Generalized FGM dependence: Geometrical representation and convex bounds on sums

Abstract

Building on the one-to-one relationship between generalized FGM copulas and multivariate Bernoulli distributions, we prove that the class of multivariate distributions with generalized FGM copulas is a convex polytope. Therefore, we find sharp bounds in this class for many aggregate risk measures, such as value-at-risk, expected shortfall, and entropic risk measure, by enumerating their values on the extremal points of the convex polytope. This is infeasible in high dimensions. We overcome this limitation by considering the aggregation of identically distributed risks with generalized FGM copula specified by a common parameter . In this case, the analogy with the geometrical structure of the class of Bernoulli distribution allows us to provide sharp analytical bounds for convex risk measures.

Keywords: Multivariate Bernoulli distributions, GFGM copulas, risk measures, convex order.

1 Introduction

Finding bounds for aggregated risks with partial information on their joint distribution is a widely adressed problem in insurance and finance. The available information about dependence is often modeled using a copula. We provide analytical bounds for aggregate risks under the assumption that their dependence is modelled using a generalized Farlie-Gumbel-Morgenstern (GFGM) copula. The aim of our work is beyond the appropriateness of adopting GFGM copulas in any specific application. We study their mathematical, and geometrical properties, that make them a powerful tool to deal with aggregated risks.

With this purpose in mind, we previously find a stochastic representation that generalizes the correspondence proved in [Blier-Wong et al., 2024a] to any random vector with dependence structure defined by a generalized FGM copula. This representation is a one-to-one correspondence between generalized FGM copulas and multivariate Bernoulli vectors. Building on this representation we prove that the class of joint distributions of random vectors with univariate marginals and generalized FGM copula with parameters is a convex polytope, that is a convex hull of a finite set of points, called extremal points. An important consequence is that many functionals , where , are bounded by their evaluations on the extremal points, see [Fontana and Semeraro, 2023]. However, the number of extremal points is huge and there are computational limitations in finding them in high dimensions. To overcome this limitation, we consider the class of GFGM copulas with , which we call GFGM copulas.

We prove that the class of joint distributions with a common univariate margin and GFGM copula share the same geometrical structure of the class of multivariate Bernoulli distributions. This analogy allows us to easily work with sums of random variables with joint distribution in , applying the results of [Fontana et al., 2021].

We also show that the convex order is preserved from the elements of the class of sums of components of random vectors following Bernoulli distributions to the class of our interest . This contribution is important because the bounds for convex risk measures, e.g. expected shortfall, of sums in can be easily found by considering the random vectors that correspond to the exchangeable Bernoulli random vectors that are minimal and maximal under the (stronger) supermodular order, provided by the author of [Frostig, 2001].

We considered two convex measures of risk, the expected shortfall, and the entropic risk measure and also the value-at-risk. We analytically find their bounds in the cases of exponential margins and discrete margins and provide numerical illustrations in these two special cases in high dimensions. Building on the geometrical structure of the joint distributions behind the sums, we exhibit some possible alternative dependence structures corresponding to minimal aggregate risk. Although the theoretical investigation of this case is beyond the scope of this paper, we also discuss some numerical examples of the generalized FGM dependence, without the assumption of identically distributed risk. In this general case, we arrive up to dimension , where we can proceed by enumeration of the extremal points. The paper is structured as follows. Section 2 introduces the preliminary notions about multivariate Bernoulli distributions and GFGM copulas with a common parameter and also their link. A new stochastic representation for GFMG copulas is proved in Section 3.2. We study the geometrical structure and the convex order in the class of uniform vectors with GFGM copulas with a common parameter in Section 4. In the subsequent section, we provide sharp bounds for the convex risk measures and the value-at-risk and we provide numerical illustrations. The last Section 6 presents an example of generalization to different values of for future research purposes and concludes.

2 Preliminaries

In this section, we recall the preliminaries on the set of -dimensional probability mass functions (pmfs) which have Bernoulli univariate marginal distributions and the preliminary notions on the class of generalized Farlie-Gumbel-Morgenstern (GFGM) copulas.

2.1 Notation

We use the following notation throughout the paper:

-

•

bold letters indicate vectors;

-

•

random variables and random vectors are denoted with capital letters ;

-

•

cumulative distribution functions (cdf) are denoted by and by if it is necessary to indicate the corresponding random variable or vector of random variables;

-

•

(joint) pmfs and probability density functions (pdfs) are denoted by small letters and by if it is necessary to indicate the corresponding random variable or vector;

-

•

if is the joint pmf of , we denote the -marginal pmf by , that is the pmf of , with and ;

-

•

classes of (joint) pmfs or (joint) cdfs are denoted with calligraphic letters ;

-

•

classes of copulas are denoted with the calligraphic letter ;

-

•

notations (), (), and () indicate that () has (joint) cdf, (joint) pmf or (joint) pdf in , respectively;

-

•

notation indicates that the joint cdf of the random vector with uniform margins is a copula ;

-

•

the notation indicates equality in distribution.

2.2 Multivariate Bernoulli distributions and convex polytopes

Let us consider the Fréchet class of multivariate Bernoulli distributions with Bernoulli marginal distributions of parameters . We assume throughout the paper that are rational, that is , . Since is dense in , this is not a limitation in applications. We denote with the class of multivariate Bernoulli distributions with identical Bernoulli marginal distributions of parameter , meaning .

If is a random vector with joint pmf in , we denote the column vector which contains the values of and over by , and , respectively; we make the non-restrictive hypothesis that the set of binary vectors is ordered according to the reverse-lexicographical criterion. As an example, we consider and we have . The notations and indicate that has joint pmf .

We assume that vectors are column vectors and we denote by the transpose of a matrix . In [Fontana and Semeraro, 2018], the authors prove that is a convex polytope (see as a standard reference [De Berg et al., 1997]); it means that admits the following representation:

where is a matrix whose rows, up to a non-influential multiplicative constant, are , and where is the vector which contains only the -th element of , , e.g for the bivariate case and . Therefore, there are joint pmfs , , and for any , there exist summing up to one such that

| (2.1) |

We call the vectors , , the extremal points of , and the corresponding joint pmfs of the random vector . Here, is the number of extremal points of which depends on and obviously on .

For low dimension , the extremal points can be found using the software 4ti2 (see [4ti2 team, 2018]). See Example 1 as an illustration when . However, their number increases rapidly with the dimension , as discussed in Section 2 of [Fontana and Semeraro, 2024].

Example 1.

We consider the class , with and . In this case, the extremal points can be found using 4ti2. The extremal points , , of the class are reported in Table 1.

| (0,0,0) | 0 | 0 | 0 | 0 | 0 | 0 | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (1,0,0) | 0 | 0 | 0 | 0 | 0 | 0 | ||||||

| (0,1,0) | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | |||

| (1,1,0) | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | |||

| (0,0,1) | 0 | 0 | 0 | 0 | ||||||||

| (1,0,1) | 0 | 0 | 0 | 0 | ||||||||

| (0,1,1) | 0 | 0 | 0 | 0 | 0 | 0 | ||||||

| (1,1,1) | 0 | 0 | 0 | 0 | 0 | 0 |

We need to introduce the following classes of distributions since they are building blocks of one of our main results:

-

•

class of exchangeable -dimensional Bernoulli distributions with mean , we recall that if and , where is any permutation of , for every ;

-

•

class of univariate discrete distributions with support on and mean .

If is a discrete random variable with pmf in , we denote the column vector containing the values of its cdf and its pmf over by , and , respectively. In other words, , . To simplify the notation, also means that .

According to the notation established in Section 2.1, or indicates that the discrete random variable has pmf . The authors of [Fontana et al., 2021] prove that is a convex polytope: it means that if and only if there exist summing up to 1 such that

where , are the extremal points of and is their number which depends on and obviously on (see Corollary 4.6 in [Fontana et al., 2021] for the computation of ). We denote by a random variable with pmf . The extremal points have at most two non-zero components, say and the extremal pmfs for any have the following analytical expression:

with , . Note that is the largest integer less than and is the smallest integer greater than . If is an integer, the pmf, given by

is also an extremal point.

In [Fontana et al., 2021], the authors show that the following relationship between classes of distributions holds:

| (2.2) |

that is, the class has a one-to-one relationship with the class of exchangeable Bernoulli distributions . From (2.2), it follows that given there is one and only one exchangeable element such that . From (2.2) it follows that is a convex polytope and that the extremal points of are the exchangeable pmfs corresponding to the extremal points of . We denote by extremal points or extremal pmfs of , . We denote with a random vector with pmf . In Table 2 we provide each convex polytope with its generators.

| Polytope | pmf-generator | rv-generator | number of generators |

|---|---|---|---|

2.3 Bernoulli distributions and GFGM copulas

We start this section by recalling the definition of a -variate FGM copula (see, e.g. Section 6.3 in [Durante and Sempi, 2015]).

Definition 2.1.

A -variate FGM copula has the following expression:

for , where and and belongs to the intersection of halfspaces

for all . We denote by the class of FGM copulas.

Let be a vector of uniformly distributed rvs with , where . Lemma 2 of [Blier-Wong et al., 2023] provides the following stochastic representation of in terms of showing the one-to-one correspondence between and :

| (2.3) |

where is a vector of independent and identically distributed (iid) random variables satisfying for and (see also [Blier-Wong et al., 2022b]).

In [Blier-Wong et al., 2024a], a class of generalized FGM copulas is introduced, building on a new stochastic representation. Let be a -variate Bernoulli random vector. Let and be vectors of independent uniform rvs. The random vectors , and are independent of each other. Further, define the representation

| (2.4) |

In [Blier-Wong et al., 2024a], the authors show that the joint cdf of the random vector in (2.4) is the generalized FGM copula provided in the following definition.

Definition 2.2.

A -variate generalized FGM (GFGM) copula with vector of parameters has the following expression

for where, for ,

where .

We denote by the class of generalized FGM (GFGM) copulas. We use the notation or to indicate the subclasses of GFGM copulas with parameters or with a common parameter . In the special case , , where is the class of FGM copulas, and the stochastic representations in (2.4) and (2.3) are equivalent.

Example 1 (continued).

In Table 3, we provide the values of the four parameters , , , and of extremal copulas , , of the class of trivariate GFGM copulas with .

| 0 | 0 | |||||||||||

3 Geometrical structure of GFGM copulas

In [Blier-Wong et al., 2024a], the authors mention in Remark 1 that the class shares the geometrical structure of . In particular, any is a convex combination of , where is built from according to (2.4), . Indeed, by using the stochastic representation in (2.4), there is such that , and we have

where equalities and follow from the independence of , and and of , and , . It follows that any GFGM copula admits the representation

| (3.1) |

where is the copula associated to , . The class of copulas is a convex polytope.

Example 1 (continued).

3.1 Class of distributions

We provide in the proposition that follows a general result for a class of multivariate distributions with dependence structure built with a family of copulas being a convex polytope. Our aim is to later investigate the specific class of distributions with marginal distributions and with copula in the class .

Proposition 3.1.

Let be a class of copulas. Let be a class of multivariate distributions with marginal distributions and with copula in the class . If is a convex polytope with extremal points , then is a convex polytope with extremal points , where

for every and .

Proof.

Consider . Then, for , we have

for some such that . Define and the desired result directly follows. ∎

Corollary 3.1.

The class of distributions is a convex polytope with extremal points the distributions associated to the extremal points of , .

3.2 A new representation theorem and consequences

We introduce a stochastic representation for any random vector with distribution in . We then use this representation in two particular cases, more precisely with exponential and discrete marginals for which the expression of the distribution of the sum is analytical.

Theorem 3.1.

Fix some margins and, for , let be vectors of independent random variables with and , for all , where and and let them be independent. Define the random vector

| (3.2) |

where . Then we have , that is the distribution of the random vector has margins and copula .

Proof.

Let and hence , where , with . In the proof of Theorem 2 in [Blier-Wong et al., 2024a], we have

where

and

Thus and , , and the assert follows. ∎

Obviously, the special case of uniform margins leads to a stochastic representation of the GFGM family of copulas similar to (2.3) and equivalent to (2.4). We notice that for we find the stochastic representation of FGM copulas in [Blier-Wong et al., 2024b].

Theorem 3.1 provides a very useful representation of the random vector . This helps us to derive plenty of results such as examining the distribution of any integrable function of and analyzing pairwise dependence properties of . The following corollary considers the expectation of functionals of for which we derive bounds, in Section 5, building on the geometrical structure of Bernoulli vectors, the distribution of the sum which may represent aggregate risks in a portfolio and some results on correlation between components of to analyze dependence corresponding to minimal aggregate risks.

Corollary 3.2.

Let , and let , , be the extremal pmfs of . The following holds.

-

1.

Let be a real-valued function for which the expectation exists, we have

(3.3) -

2.

The distribution of the sum is given by

(3.4) -

3.

The covariance between each pair of components of , , is:

(3.5) and if has continuous marginal distributions, Spearman’s rho between each pair of components of , , is:

where is the Bernoulli random vector corresponding to of Theorem 3.1. The sharp bounds of the Spearman’s rho are:

Proof.

From the stochastic representation in (3.2) of Theorem 3.1, we have

Thus, and by conditioning on , the expectation of a function of is given by

| (3.6) |

assuming that the expectations exist.

- 1.

-

2.

By choosing , where , if is true, and , otherwise, (3.4) follows.

-

3.

Spearman’s rho for any pair of continuous rvs , , is given by

(3.7) where indicates the Pearson’s correlation and . Using the representation in (2.4), the expression for , , is

where

and

(3.8) Finally, replacing (3.8) in (3.7), the expression of the Spearman’s rho is given by

for .

Assume . In Section 3.2 of [Fontana and Semeraro, 2018], the authors found the bounds for the covariance between for any pair of Bernoulli variables. The maximum value is , while the minimum value is . In the first case, and . In the second case, and . Therefore, we have the following bounds for Spearman’s rho of any pair of continuous rvs

for .

∎

Equation (3.3) in particular holds for and implies that the bounds of , for any for which the expectation exists, can be found by enumerating their values on the sums , and this is computationally feasible in low dimension.

3.3 Discrete and exponential margins

We end this section considering two examples for , where the margins are discrete in the first one and the margins are exponential in the second one.

Example 2 (Discrete margins).

Let be defined here as a -dimensional random vector, where, for every , is a discrete random variable taking values on the set , , and with cdf . When the joint distribution of belongs to the class , admits the representation in (3.2). Moreover, for all , to derive the values of the pmf of the discrete rvs , we observe that, for each , we have

and

where

and . For all , it follows that the expectations of the discrete rvs , are

and

Finally, we consider the sum , which can be rewritten using the representation in (3.2), as

| (3.9) |

From (3.9), the expression of the probability generating function (pgf) of is given by

| (3.10) |

where the pgf of is

for and . One uses the Fast Fourier Transform (FFT) algorithm of [Cooley and Tukey, 1965] to extract the values of the pmf of from its pgf in . Details about that efficient approach is explained in Chapter 30 of [Cormen et al., 2009]. See also [Embrechts et al., 1993] for FFT applications in actuarial science and quantitative risk management. This procedure is illustrated in Example 7, within Section 6. ∎

Example 3 (Exponential margins).

Assume that , where is the cdf of an exponential distribution with mean , . In [Blier-Wong et al., 2024a], they present an alternative stochastic representation of equivalent to (3.2) that allows finding an analytical expression for the distribution of the sum of the components of the random vector . This other stochastic representation is

| (3.11) |

where the components within and within are independent, with following an exponential distribution with mean and also following an exponential distribution but with mean , for . Also, the random vectors , and are independent.

Considering now the sum of the components of , the representation in (3.11) allows us to express it as follows:

| (3.13) |

To identify the distribution of , we find from (3.13), the expression of the Laplace-Stieltjes transform (LST) of , denoted by and given by

| (3.14) |

Using techniques explained in [Willmot and Woo, 2007] and [Cossette et al., 2013], the LST of admits the representation given by

where , for , and . From the expression of its LST in (3.14), it follows that the rv follows a mixed Erlang distribution. An application of (3.14) is also provided in Example 6. Details about the computation of the sequence of probabilities are explained in [Willmot and Woo, 2007] and [Cossette et al., 2013]. ∎

In Example 3, we find the distribution of , which comes with an analytical expression for because we assume that the margins are exponential. In most cases, if the margins do not belong to a class of distributions closed under convolution, one must resort to numerical approximations. One of them is to use discretization techniques as explained in Section 4.3 of [Blier-Wong et al., 2023] jointly with the method explained in Example 2.

4 Geometrical structure of GFGM() copulas

Based on the results recalled and highlighted in Section 2, we provide in this section the geometrical structure embedded within the class of sums of components of random vectors whose joint distribution belongs to the class of -variate GFGM copulas with a common parameter , that is the class .

Let us begin with the following proposition, which is a direct consequence of the one-to-one relationship given in (2.2).

Proposition 4.1.

Let and let . Then, there exists one exchangeable Bernoulli random vector such that has the same distribution as .

Proof.

Given , the sum of the components is a random variable that takes values in the set and whose mean is , that is . Therefore, from (2.2), it follows that there exists one exchangeable Bernoulli random vector such that . ∎

Lemma 4.1.

Let and let and . Let and be the GFGM(p) copulas corresponding to and , respectively. Finally, let and be uniform random vectors with joint cdfs and , respectively. If , then .

Proof.

From (2.4), we have the following stochastic representation:

where , and are vectors of independent standard uniform random variables and , and , are independent of each other. Similarly, define , , and . Let and be the cdfs of and . Then, we have

| (4.1) |

Since and are independent by construction, if , the distribution of the sum does not depend on the position of the 1’s in , but only on the number of 1’s, that is, on the sum of the components . Hence, the cdf in (4.1) becomes

| (4.2) |

where we set and . Letting and in (4.2) it follows that

| (4.3) |

Therefore, given that the first probability in the summation of (4.3) does not depend on for , we conclude that implies , for every . ∎

Let denote the class of sums of components of random vectors with multivariate distributions in . Let us indicate with , where is the random vector whose joint cdf is the copula associated to , as defined in (2.4).

We can now prove the following theorem that characterizes .

Theorem 4.1.

The class is a convex polytope and its extremal points are the cdfs of where

and is an extremal point of , for .

Proof.

Consider any , then there exists an such that . Let . There exists a unique with . Thus by Lemma 4.1, , where is the exchangeable uniform random vector with copula generated by . In other words, admits the representation

where . Let be the cdf of . Then, we have

where is the cdf of . ∎

We now study the convex order of sums of the components of random vectors with joint distribution described by a GFGM copula. We first recall the definition of the convex order.

Definition 4.1.

Given two random variables and with finite means, is said to be smaller than in the convex order (denoted ) if for all real-valued convex functions for which the expectations exist.

In the proof of the following Theorem 4.2, we need to recourse to the supermodular order that we recall below (see Definition 3.8.5 in [Müller and Stoyan, 2002]). A function is said to be supermodular if , where the operators and denote coordinatewise minimum and maximum respectively.

Definition 4.2.

We say that is smaller than under the supermodular order, denoted , if for all supermodular functions , given that the expectations exist.

Theorem 4.2.

Let be such that . Let and be the GFGM copulas associated to and and let and be uniform random vectors with joint cdf and , respectively. Then,

Proof.

By Proposition 4.1, there exist two exchangeable Bernoulli random vectors and of the class such that and . Therefore, by Lemma 4.1, we have

| (4.4) |

where and are uniform random vectors with joint distributions given by the GFGM copulas associated to and , respectively. Moreover, since by hypothesis, then . However, as a consequence of results in Section 3 of [Frostig, 2001], the following double implication holds:

Furthermore, by Theorem 4.2 in [Blier-Wong et al., 2022b], implies . Since, given a convex function , the function is supermodular, implies, in particular, . Finally, by the equality in distribution in (4.4), we have . ∎

Theorem 4.2 obviously holds for FGM copulas by setting . In this case, the proof of the Theorem can be repeated similarly using the stochastic representation in (2.3).

4.1 Class of distributions

Let us introduce the class of joint cdfs with a copula in the class and with the same marginal cdfs . Consider . From Theorem 3.1, there exists such that is built from the Bernoulli random vector , according to the stochastic representation (3.2). Using this representation, we can generalize Lemma 4.1 as follows.

Lemma 4.2.

Let be such that and are equal in distribution. Let be the random vectors corresponding to and , respectively. Then, and have the same distribution.

Proof.

Again, the stochastic representation in (3.2) helps us to find the following generalization of Theorem 4.1.

Theorem 4.3.

The class of distributions of sums of components of vectors with distribution in is a convex polytope and its extremal points are the distributions of where

| (4.5) |

where is an extremal point of , for .

Proof.

The proof is similar to the one of Theorem 4.1. ∎

Theorem 4.3 completes the relationship in (4) as follows:

From this relationship, it follows that the number of extremal points in is , that is significantly lower that the number of extremal points in and they are analytical. Therefore we can find them also in high dimension.

Finally, we have the following generalization of Theorem 4.2.

Theorem 4.4.

Let and let and , for any cdf , be respectively built from and , as in (3.2). Then,

Proof.

The proof of this Theorem follows the same idea as the one of Theorem 4.2. ∎

We conclude this section by considering the two examples with exponential and discrete margins previoulsy discussed in Section 3.3 but here in the special case of identically distributed risks.

Example 2 (Continued).

For the case of identically distributed discrete margins, we obtain the following expression for the pmf of :

| (4.6) |

where * denotes the convolution product. It follows from (3.10) that the probability generating function (pgf) of is given by

| (4.7) |

where and are the pgf of and , respectively.

Example 3 (Continued).

Firstly, assume , that is for every , with GFGM() copula. The LST of in (3.14) becomes

where . By identification of the LST transform, we conclude

where corresponds to the cdf of an distribution and corresponds to the cdf of an distribution for .

5 Sharp bounds for risk measures

The results presented in the previous sections allow us to derive sharp bounds for risk measures in the class , by enumerating their values on the extremal points. This is computationally expensive because the number of extremal points explodes and becomes larger, as highlighted by the authors of [Fontana and Semeraro, 2024]. This section proves that we can solve this problem by finding analytical sharp bounds for risk measures in the classes and , for any .

As a motivation, we start with an example showing that the assumption of common margins in Theorem 4.4 is necessary.

Example 4.

Consider the class , where , , and are the discrete cdfs provided in Table 4.

| 0 | 0.1 | 0.1 | 0.8 |

|---|---|---|---|

| 1 | 0.2 | 0.4 | 1.0 |

| 2 | 0.3 | 0.7 | 1.0 |

| 3 | 1.0 | 1.0 | 1.0 |

Let and with copulas respectively defined by the Bernoulli pmfs and given in Table 5.

| (0,0,0) | (1,0,0) | (0,1,0) | (1,1,0) | (0,0,1) | (1,0,1) | (0,1,1) | (1,1,1) | |

| 0 | 0 | 0 | 0 | |||||

| 0 | 0 | 0 | 0 | 0 |

Table 6 exhibits the values of pmfs of the discrete random variables and ; those values are computed using the pgf and the FFT algorithm as explained in the previous section. As one can see looking at the support of in Table 5, if has pmf , the variable has pmf minimal in convex order in the class , but , since .

| 0 | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | |

|---|---|---|---|---|---|---|---|---|---|---|

| 0.0080 | 0.0338 | 0.0640 | 0.1328 | 0.2467 | 0.2592 | 0.2312 | 0.0242 | 0 | 0 | |

| 0.0032 | 0.0249 | 0.0602 | 0.1556 | 0.2636 | 0.2569 | 0.2004 | 0.0352 | 0 | 0 |

We consider two convex risk measures, the widely used expected shortfall (ES), and the entropic risk measure. Then we consider, consistently with Regulation, the value-at-risk (VaR), which is not a convex measure. Below we recall the definition of these three measures of risk.

Definition 5.1.

Let Y be a random variable representing a loss with finite mean. Then, the value-at-risk at level is given by

Definition 5.2.

Let Y be a random variable representing a loss with finite mean. The expected shortfall at level is defined as

| (5.1) |

The expected shortfall defined in (5.1) also admits the following representation

Definition 5.3.

The entropic risk measure is defined by

assuming that there exists a real number such that is finite for .

5.1 Convex risk measures

This section discusses bounds for convex risk measures in the class . Following Definition 3.4 of [Puccetti and Wang, 2015], we say that is a -smallest element in a class of distributions if, for all ,

A -smallest element in a Fréchet class does not always exist, see Example 3.1 of [Bernard et al., 2014]. However, the authors of [Hu and Wu, 1999] found the distribution of the exchangeable Bernoulli random vector that is the -smallest element in the class of exchangeable Bernoulli pmfs . Since there is a one-to-one correspondence between and , see (2.2), and the sums of the components of a random vector with pmf in are rvs with distribution in , a -smallest element always exists in the class . Actually, for each , we can also build non-exchangeable -smallest elements of following Theorem 5.2 of [Fontana and Semeraro, 2024]. In the proof of Lemma 3.1 of [Bernard et al., 2017], the authors provide a way to construct a random variable with -smallest pmf.

Let and let be the corresponding uniform random vector with GFGM copula. The following corollary is a straightforward but important consequence of Theorem 4.2 and Theorem 4.4.

Corollary 5.1.

Let be a -smallest element.

-

1.

Let be a uniform random vector whose joint cdf is the GFGM copula corresponding to . Then, is a -smallest element in .

-

2.

Let with joint cdf defined with the GFGM copula corresponding to . Then, is a -smallest element in .

Consequently, distributions, for which the lower bounds of a convex functional are reached, are built using a -smallest element of . Obviously, using the upper Fréchet bound of , we build the distributions of vectors with maximal convex sums. Using the results in Section 4.1, we can analytically find the lower bounds of the risk measures considered for exponential margins and discrete margins, respectively.

5.2 Value-at-risk

In [Fontana et al., 2021], the authors prove that, in a class of univariate distributions which is a polytope, the bounds of the in the class are reached at the extremal points.

We consider here the of random variables in two convex polytopes of distributions: and . Therefore, bounds of the are reached on the extremal points of and of , that are built from extremal points of .

We focus first on the vectors of Bernoulli rvs in the class , whose sums have pmf in . We can define two functions , where and represent the lower and the upper sharp bounds of in the class , as functions of the level in . From Proposition 5.4 in [Fontana et al., 2021] (see also Equation (14) in [Bernard et al., 2017]), we have

and

where we indicate with the highest integer smaller than and with the smallest integer higher than or equal to . Contrary to the bounds of convex functions, the authors of [Fontana and Semeraro, 2024] show that the extremal points with maximum and minimum depend on and on the level .

We now consider the random vector whose sum of its components has distribution in . Let and . Algorithm 1 allows one to find the minimum and maximum in this class.

Remark 1.

In some cases, the minimum is reached on the minimal -element of the polytope. In fact, from the proof of Theorem 3.A.4 in [Shaked and Shanthikumar, 2007], it follows that, if , then there exists such that, , for every . Therefore, if is a -smallest element of its Fréchet class, then there exists such that, , for every , for every random vector of the same Fréchet class of .

Example 5.

Consider the case , . Then, and , . The class has extremal points provided in Table 7. Let us compute value-at-risk, expected shortfall, and entropic risk measures of the extremal pmfs for and . Results are reported in Table 8. The choice of has been made to exhibit the case where the minimum is not the -smallest element of the class. Table 9 reports instead the same risk measures evaluated on the corresponding FGM copulas. Notice that the bounds for the sums are at the extremal copulas corresponding to the upper Fréchet bound and to the -smallest Bernoulli pmfs for the convex measures, as proved in Section 5.1. The minimum in is reached at while for the Bernoulli case it is at . This proves that the minimum of the sum of the components of U in is not inherited from the underlying Bernoulli pmf.

| 0 | 0 | 0 | 0 | 0 | 0 | 0 | |||

|---|---|---|---|---|---|---|---|---|---|

| 1 | 0 | 0 | 0 | 0 | 0 | 0 | |||

| 2 | 0 | 0 | 0 | 0 | 0 | 0 | |||

| 3 | 0 | 0 | 0 | 0 | 0 | 0 | |||

| 4 | 0 | 0 | 0 | 0 | 0 | 0 | |||

| 5 | 0 | 0 | 0 | 0 | 0 | 0 |

| 3 | 4 | 5 | 3 | 4 | 5 | 3 | 4 | ||

| 4 | 5 | 4 | 5 | 4 | 4.5 | ||||

| 2.5584 | 2.6803 | 2.8093 | 2.5362 | 2.6121 | 2.6927 | 2.5387 | 2.5667 |

| 3.0308 | 3.3281 | 3.4928 | 3.0158 | 3.1710 | 3.2636 | 3.0180 | 3.0476 | ||

| 3.4627 | 3.7345 | 3.8401 | 3.3641 | 3.5161 | 3.5846 | 3.3228 | 3.3477 | ||

| 2.5210 | 2.5350 | 2.5486 | 2.5181 | 2.5264 | 2.5345 | 2.5180 | 2.5207 |

The following Example 6 is the main example of application of our results. We consider a high dimensional portfolio of risks for six scenarios: three different GFGM() dependence structures for two Fréchet classes, with exponential and discrete margins discussed in a theoretical setting in Examples 2 and 3.

Example 6.

Consider the classes and , where is the discrete cdf whose pmf is given by

We consider three different cases of GFGM(p) dependencies for each class, that is we consider and , where each case is associated to a common .

The bounds for the convex measures are reached at the distributions of the two classes and corresponding to the minimal and maximal convex sums in , for and . The minimal convex sum is the pmf in with support on the pair when , with support on the point when , and support on the pair when . Table 10 provides the sharp bounds for the convex risk measures with exponential and discrete margins, respectively.

| 1191.2742 | 1189.2721 | 1192.3324 | 2152.595 | 2122.718 | 2019.207 | |

| 1858.1846 | 1702.8444 | 1540.6192 | 2858.955 | 3448.241 | 4440.057 | |

| 1003.9212 | 1003.8215 | 1003.9237 | 1555.710 | 1551.957 | 1546.627 | |

| 1124.6343 | 1125.0510 | 1101.5259 | 1888.303 | 2216.540 | 2843.312 | |

The is bounded by its evaluations on the extremal pmfs of the classes and . When , the number of extremal points is lower than or equal to 2501, see Corollary 4.6 of [Fontana et al., 2021], and we find bounds by enumeration. Table 11 provides the bounds for the in the abovementioned classes and also the analytical bounds for the whole Fréchet classes given in Equation (4) of [Bernard et al., 2017]. We mention that the minimum in the class is not reached at the distribution corresponding to the minimal convex pmf in , whose is 1961.

| Lower bound | 842.3299 | 842.3299 | 842.3299 | 1045.963 | 1045.963 | 1045.963 |

|---|---|---|---|---|---|---|

| Min | 1149.7294 | 1147.0118 | 1150.2229 | 2016 | 1994 | 1960 |

| Max | 1791.3283 | 1645.0538 | 1488.2312 | 2688 | 3258 | 4225 |

| Upper bound | 3995.7323 | 3995.7323 | 3995.7323 | 9606.61 | 9606.61 | 9606.61 |

We conclude this example by considering Pearson’s correlation of the exchangeable -smallest element in and Pearson’s correlation matrix of a vector corresponding to the Bernoulli -smallest element provided in Theorem 5.2 by the authors of [Fontana and Semeraro, 2024]. Using (3.12), Pearson’s correlation (denoted by ) is equal to , for .

We therefore have to find the covariance of the exchangeable -smallest element and the covariance matrix of the -smallest element in , obtained following Theorem 5.2 of [Fontana and Semeraro, 2024], and given by

The equicorrelation of the exchangeable -smallest element in is , that is the minimal correlation in the subclass of exchangeable distributions in . Let . The entries of Pearson’s correlation matrix of are given by

The mean of Pearson’s correlations of the random vector is given by

| (5.2) |

From (5.2) we notice that , the equicorrelation of the exchangeable vector . This result is a consequence of Corollary 5.2 in [Fontana and Semeraro, 2024] and of the fact that the Pearson’s correlations in the class with the exponential margins is equal to the covariance of the corresponding Bernoulli pair.

6 Remarks and conclusion

We conclude with one example in low dimension of the general class , with , and we leave its theoretical investigation to further research. We find the risk measures’ sharp bounds for the sum , where have discrete distributions and has a GFGM copula with vector parameter . In fact, for low dimensions () we are able to find the extremal points of , to construct the corresponding copulas, and to find the generators of the convex polytope . We evaluate the risk measures on the extremal point and we find sharp bounds by enumeration. Furthermore, we find the expected allocation and the expected contribution of for each risk with extremal pmf, following [Blier-Wong et al., 2022a].

Example 7.

We consider the class of Example 1 with and . The extremal points , , of the class are reported in Table 1. Note that there are three extremal pmfs whose sum is minimal under the convex order: , , and . These three vectors have two couples of Bernoulli rvs with minimal covariance and the remaining pair — for , for , and for — has maximal covariance.

We now consider the class , where , , is the cdf whose pmf is defined by

and we choose , and . Also, we have , , and .

The lower and upper bounds for the risk measure are reached at the random vectors corresponding to the extremal points and , respectively. In Table 12, we provide Pearson’s correlation coefficients , , and for all of the twelve extremal dependence structures. Notice that the correlation matrix of also has negative entries, i.e and are negatively correlated, while has the same correlation as . This last equality follows observing that the correlation between and the correlation between are equal, in fact

and

coincide since .

| 0.0605 | -0.0605 | 0.0605 | -0.0605 | 0.0000 | 0.0302 | |

| -0.1610 | 0.1610 | -0.1610 | -0.1610 | -0.1610 | -0.0805 | |

| -0.1229 | -0.1229 | -0.0307 | 0.0615 | 0.0615 | 0.0154 | |

| -0.0605 | -0.0605 | 0.0605 | 0.0000 | 0.0605 | -0.0302 | |

| 0.1610 | 0.0000 | 0.0000 | 0.1610 | 0.1610 | 0.0805 | |

| -0.0307 | 0.0615 | 0.0615 | 0.0615 | 0.0615 | 0.0154 |

| 1532.00 | 1360.00 | 1342.00 | 1403.00 | 1479.00 | ||

| 1733.70 | 1665.46 | 1641.07 | 1683.14 | 1724.32 | ||

| 587.74 | 566.80 | 563.46 | 570.51 | 580.07 | ||

| 521.70 | 488.85 | 485.22 | 494.70 | 508.47 | ||

| 1561.00 | 1493.00 | 1567.00 | 1618.00 | 1643.00 | 1535.00 | |

| 1802.17 | 1771.05 | 1824.07 | 1888.55 | 1906.84 | 1818.89 | |

| 602.12 | 590.22 | 603.90 | 622.97 | 629.61 | 601.55 | |

| 535.91 | 518.49 | 536.10 | 558.13 | 566.39 | 531.66 |

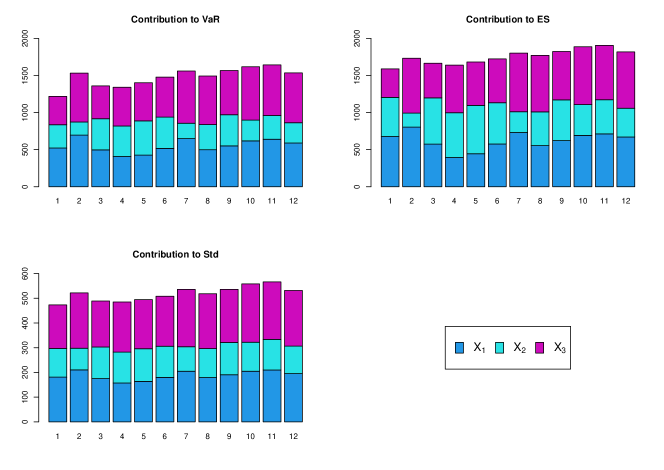

We conclude this example by finding the contribution of risk , , to the standard deviation of the sum , to the and to the , for all the extremal dependence structures. We recall the definitions of expected allocation and of expected contribution of the risk to a total outcome , for . The expected allocation of each risk in Definition 1.1 of [Blier-Wong et al., 2022a] is given by

where is the indicator function, such that , if is true, and , otherwise. The expected contribution of each risk , , is provided in Equation (6) of [Blier-Wong et al., 2022a], and is defined by

assuming that . The expected contribution of to the is given by . We now recall the expression for the contribution to the based on the Euler-based allocation rule provided in [Tasche, 1999]:

where

and

Finally, the contribution of to the standard deviation of based on Euler’s rule is given by

| (6.1) |

Figure 1 reports the contributions to the , the and the standard deviation of .

The geometrical structure of GFGM copulas inherited from the geometrical structure of multivariate Bernoulli distributions has proven to be a powerful tool for studying the properties of random vectors with GFGM dependence.

The last Example 7 finds the bounds by enumeration of their values in the extremal points, which becomes computationally challenging in high dimensions. Under the assumption of identically distributed risks with GFGM dependence structure, we show the effectiveness of our theoretical results in studying the risk of high dimensional — — portfolios. The extension of these theoretical results to the whole GFGM copulas relies on extending corresponding results in the class of multivariate Bernoulli distributions, and this is part of our ongoing research. Another, more applicative, part is to use this novel geometrical representation to investigate the dependence structure of the class and of their extremal points, which are good candidates for representing extremal dependence also in high dimension.

7 Acknowledgements

This work was partially supported by the Natural Sciences and Engineering Research Council of Canada (Cossette: 04273; Marceau: 05605). This work was also partially supported by the Italian Ministry of Education, University and Research (MIUR), PRIN 2022-PNRR project P2022XT8C8. H. Cossette and E. Marceau would like to thank Dipartimento di Scienze Matematiche ”G. L. Lagrange” (DISMA), Politecnico di Torino, for their wonderful stay during which most of the paper was written.

References

- [4ti2 team, 2018] 4ti2 team (2018). 4ti2—a software package for algebraic, geometric and combinatorial problems on linear spaces. Available at https://4ti2.github.io.

- [Bernard et al., 2014] Bernard, C., Jiang, X., and Wang, R. (2014). Risk aggregation with dependence uncertainty. Insurance: Mathematics and Economics, 54:93–108.

- [Bernard et al., 2017] Bernard, C., Rüschendorf, L., Vanduffel, S., and Yao, J. (2017). How robust is the value-at-risk of credit risk portfolios? The European Journal of Finance, 23(6):507–534.

- [Blier-Wong et al., 2024a] Blier-Wong, C., Cossette, H., Legros, S., and Marceau, E. (2024a). A new method to construct high-dimensional copulas with Bernoulli and Coxian-2 distributions. Journal of Multivariate Analysis, 201:105261.

- [Blier-Wong et al., 2022a] Blier-Wong, C., Cossette, H., and Marceau, E. (2022a). Generating function method for the efficient computation of expected allocations. arXiv preprint arXiv:2207.02654.

- [Blier-Wong et al., 2022b] Blier-Wong, C., Cossette, H., and Marceau, E. (2022b). Stochastic representation of FGM copulas using multivariate Bernoulli random variables. Computational Statistics & Data Analysis, 173:107506.

- [Blier-Wong et al., 2023] Blier-Wong, C., Cossette, H., and Marceau, E. (2023). Risk aggregation with FGM copulas. Insurance: Mathematics and Economics, 111:102–120.

- [Blier-Wong et al., 2024b] Blier-Wong, C., Cossette, H., and Marceau, E. (2024b). Exchangeable FGM copulas. Advances in Applied Probability, 56(1):205–234.

- [Cooley and Tukey, 1965] Cooley, J. W. and Tukey, J. W. (1965). An algorithm for the machine calculation of complex Fourier series. Mathematics of Computation, 19(90):297–301.

- [Cormen et al., 2009] Cormen, T. H., Leiserson, C. E., Rivest, R. L., and Stein, C. (2009). Introduction to Algorithms. MIT Press.

- [Cossette et al., 2013] Cossette, H., Côté, M.-P., Marceau, E., and Moutanabbir, K. (2013). Multivariate distribution defined with Farlie–Gumbel–Morgenstern copula and mixed Erlang marginals: Aggregation and capital allocation. Insurance: Mathematics and Economics, 52(3):560–572.

- [De Berg et al., 1997] De Berg, M., Van Kreveld, M., Overmars, M., and Schwarzkopf, O. (1997). Computational geometry. Springer.

- [Durante and Sempi, 2015] Durante, F. and Sempi, C. (2015). Principles of copula theory. CRC press.

- [Embrechts et al., 1993] Embrechts, P., Grübel, R., and Pitts, S. M. (1993). Some applications of the fast Fourier transform algorithm in insurance mathematics This paper is dedicated to Professor W. S. Jewell on the occasion of his 60th birthday. Statistica Neerlandica, 47(1):59–75.

- [Fontana et al., 2021] Fontana, R., Luciano, E., and Semeraro, P. (2021). Model risk in credit risk. Mathematical Finance, 31(1):176–202.

- [Fontana and Semeraro, 2018] Fontana, R. and Semeraro, P. (2018). Representation of multivariate Bernoulli distributions with a given set of specified moments. Journal of Multivariate Analysis, 168:290–303.

- [Fontana and Semeraro, 2023] Fontana, R. and Semeraro, P. (2023). Exchangeable Bernoulli distributions: High dimensional simulation, estimation, and testing. Journal of Statistical Planning and Inference, 225:52–70.

- [Fontana and Semeraro, 2024] Fontana, R. and Semeraro, P. (2024). High dimensional Bernoulli distributions: Algebraic representation and applications. Bernoulli, 30(1):825–850.

- [Frostig, 2001] Frostig, E. (2001). Comparison of portfolios which depend on multivariate Bernoulli random variables with fixed marginals. Insurance: Mathematics and Economics, 29(3):319–331.

- [Hu and Wu, 1999] Hu, T. and Wu, Z. (1999). On dependence of risks and stop-loss premiums. Insurance: Mathematics and Economics, 24(3):323–332.

- [Müller and Stoyan, 2002] Müller, A. and Stoyan, D. (2002). Comparison Methods for Stochastic Models and Risks. John Wiley.

- [Puccetti and Wang, 2015] Puccetti, G. and Wang, R. (2015). Extremal dependence concepts. Statistical Science, 30(4):485–517.

- [Shaked and Shanthikumar, 2007] Shaked, M. and Shanthikumar, J. G. (2007). Stochastic orders. Springer.

- [Tasche, 1999] Tasche, D. (1999). Risk contributions and performance measurement. Report of the Lehrstuhl für mathematische Statistik, TU München.

- [Willmot and Woo, 2007] Willmot, G. E. and Woo, J.-K. (2007). On the class of Erlang mixtures with risk theoretic applications. North American Actuarial Journal, 11(2):99–115.