Generalized Ridge Regression: Biased Estimation for Multiple Linear Regression Models

Abstract

When the regressors of a econometric linear model are nonorthogonal, it is well known that their estimation by ordinary least squares can present various problems that discourage the use of this model. The ridge regression is the most commonly used alternative; however, its generalized version has hardly been analyzed. The present work addresses the estimation of this generalized version, as well as the calculation of its mean squared error, goodness of fit and bootstrap inference.

Keywords: generalized ridge regression, mean squared error, norm, goodness of fit.

1 Introduction

Given the following multiple linear regression model

| (1) |

where is an matrix with full rank, is a vector with unknown parameters (to be estimated), and (being is the identity matrix), the ridge estimation proposes adding a small positive quantity to the diagonal of the matrix to mitigate the effects of nonorthogonality in the regression model, leading to biased estimators with a mean squared error lower than that obtained from the ordinary least squares (OLS). Although the first references to the ridge regression date to the 1960s (see Hoerl (1962), Hoerl (1964) and Hoerl and Kennard (1968)), it was not until the works of Hoerl and Kennard (1970b, a) that this technique was developed in depth. Hoerl (2020) presented an interesting paper reviewing the origins of ridge regression, its developments and extensions. Hastie (2020) have also collected some of the developments and applications of ridge regression within the field of applied statistics. Recently, Zhang and Politis (2022) stated that ridge regression may be worth another look since it may offer some advantages over the Lasso (Tibshirani (1996)), for example it can be easily computed with a closed-form expression.

Precisely the fact of having a closed-form expression has opened a line of research on how to theoretically justify the increase in the diagonal of matrix has been a particular research line in the ridge regression literature. In this sense, Piegorsch and Casella (1989) stated that finding a theoretically optimal basis for the ridge procedure has been a lengthy process (Rolph (1976), Strawderman (1978), Casella (1980)), and it is still not fully developed. Examining that theoretical justification, Hoerl and Kennard (1970b) indicated that the ridge estimator presented a contact point with other approximations in regression analysis and at least three of them should be commented:

The ad hoc solution presented by Hoerl and Kennard (1970b) and Hoerl and Kennard (1970a) to the collinearity presented in the design matrix has been justified post hoc. We present a brief review of the justification provided by the scientific literature:

-

•

Minimization of the ridge loss function, Harville (1998) and Fletcher (2013), similar to penalized models. The most common penalty term is the bridge penalty term (Frank and Friedman (1993), Fu (1998)):

where is an adjustment parameter. For , the ridge regression is obtained (Hoerl and Kennard (1970b) and Hoerl and Kennard (1970a)); while for , the Lasso estimator (Tibshirani (1996)) is obtained. Penalties with have also been called soft thresholding (Donoho and Johnstone (1995); Klinger (1998)). Recently, Zou and Hastie (2005) proposed elastic net regularization by using a penalty term combining the ridge and Lasso penalties:

These methods are applied not only to treat multicollinearity but also for variable selection.

- •

In any case, Hoerl and Kennard (1970b) presented a general way to obtain the ridge estimation based on the decomposition of matrix in its canonical form. Because is a symmetric positive definite matrix, it is verified that there is an orthogonal matrix (this is to say ) and a diagonal matrix (both with dimensions) such that . Matrix contains the eigenvectors of and the eigenvalues (which are real positives).

Thus, given the model (1), its canonical version is expressed as , where and . In this case, the OLS estimator of is . Then, the general ridge estimator is defined as:

| (2) |

where being for . Note that following Hoerl and Kennard (1970b), the optimal values for are , where are the elements of .

Due to , the expression (2) can be expressed as:

| (3) |

However, in the paper of Hoerl and Kennard (1970a) (page 70), the expression provided is:

| (4) |

which differs from the one obtained in expression (3).

It is true that in the particular case in which , i.e. , expressions (3) and (4) coincide because is an orthogonal matrix and consequently . Thus, in this case (which is universally used when the ridge regression is estimated), there is no contradiction. However, to analyze the generalized version of the ridge regression, the expression (3) should be used instead of (4).

The focus of this paper is to analyze this generalized version of the ridge regression: Section 2 analyzes the properties of the estimator given in (3), its norm (Section 3), the mean squared error (Section 4) and the goodness of fit (Section 5) paying special attention to the particular case when with , since, as will be seen, it has advantages over the one usually used where . Section 6 analyzes the performance of the proposed estimator under the root mean squared error matrix criterion while Section 7 proposes the implementation of inference using bootstrap methodology. Finally, Section 8 illustrates the contribution of this paper with the example of Gorman and Toman (1970) used by Hoerl and Kennard (1970a), and Section 9 summarizes the main conclusions of the work.

2 Estimation properties

This section analyzes the properties of the estimator given in (3) and shows, among other questions, that it is biased. It is calculated as its matrix of variances and covariances and its trace. The augmented model that leads to this estimator is also analyzed.

Thus, due to , it is obtained that:

| (5) |

where:

Definitely:

| (6) |

where is row of matrix and is element of , . When for all , it is verified that .

Furthermore, because the OLS estimator of model (1) is , where . In this case, unless . In addition, due to , it is verified that:

| (7) |

Finally, by following Marquardt (1970) (Theorem 8, page 594), the estimator given in expression (3) is equivalent to the OLS estimator of the augmented model where:

| (8) |

where is a vector of zeros with dimensions, due to

However, this is the unique expression that coincides in the general ridge regression and the augmented model. Thus, for example, the matrix of variances and covariances of the augmented model is , which differs from the one obtained in (7), even when it is supposed that and present the same variance.

2.1 Particular cases

- •

-

•

When it is verified that:

For the case , only the elements of the main diagonal of matrix are modified; and when , all the elements of matrix are modified. In this last case, the generalized ridge (GR), the notation will be used instead of .

Finally, from expression (6), it is obtained that:

As a consequence, , where is the element of . In other words, the estimations do not converge towards zero but around the OLS estimator.

3 The Ridge Trace and Norm

In the work presented by Hoerl and Kennard (1970b), where , the trace of the ridge estimator is used to determine the values of that provide stable estimations. Thus, values of are represented as a function of a rank of values of , usually ; and graphically is observed for what values of the estimations of are stabilized. Hoerl and Kennard (1970b) stated that coefficients chosen from a in this range will undoubtedly be closer to and more stable for prediction than the least squares coefficients.

This way to select is justified by Marquardt (1970) (Theorem 2, page 593) who shows that the norm of the ridge estimator, , decreases when increases. In addition, for , it is obtained that .

This section analyzes the properties of . Thus, considering (5), it is obtained that:

| (9) |

It is evident that when () increases, diminishes. Indeed, when for all , it is verified that .

Consequently, a combination of values for that allow stable estimations of the coefficients of the model can exist.

3.1 Particular cases

4 Mean Squared Error

Because the estimator given in (3) is biased, it is interesting to calculate its mean squared error (MSE) and compare it to the one obtained from OLS.

In this case, the MSE of will be given by:

Furthermore, as it is verified that:

| (11) | |||||

where it was applied that:

being .

As a consequence:

| (12) |

It can be noted that when for all , it is obtained that due to:

4.1 Particular cases

-

•

When , the results are the same that those obtained by Hoerl and Kennard (1970a). Thus, the expression of the MSE is given by:

(13) is a continuous and monotonically decreasing function of while is a continuous and monotonically increasing function of . In addition, if , where is the maximum value of and is the MSE for the OLS estimator of model (1).

-

•

When :

(14) and, consequently,

In that case, due to :

Additionally, the particular point is a minimum due to:

Furthermore, it is verified that:

and, consequently, if

which is true since . Then, for , the estimator given in (3) presents a lower MSE than the one obtained from the OLS estimator.

Because is increasing from (its derivative is positive for ) and decreasing before (its derivative is negative for ) and is a convex function (its second derivative is always positive), Figures 1 and 2 show the graphical representation of the MSE depending on whether the difference is negative or positive. Note that in the first case, is always lower than regardless of the value of .

5 Goodness of fit

Although cross-validation techniques are often used to analyze the goodness of fit of the performed ridge estimation, this section proposes a goodness of fit measure that is the natural extension of the one used in OLS. Thus, given a model similar to (1) with or without an intercept, it is verified111 In fact, , where it was considered that . the decomposition , where are the residuals of such a model.

In this case, the goodness of fit is defined as:

Appendix A shows that this measure is affected by origin changes but not by scale changes. A particular interesting case is when the dependent variable presents zero mean because the decomposition coincides with the sum of squares decomposition222 As shown in Rodríguez et al. (2019), this decomposition of the sum of squares is not verified in the ridge estimation and, consequently, cannot be applied to define a measure of its goodness of fit. traditionally applied to calculate the coefficient of determination, . That is, if , then (see Salmerón et al. (2020) for more details).

Defining the residuals of the ridge regression as , where is given in expression (3), it is obtained that . Since:

it is verified that:

| (15) |

where is the total sum of squares, is the residual sum of squares and is identified with the explained sum of squares of the generalized ridge regression.

In this case, the goodness of fit of the ridge estimation can be defined with the following expression:

| (16) |

Considering that and , it is obtained that:

where . Then, the expression (16) can be given by:

| (17) |

and, consequently, when for all .

Finally, given the augmented model defined by the matrices given in (8), it is verified that , where are the residuals of that model, since:

In this case, the goodness of fit can be defined as:

| (18) |

5.1 Particular cases

-

•

When , expression (16) can be expressed as:

(19) where . Analogously, expression (17) can be rewritten as:

and, then:

i.e., is decreasing as a function of . In addition, .

Furthermore, Rodríguez et al. (2019) analyzed the coefficient of determination in the ridge regression, establishing that for a correct behavior of this measure, the data should be standardized and proposed (Theorem 4) the following expression:

(20) where and are the standardized versions of and , respectively. This measure decrease as a function of .

-

•

When , from expression (17), it is obtained that:

(21) In that case:

i.e., is a decreasing function in . Finally:

6 Comparison in terms of MSE criterion

By following Theobald (1974), Farebrother (1976), Trenklar (1980) and Salmerón et al. (2024), it is possible to state the following result.

Proposition 1

Let , with , be two linear estimators of in equation (1), if it is verified that is a positive definite matrix, then the estimator is better than estimator under the root mean squared error matrix criterion and MSE criterion. That is, is better than estimator when the following inequality is verified:

being a positive definite matrix.

Then, from the previous proposition it is possible to establish that with is preferred over under the criterion of the matrix of the root mean squared if for all .

Proposition 2

The generalized ridge estimator, with , is preferred over the regular ridge estimator, , under the root mean squared error matrix criterion for values of and that satisfy the following expression:

where is a positive definite matrix.

Proof 1

Considering and , it is verified that:

where . Then, if is a positive definite matrix, as is , then their product, that is , is also a positive definite matrix.

Taking into account that with :

-

•

where is a diagonal matrix with elements for .

-

•

where is a diagonal matrix with elements for .

In that case, , and considering :

where .

As , and for all , it is clear that is a positive definite matrix if333 Note that it is not possible that for all , so there must exist an such that . for all .

Finally, from Proposition 2, it is possible to state the following corollaries.

Corollary 1

The generalized ridge estimator, with , is preferred over the OLS estimator, , under the root mean squared error matrix criterion.

Proof 2

Immediate as for all .

Corollary 2

The regular ridge estimator, , is preferred over the OLS estimator, , under the root mean squared error matrix criterion.

Proof 3

Immediate as .

Corollary 3

The regular ridge estimator, , is preferred over generalized ridge estimator, with , under the root mean squared error matrix criterion if .

Proof 4

Immediate taking into account that in this case:

if .

7 Inference

Although there have been various efforts to deal with inference in the ridge estimator (see, for example, Obenchain (1975, 1977), Halawa and El Bassiouni (2000) or Imdad et al. (2018)), in this paper we will focus on the use of bootstrap methods (see, for example, Efron and Tibshirani Efron (1986)).

Thus, given a fixed value of , obtained by any of the methods proposed in the previous subsections, the following steps will be performed:

-

(i)

Generate randomly and with replacement subsamples of equal size to the original one. The value of must be large.

-

(ii)

For each previous subsample, the statistic of is calculated. Therefore, we have values for that statistic: .

-

(iii)

Obtain the approximation of a confidence interval by the expression:

where the 0.025 and 0.975 percentiles of the values calculated in the second step have been considered as lower and upper extremes.

The cases where equals or for the two particular cases analyzed are of interest in this paper.

8 Example

The contribution of this paper is illsutrated in this section with the example previously presented by Hoerl and Kennard (1970a). We first present the results of sections 2 to 6 and then we present the results of section 7. The results obtained are compared with those provided by other R packages for the regular ridge estimator (such as, for example, lmridge (Imdad and Aslam (2023)) and lrmest (Dissanayake and Wijekoon (2016))). Note that the code in (R Core Team (2022)) used to generate the results is available in Github, specifically at https://github.com/rnoremlas/GRR/tree/main/01_Biased_estimation.

8.1 Estimation properties, ridge trace, norm, mean squared error, goodness of fit and root mean squared error matrix criterion

To illustrate the contribution of this paper, this section uses the data set of Gorman and Toman (1970) also used by Rodríguez et al. (2019, 2021) and Hoerl and Kennard (1970a), who stated that Gorman and Toman use this problem as an example to portray a shortcut method for finding a “best” subset of factors of a specified size less than ten without having to compute all regressions of the specified size. This dataset contains 11 independent variables; and contrary to Hoerl and Kennard, the intercept is considered.

In this example, from expressions (5), (12) and (16) we calculate the estimations, the mean squared error and the goodness of fit, respectively, for the following cases:

-

a)

(OLS) ;

- b)

-

c)

(GR) with for (Hoerl and Kennard (1970a)) and

-

d)

(GR) .

For all these calculations, the estimation of , 0.01216569, and (see Table 2) obtained for the OLS after centering the dependent variable (thus, the goodness of fit coincides with the coefficient of determination traditionally applied) will be used.

Note that it should be verified that since is the maximum threshold established in Hoerl and Kennard (1970a) to be verified that a value of exists such that . If this situation is not verified, , can be caused by the fact that is used in the calculation of , while the condition is established for .

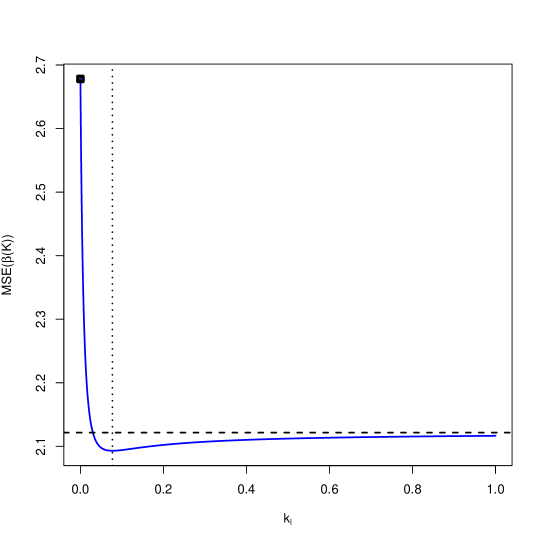

Furthermore, Table 1 shows the value of for , its MSE and whether it is verified that the MSE is always lower than the one obtained by the OLS. Note that the lowest MSE is obtained for , and in this case, the MSE will always be lower than that obtained from the OLS for any value of . The minimum MSE is obtained for . Note that the second column of this table shows the values of proposed by Hoerl and Kennard (1970a). Thus, the optimal values suggested by Hoerl and Kennard correspond to the one that minimizes the MSE when it is considered that all values of are zero except for one of them.

| 1 | 5.675967 | 2.678111 | TRUE |

|---|---|---|---|

| 2 | 5.130849 | 2.678111 | FALSE |

| 3 | 27.21801 | 2.678110 | FALSE |

| 4 | 7.085955 | 2.678110 | FALSE |

| 5 | 1.889662 | 2.678110 | FALSE |

| 6 | 84.11808 | 2.678053 | FALSE |

| 7 | 3.968410 | 2.676016 | TRUE |

| 8 | 7.126586 | 2.677647 | FALSE |

| 9 | 1.754329 | 2.670259 | FALSE |

| 10 | 7.706729 | 2.093025 | TRUE |

| 11 | 7.048761 | 2.494481 | FALSE |

From the results summarized in Table 2, it is possible to conclude that the estimation with the lowest MSE is the one obtained when for with , followed by the case where . As was previously commented, in this second case, it is verified that for any value of (see Figure 3). Furthermore, this estimation is the most similar to the one obtained from the OLS (with lowest ).

| OLS | ||||||

| -1.1480402485 | -0.615975316 | -1.0558162341 | -1.0411181661 | -0.7536100103 | -0.8289615831 | |

| -0.0281064758 | -0.028590426 | -0.0281255168 | -0.0281304843 | -0.0296059930 | -0.0309439917 | |

| -0.0109609943 | -0.010387826 | -0.0108660148 | -0.0108508010 | -0.0095889300 | -0.0108340116 | |

| -0.9948352689 | -0.899367297 | -0.9803653295 | -0.9780152042 | -0.8959178060 | -0.9926400826 | |

| -0.0546405548 | -0.057234825 | -0.0552104328 | -0.0552980693 | -0.0495166302 | -0.0545627458 | |

| -3.9596038257 | -1.825723658 | -3.5638578763 | -3.5016107255 | -3.6255322448 | -4.0218644743 | |

| 0.5449012650 | 0.415759276 | 0.5210035568 | 0.5172413161 | 0.4999095608 | 0.5316978673 | |

| 0.0278180802 | 0.018243272 | 0.0261355566 | 0.0258683518 | 0.0215278846 | 0.0248643709 | |

| 0.0480904082 | 0.049696522 | 0.0484754107 | 0.0485336645 | 0.0484407896 | 0.0456378608 | |

| 0.0008690746 | 0.001331381 | 0.0009551638 | 0.0009686944 | 0.0007518084 | 0.0008365183 | |

| 0.0075720370 | 0.007590831 | 0.0075480354 | 0.0075449443 | 0.0103226880 | 0.0080287843 | |

| 4.862431 | 0.1659039 | 0.2222425 | 0.2790656 | 0.1058898 | ||

| 2.678111 | 5.708535 | 2.438379 | 2.433703 | 1.898926 | 2.093025 | |

| 0.8966053 | 0.8857528 | 0.8962376 | 0.8961127 | 0.8932614 | 0.8959923 |

Unlike in Hoerl and Kennard (1970b), in this case, no change is observed between the estimated sign of any regressor, which can be because in this case, the data have not been transformed (Hoerl and Kennard considered and in correlation form). This fact is observed in the magnitude of the eigenvalues obtained:

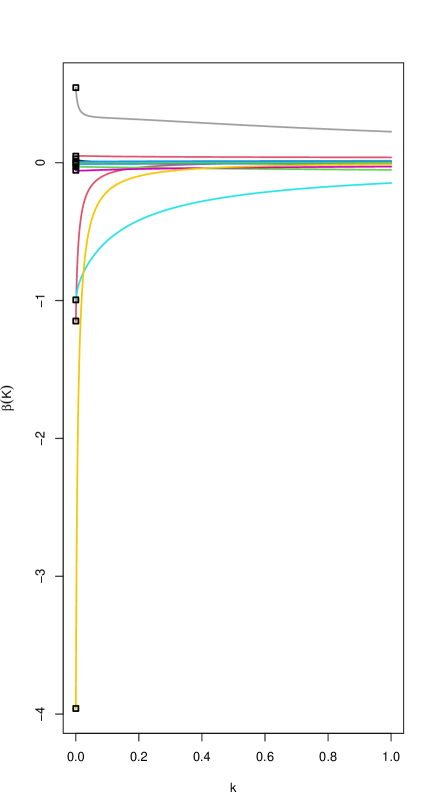

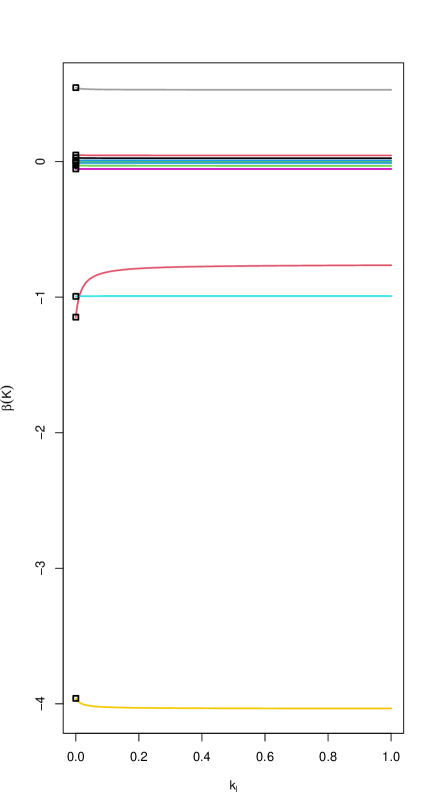

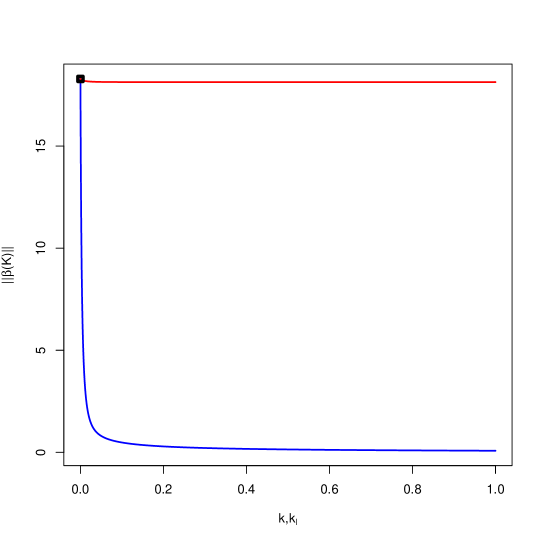

Figure 4 shows the trace for the regular and general estimators for . Note that for the regular case, the estimations converge quickly to zero; while in the generalized case, stability exists around the OLS estimator (see Figure 5). Thus, although the case is not useful to select an optimal subset of variables (objective of Gorman and Toman (1970)), it allows the obtention of an estimation with lower MSE than the one obtained from the OLS and from the regular ridge estimator (see Figure 6). In addition, its goodness of fit is quite superior to the regular case (see Figure 7).

Finally:

- •

- •

-

•

From Corollary 2, the regular ridge estimator with given by option b) is preferred over the OLS estimator under the root mean squared error matrix criterion since .

-

•

From Corollary 3, it cannot be stated that the regular ridge estimator with given by option b) is preferred over the generalized ridge estimator with given by option d) under the root mean squared error matrix criterion since .

8.2 Bootstrap inference and comparison with R packages for regular ridge regression

Considering the steps described in section 7, Table 3 shows the confidence regions for the coefficient estimates and goodness-of-fit presented in 2. It is observed that:

-

•

For and the same coefficients significantly different from zero are found as in OLS (see coefficients highlighted in bold in Table 2), it is to say, , , , , and .

-

•

For and with for , the coefficients significantly different from zero are , , and .

It is noteworthy that Hoerl and Kennard (1970a) proposed to eliminate factors 1, 4, 9 and 10 and that in all the above cases the coefficients and are found to be significantly different from zero in all the cases considered.

In our analysis, it is obtained that the coefficients not significantly different from zero in all the cases are , , , and . Therefore, citing Hoerl and Kennard (1970a), the best subset of size six would be formed by factors 3, 4, 6, 7, 8 and 9.

| OLS | |||

|---|---|---|---|

| (-3.89593670877286, 1.31771775578935) | (-1.4972235906772, 0.80361439048618) | (-3.19279865166447, 1.19026203604696) | |

| (-0.0746860210650758, 0.0288701728558158) | (-0.0681295066239293, 0.0226840137910741) | (-0.0722700019542601, 0.0272846188871276) | |

| (-0.0201978910139842, -0.00127620689098894) | (-0.0194915586692353, 0.000678416531221173) | (-0.0200400342689016, -0.00100072216525185) | |

| (-1.78077495035861, -0.166394171769138) | (-1.57061997928062, -0.228491939197713) | (-1.72844833947927, -0.194212644240152) | |

| (-0.187647062123147, 0.0957148698770658) | (-0.172852329154543, 0.102080145101977) | (-0.180611095797693, 0.0983436130632711) | |

| (-8.00272225783783, -0.948445296629561) | (-2.71473031693527, -0.295195799735598) | (-6.41502094120142, -0.818074617386231) | |

| (0.186308069223282, 0.881008395563819) | (0.0888668647118551, 0.618211914112481) | (0.167878220326808, 0.793955175670512) | |

| (0.000823469538757971, 0.0615556176023861) | (-0.000679711901738476, 0.0311983206337429) | (0.000838371938236545, 0.0517612679286025) | |

| (0.0221546964556036, 0.0791226146581368) | (0.023721596560448, 0.0741895704635099) | (0.0228830017842054, 0.0764930491373058) | |

| (-0.00220235044946133, 0.0027100927479362) | (-0.000392435367310374, 0.00394377007346599) | (-0.00162247498865634, 0.00299335075577762) | |

| (-0.00556691271200455, 0.0222622756193275) | (-0.00462494988856312, 0.0206533525888555) | (-0.00513106191290476, 0.0213688925964588) | |

| (0.857185313518575, 0.97164950986312) | (0.840186693183264, 0.959583929196788) | (0.856311324646987, 0.97068418568284) |

| (-3.09239223213121, 1.16981841814523) | (-3.38520846820602, 1.0512081553846) | (-4.2798251137177, 1.31998326926375) | |

| (-0.0720514870609311, 0.0270330434047115) | (-0.067972207973036, 0.046076825523836) | (-0.0756048479419764, 0.0272571255591297) | |

| (-0.0200072077286324, -0.00097725498919722) | (-0.0175438193378674, 0.00464366168337011) | (-0.0200130463050139, -0.000997629197896326) | |

| (-1.7234275126921, -0.19921955432199) | (-1.41926424337071, -0.11606510002292) | (-1.73791357943147, -0.164450357806185) | |

| (-0.18001713544389, 0.0983404685195195) | (-0.201733516738824, 0.0812856776180331) | (-0.183661133705017, 0.101420519265672) | |

| (-6.21419416571285, -0.794509459423308) | (-6.10934913342415, -0.526855942293644) | (-7.61576909348567, -0.620743075198675) | |

| (0.165337227615227, 0.784035140713891) | (0.158331109934828, 0.740149897755549) | (0.180033452471868, 0.866413728317379) | |

| (0.000810084536847535, 0.0505358206712533) | (-0.00499451597678027, 0.0521926397597579) | (0.0000545730315833507, 0.063577654448548) | |

| (0.0228902546019822, 0.0764945473119876) | (0.00324670854793468, 0.0684720229516689) | (0.022275040865436, 0.0766410723880503) | |

| (-0.0015571902348841, 0.00304229881108438) | (-0.00526014539785334, 0.00176650694974561) | (-0.00198860640841325, 0.00286862922654762) | |

| (-0.0051988219960957, 0.0212521270327134) | (-0.00216000114030527, 0.0273869174467935) | (-0.00551939277398953, 0.022020812221216) | |

| (0.856170314838873, 0.970331026132404) | (0.676427685731761, 0.941501956648788) | (0.847262409158761, 0.968610582604451) |

Next, the information shown in Tables 2 and 3 for the regular ridge estimator is compared with the estimation and inference obtained by the R packages lmridge (Imdad and Aslam (2023)) and lrmest (Dissanayake and Wijekoon (2016)) de R, which is presented in Table 4. Note that the package lrmest444 The command rid provides the estimation and inference of the model and the mean squared error :

-

•

provides the same estimations for the coefficients and values of MSE than the one shown in Table 2 for the regular ridge regression.

-

•

From Table 5, exactly the same coefficients significantly different from zero are identified except for the case , where it further considers that and are significantly different from zero.

While the package lmridge555 The command lmridge provides the model estimates including inference and goodness-of-fit, among other values. The command rstats1 provides, among other values, the mean square error. Finally, the command kest provides different estimates for the parameter , including . :

-

•

It provides the same estimates of the coefficients as those given in Table 2 for the regular ridge estimator only when , for all other values of the estimates are not the same but are similar.

-

•

The same applies to the goodness-of-fit: it only matches for .

- •

-

•

Finally, Table 5 Identifies exactly the same coefficients significantly different from zero as the bootstrap inference proposed in the present work and that given by the lrmest except for the case when , where it identifies significantly different from zero the same coefficients as lrmest except for .

| lrmest | lmridge | lrmest | lmridge | lrmest | lmridge | lrmest | lmridge | |

| -1.1480 (0.1980) | -1.1480 (0.3007) | -0.6160 (0.3083) | -0.8899 (0.4015) | -1.0558 (0.2146) | -1.1018 (0.3125) | -1.0411 (0.2174) | -1.0944 (0.3147) | |

| -0.0281 (0.1199) | -0.0281 (0.1131) | -0.0286 (0.0969) | -0.0264 (0.1486) | -0.0281 (0.1170) | -0.0278 (0.1174) | -0.0281 (0.1166) | -0.0277 (0.1182) | |

| -0.0110 (0.0224) | -0.0110 (0.0201) | -0.0104 (0.0291) | -0.0105 (0.0307) | -0.0109 (0.0234) | -0.0109 (0.0210) | -0.0109 (0.0236) | -0.0109 (0.0212) | |

| -0.9948 (0.0015) | -0.9948 (0.0012) | -0.8994 (0.0022) | -0.9033 (0.0026) | -0.9804 (0.0016) | -0.9812 (0.0013) | -0.9780 (0.0016) | -0.9789 (0.0014) | |

| -0.0546 (0.2555) | -0.0546 (0.2464) | -0.0572 (0.2328) | -0.0571 (0.2432) | -0.0552 (0.2505) | -0.0552 (0.2423) | -0.0553 (0.2497) | -0.0553 (0.2418) | |

| -3.9596 (0.0071) | -3.9596 (0.0062) | -1.8257 (0.0086) | -1.8627 (0.0088) | -3.5639 (0.0073) | -3.5756 (0.0063) | -3.5016 (0.0073) | -3.5150 (0.0063) | |

| 0.5449 (0.0004) | 0.5449 (0.0003) | 0.4158 (0.0009) | 0.4313 (0.0011) | 0.5210 (0.0004) | 0.5239 (0.0004) | 0.5172 (0.0004) | 0.5206 (0.0004) | |

| 0.0278 (0.0160) | 0.278 (0.0142) | 0.0182 (0.0327) | 0.0210 (0.0526) | 0.0261 (0.0179) | 0.0266 (0.0172) | 0.0259 (0.0183) | 0.0264 (0.0177) | |

| 0.0481 (0.0007) | 0.0481 (0.0006) | 0.0497 (0.0002) | 0.0515 (0.0004) | 0.0485 (0.0006) | 0.0488 (0.0005) | 0.0485 (0.0006) | 0.0489 (0.0005) | |

| 0.0009 (0.2161) | 0.0009 (0.2074) | 0.0013 (0.0449) | 0.0013 (0.0480) | 0.0010 (0.1678) | 0.0010 (0.1604) | 0.0010 (0.1610) | 0.0010 (0.1539) | |

| 0.0076 (0.2594) | 0.0076 (0.2503) | 0.0076 (0.2530) | 0.0072 (0.2883) | 0.0075 (0.2601) | 0.0075 (0.2556) | 0.0075 (0.2602) | 0.0075 (0.2565) | |

| 2.6781 | 1.8505 | 5.7085 | 4.9392 | 2.4384 | 1.6801 | 2.4337 | 1.6839 | |

| 0.896600 | 0.864300 | 0.889500 | 0.88850 | |||||

| GRR | lrmest | lmridge | GRR | lrmest | lmridge | GRR | lrmest | lmridge | GRR | lrmest | lmridge | |

It should be noted that the R packages genridge (Friendly (2023)) and ridge (Cule et al. (2022)) have also been used, obtaining from the former values very different from those presented in this paper and from the latter exactly the same values as those given by the lmridge package. Other R packages that provide estimates for regular ridge regression are listed in Imdad et al. (2018). However, in order not to extend the present work, we have considered what we believe to be the most representative.

9 Conclusions

Hoerl and Kennard (1970b, a) presented the ridge estimation for the particular case when (known as the regular ridge estimator), although they parted from a general case in which is a diagonal matrix whose elements can be all different between them. This paper develops this alternative version of the general case that was not previously analyzed to the best of our knowledge. We pay special attention to the case in which all the elements of the diagonal of matrix are equal to zero except for one, , with .

As a relevant contribution, this paper presents the expression of this general estimator, which is different from the one presented by Hoerl and Kennard. This paper also analyzed the estimator’s main characteristics (unbiased, matrix of variances and covariances and the augmented model), its norm, its mean squared error and its goodness of fit. The expressions obtained for the norm, mean squared error and goodness of fit verify its property of being continuous (i.e., coincides with the expressions of the OLS when is a null matrix). As would be desirable, the norm and the measure of goodness of fit decrease as a function of .

In relation to the particular case when , the following is observed:

-

•

All the elements of matrix are affected in the calculation of this estimator instead of in the case of the regular estimator regular, where only the elements of the main diagonal are affected. It could be interesting to analyze whether this generalization improves the calculation of the inverse matrix in comparison with the regular case. In addition, and contrary to the regular case, the estimations do not converge towards zero but are around the OLS estimation.

-

•

The norm of the estimator decreases and converges around the norm of the OLS estimator (again, it is not converging towards zero as in the regular case). This fact indicates that a range of values for that stabilize the calculated estimation can exist.

-

•

Contrary to the regular case, it is possible to calculate the value of that minimizes the MSE and that leads to a MSE lower than that obtained from the OLS. From the two scenarios obtained when analyzing its asymptotic behavior, in one of them, the MSE is always lower than the one obtained from OLS regardless of the value of .

-

•

A new original alternative for measuring the goodness of fit not only in this generalization but also in the regular case is proposed. The closed expression was obtained and analyzed being decreasing as a function of . When the dependent variable has zero mean, this alternative version coincides with the coefficient of determination traditionally applied. For standardized data and for the regular case, it coincides with the proposal presented by Rodríguez et al. (2019).

In conclusion, this particular case provides higher stability for the calculated expressions. This fact makes it preferable to the other options considered, as shown in the example. In addition, the proposed bootstrap inference identifies those coefficients significantly different from zero.

Finally, as a future research line, it could be interesting to analyze the usability of this particular case to mitigate the degree of near multicollinearity existing in the multiple linear regression model. In addition, due to the differences detected in the illustrative example regarding the results provided by the different R Core Team (2022) packages considered nd to the fact that none (to the best of our knowledge) has the option of generalized ridge regression, we consider it appropriate to approach the creation of a package that integrates the code provided in Github (https://github.com/rnoremlas/GRR/tree/main/01_Biased_estimation).

Appendix A Goodness of Fit and Data Transformation

Given the expression:

and by considering the transformation for with , it is obtained that:

and, consequently:

It is concluded that the GoF is affected by origin changes but not by scale changes.

References

- Balakrishnant (1963) Balakrishnant, A. (1963). An operator theoretic formulation of a class of control problems and a steepest descent method of solution. Journal of the Society for Industrial and Applied Mathematics, Series A: Control 1(2), 109–127.

- Casella (1980) Casella, G. (1980). Minimax ridge regression estimation. The Annals of Statistics, 1036–1056.

- Cule et al. (2022) Cule, E., S. Moritz, and D. Frankowski (2022). ridge: Ridge Regression with Automatic Selection of the Penalty Parameter. R package version 3.3.

- Dissanayake and Wijekoon (2016) Dissanayake, A. and P. Wijekoon (2016). lrmest: Different Types of Estimators to Deal with Multicollinearity. R package version 3.0.

- Donoho and Johnstone (1995) Donoho, D. L. and I. M. Johnstone (1995). Adapting to unknown smoothness via wavelet shrinkage. Journal of the american statistical association 90(432), 1200–1224.

- Efron (1986) Efron, B., T. R. (1986). Bootstrap methods for standard errors, confidence intervals, and other measures of statistical accuracy. Statistical Science 1(1), 54–75.

- Farebrother (1976) Farebrother, R. (1976). Further results on the mean square error of ridge regression. Journal of the Royal Statistical Society. Series B (Methodological), 248–250.

- Fletcher (2013) Fletcher, R. (2013). Practical methods of optimization. John Wiley & Sons.

- Frank and Friedman (1993) Frank, L. E. and J. H. Friedman (1993). A statistical view of some chemometrics regression tools. Technometrics 35(2), 109–135.

- Friendly (2023) Friendly, M. (2023). genridge: Generalized Ridge Trace Plots for Ridge Regression. R package version 0.7.0.

- Fu (1998) Fu, W. J. (1998). Penalized regressions: the bridge versus the lasso. Journal of computational and graphical statistics 7(3), 397–416.

- Gorman and Toman (1970) Gorman, J. and R. Toman (1970). Selection of variables for fitting equations to data. Technometrics 8, 27–51.

- Halawa and El Bassiouni (2000) Halawa, A. and M. El Bassiouni (2000). Tests of regression coefficients under ridge regression models. Journal of Statistical Computation and Simulation 65(1-4), 341–356.

- Harville (1998) Harville, D. A. (1998). Matrix algebra from a statistician’s perspective.

- Hastie (2020) Hastie, T. (2020). Ridge regularization: An essential concept in data science. Technometrics 62(4), 426–433.

- Hoerl (1962) Hoerl, A. (1962). Application of ridge analysis to regression problems. Chemical Engineering Progress 58, 54–59.

- Hoerl (1964) Hoerl, A. (1964). Ridge analysis. Chemical Engineering Progress Symposium Series 60, 67–77.

- Hoerl and Kennard (1968) Hoerl, A. and R. Kennard (1968). On regression analysis and biased estimation. Technometrics 10(Abstract), 422–423.

- Hoerl et al. (1975) Hoerl, A. E., R. W. Kannard, and K. F. Baldwin (1975). Ridge regression: some simulations. Communications in Statistics-Theory and Methods 4(2), 105–123.

- Hoerl and Kennard (1970a) Hoerl, A. E. and R. W. Kennard (1970a). Ridge regression: applications to nonorthogonal problems. Technometrics 12(1), 69–82.

- Hoerl and Kennard (1970b) Hoerl, A. E. and R. W. Kennard (1970b). Ridge regression: Biased estimation for nonorthogonal problems. Technometrics 12(1), 55–67.

- Hoerl (2020) Hoerl, R. W. (2020). Ridge regression: a historical context. Technometrics 62(4), 420–425.

- Imdad et al. (2018) Imdad, M., M. Aslam, and S. Altaf (2018). lmridge: A comprehensive r package for ridge regression. The R Journal 10(2), 326–346.

- Imdad and Aslam (2023) Imdad, M. U. and M. Aslam (2023). lmridge: Linear Ridge Regression with Ridge Penalty and Ridge Statistics. R package version 1.2.2.

- Jeffreys (1998) Jeffreys, H. (1998). The theory of probability. OUP Oxford.

- Klinger (1998) Klinger, A. (1998). Hochdimensionale generalisierte lineare Modelle. Shaker.

- Ljndley and Smith (1972) Ljndley, D. and A. Smith (1972). Bayes estimators for the linear model (with discussion). JR Statist. Soc, 1–41.

- Marquardt (1970) Marquardt, D. W. (1970). Generalized inverses, ridge regression, biased linear estimation, and nonlinear estimation. Technometrics 12(3), 591–612.

- Obenchain (1975) Obenchain, R. (1975). Ridge analysis following a preliminary test of the shrunken hypothesis. Technometrics 17(4), 431–441.

- Obenchain (1977) Obenchain, R. (1977). Classical f-tests and confidence regions for ridge regression. Technometrics 19(4), 429–439.

- Piegorsch and Casella (1989) Piegorsch, W. W. and G. Casella (1989). The early use of matrix diagonal increments in statistical problems. SIAM review 31(3), 428–434.

- R Core Team (2022) R Core Team (2022). R: A Language and Environment for Statistical Computing. Vienna, Austria: R Foundation for Statistical Computing.

- Raiffa and Schlaifer (1961) Raiffa, H. and R. Schlaifer (1961). Applied statistical decision theory. Technical report.

- Rodríguez et al. (2019) Rodríguez, A., R. Salmerón, and C. García (2019). The coefficient of determination in the ridge regression. Communications in Statistics - Simulation and Computation, https://doi.org/10.1080/03610918.2019.1649421.

- Rodríguez et al. (2021) Rodríguez, A., R. Salmerón, and C. García (2021). Obtaining a threshold for the stewart index and its extension to ridge regression. Computational Statistics 36, 1011–1029.

- Rolph (1976) Rolph, J. E. (1976). Choosing shrinkage estimators for regression problems. Communications in Statistics-Theory and Methods 5(9), 789–802.

- Salmerón et al. (2024) Salmerón, R., C. García, and J. García (2024). The raise regression: Justification, properties and application. International Statistical Review Accepted.

- Salmerón et al. (2020) Salmerón, R., C. G. García, and J. García Pérez (2020). Detection of near-multicollinearity through centered and noncentered regression. Mathematics 8, 931.

- Stein (1960) Stein, C. (1960). Multiple regression, contributions to probability and statistics. essays in honor of Harold Hotelling 103.

- Strawderman (1978) Strawderman, W. E. (1978). Minimax adaptive generalized ridge regression estimators. Journal of the American Statistical Association 73(363), 623–627.

- Theobald (1974) Theobald, C. M. (1974). Generalizations of mean square error applied to ridge regression. Journal of the Royal Statistical Society: Series B (Methodological) 36(1), 103–106.

- Tibshirani (1996) Tibshirani, R. (1996). Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society: Series B (Methodological) 58(1), 267–288.

- Trenklar (1980) Trenklar, G. (1980). Generalized mean squared error comparisons of biased regression estimators. Communications in Statistics-Theory and Methods 9(12), 1247–1259.

- Zhang and Politis (2022) Zhang, Y. and D. N. Politis (2022). Ridge regression revisited: Debiasing, thresholding and bootstrap. The Annals of Statistics 50(3), 1401–1422.

- Zou and Hastie (2005) Zou, H. and T. Hastie (2005). Regularization and variable selection via the elastic net. Journal of the royal statistical society: series B (statistical methodology) 67(2), 301–320.