Efficient two-sample instrumental variable estimators with change points and near-weak identification

Abstract

We consider estimation and inference in a linear model with endogenous regressors where the parameters of interest change across two samples. If the first-stage is common, we show how to use this information to obtain more efficient two-sample GMM estimators than the standard split-sample GMM, even in the presence of near-weak instruments. We also propose two tests to detect change points in the parameters of interest, depending on whether the first-stage is common or not. We derive the limiting distribution of these tests and show that they have non-trivial power even under weaker and possibly time-varying identification patterns. The finite sample properties of our proposed estimators and testing procedures are illustrated in a series of Monte-Carlo experiments, and in an application to the open-economy New Keynesian Phillips curve. Our empirical analysis using US data provides strong support for a New Keynesian Phillips curve with incomplete pass-through and reveals important time variation in the relationship between inflation and exchange rate pass-through.

Keywords: generalized method of moments; two-sample estimators, near-weak identification; change points

JEL classification: C13, C22, C26, C36, C51.

1 Introduction

The evidence for change points is pervasive in macroeconomic applications estimating key structural parameters for monetary policy rules: Clarida et al. (1999), Stock and Watson (2002) and Ahmed et al. (2004), or when estimating the relationship between inflation and unemployment via open or close-economy New Keynesian Phillips curves - Hall et al. (2012), Magnusson and Mavroeidis (2014), Antoine and Boldea (2018), Abbas (2023), Inoue et al. (2024a). There is also strong evidence that many key macroeconomic variables responses to fiscal and monetary policies change over the sample - Inoue et al. (2024b) or depend on the state of the economy - Auerbach and Gorodnichenko (2013), Owyang et al. (2013), Ramey and Zubairy (2018), Barnichon and Matthes (2018), Jordá et al. (2020), Alpanda et al. (2021), Alloza (2022), Jo and Zubairy (2024), Klepacz (2021), and Cloyne et al. (2023), and the state dependence in many of these models can be viewed as a change point upon reordering the data.

A model with endogenous regressors and a parameter change at a given point in time is usually estimated by GMM separately over the two samples before and after the change (we refer to this estimator as the split-sample estimator). This practice can lead to large efficiency losses, because it ignores the fact that a change in parameters over two samples need not imply that everything is changing across these two samples. For example, external instruments - such as the ones used in the local projection literature or for estimating structural parameters - are constructed as shocks that are only correlated with the endogenous regressors contemporaneously, and there is often no reason to suspect that this correlation also changes over time. If, in fact, the first-stage linking instruments and endogenous regressors has common parameters, this information can be used to obtain more efficient estimators for the parameters that do change across the two samples. Additionally, since in most macroeconomic models, instruments are relatively weak - Mavroeidis (2005), Dufour et al. (2006), Nason and Smith (2008), Kleibergen and Mavroeidis (2009), Ramey and Zubairy (2018), Antoine and Boldea (2018), Barnichon (2020) - splitting the sample may make instruments appear even weaker than they are, especially when ignoring information that is common across the two samples.

We start by showing how to use the information from a common first-stage to increase asymptotic efficiency of the parameter estimates that do change across samples. While a 2SLS estimator with common first-stage is available for strong instruments in Hall et al. (2012), we show that it need not be more efficient than our estimator or than the split-sample GMM estimator. We instead develop a two-sample GMM estimator with a common first-stage, and prove that it is asymptotically at least as efficient as the split-sample estimator, even when the instruments are near-weak. The asymptotic variance we derive allows us to construct a variance estimator that is guaranteed to be no larger than that of the split-sample estimator in finite samples.111Note that the estimator we derive is not a second-step GMM estimator with the 2SLS estimator in Hall et al. (2012) as a first-step, because in the case of change points, the relationship between the two breaks down - Hall et al. (2012). Because we allow for autocorrelated errors, our framework can directly be applied to local projection estimators - Stock and Watson (2018).

While our focus is on macroeconometric applications, when the change point is known, our estimator can also be viewed as a new two-sample estimator where both the first and the second-stages are observed, and therefore we also contribute to the microeconometric literature on two-sample estimators. In the original formulation of the two-sample estimators - Angrist and Krueger (1992), Inoue and Solon (2010) - the endogenous regressors and the instruments are observed in the first sample, the outcome and the instruments in the second sample, and the first-stage of the first sample is used as proxy for the first-stage in the second sample to obtain IV and 2SLS estimators, assuming that the two first-stages are common. In our case, both first-stages and second-stages are observed, yielding new two-sample estimators.

Additionally, when the change point is unknown, we show that the implied change fraction can be estimated consistently even when the instruments are near-weak, and at the fastest available rate in the presence of exogenous regressors such as an intercept. We also provide two Wald tests for a change point in the presence of near-weak instruments. The first test assumes a common first-stage: its asymptotic distribution is pivotal, and has non-trivial power even under the alternative, although the implied change point estimator need not be consistent under the alternative and this depends on how much heterogeneity is allowed in the second moments of the data. The second test assumes that the first-stage has a change point, and checks whether the second-stage exhibits the same change point. Plugging in the implied OLS change point estimator yields a chi-squared asymptotic distribution under the null, with non-trivial power under the alternative.

We also discuss a general procedure for multiple change points, and show that a two-sample estimator for the first-stage using information about the second-stage is also more efficient than its OLS counterpart over the full-sample or over sub-samples, generalizing Antoine and Boldea (2018).

A simulation study compares the performance of the split-sample GMM estimators, the two-sample 2SLS estimators in Hall et al. (2012), and the proposed two-sample GMM estimators in the case of a known change point, an unknown change point, and pre-testing for a change point. The two-sample 2SLS estimator has larger mean squared-error compared to the split-sample estimator in several designs with heteroskedastic errors, while our two-sample GMM estimator consistently displays both lower variance and lower mean squared error than both.

We illustrate our method by estimating an open-economy New Keynesian Phillips Curve (NKPC) with monthly US data. Our empirical results provide strong support for imperfect exchange-rate pass-through - Monacelli (2005). We find that this pass-through is significant and comparable in magnitude to that of the unemployment coefficient. Our results also suggest that the relationship between inflation and exchange rate pass-through exhibits important time variation.

The rest of the paper is organized as follows. Section 2 motivates our framework. Section 3 introduces our two-sample GMM estimator and derives its asymptotic properties in presence of a known change point, a common first-stage and near-weak instruments. Section 4 presents results for the change point estimator and the two Wald tests for a change point. It also proposes a general empirical approach for multiple change points. Section 6 contains the simulations, and Section 7 the empirical application. Section 8 concludes. The proofs of the theoretical results are in the Appendix.

2 Framework and examples

To motivate our framework, consider first the standard linear regression model,

where are exogenous variables, are endogenous variables, are valid instruments (with ) that include the exogenous regressors as the first elements, and is a full-rank matrix of size . The parameter of interest is the -vector (with ).

We extend this model in three directions. First, we allow the parameters of interest to change abruptly across sub-samples. Second, we allow the second moments of the data - the variance of the moment conditions, the second moment of the instruments, and the variance of the structural errors - to change over the sample and therefore to exhibit substantial time heterogeneity. Third, we allow for the instruments to be near-weak. For all three extensions, we first consider the case when the relationship between the instruments and endogenous regressors does not change over time.222In the general procedure in Section 4, we allow for this relationship to also change.

Three examples below motivate the need for such an extension and, in particular, why the first-stage may be common while the parameters of interest may change over the sample.

New Keynesian Phillips curve. Consider a model where inflation depends on current inflation predictions and unemployment gap, which are typically endogenous and often instrumented by using lags of these variables - Hall et al. (2012). As discussed in the introduction, there is strong evidence that the parameter linking inflation to the unemployment gap changed over time, while there is no reason to believe that the dynamics of measured inflation expectations or unemployment gap changed at the same time as the unemployment gap parameter. As shown in our empirical application, as well as in Abbas (2023) - there are sample periods over which the first-stage is common; that is, the parameter remains the same before and after the change point. Even when external instruments are used instead of lags, as in Inoue et al. (2024a), the same reasoning applies.

Local projections. Suppose we are interested in whether government spending multipliers are different when interests rates are at the zero lower bound - Section 5 in Ramey and Zubairy (2018). Since interest rates were close to the zero lower bound from 2008 until recently, we can write this model as a regression of output at different horizons on government spending before and after 2008. Since government spending is endogenous, we can use external instruments such as the government spending shocks in Ramey and Zubairy (2018). Since the Blanchard and Perotti (2002) shock used in Ramey and Zubairy (2018) as instrument is constructed to measure an unexpected discretionary change in fiscal policy over the sample, it is unclear why the relationship of the unexpected component of the fiscal policy with fiscal policy itself should change exactly at the time the interest rates hit the lower bound.

Two-sample IV estimators in microeconometrics. Let above refer to individuals instead of time, and suppose we are interested in the effect of age at school entry on educational attainment - Angrist and Krueger (1992). Because some parents may enroll children earlier, the age at school entry is endogenous, and Angrist and Krueger (1992) use quarter of birth dummies as instruments. They employed data on quarter of birth and age at school entry for one sample of individuals, data on quarter of birth and educational attainment on another sample, and introduced a two-sample IV estimator where the first-stage is estimated in one sample, and plugged into the IV estimator of the second sample. This plug-in approach is employed in all two-sample IV estimators that we are aware of - Inoue and Solon (2010), Sanderson et al. (2022) - and assumes that the first-stage is common for the two populations. However, if we observed the age at school entry and educational attainment in both samples - which is likely the case for new administrative data - it is conceivable that the relationship between educational attainment and age at school entry would be heterogeneous across the two samples (and that the parameters of interest would therefore change across the two samples), yet the first-stage linking quarter of birth to age at school entry would have constant parameters across the same two samples. In general, the causal effect of a treatment on an outcome can be heterogeneous across groups of populations, while the relationship between treatment uptake and intent to treat could be homogeneous over certain groups.

3 Two-sample GMM estimators with a known change point

To simplify the exposition, consider first the case when the first-stage is common; the case of change points in the first-stage is discussed in Section 4. For the remainder of this section, the reference model is:

| (3.3) | |||||

| (3.4) |

where is a known change point with , are exogenous variables, are endogenous variables, are valid instruments (with ) that include the exogenous regressors , and is a full-rank matrix of size . The instruments share the same identification strength over the whole sample, which can range from strong () to near-weak ( and ). The parameters of interest are the vectors , with . For simplicity, we assume that all elements of are different than zero, so all parameters of interest change. To streamline notations, let , , , and .333 is a generalization of the usual operator, in the sense that for general matrices , . This model can be estimated with the split-sample GMM estimator in Andrews (1993), which minimizes:

| where | ||||

Andrews (1993) introduced the split-sample GMM estimator to study the properties of a change point test. Here, we derive its asymptotic distribution under a constant first-stage and near-weak instruments: the structural parameters associated with the endogenous variables are asymptotically normally distributed at rate , whereas those associated with the exogenous regressors are asymptotically normally distributed at the standard rate , as shown in Theorem 1.444See AntoineRenault2009 who derive asymptotic properties of 2SLS and GMM in stable models with near-weak instruments. However, this GMM estimator is not the most efficient estimator of (3.3) -(3.4) as it ignores the constancy of the first-stage across the two samples.

An estimator that does take into account that the first-stage is common is the two-sample 2SLS estimator (TS2SLS) estimator in Hall et al. (2012), which estimates the first-stage on the full sample. This estimator minimizes:

| where |

With , and , such that , the implied moment conditions for this estimator are555A more efficient two-step GMM estimator for the moment conditions (3.8) exists; however, because the moment conditions are nonlinear, it will suffer from the curse of dimensionality even with moderate number of instruments . We therefore do not pursue it in this paper.

| (3.8) |

To mimic the design of the TS2SLS estimator above and still obtain a quadratic objective function, one may be tempted to add the full-sample OLS moment condition of the first-stage to the split-sample GMM estimator. However, Ahn and Schmidt (1995) showed that adding a just-identified moment condition with its own nuisance parameter does not change the asymptotic distribution of the original estimator. Instead, we propose adding first-stage moments, for the samples before and after the change point, with the restriction that is the same across the two sub-samples. Let , and the new moment conditions be:

where stacks the OLS moment conditions from the first-stage:

| (3.10) |

The two-sample GMM (TSGMM) estimators are defined as:

In Theorem 2 below, we show that the additional moment conditions (3.10) - that now overidentify - are not redundant and deliver an asymptotically more efficient estimator of . It is worth pausing first to compare these estimators to the original two-sample IV estimator in Angrist and Krueger (1992) and the two-sample 2SLS estimator in Inoue and Solon (2010). These estimators were developed when are observed in the first sample, and in the second sample. The two-sample IV estimator uses the following moment condition:

which is very different from the moment conditions above. This estimator plugs in the first-stage of the first sample for the unavailable first-stage of the second sample . In contrast, the two-sample 2SLS estimator in Inoue and Solon (2010) uses:

Inoue and Solon (2010) also show that it is more efficient than the two-sample IV in Angrist and Krueger (1992). Note that a first-step estimator of the TSGMM estimator we proposed - based on two-stage least-squares - has four sets of moment conditions, two of which are equivalent to the moment conditions above, and two of which are the equivalent moment conditions in the other samples which are observed in our paper.

Next, we derive the asymptotic distributions of the split-sample GMM, TS2SLS and TSGMM. To do so, we impose the assumptions below.

Assumption 1

(Regularity of the error terms and first-stage equation (3.4))

(i) Let with element .

- .

- The eigenvalues of are .

- and for some , for and .

- is near epoch dependent with respect to some process , with where is a -algebra based on .

- is either -mixing of size or -mixing of size .

(ii) is full column-rank equal to .

Assumption 1 part (i) states that the instruments are valid, and allows for general patterns of weak dependence in the data, including autocorrelated errors. Therefore, our paper also applies to local projection IV estimators. Assumption 1 part (ii) ensures that the instruments are not redundant.

Assumption 2

(Regularity of the change fraction and second moment matrices)

(i) .

(ii) Let and . Then and are positive definite for , where

Assumption 2(i) ensures that there are enough observations in each of the two samples to estimate parameters consistently. Note that while we defined the two samples based on a known change point, they could also be defined in terms of a state variable splitting the two samples based on a known threshold value, as in the local projection literature - Ramey and Zubairy (2018). Additionally, they could just be two groups of observations with heterogeneous parameters - Bonhomme and Manresa (2015). Assumption 2(ii) allows for general time variation (heterogeneity) in the second moments of the data.

Assumption 3

(Regularity of the identification strength)

.

Assumption 3 ensures that the identification is sufficiently strong for the structural parameters to be consistently estimated. Under these assumptions, Theorem 1 derives the asymptotic distribution of the split-sample GMM, TS2SLS and TSGMM estimators.

Theorem 1

(Asymptotic distributions of the split-sample GMM, TS2SLS and TSGMM estimators)

Let . Under Assumptions 1 to 3,

(i)

(ii)

(iii)

and , with

.

The variances , , and and are in Appendix Definition 1.

The estimators of the endogenous regressor parameters converge at rate , which is slower than usual: this rate is due to the presence of near-weak instruments. The other parameter estimators are not affected by the near-weak identification rate, and their estimators are asymptotically normally distributed at the standard rate .666See Antoine and Renault (2009) for related results without change points. More importantly, the formula for the variance of the TSGMM estimator, containing the positive semi-definite matrix , reveals that this variance is at least as small as that of the split-sample GMM estimator asymptotically. When plugging in a consistent estimator for , this guarantees lower variance of the TSGMM estimator in finite samples as well.

The next assumptions consider additional regularity conditions on homogeneity of second moments and conditional homoskedasticity, which are key to derive conditions under which the TSGMM estimators are strictly more efficient than the TS2SLS estimators, and the TS2SLS estimators are strictly more efficient than the split-sample GMM.

Assumption 4

(Homogeneity of the second moments)

(i) and ; (ii) and .

The homogeneity assumption prevents changes in the second moments of the instruments and in their correlation with the error terms of the first-stage. For example, Assumption 4(i) is violated when there is a change in , while Assumption 4(ii) is violated when there is a change in , for example.

Assumption 5

(Conditional homoskedasticity)

, , with the -algebra generated by , and .

The following theorem compares the asymptotic variance of the proposed estimators with and without Assumptions 4 and 5.777For two square symmetric matrices of size , we write iff is positive semidefinite, and if is positive definite.

Theorem 2

(Efficiency comparison)

(i) Under Assumptions 1 to 3, , with the difference being of rank . If, additionally, , respectively , the covariances between the moment conditions in the first- and second-stages of both samples, are of full column rank, and , then .

(ii) Under Assumptions 1 to 5, for ,

| (3.13) | |||||

with equalities instead of inequalities if (3.13), respectively (2), hold with equality.

Theorem 2 part (i) shows that even when the first sample moments of the first-stage are redundant for the second sample moments of the first-stage - as it is the case under homogeneity Assumptions 4 and 5 - they are not redundant overall for the estimation of . The intuition is similar to Theorem 4 in Breusch et al. (1999), where it is shown that with three moment conditions, say , the redundancy of given does not imply that is redundant given . This non-redundancy is also related to recent results by Antoine and Renault (2017) who extend Breusch et al. (1999) to frameworks that allow for heterogenous identification strengths.

The proof relies on determining the rank of defined in Theorem 1. We intentionally allowed in part (i) for moments of the data to be heterogeneous over time for two reasons. First, because the second moments of the data may also have change points at the same time as the parameters of interest. Second, because the sample split need not be due to a change point, but rather a threshold variable as in the literature on state-dependent local projections - Ramey and Zubairy (2018), Alpanda et al. (2021). Reordering the data according to whether the threshold variable is below or above a certain known value can induce heterogeneity in the second moments of the data. Nonetheless, with this reordering, we obtain the change point model in (3.3).

We also give conditions for strict efficiency of TSGMM over split-sample GMM estimators in part (i). The first condition is natural if a first-stage linking regressors and instruments exists: if the moment conditions of the first and second-stage were not correlated, then would not be endogenous according to that first-stage. The second condition is automatically satisfied if we have two or more endogenous regressors, as is the case in our empirical application, because then . If we have only one endogenous regressor, then the condition becomes , meaning we need twice as many instruments as regressors in each of the two samples.

Theorem 2 part (ii) compares the TS2SLS with the split-sample and the TSGMM estimators, a comparison that is not possible in the general case due to the moment conditions of the TS2SLS not being a special case of the moment conditions of the other estimators.

We first show that TS2SLS estimators can be more efficient than the split-sample GMM estimators. Condition (3.13),

is equivalent to . Heuristically, it states that TS2SLS estimators are more efficient when the second-stage error - obtained after plugging in the full-sample first-stage - has smaller variance than that of the structural error. This condition should induce caution when using the TS2SLS estimators in practice, because it is not satisfied, for example, if is of the same sign as .

Additionally, the TS2SLS estimators are not a special case of the TSGMM estimators either, for which a first-step estimator based on 2SLS can be constructed.888The first-stage 2SLS estimator for TSGMM based on moment conditions (3.10) is different.. Nevertheless, the TSGMM estimators are strictly more efficient than the TS2SLS estimators despite second moment homogeneity and conditional homoskedasticity, as long as (2) holds. This condition is harder to interpret, but it is automatically satisfied for at least one of the two TSGMM estimators in the case of a single endogenous regressor and no exogenous regressors, that is and . In such a case, , and the above condition becomes,

which has to hold for at least one of since we assumed there the coefficients of the endogenous regressors change over the sample ().

To interpret this condition, assume that the regressors are fixed. Then is the limiting coefficient of a regression of on , suggesting that the TSGMM estimator “purges” of the true correlation with . On the other hand, the TS2SLS estimator transforms the error into through an orthogonal projection, so that plays the role of for each sub-sample. As a result, when these two are equal, say over the first sample, the two associated estimators TS2SLS and TSGMM are asymptotically equivalent over this sample, but the TSGMM estimator will be more efficient over the second sample.

4 Two-sample GMM estimators with unknown change points

In this section, we first explain how to deal with an unknown change point in the equation of interest. First, we propose a consistent estimator of the associated change fraction, and a new test to detect its presence. Second, we propose a new test to detect whether the change point in the first also shows up in the second-stage, and extend our inference procedure to the presence of multiple change points.

4.1 Unknown change point estimation

4.1.1 Estimation of the change fraction

We extend the results in Hall et al. (2012) to show that minimizing a 2SLS criterion delivers consistent estimators of both the change fraction and the parameters in the presence of near-weak instruments. In the first-stage, is estimated over the full-sample by OLS to get , and the augmented projected regressors . In the second-stage, consider the following 2SLS criterion given a candidate change point and parameters ,

| with |

To get the 2SLS estimators for each candidate change fraction , first concentrate with respect to to get and, then, minimize over all partitions of the sample defined by to get

| (4.1) |

and for some , a cut-off to ensure enough observations in each of the two samples. The associated 2SLS estimators of the change point and parameters are then defined as:

To derive the asymptotic properties of , impose the following regularity assumptions, which extend the known change-point assumptions in Section 3 to all change point candidates.

Assumption 6

(Regularity of the change fraction)

The candidate change points satisfy for some such that . Accordingly, .

Assumption 7

(Regularity of the instrumental variables)

Let . Then , uniformly in where is positive definite and strictly increasing in .

Assumption 8

(Regularity of the variances)

uniformly in , where is positive definite and strictly increasing in , with , of size , respectively .

Assumptions 6, 7 and 8 are typical for the change point literature. Assumption 6 ensures that there are enough observations in each sub-sample to identify the true change point. Assumption 7 ensures that there is enough variation in the instruments to identify the change point. It also allows for the second moment of instruments to change over the sample. Assumption 8 allows for (unconditional) heteroskedasticity in the sample moments of the first and the second-stage. It also allows for a change in the variance of the moment conditions.

Theorem 3

Note that the estimator of the change fraction converges at the fastest available rate . This stems from the presence of fixed changes in the parameters of the exogenous regressors; intuitively, the exogenous regressors act as their own strong instruments, and the strongest instruments determine the fast convergence rate of .

4.1.2 Detection of the change point

In practice, the existence of the change point in the second-stage equation often needs to be established. To that end, we consider the sup-Wald test of Hall et al. (2012) for which the null and alternative hypotheses are: versus , with . The associated test statistic is defined as:

| (4.2) |

| where | ||||

| and | is a HAC estimator such that | |||

We impose the following additional assumption under the null hypothesis, which maintains the same homogeneity assumption as Assumption 4, but with respect to all candidate change points. Without this assumption, the asymptotic distribution of the test is not pivotal and needs to be simulated or bootstrapped - Boldea et al. (2019).

Assumption 9

(Homogeneity of the second moments)

For any , we have: (i) ; (ii) .

The following theorem provides the limiting distribution of the sup-Wald test statistic.

Theorem 4

(Test for a change in the equation of interest)

(i) Under , and Assumptions 1 and 6 to 9,

where is a vector of independent standard Brownian motions defined on .

(ii) Under , and Assumptions 1 to 3 and 6 to 8, the test statistic diverges such that

In addition, if Assumption 9 holds and either (only one endogenous regressor, no exogenous regressors) or , then the implicit change fraction estimator is consistent, . Otherwise, is not guaranteed.

We recommend using the sup-Wald test to test for a change point because of its robustness to conditional heteroskedasticity and autocorrelation. We also note that if Assumption 9 is violated, then the implicit change fraction estimator may not be consistent, a result which to our knowledge was not previously available and may be of independent interest.

Note that the global power of the test depends on the presence of exogenous regressors: without exogenous regressors, the rate of divergence is affected by the identification strength of the instruments and is equal to ; in presence of exogenous regressors, the rate is standard and equal to , and thus is not affected by the identification strength.

4.2 General framework

We now discuss a generalization of the model considered in Section 3 to allow for changes in the parameters of first and second-stages,

| (4.5) | |||||

| (4.8) |

where , or , with , and is not correlated with or . When there is no change in the identification strength (that is, ), (4.8) naturally extends the RF models considered in Hall et al. (2012) to weaker identification patterns. Otherwise, (4.8) captures changes in identification strength that may or may not be concomitant to those in the parameter of interest . Our goal is to detect and locate both parameter instability and changes in the identification strength, as well as to provide correct and sharp inference on .

4.2.1 Test for common change

This section proposes a Wald test for a common change. Consider the case where the RF change has been detected and estimated consistently by (for example, using the methods developed in Antoine and Boldea (2018) or Bai and Perron (1998)). To test whether is also a change point in the equation of interest, we test whether the 2SLS parameter estimates defined over each corresponding sub-sample are equal to each other using a standard Wald test. These parameter estimates are defined as follows for , and and ,

| with |

The Wald test statistic for a common change is defined as:

| with | ||||

| and |

The following theorem provides the limiting distribution of the above Wald test statistic.

Theorem 5

Unlike the test in the previous section, the common change point test is simpler, because it is computed directly at the estimated change point coming from the first-stage; however, note that its the rate of divergence is different in absence of exogenous regressors, since it depends on the weakest identification rate across the two samples .

4.2.2 Extension to multiple changes and inference procedure

Both the estimation and the change point detection methods can be extended to multiple changes. For detecting the number of change points, we recommend the sequential testing methods in Hall et al. (2012). Since we have shown that the sup-Wald test of zero versus one change in Hall et al. (2012) remains valid in the presence of near-weak instruments, we conjecture that the sequential tests remain valid as well. Similarly, the TSGMM estimators can be extended to multiple changes in a straightforward way.

We now present a four-stage inference procedure that builds on results developed in Sections 3 and 4.

-

1.

First stage

Find the number changes in the first-stage via the methods in Hall et al. (2012). Find their location via the methods in Hall et al. (2012) or Antoine and Boldea (2018) and collect them in the set . Use to partition the sample, and construct by OLS (over sub-samples, if is not empty, and over the full-sample, if is empty). -

2.

Second stage

Partition the sample using , and work over the associated sub-samples. Find the number of changes in the equation of interest for each of these sub-samples, via a sequential version of the sup-Wald test presented in Section 4.1.2. Estimate them via the change point estimator of Section 3, extended to multiple changes, and collect these changes in the set . -

3.

Third stage: common changes.

Partition the sample into sub-samples according to again. Test in each of these for common changes to both the first and the second-stages, via the Wald test in Section 4.2.1. Collect the common changes in the set , and obtain . -

4.

Forth stage: estimation.

Partition the sample according to : each resulting sub-sample first-stage is stable. If there are second-stage changes in any of these sub-samples according to , use the TSGMM estimators as described in Section 3; otherwise, use the standard full-sample GMM estimator.

Of course, the multiple pre-testing steps can affect the procedure, and to safeguard against this, we suggest using a Bonferroni correction.

5 Efficient estimators of the first-stage parameters

This section shows that, in the presence of second-stage change, the TSGMM estimators of the first-stage introduced in Section 3 are also more efficient than the full-sample OLS estimates and the split-sample OLS estimates that ignore the second-stage change point. To formalize this result, consider the following stable first-stage, where we are interested in estimating :

For simplicity, we consider one endogenous regressor , no additional exogenous regressor (), and we impose strong identification, i.e. . Therefore, we drop the “vec” subscript on all estimators.

The parameter is stable, but we allow for second-stage changes, as well as potential changes in , , or in all, at , which is assumed known for simplicity. Notice that a change in at means that changes once at : as a result, Assumption 4(ii) is violated. A change in implies that changes once as , so Assumption 4(i) is violated.

We introduce a third estimator that ignores the second-stage moment conditions and uses the OLS sub-sample moment conditions before and after the change - , defined in Section 3. It corresponds to the optimal (two-step) GMM estimator that uses the moments to estimate parameters and we denote it . The theorem below shows that is at least as efficient as the other two estimators.

Theorem 6

The restriction of a common first-stage delivers not only more efficient GMM estimators of the parameters of interest, but also of the first-stage parameters. Since the first-stage is part of a system of equations linked through correlation between and , the OLS estimators of the first-stage are no longer the most efficient in presence of changes in the second-stage, or in second moments of the instruments or in the variance of the OLS moment conditions. It is important to note that OLS estimators remain the most efficient among the class of estimators that ignore the second-stage, and as long as no second moments change over the sample. Consequently, our results do not conflict with the Gauss-Markov Theorem or classical results on asymptotic efficiency of OLS.

6 Monte-Carlo study

In this section, we examine by simulation the small sample behavior of the split-sample GMM estimators, TS2SLS and TSGMM estimators when the change point is known, when it is unknown and needs to be estimated, and when pre-testing for a change point.

6.1 Data generating process

We consider the following model:

| (6.1) | ||||

| (6.2) |

with explanatory variables , exogeneous variables , endogeneous variables , and parameters of interest . is a vector of instruments, including the exogeneous regressors . determines whether the structural errors are homoskedastic or heteroskedastic.

We set with . The exogenous regressor is a constant, and the number of external instruments are set to 1 or 4. The sample sizes are and , and we implement repetitions. The true change fraction is , thus the (true) change location is either or 320 depending on the sample size. The change size is assumed to be equal to one, and the true parameters are

where is referred to as the “‘change size” in the Appendix Section A Results. The errors are jointly generated as follows:

with correlation coefficient . The RMSE is computed using the sum of the average Monte carlo bias and of the average asymptotics-based standard deviation. 999This standard deviation is calculated by plugging in the Appendix, Definition 1, consistent and heteroskedasticity-robust estimators of the quantities that enter the asymptotic variance. as

for repetitions, where is short-hand for the estimators in repetition of the coefficients on the endogenous regressors in samples and of type . All GMM estimators are computed with a 2SLS first-step estimator based on their respective moment conditions.

HOM corresponds to conditional homoskedasticity and thus . HET1 corresponds to conditional heteroskedasticity given by , and HET2 to a GARCH(1,1) model with , where . Under HET2, we employ a burn-in sample of 100 observations for , and 200 observations for .

The data generating process satisfies Assumptions 1-4 and 6-9, and also Assumption 5 in the HOM case. Condition 3.13 in Theorem 2 holds with equality, so the asymptotic distributions of the TS2SLS and of the split-sample GMM are the same under HOM, as shown in Theorem 2, and the ranking of the two estimators based on asymptotic variances is unclear under HET1-HET2. However, condition 2 holds as stated in Theorem 2, so TSGMM is asymptotically strictly more efficient than both the TS2SLS and the split-sample GMM estimators under HOM, and at least as efficient as the other two estimators under HET1-HET2.

6.2 Results with a known change point

We first consider the case where the DGP displays one change point which is fully known: that is, both the existence of the change and its location are known. Estimation results for GMM, TS2SLS, and TSGMM are reported in Tables 1, 2, and 3 with sample sizes and under HOM, HET1 and HET2, respectively. We report average Monte-Carlo bias, Monte-Carlo standard deviations, as well as asymptotics-based standard deviations and RMSE of estimators (for simplicity we drop the superscript in all tables). In addition, we report the average length of a 95% confidence interval computed with the asymptotics-based standard deviations, and the associated coverage rates.

Overall, the three estimation procedures are well-behaved, and fairly close to each other: all display small biases, and coverage rates close to the nominal 95%. In addition, Monte-Carlo standard deviations are close to their asymptotics-based counterparts, but they are slightly higher, so there are benefits to using the asymptotic formulas in Appendix Definition 1. The TS2SLS estimator does not uniformly dominate the split-sample GMM estimators in terms of efficiency: the two asymptotics-based standard deviations are close as predicted by Theorem 2 in the HOM case, but with more instruments, the asymptotic standard deviations of the TS2SLS becomes larger than that of the split-sample GMM in both HOM and HET cases. In contrast, the TSGMM consistently display lower standard deviations compared to both TS2SLS and split-sample GMM, as predicted by Theorem 2 and implied by the asymptotic variance formulas. The bias of the TSGMM is also small, and as a result, TSGMM has also consistently lower RMSE than the other two procedures, while the empirical coverage of the confidence intervals is still close to the nominal size in most cases.

6.3 Results with an unknown change point

Next, we assume the researcher knows that there is one change point, but doesn’t know its location and estimates it via the method proposed in Section 4. To ensure there are enough observations in each sub-sample, the candidate change points are taken to be between and .

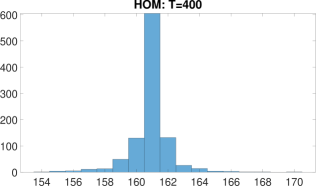

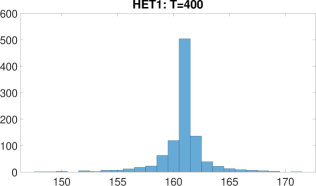

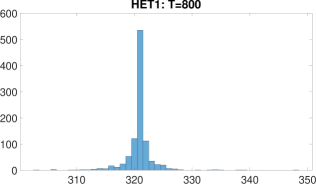

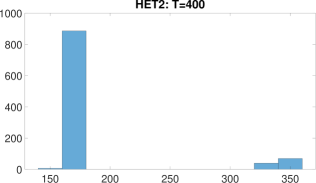

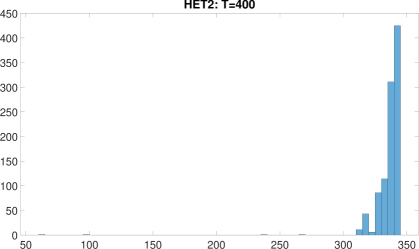

In Figure 1, we display the histograms of estimated change points with sample sizes and under HOM (top row), HET1 (middle row), and HET2 (bottom row). Note that the change points are estimated accurately in the HOM and HET1 cases, and are less accurate in the HET2 case due to the GARCH(1,1) process chosen to be close to a unit root.

Estimation results are reported in Tables 4, 5, and 6 with sample sizes and under HOM, and HET1-HET2. We also report the Monte-Carlo mean of the associated estimated change points. Due to estimation error from the change points, the differences between the three estimators are smaller, but the TSGMM continues to consistently display lower standard deviations and RMSE than the other two estimates.

As a robustness check, we also consider the case where there is no change point in the DGP, but we estimate a change point, and we set . Estimation results are reported in Table 7, while histograms of associated estimated change points are displayed in Figure 2. In all cases, the TSGMM still has lower standard errors and RMSE than the other estimates, and its coverage slightly deteriorates in the HET cases, which is to be expected due to more moment conditions than the other estimators and a small sample size.

6.4 Detection of change point

Finally, we present results related to the detection of the change point. Table 8 displays the probability of detecting a change, given that the DGP has one change point, using the sup-Wald test in Section 4.1.2. The null hypothesis of the test is that there is no change point in the data. The critical values of limiting distribution of the test are from Bai and Perron (2003). As can be seen from Table 8, the empirical size of the test is close to the nominal size, and the power is also very good as long as the magnitude of the change in both coefficients is large enough.

In Table 9, we pre-test for a change point, and subsequently estimate the parameters. If the test rejects the null, we estimate the location of the change point, and the parameters over the two sub-samples. If the test fails to reject, we estimate the parameters over the whole sample. We report Monte-Carlo bias, standard deviation, as well as asymptotic standard deviation (computed using the asymptotic theory), and RMSE: each measure is obtained as a weighted average of the corresponding quantity computed over each sub-sample. We see that pre-testing does not affect the efficiency of the TS2GMM estimators, which still displays lower standard deviations and RMSE. However, it affects coverage for all estimators in small samples such as , especially in the case HET2, where the change point is estimated less accurately.

7 Estimation of the NKPC in an open economy

The New Keynesian Phillips Curve (NKPC) played an important role in monetary policy analysis: in an open economy, it relates inflation to the movements of business cycles and expected future exchange rates. In this context, one usually assumes instantaneous import price adjustment and full transformation of exchange rate movements into consumer prices. However, it has been widely documented that the exchange rate pass-through - that is, the real marginal cost of importers - into consumer and import prices is incomplete, at least for US and other developed countries -Campa and Goldberg (2005). Accordingly, we focus here on estimating the NKPC under imperfect exchange rate pass-through (as in Monacelli (2005)) which relates inflation to a domestic driving force variable (e.g. unemployment rate) in addition to the pass-through rate measured as the difference between the exchange rate and the terms of trade:

| (7.1) |

where is the consumer price inflation, is the expected future inflation, is the unemployment rate, and is the pass-through rate.

Empirically, there does not seem to be a consensus on the exact definition of the exchange rate pass-through, and whether - and how - it might affect the Phillips curve. In the context of an incomplete pass-through, an increase in the law of one price gap, i.e. , causes an increase in inflation, similar to the one caused by a cost-push shock. Hence, an incomplete exchange rate pass-through could have relevant consequences for monetary policy. At the same time, there is also some evidence suggesting that the exchange rate pass-through has been declining, which brings into question whether it should be taken into account in any policy consideration (see e.g. Taylor (2000)).

Using monthly US data from 1990 to 2020, we find strong support for the NKPC with imperfect pass-through. The results in the next section suggest that the exchange rate pass-through plays a statistically significant role which is comparable, in magnitude, to that of unemployment - at least over part of the sample. We also find that relationship between inflation and exchange rate pass-through exhibits important time variation.

7.1 Main empirical analysis

Our main specification considers the following NKPC model with imperfect pass-through,

| (7.2) |

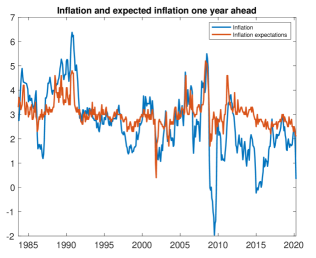

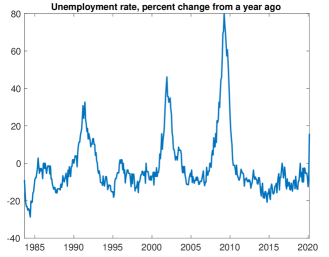

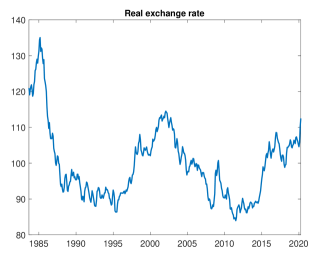

Notice that two lags of inflation are included as controls. To control for potential endogeneity of (future) expected inflation and the unemployment rate, we consider two first-stages with the following four additional instruments: one lag of expected inflation, unemployment rate, interest rate spread, and terms of trade. All variables are first de-trended using the Hodrick-Prescott filter, and we only consider their cyclical component. Our sample size consists of monthly observations over the period 1983m9-2020m4, for a total of 440 observations. The data is:

-

•

inflation : Consumer Price Index for All Urban Consumers: All Items in U.S. City Average , Percent Change from Year Ago, Monthly, Seasonally Adjusted.

-

•

expected inflation : Michigan Consumer Survey, expected inflation one-year ahead.

-

•

unemployment rate : Unemployment Rate, Percent Change from Year Ago, Monthly, Seasonally Adjusted.

- •

-

•

real exchange rate : US Exchange Rate: Relative Consumer Price Indices, index with year 2010 as base 100, monthly.

-

•

terms of trade (partially interpolated): ratio between Export Price Index (All Commodities) and Import Price Index (All Commodities). Both variables are available monthly, starting from 1982-09-01 and 1983-09-01, respectively. However, they both have missing values for the first few years, hence we use cubic splines to interpolate the missing values.

-

•

interest rate spread: difference between 3-Months Treasury Bill Secondary Market and Market Yield on U.S. Treasury Securities at 5-Year Constant Maturity.

Figure 3 plots the time series of inflation and expected inflation, unemployment rate, terms of trade, and real exchange rate.

We first estimate the change points in the two first-stage equations which we call for simplicity reduced forms henceforth (RFs), i.e. expected inflation and unemployment rate, using the Stata package Ditzen et al. (2021) that implements Bai and Perron (2003)’s algorithm. Then, we consider the segments over which both RFs are stable, and test in each for a change point in the equation of interest using the sup-Wald test described in Section 4.1; if the test rejects, wee estimate the change points in (7.2) over each such segment using the estimator described in Section 3.101010Recall that both the sup-Wald test employed and the change-point estimator is the same as in Hall et al. (2012), and in this paper we showed that they are valid in the presence of near-weak identification. Once the change location has been estimated, we estimate the model parameters in (7.2) using either TS2SLS, split-sample GMM, or TSGMM. The results are displayed in Tables 10 to 12.

In Table 10, we report the change point estimation results obtained over each RF, respectively. The RF for expected inflation has one change at 2009m3 (significant at 1%), while the RF for unemployment rate has two changes, respectively, at 2001m10 and 2008m12. Given the proximity of the first change points obtained in each reduced form, it seems plausible and reasonable to interpret them as the very same change. Accordingly, we consider the following three segments over which both reduced forms are stable:

(i) 1983m9 – 2001m10; (ii) 2001m11 – 2009m3; and (iii) 2009m4 – 2020m4.

Table 11 reports the change point estimation results obtained in the structural equation (equation of interest) using the proposed sup-Wald test in Section 4.1; this analysis is conducted over each of the three aforementioned (stable) RF segments. We find one change point in 1983m9 – 2001m10 significant at , one in 2001m11 – 2009m3 significant only at , and no change over the last period 2009m4 – 2020m4. Given the small sample size of the second segment 2001m11 – 2009m3 (less than 90 observations) - which should then be further split into two sub-periods - we limit our remaining analysis to the first segment 1983m9 – 2001m9.111111The remaining results are presented in the Supplementary appendix. The corresponding change point in the SF is estimated at 1992m4 which is significant at 1%.

Finally, Table 12 collects the estimation results of the structural parameters obtained by TS2SLS, GMM, and TSGMM over the two corresponding sub-samples, (i) 1983m9-1992m4 and (ii) 1992m5-2001m10, as well as GMM estimation results obtained over the whole segment 1983m9-2001m10 (which effectively ignores the change point discovered in the SF). These results are discussed in the next subsection.

7.2 Discussion of the empirical results

The empirical analysis of the open-economy NKPC reveals three important features with key policy implications: (i) the detection of structural change, (ii) more precise estimation of the parameters of interest, and (iii) significant time variation in these parameters of interest. If the structural change discovered by our test was ignored, traditional GMM estimates - computed over the whole sample - would imply a flat Phillips curve with respect to unemployment rate, and limited importance of the exchange rate pass-through: indeed, as can be seen from column (7) in Table 12, the estimate of is not found to be statistically significant, while the estimate of is quite small. Instead, once the (structural) change point is detected and estimated, and the sample is split accordingly, both and become statistically significant over the second interval 1992m5–2001m9. Importantly, both estimates are economically meaningful, e.g. and , and somewhat comparable in terms of magnitude; see columns (5) and (6) in Table 12 for estimation results obtained with split-sample GMM and TSGMM respectively. In addition, the estimate of is also significantly positive over the first sample, though its magnitude is more modest. Noticeably, the magnitude of each estimate obtained over a sub-sample remains much larger than the (misleading) estimate obtained by GMM over the whole sample: TSGMM estimates are respectively 0.0175 over 1983m9–1992m4 and 0.0266 over 1992m5-2001m9, while the full-sample GMM estimate is 0.0111.

Our analysis also suggests time-variation in the relationship between inflation and unemployment, and this is not surprising, as it is a prevalent finding in the NKPC literature. We also provide evidence of time-variation between inflation and the exchange rate pass-through - confirming Abbas (2023)’s findings - and the magnitude of both parameters increases from the first sub-sample to the second. When comparing sub-sample estimates obtained by TSGMM and GMM, both sets of estimates are relatively close to each other: for example, over the second sub-sample, is estimated at 0.0266 with TSGMM and 0.0267 with GMM, while corresponding estimates for are -0.0427 and -0.0434, respectively; see columns (2), (3), (5) and (6) in Table 12. One key difference between these two sets of estimates relates to their precision: TSGMM delivers more precise estimates throughout. For example, and are significant at 1% with TSGMM, and not with GMM. This is in line with our theoretical results which show that TSGMM is more efficient than GMM as long as there is any change in the structural equation over a stable reduced form. Intuitively, TSGMM exploits (useful) information that is neglected by other estimators such as split-sample GMM. Interestingly, with TSGMM, the 95%-confidence intervals obtained for both and over the two samples do not intersect, suggesting significant changes in the relationship between inflation and the exchange rate pass-through and between inflation and unemployment. Specifically, the relation between inflation and unemployment and inflation and exchange rate becomes more important in the second sample, where the estimate of the exchange rate slope increases by over 50%.

Overall, the empirical analysis provides strong support for the NKPC with imperfect pass-through.

7.3 Robustness checks

Concerns about weak identification.

In Table 13, we report results obtained by the Kleibergen-Paap rank test121212The traditional test of weak identification based on the F-test and the rule-of-thumb only applies when there is one endogenous variable. for different sub-samples. The matrix of reduced form coefficients is of size - since we have two reduced forms and four instruments - and we test the null of a rank equal to 1 over each stable RF sub-sample: the associated critical values are from the distribution with 3 degrees of freedom. The null of under-identification is rejected at 5% over the first two sub-samples, 1983m9 – 2001m10 and 2001m11 – 2009m3, while it is borderline at 10% over the last sub-sample, 2009m4 – 2020m4. Overall, the identification seems to be sufficiently strong to support our estimation results.

Alternative specification.

We consider alternative choices of instruments: specifically, we report results obtained with (i) only two instruments (one lag of unemployment rate and expected inflation), as well as with (ii) five instruments (one lag of unemployment rate, expected inflation, real exchange rate, terms of trade, interest rate spread). These results are reported Tables 14 to 17 and Tables 18 to 21, respectively. Overall, these confirm our main results: the estimates obtained with TSGMM are more precise and the parameters of interest are subject to significant changes over the sample.

8 Conclusion

In this paper, we considered a linear model with endogenous regressors. We first showed how to exploit the stability of the first-stage to deliver more efficient estimators of the parameters of interest, even in the presence of near-weak instruments. We also derived the limiting distributions of two tests that detect parameter changes in the equation of interest: the first one applies when the first-stage is stable, and the second one when the first-stage exhibits a change point that is common to the equation of interest. Third, we also showed how to exploit information from the equation of interest to obtain more efficient estimators of the (stable) first-stage parameters than the standard full-sample OLS and showed how using the TSGMM estimator can provide tighter confidence intervals in an application to the open-economy NKPC.

While the paper is focused on the efficiency of TSGMM, the moment conditions of the TSGMM estimator could also be used for identification purposes, and therefore our paper contributes to a large literature tackling identification through stability restrictions - Rigobon (2003), Magnusson and Mavroeidis (2014), Angelini et al. (2024), Angelini et al. (2024).

Acknowledgement

We would like to thank conference and seminar participants for valuable comments. B. Antoine acknowledges financial support from Social Sciences and Humanities Research Council of Canada (SSHRC). A previous version of this paper was circulated under the title “Inference in Linear Models with Structural Changes and Mixed Identification Strength”.

References

- Abbas (2023) Abbas, S. K. (2023). The New Keynesian Phillips Curve and Imperfect Exchange Rate Pass-Through. The BE Journal of Macroeconomics 23(2), 885–915.

- Ahmed et al. (2004) Ahmed, S., A. Levin, and B. Wilson (2004). Recent U.S. macroeconomic stability: good policies, good practices, or good luck? The Review of Economics and Statistics 86, 824–832.

- Ahn and Schmidt (1995) Ahn, S. and P. Schmidt (1995). Efficient estimation of models for dynamic panel data. Journal of Econometrics 68(1), 5–27.

- Alloza (2022) Alloza, M. (2022). Is fiscal policy more effective during recessions? International Economic Review 63(3), 1271–1292.

- Alpanda et al. (2021) Alpanda, S., E. Granziera, and S. Zubairy. (2021). State dependence of monetary policy across business, credit and interest rate cycles. European Economic Review 140, 103936.

- Andrews (1993) Andrews, D. (1993). Tests for Parameter Instability and Structural Change with unknown change point. Econometrica 61, 821–856.

- Angelini et al. (2024) Angelini, G., G. Cavaliere, and L. Fanelli (2024). An identification and testing strategy for proxy-svars with weak proxies. Journal of Econometrics 238(2), 105604.

- Angelini et al. (2024) Angelini, G., L. Fanelli, and L. Neri (2024). Invalid proxies and volatility changes. arXiv preprint arXiv:2403.08753. https://arxiv.org/pdf/2403.08753.

- Angrist and Krueger (1992) Angrist, J. D. and A. B. Krueger (1992). The effect of age at school entry on educational attainment: an application of instrumental variables with moments from two samples. Journal of the American Statistical Association 87(418), 328–336.

- Antoine and Boldea (2018) Antoine, B. and O. Boldea (2018). Efficient estimation with time-varying information and the New Keynesian Phillips Curve. Journal of Econometrics 204, 268–300.

- Antoine and Renault (2009) Antoine, B. and E. Renault (2009). Efficient GMM with nearly-weak identification. The Econometrics Journal 12, 135–171.

- Antoine and Renault (2017) Antoine, B. and E. Renault (2017). On the relevance of weaker instruments. Econometric Reviews 36, 928–945.

- Auerbach and Gorodnichenko (2013) Auerbach, A. and Y. Gorodnichenko (2013). Fiscal multipliers in recession and expansion. In A. Alesina and F. Giavazzi (Eds.), Fiscal Policy After the Financial Crisis, pp. 63–98. University of Chicago Press.

- Bai and Perron (1998) Bai, J. and P. Perron (1998). Estimating and testing linear models with multiple structural changes. Econometrica 66, 47–78.

- Bai and Perron (2003) Bai, J. and P. Perron (2003). Computation and analysis of multiple structural change models. Journal of Applied Econometrics.

- Barnichon (2020) Barnichon, R.and Mesters, G. (2020, 06). Identifying modern macro equations with old shocks. The Quarterly Journal of Economics 135(4), 2255–2298.

- Barnichon and Matthes (2018) Barnichon, R. and C. Matthes (2018). Functional approximation of impulse responses. Journal of Monetary Economics 99, 41–55.

- Blanchard and Perotti (2002) Blanchard, O. and R. Perotti (2002). An empirical characterization of the dynamic effects of changes in government spending and taxes on output. The Quarterly Journal of economics 117(4), 1329–1368.

- Boldea et al. (2019) Boldea, O., A. Cornea-Madeira, and A. R. Hall (2019). Bootstrapping structural change tests. Journal of Econometrics 213(2), 359–397.

- Bonhomme and Manresa (2015) Bonhomme, S. and E. Manresa (2015). Grouped patterns of heterogeneity in panel data. Econometrica 83(3), 1147–1184.

- Breusch et al. (1999) Breusch, T., H. Qian, P. Schmidt, and D. Wyhowski (1999). Redundancy of moment conditions. Journal of Econometrics 91, 89–111.

- Campa and Goldberg (2005) Campa, J. M. and L. S. Goldberg (2005). Exchange rate pass-through into import prices. Review of Economics and Statistics 87(4), 679–690.

- Clarida et al. (1999) Clarida, R., J. Galí, and M. Gertler (1999). The science of monetary policy: a New Keynesian perspective. Journal of Economic Literature 37, 1661–1707.

- Cloyne et al. (2023) Cloyne, J., O. Jordá, and A. M. Taylor (2023). State-dependent local projections: Understanding impulse response heterogeneity. NBER Working Paper (30971).

- Ditzen et al. (2021) Ditzen, J., Y. Karavias, and J. Westerlund (2021). Testing and estimating structural breaks in time series and panel data in stata. ArXiv preprint arXiv:2110.14550.

- Dufour et al. (2006) Dufour, J.-M., L. Khalaf, and M. Kichian (2006). Inflation dynamics and the New Keynesian Phillips Curve: an identification robust econometric analysis. Journal of Economic Dynamics and Control 30, 1707–1727.

- Galí and Monacelli (2005) Galí, J. and T. Monacelli (2005). Monetary policy and exchange rate volatility in a small open economy. The Review of Economic Studies 72(3), 707–734.

- Hall et al. (2012) Hall, A. R., S. Han, and O. Boldea (2012). Inference regarding multiple structural changes in linear models with endogenous regressors. Journal of Econometrics 170, 281–302.

- Inoue et al. (2024a) Inoue, A., B. Rossi, and Y. Wang (2024a). Has the Phillips curve flattened? CEPR Discussion Paper DP18846. https://cepr.org/publications/dp18846.

- Inoue et al. (2024b) Inoue, A., B. Rossi, and Y. Wang (2024b). Local projections in unstable environments. Journal of Econometrics, forthcoming.

- Inoue and Solon (2010) Inoue, A. and G. Solon (2010). Two-sample instrumental variables estimators. The Review of Economics and Statistics 92(3), 557–561.

- Jo and Zubairy (2024) Jo, Y. and S. Zubairy (2024). State dependent government spending multipliers: Downward nominal wage rigidity and sources of business cycle fluctuations. American Economic Journal: Macroeconomics, Forthcoming.

- Jordá et al. (2020) Jordá, O., M. Schularick, and A. M. Taylor (2020). The effects of quasi-random monetary experiments. Journal of Monetary Economics 112, 22–40.

- Kleibergen and Mavroeidis (2009) Kleibergen, F. and S. Mavroeidis (2009). Weak instrument robust tests in GMM and the New Keynesian Phillips Curve. Journal of Business and Economic Statistics 27, 293–311.

- Kleibergen and Paap (2006) Kleibergen, F. and R. Paap (2006). Generalized reduced rank tests using the singular value decomposition. Journal of Econometrics.

- Klepacz (2021) Klepacz, M. (2021). Price setting and volatility: Evidence from oil price volatility shocks. International Finance Discussion Paper 1316. https://www.federalreserve.gov/econres/ifdp/files/ifdp1316.pdf.

- Magnusson and Mavroeidis (2014) Magnusson, L. and S. Mavroeidis (2014). Identification using stability restrictions. Econometrica 82, 1799–1851.

- Mavroeidis (2005) Mavroeidis, S. (2005). Identification issues in forward-looking models estimated by GMM, with an application to the Phillips curve. Journal of Money, Credit and Banking 37, 421–448.

- Monacelli (2005) Monacelli, T. (2005). Monetary policy in a low pass-through environment. Journal of Money, Credit, and Banking 37, 1047–1066.

- Nason and Smith (2008) Nason, J. and G. Smith (2008). Identifying the New Keynesian Phillips Curve. Journal of Applied Econometrics 23, 525–551.

- Owyang et al. (2013) Owyang, M., V. Ramey, and S. Zubairy (2013). Are government spending multipliers greater during periods of slack? Evidence from twentieth-century historical data. American Economic Review: Papers & Proceedings 103, 129–134.

- Ramey and Zubairy (2018) Ramey, V. A. and S. Zubairy (2018). Government spending multipliers in good times and in bad: Evidence from U.S. historical data. Journal of Political Economy 126, 850–901.

- Rigobon (2003) Rigobon, R. (2003). Identification through heteroskedasticity. Review of Economics and Statistics 85(4), 777–792.

- Sanderson et al. (2022) Sanderson, E., M. M. Glymour, M. V. Holmes, H. Kang, J. Morrison, M. R. Munafò, T. Palmer, C. M. Schooling, C. Wallace, Q. Zhao, et al. (2022). Mendelian randomization. Nature Reviews Methods Primers 2(1), Article 6.

- Stock and Watson (2002) Stock, J. and M. Watson (2002). Has the business cycle changed and why?, Chapter in NBER Macroeconomics Annual, pp. 159–230. Edited by M. Gertler and K. Rogoff.

- Stock and Watson (2018) Stock, J. H. and M. W. Watson (2018). Identification and estimation of dynamic causal effects in macroeconomics using external instruments. The Economic Journal 128(610), 917–948.

- Taylor (2000) Taylor, J. B. (2000). Low inflation, pass-through, and the pricing power of firms. European Economic Review 44(7), 1389–1408.

- Wooldridge and White (1988) Wooldridge, J. M. and H. White (1988). Some invariance principles and central limit theorems for dependent heterogeneous processes. Econometric theory 4(2), 210–230.

Appendix

Appendix A Results from the Monte-Carlo study

A.1 Known change point

| Estimator | Bias | MC Std | As. Std. | RMSE | Length | Coverage |

|---|---|---|---|---|---|---|

| , | ||||||

| 0.0035 | 0.0818 | 0.0792 | 0.0793 | 0.3106 | 0.9400 | |

| 0.0015 | 0.0808 | 0.0786 | 0.0786 | 0.3080 | 0.9390 | |

| -0.0008 | 0.0749 | 0.0724 | 0.0724 | 0.2838 | 0.9330 | |

| 0.0009 | 0.0649 | 0.0646 | 0.0646 | 0.2532 | 0.9520 | |

| -0.0004 | 0.0634 | 0.0644 | 0.0644 | 0.2525 | 0.9550 | |

| -0.0012 | 0.0607 | 0.0609 | 0.0609 | 0.2388 | 0.9570 | |

| , | ||||||

| -0.0008 | 0.0393 | 0.0384 | 0.0384 | 0.1506 | 0.9310 | |

| -0.0000 | 0.0385 | 0.0391 | 0.0391 | 0.1532 | 0.9420 | |

| -0.0004 | 0.0371 | 0.0351 | 0.0351 | 0.1376 | 0.9250 | |

| -0.0010 | 0.0329 | 0.0318 | 0.0318 | 0.1245 | 0.9320 | |

| -0.0009 | 0.0325 | 0.0321 | 0.0321 | 0.1260 | 0.9360 | |

| -0.0010 | 0.0315 | 0.0299 | 0.0299 | 0.1173 | 0.9320 | |

| , | ||||||

| 0.0016 | 0.0573 | 0.0560 | 0.0561 | 0.2197 | 0.9440 | |

| 0.0004 | 0.0570 | 0.0559 | 0.0559 | 0.2190 | 0.9440 | |

| 0.0003 | 0.0514 | 0.0514 | 0.0514 | 0.2013 | 0.9530 | |

| 0.0034 | 0.0469 | 0.0459 | 0.0460 | 0.1800 | 0.9460 | |

| 0.0021 | 0.0471 | 0.0457 | 0.0458 | 0.1793 | 0.9480 | |

| 0.0022 | 0.0441 | 0.0434 | 0.0435 | 0.1701 | 0.9440 | |

| , | ||||||

| -0.0016 | 0.0292 | 0.0275 | 0.0276 | 0.1078 | 0.9340 | |

| -0.0012 | 0.0289 | 0.0278 | 0.0278 | 0.1089 | 0.9400 | |

| -0.0011 | 0.0272 | 0.0252 | 0.0252 | 0.0989 | 0.9340 | |

| 0.0004 | 0.0229 | 0.0226 | 0.0226 | 0.0885 | 0.9510 | |

| 0.0004 | 0.0231 | 0.0227 | 0.0227 | 0.0891 | 0.9440 | |

| 0.0003 | 0.0219 | 0.0213 | 0.0213 | 0.0836 | 0.9340 |

| Estimator | Bias | MC Std | As. Std. | RMSE | Length | Coverage |

|---|---|---|---|---|---|---|

| , | ||||||

| 0.0062 | 0.1145 | 0.1096 | 0.1098 | 0.4298 | 0.9340 | |

| 0.0036 | 0.1133 | 0.1087 | 0.1088 | 0.4262 | 0.9340 | |

| 0.0007 | 0.1065 | 0.1005 | 0.1005 | 0.3940 | 0.9300 | |

| 0.0011 | 0.0921 | 0.0896 | 0.0896 | 0.3510 | 0.9390 | |

| -0.0006 | 0.0867 | 0.0862 | 0.0862 | 0.3378 | 0.9500 | |

| -0.0016 | 0.0865 | 0.0847 | 0.0847 | 0.3320 | 0.9440 | |

| , | ||||||

| -0.0023 | 0.0987 | 0.0907 | 0.0908 | 0.3557 | 0.9130 | |

| 0.0028 | 0.0978 | 0.0967 | 0.0967 | 0.3789 | 0.9340 | |

| -0.0004 | 0.0939 | 0.0837 | 0.0837 | 0.3279 | 0.9180 | |

| -0.0050 | 0.0811 | 0.0765 | 0.0766 | 0.2998 | 0.9260 | |

| -0.0013 | 0.0758 | 0.0767 | 0.0767 | 0.3006 | 0.9440 | |

| -0.0043 | 0.0776 | 0.0725 | 0.0726 | 0.2842 | 0.9270 | |

| , | ||||||

| 0.0018 | 0.0814 | 0.0784 | 0.0784 | 0.3074 | 0.9340 | |

| 0.0002 | 0.0810 | 0.0782 | 0.0782 | 0.3065 | 0.9320 | |

| 0.0001 | 0.0741 | 0.0722 | 0.0722 | 0.2830 | 0.9400 | |

| 0.0044 | 0.0651 | 0.0644 | 0.0646 | 0.2525 | 0.9420 | |

| 0.0030 | 0.0628 | 0.0619 | 0.0620 | 0.2428 | 0.9430 | |

| 0.0028 | 0.0616 | 0.0611 | 0.0612 | 0.2397 | 0.9430 | |

| , | ||||||

| -0.0046 | 0.0736 | 0.0671 | 0.0672 | 0.2630 | 0.9250 | |

| -0.0022 | 0.0731 | 0.0695 | 0.0696 | 0.2725 | 0.9450 | |

| -0.0027 | 0.0698 | 0.0620 | 0.0621 | 0.2432 | 0.9190 | |

| 0.0003 | 0.0580 | 0.0557 | 0.0557 | 0.2182 | 0.9380 | |

| 0.0014 | 0.0553 | 0.0546 | 0.0546 | 0.2140 | 0.9390 | |

| 0.0005 | 0.0554 | 0.0529 | 0.0529 | 0.2075 | 0.9350 |

| Estimator | Bias | MC Std | As. Std. | RMSE | Length | Coverage |

|---|---|---|---|---|---|---|

| , | ||||||

| 0.0062 | 0.0792 | 0.0768 | 0.0770 | 0.3009 | 0.9460 | |

| 0.0047 | 0.0784 | 0.0762 | 0.0763 | 0.2987 | 0.9440 | |

| 0.0037 | 0.0750 | 0.0719 | 0.0720 | 0.2819 | 0.9420 | |

| -0.0019 | 0.4586 | 0.4242 | 0.4242 | 1.6629 | 0.9550 | |

| -0.0059 | 0.4558 | 0.4193 | 0.4194 | 1.6438 | 0.9530 | |

| -0.0091 | 0.4572 | 0.4187 | 0.4188 | 1.6411 | 0.9540 | |

| , | ||||||

| -0.0027 | 0.0366 | 0.0348 | 0.0349 | 0.1366 | 0.9440 | |

| -0.0017 | 0.0394 | 0.0375 | 0.0375 | 0.1470 | 0.9520 | |

| -0.0027 | 0.0350 | 0.0325 | 0.0326 | 0.1275 | 0.9280 | |

| -0.0001 | 0.1893 | 0.1675 | 0.1675 | 0.6565 | 0.9390 | |

| -0.0071 | 0.2341 | 0.2155 | 0.2157 | 0.8449 | 0.9600 | |

| 0.0002 | 0.1886 | 0.1657 | 0.1657 | 0.6494 | 0.9400 | |

| , | ||||||

| -0.0091 | 0.3501 | 0.3164 | 0.3166 | 1.2403 | 0.9590 | |

| -0.0108 | 0.3488 | 0.3159 | 0.3161 | 1.2384 | 0.9580 | |

| -0.0129 | 0.3471 | 0.3113 | 0.3116 | 1.2203 | 0.9580 | |

| 0.0034 | 0.0601 | 0.0588 | 0.0589 | 0.2304 | 0.9510 | |

| 0.0021 | 0.0616 | 0.0595 | 0.0595 | 0.2332 | 0.9480 | |

| 0.0022 | 0.0590 | 0.0572 | 0.0572 | 0.2241 | 0.9420 | |

| , | ||||||

| -0.0001 | 0.1275 | 0.1220 | 0.1220 | 0.4780 | 0.9590 | |

| -0.0052 | 0.1702 | 0.1581 | 0.1582 | 0.6198 | 0.9700 | |

| 0.0010 | 0.1289 | 0.1200 | 0.1200 | 0.4702 | 0.9510 | |

| 0.0015 | 0.0287 | 0.0275 | 0.0276 | 0.1079 | 0.9410 | |

| 0.0002 | 0.0313 | 0.0302 | 0.0302 | 0.1183 | 0.9490 | |

| 0.0012 | 0.0278 | 0.0267 | 0.0267 | 0.1047 | 0.9460 |

A.2 Unknown change point

| Estimator | Bias | MC Std | As. Std. | RMSE | Length | Coverage |

|---|---|---|---|---|---|---|

| , | ||||||

| Estimated change location: 161.021 | ||||||

| 0.0033 | 0.0819 | 0.0795 | 0.0796 | 0.3116 | 0.9460 | |

| 0.0013 | 0.0810 | 0.0788 | 0.0789 | 0.3091 | 0.9410 | |

| -0.0009 | 0.0751 | 0.0726 | 0.0726 | 0.2845 | 0.9370 | |

| -0.0031 | 0.0655 | 0.0655 | 0.0656 | 0.2567 | 0.9490 | |

| -0.0044 | 0.0639 | 0.0653 | 0.0654 | 0.2558 | 0.9480 | |

| -0.0051 | 0.0612 | 0.0619 | 0.0621 | 0.2426 | 0.9460 | |

| , | ||||||

| Estimated change location: 160.912 | ||||||

| 0.0042 | 0.0404 | 0.0397 | 0.0399 | 0.1557 | 0.9340 | |

| 0.0065 | 0.0400 | 0.0408 | 0.0413 | 0.1599 | 0.9410 | |

| 0.0044 | 0.0384 | 0.0365 | 0.0367 | 0.1430 | 0.9260 | |

| -0.0010 | 0.0330 | 0.0318 | 0.0318 | 0.1248 | 0.9350 | |

| -0.0008 | 0.0326 | 0.0322 | 0.0322 | 0.1263 | 0.9400 | |

| -0.0009 | 0.0316 | 0.0300 | 0.0300 | 0.1175 | 0.9350 | |

| , | ||||||

| Estimated change location: 321.038 | ||||||

| 0.0049 | 0.0575 | 0.0566 | 0.0568 | 0.2218 | 0.9490 | |

| 0.0037 | 0.0571 | 0.0564 | 0.0565 | 0.2209 | 0.9420 | |

| 0.0035 | 0.0513 | 0.0520 | 0.0521 | 0.2037 | 0.9500 | |

| 0.0035 | 0.0469 | 0.0459 | 0.0461 | 0.1801 | 0.9440 | |

| 0.0022 | 0.0472 | 0.0458 | 0.0458 | 0.1795 | 0.9470 | |

| 0.0022 | 0.0442 | 0.0434 | 0.0435 | 0.1702 | 0.9400 | |

| , | ||||||

| Estimated change location: 320.983 | ||||||

| -0.0016 | 0.0292 | 0.0275 | 0.0276 | 0.1078 | 0.9340 | |

| -0.0012 | 0.0289 | 0.0278 | 0.0278 | 0.1089 | 0.9400 | |

| -0.0011 | 0.0272 | 0.0252 | 0.0252 | 0.0989 | 0.9340 | |

| 0.0004 | 0.0229 | 0.0226 | 0.0226 | 0.0885 | 0.9510 | |

| 0.0004 | 0.0231 | 0.0227 | 0.0227 | 0.0891 | 0.9440 | |

| 0.0003 | 0.0219 | 0.0213 | 0.0213 | 0.0836 | 0.9340 |

| Estimator | Bias | MC Std | As. Std. | RMSE | Length | Coverage |

|---|---|---|---|---|---|---|

| , | ||||||

| Estimated change point: 161.071 | ||||||

| 0.0060 | 0.1147 | 0.1100 | 0.1101 | 0.4311 | 0.9380 | |

| 0.0034 | 0.1136 | 0.1091 | 0.1091 | 0.4276 | 0.9370 | |

| 0.0006 | 0.1067 | 0.1008 | 0.1008 | 0.3950 | 0.9330 | |

| -0.0029 | 0.0923 | 0.0901 | 0.0901 | 0.3531 | 0.9370 | |

| -0.0045 | 0.0869 | 0.0867 | 0.0868 | 0.3399 | 0.9480 | |

| -0.0055 | 0.0866 | 0.0853 | 0.0855 | 0.3344 | 0.9470 | |

| , | ||||||

| Estimated change point: 160.832 | ||||||

| 0.0036 | 0.0990 | 0.0912 | 0.0913 | 0.3576 | 0.9170 | |

| 0.0092 | 0.0978 | 0.0971 | 0.0976 | 0.3807 | 0.9350 | |

| 0.0054 | 0.0944 | 0.0843 | 0.0844 | 0.3303 | 0.9130 | |

| -0.0048 | 0.0813 | 0.0766 | 0.0768 | 0.3004 | 0.9290 | |

| -0.0012 | 0.0760 | 0.0768 | 0.0768 | 0.3012 | 0.9470 | |

| -0.0041 | 0.0779 | 0.0726 | 0.0727 | 0.2847 | 0.9270 | |

| , | ||||||

| Estimated change point: 321.04 | ||||||

| 0.0049 | 0.0813 | 0.0787 | 0.0789 | 0.3086 | 0.9360 | |

| 0.0033 | 0.0808 | 0.0785 | 0.0785 | 0.3075 | 0.9340 | |

| 0.0032 | 0.0738 | 0.0726 | 0.0726 | 0.2845 | 0.9430 | |

| 0.0045 | 0.0651 | 0.0645 | 0.0646 | 0.2527 | 0.9430 | |

| 0.0031 | 0.0629 | 0.0620 | 0.0621 | 0.2430 | 0.9430 | |

| 0.0029 | 0.0617 | 0.0612 | 0.0612 | 0.2398 | 0.9400 | |

| , | ||||||

| Estimated change point: 320.92 | ||||||

| 0.0010 | 0.0737 | 0.0673 | 0.0674 | 0.2640 | 0.9260 | |

| 0.0037 | 0.0733 | 0.0697 | 0.0698 | 0.2734 | 0.9400 | |

| 0.0027 | 0.0699 | 0.0624 | 0.0624 | 0.2445 | 0.9170 | |

| 0.0004 | 0.0580 | 0.0558 | 0.0558 | 0.2186 | 0.9400 | |

| 0.0016 | 0.0553 | 0.0547 | 0.0547 | 0.2144 | 0.9380 | |

| 0.0007 | 0.0554 | 0.0530 | 0.0530 | 0.2078 | 0.9340 |

| Estimator | Bias | MC Std | As. Std. | RMSE | Length | Coverage |

|---|---|---|---|---|---|---|

| , | ||||||

| Estimated change location: 203.668 | ||||||

| 0.0127 | 0.0812 | 0.0783 | 0.0794 | 0.3071 | 0.9440 | |

| 0.0113 | 0.0804 | 0.0777 | 0.0785 | 0.3045 | 0.9440 | |

| 0.0104 | 0.0775 | 0.0736 | 0.0743 | 0.2885 | 0.9410 | |

| -0.0019 | 0.4604 | 0.4261 | 0.4261 | 1.6702 | 0.9550 | |

| -0.0059 | 0.4576 | 0.4211 | 0.4211 | 1.6507 | 0.9530 | |

| -0.0092 | 0.4587 | 0.4204 | 0.4205 | 1.6481 | 0.9560 | |

| , | ||||||

| Estimated change location: 180.481 | ||||||

| 0.0127 | 0.0812 | 0.0783 | 0.0794 | 0.3071 | 0.9440 | |

| 0.0113 | 0.0804 | 0.0777 | 0.0785 | 0.3045 | 0.9440 | |

| 0.0104 | 0.0775 | 0.0736 | 0.0743 | 0.2885 | 0.9410 | |

| -0.0019 | 0.4604 | 0.4261 | 0.4261 | 1.6702 | 0.9550 | |

| -0.0059 | 0.4576 | 0.4211 | 0.4211 | 1.6507 | 0.9530 | |

| -0.0092 | 0.4587 | 0.4204 | 0.4205 | 1.6481 | 0.9560 | |

| , | ||||||

| Estimated change location: 292.366 | ||||||

| -0.0152 | 0.2785 | 0.2503 | 0.2508 | 0.9811 | 0.9610 | |

| -0.0175 | 0.2784 | 0.2498 | 0.2505 | 0.9794 | 0.9590 | |

| -0.0188 | 0.2738 | 0.2449 | 0.2457 | 0.9601 | 0.9580 | |

| -0.1168 | 0.1766 | 0.1528 | 0.1923 | 0.5990 | 0.8420 | |

| -0.1179 | 0.1758 | 0.1519 | 0.1923 | 0.5956 | 0.8390 | |

| -0.1179 | 0.1759 | 0.1517 | 0.1922 | 0.5948 | 0.8380 | |

| , | ||||||

| Estimated change location: 302.204 | ||||||

| 0.0033 | 0.1274 | 0.1219 | 0.1219 | 0.4777 | 0.9560 | |

| -0.0018 | 0.1696 | 0.1578 | 0.1578 | 0.6185 | 0.9680 | |

| 0.0043 | 0.1287 | 0.1199 | 0.1200 | 0.4699 | 0.9480 | |

| 0.0015 | 0.0287 | 0.0276 | 0.0276 | 0.1080 | 0.9410 | |

| 0.0002 | 0.0313 | 0.0302 | 0.0302 | 0.1185 | 0.9480 | |

| 0.0012 | 0.0278 | 0.0267 | 0.0268 | 0.1048 | 0.9470 |

| Estimator | Bias | MC Std | As. Std. | RMSE | Length | Coverage |

|---|---|---|---|---|---|---|

| , and | ||||||

| HOM | ||||||

| Estimated change location: 201.662 | ||||||

| -0.0006 | 0.0277 | 0.0274 | 0.0274 | 0.1072 | 0.9440 | |

| -0.0005 | 0.0276 | 0.0276 | 0.0276 | 0.1082 | 0.9420 | |

| -0.0004 | 0.0275 | 0.0266 | 0.0266 | 0.1041 | 0.9330 | |

| -0.0025 | 0.0607 | 0.0548 | 0.0548 | 0.2146 | 0.9230 | |

| 0.0002 | 0.0585 | 0.0567 | 0.0567 | 0.2222 | 0.9340 | |

| -0.0022 | 0.0561 | 0.0475 | 0.0475 | 0.1861 | 0.9080 | |

| HET1 | ||||||

| Estimated change location: 198.848 | ||||||

| -0.0030 | 0.0706 | 0.0666 | 0.0667 | 0.2612 | 0.9210 | |

| 0.0003 | 0.0698 | 0.0691 | 0.0691 | 0.2707 | 0.9450 | |

| -0.0022 | 0.0703 | 0.0649 | 0.0649 | 0.2544 | 0.9190 | |

| -0.0113 | 0.1470 | 0.1215 | 0.1220 | 0.4763 | 0.8850 | |

| 0.0007 | 0.1451 | 0.1361 | 0.1361 | 0.5333 | 0.9250 | |

| -0.0074 | 0.1361 | 0.1063 | 0.1066 | 0.4168 | 0.8660 | |

| HET2 | ||||||

| Estimated change location: 335.398 | ||||||

| -0.0008 | 0.0281 | 0.0267 | 0.0267 | 0.1046 | 0.9310 | |

| -0.0006 | 0.0303 | 0.0286 | 0.0286 | 0.1120 | 0.9390 | |

| -0.0010 | 0.0275 | 0.0262 | 0.0262 | 0.1028 | 0.9350 | |

| -0.0083 | 0.6605 | 0.5624 | 0.5624 | 2.2044 | 0.9340 | |