example assume that follows a homogenous Markov process: each year , the energy efficiency jumps from state to state , where , so that the price increases or decreases. A heat sieve that is renovated, for example, would therefore see its rating improved and then, its price jump. We would calibrate ”easily” the transition from historical data.

-

2.

We could introduce the climate transition policy by the jump term , inspired by Le Guenedal and Tankov, (2022). That climate policy is characterized, for all , by a process where the Poisson process has a constant arrival rate and is a sequence of i.i.d. random variables, independent from . The choice of expresses the fact that the climate transition could affect real estate price positively (if for example energy renovation work is carried out in a building), or negatively (if for example regulations on housing emissions are tightened.)

An example of the optimal renovation time

With the example of the carbon price in (1.8), the example of the energy price in (2.14), and the example of the renovation costs in (2.15), the optimal renovation time, solution of (2.20) is given by

| (2.24) |

We can clearly remark that the optimal renovation date depends on the climate transition policy ( and ), on the energy prices ( and ), on the renovation costs ( and ), and on the energy efficiencies ( and ).

3 Numerical experiments, estimation and calibration

In this section, we describe how the parameters of multisectoral model, of the firm valuation model, and of the credit risk model are estimated given the historical macroeconomic variables (consumption, labour, output, GHG emissions, housing prices, etc.) as well as the historical credit portfolio data (firms rated and defaulted, collateral, etc.) In a second step, we give the expression of the risk measures (PD, LGD, EL, and UL) introduced in the previous sections, that we compute using Monte Carlo simulations.

3.1 Calibration and estimation

We will calibrate the model parameters on a set of data ranging from time to . In practice, and . From now on, we will discretize the observation interval into steps for . We note . We will not be interested in convergence results here.

3.1.1 Estimation of economic parameters

Using macroeconomic data (output, labor, intermediary input , and the consumption), we can calculate the trajectory of productivity growth achieved. So we have . We can then compute the estimations , , and , parameters , , , and (all defined in Standing Assumption 1.1).

As is a centered O.-U., correspond to the mean. We have

Then, we can take so that for all , then , then

For all , we then have . If we discretize the first equation of (1.1), we also have ,

| (3.1) |

The discrete process is then a VAR process. The estimations and of and respectively are directly got.

3.1.2 Calibration of the real estate parameters

We assume that in the past, carbon price did not have impact on the dwelling price so that for all , defined in (2.17) is zero. Moreover, defined in (2.16), the value of the collateral at , is known. All that remains is to calibrate the parameters of the process defined in (2.3a) and (2.3b). Let us consider a real estate index , then for each , . For calibration, we proceed exactly as Fabozzi et al., (2012). Let assume that the long-term average of the real estate index , introduced in Assumption 2.1, is linear as Frontczak and Rostek, (2015) do, therefore for all , . The estimation of the parameters is realised prior to the others.

3.2 Simulations

In this section as well, the idea here is not to (re)demonstrate or improve convergence results.

3.2.1 Of the productivities and

3.3 Of the housing price

with , and

and is obtained by considering that from (2.17),

and where , , , , and are known, given by (2.24), , and .

Calculating these three quantities enables us to run simulations with confidence intervals.

4 Discussion

In this section, we describe the data used to calibrate the different parameters, we perform some simulations, and we comment the results.

4.1 Data

As in Bouveret et al., (2023), we work on data related to the French economy.

-

1.

Due to data availability (precisely, we do not find public monthly/quaterly data for the intermediary inputs), we consider an annual frequency.

-

2.

Annual consumption, labor, output, and intermediary inputs come from INSEE333The French National Institute of Statistics and Economic Studies from 1978 to 2021 (see INSEE, (2023) for details) and are expressed in billion euros, therefore , , and .

-

3.

For the climate transition, we consider a time horizon of ten years with as starting point, a time step of one year and as ending point. In addition, we will be extending the curves to 2034 to see what happens after the transition, even though the results will be calculated and analyzed during the transition.

-

4.

The 38 INSEE sectors are grouped into four categories: Very High Emitting, Very Low Emitting, Low Emitting, and High Emitting, based on their carbon intensities.

-

5.

The carbon intensities are calibrated on the realized emissions from Eurostat, (2023) (expressed in tonnes of CO2-equivalent) between 2008 and 2021.

-

6.

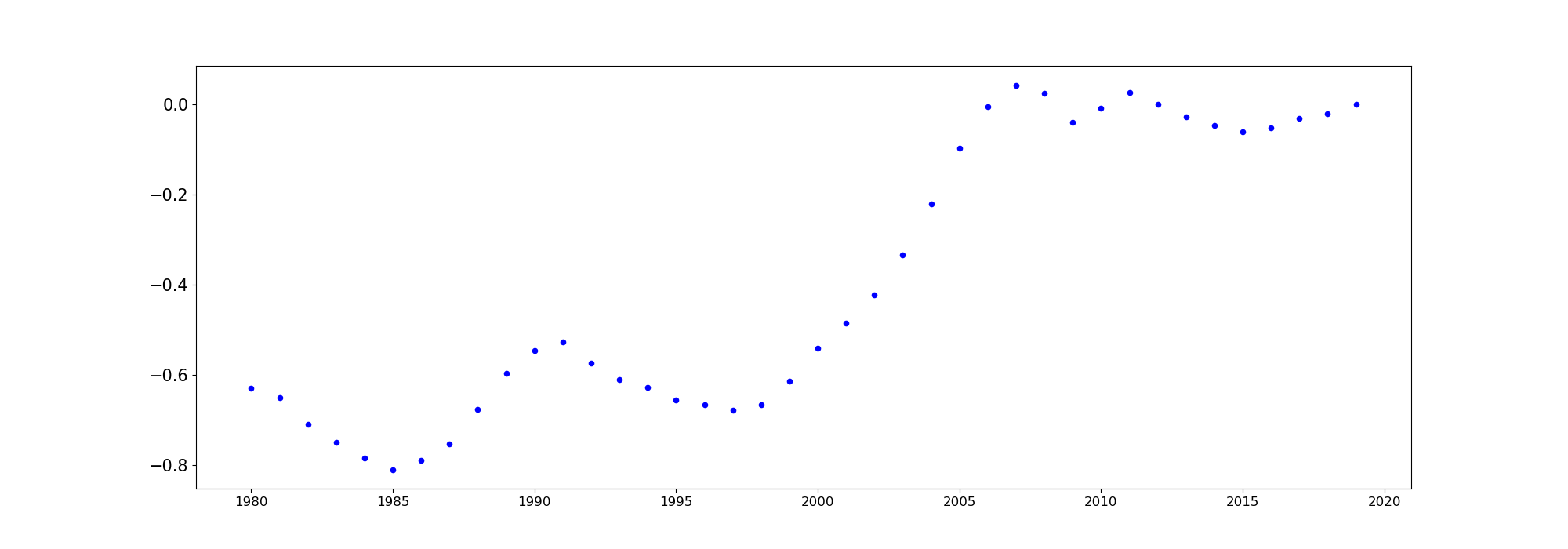

Metropolitan France housing price index comes from OECD data and are from 1980 to 2021 (see OECD Stat, (2024) for details) in Base 2015. We renormalize in Base 2021. We plot in Figure 2 below.

Figure 2: Log of the HPI in Base 2021 from 1980 to 2021

4.2 Definition of the climate transition

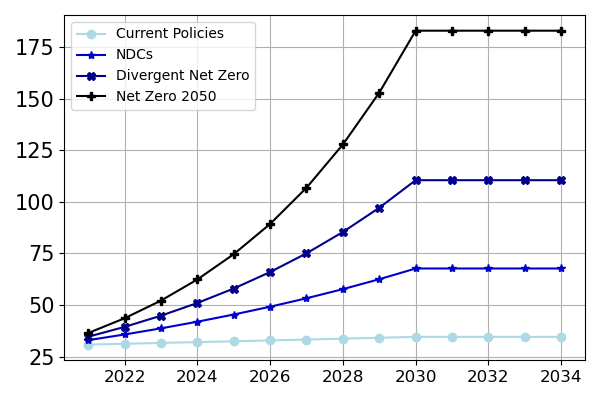

We consider four deterministic transition scenarios giving four deterministic carbon price trajectories. The scenarios used come from the NGFS simulations, whose descriptions are given by NGFS, (2022) as follows:

-

1.

Net Zero 2050 is an ambitious scenario that limits global warming to through stringent climate policies and innovation, reaching net zero emissions around 2050. Some jurisdictions such as the US, EU and Japan reach net zero for all GHG by this point.

-

2.

Divergent Net Zero reaches net-zero by 2050 but with higher costs due to divergent policies introduced across sectors and a quicker phase out of fossil fuels.

-

3.

Nationally Determined Contributions (NDCs) includes all pledged policies even if not yet implemented.

-

4.

Current Policies assumes that only currently implemented policies are preserved, leading to high physical risks.

For each scenario, we compute the carbon price in and the evolution rate as defined in (1.8).

| Current Policies | NDCs | Divergent Net Zero | Net Zero 2050 | |

|---|---|---|---|---|

| (in euro/ton) | 30.957 | 33.321 | 32.963 | 34.315 |

| (in %) | 1.693 | 7.994 | 12.893 | 17.935 |

We can then compute the carbon price, whose evolution is plotted in Figure 7(a), at each date using (1.8).

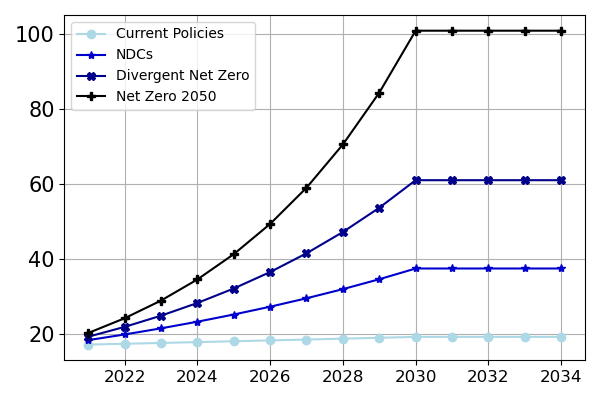

For the energy price, we consider electricity as the unique source of energy. Then, we assume a linear relation between the electricity and the carbon price inspired by Abrell et al., (2023), where a variation of the carbon price is linked withe the variation of the electricity by a the pass-through rate noted . This means that and define in (2.14) are respectively and . For France, we take the electricity price euro per Kilowatt-hour and (see Abrell et al., (2023)) ton per Kilowatt-hour. Its evolution is plotted in Figure 7(b).

For the renovation costs to improve a building for the energy efficiency to as defined in (2.15), we take euro per kilowatt-hour and per square meter (€/KWh.m2) and .

4.3 Estimations

4.3.1 Economic parameters

We therefore calibrate , , , and as an Ornstein-Uhlenbeck, we detailed in Section 3.1.1.

| Emissions Level |

|

|

|

|

||||

|---|---|---|---|---|---|---|---|---|

| 5.602 | 8.475 | 3.834 | 12.099 |

| Emissions Level |

|

|

|

|

||||

|---|---|---|---|---|---|---|---|---|

| Very High | -0.201 | -0.056 | 0.113 | -0.036 | ||||

| High | 0.091 | 0.420 | 0.214 | 0.015 | ||||

| Low | -0.103 | -0.003 | -0.122 | 0.160 | ||||

| Very Low | 0.493 | 0.168 | 0.290 | 0.652 |

The eigenvalues of are which implies that is a Hurwitz matrix, therefore is weak-stationary as assumed. Moreover, .

| Emissions Level |

|

|

|

|

||||

|---|---|---|---|---|---|---|---|---|

| Very High | 0.473 | 0.013 | 0.072 | 0.092 | ||||

| High | 0.013 | 0.208 | 0.039 | 0.037 | ||||

| Low | 0.072 | 0.039 | 0.059 | 0.020 | ||||

| Very Low | 0.092 | 0.037 | 0.020 | 0.068 |

4.3.2 The housing pricing index (HPI)

We write the housing price index in Base 2021 and we apply the logarithm function. This means that as shown in Figure 2. We can therefore calibrate , and . The values are presented in Table 5 below.

| Parameter | Value |

|---|---|

| 0.024 | |

| -0.884 | |

| 0.026 | |

| 0.050 | |

| [-0.019, -0.042, -0.017, 0.015] |

4.4 Simulations and discussions

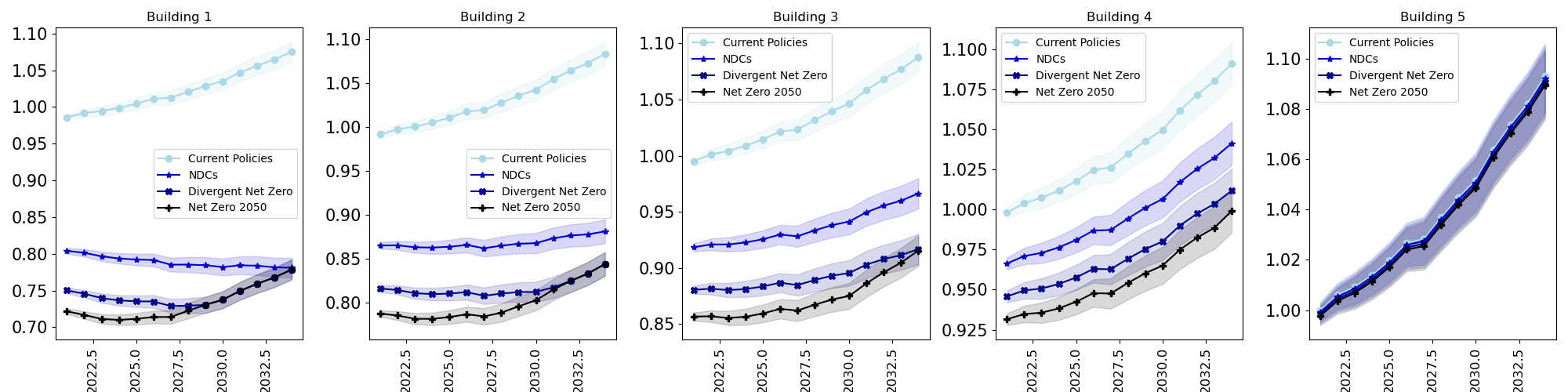

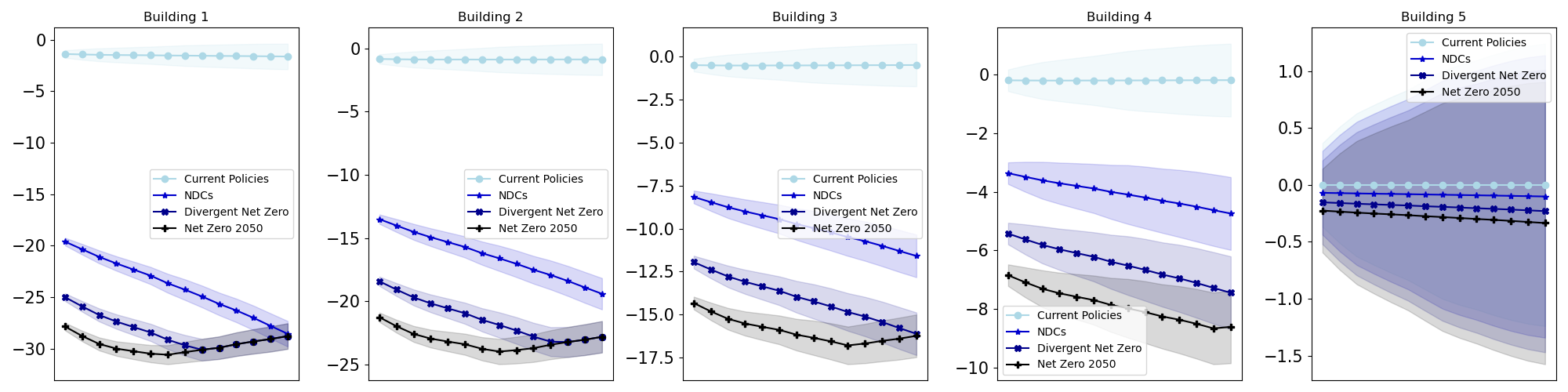

In order to illustrate the impact of the carbon price on the housing market, we consider here 5 buildings located in the French economy whose characteristics: the price at , , the energy efficiency , the surface , are given in Table 6

| Building | |||||

|---|---|---|---|---|---|

| 4000 | 4000 | 4000 | 4000 | 4000 | |

| 320. | 253. | 187. | 120. | 70. | |

| 25.0 | 25.0 | 25.0 | 25.0 | 25. |

Precisely, we consider 5 apartments of 25 square meters whose price of the square meter fixed to 4000 euros in is the same for all, but whose the energy efficiency are different. Moreover, we assume that the optimal energy efficiency equals to kilowatt hour per square meter per year (see Total Energies, (2024)) is reached. We can compute and summarize in table 7 the optimal renovation date whose the expression is given in (2.24).

| Emissions level | Building 1 | Building 2 | Building 3 | Building 4 | Building 5 |

| Current Policies | 89.32 | 115.16 | 144.325 | 185.32 | 304.14 |

| NDCs | 14.21 | 18.32 | 22.96 | 29.48 | 48.38 |

| Divergent Net Zero | 8.81 | 11.36 | 14.24 | 18.28 | 29.99 |

| Net Zero 2050 | 6.33 | 8.17 | 10.23 | 13.14 | 21.57 |

We observe in Table 7 that the optimal renovation date increases:

-

1.

when the building is efficient ( decreases) and when : there is no point in renovating an efficient building.

-

2.

when the climate transition speeds up: energy costs become unbearable if we do not renovate quickly,

-

3.

when the renovation costs increases: if renovation costs become too high, it is better to bear the energy costs.

As in the case of the firm values, we normalize the building values by the price of the most efficient building (Building 5) at the beginning of the transition for ease of reading.

We can therefore observe that, since in the scenario Current Policies, the price of electricity does not really increase (see Figure 7(b)), the optimal renovation dates are very large (much larger than the potential lifespan of the building). Therefore, if there is no climate transition, it is not necessary to renovate (for this reason at least). A direct consequence of low-cost energy and a very distant renovation date is that the price of housing continues to grow as it has historically.

| Emissions level | Building 1 | Building 2 | Building 3 | Building 4 | Building 5 |

| Current Policies | -1.506 | -0.870 | -0.506 | -0.209 | 0.000 |

| NDCs | -22.646 | -15.526 | -9.351 | -3.848 | -0.080 |

| Divergent Net Zero | -28.007 | -20.721 | -13.480 | -6.151 | -0.179 |

| Net Zero 2050 | -29.776 | -23.055 | -15.744 | -7.614 | -0.263 |

For each scenario and each building, each point of the curve represents the value of the building at date if the optimal renovation date is (if ) or was (if ) . Almost all the building prices continue to grow with time as shown on Figure 3, but these growths are more or less affected by their energy efficiency. Moreover, given that the impact of the transition on price through energy and renovation costs, the later are stronger in the beginning. In fact, the more time passes, the closer we get to the end the climate transition ( in our scenarios) as well as the potential date of renovations. If we look at Figure 4, we remark that when the valuation date is later than the optimal renovation date, the best thing to do is to renovate directly. This stabilizes or even reverses the price decline. Moreover, by adding the energy costs before renovations, we could reach 20 to 30% of depreciation when the carbon price (so the energy price) is pretty high. This seems consistent with the idea that a thermal sieve loses all its value and could become impossible to sell, because of the enormous costs involved in owning it.

Finally, it should be noted that the property value discounts obtained in this work correspond to statistical observations, for example by de Ayala et al., (2016).

Conclusion

The aim of this work was to propose a model to assess and quantify the impact of the climate transition on real estate prices. We first considered that real estate is an asset belonging to an economy organized in sectors, driven by dynamic and stochastic productivity following an Ornstein-Uhlenbeck dynamic, and subject to a dynamic and deterministic carbon price. Then, we assumed that the carbon price has two effects on an energy-inefficient building: it incurs additional energy costs, the price of energy is an increasing function of the carbon price, on the other hand, it is forced to be renovated to become efficient, but at a cost that depends on its inefficiency. The proposed model is built from two approaches to real estate modeling found in the literature: the income approach and the sales comparison approach. We obtained that the price discount due to inefficiency depends on the carbon intensity of the housing, the carbon price process, the unit renovation costs, the link between the carbon price and the energy price, etc. This work has many practical applications both in government policies (for defining of transition speed, renovation policies, etc.), in asset management (for portfolio construction notably) and in credit risk (for collateral selection and for loss modelling). Finally, it opens the door to several extensions. The building could be renovated several times over several years before reaching maximum energy efficiency. Could the renovation increase the price of the building instead of simply making it regain the historical trend? We can also model the physical risk, which would depend in particular on the location of the dwelling.

References

- Abrell et al., (2023) Abrell, J., Kosch, M., and Blech, K. (2023). Rising electricity prices in europe: The impact of fuel and carbon prices. Available at SSRN 4566679.

- Aydin et al., (2020) Aydin, E., Brounen, D., and Kok, N. (2020). The capitalization of energy efficiency: Evidence from the housing market. Journal of Urban Economics, 117:103243.

- Bouveret et al., (2023) Bouveret, G., Chassagneux, J.-F., Ibbou, S., Jacquier, A., and Sopgoui, L. (2023). Propagation of carbon tax in credit portfolio through macroeconomic factors. arXiv preprint arXiv:2307.12695.

- de Ayala et al., (2016) de Ayala, A., Galarraga, I., and Spadaro, J. V. (2016). The price of energy efficiency in the spanish housing market. Energy Policy, 94:16–24.

- de la Cruz and Jimenez, (2020) de la Cruz, H. and Jimenez, J. C. (2020). Exact pathwise simulation of multi-dimensional ornstein–uhlenbeck processes. Applied Mathematics and Computation, 366:124734.

- European Parliament, (2002) European Parliament (2002). 91/ec of the european parliament and of the council of 16 december 2002 on the energy performance of buildings. Off. J. Eur. Communities, 4(2003):L1.

- European Union, (2022) European Union (2022). Energy performance of buildings directive.

- Eurostat, (2022) Eurostat (2022). Product - products datasets - eurostat.

- Eurostat, (2023) Eurostat (2023). Air emissions intensities by NACE rev. 2 activity.

- Fabozzi et al., (2012) Fabozzi, F. J., Shiller, R. J., and Tunaru, R. S. (2012). A pricing framework for real estate derivatives. European Financial Management, 18(5):762–789.

- Franke and Nadler, (2019) Franke, M. and Nadler, C. (2019). Energy efficiency in the german residential housing market: Its influence on tenants and owners. Energy policy, 128:879–890.

- Frontczak and Rostek, (2015) Frontczak, R. and Rostek, S. (2015). Modeling loss given default with stochastic collateral. Economic Modelling, 44:162–170.

- Gobet and She, (2016) Gobet, E. and She, Q. (2016). Perturbation of Ornstein-Uhlenbeck stationary distributions: expansion and simulation. working paper or preprint.

- Gravelle and Rees, (2004) Gravelle, H. and Rees, R. (2004). Microeconomics. Pearson education.

- INSEE, (2023) INSEE (2023). Summary tables : Sut and tiea in 2021 - the national accounts … - insee. https://www.insee.fr/en/statistiques/6439451?sommaire=6439453. Accessed: Jan. 16, 2024.

- Kanagawa, (1988) Kanagawa, S. (1988). On the rate of convergence for maruyama’s approximate solutions of stochastic differential equations. Yokohama Math. J, 36(1):79–86.

- Le Guenedal and Tankov, (2022) Le Guenedal, T. and Tankov, P. (2022). Corporate debt value under transition scenario uncertainty. Available at SSRN 4152325.

- Li and Wu, (2019) Li, C. and Wu, L. (2019). Exact simulation of the ornstein–uhlenbeck driven stochastic volatility model. European Journal of Operational Research, 275(2):768–779.

- Maruyama, (1955) Maruyama, G. (1955). Continuous markov processes and stochastic equations. Rendiconti del Circolo Matematico di Palermo, 4:48–90.

- Moody’s, (2022) Moody’s (2022). Non-performing and re-performing loan securitizations methodology.

- NGFS, (2022) NGFS (2022). NGFS Scenarios Portal. NGFS Scenarios Portal.

- (22) OECD (2024a). Oecd compendium of productivity indicators 2021 – household spending.

- (23) OECD (2024b). Oecd compendium of productivity indicators 2021 – investment by asset type.

- OECD Stat, (2024) OECD Stat (2024). National and Regional House Price Indices: France. OECD Stat.

- Schulz, (2003) Schulz, R. (2003). Valuation of properties and economic models of real estate markets. PhD thesis, Humboldt University of Berlin.

- Ter Steege and Vogel, (2021) Ter Steege, L. and Vogel, E. (2021). German residential real estate valuation under ngfs climate scenarios. Technical report, Technical Paper.

- Total Energies, (2024) Total Energies (2024). Que signifie la classe énergie d’un logement? Accessed: 2024-07-15.

Appendix A Ornstein-Uhlenbeck process

Let , from the second equation of (1.1),

However, for all , from the first equation of (1.1),

therefore,

We then have

where is defined in (1.5).

Let pose and , for . Then

By integration by parts, as for all , we have

Finally

The conclusion follows.

Appendix B Figures