labelfont=bf,justification=centering \addauthor[Pan]PMMediumBlue

Stochastic Monotone Inclusion with Closed Loop Distributions

Abstract.

In this paper, we study in a Hilbertian setting, first and second-order monotone inclusions related to stochastic optimization problems with decision dependent distributions. The studied dynamics are formulated as monotone inclusions governed by Lipschitz perturbations of maximally monotone operators where the concept of equilibrium plays a central role. We discuss the relationship between the -Wasserstein Lipschitz behavior of the distribution and the so-called coarse Ricci curvature. As an application, we consider the monotone inclusions associated with stochastic optimisation problems involving the sum of a smooth function with Lipschitz gradient, a proximable function and a composite term.

Key words and phrases:

Monotone inclusions; Dynamical systems; Gradient flows; Inertial dynamics; Ollivier-Ricci curvature2020 Mathematics Subject Classification:

Primary 34G25, 37N40, 46N10, 47H05, 49M30, 60J201. Introduction

Recently, many problems in machine learning and risk management come in form of stochastic optimisation problems. Such problems aim to learn a decision rule from a data sample. This can be formulated in terms of optimization problems of the form

| (1) |

where is a probability measure, is a loss function of the decision at data point and is a convex regularizer. In this work, we are interested in (1) in the case where the distribution depends itself on the decision , i.e., problems of the form

| (2) |

In this case, one tries to learn a decision rule from a decision-dependent data distribution . Problems of the form (2) were addressed in the framework of performative prediction proposed in [47, 43] and discussed with further algorithmic aspects in [35]. A typical example concerns prediction of loan default risks, that is the chance that a borrower won’t be able to repay their loan. More precisely, banks take into account several parameters, including the default risk, to decide whether to accept a consumer’s loan application and, if so, what interest rate will apply. It is clear that a high default risk implies a high interest rate, but a high interest rate increases the consumer’s default risk. Thus, the predictive performance of the bank’s model is not calibrated with respect to future results obtained by acting on the model. Another example concerns navigation apps, such as Google Maps (see, e.g., [33, 41], which suggest routes with low travel time to users. This influences users’ decisions to pick such routes and consequently, increases traffic on these routes, impacting travel times. Further applications and illustrations can be found in [47, Appendix A].

In general, problems of the form (2) are difficult to solve. However, a natural approach consists in performing a repeated minimization procedure, i.e., throughout iterations, one solves

| (3) |

and then updates the distribution . Under suitable assumptions that will be specified later, the sequence generated by the repeated minimization procedure (3) admits a fixed point . Such a point turns out to be an equilibrium with respect to the distribution in the following sense:

| (4) |

that is, solves (2) for the induced distribution . So instead of solving (2), we look at an equilibrium point in the sense of (4). Notice that in terms of operators, (4) can be written (formally, for instance) as a monotone inclusion:

| (5) |

with and . That is is a zero of the sum of two monotone operators. One strategy to solve problems of the form (5) is to consider some continuous and discrete dynamical systems whose trajectories may converge, under suitable assumptions, to an element in , the zero set of the sum . For instance, when and where is a given convex lower semicontinuous function on , it is well known since the works of Brézis, Baillon and Bucker [21, 29], that each trajectory of the gradient flow

| (6) |

converges to a minimizer of , and thus a zero of , provided .

Designing algorithms and dynamical systems with rapid convergence properties to solve monotone inclusions is at the core of many fields in modern optimization, partial differential equation, game theory, etc. The literature is extensive, and to name only a few, the reader is referred to [2, 17, 52, 1, 7, 9, 25, 38, 40] and the references therein.

In this work, we address monotone inclusions of the form

| (7) |

where is a maximally monotone operator, and is a single valued mapping. The particularity of such a dynamic is, of course, the presence of the random operator where the random variable has a trajectory-dependent distribution . Thus, it is not straightforward how to address (7) within the classical framework (see, e.g., [27, 22]). Yet, a clever reformulation of (7), based on the notion of equilibrium, as a monotone inclusion governed by a Lipschitz perturbation of a maximally monotone operators will allow us to tackle this issue. Then we investigate inertial dynamics related to (7). Indeed, since the work of Polyak [48], who considered a system of the form

| (HBF) |

where is called the viscous damping coefficient, the introduction of inertial dynamics to accelerate optimization methods has gained a lot of attention and led to many developments (see, e.g., [15, 3, 19, 18, 10, 52] and the references therein).

In this paper, we then consider second-order dynamics of the form

| (8) |

were is the so-called Hessian-driven damping coefficient. When , (i.e., without a stochastic structure) and , systems of the form (8) were first studied in [3]. Later, this system was combined with an asymptotic vanishing damping , for in [19]. Several recent studies has been devoted to this topic (see, e.g., [38, 51, 25, 40, 9]).

1.1. Statement of the problem

Throughout, is a real Hilbert space and is a Polish metric space, i.e., separable and completely metrizable. Given a maximal monotone operator such that , a single-valued mapping , and consider the closed-loop inclusion

| (SMI) |

where is a family of probability distributions on indexed by , such that is a measurable function on for each fixed , where is the Borel -algebra of .

We call the above dynamic (SMI), which stands for Stochastic Monotone Inclusion.

Example 1.1.

Notation. To simplify the presentation, we set, for any measure

| (9) |

where is the expectation with respect to the random variable .

Using this notation, the system (SMI) can be simply rewritten as

| (SMI) |

In the sequel, we need one of the following assumptions.

Assumption 1.

We suppose that is measurable for any and that is -Lipschitz continuous for all .

The following assumption is essential for the convergence analysis. It describes the sensitivity of the distribution to shifts in the index (here trajectory). It is widely used in the literature (see, e.g., [47, 43, 35, 54]). We will discuss how it closely relates to the so-called coarse Ricci curvature in Section 5.

Assumption 2 (Lipschitz distributions).

There exists such that

The last two assumptions are standard monotonicity assumptions essential to the well-posedness of the dynamics and for the existence and uniqueness of equilibria.

Assumption 3 (Strong monotonicity).

is -strongly monotone for all , for .

Rather than using Assumption 3, one can use uniform monotonicity in the sense of Definition 3 below.

Assumption 4 (Uniform monotonicity).

For all , is uniformly monotone with a modulus such that

1.2. Organization of the paper

The paper is organized as follows. In Section 3 we address first-order monotone inclusions with closed-loop distributions. We prove the existence of equilibria as well as the well-posedness of the dynamics and convergence properties of the trajectories. In Section 4 we study asymptotic convergence properties of the trajectories of second-order dynamics with closed-loop distributions via Hessian damping. This allows us in particular to cover problems of the form (2). Section 5 contains a discussion concerning the Lipschitz behavior of the family with respect to -distance and some consequences in the framework of Markov chains on metric random walk spaces. In Section 6 we discuss the inertial primal-dual algorithm as an application of our results. Finally, Section 7 contains some conclusions and discusses some future works.

2. Notation and preliminaries

In this section we fix some notation and present some notions and results that will be used. Throughout this paper, is a real Hilbert space, is the scalar product on and is the induced norm.

2.1. Convex analysis

We denote by the class of proper, l.s.c and convex function on with values in . Given , its domain is defined by . We say that -strongly convex, for , if is convex.

The subdifferential of is defined as

We recall the following Fermat’s optimality condition for ,

Definition 1 (Differentiability).

Let and . We say that is differentiable at if there exists such that

The unique vector satisfying this condition is the gradient of at and is denote by .

This being said, we recall the following

Definition 2 (-smoothness).

Let and . We say that is -smooth over if it is differentiable over and

We denote by the class of -smooth functions over .

Given a function , it proximal mapping is defined through

When the indicator function of a nonempty closed convex set , then . For further details and notion, we refer the reader to [23].

2.2. Operator theory

We write to denote that is a set-valued operator on , its domain is defined as , its graph as and its zeros set as: . A selection of is an operator such that, for any . We write to indicate that is single-valued. In the following, we gather some main properties that are essential for the rest of the paper.

Definition 3.

-

•

We say that is -Lipschitz continuous if it is single-valued over and

(10) -

•

We say that is monotone if

(11) -

•

We say that is maximal monotone if there exists no monotone operator , i.e., satisfying (11), such that .

-

•

We say that is uniformly monotone with modulus if is increasing, , and

(12) -

•

We say that is -strongly monotone, with , if

(13)

Remark 2.1.

-

•

Note that if is -strongly montone is equivalent to saying that is monotone.

-

•

The definition of uniform monotonicity is slightly different from the one in [23, Definition 22.1].

-

•

If is -strongly monotone, then it is uniformly monotone with modulus .

Example 2.1.

-

•

The typical example of a maximal monotone operator is the subdifferential of a function . We usually refer to such an operator as a subpotential maximal monotone operator.

2.3. Monotone inclusions

Let be an operator on such that and single-valued mapping and consider the following differential inclusion

| (14) |

2.4. Transportation distance

For , the -Wasserstein distance is defined by

| (15) |

where Lip is the set of Lipschitz continuous function on .

3. First-order monotone inclusions

In this section we perform the analysis of the first-order monotone inclusion (SMI). More precisely, we discuss the existence and uniqueness of solutions as well as the convergence of trajectories. Recall that the dynamic (SMI) is governed by the operator . We first prove the existence of an equilibrium point which will allow us to reformulate (SMI) in a suitable form.

3.1. Existence and uniqueness of equilibira

Definition 5.

(Equilibrium point) We say that is at equilibrium with respect to the distribution if

| (16) |

In case and where and , this definition is to be compared to the one introduced in [47] (see also [35]). Indeed, (16) reduces to:

| (17) |

Solutions of (17) are exactly the fixed points of the repeated minimization procedure, that is, starting from some , we generate the following sequence for

| (18) |

In [47, Theorem 3.5] it is shown that if is in both variables, is Lipschitz and is -strongly convex for all with , then, under Assumption 2, the iterates of (18) converge to a unique stable point. Their proof is essentially based on a fixed point argument. In [47, Propostion 4.1], they show the existence of equilibrium points under weaker assumptions on the loss . Specifically, they demonstrate that if is convex and jointly continuous, then equilibrium points exists provided is compact. However, in this case the equilibrium is not necessarily unique. In the following lemma, we show the existence of equilibrium in the sense of (16).

Theorem 1 (Existence and uniqueness of equilibrium point).

Under Assumption 4, the map

is a contraction. In particular, the equilibrium is unique. If moreover, Assumption 3 holds instead, i.e., is -strongly monotone for , the mapping is -Lipschitz.

Proof.

First, we see that is well defined. Indeed, for any , is nonempty, and is in fact a singleton due to Assumption 4. To see this, we argue as in [23, Proposition 22.11]. Fix . We have for any :

| (19) | ||||

Since we infer that as and thus is surjective (see [23, Corollary 21.25]. Moreover, in view of strict monotonicity of , is a singleton (see, e.g., [23, Proposition 23.35]).

Now, pick . We have that and . In particular, , which gives that . We get, thanks to Assumption 4

Then, taking and , we get, using Cauchy-Schwarz inequality

We get, using Corollary 1 below

| (20) |

Since is strictly increasing, the last inequality gives thanks to Assumption 4

and by Banach’s fixed-point theorem (see Theorem 6), has a unique fixed point .

Now if is -strongly monotone, it is in particular uniformly monotone with modulus . Equation-(20) gives

with . Again, we conclude using Assumption 4 and Theorem 6. ∎

Remark 3.1.

In the strongly monotone case, Assumption 4 incorporates the parameter regime which appears in particular in [47, Theorem 3.5].

Remark 3.2.

Since , we clearly see that . Indeed, taking into account (23), we have that so that .

Notation 1.

Before stating the main result of this section, let us fix the following notation. Assume that Assumption 4 holds, and denote by

| (21) |

where is the modulus of uniform monotonicity of .

We prove the following

Lemma 1.

Let and define

| (22) |

Then is nonincreasing and .

Remark 3.3.

In the literature of ordinary differential equations, the above lemma is related to the fact that is somhow an Osgood modulus of continuity (see, e.g., [20, Definitions 2.108 and 3.1]). If , which corresponds to Lipschitz regularity, and then . If and , which corresponds to log-Lipschitz regularity, then . More generally, for are admissible choices.

3.2. Well-posedness and convergence

Now let us define the following gap

| (23) |

Using the notation in (9), we may rewrite (SMI) in the following form

| (p-SMI) |

One advantage of this formulation is that the mapping exhibits Lipschitz behaviour, and the operator depends only on instead of . This allows us to treat (p-SMI) within the framework of evolution equations governed by Lipschitz perturbations of maximal monotone operators (cf. [27, Chapter III]). This is behind the notaiton (p-SMI), which stands for perturbed stochastic monotone inclusion. This being said, our aim is to use [27, Proposition 3.13] and show the existence of a unique strong solution (cf. Definition 4) to (p-SMI) (see also [27, Definition 3.1]). To this end we begin with the following lemmas.

Lemma 2.

The operator is maximally monotone.

Proof.

Since is maximal monotone, and is -Lipschitz continuous for all , the result is a direct consequence of [27, Lemma 2.4]. ∎

For completeness of the presentation, we also recall the following elementary results.

Lemma 3.

Under Assumption 1, we have, for any

Proof.

By Assumption 1, is -Lipschitz continuous. We then have from the definition of the -Wasserstein distance (15)

Taking the supremum over yields the result. ∎

Combining Lemma 3 and Assumption 2 we get the following.

Corollary 1.

Under Assumption 1 and Assumption 2, for all

Lemma 4.

Under Assumption 1, we have for any and

Proof.

Let and . Since is -Lipschitz continuous, we have

The result follows immediately. ∎

The key ingredient to use [27, Proposition 3.13] is the Lipschitz continuity of the perturbation . This is the content of the following statement.

Lemma 5.

Suppose that Assumption 1 and Assumption 2 hold, then is -Lipschitz continuous.

Proof.

Proposition 1.

Assume Assumption 1 and Assumption 2 hold. Then, given , the dynamic (p-SMI), and hence (SMI), admits a unique solution .

Proof.

Remark 3.4.

Theorem 2.

Let be the solution of (SMI), and assume that Assumption 4 holds. We then have for all

| (25) |

where is defined in Lemma 1 and .

Proof.

Let , we observe that

We then have, for any selection of

| (27) |

Taking , we get by Assumption 3

Then, thanks to Lemma 3 and Assumption 2, equation (27) gives

| (28) | ||||

where is as introduced in (21). Hence, dividing by in both sides of (28), we get

| (29) |

We infer from (28) and (29) that

| (30) |

Integrating (30) between and , we get

Using Lemma 1, we deduce that

| (31) |

where . This proves (25), as desired.

To prove the second claim, we observe that if is -strongly monotone, so that . Assuming that , we get . So that . Plugging this in (31) we obtain

| (32) |

as desired. ∎

Remark 3.5.

As a consequence of Assumption 2 and Theorem 2, we obtain a rate of convergence, as of the measure to in .

Corollary 2.

Let be the solution of (SMI), and assume that Assumption 4 then for all

where is defined in Lemma 1 and . If Assumption 3 holds instead, we have

with

4. Second-order monotone inclusions via Hessian damping

This section is devoted to the analysis of the following second-order monotone inclusion

| (ISMI) |

where is a continuous function, usually referred to as the viscous damping coefficient. We refer to this dynamic as an Inertial Stochastic Monotone Inclusion, (ISMI) for short. In a smooth deterministic setting, i.e.,, where is a smooth, strongly convexe function, systems of the form (ISMI) were first studies by Polyak in [48] with a fixed viscous damping coefficient. Later on, this kind of systems were studied by [15] and then [52] where the authors establish the link between the continuous dynamics with and the Nesterov’s methods [44]. Further results and extensions followed (see, e.g., [16, 5, 11, 39] and the references therein).

Now, coming back to our setting, we reformulate (ISMI) using the notations of Section 3, as follows

| (p-ISMI) |

One of the drawbacks of the perturber stochastic inertial monotone inclusion (p-ISMI) is that it cannot be written as a dynamical system governed by Lipschitz perturbations of monotone operators. This being said, we shall consider (p-ISMI) with the presence of the so called Hessian damping. To avoid technicalities, we restrict ourselves to the smooth case, i.e., for so that

| (33) |

In this case the perturbation defined in (23) is given by

| (34) |

and it measure the gradient deviation. This being said, (p-ISMI) reduces to an inertial gradient system

| (35) |

which, when , is essentially a Polyak’s heavy ball (HBF) system [48] with the presence of the perturbation . The Hessian-driven damped system we shall consider reads

| (ISEHDm,γ) |

where is a continuous function usually refered to as the Hessian-driven damping coefficient, and which will be taken to be constant, i.e., . We call the above dynamic an Inertial System with Explicit Hessiang Damping, (ISEHDm,γ,ω) for short. The subscript is here to emphasize the stochastic structure of the problem. Here, the Hessian damping is said to be explicit since since, when is of class , we have

One of the main advantages of considering dynamics with Hessian-driven damping is the to attenuate the oscillation that might occur with (HBF)-like dynamics or more generally with inertial dynamics with viscous damping as was observed in [3]. Variants and generalizations were studied by multiple authors (see, e.g., [18, 19, 9]). The study of the effect of perturbed Hessian-driven damping, i.e., problems of the form (ISEHDm,γ,ω) was carried in the recent work [14].

In particular, this will allow us to proceed as in Section 3 to prove the well-posedness of the dynamics. As for convergence properties, this setting will allow us to exploite some techniques from [14].

4.1. Well-posedness

4.1.1. Equivalent formulation

Proposition 2.

Suppose that . For any initial conditions , the dynamics (ISEHDm,γ,ω) admits an equivalent formulation of the form

| (36) |

with initial conditions .

Proof.

Let be a solution of (36). By differentiation of the first equation in (36), we get

Replacing by its expression from the second equation in (36), we obtain:

| (37) |

using again the first equation in (36) to eliminate , we get:

| (38) |

and after simplifications, we recover (ISEHDm,γ,ω). Conversely, let be a trajectory solution to (ISEHDm,γ,ω) with initial conditions and define

By differentiating the previous formula and using (ISEHDm,γ,ω), we recover the second equation of (36), as desired. ∎

4.1.2. Well-posedness

Thanks to Proposition 2, one can also consider (36) in the case where . In fact, we have the following

Definition 6.

Suppose that . For any initial conditions , the dynamics (ISEHDm,γ,ω) admits an equivalent formulation of the form

| (39) |

with initial conditions .

One of the main advantages of (39) is that it can be easily recast as a monotone inclusion governed by Lipschitz perturbation of a maximal monotone operator on the product space . Indeed, setting , and

we immediately see that (39) can be written as

| (40) |

Then (39) can be written as monotone inclusion in the product space

| (MIS) |

which fits in the framework of Lipschitz perturbations of maximal monotone operators as in Section 3. Notice that this formulation is different from the classical Hamiltonian one.

Before stating the main result, let us recall that we endow the product space with the scalar product , and the induced norm . We have the following auxiliary results

Lemma 6.

Under Assumption 3, the operator is Lipschitz continuous.

Proof.

Let and set We have, for

where we have used Young’s inequality and Lemma 5 for the Lipschitz continuity of the operator . ∎

Proposition 3.

Assume that Assumption 3 and Assumption 4 hold. Then, for any initial data and , there exists a unique global solution to (MIS) such that and . Moreover, the solution satisfies the following properties

-

(i)

is continuously differentiable on , and , for all ;

-

(ii)

is absolutely continuous on and for all ;

-

(iii)

for all ;

-

(iv)

is Lipschitz continuous on any compact subinterval of

-

(v)

the function is absolutely continuous on for all ;

-

(vi)

there exists a function such that

-

(a)

for all ;

-

(b)

for almost every ;

-

(c)

for all ;

-

(d)

for almost every .

-

(a)

Proof.

Thanks to Assumption 4 and Moreau’s theorem (see, e.g., [23, Theorem 20.25]) is maximal monotone and is Lipschitz continuous thanks to Lemma 6. We conclude again the existence of a strong global solution of (MIS) via [27, Proposition 3.12]. The verification of items i-vi can be done by following the main arguments of [19, Theorem 4.4] ∎

As a consequence, we have the following

Corollary 3.

Suppose that is a convex function. For any , and any Cauchy data , there exists a unique classical global solution to

| (ISEHDm,γ,ω) |

with .

Proof.

4.2. Convergence properties

Now let us examine the convergence properties of (ISEHDm,γ,ω). Recall that we restrict ourselves here to the smooth case, that is, we assume that satisfies Assumption 3, i.e., is -strongly monotone for . Moreover, we tune the viscous damping function to the modulus of strong convexity of , by taking . From now on, we focus on the following system

| (ISEHD) |

To perform Lyapunov analysis, let us define the following function by

Following the main ideas of [9, 14] we prove the following result.

Theorem 3.

Assume that satisfies Assumption 3 and let be the solution of (ISEHD). Suppose that and that and the damping coefficient satisfy

| (41) |

We then have:

-

•

for all

In particular

-

•

There exists such that,

Proof.

We have

| (42) | ||||

We get from (ISEHD) after some simplifications

| (43) |

Using -strong convexity of , we have

| (44) |

and using this in (76), we get

| (45) |

where

Using the definition of , we may rewrite as

Consequently, (45) becomes

Using strong convexity we obtain again

and observing that for . We end up with

| (46) |

Now let us treat the right hand side of this inequality. Since , we have, using Young’s inequality

| (47) |

Using Lemma 5, we get after rearranging the terms

| (48) |

where

Setting

and and , we see that can be written as a quadratic form with . By assumption , and the discriminant of is nonpositive. Indeed, since

Hence and

which gives after integration

| (49) |

Therefore, and in particular

| (50) |

This implies, using strong convexity of

which gives that

We deduce from (50) that .

Since , we deduce from (52) that

| (53) |

where . Integrating (53), we obtain after elementary computation

as desired. ∎

Remark 4.1.

Remark 4.2.

Notice that in case , i.e., when the inertial dynamic is considered only with the viscous damping coefficient, the condition (41) reduces to . This contrasts with the convergence condition for first-order dynamics (cf. Theorem 2), where convergence is ensured in parameter regime . One possible explanation for this difference, is the potential occurrence of oscillations, which may necessitate a stricter compatibility condition between the parameters .

We end this section with a similar result to Corollary 2, which is a direct consequence of Assumption 2 and Theorem 3-• ‣ Theorem 3.

Corollary 4.

5. On coarse Ricci curvature

In this section we discuss some dynamical and geometrical properties of the family , particularly the notion of Ollivier-Ricci curvature and how it it tightly related to Assumption 2. In fact, the family of probabilities and its Lipschitz behavior with respect to the -Wasserstein distance, reveals that a natural setting to address monotone inclusions of the form (SMI), and thus stochastic optimization problems with decision-dependent distributions is the framework of metric random walk spaces (see, e.g., [45, 42]). All definitions of this section can be found in [42, 36].

5.1. Metric random walk spaces

Before going further, let us recall the following definitions to introduce a couple of probabilistic notions.

Definition 7 (Random walks [45]).

Given a Polish space . A family of probabilities is a random walk on if for each and

-

•

depends measurably on ,

-

•

Each has finite first-order moment, i.e., for some , .

Then equipped with a random walkfirst-order is a metric random walk space (m.r.w.s for short), and we denote it by .

Let us recall the notion of invariant and ergodic measures.

Definition 8 (Invariance).

Let be a -finite measure on and a random walk on . We say that is invariant with respect to if , where is the convolution of by the random walk and is defined by

As pointed out in [45], each measure can be seen as a replacement of a sphere around . While in a probabilistic framework one think about a Markov chain whose transition kernel from to in steps is defined by

| (54) |

with and .

In the sequel, we assume that is a separable real Hilbert space, and thus a Polish space, where .

5.2. Feller Property

Let us recall the following definition.

Definition 9.

We say that has the weak-Feller property if and only if for every sequence we have , i.e., for any

It turns that Assumption 2 implies directly that the family is weak-Feller.

Proposition 4.

Under Assumption 2, has the weak-Feller property. Moreover, for each , has finite first-order moment.

Proof.

Let and a sequence of such that as Then Assumption 2 gives

and thus . Thanks to [4, Proposition 7.1.5], has uniformly integrable -moments with and narrowly converges towards . In particular is weak-Feller and each has finite first-order moments. ∎

Remark 5.1.

We already know that for each and that is measurable for each . Moreover, thanks to Proposition 4, we have finiteness of first-order moments of each , so that the family satisfies the requirements of Definition 7. This shows that a natural setting to address dynamics of the form (SMI) is the metric random walk space . Many diffusion and variational problems has been studies within this framework, with allows in particular consider nonlocal continuum problems or problems on weighted graphs (see, e.g., [42] and the references therein).

Remark 5.2.

Let us point out that if is an invariant measure with respect to then it is also and invariant measure with respect to for every , where is the -step transition probability function given by (54). It turns out that weak-Feller property implies that every weak limit of is an invariant measure of cf. [36, Proposition 7.2.2] (see also [34, Proposition 12.3.4]). However, without assuming at first the existence of an invariant measure with respect to , the measure may be trivial. Without further compactness assumptions on the metric space (see, e.g., [36, Theorem 7.2.3]) one needs some Lyapunov like condition to ensure the existence of an invariant measure of the weak-Feller family (see, e.g., [36, Theorem 7.2.4] or [34, Theorem 12.3.3]). As we will se in Corollary 6, another way to obtain the existence of invariant measures is having a positive lower bound on the coarse Ricci curvature of .

5.3. Ollivier-Ricci curvature

Let us discuss here the connexion between Assumption 2 and the so-called coarse or Olliver-Ricci curvature (ORC for short). The results can be found in [45] or [46]. A more recent presentation can be found in [42].

Definition 10 (Ollivier-Ricci curvature [45]).

Let be a m.r.w.s. Then, for any distinct points , the ORC along is defined as:

| (55) |

The ORC of is defined as

| (56) |

We clearly see from (55) that . Moreover, rearranging the terms, we have

| (57) |

Consequently, having some lower bound for any gives

| (58) |

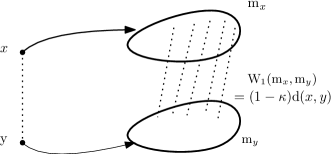

which describes a Lipschitz behavior of the random walk . This has to be compared to Assumption 2. Indeed, we see from Assumption 2 that, for

| (59) |

so according to the values of we have different regimes on the ORC (cf. Table 1).

| Values of | |||

|---|---|---|---|

| Values of |

Notice that Assumption 2 excludes both the cases and . Typically, , would give that in other words for any , i.e., the distribution is contant.

Moreover, it turns that there is equivalence between the lower bound on in (59) and the Lipschitz behavior (58). This is directly related to a -contraction property cf. [45, Proposition 20].

Proposition 5.

Let be a random walk on and assume that has finite moment for all . Then

In view of Proposition 5, taking and for , and , we get

which is exactly Assumption 2 since the above inequality is trivial for .

In the case of positive curvature, this contraction result implies the existence of a unique invariant measure for the random walk when the ORC is positive.

Corollary 5 ([42]).

Assume that for all . Then, the random walk has a unique invariant measure Moreover, for any

-

(1)

, .

-

(2)

, .

In our setting, the parameter regime would define a positive ORC. Consequently, we have the following

Corollary 6.

Assume that satisfies Assumption 2 with . Then, there exists a unique invariant measure with respect to .

6. Application: Inertial primal-dual algorithm

This section is devoted to the application of the developed results in Section 3 and Section 4 to the following class of optimization problems

| (60) |

In what follows, we make the following assumptions.

Assumption 5.

-

(a)

, with and is -strongly convex for all , and is measurable for any ,

-

(b)

and ,

-

(c)

,

where are positive constants and is the strong relative interior of (see, e.g., [23, Definition 6.9]).

Assumption 5-Item a is to be compared to Assumption 1. In particular, it ensure that for any measure , is differentiable with , moreover, strong convexity of for all implies strong convexity of for all . While Assumption 5Item b and Item c are classical for strong duality as discussed below.

Thanks to Fenchel-Rockafellar duality (see, e.g., [23, Chapter 15]) the dual problem of (60) reads

| (61) |

where is the infimal convolution of and given by

and is the adjoint operator of K. Notice that the dual problem (61) is difficult to tacle directly since cannot be computed explicitly due to the dependence of both the loss function and the measure on the state .

Problems of the form (60) arise in many fields such as image and signal processing, machine learning and partial differential equations. In the deterministic case, i.e., does not depend on the distribution and , such problems were studied in [30]. Later on, extensions were addressed in several works (see, e.g., [31, 53, 49]). In [24], the authors studied a fully stochastic variant of (60), i.e., and for some suitable functions and . Yet, the distribution does not depend on the state . To the best of our knowledge composite problems of the form (60) with state-dependent distributions have not been addressed in the literature.

6.1. Formulation as a monotone inclusion

As seen in Section 3, the appropriate notion of solutions of (60) is that of equilibria. Thus, our aim is to find an equilibrium point , i.e., a solution of the static problem

| (62) |

Problems (62) and (61) can be written in an inf-sup form

| (63) |

and is optimal for (63) if and only if the following optimality condition holds

| (64) |

Notice that the problem (63) is a saddle point problem

| (65) |

of the Lagrangian functional: defined by

For any pair we define the following restrictions of the Lagrangian functional

Then, the optimality system (64) can be written as a monotone inclusion

| (66) |

where

| (67) |

Notice that can be split into the sum of two operators: where

| (68) |

Remark 6.1.

Similar problems to (65) where addressed in [54] where the authors studied problems of the form

| (69) |

where are compact sets and is a convex-concave function that plays the role of the Lagrangian in our case. Such problems fall into the scope of (65). Indeed, changing the Lagrange functional in (65) to , where and are the indicator functions of the sets and respectively, and considering a distribution depending on both the primal and dual variables allows recovering (69).

First, let us recapitulate some facts in the following lemma.

Lemma 7.

Under Assumption 5Item aItem bItem c, the following properties hold

-

(i)

The operator is maximally monotone,

-

(ii)

The operator is maximally monotone and -Lipschitz continuous for any ,

-

(iii)

For any

-

(iv)

The operator is maximally monotone and -strongly monotone with .

Proof.

First, we see that is the sum of the maximally monotone operator (see, e.g., [23, Theorem 21.2 and Proposition 20.23]) and a skew-symmetric operator which is maximally monotone (see, e.g., [23, Example 20.35]), this proves Item i. The operator is the gradient of the function and thus is maximally monotone. Now take . We have

this proves Item ii. The proof of Item iii can be directly deduced from Corollary 1. Indeed, let us fix , we then have, for any

where the last inequality follows from Assumption 2 and Assumption 5. As for Item iv, we see that is maximally monotone, and by Item iii, is Lipschitz continuous, we conclude again using [27, Lemma 2.4]. Now take and with . Since by Assumption 5Item a is -strongly monotone and by Assumption 5Item b is -strongly monotone (see, e.g., [23, Theorem 18.15]), we get

| (70) | ||||

which proves strong monotonicity of . ∎

6.2. Existence and uniqueness of equilibrium point

We are now in a position to prove the existence and uniqueness of an equilibrium to the problem (63)

Theorem 4 (Existence and uniqueness of equilibrium point).

Under Assumption 2 and Assumption 5, the map

is -Lipschitz with

and . In particular, if , the equilibrium is unique.

Remark 6.2.

Lemma 8.

Under Assumption 2 and Assumption 5, is -Lipschitz continuous.

6.3. Related first and second-order dynamics

6.3.1. First ordre system

To simplify the presentation, we set again . Then, given an initial data , we consider the following first-order system associated to the monotone inclusion (66):

| (72) |

Or more explicitly

| (SPDS) |

with . Arguing as in Proposition 1 and Theorem 2 we have the following result.

Proposition 6.

Assume that Assumption 2 and Assumption 5 hold. Then, for any initial data , (SPDS) admits a unique global solution . Moreover,

with and .

6.3.2. second-order system

To simplify the presentation, we assume that the following assumptions hold

Assumption 5∗.

-

(a)

, with and is -strongly convex for all , and is measurable for any ,

-

(b)

is a strictly convex function, and ,

-

(c)

.

The main difference between Assumption 5 and Assumption 5∗ is strict convexity of which ensures differentiability of (see, e.g., [23, Corollary 18.12] or [37, Theorem 4.1.1]). In this case we have

| (73) |

By analogy with (ISEHD), we propose the following inertial system associated to (66)

| (ISPDS) |

Systems of the form (ISPDS) can be found for instance in [8] or [26] in an unperturbed form, i.e., without the operator . To lighten the presentation, we discuss (ISPDS) without a Hessian damping term. And for the convenience of the reader, we present the main ingredients of the Lyapunov analysis as in (3). Notice that the existence of a global strong solution to (ISPDS) can be obtained as in Section 4. One can also see [8, Section 4].

Theorem 5.

Assume that Assumption 5∗ holds and let be the solution of (ISPDS). Suppose that . We then have:

-

•

for all

In particular

(74) -

•

There exists such that,

Proof.

The proof is similar to the one of Theorem 3. At first, we have, using (ISPDS)

This gives

| (75) |

We get after some simplifications

| (76) |

That is

| (77) |

Using -strong monotonicity of , and the fact that we have

| (78) |

and using this in (77), we get

| (79) |

where

| (80) | ||||

Thus, (79) becomes

| (81) |

Again, using -strong monotonicity of we get

| (82) |

We have, using Young’s inequality

Using Lemma 7-Item iii, we get after rearranging the terms

Since , we have

which gives after integration

| (83) |

By definition of , we have

| (84) |

Coming back to (83), we have

| (85) |

with . Setting , (85) gives

which implies after integrating between and that

where the constant depends only on and . This finishes the proof. ∎

7. Comments, extensions and future work

In this paper, we adopted a dynamical system approach to study some stochastic optimization problems with state-dependent distributions. We investigated the existence and uniqueness of equilibrium points, well-posedness as well as convergence properties of the trajectories, for both first and second-order dynamics. We highlighted some dynamical and geometrical properties of the state-dependent distributions suggesting that the natural framework to study problems of the form (5) is the one of metric random walk spaces. More particularly, the notion of coarse Ricci curvature gives a new insight on the geometrical hidden structure of this kind of problems. Finally, we discussed as an application the inertial primal-dual algorithm. We present here some ongoing works, possible extensions as well as some open problems.

7.1. Inertial algorithms

Relying on the discretization of the dynamics studied in Section 4 and Section 6, more specifically, (ISEHD) and (ISPDS) , we obtain new inertial algorithms with Hessian-driven damping for stochastic optimization problems with decision-dependent distributions. These algorithms exhibit rapid convergence properties and can also be adapted to the nonsmooth case. This is being addressed in ongoing work.

7.2. Implicit Hessian damping

We focused in Section 4 on the explicit Hessian damping in the smooth case. Yet, it is possible to consider implicit damping as in [9, 14]

| (ISIHDm,γ) |

The dynamics (ISIHDm,γ) is referred to as an Inertial System with Implicit Hessian damping, since one can observe, using Taylor expansion

As it was observed in [14], higher-order moments of the perturbation are required to get fast convergence guarantees in the implicit case compared to the explicit one. Since in our analysis (see Theorem 3) no integrability assumption on is needed, it is interesting to investigate the effect of implicit Hessian damping, both in the smooth and nonsmooth cases.

7.3. Tikhonov-regularization

In Section 4 we restricted ourselves, for sake of simplicity, the analysis to the case where the operator is smooth. However, it is possible to consider second-order dynamics for general (and possibly nonpotential) operators, by considering, for the following dynamic

| (ISEHDm,λ,γ) |

where is the so-called Yosida approximation of defined by and is the resolvent of . This approach comes with several advantages. First, the Yosida approximation is single valued so that the monotone inclusion (p-ISMI) reduces to the classical differential equation (ISEHDm,λ,γ). In addition one can exploit the cocoercivity of and the fact that . The approach was used in [17] for and in the recent work [12] for Newton-like dynamics. We are exploring the adaption of this techniques to stochastic monotone inclusions with state dependent distribution in an ongoing work.

7.4. Weaker Assumptions

We have seen that one of the crucial assumptions in the analysis is Assumption 2, which concerns the Lipschitz behavior of the distribution . A natural question that arises is what happens under a weaker assumption. For example, when is Hölder continuous. We are not aware of any existing results in this direction. We plan to investigate this in future work.

Acknowledgement

The work of H.E was supported by the ANR grant, reference: ANR-20-CE92-0037.

Appendix A Gronwall inequalities

In this section we list several auxiliary results that we make use of in the paper.

Lemma 9 (Gronwall’s lemma: differential form).

Let be two (resp. ) nonnegative function on and let be a continuous function on . We assume that

| (86) |

then, for any

| (87) |

where .

Lemma 10.

Appendix B Banach Fixed point theorem Picard iterative method

References

- [1] F. Alvarez. On the minimizing property of a second order dissipative system in Hilbert spaces. SIAM J. Control Optim., 38(4):1102–1119, 2000.

- [2] F. Alvarez and H. Attouch. An inertial proximal method for maximal monotone operators via discretization of a nonlinear oscillator with damping. Set-Valued Anal., 9(1-2):3–11, 2001.

- [3] F. Alvarez, H. Attouch, J. Bolte, and P. Redont. A second-order gradient-like dissipative dynamical system with hessian-driven damping.: Application to optimization and mechanics. Journal de mathématiques pures et appliquées, 81(8):747–779, 2002.

- [4] L. Ambrosio, N. Gigli, and G. Savaré. Gradient flows in metric spaces and in the space of probability measures. Basel: Birkhäuser, 2nd ed. edition, 2008.

- [5] V. Apidopoulos, J.-F. Aujol, and C. Dossal. Convergence rate of inertial forward–backward algorithm beyond nesterov’s rule. Mathematical Programming, 180(1):137–156, 2020.

- [6] H. Attouch, G. Buttazzo, and G. Michaille. Variational analysis in Sobolev and BV spaces, volume 17 of MOS-SIAM Series on Optimization. Society for Industrial and Applied Mathematics (SIAM), Philadelphia, PA; Mathematical Optimization Society, Philadelphia, PA, second edition, 2014. Applications to PDEs and optimization.

- [7] H. Attouch, A. Cabot, and P. Redont. The dynamics of elastic shocks via epigraphical regularization of a differential inclusion. Barrier and penalty approximations. Adv. Math. Sci. Appl., 12(1):273–306, 2002.

- [8] H. Attouch, Z. Chbani, J. Fadili, and H. Riahi. Fast convergence of dynamical ADMM via time scaling of damped inertial dynamics. J. Optim. Theory Appl., 193(1-3):704–736, 2022.

- [9] H. Attouch, Z. Chbani, J. Fadili, and H. Riahi. First-order optimization algorithms via inertial systems with Hessian driven damping. Math. Program., 193(1, Ser. A):113–155, 2022.

- [10] H. Attouch, Z. Chbani, J. Peypouquet, and P. Redont. Fast convergence of inertial dynamics and algorithms with asymptotic vanishing viscosity. Mathematical Programming, 168:123–175, 2018.

- [11] H. Attouch, Z. Chbani, and H. Riahi. Rate of convergence of the nesterov accelerated gradient method in the subcritical case . ESAIM: Control, Optimisation and Calculus of Variations, 25:2, 2019.

- [12] H. Attouch and S. Csaba László. Continuous Newton-like inertial dynamics for monotone inclusions. Set-Valued Var. Anal., 29(3):555–581, 2021.

- [13] H. Attouch and A. Damlamian. On multivalued evolution equations in hilbert spaces. Israel Journal of Mathematics, 12:373–390, 1972.

- [14] H. Attouch, J. Fadili, and V. Kungurtsev. On the effect of perturbations in first-order optimization methods with inertia and Hessian driven damping. Evol. Equ. Control Theory, 12(1):71–117, 2023.

- [15] H. Attouch, X. Goudou, and P. Redont. The heavy ball with friction method, i. the continuous dynaamical system: global exploration of the local minima of a real-valued function by asymptotic analysis of a dissipative dynamical system. Communications in Contemporary Mathematics, 2(01):1–34, 2000.

- [16] H. Attouch and J. Peypouquet. The rate of convergence of nesterov’s accelerated forward-backward method is actually faster than 1/k^2. SIAM Journal on Optimization, 26(3):1824–1834, 2016.

- [17] H. Attouch and J. Peypouquet. Convergence of inertial dynamics and proximal algorithms governed by maximally monotone operators. Math. Program., 174(1-2, Ser. B):391–432, 2019.

- [18] H. Attouch, J. Peypouquet, and P. Redont. A dynamical approach to an inertial forward-backward algorithm for convex minimization. SIAM Journal on Optimization, 24(1):232–256, 2014.

- [19] H. Attouch, J. Peypouquet, and P. Redont. Fast convex optimization via inertial dynamics with hessian driven damping. Journal of Differential Equations, 261(10):5734–5783, 2016.

- [20] H. Bahouri, J.-Y. Chemin, and R. Danchin. Fourier analysis and nonlinear partial differential equations, volume 343 of Grundlehren der mathematischen Wissenschaften [Fundamental Principles of Mathematical Sciences]. Springer, Heidelberg, 2011.

- [21] J. Baillon and H. Brézis. Une remarque sur le comportement asymptotique des semigroupes non linéaires. Houston J. Math., 2:5–7, 1976.

- [22] V. Barbu. Nonlinear differential equations of monotone types in Banach spaces. Springer Monographs in Mathematics. Springer, New York, 2010.

- [23] H. H. Bauschke and P. L. Combettes. Convex analysis and monotone operator theory in Hilbert spaces. CMS Books in Mathematics/Ouvrages de Mathématiques de la SMC. Springer, New York, 2011. With a foreword by Hédy Attouch.

- [24] P. Bianchi, W. Hachem, and A. Salim. A fully stochastic primal-dual algorithm. Optimization Letters, 15(2):701–710, 2021.

- [25] R. I. Boţ, E. R. Csetnek, and S. C. László. Tikhonov regularization of a second order dynamical system with Hessian driven damping. Math. Program., 189(1-2 (B)):151–186, 2021.

- [26] R. I. Boţ, E. R. Csetnek, and D.-K. Nguyen. Fast augmented Lagrangian method in the convex regime with convergence guarantees for the iterates. Math. Program., 200(1 (A)):147–197, 2023.

- [27] H. Brézis. Opérateurs maximaux monotones et semi-groupes de contractions dans les espaces de Hilbert. North-Holland Mathematics Studies, No. 5. North-Holland Publishing Co., Amsterdam-London; American Elsevier Publishing Co., Inc., New York, 1973.

- [28] H. Brezis. Functional analysis, Sobolev spaces and partial differential equations. Universitext. Springer, New York, 2011.

- [29] R. E. Bruck Jr. Asymptotic convergence of nonlinear contraction semigroups in hilbert space. Journal of Functional Analysis, 18(1):15–26, 1975.

- [30] A. Chambolle and T. Pock. A first-order primal-dual algorithm for convex problems with applications to imaging. Journal of mathematical imaging and vision, 40:120–145, 2011.

- [31] L. Condat. A primal–dual splitting method for convex optimization involving lipschitzian, proximable and linear composite terms. Journal of optimization theory and applications, 158(2):460–479, 2013.

- [32] J. Cutler, M. Díaz, and D. Drusvyatskiy. Stochastic approximation with decision-dependent distributions: asymptotic normality and optimality. arXiv preprint arXiv:2207.04173, 2022.

- [33] A. Derrow-Pinion, J. She, D. Wong, O. Lange, T. Hester, L. Perez, M. Nunkesser, S. Lee, X. Guo, B. Wiltshire, P. W. Battaglia, V. Gupta, A. Li, Z. Xu, A. Sanchez-Gonzalez, Y. Li, and P. Velickovic. Eta prediction with graph neural networks in google maps. In Proceedings of the 30th ACM International Conference on Information & Knowledge Management, CIKM ’21, page 3767–3776, New York, NY, USA, 2021. Association for Computing Machinery.

- [34] R. Douc, E. Moulines, P. Priouret, and P. Soulier. Markov chains. Springer Series in Operations Research and Financial Engineering. Springer, Cham, 2018.

- [35] D. Drusvyatskiy and L. Xiao. Stochastic optimization with decision-dependent distributions. Mathematics of Operations Research, 2022.

- [36] O. Hernández-Lerma and J. B. Lasserre. Markov chains and invariant probabilities, volume 211 of Prog. Math. Basel: Birkhäuser, 2003.

- [37] J.-B. Hiriart-Urruty and C. Lemaréchal. Fundamentals of convex analysis. Grundlehren Text Edit. Berlin: Springer, 2001.

- [38] D. Kim. Accelerated proximal point method for maximally monotone operators. Mathematical Programming, 190(1):57–87, 2021.

- [39] S. C. László. Convergence rates for an inertial algorithm of gradient type associated to a smooth non-convex minimization. Mathematical Programming, 190(1):285–329, 2021.

- [40] T. Lin and M. I. Jordan. A control-theoretic perspective on optimal high-order optimization. Mathematical Programming, pages 1–47, 2022.

- [41] J. Macfarlane. Your navigation app is making traffic unmanageable. IEEE Spectrum, 19, 2019.

- [42] J. Mazón, M. Solera-Diana, and J. Toledo-Melero. Variational and Diffusion Problems in Random Walk Spaces. Progress in Nonlinear Differential Equations and Their Applications. Springer Nature Switzerland, 2023.

- [43] C. Mendler-Dünner, J. C. Perdomo, T. Zrnic, and M. Hardt. Stochastic optimization for performative prediction. In Proceedings of the 34th International Conference on Neural Information Processing Systems, NIPS’20, Red Hook, NY, USA, 2020. Curran Associates Inc.

- [44] Y. Nesterov. A method for solving the convex programming problem with convergence rate o(1/k^2). Proceedings of the USSR Academy of Sciences, 269:543–547, 1983.

- [45] Y. Ollivier. Ricci curvature of Markov chains on metric spaces. J. Funct. Anal., 256(3):810–864, 2009.

- [46] Y. Ollivier. A survey of ricci curvature for metric spaces and markov chains. In Probabilistic approach to geometry, volume 57, pages 343–382. Mathematical Society of Japan, 2010.

- [47] J. Perdomo, T. Zrnic, C. Mendler-Dünner, and M. Hardt. Performative prediction. In H. D. III and A. Singh, editors, Proceedings of the 37th International Conference on Machine Learning, volume 119 of Proceedings of Machine Learning Research, pages 7599–7609. PMLR, 13–18 Jul 2020.

- [48] B. T. Polyak. Some methods of speeding up the convergence of iteration methods. Ussr computational mathematics and mathematical physics, 4(5):1–17, 1964.

- [49] H. Raguet, J. Fadili, and G. Peyré. A generalized forward-backward splitting. SIAM Journal on Imaging Sciences, 6(3):1199–1226, 2013.

- [50] R. T. Rockafellar and R. J.-B. Wets. Variational analysis, volume 317. Springer Science & Business Media, 2009.

- [51] B. Shi, S. S. Du, M. I. Jordan, and W. J. Su. Understanding the acceleration phenomenon via high-resolution differential equations. Mathematical Programming, pages 1–70, 2022.

- [52] W. Su, S. Boyd, and E. J. Candès. A differential equation for modeling Nesterov’s accelerated gradient method: theory and insights. J. Mach. Learn. Res., 17:43, 2016. Id/No 153.

- [53] B. C. Vũ. A splitting algorithm for dual monotone inclusions involving cocoercive operators. Advances in Computational Mathematics, 38(3):667–681, 2013.

- [54] K. Wood and E. Dall’Anese. Stochastic saddle point problems with decision-dependent distributions. SIAM Journal on Optimization, 33(3):1943–1967, 2023.