Financial Assets Dependency Prediction Utilizing Spatiotemporal Patterns

Abstract

Financial assets exhibit complex dependency structures, which are crucial for investors to create diversified portfolios to mitigate risk in volatile financial markets. To explore the financial asset dependencies dynamics, we propose a novel approach that models the dependencies of assets as an Asset Dependency Matrix (ADM) and treats the ADM sequences as image sequences. This allows us to leverage deep learning-based video prediction methods to capture the spatiotemporal dependencies among assets. However, unlike images where neighboring pixels exhibit explicit spatiotemporal dependencies due to the natural continuity of object movements, assets in ADM do not have a natural order. This poses challenges to organizing the relational assets to reveal better the spatiotemporal dependencies among neighboring assets for ADM forecasting. To tackle the challenges, we propose the Asset Dependency Neural Network (ADNN), which employs the Convolutional Long Short-Term Memory (ConvLSTM) network, a highly successful method for video prediction. ADNN can employ static and dynamic transformation functions to optimize the representations of the ADM. Through extensive experiments, we demonstrate that our proposed framework consistently outperforms the baselines in the ADM prediction and downstream application tasks. This research contributes to understanding and predicting asset dependencies, offering valuable insights for financial market participants.

keywords:

Asset dependency , correlation , time series forecasting , portfolio optimization.[label1]organization=Hong Kong University of Science and Technology, country=Hong Kong

[label2]organization=BNU-HKBU United International College, city=Zhuhai, state=Guangdong, country=China

Model asset correlations as an Asset Dependency Matrix (ADM).

Employ static and dynamic transformation to optimize the ADM representations.

Leverage video prediction method to capture the spatiotemporal dependencies among assets.

Superior forecasting performance in ADM prediction and downstream application tasks.

1 Introduction

Financial assets, such as stocks, securities, and derivatives, exhibit diverse interdependencies, giving rise to a complex structure of dependencies among these assets (Elton and Gruber, 1973; Ane and Kharoubi, 2003). For instance, stocks within the same industry often exhibit a collective response to market news, causing them to move in a synchronized manner. Moreover, the price fluctuations observed in one industry at a specific time can subsequently impact its downstream industries. The dependency structure of the financial market is very complex, and the ability to predict it results in significant financial advantages. As an illustration, one practical approach to mitigate portfolio risk is through diversification across distinct asset classes that exhibit either independence or negative correlation. This strategy safeguards against the simultaneous loss of all assets in the event of a negative occurrence, such as an unfavorable news release.

The measurement of asset dependency encompasses various methodologies, such as analyzing the correlation and covariance coefficients between two assets. When considering a collection of assets, these pairwise dependencies can be systematically arranged within a matrix, termed Asset Dependency Matrix (ADM). For instance, when employing the correlation coefficient as a measure of asset dependency, the ADM corresponds to the widely recognized correlation matrix. Various statistical methods have been proposed for predicting future ADMs. A simple prediction model (Elton et al., 1978) uses the correlation matrix computed from the time window ending at as the predicted ADM for . Subsequent advancements have proposed enhancements considering asset groups, financial indexes, and beta estimations (Elton et al., 1977; Baesel, 1974; Blume, 1975; Vasicek, 1973). A recent study presented a methodology utilizing the Cholesky decomposition and support vector regression for dynamic modeling and forecasting of covariance matrices (Bucci et al., 2022). This methodology ensures the positive definiteness of forecasted covariance matrices, which are leveraged by different parametrizations and methodologies for accurate covariance matrix forecasting (Verzelen, 2010; Damodaran, 1999). However, prevailing financial solutions suffer from restrictive statistical assumptions and oversimplify time-varying dependence structures to linear or approximate linear relationships between variables. Furthermore, these solutions often encounter computational inefficiencies when dealing with large matrices, thereby impeding their scalability. Thus, deep learning models that are good at modeling nonlinear relationships and time-dependent patterns are a natural fit.

Asset dependencies exhibit both temporal and relational properties. Specifically, fluctuations in the return of one asset, triggered by specific events, have a consequential impact on the future price movements of both itself and other assets, thus indicating temporal dependency. In contrast, relational dependency pertains to the intricate interconnections among a set of assets, causing them to respond similarly to financial events. For example, the stocks in the high-tech sector are inherently correlated (similar) because of the common growth and high-leverage nature of the companies which tend to respond similarly to events such as an increase in interest rates. The evolution of the financial market over time is influenced by both temporal and relational dependencies among assets. A notable illustration is the phenomenon known as “sector rotation” in finance, where investors strategically adjust their investments across various sectors of the economy to leverage the diverse performance of sectors during different phases of the economic cycle. This strategic approach allows investors to capitalize on the shifting dynamics of sectors, aligning their portfolios with the prevailing economic conditions.

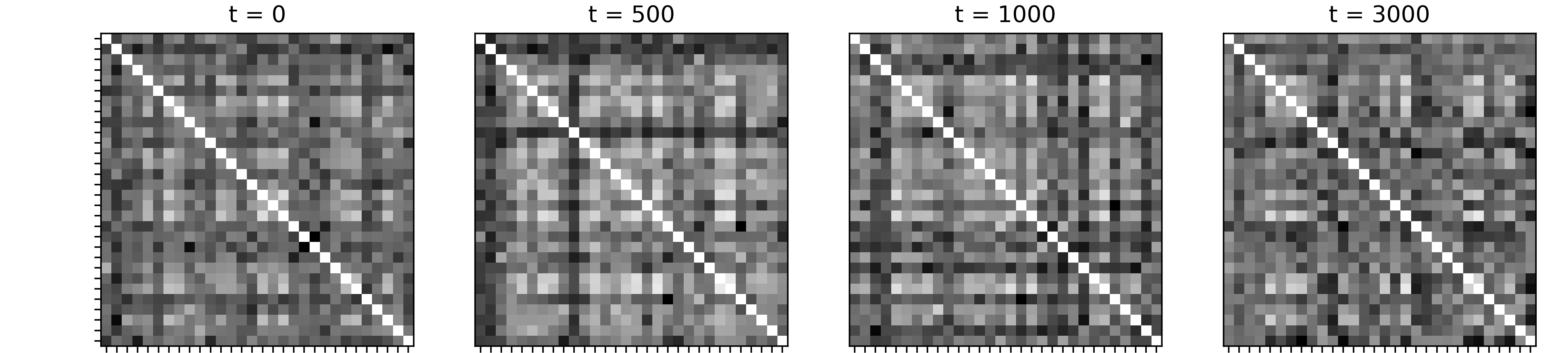

In this paper, we formulate the sequential ADM prediction task as forecasting the future ADM based on a sequence of past ADMs. We propose solutions inspired by video prediction problems (Oprea et al., 2020), aiming at predicting future image frames based on a sequence of past frames. Each frame corresponds to an ADM matrix, with each frame pixel representing the correlation between two assets. Video frame data are characterized by spatiotemporal properties since a pixel’s value is related to its neighboring pixels and pixels in previous frames. Deep learning-based spatiotemporal models, e.g., Convolutional Recurrent Neural Network (CRNN), have been successful due to their ability to extract features in both spatial and temporal dimensions (Shi et al., 2015; Mathieu et al., 2015; Hsieh et al., 2018; Babaeizadeh et al., 2017; Wang et al., 2018). A major challenge of directly applying CRNN to ADM prediction is that pixels of the same object are naturally grouped spatially in the images, while the correlation coefficients between the assets do not have predefined placement in the ADM. In Figure 1(a), assets are placed randomly in the matrix. We can see there are no clear asset dependencies shift patterns across the sequence of frames. Thus, CRNN will not be effective if it directly takes ADMs with arbitrarily placed assets as input. Hence, it is imperative to devise suitable transformation strategies to optimally align the assets for the disclosure of the evolution pattern of ADM. This is essential for enhancing the accuracy of forecasting future ADM. Since the transformation explicitly or implicitly repositions the assets in the ADM, we term the locality patterns within the transformed ADM as assets’ spatial dependencies.

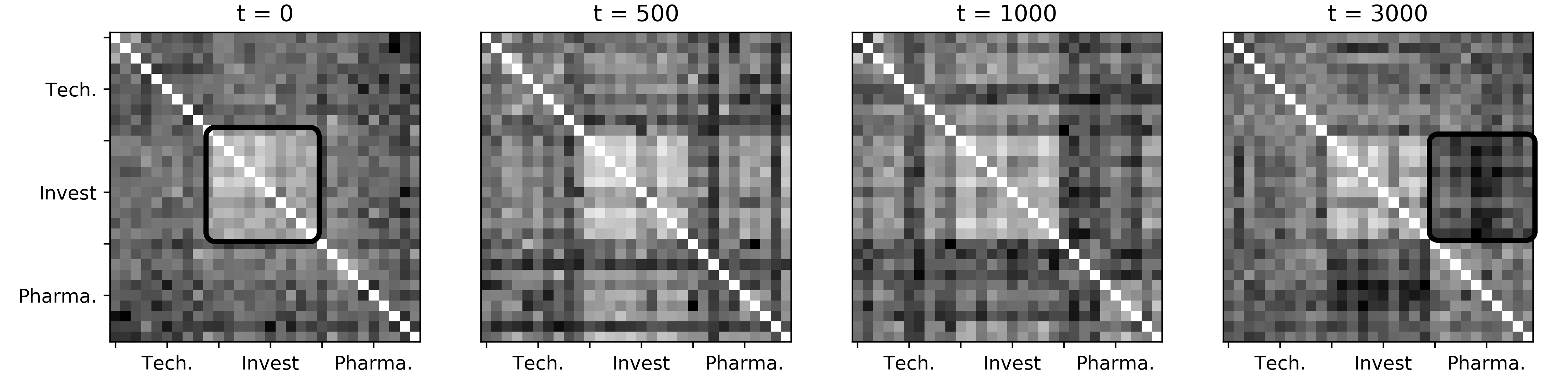

Figure 1(b) illustrates the idea. Ten assets are selected from each of the technology, investment, and pharmaceutical sectors. Assets from the same industry are placed next to each other in the matrix (i.e., having sequential indexes). Each matrix entry represents the correlation coefficient between two assets, where white indicates a coefficient of 1 and black a coefficient of -1. At , we can observe that the center region of the ADM, representing dependencies between assets in the “invest” sector, has a light color and hence positive correlations. On the other hand, the region to the right of the center, representing dependencies between assets in the “invest” sector and assets in the “pharmaceuticals” sector, has a dark color, showing weakly negative correlations between the two categories of assets. Both examples illustrate various strengths of spatial dependencies between the assets. As time elapses, groups of assets show different correlations. At , we can see that assets in “invest” remain generally positively correlated, while assets in “invest” and assets in “pharmaceuticals” have become more negatively correlated (color has become darker). Comparing Figure 1(a) and 1(b), we can see that the proper positioning of the assets can reveal the shift of asset dependencies across time. However, re-positioning assets by grouping them in the same sector, as illustrated above, is an intuitive but ad hoc solution, since there could be many driving factors that cannot be captured by a static and explicit rule (e.g. group by industry). The exploration of spatial dependency is to find an optimal way to arrange the spatially dependent assets in the asset space so that the CRNN works effectively.

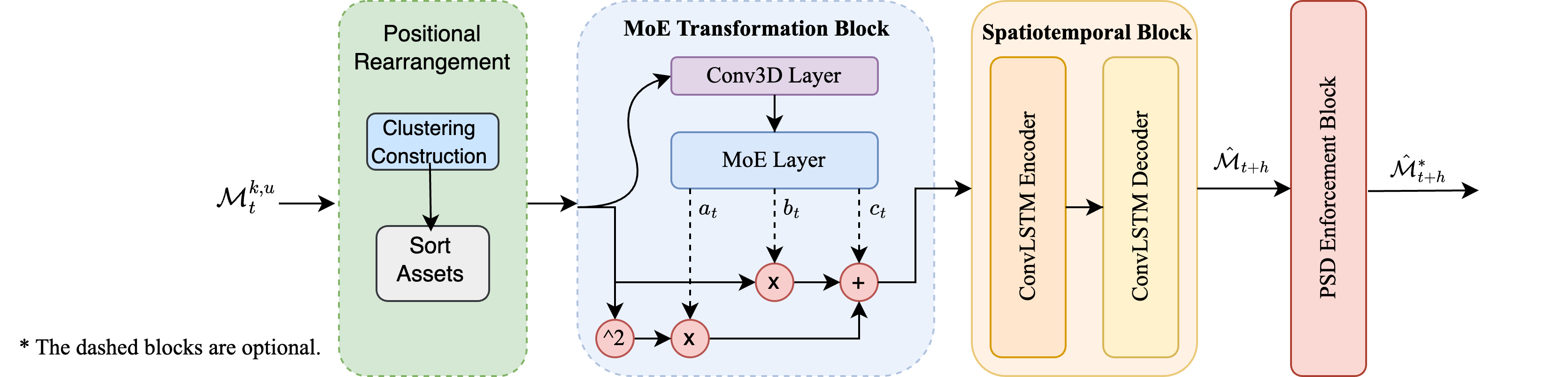

In this paper, we propose the Asset Dependency Neural Network (ADNN), an end-to-end neural network framework that unifies the ADM transformation and prediction processes. Drawing inspiration from representation learning (Bengio et al., 2014), we designate the task of mapping the ADM to its optimal representation as the ADM representation problem. We design static and dynamic transformation paradigms to address the ADM representation problem, which can be employed individually or jointly within the ADNN. For the static paradigm, we design the Positional Rearrangement algorithm that enhances ADMs’ locality property by allocating assets within the same cluster adjacent to each other. For the dynamic paradigm, we design the MoE Transformation block to address the time-varying relationships among multiple assets by dynamically reconfiguring the matrix arrangement over time. Specifically, we incorporate the Mixture of Experts (MoE) technique to capture the dynamic nature of market regimes, where each expert within the MoE framework is dedicated to modeling a specific economic period. Finally, the transformed matrix, containing fine-grained spatiotemporal patterns, is fed into the convolution recurrent neural network blocks to generate accurate forecasting. Experimental results demonstrate that the ADNN incorporating the two proposed transformation functions outperforms baseline methods in terms of ADM prediction accuracy and portfolio risk reduction.

Preliminary results of this research have been published in (Zhu et al., 2022). This comprehensive version included several new materials. Firstly, we present the Positional Rearrangement that solely alters the entry positions within the ADM, which can be used separately or combined with MoE transformation to achieve better prediction accuracy. This new approach leverages consistent grouping patterns to preprocess ADMs and excels in efficiency and effectiveness when applied to well-structured data. Furthermore, it enhances interpretability by providing insights into the repositioning of matrix entries. Secondly, we add the positive semi-definite (PSD) enforcement block to ensure the positive semi-definiteness property of the predicted ADMs, which is a common requirement in the finance domain. Thirdly, for the experiment, we add extensive ablation studies to validate the efficacy of the proposed framework components. We demonstrate how the mixture of experts, combined with a quadratic function in the current design, can effectively capture information from different regimes by visualizing the activation patterns of the experts in MoE. We study three market scenarios, starting from a simple one with only one market factor at each market phase to the real market data. The results conform to our expectation that MoE will activate a small set of experts when the market is simple and deploy more experts as the complexity of the market increases. Fourthly, to help understand the transformation, we visualize the ADMs before and after transformation. Finally, in addition to portfolio optimization presented in (Zhu et al., 2022), we study the application of ADNN to pair trading. To conclude, prior studies have primarily focused on the forecasting aspect of the ADM, considering it as a singular component of the overall framework. In contrast, this work presents a comprehensive pipeline that encompasses the entire process starting from data preprocessing to application, and substantiates the proposed framework with a broader range of experimental results.

2 Related Work

2.1 Conventional ADMs Prediction Models

Multivariate GARCH (MGARCH) models extend univariate volatility models to estimate time-varying asset dependencies. Initial MGARCH models (Bollerslev et al., 1988; Engle and Kroner, 1995) parameterize the conditional covariance matrix as a function of past information, i.e. the lagged conditional covariance matrix and returns. Although this generalization is flexible to dynamic structures, it is seldom applied to model large-scale assets due to the high number of unknown parameters to be estimated. Two modified MGARCH models were proposed to reduce the complexity of MGARCH models. One is the factor MGARCH models (Engle et al., 1990; Ng et al., 1992), which assume the dependency structure of assets generated from a few common factors, thus significantly reducing the number of parameters to be estimated. However, this modification has limitations in finding factors that can explain the dependency of assets adequately and impose an infeasible assumption that the volatilities of different assets are driven by the same factors. Another modification of MGARCH models is the Dynamic Conditional Correlation (DCC) model (Engle, 2002), which allows for different dynamics of individual assets and a linear dynamic structure of the correlation matrix. DCC models are easy to estimate because they assume a parsimonious dynamic structure of the conditional correlation matrix, with only two parameters to describe the time-varying pattern of correlations. One drawback of this simplification is that it is unjustifiable to assume all correlations evolve similarly regardless of the involved assets (Bauwens et al., 2006). In summary, MGARCH models balance between model flexibility and complexity by assuming specific structures on ADMs. Although this reduces model complexity and speeds up the estimation process, it suffers from misspecification of the dynamics of asset dependencies. Compared with existing works, our framework is more flexible since it does not require imposing structures on ADMs, making it capable of effectively capturing different temporal and spatial patterns.

2.2 Convolutional Recurrent Neural Network

Recent advances in deep learning provide abundant insights into modeling spatial and temporal signals from data. For modeling the sequential temporal information, early literature often applies Recurrent Neural Network (Ng et al., 2015; Sak et al., 2014). Long Short Term Memory (LSTM) (Hochreiter and Schmidhuber, 1997) was then proposed to tackle the vanishing and exploding gradient problems that occurred in long sequences. For modeling spatial information from data, convolutional neural network approaches (Goodfellow et al., 2016) were proposed where spatial signals are compressed and extracted through the slide of the convolution kernel over images. The encoding of the intertwined temporal and spatial relation is also discussed recently. Several works (Tran et al., 2015; Chen et al., 2018; Gebert et al., 2019) use 3D convolutional neural networks to extract spatial and temporal features. Although the additional dimensions enable neural networks to model both spatial and temporal correlations in the data, the compressed features are still local features without considering sequential patterns. To better model spatiotemporal sequence, Convolutional LSTM (ConvLSTM) (Shi et al., 2015) was proposed to model the spatial and temporal structures simultaneously by changing all the input data into tensors, through which the limitation of modeling the spatial information in LSTM and the constraint of modeling global sequential information in the 3D convolutional neural network is overcome. Based on the pioneering work of ConvLSTM, other advanced spatiotemporal modeling techniques are also proposed. For example, PredRNN (Wang et al., 2017) enables memory states to zigzag in two directions to break the constraint of memory storage in each cell unit, and Eidetic 3D LSTM (E3D-LSTM) (Wang et al., 2018) integrates 3D convolutions into its model to better store the short-term features and a gate-controlled self-attention module is designed to better model long-term relations. Due to the ADM representation problem introduced in Section 1, ConvLSTM based spatiotemporal techniques cannot be directly applied here and the transformation of ADMs is needed. In the AAAI version of this manuscript (Zhu et al., 2022), we tackle the problem with ADNN which unifies the transformation and prediction blocks and enables the transformation and prediction functions to be learned simultaneously.

2.3 Deep Learning for Portfolio Optimization

Deep learning models for financial portfolio optimization leverage the power of neural networks to learn complex patterns and relationships in financial data. Numerous research (Jiang et al., 2017; Ye et al., 2020; Wang et al., 2021; Hambly et al., 2023) have approached portfolio optimization as a strategic problem and have employed reinforcement techniques to optimize the selection of actions under different settings and constraints. Moreover, various studies have utilized deep-learning architectures to forecast stock prices and subsequently incorporated these predictions into the portfolio optimization process. These approaches encompass classical machine learning models (Ma et al., 2021; Chen et al., 2021b) for direct price prediction, Graph Convolutional Network (GCN) models (Chen et al., 2021a; Ye et al., 2021; Cheng et al., 2022) for relational property extraction, and hybrid models (Hou et al., 2021; Wu et al., 2023, 2022) that consider additional factors. Recent studies (Imajo et al., 2021; Uysal et al., 2023) have adopted an end-to-end approach that learns the optimal portfolio weights directly from raw price data as the input. Zheng et al. (2023) forecasts dynamic correlation matrix by incorporating normalizing flows to obtain high-quality hash representations and facilitates regularizers in imposing structural constraints. In this study, our focus lies in leveraging the spatiotemporal information embedded in the ADMs to forecast the asset dependencies within a group of assets, which is then employed for portfolio optimization.

3 Problem Definition

3.1 ADM Definition

In financial convention, given the historical daily prices of an asset , where denotes the price at time , the log return of the asset at time is calculated by:

| (1) |

where logarithm normalization is applied to the price data so that the derived returns are weakly stationary. Denote the return of asset at time as and denote the dependency measurement between asset and asset at time . If the sample covariance is picked, in period is calculated as follows:

| (2) |

where denotes the time span of calculating the asset dependency coefficients and means the average return of asset in the time interval. It is natural to use matrices to represent all pairwise dependencies. Hence, ADM at time , denoted as , can be formulated as:

| (3) |

3.2 ADM Prediction Model

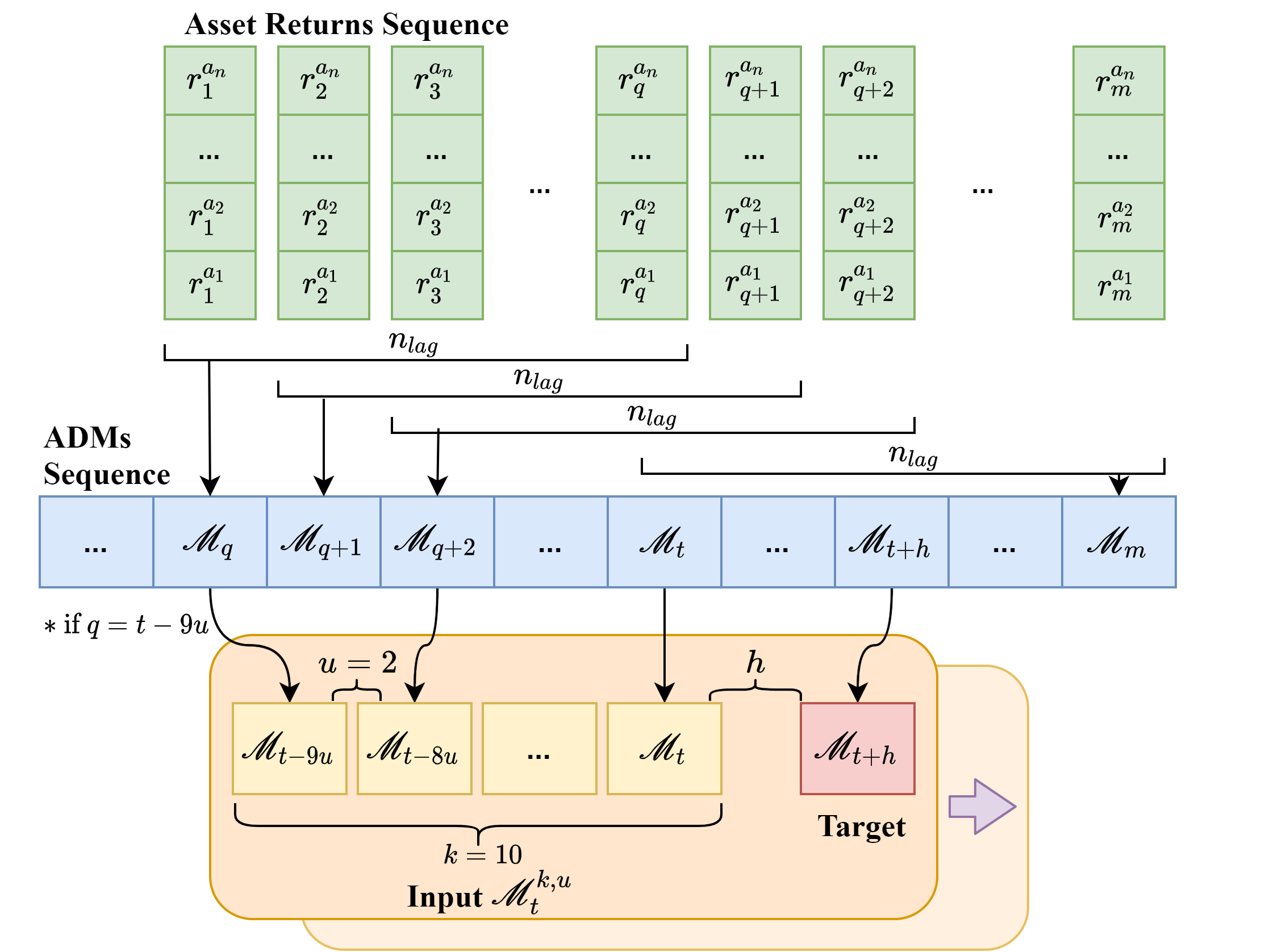

Given a historical ADM sequence denoted as:

| (4) |

where denotes the length of the input sequence, denotes the current timestamp and denotes the rolling distance between each input matrix in the day unit. Figure 2 illustrates the construction process of the ADM sequence. , where denotes the number of channels, and , respectively, denote the width and height of ADM. Our target is to predict , where denotes the horizon, which is the duration that an investor expects to hold a portfolio. For example, if the portfolio is rebalanced monthly, i.e., the investors are interested in the ADM one month later, should be set to (monthly trading days). We formulate the ADM prediction model as :

| (5) |

where denotes the model parameters of and denotes the predicted ADM.

4 Methodology

The ADM forecasting problem involves two main challenges: (1) addressing the ADM representation problem discussed in Section 1, (2) accurately modeling the temporal and spatial signals encoded in historical ADMs. For the first challenge, we propose two alternative ADM transformation strategies: (1) the positional rearrangement block which statically alters the asset order in ADM construction process, and (2) the end-to-end transformation block which dynamically learns the optimal representations of the input ADMs. To address the second challenge, we propose to integrate a spatiotemporal block into the prediction task. Figure 3 illustrates the overall architecture. Note that two transformation strategies can be combined to further strengthen the ability of the prediction model. The details of the framework are explained in the following sections.

4.1 Positional Rearrangement

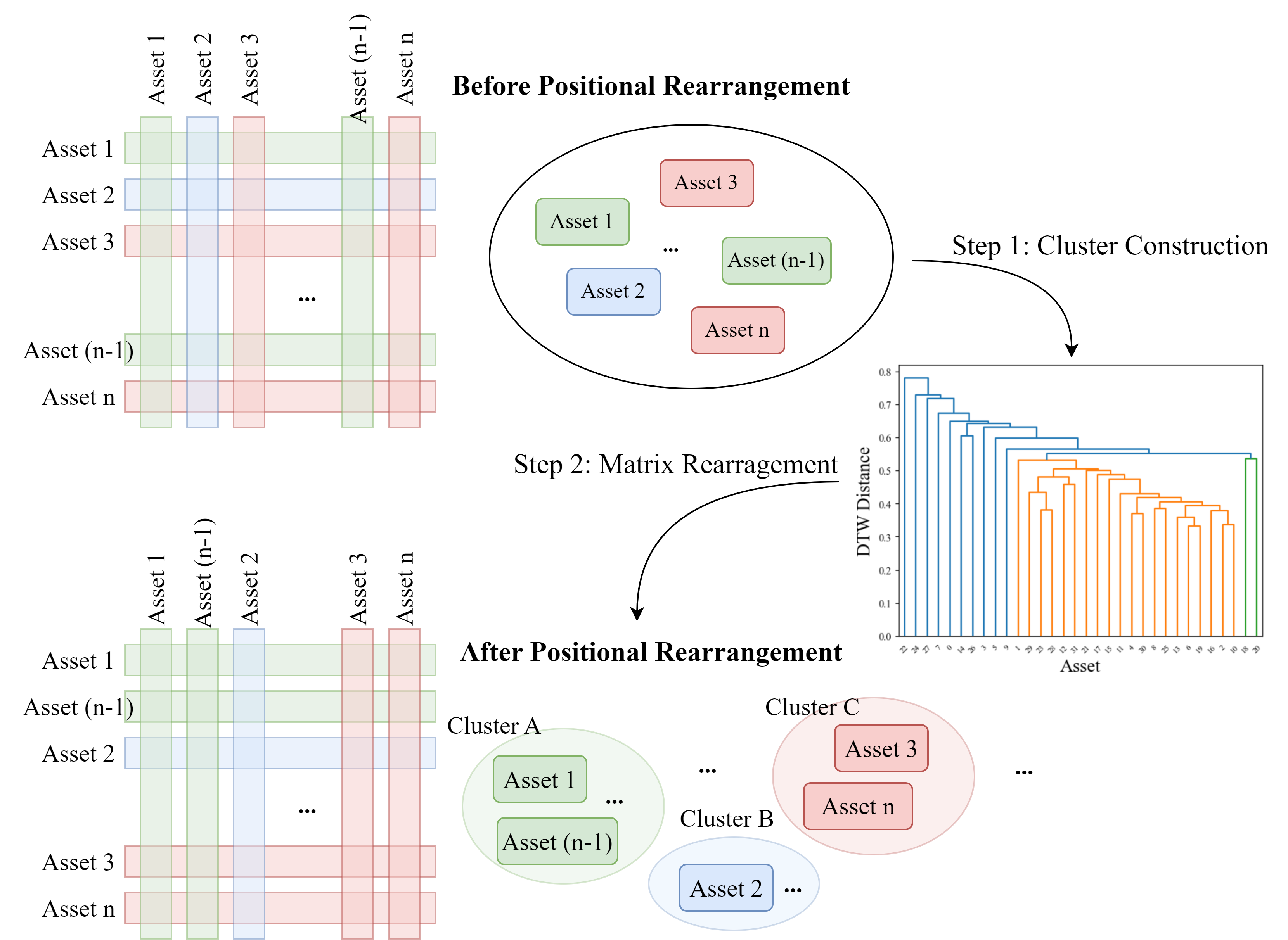

As introduced in Section 1, the direct application of spatiotemporal prediction models on ADM sequence suffers from the ADM representation problem due to entries in ADM not having predefined placement to facilitate spatiotemporal modeling, whereas pixels in images are naturally grouped according to the “shape”, “color” and “texture” features ping Tian et al. (2013). This lack of proper organization of asset dependencies obscures the information compression and boundary identification of ADM, making the convolution techniques less effective. Thus, it is necessary to transform the ADMs so that the assets’ relational features can be better revealed before the downstream convolution kernel. Given the established stock market sector analysis, assets within the same industry exhibit concurrent behavior. Our approach aims to enhance the locality property of the ADM by strategically rearranging the matrix columns and rows in the preprocessing stage. This positional rearrangement technique is employed to exploit the inherent relationships among assets, e.g., those belonging to the same industry or displaying concurrent patterns, further improving the effectiveness and accuracy of the ADM representation.

The positional rearrangement procedure involves two key steps: clustering construction and matrix rearrangement, as illustrated in Figure 4. We begin by considering a set of assets that are initially arranged randomly within the corresponding ADM. Financial data generally contains rich contextual information, including sector details, historical prices, volumes, etc., which can be used to divide the entire asset group into multiple distinct clusters. Specifically, we propose a universal approach that uses hierarchical clustering based on dynamic time warping distance (DTW) Petitjean et al. (2011) between assets’ close prices for the cluster construction step. DTW enables flexible alignment and identification of similar patterns despite temporal variations, which makes it appropriate for financial price series exhibiting variations in terms of timing and speed. In addition, hierarchical clustering provides the ability to reveal nested relationships at different levels of granularity, reflecting the varying degrees of similarity and hierarchical structures observed in financial assets based on factors such as sectors, industries, or market segments Altomonte and Rungi (2013). In the second step, we sort assets based on the clustering outcomes, deriving new ADMs that represent rearrangements compared to the original ADMs. Due to the hierarchical tree-like structure produced by agglomeration clustering, converting it into a sorted asset list is straightforward. The complete procedure of positional rearrangement is illustrated in Algorithm 1. Note that to enhance efficiency, we utilize coarse-grained monthly average return data when calculating the DTW distance.

4.2 MoE Transformation Block

Despite the effective enhancement of the ADM’s locality property through the positional rearrangement, it does not fully capture the time-varying patterns of underlying assets’ dependencies. A prime illustration is sector rotation driven by changing market conditions, economic factors, and investor sentiment. Sector rotation in finance refers to the cyclical pattern in which money flows between different sectors of assets. This concept is based on the idea that not all sectors of the economy perform equally well at the same time, due to varying economic conditions. When a particular sector comes into favor, the increased focus and investment can lead to assets within that sector moving more in unison leading to higher correlation. When the capital flows out of the sector, the assets return to normal correlation level. Thus, the dynamic and flexible end-to-end transformation is required to effectively capture the evolving dependencies.

4.2.1 Quadratic Approximation

Given the universal approximation theorem Scarselli and Chung Tsoi (1998), it is intuitive to consider the fully connected network (FCN) as the transformation function. However, due to the large size of ADMs and the high-order nature of the transformation, achieving convergence with FCN can be challenging. Therefore, we propose using the polynomial function to approximate the optimal transformation function Eden et al. (1986); Jacquin (1993). Specifically, we adopt the quadratic function, which is widely recognized as an effective solution in function approximation problems Torokhti and Howlett (2001); Boubekeur and Schlick (2007). The quadratic function strikes a balance between capturing linear and high-order dependencies, making it well-suited for modeling the intricate complexity of financial markets with less risk of over-fitting. The quadratic function performs an element-wise transformation by assigning a new value to each entry of the ADM, infusing its ability to approximate both position rearrangement and data scaling. The formula of the quadratic transformation function can be written as follows:

| (6) |

where , , and denote, respectively, the coefficient tensor of the quadratic term, the linear term, and the constant term, all of which have the shape . ‘’ denotes the Hadamard product. , where denotes the coefficient function outputting given parameter set and input . Coefficients are output by functions and similarly.

We learn the coefficient functions , , and from the input ADM by designing proper neural architectures. To enhance the feature extraction from the input ADM sequence and reduce dimensionality, we apply two consecutive 3D convolutional layers Goodfellow et al. (2016) to extract the latent feature.

| (7) |

where [, ] denote the 3D convolution layers, and ‘’ denotes the convolution operator. The resulting output is subsequently passed to the following NN blocks, where each block learns its respective coefficient function. A straightforward way to model the coefficient function is by employing the Multilayer Perceptron (MLP) Goodfellow et al. (2016) However, asset correlation could be influenced by various market factors such as macro-economy, interest rates, industry rotation, political events, etc. While MLP offers a simple means of approximating the coefficients, it fails to encode the complex market factors, leading to generalized rules that may not be suitable for all market scenarios. For example, in the presence of different market states caused by different market factors/events, the dependency between two stocks may vary across these states. Using a single MLP may result in a model that applies uniformly to all market situations, often leading to over-generalization of the model and suboptimal performance.

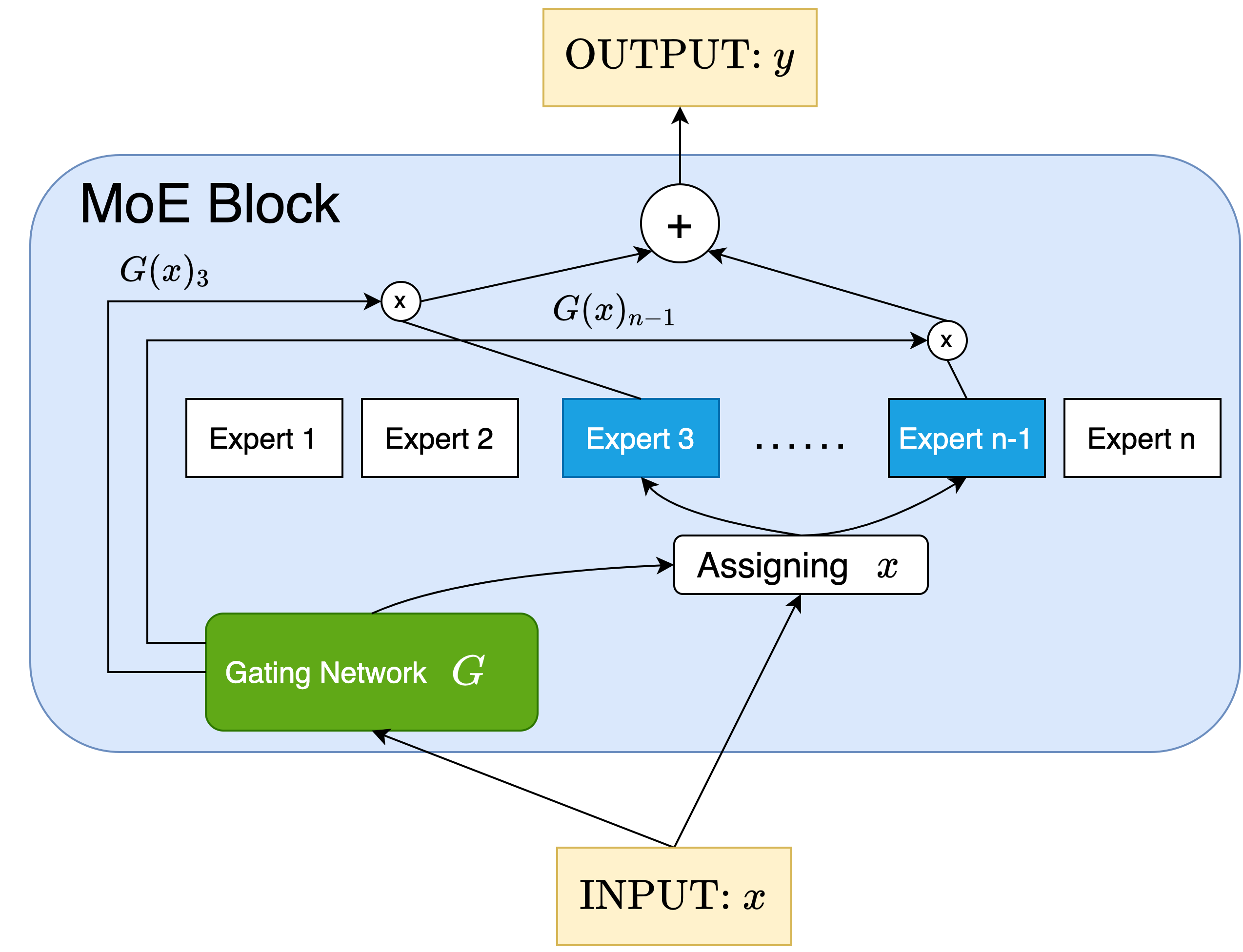

4.2.2 Mixture of Expert Transformation

Inspired by Mixture of Experts (MoE) Jacobs et al. (1991)’s success in solving complex data problems with multiple data regimes in the dataset Eigen et al. (2013); Shazeer et al. (2017); Ma et al. (2018), we apply MoE to the transformation block for learning the transformation function that can distinguish different market factors and transform input ADM to proper representation. A MoE block comprises a gating network and multiple subnets, each of which is an MLP (expert). It can achieve improvement, especially for complex datasets due to the gating network’s capability of selecting a sparse combination of experts to process inputs with different data patterns. In our case, the gating network in MoE acts as a knowledgeable manager to decide which experts should be assigned the task of transforming and combine their results afterward. The critical difference between MLP and MoE in constructing is that MLP learns a single rule that generalizes all the complex market factors while MoE introduces sparse combinations of experts that specialize in individual market factor(s) and unify their outputs to generate a better ADM representation.

The structure of an MoE block can be summarized as follows. denotes The output of the gating network, and denotes the output of the -th expert network for a given input , where (see Equation 7) in our setting. To ensure load balancing, a tunable Gaussian noise, controlled by a trainable weight matrix , is introduced to encourage the gated network to pick different sets of experts. Sparsity is achieved by selecting only the top expert values using the gating function Jordan and Jacobs (1993) with a trainable weight matrix . The output of the MoE module is calculated by:

| (8) | ||||

The sparsely-gated feature is an indispensable component to the improvement of prediction accuracy, as selecting only a sparse set of experts each time ensures less noise and over-generalization of each expert. Figure 5 illustrates the idea. Given experts, this design increases the learning capacity of the transformation function by offering different combinations of experts, whereas an MLP can only learn one generalized rule for all inputs. Moreover, it aids in noise reduction as each expert can focus on its specialized area.

In summary, we employ three separate MoE blocks to model the coefficient functions , , and used in the quadratic approximation (see Equation 6), shown as follows:

| (9) | ||||

4.3 Spatiotemporal Block

After passing through the transformation block introduced in Section 4.2, the transformed ADM sequence is sent to the spatiotemporal block for the extraction of the spatial and temporal signals encoded in . Specifically, we adopt the ConvLSTM Shi et al. (2015) as the spatiotemporal block due to its superior performance in spatiotemporal-related tasks. The core unit of the ConvLSTM network is the ConvLSTM cell. The input and intermediate states fed to the cell are tensors with the shape . Denote the input state as , memory state as , hidden state as , and gated signals as , , , at each timestamp of one cell. The future state of a certain ADM entry in the matrix is determined by the inputs and past states of its local neighbors. This can easily be achieved by using a convolution operator in state-to-state and input-to-state transitions:

| (10) | ||||

4.4 Loss Function

We employ the mean square error (MSE) loss to optimize model parameters. Denote the output matrix of the spatiotemporal block as . Considering the inherent symmetry of ADM, we confine the loss calculation to the upper triangular part of to reduce computational complexity and redundancy. The MSE loss is then computed as follows:

| (11) |

where denotes the predicted dependency measurement of two assets and . To generate the forecasted ADM, we construct a symmetric matrix by duplicating the values from the upper triangular part of as follows:

| (12) |

4.5 PSD Enforcement Block

Positive semidefiniteness (PSD) is a crucial property of ADM where all of its eigenvalues are non-negative, which ensures mathematical consistency, meaningful interpretations, and reliable subsequent applications. For example, consider portfolio variance denoted by Equation 13 where represents the weight of asset in the portfolio. If the covariance matrix fails to meet the PSD condition, the resulting portfolio will possibly incur a negative variance. This implies a constraint that the covariance matrix must be positive semidefinite.

| (13) |

The ADM forecasted by the above structure does not inherently guarantee positive semi-definiteness. To address this limitation, we introduce a PSD enforcement block. We obtain the nearly identical PSD matrix by setting negative eigenvalues of to zero Xu et al. (2021), shown as follows:

| (14) | ||||

where is an orthogonal matrix of eigenvectors and is a diagonal matrix of eigenvalues. Even though this approach does not guarantee finding the exact closest PSD matrix, it efficiently leverages the symmetry and near PSD property of matrix to approximate the closest PSD matrix.

5 Experiment

In the experiment, we assess the performance of the proposed framework using real-world datasets and conduct a comprehensive analysis of the model behaviors.

5.1 Experimental Settings

5.1.1 Datasets

We construct a pool of real-world stock data from S&P-100, NASDAQ-100, and DJI-30, encompassing the most impactful companies over the past 15 years (from 2005/09/27 to 2020/08/05). We retain stocks with complete closing price data throughout the whole period, resulting in 133 stocks in the pool, each of which has a time series of 3740 price data points. The ADM sequences can be generated from the stock price data as depicted in Figure 2. A general guideline from finance is to choose the time lag at least as large as the number of assets to avoid the out-of-sample problem Tashman (2000). However, if is too large, the model may be incapable of capturing short-term (e.g. monthly) dynamics of the ADM sequences. To strike a balance, we set and . Without the loss of generality, we construct stock datasets by randomly picking stocks from the pool, each of which contains stocks (see Appendix for detailed asset components). In each dataset, we first obtain = log return data points. By setting , we generate = ADMs. In this paper, we mainly study the ADMs’ monthly evolution. We set , , resulting in the moving window with length = . As the rolling windows move forward each day, we generate = data samples. We select the first of ADM sequences as training samples (including validation) and the remaining as testing samples. The model performance is evaluated on each stock dataset independently to guarantee the generosity of the experimental outcome.

5.1.2 Evaluation Metrics

We evaluate ADM prediction accuracy using two metrics: mean square error (MSE) and gain. The MSE metric measures the average squared difference between the predicted ADMs and the groundtruth ADMs. Given the symmetry of ADMs, we use only the upper triangular part for computation. The Gain metric quantifies the improvement in prediction accuracy compared to the conventional practice of using the previous ADM as the future ADM in finance Elton et al. (1978). A larger gain indicates better performance over the conventional approach. Denote the i-th forecasted ADM as , groundtruth ADM as , and the previous ADM as . Formally, the evaluation metrics are computed by:

5.1.3 Baselines

We compare the proposed framework to six baselines covering two classical statistical models for correlation forecasting and four spatiotemporal deep learning models specifically tailored for the sequential forecasting of ADM For fairness, we intentionally exclude methods that incorporate external information such as interest rates and financial indexes from the comparison. The baseline models are listed as follows.

- •

-

•

DCC-GarchEngle (2002) is a statistical model that incorporates the dynamic nature of correlation by parameterizing the conditional correlations. It forecasts the future correlation matrix and utilizes the predicted correlation matrix to generate covariance matrices.

-

•

Long-Short-Term-Memory network (LSTM) Hochreiter and Schmidhuber (1997) is a widely used deep learning model for sequence prediction. In our approach, we flatten each input ADM into a 1D vector and use a standard LSTM implementation.

-

•

Raw-ConvLSTM Shi et al. (2015) directly feeds the raw ADM sequences to the convolutional LSTM network (ConvLSTM) without any preprocessing or transformation.

-

•

FCN-ConvLSTM is an end-to-end framework based on ConvLSTM. It incorporates a fully connected network (FCN) to transform the input ADM, which is then passed to the ConvLSTM for the prediction task.

-

•

Convolution-3D (Conv3D) Chen et al. (2018) is a deep learning model with an encoder-decoder architecture. The encoder and decoder contain three consecutive 3D-convolution layers respectively.

| Name | Range | Optimal |

| Common | ||

| k | {2,3,6,10,12} | 10 |

| {3,5} | 5 | |

| optimizer | {Adam, SGD} | Adam |

| grad_clip | {1,5,10} | 10 |

| ADNN | ||

| {64, 128, 256, 384, 512} | 128 | |

| init_lr | {1e-2, 5e-3, 1e-3, 5e-4} | 5e-4 |

| {2, 4, 8, 16} | 8 | |

| {1,2} if | ||

| {1,2,3,4} if | ||

| {1,2,4,8} if | 4 | |

| {1,4,8,16} if | ||

| FCN-ConvLSTM | ||

| {128, 256, 384, 512, 640} | 256 | |

| init_lr | {1e-2, 5e-3, 1e-3, 5e-4} | 1e-3 |

| {2,3,4} | 3 |

5.1.4 Environment and Parameter Tuning

We run the experiment with one NVIDIA GeForce RTX 3090 Graphic Card and use the Adam optimizer Kingma and Ba (2014) to train deep learning models. We utilize the gradual warm-up learning rate scheduler Goyal et al. (2017) and the next scheduler reduces the learning rate when the validation loss stops decreasing over a certain number of epochs. For each baseline model and the proposed framework, we repeatedly run the model with various groups of hyperparameters and use the Bayesian method to fine-tune the proposed framework.

The main parameters and their corresponding range are shown in Table 1. Common refers to parameters across all the methods, where denotes the length of the input sequence, denotes the filter size of the convolution kernel in the ConvLSTM, grad_clip denotes the value for gradient clipping, denotes the batch size, and init_lr denotes the initial learning rate for the adaptive learning rate scheduler. For parameters that are specific to ADNN, degree denotes the degree of the transformation function as shown in Equation 9, denotes the number of experts in the MoE network, and denotes the number of experts participating in the generation of the result. For FCN-ConvLSTM, denotes the number of layers of FCN. The Optimal column shows the tuned optimal parameters for the experiment. For the tuned parameters listed under Common, all the methods achieve the best result at the reported value. Notice that will not affect Conv3d and LSTM. Some parameters are not included in Table 1. For DCC and CCM, we use a rolling window of size years. For Conv3d, the encoder/decoder contains three consecutive 3D-convolution layers. For FCN-ConvLSTM, the hidden size of FCN is twice the input size. Horizon is an application-specific parameter, and since our application is portfolio management with monthly portfolio adjustments, we set .

5.2 Evaluation of ADM Prediction Accuracy

| Set 1 | Set 2 | Set 3 | Set 4 | Set 5 | ||

| CCM | MSE | 0.0613 | 0.0609 | 0.0673 | 0.0686 | 0.0754 |

| Gain | -0.342 | -0.314 | -0.431 | -0.532 | -0.534 | |

| DCC | MSE | 0.0643 | 0.0647 | 0.0609 | 0.0600 | 0.0639 |

| Gain | -0.405 | -0.398 | -0.293 | -0.339 | -0.30 | |

| Conv3D | MSE | 0.0630 | 0.0643 | 0.0647 | 0.0549 | 0.0583 |

| Gain | -0.379 | -0.392 | -0.374 | -0.222 | -0.187 | |

| LSTM | MSE | 0.8346 | 0.9155 | 0.7920 | 0.8303 | 0.8261 |

| Gain | -17.3 | -18.8 | -15.8 | -15.8 | -15.8 | |

| Raw-Conv | MSE | 0.0360 | 0.0359 | 0.0378 | 0.0364 | 0.0403 |

| LSTM | Gain | 0.210 | 0.220 | 0.199 | 0.188 | 0.179 |

| FCN-Conv | MSE | 0.0581 | 0.0411 | 0.0596 | 0.0571 | 0.4939 |

| LSTM | Gain | -0.275 | 0.111 | -0.266 | -0.270 | -0.009 |

| P-ADNN | MSE | 0.0351 | 0.0353 | 0.0376 | 0.0334 | 0.0368 |

| Gain | 0.224 | 0.221 | 0.190 | 0.247 | 0.246 | |

| T-ADNN | MSE | 0.0349 | 0.0358 | 0.0367 | 0.0360 | 0.0371 |

| Gain | 0.228 | 0.210 | 0.209 | 0.198 | 0.221 | |

| PT-ADNN | MSE | 0.0336 | 0.0356 | 0.0368 | 0.0367 | 0.0363 |

| Gain | 0.256 | 0.214 | 0.207 | 0.171 | 0.256 | |

| Set 6 | Set 7 | Set 8 | Set 9 | Set 10 | Mean(Std) | ||

| CCM | MSE | 0.0686 | 0.06 | 0.0605 | 0.0724 | 0.0626 | 0.0657(0.0052) |

| Gain | -0.455 | -0.381 | -0.385 | -0.709 | -0.457 | -0.454(0.1097) | |

| DCC | MSE | 0.0669 | 0.0566 | 0.0660 | 0.0630 | 0.0609 | 0.0627(0.0029) |

| Gain | -0.416 | -0.303 | -0.514 | -0.482 | -0.424 | -0.388(0.0730) | |

| Conv3D | MSE | 0.0579 | 0.0566 | 0.0605 | 0.0605 | 0.0605 | 0.0601(0.0031) |

| Gain | -0.231 | -0.302 | -0.387 | -0.421 | -0.414 | -0.331(0.0833) | |

| LSTM | MSE | 0.8048 | 0.6813 | 0.7707 | 0.8388 | 0.8261 | 0.8120(0.0565) |

| Gain | -16.0 | -14.6 | -16.7 | -18.7 | -18.3 | -16.9(1.3637) | |

| Raw-Conv | MSE | 0.0376 | 0.0647 | 0.0334 | 0.0336 | 0.0329 | 0.0389(0.0089) |

| LSTM | Gain | 0.202 | -0.487 | 0.236 | 0.211 | 0.234 | 0.140(0.2096) |

| FCN-Conv | MSE | 0.0626 | 0.0402 | 0.0579 | 0.0592 | 0.0562 | 0.0986(0.132) |

| LSTM | Gain | -0.329 | 0.077 | -0.325 | -0.398 | -0.307 | -0.199(0.1754) |

| P-ADNN | MSE | 0.0379 | 0.0323 | 0.0322 | 0.0361 | 0.0342 | 0.0351(0.0019) |

| Gain | 0.183 | 0.258 | 0.254 | 0.130 | 0.193 | 0.215(0.0385) | |

| T-ADNN | MSE | 0.0358 | 0.0321 | 0.0320 | 0.0336 | 0.0321 | 0.0346(0.0019) |

| Gain | 0.226 | 0.262 | 0.263 | 0.218 | 0.245 | 0.228(0.0217) | |

| PT-ADNN | MSE | 0.0337 | 0.0328 | 0.0319 | 0.0324 | 0.0321 | 0.0342(0.0019) |

| Gain | 0.273 | 0.245 | 0.262 | 0.220 | 0.245 | 0.235(0.0297) | |

| Avg. MSE | Avg. Gain | ||

|---|---|---|---|

| K-means | 0.0371 | 0.181 | |

| Hierachy | AutoCorr | 0.0385 | 0.160 |

| DTW | 0.0351 | 0.215 | |

The overall prediction accuracy result is shown in Table 2. Here, P-ADNN refers to the framework in Figure 3 with only positional rearrangement block and without the MoE transformation block, T-ADNN refers to the framework with only MoE transformation and without the positional rearrangement, and PT-ADNN integrates both forms of transformation in sequential order. We can observe deep learning-based methods generally outperform statistical methods (CCM and DCC), indicating the superiority of data-oriented methods over methods that greatly depend on unrealistic statistical assumptions in the complex and dynamic financial market. LSTM/Conv3D, which are simple models that utilize only temporal/spatial information, yields unsatisfactory prediction accuracy. The inferior performance of LSTM further demonstrates the importance of including spatial signal in ADM prediction task compared to considering temporal signal only. By incorporating both spatial and temporal information, ConvLSTM improves prediction accuracy. To study if the addition of the transformation layer can help alleviate the limit imposed by the ADM representation problem on raw ConvLSTM, we evaluate the FCN-ConvLSTM and the more complex ADNN models. We can see that the performance improvement of FCN-ConvLSTM is marginal and sometimes even negative. Even though FCN-ConvLSTM uses an end-to-end architecture that should learn better representation than raw inputs in principle, it displays worse performance, which indicates that without a proper design of the transformation, the utilization of deep layers cannot boost the performance.

After comparing multiple ADNN frameworks with different transformation functions, we can observe that PT-ADNN that utilizes both positional rearrangement and MoE transformation achieves the best performance in most cases. All the proposed ADNN frameworks exhibit superior performance compared to the Raw-ConvLSTM without using any transformation, validating the necessity of a well-designed transformation function for the raw ADM to alleviate the ADM representation problem. In specific cases (e.g. set 2 and set 4), the P-ADNN, which solely utilizes positional rearrangement, exhibits superior performance. This observation can be ascribed to the stable patterns and limited variability present in the dataset. In such cases, complex transformations might be less effective as they could introduce unnecessary intricacies or capture noise, potentially resulting in overfitting. In other cases (e.g. set 7 and set 8), the T-ADNN using solely the MoE transformation outperforms others, which may be due to the absence of clear grouping behavior among assets within the group, which diminishes the effectiveness of similarity-based positional rearrangement. In conclusion, from Table 2 we can see ADNN has consistent performance advantages on different datasets over various baselines.

5.3 Ablation Study

5.3.1 Comparison of Positional Rearrangement Methods

In Section 4.1, we mention using the hierarchical clustering approach based on the DTW distance. To further validate the effectiveness of the proposed method, we compare this design to two other kinds of clustering methods: (1) The K-means approach constructs clusters by using the monthly returns series as the feature vector. (2) The hierarchical clustering approach uses autocorrelation as the distance metric. Table 3 displays the results. We can observe that hierarchical clustering using DTW achieves the best performance, which validates its efficacy in improving the locality property of ADM, thereby augmenting the performance of the spatiotemporal block. The performance improvement is likely attributed to the inherent structure of the financial market, where assets are organized into industrial sectors. Mutual and hedge funds typically engage in investment activities by tracking industrial indices. This practice results in assets within the same sector being influenced simultaneously, leading to a high correlation among them, making hierarchical clustering a good choice.

5.3.2 Comparison of Different Expert Numbers

| 2 () | 4 () | 8 () | 16 () | |

|---|---|---|---|---|

| 1 | 0.0575 | 0.0349 | 0.0349 | 0.0345 |

| 2 | 0.0566 | 0.0370 | 0.0358 | 0.0383 |

| 3 | 0.0579 | 0.0375 | 0.0367 | 0.0490 |

| 4 | 0.0362 | 0.0362 | 0.0360 | 0.0370 |

| 5 | 0.0613 | 0.0387 | 0.0371 | 0.0379 |

| 6 | 0.0358 | 0.0498 | 0.0358 | 0.0366 |

| 7 | 0.0532 | 0.0319 | 0.0321 | 0.0324 |

| 8 | 0.0554 | 0.0332 | 0.0320 | 0.0336 |

| 9 | 0.0554 | 0.0341 | 0.0336 | 0.0341 |

| 10 | 0.0554 | 0.0353 | 0.0321 | 0.0315 |

| Avg. | 0.0525 | 0.0369 | 0.0346 | 0.0365 |

In Section 4.2, we introduce the MoE transformation. The performance of MoE depends on two crucial parameters, (1) the number of experts , which determines how many experts in total are contained in the network, and (2) , which determines how many experts participate in generating the final transformation function (). Table 4 shows how these two parameters affect the learning of the transformation function and in turn the prediction MSE. The entry in the table denotes the MSE returned by the optimal on average in the 10 stock datasets for a given . For example, when , on average produces the optimal MSE among the 10 stock datasets. We have several observations from the table: (1) the optimal () pair is (8,4), (2) The effectiveness of and does not follow a simple ”larger is better” pattern. This phenomenon may arise from the initial increase of to an optimal number effectively capturing the complexities of market data. However, excessive increments in impose risks on overfitting and detrimentally impact performance.

5.3.3 Comparison of Polynomial Approximation Functions

| Avg. MSE | Avg. Gain | ||

|---|---|---|---|

| Matmul | Linear | 0.0447 | 0.026 |

| Quadratic | 0.0413 | 0.100 | |

| Cubic | 0.0417 | 0.091 | |

| Hadamard | Linear | 0.0524 | 0.026 |

| Quadratic a | 0.0346 | 0.228 | |

| Cubic | 0.0417 | 0.091 | |

-

a

Used by ADNN.

To validate the efficacy of the polynomial approximation function proposed in Equation 6, we conduct experiments involving alternative transformation functions of various degrees (linear and cubic) within the polynomial approximation function, as well as different matrix multiplication methods. We compare these approaches using the average MSE and gain performance across the ten datasets. Table 5 summarizes the results. We can observe that the approximation function in quadratic form reaches the best performance in both matrix multiplication cases. At the same time, the quadratic approximation function with the Hadamard product reaches the best performance in terms of MSE and gain. These findings indicate the importance of a well-designed transformation function for accurate forecasting of future ADM. Notably, an increase in degrees generally incurs higher costs and longer convergence times.

5.4 Explore MoE

The financial market is characterized by its dynamic nature, as different market factors come into prominence during different time periods. For instance, during a financial crisis, the dominating market factor is the fear of company bankruptcy due to the severe lack of liquidity. Consequently, most stocks experience a downturn with heightened correlations driven by the pessimistic macroeconomic sentiment. Conversely, during normal market conditions, stock prices are primarily influenced by companies’ fundamentals, resulting in relatively lower correlations among stocks from different industries. Moreover, market factors may intertwine, as macroeconomic conditions and company fundamentals might simultaneously exert their influence, resulting in correlations behaving in a sophisticated manner.

In Section 5.2, we show that the MoE block can improve the model performance because of its capability to distinguish different market scenarios and thus better model the asset correlation dynamics. In this section, we investigate how MoE distinguishes market scenarios and try to visualize the process. The intuition is as follows. If MoE can successfully distinguish different market factors, we would expect it to select similar expert combinations in the market phases dominated by the same market factors and different combinations of experts for different market phases dominated by different market factors. Since it is impossible to enumerate and quantify the market factors comprehensively in real-world financial markets, we choose to simulate different market scenarios with synthetic market data, which is a common approach in the finance field. We divide a market scenario into several market phases , each of which is generated with some market factor(s). We denote market phase that is solely generated from market factor as .

The stock price data in each market phase are generated with the multidimensional geometric Brownian motion function (MGBM), which is often used in Monte Carlo simulation in financial experiments Glasserman (2004). MGBM requires three inputs, namely, correlation matrix , expected return and volatility . The triplet forms a market factor , which is defined as follows:

-

•

Correlation Matrix (): a random correlation matrix is generated given a vector of eigenvalues following a numerically stable algorithm spelled out by Davies and Higham (2000). The random eigenvalues are generated from a uniform distribution with a lower boundary equal to 0.1 and an upper boundary equal to 2.

-

•

Expected Return (): the value is randomly sampled from a uniform distribution with a lower boundary equal to 0.1 and an upper boundary equal to 0.5.

-

•

Volatility (): the value is randomly sampled from a uniform distribution with a lower boundary equal to 0.01 and an upper boundary equal to 0.1.

The simulation of the stock price data for market phase can be formulated with the following equation:

| (15) |

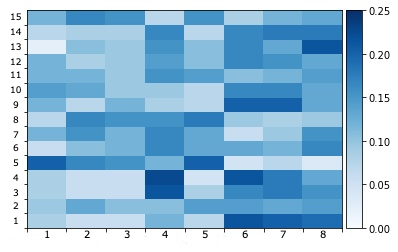

We create three different market scenarios (1 to 3) with different setups of the triplet, as outlined in Table 6. To save space, we focus our discussion solely on the quadratic-term MoE block (see in Equation 9). We finetune the model parameters based on each corresponding scenario and visualize the behavior of MoE in the optimal setting.

Figure 6 depicts the chance that the experts are selected across different market scenarios, where the -axis denotes the market phases and the -axis represents the experts in MoE. The discrete and axes divide the figure into grids and the color of a grid denotes the chance of the expert being chosen in a market phase. Given a market phase comprising input ADMs sequences, the importance weight of for is calculated by:

| (16) | ||||

For instance, in Scenario 1 where and , the weight assigned to a selected expert is . If this expert is chosen for all input sequences within this market phase, it has average weight . Notably, the maximum value of any is , while the smallest value would be zero if the expert is not selected at all.

| Scenario | 1 | 2 | 3 |

| No. Market Phases | 15 | 10 | 15 |

| Trading Days per Phase | 300 | 300 | 300 |

| Stock Prices | Simulated | Simulated | Real |

| Correlation Matrix | Random | Random | N/A |

| No. Market Factors () | 1 | 2 | N/A |

| No. Experts | 8 | 8 | 8 |

| 4 | 4 | 4 |

5.4.1 Market Scenario 1

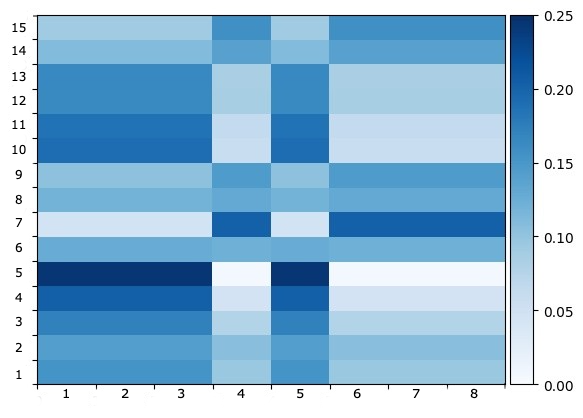

Scenario 1 uses a simple setting where each market phase is governed by one single market factor. We create 15 market phases of stock price data and divide them into 5 market regimes. Thus, each market regime comprises 3 market phases. Note that the 3 market phases within the same regime are generated from the same market factor (i.e., ), while the simulated price data in each phase are different due to the stochasticity of MGBM. Once the stock price data are generated, we create the historical ADM sequence (Section 3.2) as input to ADNN for forecasting assets dependencies.

Figure 6(a) depicts how experts are selected across the 15 market phases (market phases with the same regimes are posited adjacently, e.g. phases 1 to 3 correspond to the first regime, phases 4 to 6 the second regime, etc.). We can observe that the grid colors have similar distribution for market phases with the same market regime but different color distributions for phases within different regimes. This means that MoE picks similar combinations of experts for market phases with the same regime (sharing the same market factor), and different ones for market phases with different regimes, which aligns with the intuition.

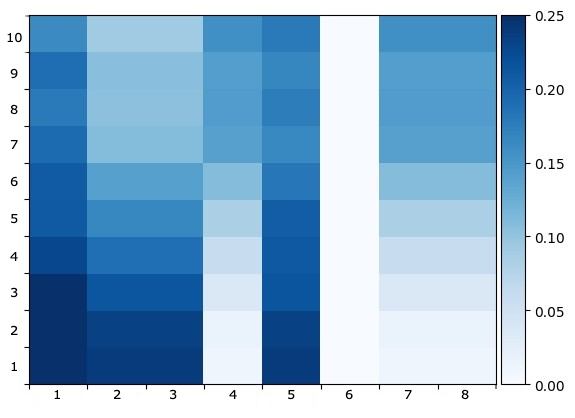

5.4.2 Market Scenario 2

The real-world financial market is highly dynamic and is always jointly influenced by multiple factors. Scenario 1’s single market factor assumption is too simple to simulate the real-world financial market. In scenario 2, we move one step forward and use two independent market factors to generate the stock price data for a better simulation of the complexity of the real market. From Figure 6(a), we observe that experts selected in the second and third market regimes (corresponding to , and ) of Scenario 1 tend to be mutually exclusive, indicating the low correlation of the two market factors in the two market regimes. Thus, in Scenario 2, we choose these two market regimes to generate the stock price data and ADMs. Specifically, we utilize the MGBM theory to derive two log-return time series, and , based on and . Subsequently, we linearly combined these time series to generate ADMs in ten distinct market phases, as illustrated below:

| (17) |

Different indicate varying strengths of the two sub-factors, with and referring to the second and the third market regime, respectively.

Figure 6(b) visualizes the results. We can see that in market phase (), the expert selection is similar to the second market regime in Scenario 1, where experts 1,2,3,5 are most frequently selected. In market phase (), the selection is closer to the third regime, where experts 4,5,7,8 are most frequently selected. As shifts from 0 to 1, we can see that the selected experts gradually transit from 1,2,3,5 to 4,5,7,8. This result demonstrates ADNN’s ability to detect and differentiate multiple market factors embedded in the input data and the capability of MoE to assign appropriate experts to model the market signals encoded in the corresponding market factors.

5.4.3 Market Scenario 3

In Scenario 3, we directly use the real-world price dataset as input to ADNN instead of using simulation data generated by MGBM. We randomly sample 32 stocks from the 15-year US market data pool described in Section 5.1.1 and divide the data into 15 market phases by year. Figure 6(c) illustrates the result. Compared to Figures 6(a) and 6(b), we can observe that the expert distribution is much more diverse. This is reasonable since Scenario 3 includes all the market signals in the input data which are sophisticated and highly dynamic, requiring a wide range of experts with different knowledge to work collaboratively.

5.5 Visualization of the transformed ADMs

We visualize the transformed ADMs and study how the positional rearrangement and the MoE transformation block improve the downstream ADM prediction task. Specifically, we train the PT-ADNN model using dataset 1 and select six ADMs from the sequential training set, starting from index 0 of the ADM sequence with a uniform gap of size 100 between each consecutive ADM. Figure 7 demonstrates the six ADMs in different periods. We can observe that the positional rearrangement technique rearranges the row and column positions in such a way that assets exhibiting concurrent patterns are brought closer to each other. Take the third ADM image in Figure 7(b) as an example. The resulting matrix bears a stronger resemblance to an image, featuring prominent, well-defined blocks with clear boundaries, each composed of uniform colors. On the other hand, the ADMs transformed by the MoE method exhibit a wider range of values and higher contrast. It shows that the MoE transformation scales up the input values and introduces more divergence to the original data, which helps the downstream convolution layer better distill the information.

5.6 Application Study

In this section, we demonstrate how the predicted ADM can be used to solve two real-world financial problems.

5.6.1 Portfolio Risk Reduction

Portfolio diversification needs to consider the dynamic property of assets dependencies, based on which the weight of each asset in the portfolio can be obtained through the famous “Modern Portfolio Theory” Markowitz (1952). Equation 18 briefly summarizes the idea:

| (18) | ||||

where denotes the predicted correlation matrix for forecasting method (here, ), s denotes the ground truth standard deviation vector111Since the main purpose of this evaluation is to examine the performance of ADM (“correlation”) prediction, we assume prior knowledge of the future standard deviation vector to eliminate the extra variability. at the time (), diag(s) is a diagonal matrix, denotes the predicted covariance matrix. We first calculate the predicted covariance matrix (first line of Equation 18) and obtain the asset weight vector (second line). Then, the actual variance of the derived portfolio can be computed with the future ground-truth covariance matrix (third line). In Equation 18, portfolio volatility is a function of , and when the optimal portfolio risk is obtained.

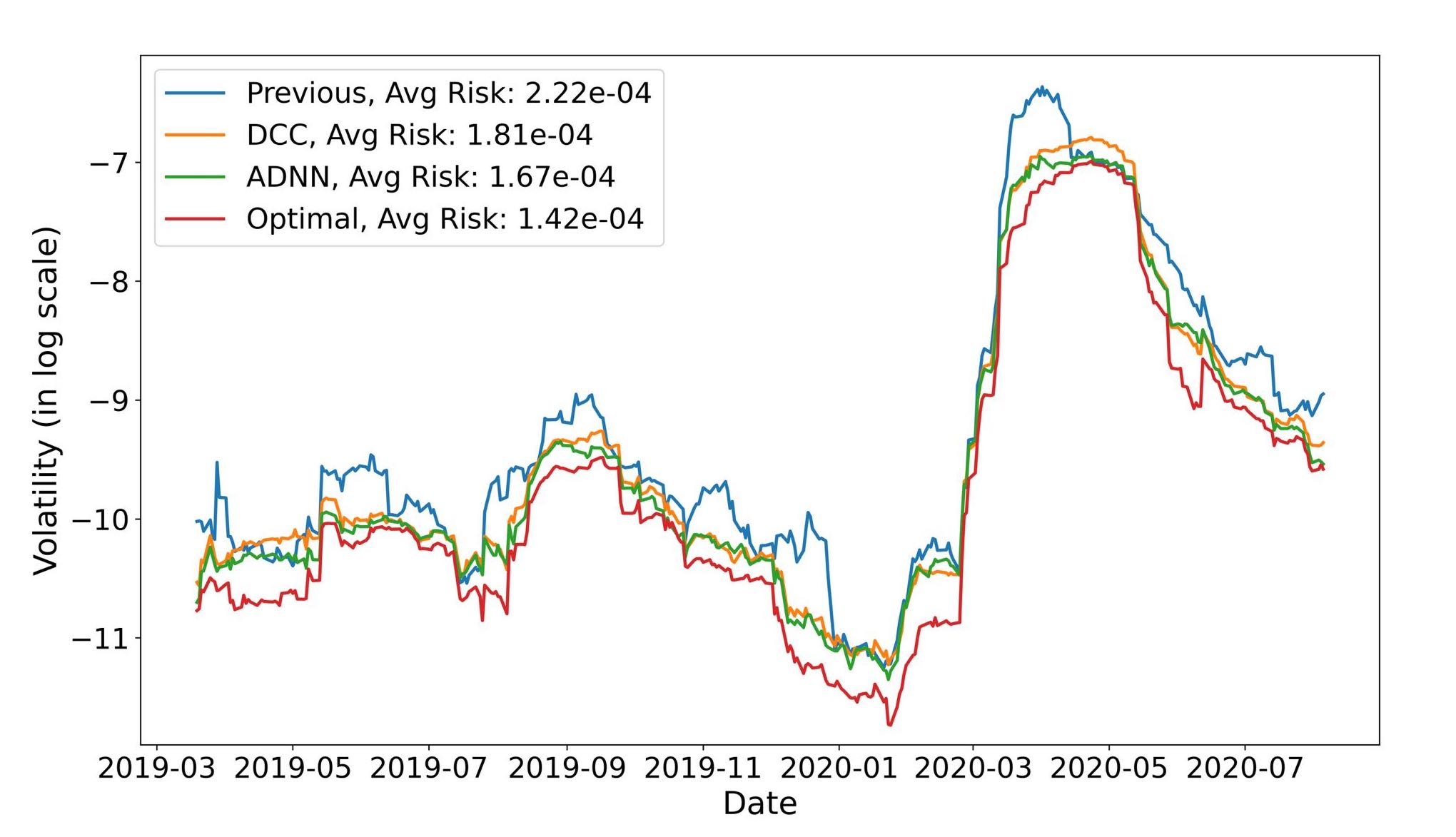

We randomly choose one stock dataset (dataset 7) as the source for constructing the diversified portfolio based on the predicted ADMs. All of the methods under evaluation build up their portfolios from the same stocks in dataset 7, which are then evaluated based on their respective portfolios’ volatility . For baselines, we choose (1) the intuitive Previous ADM (introduced at the beginning of Section 5.2), and (2) the well-known statistical method DCC-Garch. We use T-ADNN as it achieves the best performance in dataset 7. All baselines and the ADNN will be compared to Optimal (). For simplicity, we assume that no short selling is allowed, i.e. asset weight .

The comparison results are shown in Figure 8. We can observe that, as expected, both DCC and ADNN are superior to the method Previous, and they display similar trends. ADNN outperforms DCC with an average risk of , which ranks only second to the optimal portfolio. In terms of average risk, ADNN achieves an improvement of over Previous and over DCC. In conclusion, the ADNN method can generate a more diversified and lower-risk portfolio compared with the baselines.

5.6.2 Pair Trading

Pair trading is a trading strategy that involves the simultaneous buying and selling of two related securities, typically stocks, to take advantage of perceived price imbalances between them. Correlation plays a crucial role in pair trading strategies as it helps traders identify suitable pairs of assets to trade. A high correlation between two assets suggests that their prices move together, increasing the likelihood of finding profitable trading opportunities when the correlation temporarily breaks down. In this study, we utilize correlations predicted by ADNN to inform decision-making in pair trading. Algorithm 2 illustrates the strategy.

The experiment is conducted using the randomly picked dataset 7, where the top ten asset pairs with a historically high correlation are selected. We evaluate multiple approaches by calculating the average performance metrics for pair trading across ten pairs, including the Win/Loss Rate, Maximum Drawdown, and Sharpe Ratio. We use the following common strategies for pair trading as baselines.

-

•

Mean Reversion Strategy assumes that the prices of the two assets in a pair will revert to their mean relationship. When the spread between the assets widens beyond a certain threshold, it takes a long position in the underperforming asset and a short position in the outperforming asset. The positions are closed when the spread returns to its average.

-

•

Statistical Deviation Strategy takes positions expecting the spread to revert to its normal range when the spread between the assets exceeds a certain number of standard deviations or reaches extreme values. The positions are closed when the spread returns to a typical level.

-

•

S&P 500 is a widely recognized stock market index comprising the 500 largest publicly traded companies in the United States. It serves as a benchmark for evaluating the effectiveness of the pair trading strategy compared to passive investing in the market.

Table 7 displays the results. The ADNN model demonstrates superior performance in terms of the Win/Loss Rate, with a Sharpe ratio close to 2 and a maximum drawdown below 20%. This outcome indicates that the predicted correlation effectively captures market changes and validates the efficacy of the ADNN when applied to pair trading.

| Profit | Maximum | Sharpe | Win/Loss | |

| Rate | Drawdown | Ratio | Rate | |

| Mean Reversion | 7.3% | 5.6% | 1.5 | 65% |

| Statistical Deviation | 5.3% | 4.1% | 2.1 | 69% |

| S&P 500 | 8.4% | 33.9% | 0.45 | - |

| ADNN | 12.1% | 10.7% | 2.0 | 68% |

6 Conclusion

Prediction of asset dependency has been extensively researched in the financial industry. In this paper, we formulate the problem as the sequential Asset Dependency Matrix (ADM) prediction problem. We propose the Asset Dependency Neural Network (ADNN) framework to model the spatiotemporal dependencies signals in the historical ADM sequence to predict future ADM. To resolve the ADM representation problem, ADNN incorporates a Mixture of Experts (MoE) to transform input ADM to the optimal representation to facilitate ConvLSTM model in predicting the future ADMs. We validate and explain the effectiveness of ADNN on multiple real-world stock market data by comparing it with various baselines and applying it to the portfolio diversification task. For future work, we plan to extend the current research in the following three directions: (1) investigate other end-to-end transformation methods, (2) apply the ADNN framework to other kinds of ADM (e.g., covariance matrix), and (3) construct a portfolio with the consideration of realistic constraint (e.g., transaction cost).

Acknowledgements

The research reported in this paper was supported by the Research Grants Council HKSAR GRF (No. 16215019), Guangdong Provincial Key Laboratory of Interdisciplinary Research and Application for Data Science, BNU-HKBU United International College, project code 2022B1212010006, and in part by Guangdong Higher Education Upgrading Plan (2021-2025) of “Rushing to the Top, Making Up Shortcomings and Strengthening Special Features” with UIC research grant R0400001-22.

Declaration of Generative AI and AI-assisted technologies in the writing process

During the preparation of this work, the authors used ChatGPT to improve the readability and language of the manuscript. After using this service, the authors reviewed and edited the content as needed and take full responsibility for the content of the publication.

References

- Altomonte and Rungi (2013) Altomonte, C., Rungi, A., 2013. Business groups as hierarchies of firms: determinants of vertical integration and performance .

- Ane and Kharoubi (2003) Ane, T., Kharoubi, C., 2003. Dependence structure and risk measure. The journal of business 76, 411–438.

- Babaeizadeh et al. (2017) Babaeizadeh, M., Finn, C., Erhan, D., Campbell, R.H., Levine, S., 2017. Stochastic variational video prediction. arXiv preprint arXiv:1710.11252 .

- Baesel (1974) Baesel, J.B., 1974. On the assessment of risk: Some further considerations. The Journal of Finance 29, 1491–1494.

- Bauwens et al. (2006) Bauwens, L., Laurent, S., Rombouts, J.V., 2006. Multivariate garch models: a survey. Journal of applied econometrics 21, 79–109.

- Bengio et al. (2014) Bengio, Y., Courville, A., Vincent, P., 2014. Representation learning: A review and new perspectives. arXiv:1206.5538.

- Blume (1975) Blume, M.E., 1975. Betas and their regression tendencies. The Journal of Finance 30, 785–795.

- Bollerslev et al. (1988) Bollerslev, T., Engle, R.F., Wooldridge, J.M., 1988. A capital asset pricing model with time-varying covariances. Journal of political Economy 96, 116–131.

- Boubekeur and Schlick (2007) Boubekeur, T., Schlick, C., 2007. Qas: Real-time quadratic approximation of subdivision surfaces, in: 15th Pacific Conference on Computer Graphics and Applications (PG’07), pp. 453–456. doi:10.1109/PG.2007.20.

- Bucci et al. (2022) Bucci, A., Ippoliti, L., Valentini, P., 2022. Comparing unconstrained parametrization methods for return covariance matrix prediction. Statistics and Computing 32, 90.

- Chen et al. (2018) Chen, C., Li, K., Teo, S.G., Chen, G., Zou, X., Yang, X., Vijay, R.C., Feng, J., Zeng, Z., 2018. Exploiting spatio-temporal correlations with multiple 3d convolutional neural networks for citywide vehicle flow prediction, in: 2018 IEEE International Conference on Data Mining (ICDM), pp. 893–898. doi:10.1109/ICDM.2018.00107.

- Chen et al. (2021a) Chen, W., Jiang, M., Zhang, W.G., Chen, Z., 2021a. A novel graph convolutional feature based convolutional neural network for stock trend prediction. Information Sciences 556, 67–94.

- Chen et al. (2021b) Chen, W., Zhang, H., Mehlawat, M.K., Jia, L., 2021b. Mean–variance portfolio optimization using machine learning-based stock price prediction. Applied Soft Computing 100, 106943.

- Cheng et al. (2022) Cheng, D., Yang, F., Xiang, S., Liu, J., 2022. Financial time series forecasting with multi-modality graph neural network. Pattern Recognition 121, 108218.

- Damodaran (1999) Damodaran, A., 1999. Estimating risk parameters .

- Davies and Higham (2000) Davies, P.I., Higham, N.J., 2000. Numerically stable generation of correlation matrices and their factors. BIT Numerical Mathematics 40, 640–651.

- Eden et al. (1986) Eden, M., Unser, M., Leonardi, R., 1986. Polynomial representation of pictures. Signal Processing 10, 385–393.

- Eigen et al. (2013) Eigen, D., Ranzato, M., Sutskever, I., 2013. Learning factored representations in a deep mixture of experts. arXiv preprint arXiv:1312.4314 .

- Elton and Gruber (1973) Elton, E.J., Gruber, M.J., 1973. Estimating the dependence structure of share prices–implications for portfolio selection. The Journal of Finance 28, 1203–1232.

- Elton et al. (1977) Elton, E.J., Gruber, M.J., Padberg, M.W., 1977. Simple rules for optimal portfolio selection: the multi group case. Journal of Financial and Quantitative Analysis , 329–345.

- Elton et al. (1978) Elton, E.J., Gruber, M.J., Urich, T.J., 1978. Are betas best? The Journal of Finance 33, 1375–1384.

- Engle (2002) Engle, R., 2002. Dynamic conditional correlation: A simple class of multivariate generalized autoregressive conditional heteroskedasticity models. Journal of Business & Economic Statistics 20, 339–350.

- Engle and Kroner (1995) Engle, R.F., Kroner, K.F., 1995. Multivariate simultaneous generalized arch. Econometric theory , 122–150.

- Engle et al. (1990) Engle, R.F., Ng, V.K., Rothschild, M., 1990. Asset pricing with a factor-arch covariance structure: Empirical estimates for treasury bills. Journal of econometrics 45, 213–237.

- Gebert et al. (2019) Gebert, P., Roitberg, A., Haurilet, M., Stiefelhagen, R., 2019. End-to-end prediction of driver intention using 3d convolutional neural networks, in: 2019 IEEE Intelligent Vehicles Symposium (IV), pp. 969–974. doi:10.1109/IVS.2019.8814249.

- Glasserman (2004) Glasserman, P., 2004. Monte Carlo methods in financial engineering. volume 53. Springer.

- Goodfellow et al. (2016) Goodfellow, I., Bengio, Y., Courville, A., 2016. Deep Learning. MIT Press. http://www.deeplearningbook.org.

- Goyal et al. (2017) Goyal, P., Dollár, P., Girshick, R., Noordhuis, P., Wesolowski, L., Kyrola, A., Tulloch, A., Jia, Y., He, K., 2017. Accurate, large minibatch sgd: Training imagenet in 1 hour. arXiv preprint arXiv:1706.02677 .

- Hambly et al. (2023) Hambly, B., Xu, R., Yang, H., 2023. Recent advances in reinforcement learning in finance. Mathematical Finance 33, 437–503.

- Hochreiter and Schmidhuber (1997) Hochreiter, S., Schmidhuber, J., 1997. Long short-term memory. Neural Computation 9, 1735–1780.

- Hou et al. (2021) Hou, X., Wang, K., Zhong, C., Wei, Z., 2021. St-trader: A spatial-temporal deep neural network for modeling stock market movement. IEEE/CAA Journal of Automatica Sinica 8, 1015–1024.

- Hsieh et al. (2018) Hsieh, J.T., Liu, B., Huang, D.A., Fei-Fei, L., Niebles, J.C., 2018. Learning to decompose and disentangle representations for video prediction. arXiv preprint arXiv:1806.04166 .

- Imajo et al. (2021) Imajo, K., Minami, K., Ito, K., Nakagawa, K., 2021. Deep portfolio optimization via distributional prediction of residual factors, in: Proceedings of the AAAI conference on artificial intelligence, pp. 213–222.

- Jacobs et al. (1991) Jacobs, R.A., Jordan, M.I., Nowlan, S.J., Hinton, G.E., 1991. Adaptive mixtures of local experts. Neural computation 3, 79–87.

- Jacquin (1993) Jacquin, A.E., 1993. Fractal image coding: A review. Proceedings of the IEEE 81, 1451–1465.

- Jiang et al. (2017) Jiang, Z., Xu, D., Liang, J., 2017. A deep reinforcement learning framework for the financial portfolio management problem. arXiv preprint arXiv:1706.10059 .

- Jordan and Jacobs (1993) Jordan, M., Jacobs, R., 1993. Hierarchical mixtures of experts and the em algorithm, in: Proceedings of 1993 International Conference on Neural Networks (IJCNN-93-Nagoya, Japan), pp. 1339–1344 vol.2. doi:10.1109/IJCNN.1993.716791.

- Kingma and Ba (2014) Kingma, D.P., Ba, J., 2014. Adam: A method for stochastic optimization. arXiv preprint arXiv:1412.6980 .

- Ma et al. (2018) Ma, J., Zhao, Z., Yi, X., Chen, J., Hong, L., Chi, E.H., 2018. Modeling task relationships in multi-task learning with multi-gate mixture-of-experts, in: Proceedings of the 24th ACM SIGKDD International Conference on Knowledge Discovery & Data Mining, pp. 1930–1939.

- Ma et al. (2021) Ma, Y., Han, R., Wang, W., 2021. Portfolio optimization with return prediction using deep learning and machine learning. Expert Systems with Applications 165, 113973.

- Markowitz (1952) Markowitz, H., 1952. Portfolio selection. The Journal of Finance 7, 77–91. URL: http://www.jstor.org/stable/2975974.

- Mathieu et al. (2015) Mathieu, M., Couprie, C., LeCun, Y., 2015. Deep multi-scale video prediction beyond mean square error. arXiv preprint arXiv:1511.05440 .

- Ng et al. (2015) Ng, J.Y.H., Hausknecht, M., Vijayanarasimhan, S., Vinyals, O., Monga, R., Toderici, G., 2015. Beyond short snippets: Deep networks for video classification. arXiv:1503.08909.

- Ng et al. (1992) Ng, V., Engle, R.F., Rothschild, M., 1992. A multi-dynamic-factor model for stock returns. Journal of Econometrics 52, 245–266.

- Oprea et al. (2020) Oprea, S., Martinez-Gonzalez, P., Garcia-Garcia, A., Castro-Vargas, J.A., Orts-Escolano, S., Garcia-Rodriguez, J., Argyros, A., 2020. A review on deep learning techniques for video prediction. IEEE Transactions on Pattern Analysis and Machine Intelligence , 1–1URL: http://dx.doi.org/10.1109/TPAMI.2020.3045007, doi:10.1109/tpami.2020.3045007.

- Petitjean et al. (2011) Petitjean, F., Ketterlin, A., Gançarski, P., 2011. A global averaging method for dynamic time warping, with applications to clustering. Pattern recognition 44, 678–693.

- Sak et al. (2014) Sak, H., Senior, A., Beaufays, F., 2014. Long short-term memory recurrent neural network architectures for large scale acoustic modeling. Proceedings of the Annual Conference of the International Speech Communication Association, INTERSPEECH , 338–342.

- Scarselli and Chung Tsoi (1998) Scarselli, F., Chung Tsoi, A., 1998. Universal approximation using feedforward neural networks: A survey of some existing methods, and some new results. Neural Networks 11, 15–37. URL: https://www.sciencedirect.com/science/article/pii/S089360809700097X, doi:https://doi.org/10.1016/S0893-6080(97)00097-X.

- Shazeer et al. (2017) Shazeer, N., Mirhoseini, A., Maziarz, K., Davis, A., Le, Q., Hinton, G., Dean, J., 2017. Outrageously large neural networks: The sparsely-gated mixture-of-experts layer. arXiv:1701.06538.

- Shi et al. (2015) Shi, X., Chen, Z., Wang, H., Yeung, D.Y., Wong, W.K., Woo, W.c., 2015. Convolutional lstm network: A machine learning approach for precipitation nowcasting. arXiv preprint arXiv:1506.04214 .

- Tashman (2000) Tashman, L.J., 2000. Out-of-sample tests of forecasting accuracy: an analysis and review. International journal of forecasting 16, 437–450.

- ping Tian et al. (2013) ping Tian, D., et al., 2013. A review on image feature extraction and representation techniques. International Journal of Multimedia and Ubiquitous Engineering 8, 385–396.

- Torokhti and Howlett (2001) Torokhti, A., Howlett, P., 2001. On the best quadratic approximation of nonlinear systems. IEEE Transactions on Circuits and Systems I: Fundamental Theory and Applications 48, 595–602. doi:10.1109/81.922461.

- Tran et al. (2015) Tran, D., Bourdev, L., Fergus, R., Torresani, L., Paluri, M., 2015. Learning spatiotemporal features with 3d convolutional networks. arXiv:1412.0767.

- Uysal et al. (2023) Uysal, A.S., Li, X., Mulvey, J.M., 2023. End-to-end risk budgeting portfolio optimization with neural networks. Annals of Operations Research , 1–30.

- Vasicek (1973) Vasicek, O.A., 1973. A note on using cross-sectional information in bayesian estimation of security betas. The Journal of Finance 28, 1233–1239.

- Verzelen (2010) Verzelen, N., 2010. Adaptive estimation of covariance matrices via cholesky decomposition .

- Wang et al. (2018) Wang, Y., Jiang, L., Yang, M.H., Li, L.J., Long, M., Fei-Fei, L., 2018. Eidetic 3d lstm: A model for video prediction and beyond, in: International conference on learning representations.

- Wang et al. (2017) Wang, Y., Long, M., Wang, J., Gao, Z., Yu, P.S., 2017. Predrnn: Recurrent neural networks for predictive learning using spatiotemporal lstms. Advances in neural information processing systems 30.

- Wang et al. (2021) Wang, Z., Huang, B., Tu, S., Zhang, K., Xu, L., 2021. Deeptrader: a deep reinforcement learning approach for risk-return balanced portfolio management with market conditions embedding, in: Proceedings of the AAAI conference on artificial intelligence, pp. 643–650.

- Wu et al. (2023) Wu, J.M.T., Li, Z., Herencsar, N., Vo, B., Lin, J.C.W., 2023. A graph-based cnn-lstm stock price prediction algorithm with leading indicators. Multimedia Systems 29, 1751–1770.

- Wu et al. (2022) Wu, S., Liu, Y., Zou, Z., Weng, T.H., 2022. S_i_lstm: stock price prediction based on multiple data sources and sentiment analysis. Connection Science 34, 44–62.

- Xu et al. (2021) Xu, K., Huang, D.Z., Darve, E., 2021. Learning constitutive relations using symmetric positive definite neural networks. Journal of Computational Physics 428, 110072. URL: https://www.sciencedirect.com/science/article/pii/S0021999120308469, doi:https://doi.org/10.1016/j.jcp.2020.110072.

- Ye et al. (2021) Ye, J., Zhao, J., Ye, K., Xu, C., 2021. Multi-graph convolutional network for relationship-driven stock movement prediction, in: 2020 25th International Conference on Pattern Recognition (ICPR), IEEE. pp. 6702–6709.

- Ye et al. (2020) Ye, Y., Pei, H., Wang, B., Chen, P.Y., Zhu, Y., Xiao, J., Li, B., 2020. Reinforcement-learning based portfolio management with augmented asset movement prediction states, in: Proceedings of the AAAI Conference on Artificial Intelligence, pp. 1112–1119.

- Zheng et al. (2023) Zheng, X., Liu, M., Zhu, M., 2023. Deep hashing-based dynamic stock correlation estimation via normalizing flow, in: Proceedings of the Thirty-Second International Joint Conference on Artificial Intelligence, pp. 4993–5001.