Subgroup Identification with Latent Factor Structure

Abstract

Subgroup analysis has garnered increasing attention for its ability to identify meaningful subgroups within heterogeneous populations, thereby enhancing predictive power. However, in many fields such as social science and biology, covariates are often highly correlated due to common factors. This correlation poses significant challenges for subgroup identification, an issue that is often overlooked in existing literature. In this paper, we aim to address this gap in the “diverging dimension” regime by proposing a center-augmented subgroup identification method within the Factor Augmented (sparse) Linear Model framework. This method bridges dimension reduction and sparse regression. Our proposed approach is adaptable to the high cross-sectional dependence among covariates and offers computational advantages with a complexity of , compared to the complexity of the conventional pairwise fusion penalty method in the literature, where is the sample size and is the number of subgroups. We also investigate the asymptotic properties of the oracle estimators under conditions on the minimal distance between group centroids. To implement the proposed approach, we introduce a Difference of Convex functions-based Alternating Direction Method of Multipliers (DC-ADMM) algorithm and demonstrate its convergence to a local minimizer in a finite number of steps. We illustrate the superiority of the proposed method through extensive numerical experiments and a real macroeconomic data example. An R package, SILFS, implementing the method is also available on CRAN111https://cran.r-project.org/web/packages/SILFS/index.html.

keywords:

Subgroup Analysis; Factor Augmented Sparse Linear Model; Oracle Property; Center-augmented Regularization1 Introduction

With advancements in data collection and information technology, the dimensionality of data has exponentially increased across various research and application fields. Concurrently, it is believed that meaningful subgroups exist within heterogeneous populations in many real datasets. In macroeconomics, Phillips and Sul (2007) analyzes the convergence in the cost of living indices among 19 U.S. metropolitan cities, demonstrating that cities within different groups behave quite differently. In portfolio allocations, stocks within the same industries exhibit similar characteristics (Livingston, 1977). In precision medicine, patients may belong to various latent groups, and those within the same group can be considered together for making treatment decisions; see, for example, Ma and Huang (2017) and Chen et al. (2021a). Wang and Su (2021) also points out that geographic adjacency is a natural criterion for grouping when analyzing international trade and economic geography datasets. These examples underline the importance of identifying latent group structures prior to conducting statistical inference, as this approach significantly enhances statistical efficiency.

Statisticians and econometricians typically characterize group structures using group-specific parameters in statistical models. This topic is closely related to concepts such as integrative analysis, transfer learning, and multi-task representation learning. For integrative analysis, Gertheiss and Tutz (2012) and Ollier and Viallon (2017) assume that the coefficients of the -th group, denoted as , can be decomposed into and , where is a common parameter shared by all groups, and is the group-specific parameter representing the heterogeneity of group structures. Similarly, in the context of transfer learning or multi-task representation learning, Li et al. (2022) and Tian et al. (2023) also use group-specific parameters to characterize the heterogeneity of group structures. However, it is worth noting that the aforementioned works presume the group membership is known a priori, which is not the case in many real applications. In the context of subgroup analysis, Ma and Huang (2017), Zhang et al. (2019) and He et al. (2022c) employ group-specific regression coefficients while assuming unknown group membership. They aim to cluster the samples and conduct statistical inference simultaneously. In this paper, we also adopt the unknown group membership framework and consider the following linear model with group-specific intercepts:

| (1.1) |

where is the response vector, denotes the design matrix, is the noise vector, and the unknown vector of regression coefficients is sparse. The group structure is characterized by the intercept parameters , meaning that individuals within the same group share the same group-specific intercept parameter. Specifically, let the number of subgroups be , and define as a partition of , satisfying for . It is assumed that for in , and represents the centroid of the group-specific parameters. It is worth noting that may reflect heterogeneity driven by latent variables , that is, . For example, in microeconomics, the impact of education on wages is a widely studied topic. However, individuals may have different backgrounds, such as family background and work experience, which can be modeled as . See, for example, Ashenfelter and Krueger (1994), Michele and Francesco (2018) and Connolly and Gottschalk (2006). More generally, the coefficients for can be subject-specific, as the same family background and work experience may have different impacts for different individuals. In this case, the model would become

| (1.2) |

Throughout this article, we focus on the model (1.1), assuming that the heterogeneity arises from unobserved covariates . In fact, model (1.2) is similar to model (1.1), and our proposed algorithms and the associated theoretical properties for model (1.1) can be extended to model (1.2) with slight modifications.

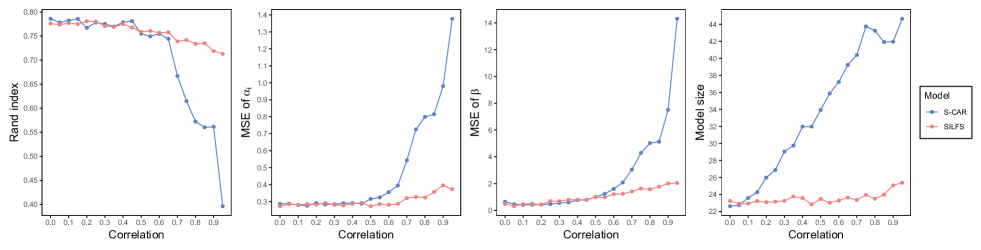

In datasets from social science and biology, high-dimensional covariates are often highly correlated, possibly due to the existence of common factors. See, for example, Stock and Watson (2002), Bai and Ng (2002), Fan et al. (2020), Vatcheva et al. (2016), Porcu et al. (2019) and He et al. (2022a). The high cross-sectional dependence among covariates can lead to unsatisfactory results in various statistical inference problems, including the subgroup identification problem discussed in this paper. In the following, we present a toy example to illustrate the impacts of high collinearity on the subgroup identification problem. For model (1.1), each group-specific takes value of either or with equal probability. We generate the residuals from , and let . Set , where the nonzero coefficients are drawn from . Let be independent copies from multivariate normal distribution , where is a covariance matrix with off-diagonal elements being and diagonal elements being . In this toy example, the parameter is varied over the interval [0, 0.95] with a step size of 0.05 to illustrate different strengths of cross-sectional dependency. For each given , we consider the Center-augmented Regularizer (CAR) method proposed by He et al. (2022c), referred to as Standard CAR (S-CAR). We report the averages of model size, estimation errors (MSE), and Rand Index over 100 replications in Figure 1. As illustrated in the Figure 1 (the blue lines), both the clustering performance and the estimation accuracy of S-CAR deteriorate as the cross-sectional dependency strength, , increases. The CAR method shows limited power in detecting group structures under high cross-sectional dependency, especially when .

To the best of our knowledge, there exists no literature addressing subgroup analysis under conditions of high collinearity among covariates, due to both computational and statistical challenges. In this work, we propose to address the high cross-sectional dependency among covariates using a factor model approach, inspired by the Factor Augmented (sparse linear) Regression Model (abbreviated as FARM) introducted in Fan et al. (2020) and Fan et al. (2023). Factor model is widely used as an effective tool for dimension reduction and can capture various levels of cross-sectional dependence. It is well recogonized that many macroeconomic and financial datasets exhibit high cross-sectional dependence. For instance, Fama and French (1992) and Fama and French (2015) provide evidence that average stock returns, characterized by high cross-sectional dependence, are driven by Fama-French factors. Additionally, McCracken and Ng (2016) confirm that the well-studied microeconomic dataset FRED-MD also exhibits latent factor structures. Johnstone and Paul (2018) investigate numerous datasets showing spiked structures in covariance matrices across various fields, including microarrays, satellite images, medical shapes, climate data, and signal detection. Therefore, it is reasonable to mitigate high collinearity and achieve dimension reduction simultaneously by assuming a latent factor model. In this paper, we adopt the FARM framework to address the challenges posed by high collinearity and high-dimensionality in the subgroup analysis problem. More specifically, we assume the vector of regression coefficients is sparse with a support set , and the observed ’s satisfy the following factor structure:

| (1.3) |

where , is the factor score matrix, is the factor loading matrix, and is the matrix of idiosyncratic errors of dimension . To illustrate the advantage of the FARM framework in the presence of high collinearity, we substitute (1.3) into (1.1) to form the following sparse regression model

| (1.4) |

where and extract essential information from , and contributes additional sparse information to the response. The identifiability condition on and will be discussed in Section 2.1. This construction augments the highly cross-dependent covariates to weakly dependent covariates . Subsequently, we adopt the FARM framework to capture the cross-sectional dependence of covariates in subgroup analysis. Our goal is to identify latent groups characterized by the intercept parameters and achieve variable selection simultaneously under model (1.4). Hereafter, we treat the group number and factor number as fixed, while allowing the dimension to increase with the sample size .

1.1 Literature Review

A closely related line of research focuses on sparse linear regression and variable selection. Over the last two decades, numerous regularization-based methods have been proposed, including well-known approaches such as LASSO (Tibshirani, 1996), SCAD (Fan and Li, 2001), elastic net (Zou and Hastie, 2005) and adaptive LASSO (Zou, 2006). The effectiveness of regularized regression methods often relies on constraints imposed on the covariance matrix of the covariates and limitations on collinearity levels. However, these constraints may be inappropriate in real macroeconomic or financial applications.

Another closely related line of research focuses on large-dimensional approximate factor models. Bai (2003) explored the theory of large-dimensional approximate factor models, and theoretical guarantees for determining the number of factors can be found in works such as Bai and Ng (2002) and Ahn and Horenstein (2013). Robust factor analysis has also gained increasing attention in recent years, as evidenced by studies like Chen et al. (2021b), He et al. (2022b) and He et al. (2023). Furthermore, Stock and Watson (2002) demonstrates the consistency of Ordinary Least Squares (OLS) estimates in factor-augmented regressions, treating latent factors as predictors. Ando and Tsay (2011) extends this approach to quantile factor-augmented regressions, with further extensions discussed in Wang et al. (2019) and Fan et al. (2021). In high-dimensional regression settings, latent factors often cannot fully explain the response, particularly when their effect is weak. Fan et al. (2020) proposes the Factor Augmented (sparse linear) Regression Model, which assumes sparsity in the coefficient vector and integrates both latent factors and idiosyncratic components into the linear regression framework. Fan et al. (2023) introduces hypothesis tests for assessing the adequacy of latent factor regression models. Additionally, Tu and Wang (2024) present a new class of information criteria aimed at achieving consistent factor and covariate selection jointly in factor-augmented regression.

The last closely related line of research focuses on subgroup analysis. Typical approaches for subgroup identification can generally be categorized into two distinct types. The first type is the finite mixture model (FMM), which employs model-based clustering techniques. Representative works include but are not limited to Banfield and Raftery (1993), Hastie and Tibshirani (1996), and Wei and Kosorok (2013) for mixture models under Gaussian distributions; Shen and Huang (2010) for logistic-normal regression; Yao et al. (2014) for the Student distribution; and Song et al. (2014) for the Laplace distribution. For finite mixture models, Khalili and Chen (2007) propose penalized likelihood methods for variable selection and establish their consistency. In high-dimensional cases, references include Zhang et al. (2020) and Wang et al. (2023). Although the EM algorithm is effective and powerful in finding maximum likelihood estimators with latent group variables in FMM, it suffers from significant computational burdens in high dimensions. The second type is regularization methods, which use fusion penalties to enforce sparsity in pairwise differences among group-specific parameters to achieve clustering. Examples include Hocking et al. (2011), Pan et al. (2013), Chi and Lange (2015), and Wu et al. (2016). For subgroup analysis of linear models, Ma and Huang (2017) propose a concave Pairwise Fusion Penalty (PFP) capable of recovering latent groups without prior information on the number of groups. Many subsequent studies adopt this penalty for its favorable statistical properties, including extensions to quantile regressions (Zhang et al., 2019) and functional regressions (Zhang et al., 2022) for group pursuits. From a computational perspective, the PFP, which pairs samples, has a computational complexity of . To mitigate this, Wang and Zhu (2024) introduce a threshold PFP method to reduce computational time and enhance group detection accuracy. Moreover, He et al. (2022c) propose a more efficient Center-augmented Regularization (CAR) method, reducing computational complexity to by incorporating group centroids as parameters. However, due to the concavity of PFP and CAR, their performance is sensitive to the selection of initial values. Therefore, choosing appropriate initial values remains a challenging task.

1.2 Contributions and Structure of the Paper

In this work, we propose a clustering method within the FARM framework, coined Subgroup Identification with Latent Factor Structures (SILFS). SILFS demonstrates superior performance compared to existing methods in two critical aspects: identifying group memberships and simultaneously recovering the support of regression coefficients in the presence of high collinearity among covariates. Returning to Figure 1 (the red lines), we observe that SILFS exhibits robust performance across varying levles of cross-sectional dependence parameterized by . Notably, for , SILFS significantly outperforms the S-CAR method, highlighting the necessity of accounting for high cross-sectional dependency among covariates in subgroup identification problems and the novelty of our approach. Additionally, the SILFS method draws inspiration from Center-augmented Regularization, offering computational advantages over pairwise fusion penalization methods. Theoretically, we establish properties of the local minima for the optimization problem under an -type CAR penalty. We provide, to the best of our knowledge, the first rigorous theoretical guarantee that CAR can effectively identify subgroups under the distance. To achieve these local minima, we propose a DC-ADMM algorithm that fully exploits the mathematical structure of the CAR penalty. In implementing the DC decomposition of the CAR penalty under inequality constraints, we convert these inequalities into equivalent equalities by introducing slack variables and incorporating indicator functions into the objective function. We derive explicit iteration formulas for the equivalent optimization problem and demonstrate that our algorithm converges to a Karush-Kuhn-Tucker (KKT) point of the objective function after a finite number of iterations.

The remainder of this paper is organized as follows. Section 2 introduces the optimization problem of SILFS and presents a two-step algorithm to solve it. In Section 3, we establish the consistency of the oracle estimators and demonstrate that they serve as local minimizers of the proposed optimization problem with probability approaching one. Section 4 presents extensive simulation studies that illustrate the superior performance of the SILFS method in both clustering and variable selection. Furthermore, computational speed comparisons with various methods highlight the computational advantages of our proposed approach. In Section 5, we apply the SILFS method to a large panel of China’s commodity trade data involving all countries worldwide from 2019. We conclude with a discussion on potential future research directions and summarize our findings in Section 6. The supplementary material includes proofs for all theorems and additional details on algorithm implementations.

To conclude this section, we introduce the notations that will be used throughout the remainder of this paper. For a matrix , denote and as its Frobenius norm and operator norm, respectively. Write , and . Let and be two subsets of . We denote as the submatrix of with row indices in and column indices in . The matrix denotes the submatrix of consisting of columns whose indices belong to the set . Here, denotes the cardinality of . Moreover, represents the -dimensional identity matrix, and denotes the zero-matrix of size of . and denote the -dimensional vectors with all elements being and , respectively. The function is defined such that if , if , and . For a set of indices and a function where , denotes the sub-gradient of with respect to , where consists of elements of indexed by . For two sequences of real numbers and , we use the notation or to indicate that as , and if there exist a positive integer and a positive constant such that for all .

2 Methodology

In this section, we introduce a two-step procedure to estimate the parameters and in model (1.4). In Section 2.1, we first estimate the unobserved and . Subsequently, in Section 2.2, we formulate a center-augmented regularization optimization problem using plug-in estimators to achieve simultaneous clustering and variable selection. Section 2.3 discusses implementation details of the algorithm, including the selection of initial values, the number of subgroups , and the shrinkage parameters and .

2.1 Estimation of Factor Model

Given the presence of an unknown factor structure in model (1.1), our first step is to estimate these factors from the observed predictors . To achieve this, we employ Principal Component Analysis (PCA) to estimate the latent factors and the factor loading matrix . Specifically, Fan et al. (2013) demonstrate that the PCA method is equivalent to the following constrained least squares:

| s.t. |

where the normalization constraints address identifiability concerns (Bai, 2003). Through simple algebra, the estimated factors correspond to the eigenvectors associated with the largest eigenvalues of , and . The idiosyncratic components can be computed straightforwardly as .

However, the number of latent factors is unknown in practice. There are various methods in the literature to derive consistent estimators of , such as the Information Criteria (IC) proposed by Bai and Ng (2002) and the Eigenvalue-Ratio (ER) criterion proposed by Lam and Yao (2012) and Ahn and Horenstein (2013). Since the estimation of is often conducted separately, we assume that the number of factors is given.

2.2 Clustering Procedure

To recovery the group membership and estimate the regression coefficients simultaneously, we plug in the PCA estimators and and formulate the following optimization problem with a given number of subgroups :

| (2.1) |

where , and are tuning parameters, and is a penalty for group pursuits. The penalty, , encourages sparsity for variable selection.

In this paper, we choose as the CAR penalty for group pursuit. The CAR method, initially proposed by He et al. (2022c), aims to estimate both the group-specific parameter and the group centroids simultaneously. This is achieved by clustering each subject into group based on the nearest distance. Specifically,

where is a distance function between and . This approach is analogous to the -means method when using -type distance () or the -median method when employing -type distance (). From an optimization perspective, CAR exhibits a computational complexity of , whereas pairwise penalties used in Ma and Huang (2017) and Zhang et al. (2019), such as with penalty function , require computational complexity. Hence, CAR significantly reduces computational burdens by incorporating centroid parameters. Furthermore, as CAR is a non-convex penalty, it presents challenges for both theoretical analysis and optimization. It is worth noting that CAR does not directly offer clustering results. If represents the estimated group centroids, our clustering rule for the -th subject is defined as if and only if for .

Recall that the optimization problem outlined in (2.1) depends on the choice of the distance function. In the following, we introduce the DC-ADMM and Cyclic Coordinate Descent (CCD) algorithm to solve the problem for -type and -type distances, respectively.

2.2.1 DC-ADMM Algorithm

In this section, we propose the DC-ADMM algorithm to solve (2.1) under the -type distance. The corresponding theoretical results are elaborated in Theorem 2.1. The optimization problem is as follows:

| (2.2) |

This optimization problem is challenging due to the identifiability issue with the parameter and its non-convex nature. For example, when and minimizes the loss function in (2.1), it is evident that also serves as a minimizer. To address the identifiability issue, we impose the condition that , which is also crucial for the following optimization. Motivated by the works of An and Tao (2005) and Wu et al. (2016) on Difference of Convex (DC) programming to address non-convex optimization problems, we reformulate the CAR penalty as a difference of convex functions under the identifiability condition of . Specifically, we have with

We reparameterize the variables by letting for . Now, both and are convex functions with respect to , where with .

Therefore, the original problem is equivalent to

We can then define a sequence of lower approximations of as

where is the sub-gradient of and is the estimator of from the -th iteration. More specifically, let be the sub-gradient of with respect to . Under the -type distance for , we have

and otherwise we have

The DC programming approach encourages us to optimize an upper approximation in the -th iteration, which is

| (2.3) | ||||

Clearly, the optimization problem (2.3) is convex with equality and inequality constraints. We denote the global minimizer in the -th iteration as . Inspired by Giesen and Laue (2019), who employed slack variables for inequality constraints in the standard ADMM, we construct the slack vector with for . To ensure , we define a loss function , where when and otherwise. By incorporating this loss function, , (2.3) transforms into the following equivalent optimization problem without inequality constraints:

| (2.4) | ||||

where

The constraint is imposed to separate the -norm of from the quadratic loss. Finally, we form the scaled Lagrangian problem as

where with , and are the Lagrangian multipliers with corresponding augmented parameters denoted as , and . The standard ADMM procedures can be expressed as

| (2.5) | ||||

where the subscript denotes the -th iteration in the standard ADMM algorithm.

Note that the first optimization in (2.5) is a quadratic form, and we can find the global minimizer by setting its derivative to zero. To update and , we apply the soft-thresholding operator to obtain the explicit forms:

where is the soft-thresholding operator applied to each element of , defined as . By some simple algebra, the updating formula for the slack vector is given by

| (2.6) |

In the above DC-ADMM algorithm, the parameters , and influence the convergence speed (Boyd et al., 2011; Wu et al., 2016). For practical implementation, we typically set . The complete DC-ADMM algorithm is summarized in Algorithm 1.

In the following theorem, we establish that the proposed DC-ADMM algorithm guarantees convergence to a local minimizer in finite steps.

Theorem 2.1.

In the DC-ADMM algorithm with -type distance, the sequence decreases with and converges in finite steps. Specifically, there exists an such that for all . Furthermore, is a KKT point of .

Although the ADMM algorithm typically ensures convergence to a global minimizer, the DC-ADMM guarantees only a KKT point due to the nonconvex nature of the CAR optimization problem. A variant DC algorithm proposed by Breiman and Cutler (1993) may achieve a global minimizer, but it is often criticized for its slow convergence speed. In Section 3, we also discuss the statistical properties of the local minimizer.

It is worth noting that the DC-ADMM can also be extended to handle -type distance by modifying the updating formula of in (2.5). However, the computational burden of DC-ADMM under -type distance can be prohibitive. Therefore, for efficiency, we propose an alternative approach using the Cyclic Coordinate Descent (CCD) algorithm to optimize under -type distance.

2.2.2 Cyclic Coordinate Decent Algorithm

In this section, we introduce the CCD algorithm tailored to optimize the problem (2.1) with -type distance. Without loss of generality, the superscript denotes the -th step estimator in the coordinate descent algorithm. For instance, and represent the -th step estimators of and , respectively. Given the estimation process, it is clear that . Consequently, we update and as follows:

| (2.7) | ||||

| (2.8) |

Clearly, the optimization problem in (2.8) is a standard LASSO problem, and many existing packages, such as the R package glmnet, can be used to solve it. Given , updating is equivalent to solve the following optimization problem:

| (2.9) |

Following procedures similar to the DC algorithm introduced in Section 2.2.1, it is straightforward to verify that both and are convex functions with respect to . Therefore, the corresponding optimization in (2.9), based on the lower approximation of , yields

| (2.10) | ||||

where is the sub-gradient of with respect to ,

Note that the objective function in (2.10) is quadratic with respect to , and the explicit form of can be derived by setting its first derivative equal to zero:

| (2.11) |

The updating formula for is defined as

| (2.12) |

This degenerates into the standard -means clustering procedure and can be implemented using existing R packages such as Ckmeans.1d.dp.

Once the main updating rules are determined, compute and update the main parameters at each iteration, repeating until the stopping criterion is met. The stopping criterion is defined such that either is sufficiently close to or the maximum number of iterations is reached. The summarized CCD algorithm for optimizing the problem with -type distance is outlined in Algorithm 2.

Note that if the -type distance in Algorithm 2 is replaced with the -type distance, the optimization problem in (2.12) becomes a standard -median algorithm, implementable using the R package Ckmeans.1d.dp. However, updating in (2.10) would lack an explicit form, necessitating complex algorithms such as ADMM to obtain iterative solutions. Moreover, it remains an open question whether the cyclic coordinate descent algorithm converges to a local minimizer for the non-convex optimization problem. Simulation results show no significant difference in performances between Algorithm 1 and Algorithm 2, despite the latter bearing greater computational burden. Hence, we recommend using Algorithm 2 for -type distance due to its computational efficiency, reserving DC-ADMM for solving (2.1) with -type distance.

2.3 Practical Implementation Details

We first investigate the method for selecting the number of subgroups and the shrinkage parameters and . To alleviate computational burdens, we use the Bayesian Information Criterion (BIC) to determine the group number . Specifically, let

where and . For better practical performance, we set . As tends to infinity, it results in for . Similarly, the sparsity of increases as grows. To minimize differences within each group, we initially set to a relatively large value and to a relatively small value to control the bias. Subsequently, we determine the optimal group number by minimizing the BIC. Similar strategies are also implemented in Ma and Huang (2017) and He et al. (2022c). With the estimated group number , we further adopt the generalized cross-validation (GCV) method by Tang et al. (2021), which is an approximate version of the method by Pan et al. (2013), to select and . Specifically, the GCV is defined as

where . Alternatively, one can simultaneously select the optimal , and by minimizing the BIC. However, this approach is computationally intensive due to the large size of the grid search.

Next, we focus on the selection of initial values (, ) in Algorithm 1. This step is more challenging because the algorithm may converge to a local minimizer due to the non-convexity of the objective function. Inspired by the ridge regression estimators used for initializing values by He et al. (2022c), we incorporate the primary factor structure and fit the following ridge regression to obtain :

| (2.13) |

where and . The tuning parameter is determined by cross-validation. Given , can be obtained using the -means (or -median) algorithm. The rationale behind using ridge regression is that the pseudo has a dimension of , which is larger than the sample size . We exclude from the regression for two reasons: firstly, due to the latent factor structure, the common factors are considered to contain the most crucial information; secondly, incorporating the idiosyncratic errors into ridge regression would introduce significant computational challenges due to its high dimensionality. Indeed, our simulation results indicate that the proposed strategy performs well and offers computational advantages.

3 Theoretical Properties

In this section, we investigate the statistical properties of our proposed estimators under mild conditions. First, we study the convergence rate of the “oracle” estimators, assuming prior knowledge of group memberships. Subsequently, we establish the asymptotic relationship between the oracle estimator and the local minimizer of the optimization problem (2.1).

Throughout the statement of the following theorems, we denote the true values of , and as , and , respectively, and define . Additionally, we use and to represent the minimum and maximum cardinalities of , respectively. Let be the matrix indicating the true group membership, where implies that subject belongs to group and otherwise. Hence, it is straightforward to verify that . In the ideal scenario where is known in advance, the oracle estimator can be defined as

| (3.1) |

Write . Note that the oracle estimator only incorporates prior grouping information , without prior knowledge of the sparsity of .

In the following, we first introduce some assumptions related to the estimation of factor models. These technical assumptions are commonly used in the literature on large-dimensional factor models, such as Fan et al. (2013), Fan et al. (2020) and Fan et al. (2023).

Assumption 1.

(Tail Probability) The sequence is strictly stationary with for all , and . Furthermore, we assume and satisfy exponential-type tail probability:

where . and are positive constants. Denote as . There exists two positive constants and such that , and .

Assumption 2.

(-Mixing Condition) Suppose and are -algebras generated by and respectively. We assume that there exists a constant such that and the following inequality holds:

where is a positive constant.

Assumption 3.

There exists some constant such that , and all the eigenvalues of are bounded away from and . Furthermore, .

Assumption 1 requires exponential-type tail probability for and , assuming they are uncorrelated. Moreover, is imposed to ensure consistent estimation of the number of factors. Assumption 2 relaxes the independence of to weak dependence. Combined with the exponential-type tail probability in Assumption 1, these conditions allow us to establish non-asymptotic bounds related to and . Assumption 3 is a standard condition for deriving the consistency of factor loadings and factor scores with a fixed , adapted from conditions in Bai (2003). Under these regular conditions, we derive the convergence rates of and , ensuring the efficiency of the plug-in estimations. In the following, we proceed to introduce some technical assumptions for subgroup identification.

Assumption 4.

Suppose has tail probability of sub-Gaussian form, that is, for any , where is a positive constant.

Assumption 5.

There exist two positive constants and such that

where stands for the support set of . Additionally, we assume the irrepresentable condition holds for , i.e., there exist a positive value such that . Moreover, we assume is bounded by some positive constant .

Assumption 4 requires that the random noise in (1.4) follows a sub-Gaussian distribution. By the definition of , we have . As , Assumption 5 implies a balanced group size: . The irrepresentable condition in Assumption 5, akin to that of Zhao and Yu (2006), ensures the sign consistency of . Moreover, the requirement that is bounded from above is equivalent to a weak correlation requirement of the idiosyncratic errors.

With these assumptions, we then present the theoretical properties of the oracle estimators in the following theorem.

Theorem 3.1.

Theorem 3.1 establishes the consistency and convergence rate of the oracle estimator when the number of subgroups is known in advance. The first term corresponds to the rate of penalized regression, similar to the LASSO estimator. The second term arises from the additional bias incurred due to the use of a plug-in estimate for the factor model. With further assumption, we can also obtain sign consistency, as stated in the following proposition.

Proposition 3.2.

Under the same conditions as in Theorem 3.1, and further assuming , where is a sufficiently large positive value, then achieves sign consistency:

Next, we establish the asymptotic relationship between the oracle estimator and the local minimizer of the optimization problem (2.1) in the following theorem.

Theorem 3.3.

Here is the refined text with some adjustments for clarity:

Theorem 3.3 asserts that the oracle estimator is a local minimizer of the optimization problem for the SILFS method with probability tending to 1. Combined with Theorem 3.1 and Proposition 3.2, we conclude that there exists a local minimizer which achieves both estimation and sign consistency. Therefore, it is crucial to identify such a (local) minimizer for the proposed SILFS method. Fortunately, the proposed DC-ADMM algorithm ensures finite-step convergence to a local minimizer. In other words, with high probability, we can obtain consistent estimators provided we start with a “good” initial value.

4 Simulation Study

In this section, we conduct thorough simulation experiments to assess the finite sample behaviors of the proposed SILFS method. In Section 4.1, we first compare the SILFS method with existing methods to evaluate empirical performance in terms of subgroup identification and variable selection. We also examine the computational time required for different methods. In Section 4.2, we investigate the sensitivity of the SILFS method to various levels of collinearity.

In the simulation studies, we use the eigenvalue-ratio method to determine the number of factors . To elaborate, we denote as the -th largest eigenvalue of , and the estimator of the factor number is determined by the modified ER method proposed by Chang et al. (2015):

where is a positive integer larger than , and is a constant that depends only on and . When itself is weakly correlated, one can directly set as 0.

4.1 Subgroup Identification and Variable Selection

In this section, we resort to Algorithm 1 to solve the optimization problem (2.1) with the -type distance. To emphasize the advantage of CAR, we construct FA-PFP for comparison. FA-PFP initially considers the FARM and then replaces CAR with in the optimization problem (2.1), where is the SCAD penalty. Tuning parameters involved in FA-PFP is selected with the same strategy as that of the SILFS. Additionally, we compare SILFS with the standard center-augmented regularization model (S-CAR), which ignores the factor structure, to assess the impact of factor structure on subgroup identification and variable selection. Furthermore, we include the oracle estimator with known factors as a comparative benchmark for all models.

We adopt a data generation process similar to that of Zhang et al. (2019) and Fan et al. (2020). Specifically, the model setting is defined as:

where and . We set are i.i.d. drawn from , and with for . For the factor model of , let are i.i.d. drawn from . Take the dependence of factor score into consideration, we employ a vector AR(1) model for : , where the noise are i.i.d. drawn from and . The idiosyncratic errors are i.i.d. generated from . As for group-specific parameters , the following two scenarios are considered.

Scenario A Set and , where .

Scenario B Set and , where .

In the simulation studies, we fix the number of factors as , set the sample size as , and vary the dimensionality across , , and . All simulation results in this paper are based on 100 replications. To evaluate the empirical performance of the estimators, we provide the following three criteria:

(i) Estimation error indices, used by both Zhang et al. (2019) and He et al. (2022c), involve the Root Mean Squared Error (RMSE). Specifically, the RMSE for and is denoted as and respectively. The is computed as , where represents the estimate of in the -th replication and is the number of replications. These indices evaluate the estimation accuracy, and a smaller implies better subgroup identification.

(ii) Variable selection indices include the mean of Sensitivity and Specificity over 100 replications. These metrics are common and crucial for assessing feature selections, as illustrated in Chen et al. (2021a).

(iii) Subgroup identification indices include the Rand index (RI), a quantity between 0 and 1. It is commonly used to measure the performance of subgroup recovery, as discussed in Rand (1971) and Zhang et al. (2019). A higher Rand index value indicates better clustering performance. Additionally, we calculate the mean value of the estimated clusters, denoted as . The frequency of overestimation/underestimation of the group number is presented in the form , where and represent the frequencies of overestimation and underestimation, respectively. These clustering-related indices are also adopted in Liu et al. (2023) to comprehensively evaluate clustering performance.

| Case | Method | Estimation Error Indices | Subgroup Identification Indices | Variable Selection Indices | ||||

| Freq | RI | Sensitivity | Specificity | |||||

| FA-PFP | 0.347 | 0.130 | 2.250(0.672) | 0.997(0.007) | 0.992(0.039) | 0.979(0.025) | ||

| SILFS | 0.128 | 0.109 | 2.100(0.302) | 0.985(0.045) | 1.000(0.000) | 0.986(0.023) | ||

| Oracle | 0.068 | 0.125 | NA | NA | NA | 0.996(0.040) | 0.996(0.009) | |

| S-CAR | 0.313 | 0.212 | 2.430(0.820) | 0.951(0.091) | 0.678(0.233) | 0.937(0.043) | ||

| FA-PFP | 0.363 | 0.094 | 2.210(0.498) | 0.997(0.006) | 0.990(0.044) | 0.978(0.019) | ||

| SILFS | 0.148 | 0.084 | 2.090(0.288) | 0.987(0.042) | 0.982(0.076) | 0.990(0.013) | ||

| Oracle | 0.067 | 0.084 | NA | NA | NA | 1.000(0.000) | 0.997(0.005) | |

| S-CAR | 0.343 | 0.158 | 2.590(0.954) | 0.932(0.104) | 0.626(0.285) | 0.950(0.028) | ||

| FA-PFP | 0.400 | 0.084 | 2.270(0.633) | 0.996(0.013) | 0.962(0.120) | 0.976(0.021) | ||

| SILFS | 0.241 | 0.097 | 2.320(0.618) | 0.960(0.076) | 0.907(0.215) | 0.999(0.003) | ||

| Oracle | 0.072 | 0.067 | NA | NA | NA | 1.000(0.000) | 0.997(0.004) | |

| S-CAR | 0.334 | 0.126 | 2.550(0.936) | 0.936(0.102) | 0.656(0.280) | 0.965(0.021) | ||

| FA-PFP | 0.558 | 0.157 | 2.160(0.507) | 0.948(0.116) | 0.942(0.042) | 0.998(0.005) | ||

| SILFS | 0.168 | 0.156 | 2.090(0.288) | 0.989(0.037) | 0.984(0.073) | 0.997(0.015) | ||

| Oracle | 0.081 | 0.120 | NA | NA | NA | 1.000(0.000) | 0.996(0.009) | |

| S-CAR | 0.334 | 0.203 | 2.520(0.904) | 0.942(0.097) | 0.702(0.270) | 0.937(0.043) | ||

| FA-PFP | 0.608 | 0.118 | 2.270(0.709) | 0.920(0.136) | 0.949(0.038) | 0.997(0.010) | ||

| SILFS | 0.137 | 0.105 | 2.070(0.326) | 0.991(0.041) | 0.980(0.115) | 0.999(0.003) | ||

| Oracle | 0.079 | 0.085 | NA | NA | NA | 1.000(0.000) | 0.996(0.007) | |

| S-CAR | 0.330 | 0.158 | 2.560(0.903) | 0.935(0.100) | 0.612(0.278) | 0.955(0.024) | ||

| FA-PFP | 0.560 | 0.098 | 2.170(0.551) | 0.936(0.124) | 0.957(0.025) | 0.998(0.005) | ||

| SILFS | 0.241 | 0.095 | 2.230(0.468) | 0.968(0.065) | 0.934(0.173) | 0.998(0.012) | ||

| Oracle | 0.073 | 0.071 | NA | NA | NA | 0.998(0.020) | 0.997(0.005) | |

| S-CAR | 0.341 | 0.128 | 2.580(0.934) | 0.935(0.098) | 0.618(0.296) | 0.968(0.018) | ||

| Case | Method | Estimation Error Indices | Subgroup Identification Indices | Variable Selection Indices | ||||

| Freq | RI | Sensitivity | Specificity | |||||

| FA-PFP | 0.689 | 0.218 | 4.140(1.181) | 0.932(0.048) | 0.778(0.244) | 0.914(0.058) | ||

| SILFS | 0.455 | 0.184 | 3.000(0.000) | 0.971(0.036) | 0.860(0.234) | 0.972(0.037) | ||

| Oracle | 0.080 | 0.113 | NA | NA | NA | 1.000(0.000) | 0.994(0.011) | |

| S-CAR | 0.733 | 0.244 | 3.100(0.560) | 0.917(0.079) | 0.550(0.252) | 0.894(0.060) | ||

| FA-PFP | 0.712 | 0.162 | 4.270(1.370) | 0.930(0.051) | 0.752(0.248) | 0.920(0.042) | ||

| SILFS | 0.526 | 0.146 | 3.000(0.000) | 0.961(0.042) | 0.770(0.285) | 0.978(0.025) | ||

| Oracle | 0.090 | 0.081 | NA | NA | NA | 1.000(0.000) | 0.995(0.007) | |

| S-CAR | 0.738 | 0.183 | 3.170(0.551) | 0.915(0.074) | 0.456(0.272) | 0.931(0.033) | ||

| FA-PFP | 0.742 | 0.142 | 4.130(1.292) | 0.925(0.053) | 0.674(0.275) | 0.926(0.042) | ||

| SILFS | 0.599 | 0.122 | 3.000(0.000) | 0.949(0.042) | 0.812(0.236) | 0.946(0.037) | ||

| Oracle | 0.076 | 0.063 | NA | NA | NA | 0.998(0.020) | 0.996(0.005) | |

| S-CAR | 0.720 | 0.152 | 3.070(0.432) | 0.923(0.060) | 0.428(0.248) | 0.942(0.027) | ||

| FA-PFP | 0.684 | 0.192 | 6.580(3.075) | 0.956(0.063) | 0.826(0.289) | 0.931(0.048) | ||

| SILFS | 0.254 | 0.130 | 3.000(0.141) | 0.997(0.014) | 0.976(0.104) | 0.986(0.044) | ||

| Oracle | 0.081 | 0.112 | NA | NA | NA | 1.000(0.000) | 0.995(0.011) | |

| S-CAR | 0.423 | 0.216 | 3.310(0.581) | 0.976(0.041) | 0.678(0.224) | 0.928(0.050) | ||

| FA-PFP | 0.644 | 0.136 | 6.520(2.761) | 0.966(0.044) | 0.864(0.225) | 0.938(0.033) | ||

| SILFS | 0.346 | 0.101 | 3.010(0.100) | 0.993(0.021) | 0.962(0.141) | 0.982(0.041) | ||

| Oracle | 0.090 | 0.078 | NA | NA | NA | 1.000(0.000) | 0.995(0.008) | |

| S-CAR | 0.480 | 0.164 | 3.310(0.506) | 0.972(0.045) | 0.592(0.224) | 0.952(0.034) | ||

| FA-PFP | 0.713 | 0.118 | 6.750(3.010) | 0.954(0.062) | 0.808(0.295) | 0.948(0.033) | ||

| SILFS | 0.423 | 0.088 | 3.000(0.000) | 0.991(0.024) | 0.934(0.184) | 0.976(0.048) | ||

| Oracle | 0.083 | 0.063 | NA | NA | NA | 0.998(0.020) | 0.996(0.005) | |

| S-CAR | 0.531 | 0.140 | 3.330(0.533) | 0.970(0.044) | 0.596(0.248) | 0.957(0.030) | ||

The simulation results for Scenario A and B are shown in Table 1 and 2 respectively. There are four main takeaways from Table 1 for Scenario A. Firstly, though the S-CAR method proficiently identifies the number of subgroups, its Rand index is relatively lower compared with the SILFS which incorporates the factor structure. Secondly, SILFS outperforms both the FA-PFP and S-CAR methods in terms of variable selection and estimation accuracy. It also demonstrates comparable performance to the oracle method, highlighting the importance of overcoming feature dependence. Moreover, despite both FA-PFP and SILFS incorporating factor structures, FA-PFP exhibits poor performance in terms of RMSE. This can be attributed to its tendency to generate isolated and small-sized subgroups, leading to an overestimation of . Lastly, as the group parameter increases, the performance of SILFS improves correspondingly with the increased distance between groups. Since the FA-PFP and SILFS is equipped with factor structures, the increase in dimensionality has no significant impact on the estimation errors. The results in Table 2 indicate that in the case of three groups, S-CAR performs worse in terms of subgroup identification and completely loses power for variable selection. FA-PFP also exhibits a significant decline in terms of variable selection. In contrast, SILFS remains stable and continues to perform closely well with the oracle estimator. Overall, SILFS performs satisfactorily in various cases.

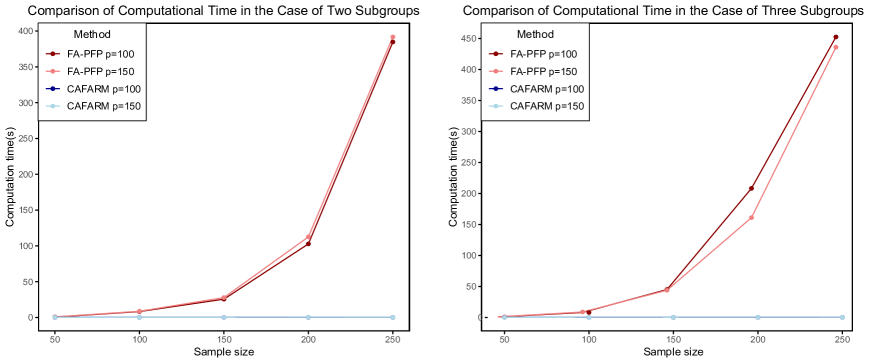

Next, we show the computing time of the SILFS and FA-PFP methods for Scenario A with and Scenario B with . For fair comparison, we use the same stopping criteria for SILFS and FA-PFP methods and only report the average time for 10 replications after selecting the optimal tuning parameters. The line charts of computing time are shown in Figure 2. As the sample size increases, the computing time for FA-PFP increases rapidly, with a quadratic curve trend. In contrast, the computational time required for SILFS increases steadily, almost linearly with respect to sample size.

In summary, based on the simulation results, we draw the following conclusions: (a) Existing methods in the literature show significantly reduced accuracy in variable selection and subgroup identification in the presence of covariate dependence. In contrast, the SILFS method performs well in both clustering and variable selection tasks. This is supported by high Rand Index and simplicity measures, as well as regression parameter estimators closely aligning with their true values; (b) Compared to the FA-PFP method, SILFS substantially reduces computational burdens, especially with large sample sizes and dimensions.

4.2 Sensitivity to the Level of Collinearity

In this section, we investigate the performance of SILFS in scenarios where the covariates exhibit high collinearity but do not have a factor structure. We also consider the uncorrelated case. Specifically, we generate the data as follows:

where with for and . For the generation of covariate matrices, we consider the following cases:

-

1.

Collinearity Case: We draw i.i.d. from , where . As for , we first generate a -dimensional random square matrix , where are i.i.d. from . Then, by QR decomposition, we have , where is an orthogonal matrix. Finally, we set . When , . In the simulation, we vary as 3, 4, and 5, respectively.

-

2.

Uncorrelated Case: We draw i.i.d. from .

| SILFS | S-CAR | |||||||||

| RI | Sensitivity | Specificity | RI | Sensitivity | Specificity | |||||

| Collinearity case with | ||||||||||

| 0.432 | 0.146 | 0.990(0.030) | 0.994(0.045) | 0.999(0.004) | 0.723 | 0.074 | 0.970(0.062) | 1.000(0.000) | 0.949(0.102) | |

| 0.530 | 0.104 | 0.985(0.033) | 0.996(0.028) | 0.998(0.007) | 0.605 | 0.055 | 0.979(0.055) | 0.998(0.020) | 0.984(0.042) | |

| 0.726 | 0.092 | 0.972(0.056) | 0.984(0.061) | 0.999(0.008) | 0.667 | 0.053 | 0.975(0.060) | 1.000(0.000) | 0.987(0.029) | |

| Collinearity case with | ||||||||||

| 0.396 | 0.145 | 0.992(0.024) | 0.998(0.020) | 0.999(0.007) | 0.770 | 0.144 | 0.972(0.054) | 0.994(0.034) | 0.963(0.031) | |

| 0.675 | 0.114 | 0.976(0.050) | 0.990(0.052) | 0.997(0.011) | 0.849 | 0.110 | 0.965(0.055) | 0.994(0.045) | 0.987(0.015) | |

| 0.796 | 0.097 | 0.965(0.055) | 0.990(0.044) | 0.996(0.009) | 0.997 | 0.103 | 0.951(0.069) | 0.982(0.064) | 0.994(0.012) | |

| Collinearity case with | ||||||||||

| 0.531 | 0.162 | 0.985(0.032) | 0.996(0.028) | 0.998(0.008) | 0.888 | 0.161 | 0.964(0.060) | 0.992(0.039) | 0.960(0.034) | |

| 0.707 | 0.115 | 0.973(0.045) | 0.994(0.034) | 0.996(0.010) | 1.011 | 0.120 | 0.950(0.079) | 0.984(0.061) | 0.985(0.017) | |

| 0.909 | 0.101 | 0.956(0.069) | 0.978(0.069) | 0.995(0.011) | 1.005 | 0.103 | 0.952(0.080) | 0.984(0.068) | 0.991(0.013) | |

| Uncorrelated case | ||||||||||

| 0.220 | 0.117 | 0.998(0.008) | 1.000(0.000) | 1.000(0.002) | 0.226 | 0.115 | 0.998(0.007) | 1.000(0.000) | 1.000(0.000) | |

| 0.551 | 0.097 | 0.984(0.044) | 0.992(0.049) | 0.999(0.006) | 0.471 | 0.093 | 0.988(0.033) | 0.998(0.020) | 0.998(0.008) | |

| 0.478 | 0.077 | 0.988(0.033) | 0.998(0.020) | 0.999(0.005) | 0.426 | 0.074 | 0.991(0.027) | 1.000(0.000) | 0.999(0.002) | |

We set the sample size as , while the dimensionality varies across 50, 100, and 150. All simulation results are based on 100 replications, and the evaluation metrics are consistent with those used in the last section. We present the simulation results in Table 3. In the collinearity case, the covariance matrix exhibits a spike structure. Therefore, although there is no factor structure, the proposed SILFS can still achieve better performance in terms of subgroup identification and variable selection simultaneously. Additionally, as Table 3 illustrates, for the cases where the covariates are uncorrelated, we find that the estimated is quite large such that we believe there is no factor structures and directly set . Therefore, the performance of SILFS is comparable with that of SCAR. This indicates that SILFS can be used as a safe replacement of the existing clustering methods, regardless of the level of collinearity among covariates.

5 A Real Data Example

In this section, we employ the proposed SILFS method to explore the relationship between China’s export value of commodities and exchange rates. The explanatory variables are sourced from the General Administration of Customs People’s Republic of China and are available for download from http://stats.customs.gov.cn/. The raw datasets comprises panel data involving 219 trading partner countries (regions) of China and 61 non-industrial commodities. We focus on the top 50 countries (regions) with the highest total trade volume in 2019, resulting in a covariate dimension of . The response variable is the Chinese exchange rates corresponding to these 50 countries (regions) in 2019. Our objective is to conduct subgroup analysis for this response variable while accounting for the effects of the covariates.

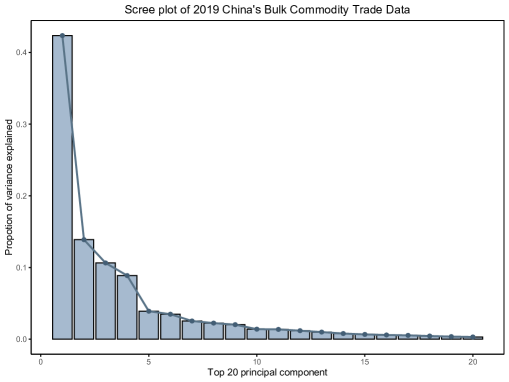

Given the possibility for high collinearity among covariates due to commodity substitutability, we first conduct PCA on the covariates. The scree plot of the top 20 principal components, depicted in the left panel of Figure 3, reveals that the first principal component explains 45% of the total variance, while the first five components collectively account for 80% of the variance. This underscores significant cross-sectional dependence among covariates, emphasizing the necessity of applying a factor model to mitigate the impact of collinearity.

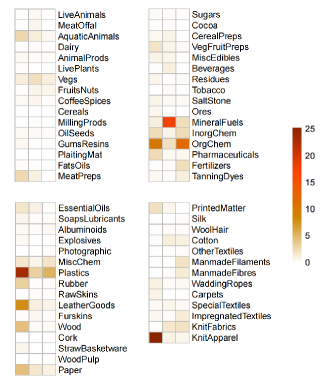

To begin with, we determine the number of factors as using the eigenvalue-ratio method. To aid in interpreting these factors, we employ varimax orthogonal rotation through the varimax function in R. The heatmap in the right panel of Figure 3 displays the absolute values of the factor loading matrix after orthogonal rotation, where darker colors indicate larger values. From Figure 3, we conclude that the first factor is associated with variables such as “Plastics,” “KnitApparel” (knitted or crocheted garments and clothing accessories), “OrgChem” (Organic Chemicals), and “Leather Goods”, representing categories related to textiles, apparel, and accessories. This aligns with China’s prominent role as an exporter of garments and textile products, as highlighted in studies such as Altenburg et al. (2020) and Hussain et al. (2020). The second factor primarily relates to “MineralFuels” (mineral fuels, mineral oils, products of their distillation; bituminous substances; mineral waxes), indicating its association with fuel and crude oil exports. In contrast, the third factor is influenced by variables such as “OrgChem,” “Plastics,” “ManmadeFilaments” (synthetic filament; flat strips and similar forms of synthetic textile materials), and “ManmadeFibres” (chemical fiber staple), suggesting a connection to light industry and manufacturing. Therefore, we deduce that China’s export structure is primarily driven by three latent factors, which we summarize as the “Textiles and Apparel Category”, “Oil and Fuel Category”, and “Light Industry Category”.

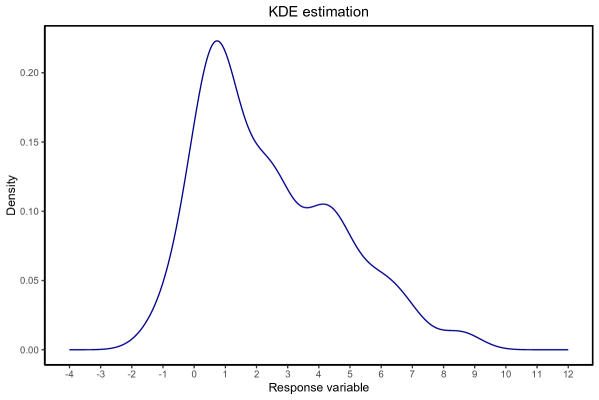

Next, we apply the FARM model proposed by Fan et al. (2020, 2023) to estimate . We further plot the kernel density estimate (KDE) of to assess its performance. According to Figure 4, it is evident that even after adjusting for the influence of covariates, the distribution still exhibits multiple modes. This heterogeneity may stem from unobserved latent factors, such as subgroups. Therefore, employing SILFS for subgroup analysis appears to be a more appropriate approach.

We present the results of subgroup identification in Table 4. Based on these findings, we cluster fifty countries (regions) into four groups. From the perspective of developmental status, the first two groups primarily comprise developed countries, including the United States, European countries, Australia and Singapore. Specifically, the first group exhibits greater concentration, while the second group displays variations in geographical location and industrial structure. The third group primarily consists of developing countries with significant growth potential. The last group mainly comprises countries with lower economic levels. Additionally, Hong Kong, China, and Taiwan, China, representing regions with smaller scales, are included in this group. From a geopolitical standpoint, the first group mainly comprises early-developed capitalist countries in Europe and America. The second group consists of countries from the Commonwealth. The third and fourth groups, which are less developed, are primarily situated in Asia and the Middle East.

| Cluster | Countries (Regions) |

| C1 | United States; Germany; United Kingdom; Netherlands; Italy; Spain; |

| France; Belgium; Poland; Panama; Greece. | |

| C2 | Australia; Canada; Singapore; New Zealand. |

| C3 | Japan; Malaysia; Brazil; United Arab Emirates; Pakistan; |

| Saudi Arabia; Israel; Peru. | |

| C4 | Hong Kong, China; Vietnam; South Korea; India; Indonesia; |

| Philippines; Thailand; Russia; Taiwan, China; Bangladesh; | |

| Mexico; Nigeria; Turkey; Myanmar; South Africa; Cambodia; | |

| Egypt; Chile; Iran; Kazakhstan; Colombia; Iraq; Kyrgyzstan; | |

| Sri Lanka; Algeria; North Korea; Argentina. |

6 Discussion

Subgroup identification is crucial for characterizing heterogeneity in datasets from various fields such as biology, economics and finance. However, existing methods often rely on the computationally intensive pairwise fusion penalty (PFP) for group pursuit (Ma and Huang, 2017; Zhang et al., 2019). Moreover, high collinearity among covariates can lead to poor performance. To address these challenges, we propose SILFS to conduct variable selection and subgroup detection simultaneously. Essentially, we adopt a factor structure to represent collinearity and use the FARM framework (Fan et al., 2021) in high dimensions for subgroup analysis. Furthermore, we introduce a novel Center-Augmented Regularization (CAR) method from He et al. (2022c) for clustering, significantly reducing computational complexity from to , where is the sample size and is the number of subgroups. We also investigate the corresponding algorithms and statistical properties of our proposed method. As a byproduct, an R package called SILFS, implementing the proposed method, is available on CRAN. Extensive simulations and real applications demonstrate the superiority of our proposed method.

Our study provides valuable insights into subgroup analysis in high-dimensional cases with collinearity among covariates. An important future research direction would be an in-depth exploration of the statistical properties of global minima and the theory of clustering consistency. Addressing these challenges will be essential for achieving a comprehensive understanding of the proposed approach. We leave this as future work.

Acknowledgements

This work was supported in part by the National Natural Science Foundation of China (grant numbers: 12171282 and 12101412) and Qilu Young Scholar program of Shandong University.

References

- Ahn and Horenstein (2013) Ahn, S.C., Horenstein, A.R., 2013. Eigenvalue ratio test for the number of factors. Econometrica 81, 1203–1227.

- Altenburg et al. (2020) Altenburg, T., Chen, X., Lütkenhorst, W., Staritz, C., Whitfield, L., 2020. Exporting out of China or out of Africa? Automation versus relocation in the global clothing industry. 1/2020, Discussion Paper.

- An and Tao (2005) An, L.T.H., Tao, P.D., 2005. The dc (difference of convex functions) programming and dca revisited with dc models of real world nonconvex optimization problems. Annals of operations research 133, 23–46.

- Ando and Tsay (2011) Ando, T., Tsay, R.S., 2011. Quantile regression models with factor-augmented predictors and information criterion. The Econometrics Journal 14, 1–24.

- Ashenfelter and Krueger (1994) Ashenfelter, O., Krueger, A., 1994. Estimates of the economic return to schooling from a new sample of twins. The American Economic Review 84, 1157–1173.

- Bai (2003) Bai, J., 2003. Inferential theory for factor models of large dimensions. Econometrica 71, 135–171.

- Bai and Ng (2002) Bai, J., Ng, S., 2002. Determining the number of factors in approximate factor models. Econometrica 70, 191–221.

- Banfield and Raftery (1993) Banfield, J.D., Raftery, A.E., 1993. Model-based gaussian and non-gaussian clustering. Biometrics , 803–821.

- Boyd et al. (2011) Boyd, S., Parikh, N., Chu, E., Peleato, B., Eckstein, J., et al., 2011. Distributed optimization and statistical learning via the alternating direction method of multipliers. Foundations and Trends® in Machine learning 3, 1–122.

- Breiman and Cutler (1993) Breiman, L., Cutler, A., 1993. A deterministic algorithm for global optimization. Mathematical Programming 58, 179–199.

- Chang et al. (2015) Chang, J., Guo, B., Yao, Q., 2015. High dimensional stochastic regression with latent factors, endogeneity and nonlinearity. Journal of Econometrics 189, 297–312.

- Chen et al. (2021a) Chen, H., Guo, Y., He, Y., Ji, J., Liu, L., Shi, Y., et al., 2021a. Simultaneous differential network analysis and classification for matrix-variate data with application to brain connectivity. Biostatistics 23, 967–989.

- Chen et al. (2021b) Chen, L., Dolado, J.J., Gonzalo, J., 2021b. Quantile factor models. Econometrica 89, 875–910.

- Chi and Lange (2015) Chi, E.C., Lange, K., 2015. Splitting methods for convex clustering. Journal of Computational and Graphical Statistics 24, 994–1013.

- Connolly and Gottschalk (2006) Connolly, H.C., Gottschalk, P., 2006. Differences in wage growth by education level: do less-educated workers gain less from work experience? .

- Fama and French (1992) Fama, E.F., French, K.R., 1992. The cross-section of expected stock returns. the Journal of Finance 47, 427–465.

- Fama and French (2015) Fama, E.F., French, K.R., 2015. A five-factor asset pricing model. Journal of financial economics 116, 1–22.

- Fan et al. (2021) Fan, J., Ke, Y., Liao, Y., 2021. Augmented factor models with applications to validating market risk factors and forecasting bond risk premia. Journal of Econometrics 222, 269–294.

- Fan et al. (2020) Fan, J., Ke, Y., Wang, K., 2020. Factor-adjusted regularized model selection. Journal of Econometrics 216, 71–85.

- Fan and Li (2001) Fan, J., Li, R., 2001. Variable selection via nonconcave penalized likelihood and its oracle properties. Journal of the American statistical Association 96, 1348–1360.

- Fan et al. (2013) Fan, J., Liao, Y., Mincheva, M., 2013. Large covariance estimation by thresholding principal orthogonal complements. Journal of the Royal Statistical Society Series B: Statistical Methodology 75, 603–680.

- Fan et al. (2023) Fan, J., Lou, Z., Yu, M., 2023. Are latent factor regression and sparse regression adequate? Journal of the American Statistical Association , 1–13.

- Gertheiss and Tutz (2012) Gertheiss, J., Tutz, G., 2012. Regularization and model selection with categorial effect modifiers. Statistica Sinica , 957–982.

- Giesen and Laue (2019) Giesen, J., Laue, S., 2019. Combining admm and the augmented lagrangian method for efficiently handling many constraints., in: IJCAI, pp. 4525–4531.

- Hastie and Tibshirani (1996) Hastie, T., Tibshirani, R., 1996. Discriminant analysis by gaussian mixtures. Journal of the Royal Statistical Society Series B: Statistical Methodology 58, 155–176.

- He et al. (2022a) He, R., Xue, H., Pan, W., Initiative, A.D.N., 2022a. Statistical power of transcriptome-wide association studies. Genetic epidemiology 46, 572–588.

- He et al. (2022b) He, Y., Kong, X., Yu, L., Zhang, X., 2022b. Large-dimensional factor analysis without moment constraints. Journal of Business & Economic Statistics 40, 302–312.

- He et al. (2023) He, Y., Li, L., Liu, D., Zhou, W.X., 2023. Huber principal component analysis for large-dimensional factor models. arXiv preprint arXiv:2303.02817 .

- He et al. (2022c) He, Y., Zhou, L., Xia, Y., Lin, H., 2022c. Center-augmented -type regularization for subgroup learning. Biometrics .

- Hocking et al. (2011) Hocking, T.D., Joulin, A., Bach, F., Vert, J.P., 2011. Clusterpath an algorithm for clustering using convex fusion penalties, in: 28th international conference on machine learning, p. 1.

- Hussain et al. (2020) Hussain, H.I., Haseeb, M., Kot, S., Jermsittiparsert, K., 2020. Non-linear impact of textile and clothing manufacturing on economic growth: The case of top-asian economies. Fibres & Textiles in Eastern Europe , 27–36.

- Johnstone and Paul (2018) Johnstone, I.M., Paul, D., 2018. Pca in high dimensions: An orientation. Proceedings of the IEEE 106, 1277–1292.

- Khalili and Chen (2007) Khalili, A., Chen, J., 2007. Variable selection in finite mixture of regression models. Journal of the american Statistical association 102, 1025–1038.

- Lam and Yao (2012) Lam, C., Yao, Q., 2012. Factor modeling for high-dimensional time series: inference for the number of factors. The Annals of Statistics , 694–726.

- Li et al. (2022) Li, S., Cai, T.T., Li, H., 2022. Transfer learning for high-dimensional linear regression: Prediction, estimation and minimax optimality. Journal of the Royal Statistical Society Series B: Statistical Methodology 84, 149–173.

- Liu et al. (2023) Liu, D., Zhao, C., He, Y., Liu, L., Guo, Y., Zhang, X., 2023. Simultaneous cluster structure learning and estimation of heterogeneous graphs for matrix-variate fmri data. Biometrics 79, 2246–2259.

- Livingston (1977) Livingston, M., 1977. Industry movements of common stocks. Journal of Finance 32, 861–874.

- Ma and Huang (2017) Ma, S., Huang, J., 2017. A concave pairwise fusion approach to subgroup analysis. Journal of the American Statistical Association 112, 410–423.

- McCracken and Ng (2016) McCracken, M.W., Ng, S., 2016. Fred-md: A monthly database for macroeconomic research. Journal of Business & Economic Statistics 34, 574–589.

- Merlevède et al. (2011) Merlevède, F., Peligrad, M., Rio, E., 2011. A bernstein type inequality and moderate deviations for weakly dependent sequences. Probability Theory and Related Fields 151, 435–474.

- Michele and Francesco (2018) Michele, R., Francesco, V., 2018. From the cradle to the grave: The influence of family background on the career path of italian men. Oxford Bulletin of Economics and Statistics 80, 1062–1088.

- Ollier and Viallon (2017) Ollier, E., Viallon, V., 2017. Regression modelling on stratified data with the lasso. Biometrika 104, 83–96.

- Pan et al. (2013) Pan, W., Shen, X., Liu, B., 2013. Cluster analysis: Unsupervised learning via supervised learning with a non-convex penalty. Journal of Machine Learning Research 14.

- Phillips and Sul (2007) Phillips, P.C., Sul, D., 2007. Transition modeling and econometric convergence tests. Econometrica 75, 1771–1855.

- Porcu et al. (2019) Porcu, E., Rüeger, S., Lepik, K., Santoni, F.A., Reymond, A., Kutalik, Z., 2019. Mendelian randomization integrating gwas and eqtl data reveals genetic determinants of complex and clinical traits. Nature communications 10, 3300.

- Rand (1971) Rand, W.M., 1971. Objective criteria for the evaluation of clustering methods. Journal of the American Statistical association 66, 846–850.

- Shen and Huang (2010) Shen, X., Huang, H.C., 2010. Grouping pursuit through a regularization solution surface. Journal of the American Statistical Association 105, 727–739.

- Song et al. (2014) Song, W., Yao, W., Xing, Y., 2014. Robust mixture regression model fitting by laplace distribution. Computational Statistics & Data Analysis 71, 128–137.

- Stock and Watson (2002) Stock, J.H., Watson, M.W., 2002. Forecasting using principal components from a large number of predictors. Journal of the American statistical association 97, 1167–1179.

- Tang et al. (2021) Tang, X., Xue, F., Qu, A., 2021. Individualized multidirectional variable selection. Journal of the American Statistical Association 116, 1280–1296.

- Tian et al. (2023) Tian, Y., Gu, Y., Feng, Y., 2023. Learning from similar linear representations: Adaptivity, minimaxity, and robustness. arXiv preprint arXiv:2303.17765 .

- Tibshirani (1996) Tibshirani, R., 1996. Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society Series B: Statistical Methodology 58, 267–288.

- Tu and Wang (2024) Tu, Y., Wang, S., 2024. Consistent model selection for factor-augmented regressions. manuscript .

- Vatcheva et al. (2016) Vatcheva, K.P., Lee, M., McCormick, J.B., Rahbar, M.H., 2016. Multicollinearity in regression analyses conducted in epidemiologic studies. Epidemiology (Sunnyvale, Calif.) 6.

- Wang et al. (2023) Wang, N., Zhang, X., Mai, Q., 2023. Statistical analysis for a penalized em algorithm in high-dimensional mixture linear regression model. arXiv preprint arXiv:2307.11405 .

- Wang et al. (2019) Wang, S., Wang, X., Zhao, Q., Yang, X., 2019. Quantile factor-augmented prediction model and its applications to alpha-arbitrage strategy in china’s stock market, in: 2019 International Conference on Big Data, Electronics and Communication Engineering (BDECE 2019), Atlantis Press. pp. 73–78.

- Wang and Su (2021) Wang, W., Su, L., 2021. Identifying latent group structures in nonlinear panels. Journal of Econometrics 220, 272–295.

- Wang and Zhu (2024) Wang, W., Zhu, Z., 2024. Homogeneity and sparsity analysis for high-dimensional panel data models. Journal of Business & Economic Statistics 42, 26–35.

- Wei and Kosorok (2013) Wei, S., Kosorok, M.R., 2013. Latent supervised learning. Journal of the American Statistical Association 108, 957–970.

- Wu et al. (2016) Wu, C., Kwon, S., Shen, X., Pan, W., 2016. A new algorithm and theory for penalized regression-based clustering. The Journal of Machine Learning Research 17, 6479–6503.

- Yao et al. (2014) Yao, W., Wei, Y., Yu, C., 2014. Robust mixture regression using the t-distribution. Computational Statistics & Data Analysis 71, 116–127.

- Zhang et al. (2020) Zhang, L., Ma, R., Cai, T.T., Li, H., 2020. Estimation, confidence intervals, and large-scale hypotheses testing for high-dimensional mixed linear regression. arXiv preprint arXiv:2011.03598 .

- Zhang et al. (2022) Zhang, X., Zhang, Q., Ma, S., Fang, K., 2022. Subgroup analysis for high-dimensional functional regression. Journal of Multivariate Analysis 192, 105100.

- Zhang et al. (2019) Zhang, Y., Wang, H.J., Zhu, Z., 2019. Robust subgroup identification. Statistica Sinica 29, 1873–1889.

- Zhao and Yu (2006) Zhao, P., Yu, B., 2006. On model selection consistency of lasso. The Journal of Machine Learning Research 7, 2541–2563.

- Zou (2006) Zou, H., 2006. The adaptive lasso and its oracle properties. Journal of the American statistical association 101, 1418–1429.

- Zou and Hastie (2005) Zou, H., Hastie, T., 2005. Regularization and variable selection via the elastic net. Journal of the Royal Statistical Society Series B: Statistical Methodology 67, 301–320.

APPENDIX

Appendix A Technical Lemmas

In this section, we introduce some useful technical lemmas. The asymptotic properties of factor model estimation are frequently used in the following proof process. Hence, we summarize some useful results from Fan et al. (2013) in the following lemma. Besides, we also deliver some lemmas related to the subgroup identification.

Lemma A.1.

The next lemma reveals the relationship of global optimum to the constrained optimum under some mild conditions.

Lemma A.2.

Fan et al. (2020) Suppose is a convex, twice continuously differentiable function defined over . Let be a convex and continuous penalty function satisfying the following properties:

-

1.

, for any and , where is a subspace of with orthogonal complement .

-

2.

There exists a continuous function , such that , for any and .

Let where and denote the constrained minimization as

| (A.1) |

If and for all , then the constrained minimization defined in (A.1) is the global minimizer of .

The following two lemmas provide the upper bound for invertible matrices.

Lemma A.3.

For two invertable matrices and , suppose where is an induced norm, we have

Lemma A.4.

Fan et al. (2020) Let be a real matrix, and let and are two symmetric matrices. Suppose is nonsingular and where is an induced norm, then

Lemma A.6.

Under the same assumptions as Lemma A.5, we have

The next lemma guarantees the separability of the oracle estimators.

Appendix B Proof of Main Theorems

B.1 Proof of Theorem 2.1

Proof.

Without loss of generality, we consider the -th iteration in the DC procedure. Recall that the optimization problem in the -th iteration under -type distance is:

| (B.1) | ||||

| subject to |

where

Since is a closed and proper convex function and the Lagragain function of (LABEL:Aopt:Upper) has saddle point by the saddle point theorem, then by the argument on convergence in the Boyd et al. (2011) and Giesen and Laue (2019), the standard ADMM converges to a global minimizer. By some primary calculations, the following equalities hold:

By the construction of , for each ,

| (B.2) |

implying that . Here the strict inequality always holds, otherwise the algorithm will be terminated when the equality is satisfied. By the monotone convergence theorem, we claim that converges as get larger.

Next, we illustrate the finite step convergence. Note that in each , determines the upper bound function only through sign function and indicator function. Thus has only a finite set of possible options across all integer . Therefore there exist a such that for any , . Note that is the global minimizer of and , thus we obtain that is a local minimizer of . ∎

B.2 Proof of Theorem 3.1 and Proposition 3.2

Proof.

Recall that the oracle estimator is defined as:

The proof proceeds in three steps. The first step is to show that the constrained optimization estimator converges to the oracle solution. In addition, the convergence rate is also provided. In the second step, we prove that the constrained optimal is equivalent to the global optimal solution. The third step proves the sign consistency of .

Step 1. In this step, we consider an optimization problem that limited to the subspace . We define

Note that this constrained optimization problem is equivalent to the following optimization problem,

| (B.3) |

The first order KKT conditions of problem (B.3) are

| (B.4) | ||||

where is the sub-gradient of . The above KKT condition implies . We consider the difference between the first order differential of the at and .

| (B.5) |

Denote

| (B.6) |

If is invertible, then left multiply both sides by matrix and take the infinite norm on both sides, we have

| (B.7) |

In the following, we need to illustrate the is invertible with probability tending to 1 and focus on the upper bounds for the two infinity norms on the right-hand side of the inequality (B.7).

To show is invertible, we set and . By Weyl theorem, we have . Thus, it is sufficient to show is . On the other hand, can be bounded by Lemma A.3

| (B.8) |

It is not hard to verify that is bounded under Assumption 5 and we assume it is smaller than . In conclusion, we should find the convergence rate of to show is invertible and then bound with infinite norm.

To analyze the gap between and , an “intermediary matrix” of them are introduced as:

By triangle inequality, we have

By the property of infinite norm, we have

| (B.9) |

Recalling the properties of the factor model estimators listed in Lemma A.1, we obtain that

Similarly, we also have

According to the result of Lemma A.6, it can be obtained that

Combining all these results and the decomposition in (B.9) , it’s obvious that

| (B.10) |

With similar arguments, we have

According to the concentration inequality in Merlevède et al. (2011), we have

which implies . Hence, we have

With similar arguments, we have

Further, by Lemma A.1,

Thus, we obtain that . Combining the upper bound of in equation (B.10), we obtain

| (B.11) |

It implies that holds with probability tending to 1. Combined with the assumptions in Theorem 3.1, we get . Thus, we obtain that is invertible with probability tending to 1. Plugging this results in the inequality (B.8) we have

| (B.12) |

holds with probability approaching to 1.

According to (B.7), in order to bound , we still need to find the upper bound of . Recall that , we have

Then, we can write as

| (B.13) |

We control the two parts of the right hand side of (B.13) separately. The first part is

| (B.14) |

Note that , the concentration inequality of sub-Gaussian random variable leads to . For , we have

Using the concentration inequality in Merlevède et al. (2011) again, we have

Thus, we know . By Cauchy-Schwarz inequality,

| (B.15) | ||||

With similar arguments of , one can obtain . Further, combining the convergence rate of factor models in the Lemma A.1, we obtain that

| (B.16) |

Recall the decomposition in (B.14), we have

| (B.17) |

Next, we bound the second part. According to the maximum inequality we have

| (B.18) |

Note that . Then we conclude

According to the Lemma A.1, the following inequality holds

Therefore,

Note that , we have

Recall that estimation of factor model produce We have

| (B.19) |

Therefore, combine the results for (B.13),(B.17) and (B.19), we get

| (B.20) |

WLOG, we let . Combining the inequality in (B.7) and the convergence rate in (B.12), we obtain

| (B.21) |

Step 2. In this step, we show that the constrained minima is the global minimum of (3.1). According to Lemma A.2, we only need to show . By Lagrange mean value theorem, we have

where is the sub-matrix of Hessian matrix of . By norm inequality we get

where is defined in (B.6) and . According to Lemma A.4,

Combining the norm inequality and the irrepresentable condition, we have

Hence, holds with probability approaching to 1. Combined with equation (B.5) and the definition of , we have

Thus, recall , we obtain

This implies is the unique global minima of the objective function, and

Thus Theorem 3.1 is proved.

Step 3. In this step, we proof the proposition 3.2. Note that

where

and

where the inequality holds element-wise. We consider the complement of and respectively.

where is the -th row of . Hence, it’s easy to show that . According to (B.12), . Thus, is bounded with high probability. There exists a constant such that

Similarly, we can prove has finite upper bound .

By concentration inequality of sub-Gaussian random variable, we obtain

where and are two positive values. Denote as the -th row of

Note that , where is a projection matrix. Hence, we obtain that for all . Further, we have

where and are two positive values. Therefore, the estimators has sign consistency, i.e. .

∎

B.3 Proof of Theorem 3.3

Proof.

Before starting the proof, we define a function to facilitate the subsequent proof process. For any vector , where , is a -dimensional vector, i.e.,

Specifically, the -th coordinate of is the common value of for . According to this definition of , represents the -dimensional vector obtained by restoring to the corresponding the true grouping structure.

With a slight abuse of notations, we define , the corresponding oracle estimator can be defined as and

| (B.22) |

We choose an open set of related to , denoted as

where is a real value sequence satisfying and hence we have .

In the neighborhood of , we show that is the local minima of with high probability in the following two steps. The first step is to prove that for any parameter belonging to satisfy . In the second step, we show that holds on . Hence, is the local minima of the objective function.

Step 1. In this step, wo focus on show that holds for any parameter .