Incentivizing Quality Text Generation

via Statistical Contracts

Abstract

While the success of large language models (LLMs) increases demand for machine-generated text, current pay-per-token pricing schemes create a misalignment of incentives known in economics as moral hazard: Text-generating agents have strong incentive to cut costs by preferring a cheaper model over the cutting-edge one, and this can be done “behind the scenes” since the agent performs inference internally. In this work, we approach this issue from an economic perspective, by proposing a pay-for-performance, contract-based framework for incentivizing quality. We study a principal-agent game where the agent generates text using costly inference, and the contract determines the principal’s payment for the text according to an automated quality evaluation. Since standard contract theory is inapplicable when internal inference costs are unknown, we introduce cost-robust contracts. As our main theoretical contribution, we characterize optimal cost-robust contracts through a direct correspondence to optimal composite hypothesis tests from statistics, generalizing a result of Saig et al. (NeurIPS’23). We evaluate our framework empirically by deriving contracts for a range of objectives and LLM evaluation benchmarks, and find that cost-robust contracts sacrifice only a marginal increase in objective value compared to their cost-aware counterparts.

1 Introduction

Modern-day LLMs are showing increasingly impressive capabilities, and simultaneously becoming increasingly costly. With rising success at handling complex tasks, conversational AI systems are seeing ubiquitous usage across critical domains such as healthcare [19, 35], financial risk assessment [28], and law [24, 36]. To achieve such levels of performance, contemporary LLM architectures contain billions and even trillions of parameters, leading to a computational pipeline that requires dedicated facilities and substantial energy to operate [34].

Since the computational requirements of modern LLMs exceed the capacity of common devices, language generation tasks are typically delegated to commercial firms (such as AWS and Microsoft Azure), which operate dedicated computational resources to generate text for a price. To address the tension between LLM performance and computational costs, such firms typically propose multiple service options, with each option offering a different trade-off between model quality and cost [1, 7, 37, 38]. Currently, the most common pricing scheme for such services is pay-per-token, in which users agree in advance to pay a fixed rate for each token of text generated by the system [10].

While simple and intuitive, the pay-per-token pricing scheme creates a misalignment of economic incentives between the firms and their consumers, known in the economic literature as moral hazard: As inference is performed internally and a fixed price is agreed upon in advance, rational firms can strategically increase their profit margin by generating text using a cheaper, lower-quality model. Due to the stochastic nature of language generation, consumers may not be able to reliably determine the quality of the model being used, exposing them to this kind of hazard.

Moral hazard is especially prevalent in cases where the text generation task is intricate, and so evaluation is hard: Consider a scenario where a healthcare provider uses conversational AI to summarize medical notes. As medical diagnosis is an intricate and critical task, the healthcare provider wishes the summaries to be generated using the most advanced language model. Under the pay-per-token pricing scheme, the healthcare provider agrees in advance to pay a fixed amount for each token generated. However, it is not hard to imagine that a firm may attempt to increase profit margins by routing some of the summarization requests to one of its cheaper models, instead of the most advanced one, without taking into account their purpose, and knowing that any lower-quality results would be attributed to the stochastic nature of LLM inference.

From pay-per-token to pay-for-performance.

In the economic literature, the canonical solution to moral hazard problems is pay-for-performance, or P4P [17]. Instead of paying a fixed price for any outcome, the parties agree in advance on a contract that specifies a differential payment scheme – e.g., agreeing in advance that the firm will receive higher pay when the generated text is considered to be high-quality. When designed correctly, contracts incentivize rational agents to invest more effort, thus providing a way to align incentives. Interaction around contracts is modeled as a principal-agent game, where the principal commits to a payment scheme, and the agent responds by rationally selecting a utility-maximizing action. Within this framework, the principal seeks to design a contract which satisfies some notion of optimality, such as requiring the least amount of expected pay (“min-pay contract”), or the lowest budget (“min-budget contract”).

In this work, we extend the theory of contract design, and use it to design optimal pay-for-performance pricing schemes for delegated text generation. Applying contract design to this setting requires us to overcome the challenges of automated evaluation and cost-robustness. The former arises from the fact that pay-for-performance pricing relies on a measure of performance, and the latter is due to the fact that LLM inference is performed internally by the agent, and therefore the principal possesses uncertainty regarding the agent’s true internal costs.

Our results.

To tackle automated evaluation, we draw upon recent advances in the LLM evaluation literature [9], and propose a modular contract design framework which uses LLM evaluators as subroutines. More specifically, upon receiving generated text, our pricing scheme is implemented by evaluating the prompt-response pair using an automated evaluator and paying accordingly. The choice of evaluator can be tailored to the task: optimal pricing schemes in code generation tasks, for example, would rely on a pass/fail code evaluator [11, 4], whereas evaluation of linguistic tasks can be achieved using an “LLM-as-a-judge” approach [42, 29, 26]. In our theoretical analysis, we show that our framework is applicable even to intricate tasks where current evaluation methods are noisy and undecisive, as the principal can compensate for the noise by paying more (Proposition 1).

To address the challenge of cost uncertainty, we propose a new notion of cost-robust contracts, which are pay-for-performance schemes guaranteed to incentivize effort even when the internal cost structure is uncertain. Our main theoretical contribution is a statistical characterization of optimal cost-robust contracts (Theorem 1): We prove a direct correspondence between optimal cost-robust contracts and statistical hypothesis tests by showing that the min-budget and min-pay contract objectives correspond to minimax risk functions of composite hypothesis tests (Type-1+Type-2 errors and FP/TP, respectively). This significantly generalizes a recent result by Saig et al. [32] to arbitrary action spaces and multiple optimality objectives. The statistical connection provides intuition and interpretation for numerical results, and the applicability to multiple objectives allows system designers to accommodate different business requirements. Intriguingly, the relation between the optimal contract and the optimal statistical risk have the same functional form in both objectives (min-budget and min-pay). Moreover, multiplying optimal hypothesis tests by a constant whose value depends only on the statistical risk yields approximately-optimal contracts (Theorem 2).

Finally, we evaluate the empirical performance of cost-robust contracts by analyzing LLM evaluation benchmarks for two families of tasks. In the first experiment, we compare the performance of two-outcome contracts across code generation tasks with varying difficulty; results show that what determines the pricing scheme is the relative success rates of the models, not the task difficulty. In the second experiment, we compute multi-outcome contracts for an intricate conversational task evaluated via LLM-as-a-judge. Numerical results show that the optimal monotone cost-robust pricing scheme has an intuitive 3-level structure: pay nothing if the quality is poor, pay extra if it is exceptional, and pay a fixed baseline otherwise. We show our framework’s flexibility by providing a comprehensive comparison across various contract objectives and monotonicity/threshold constraints.

1.1 Related work

Our main technical tool is algorithmic contract design (see [5, 20, 14] and subsequent works). We note that many works in this area address distributional robustness, e.g. [8], [14] (which also studies approximation guarantees of simple contracts), and the recent [3] which presents a distributionally-robust contract design approach for delegation of learning – but to our knowledge none address cost-robustness. Connections between contract design and statistics have long been known to exist at a high level (see, e.g., [33]), and were recently explored by [6] in the context of adverse selection, and [32] for two-action min-budget contract. From a technical standpoint, our work is closest to [32], which only proves the statistical connection for the special case of two-action min-budget contracts. Additional related work appears in Appendix A.

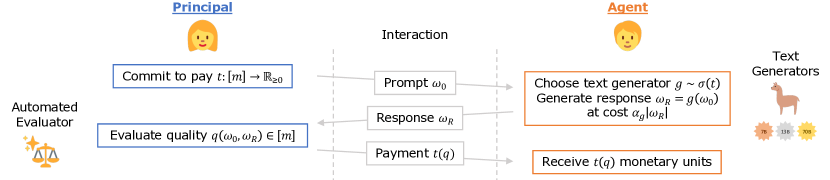

2 Problem Setting: Contract Design for Text Generation

We study the delegation of a text generation task from a strategic principal to agent, with a payment scheme designed to incentivize quality. Here we formulate the problem as a contract design instance.

2.1 Quality text generation (agent’s perspective)

The core of our setting is a standard language generation task. Let be a vocabulary of tokens, and denote the set of all token sequences by . A text generator is a mapping from a textual prompt to a response . We assume that prompts are sampled from a distribution , and denote by the distribution of (prompt, response) pairs where the prompt is sampled from and the response is generated by generator . Given a prompt and generated response, a quality evaluator is a function which scores the response on a scale of . We use to denote the distribution over scores induced by applying the quality evaluator to a random pair , and to denote the probability of score .

The agent has access to a collection of possible text generators , which we also refer to for convenience by their indices . Each model is associated with a model-dependent cost , which is the average cost (borne by the agent) of generating a single token from . For convenience we write and . Denote by the expected cost of using the th generator. We assume w.l.o.g. that the costs are non-decreasing, i.e., , and that they reflect the inherent quality of the models. In contract design terminology, the generators are the agent’s possible actions. The agent can choose a single (pure) action, or a distribution over text generators known in game theory as a mixed action.111 For example, the agent can generate responses using a larger model for 95% of requests, and apply the smaller model for the remaining 5%, corresponding to the mixed action . The cost of the lowest-cost action is the agent’s “opportunity cost”, and unless stated otherwise .222Choosing the first action can be thought of as opting out of the task at cost . If then the agent participates in the contract only if the expected utility is non-negative – a property known as individual rationality.

Connection to contract design.

The above setting is precisely a contract design setting with actions and outcomes [21]. Such a setting is defined by the pair , where is an matrix with distribution as its th row for every (known as the distribution matrix), and where is a vector of costs. For every action , and are the outcome distribution and cost, respectively.

Pay-for-performance and agent’s utility.

To incentivize high quality text generation, the principal commits in advance to a pay-for-performance contract, which specifies the amount of payment to the agent for generating a response with a certain quality. More formally, given a quality evaluator with an output scale , a contract is a mapping from the estimated quality to the size of the monetary transfer. Note that transfers are non-negative; this standard restriction is known as limited liability, and it mirrors the fact that when a principal hires an agent to perform a task, money flows in one way only (from principal to agent, and not vice versa). If transfers are increasing with score, we say is a monotone contract. Monotonicity is not without loss of generality, but is a desirable property as monotone contracts are generally simpler and easier to explain [14].

Given a contract and an action , the agent’s expected utility (a.k.a. the agent’s profit) is the difference between the expected reward and the expected cost of text generation:

where are the prompt and generated response, is the payment transferred to the agent based on the quality of response, and is the agent’s cost of generating the response. We assume the agent is rational and therefore selects, when facing contract , a pure action which maximizes their expected profit (also known as the agent’s best response):

As is standard in contract theory, we assume the agent breaks ties among different pure best responses consistently and in a way that agrees with the principal’s preferences.333In our context this means that if action is a best response for the agent, then the agent will choose that plays with probability 1 (see Section 2.2).

Figure 1 summarizes the interaction described in this section.

2.2 Designing the contract (principal’s perspective)

We assume throughout that the principal seeks to obtain text generated from the model , the most advanced model with the (strictly) highest associated cost . We refer to as the target action, i.e. the action which the principal wishes to incentivize.444For high-stake tasks such as summarizing medical information, it makes sense to target the most advanced model. In other cases, assuming a target action serves as a stepping stone towards the final contract design: the principal enumerates over different target actions and ultimately chooses the “best” among the resulting designs. Taking the role of the principal, our goal is now to design the “best” contract that incentivizes the agent to generate responses using the target model . This is formalized by the following optimization problem:

| (1) |

where is a norm of representing the principal’s economic objective (see below), and is a point-mass distribution over text generators, supported by the target generator . We denote the set of contracts incentivizing action by .

Information structure (who knows what).

The agent’s available actions and the possible scores are known to both players. As the quality distributions can be learned from past data, we assume they are known to both principal and agent. As the costs of inference depend on internal implementation details, we assume the costs are known to the agent but uncertain to the principal. We thus aim for a contract optimization framework which maximizes different types of objectives, and allows for optimization of even when the costs incurred by the agent are uncertain to the principal.

Objectives: min-budget, min-pay and min-variance contracts.

In eq. 1, different norms correspond to different possible optimization goals of the principal: For example, a contract is min-pay if it incentivizes the target action using minimum total expected payment among all contracts in [14]; In eq. 1, this corresponds to the norm weighted by the quality distribution of the target action. Similarly, a contract is min-budget if it incentivizes the target action using minimum budget [32]; In eq. 1, this corresponds to the norm. Additionally, we also consider a natural min-variance objective, which was not previously studied to our knowledge. A min-variance contract minimizes the objective , correspoding to a weighted norm (see Section B.7). We also consider approximately-optimal contracts:

Definition 1 (-optimal contract).

Let . For contract setting , let be the optimal contract with respect to objective . A contract is -optimal if .

3 Hypothesis Testing and Contracts

This section sets the stage for connecting cost-robust contracts to statistical tests in Section 4.

3.1 Preliminaries

Simple hypothesis tests

Consider two distributions . Given which is sampled from either or , a hypothesis test is a function which outputs if is likely to have been sampled from , and otherwise555When is fractional, we consider the output of the test to be with probability , and otherwise.. In the hypothesis testing literature, is a simple null hypothesis, and is a simple alternative hypothesis. Performance measures of hypothesis tests are derived from the probabilities of making different types of errors: For a test , the probability of false positives measures the rate of type-1 errors; This is when the test rejects the null hypothesis despite the sample being drawn from . Similarly, the probability of false negatives measures the rate of type-2 errors, i.e. when the test does not reject the null hypothesis despite the sample being drawn from . We also denote the true positives by ; is also known as the test’s power, and equal to .

Composite hypothesis tests.

Consider now two sets of distributions , , where for all . In hypothesis testing terms, is a composite null hypothesis. is a simple alternative hypothesis as before, and a composite hypothesis test outputs if a given is likely to have been sampled from . To define performance in the composite case, we denote by the standard type-1 error between distributions and . As the alternative hypothesis is still simple, definitions of and remain as before, using as the reference distribution. To measure the performance of hypothesis tests, it is common to take a worst-case approach, and define the composite as the standard type-1 error against the worst-case distribution in the null hypothesis set.

3.2 Risk and minimax tests

To formalize the notion of worst-case error, let be a composite hypothesis test for , . For any , define a risk function to be a mapping from to a risk score, treating as a simple hypothesis test between distributions and . A natural way of measuring risk is by combining the test’s two error types. One measure is the sum of errors, denoted by . A classic result by Neyman and Pearson shows that is minimized by the likelihood-ratio test for any fixed [30]. Another measure is the ratio of false positives to true positives, denoted by . To generalize a risk measure to a composite hypothesis test, we adopt the worst-case approach and define . Thus, , and .

Definition 2 (Minimax hypothesis test).

Let be a composite hypothesis test for , , and fix a risk function . The test is minimax optimal w.r.t. if it minimizes the worst-case risk:

The minimax sum-optimal test and minimax ratio-optimal test are the minimax optimal tests with respect to the sum and the ratio , respectively.

Observe that the optimal risk of both types of tests is bounded by , as the constant test satisfies . We assume at least a small difference between the hypotheses, such that . This allows us to define contracts based on these tests.

3.3 From tests to contracts and back

We derive “statistical” contracts from hypothesis tests by multiplying them by a function of the risk, and derive “contractual” tests from contracts by normalizing them: Consider a contract setting , with either known costs and , or a cost upper bound . Fix a risk function and a corresponding budget function .

-

•

Test-to-contract: Let be a test for sets , with budget . The corresponding statistical contract is .

-

•

Contract-to-test: Let be a contract. The corresponding contractual test is .

We are interested in the following statistical contracts corresponding to the tests from Definition 2:

Definition 3.

Consider a contract setting , with either known costs and , or a cost upper bound . The sum-optimal statistical contract is obtained from the minimax sum-optimal test multiplied by . The ratio-optimal statistical contract is obtained from the minimax ratio-optimal test multiplied by .

4 Cost-Robust Contracts

In this section we state and prove our main result – a direct connection between composite hypothesis testing and cost-robust contracts. Consider a contract design setting with increasing costs , where is the target action. In real-world settings, the principal may not have full knowledge of the agent’s internal cost structure. We model this by assuming the principal is oblivious to the precise costs, but knows an upper bound . We are interested in robust contracts that incentivize the target action for any cost vector compatible with the upper bound:

Definition 4 (Cost-robust contracts).

Consider a distribution matrix and a bound on the costs. Let be an ambiguity set of all increasing cost vectors such that . A contract is -cost-robust if it implements action for any cost vector .

Informally, our main theoretical result shows that optimal cost-robust contracts are optimal hypothesis tests up to scaling, where the scaler depends on the risk measure which the test optimizes. Our approach can be applied to several notions of optimality, and each optimality criterion for contracts corresponds to a different optimality criterion for hypothesis tests. Specifically, we derive the correspondence for min-budget and min-pay optimality of contracts. Formally (recall Definition 3):

Theorem 1 (Optimal cost-robust contracts).

For every contract setting with distribution matrix and an upper bound on the (unknown) costs, let (resp., ) be the minimax sum-optimal (ratio-optimal) test with risk ( among all composite hypothesis tests for , . Then:

-

•

The sum-optimal statistical contract is -cost-robust with budget , and has the lowest budget among all -cost-robust contracts;

-

•

The ratio-optimal statistical contract is -cost-robust with expected total payment , and has the lowest expected total payment among all -cost-robust contracts.

| Economic objective | Objective function | Statistical objective | Risk function |

| Min-budget | |||

| Min-pay |

Table 1 summarizes the contract vs. test equivalences arising from Theorem 1. In the special case of contract settings combining (i) a binary action space (), (ii) a tight upper bound (), and (iii) a zero-cost action (), the first half of Theorem 1 recovers a recently-discovered correspondence between hypothesis testing and (non-cost-robust) two-action min-budget contracts [32, Theorem 2]. Theorem 1 is more general since it applies to any number of actions as well as to the standard min-pay objective. Thus, Theorem 1 can also be seen as extending the interpretable format of optimal contracts for binary-action settings beyond two actions.

In Section B.2, we derive our main lemmas, which are used in Section B.4 to prove Theorem 1.

4.1 Additional properties of optimal cost-robust contracts

In this section, we focus for concreteness on min-budget cost-robust contracts, and establish their approximation guarantees as well as their functional form under assumptions (similar results hold for min-pay cost-robust contracts). First, in analogy to [14], a natural question is what are the approximation guarantees of cost-robust contracts. We show (recall Definition 1):

Theorem 2 (Approximation guarantees).

For every contract setting , let be a lower and upper bound on the difference between the target cost and any other cost, i.e., for all . Then the min-budget -cost-robust contract for is -optimal with respect to the budget objective , and the approximation ratio is tight.

Proof in Section B.5. As a corollary, combining this result with Theorem 1 shows that statistical contracts are approximately optimal in the global sense: For any contract setting with corresponding minimax sum-optimal hypothesis test , the contract is -optimal with respect to the budget metric and .

We next turn to consider the functional form of optimal cost-robust contracts (i.e., why their payments are as they are). One of the criticisms of optimal (non-robust) contracts is that the payments seem arbitrary and opaque. Compared to this, cost-robust contracts are more transparent and explainable. We show two additional results regarding their format, leveraging the connection to minimax hypothesis testing.

The first result explains the budget: By the minimax principle, there is a “least favorable distribution” (to use terminology from statistics) or, equivalently, a mixed strategy over the rows of (to use terminology from game theory) such that no test can achieve for it better risk than the minimax risk . We show that the budget of the optimal cost-robust contract can be interpreted using this distribution. Formally, let be the total variation distance between distributions , then the budget is as follows (see Appendix B.5 for a proof):

Proposition 1 (Distribution distance determines budget).

For every contract setting with distribution matrix and spread of costs , the minimum budget of a -cost-robust contract is

The distribution that maximizes the above expression is the least favorable one. Intuitively, the closer it is to the target distribution , the larger the budget needed for the agent to distinguish among them and prefer the target action. Finally, we add some standard structure to the distribution matrix to obtain even simpler contract formats:

Definition 5 (Monotone Likelihood Ratio (MLR)).

A distribution matrix satisfies MLR if is monotonically increasing in for all .

Intuitively, if satisfies MLR, then the higher the outcome , the more likely it is to origin from a more costly distribution than from (recall that costs are increasing in ). Consider minimax composite hypothesis tests for , ; if does not satisfy MLR, optimal such tests may require randomization (i.e., for some outcome ) and/or non-monotonicity (i.e. for some pair of outcomes ). However, if MLR holds for , then nice properties (determinism, monotonicity) hold for minimax tests (e.g., by the Karlin-Rubin theorem [30]), and consequently also for cost-robust contracts (see Appendix B.6 for a proof):

Proposition 2 (MLR induces threshold simplicity).

For every contract setting with distribution matrix that satisfies MLR, and with spread of costs , the min-budget -cost-robust contract for is a monotone threshold contract, which pays full budget to the agent for every outcome above some threshold .666For min-pay rather than min-budget, under MLR we get a monotone contract with a single positive payment, which is optimal — see [14, Lemma 7].

5 Empirical Evaluation

We evaluate the empirical performance of our cost-robust contracts using LLM evaluation benchmarks. We compute binary and multi-outcome contracts for two distinct families of tasks based on evaluation scores from known benchmark datasets, optimizing the contract objectives set forth in Section 2.2. Our action space consists of the 7B, 13B, and 70B parameter model versions of the open-sourced Llama2 and CodeLlama LLMs [38, 31], which share the same architecture and hence similar inference costs. The benchmark data is used to create an empirical outcome distribution for each LLM in the action space. In both cases, contract optimization targets of the largest model variant (70B), which is the most performant and costly. Implementation details are provided in Section C.3, and code is available at: https://github.com/edensaig/llm-contracts.

Cost estimation.

To estimate the inference costs of the language models, we leverage their open-source availability. We use energy consumption data from the popular Hugging Face LLM-Performance Leaderboard [22, 23], which we then convert to dollar values using conservative cost estimates. Estimation details are provided in Section C.1. As a first-order assumption of cost uncertainty, we assume that inference costs of alternative generators are bounded from below by the cost of the most energy-efficient alternative model (), and bounded from above by the cost of the alternative model with the highest energy consumption ().

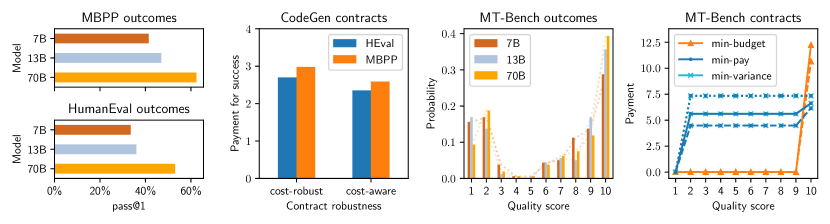

5.1 Binary-outcome contracts across tasks (code generation)

We begin by analyzing a simple contract design setting across benchmarks of varying difficulties. We use the LLM task of code-generation which has outcomes: pass or fail. The analysis of a binary outcome space is motivated by the following theoretical property:

Proposition 3.

For any contract design problem with where the most-costly (target) action has the highest pass rate, the optimal contract is identical for all optimality objectives (min-pay, min-budget, and min-variance). Moreover, the optimal contract satisfies , .

Proof in Section B.8. Proposition 3 allows us to compare performance across different evaluation tasks without being sensitive to the choice of contract objective and constraints such as monotonicity.

Datasets.

We use evaluation data from two distinct benchmarks, which represent differing degrees of task difficulty. The Mostly Basic Programming Problems (MBPP) benchmark [4] contains 974 entry-level programming problems with 3 unit tests per problem. The HumanEval benchmark [11] consists of 164 hand-written functional programming problems. Included in each programming problem is a function signature, a doc-string prompt, and unit tests. There is an average of 7.7 unit tests per problem, and the overall score is based on a pass/fail evaluation of the responses. For each of these benchmarks, we create a binary-outcome () contract from the pass rates of the CodeLlama model family (CodeLlama-{7B,13B,70B}). We use the pass@1 values from the CodeLlama paper [31] (success rates for a single response), as they capture a setting where the agent gets paid for each response.

Task difficulty and optimal pay.

Figure 2 (Left-Center) presents optimal cost-aware and cost-robust contracts for code-generation. We observe that cost uncertainty entails a consistent increase in payment across tasks: For MBPP, we observe a 14.9% increase, and for HumanEval we observe a similar 14.7% increase. Additionally, while the MBPP task is easier than HumanEval (i.e. characterized by higher pass rates), the resulting contracts for MBPP are more expensive. This demonstrates the fundamental connection between contracts and statistics: In MBPP, there is smaller gap between the performance of the target model (70B) and the performance of the alternatives. This makes the highest-performing model harder to detect, increasing the cost of the contract. The required payments in this case thus depend on the absolute differences between pass rates, rather than absolute values.

5.2 Multi-outcome contracts

To understand the relation between different optimality objectives and constraints, we analyze optimal contracts in an expressive multi-outcome () environment based on MT-Bench.

Dataset.

The MT-Bench benchmark [42] is designed to evaluate the conversational and instruction-following abilities of LLMs in multi-turn (MT) conversational settings. The benchmark consists of 80 prompts in the format of multi-turn questions, and the evaluation dataset includes LLM-as-a-judge evaluations on (prompt,response) pairs from various models, using GPT-4 as the judge. In the dataset, each (prompt,response) pair is given discrete response quality scores in the range . These scores define our contract outcome space. In consistence with the analysis in section 5.1, we use the outcome distributions of (Llama-2-{7B,13B,70B}-chat), and target the 70B model. Outcome distributions for the MT-Bench dataset are presented in Figure 2.

Simple optimal contracts.

In practical applications, contracts with a simple functional form are often preferred since they are easier to comprehend. We compute optimal contracts with two types of simplicity constraints: monotone contracts (weakly increasing payout), and threshold contracts (full budget for all scores above a threshold, and zero otherwise). Results are presented in Figure 2 (Right), and Table 2. For the min-budget and min-variance criteria, monotone cost-robust contracts have an intuitive three-level structure: Zero pay for outputs with the lowest quality score, base pay for intermediate scores, and extra pay for outputs with the highest quality score. While threshold contracts may resemble current pricing schemes more closely (see Section C.1), monotone contracts enable a lower overall budget while still maintaining a simple functional form. For min-pay, monotone cost-robust contracts are in themselves threshold contracts, however they may deter risk-averse agents as they only pay for highest-quality outputs. In Section C.2, we additionally analyze non-monotone contracts, and show that further economic efficiency can be achieved by sacrificing simplicity.

Price of cost-robustness.

Table 2 compares cost-robust and cost-aware monotone contracts across different performance metrics. We observe that cost-robust contracts setting sacrifice a marginal increase in objective values: a increase in the min-pay objective, an increase if optimizing for budget, and increase when optimizing for minimum variance. We refer to Section C.2 for further analysis of cost-robustness in the non-monotone setting.

| Cost-aware | Cost-robust | |||||

| Budget | Budget | |||||

| Min-Pay | 4.19 | 10.6 | 5.2 | 4.82 (+15%) | 12.2 | 5.98 |

| Min-Budget | 4.73 | 6.16 | 1.71 | 5.48 | 6.63 (+1.7%) | 1.83 |

| Min-Variance | 4.73 | 6.16 | 1.71 | 5.48 | 6.63 | 1.83 (+6.7%) |

6 Discussion

In this paper, we introduce cost-robust contracts as a means to address the emerging problem of moral hazards in LLM inference. Our aim is to offer flexible payment schemes that ensure integrity in current LLM markets, even when facing challenges of incomplete information. One of the key insights from our study is that cost-robust contracts can be relevant and effective in practical settings. Moreover, we generalize the work paved by Saig et al. [32] by uncovering stronger connections between the fields of contract design and statistical hypothesis testing. These connections underscore the statistical intuition that is prevalent in contract design.

Despite the promising results, our work still has several limitations that would do well to be addressed in future research. For one, the data we capture through the evaluation benchmarks does not accurately reflect real-world distributions, where the prompt space is much richer. A natural direction for future work is to explore approximation guarantees when learning contracts from data. Additionally, our analysis relies on a set of assumptions regarding the cost uncertainty and estimations, which should be carefully considered when designing contracts for Generative AI. Lastly, it would also be interesting to see our contract design framework applied to markets with a more elaborate action space.

Acknowledgements.

The authors would like to thank Nir Rosenfeld, Stephen Bates, and Michael Toker for their insightful remarks and valuable suggestions. Eden Saig is supported by the Israel Council for Higher Education PBC scholarship for Ph.D. students in data science. Funded by the European Union (ERC, ALGOCONTRACT, 101077862, PI: Inbal Talgam-Cohen).

References

- Achiam et al. [2023] Josh Achiam, Steven Adler, Sandhini Agarwal, Lama Ahmad, Ilge Akkaya, Florencia Leoni Aleman, Diogo Almeida, Janko Altenschmidt, Sam Altman, Shyamal Anadkat, et al. Gpt-4 technical report. arXiv preprint arXiv:2303.08774, 2023.

- Agrawal et al. [2018] Akshay Agrawal, Robin Verschueren, Steven Diamond, and Stephen Boyd. A rewriting system for convex optimization problems. Journal of Control and Decision, 5(1):42–60, 2018.

- Ananthakrishnan et al. [2024] Nivasini Ananthakrishnan, Stephen Bates, Michael Jordan, and Nika Haghtalab. Delegating data collection in decentralized machine learning. In International Conference on Artificial Intelligence and Statistics, pages 478–486. PMLR, 2024.

- Austin et al. [2021] Jacob Austin, Augustus Odena, Maxwell Nye, Maarten Bosma, Henryk Michalewski, David Dohan, Ellen Jiang, Carrie Cai, Michael Terry, Quoc Le, et al. Program synthesis with large language models. arXiv preprint arXiv:2108.07732, 2021.

- Babaioff et al. [2012] Moshe Babaioff, Michal Feldman, Noam Nisan, and Eyal Winter. Combinatorial agency. Journal of Economic Theory, 147(3):999–1034, 2012.

- Bates et al. [2022] Stephen Bates, Michael I Jordan, Michael Sklar, and Jake A Soloff. Principal-agent hypothesis testing. arXiv preprint arXiv:2205.06812, 2022.

- Brown et al. [2020] Tom Brown, Benjamin Mann, Nick Ryder, Melanie Subbiah, Jared D Kaplan, Prafulla Dhariwal, Arvind Neelakantan, Pranav Shyam, Girish Sastry, Amanda Askell, et al. Language models are few-shot learners. Advances in neural information processing systems, 33:1877–1901, 2020.

- Carroll [2015] Gabriel Carroll. Robustness and linear contracts. American Economic Review, 105(2):536–563, 2015.

- Chang et al. [2023] Yupeng Chang, Xu Wang, Jindong Wang, Yuan Wu, Kaijie Zhu, Hao Chen, Linyi Yang, Xiaoyuan Yi, Cunxiang Wang, Yidong Wang, Wei Ye, Yue Zhang, Yi Chang, Philip S. Yu, Qiang Yang, and Xing Xie. A survey on evaluation of large language models. arXiv preprint arXiv:2307.03109, 2023.

- Chen et al. [2023] Lingjiao Chen, Matei Zaharia, and James Zou. Frugalgpt: How to use large language models while reducing cost and improving performance. arXiv preprint arXiv:2305.05176, 2023.

- Chen et al. [2021] Mark Chen, Jerry Tworek, Heewoo Jun, Qiming Yuan, Henrique Ponde de Oliveira Pinto, Jared Kaplan, Harri Edwards, Yuri Burda, Nicholas Joseph, Greg Brockman, et al. Evaluating large language models trained on code. arXiv preprint arXiv:2107.03374, 2021.

- Diamond and Boyd [2016] Steven Diamond and Stephen Boyd. CVXPY: A Python-embedded modeling language for convex optimization. Journal of Machine Learning Research, 17(83):1–5, 2016.

- Duetting et al. [2023] Paul Duetting, Vahab Mirrokni, Renato Paes Leme, Haifeng Xu, and Song Zuo. Mechanism design for large language models. arXiv preprint arXiv:2310.10826, 2023.

- Dütting et al. [2019] Paul Dütting, Tim Roughgarden, and Inbal Talgam-Cohen. Simple versus optimal contracts. In Proceedings of the 2019 ACM Conference on Economics and Computation, pages 369–387, 2019.

- Fish et al. [2023] Sara Fish, Paul Gölz, David C Parkes, Ariel D Procaccia, Gili Rusak, Itai Shapira, and Manuel Wüthrich. Generative social choice. arXiv preprint arXiv:2309.01291, 2023.

- Goulart and Chen [2024] Paul J. Goulart and Yuwen Chen. Clarabel: An interior-point solver for conic programs with quadratic objectives, 2024.

- Greene and Nash [2009] Stuart E Greene and David B Nash. Pay for performance: an overview of the literature. American Journal of Medical Quality, 24(2):140–163, 2009.

- Harris et al. [2023] Keegan Harris, Nicole Immorlica, Brendan Lucier, and Aleksandrs Slivkins. Algorithmic persuasion through simulation: Information design in the age of generative ai. arXiv preprint arXiv:2311.18138, 2023.

- He et al. [2023] Kai He, Rui Mao, Qika Lin, Yucheng Ruan, Xiang Lan, Mengling Feng, and Erik Cambria. A survey of large language models for healthcare: from data, technology, and applications to accountability and ethics. arXiv preprint arXiv:2310.05694, 2023.

- Ho et al. [2016] Chien-Ju Ho, Aleksandrs Slivkins, and Jennifer Wortman Vaughan. Adaptive contract design for crowdsourcing markets: Bandit algorithms for repeated principal-agent problems. Journal of Artificial Intelligence Research, 55:317–359, 2016.

- Holmström [1979] Bengt Holmström. Moral hazard and observability. The Bell journal of economics, pages 74–91, 1979.

- Ilyas Moutawwakil [2023a] Régis Pierrard Ilyas Moutawwakil. Llm-perf leaderboard. https://huggingface.co/spaces/optimum/llm-perf-leaderboard, 2023a.

- Ilyas Moutawwakil [2023b] Régis Pierrard Ilyas Moutawwakil. Optimum-benchmark: A framework for benchmarking the performance of transformers models with different hardwares, backends and optimizations., 2023b.

- Lai et al. [2023] Jinqi Lai, Wensheng Gan, Jiayang Wu, Zhenlian Qi, and Philip S Yu. Large language models in law: A survey. arXiv preprint arXiv:2312.03718, 2023.

- Lehmann et al. [1986] Erich Leo Lehmann, Joseph P Romano, and George Casella. Testing statistical hypotheses, volume 3. Springer, 1986.

- Li et al. [2023a] Junlong Li, Shichao Sun, Weizhe Yuan, Run-Ze Fan, Hai Zhao, and Pengfei Liu. Generative judge for evaluating alignment. arXiv preprint arXiv:2310.05470, 2023a.

- Li et al. [2023b] Linyang Li, Pengyu Wang, Ke Ren, Tianxiang Sun, and Xipeng Qiu. Origin tracing and detecting of llms. arXiv preprint arXiv:2304.14072, 2023b.

- Li et al. [2023c] Yinheng Li, Shaofei Wang, Han Ding, and Hang Chen. Large language models in finance: A survey. In Proceedings of the Fourth ACM International Conference on AI in Finance, pages 374–382, 2023c.

- Liu et al. [2023] Yang Liu, Dan Iter, Yichong Xu, Shuohang Wang, Ruochen Xu, and Chenguang Zhu. G-eval: NLG evaluation using gpt-4 with better human alignment. In Houda Bouamor, Juan Pino, and Kalika Bali, editors, Proceedings of the 2023 Conference on Empirical Methods in Natural Language Processing, EMNLP 2023, Singapore, December 6-10, 2023, pages 2511–2522. Association for Computational Linguistics, 2023. URL https://aclanthology.org/2023.emnlp-main.153.

- Rigollet and Hütter [2015] Phillippe Rigollet and Jan-Christian Hütter. High dimensional statistics. Lecture notes for course 18S997, 813(814):46, 2015.

- Roziere et al. [2023] Baptiste Roziere, Jonas Gehring, Fabian Gloeckle, Sten Sootla, Itai Gat, Xiaoqing Ellen Tan, Yossi Adi, Jingyu Liu, Tal Remez, Jérémy Rapin, et al. Code llama: Open foundation models for code. arXiv preprint arXiv:2308.12950, 2023.

- Saig et al. [2023] Eden Saig, Inbal Talgam-Cohen, and Nir Rosenfeld. Delegated classification. arXiv preprint arXiv:2306.11475, 2023.

- Salanié [2017] Bernard Salanié. The Economics of Contracts: A Primer. MIT press, 2017.

- Samsi et al. [2023] Siddharth Samsi, Dan Zhao, Joseph McDonald, Baolin Li, Adam Michaleas, Michael Jones, William Bergeron, Jeremy Kepner, Devesh Tiwari, and Vijay Gadepally. From words to watts: Benchmarking the energy costs of large language model inference. In 2023 IEEE High Performance Extreme Computing Conference (HPEC), pages 1–9. IEEE, 2023.

- Singhal et al. [2023] Karan Singhal, Shekoofeh Azizi, Tao Tu, S Sara Mahdavi, Jason Wei, Hyung Won Chung, Nathan Scales, Ajay Tanwani, Heather Cole-Lewis, Stephen Pfohl, et al. Large language models encode clinical knowledge. Nature, 620(7972):172–180, 2023.

- Sun [2023] Zhongxiang Sun. A short survey of viewing large language models in legal aspect. arXiv preprint arXiv:2303.09136, 2023.

- Touvron et al. [2023a] Hugo Touvron, Thibaut Lavril, Gautier Izacard, Xavier Martinet, Marie-Anne Lachaux, Timothée Lacroix, Baptiste Rozière, Naman Goyal, Eric Hambro, Faisal Azhar, et al. Llama: Open and efficient foundation language models. arXiv preprint arXiv:2302.13971, 2023a.

- Touvron et al. [2023b] Hugo Touvron, Louis Martin, Kevin Stone, Peter Albert, Amjad Almahairi, Yasmine Babaei, Nikolay Bashlykov, Soumya Batra, Prajjwal Bhargava, Shruti Bhosale, et al. Llama 2: Open foundation and fine-tuned chat models. arXiv preprint arXiv:2307.09288, 2023b.

- Uchendu et al. [2020] Adaku Uchendu, Thai Le, Kai Shu, and Dongwon Lee. Authorship attribution for neural text generation. In Proceedings of the 2020 Conference on Empirical Methods in Natural Language Processing (EMNLP), pages 8384–8395, 2020.

- Yang et al. [2023a] Xianjun Yang, Wei Cheng, Linda Petzold, William Yang Wang, and Haifeng Chen. Dna-gpt: Divergent n-gram analysis for training-free detection of gpt-generated text. arXiv preprint arXiv:2305.17359, 2023a.

- Yang et al. [2023b] Xianjun Yang, Liangming Pan, Xuandong Zhao, Haifeng Chen, Linda Petzold, William Yang Wang, and Wei Cheng. A survey on detection of llms-generated content. arXiv preprint arXiv:2310.15654, 2023b.

- Zheng et al. [2024] Lianmin Zheng, Wei-Lin Chiang, Ying Sheng, Siyuan Zhuang, Zhanghao Wu, Yonghao Zhuang, Zi Lin, Zhuohan Li, Dacheng Li, Eric Xing, et al. Judging llm-as-a-judge with mt-bench and chatbot arena. Advances in Neural Information Processing Systems, 36, 2024.

Appendix A Additional Related Work

Detection.

As a possible alternative to a contract-design approach, the LLM content detection literature develops tools which attempt to detect machine-generated text, and distinguish between different text generators [39, 27, 40, 41]. Using such tools, a principal could deploy an LLM content detector and penalize firms who are not labeled as using target text generator. From this perspective, contract design is a complementary approach which provides guidelines for positive incentives in case a generated text gets accepted, an approach considered more effective at encouraging participation. Additionally, our pay-for-performance framework supports richer outcomes spaces beyond binary pass/fail, enabling more granular, and thus more efficient, control of incentives.

AGT and LLMs.

On a broader perspective, our work further promotes the role of Algorithmic Game Theory in the economics of Generative AI. Previous works include: Duetting et al. [13] who design auctions that merge outputs from multiple LLMs; Harris et al. [18] who offer a Bayesian Persuasion setting where the sender can use Generative AI to simulate the receiver’s behavior; and Fish et al. [15] who leverage the creative nature of LLMs to enhance social choice settings.

Appendix B Deferred Proofs

B.1 Linear programs and equivalent forms

In this appendix we include linear programs (LPs) for optimizing contracts and hypothesis tests. Non-negativity constraints on the variables are ommitted where clear from context.

By definition (see Section 2.2), a contract is min-budget with respect to target action if and only if it is an optimal solution to the following MIN-BUDGET LP, where IC stands for incentive compatibility (i.e., the constraints that ensure the agent’s best response to is choosing action ):

| (2) | ||||||

Proposition 4 (Equivalent form to the MIN-BUDGET LP; [32, B.2]).

When eq. 2 is feasible, the variable transformation yields an equivalent LP which we refer to as the statistical LP:

| (3) | |||||

Similarly to the MIN-BUDGET LP, we have the MIN-PAY LP:

| (4) | ||||||

There are also natural LP formulations for hypothesis testing. A hypothesis test is the minimax sum-optimal test w.r.t. risk (see Definition 2) if and only if it is an optimal solution to the following LP:

| (5) | |||||

Proposition 5 (Dual of statistical LP).

The dual of eq. 3 is given by:

| (6) | |||||

B.2 Main lemmas

The next lemmas are the workhorses of our theoretical results. We use to denote the set of contracts incentivizing the target action in a contract design setting ; the contracts in are also known as the feasible solutions of the setting. For simplicity we focus on settings for which the set of feasible solutions is nonempty (i.e., the target action is implementable). Given either a non-decreasing cost vector and an index , or a cost and a constant , define

These are vectors with uniform costs (up to . Note that the costs in are (weakly) lower than those in , and vice versa for . Intuitively, since the agent gravitates towards lower costs, it is harder to incentivize the target action against lower costs. We formalize this as follows:

Lemma 1 (Incentivizing against lower costs is harder).

Consider a distribution matrix , and two cost vectors satisfying (i.e., is dominated by ). Then the sets of feasible solutions for contract design settings and satisfy .

Corollary 1.

For every contract design setting , the set of feasible solutions satisfies

Consider now a contract setting , where the action costs are uniformly equal to except for the target action (which is more costly). We show that for such a setting, the optimal contract for incentivizing the target action has an interpretable format closely related to hypothesis testing. Recall the notions of sum-optimal and ratio-optimal statistical contracts from Definition 3; then:

Lemma 2 (Min-budget optimality in uniform-cost settings).

For every contract design setting , the min-budget contract coincides with the sum-optimal statistical contract , and the optimal budget is .

Lemma 3 (Min-pay optimality in uniform-cost settings).

For every contract design setting , the min-pay contract coincides with the ratio-optimal statistical contract , and the optimal expected total payment is .

Proofs appear in Appendix B.3, establishing also the other direction:

Observation 1.

Let be a contract design setting. Then the minimax sum-optimal test among the composite hypothesis tests for , is obtained by normalizing the min-budget contract, and the minimax ratio-optimal test is obtained by normalizing the min-pay contract.

B.3 Proofs of main lemmas

Proof of Lemma 1.

For target action and any alternative action , the (IC) constraint of the MIN-BUDGET LP (eq. 2) is given by:

Rearranging the terms yields:

| (9) |

The costs are assumed to be increasing in , and therefore for all . Moreover, as for all , the RHS of eq. 9 satisfies:

Hence, the (IC) constraints of the contract design problem are more restrictive than the (IC) constraints of the design problem. Since the design problems only differ in the RHS of the (IC) constraints, the sets of feasible solutions satisfy the desired inclusion relation. ∎

Proof of Lemma 2.

Under the “statistical” variable transformation , the MIN-BUDGET LP for is given by eq. 3:

Applying the variable transformation yields the following equivalent LP:

This LP is equivalent to the minimax sum-optimal test in eq. 5, and therefore the optimal solution is precisely this test. By the same equivalence, the optimal value of the optimization parameter satisfies , where is the minimax risk of the testing problem (i.e., the risk of ). By construction, the optimal satisfies , and therefore the minimal budget is which in the notation of Definition 3 is . Reversing the variable transformation we get , which is equal to the sum-optimal statistical contract , as required. ∎

Proof of Lemma 3.

For the min-pay contract design problem, introduce an auxiliary variable , and define a “statistical” variable transformation , where . The MIN-PAY LP (eq. 4) transforms into:

| (10) | |||||

For any given , the optimal value of is:

Therefore, eq. 10 is equivalent to:

| (11) |

Divide the numerator and the denominator by to obtain the transformed objective:

And hence eq. 11 can be written compactly as:

| (12) |

The optimal solution for eq. 12 is the minimizer of , which is equivalent to the minimax ratio-optimal test by Definition 2. The optimal expected pay is , and the optimal contract is given by:

where is as in Definition 3. We conclude that is the ratio-optimal statistical contract, as required. ∎

B.4 Proof of main theorem

We are now ready to prove our main theorem:

Proof of Theorem 1.

We prove the first half of the theorem, i.e., that the sum-optimal statistical contract is -cost-robust and has the lowest budget among all -cost-robust contracts. The second half of the theorem follows by swapping Lemma 2 with Lemma 3.

We first show that the sum-optimal statistical contract is -cost-robust, i.e., incentivizes the target action for every cost vector in the ambiguity set : Define . By Lemma 2, the min-budget contract for the setting is the sum-optimal statistical contract , i.e., , where is the minimax sum-optimal composite test for distribution sets , . Its budget is .

In particular, incentivizes the target action and so belongs to . Observe that any increasing cost vector with dominates the cost vector , and therefore by Lemma 1, contract also belongs to for any such cost vector that dominates . Furthermore, any cost vector in the ambiguity set has a corresponding cost vector in which all costs are identical except for . Lowering the target action’s cost from to can only help incentivize it, thus we conclude that , as required.

We now show optimality of the budget: Since is the min-budget contract for the setting , and since is within the ambiguity region , it holds that any -cost-robust contract must satisfy . As satisfies this bound exactly, it has the lowest budget among all -cost-robust contracts. ∎

B.5 Proof of properties of optimal cost-robust contracts

Proof of Theorem 2.

Let and be two uniform-cost profiles; for brevity we refer to these as . Since in contract setting it holds that for all , we have that for all . Thus by Lemma 1 it holds that

| (13) |

that is, any contract that incentivizes the target action in setting will incentivize it also in setting .

Consider the min-budget contracts for settings . Denote their budgets by , respectively. We deduce from Equation 13 that

| (14) |

since the min-budget contract for is feasible for . Now recall that Lemma 2 gives us an expression for the optimal budgets of the two uniform-cost settings. This expression depends on the risk of the minimax sum-optimal hypothesis test for , , which is static across the two settings. It also depends on the difference between the highest and lowest cost in each setting. Thus:

| (15) |

Combining Equation 14 and Equation 15 we get . We conclude that the min-budget contract for setting is a -min-budget contract for . By Lemma 2 the min-budget contract is the sum-optimal statistical contract , which by Theorem 1 is the -cost-robust contract with the lowest budget, as required.

We now turn to the claim of tightness. Consider the following contract design setting:

Where costs are increasing , and is a parameter satisfying:

| (16) |

The target distribution is only supported on , and therefore the minimax sum-optimal test for this setting is:

As do not overlap, the minimax risk is given with respect to by the Neyman-Pearson Lemma [30]:

and therefore the approximate contract given by Theorem 2 is:

As for the optimal contract, it satisfies because the target distribution is only supported on , and it has a threshold form due to [32, Lemma 4]. The optimal budget is:

Proof of Proposition 1.

By Theorem 1 and Lemma 2, the -cost-robust contract with minimum budget is the min-budget contract for setting where . For this setting, plugging variables , into the dual in eq. 6, we get:

Define the following variable transformation:

Under this transformation, the dual LP is equivalent to:

When the contract is implementable, the optimal solution to the primal statistical LP (eq. 3) satisfies , corresponding to the last constraint in the dual LP. Therefore, the last constraint of the dual is tight due to complementary slackness:

and the LP is equivalent to:

As we can write:

and by the definition of total variation distance (e.g by [32, Claim 4]), the optimization objective satisfies:

Applying the inverse transformation yields:

Then, by strong LP duality , and the final result is obtain by applying the nonlinear variable transformation . This gives the desired expression for the minimum budget of a -cost-robust contract: ∎

B.6 MLR

In this section, we prove that cost-robust min-budget contracts for distributions satisfying the Monotone Likelihood Ratio (MLR) property have a threshold functional form.

Proof of Proposition 2.

Let be a contract design setting with , such that satisfies monotone likelihood ratio. By the Karlin-Rubin theorem, the hypothesis test for the composite hypotheses , minimizing is a threshold function, and therefore there exists such that . By Theorem 1, the optimal contract in this case is of the form for some scalar , and therefore is a threshold contract. ∎

B.7 Min-variance contracts

Claim 1.

A min-variance contract is an optimal solution for the following quadratic program:

| (17) | ||||||

Where is a positive semi-definite matrix depending on the target action distribution .

Proof.

Denote the contract by and the probability distribution of the target action by . We use the following matrix notations:

The variance of is given by:

Denote , and . Then:

Note that is a Gram matrix. It is therefore positive semi-definite, and the quadratic program is convex. ∎

B.8 Two-outcome settings

Claim 2.

Let be a two-outcome contract design setting (). A contract with implements the target action if and only if the contract implements the target action.

Proof.

For any action , the corresponding (IC) constraint is:

| (18) |

As , are probability distributions, the following holds for any :

| (19) |

Subtracting eq. 19 from eq. 18 does not change the (IC) constraint, as both sides of eq. 19 are equal. Performing the subtraction and rearranging the terms gives:

which is equivalent to:

and this is the (IC) constraint for the contract . Therefore, the contract is feasible if and only if the contract is feasible. ∎

Claim 3.

Let be a two-outcome contract design setting (), and let . Then the contract has weakly-better expected pay, weakly-better budget requirements, and the same variance as .

Proof.

For the min-pay objective, we obtain from linearity of expectation:

and therefore has weakly-better expected pay. For the min-budget objective, it holds that :

and therefore has weakly-better budget requirement. for the min-variance objective, adding a constant to a random variable does not affect its variance:

and therefore has the same variance as . ∎

Proof of Proposition 3.

For all , let . As , any contract is a two-dimensional vector. By 2, 3, it holds that the optimal contract is of the form for any of the three objectives. To prove that the optimal payment is the same for all objectives, observe that all objective functions are monotonically-increasing in :

| (Required budget) | ||||

| (Expected pay) | ||||

| (Variance) |

Since all the optimization problems are of a single variable with identical (IC) constraints, their optimal solutions are all identical. ∎

Appendix C Experiments/Empirical Evaluation

C.1 Inference Costs

To calculate the costs for each model, we use energy data from the Hugging Face LLM Performance Leaderboard777https://huggingface.co/spaces/optimum/llm-perf-leaderboard.. The energy efficiency for each model is expressed in the leaderboard in units of output tokens per kWH. To convert to actionable costs we assume a rate of .105 $/kWH, aligning with conservative energy costs in the United States and giving us order-of-magnitude approximations of the actual inference costs. The inference costs are presented in units of $/1M tokens. The leaderboard data was taken from the experiments on the A100 GPUs,and for each model, we took the GPTQ-4bit+exllama-v2 quantization benchmark. Table 3 shows the energy costs on the leaderboard for Llama2 and CodeLlama. We note that energy data was missing for CodeLlama-70B, so we extrapolated from Llama2-70B-chat.

| Model size | Llama2 cost ($/1M tokens) | CodeLlama cost ($/1M tokens) |

|---|---|---|

| 7B | $0.182 | $0.183 |

| 13B | $0.24 | $0.24 |

| 70B | $0.64 | $0.64 |

Model verbosity.

Calculation of the per-token inference costs are not complete without an analysis of the response length produced by the various models. Table 4 shows the average verbosity (output length) of the 3 Llama models on the single-turn prompts in the MT-bench evaluation set. Since the values are of the same order of magnitude, we simplify and assume that the choice of model does not influence the verbosity, and therefore we do not include this in our cost calculations.

| Model | Verbosity |

|---|---|

| Llama-2-7B-chat | 1625 |

| Llama-2-13B-chat | 1573 |

| Llama-2-70B-chat | 1695 |

Current market pricing schemes

As alluded to in the paper introduction, current market pricing schemes for LLM generation involve pay-per-token rates for which the user pays regardless of the response quality. For open-sourced models such as Llama2, there exist API services to run model inference, such as AWS and Microsoft Azure.Alternatively, some pricing schemes behave as threshold contracts: an unsatisfied user may request from the API to regenerate a response free of charge, and hence will only pay if the response quality is above some threshold. For this reason threshold contracts can offer a "satisfaction guarantee" while retaining a simple form.

C.2 Multi-outcome contracts: Further Analysis

Non-Monotone Contracts

Table 5 shows the statistics of the various contract objectives in contracts when optimized without a monotonicity constraint, and displays how they match up to each other in cost-aware and cost-robust settings. We can observe that the min-pay contract minimizes expected pay at the expense of high budget and variance.The min-budget contract, on the other hand, is not the worst in any of the objectives. Additionally, the cost-robust setting sacrifices only a marginal increase in objective values: a increase in the Min-pay objective, an increase if optimizing for budget, and increase when optimizing for minimum variance.

| Cost-aware | Cost-robust | |||||

| Min-Pay | 0.86 | 73.4 | 7.63 | 0.92 (+6.9%) | 73.4 | 8.16 |

| Min-Budget | 2.48 | 3.59 | 1.60 | 2.78 | 3.91 (+8.7%) | 1.70 |

| Min-Variance | 3.52 | 6.31 | 1.45 | 3.84 | 6.58 | 1.53 (+6.5%) |

Price of monotonicity

It is of interest to analyze the relative difference in resulting contracts that occurs due to removing the monotonicity constraint. Table 6 shows the discrepancy in contract objectives for cost-robust contracts. We can observe that while the monotone contracts as a whole are simpler, more intuitive, and closely resemble threshold contracts, it is not without cost as they suffer a sizeable increase in contract objectives, most notably an increase of 388% when trying to minimize expected pay.

| Non-Monotone | Monotone | |||||

| Min-Pay | 0.92 | 73.4 | 8.16 | 4.82 | 12.23 | 5.98 |

| Min-Budget | 2.78 | 3.91 | 1.70 | 5.48 | 6.63 | 1.83 |

| Min-Variance | 3.84 | 6.58 | 1.53 | 5.48 | 6.63 | 1.83 |

C.3 Implementation details

Code.

We implement our code in Python. Our code relies on cvxpy [12, 2] and Clarabel [16] for solving linear and quadratic programs.

Code is available at: https://github.com/edensaig/llm-contracts.

Hardware.

All experiments were run on a single Macbook Pro laptop, with 16GB of RAM, and M2 processor, and with no GPU support. Overall computation time is approximately one minute.

Implementation of cost-robustness.

To implement cost-robustness of a contract setting with costs , we assume knowledge of only the range of costs, and calculate the contract using costs . This modeling assumption provides us with the flexibility of solving contracts in settings without full-information while maintaining the approximation guarantee set forth in Theorem 2.

C.3.1 Contract design solvers

To compute optimal contracts, we implemented the following solvers:

-

•

Convex programming solvers: Given outcome distributions and costs , we solve the MIN-PAY LP (eq. 4), the MIN-BUDGET LP (eq. 2), and the MIN-VARIANCE QP (eq. 17) using cvxpy. All optimization programs enforce incentive compatibility (IC) constraints for the target action against all other actions . We note that the Clarabel solver supports both linear and quadratic programs.

-

•

Threshold contract solver: To find threshold contracts for problems with low-dimensional outcome and action spaces (such as with MT-bench), we implement a brute-force solver which performs full enumerations of all possible thresholds, as proposed by [32]. We refer to the Full Enumeration Solver in [32, Appendix C.2.1] for further implementation details.