smAdditional References

Mixture Modeling for Temporal Point Processes with Memory

Abstract

We propose a constructive approach to building temporal point processes that incorporate dependence on their history. The dependence is modeled through the conditional density of the duration, i.e., the interval between successive event times, using a mixture of first-order conditional densities for each one of a specific number of lagged durations. Such a formulation for the conditional duration density accommodates high-order dynamics, and it thus enables flexible modeling for point processes with memory. The implied conditional intensity function admits a representation as a local mixture of first-order hazard functions. By specifying appropriate families of distributions for the first-order conditional densities, with different shapes for the associated hazard functions, we can obtain either self-exciting or self-regulating point processes. From the perspective of duration processes, we develop a method to specify a stationary marginal density. The resulting model, interpreted as a dependent renewal process, introduces high-order Markov dependence among identically distributed durations. Furthermore, we provide extensions to cluster point processes. These can describe duration clustering behaviors attributed to different factors, thus expanding the scope of the modeling framework to a wider range of applications. Regarding implementation, we develop a Bayesian approach to inference, model checking, and prediction. We investigate point process model properties analytically, and illustrate the methodology with both synthetic and real data examples.

Keywords: Bayesian hierarchical models; Cluster point processes; Copulas; Dependent point processes; Mixture transition distribution models; Self-exciting processes.

1 Introduction

Temporal point processes are stochastic models for sequences of random events that occur in continuous time, with irregular durations, i.e., intervals between successive arrival times. Throughout this article, event time and arrival time will be used interchangeably for the occurrence time of an event. Data corresponding to point patterns are common in a wide range of applications, such as earthquake occurrences (Ogata, 1988), recurrent events (Cook et al., 2007), financial high frequency trading and orders (Hautsch, 2011), and neural spike trains (Tang and Li, 2021), to name a few. For many point patterns, it is believed that occurrence of a future event depends on the past. This motivates the use of point processes with memory, for example, the Hawkes process (Hawkes, 1971) with full memory, or renewal processes with lagged dependence. The goal of this article is to propose a modeling framework for point processes with high-order memory, relaxing the assumption of independent durations in the traditional renewal process, and including the ability to model duration-clustering behaviors present in applications such as health care (Yang et al., 2018), climatology (Cowpertwait, 2001), and finance (O’Hara, 1995).

As such, this article explores construction of point processes based on models for the durations. For point processes with memory, the collection of dependent durations form a discrete-time stochastic process, and thus a time series model for durations induces conditional densities on the arrival times. Hereafter, we refer to these conditional densities as conditional arrival densities, and notice that they uniquely determine the distribution of the resulting point process (Daley and Vere-Jones, 2003). A common approach to model point process dependence is to specify the conditional intensity of the process, namely, the instantaneous event rate conditional on the process history (e.g., the Hawkes process). In fact, a point process can be equivalently characterized by its conditional intensity or the conditional arrival densities. The latter approach benefits from the vast literature on conditional density modeling. Density-based modeling naturally leads to a well-defined point process, with its conditional intensity derived through a normalization of the conditional arrival densities against the associated survival functions (Daley and Vere-Jones, 2003). Constructing point processes using duration models, usually coupled with a limited memory assumption, can be computationally attractive for inference, as this approach facilitates evaluation of the resulting likelihood. In Section 2, we provide further discussion of the duration-based approach that induces conditional arrival densities, as well as its connection to and difference from the conditional intensity approach.

Statistical models for durations date back at least to Wold (1948) who proposed a first-order Markov chain with an additive model representation. Subsequent developments (Jacobs and Lewis, 1977; Gaver and Lewis, 1980) investigate specific families for the duration process stationary marginal distribution. Since durations are positive-valued, a structure with an additive error process is in general restrictive. A popular class of models in finance is built from the autoregressive conditional duration (ACD) structure (Engle and Russell, 1998). The ACD model assumes independent and identically distributed (i.i.d.) multiplicative errors for the durations, with each multiplicative factor modeled as a linear function of the past factors and durations. Extensions of this class of models provide additional flexibility through the multiplicative factor specification or the error distribution choice. We refer to Pacurar (2008) and Bhogal and Thekke Variyam (2019) for comprehensive reviews. For these models, the conditional intensity function is obtained by scaling the baseline hazard function with multiplicative factors. The baseline hazard corresponds to the error distribution, typically chosen within a parametric family. A restriction of ACD models is their limited capacity to handle non-linear dynamics. Moreover, treating point process realizations as time series affects the distributional properties of likelihood-based estimators (Cavaliere et al., 2024). Regarding computation, the ACD model structure complicates inference when the assumption of high-order memory is necessary, e.g., estimating the correlated multiplicative factors may require approximations (Strickland et al., 2006).

A different approach to modeling duration dependence involves mixture transition distribution (MTD) models (Le et al., 1996), which describe the transition density of a time series as a weighted combination of first-order conditional densities for each one of a specified number of lags. Hassan and Lii (2006) propose a bivariate MTD model for the joint conditional distribution of the duration and a continuous mark, i.e., a random variable associated with the point events. Hassan and El-Bassiouni (2013) extend the model to include a discrete mark. However, these approaches do not investigate point process properties, such as stationarity, and require certain families of distributions for the duration and mark, which can be practically restrictive. Hassan and Lii (2006) point out the difficulties of finding suitable parameterizations to ensure model stability and prediction capability.

In this article, we introduce a class of temporal point processes that builds on the idea of describing duration process dynamics with MTD models. To use traditional high-order autoregressive models, a transformation of the durations or their conditional means is typically needed to handle the dependent, positive-valued durations. This introduces the challenge of inference under a constrained, possibly high-dimensional parameter space. For example, coefficients may need to be restricted to avoid negative-valued durations, and implementing stationarity conditions in practice can be difficult, especially under the assumption of high-order dependence. The aforementioned work that uses MTD models attempts to handle the former issue, albeit under restrictive structures. A key contribution of the present article is the development of an MTD point process (MTDPP) constructive framework that provides flexible modeling of high-order dynamics for the duration process, without parameter constraints. The framework allows for various types of practically relevant point patterns, such as those with self-excitation or self-regulation effects. In addition, it provides an efficient inferential approach, as the MTDPP likelihood evaluation grows linearly with the number of events. Thus, our proposed method is computationally scalable, especially for large point patterns with high-order memory.

Within the MTDPP framework, we provide easily-implemented conditions to construct point processes that correspond to pre-specified families of marginal distributions for the durations. In addition, we obtain a limit result for the mean value function, analogous to that for renewal processes. The resulting class of models has identically distributed, high-order dependent durations, and can be interpreted as a class of dependent renewal processes. This relaxes the assumption of independent durations that may be restrictive in practice. To the best of our knowledge, the proposed model is the first to enable simultaneous modeling of high-order dependence and stationary durations, with computationally efficient inference.

Moreover, we develop an extension to handle duration clustering, based on a two-component mixture for the conditional duration density. In this setting, one component of the mixture corresponds to an independent duration model that accounts for external factors. The other component is an MTDPP that models self-excitation. Point patterns of this type can be found, for instance, in hospital emergency department visits of patients, where long durations may be observed between clusters of multiple visits in short bursts (Yang et al., 2018), and in financial markets where fluctuation can be caused by either external or internal processes (Filimonov and Sornette, 2012). The model extension accounts for the possibility of two different factors that may drive the point process dynamics.

The rest of the article is organized as follows. Section 2 introduces the MTDPP framework, including study of model properties, approaches to constructing various types of MTDPP models, and the extension to cluster point processes. (Technical details and proofs of the theoretical results can be found in the Supplementary Material.) Section 3 develops the Bayesian model formulation, Markov chain Monte Carlo (MCMC) inference, an approach for predicting future events, and a model validation method. In Section 4, we illustrate the proposed methodology with synthetic and real data examples. Finally, Section 5 concludes with a summary and discussion.

2 Temporal MTD point processes

We consider a temporal point process defined on the positive half-line , where is a right-continuous, integer-valued function, denote the event times, and is the indicator function for set . A temporal point process is usually modeled by its conditional intensity, , where , and is the process history up to but not including . The point process has memory if depends on the process history. A Poisson process is an example of a memoryless process. A renewal process has limited memory, in particular, , where is the most recent arrival time before . In contrast, the evolution of a Hawkes process depends on the entire past. Given an observed sequence of arrival times, , the likelihood is

| (1) |

where the last component of (1) corresponds to the point process likelihood’s normalizing term, which is typically analytically intractable, especially when has a complicated form. The normalizing term also implies that building point process models through conditional intensities requires mathematical validation of the proposed intensity function.

An alternative way to characterize the point process probability structure is to use the collection of conditional arrival densities, denoted as , supported on , with associated conditional survival functions . When , and , where is the marginal density of the first event time. Now, the likelihood for point pattern is given by

| (2) |

Similar to (1), the last component of (2) defines the likelihood normalizing term, i.e., the probability of no events occurring in the interval . Since the normalizing term corresponds to a conditional cumulative distribution function (c.d.f.), it may be available in closed-form for particular model formulations for the conditional arrival densities.

Using the collection of conditional densities and survival functions , we can define the hazard functions as , for . The hazard function is naturally interpreted as the conditional instantaneous event rate. Consequently, given the set of arrival times, we can write the conditional intensity of the process as . Since , we can use the form in (2) to recover the likelihood in (1).

Although there is an one-to-one correspondence between modeling the conditional intensity and the conditional arrival densities, the computational costs of the two approaches may be different. Both approaches involve integration to obtain the corresponding normalizing term of the likelihood function, but the integration required for the conditional density approach is more efficient as it involves a conditional c.d.f., which may be readily available in closed form. Moreover, the conditional intensity function form could further complicate likelihood evaluation. For instance, the Hawkes process conditional intensity involves the sum of the excitation function over all points from the past, which poses challenges to model estimation (Veen and Schoenberg, 2008), and the likelihood evaluation cost grows quadratically with the number of observed points. Point process models defined using conditional arrival densities typically assume limited memory, with an autoregressive structure on the durations. The resulting likelihood based on (2) is similar to that of an autoregressive time series, with an extra term that corresponds to a survival function. In general, the likelihood formulation in (2) facilitates model-based inference for temporal point processes with memory.

2.1 Conditional duration density

Consider an ordered sequence of arrival times , and denote the durations by , for . The memory of the process is modeled by specifying an MTD structure for the conditional duration densities. In particular, the density of conditional on the past durations is modeled as a weighted combination of first-order transition densities, each of which depends on a specific past duration, i.e., , where , for all , and . Transforming the conditional density of to that for , for every , creates conditional arrival densities that uniquely determine the point process. The construction is motivated above for durations with . The formal MTDPP definition is given as follows.

Definition 1.

Let be a temporal point process defined on with event arrival times . Denote by the conditional duration density. Then, is said to be an MTD point process if (i) for ; (ii) for , the conditional duration density

| (3) | ||||

(iii) for , the conditional duration density

| (4) |

In both (3) and (4), the weights , for , with . The marginal density and the conditional densities , , are supported on .

Remark 1.

The marginal density and the conditional density define the conditional arrival densities for point pattern , by taking and , , for . Thus, specification of densities and suffices to characterize the probability structure of the resulting MTDPP.

Remark 2.

The two different expressions (3) and (4) for the conditional duration density allow us to study stationarity conditions for the MTDPP (Section 2.2). For brevity, we will use (4) to discuss model properties throughout the rest of the article. Regarding inference, Equation (4) is the relevant expression, since we work with a conditional likelihood. Moreover, the mixture model structure enables an efficient computational scheme for high-order dynamics (Section 3), without constraints on the parameter space.

The specification of the conditional density involves the first-order conditional density , for . Following Zheng et al. (2022), we build from a bivariate positive-valued random vector with joint density and marginals and , by taking as the conditional density of given . In general, there are two strategies to define the joint density , one through specific marginal densities, and the other through a pair of compatible conditional densities (Arnold et al., 1999). The two conditional densities and are said to be compatible if there exists a bivariate density with its conditionals given by and . We note that each strategy has its own benefits depending on the modeling objective. In Section 2.3, we illustrate construction of the conditional densities with various examples for different goals.

An important consequence of using the MTD model for the conditional duration density is a mixture formulation for the implied conditional intensity , where and are the hazard and survival function, respectively, associated with . Similarly, for the th component, we have that , where and are, respectively, the hazard and survival function associated with . We can write the conditional intensity as

| (5) |

with weights , where . Note that and for all . The time-dependent weights, , provide local adjustment, and thus the flexibility to accommodate a wide range of conditional intensity shapes.

In addition to model flexibility, the mixture formulation of guides modeling choice. Each mixture component is a first-order hazard function. If we select such that , for constant , and for all , then , for every . Similarly, we can find a lower bound for . For both cases, if as for all , we have that as . On the other hand, if one of the component hazard functions as , then . Moreover, choosing such that has certain shapes results in particular types of point processes. A point process is said to be self-exciting if a new arrival causes the conditional intensity to jump, and is called self-regulating (or self-correcting) if a new arrival causes the conditional intensity to drop. If monotonically decreases, for all , the resulting MTDPP is self-exciting; see Section 2.3 for details.

2.2 Model properties

We first investigate stationarity for MTDPPs. We focus on conditions for first-order strict stationarity, such that the MTDPP has a stationary marginal density, , for the duration process. The constructive approach to build as the conditional density based on random vector allows us to obtain a stationary marginal density , using the approach in Zheng et al. (2022). We summarize the conditions in the following proposition.

Proposition 1.

Consider an MTD point process with event arrival times , where , . Let be the duration process, such that , and , for . The duration process has a stationary marginal density if: (i) for ; (ii) the density in (3) and is taken to be the conditional density of a bivariate positive-valued random vector with marginal densities and , such that , for all and for all .

We refer to the class of MTDPPs that satisfies the conditions in Proposition 1 as stationary MTDPPs. Compared to renewal processes that have i.i.d. durations, stationary MTDPPs can be interpreted as dependent renewal processes, where the durations are identically distributed, and Markov-dependent, up to -order. In fact, the independence assumption in classical renewal processes is often unrealistic (Coen et al., 2019). For example, in reliability engineering, times to failure between component replacements can be correlated (Modarres et al., 2017). Another example involves the analysis of the recurrence interval distribution for extreme events, which is illustrated in Section 4.2.

For the class of stationary MTDPPs, it is possible to obtain a limit result analogous to that of renewal processes. In renewal theory, the rate of renewals (e.g., component replacement) in the long run corresponds to the rate at which goes to infinity, i.e., . The following theorem summarizes the limit result for stationary MTDPPs.

Theorem 1.

Consider an MTD point process such that its duration process has stationary marginal density with finite mean and finite variance. It holds that, as , almost surely.

Similar to the classical renewal theorem, Theorem 1 provides information about the average renewal rate, the difference being that the MTDPP allows dependence among waiting times between renewals. The mean-value function is defined as , and its asymptotic behavior, i.e., , is of general interest in point process theory. Obtaining function for an MTDPP involves integration with respect to the probability distribution of the point process. Thus, in general, it is not analytically available. However, a useful upper bound for the rate can be obtained for MTDPPs with bounded component hazard functions, as summarized in Proposition 2.

Proposition 2.

Consider an MTD point process with conditional intensity given by (5), such that, for all , the component hazard functions satisfy . Then, .

Proposition 2 implies that the mean renewal rate is no larger than a convex combination of the hazard rates upper bounds. The results of this section can guide modeling choices, enhancing the tools for the construction of MTDPPs presented in Section 2.3.

Finally, note that the structured mixture formulation of the MTDPP conditional duration density distinguishes it from standard finite mixture models. The mixture components of the conditional duration density are ordered by lagged durations, as lag enters into the -th component, for . Such a formulation results in likelihood asymmetry and indicates a single labeling of the components. Thus, identifiability for MTDPP models is generally not as major a challenge as for traditional finite mixture models. Study of identifiability can be conducted on a case-by-case basis; we refer to the Supplementary Material for specific results based on the models introduced in the next section.

2.3 Construction of MTD point processes

We provide guidance to construct MTDPPs, focusing on the conditional density . As discussed in Section 2.1, we derive from a bivariate density , which can be specified through compatible conditionals and , or through marginals and . The former is particularly useful when the objective is to construct self-exciting or self-regulating MTDPPs, by choosing such that its associated hazard function is monotonically decreasing or increasing, respectively. We illustrate this approach in Example 1.

In light of Proposition 1, the strategy of constructing MTDPPs through pre-specified marginals is natural for modeling dependent renewal processes. This strategy is also useful when interest lies in the shape of the marginal hazard function. For example, Grammig and Maurer (2000) point out that it may be more appropriate to consider non-monotonic hazard functions for modeling financial duration processes. We implement this MTDPP construction approach using bivariate copula functions for , illustrated in Example 2.

Example 1: Self-exciting and self-regulating MTDPPs

We build an MTDPP based on a new class of bivariate distributions, which are derived from the pair of Lomax conditionals in Arnold et al. (1999). The Lomax distribution is a shifted version of the Pareto Type I distribution, such that the support is . The density function is given by , for , where is the shape parameter and the scale parameter. Hereafter, we use to denote, depending on the context, either the density function or the distribution for a Lomax random variable (we follow the same notation approach for other distributions).

Proposition 3.

Consider a positive-valued random vector with bivariate Lomax density . Let . Then, the bivariate random vector has conditionals and , and marginals and , where , , , and .

Since is scaled by , we refer to the distribution of as the bivariate scaled-Lomax distribution. The difference with the original Lomax distribution is that the shape parameter of the scaled-Lomax distribution is part of the scale parameter. Both the Lomax and scaled-Lomax distributions have monotonically decreasing hazard functions, and thus they can be used to construct self-exciting MTDPP models.

We start with the bivariate scaled-Lomax densities with parameters . We simplify the parameterization by setting , and letting , which yields , where and , for all . Taking , we obtain the conditional duration density,

| (6) |

Setting , we complete the construction for the scaled-Lomax MTDPP, which is a self-exciting point process.

Based on Proposition 1, if and , for all , the model has stationary duration density . The next result describes the limiting behavior of the stationary scaled-Lomax MTDPP conditional duration distribution.

Proposition 4.

Consider the stationary scaled-Lomax MTDPP with marginal duration density . As , the conditional duration distribution converges in distribution to the exponential distribution with rate parameter .

According to (5), the conditional intensity of the scaled-Lomax MTDPP can be expressed as . For each , the th component of the conditional intensity is bounded above by . Thus, , for any , and, using Proposition 2, .

Finally, we note that if we remove from the scale parameter component in (6), i.e., , then corresponds to the bivariate Lomax distribution of Arnold et al. (1999). If, furthermore, we take , the resulting point process is referred to as the Lomax MTDPP, which is also a self-exciting point process. A self-regulating MTDPP can be constructed through compatible conditionals associated with monotonically increasing hazard functions, such as gamma conditionals; see Arnold et al. (1999) for relevant bivariate distributions.

Example 2: Dependent renewal MTDPPs

Motivated by Proposition 1, we can select a stationary density , and take , for every and for all . Given the desired marginals, what remains is to specify the joint density to obtain . In this example, we introduce the idea of specifying a bivariate copula function to build , which provides a general scheme to construct MTDPPs given a stationary marginal .

Let be the joint c.d.f. of the random vector , and denote by the corresponding marginal c.d.f.s. Given and , there exists a unique copula such that , and the joint density is given by , where is the copula density (Sklar, 1959). Hence, based on a marginal duration density and a copula , we have . The conditional duration density of the resulting MTDPP is

| (7) |

We refer to this class of models as copula MTDPPs. Their conditional intensity in (5) involves hazard function components , where . A closed-form expression for relies on the specific copula function (e.g., a Gaussian copula leads to an analytically intractable ).

For certain copulas, the conditional and marginal densities belong to the same family of distributions. As a particular example, consider the three-parameter Burr density, , for , with shape parameters , , and scale parameter . The corresponding hazard function is monotonically decreasing when , and hump-shaped when . In the Supplementary Material, we derive a bivariate Burr distribution built from Burr marginals and a heavy right tail copula, such that the conditionals are also Burr distributions.

To construct a class of Burr MTDPPs, for each , we specify with the bivariate Burr density such that the marginals are , where . Then, the conditional density, , where . Hence, the conditional duration density of the Burr MTDPP is

| (8) |

with stationary marginal .

The stationary Burr MTDPP model includes as a special case (with ) the Lomax MTDPP with marginal . Moreover, when , it reduces to a model with log-logistic stationary marginal density , for .

2.4 Extension to MTD cluster point processes

In practice, there may exist different factors that drive duration process dynamics. As an example from hydrology, durations of dry spells can be classified into two types, corresponding to cyclonic and anticyclonic weather (Cowpertwait, 2001). A point process model for such data should be able to account for the two weather types, as the lengths of the dry spells may be distinctly different. Here, we extend MTDPPs to MTD cluster point processes (MTDCPPs), based on a two-component mixture model.

Definition 2.

Let be a temporal point process defined on with event arrival times . Denote by the conditional duration density. Then, is said to be an MTD cluster point process if (i) for ; (ii) for , the conditional duration density is given by

| (9) |

where , is a density on , and is the conditional duration density of a self-exciting MTD point process.

Similar to the MTDPP, we use densities and to define the conditional arrival densities of event time , for an observed point pattern , by taking and , , for . When , the MTDCPP reduces to a renewal process; furthermore, if corresponds to the exponential distribution, it becomes a Poisson process. When , the model becomes an MTDPP.

Let and be the hazard and survival functions associated with . The conditional intensity of the MTDCPP, denoted as , extends the mixture form in (5) as follows:

| (10) |

where , for , , and we have that , for , and , for all .

Compared to the MTDPP conditional intensity function, the MTDCPP conditional intensity has an extra term contributed by component , with appropriately renormalized time-dependent weights. If we take an exponential density with rate parameter for , and a Lomax MTDPP for , the resulting model is referred to as the Lomax MTDCPP. Note that we consider the Lomax instead of the scaled-Lomax MTDPP to avoid potential identifiability issues, indicated by Proposition 4.

3 Bayesian implementation

3.1 Conditional likelihood and prior specification

Let be the observed point pattern, with durations , for . We outline the approach to posterior inference for MTDPP models based on a conditional likelihood. The Supplementary Material includes the corresponding details for MTDCPP models.

The point process likelihood can be expressed equivalently using event times or durations . For brevity, we use the latter, and take . Combining (2) and (4), the likelihood conditional on is

where corresponds to the conditional density in (4) with parameters , , , and . The Bayesian model formulation involves priors for and , where the prior for depends on the choice of the component densities , .

We take the weights as increments of a c.d.f. , i.e., , for , where has support on the unit interval. Flexible estimation of the weights depends on the shape of . Thus, we consider a Dirichlet process (DP) prior (Ferguson, 1973) for , denoted as , where is the baseline c.d.f., and is the precision parameter. The DP prior supports general distributional shapes for . Given and , the vector of weights follows a Dirichlet distribution with shape parameter vector , denoted as , where , for . The prior expectation is . We denote this prior for the weights as .

As it is natural to assume that near lagged durations contribute more than distant ones, our default choice for is , with . Such a choice yields a decreasing density for , and thus given the regular cutoff points, the weights exhibit a decreasing pattern in prior expectation. Given , a larger leads to a greater penalization of the weights for distant lags towards zero. The DP precision parameter represents the degree of prior belief; as increases, DP realizations for are less variable around . Our default choice is , which suggests a moderate prior belief in a decreasing pattern for the weights, while allowing for a certain amount of variation. The Supplementary Material includes results from prior sensitivity analysis for the mixture weights, using a simulation study.

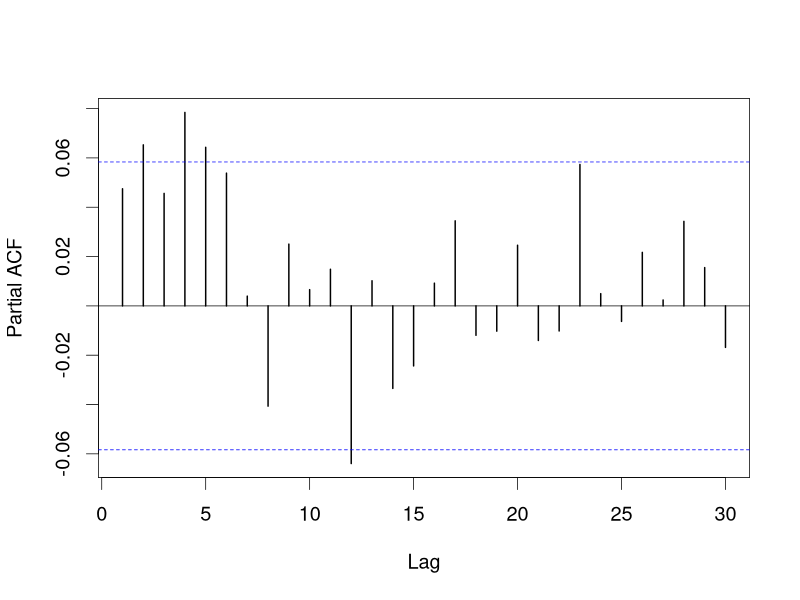

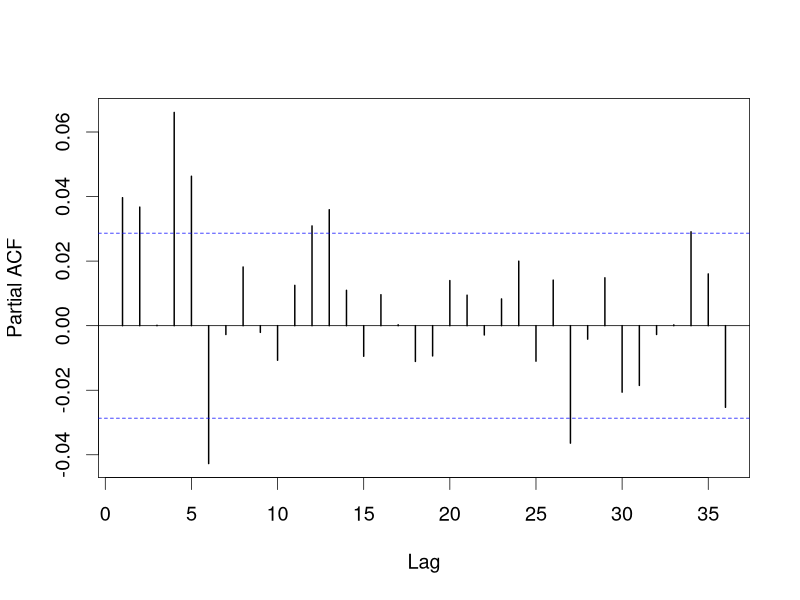

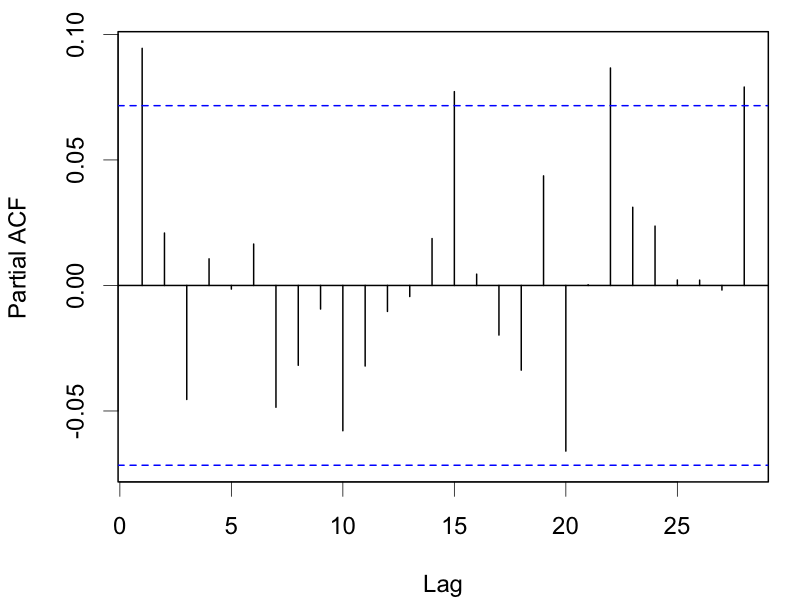

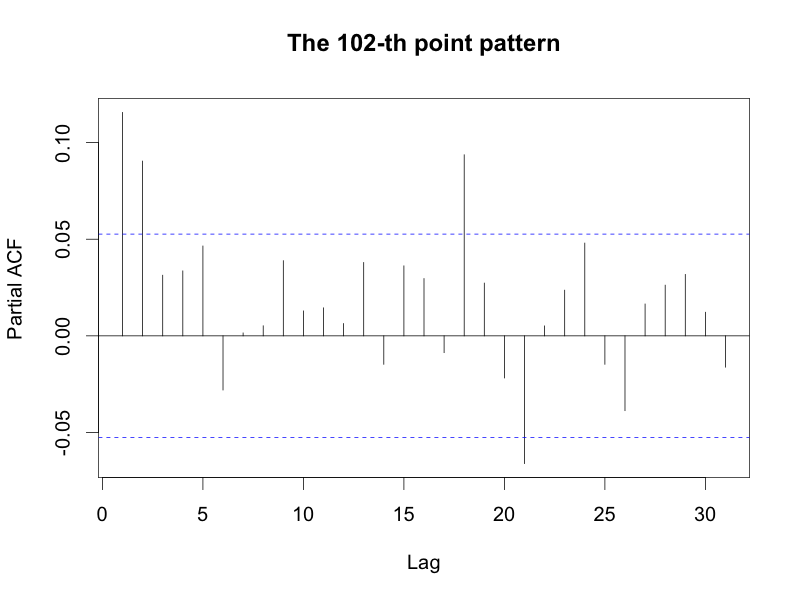

The (almost sure) discreteness of the DP prior for induces sparsity in the weights. This supports the strategy of fitting an over-specified mixture model, viewing as an upper bound on the number of effective components (Gelman et al., 2013). We select conservatively such that the weights of the last few lags are close to zero a posteriori, i.e., the nearer lags adequately account for process dependence. In practice, the autocorrelation function (ACF) and partial autocorrelation function (PACF) of the observed duration time series can be used to guide the choice of , with a sensitivity analysis to ensure that the selected is a reasonable upper bound. Results from this strategy, as implemented for the data example of Section 4.2, are provided in the Supplementary Material.

3.2 Posterior simulation

We outline an MCMC method, Metropolis-within-Gibbs, for posterior simulation. Similar to finite mixtures, we augment the model with configuration variables , taking values in , with discrete distribution , where if and otherwise, for . The posterior distribution for the augmented model is

The posterior full conditional distribution of is a discrete distribution on with probabilities proportional to , for , and with probabilities proportional to , for . Given the configuration variables, we update the weights with a Dirichlet posterior full conditional distribution with parameter vector , where , for , and returns the size of set . The updates for parameters depend on the component densities , . In the Supplementary Material, we provide details of the MCMC algorithms for specific models implemented in Section 4.

3.3 Inference, model checking, and prediction

Using the MCMC algorithm, we obtain posterior samples that provide full inference for any functional of the point process. For example, given the posterior draws for the model parameters, we obtain posterior realizations for the conditional intensity function by evaluating (5) or (10) over a grid of time points. Similarly, for stationary MTDPPs, we can obtain point and interval estimates for the marginal duration density.

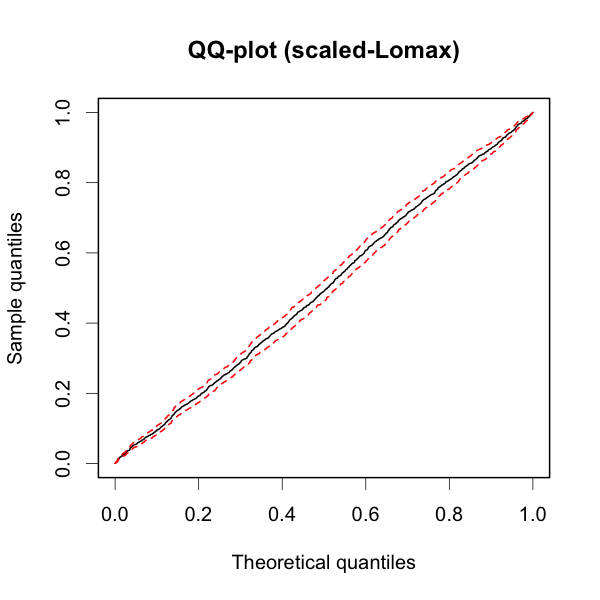

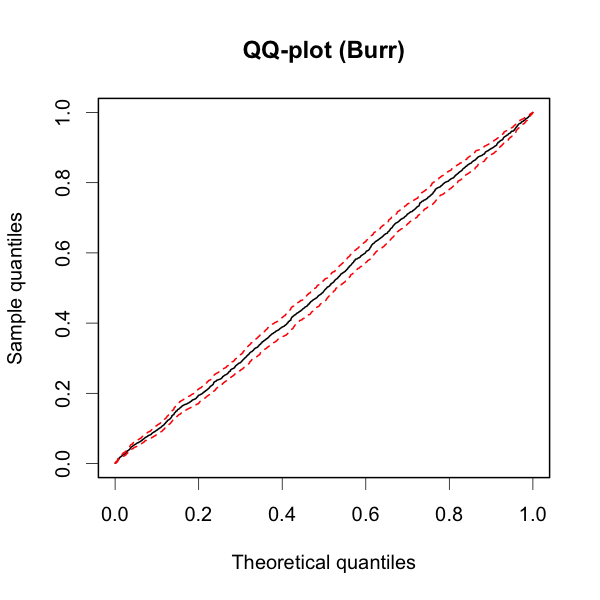

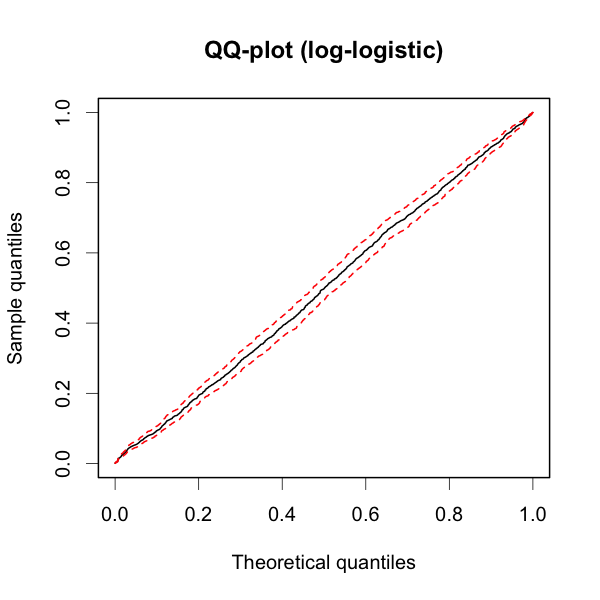

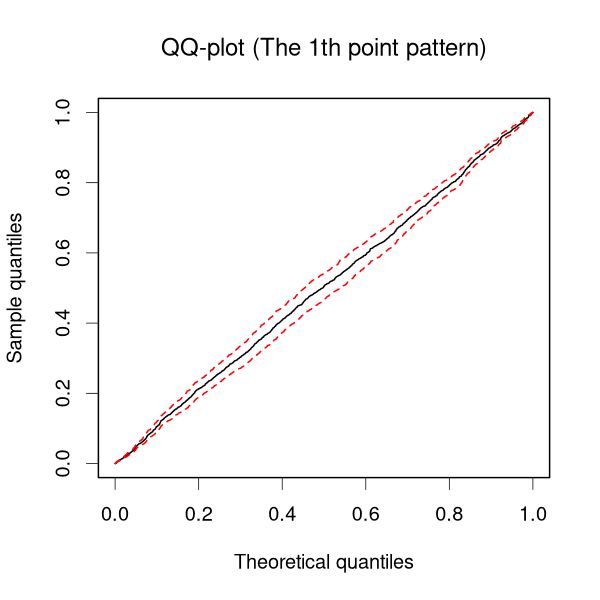

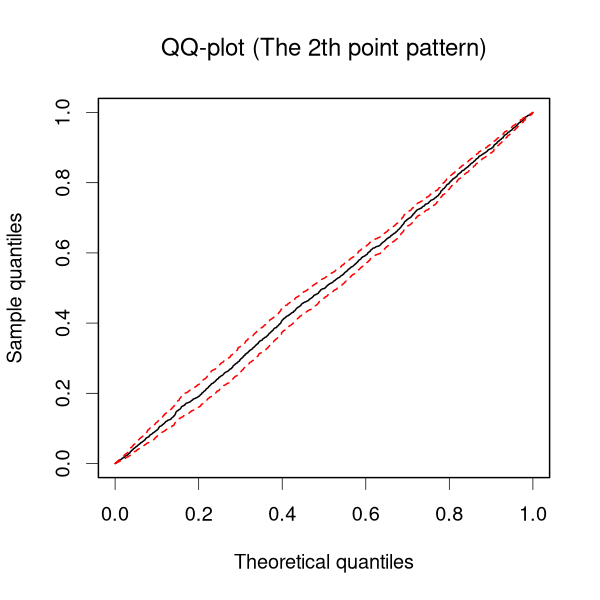

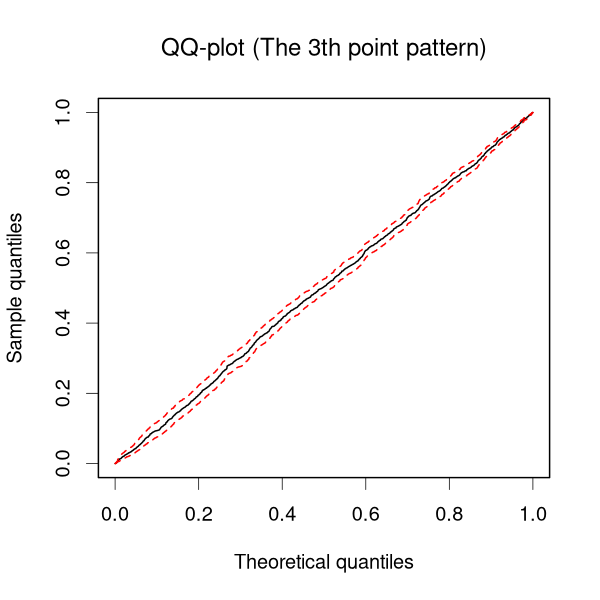

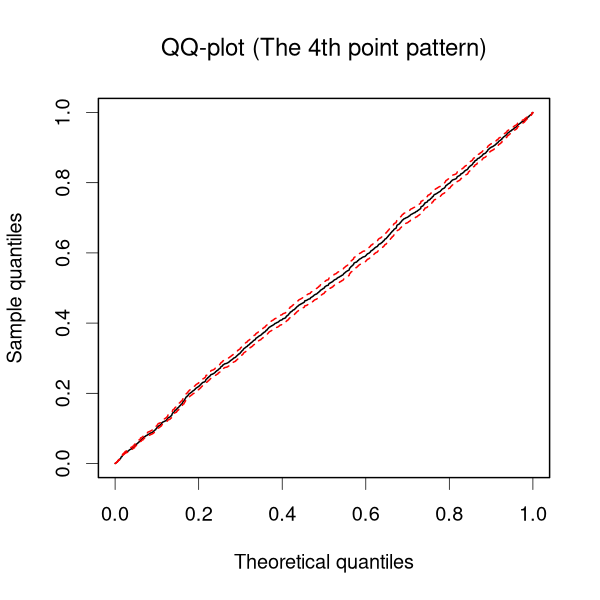

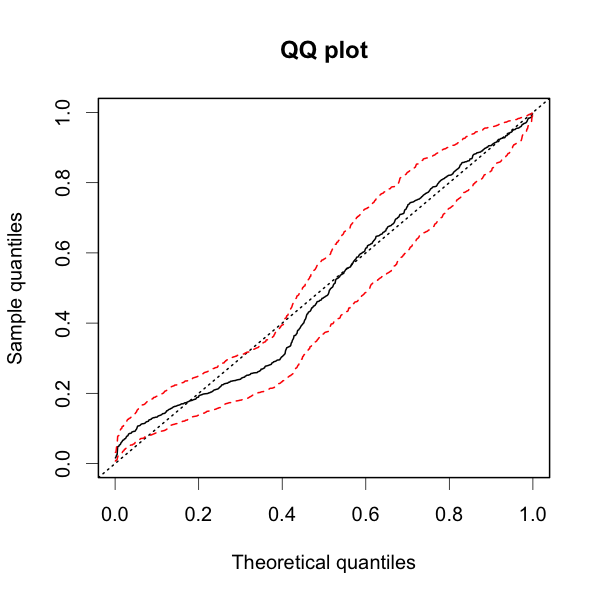

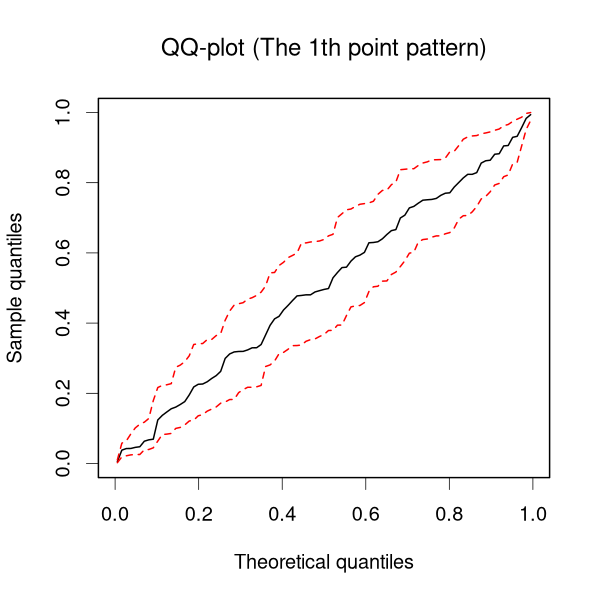

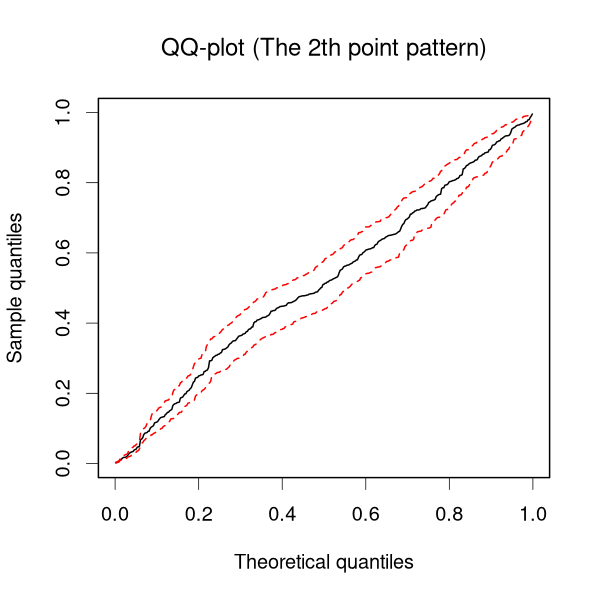

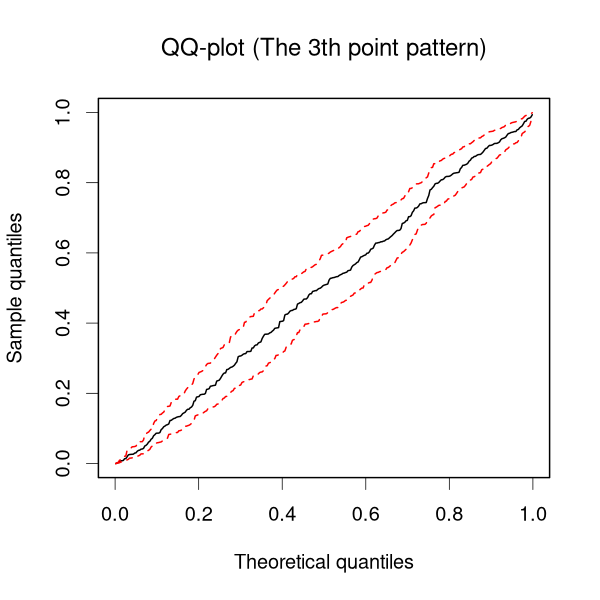

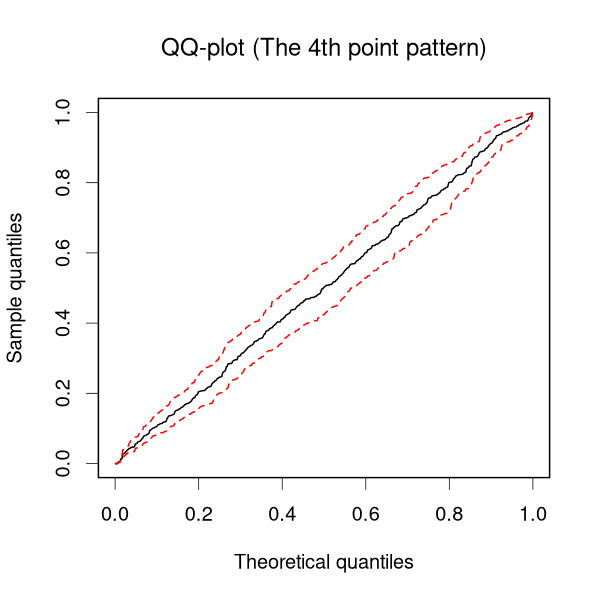

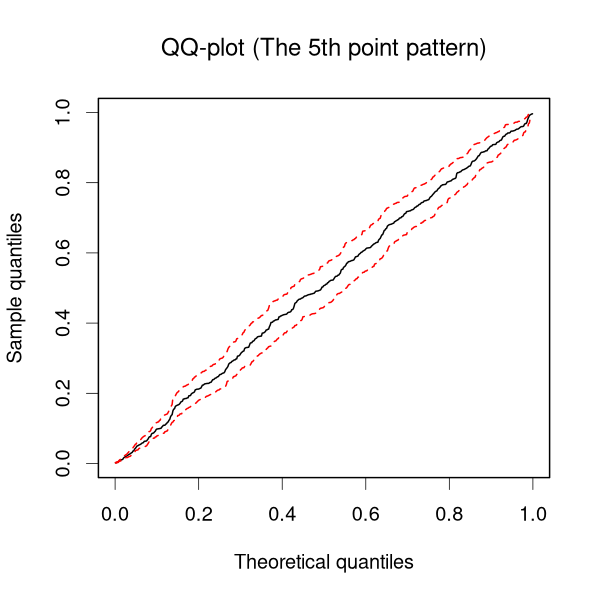

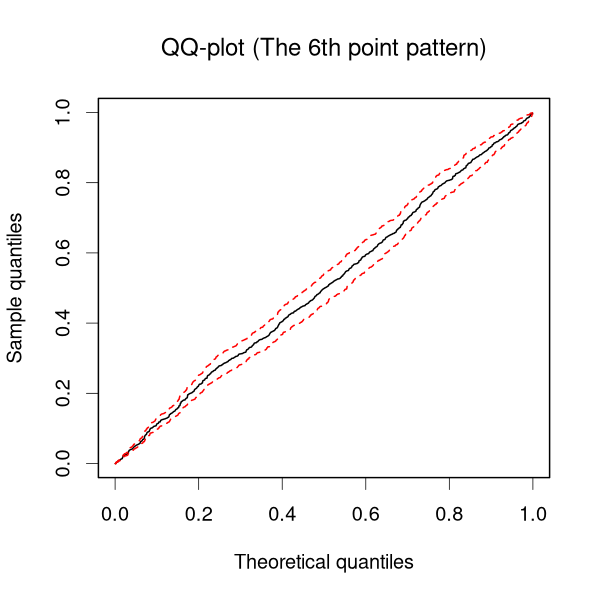

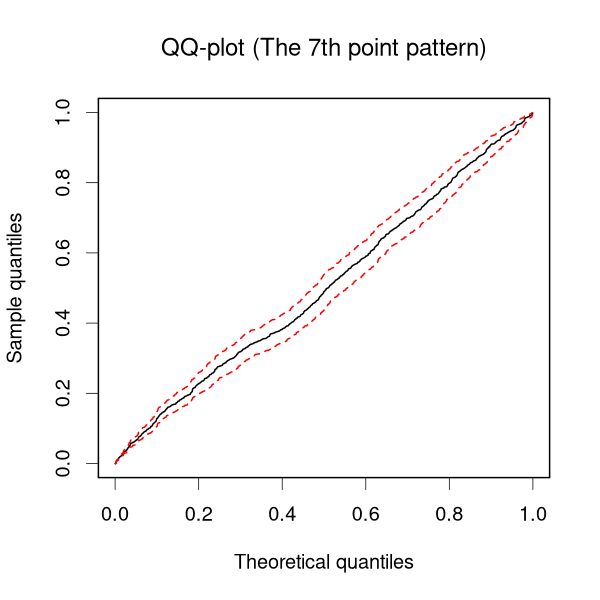

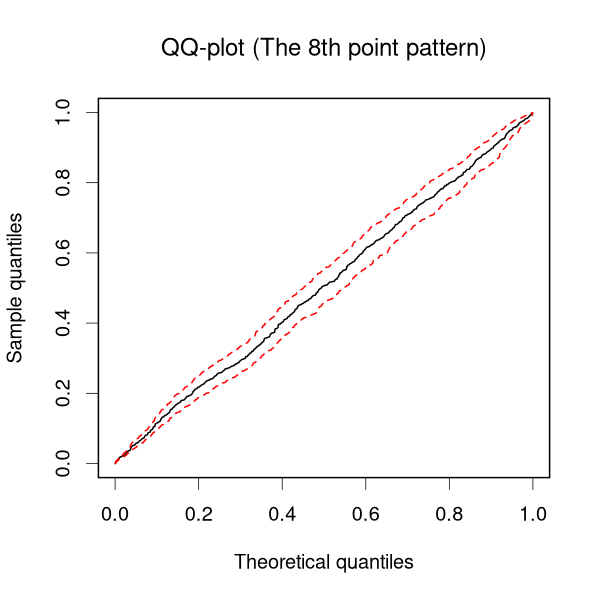

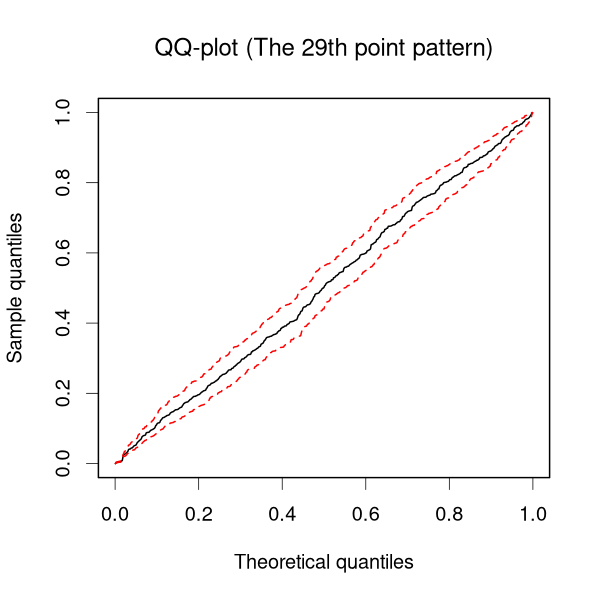

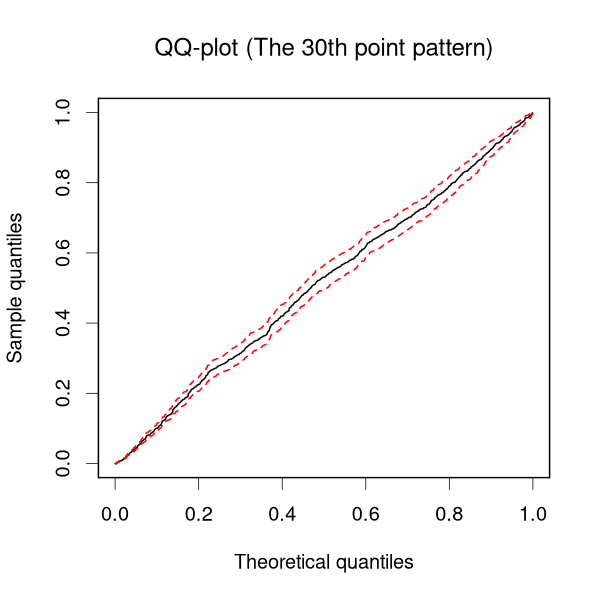

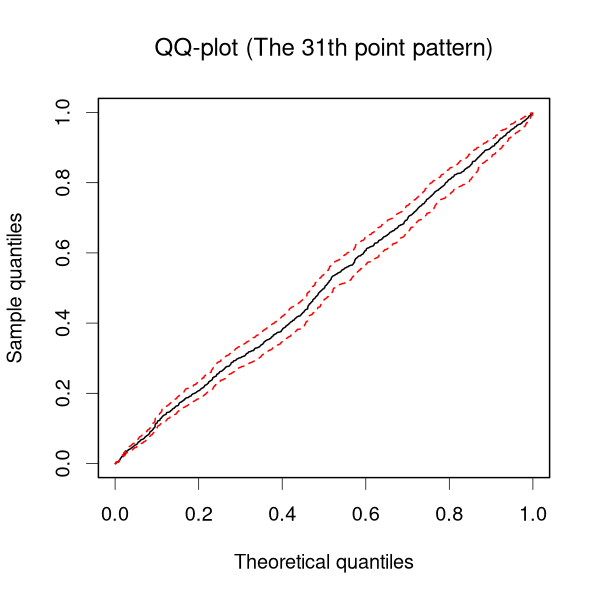

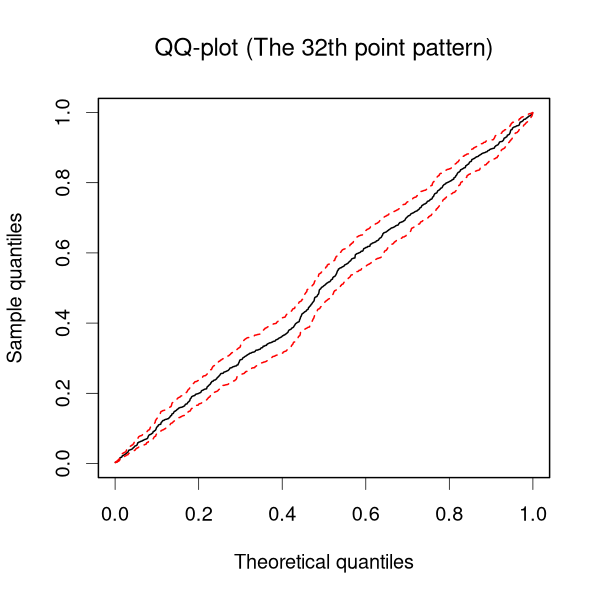

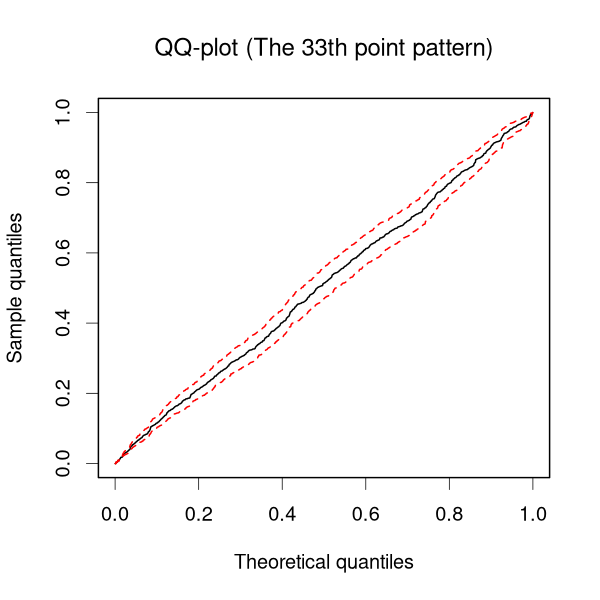

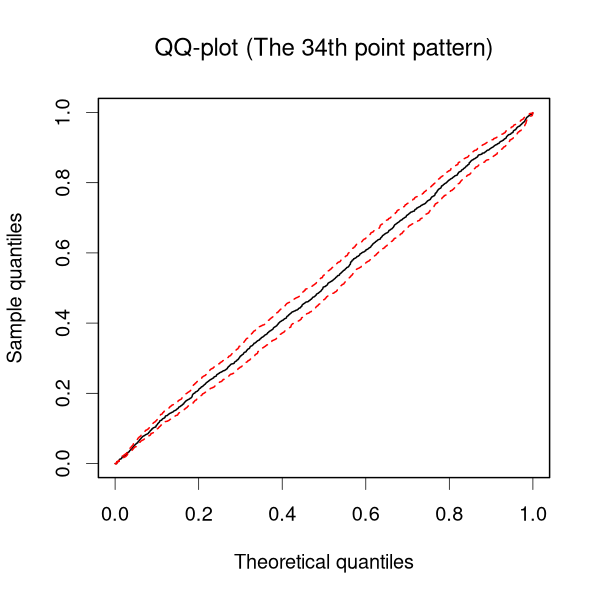

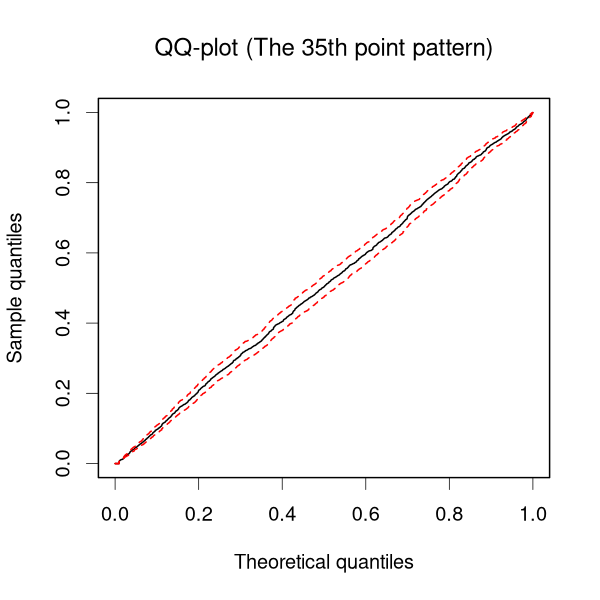

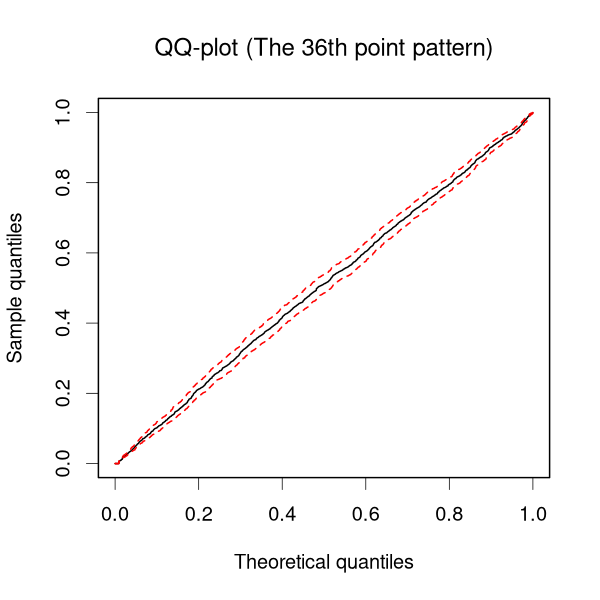

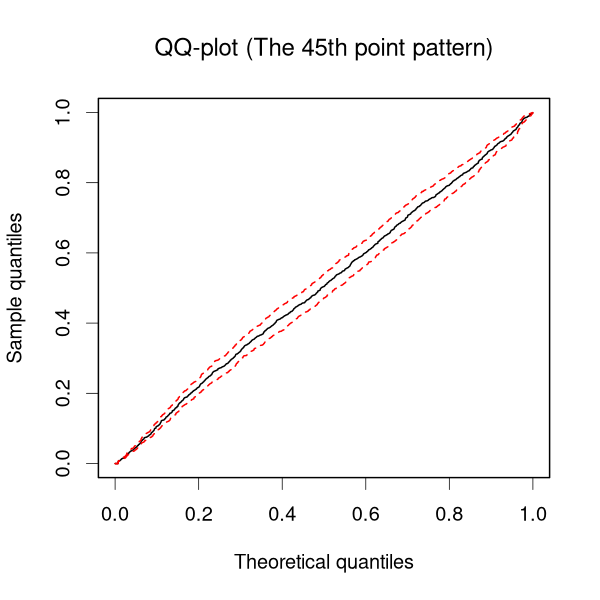

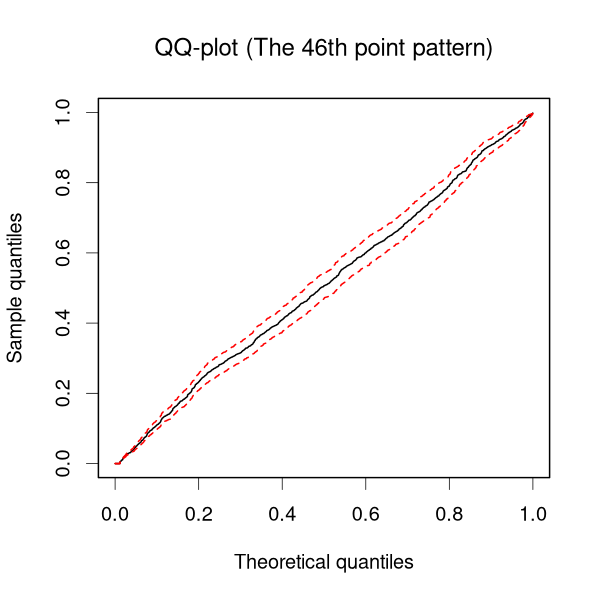

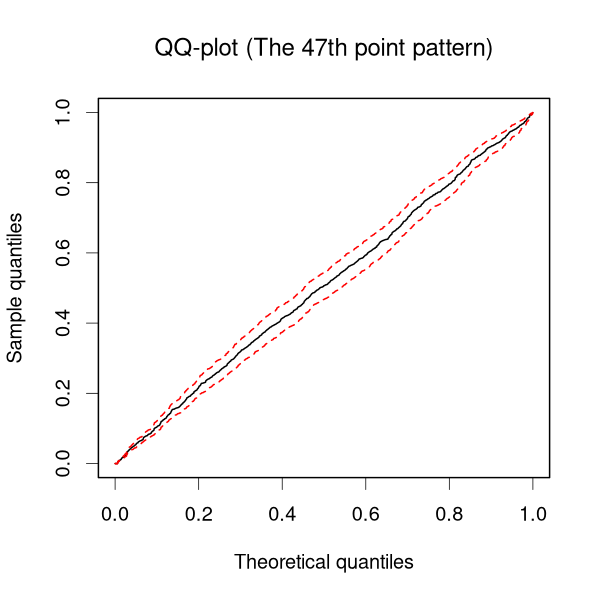

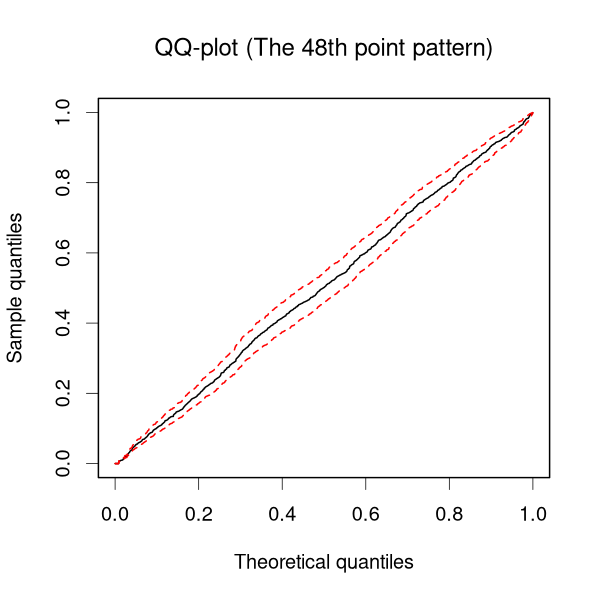

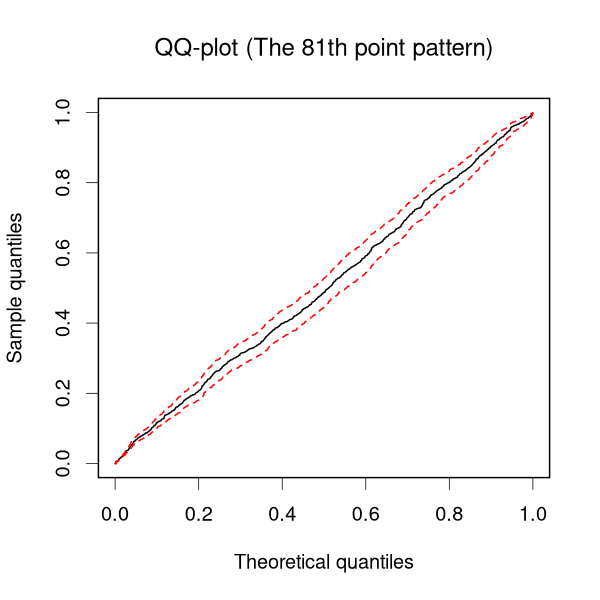

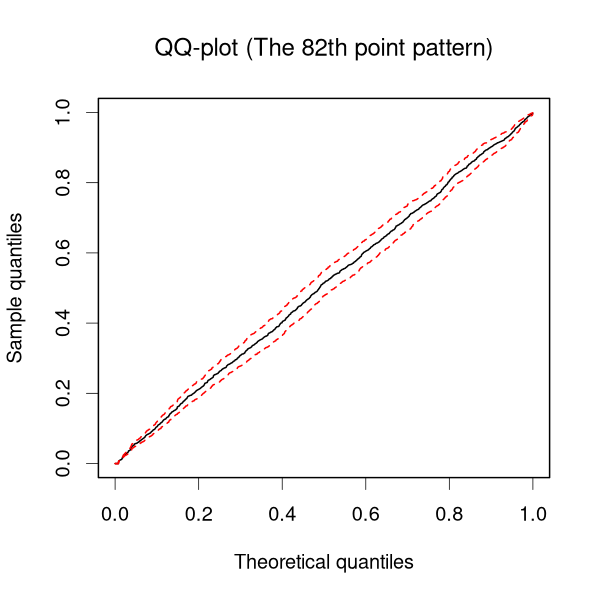

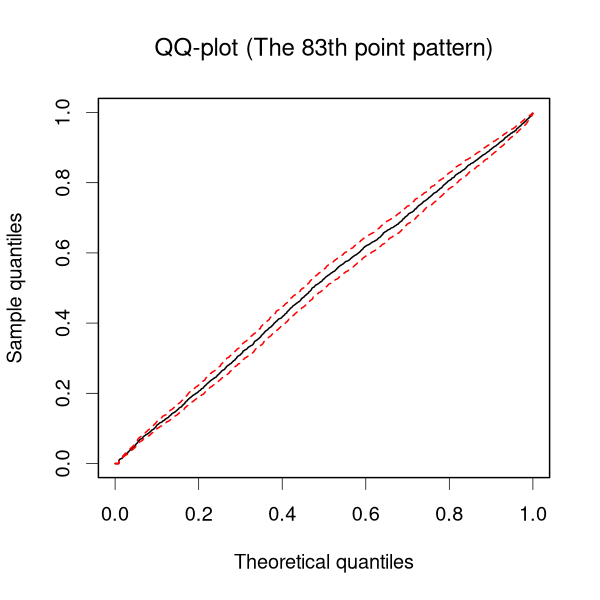

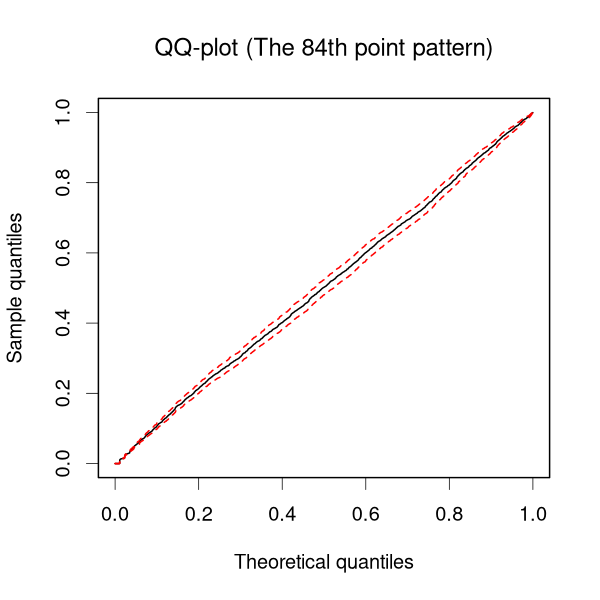

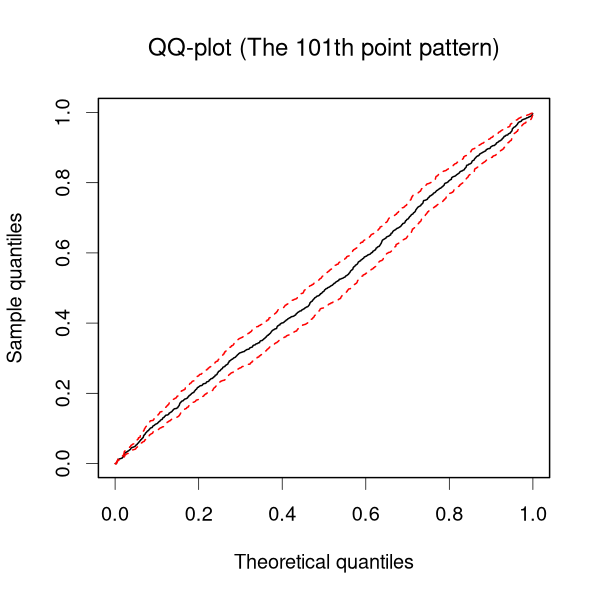

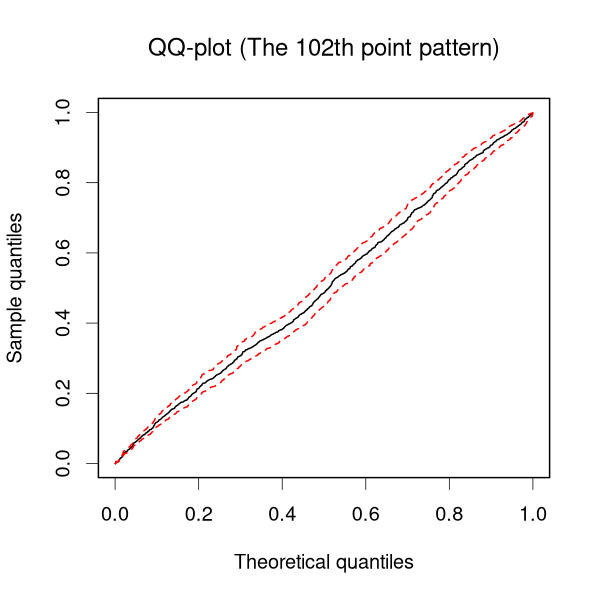

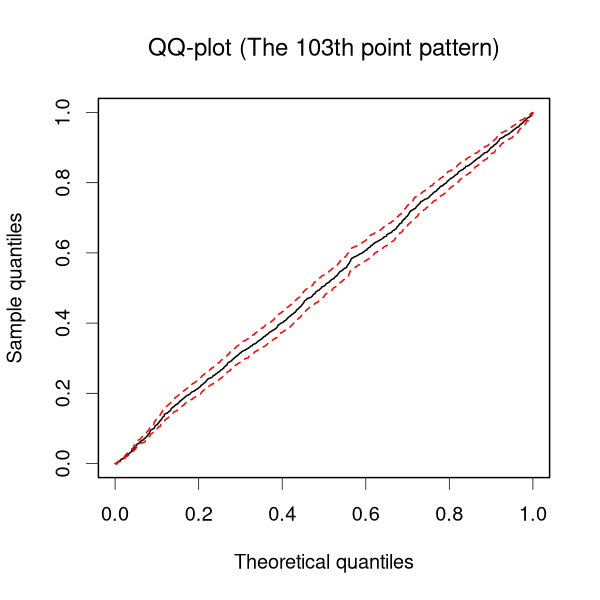

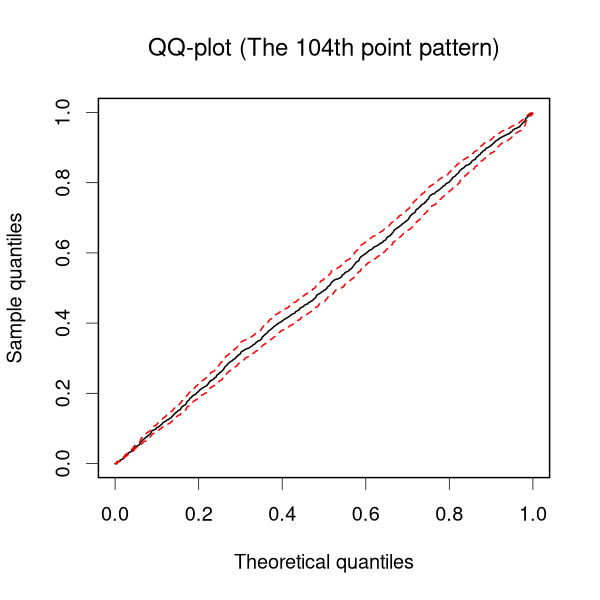

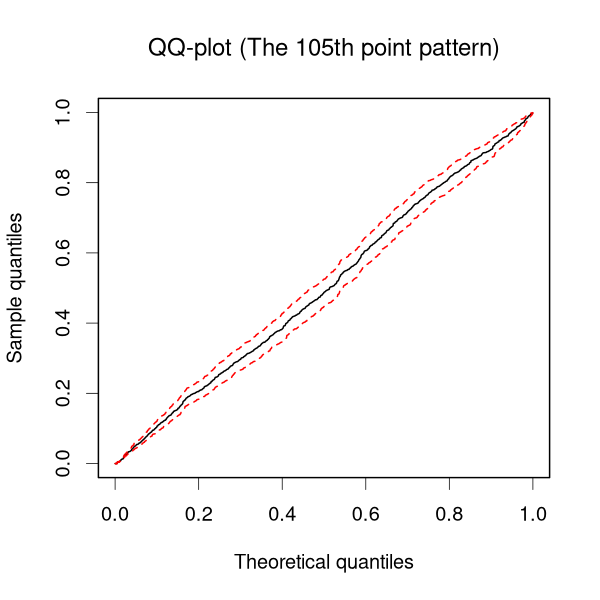

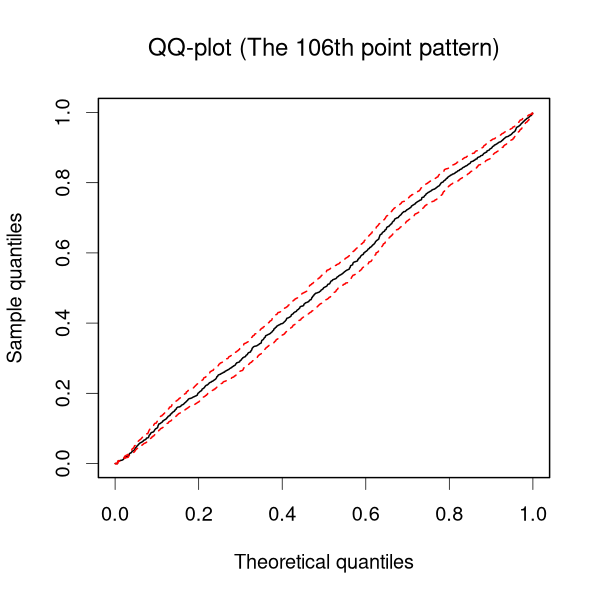

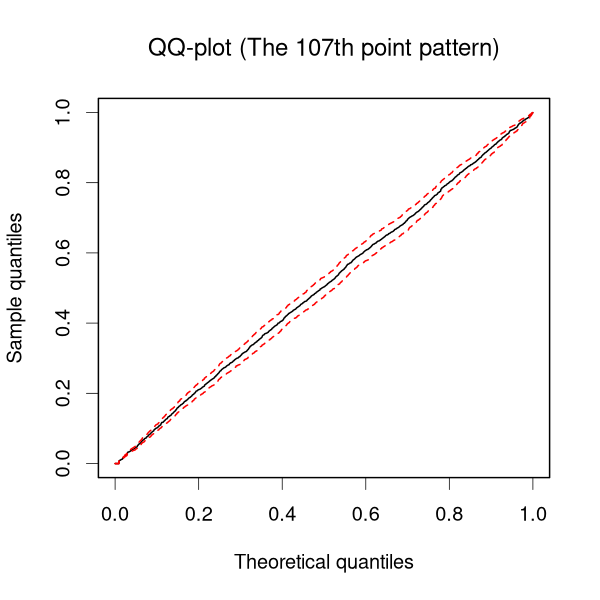

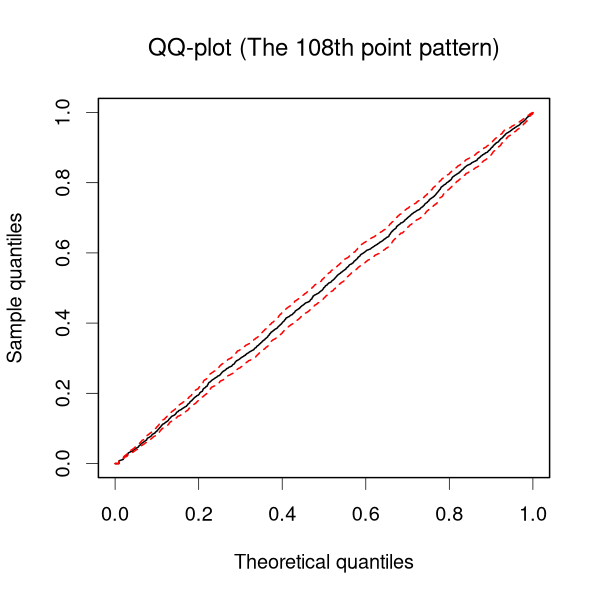

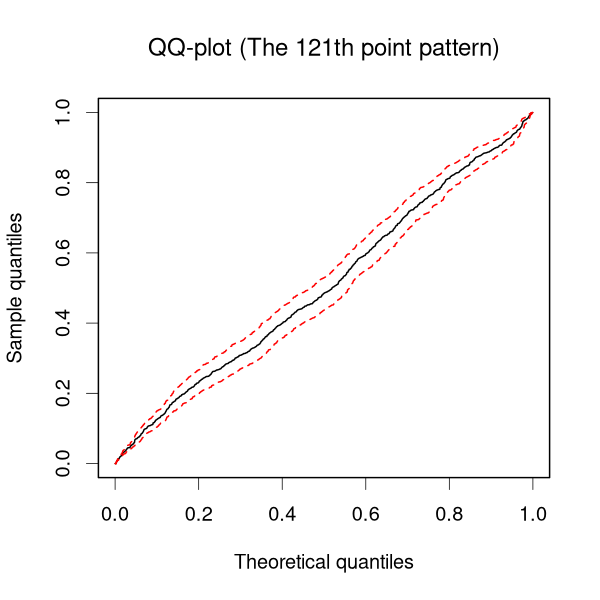

For model assessment, we use the time-rescaling theorem (Daley and Vere-Jones, 2003), according to which is a realization from a unit rate Poisson process, where is the conditional cumulative intensity, and is the observed point pattern. If the model is correctly specified, , for , are independent uniform random variables on . Thus, the model can be assessed graphically using quantile-quantile plots for the estimated .

For MTDPP models, , and thus . Using the relationship between the conditional survival and cumultive intensity functions, we have , for . Therefore, , which allows us to obtain posterior samples for the from . Replacing survival function with , the approach can also be used for MTDCPPs.

Finally, we consider prediction for future events. Let denote the observed point pattern , with corresponding observed durations , for . Note that includes the constraint that the next (unobserved) event time , i.e., that the next (unobserved) duration . We can predict via prediction of , incorporating the condition that . The posterior predictive density for the next duration can be written as

where the weights , and , for , is the -th component density truncated below at . The Supplementary Material includes details for the derivation, and the extension to -step-ahead predictions, for . Also provided in the Supplementary Material are details on prediction for MTDCPP models.

4 Data illustrations

We illustrate the scope of the modeling framework through one synthetic and two real data examples. In the simulation example, we explore inference results for conditional intensities and duration hazard functions of different shapes, using the Burr MTDPP that allows for monotonic and non-monotonic hazard functions. The goal of the first real data example is to demonstrate the practical utility of stationary MTDPPs for scenarios where the duration-independence assumption of renewal processes needs to be relaxed. The second real data example examines the capacity of MTDCPPs to detect and quantify duration clustering behaviors; this was also evaluated through a simulation study, the details of which can be found in the Supplementary Material. Also available in the Supplementary Material are additional simulated data results, including model comparison with ACD models and prior sensitivity analysis for the mixture weights, as well as graphical model assessment results for all data examples, obtained using the approach of Section 3.3. The model assessment results indicate good model fit for all data examples.

We implemented all MCMC algorithms in the R programming language, with C++ code integrated to update latent variables, on a computer with a 2-GHz Intel Core i5 processor and 32-GB RAM. Results for each data example are based on posterior samples collected after appropriate burn-in and thinning. MCMC convergence diagnostics are available in the Supplementary Material. As an example of computing times, the code for the Burr MTDPP model (Section 4.1) fitted to about observations took around four minutes to complete iterations.

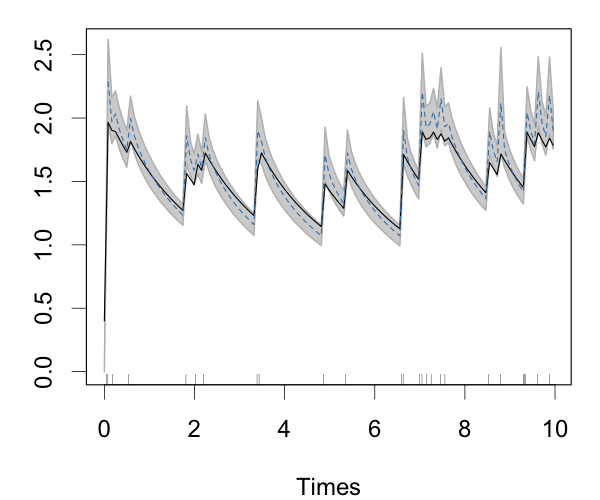

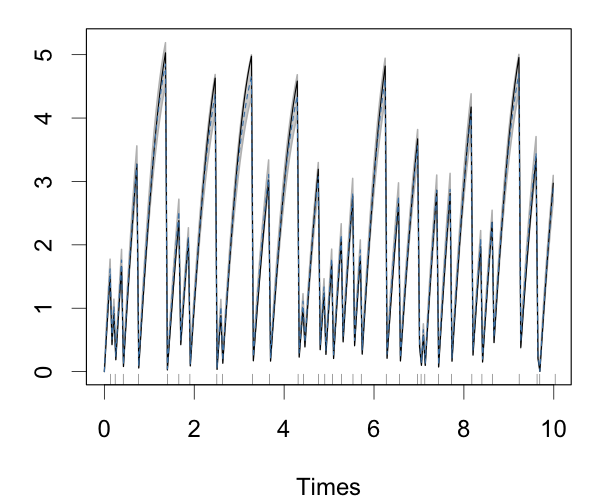

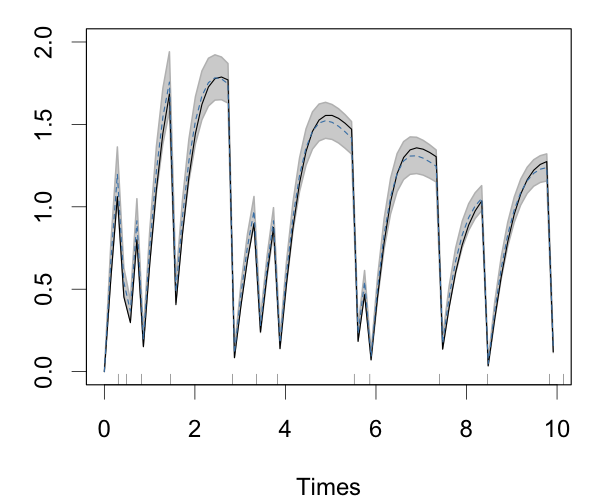

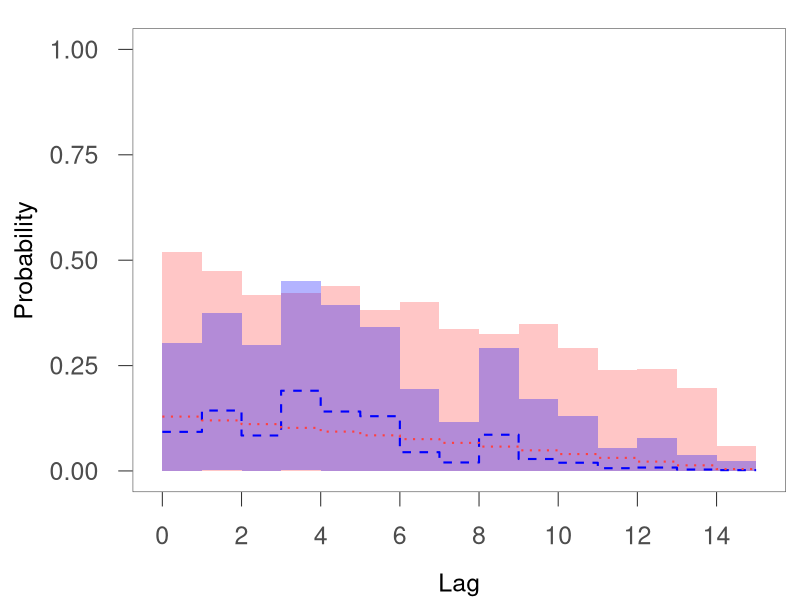

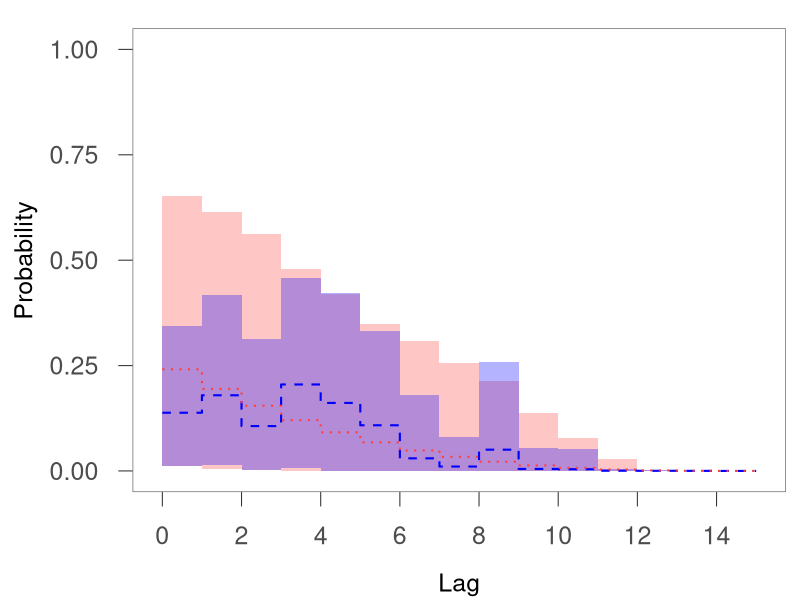

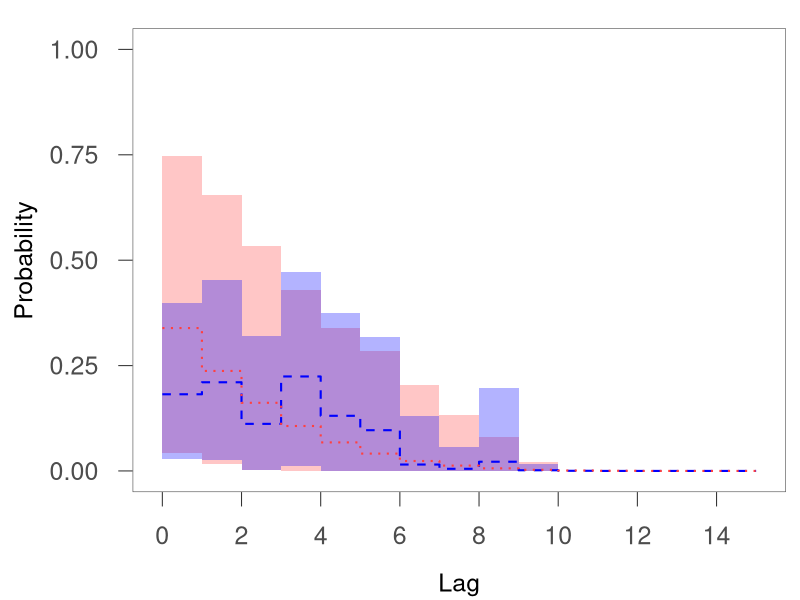

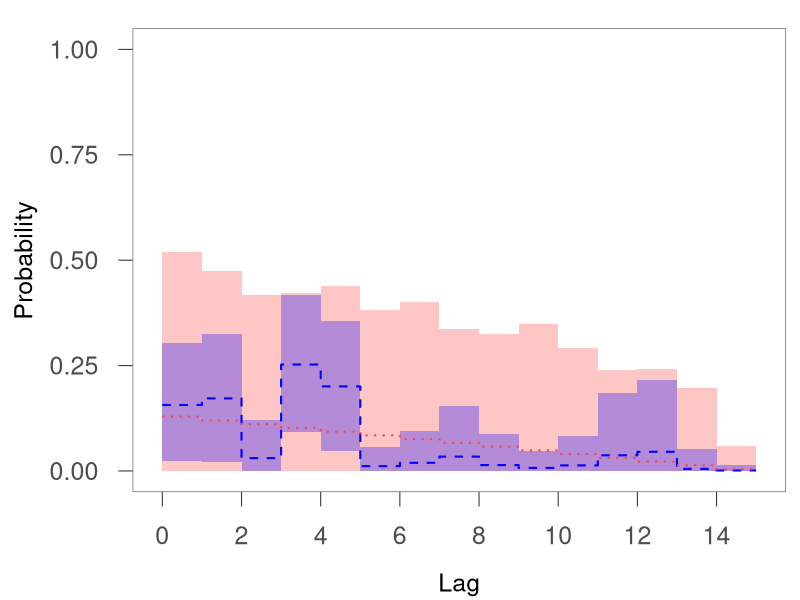

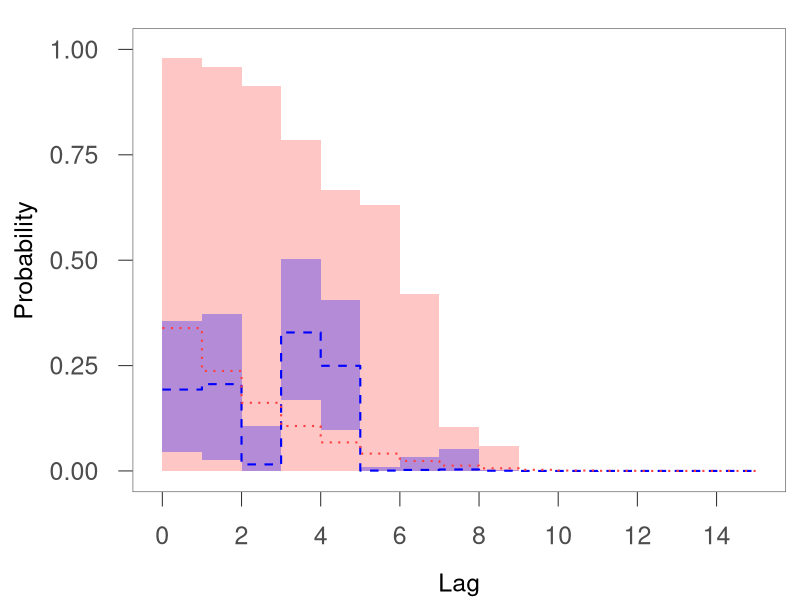

4.1 Simulation study

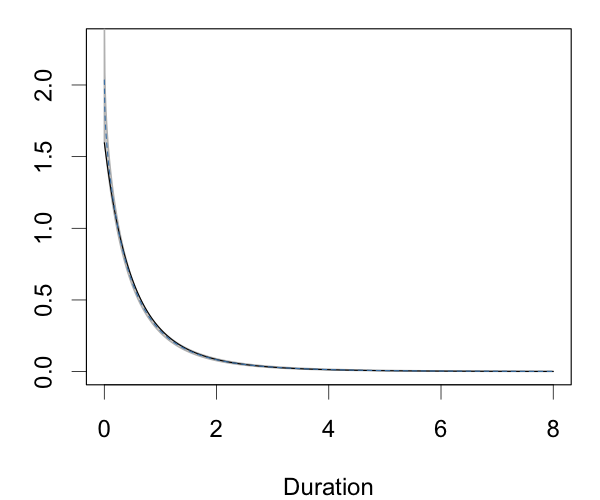

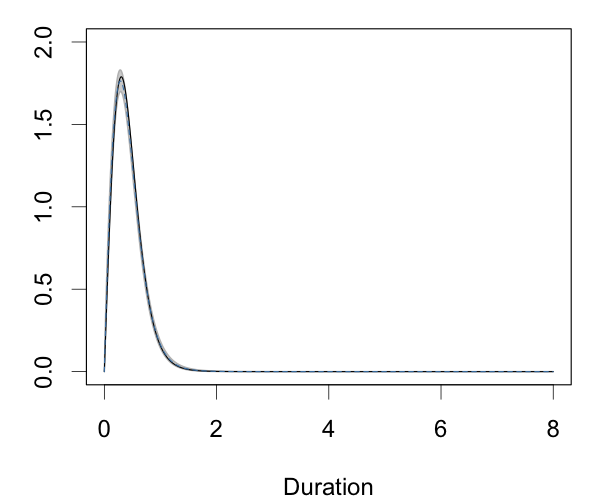

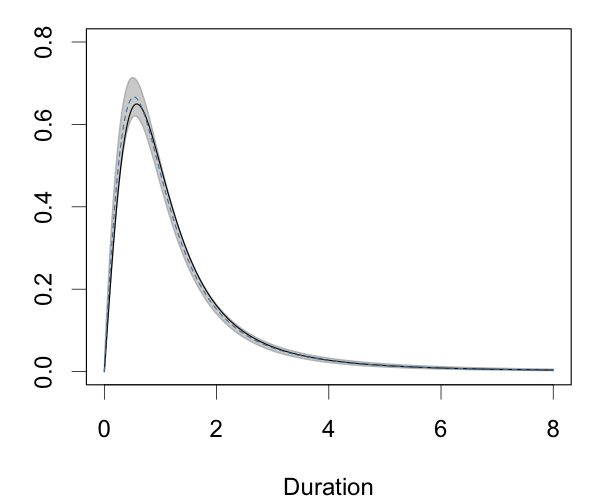

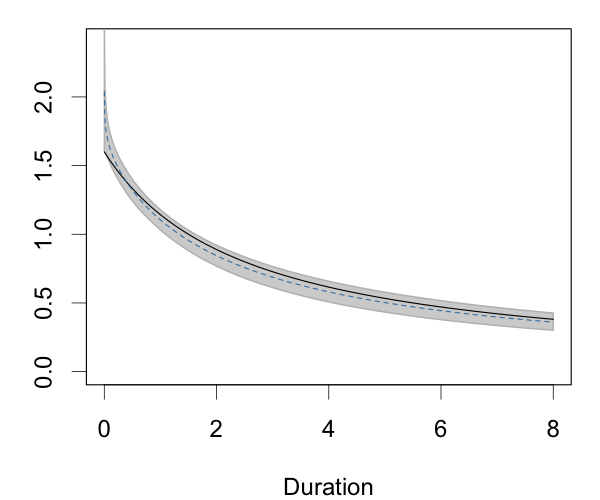

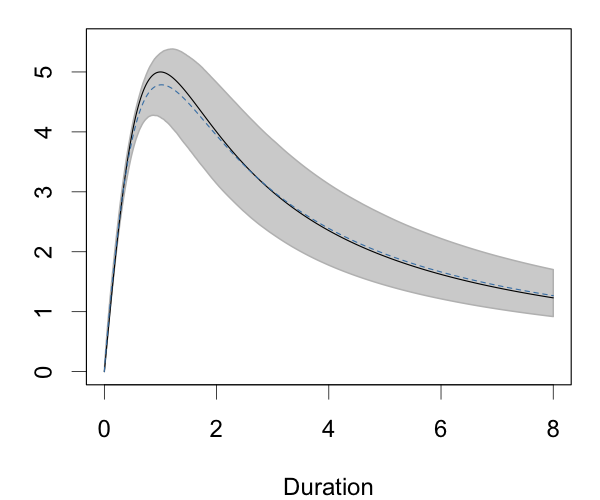

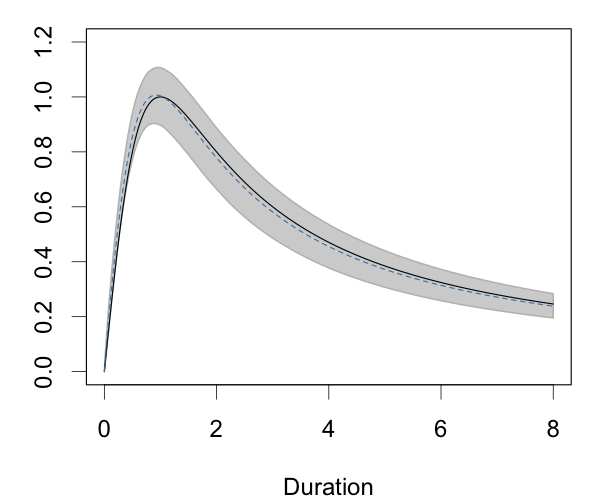

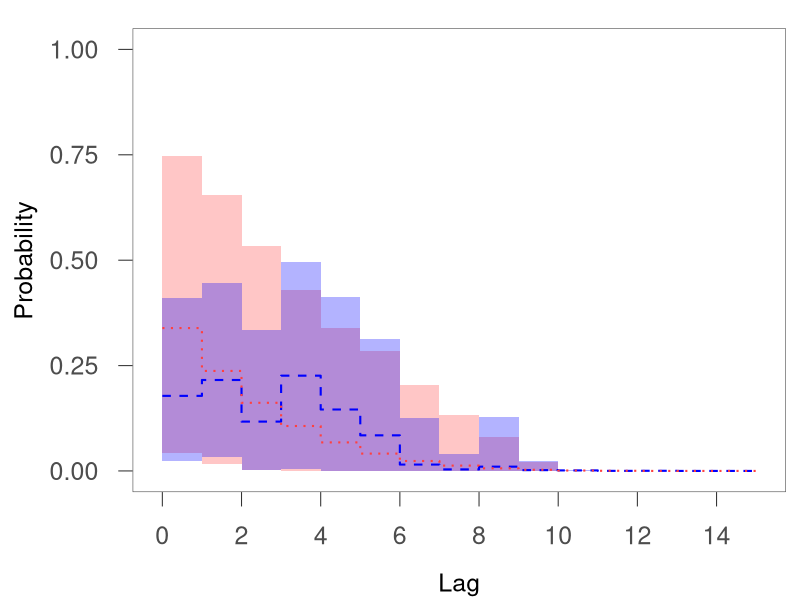

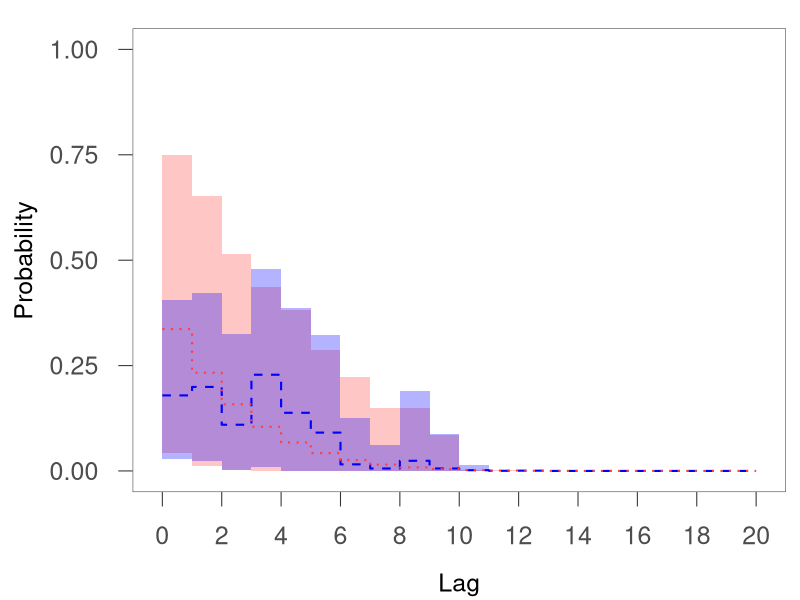

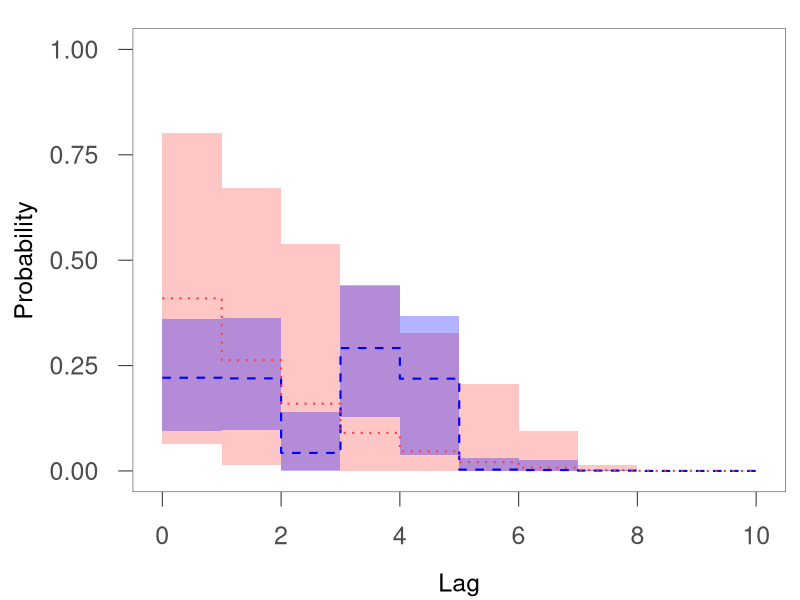

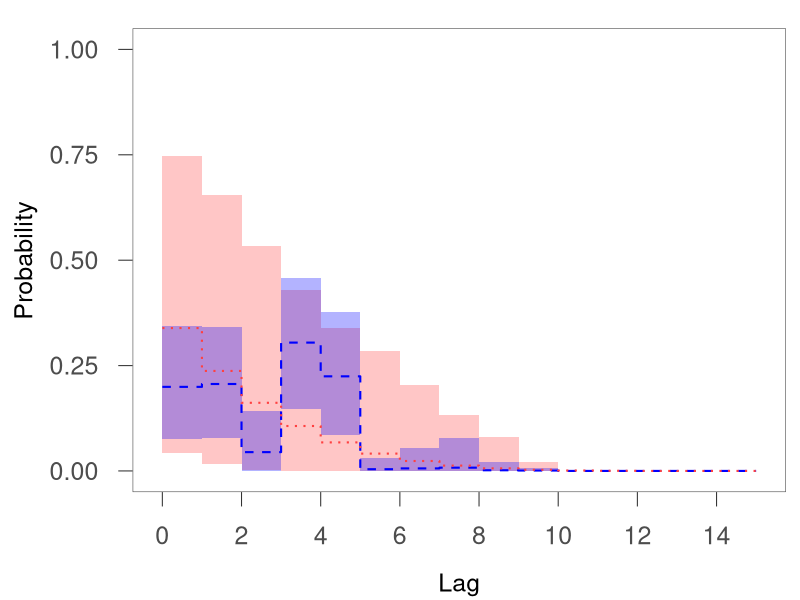

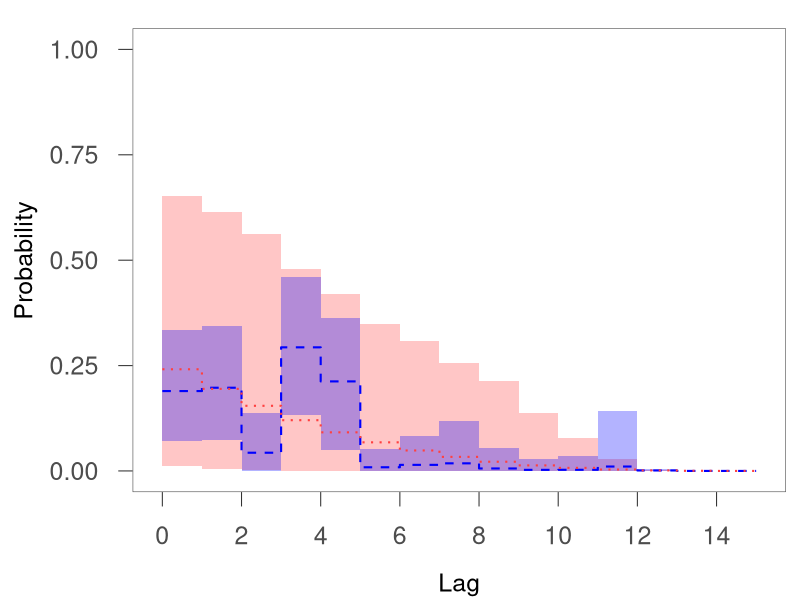

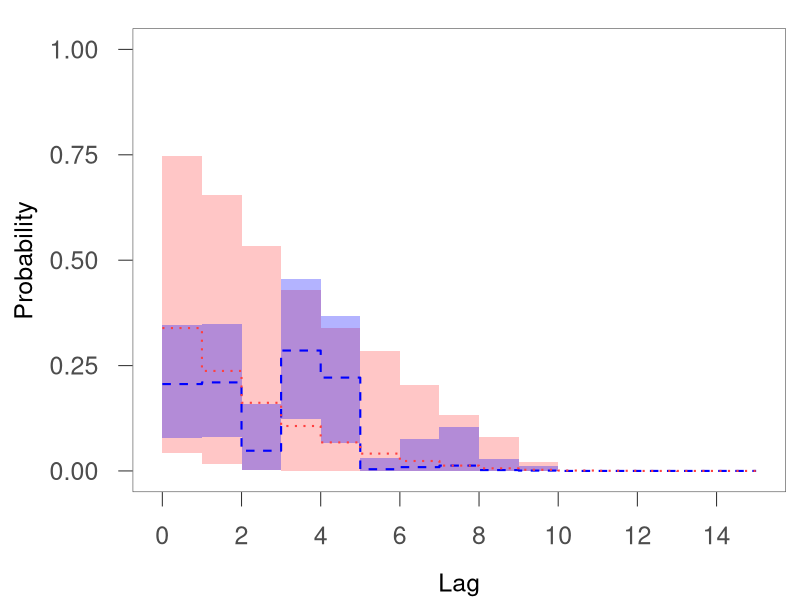

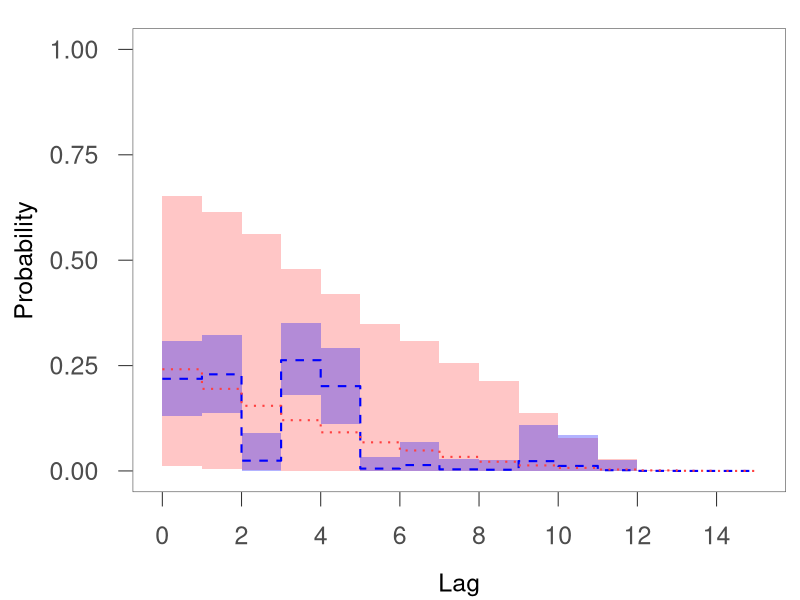

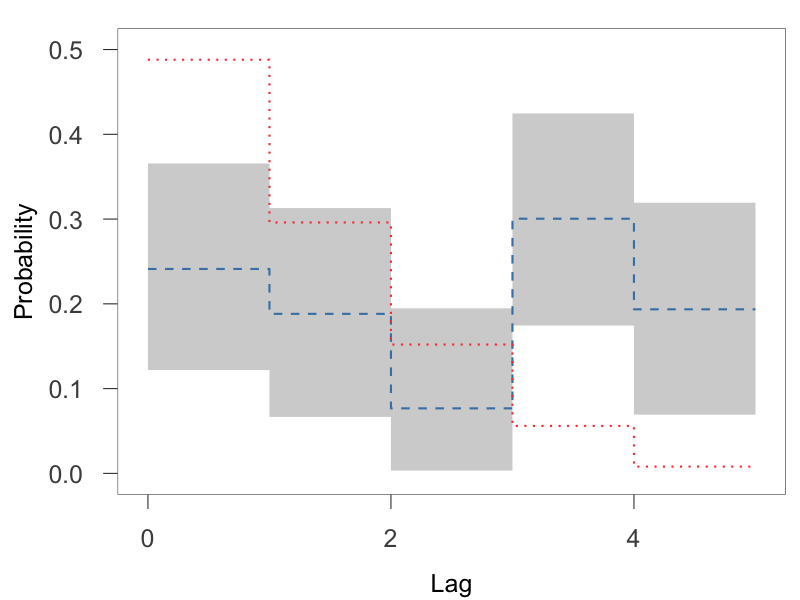

We generated data from three stationary MTDPP models (discussed in Section 2.3) with scaled-Lomax, Burr, and log-logistic marginal duration distributions. The respective parameters were set at , , and , such that the hazard function for the durations is decreasing for the scaled-Lomax MTDPP, and hump-shaped for the other two models; see Figure 1. The model order was for all simulations, with decaying weights . For each simulated point pattern, we chose the observation window to obtain around 2000 event times.

We applied the Burr MTDPP model in (8), with , to the three synthetic data sets. Recall that the hazard function of the marginal duration distribution is decreasing when , and hump-shaped when . We thus assigned a prior to , where denotes the gamma distribution with mean . Moreover, the th moment of the distribution exists if . Independently of , we placed a truncated gamma prior, , on . Since , the prior choice for and implies that, in prior expectation, the first five moments of the marginal duration distribution exist. The scale parameter was assigned a prior, and the vector of weights a CDP prior.

Figure 1 plots point and interval estimates for the point process conditional intensity, as well as for the duration process marginal density and its associated hazard function. Note that, although the true data generating mechanisms correspond to MTDPPs, the Burr MTDPP is a mis-specified model for two of the simulated data sets. However, the model is able to distinguish between monotonic and non-monotonic hazard functions for the marginal duration distribution. Overall, based on a single process realization, the Burr MTDPP model provides reasonably accurate estimates for different point process functionals, with uncertainty bands that effectively contain the true functions.

4.2 IVT recurrence interval analysis

Integrated water vapor transport (IVT) is a vector representing the total amount of water vapor being transported in an atmospheric column. Atmospheric rivers (ARs), which are corridors of enhanced IVT, play a vital role in transporting moisture into western North America. Identifying and tracking ARs is central to understanding high-impact weather events, such as extreme precipitation and flooding. Rutz et al. (2019) review several of the AR detection algorithms, most of which use IVT thresholds as input. Appropriately thresholding the IVT is important to improve AR detection; e.g., Barata et al. (2022) provide a time-varying quantile estimate of the IVT using a dynamic statistical model.

In this example, we take on a different perspective to study the IVT, based on the general idea that strong ARs tend to associate with extreme IVT magnitudes. We obtain a collection of recurrent events for which the IVT magnitude exceeds a given threshold. Modeling extreme events using a point process approach is motivated by the asymptotic behavior of threshold exceedances. This approach assumes that, for a large threshold, the exccedances and the associated event times can be considered as a marked Poisson process (e.g., Kottas and Sansó 2007). On the other hand, the Poisson process assumption may be too restrictive, as well as unsuitable for applications where the inferential interest lies in the stationary distribution of the durations between event times. Studying the recurrence interval distribution is important in many areas, such as study of earthquakes above a certain magnitude (Corral, 2004) and extreme returns (Jiang et al., 2018). Depending on the correlation structure of the original time series, the recurrence interval distribution may exhibit different types of tail behavior (e.g., power law). Furthermore, the recurrence intervals can be dependent (Santhanam and Kantz, 2008). A generalization of the renewal process is needed in order to capture the dependence among durations.

Here, we demonstrate the potential of MTDPPs for the aforementioned goal, that is, simultaneously model the stationary recurrence interval distribution and capture the recurrence intervals dependence. Comparison between a renewal process model and the MTDPP model below shows that incorporating duration dependence improves prediction (results are included in the Supplementary Material).

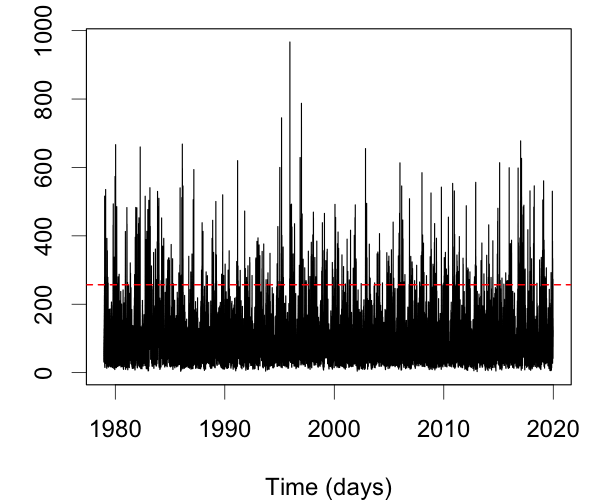

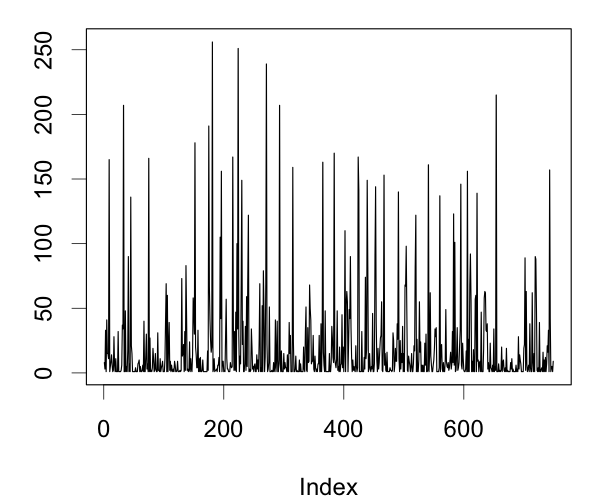

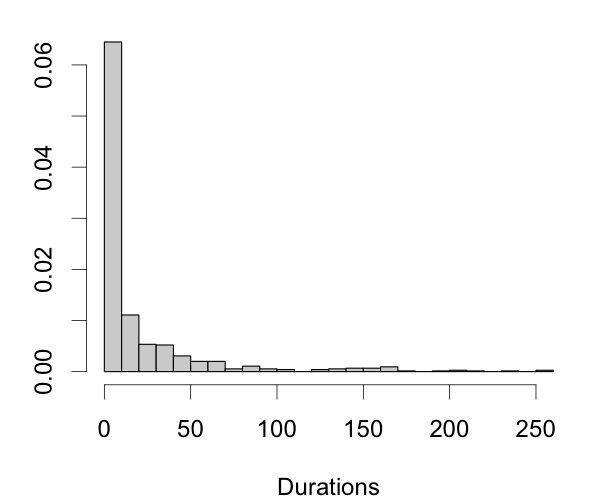

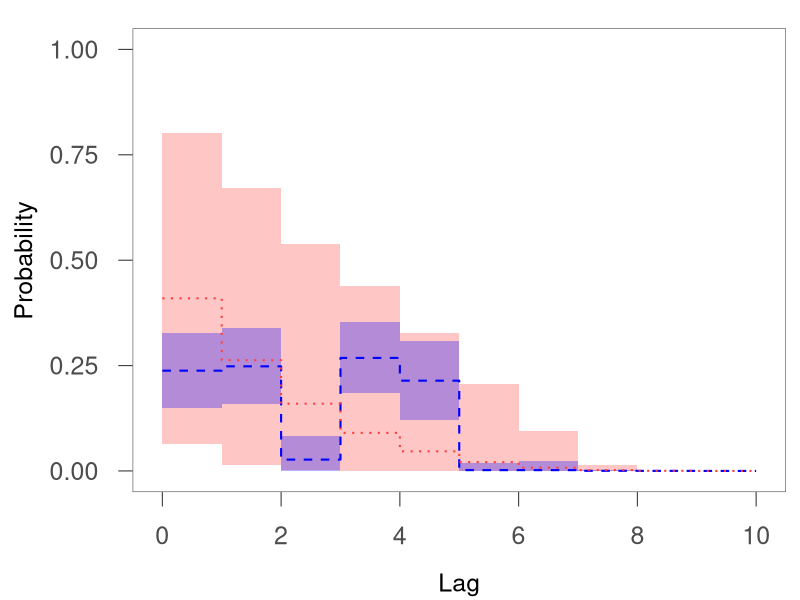

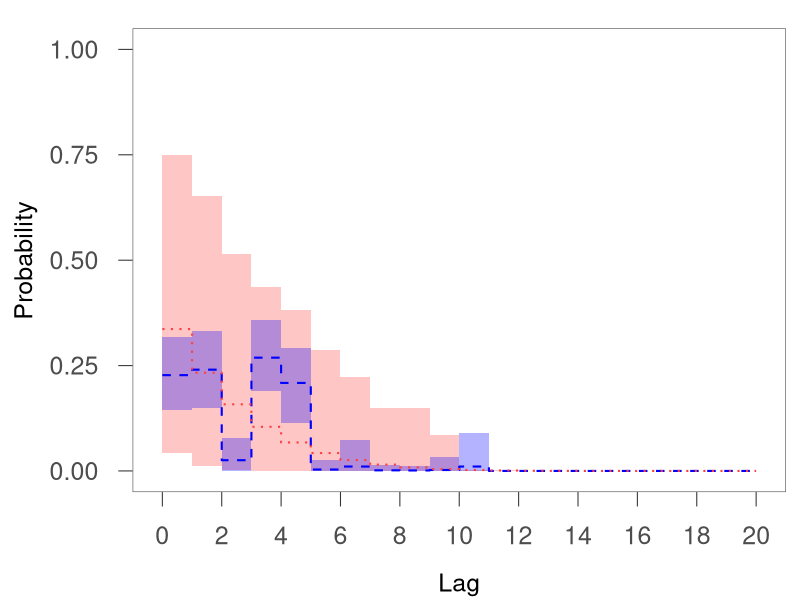

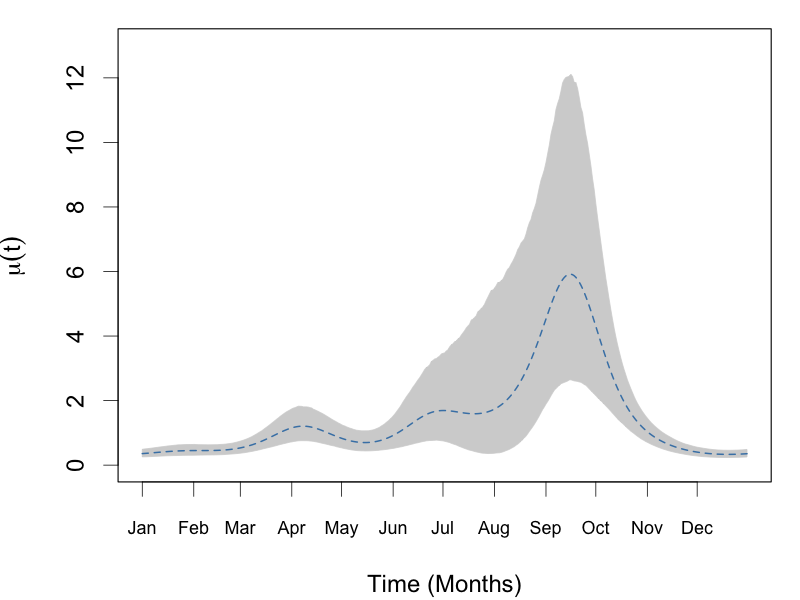

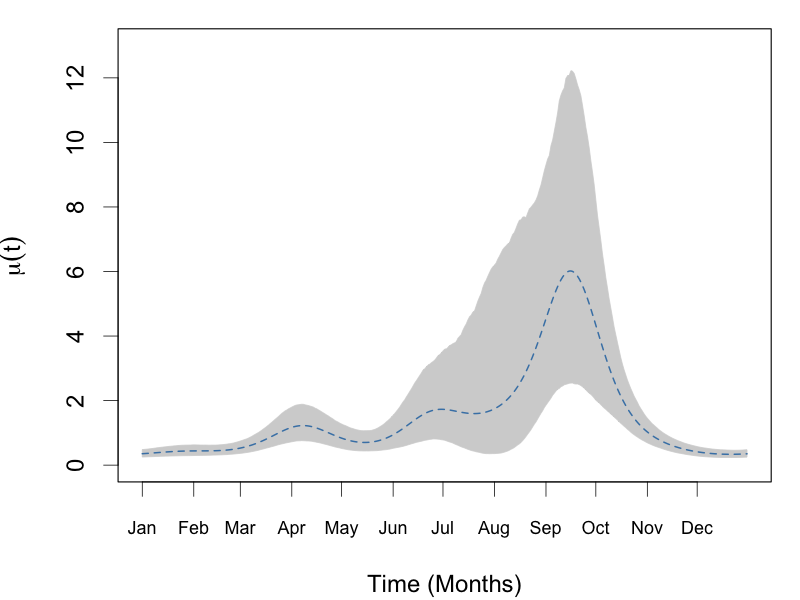

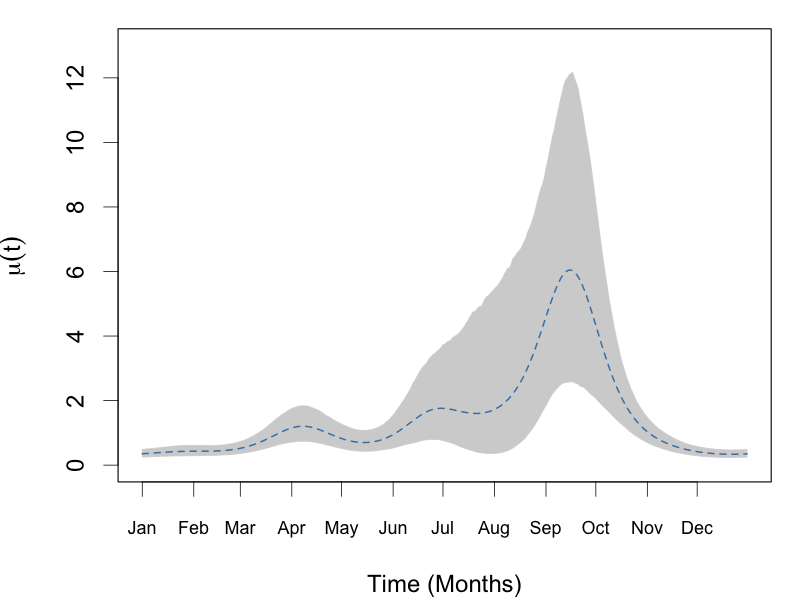

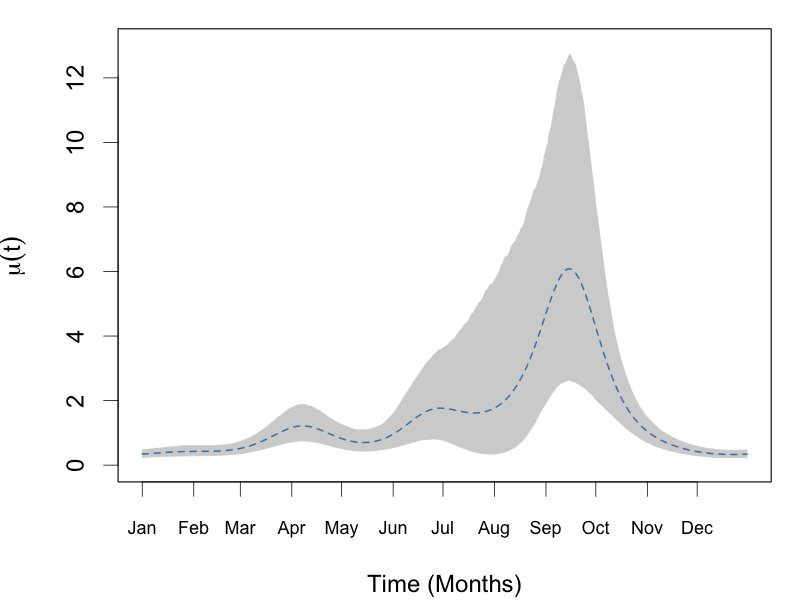

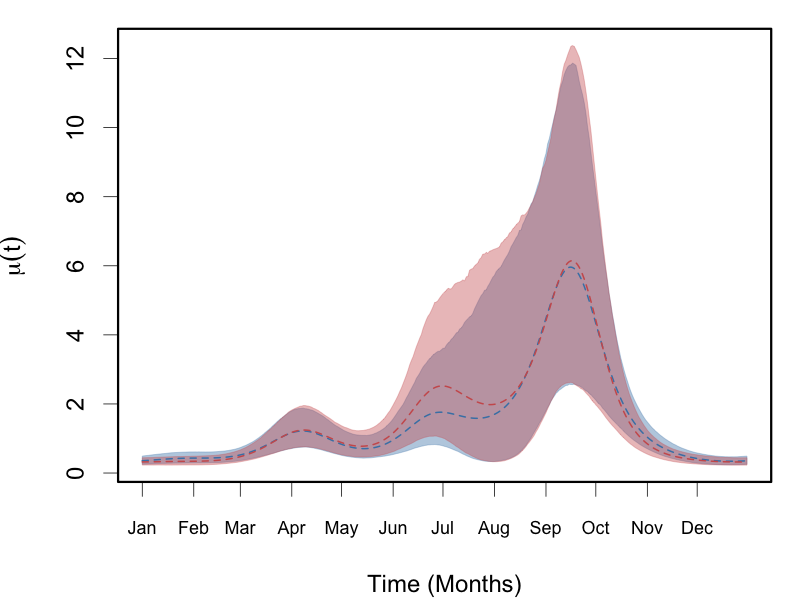

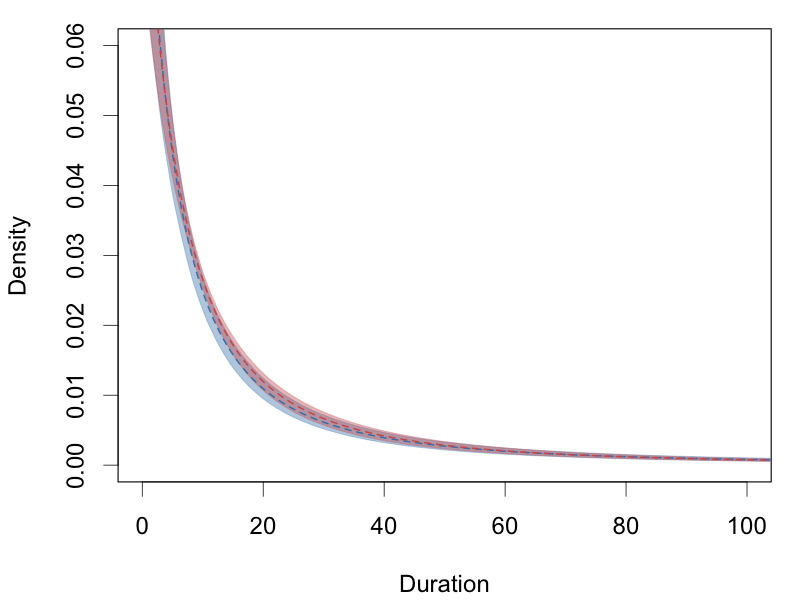

The data set involves a time series of average daily IVT magnitude calculated using ERA5, a climate reanalysis that provides hourly estimates of atmospheric variables. The time series has 14965 observations, spanning from January 1, 1979 to December 31, 2019, with all February 29s omitted, corresponding to the Santa Cruz city in California. The data are publicly available in the R package exdqlm. Using the quantile threshold, we obtained 749 point events of IVT exceedances. The histogram of the durations (Figure 2(c)) suggests a heavy right tail for the recurrence interval distribution.

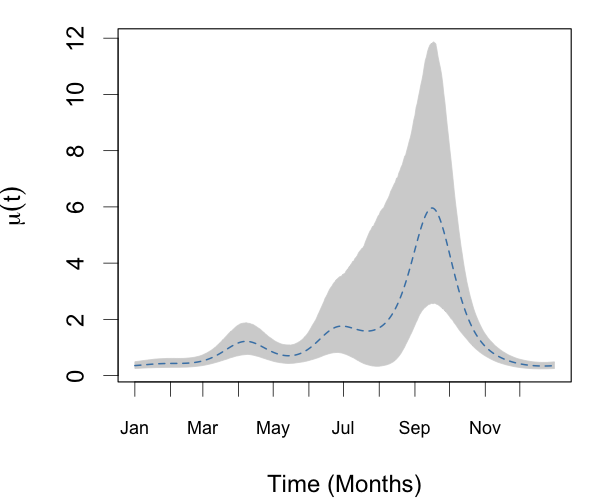

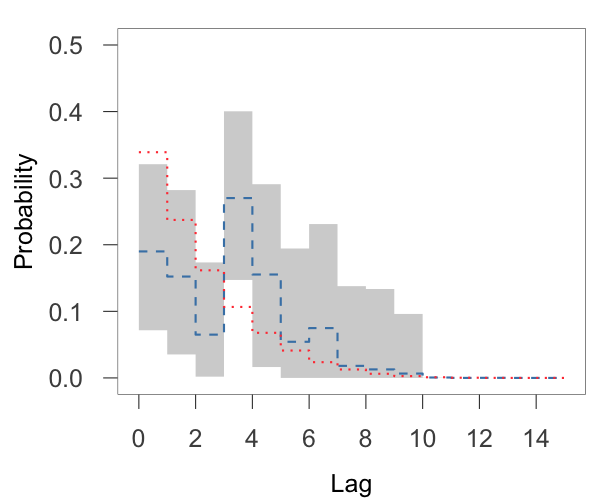

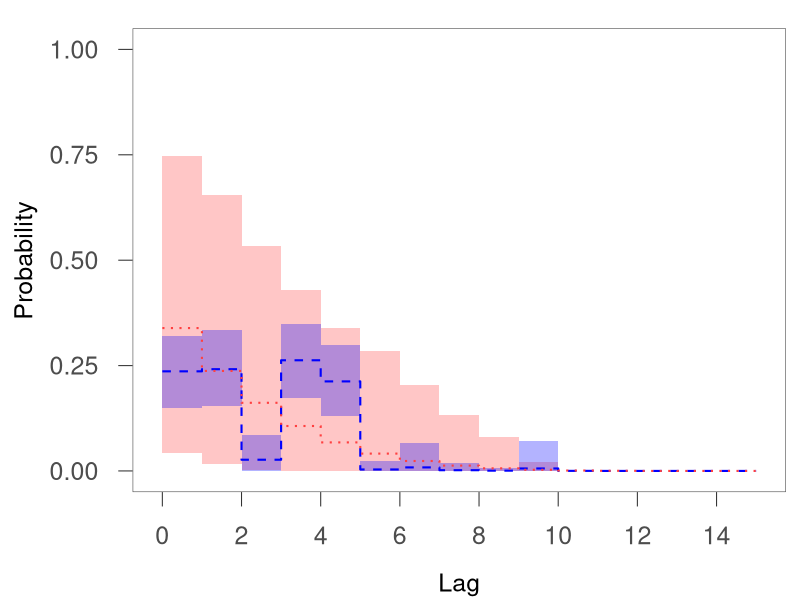

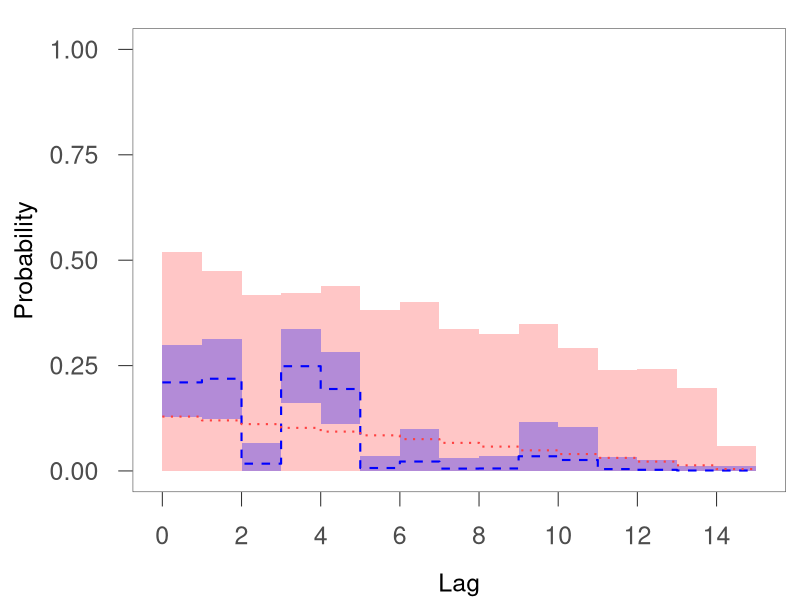

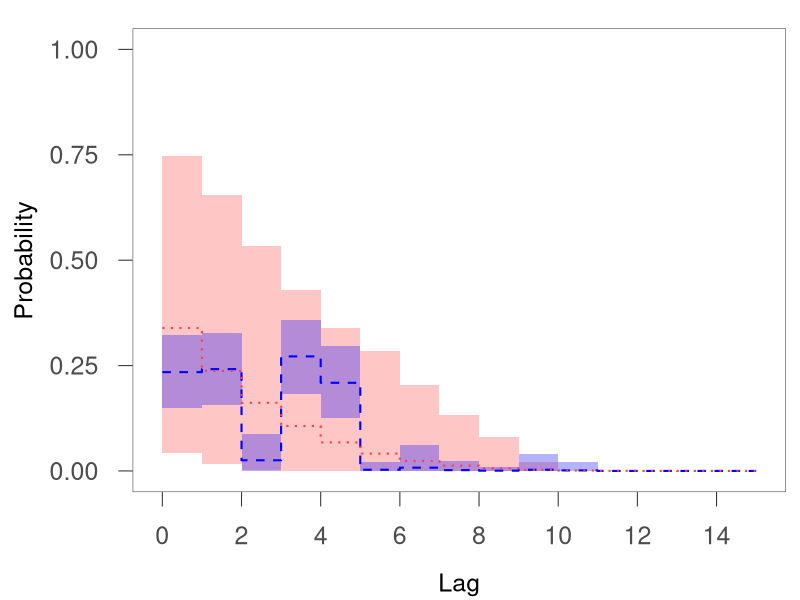

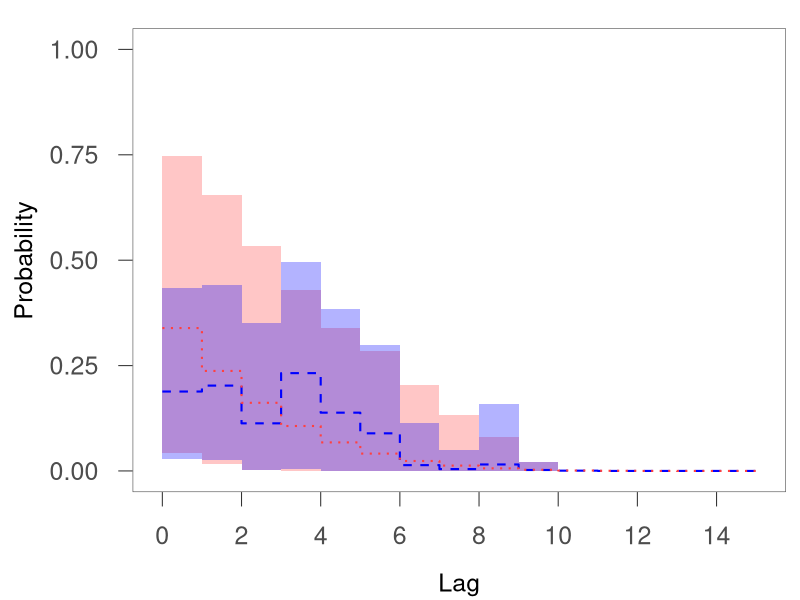

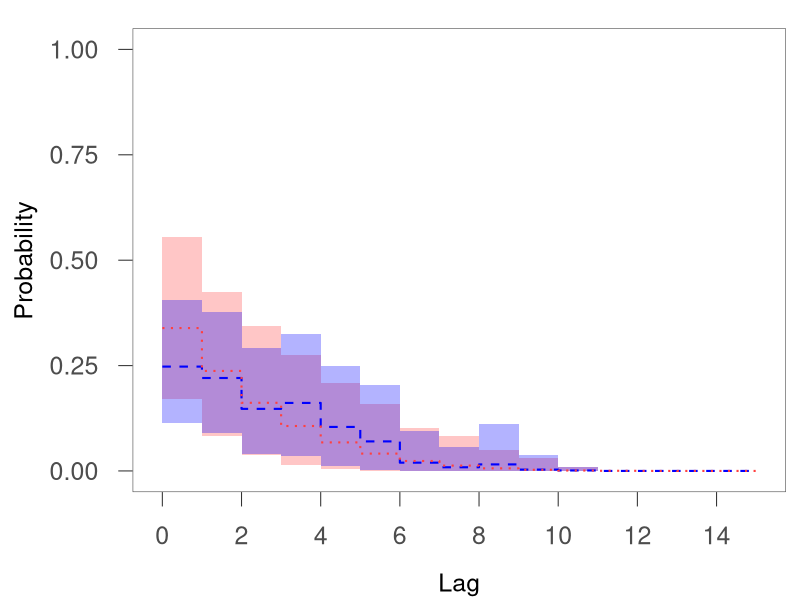

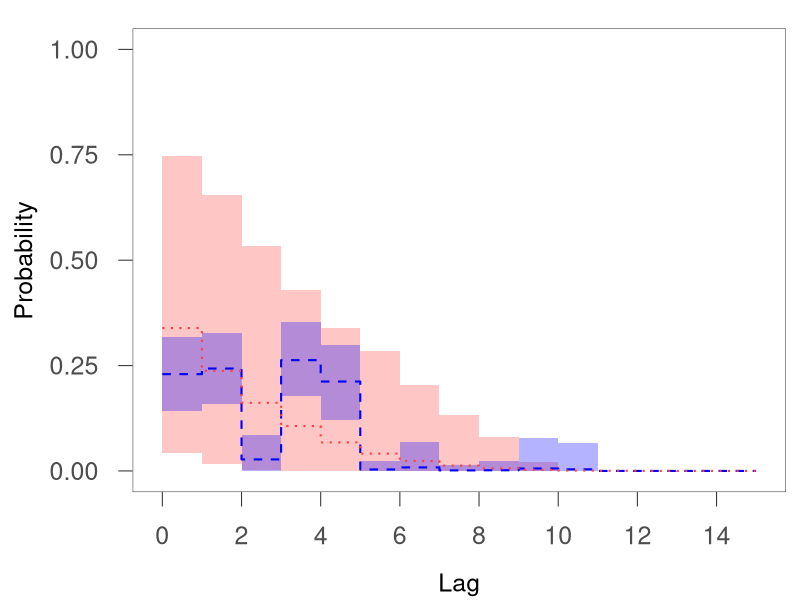

We consider the scaled-Lomax MTDPP. As previously discussed in Section 2.3, the model has a stationary scaled-Lomax marginal distribution for the recurrence intervals, and the conditional duration distribution converges to the exponential distribution with rate parameter , as . Let and be the observed event times and durations, respectively. To account for potential seasonality, we use the following multiplicative model, , with where , and is the period for daily data. We assume the stationary scaled-Lomax MTDPP model for the , such that the conditional duration density is . We took , and assigned mean-zero, dispersed normal priors to the regression parameter vector. The shape and scale parameters and received and priors, respectively. We chose model order ; this was based on the ACF and PACF plots of the original data and the detrended data based on a harmonic regression, with a sensitivity analysis for (details can be found in the Supplementary Material). For the weights, we considered a prior, which implies a decreasing trend in prior expectation (Figure 2(e)).

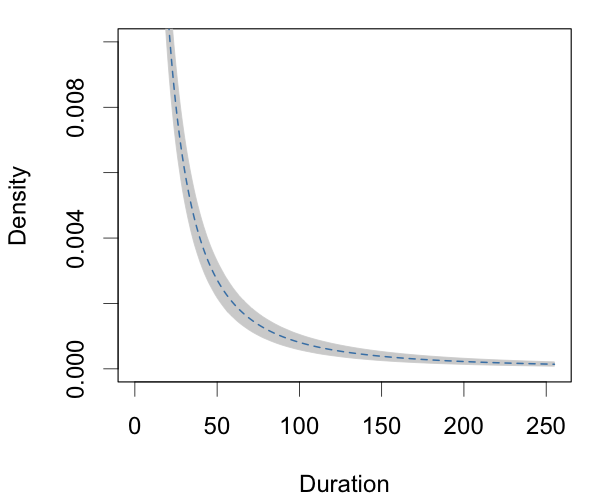

We report the results based on the multiplicative model fitted to the original data. The posterior mean and credible interval estimates of the harmonic component coefficients imply the presence of annual and semiannual seasonality. The posterior estimates of the corresponding coefficients are , , and . Figure 2(d) shows the function evaluated at a grid over a period of one year. Smaller durations between high IVT magnitudes tend to appear from November to March, corresponding to high atmospheric river frequency during that period. In fact, this time interval corresponds to the usual flooding period in California (e.g., the most recent floods in California were caused by multiple atmospheric rivers between December 2022 and March 2023). Figure 2(e) shows the estimated weights. Lags one, two, four and five are the most influential, which suggests serial dependence in the durations. The posterior mean and credible interval estimates of and were and , respectively. Note that the stationary marginal distribution of the process is , with finite mean for and finite variance for . Inference for suggests that, even after adjusting for seasonality, the distribution of the recurrence intervals is heavy tailed. In fact, Figure 2(f) shows a marginal density tail that decays very slowly, in particular when compared to the histogram of the observed durations in Figure 2(c), where the seasonality is not accounted for. The heavy-tailed recurrence interval distribution also indicates a cluster phenomenon of the IVT extremes.

4.3 Mid-price changes of the AUD/USD exchange rate

Financial markets involve complex human activities, with both external and internal factors driving market dynamics. It is suggested that, for high-frequency financial data, price dynamics is more endogenous, driven largely by internal factors within the market itself (Filimonov and Sornette, 2012). Therefore, to understand financial market microstructure, it is important to quantify the level of endogeneity, measured as the proportion of price movements due to internal rather than external processes. Here, we explore modeling for endogeneity quantification from the duration clustering perspective using the MTDCPP, where each price move is considered as an event. At the end of the section, we discuss our findings relative to alternative models.

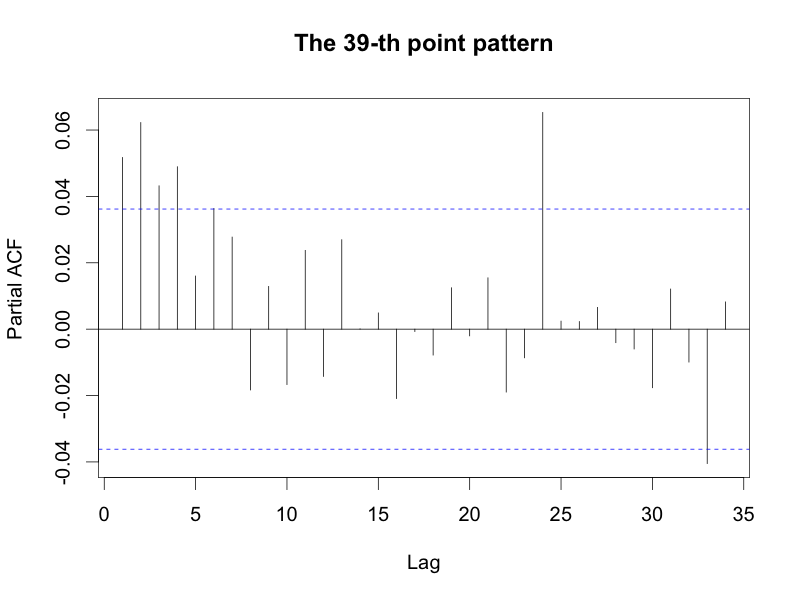

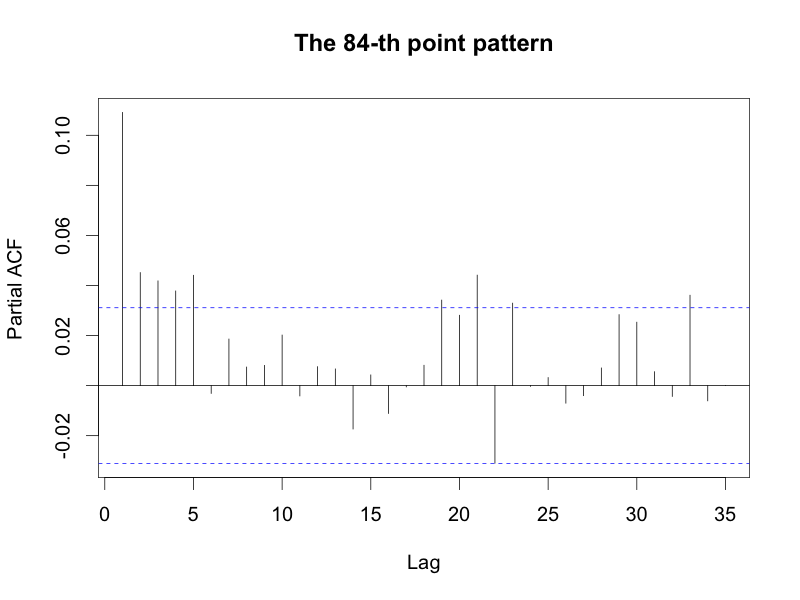

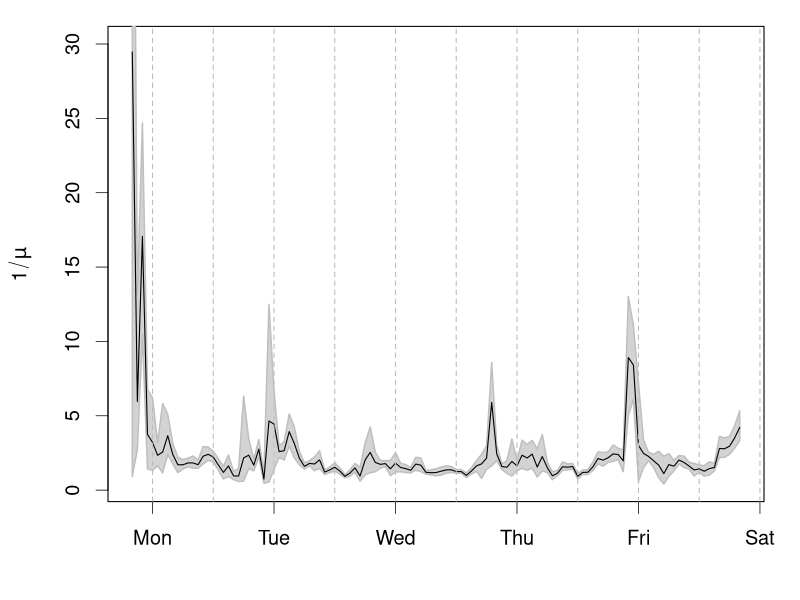

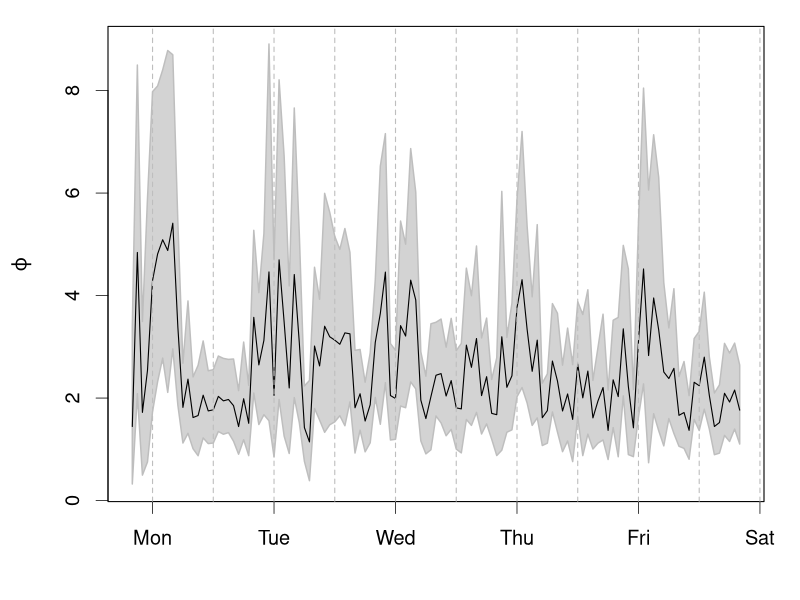

We analyze the price movements of the AUD/USD foreign exchange rate. A price movement is recorded when a mid-price change occurs, where mid-price is defined as the average of the best bid and ask prices (Filimonov and Sornette, 2012). The data set consists of 121 non-overlapping point patterns, with total number of events ranging from 108 to 3961. Each point pattern corresponds to an one-hour time window of the trading week from 20:00 Greenwich Mean Time (GMT) July 19 to 21:00 GMT July 24 in 2015. Analyzing sequences of point patterns within small time windows avoids to some extent the issue of nonstationarity, such as diurnal pattern. We refer to Chen and Stindl (2018) for more details about the data, which are available in R package RHawkes (Chen and Stindl, 2022).

We considered the Lomax MTDCPP, that is, model (9) with given by an exponential density with rate parameter , and corresponding to the stationary Lomax MTDPP. In particular, the self-exciting Lomax MTDPP is regarded as the driver of internal factors, such as market participants’ anticipations and reactions to market prices. In contrast, external information is driven by the exponential density, which is independent of the past durations. Thus, the probability corresponding to the Lomax MTDPP can be interpreted as the proportion of price movements due to endogenous interactions.

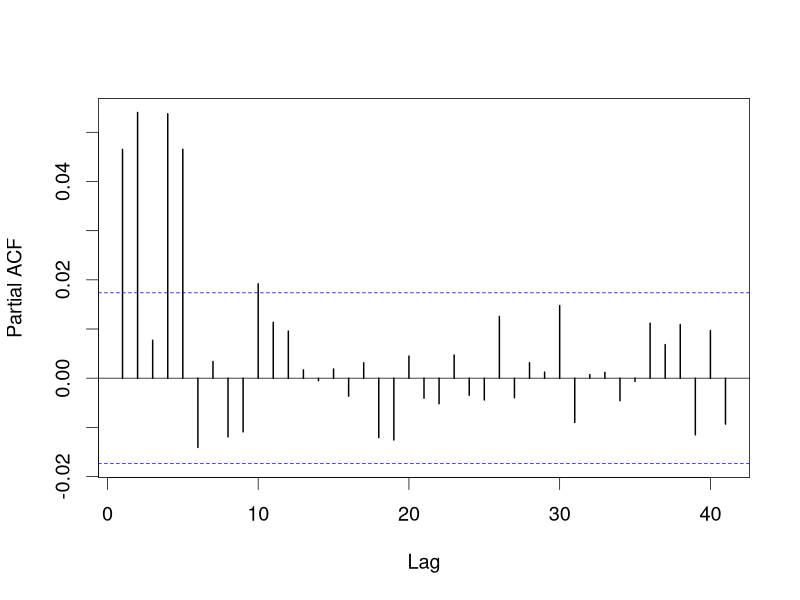

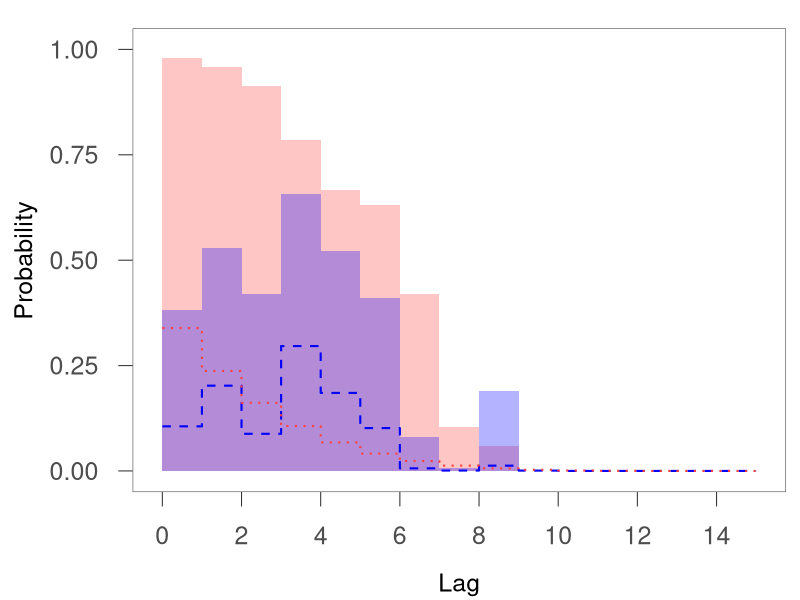

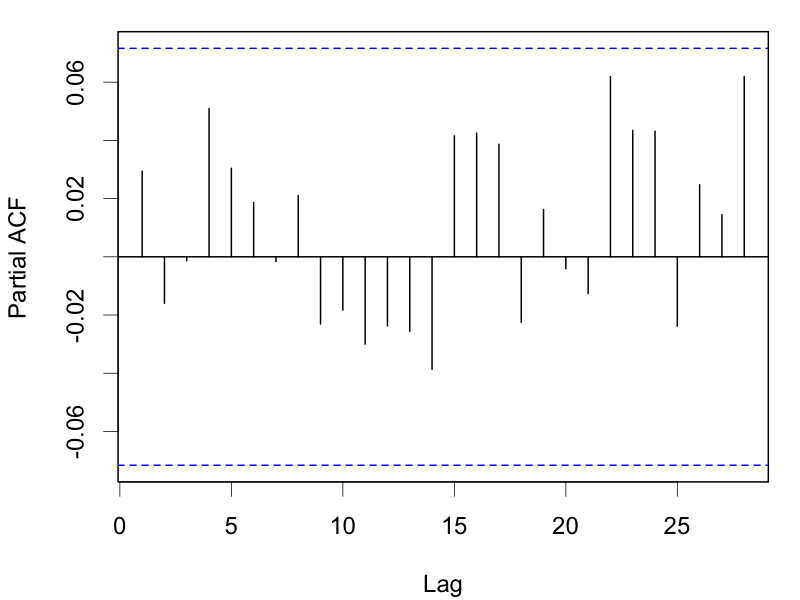

We applied the model to each of the 121 point patterns and, for illustrative purposes, considered the same model specification for all point patterns. Based on previous studies on market endogeneity, we used a prior for . The prior assigns small probabilities to values of around or , which correspond to the less likely scenarios where the market is driven by only an internal or an external process. For component-density parameters, we used a prior for , and and priors for the shape and scale parameter of the Lomax model, respectively. Based on the PACF of the observed durations (see the Supplementary Material for details), we chose model order for all point patterns, and the mixture weights were assigned a CDP prior.

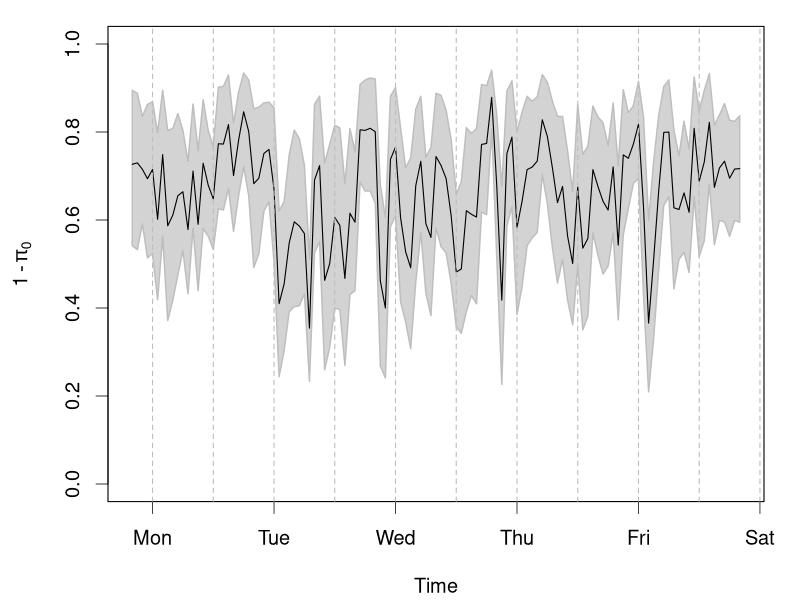

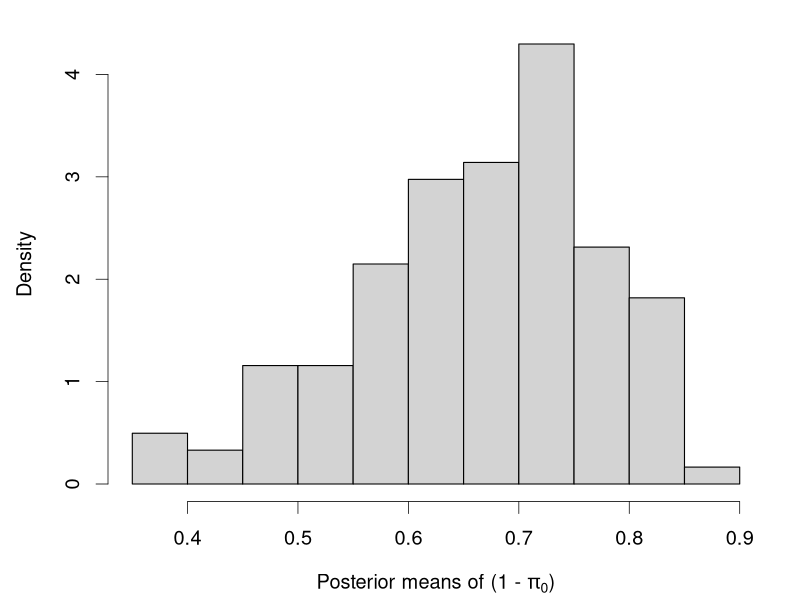

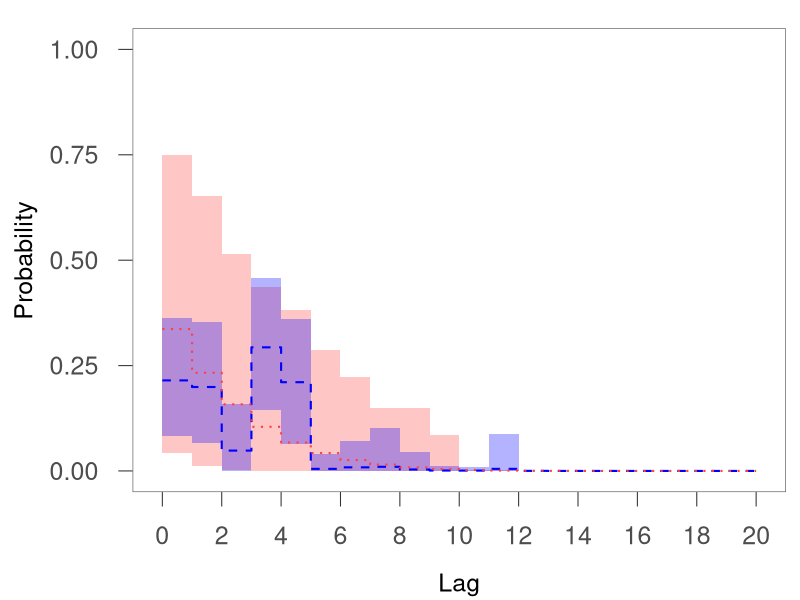

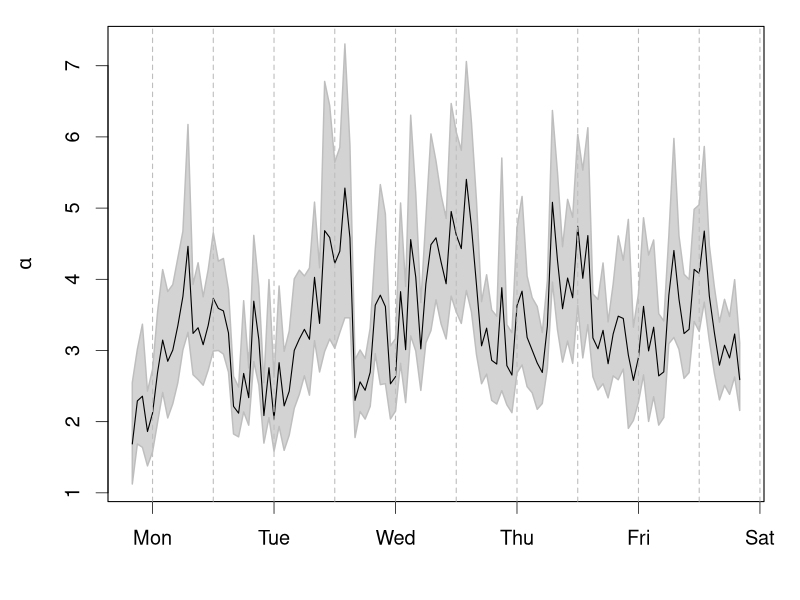

We focus on inference for the level of endogeneity ; additional results are available in the Supplementary Material. The time series of posterior means and interval estimates of (for the one-hour time windows) shows that the level of endogeneity fluctuated heavily over the trading week (Figure 3, left panel). The histogram of the posterior means is skewed to the left (Figure 3, right panel), with median and quartiles , suggesting that the market dynamics were mostly driven by internal processes.

A similar conclusion was drawn by Chen and Stindl (2018), where a renewal Hawkes process (RHawkes; Wheatley et al. 2016) was applied to the same data; the mean and quartiles of their estimates for the level of endogeneity over the trading week were, respectively, and . The RHawkes process extends the Hawkes process to capture dependence between clusters, by replacing the immigrant Poisson process with a renewal process. Both the Hawkes and RHawkes process models include a branching ratio parameter, which can be used to quantify the level of endogeneity (Filimonov and Sornette, 2012; Wheatley et al., 2016; Chen and Stindl, 2018). Under a different stochastic model structure, the Lomax MTDCPP is able to quantify the extent to which the observed dynamics are caused by internal factors versus external influences.

We note that using the MTDCPP for the present example does not require any stationarity assumptions. In contrast, stationarity is essential for both the Hawkes and RHawkes processes in order to use the branching ratio as an estimator for the level of endogeneity. However, as discussed in Filimonov and Sornette (2012), market activities are commonly nonstationary. The lack of stationarity is typically attributed to seasonal trends, which can be addressed by splitting the time window into small intervals, as shown in this example. Still, one has to balance the size of the intervals and the number of the events within the interval to ensure reliable estimates are produced. Moreover, even after removing seasonality, stationarity is not necessarily guaranteed. Therefore, MTDCPP models may be useful in applications where stationarity assumptions are not plausible.

5 Summary and discussion

We have developed a new class of stochastic models for temporal point patterns with self-excitation or self-regulation effects, identically distributed but dependent durations, or clustered durations. The modeling framework allows for different approaches to building the point process: through marginal duration distributions, when the inferential goal pertains to the intervals between event times; or through conditional hazard functions, when interest lies in the point process dependence structure on its history. Both strategies connect naturally to existing point process models. The former is analogous to renewal process modeling, while the latter involves the same motivation of Hawkes processes. We have prsented several examples of implementing these strategies. The Burr model, which allows for point process functionals with flexible shapes, can be considered as a default choice for general purposes, while the scaled-Lomax model, which provides flexible tail behavior, may be considered for scientific applications where such property is relevant.

Our framework builds from a structured mixture model for the point process conditional duration density. The resulting point process has restricted memory, i.e., its evolution depends on recent events. This assumption is generally suitable for relatively large point patterns. For scenarios where one anticipates more extensive history dependence, a large value for the order of the mixture model can be used. The nonparametric prior for the weights allows efficient inference with a large order. On the other hand, there are applications where data correspond to many processes that exhibit a relatively small number of point events, such as the analysis of recurrent event gap times for multiple patients in medical studies. For such data, a small order is more appropriate. In fact, even the special case where the conditional duration density depends on the most recent lag provides a meaningful generalization of renewal processes commonly used for this type of analysis.

In many applications, point patterns include information on marks, that is, random variables associated with each point event, such that the data generating mechanism corresponds to a marked point process. Consider, for instance, continuous marks, . The marked point process intensity can be developed from , where is the conditional intensity for the event times (referred to as the ground process intensity), and is the time-dependent mark distribution (Daley and Vere-Jones, 2003). The proposed framework can be utilized for marked point processes by combining an MTDPP or MTDCPP model for the ground process with a model for the mark distribution.

Acknowledgements

This research was supported in part by the National Science Foundation under award SES 1950902. The authors wish to thank two reviewers and an Associate Editor for valuable comments.

Supplementary Material

The Supplementary Material includes proofs for the theoretical results, details for the bivariate Burr distribution, additional details for the MCMC algorithms and predictions, additional data examples and results, MCMC diagnostics, and model checking results.

References

- Arnold et al. (1999) Arnold, B. C., Castillo, E., and Sarabia, J. M. (1999), Conditional Specification of Statistical Models, New York: Springer.

- Barata et al. (2022) Barata, R., Prado, R., and Sansó, B. (2022), “Fast inference for time-varying quantiles via flexible dynamic models with application to the characterization of atmospheric rivers,” The Annals of Applied Statistics, 16, 247–271.

- Bhogal and Thekke Variyam (2019) Bhogal, S. K. and Thekke Variyam, R. (2019), “Conditional duration models for high-frequency data: a review on recent developments,” Journal of Economic Surveys, 33, 252–273.

- Cavaliere et al. (2024) Cavaliere, G., Mikosch, T., Rahbek, A., and Vilandt, F. (2024), “Tail behavior of ACD models and consequences for likelihood-based estimation,” Journal of Econometrics, 238, 105613.

- Chen and Stindl (2018) Chen, F. and Stindl, T. (2018), “Direct likelihood evaluation for the renewal Hawkes process,” Journal of Computational and Graphical Statistics, 27, 119–131.

- Chen and Stindl (2022) — (2022), RHawkes: Renewal Hawkes Process. R package version 1.0.

- Coen et al. (2019) Coen, A., Gutiérrez, L., and Mena, R. H. (2019), “Modelling failures times with dependent renewal type models via exchangeability,” Statistics, 53, 1112–1130.

- Cook et al. (2007) Cook, R. J., Lawless, J. F., et al. (2007), The Statistical Analysis of Recurrent Events, New York: Springer.

- Corral (2004) Corral, Á. (2004), “Long-term clustering, scaling, and universality in the temporal occurrence of earthquakes,” Physical Review Letters, 92, 108501.

- Cowpertwait (2001) Cowpertwait, P. S. (2001), “A renewal cluster model for the inter-arrival times of rainfall events,” International Journal of Climatology, 21, 49–61.

- Daley and Vere-Jones (2003) Daley, D. J. and Vere-Jones, D. (2003), An Introduction to the Theory of Point Processes: Volume I: Elementary Theory and Methods, New York: Springer.

- Engle and Russell (1998) Engle, R. F. and Russell, J. R. (1998), “Autoregressive conditional duration: a new model for irregularly spaced transaction data,” Econometrica, 1127–1162.

- Ferguson (1973) Ferguson, T. S. (1973), “A Bayesian analysis of some nonparametric problems,” The Annals of Statistics, 209–230.

- Filimonov and Sornette (2012) Filimonov, V. and Sornette, D. (2012), “Quantifying reflexivity in financial markets: Toward a prediction of flash crashes,” Physical Review E, 85, 056108.

- Gaver and Lewis (1980) Gaver, D. P. and Lewis, P. (1980), “First-order autoregressive gamma sequences and point processes,” Advances in Applied Probability, 12, 727–745.

- Gelman et al. (2013) Gelman, A., Stern, H. S., Carlin, J. B., Dunson, D. B., Vehtari, A., and Rubin, D. B. (2013), Bayesian Data analysis, New York: Chapman and Hall/CRC, third edition.

- Grammig and Maurer (2000) Grammig, J. and Maurer, K.-O. (2000), “Non-monotonic hazard functions and the autoregressive conditional duration model,” The Econometrics Journal, 3, 16–38.

- Hassan and El-Bassiouni (2013) Hassan, M. Y. and El-Bassiouni, M. Y. (2013), “Modelling Poisson marked point processes using bivariate mixture transition distributions,” Journal of Statistical Computation and Simulation, 83, 1440–1452.

- Hassan and Lii (2006) Hassan, M. Y. and Lii, K.-S. (2006), “Modeling marked point processes via bivariate mixture transition distribution models,” Journal of the American Statistical Association, 101, 1241–1252.

- Hautsch (2011) Hautsch, N. (2011), Econometrics of Financial High-Frequency Data, New York: Springer Science & Business Media.

- Hawkes (1971) Hawkes, A. G. (1971), “Point spectra of some mutually exciting point processes,” Journal of the Royal Statistical Society: Series B (Methodological), 33, 438–443.

- Jacobs and Lewis (1977) Jacobs, P. and Lewis, P. (1977), “A mixed autoregressive-moving average exponential sequence and point process (EARMA 1, 1),” Advances in Applied Probability, 9, 87–104.

- Jiang et al. (2018) Jiang, Z.-Q., Wang, G.-J., Canabarro, A., Podobnik, B., Xie, C., Stanley, H. E., and Zhou, W.-X. (2018), “Short term prediction of extreme returns based on the recurrence interval analysis,” Quantitative Finance, 18, 353–370.

- Kottas and Sansó (2007) Kottas, A. and Sansó, B. (2007), “Bayesian mixture modeling for spatial Poisson process intensities, with applications to extreme value analysis,” Journal of Statistical Planning and Inference, 137, 3151–3163.

- Le et al. (1996) Le, N. D., Martin, R. D., and Raftery, A. E. (1996), “Modeling flat stretches, bursts outliers in time series using mixture transition distribution models,” Journal of the American Statistical Association, 91, 1504–1515.

- Modarres et al. (2017) Modarres, M., Kaminskiy, M. P., and Krivtsov, V. (2017), Reliability Engineering and Risk Analysis: A Practical Guide, Boca Raton: CRC Press.

- Ogata (1988) Ogata, Y. (1988), “Statistical models for earthquake occurrences and residual analysis for point processes,” Journal of the American Statistical Association, 83, 9–27.

- O’Hara (1995) O’Hara, M. (1995), Market Microstructure Theory, London: Blackwell.

- Pacurar (2008) Pacurar, M. (2008), “Autoregressive conditional duration models in finance: a survey of the theoretical and empirical literature,” Journal of Economic Surveys, 22, 711–751.

- Rutz et al. (2019) Rutz, J. J., Shields, C. A., Lora, J. M., Payne, A. E., Guan, B., Ullrich, P., O’brien, T., Leung, L. R., Ralph, F. M., Wehner, M., et al. (2019), “The atmospheric river tracking method intercomparison project (ARTMIP): quantifying uncertainties in atmospheric river climatology,” Journal of Geophysical Research: Atmospheres, 124, 13777–13802.

- Santhanam and Kantz (2008) Santhanam, M. and Kantz, H. (2008), “Return interval distribution of extreme events and long-term memory,” Physical Review E, 78, 051113.

- Sklar (1959) Sklar, M. (1959), “Fonctions de repartition an dimensions et leurs marges,” Publications de l’Institut de Statistique de L’Université de Paris, 8, 229–231.

- Strickland et al. (2006) Strickland, C. M., Forbes, C. S., and Martin, G. M. (2006), “Bayesian analysis of the stochastic conditional duration model,” Computational Statistics & Data Analysis, 50, 2247–2267.

- Tang and Li (2021) Tang, X. and Li, L. (2021), “Multivariate temporal point process regression,” Journal of the American Statistical Association, 1–16.

- Veen and Schoenberg (2008) Veen, A. and Schoenberg, F. P. (2008), “Estimation of space–time branching process models in seismology using an EM–type algorithm,” Journal of the American Statistical Association, 103, 614–624.

- Wheatley et al. (2016) Wheatley, S., Filimonov, V., and Sornette, D. (2016), “The Hawkes process with renewal immigration & its estimation with an EM algorithm,” Computational Statistics & Data Analysis, 94, 120–135.

- Wold (1948) Wold, H. (1948), “On stationary point processes and Markov chains,” Scandinavian Actuarial Journal, 1948, 229–240.

- Yang et al. (2018) Yang, C., Delcher, C., Shenkman, E., and Ranka, S. (2018), “Clustering inter-arrival time of health care encounters for high utilizers,” in 2018 IEEE 20th International Conference on e-Health Networking, Applications and Services (Healthcom), IEEE.

- Zheng et al. (2022) Zheng, X., Kottas, A., and Sansó, B. (2022), “On construction and estimation of stationary mixture transition distribution models,” Journal of Computational and Graphical Statistics, 31, 283–293.

Supplementary Material for “Mixture Modeling for Temporal Point Processes with Memory”

S1 Theoretical results

S1.1 Proofs of theorem and propositions

Proof of Theorem 1.

Consider a stationary MTD point process, that is, the corresponding duration process has a stationary marginal distribution. Thus, the durations are a collection of dependent random variables that are identically distributed. We assume that the first and second moments with respect to the stationary marginal distribution exist and are finite.

Denote by for all . Let be the last arrival time prior to or the arrival time at . For , We have that , and that . Note that is the average of the durations . By the strong law of large numbers for dependent non-negative random variables \citepsmkorchevsky2010strong, we have that, as , , since as , . Observing that , where the first term , and the second term , we can conclude that . ∎

Proof of Proposition 1.

Let be the duration associated with event time . By Definition 1 in the main paper, the conditional density of is , where , for . Then, according to (3) and (4) in the main paper, we have that , and .

Let be a marginal density of interest, and denote by the marginal density of , for . By condition (i) in Proposition 1, we have that . Then using both conditions (i) and (ii) in the proposition, we can show that for ,

| (1) |

where and is the joint density for random vector , for . The second equality in (1) follows the approach in Zheng et al. (2022).

∎

Proof of Proposition 2.

The definition of the conditional intensity function yields that , where the expectation is taken with respect to the probability distribution of the point process. Since our interest is in , consider time large enough such that .

Recall that , where and are the hazard and survival functions, respectively, associated with . Let . We have that

| (2) | ||||

For , by Jensen’s inequality, we have that

| (3) | ||||

where . Similarly, applying Jensen’s inequality, we obtain , and combining (2) and (3), we have that

If for all , then , for , and . Then we have that

Hence, the function . It follows that . ∎

Proof of Proposition 3.

Let , where the joint density of is , which corresponds to the bivariate Lomax distribution of Arnold et al. (1999). By change of variable, we obtain the joint density of , namely, , with normalizing constant . The marginal density of is

Since and are symmetric in the joint density , the marginal density . It follows that . Similarly, we have that . ∎

Proof of Proposition 4.

Consider the stationary scaled-Lomax MTDPP with marginal duration density . Suppose . The survival function of the conditional duration distribution can be expressed as

where . In particular, for , , for . When , , and . It follows that the weights satisfy for .

Then, for , we have that

| (4) | ||||

As , the limits of the first term and the second term in the th mixture component of (4) are and , respectively. More specifically, the limit of the first term is obtained by using the results that (i) ; (ii) , provided that both and exist, and .

Since , it follows that, as , the survival function of the conditional duration distribution converges to , which is the survival function of an exponential distribution with rate parameter .

∎

S1.2 Identifiability

Identifiability of a standard finite mixture model, commonly referred to as generic identifiability (e.g., \citealtsmfruhwirth2006finite), has been well addressed in the literature (see, e.g., \citealtsmteicher1961identifiability,teicher1963identifiability,yakowitz1968identifiability,chandra1977mixtures,kent1983identifiability,crawford1994application). Generally, a regular finite mixture model is said to be identifiable if no two sets of parameter values, up to permutation of the components, produce the same distribution or density \citepsmmclachlan2019finite. We refer to Chapter 3 in \citesmtitterington1985statistical for a detailed discussion of the generic identifiability and relevant theoretical results.

We present below a definition of the identifiability for MTDPPs.

Definition S3.

Given a realization of durations, , consider an MTDPP model with conditional duration density given in (4) of the main paper, with parameters , the associated parameter space, where is the vector of weights and denotes the component parameters. The MTDPP is said to be identifiable if for any two sets of parameters ,

| (5) |

for each and for all possible values of , implies that , , and , .

Definition S3 suggests that we can use established results for standard finite mixture models to verify the identifiability of an MTDPP, by treating the conditional density in (5) for each as a standard finite mixture model. A similar idea has been used in Hassan and Lii (2006) to verify the identifiability of their proposed bivariate MTD models. As examples, we demonstrate the identifiability of the Burr MTDPP, the Lomax MTDPP, and the scaled-Lomax MTDPP, which are illustrated in Section 2.3 of the main paper.

Burr MTDPP

To verify the identifiability of the class of Burr MTDPPs, it suffices to show that a finite mixture of the corresponding Burr distributions is identifiable. Identifiability for finite mixtures of Burr distributions has been studied in \citesmahmad1994small and \citesmal2016mixture. In particular, \citesmahmad1994small shows that, for the two-parameter Burr-Type-VII distribution with c.d.f. , the corresponding finite mixture model is identifiable with a common shape parameter , using Theorem 1 in \citesmteicher1963identifiability. More recently, \citesmal2016mixture shows that the finite mixtures of two-parameter Burr-Type-III distributions with c.d.f. is identifiable, using Theorem 2.4 in \citesmchandra1977mixtures.

Here, we show that the finite mixtures of three-parameter Burr-Type-VII distributions with c.d.f. is identifiable, using Theorem 2.4 in \citesmchandra1977mixtures.

Proof.

Let be the family of three-parameter Burr-Type-VII distributions. Consider the following transformation,

where is the beta function, and , for a random variable , is taken with respect to a Burr distribution with c.d.f. , where .

We order the family lexicographically by: if , or if but , or if but . Then we have that , where , . Take and note that in the closure of . Then we have that

since , , and . On the other hand, we have that

It follows that and Theorem 2.4 of \citesmchandra1977mixtures applies. ∎

Lomax and Scaled-Lomax MTDPPs

The scaled-Lomax distribution can be treated as a reparameterized Lomax distribution, and thus it suffices to prove the identifiability for the Lomax MTDPP. Note that \citesmahmad1988identifiability has verified that a finite mixture of Pareto-Type-I distributions is identifiable. Note that the Lomax distribution is a shifted version of the Pareto-Type-I distribution. Specifically, for a Pareto-Type-I distribution with c.d.f. , the c.d.f. of the corresponding Lomax distribution is . It follows that a finite mixture of Lomax distributions is identifiable. Based on Definition S3, we have that , , , and , for each and for each . It follows that for each and for each . Thus, the class of Lomax MTDPPs is identifiable, and so is the class of scaled-Lomax MTDPPs.

S2 Bivariate Burr distribution

Let be a random variable, and its cumulative distribution function (c.d.f.) is . We say that follows a three-parameter Burr distribution \citepsmtadikamalla1980look, denoted as . We will use such notation throughout to indicate either the distribution or its density for a Burr random variable, depending on the context (we follow the same notation approach for other distributions).

Consider a bivariate random vector , with marginal c.d.f.s for and given by and , respectively. The joint c.d.f. is specified by the heavy right tail (HRT) copula given by

| (6) |

where , , and \citepsmfrees1998understanding.

We set the copula parameter to be the same as the second shape parameter of the Burr distribution, that is, . Replace and with and , respectively, in (6). Then, the joint c.d.f. of the random vector is given by

The conditional c.d.f. of given is . Note that . It follows that

| (7) | ||||

where . Therefore, the conditional distribution of given is a Burr distribution, . Since the HRT copula is symmetric in its arguments, the conditional distribution of given is also a Burr distribution.

We note that the bivariate Burr distribution defined through the HRT copula and Burr marginals was considered in \citesmventer2002tails. However, the expressions for the conditional c.d.f.s reported in \citesmventer2002tails include an error. Equation (7) provides the corrected expression for the conditional c.d.f. of given .

S3 Additional details for Bayesian implementation

In Section S3.1, we provide details for posterior prediction using MTDPPs. Posterior inference and prediction for MTDCPPs are introduced in Section S3.2.

The observed point pattern comprises event times , with corresponding observed durations , for . Let , for , represent the information from the observed point pattern. Note that, as its description highlights, includes the information that the (unobserved) event time is greater than the upper bound of the time observation window, i.e., that the (unobserved) duration is greater than .

S3.1 Posterior prediction for MTDPPs

To obtain the posterior predictive density for the next duration, , we first derive the conditional density for the next duration given the model parameters, , and . As discussed above, implies conditioning on event . Therefore, using Equation (4) in the main paper, we obtain:

| (8) | ||||

Here, the weights , and , for , is the -th component density for truncated below at .

Hence, the posterior predictive density for the next duration is given by

| (9) |

for , where is the posterior distribution of .

Then, for , the -step-ahead posterior predictive density of duration ,

| (10) | ||||

For in-sample prediction of , for , given the observed point pattern , the posterior predictive density for is given by

| (11) |

S3.2 Posterior inference and prediction for MTDCPPs

Consider an MTDCPP for durations , and take . The likelihood conditional on is

| (12) | ||||

where . The vectors and , respectively, collect the parameters of the independent duration density and the MTDPP component densities , . A Bayesian model formulation involves priors for parameters . The priors for and , respectively, depend on particular choices of the densities and , . For , we consider a beta prior, denoted as . For the weight vector , we use the same prior as that for the MTDPP, which can be found in Section 3.1 of the main paper. In particular, the vector follows a Dirichlet distribution with shape parameter vector .

We outline an MCMC posterior simulation method, Metropolis-within-Gibbs, for the model parameters of MTDCPP. For more efficient notation, we rewrite the MTDCPP transition density as

where , , , for , and .

We augment the model with configuration variables , taking values in , with discrete distribution , where if and otherwise, for . Therefore, indicates that the duration is generated from , and indicates that is generated from the th component of the MTDPP, for . Note that the likelihood normalizing term in (12) can be written as , where and , for . Similarly with the observed durations, we can introduce a configuration variable to identify the component of the mixture for . The posterior distribution of the augmented model is proportional to

The posterior full conditional distribution of is a discrete distribution on with probabilities proportional to , for , and with probabilities proportional to , for . , for , where returns the size of set . Given the configuration variables, we update the weights with a Dirichlet posterior full conditional distribution with parameter vector . The beta prior for yields a conjugate posterior full conditional distribution, . Posterior updates for parameters and , respectively, depend on and , . Implementation details for the MTDCPP model in Section 4.3 of the main paper are provided in Section S4.

Turning to posterior prediction for MTDCPPs. The conditional duration density for , denoted as , can be obtained similarly by replacing and in (8), respectively, with and (both and are available in Section 2.4 of the main paper). Then, the posterior predictive density of can be obtained by marginalizing with respect to the model parameters’ posterior distribution . For , the posterior predictive density of is obtained by replacing the MTDPP conditional duration density , , and in (10), respectively, with the MTDCPP conditional duration density in (9) of the main paper, , and . Finally, for in-sample predictions, the posterior predictive density of , for , can be obtained by replacing the MTDPP conditional duration density and in (11), respectively, with the MTDCPP conditional duration density in (9) of the main paper and the posterior distribution .

S4 MCMC algorithms

We outline the posterior simulation steps for the Burr MTDPP, the extended scaled-Lomax MTDPP, and the Lomax MTDCPP models illustrated in Section 4. Given an observed point pattern , we have that for , and we take . Our posterior inference is based on a likelihood, conditional on . Posterior samples of model parameters and latent variables are obtained with Metropolis-within-Gibbs updates, by iteratively sampling from their posterior full conditional distributions. Throughout the remainder of this section, for a generic parameter or latent variable , we denote as its posterior full conditional distribution or density, depending on the context.

S4.1 Burr MTDPP

We associate each with a latent discrete variable such that

,

, and similarly, consider a latent discrete variable

for such that

.

We consider independent priors

for the Burr-distribution parameters .

Then the joint posterior distribution of

the model parameters and latent variables,

, is proportional to

where , and is the survival function associated with the Burr distribution, .

Take , where and . Then we can obtain the posterior samples of by iterating the following steps.

-

(i)

Update with target distribution , using a random walk Metropolis step implemented on the log scale with a Gaussian proposal distribution.

-

(ii)

Update with target distribution , using a random walk Metropolis step implemented on the log scale with a Gaussian proposal distribution.

-

(iii)

Sample from a gamma distribution with shape parameter and rate parameter truncated at the interval , denoted as , where and .

-

(iv)

Sample , , from

and sample from

-

(v)

Sample from a Dirichlet distribution , where , for .

S4.2 Extended scaled-Lomax MTDPP

Let , with . The conditional duration density is , for .

Denote ,

and let be the th component of , for .

We introduce a collection of configuration variables

such that .

We consider independent priors

for parameters .

Then the joint posterior distribution of the model parameters and

latent variables,

, is

proportional to

where is the survival function associated with the distribution .

Let , , and . Take

Then we can obtain the posterior samples of by iterating the following steps.

-

(i)

Update with target distribution , using a random walk Metropolis step with a Gaussian proposal distribution, for .

-

(ii)

Update with target distribution , using a random walk Metropolis step implemented on the log scale with a Gaussian proposal distribution.

-

(iii)

Update with target distribution , using a random walk Metropolis step implemented on the log scale with a truncated Gaussian proposal distribution.

-

(iv)

Sample , , from

and sample from

-

(v)

Sample from a Dirichlet distribution , where , for .

S4.3 Lomax MTDCPP

The Lomax MTDCPP conditional duration density, for , can be written as , where , , and , for . Let and be the survival functions associated with and , respectively.

We augment the model with latent variables , with discrete distribution , for . For parameters , we consider independent priors . Then the joint posterior distribution of the model parameters and latent variables, , is proportional to

Let , for . Take

where , and .

We can obtain the posterior samples of by iterating the following steps.

-

(i)

Sample from a gamma distribution with shape parameter and rate parameter .

-

(ii)

Sample from a truncated gamma distribution , with , and .

-

(iii)

Update with target distribution , using a random walk Metropolis step implemented on the log scale with a Gaussian proposal distribution.

-

(iv)

Sample , , from

and sample from

where , and, for , .

-

(v)

Sample from a Dirichlet distribution .

-

(vi)

Sample from a beta distribution .

S5 Additional simulation studies

S5.1 First simulation study: Comparison with ACD models

MTDPPs are duration-based models for point processes with memory. In this section, we compare MTDDPs with alternative duration-based models, the autoregressive conditional duration (ACD) models, which are widely used for modelling point process dynamics via dependent durations in many fields, such as healthcare, network traffic, reliability engineering, and predominantly finance and economics.

Consider an ordered sequence of event times , and durations , . We consider the following Burr ACD model:

| (13) | ||||

for , where the innovations are independent and identically distributed as the Burr distribution considered in Grammig and Maurer (2000), denoted as , with density , where and . The parameter is taken as a function of and so that , for all , to ensure identifiability of the Burr ACD model in (13). Specifically,

| (14) |