Short-maturity asymptotics for VIX and European options in local-stochastic volatility models

Abstract.

We derive the short-maturity asymptotics for European and VIX option prices in local-stochastic volatility models where the volatility follows a continuous-path Markov process. Both out-of-the-money (OTM) and at-the-money (ATM) asymptotics are considered. Using large deviations theory methods, the asymptotics for the OTM options are expressed as a two-dimensional variational problem, which is reduced to an extremal problem for a function of two real variables. This extremal problem is solved explicitly in an expansion in log-moneyness. We derive series expansions for the implied volatility for European and VIX options which should be useful for model calibration. We give explicit results for two classes of local-stochastic volatility models relevant in practice, with Heston-type and SABR-type stochastic volatility. The leading-order asymptotics for at-the-money options are computed in closed-form. The asymptotic results reproduce known results in the literature for the Heston and SABR models and for the uncorrelated local-stochastic volatility model. The asymptotic results are tested against numerical simulations for a local-stochastic volatility model with bounded local volatility.

Key words and phrases:

VIX option, short-maturity asymptotics, local-stochastic volatility models1. Introduction

The CBOE Volatility Index (VIX) is the main volatility benchmark of the U.S stock market, and provides a measure of the implied volatility of options with maturity of 30 days on the S&P 500 index. It is defined in terms of an expectation in the risk-neutral measure , where is the equity index S&P 500 at time , and days. The expectation is computed by replication in terms of market observed SPX option prices - see the VIX White Paper [9] for the details of the methodology. Since 2022, CBOE has started reporting also the CBOE 1-day Volatility Index (VIX1D) [8], which is an analog of the VIX index computed using the PM-settled weekly SPX options which mature on the same day and the next day day) as the index date.

The volatility index VIX is used by market participants to speculate on and hedge volatility risk. Several volatility derivatives which can be used for this purpose are traded on CBOE Options Exchange: futures contracts on VIX are traded since 2004, and VIX options are traded since 2006. In view of the popularity of these contracts, a great deal of work has been devoted in the literature to the valuation of volatility derivatives.

The simplest approach for pricing volatility options is based on modeling the instantaneous variance as a stochastic process. Detemple and Osakwe (2000) [11] presented both European and American volatility options pricing under several popular diffusion models for . Carr et al. (2005) [5] presented results for volatility options under pure jump models with independent increments. Sepp (2008) [38, 39] priced volatility derivatives under a square root volatility model with jumps. Goard and Mazur (2013) [18] derived analytical results for VIX options in the 3/2 stochastic volatility model, and Baldeaux and Badran (2014) [1] extended this model for VIX option pricing by adding jumps. A survey of existing results on volatility derivatives (up to 2010) was given by Carr and Lee (2010) [6].

Recently, the pricing of volatility derivatives has been extended to stochastic volatility models where the volatility is driven by a fractional Brownian motion. Horvath et al. [22] introduced the class of modulated Volterra processes which can accommodate observed VIX smiles. Jacquier et al. (2021) [24] derive short-maturity SPX and VIX option prices for a wide class of multi-factor models of this type. An empirical analysis of the SPX and VIX option markets under rough and stochastic volatility models was given by Rømer (2022) [37].

We mention also the martingale optimal transport approach which was applied to the problem of simultaneous calibration to the SPX and VIX implied volatility smiles in [19]. This approach is model-independent and aims to calibrate the joint distribution of the underlying (SPX) and of the VIX at several maturities of interest, under appropriate martingale constraints.

In this paper the asset price is assumed to follow a local-stochastic volatility model under the risk-neutral probability measure :

| (1) | |||

with initial conditions , where are correlated standard Brownian motions with correlation , is the risk-free rate and is the dividend yield. For simplicity we assume that the functions and are time-homogeneous.

The model (1) is a continuous path Markovian local-stochastic volatility model. It nests several popular models in the literature. When it reduces to the usual stochastic volatility models: for example Heston model [21] (), Hull-White model [23] (). When and it reduces to the SABR model [20].

The short maturity asymptotics of European option prices in local-stochastic models have been studied by Forde and Jacquier [14] (in the uncorrelated limit) using large deviations methods. Local-stochastic volatility models were studied by Pagliarani and Pascucci [30] and Lorig, Pagliarani and Pascucci [27], using PDE methods. These methods extend similar small maturity expansions which were obtained for stochastic volatility models in [20, 13, 15]. Bompis and Gobet (2018) [4] used Malliavin calculus methods to derive short-maturity asymptotics for the implied volatility of European options in local-stochastic volatility models with Heston-type volatility.

Fewer results are available in the literature on the short-maturity asymptotics of the VIX options in local-stochastic volatility models. We mention the work of Forde and Smith [16], where the asymptotics of VIX options is obtained in an uncorrelated local-stochastic model. As an application, they obtain the first two terms in the expansion of the VIX smile around the ATM point in the uncorrelated CEV-Heston model. However, their model includes a -dependent drift for the variance process, and is different from our model (1). To our knowledge, the short-maturity of VIX options in the correlated local-stochastic volatility model has not been treated previously in the literature.

An alternative to local-stochastic volatility models which allows independent control of the European and VIX smiles are stochastic volatility models with local correlation. The short-maturity asymptotics of VIX options in such models was obtained by Forde and Smith [16] in a Markovian setting.

The paper is organized as follows. In Section 2 we fully specify the model under appropriate technical conditions, and give the definition of the VIX volatility index and of options on this index.

Section 3 presents the short-maturity asymptotics of European (SPX) options under the model (1). The main result is Theorem 3.1, which uses large deviations theory, see [10, 41] for background, to establish the short-maturity asymptotics in terms of a rate function , which is given by the solution of a two-dimensional variational problem. After a careful application of the Cauchy-Schwarz inequality to obtain a lower bound for the variational problem and showing the lower bound can be achieved, we reduce the variational problem further to that of finding the extrema of a function of two real variables, which is feasible for practical applications. The function depends on an auxiliary function which depends only on the volatility process, and is represented as the solution of a one-dimensional variational problem.

In Section 4, we give the short-maturity asymptotics for VIX options under the model (1). The short-maturity asymptotics is given in terms of a rate function , which is given again by an extremal problem of a function of two variables. The extremal problem depends on the same auxiliary function as in the European options case.

Section 5 studies the properties of the function . We give explicit solutions for for two particular forms of the variance process which are often encountered in practice: (i) corresponding to log-normal volatility (SABR-type models), and (ii) corresponding to a square-root volatility specification (Heston-type models).

In Section 6, we present a few applications of the theoretical results obtained in the paper, and give explicit results for the asymptotic implied volatility of European and VIX options in local-stochastic volatility model with log-normal (SABR-type) and Heston-type volatility. We check explicitly that our results recover existing results in the literature in various limiting cases: uncorrelated local stochastic volatility, pure stochastic volatility models, and local volatility model.

Finally, in Section 7 we compare the theoretical predictions for the asymptotic short-maturity of European and VIX options in local-stochastic volatility models with a numerical simulation of this model using Monte Carlo methods. For this test we use the Tanh-model for the local volatility function , which was introduced previously in [14]. We observe good agreement between the asymptotic results and the numerical simulation for sufficiently small option maturity.

We present a few basic concepts about large deviations theory in Appendix A. The proofs of the results presented in the main text are presented in Appendix B, Appendix C and Appendix D. The full result for the ATM VIX implied volatility convexity in the local-stochastic volatility model with SABR-type volatility will be presented in Appendix E.

2. Model Specification

We start by formulating technical conditions and assumptions for the parameters of the model (1). First, we assume that and are uniformly bounded.

Assumption 2.1.

We assume that and are uniformly bounded:

| (2) |

We also assume that is decreasing, which satisfies the leverage effect in finance. More precisely, when is not a constant function, we assume that is strictly decreasing so that its inverse function exists. We also provide the following assumptions on Lipschitz continuity.

Assumption 2.2.

We assume that is -Lipschitz and is -Lipschitz.

In addition, we impose the following assumption on the and that appear in the diffusion terms of (1) that is needed for the small-time large deviations estimates for (1).

Assumption 2.3.

We assume that and . Moreover, there exist some constants such that for any , and .

Next, we will show that under the Assumption 2.1, all the moments of process are finite.

Proposition 2.1.

Under Assumption 2.1, for any , there exists some , such that for any sufficiently small .

Throughout the paper, we assume that the discounted asset price is a martingale. We quote the results of [26] expressed in the notations of our paper, for the stochastic volatility model obtained by taking and in Eqn. (1). 111Some typos in [26] were corrected in the paper [7].

Proposition 2.2.

Consider the stochastic volatility model

| (3) |

where are correlated standard Brownian motions with correlation . The asset price is a martingale if the following condition is satisfied

| (4) |

We have the following corollary.

Corollary 2.1.

Assume is bounded and is finite. Then the limit (4) is for positive correlation , takes a finite value if and is for . Thus, is a martingale provided that .

Finally, we assume the -th moment of is finite for some .

Assumption 2.4.

There exists some , such that there exists some , such that for any sufficiently small .

Remark 2.1.

Assumption 2.4 is a mild assumption. As an illustration, we give a condition for the stochastic volatility model (3) such that Assumption 2.4 holds. This condition follows directly from Lions and Musiela (2008) [26] which states that if the following limits exist

| (5) |

then for any

| (6) |

there exists some , such that for any sufficiently small . In particular, under Assumption 2.1, , and the condition (6) reduces to

| (7) |

which provides a sufficient condition for Assumption 2.4 to hold for the stochastic volatility model (3).

2.1. VIX futures and VIX options

The CBOE Volatility Index (VIX) is a measure of the S&P500 expected volatility, which is published by the Chicago Board Options Exchange. This index is defined by the risk-neutral expectation

| (8) |

with days. This expectation is estimated from the prices of current (as of ) call and put options on the SPX index, see [9].

CBOE lists futures and options on the index with several maturities . VIX option contracts pay at time an amount linked to the observed at the same time.

Under a model of type

| (9) |

with a non-negative stochastic process with continuous paths (no jumps) which may depend on , the index is given by the risk-neutral expectation

| (10) |

More generally, under model (1), the index is given by:

| (11) |

The price of a futures contract on the index with maturity is given by the risk-neutral expectation

| (12) |

The prices of VIX calls and puts are given by risk-neutral expectations

| (13) | |||

| (14) |

We impose the following definition to distinguish the VIX options into three cases.

Definition 2.1.

VIX options with maturity are at-the-money (ATM) if . VIX call options are in-the-money (ITM) if and out-of-money (OTM) if . Analogously, VIX put options are ITM if and OTM if .

3. Short-maturity asymptotics of European options

In this section, we consider the European options in the model (1), with denoting the price of call option and denoting the price of call option. We have the following short-maturity asymptotics for European options.

Theorem 3.1.

Suppose Assumptions 2.1, 2.3 and 2.4 hold. The short maturity asymptotics of OTM European options in the local-stochastic volatility model (1) are as follows.

(i) The short-maturity asymptotics of OTM European call options is

| (15) |

with

| (16) |

where

| (17) |

(ii) The short-maturity asymptotics of OTM European put options is

| (18) |

where is defined in (16) with .

This result simplifies in the uncorrelated case, and is expressed as the solution of a one-dimensional extremal problem. We have

| (19) |

where

| (20) |

The function coincides with the rate function for Asian options in local volatility models with local volatility . The solution of the variational problem for this function was given in [33], and explicit solutions were given for in [33] and for in [34].

Next, let us present the asymptotics for ATM European options.

Theorem 3.2.

Theorem 3.2 shows that the prices of ATM European options are of the order as , and it provides the exact formula for the leading-order term.

4. Short-maturity asymptotics of VIX options

As , the VIX futures prices in the model (1) approach to . Therefore, in the short-maturity limit, we will refer to VIX options as OTM/ITM by referencing to .

For sufficiently small , VIX options are essentially European options on combinations of and . The following result makes this statement more precise.

Proposition 4.1.

Note that is of order and is of order as . Proposition 4.1 implies that is of the order in terms of expectation. Next, as a corollary of Proposition 4.1, we will provide an upper bound for and show that it is also of the order in terms of expectation.

Corollary 4.1.

Note that in Corollary 4.1, a sufficient condition for the additional assumption as to hold is when (see the discussions in Remark 2.1).

4.1. Particular cases

For a few particular cases of the drift function for the process we have closed form expressions for in terms of . Recall that the stochastic volatility models are obtained in the limit :

| (29) | |||

with initial conditions , where are correlated standard Brownian motions with correlation , is the risk-free rate and is the dividend yield.

Proposition 4.2.

(i) Assume that the asset price follows the stochastic volatility model (29) and is constant. Then the price of a VIX call option is expressed as

| (30) |

(ii) Assume that the asset price follows the stochastic volatility model (29) and that the drift term of the process is mean-reverting , where . This includes the Cox-Ingersoll-Ross process as a special case. For this case we have

| (31) |

Remark 4.1.

In general, since is a time-homogeneous Markov process, in stochastic volatility models (29), we have

| (32) |

and the VIX option prices are given by

| (33) |

Remark 4.2.

The result of Proposition 4.2 can be extended to the more general local-stochastic volatility model (1) with for the particular case when and are uncorrelated. 222Note that does not satisfy Assumptions 2.1, 2.2 and 2.3. However, Assumptions 2.1, 2.2 and 2.3 are used to obtain the asymptotic results in Section 3 and Section 4 as , whereas here we obtain some explicit formula under this special case for any finite , that does not rely on Assumptions 2.1, 2.2 and 2.3 A similar comment holds for case 2) in Proposition 4.2 where is not bounded.

(i) Assuming we have

| (34) |

For this case VIX options become essentially options on the product .

| (35) |

and the short-maturity asymptotics can be easily obtained as a European call option.

(ii) Assuming , we have

| (36) |

such that

| (37) |

If we let , then the second term proportional to vanishes, and we obtain , which is similar to the previous case. The short-maturity asymptotics can be again easily obtained as a European call option. However, at finite , it is a bit more complicated than European options, and it will involve solving a slightly different variational problem.

4.2. The main result

We first present the main result for OTM VIX options in the local-stochastic volatility model (1).

Theorem 4.1.

Under the settings of Corollary 4.1, suppose Assumption 2.3 holds and further assume as , then the short maturity asymptotics of OTM VIX options in the local-stochastic volatility model (1) are as follows.

(i) The asymptotics of the OTM VIX call option is

| (38) |

where

| (39) |

where

| (40) |

The rate function for OTM VIX options depends on the auxiliary function . The same function appears in the short-maturity asymptotics of the European options, see (17). We study the general properties of this function and give closed form evaluations for commonly used cases for in Section 5.

Stochastic volatility models. The stochastic volatility model (29) is obtained by taking in (1). This case is not covered by directly taking into Theorem 4.1. VIX options in the stochastic volatility model are effectively European-type options on .

Restricting further to models with time-homogeneous volatility dynamics, we have , see Remark 4.1, and the VIX options are European-type options on . For these models, the VIX futures price is as .

Proposition 4.3.

Uncorrelated case. In the uncorrelated limit the variational problem for the rate function in Theorem 4.1 simplifies, as shown in the next result.

Corollary 4.2.

Next, we present the asymptotics for ATM VIX options.

Theorem 4.2.

Theorem 4.2 shows that the prices of ATM VIX options are of the order as , and it provides the exact formula for the leading-order term.

5. The function

We study in this section in more detail the function

| (46) |

which appears in the short maturity limit of both European and VIX options in the local-stochastic volatility model considered.

The function appearing in the short-maturity limit for the European options is related to as

| (47) |

Next, we will show that the function can be evaluated explicitly for two commonly used vol-of-vol functions .

5.0.1. Constant

This case corresponds to log-normal type process for . For this case we have an explicit result.

Proposition 5.1.

The function for the case is given by

| (48) |

where is

| (49) |

The function is defined as

| (50) |

where are the solutions of the equation

| (51) |

Remark 5.1.

For numerical evaluation of it is convenient to use the expansion around

| (52) |

The coefficients of the first ten terms in this expansion are tabulated in Section 5 of [29]. This series converges for , see Proposition 4.2(i) in [29]. Outside of the convergence region, the function can be well approximated by tail expansions for obtained in [32].

The function has the following properties:

(i) . At this point the optimal path is constant.

5.0.2.

This corresponds to a Heston-type model, where the variance process has a square-root type volatility:

| (54) |

Proposition 5.2.

The function for the Heston-type model is

| (55) |

where is a rate function giving the joint asymptotics of the time-integral and terminal value for the process (54) as . In this limit satisfies a LDP with rate function

| (56) |

where the cumulant function is

| (57) |

We are now in a position to compute the rate function from (56). The result can be put into an explicit form as a double expansion in .

Proposition 5.3.

The first few terms in the expansion of the rate function for the square root model are given by:

| (58) |

where we denote by the set of all terms of the form with .

Remark 5.2.

As a consistency check, we can calculate that has the expansion: . The first three terms reproduce the expansion of the rate function for Asian options in the square-root model, given in equation (19) of [34].

Remark 5.3.

In a similar way, we get that has the expansion

| (59) |

which is the same as the expansion of the rate function for European options in the square-root model

| (60) |

This follows by substituting into

and taking .

6. Detailed predictions and comparison with the literature

We present in this section predictions following from the theoretical results obtained above. We start in Section 6.1 with the example of a simple stochastic volatility model, the log-normal SABR model, for which the exact short maturity asymptotics is known. We show that the results of this paper reproduce the known results for this case.

In Sections 6.2 and 6.3 we discuss two local-stochastic volatility models with popular volatility specification: log-normal (SABR-type) and square-root (Heston-type) volatility, respectively. For both cases we derive analytical results for the ATM implied volatility and skew for both European and VIX options, for arbitrary local volatility function . These expressions are relevant for calibration to SPX and VIX smiles. We show that our results reduce to previously known expressions in various limiting cases of pure stochastic volatility models and of the uncorrelated local-stochastic volatility models [14].

6.1. Log-normal SABR model

The log-normal SABR model is obtained by taking and log-normal volatility .

European options. The rate function of the European options given by Theorem 3.1 is

| (61) |

Taking here and substituting the explicit form of the function from (48) we have

| (62) |

Denote and . The rate function becomes

| (63) |

Let us compare this with the rate function for the short maturity asymptotics of European options in the log-normal SABR model given in equation (6.2) of [35]. Expressed in the notations of the current paper, the SDE of the model becomes , which corresponds to . The rate function from [35] is

| (64) |

Substituting we see that they agree.

In [35] evidence has been presented that the solution of the extremal problem (64) can be expressed in closed form as

| (65) |

This was tested by verifying that it correctly reproduces the first two terms of the series expansion in of the solution of the extremal problem (64), and also by comparing with numerical solution of the extremal problem. In the uncorrelated limit the analytical result was proved explicitly.

The result (65) reproduces the well-known formula for the short-maturity asymptotics of the implied volatility in the log-normal SABR model [20]

| (66) |

VIX options. We consider next the short-maturity asymptotics of VIX options in the mean-reverting log-normal SABR model with volatility specification

This is a particular case of the class of models covered by Proposition 4.3. For this case we have with and .

The VIX futures price is . As , VIX call options are OTM for and VIX put options are ITM for .

The short maturity limit of the OTM VIX options is given by Proposition 4.3 with the replacement . We get

| (67) |

The short-maturity limit of the VIX implied volatility is given by:

| (68) |

This agrees with the result in Sec. 1.8.1 of Forde and Smith [16]. Denote the short-maturity asymptotics of the VIX implied volatility given by (68) as .

The first few terms in the expansion of the asymptotic VIX implied volatility in powers of log-strike are

| (69) |

The asymptotic VIX implied volatility (68) has the following properties:

-

•

The VIX implied volatility vanishes for , since the VIX is bounded below as .

-

•

From the expansion (69) we see that the ATM VIX volatility is

-

•

For , the smile is up-sloping and concave in . For the smile is flat with .

6.2. Local-stochastic volatility model with log-normal volatility

In this section we consider the local-stochastic volatility model with log-normal volatility

| (70) |

where are correlated with correlation . Denote the first few coefficients in the expansion of the local volatility function in powers of log-price around .

We give analytical results for the ATM volatility, skew and convexity of the implied volatility for the European and VIX options in this model.

6.2.1. European options

The implied volatility of European options in the lognormal local-stochastic volatility model is given by the following result.

Proposition 6.1.

The implied volatility of European options in the model (70) has the expansion in log-strike

| (71) |

where the at-the-money implied volatility is

| (72) |

the ATM skew is

| (73) |

and the ATM convexity is

| (74) |

Remark 6.2.

The ATM skew (73) is the sum of two terms, which correspond to the skew in the stochastic volatility model (obtained by taking ) , and to the skew in the local volatility model (obtained in the limit ) .

Remark 6.3.

A similar decomposition holds also for the ATM convexity (74). The first term is the ATM convexity in the log-normal SABR model, and the second term is the ATM smile convexity in the local volatility model.

Remark 6.4.

In the uncorrelated limit , the results for the European options ATM volatility, skew and convexity reproduce the results in Theorem 4.1 of Forde and Jacquier (2011) [14] for local-stochastic volatility models by specializing to the log-normal process.

6.2.2. VIX options

We give next the ATM expansion of the implied volatility of the VIX options. As shown in Corollary 4.1, we can approximate the VIX options as

and the corrections to this approximation are of order . The VIX futures price is also approximated as .

Proposition 6.2.

Remark 6.5.

Remark 6.6.

In the stochastic volatility limit , the result (76) reduces to

,

which is just the vol-of-vol of the stochastic process. In this limit the VIX skew vanishes .

Corollary 6.1.

Varying the correlation in the range gives bounds on the ATM VIX implied volatility

| (79) |

6.3. Local-stochastic volatility model with Heston-type volatility

In this section we consider the local-stochastic volatility model with square-root volatility, which we will call Heston-type

| (80) |

where are correlated with correlation . Denote the first few derivatives of the local volatility function around .

This model takes in Eqn. (1) which does not satisfy Assumptions 2.1 and 2.3. Although Theorems 3.1 and 4.1 were obtained under the Assumptions 2.1 and 2.3, one can see that these results hold also for this case as long as satisfies a sample-path large deviation principle as in the proof of Theorem 3.1 (which is true for Heston-type and CEV-type SDEs without Assumptions 2.1 and 2.3, see e.g. [2]) and the following two assumptions hold. The first assumption is on the finiteness of the moment generating function of the integrated variance , which is known to hold under the Heston model.

Assumption 6.1.

We assume that for any , there exists some , such that for any sufficiently small .

The second assumption is the finiteness of the moments of process, which also holds under the Heston model.

Assumption 6.2.

For any , there exists some , such that for any sufficiently small .

We give next a result on moment finiteness for process under a certain assumption on the moment generating function of the integrated variance so that Assumption 2.4 is satisfied.

Proposition 6.3.

Suppose that is uniformly bounded. Also, suppose Assumption 6.1 holds. Then for any , there exists some , such that for any sufficiently small .

Finally, we note that the extremal problems for the rate functions appearing in Theorem 3.1 and 4.1 are well defined, and the function is calculable as shown in Proposition 5.3.

6.3.1. European options

The implied volatility of European options in the Heston-type local-stochastic volatility model is given by the following result.

Proposition 6.4.

The implied volatility of European options in the Heston-type model (80) has the expansion in log-strike

| (81) |

where the at-the-money implied volatility is

| (82) |

the ATM skew is

| (83) |

and the ATM convexity is

| (84) |

Remark 6.7.

In the stochastic volatility limit we can compare the results with the short-maturity implied volatility expansion around the ATM point for the Heston model, which is known from the literature [25, 12, 13]. Expressed in our notations, the first three terms in this expansion are given by:

| (85) |

Our results for skew and convexity reproduce the coefficients in this expansion after taking .

Remark 6.8.

The results for the European options ATM volatility, skew and convexity in the local Heston model reproduce the results in equations (4.4)-(4.6) of Bompis and Gobet (2018) [4].

6.3.2. VIX options

The implied volatility of VIX options in the Heston-type local-stochastic volatility model is given by the following result. For this result, as shown in Corollary 4.1, VIX options can be approximated as

| (86) |

The corrections to this approximation are of order .

Proposition 6.5.

The implied volatility of VIX options in the model (80) has the expansion in log-strike :

| (87) |

where the at-the-money VIX implied volatility is

| (88) |

and the ATM VIX skew is

| (89) |

We can compare these results with the prediction for VIX options in the stochastic model with Heston-type volatility process , similar to the analysis in Section 6.1 for the SABR-type model. As before, we apply the results of Proposition 4.3 with and and .

The VIX futures price is . As , VIX call options are OTM for and VIX put options are ITM for .

The short maturity limit of the OTM VIX options is given by Proposition 4.3 with and . The rate function for OTM VIX options is

| (90) |

such that the short-maturity limit of the VIX implied volatility is:

| (91) |

This agrees with the result in Sec. 1.8.2 of Forde and Smith [16]. They choose equal mean-reverting level and spot variance to simplify the result, but the result above is more general and holds for all parameters.

In the small averaging time (or equivalently small mean-reversion limit ) we have and the asymptotic VIX smile becomes

| (92) |

The first few terms in the expansion of the asymptotic VIX implied volatility in powers of log-strike (with ) are

| (93) |

The VIX smile in the Heston model is down-sloping and convex, which is well known to contradict empirical evidence from market data, and disfavors this model for modeling volatility products.

7. Numerical Illustrations

In this section we compare the asymptotic results for the implied volatility of European and VIX options with the actual implied volatility, obtained by Monte Carlo simulations of a local-stochastic volatility model. For this test we choose the local-stochastic volatility model

| (95) |

where are correlated standard Brownian motions with correlation . The local volatility function is taken as

| (96) |

This is the so-called Tanh model which was used in Forde and Jacquier (2011) [14] to test the predictions of their asymptotic results for the uncorrelated local-stochastic volatility model. The coefficients for the model (95) are bounded, and satisfy the technical conditions assumed in our paper.

The local volatility function (96) is expanded in powers of the log-asset as

| (97) |

with

| (98) | |||

| (99) | |||

| (100) |

The short-maturity asymptotics of the implied volatility of European and VIX options in the model (95) were obtained in Section 6.2. The asymptotic predictions for European options are given in Proposition 6.1 and those for the VIX options in Proposition 6.2. The information about the local volatility function enter these predictions only through the expansion coefficients . We will compare these predictions against Monte Carlo simulations of the model.

Model parameters. In the numerical test, we will assume that the parameters for the local volatility function are given by:

| (101) |

and the parameters of the volatility process are

| (102) |

The spot asset price is taken as .

The correlation will be varied in the range . The MC simulation will use paths and time steps. The variance is simulated exactly as a geometric Brownian motion, and the process for is simulated using a Euler discretization.

7.1. Numerical tests for European options

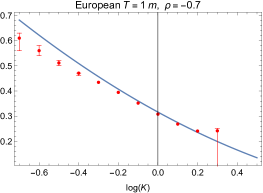

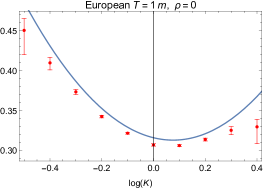

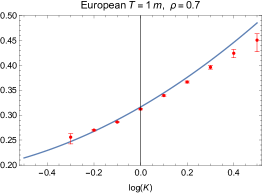

The short-maturity asymptotic implied volatility of the European options will be approximated as a quadratic function of log-strike

| (103) |

where the ATM level , skew and convexity are given in Proposition 6.1. Their numerical values for this test are shown in Table 1.

The asymptotic result (103) is shown as the solid curve in Figure 7.1. The red dots show the results of a MC simulation for European options with maturity (1 month). The agreement is reasonably good for strikes sufficiently close to the ATM point.

| 0.316 | 0.133 | 1.116 | 0.054 | 0.004 | ||

| 0 | 0.316 | 0.520 | 1.012 | 0.012 | 0.002 | |

| 0.316 | 0.271 | 0.133 | 0.896 |

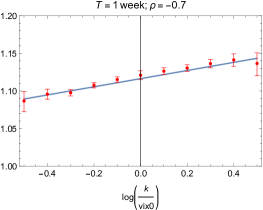

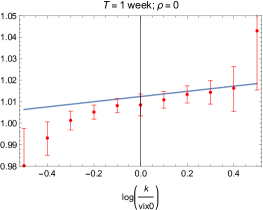

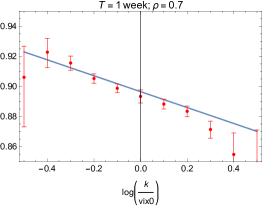

7.2. Numerical tests for VIX options

Next consider the VIX options. We compute a quadratic approximation for the VIX implied volatility as

| (104) |

where with . The ATM level , skew and convexity are given in Proposition 6.2. Their numerical values corresponding to the parameters (101), (102) are listed in Table 1.

The asymptotic prediction (104) is shown as the solid curve in Figure 7.2. The red dots show the results of a MC simulation of the model for VIX options with maturity (1 week). The range of strikes covered in the testing is constrained by the spread of the values of in the simulation. This is sufficiently wide, even for the shorter maturity considered. (On the other hand, the range of simulated values for at is less dispersed, so in order to get a wider range of strikes we used a longer maturity for the European options testing.) The agreement of the asymptotic result for the VIX implied volatility with the MC simulation is again reasonably good for strikes sufficiently close to the ATM point.

Acknowledgements

Xiaoyu Wang is supported by the Guangzhou-HKUST(GZ) Joint Funding Program

(No.2024A03J0630),

Guangzhou Municipal Key Laboratory of Financial Technology Cutting-Edge Research.

Lingjiong Zhu is partially supported by the grants NSF DMS-2053454, NSF DMS-2208303.

Appendix A Background on Large Deviations Theory

We give in this Appendix a few basic concepts of large deviations theory from probability theory which are in the proofs. We refer to Varadhan [41], Dembo and Zeitouni [10] for more details on large deviations and its applications.

Definition A.1 (Large Deviation Principle).

A sequence of probability measures on a topological space satisfies the large deviation principle with rate function if is non-negative, lower semicontinuous and for any measurable set , we have

| (105) |

where denotes the interior of and its closure.

Theorem A.1 (Contraction Principle, see e.g. Theorem 4.2.1. in [10]).

If is a continuous map and satisfies a large deviation principle on with the rate function , then the probability measures satisfies a large deviation principle on with the rate function .

Appendix B Proofs of the Main Results

We give in this Appendix the proofs of the main results in the paper.

B.1. Model specification

B.2. European options

Proof of Theorem 3.1.

(i) OTM call options . The starting point of the proof is a relation between the small-time asymptotics of the call option price with and the small-time asymptotics of the density of the asset price in the right tail

| (108) |

This relation follows by upper and lower bounds for (108).

Let us first prove the upper bound for (108). We include the following argument for the sake of completeness, which can be found in [17]. For any , by applying Hölder’s inequality, we have

| (109) |

for any such that , where is chosen such that which as under Assumption 2.4.

By taking the logarithm in (109) and multiplying with and letting , we obtain

| (110) |

Next, let us show that the limits and exist.

Under Assumptions 2.1 and 2.3, by the sample-path large deviations for small time diffusions (see for example [40] and [36]), one can see that satisfies a sample-path large deviation principle with the rate function:

| (111) |

with , and being absolutely continuous and the rate function is otherwise.

By an application of the contraction principle (see for example Theorem 4.2.1. in [10], restated in Theorem A.1), one can compute that

| (112) |

Similarly, we can obtain the limit with . Since is arbitrary, by letting in (110), we obtain the upper bound for (108), i.e.

The argument for the lower bound for (108) is standard, see e.g. [31] and we omit the details here. Hence, we proved (108).

A similar relation holds between the small-time asymptotics of the put options and of the density of in the left wing ().

For both cases, based on the previous discussions, the limit (108) can be computed using large deviations theory as:

| (113) |

Given , we can determine the optimal as follows. By Cauchy-Schwarz inequality, we have

| (114) |

where the integrals on the right-hand side can be expressed in a simpler form as

| (115) |

where and , and

| (116) |

where . Therefore, we have

| (117) |

and by Cauchy-Schwarz inequality, the equality is achieved when

| (118) |

for some constant so that can be solved via the equation:

| (119) |

where

| (120) |

Since with fixed , we can solve for the optimal , by the discussions above, we conclude that

| (121) |

where

| (122) |

(ii) OTM put options . The case for OTM put options is analogous to the case for call options. Similar to (108), we have

| (123) |

By large deviations theory, the rate function for is the same as (B.2). Following the steps to get (115), we compute

| (124) |

where . And

| (125) |

where . Therefore, we can get the inequality as follows

| (126) |

and by Cauchy-Schwarz inequality, the equality is achieved when and are linearly dependent. Hence, can be solved via the equation:

| (127) |

where

| (128) |

Since with fixed , we can solve for the optimal similar to (121) such that

| (129) |

Note that when , and is the same as the one defined in (121). Hence, the optimum is achieved in the regime where and is decreasing. The last equation in (129) holds by the simple fact that . Finally, by changing the variable in (129), we have

| (130) |

This completes the proof. ∎

Proof of Theorem 3.2.

We only provide the proof for ATM European call option. The case for the ATM European put option can be handled similarly.

Step 1. First, we define a Gaussian approximation for as

| (131) |

where and are independent standard Brownian motions and we will show that can be approximated by in the -norm. We can rewrite as

| (132) |

where is a standard Brownian motion and has correlation with . Recall that

| (133) |

Therefore,

| (134) |

Step 2. Next, let us provide an upper bound for the first term in (134). By Cauchy-Schwarz inequality,

| (135) |

where as under our assumptions.

Step 3. Next, let us provide an upper bound for the second term in (134). By Itô’s isometry,

| (136) |

Let us first bound the second term in (136). Since is -Lipschitz and -uniformly bounded, we can deduce that for any :

where . Thus, we get

| (137) |

Next, let us bound the first term in (136). We can compute that

| (138) |

where as under our assumptions and we applied Cauchy-Schwarz inequality to obtain the last inequality above.

Step 4. In order to finish the calculations to bound the second term in (136) in Step 3, we need to provide lower bounds for and and upper bounds for and that will be used to complete the upper bound in (138). Let us recall that

| (139) |

and by Jensen’s inequality,

| (140) |

Similarly,

| (141) |

On the other hand,

| (142) |

Moreover,

| (143) |

and by Cauchy-Schwarz inequality, we can further compute that

| (144) |

Hence, we have

| (145) |

Hence, by applying (140), (141), (142) and (145), we conclude that in the upper bound in (138), we have

| (146) |

for some universal constant .

Step 5. Putting everything together, i.e. by combining the estimates in Step 2, Step 3 and Step 4, we have for any ,

| (147) |

By applying Gronwall’s inequality, we conclude that

| (148) |

as .

Since is -Lipschitz,

| (149) |

as .

Finally, we can compute that

| (150) |

Therefore,

| (151) |

This completes the proof. ∎

B.3. VIX options

Proof of Proposition 4.1.

First of all, we have

| (152) |

The integrand is bounded as

| (153) |

We bound each term on the right-hand side separately, and we will show that their sum is of .

Step 1. First term in (153). The first term in (153) can be bounded as

| (154) |

We can further compute that

| (155) |

and by Jensen’s inequality and Assumption 2.1,

| (156) |

On the other hand, by Assumption 2.1,

| (157) |

and by Cauchy-Schwarz inequality, we can further compute that

| (158) |

Hence,

| (159) |

Therefore, for any ,

| (160) |

Hence, we conclude that, for any ,

| (161) |

Step 2. The second term in (153). The second term in (153) is bounded further as

| (162) |

By Itô’s formula,

| (163) |

Therefore,

| (164) |

By our assumption, is -Lipschitz, so that , which implies that is -Lipschitz. Also we have the bound (22) on the second derivative . Therefore, for any , we have

| (165) |

Proof of Corollary 4.1.

Proof of Proposition 4.2.

(i) In this case,

| (172) |

so that we can easily compute that for any ,

| (173) |

which gives the result quoted.

(ii) For this case we have

| (174) |

In this case, one can compute that for any ,

| (175) |

which yields the stated result. ∎

Proof of Theorem 4.1.

(i) OTM VIX call option ().

First, by (11) and Jensen’s inequality, we can compute that for any :

| (176) |

where under our assumption . Moreover, we can compute that

| (177) |

which implies that

| (178) |

Therefore, under the moment condition (178), by a standard argument for short-maturity options (see e.g. [31]), one can show that

| (179) |

For any , by Corollary 4.1

| (180) |

Since under Assumptions 2.1 and 2.3, satisfies a large deviation principle, by the contraction principle (see e.g. Theorem 4.2.1. in [10], restated in Theorem A.1), also satisfies a large deviation principle for any given . Since as , and as , by (180), we obtain the following superexponential estimate:

| (181) |

The above estimate (181) is also known as the exponential equivalence in large deviations theory (see e.g. [10]), which implies that

| (182) |

Under Assumptions 2.1 and 2.3, by the sample-path large deviations for small time diffusions (see for example [40] and [36]) and an application of the contraction principle (see for example Theorem 4.2.1. in [10], restated in Theorem A.1), similar to the proof of Theorem 3.1, we have

| (183) |

Given , we can determine the optimal as follows. By Cauchy-Schwarz inequality,

| (184) |

where

| (185) |

where and , and

| (186) |

where . Therefore, we have

| (187) |

and by Cauchy-Schwarz inequality, the equality is achieved when

| (188) |

for some constant so that can be solved via the equation:

| (189) |

where

| (190) |

Since with fixed , we can solve for the optimal , by the discussions above, we conclude that

| (191) |

where

| (192) |

(ii) OTM VIX put option (). Since with probability one, similar to the OTM VIX call option case, we can show that

| (193) |

Similar to the proof for the rate function for OTM European put option in Theorem 3.1, we can also get a similar result for the rate function for OTM VIX put option. Similar to (124) and (125), for put option, we can change the variables in (185) and (186) and obtain:

| (194) |

where and ,

| (195) |

where . We can follow the step for (129) to compute that

| (196) |

where denotes the inverse function of . Finally, by changing the variables in (196), we have

| (197) |

This completes the proof. ∎

Proof of Proposition 4.3.

Recall that the VIX option prices under the time homogeneous stochastic volatility model are given in (33). Consider the case of the OTM VIX call option. Proceeding as in the proof of Theorem 3.1 for OTM European options, we get, by upper and lower bounds, the relation

| (198) |

Thus, the problem has been reduced to the short maturity asymptotics for OTM European options in the local volatility model for , see for example [3, 31], which is evaluated with the stated result.

The OTM VIX put option can be handled in a similar way. This completes the proof. ∎

Proof of Theorem 4.2.

We only provide the proof for the ATM VIX call option with . The case for the ATM VIX put option can be handled similarly.

Step 1. First, by using the estimates in Corollary 4.1, we can easily show that

| (199) |

for some , as . Indeed, since is -Lipschitz, we get

| (200) |

where the last inequality follows from Corollary 4.1. Then (199) follows from the assumption .

Step 2. Next, we define

| (201) | |||

| (202) |

where are independent standard Brownian motions.

Next, let us recall that

| (204) |

and we can also re-write as

| (205) |

Under our assumptions, is -Lipschitz and -uniformly bounded. Therefore, we can compute that for any :

where . Then we can compute that

| (206) |

where we used Cauchy-Schwarz inequality as well as Itô’s isometry. Moreover, we can compute that

| (207) |

Hence, we conclude that

| (208) |

where as under our assumptions. By Gronwall’s inequality, we conclude that

| (209) |

as and hence as .

Step 3. Next, we can compute that

| (210) |

Note that the function is -Lipschitz and is -Lipschitz.

Furthermore, the first term in (210) can be bounded as:

| (212) |

Step 4. To complete the upper bound on the first term in (210) in Step 3, we need to provide upper bounds on the two terms in (212). In particular, we will use large deviations theory to bound the second term in (212) since is a rare event and we will use the -Lipschitz-continuity of for any to bound the first term in (212).

Let us first bound the second term in (212). By Cauchy-Schwarz inequality, we can compute that

| (213) |

Note that by (142)

| (214) |

and by the large deviations theory under Assumptions 2.1 and 2.3 (see the proof of Theorem 3.1).

Next, let us bound the first term in (212). Since is -Lipschitz, we have

| (215) |

By using the similar argument before by applying Cauchy-Schwarz inequality and large deviations theory, one can show that

| (216) |

as . Moreover, since is -Lipschitz for any , we have

| (217) |

as .

Step 5. By combining the estimates in Step 2, Step 3 and Step 4, we showed that can be approximated by

| (218) |

Next, we focus on the computation on (218). We will show that the term in (218) can be approximated by

| (219) |

and we will make this rigorous via a few steps.

Step 5(a). First, we will show that

can be approximated by

| (220) |

First, we can compute that

| (221) |

We recall the assumption that , Moreover, is -Lipschitz. Therefore, there exists some , such that

| (222) |

as .

Step 5(b). Next, let us show that the term in (220) can be approximated by

| (223) |

We notice that

| (224) |

uniformly in . Moreover, is -Lipschitz. Therefore, there exists some such that

| (225) |

as .

Step 5(c). Next, let us show that the term in (223) can be approximated by

| (226) |

By using the fact that is -Lipschitz and the Cauchy-Schwarz inequality, we can compute that

| (227) |

as .

Step 5(d). Next, let us show that the term in (226) can be approximated by

| (228) |

We can compute that

By the large deviations theory,

| (229) |

as .

Therefore, we conclude that

| (230) |

as .

Step 6. From the previous steps, we conclude that can be approximated by:

| (231) |

Finally, we can compute that

| (232) |

where .

Hence, we conclude that for ATM VIX call options, with ,

| (233) |

This completes the proof. ∎

Appendix C Proofs for Section 5

Proof of Proposition 5.1.

The starting point is an alternative expression for the function . An application of the contraction principle (see for example Theorem 4.2.1. in [10], restated in Theorem A.1) from large deviations theory shows that (46) is the rate function for the large deviation principle for so that

| (234) |

For the purpose of computing , it is sufficient to take , since is independent of the drift term in the underlying SDE for process. For this case we have , and the probability in (234) reduces to the joint distribution of the time average of the geometric Brownian motion and its terminal value.

A closed form expression for this joint distribution was given by Yor [42] in terms of the Hartman-Watson distribution. Define where is a standard Brownian motion. Then we have [42], see also Theorem 4.1 in [28]

| (235) |

where is the Hartman-Watson integral defined by

| (236) |

The relation (235) can be expressed alternatively as

| (237) |

Proof of Proposition 5.2.

This proposition follows directly from the Gärtner-Ellis theorem from large deviations theory; see e.g. [10]. In order to apply the Gärtner-Ellis theorem, we will show that the limit (57) exists and compute it out explicitly as follows (so that it can be seen easily that the essential smoothness condition for the Gärtner-Ellis theorem is satisfied).

The expectation can be computed exactly for the case of constant . Since the rate function is independent of (provided that satisfies the technical assumptions required for the existence of the large deviations property), we will use a constant drift function to compute the cumulant function . This has the form

| (244) |

where the function can be found in closed-form, which can be extracted from the proof of Theorem 14 in [34].

Using this result we get the following expression for the cumulant function

| (245) |

where and are the boundary curves given by the solutions of the equation:

| (246) |

or equivalently

| (247) |

This completes the proof. ∎

Proof of Proposition 5.3.

The rate function is given by the double Legendre transform

| (248) |

where the cumulant function is given in explicit form in (C).

Denote the minimizers of this problem as . They are given by the solutions of the equations

| (249) |

One can expand the minimizers in powers of as

| (250) | |||

| (251) |

The expansion of the cumulant function in powers of has the form

| (252) |

The coefficients are determined by substituting their expansion into the equations (249), and expanding in powers of . The first few terms are

| (253) | |||

| (254) |

Substituting into the expression for the rate function (248) gives an expansion in . In order to get the expansion of the rate function up to and including terms of order with , one has to compute the expansion of in to the same order. In particular, obtaining the expansion to in (58) requires the expansions of including the terms. ∎

Appendix D Proofs for Section 6

Proof of Proposition 6.1.

We would like to compute the expansion of the European rate function in powers of log-strike

| (255) |

The implied volatility option has the corresponding expansion

| (256) |

where the first term is the ATM implied volatility, the second term is the ATM skew, and so on, and is the log-strike.

The problem was reduced to that of computing the rate function for OTM European options. This rate function is given by Theorem 3.1. Using the explicit result for for in equation (48), the rate function has the form

| (257) |

Let us introduce new notation

| (258) |

The rate function becomes

| (259) |

where we defined

| (260) |

For an ATM European option we have , and the infimum in (259) is realized at . This gives .

The idea of the proof is to expand the minimizers in the extremal problem (259) in powers of log-strike

| (261) | |||

and solve explicitly the coefficients at each order in . We give the details only for the leading coefficient in the rate function , the higher order coefficients are obtained in a similar way.

We will parameterize the local volatility function as an expansion in

| (262) |

We start by expanding the integral defined in (260), as

| (263) |

where . This is obtained by expanding the integrand of using (262) and integrating term-by-term.

We expand the argument of the extremal problem (259) in powers of log-strike . The leading order term in this expansion is

| (264) |

We find the solutions of by substituting here the expansions (261) and keeping only terms of the same power in . At leading order, we get

| (265) |

Requiring that the coefficient of the term vanishes gives .

Analogously,

| (266) |

which gives a second equation for .

The solution of these equations for is

| (267) |

The expansion of (259) in powers of reads

| (268) |

Substituting here the solution (267) for gives the leading order coefficient in the expansion of the rate function

| (269) |

This yields the stated result (72) for the ATM European implied volatility.

This approach can be extended to higher orders in log-strike to compute the terms with . We get

| (270) |

and

| (271) |

Proof of Proposition 6.2.

Using the same approach as that used above for the European options, we compute the expansion of the VIX rate function around the ATM point

| (272) |

where . The implied volatility of the VIX option has the expansion

| (273) |

The first term is the ATM VIX implied volatility and the second term is the ATM VIX skew.

The rate function for VIX options is given by Theorem 4.1. Using the explicit result for for in equation (48), the rate function has the form

| (274) |

Changing variables to defined as in (258), the rate function becomes

| (275) |

where was defined above in (260), and is the solution of the equation

| (276) |

The proof parallels closely the proof of Proposition 6.1 so we give only the proof outline.

For an ATM VIX option , the infimum in (275) is realized at . This gives . We expand the minimizers in the extremal problem (275) in powers of log-strike

| (277) |

and solve for the coefficients at each order in .

The solution of the equation (276) gives an expansion for of the form

| (278) |

This can be substituted into the expansion of in (263) to get an expansion of in powers of .

Keeping only the leading order term in this expansion, the argument of (275) becomes

| (279) |

We find the solutions of by substituting here the expansions (277) and keeping only terms of the same power in . We have

| (280) |

The expansion of (275) in powers of reads

| (281) |

Substituting here the solution (280) for gives the leading order coefficient in the VIX rate function

| (282) |

Substituting into (273) gives the stated result for the ATM VIX implied volatility.

The ATM VIX skew requires the coefficient which is found by expanding to order and solving for . The result is

| (283) |

Substituting into the second term of (273) gives the stated result for the ATM VIX skew. The convexity requires also the coefficient which we do not give in complete form due to the lengthy expression. This completes the proof. ∎

Proof of Proposition 6.3.

For any , by the Cauchy-Schwarz inequality, we can compute that

| (284) |

Notice that is a non-negative local martingale. Since any local martingale that is bounded from below is a supermartingale, we conclude that for any :

| (285) |

which implies that

| (286) |

as where we applied Assumption 6.1. This concludes the proof. ∎

Appendix E At-the-Money Convexity for the VIX Options

We give in this Appendix the full result for the ATM VIX implied volatility convexity in the local-stochastic volatility model with SABR-type volatility quoted in Proposition 6.2. This is defined as the coefficient of the quadratic term in expansion of the VIX implied volatility in log-strike

| (287) |

and has the explicit result

| (288) |

where is given by

| (289) |

where the coefficients are

| (290) | |||

| (291) | |||

| (292) | |||

| (293) | |||

| (294) | |||

| (295) | |||

| (296) |

and .

References

- [1] J. Baldeaux and A. Badran. Consistent modelling of VIX and equity derivatives using a 3/2 plus jumps model. Applied Mathematical Finance, 21:299–312, 2014.

- [2] P. Baldi and L. Caramellino. General Freidlin-Wentzell large deviations and positive diffusions. Statistics and Probability Letters, 81:1218–1229, 2011.

- [3] H. Berestycki, J. Busca, and I. Florent. Asymptotics and calibration of local volatility models. Quantitative Finance, 2:61–69, 2002.

- [4] R. Bompis and E. Gobet. Analytical approximations of local-Heston volatility models and error analysis. Mathematical Finance, 28:920–961, 2018.

- [5] P. Carr, H. Geman, D.B. Madan, and M. Yor. Pricing options on realized variance. Finance and Stochastics, 9:453–475, 2005.

- [6] P. Carr and R. Lee. Volatility derivatives. Annual Reviews of Finance and Economics, 1:319–330, 2009.

- [7] P. Carr and S. Willems. A log-normal type stochastic volatility model with quadratic drift. SSRN-3421304, 2019.

- [8] CBOE Global Indices. Volatility Index Methodology: CBOE 1-Day Volatility Index. White Paper, 2023.

- [9] CBOE Global Indices. Volatility Index Methodology: CBOE Volatility Index. White Paper, 2023.

- [10] A. Dembo and O. Zeitouni. Large Deviations Techniques and Applications. Springer Verlag, 2nd edition, 1998.

- [11] J. Detemple and C. Osakwe. The valuation of volatility options. European Finance Review, 4:21–50, 2000.

- [12] V. Durrleman. From implied to spot volatilities. PhD dissertation, Princeton University, 2004.

- [13] M. Forde and A. Jacquier. Small-time asymptotics for implied volatility under the Heston model. International Journal of Theoretical and Applied Finance, 12:861–876, 2009.

- [14] M. Forde and A. Jacquier. Small-time asymptotics for an uncorrelated local-stochastic volatility model. Applied Mathematical Finance, 2:517–535, 2011.

- [15] M. Forde, A. Jacquier, and R. Lee. The small-time smile and term structure of implied volatility under the Heston model. SIAM Journal on Financial Mathematics, 3:690–708, 2012.

- [16] M. Forde and B. Smith. Markovian stochastic volatility with stochastic correlation - joint calibration and consistency of SPX/VIX short-maturity smiles. International Journal of Theoretical and Applied Finance, 2-3:2350007, 2023.

- [17] P. Friz, P. Gassiat, and P. Pigato. Precise asymptotics: robust stochastic volatility models. Annals of Applied Probability, 31:896–940, 2021.

- [18] J. Goard and M. Mazur. Stochastic volatility models and the pricing of VIX options. Mathematical Finance, 23:439–458, 2013.

- [19] J. Guyon. The joint SP500/VIX smile calibration puzzle solved. Risk, June, 2020.

- [20] P. Hagan, D. Kumar, A. Lesniewski, and D. Woodward. Managing smile risk. Wilmott, 1:84–108, 2002.

- [21] S.L. Heston. A closed-form solution for options with stochastic volatility with applications to bond and currency options. Review of Financial Studies, 6:327–343, 1993.

- [22] B. Horvath, A. Jacquier, and P. Tankov. Volatility options in rough volatility models. SIAM Journal on Financial Mathematics, 11:437–469, 2020.

- [23] J. Hull and A. White. The pricing of options on assets with stochastic volatilities. Journal of Finance, 42(2):281–300, 1987.

- [24] A. Jacquier, A. Muguruza, and A. Pannier. Rough multifactor volatility for SPX and VIX options. arxiv:2112.14310, 2021.

- [25] A.L. Lewis. Option Valuation Under Stochastic Volatility. Finance Press, 2000.

- [26] P.L. Lions and M. Musiela. Correlations and bounds for stochastic volatility models. Annales de l’Institut Henri Poincare C, Analyse non lineaire, 24:1–16, 2007.

- [27] M. Lorig, S. Pagliarani, and A. Pascucci. Explicit implied volatilities for multifactor local-stochastic volatility models. Mathematical Finance, 27:926–960, 2017.

- [28] H. Matsumoto and M. Yor. Exponential functionals of the Brownian motion. Probability Surveys, 2:312–347, 2005.

- [29] P. Nandori and D. Pirjol. On the distribution of the time integral of the geometric Brownian motion. Journal of Computational and Applied Mathematics, 402:113818, 2022.

- [30] S. Pagliarani and A. Pascucci. Local stochastic volatility with jumps: analytical approximations. International Journal for Theoretical and Applied Finance, 16:1350050, 2013.

- [31] H. Pham. Some Applications and Methods of Large Deviations in Finance and Insurance, pages 191–244. Springer Berlin Heidelberg, Berlin, Heidelberg, 2007.

- [32] D. Pirjol. Small- expansion for the Hartman-Watson distribution. Methodology and Computing in Applied Probability, 23:1537–1549, 2021.

- [33] D. Pirjol and L. Zhu. Short maturity Asian options in local volatility models. SIAM Journal on Financial Mathematics, 7(1):947–992, 2016.

- [34] D. Pirjol and L. Zhu. Short maturity Asian options for the CEV model. Probability in Engineering and Information Sciences, 33:258–290, 2019.

- [35] D. Pirjol and L. Zhu. Asymptotics of the time-discretized log-normal SABR model: The implied volatility surface. Probability in Engineering and Information Sciences, 35:942–974, 2021.

- [36] S. Robertson. Sample path Large Deviations and optimal importance sampling for stochastic volatility models. Stochastic Processes and their Applications, 120:66–83, 2010.

- [37] S.E. Rømer. Empirical analysis of rough and classical stochastic volatility models to the SPX and VIX markets. Quantitative Finance, 22:1805–1838, 2022.

- [38] A. Sepp. Pricing options on realized variance in Heston model with jumps in returns. Journal of Computational Finance, 11:33–70, 2008.

- [39] A. Sepp. VIX option pricing in a jump-diffusion model. Risk, May:84–89, 2008.

- [40] S.R.S. Varadhan. Diffusion processes in a small time interval. Communications on Pure and Applied Mathematics, 20:659–685, 1967.

- [41] S.R.S. Varadhan. Large Deviations and Applications. SIAM, Philadelphia, 1984.

- [42] M. Yor. On some exponential functionals of the Brownian motion. Journal of Applied Probability, 24:509–531, 1992.