Probabilistic Programming with Programmable

Variational Inference

Abstract.

Compared to the wide array of advanced Monte Carlo methods supported by modern probabilistic programming languages (PPLs), PPL support for variational inference (VI) is less developed: users are typically limited to a predefined selection of variational objectives and gradient estimators, which are implemented monolithically (and without formal correctness arguments) in PPL backends. In this paper, we propose a more modular approach to supporting variational inference in PPLs, based on compositional program transformation. In our approach, variational objectives are expressed as programs, that may employ first-class constructs for computing densities of and expected values under user-defined models and variational families. We then transform these programs systematically into unbiased gradient estimators for optimizing the objectives they define. Our design enables modular reasoning about many interacting concerns, including automatic differentiation, density accumulation, tracing, and the application of unbiased gradient estimation strategies. Additionally, relative to existing support for VI in PPLs, our design increases expressiveness along three axes: (1) it supports an open-ended set of user-defined variational objectives, rather than a fixed menu of options; (2) it supports a combinatorial space of gradient estimation strategies, many not automated by today’s PPLs; and (3) it supports a broader class of models and variational families, because it supports constructs for approximate marginalization and normalization (previously introduced only for Monte Carlo inference). We implement our approach in an extension to the Gen probabilistic programming system (genjax.vi, implemented in JAX), and evaluate our automation on several deep generative modeling tasks, showing minimal performance overhead vs. hand-coded implementations and performance competitive with well-established open-source PPLs.

1. Introduction

Variational inference (VI) is a popular approach to two fundamental probabilistic modeling tasks:

-

•

Fitting probabilistic models to data. Given a family of joint probability distributions defined over latent variables and observed variables , find the one that best explains an observed dataset . For example, writing for the probability density function of , we may be interested in finding that maximizes the marginal likelihood

(1) -

•

Approximating intractable posterior distributions. For a particular probabilistic model , find the best approximation to the (usually intractable) posterior distribution , from a class of tractable approximations (the variational family). For example, again using lower-case letters for probability density functions, we may be interested in finding that minimizes the reverse KL divergence

(2)

Practitioners often aim to solve both these tasks at once, simultaneously fitting a probabilistic model and approximating its posterior distribution. To do so, one defines a variational objective , mapping particular distributions and to a scalar loss (or reward). For example, one common choice is the evidence lower bound, or ELBO:

| (3) |

As the decomposition on the right-hand side suggests, maximizing the ELBO simultaneously maximizes the (log) marginal likelihood of the data and minimizes the KL divergence of the posterior approximation to the posterior. Besides the ELBO, researchers have also proposed many alternative objectives (Dempster et al., 1977; Hinton et al., 1995; Agakov and Barber, 2004; Bornschein and Bengio, 2015; Burda et al., 2016; Ranganath et al., 2016; Rainforth et al., 2018; Sobolev and Vetrov, 2019; Malkin et al., 2022), which formalize the two goals of fitting models and approximating posteriors differently (e.g., by using divergences other than the KL). Once a variational objective has been defined, practitioners aim to find parameters that maximize (or minimize) . There are many possible approaches to performing this optimization. The most popular methods rely on gradients of the objective—or more often, unbiased stochastic estimates of these gradients. Designing and implementing algorithms for estimating these gradients, with sufficiently low variance and computational expense, is the key roadblock on the path from defining a variational inference problem to solving it.

Indeed, although variational inference algorithms have found widespread adoption in Bayesian statistics (Fox and Roberts, 2012; Kucukelbir et al., 2017; Blei et al., 2016; Hoffman et al., 2013; Blei and Jordan, 2006) and in probabilistic deep learning (Kingma and Welling, 2022; Pu et al., 2016; Kingma et al., 2021; Vahdat and Kautz, 2020; Malkin et al., 2022), implementing variational inference algorithms by hand remains a tedious and error-prone endeavor. The key mathematical ingredients specifying a variational inference problem—, , and —are typically not represented directly in code; rather, the practitioner must:

-

(1)

use algebra, probability theory, and calculus to derive a gradient estimator: a way to rewrite the gradient as an expectation , for some family of distributions and some family of functions ; and then

-

(2)

write code to sample and evaluate —an unbiased estimate of .

It is often non-trivial to ensure that and are faithfully implemented, and that the math used to derive them in the first place is error-free. Small changes to , , or , or to the gradient estimation strategy employed in step (1), can require large, non-local changes to and , and in implementing these changes, it is easy to introduce hard-to-detect bugs. When optimization fails, it is often unclear whether the problem is with the math, the code, or just the hyperparameters.

Automation via Probabilistic Programming.

Reflecting the importance of variational inference, many probabilistic programming languages (PPLs) (especially “deep” PPLs, such as Pyro (Bingham et al., 2019), Edward (Tran et al., 2017, 2018), and ProbTorch (Stites et al., 2021)), feature varying degrees of automation for VI workflows. In these languages, users can express both models and variational families as probabilistic programs; the system then automates the estimation of gradients for a pre-defined set of supported variational objectives . This design significantly lowers the cost of implementing and iterating on variational inference algorithms, but several pain points remain:

-

•

Incomplete coverage. Existing PPLs offer limited or no support for many variational objectives, including forward KL objectives (Naesseth et al., 2020); hierarchical, nested, or recursive variational objectives (Ranganath et al., 2016; Zimmermann et al., 2021; Lew et al., 2022); symmetric divergences (Domke, 2021); trajectory-balance objectives (Malkin et al., 2022); SMC-based objectives (Maddison et al., 2017; Gu et al., 2015; Li et al., 2023a; Naesseth et al., 2018); and others. Today’s PPLs also do not automate many powerful gradient estimation strategies, for example those based on measure-valued differentiation (Mohamed et al., 2020).

-

•

Duplicative engineering effort. For PPL maintainers, supporting new gradient estimation strategies or language features requires separately introducing the same logic into the implementations of multiple variational objectives. Because this engineering effort is non-trivial, many capabilities are not uniformly supported. For example, as of this writing, Pyro’s ReweightedWakeSleep objective (Le et al., 2019) does not support minibatching, even though other objectives do. As another example, variance reduction strategies such as data-dependent baselines and enumeration of discrete latents are implemented for the ELBO in Pyro, but not, e.g., for the importance-weighted ELBO.

-

•

Difficulty of reasoning. The monolithic implementations of each variational objective’s gradient estimation logic intertwine various concerns, including log density accumulation, automatic differentiation, gradient propagation through stochastic choices, and variance reduction logic. This can make it difficult to reason about correctness. Indeed, while the community has made tremendous progress in understanding the compositional correctness arguments of an increasingly broad class of Monte Carlo inference methods for probabilistic programs (Ścibior et al., 2017, 2018; Lew et al., 2023a; Lundén et al., 2021; Borgström et al., 2016), pioneering work on correctness for variational inference (Lee et al., 2019, 2023; Li et al., 2023b) has generally focused on specific properties (e.g., smoothness and absolute continuity) in somewhat restricted languages, and not to end-to-end correctness of gradient estimation for variational inference.

This Work.

In this paper, we present a highly modular, programmable approach to supporting variational inference in PPLs. In our approach, all three ingredients of the variational inference problem—, , and —are encoded as programs in expressive probabilistic languages, which support compositional annotation for specifying the desired mix of gradient estimation strategies. We then use a sequence of modular program transformations—each of which we independently prove correct—to construct unbiased gradient estimators for the user’s variational objective.

Contributions.

This paper contributes:

- •

- •

-

•

Formalization: We formalize our approach as a sequence of composable program transformations (§4-5) of simply-typed -calculi for probabilistic programs (§3), and prove the unbiasedness of gradient estimation (under mild technical conditions) by logical relations (§6). Ours is the first formal account of variational inference for PPLs that accounts for the interactions between tracing, density computation, gradient estimation strategies, and automatic differentiation.

-

•

System: We contribute genjax.vi, a performant, GPU-accelerated implementation of our approach in JAX (Frostig et al., 2018), which also extends our formal modeling language with constructs for marginalization and normalization (§7) (Lew et al., 2023a). We also contribute concise, pedagogical Haskell and Julia versions. Our implementations are the first to feature reverse-mode variants of the ADEV algorithm for modularly differentiating higher-order probabilistic programs (Lew et al., 2023b).111System and code available at https://gen.dev/genjax/vi

-

•

Empirical evaluation: We evaluate genjax.vi on several benchmark tasks, including the challenging Attend-Infer-Repeat model (Eslami et al., 2016). We find that genjax.vi makes it possible to encode new gradient estimators that converge faster and to better solutions than Pyro’s estimators. We also show, for the first time, that a version of ADEV can be scalably and performantly implemented, to deliver competitive performance on realistic probabilistic deep learning workloads.222Lew et al. (2023b) present only a toy Haskell implementation of forward-mode ADEV, and report no experiments.

Programmability is sometimes seen as being at odds with automation. We emphasize that this paper expands the automation provided by the system, relative to existing VI support in PPLs, by automating a combinatorial space of gradient estimators for arbitrary objectives specified as programs (rather than the handful of objectives and estimators supported by existing PPLs).

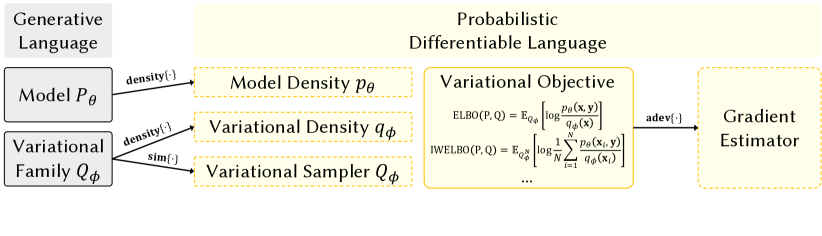

2. Overview

Fig. 1 illustrates the workflow of a typical user of our system for modular variational inference:

An illustration of our pipeline.

-

•

Model and variational programs. The user begins by writing two probabilistic programs in our generative language: a model program and a variational program. The generative language is a trace-based PPL that resembles Pyro (Bingham et al., 2019), ProbTorch (Stites et al., 2021), and Gen (Cusumano-Towner et al., 2019). The model program encodes a family of joint probability distributions , and the variational program encodes a family of distributions , possible approximations to the posterior for data .

-

•

Objective function. The user now seeks to find values of that simultaneously (1) fit to the data , and (2) make close to the posterior . To make these informal desiderata precise, the user defines an objective function, using our differentiable language. This language features constructs for taking expectations with respect to, and evaluating densities of, generative language programs, making it easy to concisely express objectives like the ELBO (Eqn. 3).

-

•

Gradient estimator. The final step is to optimize the objective function via stochastic gradient ascent. We construct unbiased gradient estimators for the user’s objective function with an extended version of the ADEV algorithm (Lew et al., 2023b). Users can rapidly explore a combinatorial space of estimation strategies with compositional annotations on their generative programs, to navigate tradeoffs between the variance and the computational cost of the automated gradient estimator.

Example.

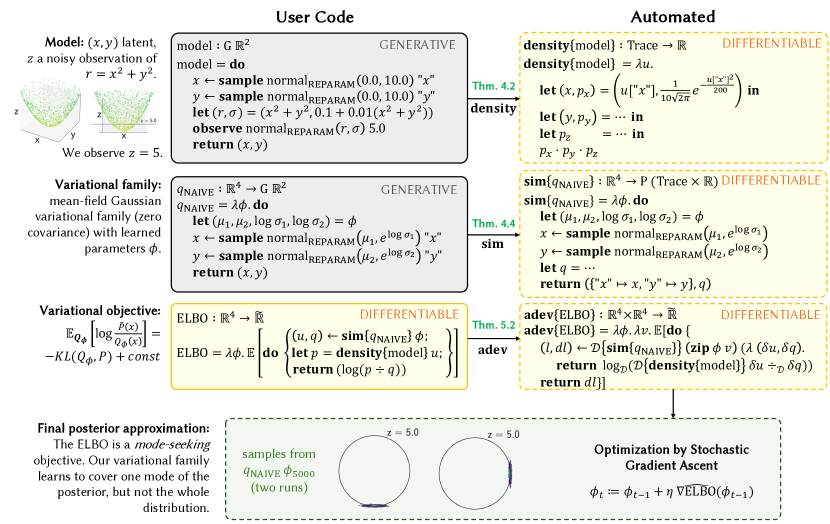

To make this concrete, consider the toy problem illustrated in Fig. 2, which we seek to solve by training a variational approximation to the posterior. We go through the following steps:

-

•

Define a model. Our model encodes a generative process for points around a 3D cone. We use sample to sample latents and with string-valued names, and observe to condition on the observation that . Our goal is to infer consistent with this observation.

-

•

Define a variational family. In the second panel of Fig. 2, we construct a variational family, a parametric family of possible approximations to the posterior distribution. Our variational inference task will be to learn parameters that maximize the quality of the approximation. Our is a mean-field variational approximation, i.e., it generates and independently. Note that primitive distributions (here, normal) are annotated with gradient estimation strategies (here, REPARAM) for propagating derivative information through the corresponding primitive.333For a primitive distribution over values of type , parameterized by arguments , a gradient estimation strategy for is an approach to unbiasedly estimating for functions . ADEV composes these primitive estimation strategies into composite strategies for estimating gradients of variational objectives. Supported strategies vary by primitive; for the Normal distribution, for instance, they include REPARAM, MEASURE-VALUED, and REINFORCE, corresponding to different approaches to gradient estimation from the literature. See §5.

-

•

Define a variational objective. We now use the differentiable language to define the objective function we wish to optimize. Three constructs are especially useful: (1) density, which computes or estimates densities of probabilistic programs; (2) sim, which generates a pair of a sample and its density from a probabilistic program; and (3) , which takes the expected value of a stochastic procedure. We use them together to implement the ELBO objective from Eqn. 3.

-

•

Perform stochastic optimization. Our objective is compiled into an unbiased estimator of its gradient with respect to the input parameters . We can then apply stochastic optimization algorithms, such as stochastic gradient ascent and ADAM. The bottom of Fig. 2 illustrates samples from after training. Because the ELBO minimizes the reverse (or mode-seeking) KL divergence, our variational approximation learns to hug one edge of the circle-shaped posterior.

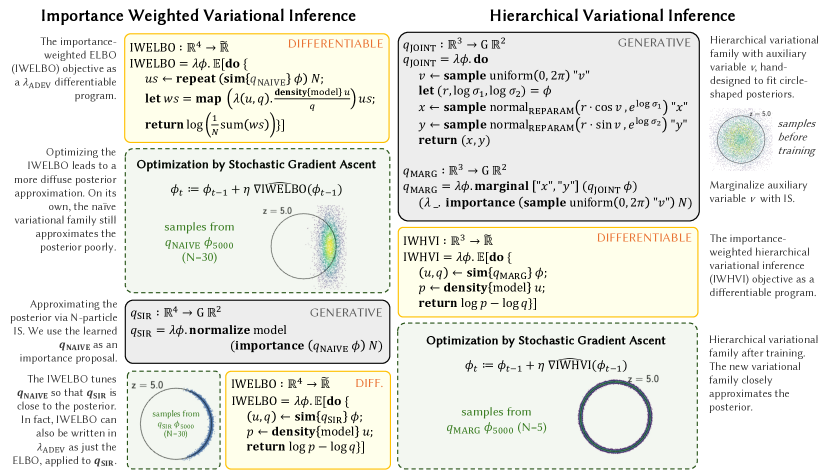

Better Inference with Programmable Objectives.

To better fit the whole posterior, we will need either a new objective function or a more expressive variational family. Our system’s programmability allows users to quickly iterate within a broad space of VI algorithms. In Fig. 3, we illustrate two possible strategies for improving the posterior approximation:

-

•

Importance-weighted variational inference. On the left side of Fig. 3, we define the IWELBO variational objective (Burda et al., 2016), as the expected value of the process that generates particles from the variational family , and computes a log mean importance weight. This objective does not directly encourage to approximate the posterior well; rather, it encourages to be a good proposal distribution for -particle importance sampling, targeting the posterior. To illustrate this, we define a new probabilistic program , which uses normalize to construct a sampling importance resampling (SIR) approximation to the posterior: it generates samples from , computes importance weights for each sample, and randomly selects a sample to return according to the weights. Drawing samples from , with and set to the parameters that optimized the IWELBO objective, yields a close approximation to a larger portion of the posterior. (In fact, the IWELBO objective can be equivalently expressed in our framework as the ordinary ELBO, but applied directly to rather than to .)

-

•

Hierarchical variational families. On the right side of Fig. 3, we define a better variational family: . First, we define a hand-designed posterior approximation , which extends with an auxiliary variable , to allow it to better fit circle-shaped posteriors. We cannot directly use with the ELBO objective, however, because it is defined over the space of triples , not the space of pairs as in our model. The marginal construct shrinks the sample space back down to just , approximating the marginal density using importance sampling. The resulting algorithm is an instance of importance weighted HVI (IWHVI) (Sobolev and Vetrov, 2019).

3. Syntax and Semantics

Shared Core

Generative Probabilistic Programming ()

Differentiable Probabilistic Programming ()

Grammar and typing rules for our languages.

We now formalize the core of our approach. Although our formal model lacks several features of our full language (see §7 and Appx. A), it is still expressive, featuring higher-order functions, continuous and discrete sampling, stochastic control flow, and discontinuous branches. Ultimately, our formalization aims to give an account of how user programs representing models, variational families, and variational objectives are transformed into compiled programs representing unbiased gradient estimators. We begin in this section by introducing two calculi for generative and differentiable probabilistic programming (Fig. 4).

3.1. Shared Core

3.1.1. Syntax

The top of Fig. 4 presents the shared core, the -calculus on which both our languages build. It is largely standard, with functions, tuples, if statements, and ground types for Booleans, strings, and numbers, but two aspects merit further discussion:

-

•

Smooth and non-smooth reals. First, following Lew et al. (2023b), we have two types for real numbers, and . Intuitively, the type is the type of “real numbers that must be used differentiably,” whereas the type is the type of “real numbers that may be manipulated in any (measurable) way.” These constraints are enforced by the types of primitive functions: non-smooth primitives like only accept inputs. Smooth primitives, by contrast, come in two varieties, smooth versions (e.g. ) and non-smooth versions (e.g. ).444The reader may wonder if we also need primitives that accept some smooth and some non-smooth inputs, but this turns out to be unnecessary, because non-smooth inputs can always be safely promoted to smooth inputs. The output will then also be smooth, but this is by design: if any input to a primitive has smooth type, then the primitive’s output must also have smooth type, to ensure that future computation does not introduce non-differentiability. We allow implicit promotion of terms of type into terms of type .

-

•

Primitive distributions. The shared core includes a type of primitive probability distributions over ground types . Again following Lew et al. (2023b), we expose multiple versions of each primitive, e.g. and . All versions denote the same distribution, and so our correctness results (which are phrased in terms of our denotational semantics) ensure that gradients will target the same objective no matter which version a program uses (Thm. 5.2). But different versions of the same primitive employ different estimation strategies for propagating derivatives, striking different trade-offs between variance and cost. Furthermore, because different estimation strategies may place different requirements on the user’s program, the typing rules for different versions of the same primitive may differ. For example, constructs a distribution of type , meaning that probabilistic programs that draw samples from it can freely manipulate those samples. By contrast, constructs a distribution of type , so samples from must be used smoothly.

3.1.2. Denotational Semantics.

We assign to each type a mathematical space , and interpret an open term as a map from , the space of environments for context , to , the space of results to which can evaluate. Formally, we work in the category of quasi-Borel spaces (Heunen et al., 2017), but to ease exposition, we present our semantics in terms of standard measure theory when possible. So, for example, we write that is the measurable space , that is the product of the measurable spaces and , and so on, but with the implicit understanding that these can equivalently be viewed as quasi-Borel spaces. For semantics of higher-order types, we use quasi-Borel spaces explicitly (e.g., we set to , the quasi-Borel space of quasi-Borel maps from to ).

To give a semantics to our primitive distributions, we need to first assign to each ground type a base measure over : for discrete types , we set , the counting measure, and for continuous types , we set , the Lebesgue measure. Given two ground types and , the base measure of the product, , is , the product of the base measures for each type. With base measures in hand, we can define , the space of probability measures on that are absolutely continuous with respect to . Absolute continuity ensures that these distributions have density functions.

3.2. Generative Probabilistic Programming with

Users write probabilistic models and variational families in , which extends the shared core with a monadic type of generative programs (Fig. 4, left). Examples of programs in include the model and variational programs (model and ) in Fig. 2.

3.2.1. Syntax

Syntactically, programs of type interleave standard functional programming logic (from the shared core) with two new kinds of statements: sample and observe. The sample statement takes as input a probability distribution to sample (of type ) and a unique name for the random variable being sampled (of type Str). The observe statement takes as input a probability distribution representing a likelihood (of type ), and a value representing an observation (of type ). A generative program can include many calls to sample and observe, ultimately inducing an unnormalized joint distribution over traces: finite dictionaries mapping the names of random variables to sampled values. Intuitively, ignoring the observe statements in a program, we can read off a sampling distribution over traces—the prior. The observe statements then reweight each possible execution’s trace by the likelihoods accumulated during that execution, yielding an unnormalized posterior over traces.

3.2.2. Denotational Semantics

Formally, we write for the space of possible traces. It arises as a countable disjoint union, indexed by possible trace shapes (finite partial maps from string-valued names to corresponding ground types ), of product spaces . We can also define a base measure over , by summing product measures for each possible trace shape:

Generative programs (of type ) induce measures on that satisfy two properties: they are absolutely continuous with respect to (and therefore have a well-defined notion of trace density ), and they are discrete-structured: for -almost-all pairs of traces , either , or there exists a string present in both and such that . In words, if two distinct traces are both in the support of a generative program, then in the two executions that those traces represent, there must have been some sample statement at which different choices were made for the same random variable. We write for the space of measures on satisfying these two properties. The semantics then assigns : a generative program denotes both a (well-behaved) measure on traces, and a return-value function that given a trace, computes the program’s -valued result when its random choices are as in the trace.

The semantics for terms of type (Fig. 4, bottom left) give a formal account of how a generative program’s source code yields a particular measure on traces and return-value function. We write for , so that computes the measure on traces and computes the return-value function. In Appx. E, we show that our term semantics really does map every program of type a well-behaved measure over traces, i.e., the absolute continuity and discrete-structure requirements are satisfied by our definitions. The semantics of each probabilistic programming construct can be understood in terms of its trace distribution and return value function:

-

•

: The simplest generative programs deterministically compute a return value . These programs denote deterministic (Dirac delta) distributions on the empty trace , because they make no random choices. The return value function then maps any trace to the program’s return value, .

-

•

: Slightly more complicated, the command denotes a measure over singleton traces , namely the pushforward of the measure by the function . The return value function for statements accepts a trace and looks up the value associated with the name , if it exists. We define to return the value associated with name in , if name is a key in , and otherwise to return a default value of the appropriate type.555All ground types are inhabited, and we can choose the default values arbitrarily.

-

•

: Like return, the statement makes no random choices, and thus has an empty trace. But it denotes a scaled Dirac delta measure: the measure it assigns to the empty trace is equal to the density of the value under the measure .

-

•

: Sequencing two generative programs concatenates their traces (which we write using the concatenation operator). The helper checks whether the names used by each of two traces are distinct, returning if so and otherwise. We use it in our definition of to model that when a program uses the same name twice in a single execution, a runtime error is raised: the semantics assigns measure 0 to those executions, leaving measure for the remaining, valid executions.666The semantics of a runtime error are equivalent to the semantics of -ing an impossible outcome. Because of this, if the user’s model contains such errors, variational inference can be seen as training a guide program to approximate the model posterior given that no errors are encountered. If the variational program itself contains either observe statements or runtime errors, it can also denote an unnormalized measure, in which case an objective like the ELBO () can no longer be interpreted as a lower bound on the model’s log normalizing constant . Our system will still produce unbiased gradient estimates for the objective, but it is likely not an objective that the user intended to optimize. This suggests that better static checks for whether a program is normalized could be useful, helping users to avoid silent optimization failures if they accidentally encode an unnormalized variational family.

3.3. Differentiable Probabilistic Programming with

3.3.1. Syntax

The right panel of Fig. 4 presents a separate extension of the shared core, , a lower-level language for differentiable probabilistic programming (Lew et al., 2023b). Like , adds a monadic type for probabilistic computations, , which supports the sampling of primitive distributions (with sample), deterministic computation (with return), scoring by multiplicative density factors (score), and sequencing (with do). But probabilistic programs do not denote distributions on traces, and the sample statements do not specify names for random variables. Rather, programs directly denote (quasi-Borel) measures on output types .

Even so, we do include syntax for constructing and manipulating traces as data. This is because, in , we will develop program transformations that turn programs into programs that (differentiably) simulate and evaluate densities of reified trace data structures.

The language also features an expected value operator , of type . Terms of type intuitively represent “losses (i.e., objectives) that can be unbiasedly estimated.” The ultimate goal of a user in is to write an objective function of type (where ), and then use automatic differentiation of expected values (§5) to obtain a gradient estimator for the loss function it denotes. These loss functions can be constructed by taking expectations of probabilistic programs (using ) or by composing existing losses using new primitives (e.g., , , and ). Example programs include the objectives defined in §2 (ELBO, IWELBO, and IWHVI), as well as the automatically compiled programs on the right-hand side of Fig. 2.

3.3.2. Denotational Semantics

Semantically, is the space of quasi-Borel measures on . The type has the same denotation as , but cannot be used monadically (i.e., it composes in a more restricted way than ). This is because it is intended to represent an unbiased estimator of a particular real number. For example, suppose denotes a probability measure over the reals with expected value . Then denotes the same probability measure, with expected value . But can be used within larger probabilistic programs; for example, we can write , which draws a sample from and exponentiates it. By Jensen’s inequality, the expected value of will generally be greater than . By contrast, the term cannot be freely sampled within probabilistic programs, but can be composed with certain special arithmetic operators, so we can write (for example) . The primitive uses special logic to construct an unbiased estimator of given an unbiased estimator of , so the program denotes a probability distribution that does have expectation .

4. Compiling Differentiable Simulators and Density Evaluators

| Spec | Syntax Semantics | |||||||||||||||||||||||||||||||||

| Wrapper | ||||||||||||||||||||||||||||||||||

| Helper |

|

|||||||||||||||||||||||||||||||||

| on types |

|

|||||||||||||||||||||||||||||||||

| on terms |

|

Spec Syntax Semantics Wrapper Helper Syntax Semantics on types on terms \DescriptionDefinitions of our program transformations for density evaluation and traced simulation.

We now show how to take programs and automatically compile them into programs that simulate traces or compute density functions. We introduce two program transformations, sim and density, which take terms to terms that implement the desired functionality. The intuition for these transformations is as follows:

-

•

() At a high level, to simulate traces, we just run the generative program and record the value of every sample we take into a growing trace data structure.777In the full specification for sim, along with the simulated trace, the transformed term also returns (with probability 1) the density of the term evaluated at the simulated trace.

-

•

() To compute the density of a trace, we execute the program, but fix the value of every primitive sample to equal the recorded value from the given trace, and multiply a running joint density by the density for the primitive. For observe, we multiply the running joint density by the density of the primitive evaluated at the value provided to the observe statement.

For example, simulating from the unnormalized model in Fig. 2 and then evaluating the density of the sampled trace — using sim and density as introduced in Fig. 5 — might produce:

Note that although they are not usually formalized as program transformations or rigorously proven correct, the techniques we describe here are well-known and widely used in the implementations of PPLs, e.g. in Gen, ProbTorch, and Pyro.

Differentiability Properties of Densities.

In the context of variational inference, density functions must satisfy certain differentiability properties—with respect to the parameters being learned, and possibly with respect to the location at which the density is being queried, depending on the gradient estimators one wishes to apply. Previous work has developed specialized static analyses to determine smoothness properties of different parts of programs, in order to reason about gradient estimation for variational inference (Lee et al., 2023). A benefit of our approach is that it greatly simplifies this reasoning: the overall differentiability requirements for gradient estimation are enforced by the type system of the target-language (), as in (Lew et al., 2023b). We translate well-typed source-language programs into well-typed target-language density evaluators and trace simulators, which can be composed into well-typed variational objectives. This implies a non-trivial result: the restrictions that enforces on models and variational families are sufficient to ensure the necessary differentiability properties for unbiased estimation of variational objective gradients. Furthermore, these guarantees can be modularly extended to new variational objectives, gradient estimation strategies, and modeling language features. We discuss this further at the end of §5.

4.1. Compiling Differentiable Density Evaluators

The density program transformation density is given in Fig. 5 (top). As input, it processes a term of type : a generative program that has some (ground type) parameter or input. The result of the transformation is a term of type , which, given a parameter and a trace , computes the density of at .

The transformation is only defined for source programs of type , but it is implemented using a helper transformation that is defined at all source-language types. The intended behavior of applied to a source-language term depends on the type of the term; we encode this type-dependent specification into a family of relations indexed by types (see Fig. 5). Each is a subset of ; if , it means that it is permissible for to translate a term denoting into a term denoting . For example, relates measures on to their density functions with respect to , to encode that should transform primitive distribution terms into terms that compute primitive distribution densities. More interesting is the specification for on full probabilistic programs, of type . Because the term under consideration may be only part of a larger program, must compute not just a density, but also a return value (for use later in the program) and a remainder of its input trace, containing choices not consumed while processing the current term. The relation encodes this intuition using the function , which splits a trace into two parts: the largest subtrace of in the support of and the remaining subtrace, or, if no such subtrace exists, all of and the empty trace (see Appx. E for a formal definition).

To prove that works correctly, we first prove that satisfies its intended specifications:

Lemma 4.1.

Let be an open term of . Then is a well-typed open term of , and .

The proof (in Appx. E) is by induction, but because the inductive hypothesis is different at each type (depending on our definition of ), it is an example of what is often called a logical relations proof. Once it is proven, we are ready to prove the main correctness theorem for densities:

Theorem 4.2.

Let be a closed term for some ground type . Then is a well-typed term and for all , is a density function for with respect to .

Proof.

Fix and let . By Lemma 4.1, we have that . Now consider a trace . The macro invokes on to obtain a triple . By the definition of , we have that and , for . Recall that if is in the support of , or if no subtrace of is in the support of , then returns , causing to enter its branch and return as desired. If is not in the support of but has a subtrace that is, then returns that subtrace, along with a non-empty . In this case the branch of correctly returns (because is not in the support). ∎

4.2. Compiling Differentiable Trace Simulators

The simulation program transformation sim is given in Fig. 5 (bottom). Like density, it processes as input a term of type , but it generates a term of type , satisfying the specification that the pushforward by is the original program’s measure over traces, , and that with probability 1, the second component is the density of evaluated at the sampled trace. Like density, sim is implemented using a helper macro defined at all types. Fig. 5 presents the logical relations specifying the helper’s intended behavior on terms of type . These relations are simpler than those for ; for example, on terms of type , has almost the same specification as sim itself, except that it must also compute a return value.

One feature of that is worth noting is its translations of primitives. If a primitive used within a traced probabilistic program is annotated with a gradient estimation strategy, then the translated program uses the same annotated primitive, and then computes a density. This is only well-typed because the density functions of primitives that return values (i.e., not values) are smooth. This is not a requirement of ADEV in general, but we require it in order to automate differentiable traced simulation.

To prove correctness, we again begin by showing the helper is sound:

Lemma 4.3.

Let be an open term of . Then is a well-typed open term of , and .

The proof is again by logical relations, and can be found in Appx. E. We can then prove the correctness of sim itself:

Theorem 4.4.

Let be a closed term. Then is a well-typed term and is the pushforward of by the function .

Proof.

Fix and let . By Lemma 4.3, we have that . The macro invokes to obtain a triple , but only returns . Observe that the requirements placed by on and are precisely the conditions we aim to prove here. ∎

5. Variational Inference via Differentiable Probabilistic Programming

| Syntax Semantics |

| Syntax Semantics |

Type Translation and Logical Relations where

Term Translation

ADEV program transformation

As we saw in §2, the density and trace simulation programs automated in the previous section can be used to construct larger programs implementing variational objectives. Once we have a program representing our objective function, we need to differentiate it. Conventional AD systems do not correctly handle randomness in objective functions, or the expectation operator , and will produce biased gradient estimators when applied naively (Lew et al., 2023b). For example, standard AD has no way of propagating derivative information through a primitive like (to do so, one would need to define the notion of derivative of a Boolean with respect to the probability that it was heads). The ADEV algorithm (Lew et al., 2023b) is designed to handle these features, and can be used to derive unbiased gradient estimators automatically.

Extending ADEV with Traces and Unnormalized Measures.

Fig. 6 gives the ADEV program transformation, extended to handle new datatypes (traces) and unnormalized measures (due to score). Fig. 6 shows two top-level transformations, and . The transformation exists solely for analytical purposes, to produce a term that must satisfy a local domination condition in order for gradient estimates to be unbiased:888We have omitted several terms from Fig. 6, denoted with “”. These terms are as in (Lew et al., 2023b, Fig. 26), and do not affect the behavior of the transformation, only .

Definition 5.1 (locally dominated).

A function is locally dominated if, for every , there is a neighborhood of and an integrable function such that .

Under this mild assumption, ADEV produces correct unbiased gradient estimators:

Theorem 5.2.

Let be a closed term, satisfying the following preconditions:

-

(1)

is finite for every .

-

(2)

is locally dominated for every and .

Then is a well-typed term, satisfying the following properties:

-

•

is a probability measure with finite expectation for all .

-

•

is differentiable and .

Static Checks and Unbiasedness.

Probabilistic programming languages like Pyro and Gen use specialized logic — also going beyond ordinary AD — to unbiasedly estimate derivatives of particular variational objectives like the ELBO, for user-defined models and variational families. But in these systems, biased gradient estimates can still arise if the user’s model or variational family violates assumptions made by the PPL backend. For example:

-

•

The user’s program may sample from a normal distribution, then branch on whether for some constant threshold , in order to decide on the distribution of another random variable . Pyro’s default gradient estimation strategy assumes that the joint density of the model is differentiable with respect to the values of Gaussian random variables like , but this assumption is violated by the user’s program, because the joint density is of the form , which may be discontinuous at .

-

•

Gen’s default gradient estimation strategy does not place differentiability assumptions on the user’s program, but does assume that the support of each primitive distribution does not depend on learned parameters. If the user’s program samples from a uniform distribution with learned endpoints and , this assumption will be violated, and Gen’s gradient estimates will be biased.

In our design, by contrast, there is no default gradient estimation strategy. Rather, the user chooses a different gradient estimation strategy for each primitive, and the overall gradient estimator is automated compositionally. Crucially, different versions of primitives (employing different gradient estimation strategies) have static types that enforce the key assumptions necessary for their unbiasedness. For example:

-

•

The primitive has type , so if is drawn from , then the type of the variable is . The type of is , and so the expression is ill-typed. Thus, the types enforce that the smoothness assumptions of the reparameterization estimator hold for the user’s program, if the user chooses to apply this estimator.

-

•

In our system, the uniform distribution with custom endpoints is , which behaves like a safe version of Gen’s uniform distribution—its output can be used non-smoothly, but its bounds must not depend directly on learned parameters. (The bounds may still depend on, e.g., Gaussian random choices with learned means.)

Our smoothness-typing discipline in is similar to, but slightly different from, that in Lew et al. (2023b). As an example, their version of ADEV can support a primitive , but we cannot introduce such a primitive that returns or . This is because the program transformation would need to translate such primitives into code for computing the uniform distribution’s density as a smooth function of its endpoints—which is not possible, since the density of the uniform distribution is discontinuous at the endpoints.

These static checks are necessary for proving unbiasedness, as without them, we could easily produce estimators that do not respect the restrictions of the estimation strategies they employ.

6. Correctness of Gradient Estimation for Variational Inference

We can put together the results of the previous two sections to prove a general correctness theorem for our approach to variational inference. Suppose the user has written the following three programs:

-

•

A model program: a closed program .

-

•

A variational program: a closed program .

-

•

An objective program: a closed program , of the form

where and do not occur free in . This program encodes the variational objective , where is an environment mapping and to densities of and (with respect to ) and and to simulators for and .

The user wants to find and that optimize . Our result is that our system estimates derivatives of this objective unbiasedly, under mild technical conditions:

Theorem 6.1.

Let . If for all and , is finite and is locally dominated for each , then for all , is a probability measure with finite expectation and

To understand the guarantee the theorem gives more concretely, consider the following objective program defining the ELBO (Eqn. 3):

We can write it in the form required by the theorem as follows:

The theorem then establishes that, under mild technical conditions, applying to yields an unbiased estimator of .

7. Full System

In the previous sections, we presented a formal model of the key features of our approach. Our full language and system (detailed in Appx. A) extends our formal model in three key ways:

-

•

New language features for probabilistic models and variational families (Appx. A.1). Our full language includes constructs for marginalizing (marginal) and normalizing (normalize) programs, making it possible to express a broader class of models and variational families than in current systems. Our versions of these constructs are designed following Lew et al. (2023a).

-

•

Differentiable stochastic estimators of densities and density reciprocals (Appx. A.2). When exact densities of programs cannot be efficiently computed, our full system can compile terms implementing differentiable unbiased estimators of the required density functions and their reciprocals. These estimators can even have learnable parameters controlling their variance, which can be optimized jointly as part of the overall variational objective.

-

•

Reverse-mode automatic differentiation of expected values (Appx. A.4). Our full language’s AD algorithm computes vector-Jacobian products for expected values of probabilistic objectives, whereas our formal development shows only Jacobian-vector products. Algorithms for vector-Jacobian products, also known as reverse-mode AD algorithms, are much more efficient when optimizing scalar losses with large numbers of parameters, common in deep learning.

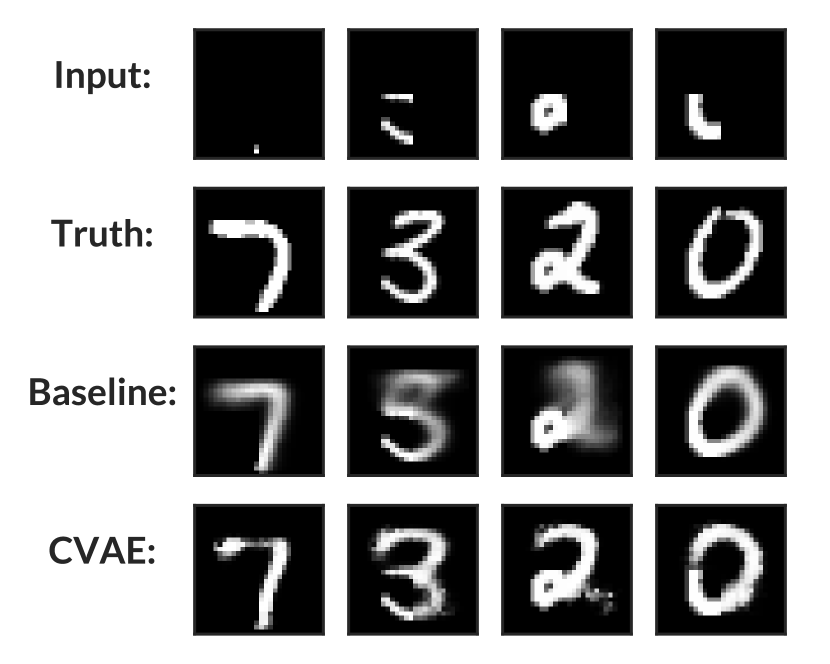

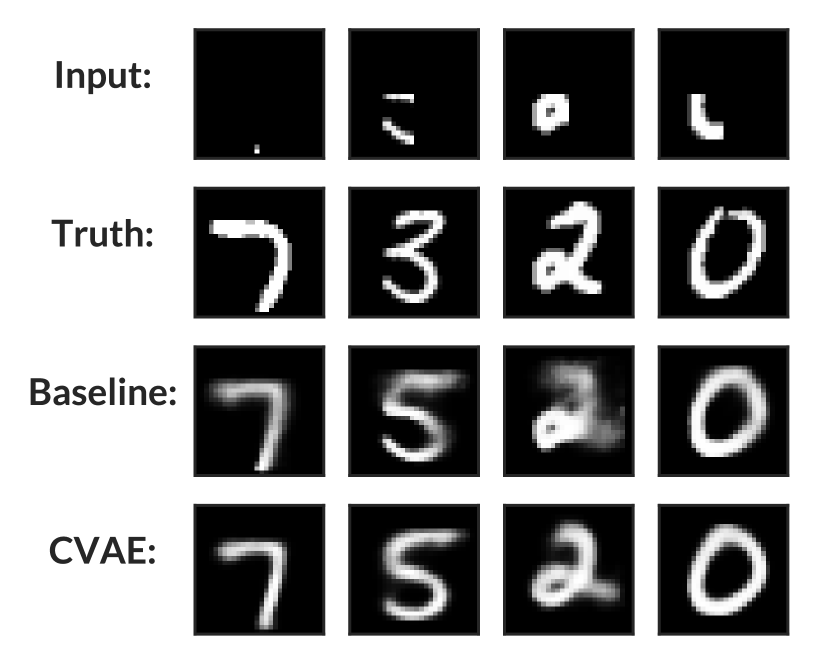

8. Evaluation

We evaluate our approach using genjax.vi, a prototype of our proposed architecture implemented as an extension to a JAX-hosted version of Gen (Cusumano-Towner et al., 2019). All experiments were run on a single device with an AMD Ryzen 7 7800X3D @ 5.050 GHz CPU and an Nvidia RTX 4090 GPU. We consider several case studies designed to answer the following questions:

-

•

Overhead. How much overhead is incurred by using our automated gradient estimators, over hand-coded versions? We compare the same gradient estimator for a variational autoencoder (Kingma and Welling, 2022) constructed (a) via a hand-coded implementation and (b) via our automation.

- •

-

•

Expressivity and compositional correctness. For the objectives and estimator strategies expressible in our system, is it possible to combine all objectives and estimator strategies while maintaining correctness? We evaluate the expressiveness of our system vs. Pyro on the AIR model, and on a hierarchical variational inference problem (Agakov and Barber, 2004).

Overhead.

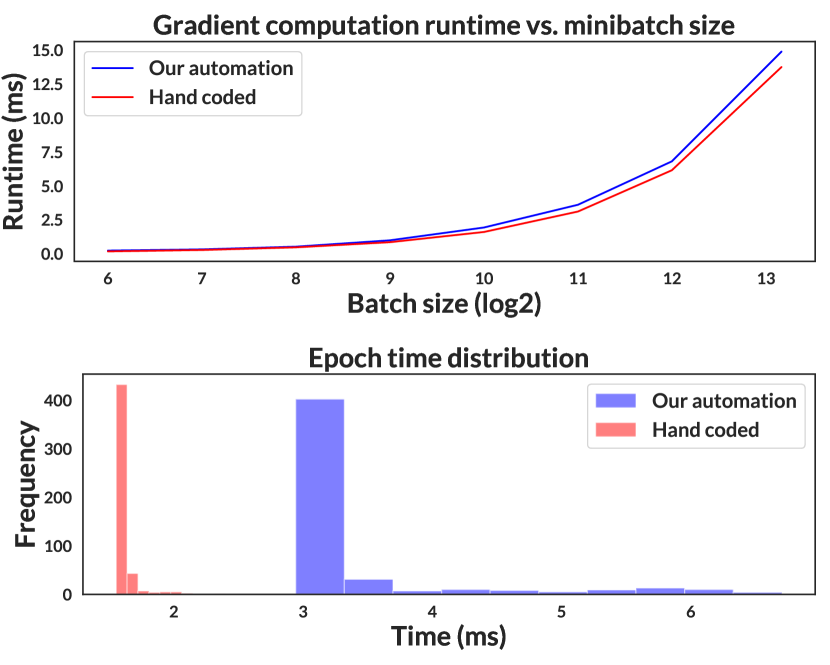

Table 1 presents a runtime comparison between genjax.vi and a hand-coded implementation of the gradient estimator in JAX (Appx. C). We measure the wall time required to compute a gradient estimate for different batch sizes . We find that our automation introduces a small amount of runtime overhead (around 3-10%) compared to our hand coded implementation (Fig. 11).

| Batch size | Ours | Hand coded |

| 64 | 0.11 0.02 | 0.09 0.04 |

| 128 | 0.22 0.2 | 0.16 0.08 |

| 256 | 0.31 0.18 | 0.29 0.17 |

| 512 | 0.56 0.35 | 0.54 0.34 |

| 1024 | 1.58 1.13 | 1.07 0.70 |

Overall Performance.

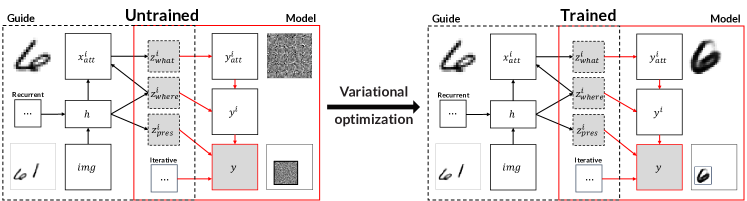

We consider the Attend, Infer, Repeat (Eslami et al., 2016) (AIR) model (Fig. 7). We plot accuracy and loss curves over time in Fig. 8, for several estimators expressed in our system and in Pyro. We also compare timing results, shown in Table 8. Our implementation’s performance is competitive, and we support a broader class of estimators and objectives than Pyro. We find that some estimators we support (in particular those based on measure-valued derivatives) lead to faster convergence than the estimators automated by Pyro.

AIR figure.

| System | Compiler | REINFORCE | ENUM | MVD | IWELBO + REINFORCE | IWELBO + MVD |

| genjax.vi | JAX (XLA) | 1.52 0.05 | 6.22 0.29 | 1.74 0.04 | 2.28 0.12 | 3.74 0.05 |

| pyro | Torch | 12.28 0.55 | 122.93 1.74 | X | 22.17 1.2 | X |

Expressivity and Compositional Correctness.

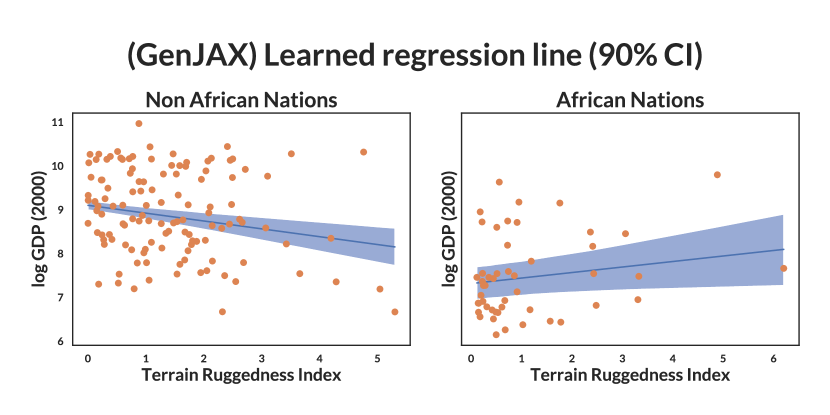

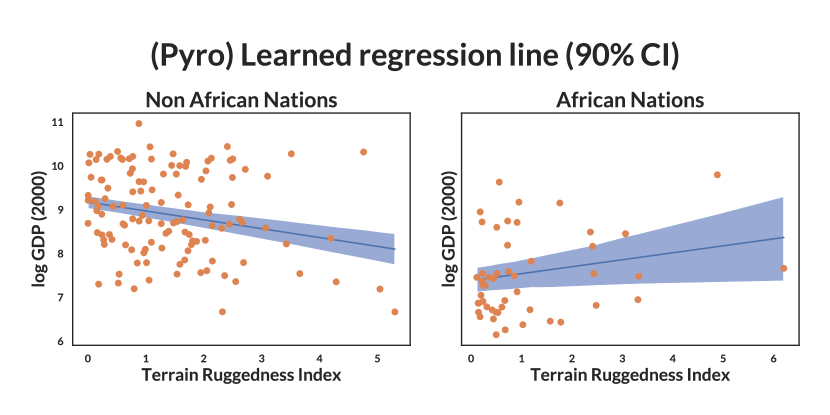

In Table 8, we enumerate several possible combinations of gradient estimation strategies and objectives for the AIR model. In Table 8, we consider the model shown in Fig. 2, and implement the model and naive variational guide in genjax.vi, Pyro and NumPyro, as well as the auxiliary variable variational guide in genjax.vi. We show statistics on final mean objective values for different variational objectives. While ELBO and IWELBO are standard, our system allows using more expressive approximations and tighter lower bound objectives compositionally (such as DIWHVI (Sobolev and Vetrov, 2019), which uses SIR to estimate densities of marginals, in the IWELBO objective) to achieve tighter variational bounds.

RE = REINFORCE estimator, EN = enumeration estimator, BL = REINFORCE with learned baselines, MV = measure-valued derivative estimator

Grad. Estimation Strategies

Objective

Batch

System

RE.

EN.

BL.

MV.

Pyro

Ours

ELBO

1

\cdashline5-8

IWAE

1

\cdashline5-8

\hdashline

ELBO

1

\cdashline5-8

IWAE

1

\cdashline5-8

\hdashline

ELBO

1

\cdashline5-8

IWAE

1

\cdashline5-8

\hdashline

ELBO

1

\cdashline5-8

IWAE

1

\cdashline5-8

\hdashline

ELBO

1

\cdashline5-8

IWAE

1

\cdashline5-8

\hdashline

ELBO

1

\cdashline5-8

IWAE

1

\cdashline5-8

\hdashline

ELBO

1

\cdashline5-8

IWAE

1

\cdashline5-8

\hdashline

ELBO

1

\cdashline5-8

IWAE

1

\cdashline5-8

\hdashline

ELBO

1

\cdashline5-8

IWAE

1

\cdashline5-8

\hdashline

ELBO

1

\cdashline5-8

IWAE

1

\cdashline5-8

\hdashline

ELBO

1

\cdashline5-8

IWAE

1

\cdashline5-8

\hdashline

ELBO

1

\cdashline5-8

IWAE

1

\cdashline5-8

\hdashline

ELBO

1

\cdashline5-8

IWAE

1

\cdashline5-8

\hdashline

ELBO

1

\cdashline5-8

IWAE

1

\cdashline5-8

\hdashline Not Exploited

RWS

1

\cdashline6-8

1

\cdashline6-8

![[Uncaptioned image]](/html/2406.15742/assets/x5.png) Figure 9. We evaluate a variety of custom estimators and objectives (ELBO, IWAE, RWS) using our system. Our on average best estimator (IWAE + MVD, not expressible in Pyro) converges an order of magnitude faster than Pyro’s recommended estimator.

Figure 9. We evaluate a variety of custom estimators and objectives (ELBO, IWAE, RWS) using our system. Our on average best estimator (IWAE + MVD, not expressible in Pyro) converges an order of magnitude faster than Pyro’s recommended estimator.

| System | ELBO | IWELBO () | HVI | IWHVI () | DIWHVI () |

| genjax.vi | -8.08 | -7.79 | -9.75 | -8.18 | -7.33 |

| numpyro | -8.08 | -7.77 | ✓/ X | X | X |

| pyro | -8.08 | -7.75 | ✓/ X | X | X |

9. Related work

Variational Inference in PPLs.

Many PPLs support some form of variational inference (Bingham et al., 2019; Stites et al., 2021; Carpenter et al., 2017; Ge et al., 2018; Cusumano-Towner et al., 2019), and it is the primary focus of Pyro (Bingham et al., 2019) and ProbTorch (Stites et al., 2021). Both Pyro and ProbTorch have endeavored to make inference more programmable. For example, ProbTorch has introduced inference combinators that make it easy to express certain nested variational inference algorithms (Zimmermann et al., 2021; Stites et al., 2021). Pyro has perhaps the most mature support for variational inference, with many gradient estimators and objectives supported. Pyro also implements some variance reduction strategies not yet supported by our system, e.g. exploiting conditional independence using their plate operator. However, extending Pyro with new variational objectives or gradient estimation strategies requires a deep understanding of its internals. Furthermore, Pyro’s modeling language does not have our constructs for marginalization and normalization (although Pyro can marginalize discrete, finite-support auxiliary variables from models). Concurrently with this work, Wagner (2023) presented a PPL with correct-by-construction variational inference, where their notion of “correctness” is stronger in some ways and weaker in others than that of this work. In particular, Wagner (2023) works with smoothed approximations of the user’s probabilistic programs, and so the gradient estimates it computes are biased for the original objective. However, the degree of error in this smoothing is gradually annealed over the course of optimization, leading to convergence to a stationary point of the original objective.

Static Analyses for Differentiability Criteria.

Within the PL community, researchers have made some progress toward formalizing and developing static analyses for ensuring soundness properties of variational inference (Lee et al., 2019, 2023; Wang et al., 2021), as well as program transformations for automatically constructing variational families informed by the model’s structure (Li et al., 2023b). By contrast, we formalize the process by which user model, inference, and objective code is transformed into a gradient estimator, tracking the interactions between density computation, simulation, and automatic differentiation. One interesting direction would be to extend Lee et al. (2023)’s analysis to automatically annotate programs with gradient estimators. Note that our current type-based analysis does not verify the local domination condition of Thm. 5.2, which Wagner (2023) does manage to check statically, by imposing restrictions on the PPL and considering only the ELBO objective.

Automated Gradient Estimation.

Due to its centrality to many applications in computer science and beyond, there has been intense interest in automating unbiased gradient estimation for objective functions expressed as expectations, yielding several frameworks for unbiasedly differentiating first-order stochastic computation graphs (Krieken et al., 2021; Schulman et al., 2015; Weber et al., 2019), imperative programs with discrete randomness (Arya et al., 2022), and higher-order probabilistic programs (Lew et al., 2023b). Some works have also investigated automated computation of biased gradient estimates via smoothing (Kreikemeyer and Andelfinger, 2023). However, these frameworks cannot be directly applied to variational inference problems, which require differentiating not just user code, but also traced simulators and log density evaluators of the probabilistic programs that users write. We address these challenges, by compiling density functions of user-defined probabilistic programs into a target language compatible with ADEV (Lew et al., 2023b). We also extend ADEV in several other ways: our version adds score to differentiate not just expected values but general integrals against (potentially unnormalized) measures; is implemented performantly on GPU; and has been extended with a reverse-mode.

Programmable Inference.

We build on a long line of work that aims to make inference more programmable in PPLs (Mansinghka et al., 2014, 2018; Narayanan et al., 2016; Cusumano-Towner et al., 2019; Lew et al., 2023a). In much the same way that this prior work has aimed to expose compositional structure in Monte Carlo algorithms and help users explore a broad class of algorithm settings, our work aims to do the same for variational inference, exposing compositional structure in gradient estimators and variational objectives.

Formal Reasoning about Inference and Program Transformations.

Our semantics builds on recent work in the denotational semantics and validation of Bayesian inference (Ścibior et al., 2017; Heunen et al., 2017; Ścibior et al., 2018), as well as semantic foundations for differentiable programming (Huot et al., 2020; Sherman et al., 2021). Our soundness proofs are based on logical relations (Ahmed, 2006; Huot et al., 2020). We also draw on a tradition of deriving probabilistic inference algorithms via program transformations (Narayanan et al., 2016).

10. Discussion

This work gives a formal account of the automation that PPLs provide for variational inference — a powerful and widely used suite of features that has not previously been completely understood in formal programming language terms. This work’s account provides a careful separation of the interactions between tracing, density computation, gradient estimation strategies, and automatic differentiation. Simultaneously, this work shows how to implement these features modularly and extensibly, addressing a number of pain points in existing implementations, and expanding the class of variational inference algorithms that users can easily express.

Limitations.

That said, the modular approach we have presented has several key limitations:

-

•

Static checks may be unnecessarily restrictive. For example, although the rectified linear unit (ReLU) is not differentiable at 0, in many (but not all) contexts it is safe to use it as though it were differentiable, without compromising unbiasedness. The type system of is not sophisticated enough to distinguish when ReLU is safe or not, and so we must give it the restrictive type . Of course, at their own risk, users of the system are free to ignore these static checks.

-

•

No parametric discontinuities. A key limitation of our language, shared by Pyro, ProbTorch, and Gen, is that parametric discontinuities (expressions that compute discontinuous functions of the input parameters) are not permitted. Variational inference is possible in these settings, and Lee et al. (2018) proposed a gradient estimator that can be automated for a restricted PPL with affine discontinuities. More recently, Bangaru et al. (2021) and Michel et al. (2024) have presented techniques for differentiating integral expressions with parametric discontinuities. It is not yet clear to what extent the design we present could be cleanly extended to exploit these techniques.

-

•

User-specified variational objectives may be ill-defined. Our correctness theorem assumes as a precondition that the objective the user has specified is well-defined (i.e., if it is defined as an expected value, that it is finite for all input parameters). Previous work has identified the verification of this condition as an important challenge for safe variational inference (Lee et al., 2019), but our system includes no static checks to do so.

-

•

Continuation-passing style (CPS) is unnatural in many host languages. transforms a program to CPS in order to automate unbiased gradient estimation. This is easy in our Haskell implementation, but in Python and Julia, it introduces some amount of friction. For example, in Julia, certain host-language features (like mutation, and therefore most imperative loops) are incompatible with our CPS implementation. By contrast, Pyro and Gen place few restrictions on the host-language features that can be used to define models and variational families.

In addition, our implementation does not yet incorporate several important insights and capabilities from existing deep PPLs, including Pyro’s use of tensor contractions to marginalize discrete variables (Obermeyer et al., 2019a, b), or the use of fine-grained control flow information to reduce the variance of gradient estimates (Schulman et al., 2015).

Future Work.

We comment on several intriguing avenues for future work:

-

•

The search for low variance estimators. Our approach automates the derivation of unbiased gradient estimators, but it says little about what estimators one should choose to achieve low variance on particular problems. Our approach should make it easier to address this challenge, by allowing rapid exploration of a large space of estimation strategies, some of which have not been previously automated. We hope that our work and implementations might be used to carry out a study of the behavior of different gradient estimators, on a broader variety of problems than those enabled by current automation.

-

•

Interaction with ADEV. Our system is the first to use ADEV (Lew et al., 2023b) for scalable learning of large parameter spaces (§A.4). ADEV provides a fundamentally new perspective on automatic differentiation, and extends the technique to expected value loss functions. Our integration with ADEV has several implications: by virtue of the fact that the target language of our language’s transformations is ADEV’s source language, our system may be used with ADEV loss functions beyond the variational loss functions which we’ve discussed in this work. Extensions to ADEV which improve variance properties of gradient estimators symbiotically improve the performance of gradient estimators in our language. Indeed, we expect new investigations into low variance gradient estimators for discrete random choices (Arya et al., 2022) to open up novel variational guide families, hitherto unexplored due to poor variance or computational intractability of discrete enumeration.

Data-Availability Statement

An artifact providing a version of genjax.vi, and reproducing our experiments, is available (Becker et al., 2024).

Acknowledgements.

The authors are grateful to Tuan Anh Le, Tan Zhi-Xuan, Cameron Freer, Andrew Bolton, George Matheos, Nishad Gothoskar, Martin Jankowiak, and Sam Witty for useful conversations and feedback, and to our anonymous referees for helpful feedback on earlier drafts of the paper. We are grateful for support from DARPA, under the DARPA Machine Common Sense (Award ID: 030523-00001) and JUMP (CoCoSys, Prime Contract No. 2023-JU-3131) programs, and DSTA, under Master Agreement No. 801899998, as well as gifts from Google, and philanthropic gifts from an anonymous donor and the Siegel Family Foundation.References

- (1)

- Agakov and Barber (2004) Felix V. Agakov and David Barber. 2004. An Auxiliary Variational Method. In Neural Information Processing (Lecture Notes in Computer Science). Springer, Berlin, Heidelberg, 561–566. https://doi.org/10.1007/978-3-540-30499-9_86

- Ahmed (2006) Amal Ahmed. 2006. Step-Indexed Syntactic Logical Relations for Recursive and Quantified Types. In Programming Languages and Systems (Lecture Notes in Computer Science). Springer, Berlin, Heidelberg, 69–83. https://doi.org/10.1007/11693024_6

- Arya et al. (2022) Gaurav Arya, Moritz Schauer, Frank Schäfer, and Christopher Rackauckas. 2022. Automatic Differentiation of Programs with Discrete Randomness. In Advances in Neural Information Processing Systems 35: Annual Conference on Neural Information Processing Systems 2022, NeurIPS 2022, New Orleans, LA, USA, November 28 - December 9, 2022, Sanmi Koyejo, S. Mohamed, A. Agarwal, Danielle Belgrave, K. Cho, and A. Oh (Eds.). http://papers.nips.cc/paper_files/paper/2022/hash/43d8e5fc816c692f342493331d5e98fc-Abstract-Conference.html

- Bangaru et al. (2021) Sai Praveen Bangaru, Jesse Michel, Kevin Mu, Gilbert Bernstein, Tzu-Mao Li, and Jonathan Ragan-Kelley. 2021. Systematically differentiating parametric discontinuities. ACM Trans. Graph. 40, 4 (2021), 107:1–107:18. https://doi.org/10.1145/3450626.3459775

- Becker et al. (2024) McCoy R. Becker, Alexander K. Lew, and Xiaoyan Wang. 2024. probcomp/programmable-vi-pldi-2024: v0.1.2. Zenodo. https://doi.org/10.5281/zenodo.10935596

- Bingham et al. (2019) Eli Bingham, Jonathan P. Chen, Martin Jankowiak, Fritz Obermeyer, Neeraj Pradhan, Theofanis Karaletsos, Rohit Singh, Paul A. Szerlip, Paul Horsfall, and Noah D. Goodman. 2019. Pyro: Deep Universal Probabilistic Programming. , 28:1–28:6 pages. http://jmlr.org/papers/v20/18-403.html

- Blei and Jordan (2006) David M Blei and Michael I Jordan. 2006. Variational inference for Dirichlet process mixtures. (2006).

- Blei et al. (2016) David M. Blei, Alp Kucukelbir, and Jon D. McAuliffe. 2016. Variational Inference: A Review for Statisticians. CoRR abs/1601.00670 (2016). arXiv:1601.00670 http://arxiv.org/abs/1601.00670

- Borgström et al. (2016) Johannes Borgström, Ugo Dal Lago, Andrew D Gordon, and Marcin Szymczak. 2016. A lambda-calculus foundation for universal probabilistic programming. ACM SIGPLAN Notices 51, 9 (2016), 33–46.

- Bornschein and Bengio (2015) Jörg Bornschein and Yoshua Bengio. 2015. Reweighted Wake-Sleep. https://doi.org/10.48550/arXiv.1406.2751 arXiv:1406.2751 [cs].

- Burda et al. (2016) Yuri Burda, Roger Grosse, and Ruslan Salakhutdinov. 2016. Importance Weighted Autoencoders. https://doi.org/10.48550/arXiv.1509.00519 arXiv:1509.00519 [cs, stat].

- Carpenter et al. (2017) Bob Carpenter, Andrew Gelman, Matthew D Hoffman, Daniel Lee, Ben Goodrich, Michael Betancourt, Marcus A Brubaker, Jiqiang Guo, Peter Li, and Allen Riddell. 2017. Stan: A probabilistic programming language. Journal of Statistical Software 76 (2017).

- Cusumano-Towner and Mansinghka (2017) Marco Cusumano-Towner and Vikash K Mansinghka. 2017. AIDE: An algorithm for measuring the accuracy of probabilistic inference algorithms. In Advances in Neural Information Processing Systems, Vol. 30. Curran Associates, Inc. https://proceedings.neurips.cc/paper/2017/hash/acab0116c354964a558e65bdd07ff047-Abstract.html

- Cusumano-Towner et al. (2019) Marco F. Cusumano-Towner, Feras A. Saad, Alexander K. Lew, and Vikash K. Mansinghka. 2019. Gen: a general-purpose probabilistic programming system with programmable inference. In Proceedings of the 40th ACM SIGPLAN Conference on Programming Language Design and Implementation (PLDI 2019). Association for Computing Machinery, New York, NY, USA, 221–236. https://doi.org/10.1145/3314221.3314642

- Dempster et al. (1977) A. P. Dempster, N. M. Laird, and D. B. Rubin. 1977. Maximum Likelihood from Incomplete Data via the EM Algorithm. Journal of the Royal Statistical Society. Series B (Methodological) 39, 1 (1977), 1–38. https://www.jstor.org/stable/2984875 Publisher: [Royal Statistical Society, Wiley].

- Domke (2021) Justin Domke. 2021. An Easy to Interpret Diagnostic for Approximate Inference: Symmetric Divergence Over Simulations. https://doi.org/10.48550/arXiv.2103.01030 arXiv:2103.01030 [cs, stat].

- Eslami et al. (2016) S. M. Ali Eslami, Nicolas Heess, Theophane Weber, Yuval Tassa, David Szepesvari, Koray Kavukcuoglu, and Geoffrey E. Hinton. 2016. Attend, Infer, Repeat: Fast Scene Understanding with Generative Models. https://doi.org/10.48550/arXiv.1603.08575 arXiv:1603.08575 [cs].

- Foerster et al. (2018) Jakob Foerster, Gregory Farquhar, Maruan Al-Shedivat, Tim Rocktäschel, Eric Xing, and Shimon Whiteson. 2018. Dice: The infinitely differentiable Monte Carlo estimator. In International Conference on Machine Learning. PMLR, 1529–1538.

- Fox and Roberts (2012) Charles W Fox and Stephen J Roberts. 2012. A tutorial on variational Bayesian inference. Artificial intelligence review 38 (2012), 85–95.

- Frostig et al. (2018) Roy Frostig, Matthew James Johnson, and Chris Leary. 2018. Compiling machine learning programs via high-level tracing. Systems for Machine Learning 4, 9 (2018).

- Ge et al. (2018) Hong Ge, Kai Xu, and Zoubin Ghahramani. 2018. Turing: a language for flexible probabilistic inference. In International conference on artificial intelligence and statistics. PMLR, 1682–1690.

- Gu et al. (2015) Shixiang (Shane) Gu, Zoubin Ghahramani, and Richard E Turner. 2015. Neural Adaptive Sequential Monte Carlo. In Advances in Neural Information Processing Systems, Vol. 28. Curran Associates, Inc. https://papers.nips.cc/paper_files/paper/2015/hash/99adff456950dd9629a5260c4de21858-Abstract.html

- Heunen et al. (2017) Chris Heunen, Ohad Kammar, Sam Staton, and Hongseok Yang. 2017. A convenient category for higher-order probability theory. In Proceedings of the 32nd Annual ACM/IEEE Symposium on Logic in Computer Science (LICS ’17). IEEE Press, Reykjavík, Iceland, 1–12.

- Hinton et al. (1995) Geoffrey E. Hinton, Peter Dayan, Brendan J. Frey, and Radford M. Neal. 1995. The ”Wake-Sleep” Algorithm for Unsupervised Neural Networks. Science 268, 5214 (May 1995), 1158–1161. https://doi.org/10.1126/science.7761831

- Hoffman et al. (2013) Matthew D Hoffman, David M Blei, Chong Wang, and John Paisley. 2013. Stochastic variational inference. Journal of Machine Learning Research (2013).

- Huot et al. (2020) Mathieu Huot, Sam Staton, and Matthijs Vákár. 2020. Correctness of Automatic Differentiation via Diffeologies and Categorical Gluing. In Foundations of Software Science and Computation Structures (Lecture Notes in Computer Science). Springer International Publishing, Cham, 319–338. https://doi.org/10.1007/978-3-030-45231-5_17

- Kingma et al. (2021) Diederik Kingma, Tim Salimans, Ben Poole, and Jonathan Ho. 2021. Variational diffusion models. Advances in Neural Information Processing Systems 34 (2021), 21696–21707.

- Kingma et al. (2014) Diederik P. Kingma, Danilo J. Rezende, Shakir Mohamed, and Max Welling. 2014. Semi-supervised learning with deep generative models. In Proceedings of the 27th International Conference on Neural Information Processing Systems - Volume 2 (NIPS’14). MIT Press, Cambridge, MA, USA, 3581–3589.

- Kingma and Welling (2022) Diederik P. Kingma and Max Welling. 2022. Auto-Encoding Variational Bayes. https://doi.org/10.48550/arXiv.1312.6114 arXiv:1312.6114 [cs, stat].

- Kreikemeyer and Andelfinger (2023) Justin N Kreikemeyer and Philipp Andelfinger. 2023. Smoothing Methods for Automatic Differentiation Across Conditional Branches. IEEE Access (2023).

- Krieken et al. (2021) Emile Krieken, Jakub Tomczak, and Annette Ten Teije. 2021. Storchastic: A framework for general stochastic automatic differentiation. Advances in Neural Information Processing Systems 34 (2021), 7574–7587.

- Kucukelbir et al. (2017) Alp Kucukelbir, Dustin Tran, Rajesh Ranganath, Andrew Gelman, and David M Blei. 2017. Automatic differentiation variational inference. Journal of machine learning research (2017).

- Le et al. (2019) Tuan Anh Le, Adam R. Kosiorek, N. Siddharth, Yee Whye Teh, and Frank Wood. 2019. Revisiting Reweighted Wake-Sleep for Models with Stochastic Control Flow. , 1039–1049 pages. http://proceedings.mlr.press/v115/le20a.html

- Lee et al. (2023) Wonyeol Lee, Xavier Rival, and Hongseok Yang. 2023. Smoothness Analysis for Probabilistic Programs with Application to Optimised Variational Inference. Proceedings of the ACM on Programming Languages 7, POPL (Jan. 2023), 12:335–12:366. https://doi.org/10.1145/3571205

- Lee et al. (2019) Wonyeol Lee, Hangyeol Yu, Xavier Rival, and Hongseok Yang. 2019. Towards verified stochastic variational inference for probabilistic programs. Proceedings of the ACM on Programming Languages 4, POPL (Dec. 2019), 16:1–16:33. https://doi.org/10.1145/3371084

- Lee et al. (2018) Wonyeol Lee, Hangyeol Yu, and Hongseok Yang. 2018. Reparameterization gradient for non-differentiable models. Advances in Neural Information Processing Systems 31 (2018).

- Lew et al. (2022) Alexander K. Lew, Marco F. Cusumano-Towner, and Vikash K. Mansinghka. 2022. Recursive Monte Carlo and variational inference with auxiliary variables. In Uncertainty in Artificial Intelligence, Proceedings of the Thirty-Eighth Conference on Uncertainty in Artificial Intelligence, UAI 2022, 1-5 August 2022, Eindhoven, The Netherlands (Proceedings of Machine Learning Research, Vol. 180). PMLR, 1096–1106. https://proceedings.mlr.press/v180/lew22a.html

- Lew et al. (2019) Alexander K Lew, Marco F Cusumano-Towner, Benjamin Sherman, Michael Carbin, and Vikash K Mansinghka. 2019. Trace types and denotational semantics for sound programmable inference in probabilistic languages. Proceedings of the ACM on Programming Languages 4, POPL (2019), 1–32.

- Lew et al. (2023a) Alexander K. Lew, Matin Ghavamizadeh, Martin C. Rinard, and Vikash K. Mansinghka. 2023a. Probabilistic Programming with Stochastic Probabilities. Proceedings of the ACM on Programming Languages 7, PLDI (June 2023), 176:1708–176:1732. https://doi.org/10.1145/3591290

- Lew et al. (2023b) Alexander K. Lew, Mathieu Huot, Sam Staton, and Vikash K. Mansinghka. 2023b. ADEV: Sound Automatic Differentiation of Expected Values of Probabilistic Programs. Proceedings of the ACM on Programming Languages 7, POPL (Jan. 2023), 121–153. https://doi.org/10.1145/3571198 arXiv:2212.06386 [cs, stat].

- Li et al. (2023b) Jianlin Li, Leni Ven, Pengyuan Shi, and Yizhou Zhang. 2023b. Type-preserving, dependence-aware guide generation for sound, effective amortized probabilistic inference. Proceedings of the ACM on Programming Languages 7, POPL (2023), 1454–1482.

- Li et al. (2023a) Michael Y. Li, Dieterich Lawson, and Scott Linderman. 2023a. Neural Adaptive Smoothing via Twisting. https://openreview.net/forum?id=rC6-kGN-0v

- Lundén et al. (2021) Daniel Lundén, Johannes Borgström, and David Broman. 2021. Correctness of Sequential Monte Carlo Inference for Probabilistic Programming Languages.. In ESOP. 404–431.

- Maaløe et al. (2016) Lars Maaløe, Casper Kaae Sønderby, Søren Kaae Sønderby, and Ole Winther. 2016. Auxiliary Deep Generative Models. In Proceedings of The 33rd International Conference on Machine Learning. PMLR, 1445–1453. https://proceedings.mlr.press/v48/maaloe16.html ISSN: 1938-7228.

- Maddison et al. (2017) Chris J. Maddison, Dieterich Lawson, George Tucker, Nicolas Heess, Mohammad Norouzi, Andriy Mnih, Arnaud Doucet, and Yee Whye Teh. 2017. Filtering Variational Objectives. https://doi.org/10.48550/arXiv.1705.09279 arXiv:1705.09279 [cs, stat].

- Malkin et al. (2022) Nikolay Malkin, Salem Lahlou, Tristan Deleu, Xu Ji, Edward Hu, Katie Everett, Dinghuai Zhang, and Yoshua Bengio. 2022. GFlowNets and variational inference. arXiv preprint arXiv:2210.00580 (2022).

- Mansinghka et al. (2014) Vikash Mansinghka, Daniel Selsam, and Yura Perov. 2014. Venture: a higher-order probabilistic programming platform with programmable inference. arXiv preprint arXiv:1404.0099 (2014).

- Mansinghka et al. (2018) Vikash K Mansinghka, Ulrich Schaechtle, Shivam Handa, Alexey Radul, Yutian Chen, and Martin Rinard. 2018. Probabilistic programming with programmable inference. In Proceedings of the 39th ACM SIGPLAN Conference on Programming Language Design and Implementation. 603–616.

- Michel et al. (2024) Jesse Michel, Kevin Mu, Xuanda Yang, Sai Praveen Bangaru, Elias Rojas Collins, Gilbert Bernstein, Jonathan Ragan-Kelley, Michael Carbin, and Tzu-Mao Li. 2024. Distributions for Compositionally Differentiating Parametric Discontinuities. Proceedings of the ACM on Programming Languages 8, OOPSLA1 (2024), 893–922.

- Mohamed et al. (2020) Shakir Mohamed, Mihaela Rosca, Michael Figurnov, and Andriy Mnih. 2020. Monte Carlo gradient estimation in machine learning. Journal of Machine Learning Research 21, 132 (2020), 1–62.

- Naesseth et al. (2018) Christian Naesseth, Scott Linderman, Rajesh Ranganath, and David Blei. 2018. Variational sequential Monte Carlo. In International conference on artificial intelligence and statistics. PMLR, 968–977.

- Naesseth et al. (2020) Christian A. Naesseth, Fredrik Lindsten, and David Blei. 2020. Markovian score climbing: variational inference with KL(p||q). In Proceedings of the 34th International Conference on Neural Information Processing Systems (NIPS’20). Curran Associates Inc., Red Hook, NY, USA, 15499–15510.

- Naesseth et al. (2019) Christian A Naesseth, Fredrik Lindsten, Thomas B Schön, et al. 2019. Elements of sequential Monte Carlo. Foundations and Trends® in Machine Learning 12, 3 (2019), 307–392.

- Narayanan et al. (2016) Praveen Narayanan, Jacques Carette, Wren Romano, Chung-chieh Shan, and Robert Zinkov. 2016. Probabilistic inference by program transformation in Hakaru (system description). In Functional and Logic Programming: 13th International Symposium, FLOPS 2016, Kochi, Japan, March 4-6, 2016, Proceedings 13. Springer, 62–79.

- Obermeyer et al. (2019a) Fritz Obermeyer, Eli Bingham, Martin Jankowiak, Du Phan, and Jonathan P Chen. 2019a. Functional tensors for probabilistic programming. arXiv preprint arXiv:1910.10775 (2019).

- Obermeyer et al. (2019b) Fritz Obermeyer, Eli Bingham, Martin Jankowiak, Neeraj Pradhan, Justin Chiu, Alexander Rush, and Noah Goodman. 2019b. Tensor variable elimination for plated factor graphs. In International Conference on Machine Learning. PMLR, 4871–4880.

- Pu et al. (2016) Yunchen Pu, Zhe Gan, Ricardo Henao, Xin Yuan, Chunyuan Li, Andrew Stevens, and Lawrence Carin. 2016. Variational autoencoder for deep learning of images, labels and captions. Advances in Neural Information Processing Systems 29 (2016).

- Radul et al. (2022) Alexey Radul, Adam Paszke, Roy Frostig, Matthew Johnson, and Dougal Maclaurin. 2022. You only linearize once: Tangents transpose to gradients. arXiv preprint arXiv:2204.10923 (2022).

- Rainforth et al. (2018) Tom Rainforth, Adam R. Kosiorek, Tuan Anh Le, Chris J. Maddison, Maximilian Igl, Frank Wood, and Yee Whye Teh. 2018. Tighter Variational Bounds are Not Necessarily Better. https://arxiv.org/abs/1802.04537v3

- Ranganath et al. (2016) Rajesh Ranganath, Dustin Tran, and David Blei. 2016. Hierarchical Variational Models. In Proceedings of The 33rd International Conference on Machine Learning. PMLR, 324–333. https://proceedings.mlr.press/v48/ranganath16.html ISSN: 1938-7228.