Information Aggregation with Costly Information Acquisition111We would like to thank Emir Kamenica, Anastasios Karantounias, Ehud Lehrer and participants at Glasgow University, the MIMA Workshop in Macroeconomic Theory at Warwick, the CEPR Workshop in Turin, Durham York Workshop in Economic Theory, the Durham Economic Theory Conference, EWMES2023 in Manchester, and SAET2023 in Paris. This research is funded under ESRC grant ES/V004425/1.

Abstract

We study information aggregation in a dynamic trading model with partially informed traders. Ostrovsky (2012) showed that ‘separable’ securities aggregate information in all equilibria, however, separability is not robust to small changes in the traders’ private information. To remedy this problem, we enhance the model by allowing traders to acquire signals with cost , in every period. We show that ‘ separable securities’ aggregate information and, as the cost decreases, nearly all securities become separable, irrespective of the traders’ initial private information. Moreover, the switch to separability happens not gradually but discontinuously, hence even a small decrease in costs can result in a security aggregating information. Finally, even with myopic traders, cheaper information may accelerate or decelerate information aggregation for all but Arrow-Debreu securities.

JEL: C91, D82, D83, D84, G14, G41

Keywords: Information Aggregation, Information Acquisition, Financial Markets, Prediction Markets.

1 Introduction

The question of whether financial markets reveal and aggregate the private information of traders has been studied at least since Hayek (1945). Ostrovsky (2012) provides a strong result, showing that information gets aggregated in all Nash equilibria, as long as the traded securities are separable and trading takes place for infinitely many periods. However, separability is not robust to small changes in the composition of the market or to the traders’ information structure. As a result, a market designer who does not know who participates or what is their information structure, cannot be sure that the equilibrium price is a good predictor of the security’s value.

In this paper, we examine whether the ability to acquire costly signals during trading can make markets more efficient at aggregating information. This question becomes more relevant as the continuous improvements in information technology have created an abundance of available information, which is now cheaper than ever to acquire, analyze, and act upon.444For example, recent advances in generative AI tools such as ChatGPT could add considerable value for investors with information processing constraints (Kim et al., 2023) and assist in picking stocks (Pelster and Val, 2023).

We use the dynamic trading model of Ostrovsky (2012) with infinitely many periods and payoffs given by the Market Scoring Rule (MSR) (Hanson, 2003, 2007). We first characterize the class of securities which are always separable, irrespective of who trades and what is their information structure. This class is very small and uninformative, as it only contains the Arrow-Debreu (A-D) security, which pays at some state and in all other states, and the security that specifies three payoffs: the largest is paid in one state of the world, the lowest in another, and the middle in all other states.555These securities are not very informative because the A-D can only predict whether one state has occurred or not, whereas the other security can only predict whether two states have occurred or not. Note that combining more than one A-D security to construct a composite and more informative security will not solve this issue, because it will be non-separable for some information structures. For any other security, there is a market (information structure and prior) at which there is no information aggregation so that the security’s price does not converge to its true value. This means that information may not aggregate in ‘most’ markets.

Does the availability of cheap information alleviate this problem? To study this question, we enhance the model of Ostrovsky (2012) by enabling traders to buy a costly signal structure in each period, before trading. We allow for a large class of information cost functions , including the Shannon entropy.

We define the class of separable securities and Theorem 6 shows that they are necessary and sufficient for information aggregation, when the cost of information is , thus generalising Ostrovsky (2012). As information acquisition costs decrease, the securities that eventually become separable, and therefore aggregate information in all equilibria and for all information structures, have a very simple structure: they specify a different payoff at each state. This class of securities with unique values is generic. Hence, the main message of the paper is that the availability of cheap information makes ‘most’ markets aggregate information.666This result is also supported by empirical evidence. (Farboodi et al., 2022) show, using a structural model, that as the value of a firm’s data grows, which is equivalent in our model to a decrease in the cost of information acquisition, then the information content of the price of the firm’s stock increases as well. Surprisingly, there is also a small class of securities, which Theorem 3 characterises, that never become separable for all information structures, and therefore may fail information aggregation, even when the cost converges to zero. Such a security specifies the same payoff in two states and, in two other states, it pays either higher or lower than .

If we can decrease the cost of information as much as we want, do we even need markets to aggregate information through prices? Each trader could buy the necessary signals and then bid very close to the true value. We argue that this intuition is incorrect, because markets become even more important in an environment with information acquisition. As cost decreases, a security switches discontinuously from non-separable to separable, hence even a slight reduction can enable a market to aggregate information. This is in contrast to the average of the traders’ opinions after receiving the information, or a poll, because its predictive accuracy improves smoothly as costs decrease. Hence, the availability of cheap information leverages the value of the markets, enabling them to aggregate information long before the cost goes to zero. Moreover, we show that a security is separable if and only if the market is more accurate than a poll, for all priors.

Finally, we examine whether information acquisition can make markets more efficient by aggregating information faster. We show that this is not true. Even in non-strategic environments, as long as the separable security is not A-D, information aggregation can happen both faster and slower, depending on the parameters. This implies that, as information becomes more affordable, markets could become less efficient if the underlying security is not A-D.

1.1 Literature

Our paper contributes to three strands of the literature. The first studies the inefficiency of information acquisition and its effect on information aggregation in markets.777See (Lim and Brooks, 2011) for a survey of the empirical literature on market efficiency. Pavan et al. (2022) show that traders acquire and use information inefficiently. Moreover, as the cost of information declines, traders over-invest in information acquisition and trade too much on their private information. Several experimental studies support these results and find that traders tend to over-acquire information. In addition, while information acquisition is positively correlated with market efficiency, market prices do not aggregate all private information (Kraemer et al., 2006; Page and Siemroth, 2017, 2021; Corgnet et al., 2022). Mele and Sangiorgi (2015) analyze costly information acquisition in asset markets with ambiguity-averse traders and show that when uncertainty is high enough, information acquisition decisions become strategic complements and lead to multiple equilibria. Our paper complements and differs from this literature. We find that, as the cost of information acquisition decreases, the number of securities (and therefore markets) that aggregate information increases. However, some securities are never able to aggregate information, even if the cost is almost zero. Finally, information aggregation can be delayed when information acquisition is cheap, thus introducing another element of inefficiency.

The second strand looks at the information aggregation properties of financial and, in particular, prediction markets.888See Wolfers and Zitzewitz (2004) for an early overview of the literature. DeMarzo and Skiadas (1998, 1999) first introduced the notion of separable securities. Ostrovsky (2012) and Chen et al. (2012) show that in a market with dynamically consistent traders, separable securities are both necessary and sufficient for information aggregation. Dimitrov and Sami (2008) and Chen et al. (2010) examine information aggregation by varying the assumptions regarding the traders’ information structure. Galanis et al. (2024) study information aggregation with ambiguity-averse traders, whereas Galanis and Kotronis (2021) allow for boundedly rational traders who are unaware of some contingencies.999Unawareness and ambiguity aversion generate dynamic inconsistency and negative value of information, which are partly responsible for no information aggregation. See (Galanis (2011, 2013)) for a model of unawareness and Galanis (2021) for a connection between dynamic inconsistency and the negative value of information. We contribute to this literature by allowing traders to acquire costly signals at every period and we characterize the separable securities which aggregate information.

Finally, the paper contributes to the growing literature on the implications of rational inattention, originated by Sims (2003). We build on the results of (Denti, 2022; Caplin et al., 2019; Matějka and McKay, 2015; Caplin and Dean, 2015) to characterize the traders’ optimal behavior in a game with infinitely many periods, where traders have posterior-separable cost functions and can buy signals in every period. We show that, in any Nash equilibrium, almost any security aggregates information for a sufficiently small marginal cost of information.101010Atakan and Ekmekci (2023) show that common value auctions with uninformed bidders who can acquire costly signals aggregate information as long as the minimum cost-accuracy ratio is equal to zero. See also Maćkowiak et al. (2023) for a recent survey of the literature on rational inattention.

We conclude by motivating our choice of the MSR model. First, in the MSR model, there are no noise traders and no strategic market makers, hence the issue of information aggregation is not intertwined with that of information revelation, as in Kyle (1985). Unlike the MSR, in Kyle (1985) it is not always the case that the price will converge to the true value of the security, even if there is only one trader and therefore information aggregation is achieved by default. Second, a prediction market with the MSR can be reinterpreted as an inventory-based market with a market maker who continuously adjusts the price of the securities depending on the orders she receives.111111See Ostrovsky (2012) and Galanis et al. (2024) for examples. The advantage of the MSR over more well-known market mechanisms, such as the continuous double auction, is that an agent can make her prediction/trade without waiting for another agent to take the opposite side, or submit a limit order and wait for it to be filled. This feature makes it an attractive mechanism for markets with relatively few participants who do not trade daily, or in markets with automated market makers.121212Automated market makers are widely used in Decentralized Finance, see Schlegel et al. (2022) for an axiomatization of the logarithmic MSR. MSR-based prediction markets have been used widely, for example, by firms such as Ford, Google, General Electric, and Chevron (see Ostrovsky (2012), Cowgill and Zitzewitz (2015)) as well as governments, for example, in the UK and the Czech Republic (The Economist (2021)).

2 The Model

2.1 Preliminaries

Uncertainty is described by a finite state space and the set of traders is denoted . Trader ’s initial private information is represented by partition of . Let be a partition element of that contains , so that . When the true state is , Trader considers all states in to be possible. We assume that the join (the coarsest common refinement) of partitions consists of singleton sets so that for all , which means that the traders’ pooled information always reveals the true state.131313This assumption is also made by Ostrovsky (2012) and it is without loss of generality because if the conjunction of the traders’ private information does not reveal the state, we cannot expect that trading the security will reveal it. This implies that, for any two states , there exists Trader such that . Let be the collection of all information structures where has at least three states and for all . Traders have a full-support common prior over and they are risk-neutral.

2.2 Trading environment

Trading is organized as follows. At time , nature selects a state and the uninformed market maker makes a prediction about the value of security . At time , Trader 1 makes a revised prediction , at trader 2 makes his prediction, and so on. At time , Trader 1 makes another prediction , and the whole process repeats until time . All predictions are observed by all traders. Each prediction is required to be within the set . At some time the true value of the security is revealed.

The traders’ payoffs are computed using a scoring rule, , where is the true value of the security and is a prediction. A scoring rule is proper if, for any probability measure and any random variable , the expectation of is maximized at . It is strictly proper if is unique. We focus on continuous strictly proper scoring rules. Examples are the quadratic, where , and the logarithmic, where with .

Under the market scoring rule (MSR) (McKelvey and Page (1990), Hanson (2003, 2007)), a trader is paid for each revision he makes. In particular, his payoff, from announcing at , is , where is the previous announcement and is the true value of the security. For all proper scoring rules, as converges to , converges to 0. Moreover, if is further away from than is from , then is strictly positive. We then say that the trader “buys out” the previous trader’s prediction. If he repeats the previous announcement, his period payoff is zero. We say that prior is non-degenerate given security if it does not assign probability 1 to a unique value of .

2.3 Two trading settings

We examine trading in two settings. In the myopic, or non-strategic, setting, each trader does not care about future payoffs when acquiring information and making an announcement. We denote this setting by , where is the set of players, is a strictly proper scoring rule, is the market maker’s initial announcement at time , is the common prior, is the set of possible announcements.

The strategic setting is studied in Section 4.4. Following Dimitrov and Sami (2008), we focus on the discounted MSR, which specifies that the payment at is , where is the common discount factor. The total payoff of each trader is the sum of all payments for revisions. We denote this setting by . In Section 4, we will add function in the specification of the game, which denotes the cost of statistical experiments.

2.4 Information aggregation

We say that information is aggregated if the traders’ predictions converge to the intrinsic value of security , for all . For every , let be the announcement of the trader who moves in period . The announcement depends on because traders have different private information across states. Because is a sequence of random variables, we need a probabilistic version of convergence.

Definition 1.

Under a profile of strategies in or , information aggregates if sequence converges in probability to random variable .

2.5 Example

Consider the following Example, which illustrates aspects of our model.

Example 1.

The state space is , the security is , and there are two myopic traders with common prior . Trader 1’s partition is and Trader 2’s is .

As traders are myopic, under the MSR they take turns in announcing their expected value of . Suppose that the true state is and traders cannot acquire costly signals. In period 1, Trader 1 with conditional beliefs will announce . The same announcement would be made by Trader 1 in all states and, thus, no information is transmitted to Trader 2. In period 2, Trader 2 also makes the same announcement at and, furthermore, the same announcement would be made in all states. Hence, no information is transmitted to Trader 1. Because the two traders agree on the announcement, there is no information updating and the process ends. We say that there is no information aggregation at because the final announcement is not equal to the intrinsic value of at , which is 0.141414Information aggregation fails in the first round in this example and no-one updates from . In general, traders could start from a different common prior , and after several rounds of updating they could update to some other posterior , at which there is no information aggregation.

Suppose now that traders are able to acquire a noisy signal about the value of the security before making their announcement. For instance, Trader 1 can acquire a statistical experiment that generates a signal , given each state, with probabilities and .

At state , Trader 1’s prior belief is and, after receiving signal , his posterior belief is . He then announces the expected value of , which is . Trader 2 considers states and to be possible. The public announcement of reveals to Trader 2 that the true state is . The reason is that, irrespective of whether Trader 1 received signal or not, his posteriors at are and he would have announced . As a result, Trader 2 announces 0 in the second round and the game ends. Note that the final price is equal to the intrinsic value of at , hence information aggregation does occur. In summary, the ability to acquire extra signals transforms from non-separable to separable, enabling information aggregation.

We make two observations. First, we have abstracted from the cost of acquiring an experiment. Each trader will acquire the signal structure only if the expected benefit from making a better prediction outweighs the cost. See Section 4 for the formal treatment. Second, Trader 2 free-rides on Trader 1 buying the signal. By moving the price from to , he books a profit, without paying the cost of a signal. This example illustrates that the ability to acquire information can turn a non-separable security into a separable.

Security is separable if whenever there is agreement about the expected value of , given a prior that does not put probability 1 to only one value of , then at least one (myopic) trader finds it profitable to acquire information. It is therefore a generalization of separability, which requires that such a prior does not exist. In Section 4.3, we formally define the notion of separability and Theorem 6 shows that this class of securities characterizes information aggregation when the cost is . A natural question is whether all securities eventually become separable, for sufficiently low cost of information. Surprisingly, Theorem 3 shows that there is a very small class of securities that never become separable, even if the cost is negligible but strictly positive. We, therefore, have a discontinuity as costs converge to zero.

3 No Information Acquisition

In an environment without information acquisition, Ostrovsky (2012) showed that separable securities are necessary and sufficient for aggregating information. In this section, we first define the class of separable securities. We then show that the class of always separable securities, which are separable for all information structures, is small and uninformative.

3.1 Separable Securities

Consider the following example, which appears in similar form in Geanakoplos and Polemarchakis (1982) and in Example 1 of Ostrovsky (2012).

Example 2.

The state space is , the security is , and there are two traders with common prior . Trader 1’s partition is and Trader 2’s is .

At all states, it is common knowledge that both traders agree that the expected value of is 0.5, hence there can be no more learning from further announcements. However, it is also common knowledge that the intrinsic value of is not 0.5; it is either 0 or 1, which implies that there is no information aggregation. When both these conditions are satisfied for some prior and some partitions, the security is non-separable.

Definition 2.

A security is called non-separable under information structure if there exists probability and value such that:

-

for some ,

-

for all and .

We then say that security is non-separable at . Otherwise, it is called separable.

A security is non-separable if, for some prior and at all states in its support, all traders’ expected value of is , yet there is uncertainty about the value of . If for any prior at least one condition is violated, then the security is separable. Note that separability (and non-separability) is a property that depends on the information structure . For a different , a security may switch from separable to non-separable and vice-versa.

Theorem (Ostrovsky (2012)).

Fix information structure . Then:

-

•

If security is separable under , then in any Nash equilibrium of game , information gets aggregated.

-

•

If security is non-separable under , then there exists prior such that for all , , , , and , there exists a Perfect Bayesian equilibrium of the corresponding game in which information does not get aggregated.

This is a powerful result because it applies to all equilibria and irrespective of the market power of traders. Separable securities can be very useful for a market designer because they always aggregate information, hence the price can predict whether an event has occurred or not. However, separability depends on the information structure . If the market maker does not know , he cannot be certain that the equilibrium price is a good predictor of the intrinsic value of the security.

3.2 Always Separable Securities

The dependence of separability on is not a problem if the security is separable for all information structures. In this section, we characterize the securities that have this property, so that information aggregation does not depend on who trades or what is their private information.

Unfortunately, the following Proposition shows that this class is very small and uninformative. It consists of just three types of securities. The first is the constant, which pays the same at all states. The second is the Arrow-Debreu (A-D), which pays at some state and at all other states. The third pays at some state , at , and at all other states, where .

proposition The only non-constant securities that are separable for all information structures in are the A-D and the security that is of the following form. There are values such that and for two states , and for all .

We start by restating a useful characterization of separable securities by Ostrovsky (2012). It specifies that is separable if and only if, for any possible announcement , we can find numbers , for each and , such that the sum over all traders has the same sign as the difference of . Intuitively, for any and at each , all traders “vote” and the sign of the sum of the votes has to agree with the sign of the difference between the value of the security and .

Proposition 1 (Ostrovsky (2012)).

Security is separable under partition structure if and only if, for every , there exist functions for such that, for every state with ,

If has up to three states, then all securities are of the two types that we have described or the uninteresting case of a constant security. Hence, without loss of generality, we fix a state space with at least four states and a security . If is constant, it is trivially separable. Ostrovsky (2012) shows that an A-D security is always separable.

We now show that is always separable if it is of the following form. Suppose there are such that and for two states , whereas for all .151515Our proof for this type of security also applies to an A-D security. Ostrovsky (2012) used Corollary 1 to show that an A-D security is always separable, however, we cannot use it for this type of security. Using Proposition 1, we need to show that for every , there exist functions for such that, for every state with ,

| (1) |

If , then condition (1) is satisfied by setting for all and . Similarly, if , we set for all and . Suppose that . For all , set and (1) is satisfied for . For all with , set , where is the number of agents. Because of our assumption that the join of all partitions consists of singleton sets, we have that for each , there exists such that . This implies that if , we also have and (1) is satisfied for . Using a symmetric argument, we can show that (1) is satisfied for , by setting and for with , for all . By applying Proposition 1, security is always separable.

Suppose that is not of the three aforementioned types. Then, we can find four distinct states where assigns values . For simplicity, we refer to the state with value as state and similarly for , and .

We will show that is non-separable for an information structure in with two agents. The partition of Trader 1 is for these four states, whereas for any other state, we have . For Trader 2 it is and for any other state we have . Hence, the information structure is in .

To show that is non-separable, it is enough to find a prior with support on such that, for some ,

-

for some ,

-

for all and .

Let be 1’s probability of state conditional on , whereas is 1’s probability of state conditional on . Let be 2’s probability of state conditional on , whereas is 2’s probability of state conditional on . Condition (ii) then translates to the following equations

| (2) |

The posteriors of the two agents can be derived by a common prior if the following conditions hold:

| (3) |

where is the prior probability of and is the prior probability of .

When , the system (2 - 3) has the following solution:

These posteriors uniquely define the respective prior probabilities.

All three types of securities are ‘uninformative’. Even when there is information aggregation and the price of always converges to the true value at state , this only reveals that either , , or neither, have occurred. In other words, the price of does not reveal information about most events in . In contrast, the most informative security pays differently across all states. If there is information aggregation, then reveals whether any event in has occurred or not. However, because is not always separable, we know that for some information structure , information does not aggregate.

4 Information Acquisition

In this section, we show how the problem of non-separability and no information aggregation can be alleviated if we enhance the model of Ostrovsky (2012), by allowing traders to acquire information in every period where they make an announcement. We define a new class of securities, called separable, where is the cost of acquiring information. Our first main result is Theorem 3, which characterizes the securities that are non-separable for some information structure but for all . Our second main result, Theorem 6, shows that separable securities characterize information aggregation, in both strategic and non-strategic settings, thus generalizing Ostrovsky (2012) in an environment with information acquisition.

4.1 Cost of Information

We first formalise the cost of acquiring information. For ease of exposition, many of the technical details are relegated to Section A.1 in the Appendix.

Let be a Polish space of possible signals with Borel -algebra . Let be the set of Borel probabilities on . Following Blackwell (1951), we model the acquisition of information using statistical experiments. A statistical experiment is a function from states into probabilities on signals, . An experiment is bounded if it does not definitely rule out any state. Let be the collection of all experiments and be the collection of all bounded experiments.

Given a prior belief , a statistical experiment induces via Bayesian updating a probability distribution over posteriors, or random posterior, . Let be the probability of posterior , be the set of all random posteriors that can be generated by some experiment , and . Note that if and only if .

A cost on experiments is a map , where is Borel measurable for each prior . The cost generates a cost structure on random posteriors, where is the unit cost of information and maps elements of , the set of all priors and all posterior distributions that can be generated by some experiment , to the extended real line.

For Theorem 3 and Proposition 2, we assume that it is prohibitively costly to acquire an unbounded experiment.

Assumption 1.

If , then .

If all unbounded experiments have infinite cost, then generating a random posterior with support on a posterior , which assigns probability 0 to a state , is infinitely costly.

A widely used class of functions is the posterior-separable cost functions (Caplin et al. (2022)).

Definition 3.

A cost of information function is posterior-separable if, given and any Bayes-consistent posteriors ,

for some function which is strictly convex and continuous in , on and .

An example of a posterior-separable cost function that satisfies Assumption 1 is the Shannon cost function,

We have described two ways of representing the cost of information acquisition. The first is in terms of costly statistical experiments, whereas the second is in terms of costly random posteriors. There is a growing literature that examines the connection between the two approaches. Bloedel and Zhong (2020) and Hébert and Woodford (2021, 2023) show how costly statistical experiments, with a function that depends both on the agent’s prior and the experiment, can generate uniformly posterior-separable cost functions for random posteriors. Denti et al. (2022), however, restrict to depend only on the experiment and show that uniformly posterior-separable cost functions cannot be generated.

We do not take a stance on which representation is the most suitable. Our results do not require any specific functional forms, such as posterior separability, however, we adopt this framework for most of the paper because it is the most well-known. When we define the game in Section 4.4, we use the standard framework of costly statistical experiments with function .

4.2 The myopic problem

Suppose that it is Trader ’s at time turn to make an announcement. Having observed all previous announcements and using the public information that is revealed, an outside observer updates the common prior to a belief over . If the true state is , then Trader ’s private information is and his posterior belief is the Bayesian update of , denoted . In other words, he updates using both his private information and the public information revealed by previous announcements.

His myopic problem consists of buying a random posterior at cost , so that when his posterior beliefs are , he optimally announces because the scoring rule is proper. The optimal solves the problem

| (4) |

where is the unit cost of information and is the previous announcement.

In the standard model of Ostrovsky (2012), without information acquisition, the previous announcement does not influence the myopic best announcement because the scoring rule is proper. The same is true here, where we allow for information acquisition.171717Interestingly, with ambiguity averse preferences, the myopic best depends on the previous announcement, as shown in Galanis et al. (2024). To see this, note that we can rewrite the expression in the parenthesis as

hence the previous announcement does not influence the choice of or the announcement.

Note that the trader can always receive a payoff of 0 by just repeating the previous announcement and not acquiring any new information. If his payoff at (4) is smaller or equal to 0 for all , we say that he does not prefer to acquire information at . If, given a common prior , no Trader prefers to acquire information at any state , we say that there is no information acquisition for security .

Definition 4.

There is no information acquisition for security , given prior and previous announcement , cost structure and information structure , if for all states , all traders , and all ,

Otherwise, there is information acquisition.

4.3 Separable Securities

The result of Proposition 3.2, that very few securities are always separable, indicates that ‘most’ markets may not aggregate information. A natural question is whether the possibility of acquiring information fixes this problem. Intuitively, a non-separable security may still aggregate information if, whenever everyone makes the same announcement, at least one trader finds it profitable to acquire more information, thus changing his posterior and his announcement.

In this section, we define the class of separable securities, where is the cost of information acquisition. In the next section, we show that they are necessary and sufficient for information aggregation, thus generalising the main result of Ostrovsky (2012).

We say that security is non-separable given an information structure and a cost structure if there is a prior such that no one is acquiring any information, yet the security is non-separable at .

Definition 5.

Security is non-separable given an information structure and cost structure , if there exists prior such that

-

•

Security is non-separable at ,

-

•

There is no information acquisition for given .

Otherwise, security X is separable.

Recall that a non-separable security is non-separable for at least one , whereas a separable security is separable for all . If security is separable, then for each there are two cases. Either is separable at , or is non-separable at but there is information acquisition.

We make the following remarks. First, separability implies separability, for all , because there does not exist a prior at which the security is non-separable. Second, non-separability implies non-separability for some , because for a high enough marginal cost , no trader will acquire any information.

Remark 1.

If security is separable given an information structure , then it is also separable for any cost structure .

Remark 2.

If security is non-separable given an information structure , then for any cost function it is non-separable for some marginal cost of information .

Note that if is non-separable, then there is a for which there is no information acquisition and is non-separable at . If we increase the marginal cost to , then there is still no information acquisition for , hence is non-separable. Conversely, if is separable, it is separable for all for which there is no information acquisition. If we decrease the marginal cost to , then the set of priors for which there is no information acquisition will shrink and therefore will be separable for all . We, therefore, have the following remark.

Remark 3.

If is non-separable (separable), then it is non-separable (separable) for all ().

It would be natural to expect that, for a sufficiently low marginal cost , any security eventually becomes separable. But this is not true. Recall Example 2 with state space , security , and two traders with the following information structure. Trader 1’s partition is and Trader 2’s is . With a uniform prior, all traders would agree that the expected value of is 0.5, at all states, hence the security is non-separable.

Consider now prior , where . Given any , each trader’s expected value of at all states is . As converges to 0, we can always specify that is sufficiently close to , so that no trader is willing to buy a signal, because this will move their expected value of from to , for small enough , hence the expected benefit is lower than . Because there is no information acquisition and all traders agree on the expected value, security is non-separable for all .

Note that this result requires Assumption 1, which specifies that it is impossible to buy an experiment that reveals the true state with certainty.181818It is interesting to note that the incompatibility of the vector with information aggregation is met in other settings as well. In the model of DeGroot (1974), agents update their beliefs naively, by looking at their immediate neighbours, according to a fixed network. If the network is represented by a periodic matrix, such as , then beliefs do not converge (Golub and Jackson (2010)). Moreover, all traders agree, at some state , that at least two values are possible, 0 and 1. Proposition 2 in the Appendix shows that this condition is necessary for a security to be non-separable for all and a specific information structure. Additionally, it specifies a second, independent condition, which is an extension of Theorem 7 in Ostrovsky (2012), a dual characterisation of separability.

However, what if we do not know the information structure of traders? The following Theorem shows that security is non-separable given some and for all , if and only if there are four states at which pays , where either or .

theorem Suppose that has at least four states. Under Assumption 1, the following are equivalent:

-

•

is non-separable given some and for all ,

-

•

pays in four states, where either or .

Suppose has at least four states and let , where pays , with either or . What pays outside is irrelevant, because we will only consider priors that have full support on , in order to show that is non-separable for all . Consider two traders with the following information structure on . Trader 1’s partition is and Trader 2’s is . We need to show that for any , is non-separable. It is enough to show that, as the marginal cost converges to 0, there is always a common prior on such that no trader acquires any information and is non-separable at .

Consider prior , where . We specify such that, given any , each trader’s expected value of is the same at all states. In the following equation, the left hand-side computes Trader 1’s expected value of at and Trader 2’s at , whereas the right hand-side computes Trader 1’s expected value at Trader 2’s at :

There is always a solution to this equation. For example, if , we can normalise to and we have that

Given this normalisation, the expected value of at all states and for all traders is . Fix any marginal cost , which may be very close to 0. We can then choose very close to 0.5 (and corresponding ) such that is very close to , say , assuming, without loss of generality, that , otherwise we have and the rest of the proof proceeds accordingly. By repeating the consensus announcement of and not acquiring any signals, both traders get 0 utility. Suppose that one trader wants to buy a signal structure , which, in the case of , will move his posterior expected value of from to , for some . The upper bound of his utility, net of the cost of the signal, is realised at and it is . This is positive because is closer to than the previous announcement, . However, by decreasing appropriately it can be made as small as needed, and therefore smaller than for all . This is a direct consequence of Assumption 1, which specifies that the cost gets arbitrarily high for posteriors which assign probability that is arbitrarily close to one for some state. For this result, we only need that the cost is non-decreasing. Hence, no trader will buy any signal structure and is non-separable.

For the converse, suppose is non-separable given some and for all . The second condition of Proposition 2 and the assumption in Section 2.1 that , for all , imply that there exist two states such that . Let be the set of states with . Given that has at least four states, we have the following cases.

Case 0. . Security is constant and therefore (trivially) always separable, for all information structures . This is a contradiction because we have assumed is non-separable given some and for all .

Case 1. There is either a unique , or there are exactly two states , such that . From Proposition 3.2, is always separable, for all information structures . As with Case 0, this is a contradiction.

The only other remaining case is that There exist with either , or , which concludes the proof.

A Corollary is that if security pays differently across all states, then it is separable for some , given any information structure . In other words, if information is sufficiently cheap to acquire, there are easily describable securities where information aggregation is achieved and this is robust to changes in who participates in the market and what is their private information.

Corollary 1.

If for all , then, given any , is separable for some .

This Corollary echoes the following result within the context of perfectly competitive markets, as pointed out in Laffont and Maskin (1990). As long as there are “enough prices”, so that trade can be made contingent on sufficiently many events, then the competitive equilibrium is generically separating and the function relating information to prices is invertible (Grossman (1976), Radner (1979), Allen (1981)). We could interpret Corollary 1 as a generalisation of this result, because our setting applies to all Nash equilibria, not just competitive equilibria.

We conclude this section with a classification of all securities, with respect to separability. Note that the classification does not depend on the information structure, just the payoff structure of the security.

Let be a security defined on that has at least four states. If there is such that for at least two states , let be the set of states with . Otherwise, set .

Case 0. . Security is constant and therefore (trivially) always separable, for all information structures .

Case 1. There is either a unique , so that the security is A-D, or there are exactly two states , such that . From Proposition 3.2, is always separable, for all information structures .

Case 2. There exist with either , or . From Theorem 3, is non-separable for all , for some information structure .

Case 3. , hence , for all . From Corollary 1, is separable for some , for all information structures .

It is interesting to note that, within our framework that has continuous values and finitely many states, all cases except Case 3 are of measure zero. Hence, if we were to randomly pick a security, generically we would pick one with unique values which aggregates information in all equilibria and given any information structure, as long as the cost of information is sufficiently low.

4.4 Strategic traders

We now show that separable securities characterize information aggregation in strategic settings where there cost of information acquisition is . Consider game , where is the set of players, is a strictly proper scoring rule, is the market maker’s initial announcement at time , is the common prior, is the cost of statistical experiments, is the set of possible announcements, and is the common discount rate. Let be a history of announcements and be a history of signals up to time . Denote by the collection of all histories about ’s signals up to time .

At time , Trader with belief can choose to acquire information in the form of a statistical experiment , with cost . Each experiment and belief uniquely induce a Bayesian plausible belief over posteriors, which costs . We can therefore analyse the game in terms of an information cost structure , which is generated by .

After receiving a signal of experiment and updating to a posterior in the support of , Trader makes an announcement . Let be the set of all functions from signals to announcements in . His mixed strategy at time is a measurable function

It specifies a statistical experiment and an announcement for each signal that is drawn from that experiment, given the element of his partition, the history of his past signals and everyone’s announcements up to time , and the realization of random variable , which is drawn from the uniform distribution. One such draw takes place at each time and the draws are independent of each other and of the true state .

The full state is and describes the initial uncertainty and the randomizations of the players. Let be the true value of at and let be the full state space. Denote by the collection of ’s strategies, at all times where it is his turn to make an announcement. Let be a profile of strategies. Given a strategy and state , let be the announcement of Trader , his belief, and his cost of information acquisition in period which is generated by the experiment he has chosen and his current beliefs.

Definition 6.

A strategy profile is a Nash equilibrium if, for every Trader and every alternative strategy , we have

where the expectation is taken with respect to the common prior .

We now show that separable securities characterize information aggregation when the cost structure is .202020Note that Assumption 1 is not needed for this result.

theorem Fix information structure and cost of experiments , which generates cost structure . Then:

-

•

If security is separable under , then in any Nash equilibrium of game , information gets aggregated.

-

•

If security is non-separable under , then there exists prior such that for all , , , , and , there exists a Perfect Bayesian equilibrium of the corresponding game in which information does not get aggregated.

We follow the proof of Theorem 1 in Ostrovsky (2012), which proceeds in four steps. In the first step, we show that there is a uniform lower bound on the expected profits that at least one trader can make by improving the forecast.

Let be a distribution over and be the previous announcement. Following Ostrovsky (2012), we define the instant opportunity of Trader as the highest expected payoff that he can achieve by changing the forecast from , if the state is drawn according to . The difference from Ostrovsky (2012) is that we allow the trader to acquire information before making an announcement. Let be the optimal experiment that Trader acquires at , given his beliefs . Trader ’s instant opportunity is

Let be the set of probability distributions for which there is uncertainty about security , so that there are states with , and .

Lemma 1.

If security is separable, then for every , there exist and Trader such that, for every , the instant opportunity of Trader given and is greater than .

Proof.

Fix . There are two cases. First, is separable with respect to . Then, the proof of Lemma 1 in Ostrovsky (2012) applies and we have the result. Second, is non-separable at and value , where for all and . Because is separable, there is information acquisition. This implies that for some , Trader receives a strictly positive payoff by acquiring information and changing the previous announcement . Note that the new announcement is not deterministic but depends on the optimal , so he announces with probability . From continuity, there is a small enough , so that for all previous announcements , Trader receives a strictly positive payoff of at least by acquiring information and changing the announcement. If , then Trader receives a strictly positive payoff of at least , by not acquiring any information and announcing the myopically best .212121This is true because a proper scoring rule is ‘order-sensitive’ so that the further away the previous announcement is from the true expected value , the higher the payoff is for Trader . The lowest payoff from the myopically best announcement is 0 and it is achieved when it is equal to the previous announcement (see p. 2618 in Ostrovsky (2012)). By setting , we have that at , Trader receives a strictly positive payoff of at least , for all previous announcements . For any , Trader can repeat and receive 0. Hence, the instant opportunity of given , which is the ex-ante expectation over all , is at least for all previous announcements.

∎

Steps 2-4 are identical to the proof of Ostrovsky (2012). The reason is that we only need to use the uniform lower bound that we have established in Step 1. Note that, once we fix an equilibrium strategy, the only difference from Ostrovsky (2012) is that players receive (up to) an extra signal in each period where they make an announcement.

The proof of the second part of the Theorem is similar to that of Ostrovsky (2012). Suppose that is non-separable. Then, there exist and at which there is no information acquisition and is non-separable at . In the corresponding game where the initial announcement is , no trader will find it profitable to acquire any information and their best response is to repeat , in every period and after every history, hence it is a Bayesian Nash equilibrium.

4.5 The value of the market

If the cost of information drops significantly, do we even need markets to aggregate information through prices? Each trader could buy the necessary signals and then trade. In this section, we argue that this intuition is not correct, because markets become even more important in an environment with information acquisition. The reason is that markets can aggregate information before it becomes economically viable for each trader to acquire the required information on their own.

To make this point, we compare the prediction accuracy of the market with that of a poll, where traders simultaneously make only one announcement and we compute the average.222222Note that there are many ways of improving the accuracy of a poll by aggregating announcements differently (Baron et al., 2014). In our framework, markets will always be more accurate than polls because more information is disseminated through multiple rounds of announcements, and the value of information is positive. Several papers have examined the two settings in experiments and real-life settings, and the results are mixed. Snowberg et al. (2013) argue that prediction markets are better. Berg et al. (2008) show that the Iowa Electronic Markets were more accurate than 964 polls in predicting the outcomes of five presidential elections between 1988 and 2004. Cowgill and Zitzewitz (2015) show that internal prediction markets in Google and Ford were more accurate than the predictions of professional forecasters. On the other hand, Atanasov et al. (2017); Dana et al. (2019) argue that while prediction markets are more accurate than the simple mean of forecasts from polls, the latter outperform prediction markets when forecasts are aggregated with transformation algorithms or made in teams. Camerer et al. (2016) show that markets are equally accurate with a survey in predicting the replicability of economic experiments. Recall from Section 4.4 that the full state describes the initial uncertainty and the randomizations of the players, as well as the signal realisations.

Definition 7.

For each and common prior , the prediction of the poll is the average of the myopic predictions, , where each Trader optimally obtains a random posterior and then they all announce simultaneously in the first period of the corresponding game :

The prediction of the market is the last price of .

We define the accuracy of the market given and as , and similarly for the poll, . The highest possible accuracy is 1, when . The expected accuracy of the market given is defined as , whereas for the poll it is .

Recall that a non-degenerate prior given does not assign probability 1 to a unique value of security . If the security is separable for some , then the information gets aggregated for some positive marginal cost of information, which is not true for polls. We, therefore, have the following remark.

Remark 4.

Under Assumption 1, fix an information structure and a cost of information acquisition . If security is separable, then for any non-degenerate given and for all , information gets aggregated by a market with cost , so that for all , but it is not aggregated by the poll, so that .

Proof.

We now show that separability is equivalent to the market being strictly more accurate than the poll, for all non-degenerate priors given .

proposition Suppose Assumption 1 and cost of information . Security is separable given if and only if for all non-degenerate priors given .

If is separable, then from Theorem 6 we have that information aggregates at all states and therefore . Assumption 1 implies that no trader would acquire full information, hence and .

If is non-separable, then we can find non-degenerate given for which there is no information acquisition and is non-separable at . This means that everyone agrees on the announcement at all states and the game ends in the first round. The announcement is the same for everyone, so the poll gives the same prediction as the market and .

To interpret this result, suppose we define the value of the market (with security ) to be , the minimum improvement in accuracy given all non-degenerate priors given . Then, Proposition 4 implies that is separable if and only if .

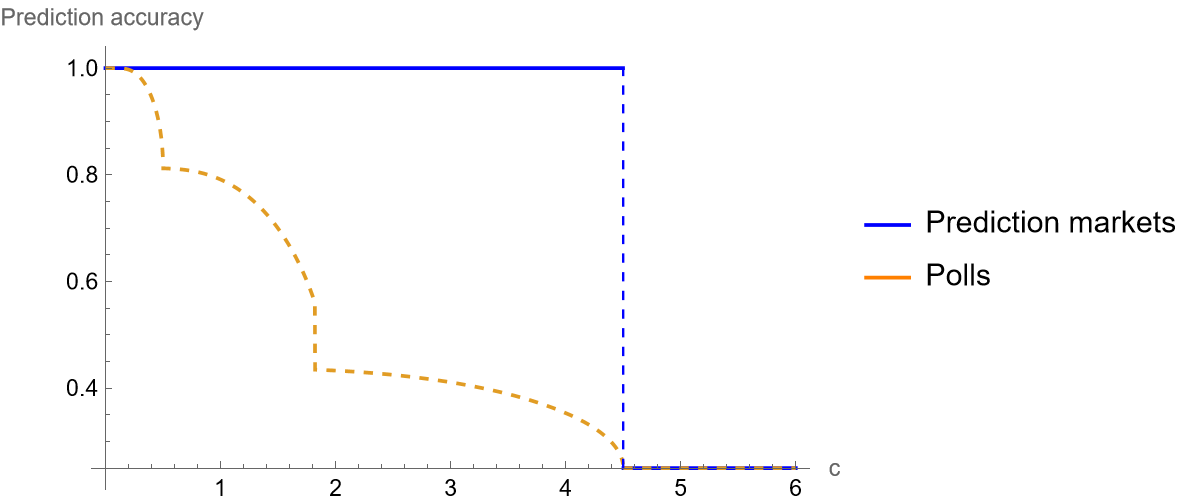

We conclude with the following example, where we show how the market compares in prediction accuracy with the poll, if we fix a prior for which the security is non-separable and we vary the marginal cost of information . Suppose that the security is and the common prior is on state space . Trader 1’s partition is and Trader 2’s is . Security is non-separable because the expected value of for both traders is at all states, yet there is uncertainty about the value of the security. Traders can acquire information, where is the Shannon cost of information. We assume that traders are myopic and proper scoring rules are used in both settings, hence each announcement is the expected value of the security given the acquired information.

Figure 1 shows the expected accuracy of markets and polls for prior . When the marginal cost of information is high (c>4.5), no trader acquires any information and the accuracy of the market is equal to that of the poll. As the marginal cost decreases below , Trader 2 starts acquiring information if the state is either 1 or 4. This implies that his announcement differs across partitions, revealing whether event or is true. Trader 1 combines this with his private information and learns which state is true, thus announcing . Therefore, a small change in the marginal cost of information allows the market to aggregate information, with a prediction accuracy of 1. In contrast, the poll’s accuracy improves gradually as information gets cheaper. This means that, as the cost of information decreases, the prediction accuracy of the market suddenly jumps to 1, whereas the accuracy of the poll gradually increases. Equivalently, the value of the market is 0 for , at it becomes positive and it decreases as decreases, converging to 0 as .

We conclude by observing that, in a strategic setting, markets can incentivize traders to acquire and utilize information more efficiently when the cost is close to the threshold of 4.5, because a small information acquisition could enable the aggregation of all available information, whereas in polls it can only marginally improve individual predictions.

5 The speed of information aggregation

Another interesting question about information acquisition is whether it makes the process of information aggregation conclude faster. If this were the case, the entire society would benefit by learning the intrinsic value of , and the corresponding event, faster.

Unfortunately, there are no good news. Even when traders are myopic, we show that information acquisition can make the process of information aggregation both slower and faster, depending on the parameters. We then show that this is true for all securities except for the Arrow-Debreu (A-D) security, when the environment is non-strategic. In particular, with A-D securities the information aggregation can never be faster (or slower) as compared to the no information acquisition case. If the process cannot get faster or slower, the competition of traders to acquire more information and appropriate more of the surplus produces neither negative nor positive externalities in society.

We begin with an example, which shows that information acquisition may make information aggregation both faster and slower.

Example 3.

The state space is , the security is , and there are two myopic traders with common prior . Trader 1’s partition is and Trader 2’s is .

Suppose that the true state is . Initially, traders cannot acquire any information. In the first period, Trader 1 announces 1. This reveals no information to Trader 2 because his private information is , and the same announcement would be made by Trader 1 in both states. In period 2, Trader 2 announces 0.5. This reveals to Trader 1 that the true state is , hence, in period 3 he announces 0 and the game ends.

Suppose now that traders are able to acquire the same signal as in the previous example. When the true state is , Trader 1 acquires signal , updates his beliefs to and announces . The announcement reveals to Trader 2 that the state is , because at Trader 1 would have announced 1. As a result, Trader 2 announces 0 in period 2 and the game ends, hence information aggregation happens faster with information acquisition.

We now show that the converse is also true, so that information acquisition may delay information aggregation. Suppose that the common prior is . At , if there is no information acquisition, Trader 1 announces . The announcement reveals to Trader 2 that the state is , hence Trader 2 announces 0 and the game ends in the second round. If there is information acquisition, Trader 1 acquires the signal and updates his beliefs to , and, therefore, he announces 1. This reveals no information to Trader 2, and he announces 0.5. This reveals to Trader 1 that the true state is , hence in the third round he announces 0 and the game ends.

Interestingly, if the security is the Arrow-Debreu (A-D), then information acquisition has no impact on the speed of information aggregation. To understand why, consider an A-D security that pays 1 at and 0 otherwise. At any period, there are two cases. First, the trader knows that either is true, or that it is not true, accordingly announcing 1 or 0. Second, he is unsure about whether is true or not. Irrespective of whether he buys a signal structure, he will announce some value . Crucially, other traders already know that his partition cell includes , hence his announcement does not reveal any public information and the speed of information aggregation is unaffected.

We now provide the formal results. Proposition 2 shows that for any security that is not A-D, we can find information structures for which is separable, and depending on the prior the process can be faster or slower. Proposition 2 shows that for an A-D security, allowing for information acquisition neither speeds up nor delays the information aggregation process.

Recall from Section 4.4 that the full state describes the initial uncertainty and the randomizations of the players. In this section, traders have a pure strategy of an announcement and the choice of the random posterior, hence denotes the realisation of the posterior in period .

Let be the period where information aggregation is achieved, given a separable security and state , in an environment where traders can get information before they make an announcement. Similarly, let be the period where information aggregation is achieved, in an environment where there is no information acquisition.

For Proposition 2, we make the following mild assumption.

Assumption 2.

Given a state space with two states and for any proper scoring rule and non-constant security , there is posterior separable cost function such that, for all , the solution to (4) is unique.

The assumption is true for a quadratic scoring rule and entropy cost function, as shown in Appendix 11 in Ilinov et al. (2024). More generally, consider cost and the payoff that is generated by making the myopic best announcement, both as functions of the posterior , where is the prior on one of the two states. Both these functions are strictly convex and a sufficient condition for a unique solution is that they do not have the same first-order condition for more than one . As we have complete freedom in choosing , it can be that we achieve this for any .232323See Tsakas (2020) for an analysis of this decision problem.

proposition Suppose Assumption 2 and that non-constant security is not A-D. Then, there is information structure for which is separable, such that for some information cost and ,

-

(i)

for some common prior ,

-

(ii)

for some common prior .

Consider non-constant security which is not A-D. Then, maps to at least three values, , and we denote the respective payoff-relevant states as , and . Note that each payoff-relevant state is associated with several full states , which resolve any uncertainty about which posteriors a trader receives at each period. To ease the notation, we omit mentioning when it is straightforward how statements about are translated to statements about .

Let the partition of Trader 1 be for these three states, whereas for any other state, we have . For Trader 2 it is and for any other state we have . Hence, the information structure is in . For Trader 1, let be the probability of state conditional on . For Trader 2, let be the probability of state conditional on .

We first show that is separable with respect to , so that are well-defined for all priors. If has more than three states, then for all and we have and . Therefore, separability only depends on the three states, , and . From Proposition 3.2, security is separable with respect to the restriction of on . But then, is separable with respect to .

Second, we show that (i) is true at state , given and some . Take a full support prior such that . This is possible because . At state , Trader 1 announces , so Trader 2 learns that is not true and announces a. We therefore have .

Because , there exists prior with full support on states and posterior probability on , such that for all .

Let be a posterior separable cost function which satisfies Assumption 2, so that the optimal random posterior is unique. Let be the function that maps each cost to the set of optimal random posteriors. Applying the Maximum Theorem, is an upper semicontinuous correspondence. From Assumption 2, is a function and therefore continuous. Let be the restriction of on one of the two posteriors that comprise the optimal random posterior, and in particular the one that takes values in .242424From Bayesian plausibility, the other posterior will take values in . For sufficiently high , will choose a posterior very close to the prior , whereas for sufficiently low , will choose a posterior very close to 1. From the Intermediate Value Theorem, there exists such that the optimal solution is .

This implies that Trader 1 optimally acquires information given and updates his beliefs from to at some , announcing . Trader 2 does not gain any new information from the announcement, because the same announcement would be made at state . The game proceeds to the next period, so However, without information acquisition, is such that for all and . Therefore, without information acquisition, after Trader 1 announces his prediction, Trader 2 will know the state and .

Finally, we show that (ii) is true at state given the same and some . Following the same argument as before, because , there exists with full support on the first three states and resulting unique such that for all . Therefore, after Trader 1 announces his prediction, Trader 2 does not know the state and . With information acquisition, we can find sufficiently low such that Trader 1 acquires information, updates his beliefs to , and announces at state which projects to . Therefore, Trader 2 realises that the state is not and

Finally, we show that the speed of aggregation is unchanged if the security is A-D.

proposition If is A-D, then for any state , cost , information structure , and common prior . {proofEnd} Without loss of generality we assume that and for all other . In every period , there are two cases. First, the trader announces 0 and the process ends. In that case, the trader does not acquire any information, because he knows that the price is 0. Second, the trader considers with to be possible, acquires information, and forms a posterior. As the posterior cannot reveal any state with certainty, his private information , where is the public event revealed by previous announcements, stays the same, but his posterior might change. Hence, no information is revealed to other traders, because he does not make a different announcement based on which partition cell he is in. Because no information is revealed to other traders conditional on the process continuing, the common knowledge event that is created by each announcement is the same with and without information acquisition, hence, the process ends in the same number of periods. Note, however, that announcements may differ across the two environments.

The property that speed is unaffected is related to the fact that the A-D security is not very informative. A trader will buy a posterior only in the partition cell where 1 is possible, as in all others he knows that the value is 0. This action does not have the positive externality of revealing to other traders what is his partition cell and therefore it does not provide any public information about what the true state is. Note, however, that some positive externality persists. The other traders can solve the announcer’s problem and therefore know the optimal signal structure he has purchased. By hearing the announcement, they also update their posteriors and they can benefit as long as it is their turn to announce and there is still some surplus to be obtained. For example, if Trader 1 buys a signal structure and moves the price from 0.5 to 0.99 (when the correct price is 1), then all other traders can only benefit by moving it from 0.99 to 1, hence the remaining surplus is very small. Finally, even though the number of periods for full aggregation remains the same, the price will get faster to the true value, hence the market will still benefit by attaching faster a higher probability to the true value of the security.

6 Concluding Remarks

One interesting question is what happens to information aggregation when the security is non-separable but the prior is generic. By perturbing the common prior slightly, a non-separable security could become separable, and therefore information could aggregate. Ostrovsky (2012) shows that information gets aggregates in all pure-strategy equilibria with a generic prior, even for non-separable securities. However, in his setting, it is an open question what happens with mixed-strategy equilibria. Intuitively, even if we perturb the initial prior, and given that agents have infinitely many available strategies, it is not clear whether they will converge to some belief at which the security is separable.

The current paper provides a different perspective on the issue of genericity, by endogenizing the perturbation of beliefs. If information is not aggregated at time , a trader could buy an additional signal, if the cost is not too high, and change her belief. By examining what happens when the cost is arbitrarily low, we effectively allow for arbitrarily small perturbations of beliefs to be feasible for traders. A “generic” security pays differently across states and Corollary 1 shows that if the cost is sufficiently low, such a security is separable, for all information structures. Therefore, using Theorem 6 we can say that generically information gets aggregated, in all mixed-strategy equilibria.

Appendix A Appendix

A.1 Cost of Information

Let be a Polish space of possible signals with Borel -algebra . Let be the set of Borel probabilities on , with generic element . We endow with the weak* topology: a sequence of probabilities converges to a probability if for every bounded continuous function , we have . Following Blackwell (1951), we model the acquisition of information using statistical experiments. A statistical experiment is a function from states into probabilities on signals, .

Following Bloedel and Zhong (2020), we say that an experiment is bounded if (i) the conditional signal distributions are mutually absolutely continuous, and (ii) there exists a constant such that the Radon-Nikodym derivatives for all . In other words, a bounded experiment does not definitively rule out any state and, moreover, has uniformly bounded likelihood ratios. Let be the set of all experiments and be the collection of all bounded experiments. Note that contains experiments that are not bounded. We say that is a garbling of given if there exists such that .

Given a prior belief , a statistical experiment induces via Bayesian updating a probability distribution over posteriors, or random posterior, . Let be the probability of posterior , be the set of all random posteriors that can be generated by some experiment , and . Note that if and only if . We endow with the weak* topology, so that it is a compact and separable topological space. The subsets of are endowed with the appropriate relative topologies.

Given a full support prior , experiment is bounded if and only if the induced random posterior satisfies for some . Let . Then, denotes the set of random posteriors that are induced by some full support prior and bounded experiment. Denote by the degenerate random posterior that puts probability 1 on .

Definition 8.

A cost on experiments is a map , where is Borel measurable for each prior and has the following properties.

-

(i)

If and , then ,

-

(ii)

If and , then ,

-

(iii)

Let be a sequence of experiment-prior pairs inducing random posteriors . If and there exists some such that , then , where ,

-

(iv)

If is a garbling of then .

Point specifies that if two bounded experiments generate the same random posterior given , then they have the same cost. Point says that a bounded experiment that is completely uninformative has a cost of zero. Point is a continuity condition that is weaker than weak* continuity, in order to allow for important classes of unbounded cost functions.252525See Bloedel and Zhong (2020) for the motivation behind this continuity condition. Finally, point specifies that more informative experiments are more costly.

The cost on experiments generates a cost structure on random posteriors, where is the unit cost of information and maps elements of , the set of all priors and all posterior distributions that can be generated by some experiment , to the extended real line.

We assume that the cost of acquiring random posterior , given belief , is determined by optimally acquiring the relevant experiment , so that

Note that Point (i) in Definition 8 ensures that all bounded experiments which induce given have the same cost, hence in that case . If only unbounded experiments generate given , we have . Moreover, the cost of learning nothing is zero, so that whenever . A cost structure consists of a cost function and a unit cost of information . Let be the collection of cost structures that are generated from the experiments.

If all unbounded experiments have infinite cost, then generating a random posterior with support on a posterior , which assigns probability 0 to a state , is infinitely costly.

Corollary 2.

Suppose Assumption 1. Given any and sequences with and with for all and some , if then .

The Corollary implies that for any induced sequences and with for all and some , if then .

Appendix B Proofs

Proposition 2 provides two independent conditions which are necessary for a security to be non-separable for all . The first condition specifies that, at some state , all traders agree that some value is possible. The second is an extension of Theorem 7 in Ostrovsky (2012) (see Proposition 1), which provides a characterization of separable securities. It says that for every value of and within all intervals around , there exists value v for which we cannot pick multipliers , for all elements of partitions and for all traders, such that the sign of is the same as the sign of , for all with .

Proposition 2.

Suppose is non-separable given an information structure and for all . Then, the following independent conditions are true.

-

•

There exists with and .

-

•

For some , for all , there exists for which there are no functions such that for all states with ,

(5)

Proof.

For the first condition, we prove the contrapositive. Suppose that for all , for all with we have . We will show that is separable for some .

For any and sufficiently low marginal cost , Assumption 1 implies that the only priors for which there is no information acquisition are the ones where the resulting posterior assigns probability close to 1 to some state , for all and . Suppose that there exists such , with for all and , where is arbitrarily close to some with .

For the security to be non-separable, there is also should be uncertainty about its value. This means that for some , . From our initial hypothesis, there exists trader such that , so that he considers to be impossible. Because he assigns probability close to 1 to some state, from continuity it must be that . Therefore, is separable at . As this is true for all that assign probability close to 1 to some state , we have that the the security is separable for some .

For the second condition, suppose is non-separable for all . Take with very small marginal cost , so that for any prior for which there is no information acquisition, at each state , and for each , assigns probability which is arbitrarily close to 1 to some state . This means that , for small enough and .

Because is non-separable, there exists a prior with no information acquisition and value for which is non-separable. This implies that, for any ,

where the last equality derives from the definition of non-separability. But then we cannot have for all , hence there are no such functions.

To show that the first two conditions are independent, consider first security . Let the partition of Trader 1 be and for Trader 2 be , which satisfies the first condition. We show that it fails the second condition. First, if , then condition (1) is satisfied by setting for all and . Similarly, if , we set for all and . Then, suppose there exist functions such that , , , , and . Consider . We then have that for , and for . Set and and (5) is satisfied. Consider . We then have that for , and for . Set and and (5) is satisfied. Finally, consider . We then have that for , and for . Set , and and (5) is satisfied. Therefore, the second condition is not satisfied.

Consider now security . Suppose there are three traders. The partition of Trader 1 is , for Trader 2 it is and for Trader 3 it is . Therefore, such security violates the first condition. We will show that it satisfies the second. Let and suppose that , for any . We then have that for , and for .

Suppose there exist functions such that , , , , and . For (5) to be satisfied, we have the following inequalities.

| (6) |

If we add the first with the fifth, we have . If we add the second with the fourth, we have . This is a contradiction and such equations do not exist, which means that the second condition is satisfied.

∎

References

- Allen [1981] Beth Allen. Generic existence of completely revealing equilibria for economies with uncertainty when prices convey information. Econometrica, pages 1173–1199, 1981.

- Atakan and Ekmekci [2023] Alp E Atakan and Mehmet Ekmekci. Information aggregation in auctions with costly information. 2023.

- Atanasov et al. [2017] Pavel Atanasov, Phillip Rescober, Eric Stone, Samuel A. Swift, Emile Servan-Schreiber, Philip Tetlock, Lyle Ungar, and Barbara Mellers. Distilling the wisdom of crowds: Prediction markets vs. prediction polls. Management Science, 63(3):691–706, 2017.

- Baron et al. [2014] Jonathan Baron, Barbara A Mellers, Philip E Tetlock, Eric Stone, and Lyle H Ungar. Two reasons to make aggregated probability forecasts more extreme. Decision Analysis, 11(2):133–145, 2014.

- Berg et al. [2008] Joyce E. Berg, Forrest D. Nelson, and Thomas A. Rietz. Prediction market accuracy in the long run. International Journal of Forecasting, 24(2):285–300, 2008.

- Blackwell [1951] David Blackwell. Comparison of experiments. In Proceedings of the Second Berkeley Symposium on Mathematical Statistics and Probability, pages 93–102. University of California Press, 1951.

- Bloedel and Zhong [2020] Alexander W Bloedel and Weijie Zhong. The cost of optimally-acquired information. Unpublished Manuscript, 2020.

- Camerer et al. [2016] Colin F Camerer, Anna Dreber, Eskil Forsell, Teck-Hua Ho, Jürgen Huber, Magnus Johannesson, Michael Kirchler, Johan Almenberg, Adam Altmejd, Taizan Chan, et al. Evaluating replicability of laboratory experiments in economics. Science, 351(6280):1433–1436, 2016.

- Caplin and Dean [2015] Andrew Caplin and Mark Dean. Revealed preference, rational inattention, and costly information acquisition. American Economic Review, 105(7):2183–2203, 2015.

- Caplin and Martin [2015] Andrew Caplin and Daniel Martin. A testable theory of imperfect perception. The Economic Journal, 125(582):184–202, 2015.

- Caplin et al. [2019] Andrew Caplin, Mark Dean, and John Leahy. Rational inattention, optimal consideration sets, and stochastic choice. The Review of Economic Studies, 86(3):1061–1094, 2019.

- Caplin et al. [2022] Andrew Caplin, Mark Dean, and John Leahy. Rationally inattentive behavior: Characterizing and generalizing shannon entropy. Journal of Political Economy, 130(6):1676–1715, 2022.