MS-0001-1922.65

Liao and Kroer

Statistical Inference in Market Equilibrium

Statistical Inference and A/B Testing in Fisher Markets and Paced Auctions

Luofeng Liao \AFFDepartment of Industrial Engineering and Operations Research, Columbia University, \EMAILll3530@columbia.edu \AUTHORChristian Kroer \AFFDepartment of Industrial Engineering and Operations Research, Columbia University, \EMAILck2945@columbia.edu

We initiate the study of statistical inference and A/B testing for two market equilibrium models: linear Fisher market (LFM) equilibrium and first-price pacing equilibrium (FPPE). LFM arises from fair resource allocation systems such as allocation of food to food banks and notification opportunities to different types of notifications. For LFM, we assume that the data observed is captured by the classical finite-dimensional Fisher market equilibrium, and its steady-state behavior is modeled by a continuous limit Fisher market. The second type of equilibrium we study, FPPE, arises from internet advertising where advertisers are constrained by budgets and advertising opportunities are sold via first-price auctions. For platforms that use pacing-based methods to smooth out the spending of advertisers, FPPE provides a hindsight-optimal configuration of the pacing method. We propose a statistical framework for the FPPE model, in which a continuous limit FPPE models the steady-state behavior of the auction platform, and a finite FPPE provides the data to estimate primitives of the limit FPPE. Both LFM and FPPE have an Eisenberg-Gale convex program characterization, the pillar upon which we derive our statistical theory. We start by deriving basic convergence results for the finite market to the limit market. We then derive asymptotic distributions, and construct confidence intervals. Furthermore, we establish the asymptotic local minimax optimality of estimation based on finite markets. We then show that the theory can be used for conducting statistically valid A/B testing on auction platforms. Synthetic and semi-synthetic experiments verify the validity and practicality of our theory.

first-price auctions, Fisher market equilibrium, statistical inference, A/B testing

1 Introduction

Statistical inference is a crucial tool for measuring and improving a variety of real-world systems with multiple agents, including large-scale systems such as internet advertising platforms and resource allocation systems. However, statistical interference is a crucial issue in such systems. Past work has often focus on interference such as networks effects, which may arise due to user interactions on social media platforms. In this paper, we focus on a different type of interference: interference effects arising from competition between agents on a platform. To be concrete, consider the case of A/B testing for internet advertising: budgets are prevalent among advertisers on such platforms, and these budgets mean that the actions of one advertiser can affect the actions of another. Often, in such systems, randomization is performed e.g. at the user level and then budget-splitting is used to clone advertisers into the A and B treatment. However, budget interactions may cause all users in e.g. the A or B treatment to be related to each other, and thus it is not at all clear that one can apply standard statistical methods that treat each user as an independent sample. Instead, a theory of equilibrium interference is needed, and we need to understand how statistical interference can be performed when such interference is present. We study statistical inference and A/B testing in two related equilibrium models: First, we study one of the most classical competitive equilibrium models: the linear Fisher market (LFM) equilibrium. Second, we study the first-price pacing equilibrium (FPPE), which is a model that captures the budget-management tools often employed on internet advertising platforms.

In a Fisher market, there is a set of budget-constrained buyers that are interested in buying goods from a seller. A market equilibrium (ME) is an allocation of the goods and a corresponding set of prices on the goods such that the market clears, meaning that demand equals supply. In a linear Fisher market, a buyers’ utility is linear in their allocation. Beyond being a classical model of price formation, the Fisher market equilibrium arises in resource allocation systems via the the competitive equilibrium from equal incomes (CEEI) mechanism (Varian 1974, Budish 2011). In CEEI, each individual is given an endowment of faux currency and reports her valuation for the goods; then, a market equilibrium is computed, and the goods are allocated accordingly. The resulting allocation has many desirable properties such as Pareto optimality, envy-freeness and proportionality. Below we list three examples of allocation systems where a Fisher market equilibrium naturally arises.

Example 1.1 (Allocation of resources)

Scarce resource allocation is prevalent in real life. In systems that assign blood donation to hospitals and blood banks (McElfresh et al. 2023), or donated food to charities in different sectors of community (Aleksandrov et al. 2015, Sinclair et al. 2022), scarce compute resources to users (Ghodsi et al. 2011, Parkes et al. 2015, Kash et al. 2014, Devanur et al. 2018), course seats to students (Othman et al. 2010, Budish et al. 2016), the CEEI mechanism is already in use or serves as a fair and efficient alternative. For systems that implement CEEI, we may be interested in quantifying the variability of the amount of resources (blood or food donation) received by the participants (hospitals or charities) of these systems as well as the variability of fairness and efficiency metrics of interest in the long run. Enabling statistical inference in such systems enables better tools for both evaluating and improving these systems.

Example 1.2 (Fair notification allocation)

In certain social media mobile apps, users are notified of events such as other users liking or commenting on their posts. Notifications are important for increasing user engagement, but too many notifications can be disruptive for users. Moreover, in practice, different types of notification are managed by distinct teams, competing for the chances to push their notifications to users. Kroer et al. (2023a) propose to use Fisher markets to fairly control allocation of notifications. They treat notification types as buyers, and users as items in a Fisher market. Platforms are often interested in measuring outcome properties of such notification systems. In Section 6.2 we will present a simulation study of our uncertainty quantification methods applied to the notification allocation problem.

The second type of equilibrium model we study is the FPPE model, which arises in internet advertising. First, we review how impressions are sold in internet advertising, where first or second-price auction generalizations are used. When a user shows up on a platform, an auction is run in order to determine which ads to show, before the page is returned to the user. Such an auction must run extremely fast. This is typically achieved by having each advertiser specify the following ahead of time: their target audience, their willingness-to-pay for an impression (or values per click, which are then multiplied by platform-supplied click-through-rate estimates), and a budget. Then, the bidding for individual impressions is managed by a proxy bidder controlled by the platform. As a concrete example, to create an ad campaign on Meta Ads Manager, advertisers need to specify the following parameters: (1) the conversion location (how do you want people to reach out to you, via say website, apps, Messenger and so on), (2) optimization and delivery (target your ads to users with specific behavior patterns, such as those who are more likely to view the ad or click the ad link), (3) audience (age, gender, demographics, interests and behaviors), and (4) how much money do you want to spend (budget). Given the above parameters reported by the advertiser, the (algorithmic) proxy bidder supplied by the platform is then responsible for bidding in individual auctions to maximize advertiser utility, while respecting the budget constraint.

An important role of these proxy bidders is to ensure smooth spending of budgets. Two prevalent budget management methods are throttling and pacing. Throttling tries to enforce budget constraints by adaptively selecting which auctions the advertiser should participate in. Pacing, on the other hand, modifies the advertiser’s bids by applying a shading factor, referred to as a (multiplicative) pacing multiplier. Tuning the pacing multiplier changes the spending rate: the larger the pacing multiplier, the more aggressive the bids. The goal of the proxy bidder is to choose this pacing multiplier such that the advertiser exactly exhausts their budget (or alternatively use a multiplier of one in the case where their budget is not exhausted by using unmodified bids). In this paper we focus on pacing-based budget management systems.

First-price pacing equilibrium (Conitzer et al. 2022a) is a market-equilibrium-like model that captures the steady-state outcome of a system where all buyers employ a proxy bidder that uses multiplicative pacing. Conitzer et al. (2022a) showed that an FPPE always exists and is unique. Moreover, as a pacing configuration method, FPPE enjoys lots of nice properties such as being revenue-maximizing among all budget-feasible pacing strategies, shill-proof (the platform does not benefit from adding fake bids under first-price auction mechanism) and revenue-monotone (revenue weakly increases when adding bidders, items or budget). The FPPE model specifically captures the setting where each auction is a first-price auction. First and second-price auctions are both prevalent in practice, but equilibrium models for second-price auctions are much less tractable (in fact, even finding one is computationally hard (Chen et al. 2023)). To that end, we focus on the first-price auction setting in this paper; the second-price setting is interesting, but we expect that it will be much harder to give satisfying statistical inference results for it.

Quantifying uncertainty in FPPE system is important for online advertising business. Basic statistical tasks, such as the prediction of bidding behavior of advertisers and revenue of the whole platform require a statistical theory to model the intricacies of the bidding process. A/B testing, a method that seeks to understand the effect of rolling out a new feature, also requires a rigorous theoretical treatment to handle the equilibrium effect. To the best of our knowledge, our results are the first to provide a statistical theory that captures the competitive interference effects due to budgets that one would expect on an internet advertising platform.

Although LFM and FPPE have vastly different use cases, each of them has an Eisenberg-Gale convex program characterization (Eisenberg and Gale 1959, Eisenberg 1961). This is the unifying theme that allows us to study these two models using similar tools. In particular, this allows us to reduce inference about market equilibrium to inference about stochastic programs, where many classical tools from mathematical programming (Shapiro et al. 2021) and empirical processes theory (Vaart and Wellner 1996) can be applied.

1.1 Contributions

Statistical models for resource allocation systems and first-price pacing auction platforms.

We leverage the infinite-dimensional Fisher market model of Gao and Kroer (2022) in order to propose a statistical model for resource allocation systems and first-price pacing auction platforms. In this model, we observe market equilibria formed with a finite number of items that are i.i.d. draws from some distribution, and aim to make inferences about several primitives of the limit market, such as revenue, Nash social welfare (a fair metric of efficiency), and other quantities of interest; see Table 1. Importantly, this lays the theoretical foundation for A/B testing in resource allocation systems and auction markets, which is a difficult statistical problem because buyers interfere with each other through the supply and the budget constraints. With the presence of equilibrium effects, traditional statistical approaches which rely on the i.i.d. assumption or SUTVA (stable unit treatment value assumption, Imbens and Rubin (2015)) fail. The key lever we use to approach this problem is a convex program characterization of the equilibria, called the Eisenberg-Gale (EG) program. With the EG program, the inference problem reduces to an -estimation problem (Shapiro et al. 2021, Van der Vaart 2000) on a constrained non-smooth convex optimization problem.

| FPPE | LFM |

| pacing multipliers revenue | inverse bang-per-bucks utilities Nash social welfare |

Convergence and inference results for LFM and FPPE.

We show that the finite market, which represents the observed data, is a good estimator for the limit market by showing a hierarchy of results: strong consistency, convergence rates, and asymptotic normality. We also establish that the observed market is an optimal estimator of the limit market in the asymptotic local minimax sense (Van der Vaart 2000, Le Cam et al. 2000, Duchi and Ruan 2021). Finally, we provide consistent variance estimators, whose consistency is proved by a uniform law-of-large-numbers over certain function classes. A common challenge for developing statistical theory for both LFM and FPPE is nonsmoothness. The objective function in the EG convex program is non-differentiable almost surely as it involves the max operator (cf. Eq. 1). For FPPE, there is a more prominent issue: the parameter-on-boundary issue, which means that the optimal population solution might be on the boundary of the constraint set. Here we briefly discuss how we handle the two issues when deriving asymptotic distribution results for FPPE, which is one of the more difficult results in the paper. First, asymptotic distribution results for M estimation are known to hold under certain regularity conditions on stochastic programs (Shapiro 1989, Theorem 3.3). One such condition is about the differentiability of the population objective. We provide low-level sufficient conditions for differentiability, and show they have natural interpretations from an economic perspective (Section 3). Another important condition to verify is stochastic equicontinuity (Cond. 12.2.c), which we establish by leveraging empirical process theory (Vaart and Wellner 1996, Kosorok 2008).

Statistically reliable A/B testing in resource allocation systems and FPPE platforms.

Applying our theory, we develop an A/B testing design for item-side randomization that resembles practical A/B testing methodology. In the proposed design, treatment and control markets are formed independently, and buyer’s budgets are split proportionally between them, while items are randomly assigned to treatment or control markets. Then, based on the equilibrium outcomes, we construct estimators and confidence intervals that enable statistical inference.

1.2 Related Works

A/B testing in two-sided markets. Empirical studies by Blake and Coey (2014), Fradkin (2019) demonstrate bias in experiments due to marketplace interference. Basse et al. (2016) study the bias and variance of treatment effects under two randomization schemes for auction experiments. Bojinov and Shephard (2019) study the estimation of causal quantities in time series experiments. Some recent state-of-the-art designs are the multiple randomization designs (Liu et al. 2021b, Johari et al. 2022, Bajari et al. 2021) and the switch-back designs (Sneider et al. 2018, Hu and Wager 2022, Li et al. 2022, Bojinov et al. 2022, Glynn et al. 2020). The surveys by Kohavi and Thomke (2017), Bojinov and Gupta (2022) contain detailed accounts of A/B testing in internet markets. See Larsen et al. (2022) for an extensive survey on statistical challenges in A/B testing. Compared to these papers, our paper is the first to focus on A/B testing with equilibrium effects.

Pacing equilibrium. Pacing and throttling are two prevalent budget-management methods on ad auction platforms. Here we focus on pacing methods since that is our setting. In the first-price setting, Borgs et al. (2007) study first price auctions with budget constraints in a perturbed model, whose limit prices converge to those of an FPPE. Building on the work of Borgs et al. (2007), Conitzer et al. (2022a) introduce the FPPE model and discover several properties of FPPE such as shill-proofness and monotonicity in buyers, budgets and goods. There it is also established that FPPE is closely related to the quasilinear Fisher market equilibrium (Chen et al. 2007, Cole et al. 2017). Gao and Kroer (2022) propose an infinite-dimensional variant of the quasilinear Fisher market, which lays the probability foundation of the current paper. Gao et al. (2021), Liao et al. (2022) study online computation of the infinite-dimensional Fisher market equilibrium. In the second-price setting, Balseiro et al. (2015) investigate budget-management in second-price auctions through a fluid mean-field approximation; Balseiro and Gur (2019) study adaptive pacing strategy from buyers’ perspective in a stochastic continuous setting; Balseiro et al. (2021) study several budget smoothing methods including multiplicative pacing in a stochastic context; Conitzer et al. (2022b) study second price pacing equilibrium, and shows that the equilibria exist under fractional allocations.

-estimation when the parameter is on the boundary There is a long literature on the statistical properties of -estimators when the parameter is on the boundary (Geyer 1994, Shapiro 1990, 1988, 1989, 1991, 1993, 2000, Andrews 1999, 2001, Knight 1999, 2001, 2006, 2010, Dupacová and Wets 1988, Dupačová 1991, Self and Liang 1987). Some recent works on the statistical inference theory for constrained -estimation include Li (2022), Hong and Li (2020), Hsieh et al. (2022). Our work leverages Shapiro (1989), which develops a general set of conditions for central limit theorems (CLT) of constrained -estimators when the objective function is nonsmooth. Working under the specific model of FPPE, we build on and go beyond these contributions by deriving sufficient condition for asymptotic normality in FPPE, establishing local asymptotic minimax theory and developing valid inferential procedures.

Statistical learning and inference with equilibrium effects Wager and Xu (2021), Munro et al. (2023), Sahoo and Wager (2022) take a mean-field game modeling approach and perform policy learning with a gradient descent method.

Statistical learning and inference has been investigated for other equilibrium models, such as general exchange economy (Guo et al. 2021, Liu et al. 2022) and matching markets (Cen and Shah 2022, Dai and Jordan 2021, Liu et al. 2021a, Jagadeesan et al. 2021, Min et al. 2022). Our work is also related to the rich literature of inference under interference (Hudgens and Halloran 2008, Aronow and Samii 2017, Athey et al. 2018, Leung 2020, Hu et al. 2022, Li and Wager 2022). In the FPPE model, the interference among buyers is caused by the supply and budget constraint and the revenue-maximizing incentive of the platform. In the economic literature, researchers have studied how to estimate auction market primitives from bid data; see Athey and Haile (2007) for a survey.

Closely related to our work is the one by Munro et al. (2023), and we discuss it here. They consider a potential outcome framework where the outcome of an agent depends on the treatments of all agents, but only through the equilibrium price. The equilibrium price is attained by a market clearance condition. Although both their work and our work consider a mean-field market equilibrium, there are differences. First, Munro et al. (2023) send the number of agents to infinity while we consider the asymptotics where the number of items grows. Second, Munro et al. (2023) present a rather general market equilibrium framework that requires abstract regularity conditions, while we focus on equilibria arising from resource allocation systems and auction pacing systems, and consequently we are able to present low-level conditions that facilitate statistical inference.

This paper builds upon two preliminary papers (Liao et al. 2023, Liao and Kroer 2023). This paper gives a more unified presentation, and provides some additional results on the statistical theory of Fisher markets and FPPE. Perhaps most importantly, this paper conducts two semisynthetic experiments based on an ad auction dataset (Liao et al. 2014) and an Instagram notification dataset (Kroer et al. 2023b), demonstrating the practicality of the proposed theory. This paper also provides strong consistency and convergence rate for FPPE, minimax optimality results for LFM, and a novel closed-form expression for the Hessian matrix of the population EG objective (Eq. 2) using results from differential geometry (Kim and Pollard 1990). Building on the preliminary versions of the present paper, Liao and Kroer (2023) extends the FPPE statistical theory to the cases where degenerate buyers are present and develops bootstrap inference methods.

1.3 Notations

Let be the -th basis vector in . Furthermore, we let be the Moore-Penrose pseudo inverse of a matrix .

Let denote the Lebesgue measure in . For a measurable space , we let (and , resp.) denote the set of (nonnegative, resp.) functions on w.r.t the integrating measure for any (including ). We treat all functions that agree on all but a measure-zero set as the same. For a sequence of random variables , we say if for any there exists a finite and a finite such that for all . We say if converges to zero in probability. We say (resp. ) if (resp. ). The subscript is for indexing buyers and superscript is for items.

2 Linear Fisher Market and First-Price Pacing Equilibrium

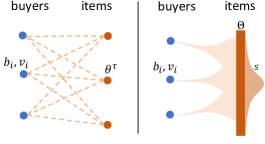

In this section we introduce the Fisher market equilibrium and the first-price pacing equilibrium, and review their properties. We start by presenting components that are common to both models, and then introduce each equilibrium concept. In both LFM and FPPE, we have a set of buyers and a set of items, and the goal is to find market-clearing prices for the items. The items are represented by a set , a compact set with . Clearly the measure sapce is atomless.

Both LFM and FPPE require the following elements; see Figure 1 for an illustration.

-

•

The budget of buyer . Let .

-

•

The valuation for buyer is a function . Buyer has valuation (per unit supply) of item . Let , . We assume . Also let be the monopolistic utility of buyer , and .

-

•

The supplies of items are given by a function , i.e., item has units of supply. Without loss of generality, we assume a unit total supply , which makes a probability measure. Let denote the probability measure induced by , i.e., for a measurable set . Given , we let and . Given i.i.d. draws from , let . Let .

Equilibria in both LFM and FPPE are characterized by a particular type of convex program known as an Eisenberg-Gale (EG) convex program. For statistical inference purposes, we will focus on the duals of these EG programs, which is a convex optimization problem over the space of pacing multipliers (these pacing multipliers turn out to represent the price-per-utility of buyers in equilibrium). In both cases, the dual EG objective separates into per-item convex terms

| (1) |

and the population and sample EG objectives are

| (2) |

The reason we focus on the duals is that they can be cast as sample average approximations of the limit convex programs. This interpretation is not possible for the original primal EG programs.

2.1 Linear Fisher Markets (LFM)

The LFM model has two primary uses. Its original intent is as a model of competition, and how prices are determined in a competitive market. An additional, and practically important, use of LFM is as a tool for fair and efficient resource allocation (with the items being the resources). If every individual in a resource allocation problem is given one unit of faux currency, then the resulting LFM equilibrium allocation is known to be both Pareto efficient and satisfy the fairness desiderata of envy-freeness and proportionality (Nisan et al. 2007). This fair allocation approach is known as competitive equilibrium from equal incomes (CEEI) (Varian 1974).

We now describe the competitive equilibrium concept. Imagine there is a central policymaker that sets prices for the items . Upon observing the prices, buyer maximizes their utility subject to their budget. Their demand set is the set of bundles that are optimal under the prices:

Of course, due to the supply constraints, if prices are too low, there will be a supply shortage. On the other hand, if prices are too high, a surplus occurs. A competitive equilibrium is a set of prices and bundles such that all items are sold exactly at their supply (or have price zero). We call such an equilibrium the limit LFM equilibrium for the supply function (Gao and Kroer 2022).

Definition 2.1 (Limit LFM)

The limit equilibrium, denoted , is an allocation-price tuple such that the following holds.

-

1.

(Supply feasibility and market clearance) and .

-

2.

(Buyer optimality) all .

Gao and Kroer (2022) show that an equilibrium of a limit LFM must exist, and that when the measure space is atomless, a pure equilibrium allocation 111An allocation is pure if . must exist. Given an equilibrium , let

be buyer ’ utility, her inverse bang-per-buck, and the (log) Nash social welfare of the whole market. The inverse bang-per-buck can also be seen as the price-per-utility of buyer in equilibrium. In a general LFM, the equilibrium allocation may not be unique, but the equilibrium quantities are unique. In order to facilitate statistical inference, we will impose certain differentiability condition, which turn out to imply uniqueness and purity of the equilibrium allocation .

Next we introduce the finite LFM, which models the data we observe in a market. The finite LFM equilibrium is nothing but a limit LFM equilibrium where the item set is the finite set of observed items . Let be i.i.d. samples from the supply distribution , each with supply .

Definition 2.2 (Finite LFM, Eisenberg and Gale (1959), Eisenberg (1961))

The finite observed LFM, denoted , is a allocation-price tuple such that the following hold:

-

1.

(Supply feasibility and market clearance) and .

-

2.

(Buyer optimality) , the demand set given the prices.

Let 222We use since the equilibrium allocation may not be unique., where and price . Buyer ’s utility is , and the inverse bang-per-buck is . The (log) Nash social welfare is .

We now introduce several properties of LFM: natural bounds on , fairness and efficiency as a resource allocation mechanism, scale-invariance, and the convex program characterization.

There exists natural bounds on in limit LFM. Recall is the expected value of buyer . By Gao and Kroer (2022), we know that . We define

| (3) |

to be the region whose interior must lie in.

A major use case for LFM is fair and efficient allocation of resources. Similar to the classical finite LFM, the infinite LFM enjoys fairness and efficiency properties (Gao and Kroer 2022). Let be an equilibrium allocation. First, this allocation is Pareto optimal, meaning there does not exist an , , such that for all and one of the inequalities is strict. The allocation is envy-free in a budget-weighted sense, meaning for all . Finally, it is proportional: , that is, each buyer gets at least the utility of its proportional share allocation.

LFM enjoys certain scale-invariance properties. First, buyers cannot change the equilibrium by scaling their value functions. Suppose are positive scalars, and that are the equilibrium allocations and prices in . Then will also be the equilibrium quantities in . This is easily seen by the fact that valuation scaling does not change the demand function. Second, if all buyers’ budgets are scaled by the same factor, or the supply is scaled by the same factor, the equilibrium does not change. That is, if are two positive scalars, and , then . These scale-invariances hold for finite LFM as well 333 That is, implies , and . Based on the invariance, we impose the normalization that and that all buyers’ expected values are 1, i.e., . Then in the limit LMF, the budge-supply ratio is . With the normalization, we have . In order for the budget-to-supply ratio to match in the sampled finite LFM and the limit LFM, we use supplies of for each item in the finite LFM. Thus we study finite LFM of the form .

2.2 First-Price Pacing Equilibrium (FPPE)

The FPPE setting (Conitzer et al. 2022a) models an economy that typically occurs on internet advertising platforms: the buyers (advertisers in the internet advertising setting) are subject to budget constraints, and must participate in a set of first-price auctions, each of which sells a single item. Each buyer is assigned a pacing multiplier by the platform to scale down their bids in the auctions, and submits bids of the form for each item . From the platform’s perspective, the goal of choosing is to ensure there is no unnecessary pacing, i.e., buyers spend their budget exactly, or they spend less than their budget but they do not scale down their bids. In the FPPE model, all auctions occur simultaneously, and thus the buyers choose a single that determines their bid in all auctions. The utility of a buyer in FPPE is quasilinear: it is the sum of their value received from items plus their leftover budget (this is equivalent for decision-making purposes to the utility being the value received from items minus the payments).

Definition 2.3 (Limit FPPE, Gao and Kroer (2022))

A limit FPPE, denoted , is the unique tuple such that there exist , satisfying

-

1.

(First-price) Prices are determined by first-price auctions: for all items , . Only the highest bidders win: for all and , implies

-

2.

(Feasibility, market clearing) Let be the expenditure of buyer . Buyers satisfy budgets: for all , . There is no overselling: for all , . All items are fully allocated: for all , implies .

-

3.

(No unnecessary pacing) For all , implies .

FPPE is a hindsight and static solution concept for internet ad auctions. Suppose the platform knows all the items that are going to show up on a platform. FPPE describes how the platform could configure the ’s in a way that ensures that all buyers satisfy their budgets, while maintaining their expressed valuation ratios between items. In practice, the ’s are learned by an online algorithm that is run by the platform (Balseiro and Gur 2019, Conitzer et al. 2022a). FPPE has many nice properties, such as the fact that it is a competitive equilibrium, it is revenue-maximizing, revenue-monotone, shill-proof, has a unique set of prices, and so on (Conitzer et al. 2022a). We refer readers to Conitzer et al. (2022a), Kroer and Stier-Moses (2022) for more context about the use of FPPE in internet ad auctions.

Gao and Kroer (2022) show that a limit FPPE always exists and is unique, and when the item space is atomless, a pure allocation exists. Let and be the unique FPPE equilibrium multipliers and prices. Revenue in the limit FPPE is

| (5) |

It is also easy to see that . Although the equilibrium allocation may not be unique in general, for statistical inference we will impose certain differentiability assumption which imply uniqueness of . When is unique, we let be the leftover budget.

In an FPPE, based on the pacing multiplier and the budget expenditure, we can categorize buyers in terms of how they satisfy the no unnecessary pacing condition. As we will see later, the statistical behavior of pacing multipliers varies by category.

-

•

Paced buyers (). We use to denote them. Due to the budget constraints, they are not able to bid their value in the auctions at equilibrium, and by the no unnecessary pacing condition in Def. 2.3, their budgets are fully exhausted, i.e. .

-

•

Unpaced buyers (). We use to denote them. They can be further divided according to their budget expenditure.

-

–

Buyers who have leftover budgets (), denoted . Note this category also includes buyers who dot not win any items ().

-

–

Degenerate buyers (), denoted . They are the edge-cases in the FPPE model. If these buyers were given more budgets, they would become -type buyers at equilibrium. For the FPPE statistical theory developed in this paper, we assume absence of such buyers (Section 5.2). In follow-up work to the conference version of the present paper, Liao and Kroer (2024) give some results for the case where degenerate buyers exist.

-

–

We let be i.i.d. draws from , each with supply . They represent the items observed in an auction market. The definition of a finite FPPE is parallel to that of a limit FPPE, except that we change the supply function to be a discrete distribution supported on .

Definition 2.4 (Finite FPPE, Conitzer et al. (2022a))

The finite observed FPPE, , is the unique tuple such that there exists satisfying:

-

1.

(First-price) For all , . For all and , implies .

-

2.

(Supply and budget feasible) For all , . For all , .

-

3.

(Market clearing) For all , implies .

-

4.

(No unnecessary pacing) For all , implies .

Let . Given the equilibrium price , the revenue in a finite FPPE is .

FPPE has some of the same scale-invariance properties as LFM. In particular, scaling the budget and supply at the same time does not change the market equilibrium. That is, given a positive scalar , if are the equilibrium pacing multiplier and prices in the market , then are the equilibrium quantities in the market . The same scale-invariance holds for the finite FPPE, i.e., if , then . Given the invariance, we can see that in order for the budget-supply ratio to match the limit market , the finite market should be configured as either or . We will study the latter, and simply refer to it as the finite FPPE. Unlike LFM, FPPE does not enjoy invariance to valuation scaling, because buyers have a pacing multiplier of at most one in FPPE.

It is well-known (Cole et al. 2017, Conitzer et al. 2022a, Gao and Kroer 2022) that in a limit (resp. finite) FPPE uniquely solves the population (resp. sample) dual EG program

| (6) |

where the objectives and are the same as in Eq. 4. The difference between the LFM and FPPE convex programs is that for FPPE we impose the constraint .

The EG program and certain quantities of the FPPE are related as follows.

Lemma 2.5

Suppose is twice continuously differentiable at , the equilibrium pacing multiplier. Then , and .

Proof sketch The first equality follows from the fact that leftover budgets are the Lagrange multipliers corresponding to the constraint . The second equality follows from the first-order homogeneity of in Eq. 1. See Section 12 for details.

3 Differentiability of EG Objective

This section is dedicated to describing the differentiability properties of the EG objective in Eq. 2. The second part of is clearly a nice function, and so we focus on its first part . Differentiability of the EG objective is important because the following assumption is needed when deriving the asymptotic distribution of LFM and FPPE.

[SMO] Let denote the equilibrium inverse bang-per-buck in LFM, or the equilibrium pacing multiplier in FPPE. Assume the map is in a neighborhood of . We let .

We start with the differential structure of . The function is a convex function of and its subdifferential is the convex hull of , with being the base vector in . When is attained by a unique , the function is differentiable. In that case, the -th entry of is for and zero otherwise.

3.1 First-order Differentiability

We introduce notation for characterizing first-order differentiability of . Define the gap between the highest and the second-highest bid under pacing multiplier by

| (7) |

here is the second-highest entry; e.g., . When there is a tie for an item , we have . When there is no tie for an item , the gap is strictly positive. The gap function characterizes smoothness of : is differentiable at iff is strictly positive.

Theorem 3.1 (First-order differentiability)

The following are equivalent. (i) The dual objective is differentiable at a point . (ii) The function is strictly positive -almost surely:

| (8) |

(iii) The set of items that incur ties under pacing profile is -measure zero: .

When one and thus all of the above conditions hold for some , the gradient is well-defined for -almost every , and . Proof and further technical remarks given in Section 8.2.

3.2 Second-order Differentiability

Given the neat characterization of differentiability of the dual objective via the gap function , it is natural to explore higher-order smoothness, which is needed for some of our asymptotic normality results. Example 8.3 in the appendix is one where Eq. 8 holds at a point, say , and is differentiable in a neighborhood of , and yet is not twice differentiable at . We now provide three sufficient conditions that imply twice differentiability of objective .

Theorem 3.2 (Second-order differentiability, informal)

If any of the following conditions hold, then and thus are at a point . (i) A stronger form of Eq. 8 holds: . (ii) The angular component of the random vector is smoothly distributed. (iii) , is the Lebesgue measure, the valuations ’s are linear functions, and is the equilibrium inverse bang-per-buck in LFM. See Appendix 8 for formal statements.

We show in Appendix 8.3 that when is twice differentiable, the Hessian matrix of has a closed-form expression.

4 Statistical Results for Linear Fisher Markets

We now turn to investigating the statistical convergence properties of finite LFMs to the limit LFM. Suppose we sample an LFM (), where consists of i.i.d. samples from . We will study how such finite LFMs are distributed around the limit LFM () as grows. In LFM we focus on convergence of the following quantities: individual utilities, (log) Nash social welfare (NSW), and the pacing multiplier vector (which characterizes the equilibrium, as shown in Eq. 4). Section 4.1 presents strong consistency and convergence rate results. Section 4.2 presents asymptotic distributions for the quantities of interest, and a local minimax theory based on Le Cam et al. (2000), showing that the finite LFM provides an optimal estimate for the limit LFM in a local asymptotic sense. Section 4.3 discusses estimation of asymptotic variance of NSW.

4.1 Basic Convergence Properties

In this section we show that we can treat observed quantities in the finite LFM as consistent estimators of their counterparts in the limit LFM. Below we state the consistency results; the formal versions can be found in Section 9.1. We say an estimator sequence is strongly consistent for if .

Theorem 4.1 (Strong Consistency)

The NSW, pacing multiplier vector, and utility vectors in the finite LFM are strongly consistent estimators of their counterparts in the limit LFM.

Next, we refine the consistency results and provide finite sample guarantees. We start by focusing on Nash social welfare and the set of approximate market equilibria. The convergence of utilities and pacing multipliers will then be derived from the latter result.

Theorem 4.2

For any failure probability , let . Then with probability greater than , we have where hides only constants. Proof in Appendix 11.2.

Theorem 4.2 establishes a convergence rate . The proof proceeds by first establishing a pointwise concentration inequality and then applies a discretization argument.

To state the result for the pacing multipliers , we define approximate market equilibria (which we define in terms of approximately optimal pacing multiplier vectors ). Let

| (9) |

be the sets of -approximate solutions to the sample and the population EG programs, respectively. The next theorem shows that the set of -approximate solutions to the sample EG program is contained in the set of -approximate solutions to the population EG program with high probability.

Theorem 4.3 (Convergence of Approximate Market Equilibrium)

By construction of we know holds, and so is not empty. In the appendix, Lemma 10.1 shows that for sufficiently large, with high probability, in which case the set is not empty. By simply taking in Theorem 4.3 we obtain the corollary below.

Corollary 4.4

Let satisfy Eq. 10. Then with probability it holds .

More importantly, it establishes the fast statistical rate for sufficiently large, where we use to ignore logarithmic factors. In words: the limit LFM objective value of the finite LFM solution converges to the optimal limit LFM objective value with a rate .

By the strong convexity of the dual objective, the containment result can be translated to high-probability convergence of the pacing multipliers and the utility vector.

Corollary 4.5

Let satisfy Eq. 10. Then with probability at least we have and .

We compare the above corollary with Theorem 9 from Gao and Kroer (2022) which establishes the convergence rate of the stochastic approximation estimator based on the dual averaging algorithm (Xiao 2010). In particular, they show that the average of the iterates, denoted , enjoys a convergence rate of , where is the number of sampled items. The rate achieved in Corollary 4.5 is . We see that our rate is worse off by a factor of . We conjecture that it can be removed by using the more involved localization arguments (Bartlett et al. 2005). And yet our estimates are produced by the strategic behavior of the agents without any extra computation at all. Moreover, in the computation of the dual averaging estimator the knowledge of the values is required, while again can be just observed naturally.

4.2 Asymptotics of Linear Fisher Market

In this section we derive asymptotic normality results for Nash social welfare, utilities and pacing multipliers. As we will see, a central limit theorem for Nash social welfare holds under basically no additional assumptions. However, the CLTs of pacing multipliers and utilities will require twice continuous differentiability of the population dual objective at optimality, with a nonsingular Hessian matrix. We present CLT results under such a premise; Theorem 3.2 gave three quite general settings under which these conditions hold.

Theorem 4.6 (Asymptotic Normality of Nash Social Welfare)

As stated previously, our asymptotic results for and require that is twice-continuously differentiable at . When this differentiability holds, by Theorem 3.1, the set of items that incur ties is -measure zero, and thus the equilibrium allocation in the limit LFM is unique and must be pure. Now we define a map , which represents the utility all buyers obtain from the item at equilibrium. Formally,

| (12) |

Since is pure, only one entry of is nonzero. Clearly .

Theorem 4.7 (Asymptotic Normality of Pacing Multipliers and Utilities)

Theorem 4.6 can also be derived from Theorem 4.7 using the delta method, since is a smooth function of .

We will show that the asymptotic variances in Theorem 4.7 are the best achievable, in an asymptotic local minimax sense. To make this precise, we need to introduce “supply neighborhoods” obtained through perturbing the original supply .

4.2.1 Perturbed Supply

First we introduce notation to parametrize neighborhoods of the supply . Let be a direction along which we wish to perturb the supply . Given a vector signifying the magnitude of perturbation, we want to scale the original supply of item by and then obtain a perturbed supply distribution by appropriate normalization. To do this we define the perturbed supply by 444 In Duchi and Ruan (2021) they allow more general classes of perturbations, we specialize their results for our purposes.

| (14) |

with a normalizing constant . As , the perturbed supply effectively approximates

We let , and be the limit inverse bang-per-buck, price and revenue in . Clearly for any and similarly for and .

4.2.2 Asymptotic Local Minimax Optimality

Given the asymptotic normality of observed LFM, it is desirable to understand the best possible statistical procedure for estimating the limit LFM. One way to discuss the optimality is to measure the difficulty of estimating the limit LFM when the supply distribution varies over small neighborhoods of the true supply , asymptotically. When an estimator achieves the best worst-case risk over these small neighborhoods, we say it is asymptotically locally minimax optimal. For general references, see Vaart and Wellner (1996), Le Cam et al. (2000). More recently Duchi and Ruan (2021, Sec. 3.2) develop asymptotic local minimax theory for constrained convex optimization, and we rely on their results.

Let be any symmetric quasi-convex loss 555A function is quasi-convex if its sublevel sets are convex.. In asymptotic local minimax theory we are interested in the local asymptotic risk: given a sequence of estimators ,

If we ignore the limits and consider a fixed , then roughly measures the worst-case risk for the estimators . Note that is a -vector, and thus the shrinking norm-balls depend on , and the expectation is taken w.r.t. the -fold product of the perturbed supply.

Similarly, define the risk for utility (resp. Nash social welfare ) given an estimator sequence (resp. ):

Theorem 4.8

4.3 Variance Estimation and Inference

In this section we show how to construct confidence intervals for Nash social welfare. We will show how to construct confidence intervals for pacing multipliers and utilities in the FPPE section. The procedure is similar for LFM, and thus we omit it here.

First, regarding inference, it is interesting to note that the observed NSW () is a negatively-biased estimate of the limit NSW (), i.e., .666Note Moreover, it can be shown that, when the items are i.i.d. by a simple argument from Proposition 16 from Shapiro (2003). Monotonicity tells us that increasing the market size produces, on average, less biased estimates of the limit NSW.

To construct confidence intervals for Nash social welfare, one needs to estimate the asymptotic variance. Let be the price of item in the finite market, and . The variance estimator is then

| (15) |

We emphasize that in the computation of the variance estimator one does not need knowledge of the valuations . All that is needed is the equilibrium prices for the items. Given the variance estimator, we construct the confidence interval , where is the -th quantile of a standard normal. The next theorem establishes validity of the variance estimator.

Theorem 4.9

It holds that . Given , it holds that . Proof in Appendix 11.6.

5 Statistical Results for FPPE

Next we study statistical inference questions for the FPPE model. Since FPPE is characterized by an EG-style program similar to that of LFM, many of the results for FPPE are similar to those for LFM. However, an important difference is that the FPPE model has constraints on the pacing multipliers, which makes the asymptotic theory more involved. As for LFM, we assume that we observe a finite auction market with being i.i.d. draws from , and we use it to estimate quantities from the limit market . In FPPE we mainly focus on the revenue of the limit market, and for the same reason as in LFM, since FPPE is characterized by EG program with optimizing variable being the pacing multiplier, we also present results for . Similarly to the LFM case, one could use results for to derive estimators for buyer utilities.

5.1 Basic Convergence Properties

Since FPPE has a similar convex program characterization as LFM, strong consistency and convergence rate results can be derived using similar ideas.

Theorem 5.1

We have , and . Proof in Appendix 13.1.

We complement the strong consistency result with the following rate results. They are derived using a discretization argument.

Theorem 5.2

It holds that and Proof in Appendix 13.2.

The above bounds hold for a broad class of limit FPPE models and may be loose for a particular model. In Section 5.2, we show that for buyers , their pacing multipliers converge at a rate faster than .

5.2 Asymptotics of FPPE

As in LFM, our statistical inference results require the limit market to behave smoothly around the optimal pacing multipliers . To that end, we will assume Section 3 as in LFM. Similar to LFM, under Section 3, the equilibrium allocation is unique and must be pure. Again we can define

| (16) |

Under Section 3, the equilibrium allocation is unique, so is also unique. Moreover, , and (the set of nondifferentiable points has measure zero, and thus we can ignore such points). Also let

| (17) |

to denote the utility from items. Note that in the FPPE model, buyers’ utility consists of two parts: utility from items and leftover budgets. In FPPE, the pacing multipliers relate budgets and utilities via (Conitzer et al. 2022a)

| (18) |

In the unconstrained case, classical -estimation theory says that, under regularity conditions, an -estimator is asymptotically normal with covariance matrix (Van der Vaart 2000, Chap. 5). However, in the case of FPPE which is characterized by a constrained convex problem, the Hessian matrix needs to be adjusted to take into account the geometry of the constraint set at the optimum . We let be an “indicator matrix” of buyers whose , and define the projected Hessian

| (19) |

It will be shown that the asymptotic variance of is and the “gradient” is exactly .

[SCS] Strict complementary slackness holds: implies .

Section 5.2 can be viewed as a non-degeneracy condition from a convex programming perspective, since corresponds to a Lagrange multiplier on . From a market perpective, Section 5.2 requires that if a buyer’s bids are not paced (), then their leftover budget must be strictly positive. This can again be seen as a market-based non-degeneracy condition: if then the budget constraint of buyer is binding, yet would imply that they have no use for additional budget. If Section 5.2 fails, one could slightly increase the budgets of buyers for which Section 5.2 fails, i.e., those who do not pace yet have exactly zero leftover budget, and obtain a market instance with the same equilibrium, but where Section 5.2 holds.

From a technical viewpoint, Section 5.2 is a stronger form of first-order optimality. Note (cf. Lemma 2.5). The usual first-order optimality condition is

| (20) |

where is the normal cone with if and if for . Then Eq. 20 translates to the condition that implies . On the other hand, when written in terms of the normal cone, Section 5.2 is equivalent to

Given that , Section 5.2 is obviously a stronger form of first-order condition. The Section 5.2 condition is commonly seen in the study of statistical properties of constrained -estimators (Duchi and Ruan 2021, Assumption B and Shapiro 1989). In the proof of Theorem 5.3, Section 5.2 forces the critical cone to reduce to a hyperplane and thus ensures asymptotic normality of the estimates. Without Section 5.2, the asymptotic distribution of could be non-normal.

5.2.1 Central Limit Theorems

We now show that the observed pacing multipliers and the observed revenue are asymptotically normal. Define the influence functions

| (21) | ||||

Recall is defined in Eq. 16, in Eq. 17, in Eq. 19. And note and .

Theorem 5.3

If Sections 3 and 5.2 hold, then

Consequently, and are asymptotically normal with means zero and variances and . Proof in Appendix 13.3.

The functions and are called the influence functions of the estimates and because they measure the change in the estimates caused by adding a new item to the market (asymptotically).

Theorem 5.3 implies fast convergence rate of for . To see this, we suppose wlog. that , i.e. the first buyers are the ones with . Then the pseudo-inverse of the projected Hessian where is the lower right block of . Consequently, the upper diagonal entries of are zeros. This result shows that the constraint set “improves” the covariance by zeroing out the entries corresponding to the active constraints . Consequently, and are of order for , and thus converging faster than the usual rate. The fast rate phenomenon is empirically investigated in Section 6.1.2.

The practical implication is the following. By Section 5.2 we have , i.e., is the set of buyers who are not budget constrained, and , i.e., is the set of buyers who exhaust their budgets. 888Without Section 5.2, it only holds and by complementary slackness. In the context of first-price auctions, the fast rate implies that the platform can identify which buyers are budget constrained even when the finite market is small.

The proof of Theorem 5.3 proceeds by showing that FPPE satisfy a set of regularity conditions that are sufficient for asymptotic normality (Shapiro 1989, Theorem 3.3); the conditions are stated in Lemma 12.2 in the appendix. Maybe the hardest condition to verify is the so called stochastic equicontinuity condition (Cond. 12.2.c), which we establish with tools from the empirical process literature. In particular, we show that the class of functions, parameterized by a pacing multiplier vector , that map each item to its corresponding first-price auction allocation under the given , is a VC-subgraph class. This in turn implies stochastic equicontinuity. Section 5.2 is used to ensure normality of the limit distribution.

Finally, we remark that the CLT result for revenue holds true even if , i.e., for all . If for all , then all buyers’ budgets are exhausted in the observed FPPE, and so we have . By the convergence , we know that with high probability for all large if . In that case, it must be that the asymptotic variance of revenue equals zero. Our result covers this case because one can show using if (Lemma 2.5), and .

In an FPPE individual utilities and Nash social welfare can be similarly defined. By applying the delta method and the results in Theorem 5.3, we can derive asymptotic distributions for individual utilities , leftover budget and Nash social welfare, since they are smooth functions of . See Section 13.4 for more details.

5.2.2 Asymptotic Local Minimax Optimality

Given the asymptotic distributions for and , we will show that the observed FPPE estimates are optimal in an asymptotic local minimax sense. Recall in Section 4.2.1 we have defined the perturbed supply family of dimension with perturbation .

Asymptotic local minimax optimality for .

We first focus on estimation of pacing multipliers. For a given perturbation , we let , and be the limit FPPE pacing multiplier, price and revenue under supply distribution . Clearly for any and similarly for and . Let be any symmetric quasi-convex loss. 999A function is quasi-convex if its sublevel sets are convex. In asymptotic local minimax theory we are interested in the local asymptotic risk: given a sequence of estimators ,

As an immediate application of Theorem 1 from Duchi and Ruan (2021), it holds that

where the expectation is taken w.r.t. a normal specified above. Moreover, the lower bound is achieved by the observed FPPE pacing multipliers according to the CLT result in Theorem 5.3.

Asymptotic local minimax optimality for revenue estimation.

For pacing multipliers, the result is a direct application of the perturbation result from Duchi and Ruan (2021). The result for revenue estimation is more involved. Given a symmetric quasi-convex loss , we define the local asymptotic risk for any procedure that aims to estimate the revenue:

Theorem 5.4 (Asymptotic local minimaxity for revenue)

If Sections 3 and 5.2 hold, then

Proof in Appendix 13.5. In the proof we calculate the derivative of revenue w.r.t. , which in turn uses a perturbation result for constrained convex programs from Duchi and Ruan (2021), Shapiro (1989). Again, the lower bound is achieved by the observed FPPE revenue according to the CLT result in Theorem 5.3. Similar optimality statements can be made for and by finding the corresponding derivative expressions.

5.3 Variance Estimation and Inference

In order to perform inference, we need to construct estimators for the influence functions Eq. 21. In turn, this requires estimators for the projected Hessian (Eq. 19) and the variance of the utility map (Eq. 16).

The Hessian. Given a sequence of smoothing parameters , we estimate the projection matrix by For the same sequence , we introduce a numerical difference estimator for the Hessian matrix , whose -th entry is

| (22) |

with , and is defined in Eq. 2. Finally, is the estimator of .

The term . Let and price be the allocation and prices in the finite FPPE. Mimicking Eqs. 16 and 17, define the finite sample analogues

| (23) |

Recall . Then we define the following influence function estimators

Given that the asymptotic variance of (resp. ) is (resp. ), plug-in estimators for the (co)variance are naturally

| (24) |

For any , the -confidence regions for and are

| (25) | |||

| (26) |

where is the -th quantile of a chi-square distribution with degree , is the unit ball in , and is the -th quantile of a standard normal distribution. The coverage rate of is empirically verified in Section 6.3.1.

Theorem 5.5

Under the conditions of Theorem 5.3, let and . Then and . Consequently, for any , and . Proof in Appendix 13.6.

The theorem suggests choosing smoothing parameter for . Section 6.1.1 studies how the choice of affects the Hessian estimation numerically.

5.4 Application: A/B Testing in First-Price Auction Platforms

Consider an auction market with buyers with a continuum of items with supply function . Now suppose that we are interested in the effect of deploying some new technology (e.g. new machine learning models for estimating click-through rates in the ad auction setting). To model treatment application we introduce the potential value functions

If item is exposed to treatment , then its value to buyer will be .

Suppose we are interested in estimating the change in the auction market when treatment 1 is deployed to the entire item set . In this section we describe how to do this using A/B testing, specifically for estimating the treatment effect on revenue. Formally, we wish to look at the difference in revenues between the markets

where is the market with treatment 1, and is the one with treatment 0. The treatment effects on revenue is defined as

where is revenue in the equilibrium .

We will refer to the experiment design as budget splitting with item randomization. The design works in two steps, and closely mirrors how A/B testing is conducted at large tech companies.

Step 1. Budget splitting. We create two markets, and every buyer is replicated in each market. For each buyer we allocate of their budget to the market with treatment , and the remaining budget, , to the market with treatment . Each buyer’s budget is managed separately in each market.

Step 2. Item randomization. Let be i.i.d. draws from the supply distribution . For each sampled item, it is applied treatment with probability and treatment with probability . The total A/B testing horizon is . When the end of the horizon is reached, two observed FPPEs are formed. Each item has a supply of in the 1-treated market and in the 0-treated market. The is the scaling required for our CLTs and the factor ensures the budget-supply ratio agrees with the limit market; due to FPPE scale-invariance, we could equivalently rescale budgets.

Let be the number of -treated items, and be the number of -treated items. Conditional on the total number of items , the random variable is a binomial random variable with mean . Let be the set of -treated items, and similarly . The total item set . The observables in the described A/B testing experiment are

both defined in Def. 2.4. Let denote the observed revenue in the -treated market. The estimator of the treatment effect on revenue is

For fixed , the variance in Theorem 5.3 is a functional of the value functions. We will use to represent the revenue variance in the equilibrium . Each variance can be estimated using Eq. 24.

Theorem 5.6 (Revenue treatment effects CLT)

Suppose Section 3 and Section 5.2 hold in the limit markets and . Then Proof in Appendix 13.7.

Based on the theorem, an A/B testing procedure is the following. Compute the revenue variance as Eq. 24 for each market, obtaining and , and form the confidence interval

| (27) |

If zero is on the left (resp. right) of the CI, we conclude that the new feature increases (resp. decreases) revenue with confidence. If zero is in the interval, the effect is undecided. See Section 6.3.2 for a semi-synthetic study verifying the validity of this procedure.

6 Experiment

6.1 Synthetic Experiment

6.1.1 Hessian Estimation

Recall that a key component in the variance estimator is the Hessian matrix, which we estimate by the finite-difference method in Eq. 22. Finite difference estimation requires the smoothing parameter . The smoothing is used to (1) estimate the active constraints and (2) construct the numerical difference estimator . Theorem 5.5 suggests a choice of for some . In Section 14.1, we investigate the effect of numerically. Here we give high-level take-aways. We find that represents a bias-variance trade-off. For small , the variance of the estimated value is small and yet bias is large. For a large variance is large and yet the bias is small (the estimates are stationary around some point). Our experiments suggest using .

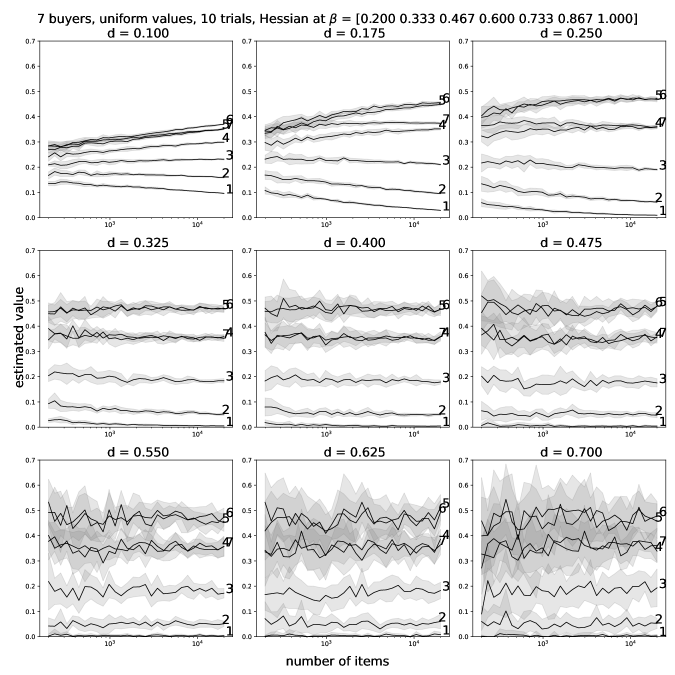

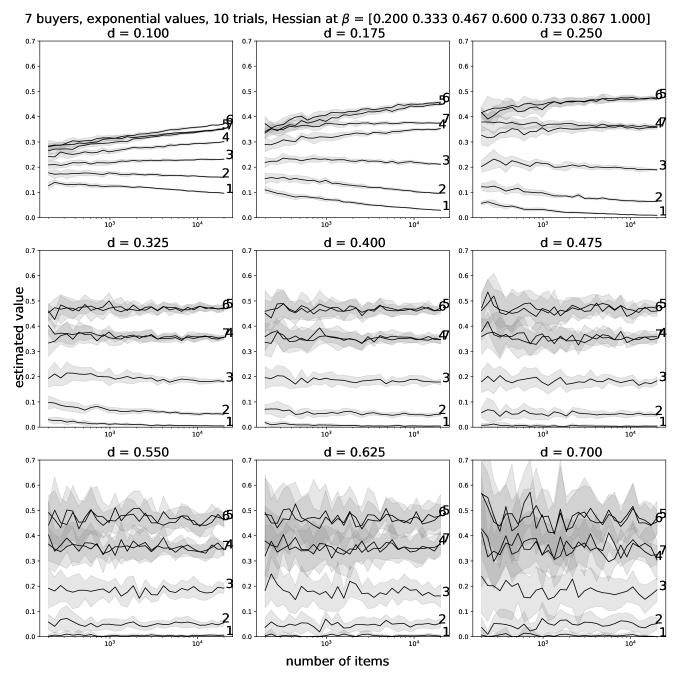

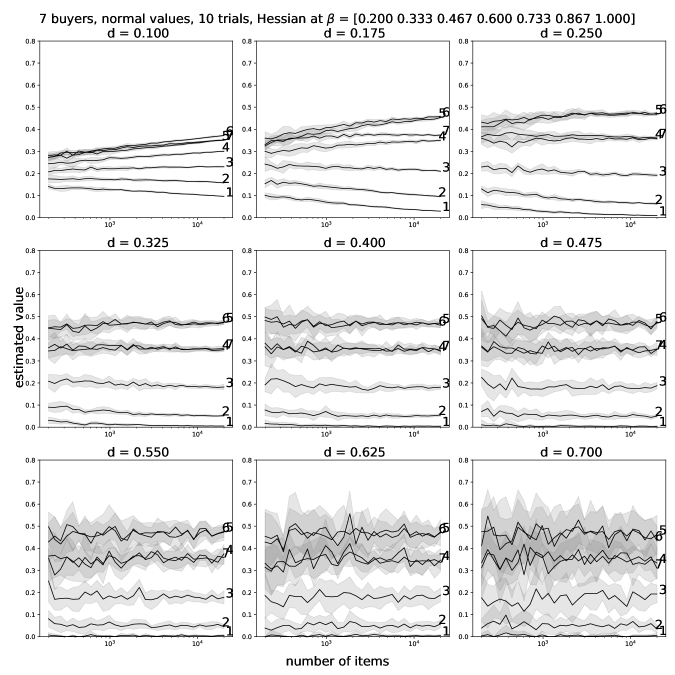

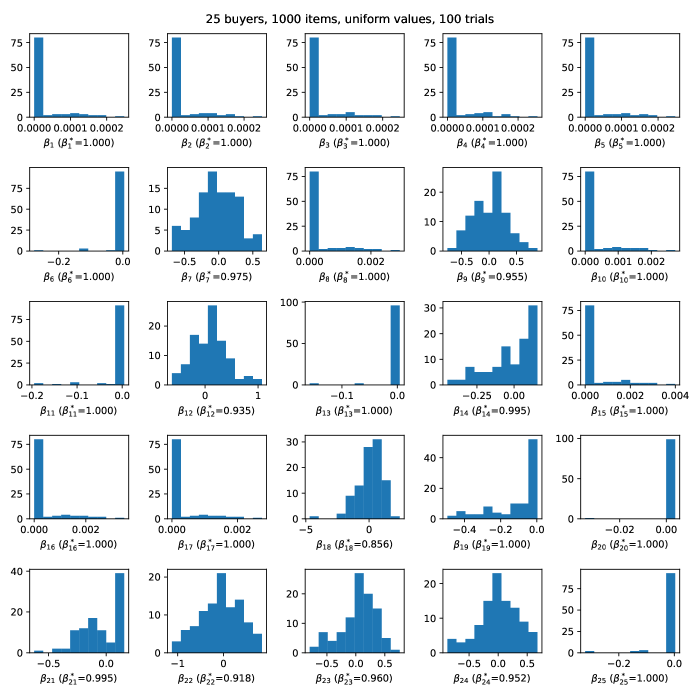

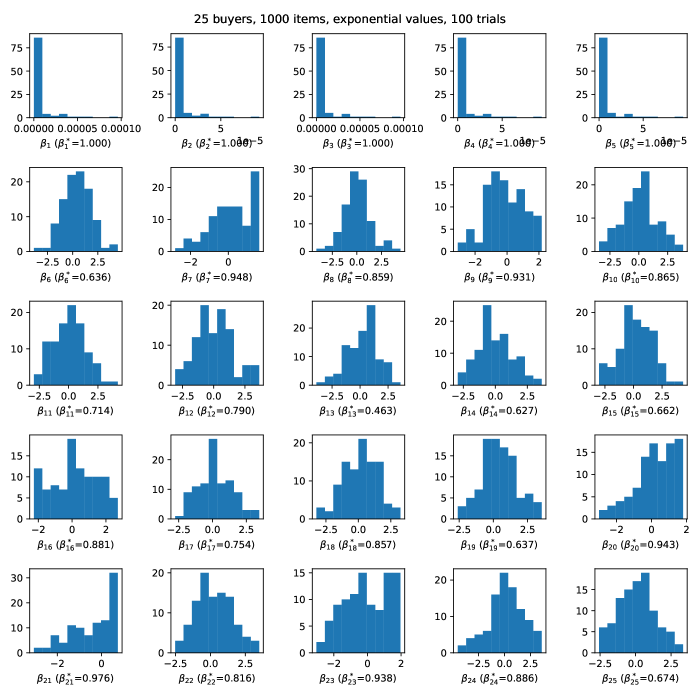

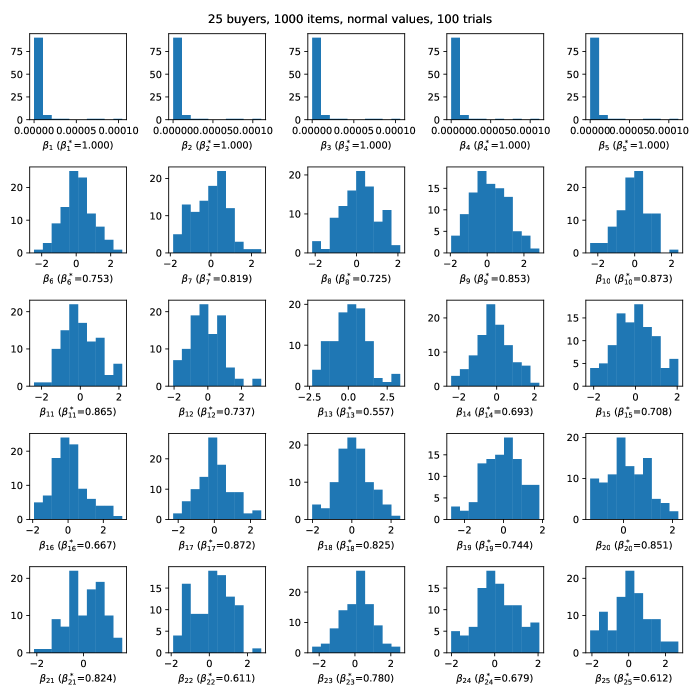

6.1.2 Visualization of the FPPE Distribution

Next we look at how the FPPE distribution behaves in a simple setting. We choose the FPPE instances as follows. Consider a finite FPPE with buyers and items. Let be i.i.d. uniform random variables on . Buyers’ budgets are generated by for and for . The extra budgets are to ensure we observe for the first few buyers. The valuations i.i.d. uniform, exponential, or truncated standard normal distributions. Under each configuration we form 100 observed FPPEs, and plot the histogram of each . The population EG Eq. 6 is a constrained stochastic program and can be solved with stochastic gradient based methods. The true value is computed by the dual averaging algorithm (Xiao 2010). The mean square error decays as with being the number of iterations, and so if we choose large enough, we should still observe asymptotic normality for the quantities .

Results.

Figure 2 shows five out of 25 distributions for pacing multipliers. Full plots for all three distributions are given in Figures 10, 11 and 12. We see that (i) if then the finite sample distribution is close to a normal distribution, and (ii) if (or very close to , such as in the uniform value plots, in exponential), the finite sample distribution puts most of the probability mass at 1. For cases where is close, but not very close, to 1, we need to further increase the number of items to observe normality.

6.2 Semi-real Experiment: Nash Social Welfare Estimation in Instagram Notification System

Notifications are important in enhancing the user experience and user engagement in mobile apps. Nevertheless, an excessive barrage of notifications can be disruptive for users. Typically, a mobile application has various notification types, overseen by separate teams, each with potentially conflicting objectives. And so it is necessary to regulate notifications and send only those of most value to users. Kroer et al. (2023b) propose to use Fisher market equilibrium-based methods to efficiently send notifications, where they treat the opportunity to send a user a notification as an item, and different types of notifications as buyers. In this section, we use the inference method developed in Section 4.3 to quantify uncertainty in equilibrium-based notification allocation methods.

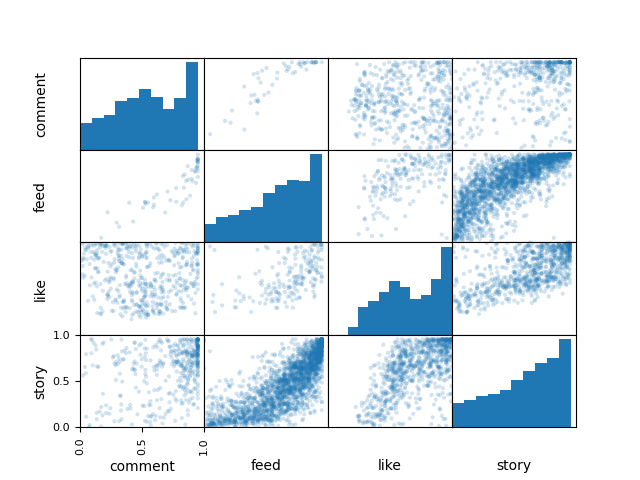

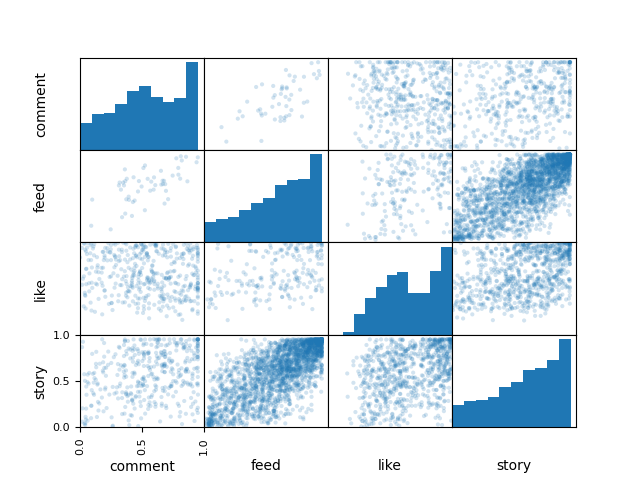

The data. The dataset released by Kroer et al. (2023b) contains about generated notifications of four types for a subset of about Instagram users from September 14–23, 2022. The four types of notifications (buyers) are likes, daily digest of stories, feed suite organic campaign (notification about new posts on the user’s feed), and comments subscribed. The value of a notification type to a user at a specific time is predicted by the platform’s algorithm and available in the dataset as a numerical value in . The budgets of notification types are also given. For a user-notification type pair, we average over the whole time window and use the average to represent , resulting in a user-notification type matrix. However, even after aggregation over time, there are lots of missing values, i.e., many users do not have every notification type generate a potential notification.

Value imputation and simulation by the Gaussian copula. We assume the values in the notification system admit the following representation. There exists unique monotone functions , such that , where follows a multivariate Gaussian distribution with standard normal marginals. Such an assumption is equivalent to assuming the value distribution possesses a Gaussian copula (Zhao and Udell 2020, Lemma 1 and Liu et al. 2009, Lemma 1). Given this representation, we propose a two-step simulation method. In the first step, we learn the monotone functions by matching the quantiles of values with the quantiles of a standard normal. We use isotonic regression to learn the monotone functions. Second, given the learned functions and inverses , we transform to , and compute the covariance matrix of , denoted . Even though some values are missing, the covariance can still be estimated by if values are missing at random. Now to simulate a new item for buyers, we draw , and return as the value. There are multiple advantages to this method. First, the dependence structure of the available dataset is preserved. Second, the generated values are within the range as the original data are. Third, the marginal distribution of values are also preserved in the simulated data.

As a final step to mimic realistic data, since some users may turn off notifications of certain types, the values of those notifications will be zero. We simulate this by setting certain values to zero according to the sparsity pattern in the original dataset. See Figure 3 for a comparison between original dataset and simulated data.

Setup and results. We apply the confidence interval in Theorem 4.9 and study the coverage properties. The nominal coverage rate is set to 95%. First, we do see that even for a small sample size of 100, the nominal coverage rate is achieved. And as we increase the size of markets , the coverage maintains at around 95% and the width of the CI shrinks roughly at the rate .

| items | (coverage rate, width of CI) |

| 100 | (0.94, 0.88) |

| 200 | (0.95, 0.63) |

| 400 | (0.93, 0.43) |

| 600 | (0.97, 0.35) |

6.3 Semi-real Experiment: A/B Testing of Revenue in First-Price Auction Platforms

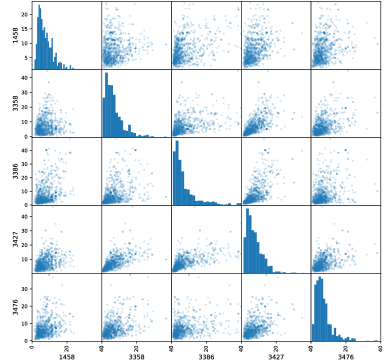

In this section we apply our revenue estimation method to a real-world dataset, the iPinYou dataset (Liao et al. 2014). The iPinYou dataset (Liao et al. 2014) contains raw log data of the bid, impression, click, and conversion history on the iPinYou platform in the weeks of March 11–17, June 8–15 and October 19–27. We use the impression and click data of 5 advertisers on June 8, 2013, containing a total of 1.8 million impressions and 1,200 clicks. As in the main text, let index advertisers (buyers) and let index impressions/users (items in FPPE terminology). The five advertiser are labeled by number and their categories are given: 1459 (Chinese e-commerce), 3358 (software), 3386 (international e-commerce) and 3476 (tire). From the raw log data, the following dataset can be extracted. The response variable is a binary variable that indicates whether the user clicked the ad or not. The relevant predictors include a categorical variable Adexchange of three levels that records from which ad-exchange the impression was generated, a categorical variable Region of 35 levels indicating provinces of user IPs, and finally 44 boolean variables, each a Usertag, indicating whether a user belongs to certain user groups defined based on demographic, geographic and other information. We select the top-10 most frequent user tags and denote them by . Both Adexchange and Usertag are masked, and we do not know their real-world meaning.

Simulate advertisers with logistic regression. The raw data contains only five advertisers. In order to simulate new realistic advertiser, we logistic regression and then perturb the fitted coefficients to generate more advertisers. We posit the following logistic regression model for click-through rates (CTRs). For a user that saw the ad of advertiser , the click process is governed by

where the weight vectors are the coefficients to be estimated from the data. Note that and are absorbed in the intercept. By running 5 logistic regressions, we obtain regression coefficients . To visualize the fitted regression, in Figure 4 we show the estimated click-through rate distributions of the five advertisers. The diagonal plots are the histogram of CTRs, and the off-diagonal panels are the pair-wise scatter plots of CTRs. To generate more advertisers, we take a convex combination of the coefficients ’s, add uniform noise, and obtain a new parameter, say . Given an item, the CTR of the newly generated advertisers will be . The value distribution is the historical distribution of the simulated advertisers’ predicted CTRs of the 1.8 million impressions.

6.3.1 Revenue Coverage

Setup. In this section we aim to produce confidence interval of the revenue with the CI constructed from Eq. 26. Firstly, the sum equals times the average price-per-utility of advertisers, a measure of efficiency of the system. Secondly, since most quantities in FPPE, such as revenue and social welfare, are smooth functions of pacing multipliers , being able to perform inference about a linear combination of ’s indicates the ability to infer first-order estimates of those quantities.

An experiment has parameters . Here is the number of items and the number of advertisers. Parameter is the exponent of the finite-difference stepsize in Eq. 22, i.e, . We try over the grid . Finally, is the proportion of advertisers that are not budget-constrained (i.e., ). To control in the experiments, we select budgets as follows. Give infinite budgets to the first advertisers. Initialize the rest of the advertisers’ budgets randomly, and keep decreasing their budgets until their pacing multipliers are strictly less than 1. In the experiment , we first compute the pacing multiplier in the limit market using dual averaging (Xiao 2010, Gao et al. 2021, Liao et al. 2022). Then we sample one FPPE by drawing values from the synthetic value distribution obtained previously. Now given one FPPE, apply the formula in Eq. 26 to construct CI and record coverage. The reported coverage rate for an experiment with parameters is averaged over 100 FPPEs.

Results. Representative results are presented in Table 3; we present the full table in Table 6. As the number of item increases, we observe the empirical coverage rate achieving the nominal 90% coverage rate, while the width of confidence interval is narrowing. We also observe that the confidence interval is robust against the Hessian estimation and the proportion of unpaced buyers; for different choices of exponent in the differencing stepsize ( in Eq. 22) and proportion of unpaced buyers (), the coverage performance remains similar.

| buyers | 20 | 50 | 80 | ||||||||||

| 0.05 | 0.10 | 0.20 | 0.30 | 0.05 | 0.10 | 0.20 | 0.30 | 0.05 | 0.10 | 0.20 | 0.30 | ||

| items | |||||||||||||

| 0.40 | 100 | 0.79 (1.72) | 0.79 (1.82) | 0.93 (1.87) | 0.9 (1.81) | 0.87 (1.84) | 0.81 (1.91) | 0.89 (1.82) | 0.88 (2.00) | 0.81 (1.89) | 0.89 (1.89) | 0.97 (1.97) | 0.9 (1.95) |

| 200 | 0.88 (1.33) | 0.88 (1.36) | 0.87 (1.35) | 0.9 (1.34) | 0.88 (1.32) | 0.93 (1.36) | 0.89 (1.37) | 0.94 (1.40) | 0.87 (1.37) | 0.93 (1.37) | 0.88 (1.42) | 0.86 (1.42) | |

| 400 | 0.84 (0.93) | 0.88 (0.99) | 0.93 (0.99) | 0.91 (0.98) | 0.9 (0.95) | 0.94 (0.98) | 0.92 (0.98) | 0.84 (1.00) | 0.88 (0.97) | 0.85 (0.98) | 0.86 (1.01) | 0.85 (1.01) | |

| 600 | 0.89 (0.76) | 0.88 (0.79) | 0.9 (0.81) | 0.89 (0.80) | 0.8 (0.77) | 0.87 (0.80) | 0.81 (0.80) | 0.92 (0.83) | 0.86 (0.80) | 0.83 (0.80) | 0.97 (0.83) | 0.89 (0.83) | |

6.3.2 Treatment Effect Coverage

Setup. In this experiment, we fix the differencing stepsize in Hessian estimation to be and the proportion of unpaced buyers to be 30%, which is a realistic number for real-world auction platforms.

An experiment has parameters , where is the number of items, the number of users, and the treatment probability (see Section 5.4). To model treatment application, we use the shift of value distribution. Choose two sets of logistic regression parameters, and . Then if a user is applied treatment , then its value to buyer will be , . In an experiment, the limit revenues in the two limit markets and , and the limit treatment effect will be calculated first. Then we perform the a/b test experiments 100 times, and construct 100 CIs for the treatment effect. We report coverage rates and widths of CIs.

Results. Representative results are presented in Table 4; in Table 5 we present the full results. First, the overall coverage rates across different market setups and treatment probabilities are around the nominal 90%, and the width of confidence interval shrinks as sample size grows. Second, when the number of items is sufficiently large (say over 400), we observe a -shape relationship between the width of CI and treatment probability ; the CI widths are wider when is close to the extreme points (say 0.1 and 0.9) than when stays away from the extreme points. This is explained by the treatment effect variance formula in Theorem 5.6. Holding the two variances fixed, the treatment effect variance tends to infinity if we send or .

| items | 100 | 200 | 400 | 600 | |

| buyers | |||||

| 50 | 0.1 | 0.88 (8.45) | 0.88 (4.75) | 0.92 (1.87) | 0.88 (1.54) |

| 0.3 | 0.95 (3.49) | 0.96 (2.37) | 0.86 (1.28) | 0.93 (1.03) | |

| 0.5 | 0.92 (3.76) | 0.95 (5.05) | 0.9 (1.26) | 0.94 (0.98) | |

| 0.7 | 0.85 (3.10) | 0.95 (2.27) | 0.98 (1.85) | 0.95 (1.28) | |

| 0.9 | 0.76 (3.36) | 0.87 (2.87) | 0.92 (2.78) | 0.96 (9.33) |

7 Conclusion

We introduced a theory of statistical inference for Fisher markets, resource allocation systems that deploy the CEEI mechanism, and first-price auction platforms. We showed that quantities observed in the finite market equilibrium observed from these systems are good estimators of their corresponding limit market values. We presented convergence rate results, asymptotic distribution characterizations, local minimax optimality results, and constructed confidence interval tools. Finally, we showed how to use these tools to develop a theory of statistical inference in A/B testing under competition effects.

A few open questions remain. In practice, the item arrival process exhibits nonstationarity and seasonality. A set of statistical theory for LFM and FPPE that incorporates temporal dependence is desirable. It would also be desirable to design a notion of online confidence intervals for the limit market, since, in practice, items arrive on the system sequentially. For FPPE we assumed the absence of degenerate buyers in Section 5.2. A fully general asymptotic and inferential theory for FPPE is also interesting. Finally, we restricted our attention to the first-price setting. In practice, second-price auctions are also widespread. A theory of statistical inference for second-price auctions is also desirable, though we expect it to be significantly weaker, due to computational complexity barriers, as well as non-uniqueness issues.

This research was supported by the Office of Naval Research awards N00014-22-1-2530 and N00014-23-1-2374, and the National Science Foundation awards IIS-2147361 and IIS-2238960. This work has been presented in Conference on Neural Information Processing Systems (2022), International Conference on Machine Learning (2023), Sequential Markets and Mechanism Design session in INFORMS annual meeting (2023) Stanford Rising Star Workshop (2024), Workshop on Marketplace Innovation (2024) for helpful discussion, and invited for presentation by the Ads Experimentation team at Meta. We thank attendees of these workshops and conferences for many helpful discussions.

References

- Aleksandrov et al. (2015) Aleksandrov M, Aziz H, Gaspers S, Walsh T (2015) Online fair division: Analysing a food bank problem. arXiv preprint arXiv:1502.07571 .

- Andrews (1994) Andrews DW (1994) Asymptotics for semiparametric econometric models via stochastic equicontinuity. Econometrica: Journal of the Econometric Society 43–72.

- Andrews (1999) Andrews DW (1999) Estimation when a parameter is on a boundary. Econometrica 67(6):1341–1383.

- Andrews (2001) Andrews DW (2001) Testing when a parameter is on the boundary of the maintained hypothesis. Econometrica 69(3):683–734.

- Aronow and Samii (2017) Aronow PM, Samii C (2017) Estimating average causal effects under general interference, with application to a social network experiment. The Annals of Applied Statistics 11(4):1912–1947.

- Athey et al. (2018) Athey S, Eckles D, Imbens GW (2018) Exact p-values for network interference. Journal of the American Statistical Association 113(521):230–240.

- Athey and Haile (2007) Athey S, Haile PA (2007) Nonparametric approaches to auctions. Handbook of econometrics 6:3847–3965.

- Bajari et al. (2021) Bajari P, Burdick B, Imbens GW, Masoero L, McQueen J, Richardson T, Rosen IM (2021) Multiple randomization designs. arXiv preprint arXiv:2112.13495 .

- Balseiro et al. (2021) Balseiro S, Kim A, Mahdian M, Mirrokni V (2021) Budget-management strategies in repeated auctions. Operations research (3):859–876.

- Balseiro et al. (2015) Balseiro SR, Besbes O, Weintraub GY (2015) Repeated auctions with budgets in ad exchanges: Approximations and design. Management Science 61(4):864–884.