Power Analysis for Experiments with Clustered Data, Ratio Metrics, and Regression for Covariate Adjustment

Abstract

We describe how to calculate standard errors for A/B tests that include clustered data, ratio metrics, and/or covariate adjustment. We may do this for power analysis/sample size calculations prior to running an experiment using historical data, or after an experiment for hypothesis testing and confidence intervals. The different applications have a common framework, using the sample variance of certain residuals. The framework is compatible with modular software, can be plugged into standard tools, doesn’t require computing covariance matrices, and is numerically stable. Using this approach we estimate that covariate adjustment gives a median 66% variance reduction for a key metric, reducing experiment run time by 66%.

Keywords:

A/B experiment, regression adjustment, CUPED, ANCOVA, variance reduction, sample size calculation, standard error, delta method.

1 Motivation

When running A/B tests (randomized controlled trials), time is money. The faster we can run experiments, the faster we can ship promising treatments. We might put a lot of effort into variance-reduction techniques to obtain more accurate answers, but if power analysis/sample size planning tools don’t reflect that then the experiments we design will run longer than necessary.

Most off-the-shelf power analysis tools handle the simple case where analysis uses -tests for independent observations, but not clustered data, ratio metrics, or variance-reduction methods.

In this article we present a framework for conducting power analysis for A/B tests that can support any combination of the following applications:

- Clustered Data:

-

If we are interested in testing a feature that improves the customer experience, then the most intuitive unit of randomization for an A/B test is the customer. However, customers may place multiple orders. If the metric of interest is at the level of the order (e.g. mean order size) then we need to take this clustering into account when calculating standard errors.

- Ratio Metrics:

-

Some metrics are a ratio between two random quantities, e.g. ‘Revenue Share from Electronics’ = (revenue from electronics)/(total revenue). Standard errors depend on the variances of the numerator, denominator, and their correlation.

- Covariate Adjustment:

-

While random assignment makes experiment arms balanced on average, random imbalances do occur. We can reduce the variance of estimates by correcting for this covariate imbalance using regression. Standard errors should reflect this improvement.

These applications reduce to four basic cases, combinations of simple means or ratio metrics (including clustered data), with or without covariate adjustment. In all cases we obtain standard errors using the sample standard deviations of certain residuals. We begin with a review of power analysis for unadjusted means in Section 2, and consider the other cases in Sections 3, 4 and 5. Section 6 includes a summary of the standard errors and residuals in Table 1, then includes an example and a meta-analysis from Instacart.

2 A Refresher on Conventional Power Analysis

Power analysis (or sample size planning) involves relationships between four parameters of interest:

-

1.

sample size () representing the number of units selected for experimental assignment,

-

2.

false positive rate (type I error rate) ,

-

3.

power (, where is the type II error rate), the probability of detecting differences of a given magnitude, and

-

4.

minimum detectable effect (MDE) — the change in the response variable that is detectable with that power.

For simplicity we focus on two-arm experiments (“control” and “treatment” arms, denoted C and T) and focus on power and sample size estimates for a single metric. Let be an estimate of the treatment effect, (e.g. difference of means between T and C), and be its standard error. We focus on one-sided tests, because the vast majority of experiments at Instacart are run for the purpose of testing whether a treatment causes a metric to improve. We assume that sample sizes are large enough that both estimates and their corresponding -statistics () are approximately normally distributed.

The four parameters are related by the equation

| (1) |

where and are the Normal quantiles corresponding to the type I and II error rates respectively, and depends on .

2.1 Difference of Means

For the simple case of a difference in means assuming equal variances, no clustering, and equal sample sizes

| (2) |

where is the sample standard deviation of the response variable. Then given and any three of , , and we can calculate the fourth.

The factor of arises in a two-armed experiment. Suppose that there are and observations in the C and T arms, with sample standard deviations and , then

| (3) |

But when planning an experiment we don’t have those sample standard deviations or the actual sample sizes; instead we typically estimate both sample standard deviations using a single value estimated from historical data, and specify what fraction of observations will be allocated to the treatment group; then Equation (3) reduces to

| (4) |

In the special case that , , as in Equation (2).

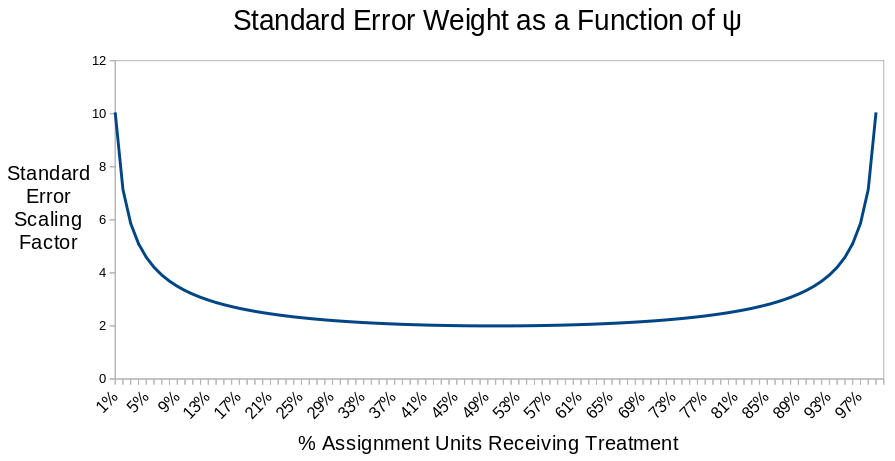

More generally, Figure 1 shows how standard errors depend on . The minimum scaling factor is at , and is slightly larger for values near , but increases dramatically when the fraction approaches or .

Also note that -values may be inaccurate if metrics are skewed and the split is not 50-50. The old “” rule for the Central Limit Theorem is badly wrong for skewed data. -values from a one-sample test are not reasonably accurate until for an exponential population111See [1] for more about skewed data. or for some important skewed metrics at Instacart. Two-sample tests with a 50-50 split are better because the skewness cancels out for .

2.2 Summary for Difference of Means

To recap, for a 50-50 split

| (5) |

The sample size necessary to achieve a specified MDE is

| (6) |

For splits other than 50-50, substitute for , but take care to check that skewness does not invalidate normal approximations.

2.3 Generalizing Beyond Difference of Means

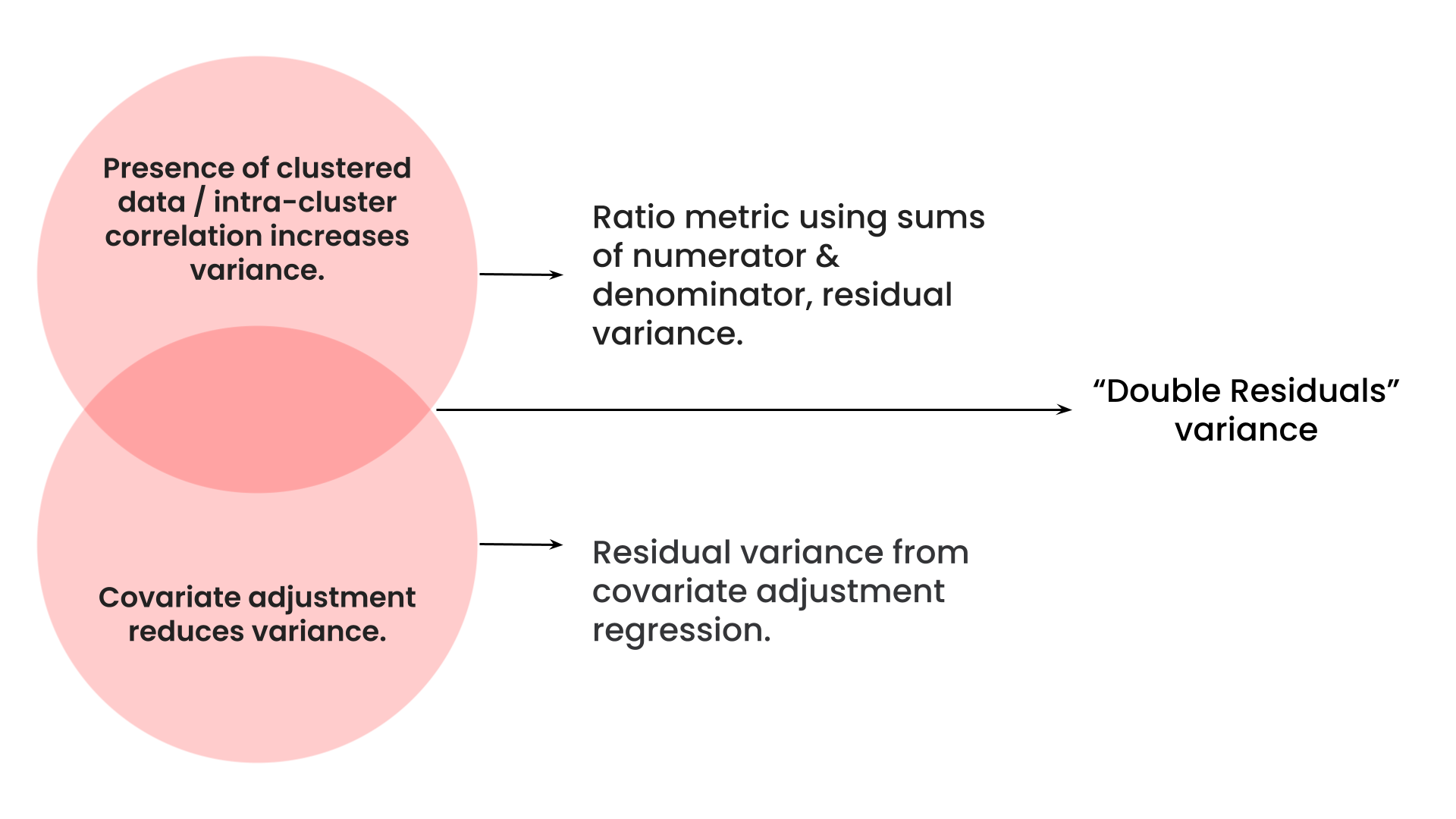

It turns out that Equations (5–6) almost work for clustered data, ratio metrics, and covariate adjustment applications — we just need to replace the value with other quantities that are based on residual standard deviations. Our broad strategy for deriving these values is shown in Figure 2.

To correctly estimate standard errors we need to account for two factors. First, when data are clustered there is intra-cluster correlation (the top portion of the Venn diagram); ignoring this typically results in standard errors that are too small, causing inflated false positive rates and too-short confidence intervals. Second, controlling for random imbalances in covariates between arms reduces the variability of estimates; ignoring this results in too-large standard errors. Finally, these factors may occur together. In subsequent sections we describe how to estimate standard errors in these cases, using ratio estimates and residual standard deviations.

3 Ratio Metrics and Clustered Data

In this section we discuss how ratio metrics arise, either due to clustering or natural ratio metrics, and derive standard errors.

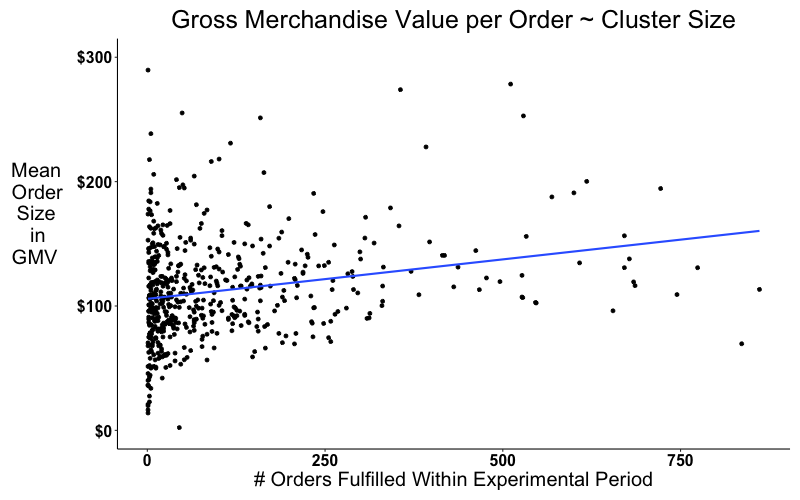

Our first challenge is clustered data. For example, consider estimating average order size (in dollars). We call this GMV per order (Gross Merchandise Value). Calculating the metric is straightforward, as the total value of items ordered divided by the number of orders. Calculating the standard error is not. We must account for correlations within clusters (for example, orders created by the same customer will tend to be of similar sizes).

We begin by aggregating the data by cluster to obtain two values for each customer: total value of items ordered by customer , and number of orders by customer . Then the metric is a ratio of , or equivalently the ratio of two sample means . This simplifies the problem in one way — we now have independent observations — but complicates it in others. Instead of a sample mean, we have a ratio of two sample means, and the numerator and denominator are dependent.

Other metrics represent naturally occurring ratios, even without clustering. For example, some retailers have their own in-store workers pick some orders, then Instacart shoppers deliver them to customers. The fraction of GMV picked by Instacart shoppers is a ratio: GMV picked by Instacart shoppers / total GMV.

Clustering may also occur with such natural ratio metrics, e.g. clustering from the order level to shopper or store level.

We use the following notation to handle ratio metrics, with or without clustering. corresponds to the metric of interest, or numerator of a ratio. Where there is clustering, we let

corresponds to the denominator, to a cluster size or count,

The individual or cluster ratio is

We estimate the metric or ratio of interest as:

| (7) |

While it might be natural to think of these metrics as weighted averages , that makes calculating standard errors tricky — see the appendix. Instead we estimate standard errors for ratio metrics using the delta method.

3.1 Standard Errors Using the Delta Method and Residuals

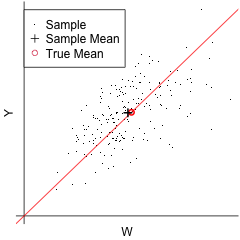

We turn now to calculating standard errors for ratio metrics, whether due to clustering or not. We use the delta method. We find a linear approximation to the ratio, based on a first-order bivariate Taylor series of the function about ,

| (8) | |||||

where and are the population means for the numerator and denominator, respectively. The estimate approximately equals the true value of the ratio, plus the mean residual divided by the true mean denominator. We visualize this in Figure 3.

Then the variance approximation is

| (9) |

A common next step would be to expand using variances and covariances. We prefer not to do this. Thinking of the variance in terms of the variance of residuals is easier to understand, particularly as we consider covariate adjustment below. Furthermore, that expansion can result in numerically-unstable estimates, including negative variances.

To use Equation (9) in practice, we substitute estimates for unknown quantities:

| (10) |

where

| (11) |

is the sample variance of the empirical residuals

| (12) |

The standard error is

| (13) |

4 Covariate Adjustment

In a randomized controlled trial the assignment of subjects to arms is fair on average, but in any trial there may be imbalances. For example, if the outcome of interest is customer spend, one arm might have more customers with high spend in the month before the experiment starts. We can improve estimates of the experimental effect by correcting for such imbalances in variables that are not affected by the treatment. This is covariate adjustment (or CUPED, ANCOVA, controls, etc. ).

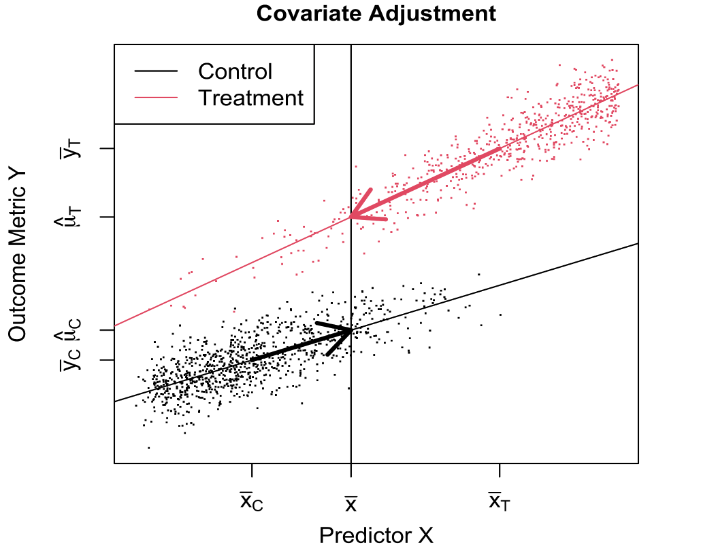

Figure 4 shows how this works for the case of one covariate (one predictor), using linear regression. The mean is clearly larger for the treatment group than for the control group. However, that is not solely due to the treatment; the treatment group also has larger values than the control group, which inflates and depresses . We correct for the imbalance using the predictions at the common mean .

For multiple regression with predictors we fit separate regression models to the control and treatment data, both of the form

| (14) |

Then revised estimates for each arm are:

| (15) |

where is the common mean of the th predictor.

Fitting separate models is equivalent to fitting a single model that includes interactions of the treatment variable with all predictors. We could fit a single model that excludes some interactions; this corresponds to fitting separate models but with the constraint that for some values of (and using the same prediction formulas).

These estimates are a special case of the general rule: let and be the control model and treatment model predictions for observation , then

| (16) |

These averages are over all observations, regardless of which arm was assigned to; in other words, we estimate what the mean responses would be, if both arms had the same distribution of values.

4.1 Standard Errors using Residuals

To calculate the standard errors for covariate adjusted estimates in Equation (15), we begin with the residuals. For each group (C and T separately), the residual standard deviation is

| (17) |

Then the standard error is

| (18) |

We are intentionally excluding a term from this standard error. Consider the control arm, and let be the variance of residuals relative to the true regression line/plane. The prediction at is , which has variance , which we estimate using . The missing term is the extra variance for predictions at other points, in particular at . But in randomized trials with large samples, is typically close to the group mean , and the additional variance is negligible.

Similarly, we are not using heteroskedasticity-consistent (HC) calculations for standard errors or covariance matrices. HC methods would have a negligible impact on variances for averages of predictions when .

In fact, our approach avoids the need to ever estimate covariance matrices for the coefficients. This makes it practical to use covariates with a large number of levels, e.g. customers, using fitting methods that do not produce covariate matrices.

5 Covariate Adjustment for Ratio Metrics

To apply covariate adjustment to ratio metrics, we use regression adjustments independently for the numerator and denominator , obtaining

| (19) |

The covariate-adjusted ratio estimates are

| (20) |

5.1 Standard Errors using Double Residuals

We use the delta method to obtain linear approximations for these estimates. Recall that standard errors for ratio metrics and covariate-adjusted non-ratio metrics both involve residuals; the standard errors here involve “double residuals” that combine elements of both residuals. For each arm, let

| (21) |

These double residuals are like the ratio method residuals in Equation (12), but with regression residuals in place of , and regression residuals in place of .

We calculate the residual variance

| (22) |

where the sum is taken across all observations in each arm, is the number of distinct units of receiving experimental assignment, and is the number of covariates in the model.

The standard error for the arm is

| (23) |

When planning an experiment we use the unadjusted estimate in Equation (21).

6 Applications

Here we review the methodology described above, then consider an example and a meta-analysis.

We began with a review of conventional power analysis methods for unadjusted differences of means, then described extensions for (1) clustered data using ratios of means, (2) ratios of means using the delta method, and (3) covariate adjustment for both means and ratios of means using regression. The standard errors of estimates ultimately depend on the sample standard deviations of certain residuals, plus division by the estimated denominator mean ( or ) for ratio estimates. This is summarized in Table 1.

| Estimate | Residual | SE | Equation | |

|---|---|---|---|---|

| mean | ||||

| ratio of means | (13) | |||

| covariate-adjusted | (18) | |||

| cov-adjusted ratio | (23) |

We could use common power analysis tools by plugging in , , or in place of .

We can incorporate those individual-arm standard errors into standard errors for the difference between arms, e.g. for an adjusted ratio metric

| (24) |

From there we can calculate the minimum detectable effect

| (25) |

sample size

| (26) |

or power

| (27) |

6.1 Example

Let’s walk through an application using real-world data. Instacart has store planogram data for some retailers — detailed descriptions of the exact location of a given product including the aisle number, shelf number, etc. Providing shoppers with this data could speed up their work and increase the proportion of items they find. This should make shoppers’ picking experience easier, and let shoppers work through their orders more quickly, increasing the average value of delivered orders as measured by GTV-per-order.

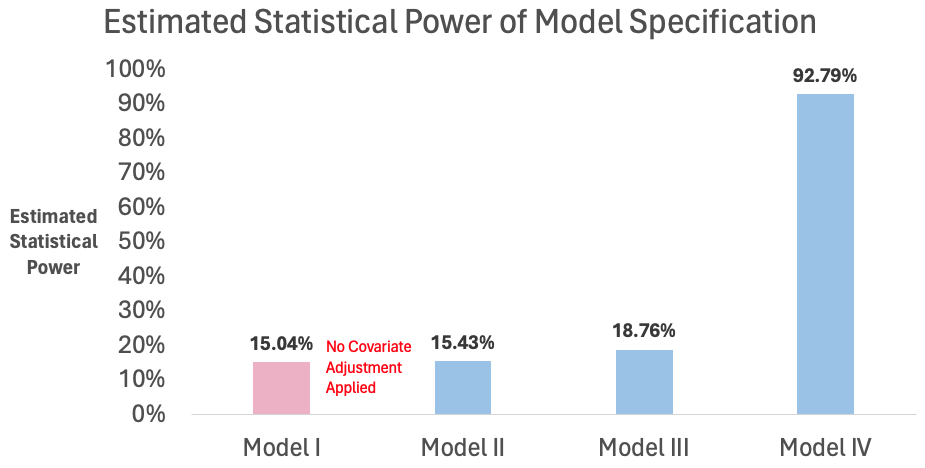

To test this, consider an A/B test randomized at the shopper level, with and 10 million orders (or approximately half a million shoppers). We estimate the variance of the average delivery value from historical data and specify an MDE of $0.05 per order. Using standard -tests would give a severely under-powered experiment, with power of (see Figure 5).

We can do better using covariate adjustment. The dollar value of the delivered order is highly correlated with the dollar value of the order the customer placed (see models 3 and 4 in Table 2). The number of items in the order is highly correlated with the sum of estimated probabilities of being in stock (models 2 and 4). Using either of these predictors alone has minimal value for covariate adjustment for the ratio of interest, but using them together gives an for of and improves power to over .

Regression Results: GMV-per-Order

Model

Response

Predictor

1

2

3

4

Intercept

1,434.8

-107.1

-2.4

-6.9

Item Availability

98.9

80.4

0.82

0.80

R-Squared

n/a

0.872

0.992

0.992

Intercept

33.7

0.187

6.43

2.31

Item Availability

2.13

2.22

0.015

-0.0004

R-Squared

n/a

0.998

0.865

0.998

R-Squared

n/a

0.034

0.257

0.927

Power

15.0%

15.4%

18.8%

92.8%

= (GMV Amount)

= # Orders Fulfilled

Item Availability = Average ML-Estimated Item Availability Score

= Tentative Chargeable Amount (pre-fulfillment)

6.2 Meta Analysis

We see how covariate adjustment can increase statistical power, but what about our original mandate — to ship promising treatments as quickly as possible? To explore the impact of covariate adjustment on experiment run times, we conducted a meta-analysis of 3,563 A/B tests comprised of 4,642 individual experiment arms. The response variable for these experiments is Gross Transaction Value (GTV) per customer (this is different from GMV-per-order in Table 2). Instacart adjusts for the following covariates: customer GTV measured during the 60-day pre-assignment period, the customer’s lifetime value (LTV) as estimated from a machine learning model, and the number of days elapsed since experimental assignment.

Holding statistical power, alpha, and the MDE constant across the covariate adjusted versus non-covariate adjusted versions of these hypothesis tests, we see that the median experiment run time for unadjusted tests is approximately 39 days. In contrast, the median run time using covariate adjustment is 13 days. As a thought exercise, if we were to apply the 26 days of run time saved to all 3,563 experiments, then the total time savings would amount to 253 years. In a world where time, is in fact, money, then the value proposition of covariate adjustment is evident.

7 Concluding Remarks

Using regression in the context of a randomized controlled trial provides a straightforward way to perform covariate adjustment. We must take care not to include covariates that are affected by the treatment, which would bias the results. Nevertheless, covariate adjustment is a powerful tool in our toolkit whenever statistical power is at a premium.

Unfortunately, most off-the-shelf power analysis tools do not support covariate adjustment. These same tools often fail when presented with clustered data and/or ratio metrics. The approach described above provides a way to conduct power analysis in these cases, without the need for complex simulations.

8 Appendix

Here we discuss issues with standard errors if we view ratio estimates (7) as weighted averages of values, i.e. .

Consider the two metrics discussed above. GMV-per-order corresponds to:

| (28) |

(shown in Figure 6), while the fraction of GMV picked by Instacart shoppers is

| (29) |

where if is true, otherwise .

To calculate standard errors for a weighted average , a convenient pair of assumptions would be that the weights are fixed values and the are independent with common variance ; then , and we could estimate using the sample variance of .

However, neither assumption is reasonable here. The weights are the cluster sizes, which are not fixed but instead depend on which shoppers are randomized into each arm. And GMV-per-order has higher variability for shoppers with few orders.

Or consider using weighted regression, with a model

| (30) |

with weights , where is treatment dummy variable. Then , and is the estimated experimental effect. There are many software programs that estimate coefficients for this weighted regression, and produce standard errors for the coefficients. Unfortunately, those standard errors would be incorrect, for the GMV-per-order data in Figure 6. The regression implicitly assumes that the weights are fixed and unaffected by the treatment, that the variance of the individual values is inversely proportional to the weights, and that the model is correct — that the expected value of depends on treatment arm but not on the number of orders. The software would estimate residual variance assuming that model. Those assumptions are incorrect — the weights are random, may be affected by the treatment, the expected value increases with the number of orders, and the variance decreases more slowly than suggested (perhaps because more-experienced shoppers handle larger orders which vary in size more).

In general it is dangerous to rely on canned software to estimate standard errors for weighted data. Standard errors depend on the randomization mechanism and how the weights arise, and the assumptions that software makes may not hold in your application.

References

- [1] Tim Hesterberg “What Teachers Should Know about the Bootstrap: Resampling in the Undergraduate Statistics Curriculum” In The American Statistician 69.4, 2015, pp. 371–386 DOI: 10.1080/00031305.2015.1089789