Not All Frequencies Are Created Equal:

Towards a Dynamic Fusion of Frequencies in Time-Series Forecasting

Abstract.

Long-term time series forecasting is a long-standing challenge in various applications. A central issue in time series forecasting is that methods should expressively capture long-term dependency. Furthermore, time series forecasting methods should be flexible when applied to different scenarios. Although Fourier analysis offers an alternative to effectively capture reusable and periodic patterns to achieve long-term forecasting in different scenarios, existing methods often assume high-frequency components represent noise and should be discarded in time series forecasting. However, we conduct a series of motivation experiments and discover that the role of certain frequencies varies depending on the scenarios. In some scenarios, removing high-frequency components from the original time series can improve the forecasting performance, while in others scenarios, removing them is harmful to forecasting performance. Therefore, it is necessary to treat the frequencies differently according to specific scenarios. To achieve this, we first reformulate the time series forecasting problem as learning a transfer function of each frequency in the Fourier domain. Further, we design Frequency Dynamic Fusion (FreDF), which individually predicts each Fourier component, and dynamically fuses the output of different frequencies. Moreover, we provide a novel insight into the generalization ability of time series forecasting and propose the generalization bound of time series forecasting. Then we prove FreDF has a lower bound, indicating that FreDF has better generalization ability. Extensive experiments conducted on multiple benchmark datasets and ablation studies demonstrate the effectiveness of FreDF.

1. Introduction

Time series forecasting is a well-established problem in various fields including energy usage (Bilal et al., 2022), economic planning (Ariyo et al., 2014), weather alerts (Duchon and Hale, 2012), and traffic forecasting (Li et al., 2015). With the development of deep learning (LeCun et al., 2015), numerous methods have emerged for this forecasting tasks (Zhu et al., 2023; Hu and Xiao, 2022; Bai et al., 2018; Wen et al., 2023; Guo et al., 2023). A central issue in time series forecasting is that existing methods could not expressively capture long-term dependency, which is often characterized as periodicity and trends (Li et al., 2021c; Box et al., 2015; Winters, 1960; Hamilton, 2020; Cheng et al., 2023). However, Fourier analysis has the strong potential to deal with long-term dependency, thereby makes related methods more flexible when adapted to different sequence prediction scenarios (Woo et al., 2022).

In the realm of TFS, an effective approach to addressing long-term dependency is to utilize Fourier analysis (Zhou et al., 2022b; Woo et al., 2022; Zhou et al., 2022a; Wu et al., 2023; Liu et al., 2023b). Fourier analysis is a powerful method that represents complex time series as a series of cosine functions, each with its unique frequency (Bracewell, 1986). This capability to represent infinitely long-term trends with a finite set of frequency components makes it efficient when applied to long-term time series forecasting.

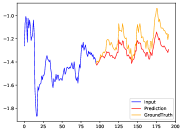

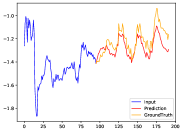

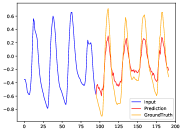

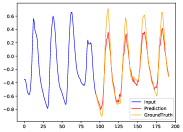

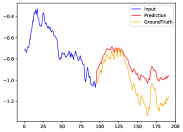

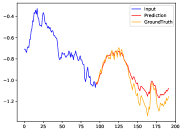

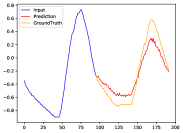

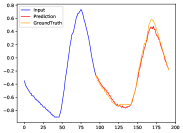

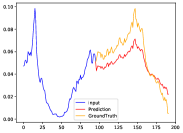

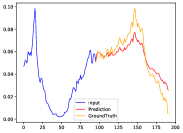

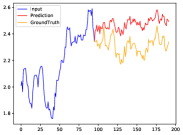

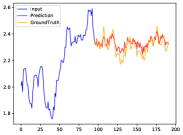

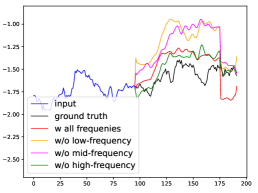

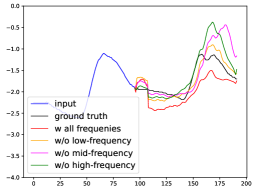

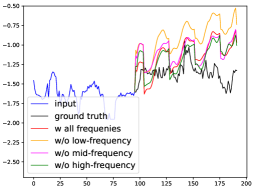

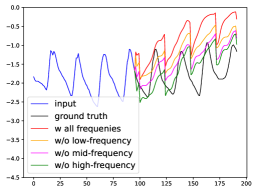

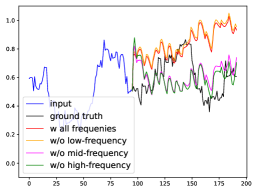

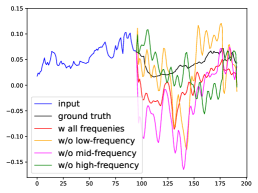

Existing methods based on Fourier analysis often assume that high-frequency components represent noise and should be discarded during forecasting tasks (Zhou et al., 2022a; Xu et al., 2024). Additionally, some methods treat all frequencies equally, without considering their varying importance across different scenarios (Yi et al., 2023c, b). However, we argue that the role of certain frequencies varies in different scenarios. To validate this assumption, we conduct experiments on three datasets, eliminating low, middle, and high-frequency components respectively from the input of the training set to train a vanilla Transformer (Vaswani et al., 2017). The results, depicted in Figure 1, suggest that eliminating certain frequencies may improve performance in specific datasets while decreasing in others. In Exchange-rate(Figure 1(e)), we get more accurate prediction results after eliminating high frequencies. But it is less precise in Figure 1(b). The same phenomenon occurs at other frequencies. More detailed experimental setup and analysis are provided in Section 3.

These findings emphasize that simply marking high-frequency components as noise is undesirable. Without prior knowledge, determining which frequencies compose noise remains uncertain (Hamilton, 2020). Consequently, it is necessary to utilize different frequencies for forecasting and assign more rational weights to these forecasting results to improve the final prediction.

To separately assess the impact of different frequencies, it is necessary to predict each frequency individually. To begin with, we propose a mathematical reformulation of the TFS task in the Fourier domain. Then we propose Frequency Dynamic Fusion (FreDF), a novel framework to process time series datasets in decomposition, forecasting, and dynamic fusion, which individually forecasts each Fourier component, and dynamically fuses the output of different frequencies. The advantage of dynamic fusion lies in its capacity to flexibly adjust the weights of each frequency component, leading to more precise predictions. Additionally, we propose the generalization bound of TFS based on Rademacher complexity (Bartlett et al., 2003), and we prove that dynamic fusion improves the model’s generalization ability. Experimental results on long-term forecasting datasets confirm the superiority of FreDF. Overall, the main contributions of this paper can be summarized as the following:

-

•

We conduct a series of experiments to explore the role of different frequencies in prediction. Based on experimental phenomena we discover that the role of certain frequencies varies depending on the scenarios.

-

•

We reformulate the TFS problem as learning a transfer function in the Fourier domain. Further, we design FreDF, which individually forecasts each Fourier component, and dynamically fuses the output of different frequencies.

-

•

We propose the generalization bound of TFS. Then we prove FreDF has a lower bound, indicating that FreDF has better generalization ability.

-

•

Extensive experiments conducted on various benchmark datasets demonstrate the effectiveness of FreDF.

2. Related Work

With the advancement of deep learning, various methods, including CNN (Zhan et al., 2023; Bai et al., 2018), RNN (Hewamalage et al., 2021; Tang et al., 2021), and Transformer-based approaches (Vaswani et al., 2017), have been developed for time series forecasting tasks. While most previous works focus on learning models in the time domain (e.g., Informer (Li et al., 2021a), PeriodFormer (Liang et al., 2023), GCformer (Zhao et al., 2023), Preformer (Du et al., 2023), and Infomaxformer (Tang and Zhang, 2023)), the core of these methods lies in utilizing correlations in the time domain to forecast future data.

In the Fourier domain, FEDformer (Zhou et al., 2022b) applies Transformer using Frequency Enhanced Blocks and Attention modules, and CoST (Woo et al., 2022) explores learning seasonal representations. TimesNet (Wu et al., 2023) utilizes frequency for analysis and period calculation, mapping one-dimensional series to two-dimensional. FiLM (Zhou et al., 2022a) retains low-frequency Fourier components. FreTS (Yi et al., 2023c) uses Frequency-domain MLPs to predict. FITS uses Low Pass Filter to filter frequency. However, these methods, involving Fourier analysis, do not explicitly model TFS problems in the Fourier domain. In contrast, we reformulate the TFS problem as learning a transfer function of each frequency in the Fourier domain.

Classical time series decomposition techniques (Box et al., 2015) have been utilized to decompose time series into seasonal and trend components for interpretability. For instance, Autoformer (Wu et al., 2021) decomposes the data into trend and seasonal components, then employs the Transformer architecture for independent forecasts. Similarly, CoST (Woo et al., 2022) decomposes series into trend and seasonal components, carrying out separate forecasts in both time and Fourier domains. Different from these methods, our approach introduces a novel framework for dynamic decomposition, prediction, and fusion.

3. Empirical Analysis

Several studies suggest that high-frequency signals often represent noise and therefore should be discarded (Zhou et al., 2022a). However, we argue that the role of certain frequencies is not universal and can be varied across different scenarios. In some cases, high-frequency signals may indeed be noise, while in others, they may hold valuable information. To confirm this idea, we conduct experiments on three datasets. The experimental settings and analysis are detailed below.

3.1. Experimental Setup

We conduct experiments on six datasets: ETT(ETTm1, ETTm2, ETTh1, ETTh2), Weather, ECL, and Exchange-rate. For each dataset, we conduct a set of four forecasting tasks with the lookback length and prediction length both fixed to 96. The first task is the regular forecasting task. For the other three tasks, we transform the input series from the training set to the Fourier domain using Fast Fourier Transform (FFT) (Nussbaumer and Nussbaumer, 1982) and divide the frequency spectra into three subsets: the first third of the spectrum as low-frequency, the second third as middle-frequency, and the final third as high-frequency. We randomly set the Fourier coefficients corresponding to different subsets of the frequency spectrum to zero respectively in different experiments, and convert it back into the time domain as the input series. This step is to eliminate the influence of a certain subset of frequencies when training the model. We train an individual vanilla Transformer (Vaswani et al., 2017) following the standard setting (Liu et al., 2023a) for each task in all three datasets. We visualize the prediction and ground truth of future series for all tasks and all datasets in Figure 1.

3.2. Experimental Observations and Analysis

Figure 1(a) shows that in the ETTm1 dataset, after eliminating high-frequency signals, the prediction results are closer to the ground truth compared to using all frequencies. However, the prediction results are further from the ground truth after eliminating low-frequency or mid-frequency signals. Figure 1(b) shows that in the ETTm2 dataset, we will get more accurate prediction results after eliminating low-frequency from historical time series. On the contrary, we will get worse prediction results after eliminating low-frequency form historical time series, shown in Figure 1(c). In Figure 1(d), no matter which subsets of the frequency we eliminate in the ETTh2 dataset, the prediction results are more accurate than those obtained using the original frequency for prediction, among which, eliminating high frequency has a better effect. As shown in Figure 1(e), in the Exchange-rate dataset, the prediction results are more accurate in the long term after eliminating mid or high-frequency signals. Conversely, the results predicted by eliminating low-frequency signals or using all signals are closer to ground truth in the mid-term. In the weather dataset, which is shown in Figure 1(f), the results predicted by eliminating low-frequency signals are more accurate in the short-term, predicted by eliminating high-frequency are more accurate in the mid-term, and predicted by eliminating mid-frequency are more accurate in the long term.

Yet, with the absence of prior knowledge, it remains challenging to distinguish noise from vital features. Therefore, we cannot merely mark high-frequency signals as noise. Considering this, it is necessary to utilize different frequencies for forecasting and subsequently adopt a more rational method to weight these forecasting results, thus attaining the final prediction.

4. Method

In this section, we begin by reformulating the TFS problem in the Fourier domain. Subsequently, we propose FreDF, a model designed to predict the output of each frequency component respectively, then combine each output using a dynamic fusion strategy. We also present theoretical evidence supporting the idea that this dynamic fusion strategy enhances the generalization ability of FreDF.

4.1. Time series forecasting in Fourier domain

To achieve effective long-term forecasting, the model must go beyond merely memorizing past data points; it needs to grasp the underlying physical rules or inherent dynamics of the observed phenomena (Luenberger, 1979). These dynamics governing the behavior of the time series, are presumed to be independent and unchanging over time (Oppenheim et al., 1997). In Fourier analysis, any time series can be represented by a set of orthogonal bases, i.e., the Fourier components; this orthogonal characteristic helps represent each rule with the dynamic of a single Fourier component (Lange et al., 2021). In this section, we assume that the time series forecasting task is under a Linear Time-invariant (LTI) condition for the independent and time-invariant property of the inherent dynamics without loss of generality.

Specifically, from (Oppenheim et al., 1997), let be the input function and be the output function, they are both functions of time defined in Banach space and . The output of the LTI system can be defined as:

| (1) |

The goal of time-series forecasting can be regarded as finding a suitable transfer function .

In discrete case, the Equation 1 can be express as:

| (2) |

and is the discrete form of and , respectively, , is the length of time series, and is the convolution operator. The output series are obtained by applying the convolution operator between and .

The Discrete Fourier Transform (DFT) (Oppenheim et al., 1999) can transform from a function of discrete time to a function of Fourier component:

| (3) |

where is the imaginary unit, is the -th Fourier components, and is the total number of Fourier components.

Theorem 4.1.

(The convolution theorem (Katznelson, 2004)). The convolution theorem states that the Fourier transform of a convolution of two functions equals the point-wise product of their Fourier transform:

| (4) |

Applying DFT to the output sequence according to Theorem 4.1 can convert the convolution in Equation 24 into a multiplication in the Fourier domain as:

| (5) |

Note that is an unknown operator in the aforementioned analysis. Therefore we propose to estimate directly with a learnable matrix , where is the parameter. The transfer process is:

| (6) |

where is the estimated output in Fourier domain.

Applying inverse Discrete Fourier transform (iDFT) can convert the estimated output back to the time domain with:

| (7) |

The learning objective for the learnable matrix is then to minimize the Mean Square Error (MSE) between the estimated output and the ground truth of the output:

| (8) |

So far, the TFS problem in the time domain has been reformulated as learning a transfer function in the Fourier domain.

4.2. Frequency Dynamic Fusion

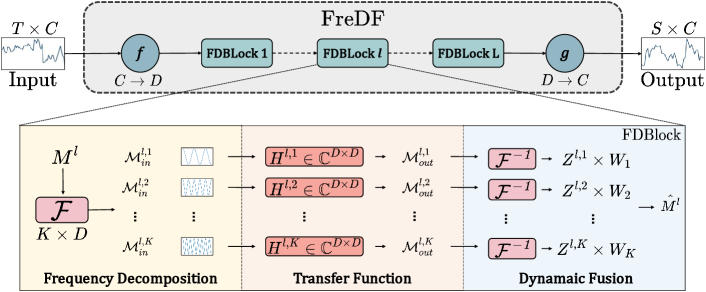

Based on the findings in Section 3, there is no universal criteria to determine the importance of a specific frequency in different situations, for the role of certain frequency changes across various scenarios. For instance, a frequency may be crucial in one scenario but negatively impact performance in another. To address this variability, we propose FreDF (Frequency Dynamic Fusion), which dynamically calculates the weights for the estimated prediction of each frequency, taking their importance into account. Our proposed FreDF consists of the Embedding, the FDBlock, and the Projection layers. We provide the pseudo-code of FreDF in algorithm 1.

To predict the future timestamps, we padding in time dimension with zeros as unknown data.

4.2.1. Embedding

In the Embedding module, we lift the input time series into an embedding space:

| (9) |

here, is the embedded representation of the input time series, is a multi-layer perceptron (MLP) used for the embedding, is the number of variables in the input time series, and is the dimension of the embedding space. It’s crucial to note that we are embedding the feature dimensions, not the time dimensions. This means that the transformation does not affect the temporal characteristics of the data. Therefore, subsequent operations, such as Fourier transformations that target the time dimensions, remain unaffected by the embedding process.

Input: Time series data , lookback length , predict length , variables number , FDBlock number , token dimension , is computed as , frequency spectrum length .

| Models |

FreDF(Ours) |

iTransformer |

PatchTST |

Crossformer |

TiDE |

TimesNet |

DLinear |

SCINet |

FEDformer |

Stationary |

Autoformer |

||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Metric | MSE | MAE | MSE | MAE | MSE | MAE | MSE | MAE | MSE | MAE | MSE | MAE | MSE | MAE | MSE | MAE | MSE | MAE | MSE | MAE | MSE | MAE | |

| ETTm1 | 96 | 0.324 | 0.367 | 0.334 | 0.368 | 0.329 | 0.367 | 0.404 | 0.426 | 0.364 | 0.387 | 0.338 | 0.375 | 0.345 | 0.372 | 0.418 | 0.438 | 0.379 | 0.419 | 0.386 | 0.398 | 0.505 | 0.475 |

| 192 | 0.365 | 0.387 | 0.377 | 0.391 | 0.367 | 0.385 | 0.450 | 0.451 | 0.398 | 0.404 | 0.374 | 0.387 | 0.380 | 0.389 | 0.439 | 0.450 | 0.426 | 0.441 | 0.459 | 0.444 | 0.553 | 0.496 | |

| 336 | 0.391 | 0.405 | 0.426 | 0.420 | 0.399 | 0.410 | 0.532 | 0.515 | 0.428 | 0.425 | 0.410 | 0.411 | 0.413 | 0.413 | 0.490 | 0.485 | 0.445 | 0.459 | 0.495 | 0.464 | 0.621 | 0.537 | |

| 720 | 0.459 | 0.436 | 0.491 | 0.459 | 0.454 | 0.439 | 0.666 | 0.589 | 0.487 | 0.461 | 0.478 | 0.450 | 0.474 | 0.453 | 0.595 | 0.550 | 0.543 | 0.490 | 0.585 | 0.516 | 0.671 | 0.561 | |

| Avg | 0.384 | 0.398 | 0.407 | 0.410 | 0.387 | 0.400 | 0.513 | 0.496 | 0.419 | 0.419 | 0.400 | 0.406 | 0.403 | 0.407 | 0.485 | 0.481 | 0.448 | 0.452 | 0.481 | 0.456 | 0.588 | 0.517 | |

| ETTm2 | 96 | 0.175 | 0.257 | 0.180 | 0.264 | 0.175 | 0.259 | 0.287 | 0.366 | 0.207 | 0.305 | 0.187 | 0.267 | 0.193 | 0.292 | 0.286 | 0.377 | 0.203 | 0.287 | 0.192 | 0.274 | 0.255 | 0.339 |

| 192 | 0.241 | 0.299 | 0.250 | 0.309 | 0.241 | 0.302 | 0.414 | 0.492 | 0.290 | 0.364 | 0.249 | 0.309 | 0.284 | 0.362 | 0.399 | 0.445 | 0.269 | 0.328 | 0.280 | 0.339 | 0.281 | 0.340 | |

| 336 | 0.303 | 0.341 | 0.311 | 0.348 | 0.305 | 0.343 | 0.597 | 0.542 | 0.377 | 0.422 | 0.321 | 0.351 | 0.369 | 0.427 | 0.637 | 0.591 | 0.325 | 0.366 | 0.334 | 0.361 | 0.339 | 0.372 | |

| 720 | 0.405 | 0.396 | 0.412 | 0.407 | 0.402 | 0.400 | 1.730 | 1.042 | 0.558 | 0.524 | 0.408 | 0.403 | 0.554 | 0.522 | 0.960 | 0.735 | 0.421 | 0.415 | 0.417 | 0.413 | 0.433 | 0.432 | |

| Avg | 0.281 | 0.323 | 0.288 | 0.332 | 0.281 | 0.326 | 0.757 | 0.610 | 0.358 | 0.404 | 0.291 | 0.333 | 0.350 | 0.401 | 0.571 | 0.537 | 0.305 | 0.349 | 0.306 | 0.347 | 0.327 | 0.371 | |

| ETTh1 | 96 | 0.367 | 0.397 | 0.386 | 0.405 | 0.414 | 0.419 | 0.423 | 0.448 | 0.479 | 0.464 | 0.384 | 0.402 | 0.386 | 0.400 | 0.654 | 0.599 | 0.376 | 0.419 | 0.513 | 0.491 | 0.449 | 0.459 |

| 192 | 0.416 | 0.424 | 0.441 | 0.436 | 0.460 | 0.445 | 0.471 | 0.474 | 0.525 | 0.492 | 0.436 | 0.429 | 0.437 | 0.432 | 0.719 | 0.631 | 0.420 | 0.448 | 0.534 | 0.504 | 0.500 | 0.482 | |

| 336 | 0.477 | 0.443 | 0.487 | 0.458 | 0.501 | 0.466 | 0.570 | 0.546 | 0.565 | 0.515 | 0.491 | 0.469 | 0.481 | 0.459 | 0.778 | 0.659 | 0.459 | 0.465 | 0.588 | 0.535 | 0.521 | 0.496 | |

| 720 | 0.478 | 0.458 | 0.503 | 0.491 | 0.500 | 0.488 | 0.653 | 0.621 | 0.594 | 0.558 | 0.521 | 0.500 | 0.519 | 0.516 | 0.836 | 0.699 | 0.506 | 0.507 | 0.643 | 0.616 | 0.514 | 0.512 | |

| Avg | 0.435 | 0.431 | 0.454 | 0.447 | 0.469 | 0.454 | 0.529 | 0.522 | 0.541 | 0.507 | 0.458 | 0.450 | 0.456 | 0.452 | 0.747 | 0.647 | 0.440 | 0.460 | 0.570 | 0.537 | 0.496 | 0.487 | |

| ETTh2 | 96 | 0.292 | 0.341 | 0.297 | 0.349 | 0.302 | 0.348 | 0.745 | 0.584 | 0.400 | 0.440 | 0.340 | 0.374 | 0.333 | 0.387 | 0.707 | 0.621 | 0.358 | 0.397 | 0.476 | 0.458 | 0.346 | 0.388 |

| 192 | 0.376 | 0.391 | 0.380 | 0.400 | 0.388 | 0.400 | 0.877 | 0.656 | 0.528 | 0.509 | 0.402 | 0.414 | 0.477 | 0.476 | 0.860 | 0.689 | 0.429 | 0.439 | 0.512 | 0.493 | 0.456 | 0.452 | |

| 336 | 0.415 | 0.426 | 0.428 | 0.432 | 0.426 | 0.433 | 1.043 | 0.731 | 0.643 | 0.571 | 0.452 | 0.452 | 0.594 | 0.541 | 1.000 | 0.744 | 0.496 | 0.487 | 0.552 | 0.551 | 0.482 | 0.486 | |

| 720 | 0.420 | 0.439 | 0.427 | 0.445 | 0.431 | 0.446 | 1.104 | 0.763 | 0.874 | 0.679 | 0.462 | 0.468 | 0.831 | 0.657 | 1.249 | 0.838 | 0.463 | 0.474 | 0.562 | 0.560 | 0.515 | 0.511 | |

| Avg | 0.376 | 0.399 | 0.383 | 0.407 | 0.387 | 0.407 | 0.942 | 0.684 | 0.611 | 0.550 | 0.414 | 0.427 | 0.559 | 0.515 | 0.954 | 0.723 | 0.437 | 0.449 | 0.526 | 0.516 | 0.450 | 0.459 | |

| Exchange | 96 | 0.082 | 0.199 | 0.086 | 0.206 | 0.088 | 0.205 | 0.256 | 0.367 | 0.094 | 0.218 | 0.107 | 0.234 | 0.088 | 0.218 | 0.267 | 0.396 | 0.148 | 0.278 | 0.111 | 0.237 | 0.197 | 0.323 |

| 192 | 0.172 | 0.294 | 0.177 | 0.299 | 0.176 | 0.299 | 0.470 | 0.509 | 0.184 | 0.307 | 0.226 | 0.344 | 0.176 | 0.315 | 0.351 | 0.459 | 0.271 | 0.315 | 0.219 | 0.335 | 0.300 | 0.369 | |

| 336 | 0.316 | 0.405 | 0.331 | 0.417 | 0.301 | 0.397 | 1.268 | 0.883 | 0.349 | 0.431 | 0.367 | 0.448 | 0.313 | 0.427 | 1.324 | 0.853 | 0.460 | 0.427 | 0.421 | 0.476 | 0.509 | 0.524 | |

| 720 | 0.835 | 0.687 | 0.847 | 0.691 | 0.901 | 0.714 | 1.767 | 1.068 | 0.852 | 0.698 | 0.964 | 0.746 | 0.839 | 0.695 | 1.058 | 0.87 | 1.195 | 0.695 | 1.092 | 0.769 | 1.447 | 0.941 | |

| Avg | 0.351 | 0.396 | 0.360 | 0.403 | 0.367 | 0.404 | 0.940 | 0.707 | 0.370 | 0.413 | 0.416 | 0.443 | 0.354 | 0.414 | 0.750 | 0.626 | 0.519 | 0.429 | 0.461 | 0.454 | 0.613 | 0.539 | |

| Weather | 96 | 0.157 | 0.208 | 0.174 | 0.214 | 0.177 | 0.218 | 0.158 | 0.230 | 0.202 | 0.261 | 0.172 | 0.220 | 0.196 | 0.255 | 0.221 | 0.306 | 0.217 | 0.296 | 0.173 | 0.223 | 0.266 | 0.336 |

| 192 | 0.205 | 0.246 | 0.221 | 0.254 | 0.225 | 0.259 | 0.206 | 0.277 | 0.242 | 0.298 | 0.219 | 0.261 | 0.237 | 0.296 | 0.261 | 0.340 | 0.276 | 0.336 | 0.245 | 0.285 | 0.307 | 0.367 | |

| 336 | 0.259 | 0.287 | 0.278 | 0.296 | 0.278 | 0.297 | 0.272 | 0.335 | 0.287 | 0.335 | 0.280 | 0.306 | 0.283 | 0.335 | 0.309 | 0.378 | 0.339 | 0.380 | 0.321 | 0.338 | 0.359 | 0.395 | |

| 720 | 0.341 | 0.339 | 0.358 | 0.349 | 0.354 | 0.348 | 0.398 | 0.418 | 0.351 | 0.386 | 0.365 | 0.359 | 0.345 | 0.381 | 0.377 | 0.427 | 0.403 | 0.428 | 0.414 | 0.410 | 0.419 | 0.428 | |

| Avg | 0.241 | 0.270 | 0.258 | 0.279 | 0.259 | 0.281 | 0.259 | 0.315 | 0.271 | 0.320 | 0.259 | 0.287 | 0.265 | 0.317 | 0.292 | 0.363 | 0.309 | 0.360 | 0.288 | 0.314 | 0.338 | 0.382 | |

| ECL | 96 | 0.150 | 0.242 | 0.148 | 0.240 | 0.181 | 0.270 | 0.219 | 0.314 | 0.237 | 0.329 | 0.168 | 0.272 | 0.197 | 0.282 | 0.247 | 0.345 | 0.193 | 0.308 | 0.169 | 0.273 | 0.201 | 0.317 |

| 192 | 0.161 | 0.253 | 0.162 | 0.253 | 0.188 | 0.274 | 0.231 | 0.322 | 0.236 | 0.330 | 0.184 | 0.289 | 0.196 | 0.285 | 0.257 | 0.355 | 0.201 | 0.315 | 0.182 | 0.286 | 0.222 | 0.334 | |

| 336 | 0.176 | 0.268 | 0.178 | 0.269 | 0.204 | 0.293 | 0.246 | 0.337 | 0.249 | 0.344 | 0.198 | 0.300 | 0.209 | 0.301 | 0.269 | 0.369 | 0.214 | 0.329 | 0.200 | 0.304 | 0.231 | 0.338 | |

| 720 | 0.217 | 0.311 | 0.225 | 0.317 | 0.246 | 0.324 | 0.280 | 0.363 | 0.284 | 0.373 | 0.220 | 0.320 | 0.245 | 0.333 | 0.299 | 0.390 | 0.246 | 0.355 | 0.222 | 0.321 | 0.254 | 0.361 | |

| Avg | 0.176 | 0.268 | 0.178 | 0.270 | 0.205 | 0.290 | 0.244 | 0.334 | 0.251 | 0.344 | 0.192 | 0.295 | 0.212 | 0.300 | 0.268 | 0.365 | 0.214 | 0.327 | 0.193 | 0.296 | 0.227 | 0.338 | |

| Solar-Energy | 96 | 0.214 | 0.247 | 0.203 | 0.237 | 0.234 | 0.286 | 0.310 | 0.331 | 0.312 | 0.399 | 0.250 | 0.292 | 0.290 | 0.378 | 0.237 | 0.344 | 0.242 | 0.342 | 0.215 | 0.249 | 0.884 | 0.711 |

| 192 | 0.230 | 0.255 | 0.233 | 0.261 | 0.267 | 0.310 | 0.734 | 0.725 | 0.339 | 0.416 | 0.296 | 0.318 | 0.320 | 0.398 | 0.280 | 0.380 | 0.285 | 0.380 | 0.254 | 0.272 | 0.834 | 0.692 | |

| 336 | 0.242 | 0.266 | 0.248 | 0.273 | 0.290 | 0.315 | 0.750 | 0.735 | 0.368 | 0.430 | 0.319 | 0.330 | 0.353 | 0.415 | 0.304 | 0.389 | 0.282 | 0.376 | 0.290 | 0.296 | 0.941 | 0.723 | |

| 720 | 0.245 | 0.271 | 0.249 | 0.275 | 0.289 | 0.317 | 0.769 | 0.765 | 0.370 | 0.425 | 0.338 | 0.337 | 0.356 | 0.413 | 0.308 | 0.388 | 0.357 | 0.427 | 0.285 | 0.295 | 0.882 | 0.717 | |

| Avg | 0.232 | 0.259 | 0.233 | 0.262 | 0.270 | 0.307 | 0.641 | 0.639 | 0.347 | 0.417 | 0.301 | 0.319 | 0.330 | 0.401 | 0.282 | 0.375 | 0.291 | 0.381 | 0.261 | 0.381 | 0.885 | 0.711 | |

| Count | 34 | 36 | 2 | 2 | 3 | 2 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | |

4.2.2. FDBlocks

Within each FDBlock, we apply Fast Fourier Transform (FFT)(Nussbaumer and Nussbaumer, 1982) to the input embedding , transforming it into the Fourier domain, which is an efficient algorithm to perform DFT:

| (10) |

here is the Fourier components, denotes the -th FDBlock and is the total number of FDBlocks.

To facilitate independent processing, we propose a decoupling strategy. Instead of treating the Fourier components as a whole, we create copies of each frequency component and only retain the -th frequency in -th copy, denoted as :

| (11) |

This strategy allows us to maintain the original dimensionality of the data while enabling independent processing of each frequency. Next, based on subsection 4.1, we aim to learn transfer functions , for each independent component , , and obtain the estimated output in the Fourier domain with:

| (12) |

The estimated output for frequency in the time domain can be obtained by applying inverse Fast Fourier Transform (iFFT) to . The result of this operation is represented as:

| (13) |

So far, we have decomposed the prediction process of each individual frequency .

Next, we apply a trainable weight vector , where each component represents the importance of the -th frequency when predicting the output embedding. The estimated output is then represented as a weighted sum of all the individual frequency predictions , with each prediction multiplied by its corresponding weight . The estimated output is represented as a weighted sum of all the individual frequency predictions , as given by the following equation:

| (14) |

where prediction is multiplied by its corresponding weight and can be either static or dynamic, i.e. fixed or learnable.

The FDBlock is formulated as an iterative architecture, where output of the -th layer serves as input of the -th layer.

During the training process, we aim to learn the transfer functions and the weight vector by minimizing a loss function, which measures the difference between the estimated output and the true output .

4.2.3. Projection

After FDBlocks, we apply another MLP to the final estimated output , projecting it back to the variable space. The result of this operation is represented as:

| (15) |

4.3. Theoretical Analysis

In this subsection, we provide a theoretical analysis to demonstrate the effectiveness of our dynamic fusion method. Without loss of generality, time series forecasting methods could be regarded as auto-regressive models (Box et al., 2015), from this perspective, we indicate that the generalization ability of time series prediction models could be reflected in the following two aspects: the capacity to capture the long-term dependency of time series, as well as the capacity to achieve good prediction results in different scenarios.

For simplicity, consider the fusion strategy in a regression setting using a mean squared loss function. Firstly, we propose to characterize the generalization error bound using Rademacher complexity (Bartlett et al., 2003) and separate the bound into three components (Theorem 4.2). Meanwhile, we also give further proof based on the above separation to illustrate that the dynamic fusion method achieves a better ability to capture long-term dependency under certain conditions (Theorem 4.3). Secondly, we demonstrate that the quantity of parameters in our method is fewer than compared methods, which indicates that our method is more flexible to apply to more scenarios, experiment results in Section 5.2 also validate our illustration as well. See Appendix A for details.

Specifically, we use , , and to denote the input space (historical sequence), target space (prediction sequence), and latent space. Define is a fusion mapping from the input space to the latent space, is a task mapping. Our goal is to learn the fusion operator , which is essentially a regression model. Under an frequency components scenario, is the frequency-specific composite function of frequency component . The final prediction of the dynamic fusion method is calculated by: , where denotes the final prediction. In contrast to static fusion, i.e., every frequency is given a predefined weight which is a constant, dynamic fusion calculates the weights of every frequency dynamically. To distinguish them, denotes the weight of frequency in static situation and the weight of frequency in dynamic situation. The generalization error of regression model is defined as:

| (16) |

where is the unknown joint distribution, is mean squared loss function. Conveniently, we simplify the regression loss as . Now we present the first main result of frequency fusion.

Theorem 4.2.

Given the historical sequence and the ground truth of prediction sequence , is the empirical error of on frequency . Then for any hypothesis in the finite set and , with probability at least , it holds that

| (17) |

where represents the expectations of fusion weights on joint distribution , represents Rademacher complexity, and represents covariance between fusion weight and loss.

Theorem 4.2 demonstrates that the generalization error of the regression model is bounded by the weighted average performances of all regression operators for each frequency in terms of empirical loss, model complexity, and the covariance between fusion weight and regression loss of all frequencies. Next, we aim to confirm whether dynamic fusion offers a tighter general error bound than static fusion. Informally, in Equation 17, the covariance term measures the joint variability of and . However, in static fusion, is a constant, which means that the covariance is equal to zero for any static fusion method. Thus the generalization error bound of static fusion methods is reduced to:

| (18) | ||||

So when the summation of the average empirical loss, the average complexity is invariant or smaller in dynamic fusion and the covariance is no greater than zero, we can ensure that dynamic fusion provably outperforms static fusion. This theorem is formally presented as:

Theorem 4.3.

Let , be the upper bound of generalization regression error of dynamic and static fusion method respectively. is the empirical error defined in Theorem 4.2. Then for any hypothesis , in finite set and , it holds that

| (19) |

with probability at least , if we have

| (20) |

and

| (21) |

for all frequencies, where is the Pearson correlation coefficient which measures the correlation between fusion weights and the loss of each frequency .

Theorem 4.2 and Theorem 4.3 verify that the dynamic fusion method has a lower generalization bound, which indicates the capacity to capture the long-term dependency of our method. Furthermore, suppose for each frequency, the regression operator used in dynamic and static fusion are of the same architecture, then the intrinsic complexity can be invariant. Thus, it holds that

| (22) |

In Equation 22, it is easy to derive the conclusion that our model has a lower average complexity, corresponding to a lower quantity of parameters during the training process. Experiment results in Section 5.2 also validate this conclusion.

5. Experiments

In this section, we first provide the details of the implementation and datasets. Next, we present the comparison results on eight benchmark datasets. Lastly, we conduct ablation studies to evaluate the effectiveness of each module in our method.

| Methods | Metric | ETTh1 | ETTm1 | Exchange-rate | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 96 | 192 | 336 | 720 | 96 | 192 | 336 | 720 | 96 | 192 | 336 | 720 | ||

| W Transfer function | MSE | 0.367 | 0.416 | 0.477 | 0.478 | 0.324 | 0.365 | 0.391 | 0.459 | 0.082 | 0.172 | 0.316 | 0.835 |

| MAE | 0.397 | 0.424 | 0.443 | 0.458 | 0.367 | 0.387 | 0.405 | 0.436 | 0.199 | 0.294 | 0.405 | 0.687 | |

| W/O Transfer function | MSE | 0.439 | 0.492 | 0.529 | 0.522 | 0.378 | 0.421 | 0.441 | 0.518 | 0.129 | 0.218 | 0.254 | 0.897 |

| MAE | 0.444 | 0.505 | 0.561 | 0.541 | 0.405 | 0.432 | 0.439 | 0.487 | 0.251 | 0.344 | 0.312 | 0.709 | |

5.1. Main Results

We thoroughly evaluate the proposed FreDF on various long-term time series forecasting benchmarks. For better comparison, we follow the experiment settings of iTransformer in (Liu et al., 2023a) the prediction lengths for both training and evaluation vary within the set , with a fixed lookback length of .

5.1.1. Baselines

We carefully choose 10 well-acknowledged forecasting models as our benchmark, including (1) Transformer-based methods: iTransformer (Liu et al., 2023a), Autoformer (Wu et al., 2021), FEDformer (Zhou et al., 2022b), Stationary (Liu et al., 2022a), Crossformer (Zhang and Yan, 2023), PatchTST (Nie et al., 2023); (2) Linear-based methods: DLinear (Zeng et al., 2023), TiDE (Das et al., 2023); and (3) TCN-based methods: SCINet (Liu et al., 2022b), TimesNet (Wu et al., 2023).

5.1.2. Forecasting Results

Table 1 presents the results of FreDF in long-term multivariate forecasting with the best in bold and the second underlined. The lower MSE/MAE indicates the more accurate prediction result. Results demonstrate that our model performs optimally in 70 out of 80 benchmarks. Compared to FEDformer (Zhou et al., 2022b), FreDF shows an average improvement of in terms of MSE and MAE, reaching up to improvement on the Exchange-rate dataset. Compared to the best-performing Transformer-based model:iTransformer (Liu et al., 2023a), FreDF consistently achieves superior performance across almost all datasets.

| Models |

FreDF |

FreSF |

|||

|---|---|---|---|---|---|

| Metric | MSE | MAE | MSE | MAE | |

| Weather | 96 | 0.153 | 0.199 | 0.175 | 0.239 |

| 192 | 0.205 | 0.246 | 0.215 | 0.276 | |

| 336 | 0.259 | 0.587 | 0.263 | 0.312 | |

| 720 | 0.341 | 0.339 | 0.343 | 0.377 | |

| Exchange | 96 | 0.082 | 0.199 | 0.129 | 0.239 |

| 192 | 0.172 | 0.294 | 0.231 | 0.332 | |

| 336 | 0.316 | 0.405 | 0.360 | 0.451 | |

| 720 | 0.835 | 0.687 | 0.891 | 0.741 | |

| ETTh1 | 96 | 0.367 | 0.397 | 0.428 | 0.437 |

| 192 | 0.416 | 0.424 | 0.475 | 0.456 | |

| 336 | 0.477 | 0.443 | 0.509 | 0.477 | |

| 720 | 0.478 | 0.458 | 0.509 | 0.490 | |

| ETTm1 | 96 | 0.324 | 0.367 | 0.369 | 0.401 |

| 192 | 0.365 | 0.387 | 0.419 | 0.430 | |

| 336 | 0.391 | 0.405 | 0.440 | 0.438 | |

| 720 | 0.459 | 0.436 | 0.497 | 0.468 | |

5.2. Ablation Study

In this section, we conduct ablation studies to examine the influence of transfer functions, dynamic fusion mechanisms, and the number of parameters in the proposed FreDF.

5.2.1. Influence of transfer function

We conduct an ablation study about the influence of the transfer function. We remove the transfer function in FreDF as the control group, follow the setup in Section 5.1, and carry out predictions on the ETTh1, ETTm1, and Exchange-rate dataset. We present the results in Table 2, which illustrates the crucial role of the transfer function and confirms the correctness of our analysis in Section 4.1.

5.2.2. Influence of dynamic fusion

We conduct an ablation study to investigate the influence of dynamic fusion. We replace the learnable weight vector with a fixed weight vector and name this modified model FreSF. Predictions are carried out on the ETT(ETTh1, ETTh2, ETTm1, ETTm2), Weather, and Exchang-rate datasets using the setup outlined in Section 5.1. The results are presented in Table LABEL:tab:ab2. Additionally, we visualize the prediction results (with a prediction length ) for both FreSF and FreDF in Appendix D. The experimental results demonstrate the effectiveness of the dynamic fusion strategy.

| Models | Ours | iTransformer | PatchTST | FEDformer | FiLM |

|---|---|---|---|---|---|

| params | 151.4K | 3.1M | 3.5M | 14.0M | 12.0M |

5.2.3. Number of parameters

We use iTransformer (Liu et al., 2023a), patchTST (Nie et al., 2023), FEDformer (Zhou et al., 2022b) and FiLM (Zhou et al., 2022a) for comparison, and calculate the number of model parameters when forecasting the same task, present the results in Table 4. Our model despite using a relatively small number of parameters, can achieve good accuracy in prediction tasks. This also validates the superiority of our model, which is consistent with the theoretical analysis in Section 4.3.

6. Conclusion

In this paper, we experimentally explore the different roles of frequency in various scenarios. To better utilize these distinctions, we reformulate the problem of time series forecasting as learning transfer functions in the Fourier domain and design the FreDF model, which can independently forecast each Fourier component and dynamically fuse outputs from different frequencies. Then, we provide a novel understanding of the generalization ability of time series forecasting. Further, we also propose the generalization bound for time series forecasting and demonstrate that FreDF has a lower generalization bound, indicating its better generalization ability. Extensive experiments validate the effectiveness of FreDF on multiple benchmark datasets.

Acknowledgements.

The authors would like to thank the anonymous reviewers for their valuable comments. This work was supported in part by the Postdoctoral Fellowship Program of CPSF (Grant No. GZB20230790), the China Postdoctoral Science Foundation (Grant No. 2023M743639), and the Special Research Assistant Fund, Chinese Academy of Sciences (Grant No. E3YD590101).References

- (1)

- Adams ([n. d.]) Michael D Adams. [n. d.]. Signals and Systems. ([n. d.]).

- Al-Turjman et al. (2023) Fadi Al-Turjman, Mohsin Nawaz, Utku Ulusar, and Raed I. Saeed. 2023. Artificial intelligence-based traffic flow prediction: a comprehensive review. Journal of Electrical Systems and Information Technology (2023). https://doi.org/10.1186/s43067-023-00081-6

- Ariyo et al. (2014) Adebiyi A Ariyo, Adewumi O Adewumi, and Charles K Ayo. 2014. Stock price prediction using the ARIMA model. In 2014 UKSim-AMSS 16th international conference on computer modelling and simulation. IEEE, 106–112.

- Bai et al. (2018) Shaojie Bai, J. Zico Kolter, and Vladlen Koltun. 2018. An Empirical Evaluation of Generic Convolutional and Recurrent Networks for Sequence Modeling. arXiv:1803.01271 [cs.LG]

- Bartlett et al. (2003) Bartlett, Peter, L., Mendelson, and Shahar. 2003. Rademacher and Gaussian Complexities: Risk Bounds and Structural Results. Journal of Machine Learning Research 3, 3 (2003), 463–463.

- Bilal et al. (2022) Muhammad Bilal, Hyeok Kim, Muhammad Fayaz, and Pravin Pawar. 2022. Comparative Analysis of Time Series Forecasting Approaches for Household Electricity Consumption Prediction. arXiv:2207.01019 [cs.LG]

- Box et al. (2015) George EP Box, Gwilym M Jenkins, Gregory C Reinsel, and Greta M Ljung. 2015. Time series analysis: forecasting and control. John Wiley & Sons.

- Box ([n. d.]) George E P Box. [n. d.]. Time Series Analysis. ([n. d.]).

- Bracewell (1986) R. N. Bracewell. 1986. The Fourier Transform and its Applications. McGraw Hill.

- Brillinger (1981) David R. Brillinger. 1981. Time Series: Data Analysis and Theory. Holden-Day.

- Chen et al. (2024) Peng Chen, Yingying ZHANG, Yunyao Cheng, Yang Shu, Yihang Wang, Qingsong Wen, Bin Yang, and Chenjuan Guo. 2024. Pathformer: Multi-scale Transformers with Adaptive Pathways for Time Series Forecasting.

- Cheng et al. (2023) Yue Cheng, Weiwei Xing, Witold Pedrycz, Sidong Xian, and Weibin Liu. 2023. NFIG-X: Non-linear fuzzy information granule series for long-term traffic flow time series forecasting. IEEE Transactions on Fuzzy Systems (2023).

- Chiarot and Silvestri (2023) Giacomo Chiarot and Claudio Silvestri. 2023. Time Series Compression Survey. Comput. Surveys 55, 10 (Feb. 2023), 1–32. https://doi.org/10.1145/3560814

- Das et al. (2023) Abhimanyu Das, Weihao Kong, Andrew Leach, Rajat Sen, and Rose Yu. 2023. Long-term Forecasting with TiDE: Time-series Dense Encoder. arXiv preprint arXiv:2304.08424 (2023).

- Du et al. (2023) Dazhao Du, Bing Su, and Zhewei Wei. 2023. Preformer: predictive transformer with multi-scale segment-wise correlations for long-term time series forecasting. In ICASSP 2023-2023 IEEE International Conference on Acoustics, Speech and Signal Processing (ICASSP). IEEE, 1–5.

- Duchon and Hale (2012) Claude Duchon and Robert Hale. 2012. Time Series Analysis in Meteorology and Climatology: An Introduction. John Wiley & Sons, Ltd.

- Evans (2022) Lawrence C. Evans. 2022. Partial differential equations. Vol. 19. American Mathematical Society. https://books.google.com/books?hl=zh-CN&lr=&id=Ott1EAAAQBAJ&oi=fnd&pg=PP1&dq=Partial+Differential+Equations+evans&ots=cUNzAH2MyK&sig=yAAqmzvrLLXVgW7JzKTZ3qzvlqo

- Guo et al. (2023) Jinkang Guo, Zhibo Wan, and Zhihan Lv. 2023. Digital Twins Fuzzy System Based on Time Series Forecasting Model LFTformer (MM ’23). Association for Computing Machinery, 7094–7100.

- Hamilton (2020) James D Hamilton. 2020. Time series analysis. Princeton university press.

- Hewamalage et al. (2021) Hansika Hewamalage, Christoph Bergmeir, and Kasun Bandara. 2021. Recurrent Neural Networks for Time Series Forecasting: Current status and future directions. International Journal of Forecasting 37, 1 (Jan. 2021), 388–427. https://doi.org/10.1016/j.ijforecast.2020.06.008

- Hidalgo (2009) Javier Hidalgo. 2009. Journal of Time Series Econometrics. De Gruyter (2009). https://www.degruyter.com/journal/key/jtse/html

- Hoffmann et al. (2020) Maximilian Hoffmann, Leander Kotzur, Detlef Stolten, and Martin Robinius. 2020. A Review on Time Series Aggregation Methods for Energy System Models. Energies 13, 3 (2020), 641. https://doi.org/10.3390/en13030641

- Hu and Xiao (2022) Yuntong Hu and Fuyuan Xiao. 2022. Time-Series Forecasting Based on Fuzzy Cognitive Visibility Graph and Weighted Multisubgraph Similarity. IEEE Transactions on Fuzzy Systems 31, 4 (2022), 1281–1293.

- Katznelson (2004) Yitzhak Katznelson. 2004. An introduction to harmonic analysis. Cambridge University Press.

- Kim et al. (5555) H. Kim, S. Kim, S. Min, and B. Lee. 5555. Contrastive Time-Series Anomaly Detection. 01 (nov 5555), 1–14. https://doi.org/10.1109/TKDE.2023.3335317

- Kingma and Ba (2015) Diederik P. Kingma and Jimmy Ba. 2015. Adam: A Method for Stochastic Optimization. ICLR (2015).

- Lange et al. (2021) Henning Lange, Steven L. Brunton, and J. Nathan Kutz. 2021. From Fourier to Koopman: Spectral methods for long-term time series prediction. The Journal of Machine Learning Research 22, 1 (2021), 1881–1918. Publisher: JMLRORG.

- LeCun et al. (2015) Yann LeCun, Yoshua Bengio, and Geoffrey Hinton. 2015. Deep learning. Nature 521, 7553 (May 2015), 436–444. https://doi.org/10.1038/nature14539 Number: 7553 Publisher: Nature Publishing Group.

- Li et al. (2021c) Fang Li, Yuqing Tang, Fusheng Yu, Witold Pedrycz, Yuming Liu, and Wenyi Zeng. 2021c. Multilinear-trend fuzzy information granule-based short-term forecasting for time series. IEEE Transactions on Fuzzy Systems 30, 8 (2021), 3360–3372.

- Li et al. (2021a) Jianxin Li, Xiong Hui, and Wancai Zhang. 2021a. Informer: Beyond efficient transformer for long sequence time-series forecasting. arXiv: 2012.07436 (2021).

- Li et al. (2015) Li Li, Xiaonan Su, Yi Zhang, Yuetong Lin, and Zhiheng Li. 2015. Trend modeling for traffic time series analysis: An integrated study. IEEE Transactions on Intelligent Transportation Systems 16, 6 (2015), 3430–3439.

- Li et al. (2021b) Zongyi Li, Nikola Kovachki, Kamyar Azizzadenesheli, Burigede Liu, Kaushik Bhattacharya, Andrew Stuart, and Anima Anandkumar. 2021b. Fourier Neural Operator for Parametric Partial Differential Equations. https://doi.org/10.48550/arXiv.2010.08895 arXiv:2010.08895 [cs, math].

- Liang et al. (2023) Daojun Liang, Haixia Zhang, Dongfeng Yuan, Xiaoyan Ma, Dongyang Li, and Minggao Zhang. 2023. Does Long-Term Series Forecasting Need Complex Attention and Extra Long Inputs? arXiv preprint arXiv:2306.05035 (2023).

- Liu et al. (2022b) Minhao Liu, Ailing Zeng, Muxi Chen, Zhijian Xu, Qiuxia Lai, Lingna Ma, and Qiang Xu. 2022b. SCINet: time series modeling and forecasting with sample convolution and interaction. NeurIPS (2022).

- Liu et al. (2023a) Yong Liu, Tengge Hu, Haoran Zhang, Haixu Wu, Shiyu Wang, Lintao Ma, and Mingsheng Long. 2023a. iTransformer: Inverted Transformers Are Effective for Time Series Forecasting. arXiv:arXiv:2310.06625

- Liu et al. (2023b) Yong Liu, Chenyu Li, Jianmin Wang, and Mingsheng Long. 2023b. Koopa: Learning Non-stationary Time Series Dynamics with Koopman Predictors. arXiv preprint arXiv:2305.18803 (2023).

- Liu et al. (2022a) Yong Liu, Haixu Wu, Jianmin Wang, and Mingsheng Long. 2022a. Non-stationary Transformers: Rethinking the Stationarity in Time Series Forecasting. NeurIPS (2022).

- Lonlac et al. (2020) Jerry Lonlac, Arnaud Doniec, Marin Lujak, and Stephane Lecoeuche. 2020. Extracting Seasonal Gradual Patterns from Temporal Sequence Data Using Periodic Patterns Mining. (2020). https://arxiv.org/abs/2010.10289

- Lorenz (1956a) Edward N Lorenz. 1956a. Empirical orthogonal functions and statistical weather prediction. Vol. 1. Massachusetts Institute of Technology, Department of Meteorology Cambridge.

- Lorenz (1956b) Edward N Lorenz. 1956b. Empirical orthogonal functions and statistical weather prediction. Vol. 1. Massachusetts Institute of Technology, Department of Meteorology Cambridge.

- Luenberger (1979) David G Luenberger. 1979. Dynamic Systems. J. Wiley Sons.

- Mitrovic et al. (2020) Jovana Mitrovic, Brian McWilliams, Jacob Walker, Lars Buesing, and Charles Blundell. 2020. Representation learning via invariant causal mechanisms. arXiv preprint arXiv:2010.07922 (2020).

- Nie et al. (2023) Yuqi Nie, Nam H Nguyen, Phanwadee Sinthong, and Jayant Kalagnanam. 2023. A Time Series is Worth 64 Words: Long-term Forecasting with Transformers. ICLR (2023).

- Nussbaumer and Nussbaumer (1982) Henri J Nussbaumer and Henri J Nussbaumer. 1982. The fast Fourier transform. Springer.

- Oppenheim et al. (1999) Alan V. Oppenheim, Ronald W. Schafer, and John R. Buck. 1999. Discrete-Time Signal Processing (second ed.). Prentice-hall Englewood Cliffs.

- Oppenheim et al. (1997) Alan V Oppenheim, Alan S Willsky, Syed Hamid Nawab, and Jian-Jiun Ding. 1997. Signals and systems. Vol. 2. Prentice hall Upper Saddle River, NJ.

- Paszke et al. (2019) Adam Paszke, S. Gross, Francisco Massa, A. Lerer, James Bradbury, Gregory Chanan, Trevor Killeen, Z. Lin, N. Gimelshein, L. Antiga, Alban Desmaison, Andreas Köpf, Edward Yang, Zach DeVito, Martin Raison, Alykhan Tejani, Sasank Chilamkurthy, Benoit Steiner, Lu Fang, Junjie Bai, and Soumith Chintala. 2019. PyTorch: An Imperative Style, High-Performance Deep Learning Library. NeurIPS (2019).

- Qin et al. (2021) Zequn Qin, Pengyi Zhang, Fei Wu, and Xi Li. 2021. FcaNet: Frequency Channel Attention Networks. arXiv:2012.11879 [cs.CV]

- So (2024) H.C. So. 2024. Discrete-Time Fourier Transform. City University of Hong Kong (2024). [^1^][5]

- Tang and Zhang (2023) Peiwang Tang and Xianchao Zhang. 2023. Infomaxformer: Maximum Entropy Transformer for Long Time-Series Forecasting Problem. arXiv preprint arXiv:2301.01772 (2023).

- Tang et al. (2021) Yuqing Tang, Fusheng Yu, Witold Pedrycz, Xiyang Yang, Jiayin Wang, and Shihu Liu. 2021. Building trend fuzzy granulation-based LSTM recurrent neural network for long-term time-series forecasting. IEEE transactions on fuzzy systems 30, 6 (2021), 1599–1613.

- Tolstikhin et al. (2021) Ilya O Tolstikhin, Neil Houlsby, Alexander Kolesnikov, Lucas Beyer, Xiaohua Zhai, Thomas Unterthiner, Jessica Yung, Andreas Steiner, Daniel Keysers, Jakob Uszkoreit, et al. 2021. Mlp-mixer: An all-mlp architecture for vision. NeurIPS (2021).

- Vaswani et al. (2017) Ashish Vaswani, Noam Shazeer, Niki Parmar, Jakob Uszkoreit, Llion Jones, Aidan N Gomez, Łukasz Kaiser, and Illia Polosukhin. 2017. Attention is all you need. Advances in neural information processing systems 30 (2017).

- Wang et al. (2024) Shiyu Wang, Haixu Wu, Xiaoming Shi, Tengge Hu, Huakun Luo, Lintao Ma, James Y. Zhang, and JUN ZHOU. 2024. TimeMixer: Decomposable Multiscale Mixing for Time Series Forecasting. In The Twelfth International Conference on Learning Representations. https://openreview.net/forum?id=7oLshfEIC2

- Wen et al. (2023) Qingsong Wen, Tian Zhou, Chaoli Zhang, Weiqi Chen, Ziqing Ma, Junchi Yan, and Liang Sun. 2023. Transformers in Time Series: A Survey. arXiv:2202.07125 [cs.LG]

- Winters (1960) Peter R Winters. 1960. Forecasting sales by exponentially weighted moving averages. Management science 6, 3 (1960), 324–342.

- Woo et al. (2022) Gerald Woo, Chenghao Liu, Doyen Sahoo, Akshat Kumar, and Steven Hoi. 2022. CoST: Contrastive learning of disentangled seasonal-trend representations for time series forecasting. arXiv preprint arXiv:2202.01575 (2022).

- Wu et al. (2023) Haixu Wu, Tengge Hu, Yong Liu, Hang Zhou, Jianmin Wang, and Mingsheng Long. 2023. TimesNet: Temporal 2D-Variation Modeling for General Time Series Analysis. ICLR (2023).

- Wu et al. (2021) Haixu Wu, Jiehui Xu, Jianmin Wang, and Mingsheng Long. 2021. Autoformer: Decomposition Transformers with Auto-Correlation for Long-Term Series Forecasting. NeurIPS (2021).

- Xu et al. (2020) Kai Xu, Minghai Qin, Fei Sun, Yuhao Wang, Yen-Kuang Chen, and Fengbo Ren. 2020. Learning in the Frequency Domain. arXiv:2002.12416 [cs.CV]

- Xu et al. (2024) Zhijian Xu, Ailing Zeng, and Qiang Xu. 2024. FITS: Modeling Time Series with $10k$ Parameters. In The Twelfth International Conference on Learning Representations. https://openreview.net/forum?id=bWcnvZ3qMb

- Xu (2020) Zhi-Qin John Xu. 2020. Frequency Principle: Fourier Analysis Sheds Light on Deep Neural Networks. Communications in Computational Physics 28, 5 (June 2020), 1746–1767. https://doi.org/10.4208/cicp.oa-2020-0085

- Yang et al. (2023) Chunwei Yang, Xiaoxu Chen, Lijun Sun, and Hongyu Yang. 2023. Enhancing Representation Learning for Periodic Time Series with Floss: A Frequency Domain Regularization Approach. (2023). https://arxiv.org/pdf/2308.01011.pdf

- Yang et al. (2020) Zhangjing Yang, Weiwu Yan, Xiaolin Huang, and Lin Mei. 2020. Adaptive temporal-frequency network for time-series forecasting. IEEE Transactions on Knowledge and Data Engineering 34, 4 (2020), 1576–1587.

- Yi et al. (2023a) Kun Yi, Qi Zhang, Longbing Cao, Shoujin Wang, Guodong Long, Liang Hu, Hui He, Zhendong Niu, Wei Fan, and Hui Xiong. 2023a. A Survey on Deep Learning based Time Series Analysis with Frequency Transformation. arXiv:2302.02173 [cs.LG]

- Yi et al. (2023b) Kun Yi, Qi Zhang, Wei Fan, Hui He, Liang Hu, Pengyang Wang, Ning An, Longbing Cao, and Zhendong Niu. 2023b. FourierGNN: Rethinking Multivariate Time Series Forecasting from a Pure Graph Perspective. arXiv:2311.06190 [cs.LG]

- Yi et al. (2023c) Kun Yi, Qi Zhang, Wei Fan, Shoujin Wang, Pengyang Wang, Hui He, Defu Lian, Ning An, Longbing Cao, and Zhendong Niu. 2023c. Frequency-domain MLPs are More Effective Learners in Time Series Forecasting. arXiv:2311.06184 [cs.LG]

- Young et al. (1999) Peter C Young, Diego J Pedregal, and Wlodek Tych. 1999. Dynamic harmonic regression. Journal of forecasting 18, 6 (1999), 369–394.

- Zeng et al. (2023) Ailing Zeng, Muxi Chen, Lei Zhang, and Qiang Xu. 2023. Are Transformers Effective for Time Series Forecasting? AAAI (2023).

- Zhan et al. (2023) Tianxiang Zhan, Yuanpeng He, Yong Deng, and Zhen Li. 2023. Differential Convolutional Fuzzy Time Series Forecasting. IEEE Transactions on Fuzzy Systems (2023).

- Zhang et al. (2022) Xiang Zhang, Ziyuan Zhao, Theodoros Tsiligkaridis, and Marinka Zitnik. 2022. Self-Supervised Contrastive Pre-Training For Time Series via Time-Frequency Consistency. arXiv:2206.08496 [cs.LG]

- Zhang and Yan (2023) Yunhao Zhang and Junchi Yan. 2023. Crossformer: Transformer utilizing cross-dimension dependency for multivariate time series forecasting. ICLR (2023).

- Zhao et al. (2023) Yanjun Zhao, Ziqing Ma, Tian Zhou, Mengni Ye, Liang Sun, and Yi Qian. 2023. GCformer: An Efficient Solution for Accurate and Scalable Long-Term Multivariate Time Series Forecasting. In Proceedings of the 32nd ACM International Conference on Information and Knowledge Management. 3464–3473.

- Zhou et al. (2022c) Kun Zhou, Hui Yu, Wayne Xin Zhao, and Ji-Rong Wen. 2022c. Filter-enhanced MLP is All You Need for Sequential Recommendation. In Proceedings of the ACM Web Conference 2022 (WWW ’22). ACM. https://doi.org/10.1145/3485447.3512111

- Zhou et al. (2022a) Tian Zhou, Ziqing Ma, Qingsong Wen, Liang Sun, Tao Yao, Wotao Yin, Rong Jin, et al. 2022a. Film: Frequency improved legendre memory model for long-term time series forecasting. Advances in Neural Information Processing Systems 35 (2022), 12677–12690.

- Zhou et al. (2022b) Tian Zhou, Ziqing Ma, Qingsong Wen, Xue Wang, Liang Sun, and Rong Jin. 2022b. FEDformer: Frequency enhanced decomposed transformer for long-term series forecasting. ICML (2022).

- Zhu et al. (2023) Chenglong Zhu, Xueling Ma, Weiping Ding, and Jianming Zhan. 2023. Long-term time series forecasting with multi-linear trend fuzzy information granules for LSTM in a periodic framework. IEEE Transactions on Fuzzy Systems (2023).

The Appendix provides supplementary information and additional details that support the primary discoveries and methodologies proposed in this paper. It is organized into several sections: Appendix A contains the proof of Theorem 2 and Theorem 3.

Appendix A Proofs

In this section, we will prove Theorem 2 and Theorem 3, which is used for the theoretical analysis.

A.1. Proof of Theorem 2

Note that is a convex regression loss function, which indicates that

| (23) |

Then we take the expectation on both sides of the above equation

| (24) |

since expectation is a linear operator and the expected value of the product is equal to the product of the expected values plus the covariance, we can further decompose the right-hand side of the equation into

| (25) | |||

Next, we recap the Rademacher complexity measure for model complexity. We use complexity based learning theory to quantify the generalization error of the proposed model.

Given the historical sequence and the ground truth of the prediction sequence, is the empirical error of . Then for any hypothesis in the finite set and , with probability at least , we have

| (26) |

where is the Rademacher complexities.

Finally, it holds with probability at least that

| (27) |

A.2. Proof of Theorem 3

Let , be the upper bound of the generalization regression error of dynamic and static fusion method, respectively. is the empirical error defined in Theorem 1. Theoretically, optimizing over the same function class results in the same empirical risk. Therefore,

| (28) |

Additionally, the intrinsic complexity is also invariant

| (29) |

Thus in this special case, it holds that

| (30) |

and

| (31) |

if .

Since the covariance and the correlation coefficient have the same sign, when , the covariance is also less than or equal to zero. Therefore, it holds that

| (32) |

with probability at least , if we have

| (33) |

and

| (34) |

for all frequencies .

Appendix B Implement Details

All the experiments are implemented in PyTorch (Paszke et al., 2019) and trained on NVIDIA V100 32GB GPUs. We use ADAM (Kingma and Ba, 2015) with an initial learning rate in and MSELoss for model optimization. An early stopping counter is employed to stop the training process after three epochs if no loss degradation on the valid set is observed. The mean square error (MSE) and mean absolute error (MAE) are used as metrics. All experiments are repeated 3 times and the mean of the metrics is used in the final results. The transfer function is implemented using the complex 64 data type in PyTorch. The batch size is set to 4 and the number of training epochs is set to 10. We set the number of FDBlocks in our proposed model . The dimension of series representations , or it is not embedded at all. We set the dropout rates in .

| Dataset | Dim | Prediction Length | Dataset Size | Frequency | Information |

|---|---|---|---|---|---|

| ETTh1,ETTh2 | 7 |

{96, 192, 336, 720} |

(8545, 2881, 2881) | Hourly | Electricity |

| ETTm1,ETTm2 | 7 |

{96, 192, 336, 720} |

(34465, 11521, 11521) | 15min | Electricity |

| Exchange | 8 |

{96, 192, 336, 720} |

(5120, 665, 1422) | Daily | Economy |

| Weather | 21 |

{96, 192, 336, 720} |

(36792, 5271, 10540) | 10min | Weather |

| ECL | 321 |

{96, 192, 336, 720} |

(18317, 2633, 5261) | Hourly | Electricity |

| Solar-Energy | 137 |

{96, 192, 336, 720} |

(36601, 5161, 10417) | 10min | Energy |

Appendix C Dataset Descriptions

In this paper, we conducted tests using eight real-world datasets. These datasets include:

-

•

ETT contains two sub-datasets: ETT1 and ETT2, collected from two electricity transformers at two stations. Each of them has two versions in different resolutions (15 minutes and 1h). ETT dataset contains multiple series of loads and one series of oil temperatures.

-

•

Weather covers 21 meteorological variables recorded at 10-minute intervals throughout the year 2020. The data was collected by the Max Planck Institute for Biogeochemistry’s Weather Station, providing valuable meteorological insights.

-

•

Exchange-rate, which contains daily exchange rate data spanning from 1990 to 2016 for eight countries. It offers information on the currency exchange rates across different time periods.

-

•

ECL contains the electricity consumption of 370 clients for short-term forecasting while it contains the electricity consumption of 321 clients for long-term forecasting. It is collected since 01/01/2011. The data sampling interval is every 15 minutes.

-

•

Solar-Energy is about the solar power collected by the National Renewable Energy Laboratory. We choose the power plant data points in Florida as the data set which contains 593 points. The data is collected from 01/01/2006 to 31/12/2016 with the sampling interval of every 1 hour.

We follow the same data processing and train-validation-test set split protocol used in iTransformer, where the train, validation, and test datasets are strictly divided according to chronological order to make sure there are no data leakage issues. As for the forecasting settings, the lookback length is set to 96, while their prediction length varies in . The details of the datasets are provided in Table 5.

Appendix D Influence of dynamic fusion

We conduct an ablation study to investigate the influence of dynamic fusion. We replace the learnable weight vector with a fixed weight vector and name this modified model FreSF. Predictions are carried out on the ETT(ETTh1, ETTh2, ETTm1, ETTm2), Weather, and Exchang-rate datasets. We visualize the prediction results (with a prediction length ) for both FreSF and FreDF in Figure 3. In the ETTh1 and ETTm1 datasets, static fusion manages to capture the overall trends and detailed shifts, but the predicted values deviate significantly from the actual figures. This issue can be effectively addressed by employing dynamic fusion. Similarly, in the ETTh2 and ETTm2 datasets, static fusion’s predictions are not quite accurate at the extreme points, a problem that dynamic fusion can effectively solve. Likewise, when dynamic fusion is applied to the Weather and Exchange-rate datasets, the prediction curve aligns more closely with the ground truth.

Appendix E Ablation on the influence of operation sequence

We conduct an ablation study about the influence of operation sequence. Our model initially conducts an inverse fast Fourier transform(iFFT) on the spectrum obtained from the transfer function for each frequency . We then dynamically fusion the predicted results for each frequency. In this section, we first dynamically fuse the spectrums obtained from the transfer function for each frequency, followed by an iFFT on the result of this fusion. We prevent the result in Table 6

| Methods | Metric | Weather | ECL | Exchange-rate | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 96 | 192 | 336 | 720 | 96 | 192 | 336 | 720 | 96 | 192 | 336 | 720 | ||

| Dynamic Fusion on (Our) | MSE | 0.157 | 0.205 | 0.259 | 0.341 | 0.150 | 0.161 | 0.176 | 0.217 | 0.082 | 0.172 | 0.316 | 0.835 |

| MAE | 0.208 | 0.246 | 0.287 | 0.339 | 0.242 | 0.253 | 0.268 | 0.311 | 0.199 | 0.294 | 0.405 | 0.687 | |

| Dynamic Fusion on spectrums | MSE | 0.161 | 0.209 | 0.262 | 0.345 | 0.154 | 0.163 | 0.176 | 0.221 | 0.083 | 0.174 | 0.318 | 0.839 |

| MAE | 0.214 | 0.253 | 0.292 | 0.347 | 0.242 | 0.253 | 0.270 | 0.313 | 0.199 | 0.295 | 0.406 | 0.670 | |

Appendix F Ablation on the influence of FDBlock number:

To further figure out the impact of different numbers of FDBlock, we perform experiments with three different ranging from 1 to 3. As shown in Table 7. And is a generally good choice.

| FDBlock |

ETTh2 |

ETTm2 |

Weather |

||||

|---|---|---|---|---|---|---|---|

|

Metric |

MSE |

MAE |

MSE |

MAE |

MSE |

MAE |

|

|

96 |

0.292 |

0.341 |

0.175 |

0.257 |

0.157 |

0.208 |

|

|

192 |

0.376 |

0.391 |

0.242 |

0.300 |

0.205 |

0.246 |

|

|

336 |

0.419 |

0.428 |

0.303 |

0.341 |

0.260 |

0.287 |

|

|

720 |

0.420 |

0.439 |

0.405 |

0.396 |

0.341 |

0.339 |

|

|

96 |

0.295 |

0.342 |

0.176 |

0.257 |

0.157 |

0.209 |

|

|

192 |

0.377 |

0.390 |

0.241 |

0.300 |

0.206 |

0.246 |

|

|

336 |

0.415 |

0.426 |

0.304 |

0.343 |

0.259 |

0.287 |

|

|

720 |

0.422 |

0.440 |

0.406 |

0.398 |

0.342 |

0.339 |

|

|

96 |

0.293 |

0.341 |

0.176 |

0.258 |

0.158 |

0.208 |

|

|

192 |

0.378 |

0.394 |

0.241 |

0.299 |

0.207 |

0.248 |

|

|

336 |

0.416 |

0.426 |

0.304 |

0.345 |

0.262 |

0.289 |

|

|

720 |

0.421 |

0.440 |

0.407 |

0.397 |

0.343 |

0.340 |

|

Appendix G Motivation Experiments

We present the full results of motivation experiments in Table 8. After eliminating low-frequency, we observe enhanced accuracy in the ETTm2 and ETTh2 datasets. Similarly, eliminating mid-frequency signals led to improved results in the ETTh2 and Exchange-rate datasets. The elimination of high-frequency results in more precise results in ETTh1, ETTm2, ETTh1, ETTh2, Exchange-rate, and weather datasets. The most significant improvement is seen when eliminating high-frequency signals. Nevertheless, removing low-frequency and mid-frequency signals can also improve prediction performance on some datasets.

Appendix H Compared with model that discards high frequencies

Appendix I Compared with model that treats all frequencies equally

Appendix J Lookback Window: ModernTCN vs Us

At the 2024 International Conference on Learning Representations (ICLR), a groundbreaking approach, ModernTCN, was presented for time series forecasting. However, it’s worth mentioning that the lookback window length used in their study consistently surpasses 96. In our case, all experiments utilize a lookback window length of 96, which makes a direct comparison not feasible.

| Models |

W all frequency |

W/O low-frequency |

W/O mid-frequency |

W/O high-frequency |

||||

|---|---|---|---|---|---|---|---|---|

|

Metric |

MSE |

MAE |

MSE |

MAE |

MSE |

MAE |

MSE |

MAE |

|

ETTm1 |

0.0221 |

0.0954 |

0.0839 |

0.1827 |

0.0723 |

0.1683 |

0.0116 |

0.0583 |

|

ETTm2 |

0.0601 |

0.1544 |

0.0185 |

0.0850 |

0.0852 |

0.1468 |

0.0511 |

0.1149 |

|

ETTh1 |

0.0475 |

0.1352 |

0.1333 |

0.2351 |

0.0543 |

0.1432 |

0.0409 |

0.1193 |

|

ETTh2 |

0.5288 |

0.4734 |

0.2559 |

0.3178 |

0.1396 |

0.2217 |

0.1041 |

0.1848 |

|

Exchange |

0.0436 |

0.1218 |

0.0482 |

0.1292 |

0.0156 |

0.0745 |

0.0157 |

0.0733 |

|

Weather |

0.0011 |

0.0217 |

0.0015 |

0.0207 |

0.0041 |

0.0379 |

0.0011 |

0.0186 |

| Dataset | ETTh1 | ETTm1 | ECL | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Horizon | 96 | 192 | 336 | 720 | 96 | 192 | 336 | 720 | 96 | 192 | 336 | 720 |

| FITS | 0.372 | 0.404 | 0.427 | 0.424 | 0.303 | 0.337 | 0.366 | 0.415 | 0.134 | 0.149 | 0.165 | 0.203 |

| FreDF | 0.351 | 0.395 | 0.409 | 0.412 | 0.291 | 0.319 | 0.352 | 0.408 | 0.126 | 0.138 | 0.151 | 0.196 |

| Dataset | ECL | Weather | Exchange | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Horizon | 96 | 192 | 336 | 720 | 96 | 192 | 336 | 720 | 96 | 192 | 336 | 720 |

| FreTS | 0.039 | 0.040 | 0.046 | 0.052 | 0.032 | 0.040 | 0.046 | 0.055 | 0.037 | 0.050 | 0.062 | 0.088 |

| FreDF | 0.032 | 0.034 | 0.042 | 0.049 | 0.028 | 0.035 | 0.042 | 0.049 | 0.032 | 0.048 | 0.059 | 0.084 |