Onsager-Machlup functional for stochastic differential equations with time-varying noise

Abstract

This paper is devoted to studying the Onsager-Machlup functional for stochastic differential equations with time-varying noise of the -Hölder, ,

Our study focuses on scenarios where the diffusion coefficient exhibits temporal variability, starkly contrasting the conventional assumption of a constant diffusion coefficient in the existing literature. This variance brings some complexity to the analysis. Through this investigation, we derive the Onsager-Machlup functional, which acts as the Lagrangian for mapping the most probable transition path between metastable states in stochastic processes affected by time-varying noise. This is done by introducing new measurable norms and applying an appropriate version of the Girsanov transformation. To illustrate our theoretical advancements, we provide numerical simulations, including cases of a one-dimensional SDE and a fast-slow SDE system, which demonstrate the application to multiscale stochastic volatility models, thereby highlighting the significant impact of time-varying diffusion coefficients.

keywords:

[class=MSC]keywords:

, ††thanks: corresponding author..

Statements and Declarations

-

•

Ethical approval

Not applicable. -

•

Competing interests

The authors have no competing interests as defined by IOP PUBLISHING LTD, or other interests that might be perceived to influence the results and/or discussion reported in this paper. -

•

Authors’ contributions

X. Zhang wrote the main manuscript text and prepared figures 1-3. Y. Li provided ideas and explored specific research methods. All authors reviewed the manuscript. -

•

Funding

The second author was supported by National Natural Science Foundation of China (Grant No. 12071175) -

•

Availability of data and materials

Not applicable.

1 Introduction

In the field of stochastic dynamical systems, it is crucial to understand how systems transition between metastable states. This involves studying Stochastic Differential Equations (SDEs) to identify deterministic and significant quantities such as solution paths, mean exit time, and escape probability. An essential tool in this context is the Onsager-Machlup function, which serves as a deterministic quantity used to characterize the most probable transition paths between metastable states in a system.

The concept of the Onsager-Machlup function was initially proposed by Onsager and Machlup [19, 16] in 1953, where they defined it as the probability density functional for a diffusion process characterized by linear drift and constant diffusion coefficients. Following this foundational work, Tizsa and Manning [23] extended the application scope of the Onsager-Machlup function to nonlinear equations in 1957. In parallel, Stratonovich [20] introduced a rigorous mathematical approach in the same year, significantly enriching the theoretical underpinnings of the Onsager-Machlup function.

The Onsager-Machlup functional for SDEs driven by Brownian motion has been the subject of extensive research, as documented in numerous studies [8, 21, 22, 17, 14, 3]. In recent years, Moret and Nualart [18] studied the Onsager-Machlup functional of SDEs driven by fractional Brownian motion. Here, hurst index is divided into two situations: and ; Chao and Duan [4] derived the Onsager-Machlup function for a class of stochastic dynamical systems under (non-Gaussian) Lévy noise as well as (Gaussian) Brownian noise, and examined the corresponding most probable paths; Li and Li [13] demonstrated that the -limit of the Onstage-Machlup functional on the space of curves is the geometric form of the Freidlin-Wentzell functional in a proper time scale; Du et al. [6] proved that as time approaches infinity, an unbounded OM functional minimum sequence contains a convergent subsequence in the curve space, and the graph limit of this minimum subsequence is the extremum of the action functional. And based on this, a geometric minimization algorithm for energy climb is proposed; Liu et al. [15] obtained the Onsager-Machlup functional for McKean-Vlasov SDEs in a class of norms that dominate .

Nevertheless, there has been few research on SDEs where the diffusion coefficients are not constants but vary over time. Bardina et al. [2] explored additive noise in SDEs, involving the diffusion term coefficient , where is a non-negative bounded linear operator but not depending on time . Coulibaly-Pasquier [5] made the computation of the Onsager-Machlup functional of an inhomogeneous uniformly elliptic diffusion process, and provided the application of ball probability. Such observations significantly fuel our motivation to explore the Onsager-Machlup functionals for SDEs with time-varying noise in the of the -Hölder,

| (1) |

where and , represents the space of second derivative continuous bounded mappings from to , is an -dimensional Brownian motion.

This paper is devoted to deriving the Onsager-Machlup functional for SDEs driven by time-varying noise, covering both -dimensional and -dimensional cases. The 1-dimensional scenario, due to its favorable properties, enables us to achieve superior results under a wider range of conditions. Conversely, the analysis in the higher-dimensional context demands careful matrix analysis and computations, necessitating stricter conditions on the coefficients to derive meaningful outcomes. Ultimately, we successfully derive the Onsager-Machlup function, maintaining its interpretation as a Lagrangian function. This achievement enables us to delineate the most probable transition paths surrounding smooth trajectories within diffusion processes.

The challenge of this study lies in the diffusion coefficient in SDEs being tied to the time variable . In the -dimensional case, we draw inspiration from [18], define a new norm, and prove its measurability. To apply the Girsanov transformation, it is essential to ensure that is an invertible matrix for all . Subsequent analysis and computations leverage techniques such as Taylor expansion, matrix trace, and martingales. Through extensive estimation, we ultimately achieve the desired functional.

The structure of the paper is as follows. In Section 2, we collect some known notions and facts. Namely we give the definitions of measurable norm and Onsager-Machlup functional, and introduce several important technical lemmas and theorems. In Section 3, we study the Onsager-Machlup functional for -dimensional SDEs. In Section 4, we further study the Onsager-Machlup functional for -dimensional SDEs. In Section 5, we test some specific examples to illustrate our results.

2 Preliminaries

2.1 Approximate limits in Wiener space

In this section, we recall some fundamental definitions and results concerning approximate limits in Wiener space. Specifically, we focus on the measurable semi-norm, which pertains to the exponentials of random variables in the first and second Wiener chaos (reference [11]).

Let be a Brownian motion (Wiener process) defined in the complete filtered probability space . Here, represents the space of continuous functions vanishing at zero, and denotes the Wiener measure. Let be a Hilbert space and be the Cameron-Martin space defined as follows:

The scalar product in is defined as follows:

for all . Let be an orthogonal projection with and the specific expression

where is a set of orthonormal basis in . In addition, we can also define the -valued random variable

where does not depend on .

Definition 2.1.

We say that a sequence of orthogonal projections on is an approximating sequence of projections, if and converges strongly to the identity operator in as .

Definition 2.2.

We say that a semi-norm on is measurable, if there exists a random variable , satisfying a.s, such that for any approximating sequence of projections on , the sequence converges to in probability and for any . Moreover, if is a norm on , then we call it a measurable norm.

For proving the measurability of the semi-norm defined in this paper, it is necessary to introduce the following lemma (see [10]).

Lemma 2.3.

Let be a nondecreasing sequence of measurable semi-norms. Suppose that exists and for any . In addition, if the limit exists on , then is a measurable semi-norm.

Definition 2.4.

Let be a function defined on . For , we introduce Hölder norm (-Hölder)

where represents the supremum norm of on , and represents the Hölder semi-norm of on . The specific expression is as follows:

Throughout this paper, if not mentioned otherwise, norm denotes Hölder norm .

2.2 Onsager-Machlup functional

For the problem of finding the most probability path of a diffusion process, since the probability of a single path is zero, we can search for the probability that a path is located in a certain region, which may be a tube along a differentiable function. Therefore, the Onsager-Machlup function can be defined as the Lagrangian that gives the most probable tube. We now introduce definitions of Onsager-Machlup function and Onsager-Machlup functional.

Definition 2.5.

Consider a tube surrounding a reference path with initial value and belongs to . Assuming is given and small enough, we estimate the probability that the solution process is located in that tube as:

where denotes the equivalence relation for small enough. Then we call the integrand the Onsager-Machulup function and also call integral the Onsager-Machulup functional. In analogy to classical mechanics, we also refer to the Onsager-Machulup function as the Lagrangian function and the Onsager-Machulup functional as the action functional.

2.3 Technical lemmas and theorems

In this section, we will introduce several commonly utilized technical lemmas and theorems. Throughout this paper, if not mentioned otherwise, represents the conditional expectation of under .

When we derive the Onsage-Machup functional of SDEs with additive noise, the following lemma is the most basic one, as it ensures that we handle each term separately. Its proof can be found in [12].

Lemma 2.6.

For a fixed integer , let be random variables defined on and be a family of sets in . Suppose that for any and any , we have

Then

The following two theorems are fundamental parts of calculating Onsage-Machup functional. Their proofs can be found in [11].

Theorem 2.7.

Let be a measurable norm on . For any , we have

where is defined by Definition 1.

Definition 2.8.

We say that an operator is nuclear, if

for any orthonormal sequences and in .

We define the trace of a nuclear operator as follows:

for any orthonormal sequence in . The definition of trace is independent of the orthonormal sequences we choose. For a given symmetric function , the Hilbert-Schmidt operator is defined as:

is nuclear if for any orthonormal sequence in . When the function is continuous and the operator is nuclear, the trace of has the following expression(see [1]):

Furthermore, when is a continuous covariance kernel in the square , the corresponding operator is nuclear and the expression for its trace is as follows:

Theorem 2.9.

Let be a symmetric function in and let be a measurable norm. If is nuclear, then

The following theorem and lemma are about the probability estimation of Brownian motion balls, which are the basis for the theorem in this article. The proof of the theorem can be found in [7].

Theorem 2.10.

Let be a sample continuous Brownian motion in and set

If , then

exists with

where

Lemma 2.11.

We define the following norms on :

In order to apply the above theorems in this paper, we need the following lemma.

Lemma 2.12.

with is measurable norms and we have .

Proof.

According to the properties of norm and semi-norm, it suffices to show that is a measurable norm and is a measurable semi-norm. Below, we will only prove that is a measurable norm, because the proof of is similar to . Fix and define the continuous linear functional as follows:

Then we can show that represents a measurable norm. Define the measurable norms . In addition, we have the following convergence regarding limits :

and by lemma 2.11, we have

According to Lemma 2.3, is a measurable norm. ∎

3 Onsager-Machlup functional for 1-dimensional SDEs

In this section, we focus on the -dimensional case, thus set and consider to be a -dimensional Brownian motion. We proceed to present our principal findings related to the Onsager-Machlup functional for equation .

Theorem 3.1.

Assume that is a solution of equation , the reference path is a function such that belongs to Cameron-Martin space and the following conditions hold:

-

(1)

and is globally Lipschitz continuous with constant for the second variable;

-

(2)

and there exist , such that for any .

Then, if we use the Hölder norm with , the Onsager-Machlup functional of exists and is given by

| (2) |

where , .

Proof.

Let be the solution for following stochastic integral equation:

where . For convenience, denote . Firstly, let’s consider the relationship between and . Under condition , by Lemma 2.11 we have

Applying Theorem 2.10, we can show that the ratio of to is bounded. Define

| (3) |

where is a constant that is related to and .

Due to , and , the Novikov condition is clearly satisfied. Girsanov theorem implies that is a -dimensional Brownian motion under new probability , which defined by with

So we have

| (4) | ||||

where

For the third term ,

Using that is Lipschitz continuous for the second variable, we have

When , we obtain

| (6) |

Inequality and the boundedness of and imply that

| (7) |

for all .

For the fourth term , applying inequality and the boundedness of , we have

| (8) |

for all .

For the first term , applying Taylor expansion, we have

and when , there exists a constant such that

Hence can be written

Applying Theorem 2.7 to and Lemma 2.12, we have

| (9) |

for all . In order to apply Theorem 2.9 we will express the term as a double stochastic integral with respect to . We have

Define

Hence, , where is the symmetrization of . The operator is nuclear, and its trace can be computed as follows:

By Theorem 2.9 and Lemma 2.12, we have

| (10) |

for all . Finally, we study the behaviour of the term . For any and , we have

| (11) | ||||

Define the martingale . We have estimate about its quadratic variation

for some . Using the exponential inequality for martingales we have

Then, by Lemma 2.11, we have

Applying the latter estimate and taking limits in , if , we have

| (12) |

for all , as and .

4 Onsager-Machlup functional for -dimensional SDEs

In this section, our exploration extends to the -dimensional scenario, with representing an -dimensional Brownian motion. For functions , we introduce the following definitions for spaces and norms:

where , is a set of orthonormal basis in space and denotes the tensor product. Additionally, we assume that represents the inner product between vectors and , while represents the product between matrices and vectors (or matrices) .

To elaborate on the Onsager-Machlup functional for equation , it becomes necessary to further define and .

Definition 4.1.

We define some conditions regarding and :

-

(C1)

and is globally Lipschitz continuous with constant for the second variable;

-

(C2)

, and is positive and bounded, that is, there existing , such that for any ;

-

(C3)

, generalized inverse matrix of , is continuous for any .

Definition 4.2.

Assumming is nondegenerate, that is, for any , we say that is the generalized inverse matrix of the function matrix , if for any . We will denote the generalized inverse matrix as .

Theorem 4.3.

Assume that is a solution of equation , the reference path is a function such that belongs to Cameron-Martin . And assume that and satisfy continuous , and . If we use the Hölder norm with , then the Onsager-Machlup functional of exists and has the form

| (13) |

where , .

Proof.

Similar to the proof method of Theorem 3.1, let be the solution for following stochastic integral equation:

where . For convenience, denote . In the -dimensional case, we can verify that still holds. Due to , and , the Novikov condition is clearly satisfied. Girsanov theorem implies that is an -dimensional Brownian motion under new probability , which defined by with

So we have

| (14) | ||||

where

Under conditions , we can show that is a positive, bounded and continuous function matrix. Note that . Let , we have .

For the second term , we have

Applying Theorem 2.7 to and Lemma 2.6, Lemma 2.12, we obtain

| (15) |

for all .

For the third term ,

Using that is Lipschitz continuous for the second variable, we have

When , we obtain

| (16) |

Inequality and the boundedness of and imply that

| (17) |

for all .

For the fourth term , applying inequality and the boundedness of and , we have

| (18) |

for all .

For the first term , applying Taylor expansion, we have

where is gradient operator. For , we have

Hence, can be written

The term has the same expression as

Due to , we can show that . Using the same method as item yields

| (19) |

for all . In order to apply Theorem 2.9, we will express the term as a double stochastic integral with respect to . We have

Define

Hence, , where is the symmetrization of . According to conditions and , the operator is nuclear, and its trace can be computed as follows:

By Theorem 2.9 and Lemma 2.12, we have

| (20) |

for all . Finally, we study the behaviour of the term . For any and , we have

| (21) | ||||

Define the martingale . We have estimate about its quadratic variation

for some . Using the exponential inequality for martingales, we obtain

Then, by Lemma 2.11, we have

Applying the latter estimate and taking limits in , if yields

| (22) |

for all , as and .

5 Numerical experiments

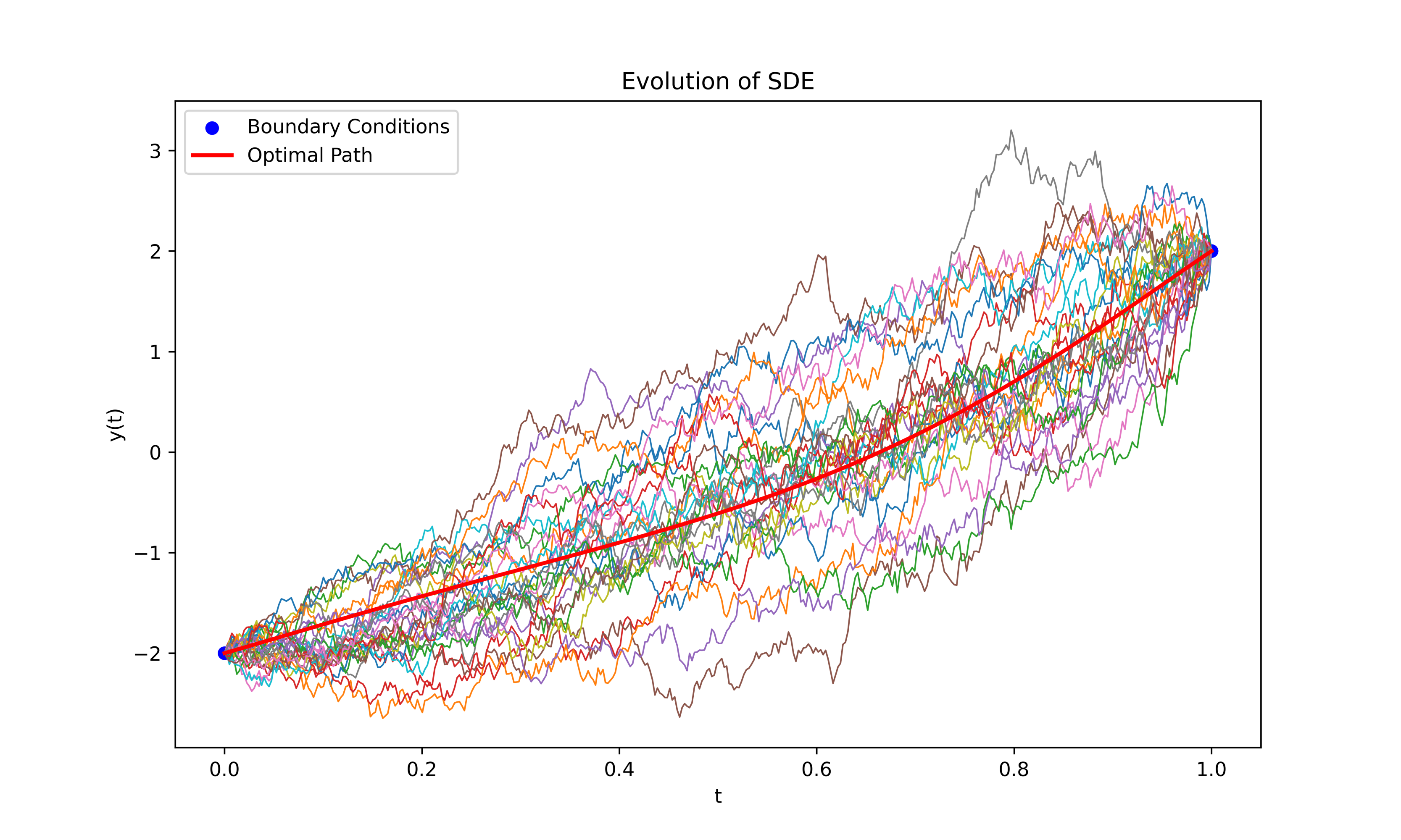

In this section, drawing upon the foundational insights from Theorem 4.3 and Theorem 3.1 of this paper, we illustrate our methodology through examples and numerical simulations for a one-dimensional SDE and a fast-slow SDE system. Specifically, we first calculate the respective equations’ Onsager-Machlup functionals. Then, by minimizing the OM functionals, we determine the most probable pathway between two metastable states. Finally, computer simulations are employed to generate visual representations, validating the accuracy of our theoretical findings.

Example 5.1.

Consider the following -dimensional SDE:

| (23) |

where , . We define and . It is demonstrable that the functions and meet the criteria stipulated by Theorem 3.1. Given ’s properties, the system’s metastable states are identified at and , allowing us to calculate the most probable path between these states.

By Theorem 3.1 we can obtain the Onsager-Machlup functional for :

Then we can find the most probable path for by minimizing the corresponding Onsager-Machlup functional with the help of variational principle. Firsy, we define the Lagrangian :

Then, we can obtain the Euler Lagrange equation,

| (24) |

where

| (25) | ||||

| (26) |

By bringing and into , we can obtain

| (27) |

Under conditions and , according to equation , we obtain the most probable path of system between two different metastable states through numerical simulation (see ).

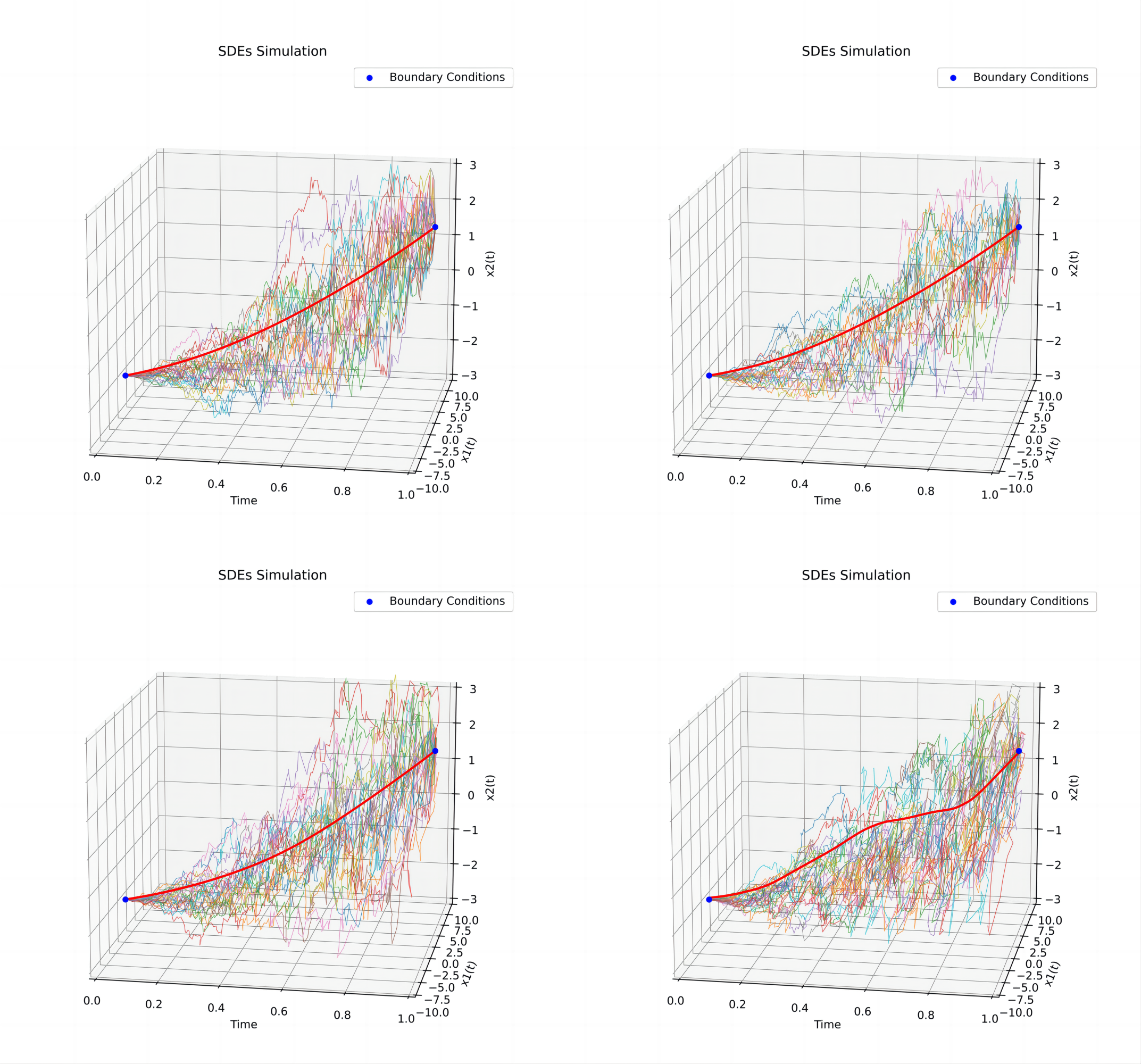

Example 5.2.

The significance of stochastic volatility in the domains of option pricing and asset risk management is well-established. Jean-Pierre Fouque et al. [9] have introduced a spectrum of multiscale stochastic volatility models characterized by dual diffusions operating on distinct temporal scales: one exhibiting rapid fluctuations and the other manifesting more gradual changes. This approach has been demonstrated to enhance model fitting accuracy substantially. In this framework, the price of the underlying asset, denoted by , is represented as the solution to a SDE:

where the volatility process is driven by two diffusion processes fast scale volatility factor and slow scale volatility factor :

where signifies the parameter governing the fast scale, while denotes the parameter for the slow scale. It can be demonstrated that the Onsager-Machlup functional effectively identifies the most probable path for multiscale factor random volatility. Moreover, our analysis extends to more intricate scenarios where factors influencing fast scale fluctuations are interlinked with those affecting slow scale fluctuations. To illustrate this, we present an example involving a -dimensional stochastic differential equation:

| (28) |

where , and is fast scale, is slow scale. We set , , and and are independent -dimensional Brownian motions. It is demonstrable that the functions and meet the criteria stipulated by Theorem 4.3. Given ’s properties, the system’s metastable states are identified at and , allowing us to calculate the most probable path between these states.

By Theorem 4.3 we can obtain the Onsager-Machlup functional for :

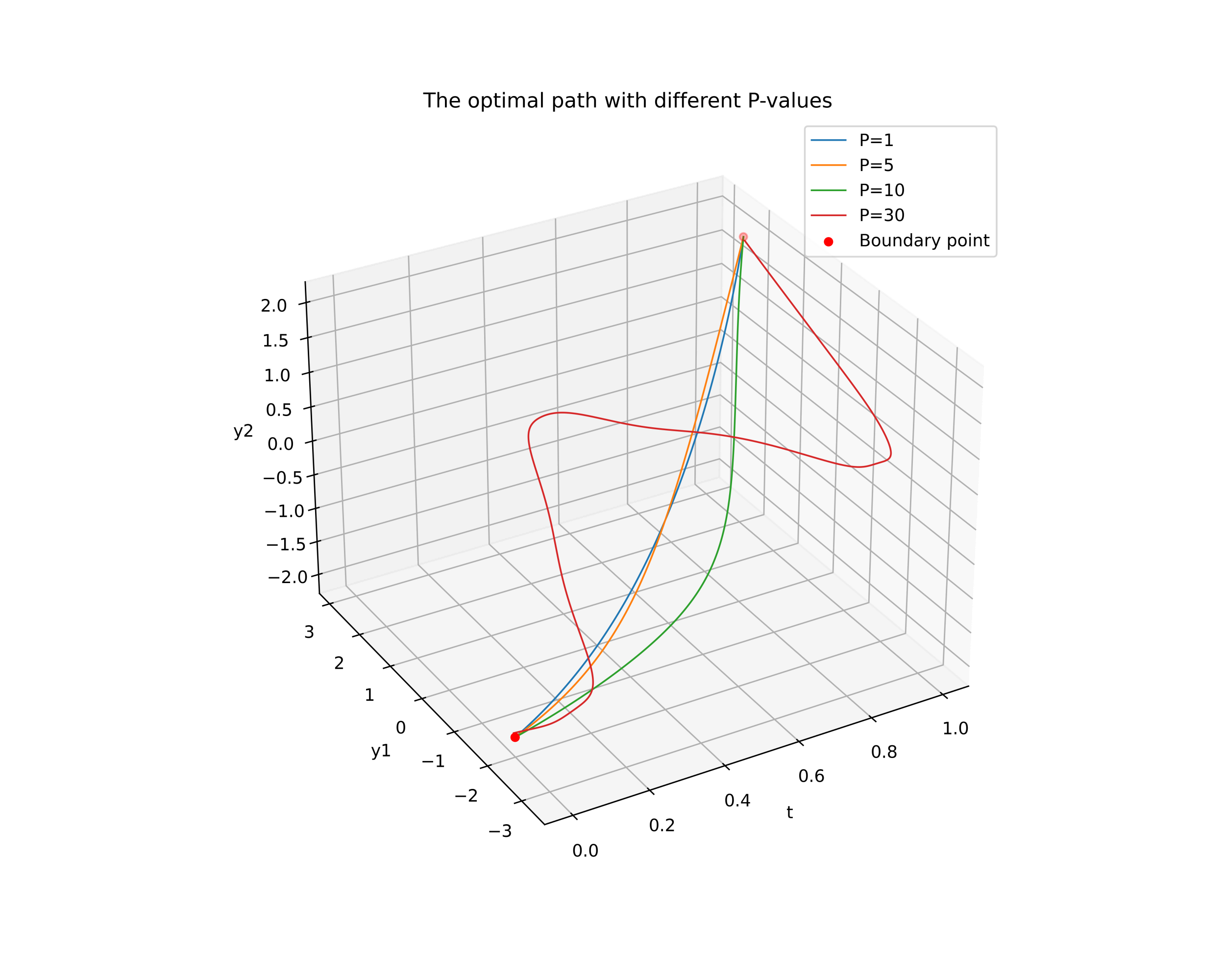

Using the same method as Example 5.1, we can obtain the most probable path of system between two different metastable states (see ). We define . For different scales of and , we can obtain the optimal paths with different -values, which can be referred to for details.

References

- [1] A. V. Balakrishnan. Applied functional analysis, volume No. 3 of Applications of Mathematics. Springer-Verlag, New York-Heidelberg, 1976.

- [2] Xavier Bardina, Carles Rovira, and Samy Tindel. Onsager-Machlup functional for stochastic evolution equations. Ann. Inst. H. Poincaré Probab. Statist., 39(1):69–93, 2003.

- [3] René A. Carmona and David Nualart. Traces of random variables on Wiener space and the Onsager-Machlup functional. J. Funct. Anal., 107(2):402–438, 1992.

- [4] Ying Chao and Jinqiao Duan. The Onsager-Machlup function as Lagrangian for the most probable path of a jump-diffusion process. Nonlinearity, 32(10):3715–3741, 2019.

- [5] Koléhè A. Coulibaly-Pasquier. Onsager-Machlup functional for uniformly elliptic time-inhomogeneous diffusion. In Séminaire de Probabilités XLVI, volume 2123 of Lecture Notes in Math., pages 105–123. Springer, Cham, 2014.

- [6] Qiang Du, Tiejun Li, Xiaoguang Li, and Weiqing Ren. The graph limit of the minimizer of the Onsager-Machlup functional and its computation. Sci. China Math., 64(2):239–280, 2021.

- [7] T. Dunker, W. V. Li, and W. Linde. Small ball probabilities for integrals of weighted Brownian motion. Statist. Probab. Lett., 46(3):211–216, 2000.

- [8] Detlef Dürr and Alexander Bach. The Onsager-Machlup function as Lagrangian for the most probable path of a diffusion process. Comm. Math. Phys., 60(2):153–170, 1978.

- [9] Jean-Pierre Fouque, George Papanicolaou, Ronnie Sircar, and Knut Solna. Multiscale stochastic volatility asymptotics. Multiscale Model. Simul., 2(1):22–42, 2003.

- [10] Leonard Gross. Measurable functions on Hilbert space. Trans. Amer. Math. Soc., 105:372–390, 1962.

- [11] Gilles Hargé. Limites approximatives sur l’espace de Wiener. Potential Anal., 16(2):169–191, 2002.

- [12] Nobuyuki Ikeda and Shinzo Watanabe. Stochastic differential equations and diffusion processes, volume 24 of North-Holland Mathematical Library. North-Holland Publishing Co., Amsterdam; Kodansha, Ltd., Tokyo, second edition, 1989.

- [13] Tiejun Li and Xiaoguang Li. Gamma-limit of the Onsager-Machlup functional on the space of curves. SIAM J. Math. Anal., 53(1):1–31, 2021.

- [14] Shanqi Liu and Hongjun Gao. The Onsager-Machlup action functional for degenerate stochastic differential equations in a class of norms. Statist. Probab. Lett., 206:Paper No. 110009, 9, 2024.

- [15] Shanqi Liu, Hongjun Gao, Huijie Qiao, and Nan Lu. The Onsager-Machlup action functional for McKean-Vlasov stochastic differential equations. Commun. Nonlinear Sci. Numer. Simul., 121:Paper No. 107203, 12, 2023.

- [16] S. Machlup and L. Onsager. Fluctuations and irreversible process. II. Systems with kinetic energy. Phys. Rev. (2), 91:1512–1515, 1953.

- [17] Eddy Mayer-Wolf and Ofer Zeitouni. Onsager Machlup functionals for non-trace-class SPDEs. Probab. Theory Related Fields, 95(2):199–216, 1993.

- [18] Sílvia Moret and David Nualart. Onsager-Machlup functional for the fractional Brownian motion. Probab. Theory Related Fields, 124(2):227–260, 2002.

- [19] L. Onsager and S. Machlup. Fluctuations and irreversible processes. Phys. Rev. (2), 91:1505–1512, 1953.

- [20] R. L. Stratonovič. On the probability functional of diffusion processes. In Proc. Sixth All-Union Conf. Theory Prob. and Math. Statist. (Vilnius, 1960) (Russian), pages 471–482. Gosudarstv. Izdat. Političesk. i Naučn. Lit. Litovsk. SSR, Vilnius, 1960.

- [21] Y. Takahashi and S. Watanabe. The probability functionals (Onsager-Machlup functions) of diffusion processes. In Stochastic integrals (Proc. Sympos., Univ. Durham, Durham, 1980), volume 851 of Lecture Notes in Math., pages 433–463. Springer, Berlin, 1981.

- [22] Tooru Taniguchi and E. G. D. Cohen. Onsager-Machlup theory for nonequilibrium steady states and fluctuation theorems. J. Stat. Phys., 126(1):1–41, 2007.

- [23] Laszlo Tisza and Irwin Manning. Fluctuations and irreversible thermodynamics. Phys. Rev. (2), 105:1695–1705, 1957.