When can weak latent factors be statistically inferred?

Abstract

This article establishes a new and comprehensive estimation and inference theory for principal component analysis (PCA) under the weak factor model that allow for cross-sectional dependent idiosyncratic components under nearly minimal the factor strength relative to the noise level or signal-to-noise ratio. Our theory is applicable regardless of the relative growth rate between the cross-sectional dimension and temporal dimension . This more realistic assumption and noticeable result requires completely new technical device, as the commonly-used leave-one-out trick is no longer applicable to the case with cross-sectional dependence. Another notable advancement of our theory is on PCA inference — for example, under the regime where , we show that the asymptotic normality for the PCA-based estimator holds as long as the signal-to-noise ratio (SNR) grows faster than a polynomial rate of . This finding significantly surpasses prior work that required a polynomial rate of . Our theory is entirely non-asymptotic, offering finite-sample characterizations for both the estimation error and the uncertainty level of statistical inference. A notable technical innovation is our closed-form first-order approximation of PCA-based estimator, which paves the way for various statistical tests. Furthermore, we apply our theories to design easy-to-implement statistics for validating whether given factors fall in the linear spans of unknown latent factors, testing structural breaks in the factor loadings for an individual unit, checking whether two units have the same risk exposures, and constructing confidence intervals for systematic risks. Our empirical studies uncover insightful correlations between our test results and economic cycles.

Keywords: factor model, principal component analysis, weak factors, cross-sectional correlation, inference, signal-to-noise ratio.

1 Introduction

The factor model, a pivotal tool for analyzing large panel data, has become a significant topic in finance and economics research (e.g., Chamberlain and Rothschild,, 1983; Fama and French,, 1993; Stock and Watson,, 2002; Bai and Ng,, 2002; Giglio and Xiu,, 2021; Fan et al., 2021b, ). The estimation and inference for factor models are crucial in economic studies, particularly in areas like asset pricing and return forecasting. In the era of big data, the factor model has gained increased prominence in capturing the latent common structure for large panel data, where both the cross-sectional and temporal dimensions are ultra-high (see, e.g., recent surveys Bai and Wang,, 2016; Fan et al., 2021a, ). Principal component analysis (PCA), known for its simplicity and effectiveness, is closely connected with the factor model and has long been a key research topic of interest in the econometric community (e.g., Stock and Watson,, 2002; Bai and Ng,, 2002; Bai,, 2003; Onatski,, 2012; Fan et al.,, 2013; Bai and Ng,, 2013, 2023).

As pointed out by Giglio et al., (2023), most theoretical guarantees for the PCA approach to factor analysis rely on the pervasiveness assumption (e.g., Bai and Ng,, 2002; Bai,, 2003). This assumption requires the signal-to-noise ratio (SNR), which measures the factor strength relative to the noise level, to grow with the rate of – the square root of the cross-sectional dimension. However, many real datasets in economics do not exhibit sufficiently strong factors to meet this pervasiveness assumption. When the SNR grows slower than , the resulting model is often called the weak factor model (e.g., Onatski,, 2009, 2010). Extensive research has been dedicated to the weak factor model (e.g., Onatski,, 2012; Bailey et al.,, 2021; Freyaldenhoven,, 2022; Uematsu and Yamagata, 2022a, ; Uematsu and Yamagata, 2022b, ; Bai and Ng,, 2023; Jiang et al.,, 2023; Choi and Yuan,, 2024), among which the PC estimators (the estimators via the PCA approach) have been a primary subject. Recently, Bai and Ng, (2023); Jiang et al., (2023); Choi and Yuan, (2024) studied the consistency and asymptotic normality of the PC estimators for factors and factor loadings in the weak factor model. In the extreme case (also called the super-weak factor model) where the SNR is , Onatski, (2012) showed that the PC estimators are inconsistent.

This paper establishes a novel and comprehensive theory for PCA in the weak factor model. Our theory is non-asymptotic and can be easily translated to asymptotic results. The conditions we propose for the asymptotic normality of PC estimators are optimal in the sense that, surprisingly different from the existing literature, the required growth rate of the SNR for consistency aligns with that for asymptotic normality, differing only by a logarithmic factor. In particular, in the regime , where is the temporal dimension, we prove that asymptotic normality holds as long as the SNR grows faster than a polynomial rate of , and this result is a substantial advance compared with the existing results that require the SNR to grow with a polynomial rate of (e.g., Bai and Ng,, 2023; Jiang et al.,, 2023; Choi and Yuan,, 2024).

The most innovative part of our theory lies in establishing a closed-form, first-order approximation of the PC estimator, that is, we decompose the PC estimator into three components — the ground truth, a first-order term, and the higher-order negligible term. We express the first-order term explicitly using the parameters in the factor model. This closed-form characterization paves the way for us to establish the asymptotic normality and design various test statistics for practical applications. Our theory is based on novel applications of the leave-one-out analysis and matrix concentration inequalities. Moreover, our findings provide valuable insights and practical implications for a range of econometric problems related with PCA, e.g., macroeconomic forecasting based on factor-augmented regressions (e.g., Bai and Ng, 2006a, ).

We demonstrate the practical applications of our theories using both synthetic and real datasets. First, we design an easy-to-implement statistic for factor specification test (e.g., Bai and Ng, 2006b, ) — whether an observed factor is in the linear space spanned by the latent common factors or not. A key innovation of our approach is the ability to conduct this test in any flexible subset of the whole period, owing to the row-wise error bound in our theory. We utilize the monthly return data of the S&P 500 constituents from 1995 to 2024, along with the data of the Fama-French three factors, then run the factor test in a rolling window manner (e.g., Fan et al.,, 2015). Our results uncover a notable decline in the importance and explanatory power of the size factor during the 2008 financial crisis, and of both the size and value factors during the COVID-19 pandemic around 2019. These findings are supported by our test results, which reject the null hypothesis that these factors are in the linear space of latent factors.

Then, we design a test statistic for the structural break of betas (e.g., Stock and Watson,, 2009; Breitung and Eickmeier,, 2011), and apply it to the aforementioned S&P 500 constituents data. Our novelty is that our test statistic works in the weak factor model without the pervasiveness assumption, which is required in prior work. We test for each stock to determine if the beta has changed before and after the three recessions covered by our data — the Early 2000s Recession, the 2008 Great Recession, and the COVID-19 Recession. We find that in each recession, the sectors most affected by the shocks, where many stocks exhibited structural breaks in betas, correspond reasonably to the causes of these economic recessions. For example, during the 2008 Great Recession, marked by the subprime mortgage crisis, the financial sector experienced a strong impact, which aligns with its exposure to mortgage-backed securities and other related financial instruments. During the COVID-19 Recession, the Health Care and Real Estate sectors were significantly impacted, reflecting the uncertainties brought about by lockdowns and health crises due to the pandemic. Additionally, we develop statistical tests for the betas to evaluate the similarity in risk exposure between two stocks and construct valid confidence interval for the systematic risk of each stock.

The rest of the paper is organized as follows. Section 2 introduces the model setup, basic assumptions, and notation. In Section 3, we show our main results on the first-order approximations for the PC estimators, and present the asymptotic normality results as corollaries. Section 4 provides a detailed comparison of our results with related work. In Section 5, we showcase four applications in econometrics based on our main results. Section 6 collects the numerical results in both simulated data and real data. More related works are discussed in Section 7, and the paper concludes with a discussion on future directions in Section 8.

2 Models, assumptions, and notation

2.1 Model setup

Let be the number of cross-sectional units and be the number of observations. Consider the factor model for a panel of data

| (2.1) |

where is the latent factor, is the number of factors, is a vector of factor loadings, and represents the idiosyncratic noise. Viewing as the excess return of the -th asset at time , the model (2.1) is intimately linked with the multi-factor pricing model. This model originates from the Arbitrage Pricing Theory (APT) developed by Ross, (1976) and finds extensive applications in finance.

To compact the notation, we denote by the factor loading matrix. Let and . Then, the factor model (2.1) can be expressed as , or written in a matrix form as follows

| (2.2) |

where , , and are the panel data, the factor realizations, and the idiosyncratic noise matrix, respectively.

In our setup, the only observable part is the panel data . We are interested in the estimation and inference for both the latent factors and factor loadings via the PCA approach.

2.2 Basic assumptions

We propose some basic assumptions as follows. Note that the factor model has the rotation (indeed affine transform) ambiguity (e.g., Bai and Ng,, 2013), that is, the factor loadings and latent factors are not identifiable since holds for any invertible matrix . Without loss of generality, we assume that the columns of are orthogonal and the covariance of is the identity matrix, as stated in Assumption 1 below.

Assumption 1.

For , the factor has mean zero and the identity covariance matrix. The factor loading matrix has orthogonal columns:

| (2.3) |

where .

Assumption 1 is a standard identification condition for the factor model (e.g., Fan et al.,, 2013). The singular values of the factor loading matrix characterize the strengths of the latent factors.

Next, to accommodate the cross-sectional correlation in the noise and to facilitate leave-one-out analysis in our technical proof, we propose Assumption 2 for the noise matrix , specifying its structure and the distribution of its entries.

Assumption 2.

The idiosyncratic noise matrix is given by

| (2.4) |

Here, is a positive definite matrix and is the symmetric square root of ; is a matrix; The entries of are independent sub-Gaussian random variables that satisfy

for , where is the sub-Gaussian norm (see Definition 2.5.6 in Vershynin,, 2017).

The nonzero off-diagonal entries of characterize the cross-sectional correlations in the idiosyncratic noise . Though the noise terms are independent under Assumption 2, our theory could potentially be generalized to the cases where the temporal correlations are present in the noise matrix , and this generalization is an interesting future direction. The formulation (2.4) imposes additional structural constraints on the noise matrix. However, such assumptions are commonplace in the study of the weak factor model; see similar assumptions in Onatski, (2010, 2012).

Then, to establish the non-asymptotic results via the concentration inequalities, we propose the following assumption on the distribution of the factors.

Assumption 3.

The factor realization is independent with the noise matrix ; The factors are independent and sub-Gaussian random vectors in satisfying that

2.3 Notation

We introduce some notation that will be used throughout the paper. For two sequences and , we write (or equivalently, ) if , i.e., there exist a constant and an integer such that, holds for any ; write if both and hold and (or equivalently, ) if .

For a symmetric matrix , we denote by and its minimum and maximum eigenvalues. For a vector , we denote , , and as the -norm, -norm, and supremum norm, respectively. Consider any matrix . We denote by and the -th row and the -th column of . We let and denote the spectral norm, the Frobenius norm, and the -norm (i.e., ), respectively. For an index set (resp. ), we use to denote its cardinality, and use (resp. ) to denote a submatrix of whose rows (resp. columns) are indexed by . We let , , and denote the column subspace of , the generalized inverse of , and the projection matrix onto the column space of .

We denote by the diagonal matrix whose diagonal entries are given by . Let be the identity matrix. We denote by the set of all orthonormal (or rotation) matrices. For a non-singular matrix with SVD , we denote by the following orthogonal matrix . Then we have that, for any two matrices with , among all rotation matrices, the one that best aligns and is precisely (see, e.g., Appendix D.2.1 in Ma et al.,, 2020), namely,

3 Main results

In this section, we demonstrate the desirable statistical performance of PCA in weak factor models. We will first present a master result (cf. Theorem 1) on subspace error decomposition. Based on this key result, we derive non-asymptotic distributional characterization for our estimators for the factors and factor loadings, paving the way to data-driven statistical inference.

First, we formally introduce the PC estimators of the factor and factor loadings in Algorithm 1.

Our master result focuses on the subspace estimates and . We define some relevant quantities first. Denote by the SVD of , where both and have orthonormal columns, and satisfies that . We define .

3.1 A first-order characterization of subspace perturbation errors

Before presenting our master results, we list two key assumptions on the SNR. To characterize the SNR, we define

Here, the signal strength, which is the factor strength in our case, is effectively represented by , the smallest singular value of the factor loading matrix . The noise level is captured by the norm of the covariance matrix for the idiosyncratic noise (cf. (2.4)). The SNRs , , and are similar, though their denominators adopt different norms of . The inclusion of -norms and , though less common than the spectral norm , is that our main results are on the row-wise error bound and we need these norms in the matrix inequalities for technical reasons. Then, two crucial assumptions on SNR are as follows.

Assumption 4.

There exists a sufficiently large constant such that

| (3.1) |

Assumption 5.

There exists a sufficiently large constant such that

| (3.2) |

Assumption 4 implies Assumption 5 due to the elementary inequality . On the other hard, , where is the maximum number of nonzero elements of in each row, which is small when is sparse. In particular, when the noise covariance matrix is diagonal (i.e., no cross-sectional correlations, also known as the strict factor model (Ross,, 1976; Fan et al.,, 2008; Bai and Shi,, 2011)), we have that . In this case, Assumption 4 is equivalent with Assumption 5. Throughout the paper, we denote by , , , , , , etc. the generic constants that may vary from place to place. We are now ready to present our main results as follows.

Theorem 1.

Assume that and for some sufficiently large constant . Consider the first-order expansions

| (3.3a) | ||||

| (3.3b) | ||||

where and are two global rotation matrices. Under Assumptions 1, 2, and 3, we have, with probability at least , the remainder terms and are higher-order negligible terms that satisfy the following bounds:

(i) Under Assumption 4, there exists some universal constant such that, uniformly for all ,

(ii) Under Assumption 5, there exists some universal constant such that, uniformly for all ,

The perturbation bounds in Theorem 1 pave the way for the statistical inference of the factor loadings and factors. The reasons why the quantities presented in Theorem 1 relate to the factor loadings and factors are that, as demonstrated in Lemma 2, the column subspaces of and are identical, as are those of and .

To show how strong our SNR condition is, we examine scenarios where there is no correlation in the noise matrix , i.e., is diagonal as in the strict factor model. In this case, the SNRs satisfy , where . Then Assumptions 4 and 5 match the minimal condition required for the consistent estimations of the left and right singular subspaces (e.g., Yan et al.,, 2024), up to log factors.

To explain that why and are higher-order negligible terms, we compare their bounds with the magnitude of the first-order terms and . For simplicity, we consider the setting where , , is well-conditioned (i.e., ), and is incoherent (see, e.g., Definition 3.1 in Chen et al., 2021a, ); the matrix can be proven to be incoherent since . Then, the typical size of the -th row of the first-order term can be measured by . Standard computations yield . Similarly, for the first-order term , we have that . Then, using the row-wise bounds for and in Theorem 1, we obtain that

| (3.4a) | |||

| and | |||

| (3.4b) | |||

The last inequality in (3.4a) (resp. (3.4b)) implies that the first-order term (resp. ) dominates the higher-order term (resp. ), provided that the SNRs grow at polynomial rate of : and (resp. ). These conditions are less stringent than the assumptions in the prior work (e.g., Bai and Ng,, 2023; Jiang et al.,, 2023; Choi and Yuan,, 2024) that required the SNR to grow with a polynomial rate of .

As we will show later, Theorem 1 is the foundation to design test statistics and conduct statistical inference for the factors, factor loadings, and other parameters of interest. To the best of our knowledge, the non-asymptotic first-order approximations (3.3a)–(3.3b) are new in the statistics and econometrics literature. While similar findings exist in the fields of low-rank matrix completion and spectral methods, the closest result to ours is Theorem 9 of Yan et al., (2024). However, they assumed that the entries of the noise matrix are independent, while we allow the presence of cross-sectional correlations in the noise matrix .

Our results in Theorem 1 are nontrivial generalizations of those in Yan et al., (2024). We note that their proof of row-wise error bounds via leave-one-out (LOO) technique requires constructing an auxiliary matrix that is independent with the target row. This contruction is obtained by zeroing the row with the same position in noise matrix. However, this approach does not work in our case because it is still correlated with the target row due to the cross-sectional correlation among all rows. We overcome this challenge through applications of matrix concentration inequalities, and our results do not need any additional structural assumption (e.g., sparsity) on the noise covariance matrix . An additional advance of our theory compared with Yan et al., (2024) lies in that, our bounds for and are free of condition number , making our theory work even when the factor loading matrix is near-singular and ill-conditioned, i.e., is very large. In particular, our result accomodates the heterogeneous case of Bai and Ng, (2023).

3.2 Implications: estimation guarantees and distributional characterizations

In this section, we present the immediate consequences of Theorem 1 — estimation error bounds and distributional characterization for the PC estimators. Later in Section 4, we will compare these results with the recent work (Bai and Ng, (2023); Jiang et al., (2023); Choi and Yuan, (2024)), and highlight the advantages of our theory.

Recall that our estimators for the factors and factor loadings in Algorithm 1 are given by and respectively. Let us take a moment to see how to quantify the estimation error for in the face of rotational ambiguity. In view of Theorem 1, we know that should be close to in Euclidean distance. In addition, recall that is the SVD of the rank- matrix , which suggests the existence of an invertible, -measurable matrix such that . Hence, by defining , we may use to evaluate the estimation error of . Similarly, we define and use to measure the estimation error of .

We will show in Lemma 2 that and are close to rotation matrices. Indeed, in the study of PC estimators for factor model (e.g., Bai and Ng, (2023); Jiang et al., (2023); Choi and Yuan, (2024)), it is quite common to take and , rather than and , as the groundtruth, though the specific choices of and vary across different works. Both the averaged and the row-wise estimation error bound can be deduced from Theorem 1. We record the results in the following corollary.

Corollary 1 (Estimation guarantees for factors and factor loadings).

Suppose that the assumptions in Theorem 1 hold. Then there exists a universal constant such that: with probability at least , for factors, the averaged and the row-wise estimation error are given by

| (3.5) |

respectively; for factor loadings, we define , if there exists some universal constant such that , and , then the averaged estimation error bound is given by

| (3.6a) | |||

| and the row-wise estimation error bound is given by | |||

| (3.6b) | |||

Let us interpret the above bounds under some specific settings. For simplicity, we ignore the log factors and consider the setting discussed after Theorem 1, with the assumption that . Under this setting, to make the assumptions on hold, it suffices to assume that , where is the SNR. For factors, the upper bounds for the averaged and row-wise estimation error rates in (3.5) are given by and , respectively; for factor loadings, the two bounds in (3.6a)–(3.6b) are given by and , respectively. All these bounds go to zero under the condition that , which match the minimal condition required for the consistent estimations of the left and right singular subspaces if there is no correlation in the noise matrix (e.g., Yan et al.,, 2024).

Next, we present our results on the inference for factors and factor loadings in Corollaries 2 and 3, respectively.

Corollary 2 (Distributional theory for factors).

Remark 1.

If all the entries of the matrix are Gaussian, i.e., the noise is Gaussian, then the result (3.7) holds without the assumption that . Indeed, in the scenario where and is -incoherent, fulfilling our assumption on merely requires that on the growth rate of cross-sectional dimension .

Corollary 3 (Distributional theory for factor loadings).

Suppose that Assumptions 1, 2, and 3 hold. Assume that there exists a constant such that . For any given target error level , assume that , , ,

for some universal constant and sufficiently large constant . Then, for any , it holds that

where is the collection of all convex sets in , and the covariance matrix is given by .

Let us look at the assumptions about the SNRs and in Corollaries 2 and 3. Consider the setting where , , , , , and is well-conditioned. Then, the SNR condition in Corollary 2 (resp. Corollary 3) is equivalent to (resp. and ), indicating that inference of factors and factor loadings is achievable as long as the SNR grows faster than a polynomial rate of . Our SNR condition is less restrictive than the prior work (e.g., Bai and Ng,, 2023; Jiang et al.,, 2023; Choi and Yuan,, 2024) that required the SNR to grow with a polynomial rate of . Regardless of log factors, our SNR condition for inference is equivalent to , which is optimal since it matches the same condition required for consistency as commented after Corollary 1. Also, in the special case where is diagonal, i.e., there is no correlation in the noise matrix, our SNR condition for inference matches the minimal condition required for the subspace inference (e.g., Yan et al.,, 2024).

Both Corollaries 2 and 3 are stated in a non-asymptotic sense, and can be easily translated to asymptotic normality results. In practice, the confidence regions for the factors and the factor loadings can be constructed by replacing the asymptotic covariance matrices and with their consistent estimators:

respectively. Here, is the estimator of the noise covariance matrix which we will introduce in detail in Section 5.1.1. The intuition behind the above consistent estimators is that, and are the consistent estimators of and , respectively, and we will show this fact in the proof of Theorem 1.

4 Comparison with previous work

In this section, we compare our main results with related ones established in prior works Bai and Ng, (2023); Jiang et al., (2023); Choi and Yuan, (2024). All of them studied the PC estimators in weak factor models, and established estimation error bounds and asymptotic normality under different assumptions. Distinct from these three papers, all our results are entirely non-asymptotic, providing finite-sample characterizations for both the estimation error and the uncertainty level of statistical inference. From a technical viewpoint, in the regime , a notable advancement of our theory is that, our assumptions for inference require the growth rate of SNR to be faster than a polynomial rate of , unlike the polynomial rate of required in these three papers. Also, all these three papers assume that the singular values of factor loading are distinct, while our theory does not require such eigengap condition.

Having provided an overview of the advantages of our theory, we now make the comparisons in detail.

-

•

Bai and Ng, (2023) studied both the homogeneous case where for , and the heterogeneous case where with . They required to prove the asymptotic normality for inference. However, the case when has not been covered by their inferential theory. Our theory fills this gap and establishes the inference results even when do not grow with a polynomial rate of . Besides the inference, our theory provides row-wise estimation error bounds for factors and factor loadings as detailed in Section 3.2, while the bounds in Bai and Ng, (2023) are Frobenius norm bounds measuring the average error over all rows. The consistency and asymptotic normality results in Jiang et al., (2023) are similar to those in Bai and Ng, (2023), while the focus of Jiang et al., (2023) is to identify the so-called pseudo-true parameter that is consistently estimated by the PCA estimator. We note that both their frameworks accommodate temporal correlation, an aspect not covered by our theory.

-

•

Choi and Yuan, (2024) adopted the leave-one-out analysis similar in spirit to those used in matrix completion to investigate the PCA estimators. The setup they studied is the homogeneous case in Bai and Ng, (2023) because they assumed that , which requires for all the singular values of factor loading . When temporal correlation does not exist, similar to our results, they also filled the gap to establish the inference results for . In comparison, our theory is fully non-asymptotic and does not assume any asymptotic growth assumptions on the singular values. Also, the homogeneous case they studied assumes that the condition number satisfies that , while our theory does not need this assumption and allows any growth rate of the condition number .

To enhance the clarity of the comparison of the SNR assumption for inference, we detailed the results in Table 1 under a specific setup: Assumptions 1, 2, 3 hold; The cross-sectional and temporal dimensions satisfy that ; the number of factors satisfies ; the noise covariance matrix satisfies , , and . Since the scale of the noise is reflected by and in our current setup we have that and , the assumptions on the SNRs and defined in Section 3 are fully represented by the growth rate of the smallest singular value of factor loading matrix .

| Factor | Factor loading | |

|---|---|---|

| Bai and Ng, (2023) | ||

| Jiang et al., (2023) | ||

| Choi and Yuan, (2024) | ||

| Our Theory |

Table 1 demonstrates the advancement of our theory. For the conditions of Choi and Yuan, (2024) in Table 1, the parameter is defined in Assumption B” (iv) therein on the noise structure and they need two additional growth rate assumptions on (see Assumption D” (i) therein). For other regimes where or , similar comparisons can be made, so we omit the details for the limit of space.

5 Applications in econometrics

Our first-order approximations do not only advance the existing theories on the PCA under the weak factor model, but also pave the path for various statistical tests that are useful in economics and finance. In this section, we show four applications of our results.

5.1 The factor specification tests

Recall that the factor model is given by , where the matrix is the realization of latent factors. Suppose we have time series data of some observed factors, e.g., the Fama-French factors. Our focus is on testing if the observed factor is in the linear space spanned by the latent factors . In particular, we examine this linear dependence in a flexible range of the whole period . Formally, we consider an index set of interest, and we have the data of an observed factor recorded at the time index set . We test the hypothesis as follows,

| (5.1) |

Under the null hypothesis , we have that for any .

Under the strong factor model where the pervasiveness assumption holds, Bai and Ng, 2006b studied this problem and designed test statistics for the whole set, i.e., . Our study extends to the case when is a subset of the whole time span under the weak factor model. The subset can be any specific time window of interest. This scenario is economically meaningful because the relationship may only be valid for relatively short periods, not necessarily across the entire span; see Bai and Ng, 2006b for the connections between the CAPM analysis and this problem. In Section 6, we show that our factor specification test results strikingly reconcile with the economic cycles and financial crisis.

Our test statistic relies on the estimation of the noise covariance matrix . We denote by the estimator of and we will elaborate its construction in the next section. In Theorem 2 below, we keep the error bound in the final result.

Theorem 2.

For any given target error level , assume there exist some universal constants and sufficiently large constant such that, , , ,

| (5.2) |

and that for the estimator of the noise covariance matrix , it holds

Then, under Assumptions 1, 2, 3, and the null hypothesis in (5.1), we have that

| (5.3) |

where the test statistic is defined by

Remark 2.

The idea of the test statistic is to utilize the fact that, under the null hypothesis , the residual vector of is zero after projection onto the column space of . Note that estimates the column space of . So, we construct by computing the -norm of the projection residual vector . The component estimates the variance of , and needs the estimator of noise covariance matrix as input.

Our focus is on the regime where the size of subset is small. This is economically meaningful because the linear relationship between observed factors and latent factors usually holds only for a short horizon. Based on our distributional results in (5.3), the case when is the whole period, i.e., , can be handled straightforwardly by applying the Gaussian approximation to the Chi-square distribution. Our assumption on the size can be summarized as . On the one hand, we require that cannot be too small so that is of full column rank and its singular value is close to , which is crucial for our proof. On other hand, we require that cannot be too large, otherwise the null distribution with mean would diverge in such a case, complicating the proof of proximity between and the law of test statistic .

The assumption on SNR is that . Consider the setting where , , and is well-conditioned (i.e., ). Then, the SNR condition becomes , illustrating the effect of the subset size on the growth rate required for SNR . The factor appears in the SNR because we use the Chi-square distribution as the null distribution to accommodate the general case when is small. When , regardless of the log factors, the SNR condition is equivalent to , which match the minimal condition required for the consistent estimations of the left and right singular subspaces if there is no correlation in the noise matrix (e.g., Yan et al.,, 2024).

Bai and Ng, 2006b studied the factor specification test under the whole period case, i.e., . They derived the approximate cumulative distribution function (CDF) for their test statistic, but they did not provide a finite sample error bound for it and their results were under the strong factor model. In comparison, our results give a precise characterization of the error and adapt to the weak factor model. In our case, both the low SNR in the weak factor model and the subset in the hypothesis make it challenging to design the test statistics. The subspace perturbation bounds in Theorem 1 enable us to conquer these difficulties and establish non-asymptotic analysis of our test statistic for any arbitrary subset .

5.1.1 Estimation of the noise covariance matrix

We accommodate the case where the cross-sectional dimension is much larger than the temporal dimension . In such case, estimating the high-dimensional covariance matrix becomes challenging yet is vital for numerous statistical tests, including the factor specification test and the two-sample test for betas discussed in the next section. Following the approaches in, e.g., Bickel and Levina, (2008); Fan et al., (2011, 2013), we assume that the error covariance matrix is sparse in a suitable sense and use the adaptive thresholding method to estimate . It’s important to note that the assumed sparsity of is solely for our statistical tests and is not a required condition to establish our main theories on the subspace perturbation bounds in Theorem 1.

Assumption 6.

For some , there exists a constant such that

The assumption is slightly weaker than those in, e.g., Bickel and Levina, (2008); Fan et al., (2013), where they assumed that , , and for some sparsity parameter . In particular, for , it constrains on the maximum number of nonzero elements of . This sparsity assumption for the noise covariance is also natural in economics and finance. As the latent common factors largely explain the co-movements in the panel data, the correlation among individual asset’s idiosyncratic noises should be close to zero. A specific example of the sparse structure of arises from the remaining sector effects (Gagliardini et al.,, 2016).

We estimate the idiosyncratic noise matrix using , where and are the PCA estimators of factor loadings and factors defined in Section 3.2. Then, the pilot estimator of the covariance matrix is given by . We will show in Lemma 1 later that , where is negligible as . Then we apply an adaptive thresholding method (Bickel and Levina,, 2008) to obtain the sparse covariance matrix estimator as follows,

where is a thresholding function with the threshold value . Here, the threshold value is set adaptively to with some large constant . The idea behind the adaptive thresholding is examining the sample correlation matrix and retaining entries exceeding in magnitude. The specific examples of the function include the hard-thresholding function , among other common thresholding functions like the soft-thresholding function and SCAD (Fan and Li,, 2001). In general, we require that the thresholding function to satisfy: (i) ; (ii) . The estimation error is given as follows.

Lemma 1.

Suppose that all the assumptions in Corollary 1 hold, and that there exists a sufficiently small constant such that

| (5.4) |

where

Then, we have that, with probability at least , it holds , for a universal constant . Further, under Assumption 6, the generalized thresholding estimator satisfies that, there exists some universal constant such that, with probability at least ,

The above error bounds for the estimators and differ from the existing literature owing to our row-wise subspace perturbation bounds in Theorem 1. Let us interpret the condition (5.4) under some specific settings. Consider the setting where , , is -incoherent, and is well-behaved such that , , and . Then, the condition (5.4) is equivalent to , which requires the sample size is sufficiently large. According to Lemma 1, fulfilling our assumption on the estimation error required for Theorem 2 merely requires that the estimation error satisfies

In subsequent applications, we will directly use , instead of , to express assumptions on the estimation error of the noise covariance matrix.

5.2 Test for structural breaks in betas

The discussion so far has studied the factor models with constant betas. However, in many cases, there is a possibility of time-variant betas, and it is important to test for structural changes in betas (e.g., Stock and Watson,, 2009; Breitung and Eickmeier,, 2011; Chen et al.,, 2014; Han and Inoue,, 2015). We test for two time periods and that are possibly not consecutive, i.e., . The factor models in these two periods are subject to a structural break in beta: for each given individual unit ,

where is the index of the cross-sectional unit of interest. Here, we assume that the factors are the same, but the betas can be different. For example, we might ask if a external shock such as the 2008 financial crises has caused the changes in factor loadings before and after the shock with a transition period .

The data consist of two panels, and , during and , respectively, where and . We test the hypothesis as follows:

Different from our approach, Chen et al., (2014); Han and Inoue, (2015) tested for the entire factor loading, with their null hypothesis being . Stock and Watson, (2009); Breitung and Eickmeier, (2011) also studied the test for a given like ours, while Stock and Watson, (2009) focused on empirical studies and Breitung and Eickmeier, (2011) developed and established theories for the test statistics. Our work differs in that, as we will show below, the effectiveness of our test statistic does not require the pervasiveness assumption needed in Breitung and Eickmeier, (2011). In addition, our formulation allows the gap between the two periods and , which can model the special transition periods we purposely, e.g., financial crisis, enabling us to test for structural breaks before and after these special periods.

To construct the test statistic, we first merge the two panels and into a -dimensional data matrix . Next, we apply SVD as described in Algorithm 1 to obtain an estimator of the factors: , where and is the truncated rank- SVD of with and . Then, we split the estimated factors into according to two time periods and , where . Subsequently, we obtain the estimator for by regressing on :

Finally, under null hypothesis , we show that is approximately Gaussian via the first-order approximation results in Theorem 1, and construct the test statistic using the plug-in estimator of the covariance matrix.

Theorem 3.

Suppose that the assumptions in Theorem 1 hold, and the covariance estimator satisfies the conditions as in Lemma 1. For any given target error level , assume there exists some universal constants such that , , , ,

and , where is a vector defined as ; for the parameter (cf. Lemma 1) that captures the estimation error of the noise covariance matrix , assume that and . Then, under the null hypothesis , we have that

where the test statistic is given by

with .

Remark 3.

If all the entries of the noise matrix in (2.4) are Gaussian, then we do not need the assumption that , where .

To illustrate our assumptions, we consider the following setting similar to that discussed after Theorem 1: , , , is well-conditioned and its sparsity parameter satisfies , and the column subspace of is incoherent. Then, fulfilling our assumptions merely requires that, and for the SNR, for the sample size, and for the estimation error of . In particular, our SNR conditions are less restrictive than prior work (e.g., Breitung and Eickmeier,, 2011) that needed the pervasiveness assumption, which required the SNR to grow as . Our results adapt to the weak factor model with the cross-sectional correlations, and to the best of our knowledge, no prior work has developed the test statistics for the structural break test under this case.

5.3 The two-sample test for betas

In finance and economics, besides the latent common factors that drive the co-movements of asset returns, the factor loadings, also known as betas, are important as well, which measure the sensitivity of asset return to the movements of the factors. Consider the example that the panel data is the stock return, where the -th row of represents the time series data of the -th stock. Then, the factor loadings assess the risk exposure of these stocks to the latent common factors , with the -th row being the -th stock’s beta.

For any distinct and , we aim to test the hypothesis that , i.e., if the -th and the -th stocks have the same risk exposure on the common factors. It is a statistical approach to evaluate the similarity in risk structure between two stocks. Our test statistic is similar to the idea of two-sample test: we show that is approximately Gaussian and then derive a Chi-square test statistic. In Theorem 2 below, we construct the test statistic and show its validity.

Theorem 4.

Suppose that the assumptions in Theorem 1 hold. Assume that for some universal constant , and the covariance estimator satisfies the conditions as in Lemma 1. For any given target error level , assume there exists some universal constants such that ,

| (5.5a) | |||

| and | |||

| (5.5b) | |||

for the parameter (cf. Lemma 1) that captures the estimation error of the noise covariance matrix , assume that . Then, for any satisfying , under the null hypothesis , we have that

where the test statistic is given by

Remark 4.

If all the entries of the noise matrix in (2.4) are Gaussian, then we do not need the assumption that on the sample size .

To illustrate the SNR conditions (5.5a)–(5.5b), we consider the setting discussed after Theorem 1, i.e., , , is well-conditioned, and the column subspace of is incoherent. Then, fulfilling our assumptions (5.5a)–(5.5b) merely requires that and . These SNR conditions are less restrictive than the prior work (e.g., Bai and Ng,, 2023; Jiang et al.,, 2023; Choi and Yuan,, 2024) that required the SNR to grow with a polynomial rate of .

To the best of our knowledge, no prior work has developed the test statistics for this two-sample test of betas. Our results are applicable to the weak factor model with the cross-sectional correlations. The subspace perturbation bounds in Theorem 1 pave the way for us to statistically assess the similarity for arbitrary two rows of factor loadings .

5.4 Statistical inference for the systematic risks

In the factor model , the risk associated with stock return is decomposed into two parts (e.g., Bai,, 2003) — systematic risk from the common component and idiosyncratic risk from the noise . Systematic risk, often referred to as market risk, is integral in financial economics as it represents the inherent risk affecting the entire market or market segment. This risk, driven by broader economic forces such as inflation, political events, and changes in interest rates, comes from the risk factors that explain the systematic co-movements and impacts all the stocks.

A standard metric of the systematic risk is the variance of , which is given by . Our focus is on constructing the confidence interval (CI) for systematic risk . Similar to the idea we conduct the inference for beta in Corollary 3 where the estimator of is , we show that is approximately Gaussian and then construct the CI for . We present the CI and its validity in Theorem 5.

Theorem 5.

Suppose that the assumptions in Theorem 1 hold. Assume that covariance estimator satisfies the conditions as in Lemma 1. For any given target error level , assume there exist some universal constants such that , , , , ,

| (5.6a) | |||

| (5.6b) |

for the parameter (cf. Lemma 1) that captures the estimation error of the noise covariance matrix , assume that . Then we have that, for any ,

where the confidence interval is constructed as

and is the -quantile of the standard Gaussian .

Remark 5.

If all the entries of the noise matrix in (2.4) are Gaussian, then we do not need the assumption that on the sample size .

We now explain the assumptions under the setting discussed after Theorem 4. In this case, to make (5.6a) hold, it suffices to assume that and ; to make (5.6b) hold, it suffices to assume that , , and . All these conditions require only polynomial growth rates of for the SNRs , , and . The assumption on is the same with that we required in Corollary 1 to prove the estimation error for factor loading.

On one hand, as shown in Theorem 5, the CI width is proportional to the square root of the product of noise level estimator and systematic risk estimator . On the other hand, in the proof of Theorem 5, we show that the bias of systematic risk estimator is proportional to . Thus, the assumption that is essential because the validity of inference hinges on the dominance of the CI width over the bias. Consequently, we assume that the ratio between systematic risk and noise level cannot be too large. The row-wise subspace perturbation bounds in Theorem 1 facilitate us to conduct statistical inference for the systematic risk of any given stock in the panel data.

6 Numerical experiments

In this section, we conduct Monte Carlo simulations to demonstrate our inferential theories for the PC estimators in the weak factor models. Additionally, our empirical studies reveal that the testing results based on our test statistics surprisingly align with the economic cycles and financial crisis periods.

6.1 Monte Carlo simulations

To make our simulations similar to the real applications, we use the standard Fama-French three-factor model:

where the dimension of the latent factor is set to . The idiosyncratic noise exhibits cross-sectional correlations, and the noise covariance matrix is sparse.

We generate the factor loadings , the factors , and the noise terms independently from , , and , respectively, where . Both and are set to identity matrices. We generate as a block-diagonal matrix , where the number of blocks is set to . We set and . For each , we construct it as an equi-correlation matrix , where the block size is set to , is the -dimensional vector of ones, and is drawn from a uniform distribution on . To validate our test statistic for two-sample test of betas, we set equal to after generating the loading matrix . This slight modification allows us to examine our test statistics under the null hypothesis . In our simulation results, we report the values of to reflect different levels of SNR.

First, we demonstrate the practical validity of the confidence regions constructed using Corollaries 2–3 and Theorem 5, for the factors, betas (i.e., factor loadings), and systematic risks, respectively.

-

•

For factors (resp. betas), we construct 95% confidence regions by substituting the asymptotic covariance matrix (resp. ) with their consistent estimators as commented after Corollary 3. We define (resp. ) as the empirical probability that the constructed confidence region covers (resp. ) over 200 Monte Carlo trials, where (resp. ) is the rotation matrix defined in Corollary 2 (resp. Corollary 3).

-

•

For systematic risks, similarly, we define as the empirical probability that the 95% confidence interval constructed via Theorem 5 covers over 200 Monte Carlo trials.

Finally, we compute the mean and standard deviation for , , and , then present these as and , with the results reported in Table 2. As indicated in Table 2, the coverage probabilities are close to 0.95 according to the mean value, and exhibit stability across different rows of and as evidenced by low standard deviation. As SNR goes down, the slight slippage of the coverage probabilities of the systematic risks reconciles with our comments after Theorem 5 that, , which is close to SNR, reflects the ratio between the bias and the CI width and cannot be too large. These favorable numerical results persist even under low SNR, supporting our inferential theory under the weak factor model.

| Factor | Beta | Systematic Risk | ||||

|---|---|---|---|---|---|---|

| SNR | ||||||

Next, we demonstrate the effectiveness of our test statistics in Theorems 2 and 4 by showing their satisfactory size and power.

-

•

For the null hypothesis in the factor specification test of Theorem 2, the time index subset is chosen as with , and the observed factors is set as

The vector is set as , and the parameter controls the deviation of the alternatives from the null distribution. The vector is constructed as follows: a vector is drawn from the standard Gaussian and the projection residual is computed, where is the projection matrix on the column space of . Then, we set . The formulation of ensures that the signal strength from the column space of , which is captured by , is balanced with that from the space orthogonal to . The null hypothesis should not be rejected when , and should be rejected when .

-

•

For the null hypothesis in the structural break test of betas in Theorem 3, the cross-sectional unit is set as , and the time subsets are set as and with . The beta on period is generated by the aforementioned procedure, while the beta on period is set as

where . The null hypothesis should not be rejected when , and should be rejected when .

-

•

For the null hypothesis in the two-sample test of betas in Theorem 4, we set and study two cases for and respectively. According to our simulation setup, the null hypothesis should not be rejected when , and should be rejected when .

Tables 3–4 report the empirical rejections rates at 5% significance level over 200 Monte Carlo trials. Table 3 (resp. 4) shows that for the test statistics in Theorem 2 (resp. Theorems 3 and 4), the results are favorable, exhibiting appropriate size and power, even under a weak signal setup where the SNR is small.

| Factor specification test | |||||

| SNR | |||||

| Structural break test | Two-sample test | ||||||

|---|---|---|---|---|---|---|---|

| SNR | |||||||

6.2 Empirical studies

We analyze the monthly returns data of the S&P 500 constituents from the CRSP database for the period from January 1995 to March 2024. We apply the factor specification test in Theorem 2 and the structural break test for betas in Theorem 3 to the stock returns.

First, we consider the factor specification test. The observed factors we study are the Fama-French three factors: market (MKT), size (SMB), and value (HML), denoted as , , and , respectively. We obtain the time series data for these factors from Kenneth French’s website. We conduct our tests via a rolling window approach, moving a 60-month window () through the dataset. To mitigate the survival bias, we keep the time series that have no more than 50% missing values in each window, i.e., the number of missing values is less than , and fill the missing values by the median of each time series. For each window, the formed data matrix is an matrix, where the cross-sectional dimension varies with . We assume that satisfies the factor model as in (2.2), i.e.,

Here, the superscript is added to each matrix to emphasize that we apply the PCA method across different time windows . The number of factors is fixed as . We conduct the factor specification test in Theorem 2 to test the null hypothesis

for the three factors, corresponding to , respectively. The time index subset is set as with .

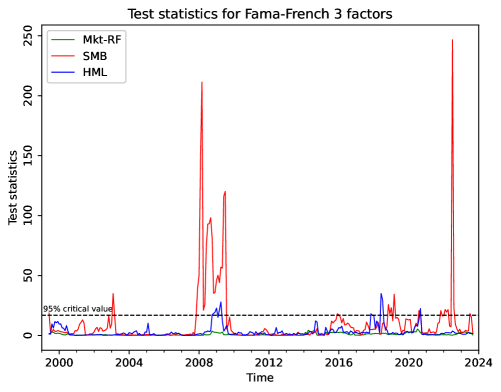

The above procedure implies that, for each 12-month period , to test if the observed factors are in the column space of the latent factors, we look back and utilize a broader historical data window () to estimate the latent common factors . Then we test the null hypothesis for this specific 12-month period , a subset at the end of the whole window . Finally, we plot in Figure 1 the test statistics against the time index for each factor, underscoring the 95% critical value. As highlighted by Fan et al., (2015), this rolling window manner not only utilizes the up-to-date information in the equity universe, but also alleviates the impacts of time-varying betas and sampling biases.

|

In Figure 1, our findings indicate that during the financial crisis of 2007-2009, the null hypothesis that the size factor SMB lies in the latent factors’ column space, is rejected at 95% confidence level. This suggests a diminished importance and reduced explanatory power of the size factor SMB for stock return data in this period. Note that the sizes of stocks can still be important or even more important than that in the normal period, but not necessarily captured by the variable SMB. Similar interpretations hold for the value factor HML around 2009. During the COVID period around 2019, both the size factor SMB and the value factor HML exhibit a loss in explanatory power. The spike for the size factor SMB during 2022 is probably due to the war between Russia and Ukraine that started in February 2022, which is an unexpected economic shock to the stock market. Notably, the market portfolio maintains its explanatory strength throughout, indicating its stability and resilience as an explanatory variable, even during distinct economic cycles.

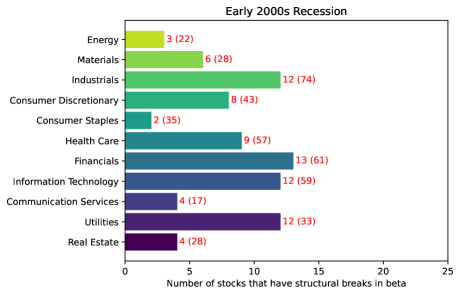

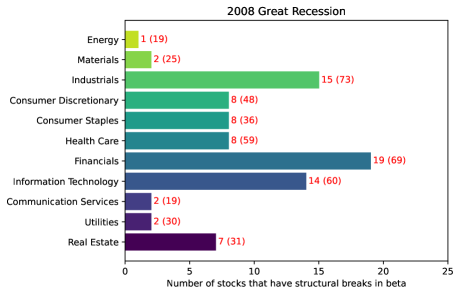

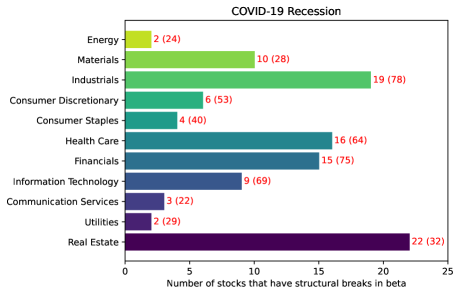

Next, we consider the structural break test for betas for individual stocks. We test whether the betas have changed before and after the three economic recessions covered by the time horizon of our data – the Early 2000s Recession (Mar. 2001–Nov. 2001) due to the dot com bubble, the 2008 Great Recession due to housing bubble and financial crisis (Dec. 2007–Jun. 2009), and the COVID-19 Recession (Feb. 2020–Apr. 2020). Here, the start and the end of each recession are according to the NBER’s Business Cycle Dating Committee.

For each recession period , we first take the data and lying in the time window and , respectively, where . Next, we merge the two panels to get , and fill the missing values in the same manner as in the factor specification test. We assume that satisfies the factor model as follows

The number of factors is chosen by a scree plot of the eigenvalues of , which is , , and for the three recessions, respectively. We test the hypothesis for each cross-sectional unit using the test statistic in Theorem 3. To report the test results, we group the stocks into 11 sectors by Global Industrial Classification Standard (GICS), and then count the numbers of stocks in each sector that reject the null at the 95% confidence level. The test results for the three recessions are illustrated in Figures 2, 3, and 4, respectively.

|

In Figure 2, we observe that the sectors with the highest number of stocks experiencing structural breaks in betas are Financials, Information Technology, Industrials, and Utilities. The impact on the Information Technology sector is likely due to the dot-com bubble burst, which was one of the triggers of the Early 2000s Recession. Another significant cause of this recession was the 9/11 attacks. Such severe economic shocks are possible reasons why typically stable sectors like Industrials and Utilities were also affected.

|

In Figure 3, the 2007-2009 financial crisis, marked by the subprime mortgage crisis and the collapse of the United States housing bubble, affected many sectors. The financial sector experienced a strong impact due to direct exposure to mortgage-backed securities and other related financial instruments. The crisis led to the failure or collapse of many of the United States’ largest financial institutions. Even though our analysis is inevitably influenced by survival bias, as we can only analyze stocks that existed before and after the crisis, we still observe that the financial sector had the most affected stocks. The impact in Real Estate reflects the direct consequences of the housing bubble burst. For sectors related to consumer spending, such as Consumer Discretionary, Consumer Staples, and Health Care, the shocks can be attributed to reduced consumer spending due to increased unemployment and economic uncertainty.

|

In Figure 4, the economic effects of the pandemic can be seen in many affected sectors, such as Real Estate, Industrials, Health Care, and Financials. The significant changes in Real Estate likely reflect the uncertainties brought about by lockdowns and health crises, resulting in severe fluctuations in property values and rent payments. The impact on the Health Care sector may be tied to the heightened demand for medical services and supplies, alongside volatility in biotechnology investments. Notably, Utilities and Energy showed smaller changes, suggesting relative stability in these sectors despite overall market volatility. During the 2008 Great Recession, these sectors also demonstrated similar stability. This resilience could be attributed to the essential nature of services provided by these sectors, making them less susceptible to economic disruptions.

7 Other related works

The factor model is an important topic in finance and economics. The early econometric studies on factor model can be dated back to Forni et al., (2000); Stock and Watson, (2002). Most previous works on factor model assumes that all factors are strong or pervasive, that is, the SNR grows at rate (e.g., Bai and Ng,, 2002; Bai,, 2003; Fan et al.,, 2013). When the SNR grows at a rate slower than , the model is often called the weak factor model, which has been a popular research topic in recent years. The method for determining the number of factors under the weak factor model has been studied by a few papers (e.g., Onatski,, 2009, 2010; Freyaldenhoven,, 2022). Several recent works have pursued the estimation and inference in the weak factor model. To name a few examples, Bai and Ng, (2023); Jiang et al., (2023); Choi and Yuan, (2024) studied the consistency and asymptotic normality of PC estimators; Uematsu and Yamagata, 2022a ; Uematsu and Yamagata, 2022b ; Wei and Zhang, (2023) studied the sparsity-induced weak factor models where the low SNR is due to the sparsity of the factor loading matrix; Bailey et al., (2021) proposed an estimator of factor strength and established its theoretical guarantee; Onatski, (2012) showed that the PC estimators are inconsistent in the extreme case (also known as the super-weak factor model) where the SNR is .

The PCA is one of the most popular methods for the factor model, and has been studied in many papers mentioned previously (e.g., Stock and Watson,, 2002; Bai and Ng,, 2002; Bai,, 2003; Onatski,, 2012; Fan et al.,, 2013; Bai and Ng,, 2023; Jiang et al.,, 2023; Choi and Yuan,, 2024). Among the enormous literature, Bai and Ng, (2023); Jiang et al., (2023); Choi and Yuan, (2024) are the most recent and closest to our paper, since we all focus on the PC estimators, especially on the inference side, under the weak factor model. Besides the theoretical analysis, the variants of PCA under the weak factor model have also been applied to empirical asset pricing, macroeconomic forecasting, and many other important problems in finance (e.g., Giglio et al.,, 2021, 2023). The estimation of factor model is closely related to the low-rank matrix denoising in the statistical machine learning community. In recent years, studying the factor model from the view of low-rank matrix denoising has provided lots of exciting findings and understandings (see Fan et al., 2021a ; Yan et al., (2024) for comprehensive reviews), and our theory is partly inspired by this low-rank structure of factor model.

From a technical perspective, our estimation procedure is a spectral method, and is related to previous studies of spectral methods on PCA and subspace estimation (Abbe et al.,, 2022; Cai et al.,, 2021; Chen et al., 2021b, ; Yan et al.,, 2024; Zhou and Chen,, 2023). Our analysis relies on the leave-one-out techniques that have found wide applications in analyzing spectral estimators and nonconvex optimization algorithms (El Karoui,, 2015; Abbe et al.,, 2020; Ma et al.,, 2020; Chen et al.,, 2020, 2023); see the recent monograph Chen et al., 2021a for more details. In addition, the problem and analysis in this paper is also related to past works on inference for other low-rank models (Chen et al.,, 2019; Xia and Yuan,, 2021; Chernozhukov et al.,, 2023; Choi et al.,, 2023, 2024; Yan and Wainwright,, 2024).

8 Conclusions and discussions

In this paper, we establish a novel theory for PCA under the weak factor model, offering significant advancements on the inference of PCA over the existing literature. The weak factor model removes the pervasiveness assumption that requires of SNR growing at a rate, where is the cross-sectional dimension. Our theory covers both estimation and inference of factors and factor loadings. Notably, in the regime , where is the temporal dimension, we show that the asymptotic normality of PC estimators holds as long as the SNR grows faster than a polynomial rate of , while the previous work required a polynomial rate of . The optimality of our theory is in the sense that, the required growth rate of the SNR for consistency aligns with that for asymptotic normality, differing only by some logarithmic factors. Our theory paves the way to design easy-to-implement test statistics for practical applications, e.g., factor specification test, structural break test for betas, and build confidence regions for crucial model parameters, e.g., betas and systematic risks. We validate our statistical methods through extensive Monte Carlo simulations, and conduct empirical studies to find noteworthy correlations between our test results and specific economic cycles.

While the current scope of our theory is considerably wide-ranging, it is possible to further widen it and there are lots of topics that are worth pursuing. For instance, how to extend the theory to the setting where each observed variables have only fouth moment via robustification of the covariance input (Fan et al., 2021c, )? How to generalize our inferential theory to the case where the time-serial correlation also appears in the idiosyncratic noise? If the panel data is missing at random, are the PC estimators still valid under the weak factor model, and how to conduct statistical inference in this case? What benefit could our new theory bring to forecasting methods based on the factor-augmented regression? Among many directions, these topics can be investigated in future research.

Acknowledgements

J. Fan is supported in part by the NSF grants DMS-2053832 and DMS-2210833, and ONR grant N00014-22-1-2340. Y. Yan is supported in part by the Norbert Wiener Postdoctoral Fellowship from MIT.

Appendix A Proof of Theorem 1: First-order approximations

For ease of exposition, we introduce some additional notation that will be used throughout the proofs. For any matrix , we let , , and denote the -th largest, the minimum, and the maximum singular value of , respectively. For a symmetric matrix , we denote by tr its trace.

A.1 Some useful lemmas

To prove Theorem 1, we collect some useful lemmas as preparations. We start with a lemma to reveal the close relations between the SVD and the common component in the factor model (2.2), where .

Lemma 2.

Suppose that Assumptions 1 and 3 hold. Assuming that

| (A.1) |

then we have that, there exists a -measurable event with , where is the -algebra generated by , such that, the following properties hold when happens: (i) rank,

(ii) There exists a -measurable matrix satisfying that and is a rotation matrix, i.e., .

(iii) for .

(iv) There exists a -measurable matrix satisfying that and is a invertible matrix satisfying that for . Further, it holds

Proof.

Since , and are independent sub-Gaussian random vectors under Assumption 3, we obtain by (4.22) in Vershynin, (2017) that,

| (A.2) |

with probability at least , where the last inequality is owing to (A.1) and the fact that . Then using the sub-Gaussian property of and the standard concentration inequality, we have that

| (A.3) |

with probability at least . In particular, we let be the event that both (A.2) and (A.3) happen, then we have that . In what follows, we show that satisfies all the requirements.

When (A.2) happens, since (A.1) implies that , we have that , and thus for , implying that for . Since implies that , we obtain that , i.e., has full column rank.

By definition, the columns of (resp. ) are the left singular vectors of (resp. ). When (A.2) happens, since , the -dimensional column spaces of and are the same with each other. Then since the columns of both and are orthonormal, we obtain that there exists a rotation matrix such that . By construction we have that is -measurable.

Next, we prove the relations for eigenvalues. By definition, we have that are the eigenvalues of , and are the eigenvalues of . By Theorem A.2 in Braun, (2006), we obtain that

where the last inequality is owing to (A.1). So we obtain that for .

By the property of SVD, we have that , where is given by and is invertible. So we have that and thus . Then, we obtain that , and thus we obtain that for . As a result, we have that

where (i) and (ii) use and in (A.3), respectively. ∎

Lemma 2 shows how the SVD relates with and constructs a good event on which we have nice properties of the quantities in our setup. Lemma 3 below establishes some useful results on the random matrix which characterizes the noise matrix in (2.4).

Lemma 3.

Under Assumption 2, for any fixed matrices and with , we have that, with probability at least ,

| (A.4) |

and

Proof.

It suffices to prove that every inequality holds with probability at least . Since the entries of are independent and sub-Gaussian under Assumption 2, we obtain by the union bound argument that

| (A.5) |

where is a constant. Given , it follows from (3.9) in Chen et al., 2021a that, with probability at least , i.e., where . So, we obtain

| (A.6) |

implying that our desired result . Indeed, the argument for in (A.6) adapts to all the events which we will prove to hold with probability at least . In other words, for any event to prove , it suffices to prove that . So, in what follows, we conduct the proofs conditioning on .

It is easy to see that, follows from

Then, we prove that

| (A.7) |

To prove (A.7), we note that, for , is a sum of independent mean zero random vectors. Given , it holds for . Then, using the matrix Hoeffding inequality (Tropp,, 2012, Theorem 1.3), we obtain that

where . Then we obtain by the union bound argument that . Letting , we obtain that , which implying (A.7). The proof for follows from the same manner, so we omit the details for the sake of brevity. ∎

Next, we consider the truncated rank- SVD of . We define

Lemma 4 below give the perturbation bounds for the singular spaces, i.e., the column spaces of and , under the spectral norm, and some basic facts on , , and .

Lemma 4.

Proof.

Using the argument as discussed after (A.6), for any event to prove , it suffices to prove that . Here, the event is defined in (A.5) and the event is defined in Lemma 2. To see this, we note that, as long as , it holds

| (A.10) | ||||

So, in what follows, we conduct the proofs conditioning on .

Recall that is the truncated rank- SVD of , and is the SVD of . Note that , and it follows from (A.4) in Lemma 3 that

where the last inequality is owing to (A.9). So we obtain , since for according to Lemma 2. We write the full SVD of as

where and are the orthogonal complements of and , and contains the smaller singular values and is not necessarily a diagonal matrix. Then by Wedin’s theorem (Chen et al., 2021a, , (2.26a)–(2.26b)), we have that

| (A.11) |

and , and similarly , where we use the fact that and , since is the -th largest singular value of and rank. Next, for , using the arguments in Section C.3.1 of Yan et al., (2024) based on Wedin’s theorem, we obtain that . Then, since implies that for , we obtain for . The results for can be proven in the same manner. Also, we obtain by Weyl’s inequality (Chen et al., 2021a, , Lemma 2.2) that, for , , implying that for .

We now prove the results for and . Similar to the arguments for proving (F.33) in Yan and Wainwright, (2024), we have that

and , where is the orthogonal complement of . Next, we have that

where (i) uses (G.3) in Lemma 19 of Yan and Wainwright, (2024) and the fact that , (ii) follows from (A.4) and , and (iii) is because as we assumed. So we conclude that

The results for can be proven in the same manner. ∎

Then we establish the close relation between and . In particular, when we prove all of the following results, we will use the results that have been proven to hold with probabilities at least in the previous lemmas. When we use these previous results, it is equivalent to add a new event in and then repeat the argument in (A.10). Since all of our results are to be proven to hold with probabilities at least , the argument in (A.10) always works and in what follows we will use it many times without mentioning it.

Lemma 5.

Proof.

Note that

For , using the full SVD of in the proof of Lemma 4, we have that

By (A.4) in Lemma 3 and Weyl’s inequality (Chen et al., 2021a, , Lemma 2.2), we have

By Lemmas 2.5-2.6 in Chen et al., 2021a and Lemma 4, we have that and . So we obtain

For , we start by writting

Using (G.3) in Lemma 19 of Yan and Wainwright, (2024), we obtain that

Then, we conclude that

We now prove an important lemma where the leave-one-out (LOO) technique plays a key role.

Lemma 6.

Proof.

The proof consists of four steps. In the first (resp, third) step, we prove the upper bound for (resp. ), and in the second (resp. fourth) step, we add the details of the proof for an important inequality used in the proof for (resp. ).

Step 1 – By calculations, we have that, for ,

For , using the full SVD of in the proof of Lemma 4, we have that, similar to Step 1 in Section F.2.3 of Yan and Wainwright, (2024), it holds

Using (A.11), the spectral norm of the first matrix can be bounded by

where we use the fact that . The spectral norm of the second matrix can be bounded by

where (i) uses (G.3) in Lemma 19 of Yan and Wainwright, (2024) and the fact that implying according to (A.11). So, we obtain that

| (A.13) |

For , we use the leave-one-out (LOO) technique. We define as the matrix obtained by replacing the th column of with a zero vector, and define . Then, we define and w.r.t. , in the same way as how we define and w.r.t. . We have that

| (A.14) |

For , since is independent with , we apply Lemma 3 to obtain that . Note that

Then since , we obtain that

| (A.15) |

where the last inequality is from Lemma 4. So, we conclude that

| (A.16) |

For , using the event defined in (A.5), we have that

| (A.17) |

with probability at least . Combining the bounds for and , we obtain that

| (A.18) |

We will use self-bounding technique to prove in Step 2 that

As long as we have this, pluging the above upper bound of into (A.18), and combining (A.13) and (A.18), we obtain the desired bound for as below,

Step 2 – Recall that as defined in (A.16). We define

By definition, we have that , so , and similarly we have . Denote by . Then using (A.9) and our argument in proof of Lemma 4, we have that , and for , and . By Wedin’s theorem (Chen et al., 2021a, , Theorem 2.9), we obtain that

Next, by calculations we have that

Here, (i) is because , which can be proven in the same manner as we prove in Lemma 4; the last inequality uses the bound (A.16) for defined in (A.14) and the fact that, by Lemma 3,

Also, we have that

Here (i) is because , which can be proven in the same manner as we prove in Lemma 4; the last inequality uses the event defined in (A.5).

Combining the above bounds for and , and using , we obtain

Note that both sides of the above inequality include the term . Then, since according to (3.2), we obtain that

Step 3 – For , in the same manner as we did for in (A.13), we have that . For , our starting point is the following inequality

| (A.19) |

Then, the problem boils down to deriving an upper bound for . We use the LOO technique to handle for any . We define as the matrix obtained by replacing the th row of with a zero vector, and define . Then, we define and w.r.t. , in the same way as how we define and w.r.t. . We have that

| (A.20) |

For , since is independent with , we apply Lemma 3 to obtain that . Note that

Here, the last inequality is because , which can be proven in the same manner as (A.15). So, we conclude that

| (A.21) |

For , using the event defined in (A.5), we have that

with probability at least . Combining the bounds for and , we obtain that

| (A.22) |

We will use self-bounding technique to prove in Step 4 that

As long as we have this, pluging the above upper bound of into (A.22), we obtain the upper bound for , which leads to an upper bound for in (A.19). Finally, combining the bound for and the bound for in (A.19), we obtain the desired bound for as below,

Step 4 – Recall that as defined in (A.21). We define

By definition, we have that , so , and similarly we have . Denote by . Then using (A.9) and our argument in proof of Lemma 4, we have that , and for , and . By Wedin’s theorem (Chen et al., 2021a, , Theorem 2.9), we obtain that

Next, by calculations we have that

Here (i) is because , which can be proven in the same manner as we prove in Lemma 4, and the last inequality uses the event defined in (A.5).

Also, we have that

Here, (i) is because , which can be proven in the same manner as we prove in Lemma 4; the last inequality uses the bound (A.21) for defined in (A.20) and the fact that, by Lemma 3, .

Combining the above bounds for and , and using , we obtain

Note that, both sides of the above inequality include the term . Then, since according to (3.1), we obtain that

∎

Then we handle and .

Lemma 7.

(i) Assuming (3.2), i.e., , then we have that, for , with probability at least ,

Proof.

We will prove (i) and (ii) in Step 1 and Step 2, respectively.

Step 1 – Since according to Lemma 2, we obtain that . Next, by calculations, we have that

So we obtain that

The term can be bounded using Lemma 6. For , we obtain by Lemma 3 that

For , we have that and we will handle the two terms in the right hand side. For , since in Lemma 4, we have that

For , using the full SVD of in the proof of Lemma 4, we have that

Thus, we obtain that

where (i) is because in Lemma 4, (ii) uses (G.3) in Lemma 19 of Yan and Wainwright, (2024) and the upper bound for is similar to that in (A.11). Combing the bounds for and , we obtain that

Finally, we combine the bounds for , , and to obtain that, for ,

where we use in (3.2). Then using the self-bounding technique , since owing to (3.2) and (A.23), we conclude that

Step 2 – Since according to Lemma 2, we obtain that . Next, by calculations, we have that

So we obtain that

The term can be bounded using Lemma 6. For , we obtain by Lemma 3 that

For , we have that and we will handle the two terms in the right hand side. For , since in Lemma 4, we have that

For , similar to the upper bound for in Step 1, we have that

Combining the bounds for and , we obtain that

Finally, we combine the bounds for , , and to obtain that, for ,

where we use the fact that . Taking supremum w.r.t. , we obtain that

Then using the self-bounding technique for , since and and , we conclude that

Plugging the above bound of into the previous inequality for , we obtain that

Then using the self-bounding technique for , since in (3.1), we conclude that

∎

A.2 Proof of Theorem 1

We are now ready to prove Theorem 1. We will prove (i) and (ii) in Step 1 and Step 2, respectively.

Step 1 – By calculations, we have that

Since , we obtain that

where (i) is owing to the inequalities in Lemmas 4 and 5. Using in Lemma 4, we have that . Then, we obtain by Lemma 6 that,

Finally, we obtain by Lemma 7 that,

where, in the last inequality, we use the assumptions that , , and owing to (3.2) and (3.1), and as well as .

Appendix B Proof of Corollary 1

For the first-order terms and in Theorem 1, we obtain by Lemma 3 that, with probability at least ,

and similarly we obtain that

Step 1 – Derive the error bounds for factors.

Using the upper bounds for and in Lemma 4 and the upper bound for in Lemma 5, we have that

For , using the fact that in Lemma 2, we obtain that,

where the last inequality is because and . Since , we obtain that , which implies the row-wise error bound for .

Step 2 – Derive the error bounds for factor loadings.

For , the problem boils down to comparing the upper bounds of and . For the first term in the upper bound of , we obtain by that . Next, for the second and the third terms in the upper bound of , we have that

and

So we obtain that

The row-wise error bound for follows from combining the error bounds of and . Then the averaged estimation error bound follows from averaging the row-wise error bounds.

Appendix C Inference for the factors and the factor loadings

C.1 Proof of Corollary 2

Step 1 – bounding .

It follows from Lemma 2 that, there exists a -measurable matrix satisfying that and is a invertible matrix satisfying that for . We define

then we obtain by Theorem 1 that