Shape-Constrained Distributional Optimization via Importance-Weighted Sample Average Approximation

Abstract

Shape-constrained optimization arises in a wide range of problems including distributionally robust optimization (DRO) that has surging popularity in recent years. In the DRO literature, these problems are usually solved via reduction into moment-constrained problems using the Choquet representation. While powerful, such an approach could face tractability challenges arising from the geometries and the compatibility between the shape and the objective function and moment constraints. In this paper, we propose an alternative methodology to solve shape-constrained optimization problems by integrating sample average approximation with importance sampling, the latter used to convert the distributional optimization into an optimization problem over the likelihood ratio with respect to a sampling distribution. We demonstrate how our approach, which relies on finite-dimensional linear programs, can handle a range of shape-constrained problems beyond the reach of previous Choquet-based reformulations, and entails vanishing and quantifiable optimality gaps. Moreover, our theoretical analyses based on strong duality and empirical processes reveal the critical role of shape constraints in guaranteeing desirable consistency and convergence rates.

Keywords— shape constraint, distributionally robust optimization, sample average approximation, strong duality, empirical process

1 Introduction

This paper studies optimization problems in the form

| subject to | (1) | |||

where the decision variable is a probability density that controls the expectation on the random variable . The functions are known functions from to that give rise to the objective and moment constraints. In particular, one of these in the moment constraints is chosen to be the indicator function to assert a total mass. Importantly, and as our main focus, the function class contains shape information on , such as monotonicity, convexity and various forms of unimodality. Note that one could generalize formulation (1) to allow probability distributions without densities, but at the expense of more technicality that we avoid digressing to in this paper.

Our primary motivation for studying (1) is that it gives rise to sharp worst-case bounds on expectation-type performance measures when only partial information on is known. This problem arises generically in distributionally robust optimization (DRO) (Delage and Ye (2010); Goh and Sim (2010); Kuhn et al. (2019)), a methodology to tackle optimization under uncertainty that can be viewed as a generalization of classical robust optimization (Ben-Tal et al. (2009); Bertsimas et al. (2011)) when the uncertain parameter refers to the underlying probability distribution in a stochastic problem. Like classical robust optimization, DRO advocates decision-making that optimizes the worst-case scenario, and thus leads to a minimax problem where the outer minimization is over the decision and the inner maximization is over the uncertain probability distribution. In this regard, formulation (1) is precisely the inner maximization of a DRO, or can simply represent a worst-case estimation without reference to a decision. Here, the feasible region, known as the ambiguity set or uncertainty set, captures partial information on the uncertain distribution via moment and distributional shape constraints.

1.1 Background and Existing Challenges

Let us elaborate further and explain the challenges on the aforementioned problem that motivates this paper. First of all, the uncertainty sets in the DRO literature can be generally categorized into two major types. The first type is a neighborhood ball surrounding a baseline distribution, where the ball size is measured via a statistical distance. Common choices of distance include the class of -divergence (Ben-Tal et al. (2013); Bertsimas et al. (2018); Bayraksan and Love (2015); Iyengar (2005); Hu and Hong (2013)) which also covers particular cases like the Renyi divergence (Atar et al. (2015); Dey and Juneja (2012)) and total variation distance (Jiang and Guan (2018)), and the Wasserstein metric (Esfahani and Kuhn (2018); Blanchet and Murthy (2019); Gao and Kleywegt (2023); Xie (2021); Chen and Paschalidis (2018)). This type of DRO originates from stochastic control (Petersen et al. (2000)), and since then has found applications in various disciplines in economics (Hansen and Sargent (2008)), finance (Glasserman and Xu (2014)), queueing (Jain et al. (2010)) and simulation output analysis (Lam (2018)). More recently, it has been shown to have close connections with regularization and solution generalization behaviors (Lam and Zhou (2017); Duchi et al. (2021); Gotoh et al. (2018); Lam (2016, 2019); Gupta (2019); Blanchet and Kang (2021); Blanchet et al. (2022); Gao (2022); Shafieezadeh-Abadeh et al. (2019)), and as such gains surging popularity in machine learning and statistics.

The second major type of uncertainty sets, which is the focus of this paper, represents partial information on the distribution through moments and support (Delage and Ye (2010); Bertsimas and Popescu (2005); Wiesemann et al. (2014); Goh and Sim (2010); Ghaoui et al. (2003); Hanasusanto et al. (2015); Zhang et al. (2018); Xie and Ahmed (2018)), marginal constraints (Doan et al. (2015); Dhara et al. (2021)), and shape constraints (Van Parys et al. (2016); Li et al. (2019); Lam and Mottet (2017); Chen et al. (2021)). These uncertainty sets are especially useful in limited data situations or when data are partially unobservable due to limitations in the data collection process. Moment constraints are intuitive and easy to calibrate from either expert knowledge or data. On the other hand, shape constraints acts as an important complement to moments, one reason being that moment constraints alone can lead to unrealistic worst-case distributions, namely with sparsely discrete support and thus becoming overly conservative. Another reason is that shape constraints need no calibration and hence can be used with little or no data. Thanks to these advantages, shape constraints have been demonstrably useful in, for instance, extremal estimation where the objective function denotes a tail probability or related risk quantity (Van Parys et al. (2016); Lam and Mottet (2017)). In this situation, by the very definition of a tail, data are scarce and shape constraints offer plausible extrapolations that balance conservativeness and obtainable statistical information. It is worth noting that both moments and shape are important: Using moments alone can lead to unrealistically pessimistic distributions concentrated on a small handful of points (Popescu (2005)), while using shape alone can lead to the density being too “free” and does not conform to the natural boundary of the considered problem (Lam and Mottet (2017)). In our main problem (1), we thus consider the shape and the moment constraints both as integral parts of the formulation.

To this end, various types of shape constraints have been considered in the literature, including monotonicity, unimodality and convexity (Popescu (2005)) in the one-dimensional case, and -unimodality (with star-unimodality as a special case; Dharmadhikari and Joag-Dev (1988); Van Parys et al. (2016); Li et al. (2019)), block unimodality (Dharmadhikari and Joag-Dev (1988)) and orthounimodality (Lam et al. (2021)) in the multidimensional case. In terms of methodologies to solve these shape-constrained problems, a major technique is to use the Choquet representation theorem. This theorem asserts that probability measures with a shape constraint can be represented as a mixture of more “elementary” distributions. More concretely, given a cumulative distribution function in a convex shape-constrained class of distributions, the Choquet representation establishes that:

| (2) |

where are the more “elementary” distributions (indexed by ) in this class and is the mixing distribution. In this representation, are fixed (as the extreme points of this convex class) and the mixing distribution varies as varies. Such a representation helps to reformulate the objective function and moment constraints in (1) as mixtures of moments over these elementary distributions, i.e.,

which turns the decision variable into the mixing distribution. When the inner expectation can be easily computed, the resulting optimization with respect to the mixing distribution (i.e., the distribution of ) could be reducible to a solvable optimization problem (e.g., semidefinite program) and hence the exact optimal value can be obtained.

While powerful, there are two main challenges of the Choquet representation that can hammer ultimate solvability. First is that the index in (2) can still be infinite-dimensional depending on the shape constraint (e.g., orthounimodality; Lam et al. (2021)), and thus the optimization problem with respect to the mixing distribution is still infinite-dimensional. In this case, unless a further finite-dimensional reduction can be found, the problem can remain intractable. Another more important challenge is that the moments in the objective function and constraints must be in certain restrictive forms so that the inner expectation can be easily computed. Consequently, in Popescu (2005) which focuses on one-dimensional shapes including convexity and unimodality, the functions in the objective and moment constraints must be piecewise polynomial. In Lam et al. (2021) that considers orthounimodality, the constraints must be expressed as probabilities but not general moments, and the objective function must be the probability of a set that is expressed as an epigraph of a function. Additionally, both Van Parys et al. (2016) and Li et al. (2019) can only handle the first and second moment constraints for -unimodality, with the objective function in Van Parys et al. (2016) restricted to the probability of the random vector falling outside a prescribed polyhedron, and the objective function in Li et al. (2019) being either the probability of the random vector lying in a hyperplane or a special function derived from the conditional value-at-risk. The left half of Table 1 summarizes the requirements in this existing literature for all the shape constraints that we contribute to in this paper.

| Existing literature | IW-SAA | |||

| Shape constraints | Objective | Additional moment | ||

|---|---|---|---|---|

| constraints | Objective | Additional moment | ||

| constraints | ||||

| monotonicity* | piecewise polynomial | |||

| (Popescu (2005)) | piecewise polynomial | |||

| & Slater’s condition | ||||

| (Popescu (2005)) | mild integrability | |||

| condition | ||||

| (Corollaries 1-5) | mild integrability | |||

| condition | ||||

| & Slater’s condition | ||||

| (Corollaries 1-5) | ||||

| convexity* (bounded domain) | ||||

| unimodality* | ||||

| orthounimodality† | indicator of the | |||

| epigraph of a function | ||||

| (Lam et al. (2021)) | indicator of | |||

| hyperrectangles | ||||

| (Lam et al. (2021)) |

1.2 Contributions

Motivated by the above challenges, we propose an alternative sampling-based approach to solve shape-constrained distributional optimization. Rather than using the mixture idea in the Choquet representation, our approach first conducts a change of measure from the underlying distribution to a pre-selected sampling distribution. Then, by drawing Monte Carlo samples from this latter distribution, we formulate a suitable sample average approximation (SAA) (Shapiro et al. (2021)) where the decision variable is now the importance weights between the original and the sampling distributions.

We call our approach importance-weighted (IW) SAA. The change of measure idea underpins the technique of importance sampling, which is especially useful as a variance reduction method (Bucklew and Bucklew (2004); Juneja and Shahabuddin (2006); Blanchet and Lam (2012)) and in Bayesian inference (Liu (2001)). In our setting, importance sampling is used to translate the decision variables from the underlying distribution in (1) to the importance weights, so that we can now sample from a known distribution to conduct SAA. In this regard, the closest works to our approach are Glasserman and Xu (2014) and Ghosh and Lam (2019), which like us consider worst-case distributional optimization problems. In particular, Glasserman and Xu (2014) considers uncertainty sets constructed as divergence-based neighborhood balls surrounding a baseline distribution, while Ghosh and Lam (2019) considers additionally moment-based uncertainty sets and essentially discrete distributions. Nonetheless, when shape constraints are present, challenges arise regarding the representability of these shapes in terms of SAA. Moreover, the SAA solution may violate the feasibility of the additional moment constraints in (1), which adds complications in convergence analyses as it necessitates the consideration of both optimality and feasibility. These challenges motivate us to develop strong duality results for both the original and SAA counterparts in order to remove the need to check feasibility for the moment constraints. With this, we study statistical consistency and convergence rates of our IW-SAA, by leveraging tools from empirical processes (van der Vaart and Wellner (1996)) that critically hinge on the functional complexities of the shape constraints. Our study on this interplay of duality and empirical process machinery to analyze shape-constrained optimization appears to be the first in the literature. It ultimately leads to solution schemes for problems that are beyond the reach of existing Choquet-based approaches; see the right half of Table 1.

1.3 Other Related Works

We close this introduction by comparing our study with several lines of related works. First is shape-constrained nonparametric -estimation in statistics, which concerns the optimization of likelihood function or empirical loss function subject to shape constraints as a means to obtain estimators for statistical quantities. Royset and Wets (2015), Pavlides and Wellner (2012), and Sager (1982) and Polonik (1998) study density estimation under one-dimensional shape constraints, the so-called scale mixture of uniform class of distributions, and orthounimodal constraints respectively. Royset and Wets (2020) and Royset (2020) investigate consistency and convergence rates. Seijo and Sen (2011); Guntuboyina and Sen (2015); Mukherjee et al. (2024) study (quasi)convex least squares estimation. Fang et al. (2021) study multivariate extensions of isotonic regression and total variation denoising. Compared with this literature, our shape-constrained distributional optimization bears two key differences. First is our focus on the optimal value instead of the optimal solution, which arises from our disparate motivation from nonparametric -estimation. In DRO, the optimal value of (1) is the worst-case value of the objective function, which signifies and provides an upper bound on the actual decision performance. In contrast, the optimal solution in nonparametric -estimation corresponds to the statistical estimator and is thus of primary interest in statistics. The second difference is the lack of moment constraints in nonparametric -estimation, compared to our formulation (1) that critically comprises both moments and shape constraints as discussed above. These differences lead us to develop new results on the interaction of duality with empirical processes and convergence guarantees for optimal values that are not studied in the nonparametric -estimation literature.

Our work is also related to functional optimization that, like our problem, is infinite-dimensional in nature, but its decision variable is not necessarily a density. In contrast to deterministic calculus of variation problems (Gelfand and Fomin (2000)), some recent work studies stochastic counterparts. Singham and Cai (2017) first propose to use SAA to approximate functional optimization formulations motivated from principal-agent problems that are analytically intractable. Singham (2019) further studies bootstrapping to estimate the optimal value, though without consistency guarantees. Singham and Lam (2020) investigates bounding techniques (Mak et al. (1999); Bayraksan and Morton (2006)) for optimal values and theoretical convergence. Similar to our work, these studies involve SAA problems with decision variables of growing dimensions. On the other hand, they focus on essentially one-dimensional monotonic functions as decision variables, and do not include auxiliary moment constraints or distributional variables that necessitate changes of measure. As such, they do not investigate duality theory and the elaborate usage of empirical processes for general shapes. Lastly, Zhou et al. (2022) studies the convergence of SAA in functional optimization that is driven by Gaussian processes. However, their sampling is on the underlying Gaussian variable that is different from our change of measure and subsequent developments to address shape-constrained problems.

The remainder of this paper is organized as follows. Section 2 gives an overview of our IW-SAA approach and theoretical guarantees. Section 3 specializes our main guarantees to various shape constraints, and discusses our scope of applicability and limitations. Section 4 discusses computational challenge and remedies associated with the number of constraints. Section 5 presents numerical results to validate our theorems and demonstrates our empirical performances. The Appendix contains additional technical details and proofs for all results in this paper.

2 IW-SAA and General Theoretical Guarantees

We present our IW-SAA to solve (1). First, we select a suitable known and simulatable (i.e., allows the generation of random copies) positive probability density on , and rewrite (1) via a change of measure from to as

| subject to | (3) | |||

where is the likelihood ratio and contains the corresponding shape constraints for . We require the positivity of to ensure the existence of the likelihood ratio. Now, since the probability density is known and simulatable, we can draw i.i.d. samples from and formulate the SAA counterpart of () as

| subject to | (4) | |||

Note that the SAA problem () is potentially infinite-dimensional, since its decision space is the same as that of problem (). To obtain a finite-dimensional reduction of (), we need to discretize the shape constraint in terms of samples that leads to what we call finite-dimensional reducibility. To explain, consider the example where is the class of monotonically increasing functions. The space can be written as . A corresponding discretized version, denoted by , can be written as which is a subset of . This discretized version is invertible in the sense that, given any discrete values , we can recover a function such that for all by interpolation:

where is a permutation of such that . Consequently, we can replace by in () without changing its optimal value, and the resulting optimization problem is a finite-dimensional linear program with decision variables . In general, we say the SAA problem () has a finite-dimensional reduction if the discretization of like above is invertible, in which case the decision variable can be chosen as without loss of generality. The left half of Table 2 displays, for various shape constraints, whether () has a finite-dimensional reduction. In particular, the four constraints listed in Table 1 are finite-dimensionally reducible and result in readily solvable linear programs. Details of these reformulations will be presented in Section 3.

2613

| Shape constraints | Finite-dimensional reducibility | Consistency | Canonical convergence rate |

|---|---|---|---|

| monotonicity | |||

| convexity (bounded domain) | |||

| convexity (unbounded domain) | |||

| unimodality | |||

| -unimodality |

\usym

2613 |

\usym

2613 |

|

| block unimodality | |||

| orthounimodality |

In the next two subsections, we present our main theoretical results on IW-SAA, including strong duality (Section 2.1) and statistical guarantees (Section 2.2).

2.1 Strong Duality

We prove strong duality to transform () and () into unconstrained optimization problems. The Lagrangian dual problems of () and () are given by

| (5) |

| (6) |

The following assumptions are needed to establish strong duality.

Assumption 1.

For any , the random variables are integrable with respect to .

Assumption 2.

is a convex set.

Assumption 3.

There exists a feasible function s.t.

Additionally, is an interior point of the following set

Assumption 1 ensures the dual problem is well-defined. Assumption 2 guarantees the optimization problem is convex, which is the usual assumption when establishing strong duality. Assumption 3 is a Slater condition for the distributional optimization problem, similar to the conditions in, e.g., Karlin and Studden (1966); Smith (1995); Shapiro (2001); Bertsimas and Popescu (2005); Popescu (2005). Note that whether Assumptions 1-3 hold or not depends only on and but not the choice of sampling distribution .

Under these assumptions, we develop strong Lagrangian duality in both the distributional optimization problem and its SAA counterpart. We use to denote the optimal value of optimization problems. Since the SAA optimal value is the supremum of possibly an uncountable number of random variables, it may not be measurable. As such we employ outer (with a superscript ) and inner (with a subscript ) probabilities and expectations to handle the measurability issue. Stochastic convergence is understood under the outer expectation. We delegate these technical measurability details to Appendix A.

Theorem 1 (Strong duality for ).

2.2 Statistical Guarantees

We prove the consistency and canonical convergence rate of IW-SAA. We first introduce some notation. We write as the probability measure induced by and define the corresponding empirical distribution based on observations from as , where is the point mass at . Following the convention in empirical processes, the expectations of under and are written as and . An envelope of a function class is any function such that . We write for any signed measure and function class . We define the empirical process as .

Now we state our assumptions. We begin with the finiteness of the optimal value.

Assumption 4.

is finite.

The next assumption states that the function in the objective and constraints in () are so-called -Glivenko-Cantelli (-GC), i.e., they satisfy the uniform law of large numbers.

Assumption 5.

The function classes have integrable envelopes and are -GC, i.e., , for any .

With these, we have the consistency of IW-SAA.

Establishing canonical convergence rates requires an additional maximal inequality holds for , which helps bound the probability .

Assumption 6.

a constant s.t.

In deriving Theorems 3 and 4, we leverage tools from empirical processes to bound the uniform discrepancy between expectations and their sample averages over a class of functions signified by the likelihood ratios. This class of functions are defined by the feasible region specified by both the moment and shape constraints. However, an issue arises that the moment constraints in () and () may not be the same due to the discretization in (), and in fact the moment constraints in () can even change with the sample size . Thus, a likelihood ratio that satisfies the moment constraints in () may not satisfy the ones in () and vice versa. To this end, strong duality helps move the moment constraints to the objective function and thus unifies the feasible region to be in both () and (), which makes the empirical process theory applicable to our problem. With this remedy, the shape constraints are instrumental in reducing the complexity of the feasible decision space and rendering Assumptions 5 and 6 verifiable.

In the next section, we specialize our general results obtained in this section to various shape constraints. In particular, we demonstrate how we are able to handle objectives and moment constraints beyond the existing Choquet-based technique, which is a key implication in this paper.

3 Applications to Various Shape Constraints

We apply Theorems 3 and 4 to the shape constraints in Table 1, and also discuss the limitations of our approach to other remaining constraints in Table 2. First of all, note that our shape constraints are imposed on the unknown density but Assumptions 5 and 6 are imposed on the function classes . So we need a lemma that can verify Assumptions 5 and 6 by the conditions on . We first introduce some notation (from van der Vaart and Wellner (1996) Section 2.1.1). Let be a normed function space, where is the -norm, i.e., . For two functions (not necessarily in ), the bracket is the class of functions satisfying . The bracket is called an -bracket if and . We define the bracketing number as the minimum number of -brackets to cover . For , we define .

Lemma 1.

Lemma 1 provides two types of conditions to verify Assumptions 5 and 6. One is based on the moment conditions on , i.e., (7) and (9). Recall that in our formulation one of the functions must be the indicator function to represent the total mass constraint on . Therefore, (7) and (9) can hold only when is bounded. The other type, i.e., (8) and (10), is based on the moment conditions on but with an additional condition . This type of condition can be applied when is unbounded and the additional condition essentially says the sampling distribution should be heavier-tailed than any . A common situation (also used in the following examples) of the second type is that the density is known to be lighter-tailed than some density , i.e., for any and some constant . Then the envelope can be chosen as with the sampling distribution . In data-driven settings, this can be conducted by estimating the tail index from the data and choosing that is heavier-tailed than the true distribution with high confidence.

Now we are ready to study the six shape constraints in Table 2. In particular, all finite-dimensional reductions, if available, will be in the following form:

| subject to | |||

To avoid repetition, we will only specify the “discrete shape constraint” in the following subsections. As discussed above, we will distinguish between bounded domains and unbounded domains since they require different conditions.

3.1 Compact Domain

We first consider three one-dimensional shapes: monotonicity, convexity and unimodality (a function is said to be unimodal about a mode if is non-decreasing when and is non-increasing when ). More precisely, letting be the order statistics of , we have the following:

Corollary 1 (One-dimensional shapes).

Let , and the shape-constrained function class be one of the following:

where is a fixed point. Suppose the sampling distribution satisfies , the functions satisfy for some and Assumption 3 holds. Then the IW-SAA problem with one of the above is equivalent to the linear program with the corresponding discrete shape constraint:

i.e., is finite-dimensionally reducible. Additionally, and .

Corollary 1 concludes that under our assumptions, the three one-dimensional shapes elicit IW-SAAs that are finite-dimensionally reducible and exhibit consistency and -convergence. Corollary 1 can be also applied to the non-decreasing shape constraint and concave shape constraint with obvious modifications. For unimodality, the mode must be pre-specified. Otherwise the function spaces and are no longer convex, in which case Assumption 2 fails.

Note that the shape constraint in Corollary 1 contains an upper bound . The impact of this bound can be divided into two cases. First is that the optimization problem without this boundedness constraint admits a bounded density as an optimal solution. In this case, selecting a large enough as the upper bound retains the optimal solution and optimal value. Another possibility is that either the problem without this boundedness constraint has no optimal solution or any optimal solution must be unbounded. In this situation, including an upper bound affects the optimal value. However, this situation itself indicates that the starting formulation can be problematic, as the worst-case scenario is achieved by an unbounded density that is typically unrealistic in practice. This discussion also carries over to the subsequent shape constraints that we study.

Next we discuss orthounimodality, which is a generalization of unimodality to the multidimensional case. A function on is said to be orthounimodal about the mode , if for each and any fixed , the function is non-decreasing on and non-increasing on . Orthounimodality is recently studied in Lam et al. (2021) as a multidimensional shape constraint well-suited to model tail distributional behaviors and thus is attractive for extreme event analysis. For two vectors , and are interpreted in the component-wise sense and denotes the hyperrectangle (similar for , and ). We show that orthounimodality entails a consistent IW-SAA.

Corollary 2 (Orthounimodality).

Let () be a hyperrectangle, and the shape-constrained function class . Suppose the sampling distribution satisfies , the functions satisfy for some and Assumption 3 holds. Then the IW-SAA problem is equivalent to the linear program with the following discrete shape constraint:

i.e., is finite-dimensionally reducible. Additionally, .

In Corollary 2, for ease of exposition, we assume the mode is a vertex of the domain . When is in a general position, the discrete shape constraint can be modified accordingly and the same conclusion holds. This observation also carries over to the subsequent cases with unbounded domain. Note that, although is consistent, unlike in Corollary 1, orthounimodality may not have a convergence rate because Assumption 6 may not hold. In fact, the lower bound in Theorem 1.1 of Gao and Wellner (2007) implies that if , then for any fixed , for some constant when . Therefore, the sufficient condition (9) for Assumption 6 does not hold. Even if one would like to directly verify Assumption 6, one may still need to show the bracketing integral condition for some and all (or the finiteness of the uniform entropy integral; see, e.g., Van der Vaart (2000) Chapter 19) since these conditions may give the easiest way to prove the maximal inequality (see, e.g., the results in Van der Vaart (2000) Chapter 19 starting from Lemma 19.34). However, recall that one of , say , is the indicator function which denotes the total mass condition. Therefore, when , the lower bound in Theorem 1.1 of Gao and Wellner (2007) also implies , which makes the bracketing integral condition fail for the function class associated with . The uniform entropy integral condition is also likely not to hold because the lower bound in Theorem 1.1 of Gao and Wellner (2007) also applies to the covering number.

3.2 Unbounded Domain

For unbounded domains, as we discussed previously following Lemma 1, (8) and (10) should be used to justify Assumptions 5 and 6. Conditions (8) and (10) are naturally applied to the case where the densities are known to be lighter-tailed than some density , i.e., for any because the sampling density will automatically satisfy the requirements. We will focus on this case in the following.

Corollary 3 (Monotonicity with unbounded domain).

Let and the shape-constrained function class , where , and is a non-increasing positive probability density on with . Let be the sampling distribution. Suppose the functions satisfy for some and Assumption 3 holds. Then the IW-SAA problem is equivalent to the linear program with the following discrete shape constraint:

i.e., is finite-dimensionally reducible. Additionally, and .

We comment that the requirement of being non-increasing and positive is without loss of generality. Suppose is not non-increasing. We define . It is easy to see is unchanged if is replaced by . We can also normalize to make it a probability density with a corresponding change of ( has finite integral since it is bounded by ). Moreover, if for some , we can see the effective domain is actually because for any . In this case, we can take as the new domain and apply Corollary 1. Similar discussion also applies to the remaining shape constraints in this subsection.

Corollary 4 (Unimodality with unbounded domain).

Let and the shape-constrained function class , where , , and is a positive unimodal (about ) probability density on with . Let be the sampling distribution. Suppose the functions satisfy for some and Assumption 3 holds. Then the IW-SAA problem is equivalent to the linear program with the following discrete shape constraint:

i.e., is finite-dimensionally reducible. Additionally, and .

Corollary 4 still holds if is the half line or .

Corollary 5 (Orthounimodality with unbounded domain).

Let (), and the shape-constrained function class , where , and is a positive orthounimodal (about ) probability density on with . Let be the sampling distribution. Suppose the functions satisfy for some and Assumption 3 holds. Then the IW-SAA problem is equivalent to the linear program with the following discrete shape constraint:

i.e., is finite-dimensionally reducible. Additionally, .

Corollaries 3, 4 and 5 together stipulate that under the corresponding assumptions, monotonic and unimodal densities in single dimension, and orthounimodal densities in multiple dimension, elicit finite-dimensional reducibility. Moreover, the single-dimensional solutions exhibit consistency and canonical convergence rates, while the orthounimodal solutions exhibit only consistency and there is no guarantee on the canonical rate, much like the situation in the bounded domain case presented in Section 3.1.

3.3 Limitations

While our approach works for the cases presented in Sections 3.1 and 3.2, it bears limitations when applying to some other shape constraints, either due to a failure of finite-dimensional reducibility or consistency. We discuss these limitations as follows. Note that, while these are negative results at the moment, they also open up potential future developments along our current direction that can remedy these issues.

3.3.1 Convexity in unbounded domain.

Let . Note that a convex function can be a density on only if it is non-increasing. As discussed in Lemma 1, a shape-constrained function class in an unbounded domain should be chosen to be , where , and is a positive probability density on . Unfortunately, in this case, convexity does not allow a finite-dimensional reduction of () even though is still consistent and has -convergence. Notice that for the discrete points , the constraint is naturally expressed in the following way as in Corollary 1:

| (11) |

However, (11) is not an equivalent reformulation of since we may not be able to extend the discrete values to a real function . Although we can use, e.g., linear interpolation to get a convex function , the constraint could be violated. In other words, the requirement imposes a special structure on the convex functions , but the simple discrete version (11) cannot capture it. Therefore, () may not admit a finite-dimensional reduction.

3.3.2 -unimodality.

A function is said to be -unimodal about the mode (also called star unimodal if ) if is non-increasing in for any nonzero vector . The problem with the function class of -unimodality is that it is too large to satisfy Assumptions 5 and 6. More precisely, -unimodality neither has a finite bracketing number nor satisfies Assumptions 5 or 6 even if assumed to be bounded when (-unimodal functions cannot be bounded when unless it is zero almost everywhere with respect to the Lebesgue measure).

Proposition 1 (Failure of sufficient conditions for -unimodality).

Let () be a hyperrectangle and be an arbitrary constant. Define the -unimodal function class as if , and if . Let be any probability density on that is equivalent to the Lebesgue measure, i.e., they are absolutely continuous with respect to each other. Then for any , for all sufficiently small . Also, if is not almost everywhere zero (with respect to Lebesgue measure), then does not satisfy Assumptions 5 or 6.

Proposition 1 stipulates that -unimodality fails to satisfy the sufficient conditions for consistency and -convergence. Next, we provide a counterexample to directly show the IW-SAA optimal value for -unimodality may not be consistent.

Consider the following two-dimensional -unimodal shape-constrained problem

| subject to | |||

where , , denotes the usual Euclidean norm, and the shape constraint is if and for any if . Given a sampling distribution on , the corresponding IW-SAA problem is given by

| subject to | |||

where . For this example, we have:

Proposition 2 (Lack of consistency for -unimodality).

The optimal value of satisfies . For any sampling distribution , the IW-SAA optimal value satisfies . Consequently, the IW-SAA optimal value is not consistent.

3.3.3 Block unimodality.

A function is said to be block unimodal about the mode on , if it is orthounimodal and satisfies a nonnegativity condition: for any vectors with , the alternating sum satisfies

| (12) |

where are the vertices of the hyperrectangle . This nonnegativity condition is similar to that for a cumulative distribution function, i.e., if denotes a cumulative distribution function, then this condition means that has nonnegative mass in the hyperrectangle . Let () and , is block unimodal about on . Since block unimodality contains fewer functions than orthounimodality, condition (7) in Lemma 1 must hold for block unimodality when it holds for orthounimodality. Therefore, we can show is consistent with proper conditions as in Corollary 2. However, the equivalent reformulation of using discrete values in () is hard to obtain. In fact, condition (12) vanishes if it is restricted to discrete values because any subset of with cardinality cannot constitute the vertices of any hyperrectangle with probability 1. If this condition is ignored in the IW-SAA, then the problem () for block unimodality reduces to the same linear program for orthounimodality in Corollary 2. However, it is not guaranteed that each discrete feasible solution in this linear program can be extended to a function that satisfies block unimodality. Thus, there is no equivalent reformulation of for block unimodality that only involves .

Finally, we note that in the multidimensional case, Lam et al. (2021) explains how orthounimodality can be more well-suited for extreme event applications compared to -unimodality and block unimodality. This is due to the sensitivity of -unimodality with respect to its mode and the difficulty in interpretability for block unimodality. Orthounimodality, on the other hand, is demonstrably less sensitive to the mode and easy to intuit. From this perspective, while currently IW-SAA faces limitations in applying to -unimodality and block unimodality, it encouragingly applies to the important case of orthounimodality.

3.4 Summary of Results for the Considered Shape Constraints

We close this section by connecting all our derived results back to Table 2. Corollaries 1-5 in Sections 3.1 and 3.2 show that IW-SAAs applied to monotonicity, convexity (bounded domain), unimodality and orthounimodality are finite-dimensionally reducible to linear programs, which are indicated as the checks in the second column in Table 2. Moreover, these corollaries show that their IW-SAAs are consistent and, except for orthounimodality, exhibit canonical convergence rates, which are indicated as the checks in the third and fourth columns in Table 2. The remaining cases are discussed in Section 3.3. Although IW-SAA applied to convexity (unbounded domain) is consistent and has canonical convergence rate, we have not found its finite-dimensional reduction. For -unimodality, Proposition 2 provides a counterexample to show its IW-SAA may not be consistent, let alone have canonical convergence rate. Hence, there is no reason to study its finite-dimensional reduction. For block unimodality, the only property we can obtain is consistency as explained in Section 3.3.3. All these results are indicated by the checks, crosses and blanks in the corresponding rows in Table 2.

4 Complexity in the Number of Constraints

We have so far focused on the convergence properties of our IW-SAA. On the other hand, as the simulated scenario size increases, IW-SAA requires an increasing number of decision variables and constraints, making the linear program harder to solve. In this section, we discuss computationally efficient ways to encode our IW-SAA and the corresponding complexity with respect to the number of constraints therein.

First, for one-dimensional shape constraints, by using order statistics, the number of discrete shape constraints is as in Corollary 1, which is not improvable.

For orthounimodality, the above sorting method does not work because orthounimodality relies on a partial order. In this case, a naive approach is to construct an orthounimodality constraint for each pair . To study the complexity of this approach, we assume that the components of are continuously distributed and mutually independent. Let denote the number of orthounimodality constraints constructed from samples in using this approach. We have

where is due to the mutually independent and continuously distributed components. We observe that the complexity of this naive approach is for a fixed dimension, which is larger than that of the one-dimensional shapes. Additionally, the complexity is decreasing in because the condition is harder to achieve for higher dimensions.

One clear drawback of the above naive approach is that it includes many redundant constraints. For example, if we have a chain , then it suffices to specify the constraints for and but the naive approach still includes the redundant constraint . In fact, if we have such an inequality chain with length , then this approach will specify orthounimodality constraints from the chain while only of them are non-redundant. Removing such redundant constraints can significantly reduce the complexity, especially for low dimensions when the chain tends to be long. This removal procedure is known as transitive reduction in graph theory. Here we explain how this can be done via adjacency matrix multiplication. We construct a direct graph where the vertices denote all samples and a directed edge exists if and only if . We notice that a orthounimodality constraint for is non-redundant if and only if there is no other sample that is in between them, or equivalently, there is no path of length two that is from to . Let be the adjacency matrix (a boolean matrix) of graph . Then we compute the “two-step adjacency matrix” via boolean matrix multiplication and notice that the element in is if and only if there is no path of length two that is from to . Therefore, it suffices to pick all pairs whose element in is but in and they correspond to all non-redundant orthounimodality constraints. We summarize this algorithm in Algorithm 1. Its time complexity is using the best exact algorithms for matrix multiplication (Le Gall (2014)). However, if we leverage the sparse structure of and use a sparse matrix to represent and do matrix multiplication, the algorithm can be accelerated.

Inputs: Samples and sampling density

Let denote the number of non-redundant orthounimodality constraints from samples in after the transitive reduction. We have:

Theorem 5.

Suppose the IW-SAA samples are i.i.d. from which have continuously distributed and mutually independent components. Then

In particular, when , can be simplified as

Additionally, we have

5 Numerical Experiments

We present numerical results to validate our theory and demonstrate the performances of our IW-SAA. Section 5.1 first verifies the consistency and convergence rate of the IW-SAA optimal value for the one-dimensional case, and suggests a similar rate even for the multidimensional case. Section 5.2 investigates the influence of the choice of sampling distribution. Section 5.3 demonstrates the capability of our IW-SAA in solving a complicated multidimensional orthounimodal distributional optimization problem with more than 50 constraints. Finally, Section 5.4 uses our IW-SAA to solve shape-constrained distributional optimization motivated from rare-event estimation. Each experiment is replicated 100 times without further clarification.

5.1 Validation of Convergence Rates

We first use a relatively simple unimodal distributional optimization problem to validate our theoretical consistency and convergence rate. Then we investigate these convergence behaviors for a 4-dimensional orthounimodal distributional optimization problem. Specifically, we consider the following two problems:

where , and denotes the usual Euclidean norm. For these problems, by calculus and direct usage of the shape properties, we can obtain their optimal values, with the first one being attained by the uniform distribution on , and the second one being attained by the uniform distribution on . On the other hand, note that both problems cannot be handled by existing Choquet-based solutions. The first problem contains inequality moment constraints together with the density constraint , while the second problem violates both the epigraph requirements for the objective and the hyperrectangle requirements for the moment functions; see Table 1.

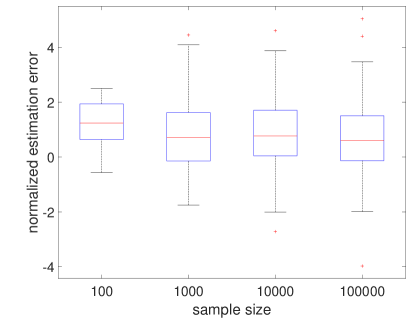

For IW-SAA, the sampling distributions are chosen as uniform distributions on and respectively. Figure 1 shows the boxplots of the normalized estimation errors of our IW-SAA outputs against the true optimal values, i.e., times the difference between the IW-SAA output and optimal value. We observe that the normalized estimation errors in both problems mostly lie in bounded regions as grows. These validate our consistency results in Corollaries 1 and 2 since they imply that the unnormalized estimation errors shrink to 0 as grows. More precisely, for the unimodal distributional optimization problem, bounded normalized estimation errors validate the convergence rate, i.e., in Corollary 1. For the orthounimodal distributional optimization problem, the similar trend hints that this rate may continue to apply to this case even though no rate result has been established for this setting.

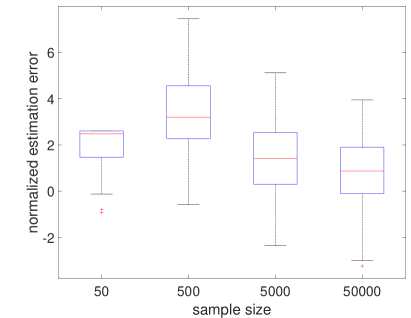

5.2 Influence of the Sampling Distribution

We examine the influence of the sampling distribution on the quality of the IW-SAA optimal value. We consider the following unimodal distributional optimization problem

| subject to | |||

where and the values of are calibrated by , with being the distribution of conditional on that it is in (same for the following without further clarification). We test four sampling distributions: uniform distribution on , , and . We use a sample size . Note that, like in Section 5.1, this example cannot be handled by existing Choquet-based solutions as the objective function is not semi-algebraic; see Table 1.

Figure 2 displays the results. We observe that IW-SAA using the uniform distribution, and converge to almost the same value with the considered sample size, while IW-SAA using has not. On one hand, the similar convergences using and are coherent with the consistency of IW-SAA in Corollary 1. On the other hand, it appears that using underestimates the optimal value with as large as samples, since is too concentrated and cannot explore the whole domain broadly enough. This suggests that, in order to ensure IW-SAA results in a good-quality solution, the sampling distribution needs to be chosen suitably to be able to sufficiently explore the domain.

5.3 High-Dimensional Many-Constraints Orthounimodal Distributional Optimization

While the previous two subsections have exemplified problems that cannot be solved by existing Choquet-based methods, some of these problems could still be viewed as somewhat simple as we can find other means to obtain their true optimal values. In this section, we consider a significantly more complicated 10-dimensional orthounimodal distributional optimization problem with more than 50 moment constraints. We demonstrate how IW-SAA is capable of solving it. Specifically, consider the following problem:

| subject to | |||

where , , are calibrated by the true density ( is the identity matrix in ), is the density of and . We use samples from to drive the IW-SAA problem. The result is displayed in Figure 3. We see that the range of the boxplot is quite small, suggesting the convergence of our IW-SAA and coherence with Corollary 5. This result demonstrates that our IW-SAA is able to solve high-dimensional many-constraints distributional optimization problems.

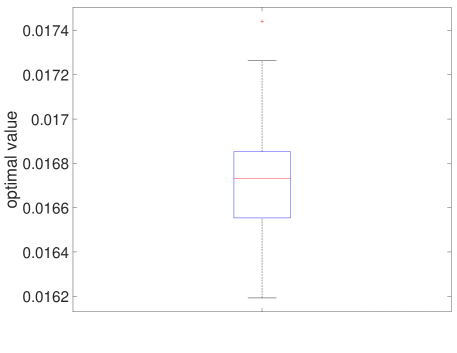

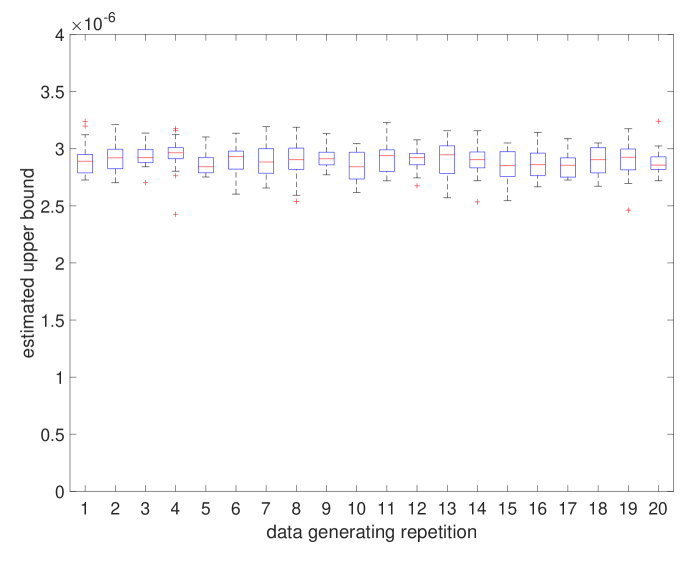

5.4 Extreme Event Analysis

In this experiment, we use our IW-SAA to solve a shape-constrained distributional optimization problem motivated from extreme event estimation. Suppose we have samples from the unknown true distribution . Suppose we want to estimate the 10-dimensional rare-event probability whose true value is around . The empirical distribution cannot be used to estimate such a tiny probability because typically none of samples will fall into target region. Instead, following the argument in Lam et al. (2021), we find an upper bound on the true probability by imposing the following orthounimodal distributional optimization problem

| subject to | |||

where , , is the density of and . The moment constraints can be calibrated via the confidence intervals constructed from data. In particular, the first one is directly obtained from the usual two-sided normal confidence interval, while the remaining ones are calibrated from the Kolmogorov–Smirnov (KS) two-sided statistic that gives a simultaneous confidence band for using the conditional empirical distribution of given . Then taking and multiplying the confidence bounds of leads to the desired confidence intervals in the DRO constraints, where is the -quantile of the conditional empirical distribution of . Other constraints are calibrated in the same way where are the quantiles of the conditional empirical distributions of , and . In particular, we calibrate each constraint with level and the Bonferroni correction ensures that all moment constraints simultaneously hold with level ( in our experiment).

We independently generate 20 different data sets. For each data set, we calibrate the constraints as in the above and run IW-SAA using samples from 20 times. Figure 4 shows the boxplot of the IW-SAA optimal values (the -axis denotes different data sets and the -axis denotes different IW-SAA runs for each data set). We see that the IW-SAA optimal values deliver an upper bound the true rare-event probability. Moreover, considering the tiny magnitude of the the true objective value, the estimated values appear reasonably tight.

6 Conclusion and Discussion

This paper proposes a new approach, which we call IW-SAA, to solve shape-constrained distributional optimization that arises prominently in DRO. Our approach is motivated from the tractability challenges faced by the existing Choquet-based method, which uses a mixture representation whose resulting solvability is confined by the geometries and the compatibility between the shape and the objective function and moment constraints. Instead of using such a mixture idea, IW-SAA uses a change of measure to convert the distributional decision variable into likelihood ratio with respect to a known sampling distribution, and uses SAA to approximate the objective and constraints. In order to analyze the consistency and canonical convergence rate of our approach, we develop a strong duality theory to remedy the mismatch of feasibility between original and sampled problems, and couple the duality with empirical processes, where the geometries of shape constraints are shown to play a critical role in controlling the corresponding function class complexities. We apply IW-SAA to various one-dimensional shape-constrained distributional optimization and a recent multidimensional orthounimodal distributional optimization, and show that these formulations can be reduced to finite-dimensional linear programs and exhibit desirable convergence behaviors.

We view our study as a starting point in researching this new IW-SAA approach to tackle shape-constrained optimization. While our IW-SAA applies to a range of shapes, it also incurs limitations in some contexts, which prompt several immediate future directions. First, convexity (unbounded domain) and block unimodality lack finite-dimensional reducibility although they have statistical guarantees. To make IW-SAA applicable, an approach is to develop tractable reduction of the current infinite-dimensional sample problems by possibly leveraging specific function structure and shapes. Second, the convergence rate of IW-SAA for orthounimodality is still open, even though the numerical results in Section 5.1 hint that it could continue to be canonical. To either prove or disprove this conjecture, a more refined maximal inequality for empirical processes needs to be developed. Third, we have proved that IW-SAA for -unimodality is not consistent. Hence, solving -unimodal distributional optimization may still rely on the Choquet representation theorem like the existing literature. However, it is possible that by injecting further suitable constraints into the formulation that reduces the corresponding function class complexity, we can obtain consistency or even canonical convergence rates for such shape-constrained problems.

Acknowledgements

We gratefully acknowledge support from the InnoHK initiative, the Government of the HKSAR, Laboratory for AI-Powered Financial Technologies, and Columbia Innovation Hub grant. We would also like to thank Raghu Pasupathy and Johannes Royset for their very kind suggestions that have helped improve this paper.

References

- Atar et al. [2015] Rami Atar, Kenny Chowdhary, and Paul Dupuis. Robust bounds on risk-sensitive functionals via Rényi divergence. SIAM/ASA Journal on Uncertainty Quantification, 3(1):18–33, 2015.

- Bayraksan and Love [2015] Güzin Bayraksan and David K Love. Data-driven stochastic programming using phi-divergences. In The Operations Research Revolution, pages 1–19. INFORMS, 2015.

- Bayraksan and Morton [2006] Güzin Bayraksan and David P Morton. Assessing solution quality in stochastic programs. Mathematical Programming, 108(2):495–514, 2006.

- Ben-Tal et al. [2009] Aharon Ben-Tal, Laurent El Ghaoui, and Arkadi Nemirovski. Robust Optimization, volume 28. Princeton University Press, 2009.

- Ben-Tal et al. [2013] Aharon Ben-Tal, Dick Den Hertog, Anja De Waegenaere, Bertrand Melenberg, and Gijs Rennen. Robust solutions of optimization problems affected by uncertain probabilities. Management Science, 59(2):341–357, 2013.

- Bertsimas and Popescu [2005] Dimitris Bertsimas and Ioana Popescu. Optimal inequalities in probability theory: A convex optimization approach. SIAM Journal on Optimization, 15(3):780–804, 2005.

- Bertsimas et al. [2011] Dimitris Bertsimas, David B Brown, and Constantine Caramanis. Theory and applications of robust optimization. SIAM Review, 53(3):464–501, 2011.

- Bertsimas et al. [2018] Dimitris Bertsimas, Vishal Gupta, and Nathan Kallus. Robust sample average approximation. Mathematical Programming, 171(1):217–282, 2018.

- Blanchet and Kang [2021] Jose Blanchet and Yang Kang. Sample out-of-sample inference based on Wasserstein distance. Operations Research, 69(3):985–1013, 2021.

- Blanchet and Lam [2012] Jose Blanchet and Henry Lam. State-dependent importance sampling for rare-event simulation: An overview and recent advances. Surveys in Operations Research and Management Science, 17(1):38–59, 2012.

- Blanchet and Murthy [2019] Jose Blanchet and Karthyek Murthy. Quantifying distributional model risk via optimal transport. Mathematics of Operations Research, 44(2):565–600, 2019.

- Blanchet et al. [2022] Jose Blanchet, Karthyek Murthy, and Nian Si. Confidence regions in Wasserstein distributionally robust estimation. Biometrika, 109(2):295–315, 2022.

- Bucklew and Bucklew [2004] James Antonio Bucklew and J Bucklew. Introduction to Rare Event Simulation, volume 5. Springer, 2004.

- Chen and Paschalidis [2018] Ruidi Chen and Ioannis C Paschalidis. A robust learning approach for regression models based on distributionally robust optimization. Journal of Machine Learning Research, 19(13):1–48, 2018.

- Chen et al. [2021] Xi Chen, Simai He, Bo Jiang, Christopher Thomas Ryan, and Teng Zhang. The discrete moment problem with nonconvex shape constraints. Operations Research, 69(1):279–296, 2021.

- Delage and Ye [2010] Erick Delage and Yinyu Ye. Distributionally robust optimization under moment uncertainty with application to data-driven problems. Operations Research, 58(3):595–612, 2010.

- Dey and Juneja [2012] Santanu Dey and Sandeep Juneja. Incorporating fat tails in financial models using entropic divergence measures. arXiv preprint arXiv:1203.0643, 2012.

- Dhara et al. [2021] Anulekha Dhara, Bikramjit Das, and Karthik Natarajan. Worst-case expected shortfall with univariate and bivariate marginals. INFORMS Journal on Computing, 33(1):370–389, 2021.

- Dharmadhikari and Joag-Dev [1988] Sudhakar Dharmadhikari and Kumar Joag-Dev. Unimodality, Convexity, and Applications. Elsevier, 1988.

- Doan et al. [2015] Xuan Vinh Doan, Xiaobo Li, and Karthik Natarajan. Robustness to dependency in portfolio optimization using overlapping marginals. Operations Research, 63(6):1468–1488, 2015.

- Duchi et al. [2021] John C Duchi, Peter W Glynn, and Hongseok Namkoong. Statistics of robust optimization: A generalized empirical likelihood approach. Mathematics of Operations Research, 46(3):946–969, 2021.

- Esfahani and Kuhn [2018] Peyman Mohajerin Esfahani and Daniel Kuhn. Data-driven distributionally robust optimization using the Wasserstein metric: Performance guarantees and tractable reformulations. Mathematical Programming, 171(1):115–166, 2018.

- Fang et al. [2021] Billy Fang, Adityanand Guntuboyina, and Bodhisattva Sen. Multivariate extensions of isotonic regression and total variation denoising via entire monotonicity and Hardy–Krause variation. Annals of Statistics, 49(2):769 – 792, 2021.

- Gao and Wellner [2007] Fuchang Gao and Jon A Wellner. Entropy estimate for high-dimensional monotonic functions. Journal of Multivariate Analysis, 98(9):1751–1764, 2007.

- Gao [2022] Rui Gao. Finite-sample guarantees for Wasserstein distributionally robust optimization: Breaking the curse of dimensionality. Operations Research, 2022.

- Gao and Kleywegt [2023] Rui Gao and Anton Kleywegt. Distributionally robust stochastic optimization with Wasserstein distance. Mathematics of Operations Research, 48(2):603–655, 2023.

- Gelfand and Fomin [2000] IM Gelfand and SV Fomin. Calculus of Variations. Dover Publications, 2000.

- Ghaoui et al. [2003] Laurent El Ghaoui, Maksim Oks, and Francois Oustry. Worst-case value-at-risk and robust portfolio optimization: A conic programming approach. Operations Research, 51(4):543–556, 2003.

- Ghosh and Lam [2019] Soumyadip Ghosh and Henry Lam. Robust analysis in stochastic simulation: Computation and performance guarantees. Operations Research, 67(1):232–249, 2019.

- Glasserman and Xu [2014] Paul Glasserman and Xingbo Xu. Robust risk measurement and model risk. Quantitative Finance, 14(1):29–58, 2014.

- Goh and Sim [2010] Joel Goh and Melvyn Sim. Distributionally robust optimization and its tractable approximations. Operations Research, 58(4-part-1):902–917, 2010.

- Gotoh et al. [2018] Jun‐ya Gotoh, Michael Jong Kim, and Andrew E. B. Lim. Robust empirical optimization is almost the same as mean–variance optimization. Operations Research Letters, 46(4):448 – 452, 2018. ISSN 0167-6377.

- Guntuboyina and Sen [2015] Adityanand Guntuboyina and Bodhisattva Sen. Global risk bounds and adaptation in univariate convex regression. Probability Theory and Related Fields, 163(1):379–411, 2015.

- Gupta [2019] Vishal Gupta. Near-optimal Bayesian ambiguity sets for distributionally robust optimization. Management Science, 65(9):4242–4260, 2019.

- Hanasusanto et al. [2015] Grani A Hanasusanto, Vladimir Roitch, Daniel Kuhn, and Wolfram Wiesemann. A distributionally robust perspective on uncertainty quantification and chance constrained programming. Mathematical Programming, 151(1):35–62, 2015.

- Hansen and Sargent [2008] Lars Peter Hansen and Thomas J Sargent. Robustness. Princeton University Press, 2008.

- Hu and Hong [2013] Zhaolin Hu and L Jeff Hong. Kullback-Leibler divergence constrained distributionally robust optimization. Available at Optimization Online, 2013.

- Iyengar [2005] Garud N. Iyengar. Robust dynamic programming. Mathematics of Operations Research, 30(2):257–280, 2005.

- Jain et al. [2010] Ankit Jain, Andrew EB Lim, and J George Shanthikumar. On the optimality of threshold control in queues with model uncertainty. Queueing Systems, 65(2):157–174, 2010.

- Jiang and Guan [2018] Ruiwei Jiang and Yongpei Guan. Risk-averse two-stage stochastic program with distributional ambiguity. Operations Research, 66(5):1390–1405, 2018.

- Juneja and Shahabuddin [2006] Sandeep Juneja and Perwez Shahabuddin. Rare-event simulation techniques: An introduction and recent advances. Handbooks in Operations Research and Management Science, 13:291–350, 2006.

- Karlin and Studden [1966] S. Karlin and W.J. Studden. Tchebycheff Systems: With Applications in Analysis and Statistics. Pure and Applied Mathematics: Interscience. Interscience Publishers, 1966.

- Kuhn et al. [2019] Daniel Kuhn, Peyman Mohajerin Esfahani, Viet Anh Nguyen, and Soroosh Shafieezadeh-Abadeh. Wasserstein distributionally robust optimization: Theory and applications in machine learning. In Operations Research & Management Science in the Age of Analytics, pages 130–166. INFORMS, 2019.

- Lam [2016] Henry Lam. Robust sensitivity analysis for stochastic systems. Mathematics of Operations Research, 41(4):1248–1275, 2016.

- Lam [2018] Henry Lam. Sensitivity to serial dependency of input processes: A robust approach. Management Science, 64(3):1311–1327, 2018.

- Lam [2019] Henry Lam. Recovering best statistical guarantees via the empirical divergence-based distributionally robust optimization. Operations Research, 67(4):1090–1105, 2019.

- Lam and Mottet [2017] Henry Lam and Clementine Mottet. Tail analysis without parametric models: A worst-case perspective. Operations Research, 65(6):1696–1711, 2017.

- Lam and Zhou [2017] Henry Lam and Enlu Zhou. The empirical likelihood approach to quantifying uncertainty in sample average approximation. Operations Research Letters, 45(4):301 – 307, 2017. ISSN 0167-6377.

- Lam et al. [2021] Henry Lam, Zhenyuan Liu, and Xinyu Zhang. Orthounimodal distributionally robust optimization: Representation, computation and multivariate extreme event applications. under review in Mathematics of Operations Research, arXiv preprint arXiv:2111.07894, 2021.

- Le Gall [2014] François Le Gall. Powers of tensors and fast matrix multiplication. In Proceedings of the 39th International Symposium on Symbolic and Algebraic Computation, pages 296–303, 2014.

- Li et al. [2019] Bowen Li, Ruiwei Jiang, and Johanna L Mathieu. Ambiguous risk constraints with moment and unimodality information. Mathematical Programming, 173(1):151–192, 2019.

- Liu [2001] Jun S Liu. Monte Carlo Strategies in Scientific Computing, volume 10. Springer, 2001.

- Mak et al. [1999] Wai-Kei Mak, David P Morton, and R Kevin Wood. Monte carlo bounding techniques for determining solution quality in stochastic programs. Operations Research Letters, 24(1-2):47–56, 1999.

- Mukherjee et al. [2024] Somabha Mukherjee, Rohit K Patra, Andrew L Johnson, and Hiroshi Morita. Least squares estimation of a quasiconvex regression function. Journal of the Royal Statistical Society Series B: Statistical Methodology, 86(2):512–534, 2024.

- Pavlides and Wellner [2012] Marios G Pavlides and Jon A Wellner. Nonparametric estimation of multivariate scale mixtures of uniform densities. Journal of Multivariate Analysis, 107:71–89, 2012.

- Petersen et al. [2000] Ian R Petersen, Matthew R James, and Paul Dupuis. Minimax optimal control of stochastic uncertain systems with relative entropy constraints. IEEE Transactions on Automatic Control, 45(3):398–412, 2000.

- Polonik [1998] Wolfgang Polonik. The silhouette, concentration functions and ML-density estimation under order restrictions. Annals of statistics, pages 1857–1877, 1998.

- Popescu [2005] Ioana Popescu. A semidefinite programming approach to optimal-moment bounds for convex classes of distributions. Mathematics of Operations Research, 30(3):632–657, 2005.

- Royset [2020] Johannes O Royset. Approximations of semicontinuous functions with applications to stochastic optimization and statistical estimation. Mathematical Programming, 184(1):289–318, 2020.

- Royset and Wets [2015] Johannes O Royset and Roger JB Wets. Fusion of hard and soft information in nonparametric density estimation. European Journal of Operational Research, 247(2):532–547, 2015.

- Royset and Wets [2020] Johannes O Royset and Roger JB Wets. Variational analysis of constrained M-estimators. Annals of Statistics, 48(5):2759–2790, 2020.

- Sager [1982] Thomas W Sager. Nonparametric maximum likelihood estimation of spatial patterns. Annals of Statistics, pages 1125–1136, 1982.

- Seijo and Sen [2011] Emilio Seijo and Bodhisattva Sen. Nonparametric least squares estimation of a multivariate convex regression function. Annals of Statistics, 39(3):1633–1657, 2011.

- Shafieezadeh-Abadeh et al. [2019] Soroosh Shafieezadeh-Abadeh, Daniel Kuhn, and Peyman Mohajerin Esfahani. Regularization via mass transportation. Journal of Machine Learning Research, 20(103):1–68, 2019.

- Shapiro [2001] Alexander Shapiro. On duality theory of conic linear problems. In Semi-Infinite Programming, pages 135–165. Springer, 2001.

- Shapiro et al. [2021] Alexander Shapiro, Darinka Dentcheva, and Andrzej Ruszczynski. Lectures on Stochastic Programming: Modeling and Theory. SIAM, 2021.

- Singham [2019] Dashi I Singham. Sample average approximation for the continuous type principal-agent problem. European Journal of Operational Research, 275(3):1050–1057, 2019.

- Singham and Cai [2017] Dashi I Singham and Wenbo Cai. Sample average approximations for the continuous type principal-agent problem: An example. In 2017 Winter Simulation Conference (WSC), pages 2010–2020. IEEE, 2017.

- Singham and Lam [2020] Dashi I Singham and Henry Lam. Sample average approximation for functional decisions under shape constraints. In 2020 Winter Simulation Conference (WSC), pages 2791–2799. IEEE, 2020.

- Smith [1995] James E Smith. Generalized Chebychev inequalities: Theory and applications in decision analysis. Operations Research, 43(5):807–825, 1995.

- Van der Vaart [2000] Aad W Van der Vaart. Asymptotic Statistics, volume 3. Cambridge University Press, 2000.

- van der Vaart and Wellner [1996] AW van der Vaart and J. Wellner. Weak Convergence and Empirical Processes: With Applications to Statistics. Springer Series in Statistics. Springer, 1996.

- Van Parys et al. [2016] Bart PG Van Parys, Paul J Goulart, and Daniel Kuhn. Generalized Gauss inequalities via semidefinite programming. Mathematical Programming, 156(1-2):271–302, 2016.

- Wiesemann et al. [2014] Wolfram Wiesemann, Daniel Kuhn, and Melvyn Sim. Distributionally robust convex optimization. Operations Research, 62(6):1358–1376, 2014.

- Xie [2021] Weijun Xie. On distributionally robust chance constrained programs with Wasserstein distance. Mathematical Programming, 186(1):115–155, 2021.

- Xie and Ahmed [2018] Weijun Xie and Shabbir Ahmed. On deterministic reformulations of distributionally robust joint chance constrained optimization problems. SIAM Journal on Optimization, 28(2):1151–1182, 2018.

- Zhang et al. [2018] Yiling Zhang, Ruiwei Jiang, and Siqian Shen. Ambiguous chance-constrained binary programs under mean-covariance information. SIAM Journal on Optimization, 28(4):2922–2944, 2018.

- Zhou et al. [2022] Zihe Zhou, Harsha Honnappa, and Raghu Pasupathy. Sample average approximation over function spaces: Statistical consistency and rate of convergence. In 2022 Winter Simulation Conference (WSC), pages 61–72. IEEE, 2022.

Appendix A Measurability

We employ the outer and inner probability and expectation to handle the measurability issue (see van der Vaart and Wellner [1996] Section 1.2). Let be a probability space. The outer probability and the inner probability of an arbitrary subset are defined as

The inner and outer probability are related via , where denotes the complement of . Similarly, for an arbitrary map , its outer expectation is defined as

The inner expectation can be defined similarly. For the map , there is a measurable map (unique up to a null set) called the minimal measurable majorant of satisfying (i) ; (ii) a.s. for any measurable map with a.s.; (iii) provided exists. The existence of can be found in van der Vaart and Wellner [1996] Lemma 1.2.1. It also satisfies for any .

We next introduce stochastic convergence under the outer expectation (van der Vaart and Wellner [1996] Section 1.9). Let be arbitrary maps. We say converges outer almost surely to , denoted , if a.s., where is the minimal measurable majorant of . We say converges in outer probability to , denoted , if in probability, which is equivalent to for any . Clearly, implies .

Appendix B Proofs

Proof of Theorem 1..

We first prove weak duality . For any feasible solution of the problem () (3), we have

| (13) |

Thus, for any , we have

Taking the supremum over the feasible solutions of the problem () (3), we have

Then we take the infimum over on the right hand side and get .

Next, we prove strong duality. Notice that if , then weak duality implies strong duality. Also, must hold because Assumption 3 ensures the existence of a feasible solution. So in the following, we assume . We will prove . We define a set

By Assumption 2, we can see is a convex set. Note that is a boundary point of . By the supporting hyperplane theorem, there exists in such that

| (14) |

We claim that (component-wise) and . First, if doesn’t hold, we assume without loss of generality that . We choose any feasible solution satisfying (13), then by setting , (with ), we have . Letting , we can see , which contradicts (14). Second, if doesn’t hold, we have either or . If , we know that for . Letting , we obtain again, which contradicts (14). If , we consider two cases depending on : or with at least one positive component. If and , we must have because . By Assumption 3, we know that is an interior point of

Thus, there exists s.t. . In this case (recall that ), we have but , which contradicts (14). If and with at least one positive component, by Assumption 3, there exists s.t.

Therefore, we have (by ) but

which contradicts (14). Therefore, we must have .

Proof of Theorem 2..

We notice that the proof of Theorem 1 does not rely on a specific choice of . Therefore, to prove Theorem 2, it suffices to verify the empirical version of Assumptions 1-3 where the distribution is replaced by the empirical distribution of . Since the empirical version of Assumptions 1-2 automatically holds, weak duality automatically holds. To prove strong duality, it remains to show the empirical version of Assumption 3 holds with probability approaching .

We first assume that in the distributional optimization formulation, , i.e., both the equality and inequality moment constraints exist. The challenge will be to show there exists a feasible solution meeting the equality constraints. By Assumption 3, there exists a small s.t.

and the different vectors are contained in the set

say, they are achieved by . We define and . Now we consider the event

By the strong law of large numbers, for almost all samples , happens when is large enough. In other words,

| (15) |

Next, we will show on the event , the empirical version of Assumption 3 holds. By the last requirement in and the choice of , we know that there is one and only one vector

among in each orthant with respect to the center . Additionally, they are all outside the hyperrectangle , that is,

Consequently, we know that

| (16) | |||

where the last inclusion is due to the convexity in Assumption 2. This proves the interior point condition in the empirical version of Assumption 3. Then it remains to show the existence of a strictly feasible solution to the IW-SAA problem. We define

According to the second requirement in , , which implies . By (16), there exists a convex combination such that

We claim that the convex combination is a strictly feasible solution for the IW-SAA problem. First, it satisfies the inequality constraints since for

by the first and third requirements in and the definition of . It also satisfies the equality constraints since for

Hence, is a strictly feasible solution for the IW-SAA problem, which proves the empirical version of Assumption 3. Therefore, the above argument and the proof of Theorem 1 shows the inclusion . Then we deduce that

which implies (because may be non-measurable) by (15). Finally, by the weak law of large numbers, which implies .

If there is no inequality constraint in the distributional optimization formulation, the above argument still holds by removing the part regarding the inequality constraint. If there is no equality constraint in the distributional optimization formulation, then is a strictly feasible solution (when is large) for the IW-SAA problem by the law of large numbers, which again proves the empirical version of Assumption 3. This completes our proof. ∎

Now we prove Theorem 3. By strong duality, it suffices to consider and . However, the outer minimization over in () and () is conducted on a unbounded region on which the uniform law of large numbers usually fails. Thus, we first establish the following technical lemma which ensures the minimization over can be conducted on a compact set under certain conditions and thus quantifies the difference between two Lagrangian dual problems.

Lemma 2.

Let and be two functions defined on and taking values in , where is an index set with arbitrary cardinality and . Assume that (i) with , (ii) s.t. for any , there exists an index satisfying and . (iii) and , where

Then we have and

where is defined as

and

Proof of Lemma 2..

The proof includes two steps. The first step is to bound and when the infimum is taken over compact sets of . The second step is to show the optimization problem can be restricted over a compact set.

For any , we have , i.e.,

By taking the supremum over , we have

| (17) |

We can see the inequality (17) holds even if or (actually it tells us ). Applying (17) to , we get

| (18) |

When , (17) implies that

| (19) |

By assumption (i) in this lemma, we know that . Then it follows from (19) that

Now, let’s find the lower bound for when is large. For any , consider , where is the sign function. By assumption (ii), there exists an index satisfying and . Thus, we have

| (20) |

where

| (21) |

Combining the bounds in (18) and (21), we can see if satisfies

then . Thus, by choosing

we will get

where the first equality follows from assumption (i) of this lemma and the second one follows from when . Moreover, (19) gives us a bound for the difference of the optimal values:

Finally, note that . This concludes our proof. ∎

Proof of Theorem 3..

We make use of Lemma 2 by taking

By Assumption 5, have integrable envelopes (say ) and thus is a real-valued convex function. Moreover, is a Lipschitz continuous function by the triangular inequality . Now we verify the conditions (i)-(iii) in Lemma 2.

We first verify condition (ii). By Assumption 3, there exists a feasible function s.t.

Additionally, is an interior point of the following set

Therefore, s.t. for any , there exists with . So we can choose small enough s.t. for any , the th component of the vector

| (22) |

is negative for and equal to for . Additionally, since is a convex set. This proves condition (ii).

Next, we verify condition (i). As in the statement of Lemma 2, we define

Then according to (20), we have , which implies . By strong duality and Assumption 4, we know that , which implies the existence of a minimizer due to and continuity of .

Finally, we verify condition (iii) along with the main argument for this proposition. Notice that under our choice of and , we actually have

We consider the event

On this event, when is large enough, we have and , which implies condition (iii) in Lemma 2. Then by Lemma 2, we obtain that, on the above event and for large enough,

| (23) |

Since the quantity in (23) is measurable and converges to , we obtain that . Hence, we have proved that

Finally, we notice that

where we make use of almost surely by Assumption 5 and the strong duality result in Theorem 2. Therefore, we obtain almost surely, i.e., ∎

Proof of Theorem 4..

We follow the proof of Theorem 3 but modify the argument starting from the verification of condition (iii) of Lemma 2. We define the set . Assumption 5 and Theorem 2 ensure as . Now condition (iii) holds on . By Lemma 2, the following holds on :

where in Lemma 2 is upper bounded by

So on , we will have

i.e.,

Now, for any , we choose , where is the constant in Assumption 6. Then we can see

By taking the limsup, we finally get

∎

Proof of Lemma 1..

We first consider the verification of Assumption 5. It suffices to show each has an integrable envelope and for any by van der Vaart and Wellner [1996] Theorem 2.4.1. Suppose (7) holds. Then has an integrable envelope . Next, we show for any . We take -brackets that cover . Without loss of generality, we can assume . For each , s.t. . Let and be the positive and negative part of , i.e., and . Then we can see

Therefore, forms a cover of . Moreover, they satisfy

So they are -brackets for , which proves