dateJuly2024

The Pass-through of Retail Crime††thanks: We thank Thorsten Schank, Thomas Otter, Guido Friebel, Markus Reisinger, Michael Pollmann, and seminar participants at Tilburg University, NASMES, CAED, EMAC and Marketing Science for helpful comments. We are grateful to Tim Haggerty, Chuck Groom, Erik Skaar, and Ian Eisenberg for invaluable insights on the cannabis industry and the traceability data.

Abstract

This paper shows that retailers increase prices in response to organized retail crime, revealing a substantial aspect of retail crime’s social costs. We match detailed information on store-level crimes to administrative scanner data from the universe of transactions for cannabis retailers in Washington state. Exploiting quasi-experimental variation from the timing of store-level robberies and burglaries, we find that crimes cause a 1.8% increase in retail prices at victimized stores. Nearby rivals of victimized stores increase prices by a similar amount with a two-month lag. Retailers’ price responses are not driven by demand effects, increased wholesale costs, or strategic price responses. Instead, they are consistent with precautionary security expenditures. We find the largest pass-through rates for independent stores and in less concentrated markets. We estimate that crime imposes a 1% “hidden” unit tax on affected stores, implying an annual negative welfare effect of approximately $30.6 million, with consumers bearing two-thirds of this burden.

Keywords: Retail crime, pass-through, retail pricing, market power, tax incidence

JEL Codes: L11, L81, H22, H23, K49

1 Introduction

Retail crime has surged to the forefront of public discourse in the United States, fueled by an apparent rise in organized retail crime.111In contrast to petty theft or shoplifting, organized retail crime involves large-scale theft of merchandise or cash with the intent to resell, often as part of a criminal enterprise. In line with this definition, we limit our analysis to robberies and burglaries in our examination of retail crime. Throughout the paper, we use the terms ”organized retail crime” and ”retail crime” interchangeably. More details on organized retail crime can be found in Section 2.2. Retail crime imposes direct and indirect costs on businesses, individuals, and society. A comprehensive assessment of these costs is central for determining the optimal level of public crime prevention (Stigler,, 1970; Owens and Ba,, 2021). One factor often overlooked when considering the social costs of retail crime is its impact on market outcomes. In particular, crime-induced price changes, i.e., the pass-through of retail crime, have critical distributional implications and can introduce an excess burden by distorting firms’ and consumers’ decisions. Yet, evidence of a causal link between retail crime and market prices is nonexistent and the literature lacks a thorough analysis of the associated welfare effects.

We investigate the impact of organized retail crime on prices and the resulting welfare implications using the Washington state retail cannabis industry as a natural laboratory.222The US cannabis industry generates over $25 billion in annual revenue. More than half of Americans live in states with legal retail cannabis markets, and about one-third of adults regularly consume cannabis in those states (Chapekis and Shah,, 2024; Statista,, 2024). We choose this context for three main reasons. First, similar to other retail sectors, retail crime is a common occurrence at cannabis stores and has garnered the attention of policymakers (Washington State Office of the Attorney General,, 2022). Second, rich scanner data covering the universe of upstream and downstream transactions for every cannabis store can be matched with store-level information on retail crime incidents, permitting a clean identification of the effects of retail crime on store-level outcomes and their underlying mechanisms. The detailed data further enables us to conduct a comprehensive welfare analysis using a sufficient statistics approach, drawing on insights from the tax incidence literature (Weyl and Fabinger,, 2013). Third, online sales and interstate transactions are not permitted in the Washington state cannabis industry, implying that cannabis retailers compete locally. This segregation allows us to investigate spillover effects of retail crime from victimized stores to competitors and examine the impact on aggregate market outcomes.

Exploiting quasi-experimental variation from the timing of store-level crime incidents, we use a difference-in-differences framework and compare store-level outcomes at victimized stores to outcomes in unaffected local markets.333In contrast to other studies exploiting spatial treatment variation, a major advantage in our setting is that we observe the universe of vertical transactions between producers and retailers. This allows us to estimate retailers’ spatial sensitivity to competitors’ unit cost shocks and identify a valid control group that is not contaminated by strategic price competition (Hollenbeck and Uetake,, 2021; Muehlegger and Sweeney,, 2022). We find that victimized stores increase prices by 1.8 percent after a crime incident. The price increases remain persistent and stable nine months after an incident. In contrast, quantities sold at victimized stores return to pre-crime levels after a short but insignificant dip in the month after the crime. Similarly, we find no effect of crime incidents on wholesale costs at victimized stores. Since idiosyncratic fixed cost shocks such as property loss do not influence marginal costs, our combined results suggest that the rise in prices is consistent with increased expenditures on security or crime insurance. This is corroborated by evidence from a multitude of industry surveys, news articles and reports documenting a marked increase in crime prevention spending by retailers across diverse retail markets (U.S. Chamber of Commerce,, 2023; Dunham,, 2021; National Retail Federation,, 2022; U.S. Department of Homeland Security,, 2022).

We also investigate spillover effects from victimized stores to nearby rival stores, e.g. due to demand substitution on the part of consumers, strategic price responses, or an own-cost shock. We find that rivals of victimized stores—i.e. stores within a 5-mile radius of a victimized store—increase prices by 1.6 percent. However, in contrast to victimized stores, this price increase materializes with a two-month lag. Again, we find no effects on wholesale costs or quantities sold. The latter finding rules out demand substitution as a mechanism driving the price response at rival stores. To assess whether rivals’ price response reflects strategic complementarity in prices, we leverage the fact that—in addition to retail transactions—we observe the universe of vertical transactions between producers and retailers. This allows us to estimate the extent to which changes in stores’ own wholesale costs and the costs of their competitors are passed through to retail prices. Our results indicate that stores primarily adjust prices in response to their own costs rather than rivals’ costs. We find a marginal cost pass-through rate of 1.65, i.e. a $1 increase in a product’s wholesale price corresponds to a $1.65 increase in its retail price. The influence of rivals’ cost changes is statistically significant but economically negligible at $0.02 (from a $1 increase in wholesale price). Thus, rivals’ substantial price hikes in the wake of nearby retail crimes cannot be attributed to strategic complementarity in prices. Instead, rivals’ price effects appear consistent with an own-cost shock, e.g. due to precautionary security expenditures or higher crime insurance premiums.

The richness of our data further allows us to identify heterogeneity in price effects conditional on store and local market characteristics. First, we find that crime pass-through is higher at independent stores as compared to chains. Our findings suggest that retail crime pass-through is particularly relevant for mom-and-pop shops, while owners of multiple stores can offset costs across locations, mitigating retail crime’s impact on prices. Second, we find the largest price increases for stores operating in markets with comparably low market concentrations. This finding aligns with the idea that pass-through rates and market power are inversely related, as increased competition makes prices more sensitive to marginal costs—a theoretical prediction that relies on the curvature of firms’ cost functions (Ritz,, 2024) and on whether pass-through rates exceed unity (Miller et al.,, 2017).

Our main specification builds on the stacked difference-in-differences (DiD) estimator introduced by Cengiz et al., (2019) with treatment timing defined as the store-specific month of a crime incident. Similar to other DiD frameworks, stacked DiD estimates the causal treatment effect under the assumption of parallel trends and no anticipation. To account for biases from heterogeneous treatment effects and timing (De Chaisemartin and d’Haultfoeuille,, 2020; Goodman-Bacon,, 2021), stacked DiD creates crime incident-specific sub-experiments comparing treated stores to “clean” control stores, i.e., never-treated or not-yet-treated stores for a particular crime incident. We choose stacked DiD over related estimators (e.g., Callaway et al.,, 2024; Borusyak et al.,, 2024) because the rules for defining clean controls can be readily extended to geographic criteria. In addition to the timing-based criteria, we require incident-specific clean control stores to be located between 30 to 50 miles from the respective victimized store (which we refer to as unaffected local markets). These conditions ensure a sizeable control group that is comparable to our treatment group while at the same time minimizing confounding effects from spillovers to nearby stores (Muehlegger and Sweeney,, 2022).444We conduct several robustness checks that show that our main findings are not sensitive to our choice of estimator or the definition of unaffected local markets. Our paper is one of the first to extend the stacked DiD framework to spatial criteria, contributing to the advancing literature on this methodology (Cengiz et al.,, 2019; Deshpande and Li,, 2019; Butters et al.,, 2022; Wing et al.,, 2024).555Using a stacked DiD estimator, Deshpande and Li, (2019) investigate spillover effects of social security field office closings to nearby offices. However, they use timing-based clean control inclusion criteria that do not incorporate geospatial distance. Our estimator combines both timing and geospatial distance in defining clean controls. Butters et al., (2022) investigate spillover effects of state excise taxes on chain stores in nearby states. Their approach is similar to ours in that they exclude chain stores whose parent company is affected by a tax hike in another state within the event window.

To derive the welfare implications of retail crime pass-through, we draw from the imperfect competition model by Weyl and Fabinger, (2013) which nests standard imperfect competition models, as well as the monopoly and perfect competition cases. We postulate that retail crime incidents constitute a positive marginal cost shock to affected stores that can be understood as a hidden crime tax.666The idea of treating crime as a hidden tax was initially proposed by Jackson and Tran, (2020). Crime usually also constitutes an idiosyncratic (fixed) cost shock due to stolen or damaged property. However, as a fixed cost shock does not affect (long-run) pricing decisions of firms according to standard theory, we abstract from fixed cost shocks in this paper. The implications of standard tax theory carry over to our case: i) the burden of the hidden crime tax falls disproportionately on the more inelastic side of the market; ii) under imperfect competition, there is a deadweight loss that increases with firms’ market power; iii) the pass-through rate serves as a sufficient statistic for tax incidence and the deadweight loss.

Next, we employ the framework from Weyl and Fabinger, (2013)—together with our marginal cost and retail crime pass-through estimates—to quantify the welfare effects of the crime-related price increases in the Washington state cannabis industry. At the average unit price, our estimated retail crime pass-through rate implies a $0.45 unit price increase from crime in affected markets. This unit price increase corresponds to a hidden unit tax of approximately $0.27, or about 1% of the average unit price. Given the average annual quantity sold in affected markets, our results imply an annual decrease in consumer surplus of about $20.5 million due to crime-induced price increases. In addition, we estimate a negative effect on producers of around $10.1 million, implying an incidence of the hidden crime tax on consumers of around 67% and a total social cost of retail-crime pass-through of $30.6 million. Even if we assume that the entire fictional tax revenue (the implied increase in total security expenditures at affected stores) stays within the Washington economy, our findings indicate a deadweight loss of more than $18 million from retail crime pass-through.

The implications of our findings extend well beyond the cannabis industry. Organized retail crime is common in many retail sectors and firms invest heavily in strategies to prevent retail crime (see Section 2.2). Numerous industry surveys suggest that retailers across different industries pass these costs through to consumers U.S. Department of Homeland Security, (2022); Dunham, (2021). This conjecture is supported by the findings of a study by Jackson and Tran, (2020), which reveals that increased felony larceny thresholds are associated with higher prices for automobiles and computers. The generalizability of our results is reinforced by the similarities between the retail cannabis industry and conventional retail settings in terms of cost structures and demand elasticities (Hollenbeck and Uetake,, 2021). The absence of a prevalent black market competing with legal cannabis sales further supports the broad applicability of our findings (Hollenbeck and Uetake,, 2021). A naive extrapolation of our social cost estimate, using relative sales shares and assuming retail crime impacts other retail industries similarly, suggests that the U.S.-wide social costs of retail crime pass-through exceed $120 billion. While effects are likely to be less pronounced in other sectors due to different market structures and retail crime incidence, the estimate highlights that the social costs of retail crime are significantly underappreciated when not accounting for pass-through effects.

We contribute to two broad strands of the literature. First, our study contributes to the extensive literature on the economic impact of crime and the related policy discussion on the optimal level of crime prevention. Much of this literature studies the trade off between the social costs of crime and the benefits of crime prevention (Stigler,, 1970; Owens and Ba,, 2021).777Following the seminal work by Becker, (1968), have historically focused on the trade-offs influencing the decision to engage in criminal activity. These considerations encompass aspects like the price elasticity of goods that criminals might target for theft, as explored in Draca et al., (2019). We are the first to document a causal relationship between retail crime and market prices. Additionally, we provide a thorough discussion of the associated welfare implications highlighting an often neglected aspect of retail crime’s social costs.

Previous research has linked property and violent crimes to a range of economic outcomes: increased property prices (Lynch and Rasmussen,, 2001; Gibbons,, 2004; Linden and Rockoff,, 2008), economic growth (Fenizia and Saggio,, 2024), urban depopulation (Cullen and Levitt,, 1999), elevated savings levels (De Mello and Zilberman,, 2008), changes in working time (Hamermesh,, 1999), land use and crop yields (Dyer,, 2023), and even increased physical activity (Janke et al.,, 2016). More specific to our focus, several studies examine crime’s impact on consumer behavior and business dynamics. Mejia and Restrepo, (2016) highlight how crime reduces the consumption of conspicuous goods. Fe and Sanfelice, (2022) observe a crime-related decline in local food and entertainment consumption, while others identify a connection between crime and overall business activity and entrepreneurial decisions (Greenbaum and Tita,, 2004; Hipp et al.,, 2019; Rosenthal and Ross,, 2010). Using increased security expenditures as an instrument for violent crime in Columbia, Rozo, (2018) shows that increased violence leads to lower output and prices, along with a rise in firms exiting the market. Stolkin, (2023) links organized drug trafficking to higher consumer prices in Mexico, and Jackson and Tran, (2020) finds larceny thefts are positively associated with prices for computers and cars. In contrast to existing studies, we focus on organized retail crime in the U.S. and identify underlying factors behind the rise in retail prices.

Second, we contribute to the extensive literature studying the pass-through of different cost shocks, the underlying drivers, and their implications (Weyl and Fabinger,, 2013; Miravete et al.,, 2018; Miller et al.,, 2017). In our study, we examine a distinctive type of cost shock—retail crime—where costs are endogenous to firms updating their beliefs about the probability of future crime risks and outcomes. Our analysis shows that rivals’ price adjustments seem less a strategic response and more a reaction to their own increased marginal costs (e.g. due to precautionary security expenditures or increased business crime insurance premia). Such spillovers are not only relevant in the context of retail crime but also in other settings where firms compete in local markets and learning from competitors is central to firms’ costs. In these cases, price changes driven by knowledge spillovers could be mistakenly interpreted as strategic pricing.

Our heterogeneity analyses also contribute to the discussion on asymmetric strategies and market outcomes between chain and independent stores (e.g. Jia,, 2008; Hollenbeck,, 2017; Hollenbeck and Giroldo,, 2022; Janssen and Zhang,, 2023; Klopack,, 2024). We find that the pass-through of retail crime is considerably smaller for chain stores, aligning with studies that show a lack of within-chain price adjustments to local conditions (Hitsch et al.,, 2021; DellaVigna and Gentzkow,, 2019). From a welfare perspective, this pattern suggests a potential benefit to increasing the presence of chain stores within an industry. Additionally, our finding of higher pass-through rates in less concentrated markets adds to the ongoing discussion about the relationship between market competition and pass-through rates (Miller et al.,, 2017; Cabral et al.,, 2018; Genakos and Pagliero,, 2022; Ritz,, 2024).

This paper proceeds as follows. Section 2 describes the institutional context of our study, including retail crime in the United States and the retail cannabis industry. Section 3 details our data and Section 4 describes our main empirical strategy. Section 5 presents our main findings. Section 6 discusses potential endogeneity concerns and robustness checks. Section 7 outlines our policy analysis and derives the welfare implications. Section 8 concludes.

2 Institutional Background

2.1 The cannabis industry in Washington state

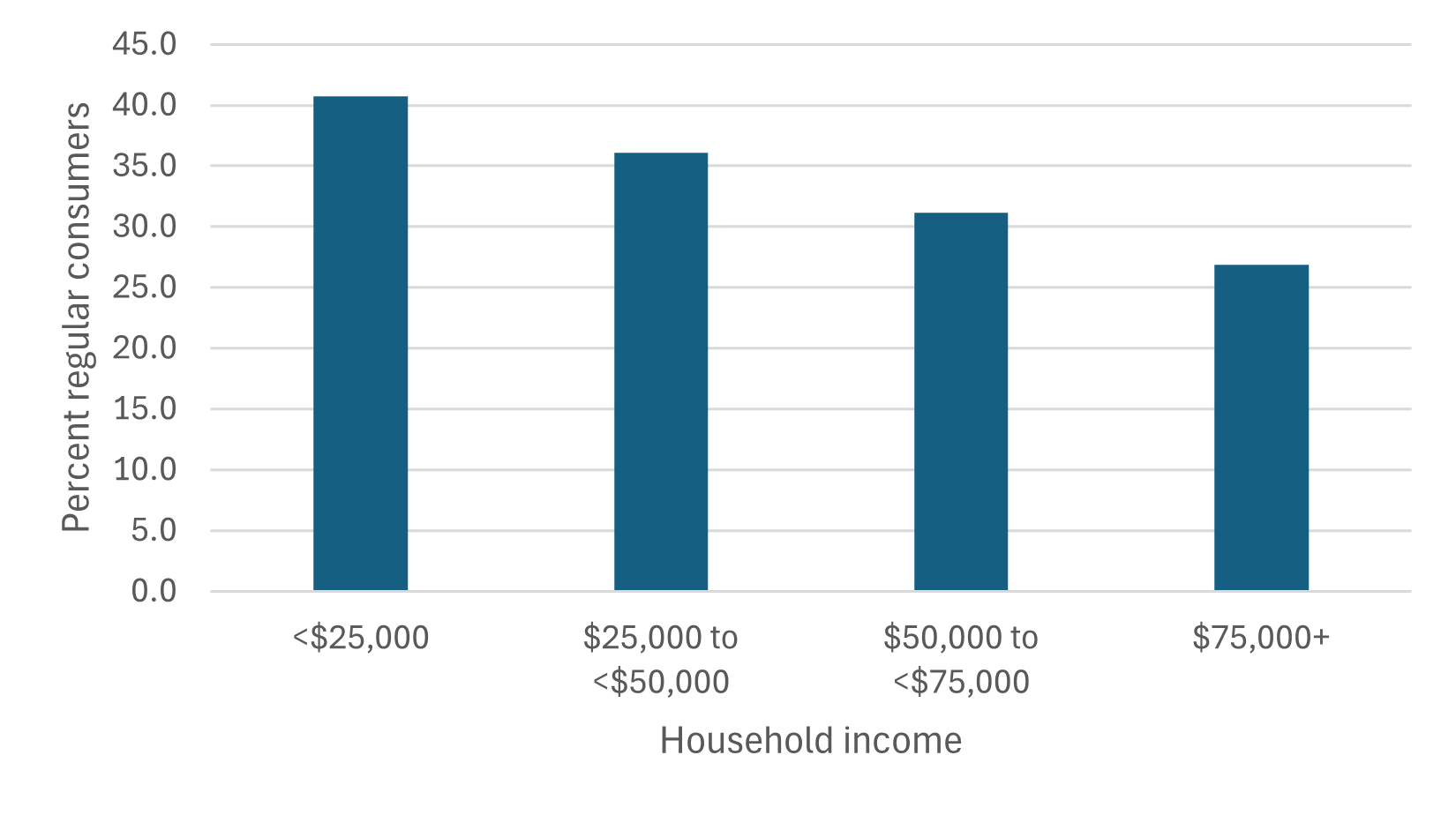

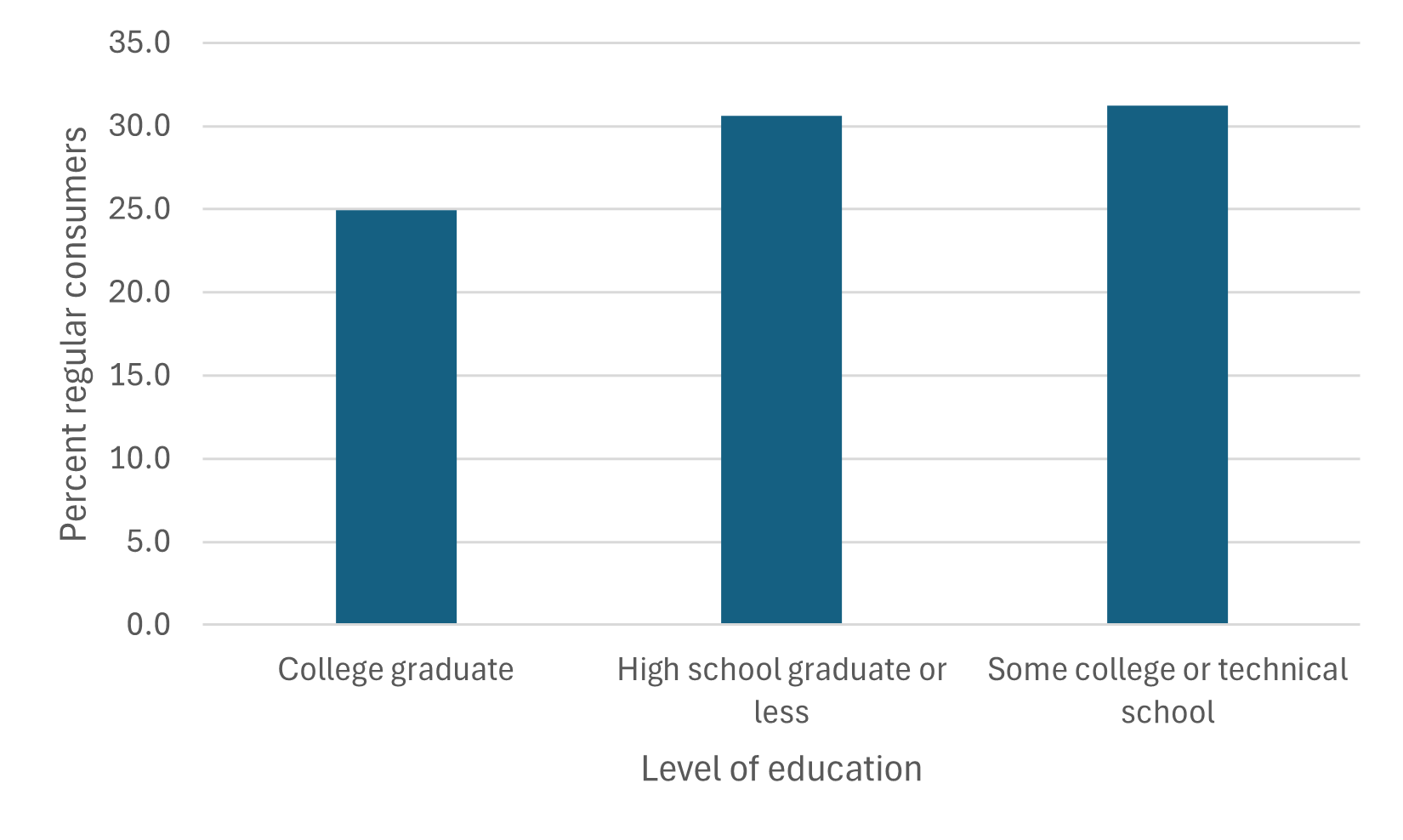

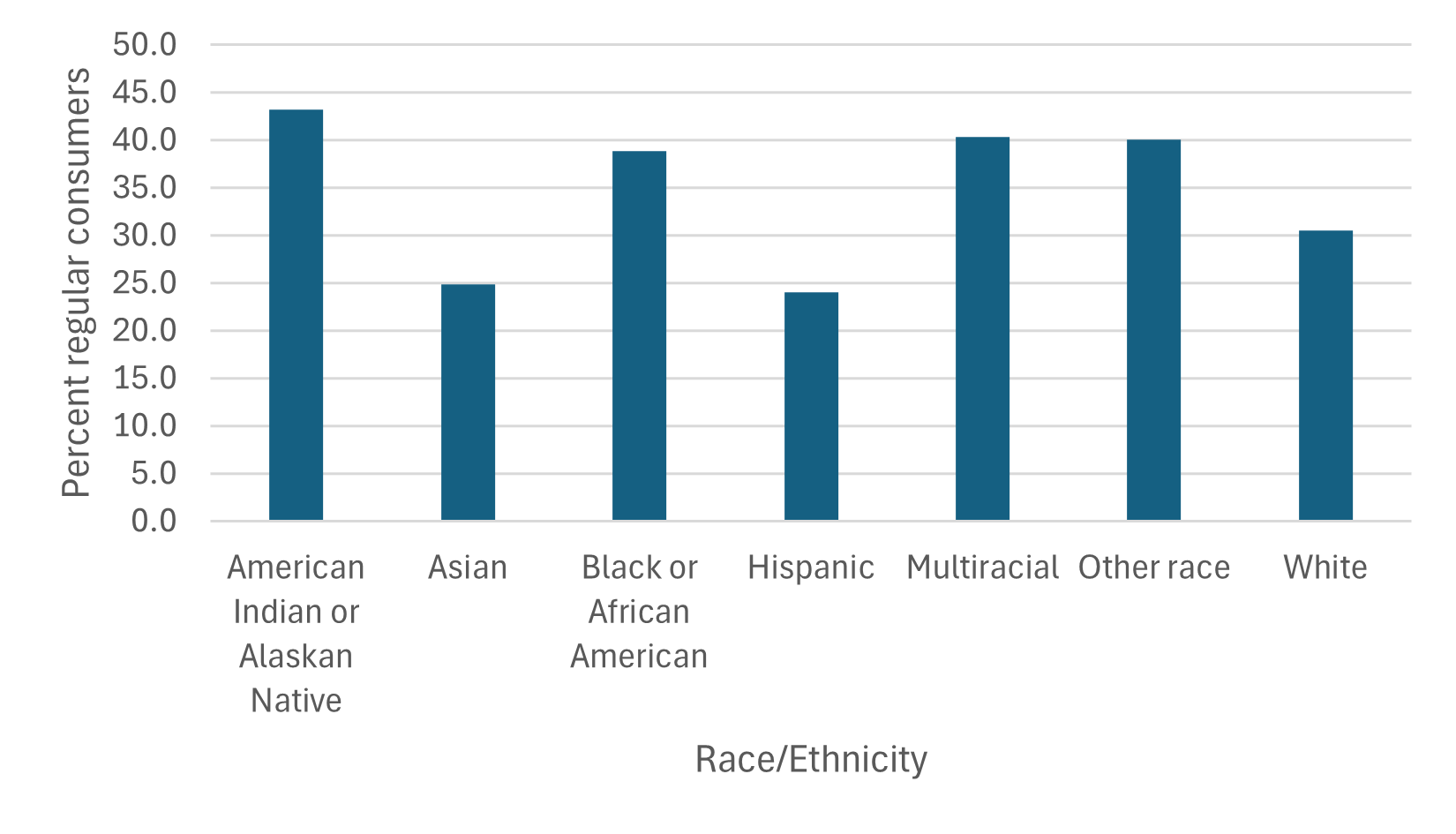

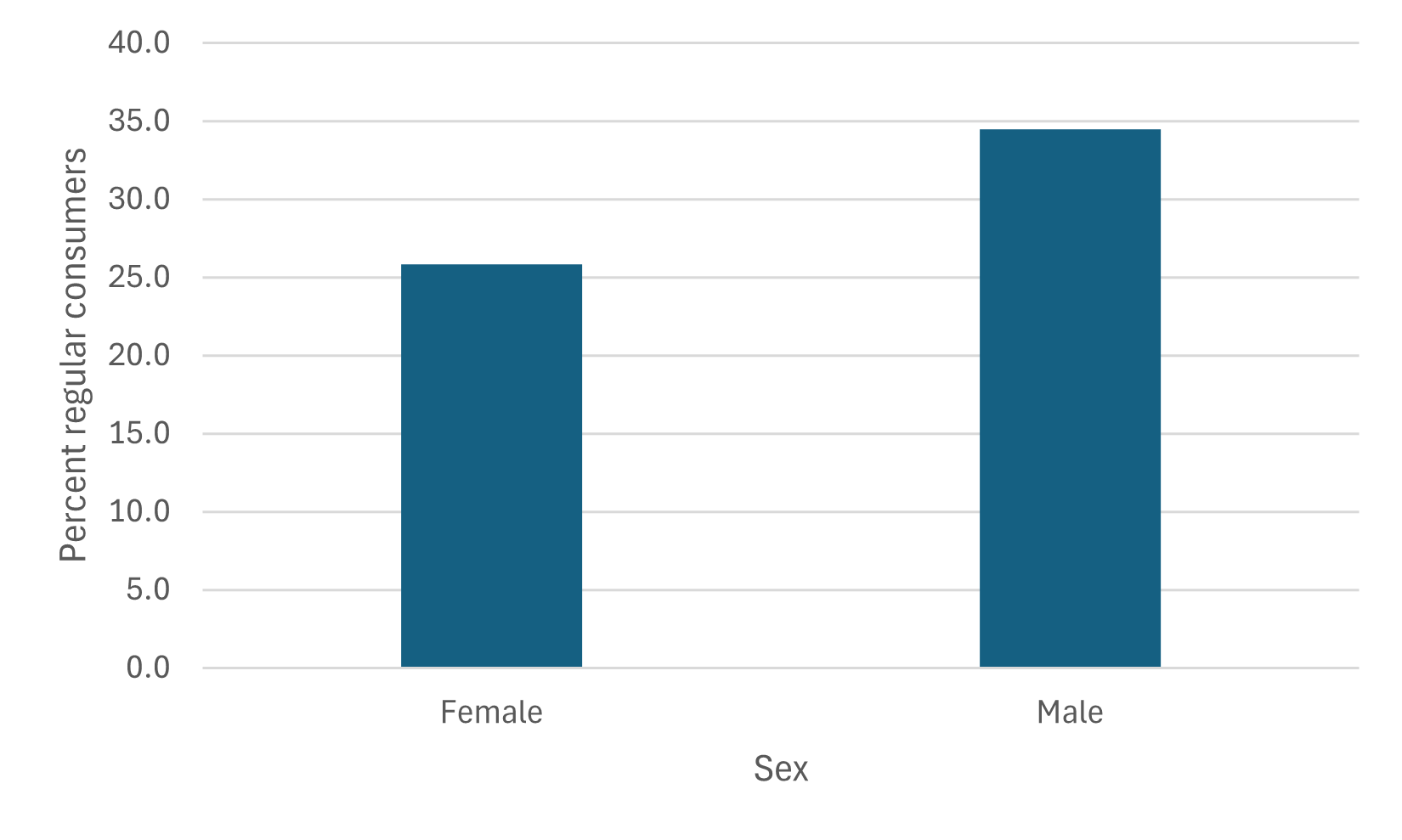

Approximately 50% of U.S. states have legal recreational cannabis markets.888While cannabis production and consumption remain prohibited at the federal level, in 2013 the United States Department of Justice announced that it would not interfere with state-level legalization as long as distribution and sales were strictly regulated by the states (Cole,, 2013). Washington state’s cannabis market opened in July 2014 for adults 21 years and older. Cannabis has since become one of the largest agricultural industries in the state, contributing $1.85 billion to gross state product (Nadreau et al.,, 2020). Cannabis consumption is widespread, with approximately 30% of Washington adults consuming cannabis on a monthly basis (Washington State Department of Health,, 2024). Consumption is relatively equal across race/ethnicity, education, and gender, but decreases monotonically with income and age. We detail the demographic characteristics of cannabis consumers in Appendix A.

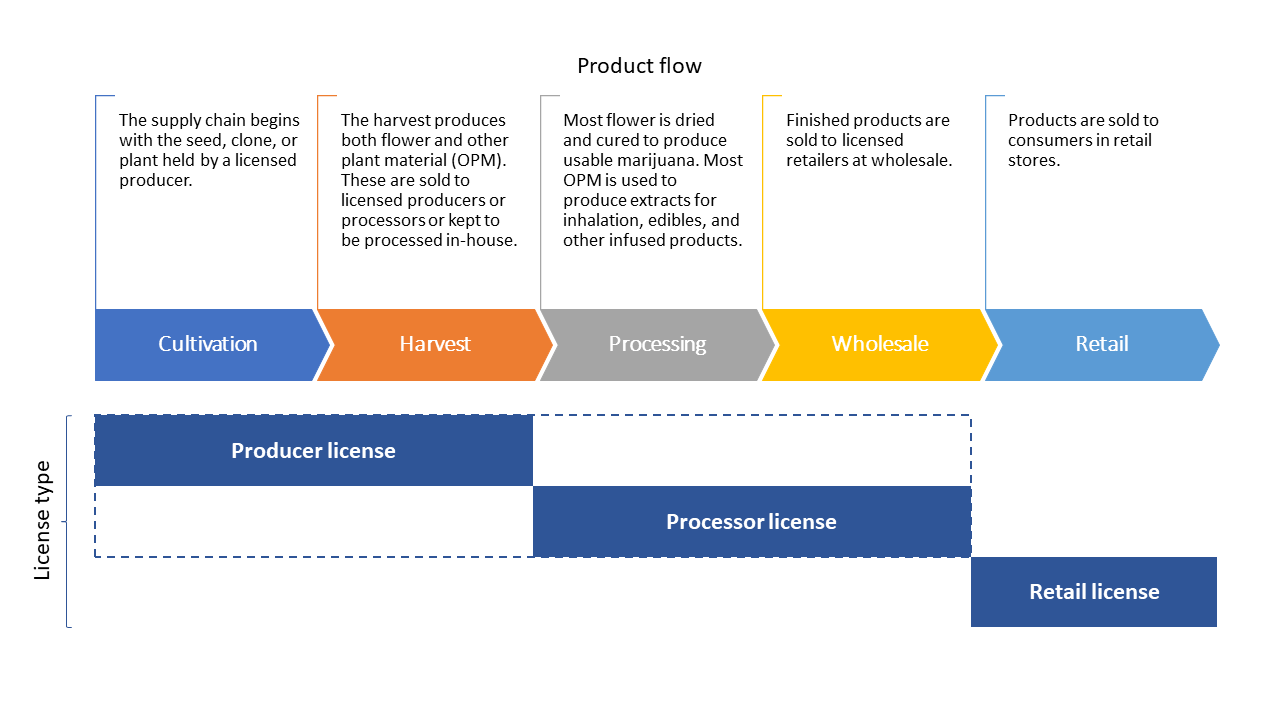

The industry is regulated by the Washington State Liquor and Cannabis Board (LCB) which offers separate business licenses for upstream and downstream establishments . Producer-processors (i.e. upstream establishments) can cultivate, harvest, and process cannabis but cannot sell to end consumers. Retailers (i.e., downstream establishments) can purchase fully packaged and labeled products from producer-processors and sell them in retail stores. Producer-processors cannot own retail licenses and vice versa, creating complete vertical separation along the supply chain. Retailers can only buy from producer-processors located in Washington state and producer-processors can only sell to retailers in the state. This seals off the core of the supply chain from other U.S. states with legal recreational markets. Retailers cannot sell online, meaning retailers operate brick-and-mortar stores. Appendix A contains additional information on the cannabis supply chain.

Cannabis business licenses are capped by the LCB at 556 retailers and 1,426 producer-processors (Washington State Liquor and Cannabis Board,, 2020). Licenses are granted at the establishment level so that a single firm can own several licenses. However, a firm can only own licenses of the same type. Approximately 65% of retail stores belong to one- or two-store firms; 25% of stores belong to 3-5 store chains; less than 11% of stores belong to chains with more than 5 stores.999When the market was created in 2014, the LCB allocated licenses according to a lottery. Since a single firm could apply for more than one license, the lottery created exogenous variation in firm size (see e.g. Hollenbeck and Giroldo,, 2022). Not all licenses are actively in business, meaning that some license holders have not opened an establishment and have no reported sales activity, especially at the producer-processor level. During our sample period, there were 508 active retailers and 692 active producer-processors.

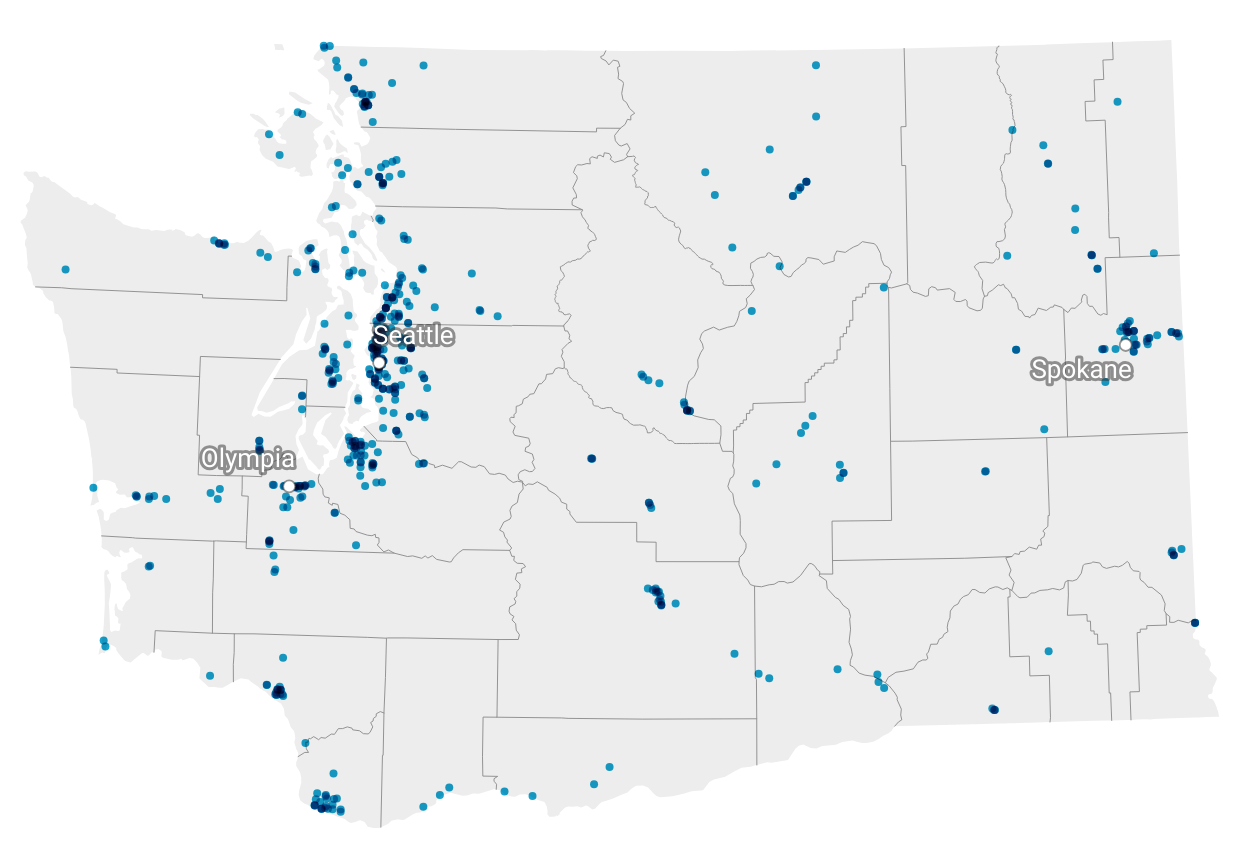

The LCB distributes retail licenses to counties according to population density (there are no restrictions on where producer-processors can be located). Retailers are located in 37 of the 39 counties in Washington state. The average cannabis consumer in Washington is located approximately five miles from the nearest retailer (Ambrose et al.,, 2021). The geographic distribution of retail stores is illustrated in Figure 2(b), Panel (a).

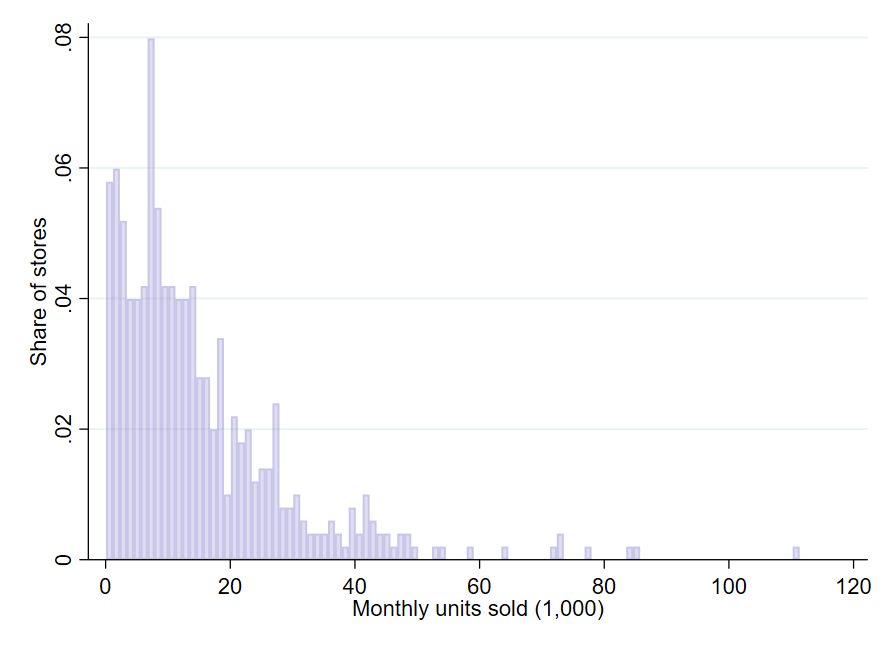

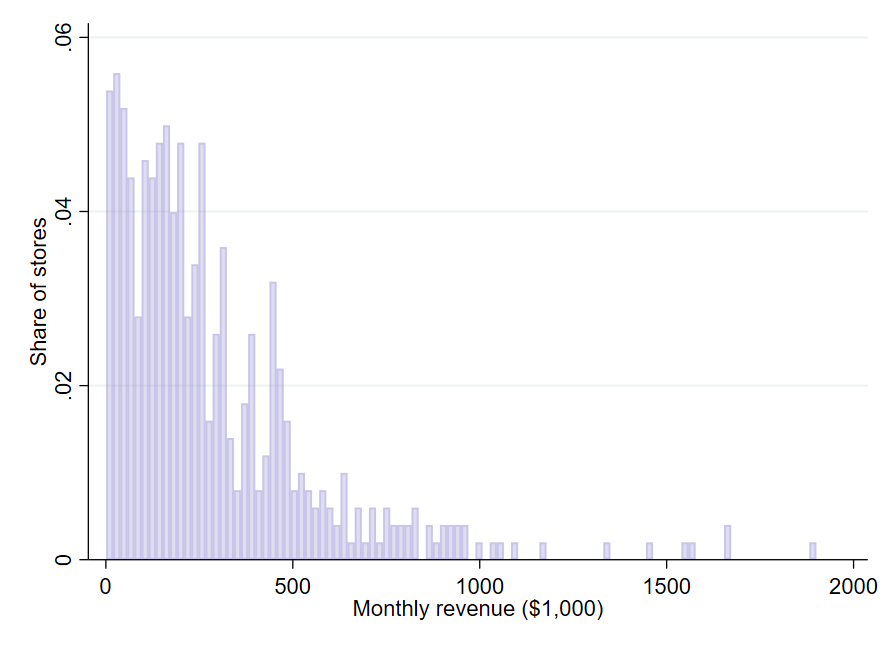

Retail sales are subject to a 37% sales tax but there is no tax on upstream sales. Per month, retailers sell approximately 14,500 units and earn about $280,000 in (tax-inclusive) revenue (see Table 1(b)). However, there is substantial variation across stores, with the average monthly revenue ranging from $6,900 at the smallest store to $475,000 at the largest.101010For context, the average cannabis retailer generates about twice the revenue of an average convenience store or one-fifth of an average supermarket in the United States (Statista,, 2022, 2024). For more information on the distribution of store characteristics, see Appendix A.

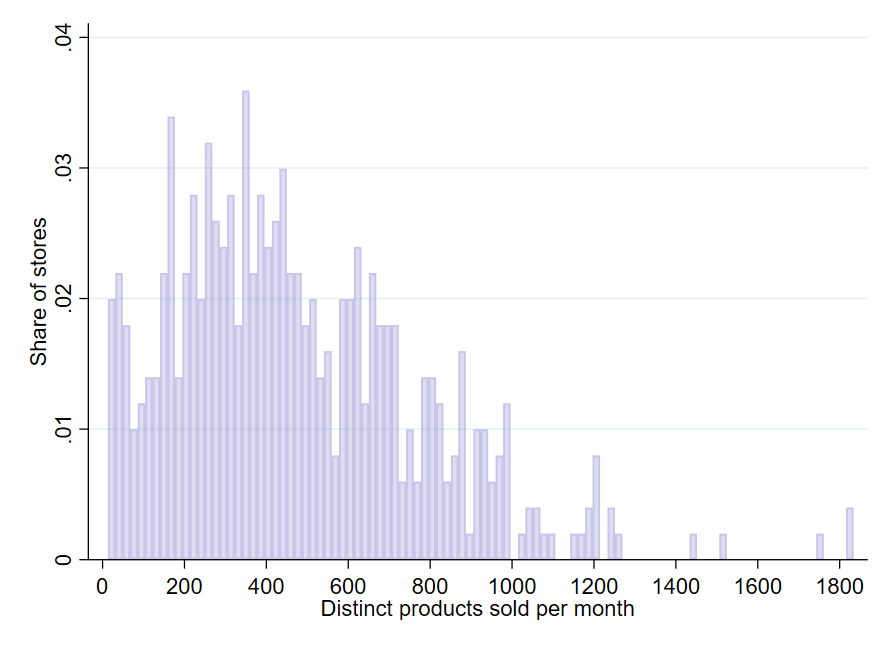

Table 1(b) provides an overview of the cannabis product market. Retail stores sell a variety of cannabis products—around 470 distinct products per month on average. The LCB classifies products according 12 categories (Washington State Legislature,, 2015). As Table 1(b) illustrates, usable marijuana (i.e. unprocessed dried flower) and concentrate for inhalation (e.g. for use in vape pens) account for more than 80% of all retail sales. Another 14% of retail sales comes from solid edibles (chocolate bars, gummies, etc), liquid edibles (soda and other infused drinks), and infused mix (e.g. pre-roll joints infused with concentrates). The remaining categories make up less than 2% of total revenue; these are topical products (e.g. creams and ointments), packaged marijuana mix (e.g. pre-roll joints), capsules, tinctures, transdermal patches, sample jar, and suppository.

| Monthly average per store | Sample total | |

|---|---|---|

| Establishments | 508 | |

| Units sold | 15,157 | 263 million |

| (5,829) | ||

| Distinct products | 470 | 210,842 |

| (305) | ||

| Sales | $282,857 | $5.07 billion |

| ($273,082) |

Notes: Column 1 reports monthly averages at the store level. Standard deviations are in parentheses. Column 2 reports totals across all stores and months in the sample period. Sales are tax-inclusive.

| Product category | Monthly sales (in millions of $) | Market share |

|---|---|---|

| Usable marijuana | $58.77 | 0.52 |

| Concentrate for inhalation | $34.70 | 0.31 |

| Solid edible | $8.45 | 0.08 |

| Infused mix | $5.40 | 0.05 |

| Liquid edible | $2.96 | 0.03 |

| Other | $2.16 | 0.02 |

Notes: Column 1 reports the average monthly retail sales (in millions of dollars) across Washington state for the major product categories; Column 2 shows the corresponding market shares. Sales are tax-inclusive.

2.2 Organized retail crime

Organized retail crime in the United States

Organized retail crime is defined as large-scale theft of retail merchandise or cash, typically by two or more people, often as part of a criminal enterprise. While the exact definition varies across law enforcement agencies and jurisdictions, a defining characteristic of organized retail crime is that merchandise is not stolen for personal use but is instead resold through third-party outlets. This contrasts with petty theft (e.g. stealing baby powder because one cannot afford it), which is not the focus of our study. For ease of notation, we refer to organized retail crime and retail crime interchangeably throughout the paper.

In 2022, the U.S. Chamber of Commerce declared organized retail crime a “national crisis” (U.S. Chamber of Commerce,, 2022). According to the National Retail Security Survey (NRSS), organized retail crime is responsible for nearly $5 billion in annual losses (National Retail Federation,, 2020). Organized retail crime is pervasive in scope, with criminals targeting a variety of stores and goods (U.S. Department of Homeland Security,, 2022). Incidents are often violent in nature and threaten employee and customer safety.111111In 2023, 81% of NRSS respondents reported an increase in retail crime-related violence against employees (National Retail Federation,, 2023). In a separate survey, more than three-quarters of retailers stated that a criminal had threatened to use a weapon against an employee, while 40% of Asset Protection Managers reported incidents where an organized retail criminal used a weapon to inflict harm on an employee (Dunham,, 2021). Many retailers invest heavily in strategies to prevent retail crime, including third-party guard services, enhanced surveillance technologies, locking cases, and employee safety and de-escalation training (see e.g. Target, (2023); Reagan and Schlesinger, (2019); Fonrouge, (2022)).121212In 2023, for example, 34% of National Retail Security Survey respondents increased payroll to support security and 45% increased the use of third-party security personnel as a measure of crime prevention (National Retail Federation,, 2023).

Many states have enacted legislation specifically targeting retail crime, including stiffer penalties for people caught stealing from stores with the intent to resell merchandise, and adding language targeting organized groups that rob multiple retail outlets (Lewis,, 2023).131313In Louisiana, for example, anyone caught stealing retail merchandise as part of a group of three or more people may now face up to seven years in prison . In addition to legislation, numerous local, state, and federal law enforcement agencies have created retail crime task forces across the United States (Washington State Office of the Attorney General,, 2022; U.S. Department of Homeland Security,, 2022).

Organized retail crime in cannabis

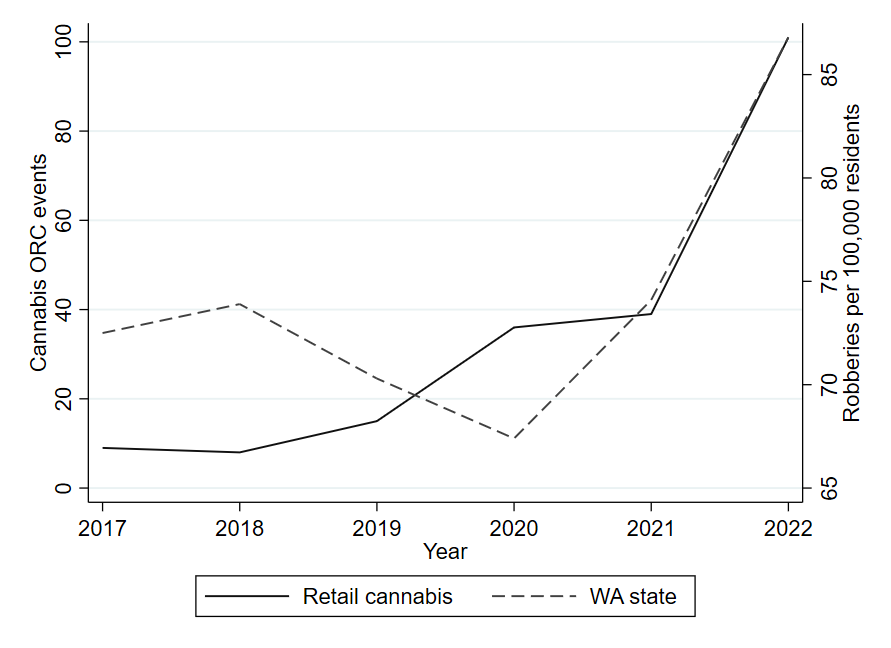

Similar to other retail sectors, retail crime is pronounced at cannabis stores. Between 2017 and 2023 there were 210 reported robberies and burglaries at cannabis retailers in Washington state. Figure 1 illustrates that retail crime in cannabis has increased over time and that the trend largely tracks data provided by the FBI on overall robberies in Washington state. This trend has prompted policymakers to take action. Retail cannabis was cited by the Washington state attorney general when creating the state’s retail crime task force (Washington State Office of the Attorney General,, 2022), and in 2023 a senate bill was introduced in the state legislature aimed at providing tax relief for security improvements at cannabis retail stores (Washington State Legislature,, 2023).141414The state senate introduced a separate bill that would have increased the prison sentences for those convicted of first- or second-degree robbery at a cannabis retail store. The bill did not advance to the house floor for a vote (Washington State Legislature,, 2021).

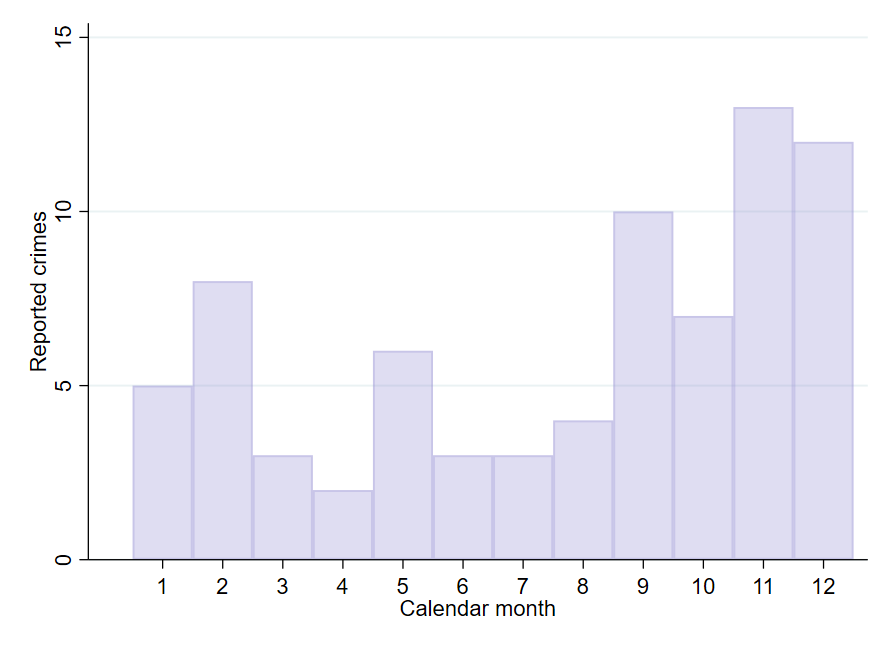

Notes: The figure displays annually reported organized retail crime incidents in the Washington state cannabis industry (solid line) and robberies per 100,000 inhabitants in Washington state (dotted line) from 2017 to 2022. Data sources: Uncle Ike’s Robbery Tracker for cannabis industry incidents and the FBI Crime Data Explorer for state-wide robbery statistics.

Organized retail crimes in cannabis are predominantly armed robberies involving a group of perpetrators entering a store during store hours with guns drawn. Perpetrators typically extract cash from the register, demand that employees give them access to the safe, or clear shelves of merchandise. Since cannabis remains illegal at the federal level, cannabis stores do not have access to electronic payment processing services like Visa and Mastercard and nearly all retail transactions are cash-based. Stores thus handle a large amount of cash, making them prime targets for retail crime.

Robberies are often violent: in several instances, consumers or employees have been temporarily taken hostage, physically assaulted, shot at, or even killed. Victimized stores often respond to retail crime incidents by increasing security expenditures. According to the state’s Organized Retail Crime Task Force, interviews with store owners, and numerous news reports, the most common expenditure involves hiring additional security guards (Washington State Liquor and Cannabis Board,, 2022; Saldanha,, 2022; Phan,, 2022).151515Since contracted security guards often cost between $75-100 per hour in Washington state, this amounts to a sizeable labor cost shock for cannabis retailers (Saldanha,, 2022; Phan,, 2022). Further preventative measures include installing panic buttons, two-way door systems, and investing in employee de-escalation training.161616Stores are required by law to have comprehensive round-the-clock video surveillance.

3 Data

3.1 Price data

To monitor developments in the cannabis market, legalization came with stringent data reporting and sharing requirements for cannabis businesses. Retailers must record all sales and regularly upload data feeds to the LCB. Compliance with data reporting is strictly enforced by the LCB. When a business is issued a violation, it can receive a fine, a temporary license suspension, or both. In cases of repeated violations, a license can be revoked by the LCB board. Given such strict enforcement, violations are uncommon. In 2022 for example, the LCB issued 63 violations among over 1,100 active licensees (Washington State Liquor and Cannabis Board,, 2024).

The data, which is reported weekly, contains detailed information on the price and quantity of each product sold by a producer-processor to a retailer, and the subsequent price and quantity of that very same product sold at the retail level. We refer to the price charged by a producer-processor as the wholesale price, and the price charged by retailers as the retail price. This reflects that producer-processors resemble wholesalers when viewed from the perspective of retailers.

The data captures granular product differentiation. To give an example, a 1.0 gram package and a 2.0 gram package of Sunset Sherbert usable marijuana (i.e. unprocessed dried flower) produced by Northwest Harvesting Co are treated as different products in the data.171717Similar to how wines can be distinguished by the grape variety (e.g. Riesling, Chardonnay, etc), cannabis comes in many strains, which is ’Sunset Sherbert’ in the given example.

The LCB switched providers for its traceability system in October 2017 and again in December 2021, creating two structural breaks in the price data. Our sample period lies between these breaks and spans March 2018 through December 2021. We obtained the data from Top Shelf Data, a data analytic firm that ingests the raw tracking data from the LCB and matches it with additional product information. The estimation sample covers the universe of sales from all 508 active retail establishments. Per month, retailers sell approximately 14,500 units and earn about $280,000 in tax-inclusive sales revenue (see Table 1(b)). Over the entire sample period, the data contain $5.07 billion in tax-inclusive retail sales. All retail prices and revenues reported in this paper are tax-inclusive.

To estimate pass-through semi-elasticities, we follow previous studies (e.g., Renkin et al.,, 2022; Leung,, 2021; Harasztosi and Lindner,, 2019) and use as our dependent variable the natural logarithm of the monthly store-level price index. The log price index measures the price inflation for store in month , and is denoted as :

| (1) |

is an establishment-level Young price index that aggregates price changes across product subcategories , where each subcategory is a unique category-unit weight combination. The index weight is the revenue share of subcategory in establishment during the calendar year of month .181818As pointed out by Renkin et al., (2022), price indexes are often constructed using lagged quantity weights. Since product turnover is high at retail stores, lagged weights would limit the number of products used in constructing the price indexes. Thus, contemporaneous weights are used. The dependent variable is equivalent to the first difference of the log of the weighted store price level between month and . Store-level indices are common in the literature on retail price movements and carry several advantages over more disaggregated product-level price data. First, retail crime occurs at the store level, making the store a natural unit of analysis. Second, a store-level index allows the researcher to weigh products by their importance for each store. Finally, entry and exit occur at a much higher frequency for products compared to stores, and a product-level time series would contain frequent gaps. Since the vast majority of cannabis businesses have succeeded at staying in business, the store-level panel is much more balanced. We describe the establishment-level price index in more detail in Appendix B.

Besides prices, we are also interested in the effect of retail crime on other store-level outcomes. First, we consider the possibility that consumers substitute out of victimized and into nearby rival stores following crime incidents (e.g. due to increased prices or fear of physical harm). To investigate this, we construct a store-level quantity index measuring the monthly percent change in quantity sold. The quantity index is constructed similarly as the price index with index weights based on annual revenue shares (see Appendix B).

It is also possible that stores adjust their wholesale expenditures to offset the costs of crime. Wholesale costs are particularly important since the Cost of Goods Sold (COGS) accounts for 80% of cannabis retailers’ variable costs (see Appendix A), similar to other retail sectors (Renkin et al.,, 2022). An advantage in our setting is that we directly observe wholesale prices and quantities at the store-product-month level. We construct a wholesale cost index that captures the month over month percent change in wholesale prices paid by a store. The index weights are based on retailers’ annual wholesale expenditures (rather than annual revenue as with the price index).191919In a robustness check, we construct monthly (rather than annual) expenditure weights which capture potential wholesale substitution patterns on the part of retailers. Results are similar to our main specification that uses annual weights.

Finally, we investigate whether stores adjust retail margins in response to crime. We construct a store-level margins index that measures the monthly percent change in the ratio of unit retail price to unit wholesale cost (using annual revenue weights).

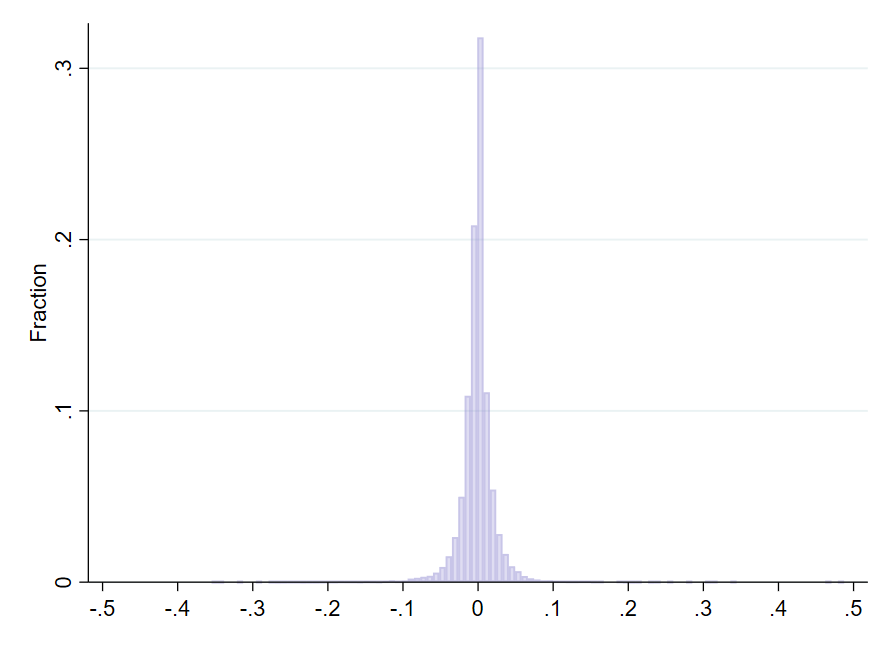

Table 2 provides descriptive statistics for our indices. The price, wholesale cost, and margins indices are centered around zero and have means close to zero. Standard deviations for these indices range from 0.002 to 0.029. The quantity index has a larger variance than the other indices. This is a common characteristic of quantity indices constructed from store-level scanner data, and is similar to what is found elsewhere in the literature (see e.g. Renkin et al.,, 2022). The distributions of the indices can be found in Appendix Figure 8.

| Mean | SD | Median | |

|---|---|---|---|

| Log price index | -0.001 | 0.029 | 0 |

| Log quantity index | -0.008 | 0.21 | -0.012 |

| Log wholesale cost index | 1.18e-05 | 0.002 | 0 |

| Log margins index | -0.001 | 0.029 | 0 |

Notes: This table presents the mean, standard deviation, and median of our main dependent variables: Log price index, Log quantity index, Log wholesale cost index, and Log margins index.

3.2 Retail crime data

Crime at retail cannabis stores is not formally tracked or aggregated by law enforcement agencies. However, on behalf of the market at large, Uncle Ike’s, a retailer and member of Washington’s Craft Cannabis Coalition of over 70 small businesses, maintains a public database of retail crime incidents reported by businesses, law enforcement, and the news media. While the database offers a reasonably accurate list of crimes reported to local police departments, it is not an official census of retail crime at cannabis stores.202020For instance, the database’s tally aligns perfectly with the Bellevue Police Department’s data on armed robberies at cannabis retailers (Saldanha,, 2022). We view this as unproblematic for two reasons. First, each incident in our sample period is cross-referenced with either a police report, police case number, or a news article that references a police investigation. This makes it highly unlikely that treatment is falsely assigned to a store that is, in fact, untreated. Conversely, it is possible that not all crimes are reported to the police or news media and, hence, do not appear in the database. In that case, treated stores would potentially be misclassified as controls, leading to attenuation bias and conservative treatment effect estimates. However, since the control group is much larger than the treatment group in our setting, misclassified controls will be dominated by correctly classified controls. As a result, we expect attenuation bias from misclassified controls to be minimal.

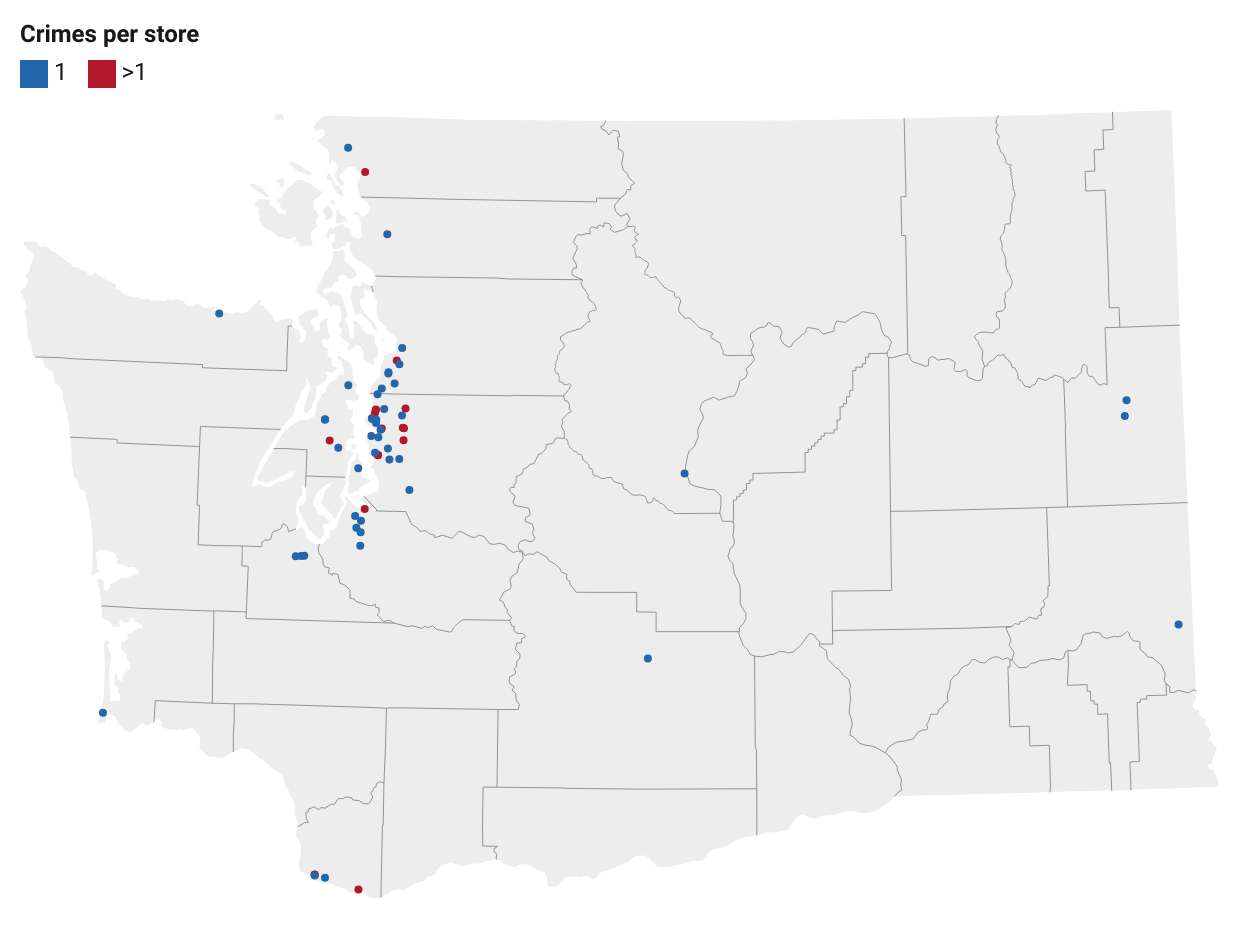

Figure 2(b) shows the locations of stores with a reported crime during our sample period. There were 76 reported crimes at 57 different stores (46 stores were victimized only once and 12 stores were victimized more than once).212121One additional store is victimized during our sample period, but the store has no clean controls since there are no other stores within 30-50 miles. We describe our criteria for defining clean control in Section 4. Of these crimes, 62 were armed robberies and 14 were burglaries. Approximately two-thirds of these crimes occurred at stores in the Seattle area and the neighboring cities of Tacoma and Bellevue, which roughly corresponds to the share of stores in those cities compared to the rest of the state. In general, crime incidence at cannabis stores reflects the geographic distribution of stores.

There is some evidence of seasonality in crime incidents at cannabis retailers, with more crimes occurring in the fourth quarter compared to other quarters (see Appendix Figure 7). Over the entire sample period, crime incidents at cannabis retailers increased, which roughly tracks the increase in reported crime in Washington state more generally (see Figure 1).

Notes: Panel (a) illustrates the geographical distribution of cannabis retail stores in our sample. Panel (b) shows the geographical distribution of victimized stores, with stores reporting one crime incident marked by blue dots and those with at least two reported crime incidents marked by red dots.

4 Empirical strategy

We are interested in the effect of retail crime on store-level prices. To identify a causal effect, we exploit the quasi-experimental variation in the time and location of retail crimes using a (stacked) difference-in differences (DiD) estimator. The following subsections describe our empirical strategy in more detail.

4.1 Treatment and control groups

Two treatment groups: victimized and rival stores

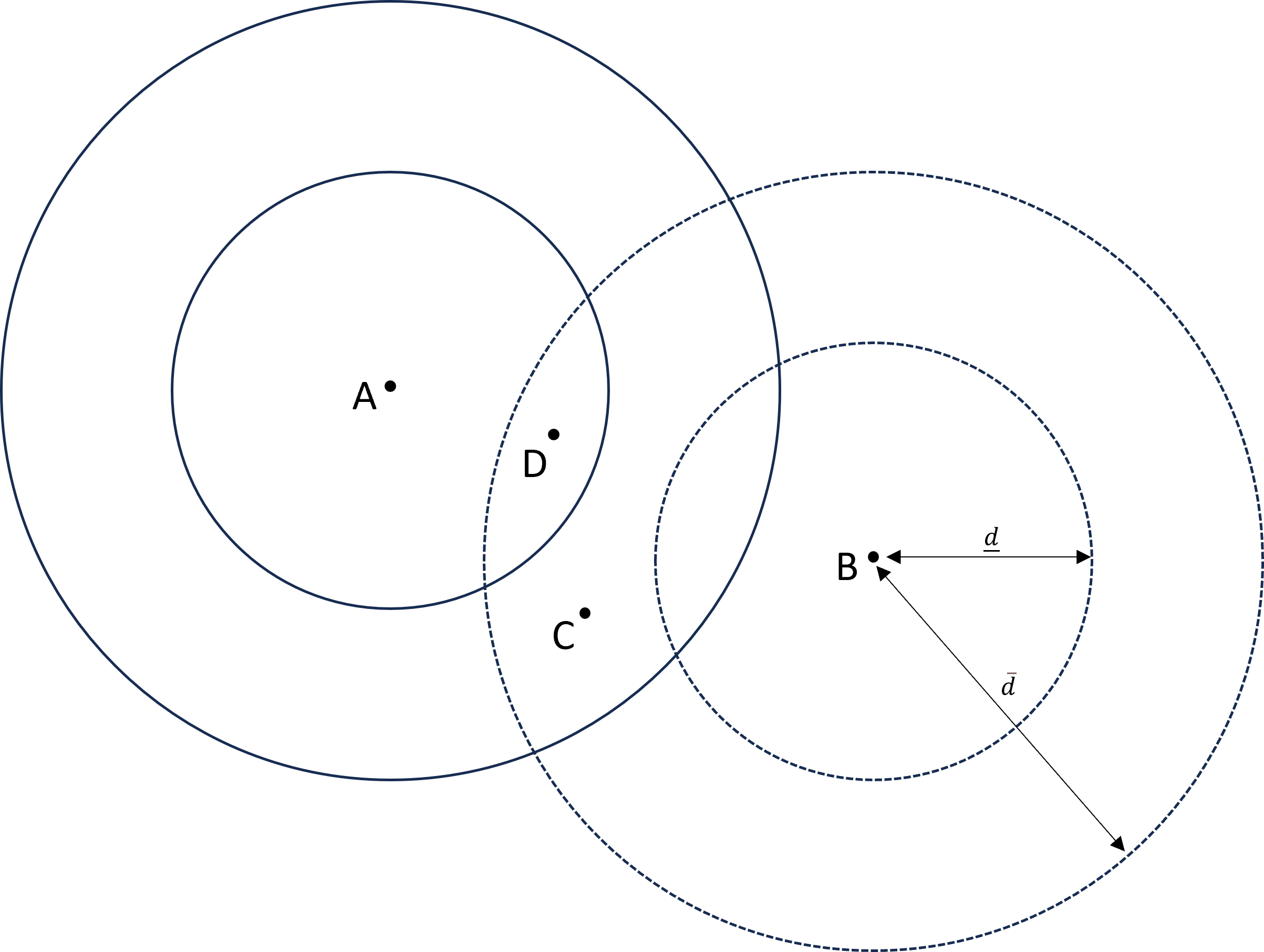

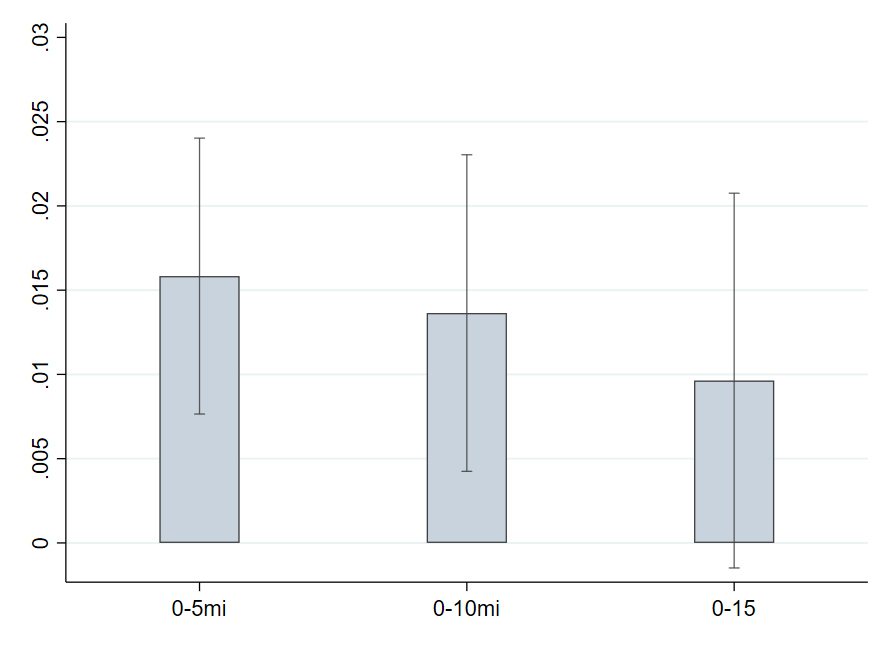

We define treatment timing as the store-specific month of a robbery or burglary. We distinguish between two treatment groups based on their exposure to retail crime: i) victimized stores, i.e., all stores that directly experience a robbery or burglary, and ii) rival stores, i.e., stores located within a 5-mile radius of a victimized store. The first treatment group allows us to analyze the direct impact of crime on victimized stores’ pricing strategies, while the second accounts for potential spillovers to nearby stores. Such spillovers could result from demand substitution, strategic complementarity in prices, or an own-cost shock (e.g. from precautionary security expenditures or higher business crime insurance premia). We choose the 5-mile radius for several reasons. First, victimized stores have an average of nine competing stores within this radius. This implies that a consumer at the average store can choose between several alternative stores. To the extent that crime induces changes in consumer behavior, we view it as plausible that these nearby stores may be affected. Second, the 5-mile radius is sufficiently small so as to reasonably capture local market characteristics that may influence how rival stores react to a nearby store being victimized. Results are robust to adjusting the boundary (see Appendix F). In assigning treatment to a larger group of nearby units, our strategy resembles those from the spatial treatment literature (see e.g. Keiser and Shapiro,, 2019; Lipscomb and Mobarak,, 2017).

Control group: unaffected local markets

We compare both treatment groups to a common control group: stores in unaffected local markets. In defining unaffected local markets, we face a tradeoff. On the one hand, we want to ensure that stores in the control group are in markets that are comparable to (and hence near) the treated group. At the same time, if there are spillovers from the treated group to nearby stores, then including nearby stores in the control group leads to biased estimates. In this subsection, we identify potential spillovers and use them to guide our definition of unaffected local markets.

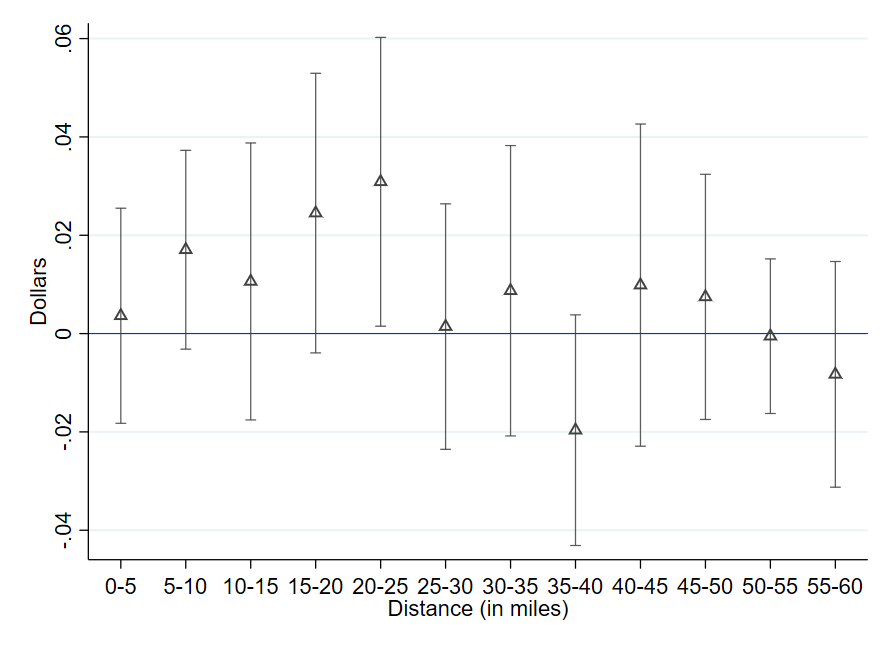

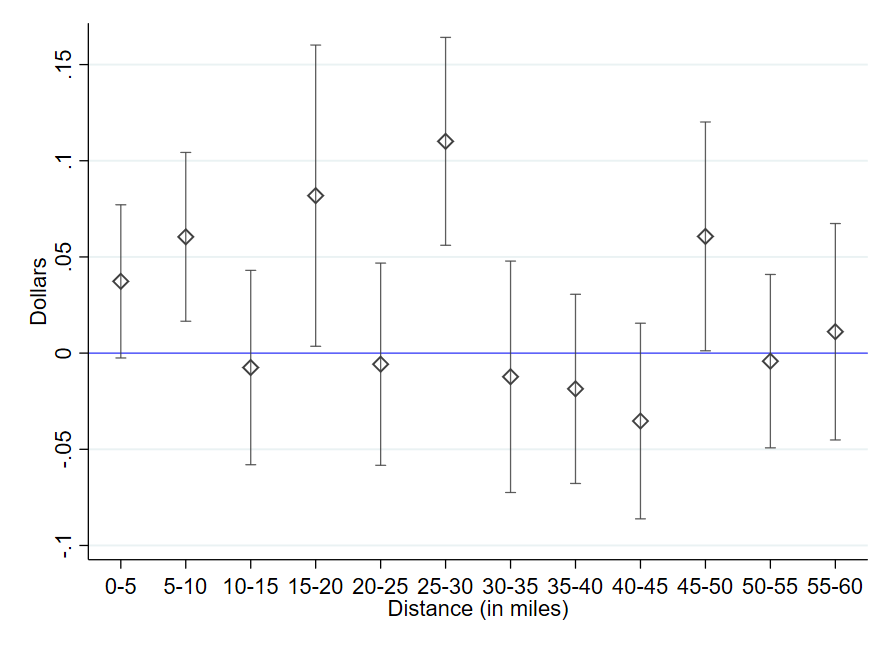

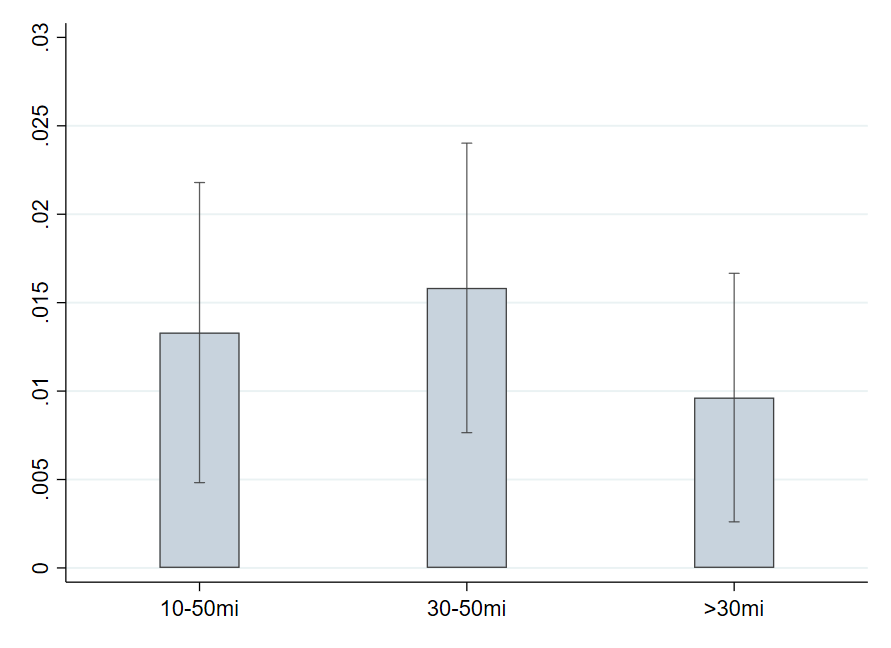

One concern is strategic complementarity in pricing. Muehlegger and Sweeney, (2022) show that in the presence of imperfect competition, the strategic response of (untreated) competitors may disqualify them as a valid control group. In practice, this implies that the price a firm sets is a function of not just its own costs, but also those of its rivals. A major advantage in our setting is that—in addition to retail prices and quantities—we also observe prices and quantities for the universe of vertical transactions between producer-processors and retailers. This allows us to measure retailers’ spatial sensitivity to competitors’ costs and identify the distance at which retailers no longer compete in prices. In Appendix D, we estimate the pass-through of the average wholesale costs of competing stores within a certain distance from store on store ’s retail prices. We find that sensitivity to competitors’ unit costs dissipates by the 30-mile mark under a variety of specifications (see Appendix D for more details). This suggests that stores located more than 30 miles from a victimized store will not have a strategic price response to the victimized store’s crime pass-through, and hence serve as valid controls from a strategic pricing standpoint.

Spillovers can also arise if consumers substitute demand out of victimized stores and into nearby competitors, e.g. out of fear for their own safety or temporary crime-induced store closures. While demand substitution is distinct from strategic complementarity in pricing, at a mechanical level both entail consumers choosing between stores from the same choice set. Therefore, we view the 30-mile boundary for strategic pricing as a plausible boundary for demand substitution as well.

Finally, spillovers can occur if crime incidents induce a cost shock at rival stores. There are at least two potential reasons for such a cost shock. First, upon learning about crime at a victimized store, rival stores may update their own expectations of being victimized and invest in precautionary security measures. While the geographic scope of such knowledge spillovers and precautionary expenditures is difficult to measure, it is plausible that stores located close to a victimized store are more likely to update their expectations of being victimized compared to stores located further away, e.g. due to local market characteristics. Therefore, we expect this channel to operate within a similar geographic radius as strategic complementarity in pricing and demand substitution. Second, if crime incidents cause insurers to reevaluate the crime risk in local markets, then retailers may face higher crime insurance premia. Since crime insurance premia are typically a function of the number of employees at a store as well as store revenues and size, a hike in premia may amount to a marginal cost shock.222222Standard commercial property insurance policies do not typically cover losses from business-related crimes. Instead, business crime insurance is an optional policy. Data on the share of retailers (cannabis or otherwise) with business crime insurance is sparse.

While potential spillovers require omitting nearby stores from the control group, it is important to ensure that the control group remains comparable to the treated stores to the greatest possible extent. We therefore limit the distance at which a store can serve as a control to 50 miles. Unaffected local markets thus consist of stores located in the concentric “donut” between 30 and 50 miles from a victimized store. We conduct several robustness checks to test the sensitivity of our main results to adjusting the boundaries for unaffected local markets (see Appendix F).

Panel (a) in Table 3 compares pre-treatment characteristics of treated and untreated stores in our study. Columns 1 and 2 show that the average unit price at victimized and rival stores is similar prior to treatment. Victimized stores sell more products per month, have higher monthly revenue, and have more product variety compared to rival stores, though the differences are small and never statistically significant. The similarities between victimized and rival stores prior to crimes support our assertion that the location of crime incidents is conditionally quasi-random. Column 3 summarizes the never-treated group and is based on the entire sample period. Note that never-treated stores may or may not serve as controls depending on their location. The mean price at never-treated stores is similar to victimized and rival stores, but the quantity sold, monthly revenue, and product variety are lower than at victimized and rival stores. This could reflect that victimized and rival stores are primarily located in densely populated urban areas, whereas never-treated stores may contain a larger share of rural stores. Our definition of unaffected local markets effectively controls for such differences. Panel (b) of Table 3 shows the number of stores in each group (victimized, rivals, and never-treated).

| (a) Pre-treatment characteristics | |||

|---|---|---|---|

| (1) | (2) | (3) | |

| Victimized | Rivals | Never-treated | |

| Unit price (in dollars) | 26.24 | 25.47 | 26.00 |

| (4.33) | (4.49) | (4.50) | |

| Units sold per month | 13,260 | 12,304 | 10,908 |

| (12,409) | (11,931) | (11,617) | |

| Monthly revenue (in dollars) | 248,516 | 215,201 | 210,416 |

| (234,911) | (217,957) | (235,890) | |

| Unique products per month | 505 | 425 | 393 |

| (388) | (346) | (324) | |

| (b) Treatment group sizes | |||

| Stores | 57 | 264 | 137 |

| Control stores | 329 | 321 | |

| Total store-months | 15,949 | 17,055 | |

Notes: Panel (a) summarizes store-level variables prior to treatment, with statistics for the never-treated group based on the entire sample period. Standard deviations are in parentheses. The reported variables include unit price, average store quantity sold per month, average store revenue per month, and average number of distinct products sold per month. Columns 1-2 display summary statistics for the two treatment groups: victimized stores and rival stores. Column 3 presents data for stores that are never in one of the treatment groups and may or may not serve as controls depending on their location. Panel (b) shows the number of stores in each treatment group.

4.2 Main specification

Our main specification builds on the stacked DiD estimator. Stacked DiD has been applied in a variety of settings, including investigating the effect of local cost shocks on national retail chains (Butters et al.,, 2022), the effect of application costs on the targeting of disability programs (Deshpande and Li,, 2019), and the effects of minimum wage hikes on low wage employment (Cengiz et al.,, 2019). Stacked DiD overcomes issues with canonical DiD which can yield biased estimates under staggered treatment adoption and heterogeneous treatment effects (see, e.g., Baker et al., (2022); Goodman-Bacon, (2021); Sun and Abraham, (2021); Callaway and Sant’Anna, (2021)). Similar to other DiD estimators, the stacked DiD estimator identifies the causal treatment effect under the assumption of parallel trends and no anticipation. We discuss these identifying assumptions and other threats to identification in more detail in Section 6.

The idea behind stacked DiD is to create a separate dataset (i.e. sub-experiment) for each crime incident comparing the treated group for that incident to a set of “clean” controls. An identifying variable is generated for each dataset and the datasets are concatenated to create a single “stacked” dataset. The model is estimated on the stacked data with sub-experiment-specific unit- and time-fixed effects.

Most studies using stacked DiD define clean controls solely based on treatment timing as this accounts for biases from heterogeneous treatment effects under staggered adoption.232323An exception is Butters et al., (2022), who investigate spillover effects of state excise taxes on chain stores in nearby states. Their approach is similar to ours in that they exclude chain stores whose parent company is affected by a tax hike in another state within the event window. We add a geographic layer to the clean control criteria to remove additional contamination from treatment effect spillovers. Thus, to be considered a clean control for a given sub-experiment, a store must be (i) a never-treated or not-yet-treated store outside of its own event window, (ii) located between 30-50 miles of the corresponding crime incident, and (iii) cannot be within 30 miles of a victimized store whose event window overlaps with the focal incident.

The flexibility of the stacked DiD estimator in extending rules for clean controls to geographic criteria is crucial in our setting. In particular, stacked DiD reduces biases from spillovers to untreated stores, maintains geographically comparable treatment and control stores, and ensures a large pool of clean control stores. This feature is the primary reason we choose the stacked DiD estimator over related estimators (Callaway and Sant’Anna,, 2021; Borusyak et al.,, 2024) which typically impose restrictions on the control group composition for the entire sample and thereby significantly reduce the pool of valid control observations. Details about our inclusion criteria for clean controls and the advantages of using stacked DiD compared to other estimators are discussed in Appendix E.

For each sub-experiment, stacked DiD identifies a group average treatment effect for the treated (ATT), similar to the cohort-specific ATT in Sun and Abraham, (2021) and the group-time ATT in Callaway et al., (2024). Moreover, when there is balance in the number of pre-and post- treatment periods across sub-experiments, the stacked DiD regression recovers an aggregate ATT that is a convex combination of underlying causal effects (Wing et al.,, 2024). Since our setting contains several crime incidents near the beginning and end of the sample period, dropping these incidents substantially reduces our treatment sample size. Therefore, in our main specification we allow for compositional imbalance in pre- and post-treatment periods across sub-experiments. Nevertheless, we impose compositional balance in a robustness check and find very similar results (see Section 6).242424In addition to compositional balance we apply a weighted aggregation to recover the “trimmed aggregate ATT” (Wing et al.,, 2024). See Section 6 for details.

For estimation, we specify a distributed lag model with leads and lags before and after treatment adoption. We define treatment adoption, , as a dummy variable that is equal to one if store is treated months after period (or months before when is negative), and equal to zero otherwise. In our main specification, we drop stores with multiple treatments from the sample prior to the second treatment so as to isolate the effect of the first crime on store prices (we allow for multiple treatments in a robustness check in Section 6).252525Stores with multiple treatments are dropped from the sample the month prior to the second treatment. For a small number of stores, the second treatment occurs during the event window of the first treatment, meaning the post-treatment period is shorter for these stores. Since the store-level price indexes and the treatment adoption indicators are in first-differences, we estimate the following model in first-differences:

| (2) |

Equation 2 relates the monthly inflation rate at store , , to leads and lags of the treatment adoption indicator, , for store in sub-experiment . We control for sub-experiment-by-time fixed effects, . Since the model is in first differences, store FE are swept out. Since the identifying variation is at the store level, standard errors are clustered by store to allow for autocorrelation in unobservables within stores, similar to Butters et al., (2022); Deshpande and Li, (2019).262626Wing et al., (2024) show that clustering at the level of the treatment (i.e. stores) leads to valid inference with a stacked DiD estimator.

The parameter measures the change in establishment ’s inflation resulting from a robbery or burglary months after a crime (or months before when is negative) compared to the control group.272727Since distributed lag coefficients measure incremental treatment effects, one fewer lead has to be estimated compared to an event study specification. Thus, an 11-month event window requires estimating 10 distributed lag coefficients (Renkin et al.,, 2022; Schmidheiny and Siegloch,, 2023). While inflation is the dependent variable, we follow previous studies and present the estimates as the effect of treatment on the price level (see e.g. Renkin et al., (2022); Leung, (2021)). We thus normalize the effect on the price level to zero in the baseline period one month before treatment and report the cumulative treatment effect as the sum of at various lags: . The pre-treatment coefficients are reported in a similar manner with . This linear transformation is commonly applied in studies with a dependent variable that is in first-differences (Renkin et al.,, 2022; Leung,, 2021).282828The linear transformation transfers the statistical properties (consistency and asymptotic normality) of to the cumulative and . Standard errors of and are calculated from the variances and covariances of the vector by the standard formula for linear combinations (Schmidheiny and Siegloch,, 2023). The cumulative distributed lag coefficients are numerically equivalent to the parameter estimates from an event study design under constant treatment effects outside the effect window (Schmidheiny and Siegloch,, 2023).

An important consideration is the number of leads and lags to include in equation 2. One limitation is that the establishment panel is not balanced, meaning that changes in the underlying sample may affect estimates when is large. Therefore, in our baseline estimation, we set . This implicitly assumes constant treatment effects outside of the 11-month event window, i.e. . We show in Appendix F that treatment effects remain stable over a longer event window.

Our main analysis investigates the effects of retail crime on prices at retail cannabis stores. However, we are also interested in the effects of retail crime on other store-level outcomes, as this sheds light on the underlying factors driving retail crime pass-through. For this purpose, we estimate equation 2 using the store-level quantity indexes, wholesale cost indexes and retail margin indexes as dependent variables (we describe these variables in detail in Section 3).

5 Results

5.1 Main results

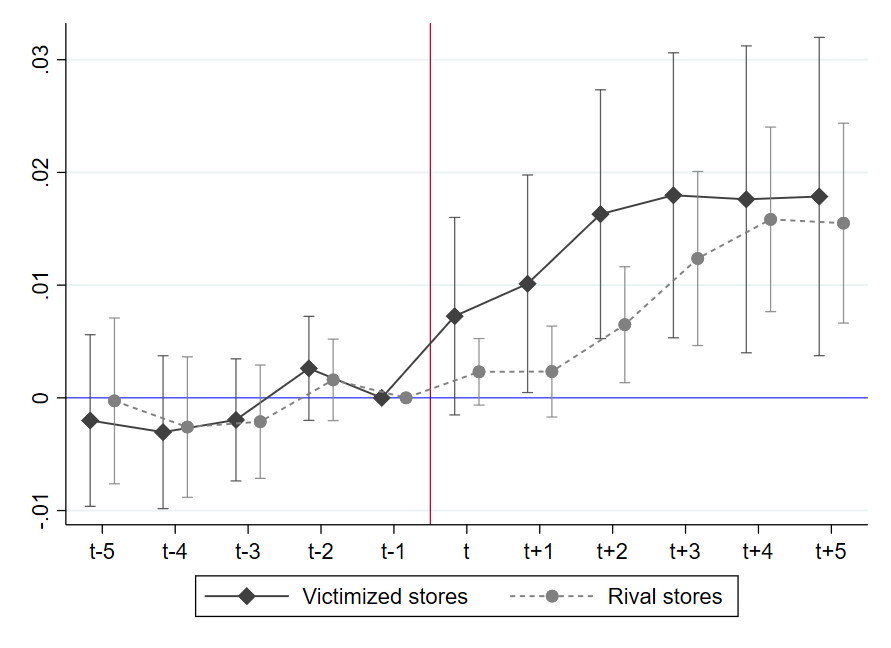

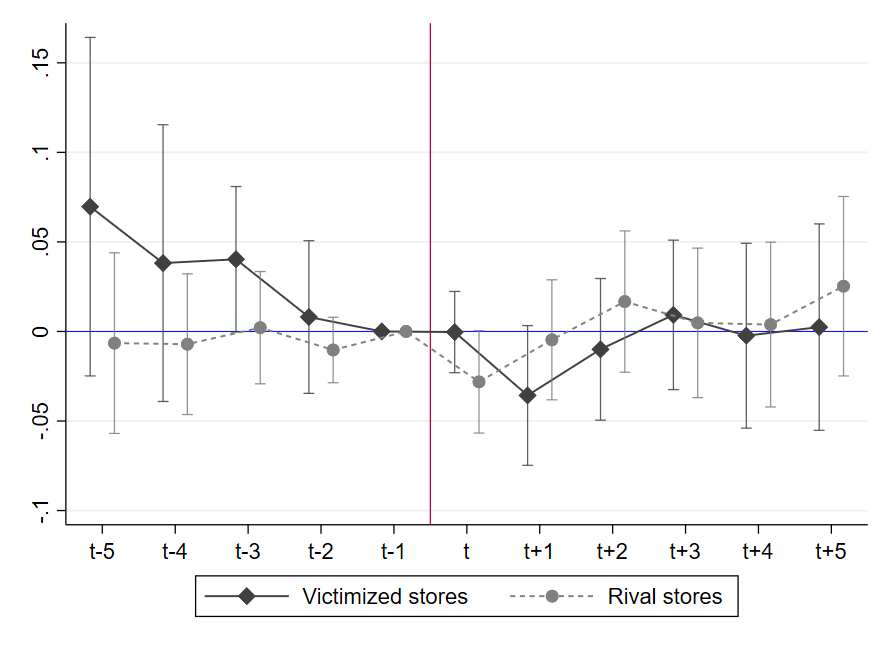

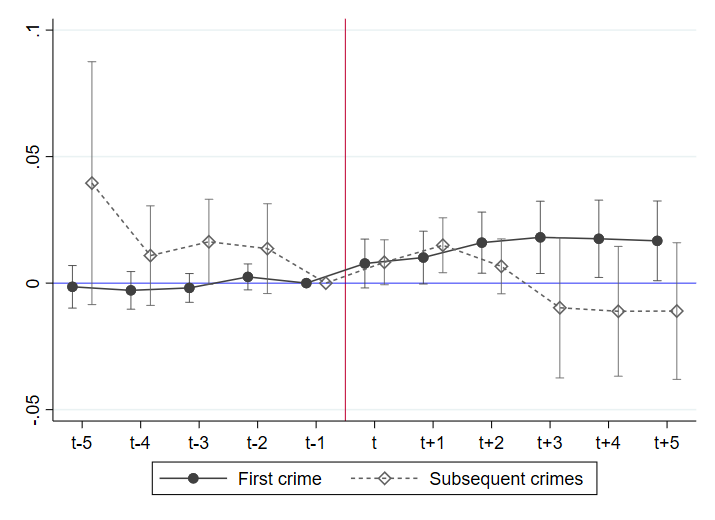

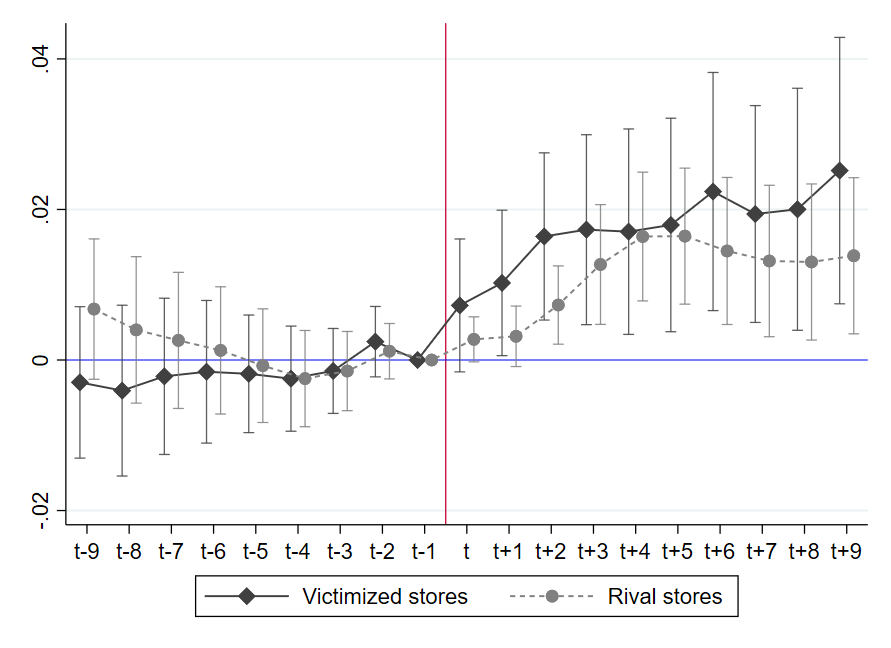

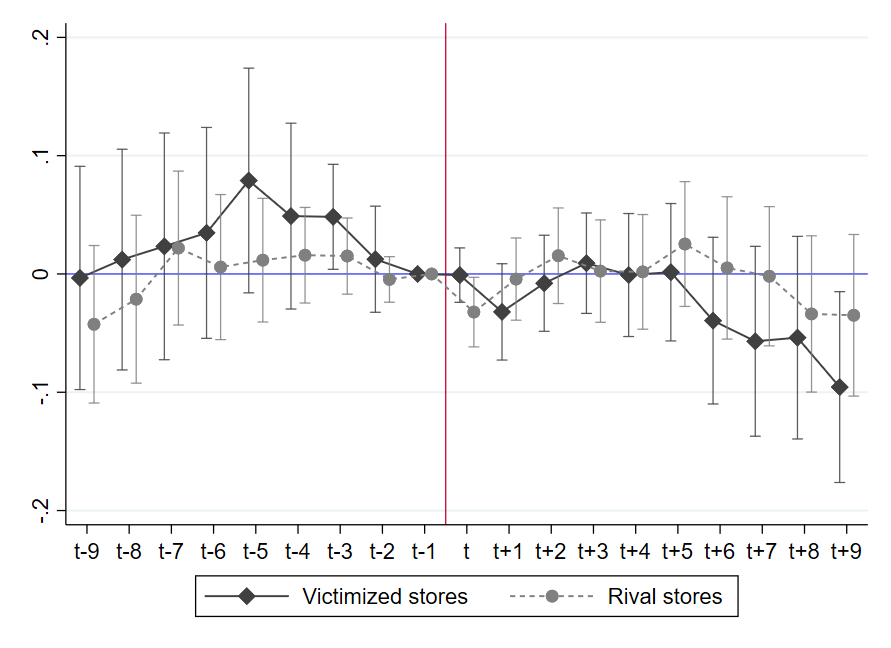

Figure 3(a) shows the estimated price level effects for victimized and rival stores according to our main specification. We report cumulative effects, i.e. the effect on the price level (in percent) relative to the baseline period in (see Section 4 for details).292929The estimated distributed lag coefficients are equivalent to the change in price level effects from one period to the next are equivalent (see e.g. Renkin et al.,, 2022; Leung,, 2021). For both groups, the figure shows no significant pre-treatment effects. In the month of a retail crime incident, however, prices at victimized stores increase and continue to rise for three months. Four months after the crime, prices at victimized stores are 1.8% higher compared to the month before the crime and stay at this higher price level for the following months. In contrast, rival stores show no price increase in the month that a retail crime hits a nearby store. Nevertheless, two months after crime incidents at victimized stores, a very similar price increase can be observed at rival stores. Four months after the crime, rival store prices are 1.6% higher than the month before the crime, and the effect is not statistically significantly different from that at victimized stores. Overall, our estimates reveal that retailers in the Washington state cannabis market increase their prices following retail crime incidents.

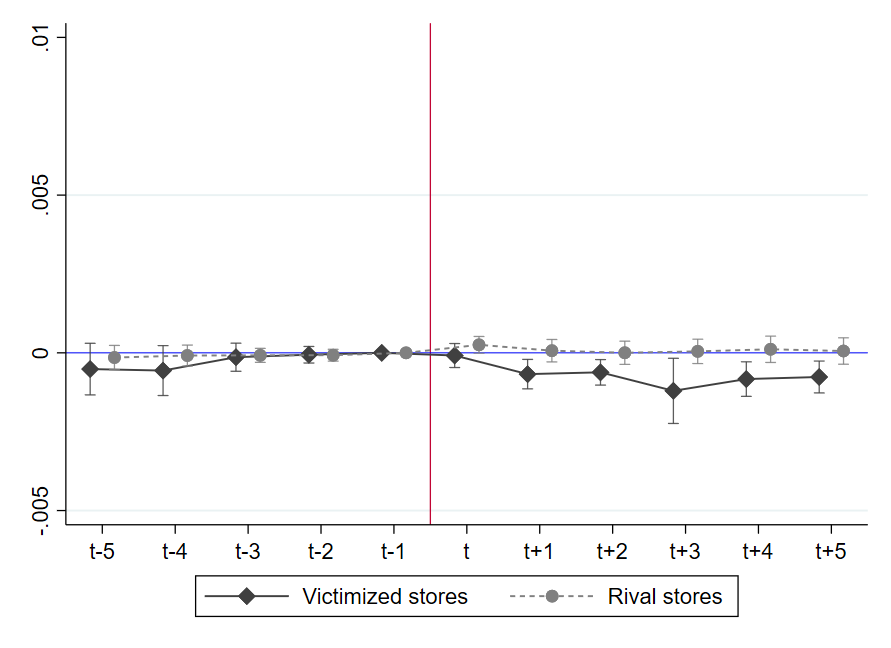

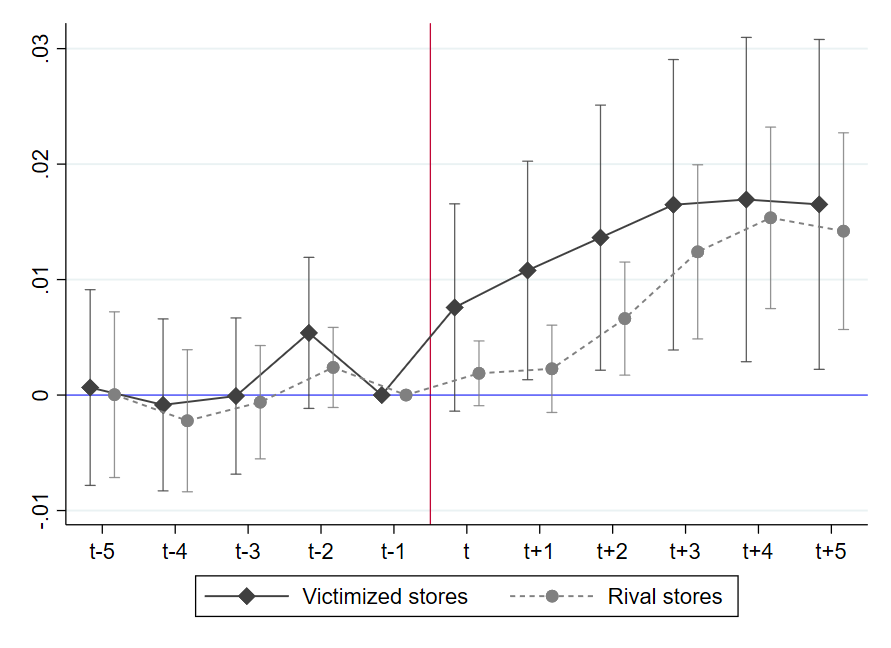

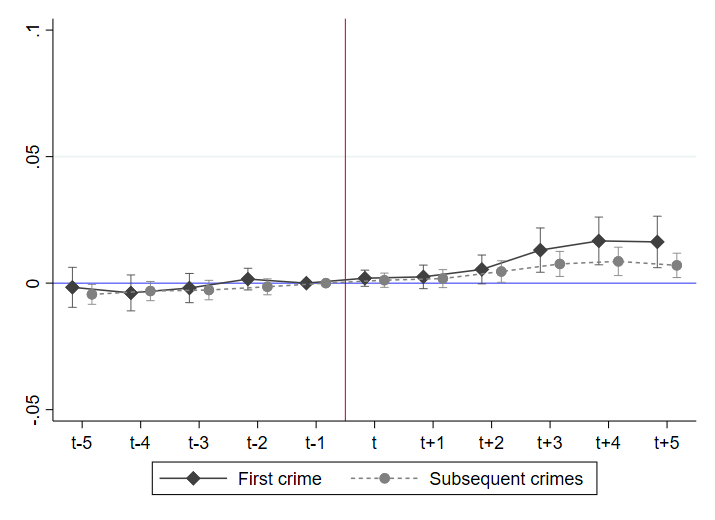

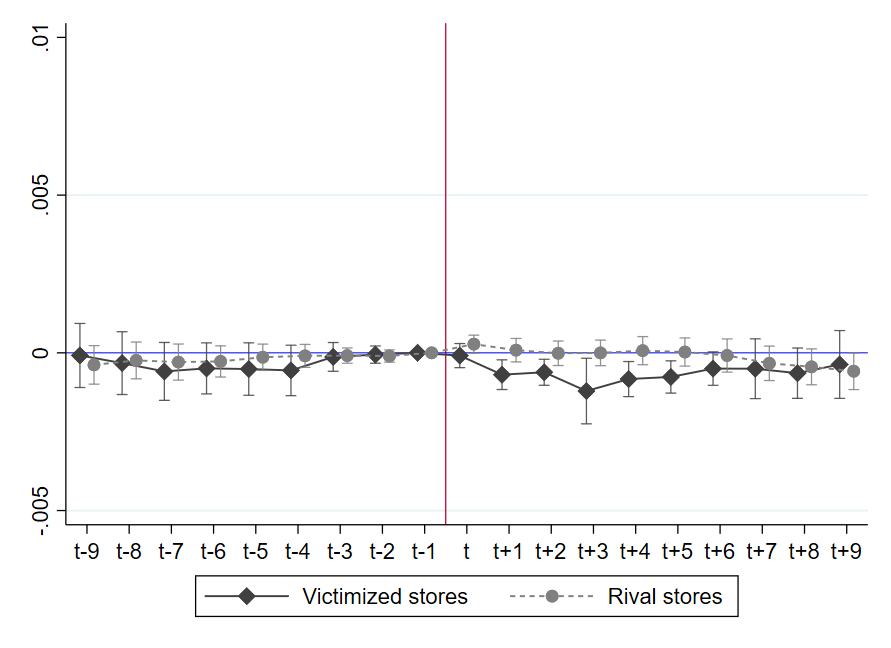

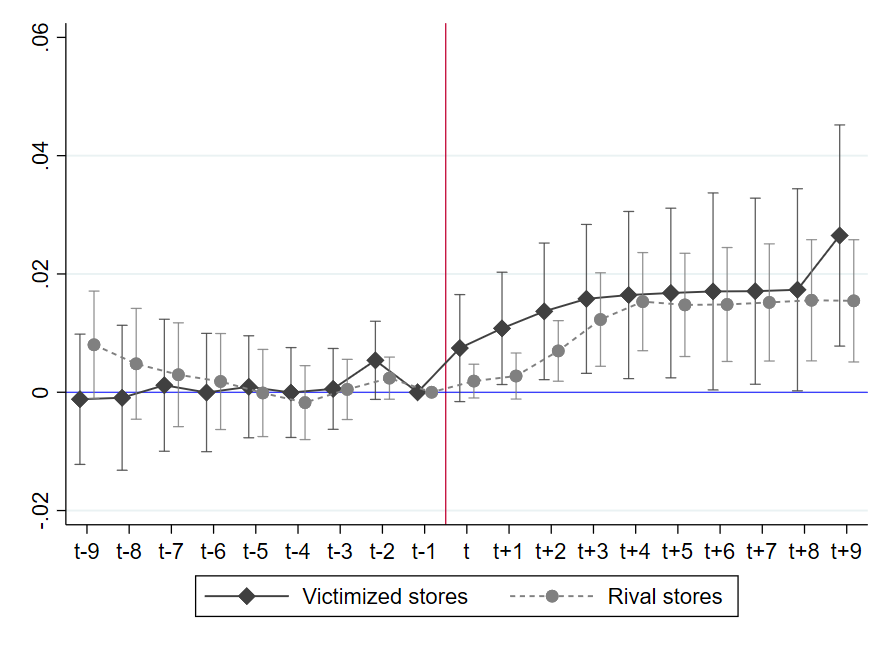

Notes: Each panel shows the cumulative treatment effects () months after a crime on different outcomes, along with corresponding 90% confidence intervals based on standard errors clustered at the store level. Coefficients are interpretable as percent increases in outcome levels relative to the month before a crime incident. The black line depicts the cumulative effects of crime on outcomes at victimized stores, while the grey line represents rival stores. The dependent variables are: store-level price index (Panel (a)), store-level quantity index (Panel (b)), store-level wholesale cost index (Panel (c)), and store-level margins index (Panel (d)).

Figure 3(b) presents estimates from equation 2 when using the quantity index as the dependent variable. Pre-incident estimates are insignificant at the 10% level for both store types. Our findings indicate a 3% (but insignificant) decrease in quantity sold for both victimized and rival stores immediately after a crime incident. However, the quantity sold returns to pre-incident levels within a month. This finding speaks against demand substitution out of victimized and into rival stores due to, e.g., stigmatization or personal safety concerns on the part of consumers. Moreover, our findings suggest that demand in our setting is relatively inelastic. This is consistent with high search costs and aligns with previous evidence from Hollenbeck and Uetake, (2021). Finally, the results indicate that our estimated price effects are not confounded by underlying changes in demand.

Figure 3(c) shows estimates with the wholesale cost index as the dependent variable. Estimated monthly treatment effects on wholesale costs are statistically significant but economically small, at approximately 0.1%. These negligible effect sizes imply that retailers do not meaningfully adjust their wholesale expenditures in response to retail crime incidents, and also indicate no major reaction from wholesalers to the crime incidents at their client stores. Additionally, these results provide reassurance that changes in COGS are not a confounder driving the observed retail price effects in Figure 3(a). Pre-incident effects show no discernible divergence in the evolution of wholesale costs between the treatment and control groups.

Lastly, we explore the impact of retail crime on retail margins, which serve as a proxy for retailers’ profits. Given the absence of effects on wholesale costs, the treatment effects on retail margins expectedly reflect the estimated price effects, as shown in Figure 3(d). Unfortunately, we do not observe detailed profit data for retailers, which could provide further insights into other factors driving the price effects.

5.2 Heterogeneity analysis

In this subsection, we conduct two main heterogeneity analyses to gain more insight into the role of market structure in crime pass-through.

Chain vs Independent stores

We first examine whether crime pass-through differs between chain and independent stores. One concern is that chain size may correlate with profitability and is therefore endogenous. This is less of a concern in our setting for two reasons. First, when the market was initially created, the LCB randomly assigned licenses to applicants, reducing self-selection bias for store types Hollenbeck and Giroldo, (2022). Second, the number of licenses is capped by the LCB, meaning that profitable firms cannot easily increase their chain size.

We define chains as stores belonging to firms running three or more stores and consider all other stores as independent. Of the 508 stores in our sample, 330 are independent and 181 belong to a chain. We split our sample into two subgroups according to this definition and estimate our main specification separately for each subgroup. Table 4 reports the results of the subsample analyses. Columns 1 and 2 show that among victimized stores, the pass-through of crime is large at independent stores but small and not statistically significantly different from zero at chain stores. Columns 5 and 6 show that the same pattern holds among rival stores. Results are similar when defining independent as single-store firms and chains as firms with two or more stores (see Appendix Table 11). Our findings align with studies showing little within-chain price adjustments to local conditions (Hitsch et al.,, 2021; DellaVigna and Gentzkow,, 2019) and suggest that owning multiple stores may serve as insurance against negative cost shocks, possibly due to better financing conditions or high returns to scale (Hollenbeck and Giroldo,, 2022). Alternatively, or as an additional mechanism, the results suggest that chains may already have more effective crime prevention strategies or insurance plans in place that require less adjustment, supporting the notion of firm learning.

Market concentration

Next, we investigate whether effects vary by market concentration. Concentration is endogeneous if profitability affects market entry. However, since the LCB caps the number of cannabis store licenses and distributes them according to population density, profitability does not directly affect concentration in our setting. We consider each store in our sample (including non-treated stores) as the focal point of its own market comprising the set of stores (including the focal store) within a 5-mile radius. We calculate the Herfindahl–Hirschman Index (HHI) for each market in the sample, and we then divide the sample into two subgroups for stores above and below the sample median HHI. A high HHI implies high concentration and thus low market competition. We provide descriptive statistics on the HHI in Table 9.

We estimate our main specification on each subsample to test whether crime pass-through differs between stores above and below the median HHI. We report results in Table 4. Columns 3 and 4 show that among victimized stores, crime causes prices to increase 3.1% in low-concentration markets while in high-concentration markets the effect is not significantly different from zero. Moreover, the difference in effect sizes is statistically significant. This pattern carries over to rival stores, though the difference in effects sizes between low and high market concentration is less pronounced. Prices in low-concentration markets increase 2.2% while in high-concentration markets they increase 1.1%.

The heterogeneous pass-through rates may be attributable to differences in rural and urban markets. The LCB awards licenses to counties according to population density, and market concentration likely decreases with population density. Since wages are higher in more populated areas, and crime may induce a labor cost shock, it is plausible that crime induces a larger cost shock at stores in densely populated urban areas. In a robustness check, we find that once rural-urban differences in market concentration are accounted for, the difference in effect size between low- and high-concentrated markets becomes slightly smaller but largely persists (see Appendix Table 11). We explore this issue in more detail in Appendix C.

These results are in line with standard imperfect competition models (e.g. the canonical Cournot model) which predict that when competition increases, prices become more sensitive to marginal costs and pass-through rates rise. However, if marginal cost pass-through rates exceed unity, predictions regarding the relationship between competition and pass-through rates can change (Weyl and Fabinger,, 2013; Miller et al.,, 2017). This is an important consideration in our context, as we find marginal cost pass-through rates greater than one in Section 7. Moreover, Ritz, (2024) show that the positive relationship between competition and pass-through rates is sensitive to the shape of the cost function. Empirical findings on the relationship between competition and cost pass-through rates are similarly mixed. Some studies report that pass-through rates increase with competition (Cabral et al.,, 2018; Genakos and Pagliero,, 2022), while other studies find the opposite (Doyle Jr and Samphantharak,, 2008; Miller et al.,, 2017).

| Victimized | Rivals | |||||||

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

| Indep. stores | Chain stores | Low concentration | High concentration | Indep. stores | Chain stores | Low concentration | High concentration | |

| 0.010 | 0.0014 | 0.012 | 0.0019 | 0.0025 | 0.0033 | 0.0019 | 0.0038 | |

| (0.0078) | (0.0027) | (0.0097) | (0.0027) | (0.0022) | (0.0029) | (0.0026) | (0.0023) | |

| 0.021** | 0.0063 | 0.024** | 0.0075 | 0.010*** | 0.00062 | 0.0077 | 0.0062* | |

| (0.0096) | (0.0050) | (0.011) | (0.0060) | (0.0037) | (0.0048) | (0.0049) | (0.0033) | |

| 0.024** | 0.0035 | 0.031** | 0.0011 | 0.024*** | 0.0042 | 0.022*** | 0.011* | |

| (0.012) | (0.0056) | (0.013) | (0.0088) | (0.0060) | (0.0076) | (0.0073) | (0.0063) | |

| -0.0016 | -0.0013 | 0.0015 | -0.0059 | -0.0030 | -0.00014 | 0.00049 | -0.0053 | |

| (0.0063) | (0.0055) | (0.0063) | (0.0067) | (0.0050) | (0.0075) | (0.0073) | (0.0058) | |

| 15,355 | 14,929 | 15,197 | 15,087 | 13,863 | 11,657 | 13,231 | 12,289 | |

Notes: Each column shows the cumulative treatment effects on store price levels for different subsamples zero, two, and four months after a crime, along with the sums of pre-treatment coefficients. Coefficients are interpretable as percent increases in outcome levels relative to the month before a crime incident. The first four columns use victimized stores as the treatment group, and the last four columns consider rival stores. Columns 1 and 5 show effects for independent stores (i.e., owned by firms running one or two stores only), while columns 2 and 6 show effects for stores owned by firms running at least three stores. For the other columns, the Herfindahl-Hirschman Index is calculated for the market around each store (including non-treated stores) within a 5-mile radius, and the sample is split according to the median market concentration across all markets. Columns 3 and 7 show effects for treated stores in markets with below median concentration, and columns 4 and 8 for treated stores in markets with above median concentration. Standard errors of the sums are clustered at the store level and shown in parentheses. ∗ , ∗∗ , ∗∗∗ .

6 Threats to identification, robustness checks and alternative specifications

In this section, we address potential endogeneity concerns in our setting. We present various alternative specifications, robustness checks and placebo tests to corroborate the validity of our results.

Endogenous treatment timing and parallel trends

The key identifying assumption of our empirical strategy is the parallel trends assumption. This implies that store-level prices in the control and treatment groups would have followed a common trend in the absence of retail crime incidents.

In our framework, we account for all time-invariant factors that could influence treatment, such as store location and average revenues, through the inclusion of store-fixed effects. Similarly, we account for all time-varying factors that equally apply to all stores, such as the seasonality of robberies or COVID-19 effects, through the month-year fixed effects. However, the parallel trends assumption can be violated if the timing and location of retail crimes are correlated with changes in our outcome variables. An example is if stores that strongly increase or decrease revenues are more likely to be robbed or burglarized. This is less of a concern with rival stores’ treatment timing. However, it is also possible that changes in policing in certain areas are correlated with revenues in those areas, which could also threaten the causality for our rival store regression.

The first clear indication of the validity of the parallel trends assumption in our setting is the lack of significant pre-trends across all main specifications. Figure 3 shows no pre-treatment differences for prices, quantity sold and wholesale cost between victimized, rival, and control stores. Furthermore, pre-trends remain insignificant for alternative specifications, for instance, if we expand the event window (Figure 12) or when using alternative estimators (Appendix E.1). Additionally, the lack of observable pre-trends supports the validity of the second identifying assumption regarding no anticipation. If store owners anticipate robberies, we would expect to see changes in the outcome variables before the actual events.

To further corroborate our findings, we conduct placebo tests, in which we run our main regression analysis with the actual treatment timing shifted by 12 months in both directions. This approach tests for the presence of non-parallel trends or seasonal variations not fully addressed by our fixed effects. The placebo test results, detailed in Appendix Table F.14, reveal no discernible patterns, reinforcing our confidence in the validity of the parallel trends assumption and our empirical model.

Alternative estimators

The stacked DiD estimator offers advantages over related estimators due to its flexibility for applying rules for clean controls based on geographic criteria (for more details, see Appendix E). Nevertheless, other estimators may have advantages in terms of efficiency and comparability to other studies. To assess whether our findings are sensitive to the choice of estimator, we estimate dynamic treatment effects using three alternative estimators: i) the canonical two-way fixed effect DiD estimator ii) the imputation estimator developed by Borusyak et al., (2024) (BSJ); and iii) the estimator proposed by Callaway and Sant’Anna, (2021) (CS).303030The canonical TWFE estimator is prone to biases under staggered treatment adoption. The BSJ and CS estimators address these biases in a different way than the Stacked DiD estimator. Following our main approach, we first estimate a distributed lag model (Equation 2) for the designated event window and then calculate cumulative treatment effects using the last pre-treatment period as our baseline. We discuss the details of the alternative estimators in Appendix E.1.

The dataset used for alternative estimators includes all stores, which means the control group may comprise stores within 30 miles of victimized stores. Positive price effects at these nearby stores, as suggested by our main results, would thus imply that treatment effects are attenuated in these models. Restricting the sample to stores more than 30 miles away from any treated stores reduces the number of (potential) control stores from 329 to just 78 stores, highlighting the benefits of using the stacked DiD framework in our setting.

Table 13 displays the cumulative treatment effects at , , and for the alternative estimators. As expected, the effects are slightly smaller than in our main specification—about 1.5% for victimized stores and 1% for rival stores, except for the CS specification, which yields higher effects for victimized stores. However, in the majority of these alternative specifications, treatment effects are statistically significant and not different from our main specification, demonstrating that our findings are not driven by the choice of our estimator.

Alternative definitions of unaffected local markets and rival stores

When defining clean control stores, we balance comparability with treated stores against potential biases from treatment spillovers, as discussed in Section 4. To investigate whether our estimated effects are sensitive to our definition of clean control stores, we estimate our model using alternative definitions of unaffected local markets and rival stores.

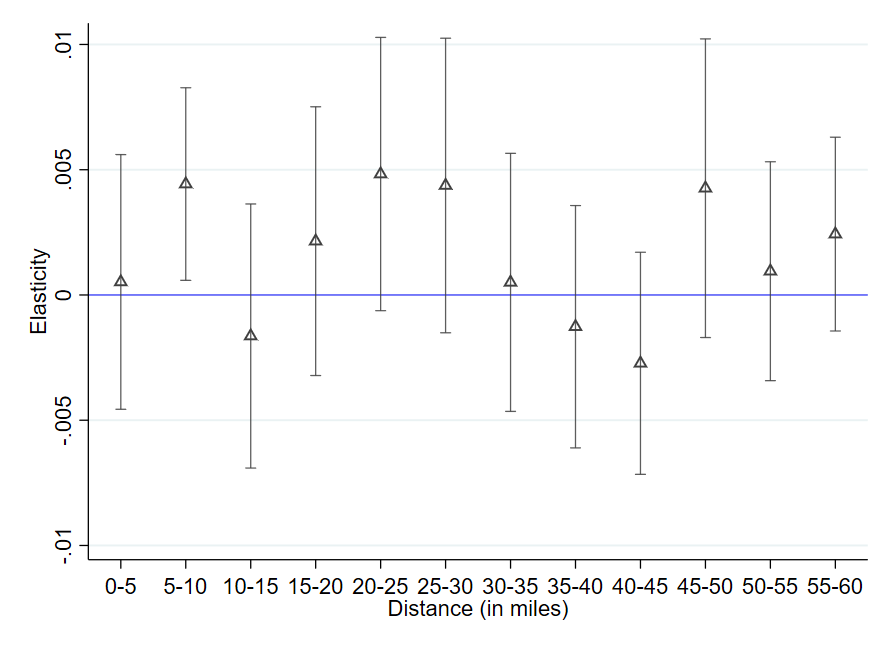

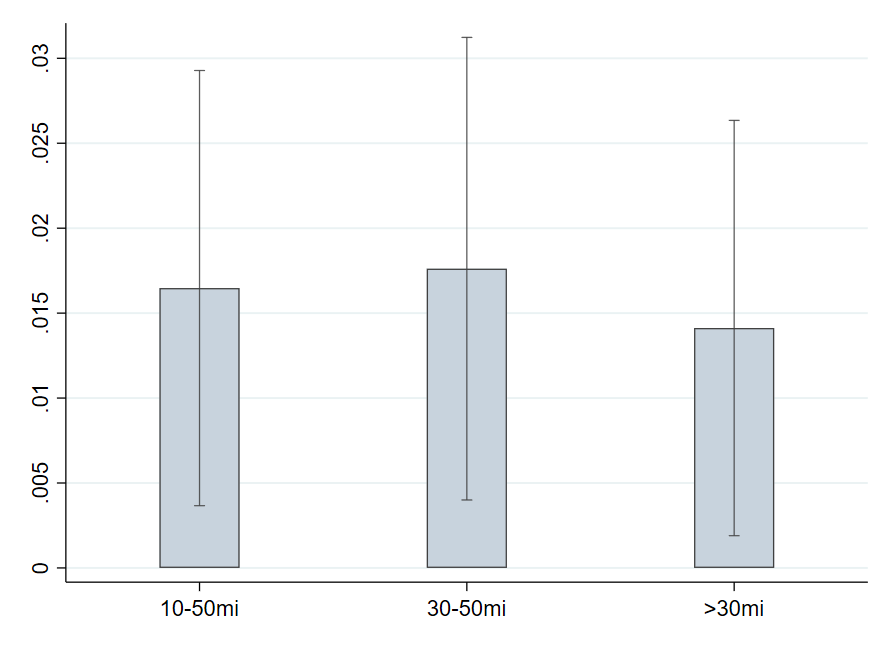

First, we expand the area of unaffected local markets along two dimensions: i) including all stores within 10 and 50 miles of victimized stores; ii) including all stores that are located more than 30 miles away from victimized stores. Figures 13(a) and 13(b) in Appendix F show that, as anticipated under positive spillover effects, treatment effects fall slightly to around 1.6% (victimized) and 1.3% (rivals) when expanding the inner boundary, but remain statistically significant. A similar picture emerges if we include more distant stores in the control group, as treatment effects slightly decrease but remain statistically significant.

Next, we inspect the sensitivity of our results to expanding the inner ring that defines rival stores. We report results in Figure 13(c) in Appendix F. Interestingly, the treatment effect remains roughly constant when we include all stores within a 10-mile radius as rivals, and only declines for stores located further away. These results suggest that spillover effects may apply to a larger set of stores than initially thought. Furthermore, the declining treatment effect beyond the 10-mile radius indicates that spillovers decrease with distance from the crime incident. This provides supportive evidence for our choice of control stores, as it suggests that stores located further away from victimized stores are less likely to be contaminated by spillovers.

Additional Robustness checks

We conduct a number of additional robustness checks to rule out other factors potentially driving our findings. We present the results of these robustness checks in Table 5. In both panels, Column 1 reproduces our baseline specification from Figure 3(a). Column 2 shows that our results are similar when we include control variables such as county population, the local house price index (at the three-digit zip code level), and average county wage. These control variables absorb variation in prices stemming from local business cycles, population growth, or fluctuations in the housing market (Stroebel and Vavra,, 2019).

Since our price indexes are store-level aggregations of diverse sets of products and product categories, it is important to check whether results hold for a narrower set of homogeneous products. Therefore, in Column 3 we restrict the sample to products belonging to the usable marijuana product category and convert all prices to price per gram.313131All products in the Usable Marijuana product category contain information on the package weight measured in grams. This enables us to convert prices into prices per gram for this product category. Effect sizes are larger using this price index, though we show in Appendix 5.2 that this is due to larger effects for usable marijuana compared to other product categories. In Column 4 we winsorize inflation rates below the bottom 0.5 percentile and above the 99.5 percentile to show that our results are not driven by outliers.

Our price indexes are constructed with weights based on calendar year revenue shares (see Section 3). To ensure that our main effects are not an artifact of this weighting scheme, in Column 5 we use indexes constructed with weights based on the fiscal year running from July through June. Estimates are similar to our baseline specification, though for victimized stores the standard errors are larger at higher lags.