Combining Gradient Information and Primitive Directions for High-Performance Mixed-Integer Optimization

Abstract

In this paper we consider bound-constrained mixed-integer optimization problems where the objective function is differentiable w.r.t. the continuous variables for every configuration of the integer variables. We mainly suggest to exploit derivative information when possible in these scenarios: concretely, we propose an algorithmic framework that carries out local optimization steps, alternating searches along gradient-based and primitive directions. The algorithm is shown to match the convergence properties of a derivative-free counterpart. Most importantly, the results of thorough computational experiments show that the proposed method clearly outperforms not only the derivative-free approach but also a state-of-the-art solver both in terms of efficiency and effectiveness.

Keywords Mixed-integer nonlinear optimization Gradient-based optimization Primitive directions Global convergence

Mathematics Subject Classification (2020) 90C11 90C26 90C30

1 Introduction

In this paper, we deal with nonlinear mixed-integer optimization problems of the form

| (1) | ||||

| s.t. | ||||

where , with , are bounds on the feasible values of the continuous variables and , with , are the bounds for the integer variables . We denote by and the sets and , respectively, and . Further, we assume that is a compact, non-empty set and the function is continuously differentiable w.r.t. the continuous variables, i.e., exists and is continuous over for any . In what follows, the Euclidean norm in will be denoted as . Finally, we denote by and , with , the -dimensional vectors of all ones and all zeros, respectively.

Real world problems presenting this structure are not uncommon. For instance, we can consider design problems where the values of integer variables induce the overall structure of some object or building. Once the structure is fixed, geometry and material properties can be varied with continuity, according to some well-known law, to obtain an overall result with the desired property [20, 1, 22]. Other examples of applications can be found for generalized Nash equilibrium [10] and diffusion processes statistical inference problems [21].

The main algorithmic approaches from the literature to deal with nonlinear mixed-integer problems work under the assumption that the objective function is computed by a black-box oracle whose internal mechanisms are inaccessible [12, 18, 2, 5, 7, 17]. However, as noted above, this is not necessarily the case; in this paper, we argue that the employment of first-order information, when available, shall be fostered, as it can lead to substantial improvements in both efficiency and effectiveness of black-box algorithmic frameworks.

Here, we put particular emphasis on the DFNDFL framework from [12], which combines:

-

•

local searches, based on derivative-free line searches along both special unitary directions and the coordinate directions, to carry out an exploration with respect to the continuous variables;

-

•

local searches, along so-called primitive directions, to perform an optimization with respect to the integer variables.

The line search carried out along the dense direction in DFNDFL conveys properties on the initial point, whereas the discrete search conveys properties on the intermediate point where only continuous variables have been moved. The convergence of particular subsequences is then obtained by exploiting the fact that the steps used in the continuous search vanish in the limit. Then, limit properties can be showed for the sequence .

According to the above principles, we could think of employing gradient-based line searches for the continuous part of the problem, when derivatives are available. In fact, from the one hand we underline that this change leads, somewhat unsurprisingly, to no loss of convergence guarantees; from the other hand, we show by thorough computational experiments that the resulting algorithm exhibits much better performance than the original derivative-free counterpart.

We shall note that recently, in [8], a related approach (MIX-ALM) has been proposed for mixed-integer problems with general nonlinear constraints. The algorithm follows a similar scheme: it proceeds by alternating a first step of optimization of the continuous variables and a second step of exploration of the discrete ones. In particular, with respect to the continuous variables, the (approximate) minimization of the augmented Lagrangian function is required to be carried out at each iteration. This strategy allows to assess properties on the point obtained by moving the continuous variables. Then, limit properties can be proved for the sequence .

A strategy of this kind could naturally be adopted also in the present unconstrained setting. However, in this paper we focus on a strategy more closely resembling that of DFNDFL: a single (derivative-based) line search is required to update the continuous variables, rather than a full minimization.

The rest of the paper is organized as follows. In Section 2, we report some preliminary definitions and properties and we recall the DFNDFL algorithm which inspired the present work. The proposed algorithm to solve problem (1) is presented in Section 3. Then, in Section 4, we analyze the convergence properties of the algorithm. Section 5 is devoted to the numerical experiments. Finally, in Section 6 we draw some conclusions and discuss possible lines of future research. Appendix A contains the formal proof that first step of the L-BFGS-B algorithm is performed moving along a gradient-related direction, which is important to assess the convergence guarantees of the implemented version of the algorithm.

2 Preliminaries

The algorithmic framework considered in this manuscript makes use of directions that are completely null in the continuous or in the integer part; in other words, variables update concern continuous variables only or integer variables only.

Now, updates of integer variables exploit particular search directions, which we formally characterize hereafter.

Definition 1 ([19, Def. 4]).

A vector is called primitive if the greatest common divisor of its components is equal to 1.

Local searches w.r.t. integer variables will be thus carried out checking steps along some primitive vectors. This concept needs the following definition to be formalized.

Definition 2 ([12, Def. 4]).

Given a point , the set of feasible primitive directions at with respect to is given by

We then provide some additional definitions in order to characterize local optimality and stationarity for problem (1).

Definition 3 ([12, Def. 5]).

Given a point , the discrete neighborhood of is defined as

Definition 4 ([12, Def. 6]).

Given a point and a scalar , the continuous neighborhood of is given by

Definition 6.

A point is a stationary point of problem (1) if

It is easy to observe that stationarity is actually a necessary condition for local optimality. In the following, we also indicate a point satisfying the first condition of Definition 6 as stationary w.r.t. the continuous variables.

Finally, we recall the notion of convergence to a point reported in [16] for the mixed-integer scenario.

Definition 7 ([16, Def. 3.1]).

A sequence converges to a point if for any there exists an index such that for all we have that and .

The DFNDFL approach from [12] is formally described in Algorithm 1. The method consists of an alternate minimization w.r.t. continuous and discrete variables and, hence, is divided into two main phases. At each iteration of the algorithm, minimization w.r.t. the continuous variables is first carried out starting at the current iterate (steps 1-1). Then, the updated solution, named , is used as starting point for the Discrete Search (DS) phase (step 1), where a set of primitive directions is investigated. Step 1 finally allows to define the next iterate as any solution improving , making the framework quite flexible.

The two key phases are based on line search algorithms exploring feasible search directions: the goal is to return a positive stepsize which leads to a new point providing sufficient decrease of the objective function. If such a point can be determined, an expansion step is tried out to possibly obtain sufficient decrease with an even larger stepsize. Otherwise, the initial tentative stepsize is reduced for the next iteration.

For the continuous variables, these operations are expressed in steps 1 and 1. On the other hand, we report the detailed scheme of the DS phase in Algorithm 2, as it will be crucial for the rest of the paper. The discrete search (steps 2-2) terminates as soon as a point providing sufficient decrease of the objective function is reached (step 2), or after all directions in have been processed. If the line search fails for some direction , its associated initial stepsize is halved for the next DS execution (step 2).

Note that, for computational reasons, only a subset of the directions set is employed. Whenever the DS phase does not return a new point and each direction is associated with a stepsize , the sufficient decrease parameter is reduced and the set is enriched, if possible, with new primitive directions contained in (steps 2 and 2).

For Algorithm 1, some nice properties, including convergence results, have been proved.

Lemma 2 ([12, Prop. 4]).

Let be the sequence produced by DFNDFL. Then, .

Lemma 3 ([12, Theorem 1]).

Let be the sequence of points genebasedrated by DFNDFL. Let be defined as

and let be a dense subsequence in the unit sphere. Then,

-

(i)

a limit point of exists;

-

(ii)

every limit point of is stationary for problem (1).

Remark 1.

Since we assume in this paper that is continuously differentiable over , the Clarke–Jahn stationarity result from [12, Theorem 1] immediately translates into a standard stationarity result in Lemma 3. In fact, a convergent version of DFNDFL taking into account the continuous differentiability of with respect to could be devised by using a set of directions which positively spans , i.e., the set .

3 The Algorithmic Framework

In this section, we describe our proposed approach, called Grad-DFL (G-DFL), whose algorithmic scheme is reported in Algorithm 3. The main difference w.r.t. DFNDFL lies in the optimization step of continuous variables: here, continuous local search steps are carried out by means of a first-order optimizer for bound-constrained nonlinear optimization (e.g., Projected Gradient method [3], Frank-Wolfe algorithm [11] or L-BFGS-B [6]).

At each iteration of G-DFL, we start moving the discrete variables through the DS phase (step 3); if this step is successful, we are actually allowed to move to any other configuration of integer variables that further improves the objective value. Then, we perform a gradient-based minimization for the continuous ones (steps 3-3). First, in step 3 we check if the current point is stationary w.r.t. the continuous variables; if it is not, we can then find a feasible descent direction at (step 3). Given such direction, we employ an Armijo-type line-search [3] in step 3, so that the stepsize leads to a new feasible point satisfying the Armijo sufficient descent condition. Like in DFNDFL, step 3 allows the employment of additional minimization procedures to find the new iterate from the point .

Remark 2.

Note that, in a single iteration of G-DFL, we can actually carry out multiple continuous local search steps without spoiling the convergence results of the algorithm presented in the following Section 4. In fact, these additional steps can be encapsulated in step 3 of Algorithm 3. Similarly, steps 3-3 allow us to incrementally perform a sequence of DS-type steps, rather than a single one.

Remark 3.

Unlike DFNDFL, G-DFL performs the two minimization phases in inverted order. This is due to issues in the convergence analysis presented in the following section. From an experimental point of view, this structural change should have no relevant impact on the performance of the approach. We assessed this fact by some computational experiments that we do not report for the sake of brevity.

4 Convergence Analysis

In this section, we report the theoretical analysis for the G-DFL approach. First, we can easily see that Lemmas 1 and 2 also hold for G-DFL. Then, the set of iteration indices

| (2) |

is infinite.

Moreover, since in step 3 of the approach we employ a feasible descent direction , we immediately get that standard line searches from the literature to find a stepsize satisfying the Armijo rule are well-defined (see, e.g., [14, Proposition 20.4]). Thus, putting this result together with Lemma 1, we have that the entire procedure is well-defined.

In the next proposition, we state the convergence property of G-DFL related to the discrete variables.

Proposition 1.

Let and be the sequences produced by G-DFL. Let be defined as in (2) and be any accumulation point of . Then

Proof.

Let be an index set such that

By Definition 7, the definition of and instructions 3-3 of the algorithm, we thus have that for sufficiently large

| (3) |

Now, let us consider a point . By definition of discrete neighborhood, there exists a direction such that and . Considering this result together with (3), we obtain that, for sufficiently large, . We can then deduce that, by definition of discrete neighborhood, . Taking into account the definitions of and , we thus have that for sufficiently large. Taking the limits for , with , and recalling Lemma 2, we get the thesis. ∎

As for the convergence property related to the continuous variables, we will assume that the employed gradient-based search directions are gradient-related, whose definition [3, Sec. 2.2.1] is adapted below for the mixed-integer scenario.

Definition 8.

Let be the sequence generated by a feasible direction method where , , are such that and the continuous variables are updated as , with . We say that the direction sequence is gradient-related to if, for any subsequence that converges to a nonstationary point w.r.t. the continuous variables, the corresponding subsequence is bounded and satisfies

Note that this assumption, which at first glance could seem strong, is indeed quite reasonable, since many standard approaches for continuous bound-constrained optimization problems, including the Frank-Wolfe [3, Section 2.2.2] and the Projected Gradient [3, Proposition 2.3.1] methods, actually rely on directions of this type. In Appendix A we furthermore show that the employment of L-BFGS-B is also theoretically sound.

Proposition 2.

Let , be the sequences of points produced by G-DFL. Let be any accumulation point of . If the sequence is gradient-related to , then

| (4) |

Proof.

Let be an index set such that

| (5) |

By Definition 7, we thus have there exists such that, for all with ,

| (6) |

By the instructions of Algorithm 3, we know that the entire sequence is monotonically non-increasing and thus, it admits limit , which is finite given the compactness of . Hence, . By steps 3, 3 and 3, we get that, for all ,

Then, taking the limits for , we obtain that

| (7) |

Now, let us suppose by contradiction that is such that equation (4) does not hold, i.e., is not stationary w.r.t. the continuous variables. In particular, since is gradient-related to , this means that

| (8) |

Combining (7) and (8), it immediately follows that

| (9) |

Thus, we have that, for with sufficiently large, (6) holds and . Hence, by definition of (step 3) and of the Armijo rule, we must have that

By using the Mean Value Theorem, we also get that

with . Thus, putting together the two results, we obtain that

| (10) |

Since is gradient-related, is bounded and, then, there exists a subsequence such that for with . Thus, taking the limits in (10) for with , recalling the continuity of , (5) and (9), we obtain that

Since and is gradient-related, we have a contradiction with (8). Thus, the thesis follows. ∎

Proposition 3.

Let , be the sequences of points produced by G-DFL. Let be defined as in (2) and let be any accumulation point of . If the sequence is gradient-related to , then

Proof.

We conclude the section with the main convergence result of the proposed algorithm.

Proposition 4.

5 Numerical Experiments

In this section, we report the results of thorough computational experiments, by which we assess the potential of G-DFL. The code111The implementation code of the G-DFL algorithm can be found at github.com/pierlumanzu/g_dfl. for the experiments was written in Python3. The experiments were run on a computer with the following characteristics: Ubuntu 22.04, Intel Xeon Processor E5-2430 v2 6 cores 2.50 GHz, 32 GB RAM.

Concerning G-DFL, we tested three different optimizers for the update of continuous variables: L-BFGS-B [6], the Projected Gradient method (PG) [3] and Frank-Wolfe algorithm (FW) [11]. As underlined in Section 4 and Appendix A, the employment of all the three procedures within G-DFL is theoretically sound.

As for the parameters setting, for the Armijo-type line search used in PG and FW, the values were chosen based on some preliminary experiments, which we do not report here for the sake of brevity. We finally set and .

The local solvers have been used in two different ways: we tried both to carry out a single descent step or to perform a number of consecutive updates proportional to the number of variables. The variants of G-DFL where multiple steps of local search are carried out at each iteration are denoted by a symbol “+” in the name. Moreover, based again on some preliminary experiments, we set . Obviously, the local search is anyway stopped earlier if an approximately stationary point is reached; the stationarity approximation tolerance is set to .

We considered for comparison the DFNDFL algorithm [12], to show that gradient-based steps can indeed be beneficial within the framework, and a state-of-the-art branch-and-bound based approach for bound-constrained mixed-integer nonlinear optimization, namely B-BB, available in the open source library Bonmin [4]. For both solvers, we set the parameters as suggested in the corresponding reference papers and the available codes. For DFNDFL, Sobol [23] and Halton [15] sequences are used to generate dense continuous and primitive discrete directions, respectively. Note that, since the same discrete local search is employed both in DFNDFL and in G-DFL, the parameter settings related to this phase are the same in both algorithms. On the other side, B-BB was run in an AMPL environment, which is in turn managed through the amplpy Python interface.

In addition to the standard setup for DFNDFL, we also tested a variant (referred to as DFNDFL-C) that only considers coordinate directions for the update of continuous variables; since we have assumed to be differentiable w.r.t. continuous variables, the dense of variables is indeed no more strictly necessary to have convergence guarantees.

In many real-world problems of the form (1), integer variables denote physically integer quantity that are unrelaxable, i.e., measures of do not exist at all if non-integer values are provided in input for variables . Therefore, we also had interest in measuring the performance of B-BB when the values of variables are always rounded up to integers before evaluating in the branch-and-bound process; we refer to this setup by B-BB-T. Note that DFNDFL and G-DFL naturally handle this scenario, as they do not work with continuous relaxations of the problem.

Since all the approaches include some non-deterministic operations, they were run 5 times with 5 different seeds for the pseudo-random number generator. The results for the analysis were then obtained by calculating the averages of the metrics values over the 5 runs. Each solver is given a budget of 2 minutes of computation before stopping; the choice of this stopping condition is due to the proper termination criteria of the algorithms being structurally too different. Yet, early termination was enabled for G-DFL and DFNDFL when hitting a maximum number of tested discrete directions, set equal to 300. Of course, all natural stopping conditions employed in B-BB, indicating that the solution cannot provably be improved anymore, have also been considered.

We ran the approaches on a collection of 19 problems, each of which can be tested with different numbers of variables and, thus, with various choices of and (Table 1); the total number of considered instances was thus 304. The problems are the following: rastrigin, ackley, dixon-price (also considered in [12] with the names problem115, problem206, problem208), expquad, mccormck, qudlin, probpenl, sineali, nonscomp, explin, explin2, biggsb1, bdexp, cvxbqp1, ncvxbqp1, ncvxbqp2, ncvxbqp3, chenhark and pentdi, selected from the Cutest222github.com/ampl/global-optimization/tree/master/cute collection [13]. In most of the experiments, we configured the problems so as to have the ratio . We will specify in the following when a different ratio will be considered. Note that all the tested instances are originally bound constrained continuous problems; in order to transform each one into a mixed-integer problem, we added the integrity constraint for the last variables.

| 100 | 2, 5, 7, 10, 20, 40 |

|---|---|

| 200 | |

| 500 | |

| 1000 | 2, 5, 10, 20, 50, 100 |

| 2000 | 40 |

| 5000 | 100 |

Algorithms have been compared based on the following metrics: the objective value of the returned solution , the runtime , the number of iterations and the number of function (and derivatives) evaluations . We also took into account the values of the latter three metrics attained at the moment the best solution is found; we denote these values by , and respectively. To provide compact views of the results, we systematically make use of performance profiles [9]. Unless stated otherwise, performance profiles of , , and have been computed considering only the problem instances where the involved solvers reached the same solution.

To summarize results in terms of , we instead show the cumulative distribution of relative gap to the optimal value, i.e., we plot the cumulative distribution function of the relative gap between the score achieved by a solver and the best score among those obtained by all the tested solvers. This kind of plot is more suitable than standard performance profiles when the considered metric can take both positive and negative values and does not indicate an absolute cost.

5.1 Preliminary Analysis of Grad-DFL

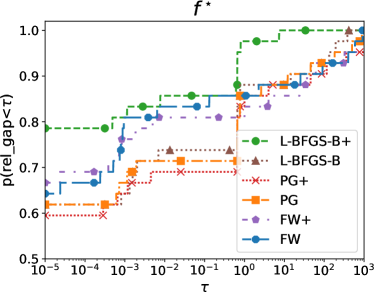

Before comparing G-DFL with other approaches, an analysis is needed of the local optimizers it can be equipped with. For this preliminary stage, we considered a subset of the problems listed in Section 5: rastrigin, ackley, dixon-price, expquad, mccormck, explin and ncvxbqp1. In Figure 1, we show the cumulative distributions of the relative gap to the best function value and the performance profiles w.r.t. for G-DFL equipped with PG, PG+, FW, FW+, L-BFGS-B and L-BFGS-B+.

We observe that the employment of L-BFGS-B+ led to far superior performance than any other variant in terms of , and it also appears to be the best option in terms of efficiency. It is interesting to note that the performance of PG and L-BFGS-B, in terms of objective value, is similar; this shall not be surprising taking into account the discussion in Appendix A.

It is also worth noting that the execution of multiple continuous steps at each iteration is apparently crucial to boost the performance of L-BFGS-B, whereas the differences between PG/PG+ and FW/FW+ are less marked. This is arguably due to the fact that a bunch of iteration is needed for matrix to provide significant second order information.

The results of these preliminary experiments clearly lead us to use L-BFGS-B+ as continuous local search in G-DFL for the rest of the work.

5.2 Efficiency Evaluation

In this section, we measure the efficiency of G-DFL upon the entire considered benchmark of problems, comparing it with DFNDFL and B-BB.

Since in the following we will be comparing derivative-free and gradient-based approaches, it is crucial for getting intelligible results to know the ratio between the cost of computing and . We noticed in fact that the usual assumption represents a very rough approximation. Indeed, a more careful analysis, reported in Figure 2 and Table 2, hints that the cost of evaluating gradients is often over-estimated. Here, we considered a subset of problems (rastrigin, biggsb1, bdexp, mccormck, ncvxbqp2) and for different values of we evaluated the computational time for calculating the gradient () and the objective function () at 500 randomly drawn feasible solutions.

![[Uncaptioned image]](/html/2407.14416/assets/x3.png)

| / | ||

|---|---|---|

| Min | Max | |

| 95 | 1.444 | 2.47 |

| 195 | 1.492 | 2.852 |

| 495 | 1.781 | 4.999 |

| 995 | 2.771 | 7.543 |

| 1995 | 3.656 | 10.908 |

| 4995 | 16.441 | 44.513 |

In order to make the comparison in terms of and useful, we decided to weigh the gradient evaluations by a factor equal to the maximum cost ratio attained at the corresponding problem size (Table 2).

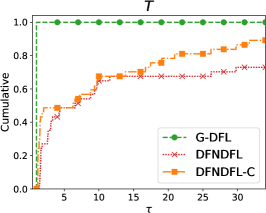

In Figure 3, we report the performance profiles for G-DFL, DFNDFL and DFNDFL-C. We observe that, maybe unsurprisingly, the results in terms of computation time are highly correlated to those about function evaluations. Indeed, G-DFL and DFNDFL share the overall structure and most basic operations, so that the difference lies in the end in the effort spent at evaluating functions. G-DFL clearly outperformed its derivative-free counterpart. We might also note that, while DFNDFL-C performed slightly better than DFNDFL in terms of and , the difference becomes negligible when we consider and .

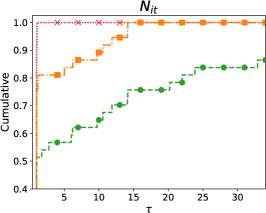

The performance profiles w.r.t. and highlight other computational aspects of the considered procedures. We see that G-DFL consistently carries out a larger number of iterations ; yet, being it also the fastest method, we deduce that G-DFL iterations are less computationally demanding than those of DFNDFL. Moreover, the greater computational cost required by an iteration of DFNDFL does not lead to the best solution with fewer iterations, as the plot w.r.t. attests.

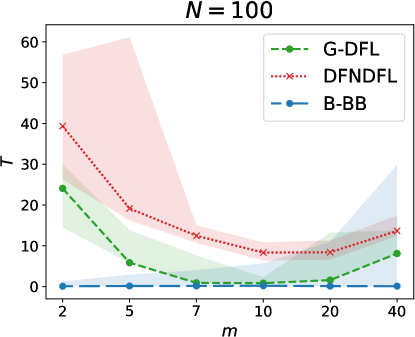

For the last part of this section, we included in the comparison the B-BB algorithm. We start showing Figure 4, where we plot the median runtime for G-DFL, DFNDFL and B-BB as the percentage of discrete variables grows on the problems where the three solvers reached the same solution, with a fixed number of 100 total variables. Shaded areas denote the range between the maximum and minimum runtimes of a solver for a given .

G-DFL and DFNDFL required higher runtimes than B-BB, especially when the number of integer variables is too small or too high. In the case of small , we found the processing cost to be dominated by the computation of the 300 primitive discrete directions, which becomes increasingly difficult. On the other hand, when is large, defining 300 primitive directions is trivial, but testing each one of them is computationally expensive. Still, the use of derivatives within DFL-based approaches again appears beneficial, as G-DFL outperforms DFNDFL in all cases. As for B-BB, it overall obtained the best results in terms of runtime, exploiting its capability of certifying the optimal solution and thus stopping earlier; yet, worst cases become worryingly more expensive as grows.

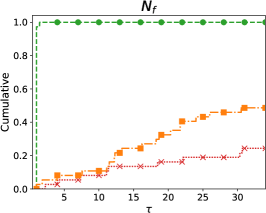

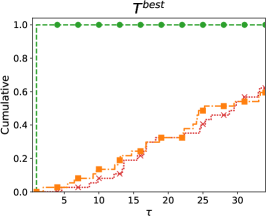

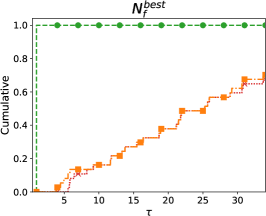

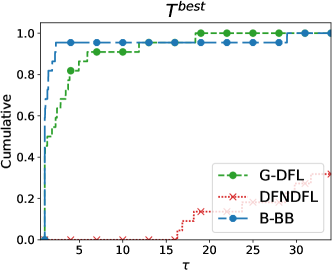

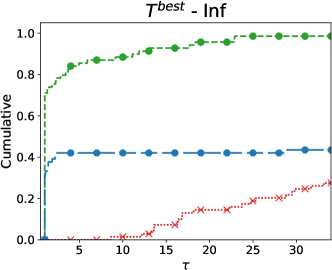

In Figure LABEL:fig::tfb_a, we show the performance profiles w.r.t. for G-DFL, DFNDFL and B-BB. The performance difference between G-DFL and B-BB appears much smaller here, whereas DFNDFL continues to struggle. We have to point out that Figure LABEL:fig::tfb_a is based on the 22 problems where the three solvers reach the same solution. If, instead, all the benchmark problems are considered and an infinity value to the metric is set if the tested solver does not reach the optimum (Figure LABEL:fig::tfb_b), G-DFL becomes by far the best choice.

5.3 Effectiveness Analysis

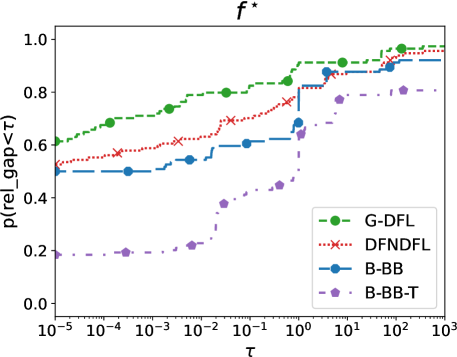

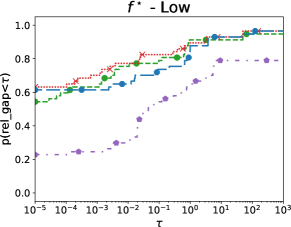

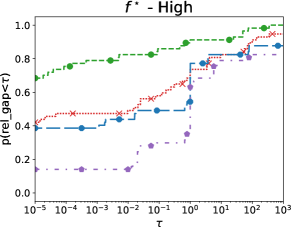

In this last section of the computational experiments, we carry out a detailed comparison in terms of the values of , reporting in Figure 6 the cumulative distributions of the relative gap to the best value for G-DFL, DFNDFL, B-BB and B-BB-T. In particular, we considered three scenarios: in the first one all the benchmark problems were considered; in the second one only the low-dimensional problems () were taken into account; in the last one, we considered the high-dimensional instances ().

Overall, G-DFL proved to be the most robust algorithm when all the benchmark problems were considered. In low-dimensional problems, the situation is more balanced, with all the methods performing similarly. On the other hand, when the number of variables becomes very large, G-DFL is by far the preferable option. It is particularly important to note that the performance of B-BB dramatically drops if relaxation of the integer variables is not possible (i.e, if we consider B-BB-T).

6 Conclusions

In this paper we proposed an algorithmic framework for bound-constrained mixed-integer nonlinear optimization. The distinctive characteristic of the method is that of exploiting, in an alternate fashion, descent steps along gradient-based directions to update continuous variables and steps along primitive directions to update integer variables.

We provide for the method a solid theoretical analysis, showing that the sequence of produced solutions has at least a limit point satisfying a suitable necessary optimality condition. This property is shown to actually hold true when the most common solvers are employed for the update of continuous variables.

Moreover, we carried out thorough computational experiments assessing i) the superiority of the method with respect to a derivative-free counterpart, encouraging the use of first-order information when possible, and ii) the good performance of the algorithm compared to a state-of-the-art solver, especially when the number of continuous variables is large or when integer variables are unrelaxable.

Future work might focus on obtaining stronger convergence properties for the algorithm without losing efficiency in practice. Moreover, the employment of second-order information on the continuous variables might also be considered.

Disclosure statement

The authors report there are no competing interests to declare.

Notes on contributors

Matteo Lapucci received his bachelor and master’s degree in Computer Engineering at the University of Florence in 2015 and 2018 respectively. He then received in 2022 his PhD degree in Smart Computing jointly from the Universities of Florence, Pisa and Siena. He is currently Assistant Professor at the Department of Information Engineering of the University of Florence. His main research interests include theory and algorithms for sparse, multi-objective and large scale nonlinear optimization.

Giampaolo Liuzzi is Associate Professor of operations research in the Department of Computer, Control, and Management Engineering at the University of Rome "La Sapienza." His research activities are primarily focused on the study of models for decision analysis and mathematical optimization, the study and development of methods for solving industrial problems, and the design of methods for machine learning.

Stefano Lucidi received the M.S. degree in Electronic Engineering from the University of Rome “La Sapienza”, Italy, in 1980. From 1982 to 1992 he was Researcher at the Istituto di Analisi e dei Sistemi e Informatica of the National Research Council of Italy. From September 1985 to May 1986 he was Honorary Fellow of the Mathematics Research Center of University of Wisconsin, Madison, USA. From 1992 to 2000 he was Associate Professor of Operations Research of University of Rome “La Sapienza”. Since 2000 he is Full Professor of Operations Research of the University of Rome “La Sapienza”. He teaches courses on Operations Research and Global Optimization methods in Engineering Management. He belongs to the Department of Computer, Control, and Management Engineering “Antonio Ruberti” of the University of Rome “La Sapienza”. From November 2010 to October 2012, he was the Director of the PhD Programme in Operations Research of the University of Rome “La Sapienza”. His research interests are mainly focused on the study, definition and application of nonlinear optimization methods and algorithms.

Pierluigi Mansueto received his bachelor and master’s degree in Computer Engineering at the University of Florence in 2017 and 2020, respectively. He then obtained his PhD degree in Information Engineering from the University of Florence in 2024. Currently, he is a Postdoctoral Research Fellow at the Department of Information Engineering of the University of Florence. His main research interests are multi-objective optimization and global optimization.

References

- [1] S. F. Arroyo, E. J. Cramer, J. E. Dennis, and P. D. Frank. Comparing problem formulations for coupled sets of components. Optimization and Engineering, 10(4):557–573, Dec 2009.

- [2] C. Audet and W. Hare. Introduction: Tools and Challenges in Derivative-Free and Blackbox Optimization, chapter 1, pages 3–14. Springer International Publishing, Cham, 2017.

- [3] D. P. Bertsekas. Nonlinear programming. Athena Scientific, Belmont, MA, 2 edition, 1999.

- [4] P. Bonami, L. T. Biegler, A. R. Conn, G. Cornuéjols, I. E. Grossmann, C. D. Laird, J. Lee, A. Lodi, F. Margot, N. Sawaya, and A. Wächter. An algorithmic framework for convex mixed integer nonlinear programs. Discrete Optimization, 5(2):186–204, 2008. In Memory of George B. Dantzig.

- [5] F. Boukouvala, R. Misener, and C. A. Floudas. Global optimization advances in mixed-integer nonlinear programming, MINLP, and constrained derivative-free optimization, CDFO. European Journal of Operational Research, 252(3):701–727, 2016.

- [6] R. H. Byrd, P. Lu, J. Nocedal, and C. Zhu. A limited memory algorithm for bound constrained optimization. SIAM Journal on Scientific Computing, 16(5):1190–1208, 1995.

- [7] A. R. Conn, K. Scheinberg, and L. N. Vicente. Introduction to derivative-free optimization. SIAM, 2009.

- [8] A. Cristofari, G. Di Pillo, G. Liuzzi, and S. Lucidi. An augmented lagrangian-based method using primitive directions for mixed-integer nonlinear problems. Submitted to Computational Optimization and Applications, 2024.

- [9] E. D. Dolan and J. J. Moré. Benchmarking optimization software with performance profiles. Mathematical Programming, 91(2):201–213, Jan 2002.

- [10] F. Facchinei and C. Kanzow. Penalty methods for the solution of generalized nash equilibrium problems. SIAM Journal on Optimization, 20(5):2228–2253, 2010.

- [11] M. Frank, P. Wolfe, et al. An algorithm for quadratic programming. Naval research logistics quarterly, 3(1-2):95–110, 1956.

- [12] T. Giovannelli, G. Liuzzi, S. Lucidi, and F. Rinaldi. Derivative-free methods for mixed-integer nonsmooth constrained optimization. Computational Optimization and Applications, 82(2):293–327, 2022.

- [13] N. I. M. Gould, D. Orban, and P. L. Toint. Cutest: a constrained and unconstrained testing environment with safe threads for mathematical optimization. Computational Optimization and Applications, 60(3):545–557, Apr 2015.

- [14] L. Grippo and M. Sciandrone. Introduction to Methods for Nonlinear Optimization, volume 152. Springer Nature, 2023.

- [15] J. H. Halton. On the efficiency of certain quasi-random sequences of points in evaluating multi-dimensional integrals. Numerische Mathematik, 2(1):84–90, Dec 1960.

- [16] M. Lapucci, T. Levato, F. Rinaldi, and M. Sciandrone. A unifying framework for sparsity-constrained optimization. Journal of Optimization Theory and Applications, 199(2):663–692, Nov 2023.

- [17] J. Larson, M. Menickelly, and S. M. Wild. Derivative-free optimization methods. Acta Numerica, 28:287–404, 2019.

- [18] S. Le Digabel and S. M. Wild. A taxonomy of constraints in black-box simulation-based optimization. Optimization and Engineering, pages 1–19, 2023.

- [19] G. Liuzzi, S. Lucidi, and F. Rinaldi. An algorithmic framework based on primitive directions and nonmonotone line searches for black-box optimization problems with integer variables. Mathematical Programming Computation, 12:673–702, 2020.

- [20] G. Liuzzi and A. Risi. A decomposition algorithm for unconstrained optimization problems with partial derivative information. Optimization Letters, 6:437–450, 2012.

- [21] A. Pedersen. Likelihood inference by monte carlo methods for incompletely discretely observed diffusion processes. Research Report, 2001-1:21, 2001.

- [22] J. Sobieszczanski-Sobieski and R. T. Haftka. Multidisciplinary aerospace design optimization: survey of recent developments. Structural optimization, 14(1):1–23, Aug 1997.

- [23] I. Sobol. Uniformly distributed sequences with an additional uniform property. USSR Computational Mathematics and Mathematical Physics, 16(5):236–242, 1976.

Appendix A L-BFGS-B first step is gradient-related

We show in this section that the assumptions for convergence results of G-DFL are indeed satisfied if L-BFGS-B is employed as optimizer in the continuous variables update step.

As noted in Remark 2, once a gradient-related step is carried out at each iterations, any additional optimization of continuous variables can be conceptually embedded within step 3 of Algorithm 3, as long as the objective value is nonincreasing. Therefore, focusing on the first iteration of L-BFGS-B can be sufficient to study the convergence.

Actually, L-BFGS-B employs a Wolfe line search at each iteration; the Armijo condition is thus certainly satisfied. It remains to understand whether the first direction is gradient-related. We show hereafter that the direction actually coincides with that of the gradient projection method, which is well-known to be gradient-related.

L-BFGS-B makes a sequence of operations to define the search direction, that are summarized here below:

-

(i)

given a positive definite matrix , define the quadratic model

-

(ii)

let be the piece-wise linear path in obtained projecting onto the box for values of ;

-

(iii)

find the first local minimizer of along the path ; we thus obtain the Cauchy point

where

-

(iv)

fixing the active constraints and ignoring the other constraints, (approximately) solve

(11) s.t. the resulting point can be obtained by an iterative algorithm starting at and must satisfy ;

-

(v)

the path from to is truncated so as to obtain a feasible solution ;

-

(vi)

the search direction is given by .

We now consider the special case of the first iteration of L-BFGS-B; the peculiarity of this iteration is that , ; the quadratic model is therefore given by . Let us now consider the problem . We have

We deduce that the (unique) global minimizer of the quadratic model on the entire feasible region actually lies in the piece-wise linear path and is obtained for . We point out that this point is actually the first local minimizer of along .

The path is characterized by breakpoints ; within each interval function , which is equivalent to in optimization terms as shown above, is continuously differentiable; moreover, the values of a subset of variables are constantly fixed to the bounds, whereas for all we have . We thus have

Since function is convex in , the necessary and sufficient condition of optimality for in this interval is

i.e.,

which is the unique globally optimal solution. Thus, local, yet not global minimizers might only be found at the breakpoints. Yet, we shall outline that the function is continuous at the breakpoints; moreover, even if the derivative does not exist at , we have

At a local minimizer, the first limit cannot be strictly positive and the second limit cannot be strictly negative. Therefore, one of the following cases would hold:

-

•

, i.e., would again be the global minimizer;

-

•

, i.e., the global minimizer appears along the path before the considered local minimizer ;

-

•

, with

the second condition implies for all ; but then, by definition of and noting that for all , we have for all . Hence, ; the solution thus coincides once again with the global minimizer.

We have finally got that the Cauchy point will surely given by the global optimizer of the model on the entire feasible region and has the form ; furthermore, is optimal for subproblem (11) and it is a feasible solution; thus, we have .

We have finally found that the direction at the first iteration of L-BFGS-B is given by

i.e., it is a gradient projection type direction, which is gradient-related.