11email: {nicolas.michel, menajd, ghada}@uconn.edu

: State Growth Control for AMMs

Abstract

Automated market makers (AMMs) are a form of decentralized cryptocurrency exchanges and considered a prime example of Decentralized Finance (DeFi) applications. Their popularity and high trading activity have resulted in millions of on-chain transactions leading to serious scalability issues. In this paper, we address the on-chain storage overhead problem of AMMs by utilizing a new sidechain architecture as a layer 2 solution, building a system called . Our system reduces the amount of on-chain transactions, boosts throughput, and supports blockchain pruning. We devise several techniques to enable layer 2 processing for AMMs while preserving correctness and security of the underlying AMM. We also build a proof-of-concept of for a Uniswap-inspired use case to empirically evaluate its performance. Our experiments show that decreases the gas cost by 94.53% and the chain growth by at least 80%, and that it can support up to 500x of the daily traffic volume observed for Uniswap in practice.

1 Introduction

Cryptocurrencies and blockchain technology provide an innovative model that led to new applications and research frontiers, as well as reshaping the Internet and its digital services. Decentralized Finance (DeFi) is one of these applications in which blockchains are used to transform traditional financial services, that are usually centrally-managed, into fully decentralized ones. Many of these systems operate in open-access settings, thus removing market entrance barriers for customers, and enabling a transparent and intermediary-free interaction. Smart contracts strengthen this model by providing an automated way to negotiate contract terms and enforce agreements.

Automated market makers (AMMs) are considered a prime example of DeFi services [64]. They build a platform for automated token trading by establishing liquidity pools for trading token pairs. An AMM is usually implemented as a dApp; a set of smart contracts on top of a smart contract-enabled blockchain, where Ethereum is the dominant choice so far. AMMs in general include operations for trading, called swaps, and other for managing liquidity and fee collection including mints, burns, and collects. Many popular AMMs are deployed in practice and widely used. Examples include Uniswap [26], Curve [6], DODO [7], and Sushiswap [21], which during the first half of 2023 commanded around 62-71%, 6.38-14.01%, 4.04-7.16%, and 0.69-3.67% of the top ten AMMs market share, respectively [1]. During the same period, the AMM industry has a total monthly trading volume of $46 - $95 billion, and an estimated total market cap of nearly $16 billion as of January 2024 [23].

Challenges. The popularity and high trading activity of AMMs led to efficiency problems. AMMs produce a massive number of on-chain transactions. On the one hand, this increases the underlying blockchain size or storage overhead, and on the second hand, it incurs large (gas) fees. This large workload does not only amplify storage cost, but also transaction processing/confirmation delays due to the low throughput of blockchains (Ethereum’s throughput is around 12 transaction/sec on average [9]).

Concretely, and based on the traffic analysis that we conducted for 2023 (see Appendix 0.C), users of Uniswap V3 produced 20 million transactions on Ethereum in 2023 (the size of these transactions range from bytes to bytes). This translates to adding around GB to the Ethereum blockchain. In its year of deployment (Nov 2018), Uniswap V1 generated 34,000 transactions, and in 2023, Uniswap’s various versions on Ethereum generated around 80 million transactions, leading to 231,7% increase in transaction volume. These numbers indicate that the scalability problem of AMMs is amplified over the years.

Limitations of prior work. Improving blockchain scalability is an active research area. Many solutions have been proposed; some of them target layer 1 improving on the consensus itself, such as sharding [41, 66, 51], while others target layer 2 allowing for some form of off-chain processing while logging only state changes on the blockchain, such as payment channels and networks [42] and rollups [15, 30]. However, when it comes to AMMs, applying these solutions impact performance and security, and may not even reduce the storage cost. In sharding, localized workload division policies are used to reduce cross-shard transactions. For smart contract-enabled blockchains, this means that a dApp will be contained in one shard [32, 61], so the whole AMM will be on one shard. Thus, parallel processing among shards is not utilized. Others [57] attempt to shard the AMM by distributing liquidity pools among several shards, but still reliance on locked cross-shard transactions may degrade the AMM performance. Furthermore, in all sharding solutions all transactions are logged on-chain, so they do not cut the storage cost.

Layer 2 solutions that allow computations, i.e., beyond just payment transfer as in payment networks [42], have limitations. Optimistic rollups have long contestation periods that may reach one week as in Optimism and Arbitrum [15, 48]. Moreover, they have security issues—verifiers could be centralized trusted entities [60], while incentive compatibility of non-trusted verifiers is still an open question [53, 4, 16] which may lead to adopting incorrect ledger state changes (as they are not incentivized to verify the submitted changes). Zero knowledge (ZK)-rollups [20, 38, 37] are costly; proof generation may take several minutes and it becomes worse when attesting to complex transactions. They also may have long transaction confirmation delay that may reach 24 hours as in zkSync Era [30]. Not to mention that many of these systems require a trusted setup.

Sidechains [35, 45, 46, 49] are another instance of layer 2 solutions that can improve scalability. Despite their potential, existing efforts mostly focus on two-way peg, i.e., currency transfer between the sidechain and the mainchain, and all of them considered independent sidechains. That is, each chain has its own transactions, miners, and tokens. Such Independence and the focus on two-way peg limit the performance gains that can be achieved, and do not allow for workload sharing between the chains. Moreover, none of these solutions allow pruning stale records.111Polygon [17] operates a fast (block time is around 2 sec) EVM-compatible sidechain. The whole AMM is run on this sidechain and tokens can be transferred to Ethereum, if desired, using bridges or atomic swap techniques. While polygon can benefit from a decrease in latency, by virtue of running a fast blockchain, it suffers from the same problems outlined above. Lastly, isolating an AMM on an independent sidechain impacts composability with other dApps running on Ethereum.

A new approach. Sidechains seem to have potential in building an effective layer 2 solution to promote scalability. This has been observed in [54], who proposed a framework called chainBoost with a new sidechain architecture that permits workload sharing and arbitrary data exchange between the side and main chains, as well as blockchain pruning. chainBoost targets resource markers—Web 3.0 systems that offer decentralized digital services on top of the currency exchange medium, e.g., Filecoin [10] and Livepeer [14]. chainBoost directs all heavy/frequent service-related traffic to the sidechain, which in turn processes this traffic and produces concise summaries of the state changes that are used to sync the mainchain. Once these summaries are confirmed on the mainchain, the temporary blocks containing the actual traffic on the sidechain will be pruned. The empirical results in [54] show substantial performance gains in terms of blockchain size, transaction confirmation delays, and throughput. All of these are achieved without compromising security and while keeping the mainchain as the single truth of the system state.

These advantages motivated us to explore the following: Can we apply the chainBoost framework to AMMs and achieve similar performance gains and security guarantees?

Contributions. In this paper, we answer this question in the affirmative and propose ; a storage control and throughput boosting solution for AMMs. introduces a novel approach for dividing the AMM functionality into two modules: one that resides on the mainchain (i.e., the underlying smart contract-enabled blockchain) and another that is operated by the sidechain. In particular, offloads processing most transactions (including swaps, mints, collects, and burns) to the sidechain, and minimizes the functionality remaining on the mainchain. The latter is encapsulated in a base smart contract called , that manages the actual tokens that are being traded by tracking only the transaction summaries produced by the sidechain. It also includes all operations that must happen in real time, and so must be handled by the mainchain, such as flash loans.

solves several challenges related to applying sidechains to AMMs. The chainBoost framework assumes a mutual-dependency relation between the mainchain and the sidechain. That is, both chains operate in the same domain and have the same transaction format, services, and miner population. This is not the case for . The AMM is merely a dApp deployed at the application layer, so it does not modify how the mainchain protocol works. Also, the mainchain miners do not maintain the sidechain as in chainBoost, even they might not be aware of its existence. However, ’s sidechain is impacted by the mainchain since the tokens and the AMM state (and some core functionalities) are on the mainchain. Thus, introduces a unidirectional dependency relation: the sidechain is impacted by the mainchain but not vice versa. Furthermore, the sidechain is supposed to process all trading activities while the actual tokens reside on the mainchain.

We resolve these challenges by introducing several techniques. First, we require the AMM to have its own miners to maintain the sidechain. So, like any blockchain, these miners are assumed to have a mining power with honest majority, they need to build a Sybil-resistant identity by, e.g., using a proof-of-stake approach, and they will be rewarded for maintaining the sidechain using, e.g., the AMM native token. Second, we introduce epoch-based deposits, where a user has to deposit on the mainchain the anticipated amount of tokens needed to back up her activities (or issued transactions) during an epoch on the sidechain. Third, we introduce pool snapshot-based and delayed token-payout trading. That is, the pool token balances are retrieved from the mainchain at the beginning of the epoch, which are used to compute swap prices processed on the sidechain. These balances evolve during the epoch based on transactions processed during that epoch. Users, however, do not get their actual tokens resulting from the processed transactions immediately. They have to wait until the end of the epoch once the that resides on the mainchain is synced. At that point, the mainchain AMM state is updated, tokens are paid out to users, and any leftover in the epoch deposits is refunded to their owners.

We analyze the security of showing that it preserves the correct and secure operation of the underlying AMM. We also build a proof-of-concept implementation for a Uniswap-inspired use case, and conduct experiments to empirically evaluate the performance gains, in terms of blockchain size, confirmation delay, and throughput, that can achieve. Our experiments show that achieves a 94.53% gas cost reduction and 80.25% chain growth reduction (when compared to a Uniswap version deployed on Sepolia). Furthermore, they show that can support large traffic volume, on the order of up to 500x of Uniswap’s daily transaction volume.

Although the focus of this work is on controlling the storage overhead of AMMs and boosting their throughput, we believe that may have far reaching impact. Its paradigm can enable more optimizations for AMMs, e.g., integration of privacy-preserving techniques via the sidechain. Also, could be beneficial for other DeFi applications, and dApps in general, as it introduces a framework for operating application-specific sidechains interacting with smart contract-enabled blockchains.

2 Background

In this section, we provide an overview of the general functionality of AMMs and the chainBoost framework that we use in the design of .

Automated market makers. AMMs build platforms for token trading powered by the users themselves. This is done by establishing liquidity pools such that a pool trades a pair of tokens, say tokens and , against each others. Users are divided into: clients which could be sellers and buyers, and liquidity providers (LPs). Providing liquidity comes from the sellers themselves since buying token requires paying the price using token (and vice versa), and from LPs who deposit tokens in the pool and obtain fees or rewards in return.

Constant function market makers (CFMM) is a popular implementation choice for computing the trading price in AMMs. This formula keeps the ratio of token reserves, and consequently prices, in the pool as balanced as possible to reduce price slippage. In particular, the price of token multiplied by the price of token equals a constant. Let the reserves of tokens and , i.e., their total amounts, in the pool be and , respectively, then the price of token is and the price of token is . Accordingly, for an order trading an amount of token , , the amount of token , , that this order receives is computed as: .

At a basic level, an AMM implementation supports several transaction types. Among them there are exact output and input swaps, which allow users to specify the exact method to process their trades. For liquidity management, mints, burns and collects allow LPs to submit liquidity positions, collect their fees, and edit or even withdraw these positions, respectively. AMMs may provide additional services, such as flash loans [63] allowing clients to take advantage of arbitrage opportunities across different platforms. Furthermore, more sophisticated liquidity approaches are being adopted, e.g., concentrated liquidity [43]. It allows LPs to define the price range on which they desire their liquidity to be applied. The goal is to solve the inefficient use of provided funds in the older schemes that evenly distribute the provided liquidity across the pool’s price curve.

The functionality of an AMM is commonly implemented as a set of smart contracts on top of a smart contract-enabled blockchain, where Ethereum is the dominant choice so far. These contracts create and manage the liquidity pools, and provide the API needed to interact with the AMM. Residing on a public blockchain led to several financial and security issues [36, 55, 58], e.g., front-running attacks, sandwich attacks, miner/maximal extractable value, etc. Understanding and solving these issues are active research areas. We do not discuss these issues further since they are not the focus of this work; we target the on-chain storage cost and throughput of AMMs.

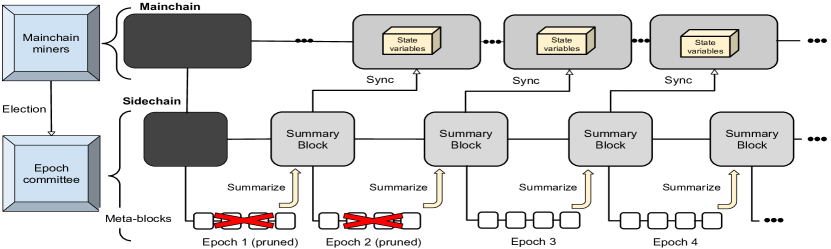

The chainBoost framework. chainBoost [54] is a sidechain-based solution that aims to reduce the blockchain storage footprint and confirmation delays, and boost transaction throughput. It introduces a new sidechain architecture that shares the workload with the mainchain, and enables pruning stale records. As such, this sidechain has a mutual-dependence relation with the mainchain. Transactions are classified into sidechain and mainchain transactions, where all service-related operations that can be summarized go to the sidechain, while the rest stay on the mainchain. The sidechain works in parallel to the mainchain, and operates in epochs and rounds (an epoch is consecutive rounds and a round is the period during which a new block is mined). At the end of each epoch, the mainchain is synced with summaries of the workload processed by the sidechain in that epoch.

As shown in Figure 1, the sidechain is managed by the mainchain miners, where for each epoch, a committee is elected to process the sidechain traffic during that epoch. The rest of the mainchain miners, who are not on the committee, do not process the sidechain traffic, thus reducing their load. To speedup agreement, chainBoost employs a practical Byzantine fault tolerance (PBFT)-based consensus (similar to those in [50, 47]) for the sidechain.222Similar to chainBoost, to simplify the presentation, we adopt a leader-based PBFT in which a leader proposes a block for the committee to agree on (as in [50]. Nonetheless, voting-based PBFT (as in [47]) in which a set of proposers can propose blocks and voters will choose one of them can be used instead.

As shown in Figure 1, the sidechain is composed of two types of blocks: temporary meta-blocks and permanent summary-blocks. For each sidechain round, the committee mines a meta-block containing the transactions they processed, so that once a transaction appears in a meta-block it is considered final. In the last round of the epoch, this committee mines a summary-block summarizing all state changes induced by the meta-blocks within that epoch. After that, it issues a sync-transaction containing the summarized state changes, which the mainchain miners use to update the relevant state variables on the mainchain. Once the sync-transaction is confirmed on the mainchain, all meta-blocks used to produce the respective summary-block are discarded. This significantly reduces the sidechain size, and subsequently, the mainchain size. At the same time, having permanent summary-blocks allows anyone can verify the source of the state changes recorded on the mainchain.

Applicability of chainBoost to our setting. Our setting is different from the one in [54]: First, the mainchain and sidechain miners are different. In , the mainchain miners belong to a smart contract-enabled blockchain, and the AMM is simply an application deployed on that blockchain. Thus, the sidechain must have its own miner population from which the committee is elected, and a technique, such as proof-of-stake, to mitigate Sybil attacks. Second, in chainBoost the two chains are mutually-dependent, i.e., their security and valid operation depend on each other. In , the dependence is unidirectional; interruptions on the mainchain impact the sidechain since the base contract that keeps track of the AMM state resides on the mainchain, but not vice versa. Sidechain interruptions will indeed lead to invalid state of the base AMM contract, but this contract resides on the application layer and does not impact the underlying mainchain or other deployed dApps. Third, in , the actual token pools reside on the mainchain, while the trading and liquidity-related activities are handled by the sidechain. Thus, a mechanism is needed to handle token payouts and deposits to enable accepting and processing only valid transactions. We address these issues in our system design in Section 4.

3 Preliminaries

Notation. We use to denote the security parameter, and to denote the system public parameters. We use to denote a ledger (or blockchain), to denote the mainchain ledger, and to denote the sidechain ledger. The former is the smart contract-enabled blockchain on top of which the AMM base smart contract is deployed, while the latter is the blockchain of the AMM ecosystem. Each party maintains a secret key and a public key . Lastly, we use as a shorthand for probabilistic polynomial time.

System model. involves a base smart contract representing the AMM on the mainchain, and a sidechain that processes most of the AMM workload. Anyone can join/leave the AMM at anytime, and these parties are known using their public keys. Participants are three types: clients who are only interested in using the AMM trading services, liquidity providers who provide liquidity for the pools operated by the AMM, and miners who maintain the AMM sidechain. We do not place any restrictions on the mainchain beyond being a secure smart contract-enabled blockchain. operates in rounds and epochs (as defined earlier). The sidechain is managed by a committee elected from the sidechain miners, where a new committee is elected for each epoch. This committee runs a PBFT-based consensus to mine new blocks. These blocks are as in the chainBoost framework: temporary meta-blocks that record transactions, and permanent summary-blocks that summarize meta-blocks mined in an epoch. The committee also issues sync-transactions to sync the base AMM smart contract deployed on the mainchain.

Accordingly, the framework provides the following functionalities:

- :

-

Takes as input the the security parameter and the mainchain . It configures the system public parameters , and deploys a base AMM smart contract on . It outputs and the initial sidechain ledger state (which is the genesis block referencing the mainchain block containing the base contract).

- :

-

Takes as input and outputs the initial local state of the party , which contains a keypair , and in case of miners, the current view of .

- :

-

Takes as input transaction type and any additional information/inputs , and outputs a transaction of one of the following types:

-

•

: Allows a user (client or LP) to deposit funds on the mainchain to support her activities on the sidechain.

-

•

: Allows a client to submit a trade.

-

•

: Allows an LP to provide liquidity to a particular pool.

-

•

: Allows an LP to collect fees accrued due to providing liquidity.

-

•

: Allows an LP to withdraw her liquidity position.

-

•

: Allows a sidechain committee to sync the AMM base contract on the mainchain.

-

•

- :

-

Takes as input a transaction , and outputs 1 if is valid based on the syntax/semantics of its type, and 0 otherwise.

- :

-

Takes as input the current sidechain ledger state , a new block with type or . It outputs 1 if is valid based on the syntax/semantics of the particular block type, and 0 otherwise.

- :

-

Takes as input the current sidechain state , and a set of pending transactions (if ) or (if since the inputs are the last epoch meta-blocks from ). It reflects the changes induced by and outputs a new ledger state .

- :

-

Takes as input the current state of the sidechain ledger , and outputs an epoch committee and its leader .

- :

-

Takes as input the current sidechain ledger state , and produces an updated state in which all stale meta-blocks are dropped.

Note that is the process of mining a new block on the sidechain. Agreement on this block is governed by the sidehchain consensus protocol.

Security model. We aim to develop a secure state growth control solution that preserves the valid and secure operation of the underlying AMM. builds a sidechain, which is basically a blockchain, that interacts with the application layer of the mainchain through the base AMM smart contract. This sidechain must be a secure ledger as defined below.

Ledger security. A ledger is secure if it satisfies the following properties [44]:

- Safety:

-

For any two time rounds and such that , and any two honest parties and , the confirmed state of (which includes all blocks buried under at least blocks, where is the depth parameter) maintained by at is a prefix of the confirmed state of maintained by party at time with overwhelming probability.

- Liveness:

-

If a valid transaction is broadcast at time round , then with overwhelming probability it will be recorded on at time at most , where is the liveness parameter.

A ledger must record only valid transactions and blocks, thus its protocol is parameterized by predicates to verify transaction and block validity. For dApps, validity is governed by the code of their smart contracts, and miners ensure that the ledger state changes have been produced by a successful execution of this code. reduces the AMM functionality deployed on the mainchain, and it processes most of the workload (following the same logic of the AMM) on the sidechain. Thus, in our security analysis, we show that preserves the security and correct operation (i.e., safety and liveness) of the original AMM.

Adversary model. Our model is very similar to the one in [54]. In particular, we assume the mainchain to be secure as defined above. For the sidechain, we have honest miners who follow the protocol, and malicious miners controlled by the adversary who may behave arbitrarily. The adversary can deploy new miners or corrupt existing ones, without going above the threshold of faulty nodes required by the sidechain consensus protocol. The adversary can see all messages and transactions sent in the system (since we deal with public open-access blockchain systems) and can reorder these messages and delay them. We assume bounded-delay message delivery, so any sent message (or transaction) will be delivered within time as in [47, 56, 51]. We assume slowly-adaptive adversaries [33] that can corrupt miners only at the beginning of each epoch. Lastly, we deal with adversaries.

4 System Design

changes the AMM deployment structure, as shown in Figure 2. The smart contract on the mainchain will become minimal; it mainly tracks the token balances of the liquidity pools and the users, while most of the transaction processing is moved to the sidechain. Summaries of the sidechain processed traffic are used to sync the AMM smart contract on the mainchain. Also, the AMM now has its own miners to maintain the sidechain. In this section, we present the design of including system setup, architecture and operation, handling interruptions, and its security.

4.1 System Setup

The setup phase, as depicted in Figure 3, mainly specifies the traffic split between the chains and the summary rules for the sidechain traffic. Also, this phase involves deploying the AMM base smart contract on the mainchain and creating the sidechain.

Traffic classification and summary rules. AMM transactions and operations are divided into two groups: pool management and trading-related operations. Creating and managing token pools, as well as dispensing tokens to clients and LPs, are done on the mainchain (using the contract as we explain shortly). Flashes are also processed on the mainchain since they require instant token dispensing rather than at the end of the epoch (which is the case for any operation done on the sidechain). The rest of the transactions, including swaps, mints, burns, and collects, are handled by the sidechain.

In , the sidechain does not store any real tokens, it just tracks their balances and update them based on the transactions this sidechain processes. That is, during each epoch, two structures are produced:

-

•

A payout list containing users’ public keys and the amount/type of tokens they should receive. These result from swaps, withdrawal of liquidity positions, and fee collection.

-

•

A payin list containing also the users’ public keys and the amount/type of tokens that should be deducted from their mainchain deposits for their sidechain activities. These result from swaps and mints.

: Takes as input the security parameter and the current state of the mainchain , and does the following:

1. Generate the sidechain configuration parameters:

-

•

The epoch length .

-

•

All parameters needed for the sidechain consensus protocol.

-

•

Traffic classification rules.

-

•

Summary rules and state variables.

2. Deploy the AMM base smart contract on the mainchain.

Outputs: epoch length , sidechain genesis block (that references the block in the updated state containing ), and the address of .

The actual token dispensing and deduction happens at the end of an epoch when the sidechain summaries are received. The new state of the pool token balances on the mainchain will be computed based on these lists. Also, tokens will be sent to users (i.e., payouts) or added to the pool from the users’ deposits (i.e., payins). In Section 4.2, we show the summary rules for each transaction type and how they contribute to the payout and payin lists.

// ** State variables **

: token-pair pools managed by the AMM.

: a map of users’ public keys and the type/amount of tokens they deposited.

: a map of users’ public keys and the liquidity positions they own.

// ** Functions **

: initializes a pool for the token pair (, ).

: allows a user to deposit an amount of token with type to back up her activities for the next epoch.

: Sync the on-chain AMM state based on the sidechain epoch summaries. The input contains the updated balances of the pools, updated liquidity positions, and the payin/payout lists.

: Receive a flash loan request where contains all required inputs, then calculate the token amount the pool can provide and initiate the callback process (more details can be found in Section 4.2).

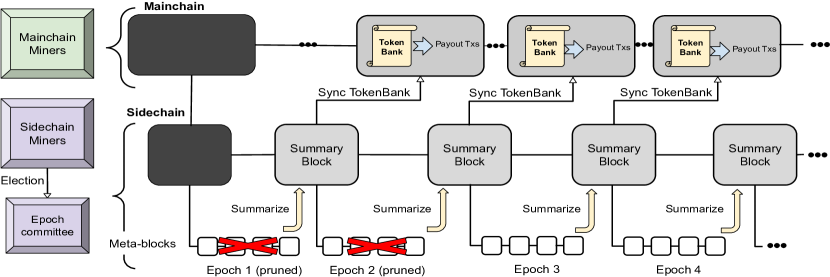

Base smart contract . The mainchain part of the AMM is a base smart contract called . At an abstract level, and as shown in Figure 4, this contract supports creating and managing token pools (the latter involves tracking the token balances in these pools and their liquidity positions). It also provides the minimal interface needed to support users’ activities on the sidechain, which is mainly creating deposits on the mainchain of the tokens they want to trade or provide as liquidity. This is needed since the sidechain does not receive or send actual tokens, but rather it tracks their state evolution. Hence, a user deposits the total amount of tokens, in the account, that is needed to support their activities during an epoch before this epoch starts. This also means that handles payouts and payins that the sidechain produces at the end of any epoch.

As shown in Figure 3, system designers create and deploy the contract on the mainchain. Once the mainchain block containing this contract is confirmed, the genesis block of the sidechain can be created such that it references this mainchain block.

Sidechain management. The sidechain in is managed in a similar way as in chainBoost. At the beginning of each epoch, a committee from the sidechain miners is elected, which runs a PBFT consensus protocol to agree on mining meta/summary blocks and issuing sync-transactions. That is, the committee leader proposes new blocks or sync-transactions, and collect votes from the committee members. Once a vote majority is reached, the new block is added to the sidechain or the sync-transaction is sent to the mainchain. In , a sync-transaction is basically a call to the function in shown in Figure 4.

differs from chainBoost in the aspect that the sidechain has its own miner population. In other words, mainchain miners are not responsible of managing the sidechain, and even may not know that a sidechain exists in the first place. Executing the contract is like executing any other contract deployed at the application layer of the mainchain. As such, sidechain miners must posses some mining power to establish Sybil resistant identities to be used in the committee election process. Any secure PBFT protocol in which election is based on the mining power can be used here, e.g., the proof-of-stake based protocol in [47].

4.2 System Operation

As mentioned before, operates in epochs and rounds. The sidechain committee begins the epoch by retrieving the latest state, i.e., pool token balances, liquidity positions, and the deposit balances of users (both clients and LPs) from the mainchain. It then processes all valid sidechain transactions, including swap, mint, burn, and collect. These are packaged into meta-blocks such that a meta-block is mined in each round. In the last round of the epoch, this committee produces a summary-block capturing the payouts and payins for participating users, any changes on liquidity positions’ ownership and amounts, and the updated liquidity pool balance. After that, it invokes the function in that resembles submitting a sync-transaction to update the AMM state on the mainchain, which is basically the state of the contract.

In what follows, we describe how the various transactions are processed and summarized (Figure 5 captures how the sidechain workload is summarized in ).

Swaps. A swap transaction is a trade between the two tokens managed by a liquidity pool. A client provides an input of tokens and receives an output of the other token type with an amount based on the price derived from the pool token balances and any user-defined trade conditions.

Input: meta-blocks from an epoch.

Initialize empty summary structures , , and

for and every do

if then

Update fees in for all positions used to fill

// Liquidity amounts are computed as explained under mints and burns.

elseif then

elseif then

elseif then

Output , , and

In order to execute a swap transaction, a user must have already deposited their input tokens in the contract. Then, they can broadcast their swap transaction to the sidechain. An exact input swap transaction contains the following arguments: type and amount of input tokens to be traded, the minimum amount of output tokens the trade will accept (as a protection against slippage), a price limit that the trade should not exceed, and a deadline which is a round number after which the trade becomes invalid if not executed by that time.333The recipient of the traded tokens is by default the issuer of the swap transaction. This can be extended to allow for stating an explicit recipient that could be different from the issuer. In the case of an exact output swap, the goal is no longer to trade the exact amount of input tokens for the maximum amount of output tokens, but rather to minimize the amount of input tokens required to trade for the desired exact output. As such, the arguments of the function naturally change to reflect that, with the minimum output slippage protection changing to a maximum input slippage protection.

Processing. This is done using the original AMM logic for price balancing and output calculation. That is, does not change the logic based on which an AMM operates, but it rather migrates that process to the sidechain (and this applies to the rest of the transactions as well). Thus, for an exact input swap, the sidechain committee computes the maximum amount of output tokens the user will receive for all of the input tokens provided. While for an exact output swap, the committee computes the minimum amount of input tokens needed to purchase the defined output. In both cases, these computations are based off the updated pool balance on the sidechain. In other words, as transactions are processed, the committee updates the pool state that was retrieved at the beginning of the epoch.

Furthermore, the fees for LPs whose liquidity was used in filling a swap will be computed. To elaborate, when a user submits a swap transaction, they pay a small additional fee, like of their transactions input or output value. It is paid in the token pair of the pool based off its net liquidity such that the token with the largest amount of net liquidity is used. For example, if a user provides 100 input tokens in an exact input swap, and token is the dominant token, then 0.3 tokens are used for the LP fee, and 99.7 tokens is used for the swap transaction. These fees are split up proportionally amongst the positions (based on the amount of liquidity they provide) that occupy the price range for which the swap was executed. maintains a per-position fee balance, which is updated on every swap transaction, again using the same logic used by the underlying AMM to compute these fees.

Lastly, recall that a user’s deposit state is retrieved from at the beginning of each epoch, and swaps (and mints as we will see shortly) will be accepted as long as there is enough deposit to support them. Moreover, a user will not get her actual traded tokens until the end of the epoch. However, this user can use these tokens for trading on the sidechain since the sidechain tracks all balances. So basically, when a swap is executed, the input token amount are deducted from the deposit while the output token amount is added to another deposit balance (maintained on the sidechain) allowing the user to use them immediately for swaps and mints. As a result, the sidechain committee maintains two deposit variables for each user: one for the mainchain deposit and initialized with the value found in , and another for accrued sidechain deposit that is initialized to 0 at the beginning of each epoch. Whenever the user issues a swap that uses the sidechain deposit, the amount of input tokens is deducted. This also means that for each swap, the sidechain committee first checks if the mainchain deposit can cover it, and if not checks if the sidechain deposit can cover it and adjust the used deposit balance accordingly.

Summary rules. In the summary-block, the sidechain committee summarizes all swap transactions as follows: for every client of a pool, all of the swaps are combined into a single tuple. The tuple contains the public key of the client, the total payin that should be deducted from her mainchain deposit (i.e., initial mainchain deposit balance minus the updated balance computed on the sidechain), and the total payout that this user should receive, which is simply the updated sidechain deposit.

Mints. Mint transactions consist of either the creation of a new liquidity position, or supplementing additional liquidity into an already existing one.

In order to execute a mint transaction, an LP must begin by first transferring tokens to the contract before the epoch begins so these will be used to provide liquidity as desired. During the epoch, the LP can broadcast a mint transaction that contains the following inputs: the lower and upper ticks, representing the price range for which the liquidity is to reside in, and the type/amount of the token to be used as liquidity.

Processing. This is also processed using the same logic used by the AMM. We resort to a simple approach to track ownership of positions; the sidechain committee generates a unique identifier (e.g., the hash of the mint transaction along with the LP’s public key) for a new position, and the owner is the public key of the issuer LP. An existing position will receive an increase in its balance (or any other modifications on its price range) after verifying that the transaction issuer is indeed the rightful owner of the position. The latter is simply done by comparing the public keys of the owner and the transaction issuer. Mint transactions are initially invoked with a desired amount of token and token as input. The underlying AMM algorithms compute the maximum amount of liquidity (based off the input tokens) that the pool can take in at the current moment and return that value as an amount of token and token (this amount is usually less or equal to the LP’s desired amount). These values represent the share of the pools liquidity now owned by the newly minted or modified position. The mint will be accepted if the issuer LP’s deposit (either the mainchain or sidechain one) can cover the provided liquidity amount (from both tokens managed by the pool), and then this amount will be deducted from the corresponding deposit.

Summary rules. All mint transactions are summarized as follows: a list of liquidity positions will be produced with each position consisting of a tuple containing: the position identifier, the public key of the owner, total amount of liquidity provided (or net change) for each token type under this position, and total amount of accrued fees. Note that the payin of the LP is also updated when summarizing mint transactions; all provided liquidity token amounts are deducted from their deposit and reflected on the payin structure.

Burns. Burn transactions consist of a partial or complete liquidity withdrawal from a position (the latter will result in deleting the position). In order to execute a burn transaction, an LP broadcasts their burn transaction containing the following inputs: the position ID, the tick price limits and the desired amounts of tokens and to be burned. The algorithm then calculates the amount of liquidity that can be burnt from the position, given those inputs, and then returns the calculated amounts of tokens and .

Processing. Processing a burn transaction boils down to determining if the issuer LP owns the position, then calculating the amount of liquidity this LP owns in a share, and converting that amount of liquidity into an amount of both tokens. This would lead to an update to the position range (upper and lower price ticks), or a deletion of the position if all its associated liquidity is withdrawn. If a deleted position has fees owed to it, the owner LP will receive these fees as part of her total payout computed at the end of the epoch, i.e., will be added to their sidechain deposit.

Summary rules. Burns are summarized as part of summarizing mint transactions detailed above. Burns adjust the net changes of the pool liquidity balance, i.e., they decrement this balance. Any fully withdrawn position, i.e., has zero remaining liquidity balance, will be removed from the state. The payin and payout for each LP will be computed as done for mints above. That is, provided liquidity will be deducted from the corresponding deposit that covered the mint transactions, and withdrawn liquidity will be added to sidechain deposit balance to be reflected on the payout.

Collects. Collect transactions allow LPs to collected the fees earned by their liquidity positions. An LP broadcasts a collect transaction containing the identifier of the position and the amount of fees to collect.

Processing. This includes determining if the issuer LP owns the position, and checking if the amount they want to collect can be covered by their fee balance. If all is fine, the LP sidechain deposit of the issuer LP is updated to reflect the amount of collected fees, and the fee balance for that position is adjusted accordingly.

Summary rules. Summarizing collect transactions is also part of summarizing mints/burns and the LP payout structure. That is, fee balance of the referenced position is decreased based on the collected amount, and the payout to the issuer LP is computed based on the remaining sidechain deposit balance (to which the collected fee amount has been added).

Flashes. Flash transactions allow users to request short-term loans within the duration of one mainchain block. Flashes are the only transaction type which does not offload to the sidechain; the delay in paying out the actual tokens (which happens at the end of an epoch) limits the intended use of flash loans that span a very short period. As such, in , flash transactions happen on the mainchain as in the original AMM architecture. Since flash loans take place in a singular block, they do not impact the pool balances; the amount of loaned tokens should be returned within one block period or the loan will be inverted. As a result, they do not invalidate any of the transactions processed on the sidechain based off the balance snapshot taken at the beginning of an epoch.

Syncing . After producing a summary-block containing all the summaries detailed earlier, the sidechain committee leader calls the function in that resembles a sync-transaction submission. The inputs to this function call include: the list of payouts and payins for all clients and LPs, the list of liquidity positions with their updated information (i.e., balances of each token type, price range, and fees), and the updated pool balances.

Authentication. must ensure that the function invocation is issued by the rightful sidechain committee of the epoch. We use a modified idea of quorum certificates (QC) [52, 65] combined with threshold signatures. In detail, to authenticate the call for epoch , the election of committee must happen during epoch . Then, this committee runs a distributed key generation (DKG) [34] to generate a public verification key for the committee and shares of the signing key (one share per committee member) with a threshold of (so a committee size is and is the maximum number of faulty nodes as in PBFT protocols). This committee initiates an agreement on , and then sends agreement output to the committee along with their proofs of election of each member participated in the agreement.444In our implementation, this election proof is basically the output of the verifiable random function (VRF) used in the election mechanism. Committee verifies the election proofs, and then verifies that there is an agreement on . If everything is correct, committee records on by adding that to the function call inputs submitted at the end of epoch . During epoch , committee runs an agreement over the function call inputs (which are the summaries used for syncing as detailed before) and sign using there signing key shares, which result in one signature over these inputs. The leader them invokes with the inputs and this signature. In turn, verifies the signature using the recorded before accepting the summaries. By the security of the threshold signature scheme, this signature will be valid only if at least the required threshold of the committee has signed.

Processing. If successfully verified, processes the function call by updating the list of positions based on the summaries, i.e., delete fully withdrawn positions, create new positions, or adjust the parameters of existing ones. Lastly, it updates the pool balance based on the reported values. Then it dispenses the payouts to the referenced clients/LPs, deducts payins from their deposits, and refunds the residual of the deposits (if any) to their owners. Note that since we allow users to use the newly claimed tokens (tracked using the sidechain deposits) in transactions during an epoch, if a total payin of a particular user exceeds the mainchain deposit, the rest is deducted from the total payouts this user will get.

Sidechain pruning. uses the block suppression technique from chainBoost. Once the transaction encapsulating the function call is confirmed on the mainchain, all meta-blocks associated to this transaction will be pruned. The summary-blocks, as mentioned before, are permanent and represent checkpoints of the sidechain state in each epoch. So they can be used to verify the state of the AMM reflected by state variables.

Handling interruptions. We identify the scenarios that can lead to operation interruption in and how to recover from them. Recall that the sidechain committees use a PBFT-based consensus that assumes up to of the elected miners can be malicious.555This is valid under a committee size that guarantees satisfying this condition with overwhelming probability, where we adopt the committee size analysis from [54]. Thus, interruptions that could happen result from having a malicious or unresponsive leader. This leader may either propose an invalid meta/summary-blocks or invalid function call to , or not initiate the agreement in the first place. Another interruption could result from rollbacks on the mainchain. That is, when the mainchain miners switch their canonical chain to track the one satisfying the fork resolution system of the blockchain system (i.e. the longest blockchain, or the heaviest one), causing the most recent blocks to be abandoned. This is an issue if the abandoned blocks contain transactions.

Detection and recovery from these interruptions are done as proposed in chainBoost (which we review briefly here while full details can be found in [54]). A leader that proposes an invalid block or call inputs, can be easily detected by the committee by verifying the proposed blocks and the syncing inputs. Once detected, the view-change technique [40] is used to elect a new leader. In case of unresponsive leader, there is a time out so that if no agreement is initiated within that time, this triggers a leader change. The outcome of the view-change operation is recorded on the meta-blocks and is included in the summary-block for accountability. As for a leader that proposes invalid inputs, a leader-change will not help since this happen at the end of an epoch when it is time for the new committee to take over. We handle this case, and the rollback interruption, using the mass-syncing technique. The new committee issues a call covering the summaries they produced in their epoch and those produced earlier in the impacted epochs.

4.3 Security

Since delegates the processing of the AMM transactions to the sidechain, and introduces pruning and state synchronization, we show that under this new architecture the security and correct operation (i.e., safety and liveness) of the underlying AMM are preserved. In Appendix 0.A, we prove the following theorem:

Theorem 4.1

preserves the safety and liveness of the underlying AMM.

5 Implementation

To assess the performance gains that provides for AMMs, we implement a proof-of-concept and conduct a varied set of performance evaluations. We chose a Uniswap-inspired use case to represent the underlying AMM. This section discusses the implementation details, while the experimental setup and results are discussed in the next section.

Sidechain Implementation. For the sidechain, we use the chainBoost implementation from [2]. This code uses cryptographic sortition-inspired election mechanism [47] for the committee election, and this committee runs a BLS collective signing (CoSi)-based PBFT-based consensus algorithm [5]. We add the modifications needed in ; our sidechain implementation deploys its own miners, and adopts the summary rules defined in Section 4. We also modify the syncing process to be an invocation to the function in authenticated using the threshold signature-based quorum certificate approach discussed earlier. We use a simplified version of the golang BLS library [62], and a pre-generated key to sign the transaction. Furthermore, our sidechain implements two extra functions to aid in performing the AMM functionality:

-

•

: creates the inputs of the call using the information found in a summary-block. This is called by the sidechain committee leader at the end of the epoch.

-

•

retrieves users’ deposits at the beginning of an epoch.

Mainchain details. For the mainchain, we utilize the Ethereum Sepolia testnet [18] using the hardhat development environment [12]. We implemented the smart contract in Solidity [19] and deployed it on Sepolia. handles users’ deposit, storage of tokens, and the syncing and payout processes. In our implementation, the interfacing between the sidechain miners and the mainchain is handled through functionality provided by the Go-Ethereum project [11]. To allow to authenticate the function call, we implement BLS signature verification in solidity, where we use the implementation of the 256-bit Barreto-Naehrig (BN256) curve operations defined in the Ethereum precompiles [59, 39]. We implement our hash-to-point functionality as the scalar multiplication of a Keccak256 hash of the entries and the generator of the curve of BN256.

Use case: Uniswap-inspired AMM. We implement swaps, mints, burns, and collects using the same logic as in Uniswap (Appendix 0.B). We do not implement flashes since they make up a small portion of the traffic so they will not impact the performance gains we report. For simplicity, our use case implementation manages a single pool. We deployed two standard ERC20 contracts to provide the token pair traded in this pool and used in both the ammBoost and baseline experiments. Naturally, to test Uniswap V3 in an isolated environment, we used the UniswapV3Factory contract to deploy a new liquidity pool which hosts the two ERC20 tokens. In order to test against the baseline implementation of Uniswap V3, we wrote and deployed a smart contract to interface with the various Uniswap contracts as detailed in the Uniswap documentation [25]. This smart contract, from here on out referred to as the interface contract, acts as our point of contact for the Uniswap smart contracts. The interface contract routes swaps to the swapRouter contract and mints/burns/collects to the NFPM. Additionally it receives and keeps track of all of the NFT liquidity positions (through the ERC721Reciever interface) created by the users in our experiments.

Traffic generation. Users generate traffic on both the mainchain and the sidechain. On the sidechain, the traffic follows the same distribution as in Uniswap (see Appendix 0.C), i.e., 93.19% of the traffic is , 2.14% is , 2.38% is and 2.27% is . Our implementation provides configuration settings to modify the distribution and volume of the generated transactions to test their impact on the reported performance metrics.

6 Performance Evaluation

Experiment setup. We deploy our system on a computing cluster composed of 8 hypervisors, each running a 12-Core, 130 GiB RAM, VM, connected with 1 Gbps network link. This setup is capable of running around 8000 sidechain miners. Unless stated otherwise, an experiment length is 11 epochs with each epoch consists of 10 mainchain rounds (which corresponds to 30 sidechain rounds per epoch). Our default meta-block size is 1 MB and a sidechain committee contains 500 miners. We deploy 100 users to participate in the AMM, generating traffic that arrives at a constant rate of where is the chosen daily volume of transactions. We benchmark our system against a baseline, which is a deployment of Uniswap V3 on Sepolia, as mentioned earlier. We test the impact of multiple parameters on ’s performance, including various traffic amounts and distributions, block size, sidechain round duration, and number of sidechain rounds per epoch. In reporting the results, we measure the following metrics:

-

1.

Throughput: The number of transactions processed per mainchain round.

-

2.

Transaction latency: The delay between a transaction submission and its appearance in a meta-block. To obtain an accurate representation of this metric, and thus process a comparable amount of traffic, we empty the transaction queues after the end of each run.

-

3.

Payout latency: The delay between the submission of a transaction and the completion of syncing using the summary-block of the epoch in which this transaction has been published on the sidechain. We measure this metric by reporting the sum of the transaction latency (previous metric), the time needed to issue a call for the epoch during which a transaction appeared in a meta-block, and the time needed to process the transaction encapsulating the call.

-

4.

Gas cost: The average number of gas units paid to process critical transactions (such as user deposits and the call).

-

5.

Main and side chain growth: The growth (in bytes) of both the main and side chains.

Scalability. In this experiment, we test the scalability of a single pool to understand its behavior under heavy traffic. We follow the same traffic distribution as in Uniswap and vary the daily volume . We record the impact on the throughput, as well as transaction and payout latency. Our results are shown in Table 1.

| Daily volume | 5K | 50K | 500K | 25M |

|---|---|---|---|---|

| Throughput (tx/s) | 0.75 | 6.0 | 58.0 | 242.35 |

| Average sidechain latency (s) | 0.075 | 0.075 | 0.075 | 128.29 |

| Average payout latency (s) | 75.53 | 75.53 | 75.53 | 204.54 |

| BlockSize (MB) | 0.5 | 1 | 1.5 | 2 |

|---|---|---|---|---|

| Throughput (tx/s) | 121.71 | 241.61 | 362.52 | 483.43 |

| Average sidechain latency (s) | 2487.35 | 913.20 | 389.89 | 128.03 |

| Average payout latency (s) | 2562.90 | 988.89 | 466.01 | 203.64 |

Throughput wise, we record a low throughput of 0.75 tx/s up to 78 tx/s when the daily volume is between 50K and 5M transactions (roughly equivalent to 1x-100x Uniswap’s daily volume). This is mainly due to the mainchain blocks not being full as this workload is way below the capacity that our system can handle. The maximum throughput we can achieve is 242.35 tx/s when then traffic is 500x Uniswap’s daily volume.

Latency wise, we achieve a quasi-instant when the daily volume is between 50K and 5M (transactions that arrive at the beginning of the round get processed within the same round, while the residual amount of latency is due to transactions generated at the end of the epoch and processed in the next epoch). This leads to payouts being processed within one epoch (including the time needed to confirm the transaction encapsulating the function call on the mainchain). Transaction congestion happens when the daily volume is 25M, resulting in higher average transaction and payout latency as the table shows.

Impact of block size. In this experiment, we test the impact of the sidechain block size. As this experiment is primarily geared towards finding an optimal block size for our system, we compare different deployments of with different block sizes against Uniswap’s Sepolia deployment. We run the protocol with the following block sizes {} MB. We measure the impact on throughput and transaction and payout latency with the goal of identifying the block size that maximizes throughput while minimizing latency. For this experiment, we increase the daily volume to 50M transactions. Our results are in Table 2.

As shown, throughput increases as the block size increases since more transactions can be packed in a block. Increasing the block size also improves latency, as packing more transactions in a block reduces the queue congestion. However, larger block sizes mean a larger propagation delay that could be problematic for short sidechain round duration. Thus, system designers should be careful when choosing an optimal sidechain block size, balancing between the block size needed for the volume of transactions they are facing while capturing the intricacies of large network transfers.

Impact of sidechain round duration. In this experiment, we study the impact of the sidechain round duration. An ideal round duration should allow for consensus to conclude while maximizing throughput and minimizing latency. Inspired by Polygon [29] (which has a block time of 2 seconds and Algorand [13] which has a block time of around 3.6 seconds), we test the following round duration values: 4, 6, 9, and 12 seconds, and report the performance metrics as before (Table 3).

| Sidechain round duration (s) | 4 | 6 | 9 | 12 |

|---|---|---|---|---|

| Throughput (tx/s) | 241.61 | 161.33 | 108.06 | 81.05 |

| Average sidechain latency (s) | 128.29 | 520.65 | 1105.81 | 1688.51 |

| Payout latency (s) | 204.54 | 628.23 | 1260.17 | 1889.47 |

| Epoch Length (sc rounds) | 5 | 10 | 20 | 30 | 60 | 96 |

|---|---|---|---|---|---|---|

| Throughput (tx/s) | 199.98 | 224.94 | 237.82 | 241.61 | 246.16 | 247.68 |

| Sidechain latency (s) | 291.98 | 186.59 | 142.04 | 128.29 | 114.96 | 110.03 |

| Payout latency (s) | 318.04 | 222.47 | 197.87 | 204.54 | 255.08 | 318.57 |

| Swap % | 60 | 80 | ||||

|---|---|---|---|---|---|---|

| (Mint %, Burn %, Collect %) | (10,20,10) | (10,20,10) | (10,10,20) | (10,5,5) | (5,10,5) | (5,5,10) |

| Throughput (tx/s) | 254.04 | 251.59 | 251.22 | 246.59 | 245.40 | 245.24 |

| Sidechain latency (s) | 88.72 | 96.20 | 97.36 | 111.70 | 118.89 | 116.89 |

| Payout latency(s) | 165.40 | 172.86 | 173.99 | 187.82 | 195.01 | 191.82 |

| Max sidechain growth (B) | 31831 | 31831 | 31831 | 31831 | 31831 | 31831 |

Throughput wise, we observe that as the block time increases, throughput decreases. This is due to processing the same amount of transactions while increasing the time needed to produce a block. Increasing block time also increases latency as it takes longer to have transactions published in a block. To choose the optimal block time, system designers need to take into consideration the time required for the sidechain consensus and network propagation delays, while aiming to generate new blocks as fast as possible.

Impact of the number of sidechain rounds per epoch. Here, we test the performance impact of the number of sidechain rounds within an epoch. The goal is to find an epoch that maximizes throughput, minimizes transaction latency and payout delay, based on the optimal sidechain round duration from the experiment above. Thus, we pick our epoch to have sidechain rounds, and report the performance metrics (Table 4)

Having very short epochs negatively affects throughput and the sidechain latency. That is, frequent summary-blocks harm performance since this leads to a larger number of calls that are costly. At the same time, fewer transactions are processed within epoch, thus affecting both latency and throughput. Longer epoch duration reduces the sidechain latency and increases throughput. However, this affects the payout latency adversely since calls now are much fewer and spaced out (so users have to wait longer, as the epoch itself is longer, to obtain their actual token payouts). Also, this means that these users have to put larger deposits to cover their (long) epoch activities, which could be undesirable. Based on our results, we achieve the best payout latency when the epoch lasts for 20 sidechain rounds, which is equivalent to 80 sec.

Impact of traffic distribution. In this experiment, we evaluate different traffic distributions as follows (where we keep the swap operations dominant and all the number are percentages): , , where stand for swaps, mints, burns, and collects, respectively. Our results can be found in Table 5.

When varying the traffic distribution, the metrics we report remain similar. This is because transaction sizes are very close, this yields blocks containing approximately the same number of transactions, regardless of the transaction distribution. As for the maximum chain growth, it is bounded by the number of users participating during an epoch and the number of positions they create. Thus, it remains invariant even with a variation of transaction distributions since the number of users is the same.

On-chain per-operation overhead. In this experiment, we evaluate the overhead of the deposit and the syncing process and compare that to the baseline Uniswap on-chain operations. We set the daily volume to be K transactions (10x Uniswap). We use a Gas Profiler [22] to measure the gas cost of the different components of the transaction. We find that storing the state of the liquidity positions is the most expensive, as each consists of 192 bytes (or 6 words), incurring 22,100 Gas units per word. Each payout transaction incurs a constant fee of 15,771. The threshold signature-based quorum certificate incurs a fixed fee that corresponds to the gas cost of the BN256 operations, and a fee that is proportional to the length of the summary data structure. We present an itemized gas cost analysis for the sync and deposit transactions in Table 6.

—c—l—c—c—c—c—c—c—

Transaction Sync Deposit

\Block3-1¡\rotate¿ Component Payout Storage Authentication

(each) (per 32 byte) Hash To Point Verify Pairing

Keccak256 ecMUL

Average Gas 15,771 22,100 6,000 113,000 52,696

Latency(s) 15.28 54.60

\Block3-1¡\rotate¿ Operation Swap Mint Burn Collect

Average gas 160,601.45 435,609.86 158,473.43 163,743.04

Latency (s) 31.34 42.24 12.72 13.45

| component | Swap entry | Position entry | Signature | |

|---|---|---|---|---|

| Size on mainchain (B) | 352 | 416 | 128 | 64 |

| Size on sidechain (B) | 97 | 215 | ||

| Uniswap operation | Swap | Mint | Burn | Collect |

| Size on mainchain (B) | 365.27 | 565.55 | 280.21 | 150.18 |

Overall, the gas cost of the call is affected by the number of positions processed in an epoch; this cost does not scale with the number of processed transactions, but rather with the number of users. On the other hand, in baseline Uniswap the gas cost is proportional to the total generated traffic, where the numbers in Table 6 are per one transaction from each type. For the average latency, a transaction does not depend on any other mainchain transactions, so it is confirmed within one block on average. However, since a deposit depends on two ERC20 approvals, and performs 2 transfers, it takes around 4 blocks. The same behavior is observed in our Uniswap baseline, as a swap requires 1 approval and a mint requires 2 approvals.

We also report the per-operation storage cost. In particular, we report the cost breakdown for the call the mainchain and the summary-block size for , and the transaction sizes for baseline Uniswap on the mainchain. For the call, the sizes of swap and position entries vary greatly between the summarized changes in a summary-block and the inputs submitted to the mainchain. This is due to the difference in encoding and binary packing between the sidechain and the mainchain. On the mainchain, Ethereum’s application binary interface (ABI) packing keeps track of the data and all the information needed to reinterpret it back, while on the sidechain we resort to using simple binary packing. We also have an extra 6 words (192 bytes) storage overhead on the mainchain needed for the BLS signature and its public key (namely, ) for authenticating the call. We present our findings in Table 7.

For Uniswap, we notice that the transactions on Sepolia (Table 7) are smaller than the ones we observe on Ethereum (Appendix 0.C). This is because these chains use different Uniswap transaction routers. The calls to the universal router used on Ethereum end up requiring more arguments, resulting in longer transactions. Uniswap on Sepolia deploys a simpler transaction router. Of note is that the simple router contract (Uniswap V3 router) and the more complex of the two (the Universal router) are both available on Ethereum, but the Universal router is not deployed to Sepolia.

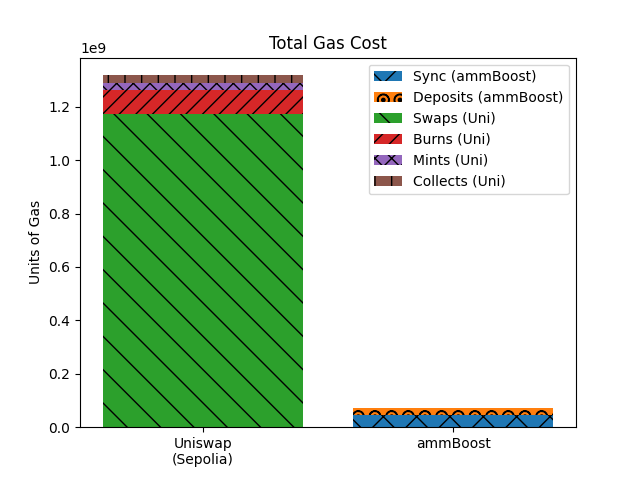

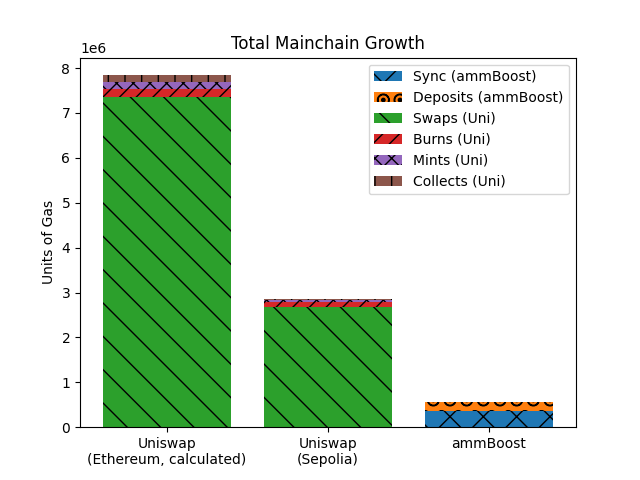

Overall comparison to Uniswap V3. We report the total gas cost and the mainchain state growth of the baseline Uniswap and . We set the daily volume to be K transactions (10x Uniswap) with the default traffic distribution. We measure the overall mainchain gas cost of relevant operations, and the state growth of the mainchain.

As shown in Figure 6, even if the sync transactions end up being heavy on gas as the number of positions increases, we achieve a 94.53% gas reduction when compared to Uniswap Sepolia. The high gas cost of the transaction is offset by it being uncommon (one occurrence per epoch). On the other hand, the gas cost of swaps, mints, burns, and collects in Uniswap are high since all are processed on the mainchain (while in these are processed on the sidechain). A similar trend is observed for the mainchain state growth, where provides 80.25% decrease in growth compared to Uniswap on Sepolia, and 92.80% decrease when compared to Uniswap on production Ethereum.666The growth for Uniswap on production Ethereum is calculated by multiplying the count of each transaction type in our experiment by its size as reported in Appendix 0.C.

7 Conclusion

We presented , a secure state growth controller and throughput booster for AMMs. It combines a new sidechain architecture, called chainBoost, with a functionality split of the AMM. The AMM is divided into two parts: a base smart contract called residing on the mainchain, which manages token pools, users’ deposits and payouts, and any transaction type that must be handled by the mainchain. And a sidechain part that does most of the heavy lifting by processing swaps, mints, burns, and collects. introduces several techniques to address challenges resulting from the unidirectional dependency between the mainchain and the sidechain. We analyze the security of our system and conduct thorough performance evaluation experiments. The results show the great potential of in reducing the on-chain storage footprint of AMMs and boosting their scalability.

Acknowledgments

The work of M.E.N. is supported by NSF under Grant No. CNS-2226932, and the work of G.A. is supported by the Latest in DeFi Research (TLDR) fellowship funded by Uniswap Foundation.

References

- [1] Amms market share. https://www.coingecko.com/research/publications/centralized-crypto-exchanges-market-share.

- [2] chainboost source code. https://github.com/CSSL-UConn/chainboost-release.

- [3] Chainstack. https://chainstack.com/.

- [4] The cheater checking problem: Why the verifier’s dilemma is harder than you think. https://medium.com/offchainlabs/the-cheater-checking-problem-why-the-verifiers-dilemma-is-harder-than-you-think-9c7156505ca1.

- [5] cothority/blscosi. https://github.com/dedis/cothority/tree/main/blscosi/blscosi.

- [6] Curve amm. https://curve.fi/#/ethereum/swap.

- [7] Dodo dex. https://dodoex.io/en.

- [8] Dune query to retrieve the number of each transaction type per year. https://dune.com/queries/3591431/6049916/92e6972f-2f75-42dc-bee9-bcf28fb46afe.

- [9] Etehreum blockchain explorer. https://etherscan.io/txs.

- [10] Filecoin. https://filecoin.io/.

- [11] Go-ethereum docs. https://geth.ethereum.org/docs.

- [12] The hardhat ethereum development environment. https://hardhat.org/.

- [13] Jump into Web3 with Algorand — Algorand Foundation News — algorand.foundation. https://www.algorand.foundation/news/jump-into-web3-with-algorand. [Accessed 22-05-2024].

- [14] Livepeer. https://livepeer.com/.

- [15] Optimism. https://www.optimism.io/.

- [16] Optimistic rollup is not secure enough than you think — game theoretic approach for more verifiable rollup. https://medium.com/onther-tech/optimistic-rollup-is-not-secure-enough-than-you-think-cb23e6e6f11c.

- [17] Polygon. https://polygon.technology.

- [18] Sepolia ethereum testnet. https://sepolia.etherscan.io/.

- [19] Solidity scripting language. https://docs.soliditylang.org/en/v0.7.4/.

- [20] Starkware solutions. https://starkware.co/.

- [21] Sushiswap. https://www.sushi.com/swap.

- [22] Tenderly — full-stack web3 infrastructure. https://tenderly.co/.

- [23] Top automated market maker (amm) coins today by market cap. https://www.forbes.com/digital-assets/categories/automated-market-maker-amm/?sh=3488af897b18.

- [24] Uniswap documentation. https://docs.uniswap.org/contracts/v3/overview.

- [25] Uniswap pool interaction guide. https://docs.uniswap.org/contracts/v3/guides/providing-liquidity/the-full-contract.

- [26] Uniswap protocol. https://uniswap.org/.

- [27] Uniswap reference implementation. https://github.com/Uniswap.

- [28] Uniswapv3subgraph. https://thegraph.com/hosted-service/subgraph/uniswap/uniswap-v3.

- [29] What is the block time on Polygon Network? — stakepolygon.com. https://stakepolygon.com/docs/faq/what-is-the-block-time-on-polygon-network/. [Accessed 22-05-2024].

- [30] zksync. https://zksync.io/.

- [31] Hayden Adams, Noah Zinsmeister, Moody Salem, River Keefer, and Dan Robinson. Uniswap v3 whitepaper. 2021.

- [32] Mustafa Al-Bassam, Alberto Sonnino, Shehar Bano, Dave Hrycyszyn, and George Danezis. Chainspace: A sharded smart contract platform. In NDSS, 2018.

- [33] Georgia Avarikioti, Eleftherios Kokoris-Kogias, and Roger Wattenhofer. Divide and scale: Formalization of distributed ledger sharding protocols. arXiv preprint arXiv:1910.10434, 2019.

- [34] Renas Bacho and Julian Loss. On the adaptive security of the threshold bls signature scheme. In ACM CCS, 2022.

- [35] Adam Back, Matt Corallo, Luke Dashjr, Mark Friedenbach, Gregory Maxwell, Andrew Miller, Andrew Poelstra, Jorge Timón, and Pieter Wuille. Enabling blockchain innovations with pegged sidechains. 2014.

- [36] Massimo Bartoletti, James Hsin-yu Chiang, and Alberto Lluch Lafuente. Maximizing extractable value from automated market makers. In Financial Cryptography and Data Security, 2022.

- [37] Joseph Bonneau, Izaak Meckler, Vanishree Rao, and Evan Shapiro. Coda: Decentralized cryptocurrency at scale. IACR Cryptol. ePrint Arch., 2020.

- [38] Sean Bowe, Alessandro Chiesa, Matthew Green, Ian Miers, Pratyush Mishra, and Howard Wu. Zexe: Enabling decentralized private computation. In IEEE S&P, 2020.

- [39] Vitalik Buterin and Christian Reitwiessner. Eip-197: Eip-197: Precompiled contracts for optimal ate pairing check on the elliptic curve alt_bn128, 2018. https://eips.ethereum.org/EIPS/eip-197.

- [40] Miguel Castro, Barbara Liskov, et al. Practical byzantine fault tolerance. In Usenix OsDI, 1999.

- [41] George Danezis and Sarah Meiklejohn. Centrally banked cryptocurrencies. In NDSS, 2016.

- [42] Christian Decker and Roger Wattenhofer. A fast and scalable payment network with bitcoin duplex micropayment channels. In Symposium on Self-Stabilizing Systems, 2015.

- [43] Robin Fritsch. Concentrated liquidity in automated market makers. In ACM CCS Workshop on Decentralized Finance and Security, 2021.

- [44] Juan Garay, Aggelos Kiayias, and Nikos Leonardos. The bitcoin backbone protocol: Analysis and applications. In EUROCRYPT, 2015.

- [45] Alberto Garoffolo, Dmytro Kaidalov, and Roman Oliynykov. Zendoo: A zk-snark verifiable cross-chain transfer protocol enabling decoupled and decentralized sidechains. In IEEE ICDCS, 2020.

- [46] Peter Gaži, Aggelos Kiayias, and Dionysis Zindros. Proof-of-stake sidechains. In IEEE S&P, 2019.

- [47] Yossi Gilad, Rotem Hemo, Silvio Micali, Georgios Vlachos, and Nickolai Zeldovich. Algorand: Scaling byzantine agreements for cryptocurrencies. In ACM SOSP, 2017.

- [48] Harry Kalodner, Steven Goldfeder, Xiaoqi Chen, S Matthew Weinberg, and Edward W Felten. Arbitrum: Scalable, private smart contracts. In USENIX Security, 2018.

- [49] Aggelos Kiayias and Dionysis Zindros. Proof-of-work sidechains. In International Conference on Financial Cryptography and Data Security, 2019.

- [50] Eleftherios Kokoris Kogias, Philipp Jovanovic, Nicolas Gailly, Ismail Khoffi, Linus Gasser, and Bryan Ford. Enhancing bitcoin security and performance with strong consistency via collective signing. In Usenix Security, 2016.

- [51] Eleftherios Kokoris-Kogias, Philipp Jovanovic, Linus Gasser, Nicolas Gailly, Ewa Syta, and Bryan Ford. Omniledger: A secure, scale-out, decentralized ledger via sharding. In IEEE S&P, 2018.

- [52] Jae Kwon. Tendermint: Consensus without mining. Draft v. 0.6, fall, 1(11):1–11, 2014.

- [53] Jiasun Li. On the security of optimistic blockchain mechanisms. Available at SSRN 4499357, 2023.

- [54] Zahra Motaqy, Mohamed Najd, and Ghada Almashaqbeh. chainboost: A secure performance booster for blockchain-based resource markets. In EuroS&P, 2024.

- [55] Andreas Park. The conceptual flaws of constant product automated market making. Available at SSRN 3805750, 2021.

- [56] Rafael Pass, Lior Seeman, and Abhi Shelat. Analysis of the blockchain protocol in asynchronous networks. In EUROCRYPT, 2017.

- [57] Mohsen Pourpouneh, Kurt Nielsen, et al. Automated market makers for cross-chain defi and sharded blockchains. arXiv preprint arXiv:2309.14290, 2023.

- [58] Kaihua Qin, Liyi Zhou, and Arthur Gervais. Quantifying blockchain extractable value: How dark is the forest? In IEEE S&P, 2022.

- [59] Christian Reitwiessner. Eip-196: Precompiled contracts for addition and scalar multiplication on the elliptic curve alt_bn128, 2017. https://eips.ethereum.org/EIPS/eip-196.

- [60] Ionut Rosca, Alexandra-Ina Butnaru, and Emil Simion. Security of ethereum layer 2s. Cryptology ePrint Archive, 2023.

- [61] Yuechen Tao, Bo Li, Jingjie Jiang, Hok Chu Ng, Cong Wang, and Baochun Li. On sharding open blockchains with smart contracts. In IEEE 36th International Conference on Data Engineering (ICDE), 2020.

- [62] Bjorn van der Laan. GitHub - BjornvdLaan/BGRVerify — github.com. https://github.com/BjornvdLaan/BGRVerify. [Accessed 21-05-2024].

- [63] Dabao Wang, Siwei Wu, Ziling Lin, Lei Wu, Xingliang Yuan, Yajin Zhou, Haoyu Wang, and Kui Ren. Towards a first step to understand flash loan and its applications in defi ecosystem. In the International Workshop on Security in Blockchain and Cloud Computing, 2021.

- [64] Jiahua Xu, Krzysztof Paruch, Simon Cousaert, and Yebo Feng. Sok: Decentralized exchanges (dex) with automated market maker (amm) protocols. ACM Computing Surveys, 55(11):1–50, 2023.

- [65] Maofan Yin, Dahlia Malkhi, Michael K Reiter, Guy Golan Gueta, and Ittai Abraham. Hotstuff: Bft consensus with linearity and responsiveness. In Proceedings of the 2019 ACM Symposium on Principles of Distributed Computing, 2019.

- [66] Mahdi Zamani, Mahnush Movahedi, and Mariana Raykova. Horizontal scaling blockchain via full sharding. In ACM CCS, 2018.

Appendix 0.A Security Analysis

Informally, preserves the correct behavior of the AMM since it processes the workload using the same logic adopted by the AMM itself. Also, since the sidechain adopts a secure PBFT consensus protocol, with the assumption that only up to miners in any epoch elected committee can be malicious, the committee only agrees on valid records that conform with the AMM operation and rules. Furthermore, since the AMM is a dApp deployed on top of a secure smart contract-enabled blockchain (i.e., the mainchain), will not impact the liveness and safety of other applications deployed on this chain or the security of the mainchain. Thus, we focus on the safety and liveness of the AMM, i.e., honest miners agree on the confirmed state of the AMM contract, the AMM state grows over time meaning that its workload is being processed, and that the produced state changes are valid based on the AMM logic.

In order to prove Theorem 4.1, we prove two lemmas showing that preserves safety and liveness of the underlying AMM (the proofs of these lemmas are inspired by the proofs found in [54]).

Lemma 1

preserves the safety of the underlying AMM.

Proof

Since implements meta-block pruning and sidechain state syncing, we identify the following threats that may impact safety in our system:

-

•

Invalid processing of AMM transactions: the sidechain committee does not follow the AMM logic in processing transactions, or accept transactions from users who do not own proper deposits on the mainchain, or process these transactions based off an invalid initial state of the token pool.

-

•

Out-of-sync AMM state on the mainchain: A committee leader does not issue a function call at the end of the epoch, causing the state of the AMM on the mainchain and the state maintained on the sidechain to be out of sync.

-

•