Hedging Beyond the Mean: A Distributional Reinforcement Learning Perspective for Hedging Portfolios with Structured Products

Abstract

Research in quantitative finance has demonstrated that reinforcement learning (RL) methods have delivered promising outcomes in the context of hedging financial portfolios. For example, hedging a portfolio of European options using RL achieves better distribution than the trading hedging strategies like Delta neutral and Delta-Gamma neutral Cao et al. (2020). There is great attention given to the hedging of vanilla options, however, very little is mentioned on hedging a portfolio of structured products such as Autocallable notes. Hedging structured products is much more complex and the traditional RL approaches tend to fail in this context due to the underlying complexity of these products. These are more complicated due to presence of several barriers and coupon payments, and having a longer maturity date (from years to a decade), etc. In this direction, we propose a distributional RL based method to hedge a portfolio containing an Autocallable structured note. We will demonstrate our RL hedging strategy using American and Digital options as hedging instruments. Through several empirical analysis, we will show that distributional RL provides better distribution than traditional approaches and learns a better policy depicting lower value-at-risk () and conditional value-at-risk (), showcasing the potential for enhanced risk management.

1 Introduction

In the dynamic landscape of financial markets, portfolio managers are faced with the challenge of managing risks associated with their investment holdings. These portfolio managers employ several hedging strategies to minimize the associated risks, for example, using Delta-Gamma neutral hedging strategies to create a Gamma neutral portfolio. The portfolio manager needs to not only identify suitable hedging instruments but also determine the optimal hedging ratios to effectively mitigate these risks. Moreover, the dynamic nature of financial markets demands a hedging strategy that can adapt in real-time to evolving market conditions. Traditional approaches to hedging do not provide the flexibility and adaptability required for such dynamic decision-making. However, the emergence of Reinforcement Learning (RL) presents a promising avenue for addressing these challenges.

Researchers have demonstrated that RL is an attractive alternative to traditional hedging strategies based on the performance and Profit and Loss () distribution as compared to the baseline Delta neutral and Delta-Gamma neutral strategies Cao et al. (2020); Kolm and Ritter (2019); Cao et al. (2023). When undertaking the hedging of a portfolio containing vanilla options (eg., European and American), better was achieved than these traditional hedging strategies. Researchers have greatly focused on using RL for hedging of European options Cao et al. (2023, 2020); Kolm and Ritter (2019) and Chen et al. (2023) have proposed a new RL based hedging method for Barrier options. Recently, Cui et al. (2023) proposed a method for pricing Autocallable notes and employing a Delta neutral strategy for hedging. They emphasized that hedging Autocallable notes is complex due to their intricate structure. Similarly, we investigate Autocallable structured note hedging using RL. To the best of our knowledge, we are the first in the public domain to investigate the hedging of structured products using RL. We propose a new RL based method to hedge a portfolio containing a short Autocallable note, where we achieve better distribution than traditional methods.

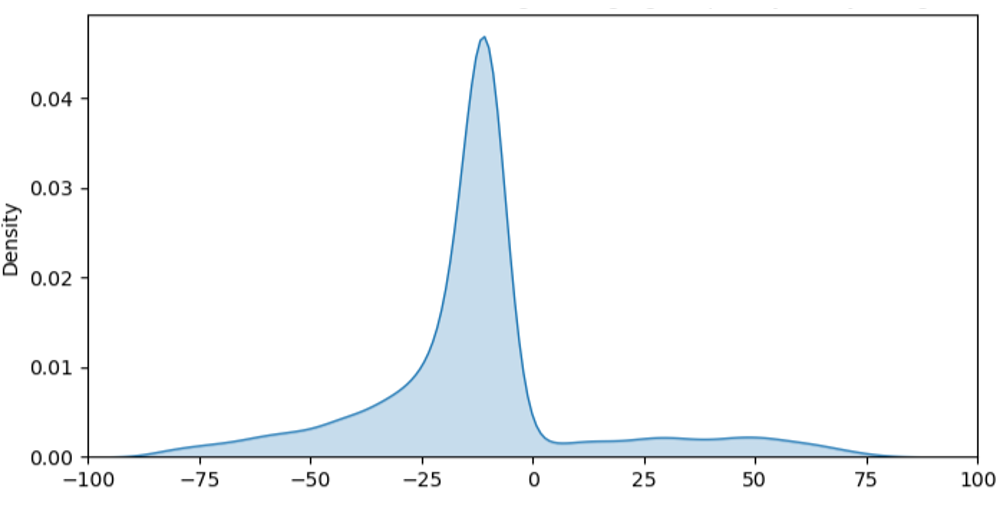

Unlike vanilla options, Autocallable notes are a structured product having an embedded exotic nature through several barriers and coupon payments. These are more complicated than vanilla options and have longer maturity (for example, years to a decade). Due to this complicated structure, hedging of Autocallable notes is a complex task. Hence, Autocallable notes, with their inherent exposure to market fluctuations, require careful risk management to safeguard against adverse movements in the portfolio Gamma. In this paper, we investigate an Autocallable note structure with the underlying as a simulated Geometric Brownian Motion (GBM) process with a SABR volatility model. We propose a hedging method using RL to hedge a trader’s portfolio having a short Autocallable note. The probability distribution of the unhedged for vanilla options is highly symmetrical and hence helps to learn an optimal policy when used as a reward function in the RL algorithm. Also, Cao et al. (2023) demonstrated that the distributional RL method achieves better for European options as compared to the classical RL methods (classical RL uses expected reward as a learning criteria). We extend their approach to American options with early exercise using the Longstaff Schwartz algorithm Schwartz (2001) which helps to address the complexities introduced by the option’s early exercise feature. In contrast, for the Autocallable note with a maturity of 7 years, the distribution is characterized by significant skewness, as illustrated in Figure 1. This skewness is due to the several coupon payments after a monthly call barrier. Therefore, hedging such a portfolio is more complicated due to the skewed reward function. In this paper, we demonstrate learning a policy for hedging under this skewed reward distribution.

In our approach, we use Distributed Distributional DDPG algorithm with Quantile Regression (QR) to learn an optimal policy for hedging. The distributional RL enables a more nuanced understanding of uncertainty and risk in the learning process. Specifically, we use a Digital/American option as hedging instruments and the trained RL agent selects an action which quantifies the amount of hedging that needs to be performed. We compare the distribution, Value at Risk (), and Conditional Value at Risk () of different hedging strategies and show that the RL algorithm not only reduces , but also makes the distribution more symmetric and retains positive returns.

Our specific contributions are the following:

-

1.

We propose a distributional RL based method to hedge a portfolio containing one short Autocallable note. We conduct a thorough analysis and introduce a novel objective function which helps to learn a generalized policy for several portfolio parameters.

-

2.

We demonstrate the intricacies associated with hedging structured products, highlighting the inadequacies of classical RL approaches, particularly in the context of the skewed unhedged distribution.

-

3.

We compare with traditional hedging strategies, including Delta neutral and Delta-Gamma neutral.

2 Related Works

Recently, Reinforcement Learning (RL) based methods have been explored extensively in finance, for example, optimal trade execution Zhang et al. (2023), credit pricing Khraishi and Okhrati (2022), market making Ganesh et al. (2019), learning exercise policies for American options Li et al. (2009), optimal hedging Cao et al. (2020); Kolm and Ritter (2019); Gao et al. (2023); Murray et al. (2022), etc.

Hedging a portfolio of exotic options is a fundamental research problem which requires sequential decision making to re-balance the portfolio at different intervals for hedging. This sequential decision making has attracted reinforcement learning based solutions which outperform traditional hedging strategies. For example, Kolm and Ritter (2019) have used Deep Q-learning and Proximal Policy Optimization (PPO) algorithms in RL to learn a policy for option replications with market frictions. They learn a single policy which works with several strike prices. Giurca and Borovkova (2021) used RL for delta hedging under various parameters such as transaction cost, option maturity, and hedging frequency. They applied transfer learning to use the policy trained on simulated data for real data. Cao et al. (2020) and Gao et al. (2023) used DDPG (Deep Deterministic Policy Gradient) RL algorithm to perform hedging under SABR and Heston volatility models respectively.

Mikkilä and Kanniainen (2023) trained an RL algorithm directly on real data for intraday options, over 6 years, on the index. Buehler et al. (2020) hedged over-the-counter derivatives using RL algorithm under market frictions like trading cost and liquidity constraints. Daluiso et al. (2023) used reinforcement learning for CVA hedging. The literature has given much attention on using RL based sequential decision making on several European Kolm and Ritter (2019); Cao et al. (2020); Halperin (2019), American Li et al. (2009), and Barrier options Chen et al. (2023). These methods have demonstrated that RL is an attractive alternative to traditional hedging strategies based on the performance and distribution. However, there is little attention on hedging very risky options such as Autocallable notes. Recently, Cui et al. (2023) proposed a method for pricing Autocallable notes and employing a Delta neutral strategy for hedging. They emphasized that the hedging is very complicated due to presence of several barriers, noting the high cost of Delta hedging near these barriers. In contrast, our approach involves training a RL policy for hedging of a 7-year maturity Autocallable note portfolio. We show the performance of an RL agent under varying transaction cost and choosing different options as hedging instruments. We demonstrate that the RL agent provides better distribution than traditional hedging strategies.

3 Problem Formulation

In this section, we will describe the simulation which generates the asset and the Autocallable note price, followed by the problem formulation using Markov Decision Process (MDP).

3.1 The Asset and Option Pricing

In actual examples, traders have extensively used the SABR volatility model Cao et al. (2020, 2023) to simulate the stock paths with volatility and to perform automated trading/hedging decisions. The SABR model, named (Stochastic Alpha, Beta, Rho), is a widely employed framework to capture different aspects of the asset volatility. In this paper, we also utilize the SABR volatility model in our simulation, assuming the underlying stock price follows a Geometric Brownian motion (GBM) with SABR volatility.

| Variable | Value |

|---|---|

| Reference Index | Solactive United States Select |

| Regional Bank Index AR | |

| Initial Price | $100 |

| Term (0% fee) | years |

| Coupon Frequency | Monthly |

| Coupon Rate | 0.95% |

| Coupon Barrier | -35.00% |

| Autocall Frequency | Semi-Annual |

| Call Barrier | 0.00% |

| Contingent Principal | |

| Protection | -35.00% |

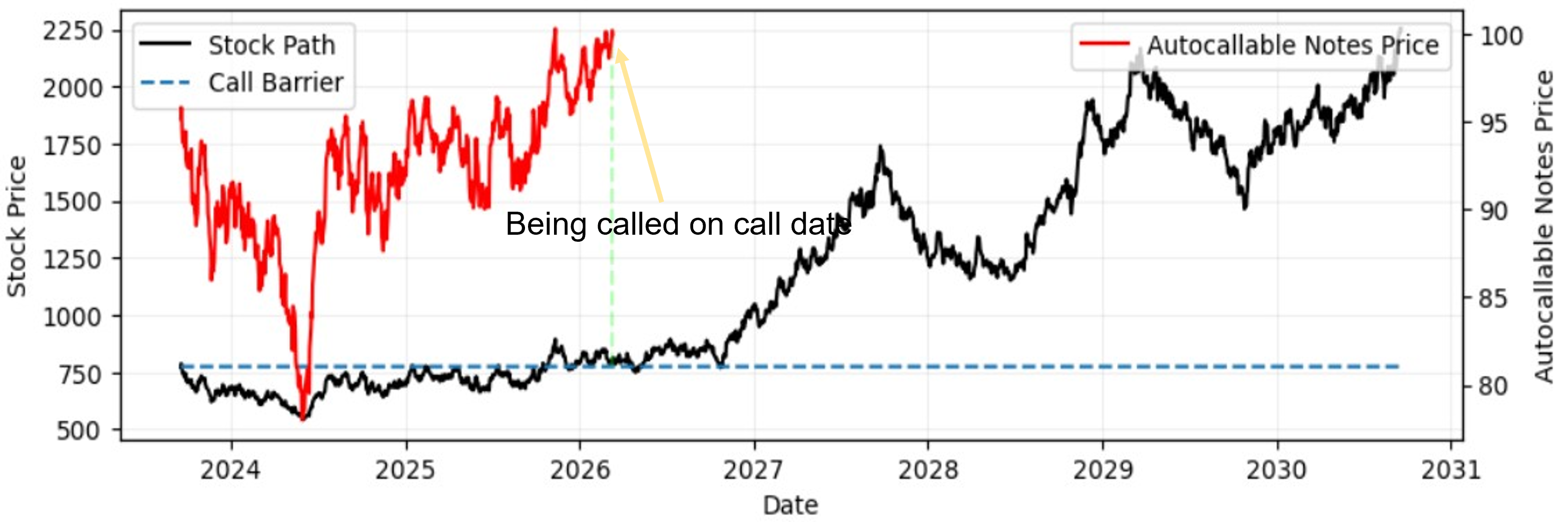

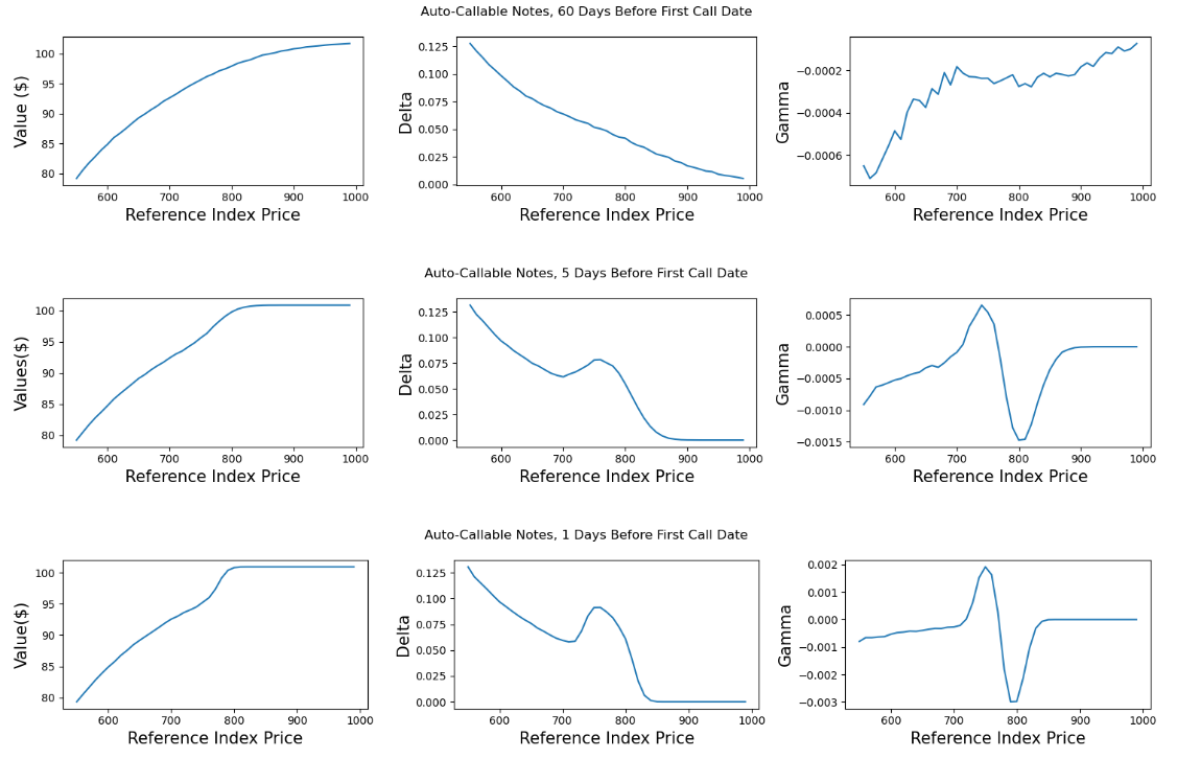

Autocallable notes are structured products that provide the investors with an opportunity to earn extra interest in terms of coupon payments if the underlying asset price closes above a specific threshold on periodic observation dates (barriers). In addition, the note will be autocalled or redeemed on an observation date if asset price return is above or equal to autocall barrier. Otherwise, it may offer contingent downside protection when the notes are held to maturity. Figure 2 shows this example when the note is auto called by the bank before the maturity of years. The note also provides principal protection at maturity if the Reference Index Return is greater than or equal to -35% on the final valuation date. Table 1 shows the note structure that we used in our experiments. We perform Monte Carlo simulation to simulate the note price. The note greeks ( and ) are generated using the finite difference method. Figure 3 shows the variation of the option value, , and the value day, days and days before the call date. The note greeks change significantly near the observation date, making it difficult to maintain a Delta/Gamma neutral portfolio (as also highlighted in Cui et al. (2023)).

3.2 Problem Formulation as an MDP

The RL Pipeline uses a MDP (Markov Decision Process) to frame the problem of our RL agent interacting with the environment to maximize our potential reward. An MDP is defined as a tuple of elements (), where is the state space, is the action space, is the state transition function, is the reward function and is the discount factor. We formulate a finite horizon discounted sum reward problem where the horizon length is the maturity of the option.

The individual elements of the MDP are described below:

State: States are the observations that the agent receives from the environment at each time step. In the current hedging pipeline, the state at time t is defined as , where is the stock price, is the portfolio gamma, and is the time to next call date.

Action: RL hedging agent’s action at any instant is the proportion of maximum hedging that can be done. For example, if the selected action is , then the RL agent takes a position equal to the of the maximum hedge allowed. This proportion is then translated into actual number of units in the hedging instrument and those units are used to simulate the portfolio for the next time step.

Reward: Reward is defined as the following:

| (1) |

where is the value of the digital option at time , is the position taken in digital option, is the transaction cost, is portfolio’s market value before time , is portfolio’s market value after time , is the transaction cost paid at time , and is the change in portfolio value from time to .

State transition function: With as the state at time , the policy selects an action . The next state is updated based on the amount of hedging done at the current instant. The updated gamma of the portfolio and the new underlying price are then used in the state variable at the next instant.

Using the above MDP, an RL environment was created which gives the next state of the environment based on the actions selected by the RL agent. At any given time, the RL agent interacts with the environment simulator by providing an action and the environment returns the next state and the reward.

4 Proposed Method

We will now describe the RL method, it’s architecture and the training procedure which learn the optimal policy.

4.1 Classical Reinforcement Learning

In a sequential decision making process, reinforcement learning is found to make optimal decisions in the stochastically changing environment. At any time instant , an RL agent takes an action , and the environment, in response, returns the next state and the reward as a feedback of that action. The process continues until the maturity or maximum time reached Sutton and Barto (1998). The goal of the RL agent is to maximize the expected future reward at any time instant. The expected future reward at time (starting from state and taking action ) is:

| (2) |

where is a horizon date and is a discount factor. is the reward received from the environment at time .

Classical RL estimates the expected value of the future reward by learning a policy . maps state to action for any time instant. If the current state is then the RL agent’s action is determined as . The policy is iteratively learned using reinforcement learning algorithms Sutton and Barto (1998), such as deep Q-learning (DQN), policy gradient, PPO, among others.

Classical RL has shown tremendous improvement in several domains but in the realm of risk management, distributional RL is found to be more effective Cao et al. (2023) to reduce the value-at-risk (). We utilize distributional RL Dabney et al. (2017); Barth-Maron et al. (2018) to hedge the skewed distribution of the Autocallable structured note.

4.2 Distributional Reinforcement Learning

We use Distributional Reinforcement Learning (DRL) in our proposal. DRL is an advanced paradigm which focuses on modeling the entire distribution of returns, rather than solely estimating the expected value. In DRL, the return is modelled as a distribution for a fixed policy . The return distribution provides more information and is more robust as compared to only the expectation. Classical RL tries to minimize the error between two expectations, expressed as ,

where is the output of the policy and is the target function. In contrast, in DRL, the objective is to minimize a distributional error, which is a distance between full distributions Bellemare et al. (2017); Dabney et al. (2017).

The optimal action is selected from the value function:

| (3) |

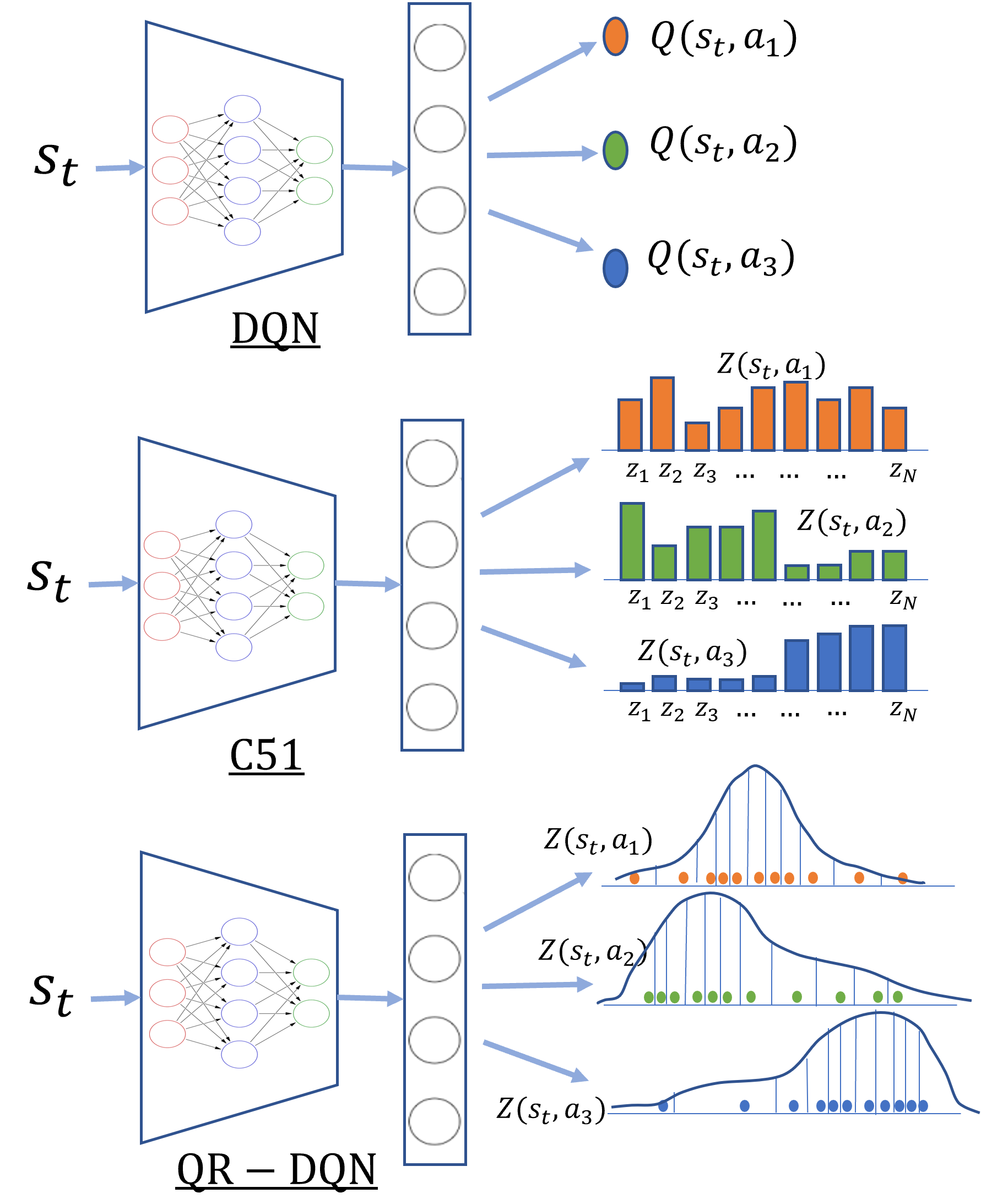

In DRL, the distribution of returns is represented as a PMF (Probability Mass Function) and generally, the probabilities are assigned to discrete values that denote the possible outcome of the RL agent. Let’s say we have a neural network that predicts this PMF by taking a state and returning a distribution for each action. Categorical distributions are commonly employed to model these distributions in some DRL algorithms like C-51 Bellemare et al. (2017) where the action distribution is modelled using a finite number of possible outcomes. In C-51, probabilities are estimated to these fixed locations. We employ Quantile Regression (QR) to learn the distribution of returns and unlike C-51, QR estimates the quantile locations where each quantile corresponds to a fixed uniform probability. That means, QR provides the flexibility to stochastically adjust the quantile locations in place of fixed locations in C-51. QR is a popular approach in DRL which is combined with several distributional RL algorithms such as in QR-DQN Dabney et al. (2017). QR-DQN uses quantile regression with traditional DQN to learn a distribution of outcomes. The goal of distributional DQN is that we want the distribution and target distribution as similar as possible, which is learned by minimizing the Wasserstein distance Dabney et al. (2017) in the neural network model. Figure 5 illustrates the different variants to incorporate a distributional architecture with classical DQN. We have used QR with D4PG.

4.2.1 Distributed Distributional DDPG (D4PG)

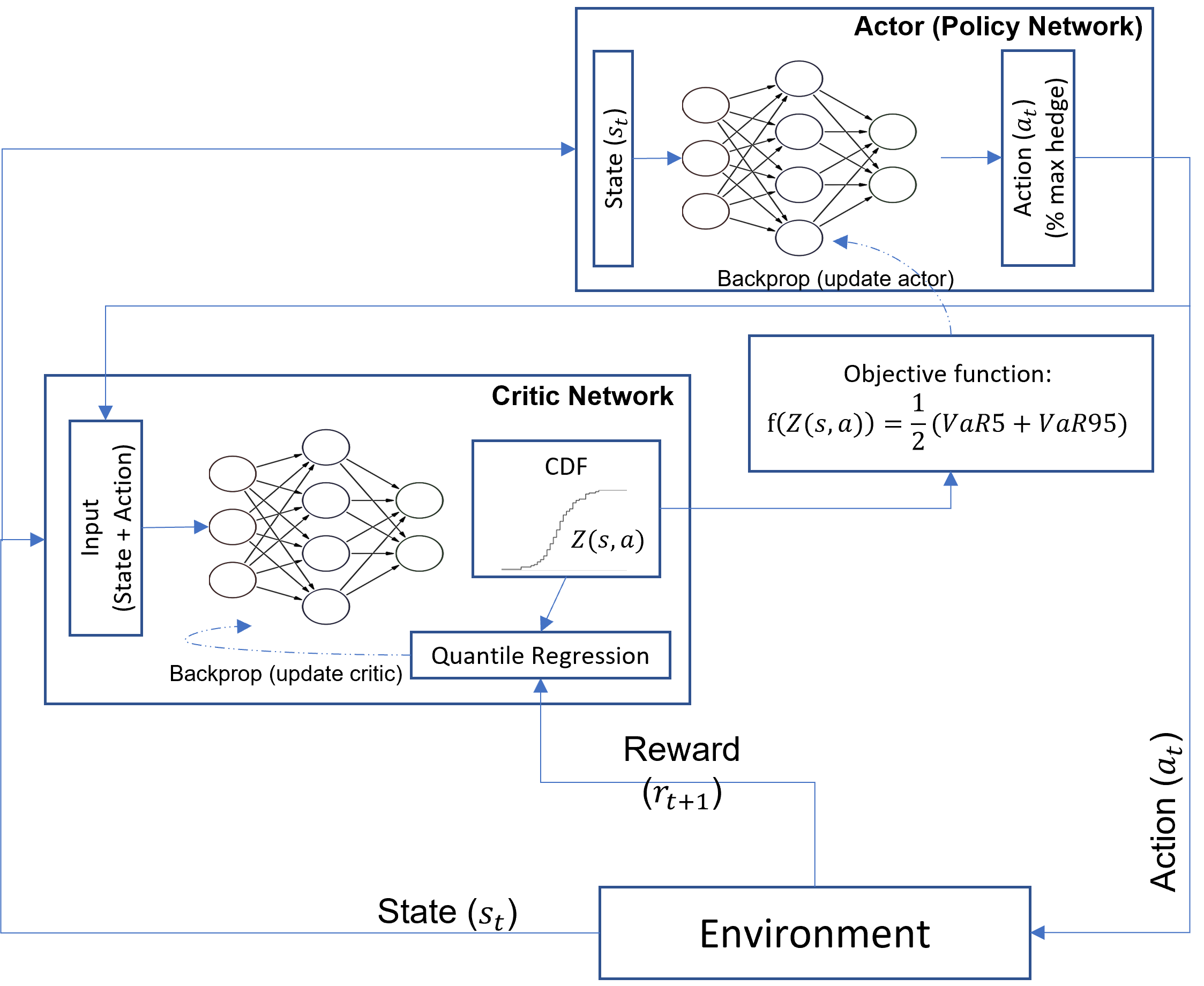

We use the Deep Deterministic Policy Gradients (DDPG) algorithm to learn the underlying distribution of returns. DDPG is an Actor-Critic based method which helps to learn a policy in continuous action space. Specifically, we use D4PG (Distributed Distributional DDPG) Barth-Maron et al. (2018) to learn the optimal policy. D4PG is a distributional RL algorithm which estimates the distribution of the return (unlike the mean in classical RL). Figure 4 shows the model architecture that we utilized in our experiments to train the D4PG algorithm. There are three components:

-

1.

The trading environment: One essential component of the architecture is the trading environment, which simulates the stock and option prices. It tracks how the portfolio evolves over time based on the agent’s hedging position, market dynamics (e.g., SABR volatility), and the arrival of the client options. At any particular time, the environment receives the hedging action and returns the next state and the reward.

-

2.

The actor neural network (also known as policy network) implements the hedging strategy. It is a neural network of size . At any instant , it takes as input a state and outputs the amount of hedging () that the agent should perform. The objective function for training the agent’s neural network is ½(5% +95% ).

-

3.

The critic neural network takes as inputs a state, , and the action from the actor’s output, . Its role is to (a) estimate the distribution of the trading loss at the end of the hedging period, , when taking action in state , and (b) compute gradients that minimize the objective function . We use a neural network of size as the critic network. We use the reward from the environment to train the agent’s critic network.

We utilize quantile regression (QR) Dabney et al. (2017) in combination with D4PG to approximate the distribution with the help of quantiles at the output of critic neural network. We use quantiles in our experiments for D4PG policy learning. Each quantile has a fixed probability but the location is stochastically adjusted during training. During agent-environment interaction in the training phase, an experience is saved in a replay buffer which is repeated at every step. To update the policy, a batch of experiences are extracted from the replay buffer and the target distribution is used to compute the error from the policy output. Wasserstein distance Dabney et al. (2017) is used as the loss function to estimate the quantiles.

5 Experiments and Results

In this section, we will describe the different empirical analysis that we performed on vanilla options and Autocallable notes, along with the experimental setup and the performance metrics.

| Strategy | Mean | Std | Mean-Std | 5% | 5% | 95% | 95% | Gamma Ratio |

|---|---|---|---|---|---|---|---|---|

| Delta Neutral (no Ex.) | 0.1 | 12.58 | -20.59 | 19.85 | -1.43 | -19.93 | -30.45 | 0.0 |

| Del-Gamma N. (no Ex.) | -11.4 | 2.61 | -15.68 | -7.63 | -11.64 | -15.92 | -17.80 | 1.0 |

| RL (no Ex.) | -5.27 | 3.17 | -10.49 | -0.37 | -5.60 | -10.65 | -12.50 | 0.31 |

| Delta Neutral (Early Ex.) | 0.37 | 11.09 | -17.87 | 17.76 | -0.98 | -16.72 | -26.16 | 0.0 |

| Del-Gamma N. (Early Ex.) | -11.76 | 2.71 | -16.22 | -7.84 | -12.01 | -16.47 | -18.40 | 1.0 |

| RL (Early Ex.) | -4.72 | 3.92 | -11.18 | 0.94 | -5.08 | -11.76 | -14.40 | 0.30 |

5.1 Experimental Setup

We are hedging a trader’s portfolio which contains risky options - the trader hedges the portfolio by adding other instruments to a hedging portfolio at every hedging instant. In other words, the trader rebalances the portfolio at every time interval for hedging. The hedging action involves selecting the percentage of to hedge at any rebalancing instant. For example, in the experiments for Autocallable note hedging, the trader’s portfolio contains one short Autocallable note with years of maturity. The trader also keeps a hedging portfolio and at every hedging instant ( month), the trader adds an at-the-money American call/put option or out-of-money Digital option to the hedging portfolio for hedging. A hedging strategy decides how much hedging needs to be performed based on the different portfolio Greeks such as , , etc. tells how much the option’s price will change for a one-point change in the underlying asset’s price, while tells how much the will change for a one-point change in the underlying asset’s price. Trader’s use these Greeks to manage risk and make informed decisions. For example, a Delta neutral strategies hedges the entire of the portfolio by creating a position with a value of zero, or very close to zero. We propose a RL based hedging strategy which learns to decide the percentage of the that needs to be hedged. We compare the hedging performance of our RL agent with traditional hedging strategies, Delta neutral and Delta-Gamma neutral.

Our RL agent uses the D4PG (Distributed Distributional DDPG) algorithm with quantile regression to learn an optimal policy. The RL agent selects an optimal action using the learned policy from interval . The RL agent is trained for episodes (where one episode is one stock path till note maturity or auto-call). To compare the performance for all methods, we generate an additional episodes on which KPI metrics are reported. The prices for the underlying asset are generated using Geometric Brownian motion (GBM) with a SABR volatility model. We evaluate the hedging performance using percentile of the value-at-risk () and conditional value-at-risk () distribution.

| Strategy | Mean | Std | Mean-Std | 5% | 5% | 95% | 95% | Gamma Ratio |

|---|---|---|---|---|---|---|---|---|

| Delta Neutral | -12.1 | 10.41 | -29.23 | -2.61 | -12.66 | -34.06 | -42.93 | 0.0 |

| Delta-Gamma Neutral | -10.15 | 8.99 | -24.94 | -1.21 | -10.69 | -28.12 | -36.13 | 1.0 |

| RL [Digital] | -3.99 | 13.08 | -25.51 | 12.6 | -5.33 | -27.21 | -39.18 | 3.46 |

| RL [Am. Put & Call] | -3.84 | 13.46 | -25.97 | 20.82 | -5.92 | -22.61 | -32.00 | 2.58 |

Implementation: We implemented the D4PG algorithm using the ACME library from Deepmind Hoffman et al. (2020) with Tensorflow backend. We utilized a server with -GBs of RAM with -CPU cores for training. To train the model, we employ a deep neural network with three hidden layers with Adam optimizer for both actor and critic networks. The subsequent sections present the performance on the optimal parameters.

5.2 RL Agent for Hedging

We now describe the performance of the RL agent trained with a trader’s portfolio containing client options. We first describe the performance of our RL agent on vanilla options where we achieve higher than baseline hedging strategies with simple training coupled with early exercise. We then describe the challenges in hedging a portfolio containing a structured product (Autocallable note) which contains several barriers and coupon payments. At the end, we show the performance comparison of the RL agent with traditional hedging strategies.

Hedging vanilla Options: In this experiment, we hedge a trader’s portfolio containing American options where the portfolio is evolving regularly with time. The options are assumed to arrive as a Poisson process with . Each arrival option could be a call/put with long/short position with equal probability with a maturity of month. For this experiment, we use the portfolio structure as used by Cao et al. (2023) to hedge a portfolio containing European options. Similar to European option, the American option also has a maturity of month but offers an extra feature to allow early exercise of the option before the maturity date. The method proposed by Cao et al. (2023) doesn’t support early exercise and we employ the Longstaff Schwartz algorithm Schwartz (2001) to decide when to early exercise any American option in the portfolio. For hedging, American call and put options are used as hedging instruments. The hedging strategy decides how much hedging needs to be performed in terms of value of the portfolio. The delta-neutral strategy hedges gamma (hedges only the exposure) and delta-gamma neutral strategy hedges gamma. The RL agent selects an action from .

To early exercise the American option, we train the Longstaff Schwartz based regression method to predict the continuation value of the option given the stock path till date. The continuation value is the value of the option if it is not exercised at the current instant, while the exercise value is the payoff received when the option is executed at the current instant. For example. for a put option, the payoff , where is the strike price and is the stock price at time . We train the regression based algorithm on stock paths with several strike prices. At each instant during evaluation, the algorithm steps backward and approximates the continuation value of the stock. At any instant, if the current exercise value is greater than the continuation value, then the option is exercised, else continued. This early exercise method is integrated with the RL method which uses D4PG with QR. Table 2 shows the performance of different hedging strategies on the portfolio containing American options (without and with early exercise). Figure 6 shows the distribution of several hedging strategies, and shows significant improvement using our RL approach with early exercise of the American options (please note in Table 2). In the figure, the distribution plot for the Delta neutral agent is quite wide but narrower for the Delta-Gamma neutral agent. Whereas, the distribution of the RL agent is a little wider than that with Delta-Gamma, and it is more on the positive side of the graph. The trend of the distribution for the RL agent on American options is that it achieves better results. The values in the table and the figure are on the evaluation episodes.

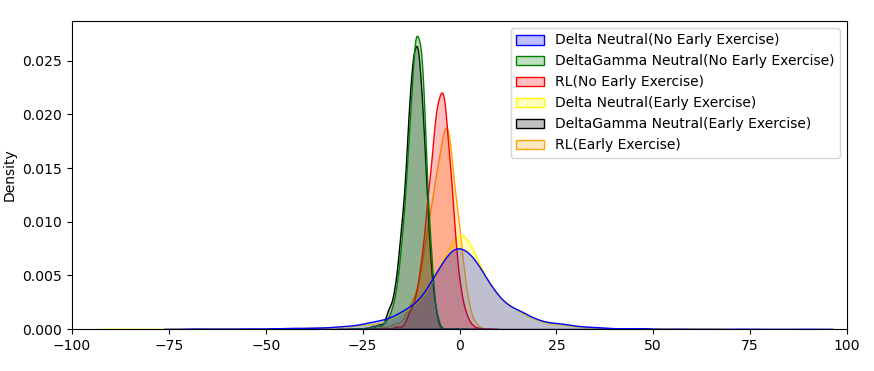

Hedging Autocallable structured note: In this experiment, we hedge a trader’s portfolio containing one short Autocallable note with maturity of years. We run two experiments, one with a digital option as the hedging instrument and another using American call/put options. We use digital option as the hedging instrument because a digital option also contains a barrier similar to Autocallable notes but for a shorter maturity. For this experiment, the state () at any time instant contains the stock price (), portfolio gamma () and the days to the next call date (). The trader rebalances the portfolio every month by adding one digital/American option in the hedging portfolio. We choose month as the rebalancing interval because of the longer maturity time of years for the Autocallable note. The hedging agent strategy decides how much hedging needs to be performed in terms of value of the portfolio. The unhedged distribution for the Autocallable note is skewed as shown in figure 1. Unlike the vanilla option, the RL method that we applied for the vanilla options doesn’t scale to this portfolio. We observed that the RL agent was not able to hedge the positive tail of the unhedged distribution. As a result, the RL agent selects only one action () irrespective of the state- i.e., it behaves like the Delta-Gamma neutral agent.

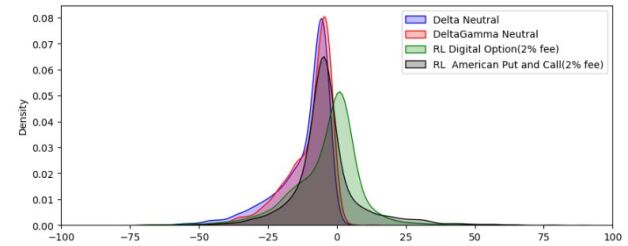

Further investigation of this behavior during training, showed that the as objective function makes the RL agent behaves similar to the delta-gamma agent. To add the positive in the objective function, we explored several variants and found experimentally that is the objective function that assists to learn the optimal policy. Figure 7 shows the comparison of the two objective functions and (). We observed that the Autocallable barriers and regular coupon payments disturbed the reward function, leading to an inaccurate objective function at the critic. As a result, an optimal policy was not learned. The newly modified objective function generated the best payoff and the policy selected diverse actions. Figure 8 shows the distribution of our RL agent with the new objective function which learns the best distribution. The RL algorithm not only reduced and increased but also made the distribution more symmetric and shifted the distribution toward the more positive side. Table 3 shows the , , mean and standard deviation of the over evaluation episodes for the traditional strategies, namely delta-neutral, delta-gamma neutral, and our proposed RL method.

6 Conclusion

We proposed a reinforcement learning based method to hedge a portfolio of structured products such as Autocallable notes. The results showed that it is much more complex than the use of the traditional RL approach, which tends to fail. In this direction, we proposed a distributional RL based method to hedge a portfolio containing Autocallable structured notes.

References

- Barth-Maron et al. [2018] Gabriel Barth-Maron, Matthew W. Hoffman, David Budden, Will Dabney, Dan Horgan, Dhruva TB, Alistair Muldal, Nicolas Heess, and Timothy Lillicrap. Distributed distributional deterministic policy gradients, 2018.

- Bellemare et al. [2017] Marc G. Bellemare, Will Dabney, and Rémi Munos. A distributional perspective on reinforcement learning, 2017.

- Buehler et al. [2020] Hans Buehler, Lukas Gonon, Josef Teichmann, Ben Wood, Baranidharan Mohan, and Jonathan Kochems. Deep hedging: Hedging derivatives under generic market frictions using reinforcement learning. Available at SSRN, 2020.

- Cao et al. [2020] Jay Cao, Jacky Chen, John Hull, and Zissis Poulos. Deep hedging of derivatives using reinforcement learning. The Journal of Financial Data Science, 3(1):10–27, December 2020.

- Cao et al. [2023] Jay Cao, Jacky Chen, Soroush Farghadani, John Hull, Zissis Poulos, Zeyu Wang, and Jun Yuan. Gamma and vega hedging using deep distributional reinforcement learning, 2023.

- Chen et al. [2023] Jacky Chen, Yu Fu, John C Hull, Zissis Poulos, Zeyu Wang, and Jun Yuan. Hedging barrier options using reinforcement learning. 2023.

- Cui et al. [2023] Yeda Cui, Lingfei Li, and Gongqiu Zhang. Pricing and hedging autocallable products by markov chain approximation. Available at SSRN 4557397, 2023.

- Dabney et al. [2017] Will Dabney, Mark Rowland, Marc G. Bellemare, and Rémi Munos. Distributional reinforcement learning with quantile regression, 2017.

- Daluiso et al. [2023] Roberto Daluiso, Marco Pinciroli, Michele Trapletti, and Edoardo Vittori. Cva hedging with reinforcement learning. In Proceedings of the Fourth ACM International Conference on AI in Finance, ICAIF ’23, page 261–269, New York, NY, USA, 2023. Association for Computing Machinery.

- Ganesh et al. [2019] Sumitra Ganesh, Nelson Vadori, Mengda Xu, Hua Zheng, Prashant Reddy, and Manuela Veloso. Reinforcement learning for market making in a multi-agent dealer market, 2019.

- Gao et al. [2023] Kang Gao, Stephen Weston, Perukrishnen Vytelingum, Namid Stillman, Wayne Luk, and Ce Guo. Deeper hedging: A new agent-based model for effective deep hedging. In 4th ACM International Conference on AI in Finance, ICAIF ’23. ACM, November 2023.

- Giurca and Borovkova [2021] Alexandru Giurca and Svetlana Borovkova. Delta hedging of derivatives using deep reinforcement learning. Available at SSRN 3847272, 2021.

- Halperin [2019] Igor Halperin. Qlbs: Q-learner in the black-scholes(-merton) worlds, 2019.

- Hoffman et al. [2020] Matthew W. Hoffman, Bobak Shahriari, John Aslanides, Gabriel Barth-Maron, Nikola Momchev, Danila Sinopalnikov, Piotr Stańczyk, Sabela Ramos, Anton Raichuk, Damien Vincent, Léonard Hussenot, Robert Dadashi, Gabriel Dulac-Arnold, Manu Orsini, Alexis Jacq, Johan Ferret, Nino Vieillard, Seyed Kamyar Seyed Ghasemipour, Sertan Girgin, Olivier Pietquin, Feryal Behbahani, Tamara Norman, Abbas Abdolmaleki, Albin Cassirer, Fan Yang, Kate Baumli, Sarah Henderson, Abe Friesen, Ruba Haroun, Alex Novikov, Sergio Gómez Colmenarejo, Serkan Cabi, Caglar Gulcehre, Tom Le Paine, Srivatsan Srinivasan, Andrew Cowie, Ziyu Wang, Bilal Piot, and Nando de Freitas. Acme: A research framework for distributed reinforcement learning. arXiv preprint arXiv:2006.00979, 2020.

- Khraishi and Okhrati [2022] Raad Khraishi and Ramin Okhrati. Offline deep reinforcement learning for dynamic pricing of consumer credit, 2022.

- Kolm and Ritter [2019] Petter N Kolm and Gordon Ritter. Dynamic replication and hedging: A reinforcement learning approach. The Journal of Financial Data Science, 1(1):159–171, 2019.

- Li et al. [2009] Yuxi Li, Csaba Szepesvari, and Dale Schuurmans. Learning exercise policies for american options. In David van Dyk and Max Welling, editors, Proceedings of the Twelth International Conference on Artificial Intelligence and Statistics, volume 5 of Proceedings of Machine Learning Research, pages 352–359, Hilton Clearwater Beach Resort, Clearwater Beach, Florida USA, 16–18 Apr 2009. PMLR.

- Mikkilä and Kanniainen [2023] Oskari Mikkilä and Juho Kanniainen. Empirical deep hedging. Quantitative Finance, 23(1):111–122, 2023.

- Murray et al. [2022] Phillip Murray, Ben Wood, Hans Buehler, Magnus Wiese, and Mikko S. Pakkanen. Deep hedging: Continuous reinforcement learning for hedging of general portfolios across multiple risk aversions, 2022.

- Schwartz [2001] Francis A Longstaff Eduardo S Schwartz. Valuing american options by simulation: A simple least—squares. 2001.

- Sutton and Barto [1998] Richard S. Sutton and Andrew G. Barto. Introduction to Reinforcement Learning. MIT Press, Cambridge, MA, USA, 1st edition, 1998.

- Zhang et al. [2023] Chuheng Zhang, Yitong Duan, Xiaoyu Chen, Jianyu Chen, Jian Li, and Li Zhao. Towards generalizable reinforcement learning for trade execution, 2023.