Topological Analysis for Detecting Anomalies (TADA)

in Time Series.

Abstract

This paper introduces new methodology based on the field of Topological Data Analysis for detecting anomalies in multivariate time series, that aims to detect global changes in the dependency structure between channels. The proposed approach is lean enough to handle large scale datasets, and extensive numerical experiments back the intuition that it is more suitable for detecting global changes of correlation structures than existing methods. Some theoretical guarantees for quantization algorithms based on dependent time sequences are also provided.

Keywords: Topological Data Analysis, Unsupervised Learning, Anomaly Detection, Multivariate Time Series, -mixing coefficients.

1 Introduction

Monitoring the evolution of the global structure of time-dependent complex data, such as, e.g., multivariate times series or dynamic graphs, is a major task in real-world applications of machine learning. The present work considers the case where the global structure of interest is a weighted dynamic graph encoding the dependency structure between the different channels of a multivariate time series. Such a situation may be encountered in various fields, such as e.g. EEG signal analysis Mohammed et al. (2023) or monitoring of industrial processes Li et al. (2022), and has recently given rise to an abundant literature - see, e.g. Zheng et al. (2023); Ho et al. (2023) and references therein.

The specific monitoring task addressed in this paper is unsupervised anomaly detection, that is to detect when the dependency structure is far enough from a so-called ”normal” regime to be considered as problematic. From the mathematical point of view, this problem, in its whole generality, is ill-posed: one has access to unlabeled data, in which it is tacitly assumed that the normal regime is prominent, the goal is then to label data points as normal or abnormal in a fully unsupervised way. In this sense, anomaly detection shows clear connection with outlier detection in robust machine learning (for instance robust clustering as in Brécheteau et al. (2021); Jana et al. (2024)). For more insights and benchmarks on the specific problem of anomaly detection in times series the reader is referred to Paparrizos et al. (2022b) (univariate case) and to Wenig et al. (2022) for the multivariate case.

We introduce a new framework, coming with mathematical guarantees, based upon the use of Topological Data Analysis (TDA), a field that has know an increasing interest to study complex data - see, e.g. Chazal and Michel (2021) for a general introduction. Application of TDA to anomaly detection in time series have raised a recent and growing interest: in medicine (Dindin et al. (2019); G. et al. (2014); Chrétien et al. (2024)), cyber security (Bruillard et al. (2016))… And, some general surveys on TDA applications to time series may be found in Ravishanker and Chen (2019); Umeda et al. (2019).

In this paper, the adopted approach proceeds in three steps. First, the time-dependency structure of a time series is encoded as a dynamic graph in which each vertex represents a channel of the time series and each weighted edge encodes the dependency between the two corresponding vertices over a time window. Second, persistent homology, a central theory in TDA, is used to robustly extract the global topological structure of the dynamic graph as a sequence of so-called persistence diagrams. Third, we introduce a specific encoding of persistence diagrams, that has been proven efficient and simple enough to face large-scale problems in the independent case (Chazal et al. (2021)), to produce a topological anomaly score. As detailed throughout the paper, the scope of the proposed method may be extended in several ways, encompassing dependent sequences of measures and dependent sequences of general metric spaces.

1.1 Contributions

Our main contributions are the following.

-

-

We produce a new machine learning methodology for learning the normal topological behavior in the data spatial dependency structure. This methodology is fully unsupervised, it does not need to be calibrated on uncorrupted data, as long as the amount of corrupted data remains limited with respect to the uncorrupted one. The captured information is numerically proved different and, in several cases, more informative than the one captured by other state-of-the-art approaches. This methodology is lean by design, and enjoys novel interpretable properties with regards to anomaly detection that have never appeared in the literature, up to our knowledge;

-

-

The proposed pipeline is easy to implement, flexible and can be adapted to different specific applications and framework involving graph data or more general topological data;

-

-

The resulting method can be deployed on architectures with limited computational and memory resources: once the training phase realized, the anomaly detection procedure relies on a few memorized parameters and simple persistent homology computations. Moreover, this procedure does not require any storage of previously processed data, preventing privacy issues;

-

-

Some convergence guarantees for quantization algorithms - used to vectorize topological information - in a dependent case are proven. These results do not restrict to the specific setting of the paper and may be generalized in the general framework of -estimation with dependent observations;

-

-

Extensive numerical investigation has been carried out in three different frameworks. First on new synthetic data directly inspired from brain modelling problems as exposed in Bourakna et al. (2022), that are particularly suited for TDA-based methods and may be used as novel benchmark. They are added to the public The GUDHI Project (2015) library at github.com/GUDHI/gudhi-data. Second on the comprehensive benchmark ”TimeEval”, that encompasses a large array of synthetic datasets Schmidl et al. (2022). And third on a real-case ”Exathlon” dataset from Jacob et al. (2021-07). All of these experiments assess the relevance of our approach compared with current state-of-the-art methods. Our procedure, originating from concrete industrial problems, is implemented and has been deployed within the Confiance.ai program and an open-source release is incoming. Its implementation involves only standard, tested machine learning tools.

1.2 Organization of the paper

A complete description of the proposed methodology in provided in Section 2, giving details on the several steps to build an anomaly score from a multivariate time series. Next, Section 3 theoretically grounds the centroid computation step as well as the anomaly test proposed in the previous section. Section 4 gathers the numerical experiments in the three different settings introduced above (synthetic TDA-friendly, TimeEval synthetic, real Exathlon data). Proofs of our results are postponed to Section 7.

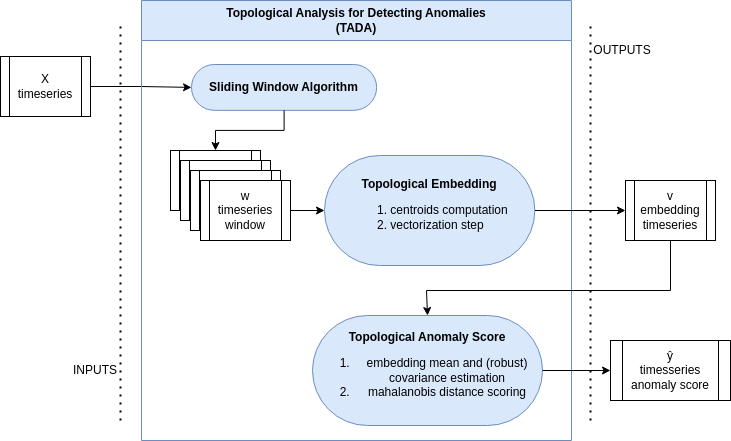

2 Methodology

This section describes the pipeline to build an anomaly score from raw multivariate time series data . We start with a brief description of the TDA tools that we use.

2.1 Vietoris-Rips persistent homology for weighted graphs

In this section we briefly explain how discrete measures are associated to weighted graphs, encoding their multiscale topological structure through persistent homology theory. We refer the reader to Edelsbrunner and Harer (2010); Chazal et al. (2016); Boissonnat et al. (2018) for a general and thorough introduction to persistent homology.

Recall that given a set V , an (abstract) simplicial complex is a set K of finite subsets of V such that and implies . Each set is called a simplex of . The dimension of a simplex is defined as and the dimension of is the maximum dimension of any of its simplices. Note that a simplicial complex of dimension is a graph. A simplicial complex classically inherits a canonical structure of topological space obtained by representing each simplex by a geometric standard simplex (convex hull of a finite set of affinely independent points in an Euclidean space) and “gluing” the simplices along common faces. A filtered simplicial complex , or filtration for short, is a nested family of complexes indexed by a set of real numbers : for any , if then . The parameter is often seen as a scale parameter.

Let be a complete non-oriented weighted graph with vertex set and real valued edge weight function , , satisfying for any pair of vertices .

Definition 1

Let and be two real numbers. The Vietoris-Rips filtration associated to is the filtration with vertex set defined by

for , and for any and any .

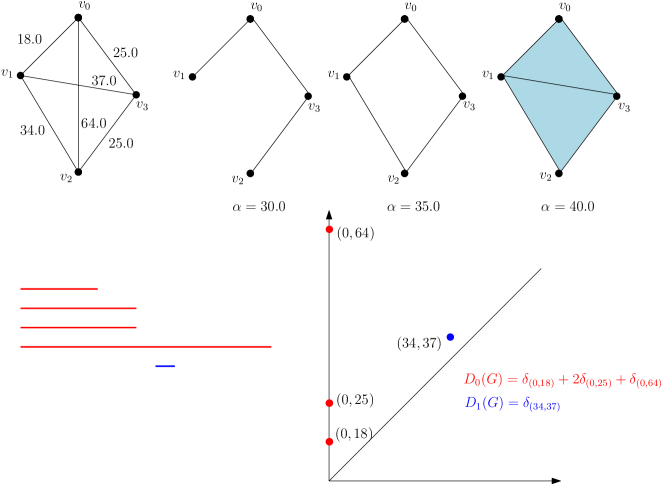

The topology of changes as increases: existing connected components may merge, loops and cavities may appear and be filled, etc… Persistent homology provides a mathematical framework and efficient algorithms to encode this evolution of the topology (homology) by recording the scale parameters at which topological features appear and disappear. Each such feature is then represented as an interval representing its life span along the filtration. Its length is called the persistence of the feature. The set of all such intervals corresponding to topological features of a given dimension - for connected components, for -dimensional loops, for -dimensional cavities, etc… - is called the persistence barcode of order of . It is also classically represented as a discrete multiset where each interval is represented by the point with coordinates - a basic example is given on Figure 1. Adopting the perspective of Chazal and Divol (2018); Royer et al. (2021); Chazal et al. (2021), in the sequel of the paper, the persistence diagram will be considered as a discrete measure: where is the Dirac measure centered at . In many practical settings, to control the influence of the, possibly many, low persistence features, the atoms in the previous sum can be weighted:

where may either be a continuous function which is equal to along the diagonal or just a constant renormalization factor equal to the total mass of the diagram. Notice that, in practice, there exist various libraries to efficiently compute persistence diagrams, such as, e.g., The GUDHI Project (2015).

The relevance of the above construction relies on the persistence stability theorem Chazal et al. (2016). It ensures that close weighted graphs have close persistence diagrams. More precisely, if are two weighted graphs with same vertex set and edge weight functions and respectively, then for any order , the so-called bottleneck distance between the persistence diagrams and is upperbounded by - see Chazal et al. (2014) for formal persistence stability statements for Vietoris-Rips complexes.

2.2 From similarity matrices to persistence diagrams

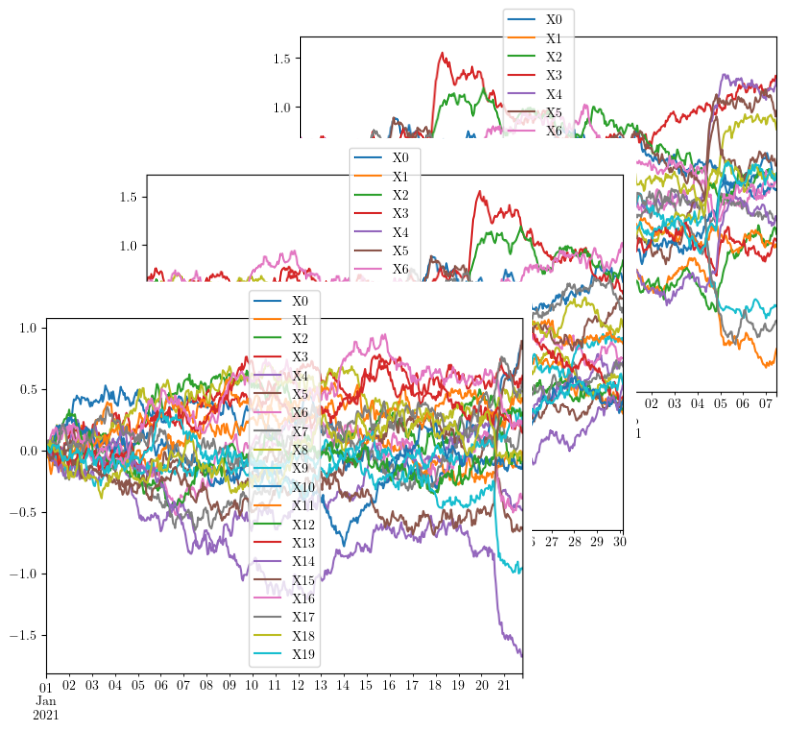

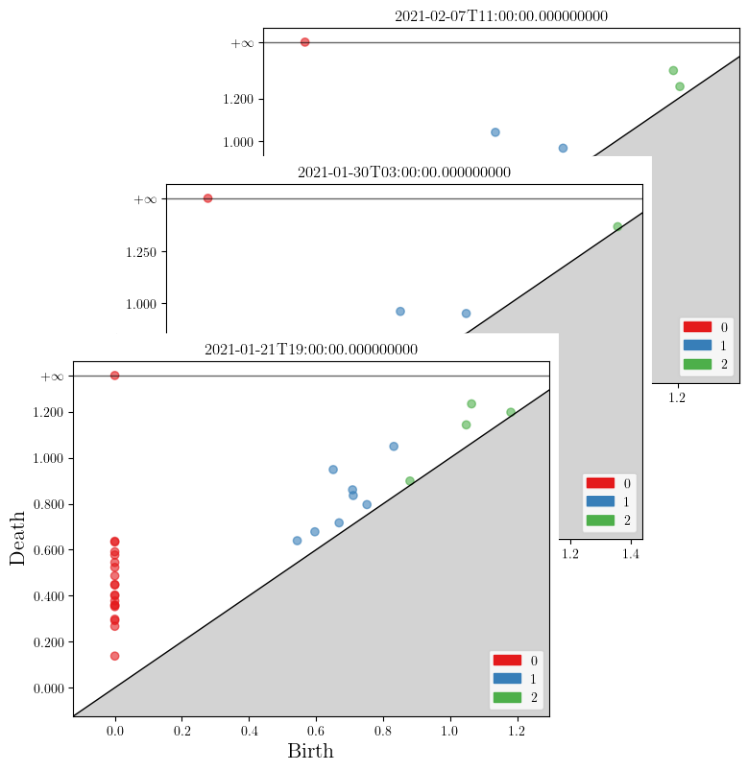

Our first step is to extract the topological information pertaining to the dependency structure between channels. To do so, for a window size , the -dimensional time serie is sliced into sub-intervals. For each sub-interval , we build a coherence graph , starting from the fully-connected graph and specifying edge values as , that is minus the correlation between channels and computed in the interval .

Then, the persistence diagrams of the Vietoris-Rips filtration are computed (one per homology order), resulting in sequences of diagrams , with and is the homological order. An example of sequences of windows and corresponding persistence diagrams is represented Figure 2. In what follows, a fixed homology order is considered, so that the index is removed. In practice, the vectorization steps that follows are performed order-wise, as well as the anomaly detection procedure.

It is worth noting that other dependency measures such as the ones based on coherence Ombao and Pinto (2021) may be chosen instead of correlation to build the weighted graphs. Such alternative choices do not affect the overall methodology as well as the theoretical results provided below.

In the numerical experiments, we give results for the correlation weights, that have the advantages of simplicity and carry a few insights: following Bourakna et al. (2022), such weights are enough to detect structural differences in the case where the channels are mixture of independent components ’s, the weights of the mixture being given by a (hidden) graph on the ’s whose structure drives the behavior of the observed persistence diagrams.

At last, it is worth recalling here that Vietoris-Rips filtration may be built on top of arbitrary metric spaces, so that the persistence diagram construction may be performed in more general cases, encompassing valued graphs (with value on nodes or edges) for instance. The vectorization and detection steps below being based on the inputs of such persistence diagrams, the scope of our approach is easily extended beyond the analysis of multivariate time series.

2.3 Centroids computation

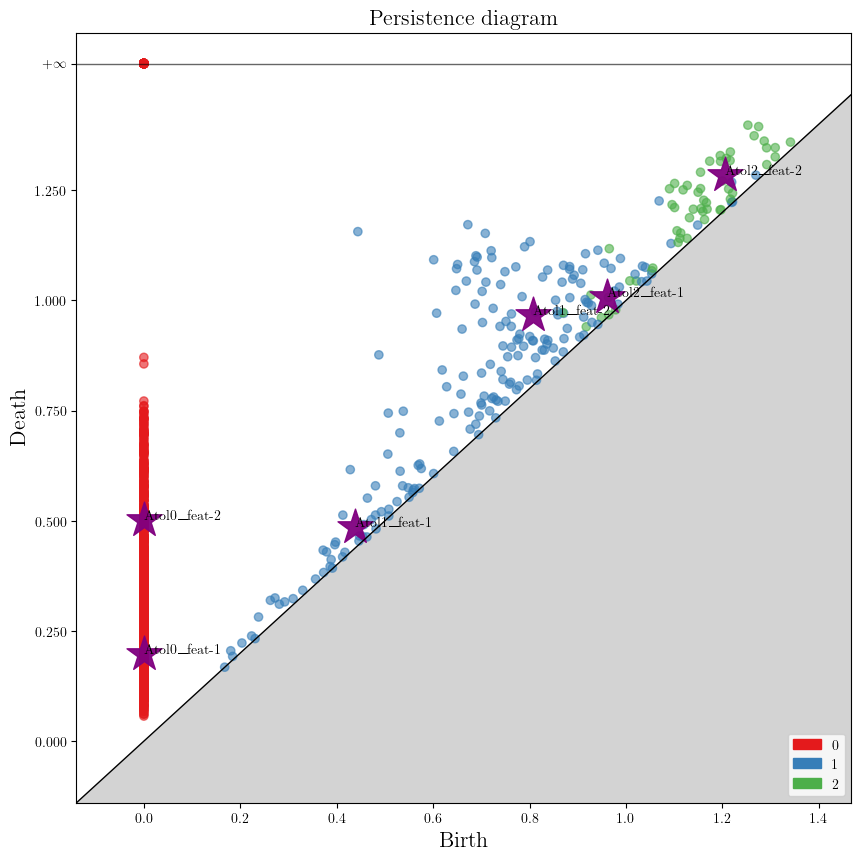

Once the mutivariate time series are converted into a sequence of persistence diagrams , the next step is to convert these persistence diagrams into vectors, that roughly encode how much mass do these diagrams spread into well-chosen areas of . To do so, we begin by automatically choosing these areas, or equivalently centers of these sub-areas, using the ATOL procedure of measure quantisation from Royer et al. (2021).

The batch algorithm for computing centers is recalled below. As introduced in Section 2.1, a persistence diagram is thought of as a discrete measure on , that is

where is the -th persistence diagram considered as a multiset of points, and are weights given to points in the persistence diagram (usually given as a function of the distance from the diagonal, see e.g., Adams et al. (2017) for instance). For the batch algorithm, a special interest is paid to the empirical mean measure:

Algorithm 2 is the same as in the i.i.d. case (Chazal et al., 2021, Algorithm 1). Moreover, almost the same convergence guarantees as in the i.i.d. case may be proven: for a good-enough initialization, only iterations are needed to achieve a statistically optimal convergence (see Theorem 5 below). Therefore, a practical implementation of Algorithm 2 should perform several threads based on different initializations (possibly in parallel), each of them being stopped after steps, yielding a complexity in time of (where ) is the number of threads.

As for the i.i.d. case, an online version of Algorithm 2 may be conceived, based on mini-batches. In what follows, for a convex set , we let denote the Euclidean projection onto .

Contrary to Algorithm 2, Algorithm 3 differs from its i.i.d. counterpart given in Chazal et al. (2021). First, the theoretically optimal size of batches is now driven by the decay of the -mixing coefficients of the time serie, as will be made clear by Theorem 6 below.

Second, half of the sample are wasted (the ’s with even ). This is due to theoretical constraints to ensure that the mini-batches that are used are spaced enough to guarantee a prescribed amount of independence. Of course, the even ’s could be used to compute a parallel set of centroids. However, in the numerical experiments, all the sample is used (without leaving some space between minibatches), without noticeable side effect.

From a computational viewpoint, Algorithm 3 is single-pass, so that, if threads are run, the global complexity is in .

See an instance of the centroid computations on Figure 3.

2.4 Conversion into vector-valued time series

Once the centroids built, the next step is to convert the persistence diagrams into vectors. The approach here is the same as in Royer et al. (2021) denoting by , a persistence diagram is mapped onto

| (1) |

where the bandwiths ’s are defined by

| (2) |

that roughly seizes the width of the area corresponding to the centroid . Other choices of kernel are possible (see e.g. Chazal et al. (2021)), as well as other methods for choosing the bandwidth. The proposed approach has the benefit of not requiring a careful parameter tuning step, and seems to perform well in practice.

We encapsulate this vectorization method as follows, and an example vectorization is shown in Figure 4.

2.5 Anomaly detection procedure

We assume now that we observe the vector-valued time serie of vectorized persistence diagrams, and intend to build a procedure to determine whether a new diagram (processed with Algorithm 4) may be thought of as an anomaly.

Our first step is to build a score, based on the ”normal” behaviour of the vectorizations ’s that are thought of as originating from a base regime. Namely, we build the sample means and covariances

| (3) |

In the case where the base sample can be corrupted, robust strategies for mean and covariance estimation such as Rousseeuw and Driessen (1999); Hubert et al. (2018) may be employed. To be more precise, for a contamination parameter , we choose the Minimum Covariance Determinant estimator (MCD), defined by

| (4) |

where denotes empirical mean on the subset , and is a normalization constant that can be found in Hubert et al. (2018). In all the experiments exposed in Section 4, we use the approximation of (2.5) provided in Rousseeuw and Driessen (1999).

Now, for a new vector , a detection score is built via

| (5) |

that expresses the normalized distance to the mean behaviour of the base regime. We refer to an illustrative example in Figure 5.

If we let denote the score function based on data , then anomaly detection tests of the form

may be built. The relevance of this family of test based on is assessed via the ROC_AUC and RANGE_PR_AUC metrics of the Application Section 4, see there for more details. Should a test with specific type I error be needed, a calibration of as the quantile of scores on the base sample could be performed. Section 3.2 theoretically proves that this strategy is grounded.

2.6 Summary

We can now summarize the whole procedure into the following algorithm, with complementary descriptive scheme in Figure 6.

Note that using Algorithm 2 with (see Theorem 5) and assuming that base observations are not corrupted results in only two parameters specification for Algorithm 5: the window size onto which correlation are computed, and the size of the vectorizations of persistence diagrams. At first it seems that choosing the right has the same amount of constraints than choosing the right for k-means imply, but it is actually made slightly easier by the fact that in this instance the k-means like procedure of Atol operates on the space of diagrams . As for it is very data-dependent, and optimizing for it is outside of the scope of this paper. In practice we will use a fixed contamination parameter of 0.1, a default fixed topological embedding size , a default fixed number of restart for the k-means initialisations . As for the sliding window algorithm we use by default a window of size with a stride of . The window size is the parameter that most needs to adapt to the data or learning needs, see more on this in Section 4 Applications.

Our proposed anomaly detection procedure Algorithm 5 has a lean design for the following reasons. First it has very few parameters coming with default values. Second, very little tuning is needed. Note that in the entire application sections to come, the only parameter to change will be the window resolution parameter, a parameter shared with other methods. Third, upon learning some data, TADA does not require a lot of memory: only the results of Algorithms 4 (centroids) and 5 (training vectorization mean and variance) are needed in order to produce topological anomaly scores. This implies that our methodology is easy to deploy, and requires no memory of training data which is often welcome in contexts of privacy for instance. It also means that the methodology will compare very favorably to methods that are memory-heavy such as tree-based methods, neural networks, etc.

3 Theoretical results

In this section we intend to assess the relevance of our methodology from a theoretical point of view. Sections 3.1 and 3.2 gives results in the general case where the sample is a stationary sequence of random measures. Section 3.3 provides some details on how persistence diagrams built from mulitvariate time series as exposed in Section 2.1 can be casted into this general framework.

3.1 Convergence of Algorithms 2 and 3

In what follows we assume that is a stationary sequence of random measures over , with common distribution . Some assumptions on are needed to ensure convergence of Algorithms 2 and 3.

First, let us introduce here as the set of random measures that are bounded in space, mass and support size.

Definition 2

For and , we let denote the set of discrete measures on that satisfies

-

1.

,

-

2.

,

-

3.

.

Accordingly, we let denote the set of measures such that and hold.

With a slight abuse, if denote a distribution of random measures, we will write whenever almost surely. As detailed in Section 3.3, persistence diagrams built from correlation matrices satisfy the requirements of Definition 2.

In the i.i.d. case, Chazal et al. (2021) proves that the output of Algorithm 2 with iterations returns a statistically optimal approximation of

| (6) |

where is the so-called mean measure . Note here that ensures that is non-empty (see, e.g., (Chazal et al., 2021, Section 3)). For the aforementioned result to hold, a structural condition on is also needed.

For a vector of centroids , we let

so that forms a partition of and represents the skeleton of the Voronoi diagram associated with . The margin condition below requires that the mass of around is controlled, for every possible optimal . To this aim, let us denote by the -neighborhood of , that is , for any and . The margin condition then writes as follows.

Definition 3

satisfies a margin condition with radius if and only if, for all ,

where denotes the -neighborhood of and

-

1.

,

-

2.

.

According to (Chazal et al., 2021, Proposition 7), and are positive quantities whenever . In a nutshell, a margin condition ensures that the mean distribution is well-concentrated around poles. For instance, finitely-supported distributions satisfy a margin condition. Up to our knowledge, margin-like conditions are always required to guarantee convergence of Lloyd-type algorithms Tang and Monteleoni (2016); Levrard (2018) in the i.i.d. case.

Turning back to our base case of time series of persistence diagrams, we cannot assume anymore independence between observations. To adapt the argument of Chazal et al. (2021) in our framework, a quantification of dependence between discrete measures is needed. We choose here to seize dependence between observation via -mixing coefficients, whose definition is recalled below.

Definition 4

For we denote by (resp. ) the -fields generated by (resp. ). The beta-mixing coefficient of order is then defined by

Recalling that the sequence of persistence diagrams is assumed to be stationary, its beta-mixing coefficient of order may be subsequently written as

where denotes the total variation distance and denotes the distribution of , for a generic random variable . As detailed in Section 3.3, mixing coefficients of persistence diagrams built from a multivariate time serie may be bounded in terms of mixing coefficients of the base time serie. Whenever these coefficients are controlled, results from the i.i.d. case may be adjusted to the dependent one.

We begin with an adaptation of (Chazal et al., 2021, Theorem 9) to the dependent case.

Theorem 5

Assume that is stationary, with distribution , for some . Assume that satisfies a margin condition with radius , and denote by , . For , choose , and let denote the output of Algorithm 2.

If is such that , and , then, for large enough, with probability larger than , we have

for all , where is a constant.

Moreover, if is such that and , it holds

Intuitively speaking, Theorem 5 provides the same guarantees as in the i.i.d. case, but for a ’useful’ sample size that corresponds to the number of sample measures that are spaced enough (in fact -spaced) so that they are independent enough in view of the targeted convergence rate in . This point of view seems ubiquitous in machine learning results based on dependent sample (see, e.g., (Agarwal and Duchi, 2013, Theorem 1) or (Mohri and Rostamizadeh, 2010, Lemma 7)).

Assessing the optimality of the requirements on seems a difficult question. Following (Mohri and Rostamizadeh, 2010, Corollary 20) and comments below, the condition we require to get a convergence rate in expectation seems optimal for polynomial decays (, ) in an empirical risk minimization framework. However, this choice leads to a convergence rate in for Mohri and Rostamizadeh (2010), larger than our rate. Though the output of Algorithm 2 is not an empirical risk minimizer, it is likely that it has the same convergence rate as if it were (based on a similar behavior for the plain -means case, see e.g., Levrard (2018)). The difference between convergence rates given in Mohri and Rostamizadeh (2010) and Theorem 5 might be due to the fact that Mohri and Rostamizadeh (2010) settles in a ’slow rate’ framework, where the convexity of the excess risk function is not leveraged, whereas a local convexity result is a key argument in our result (explicited by (Chazal et al., 2021, Lemma 21)).

In a fast rate setting (i.e. when the risk function is strictly convex), (Agarwal and Duchi, 2013, Theorem 5) also suggests that a milder requirement in might be enough to get a convergence rate in expectation, for online algorithms under some assumptions that will be discussed below Theorem 6 (convergence rates for an online version of Algorithm 2). Up to our knowledge there is no lower bound in the case of stationary sequences with controlled coefficients that could back theoretical optimality of such procedures.

At last, the sub-exponential rate we obtain in the deviation bound under the stronger condition seems better than the results proposed in (Mohri and Rostamizadeh, 2010, Corollary 20) or (Agarwal and Duchi, 2013, Theorem 5) in terms of ’large deviations’ (in here to get an exponential decay). Determining whether the same kind of result may hold under the condition remains an open question, as far as we know.

Nonetheless, Theorem 5 provides some convergence rates (in expectation) for several decay scenarii on :

-

•

if , for , then an optimal choice of is , providing the same convergence rate as in the i.i.d. case (Chazal et al., 2021, Theorem 9), up to a factor.

-

•

if , for , then an optimal choice of is , that yields a convergence rate in .

In the last case, letting allows to retrieve the i.i.d. case, whereas has for limiting case the framework when only one sample is observed (thus leading to a non-learning situation).

Whatever the situation, a benefit of Algorithm 2 is that a correct choice of , thus the prior knowledge of , is not required to get an at least consistent set of centroids, by choosing . This will not be the case for the convergence of Algorithm 3, where the size of minibatches is driven by a prior knowledge on .

Theorem 6

As in Rio (1993), the generalized inverse is defined by . In particular, for , is finite only if (that precludes the asymptotic ).

The requirement is stronger than in Theorem 5, thus stronger that the suggested by (Agarwal and Duchi, 2013, Theorem 5) in a similar online setting. Note however that for (Agarwal and Duchi, 2013, Theorem 5) to provide a rate under the requirement , two other terms have to be controlled:

-

1.

a total step sizes term in that must be of order . Controlling this term would require an slight adaptation of Algorithm 3, for instance by clipping gradients.

-

2.

a regret term in that must be of order . The behavior of this term remains unknown in our setting, so that determining whether the milder condition is sufficient remains an open question.

Let us emphasize here that, to optimize the bound in Theorem 6, that is to choose the smallest possible , a prior knowledge of is required. This can be the case when the original multivariate time serie follows a recursive equation as in Bourakna et al. (2022). Otherwise, these coefficients may be estimated, using histograms as in McDonald et al. (2015) for instance.

As in the batch case, the required lower bound on corresponds to the ”optimal” choice of minibatch spacings so that consecutive even minibatches may be considered as i.i.d.. It is then not a surprise that we recover the same rate as in the i.i.d. case, but with samples (see (Chazal et al., 2021, Theorem 10)). As for the batch situation, several decay scenarii may be considered:

- •

-

•

for , . An optimal choice for is then , leading to a convergence rate in .

Let us mention here that the stronger condition in Theorem 6 leads to a slower convergence bound for the polynomial decay case, compared to the output of Algorithm 2. Again, assessing optimality of exposed convergence rates remains an open question, up to our knowledge.

3.2 Test with controlled type I error rate

In this section, we investigate the type I error of the test

where is the score function built in Section 2.5 and will be built from sample to achieve a type I error rate below .

To keep it simple, we assume that and in (2.5) are computed from a separate sample, so that we observe

from a stationary sequence of measures, resulting in a stationary sequence of vectors. Whether and should be computed on the same sample, extra terms involving concentration of and around their expectations should be added, as in the i.i.d. case.

We let denote the common distribution of the ’s, that represent the ”normal” behavior distribution of the time serie structure. For the test introduced above, its type I error is then

A common strategy here is to choose a from sample, such as

for a suitable . In what follows we denote by such an empirical choice of threshold. The following result ensures that this natural strategy remains valid in a dependent framework.

Proposition 7

Let , and , be positive quantites that satisfy

If is chosen such that

then, with probability larger than , it holds

In other words, Proposition 7 ensures that the anomaly detection test has a type I error below , with high probability. Roughly, this bound ensures that, for confidence levels above the statistical uncertainty of order , tests with the prescribed confidence level may be achieved via increasing the threshold by a term of order .

As for Theorem 5 or 6, choosing the smaller that achieves optimizes the probability bound in Proposition 7:

-

•

for , of order is enough to satisfy , providing the same results as in the i.i.d. case, up to a factor.

-

•

for , an optimal choice for is of order , that leads to the same bounds as in the i.i.d. case, but with useful sample size .

Although this bound might be sub-optimal, it can provides some pessimistic prescriptions to select a threshold , provided that the useful sample size is known. For instance, assuming , for the minimal is of order , that is neglictible with respect to whenever is large compared to roughly .

3.3 Theoretical guarantees for persistence diagrams built from multivariate time series

We discuss here how the outputs of Algorithm 1, based on a -dimensional time serie , fall in the scope of the previous sections. Recall that a persistence diagram may be thought of as a discrete measure on (see Section 2.3). In a nutshell, if is stationary with a certain profile of mixing coefficients, then so would .

Stationarity: Since, for , may be expressed as , for some function , then stationarity of follows from stationarity of .

Boundedness: We intend to prove that the outputs of Algorithm 1 are in the scope of Definition 2. Let be an homology dimension, , and recall that is the order persistence diagram built from the Vietoris-Rips filtration of , where is the set of all edges and gives the weights that are filtered (see Section 2.1). First note that, for every , , so that every point in the persistence diagram is in . Next, since a birth of a -order feature is implied by an addition of a -order simplex in the filtration (see for instance Boissonnat et al. (2018) Section 11.5, Algorithm 11), the total number of points in the diagram is bounded by . At last, for a bounded weight function , the total mass of may be bounded by . We deduce that (Definition 2), with , , and . Note that in the experiments, we set .

Mixing coefficients: Here we expose how the mixing coefficients of (Definition 4) may be bounded in terms of those of . Let us denote these coefficients by and . If the stride is larger than the window size , then it is immediate that, for all , . If the stride is smaller (or equal) than , then, denoting by , we have, for , (overlapping windows), and, for , . The mixing coefficients of may thus be controlled in terms of those of . For fixed and , this ensures that mixing coefficients of and have the same profile (and leads to the same convergence rates in Theorem 5 and 6).

-

•

If , for , then, for any , , so that , for some constant (depending on , and ).

-

•

If , for and , then, for any , , so that , for some and depending on , and .

In turn, mixing coefficients of may be known or bounded, for instance in the case where it follows a recursive equation (see, e.g., (Pham and Tran, 1985, Theorem 3.1)), or inferred (see, e.g., McDonald et al. (2015)). Interestingly, the topological wheels example provided in Section 4.1 (borrowed from Bourakna et al. (2022)) falls into the sub-exponential decay case.

Margin condition: The only point that cannot be theoretically assessed in general for the outputs of Algorithm 1 is to know whether satisfies the margin condition exposed in Definition 3. As explained below Definition 3, a margin condition holds whenever is concentrated enough around poles. Thus, structural assumptions on (for instance prominents loops) might entail to fulfill the desired assumptions (as in Levrard (2015) for Gaussian mixtures). However, we strongly believe that the requirements of Definition 3 are too strong, and that convergence of Algorithms 2 and 3 may be assessed with milder smoothness assumptions on . This fall beyond the scope of this paper, and is left for future work. The experimental Section 4 to follow assesses the validity of our algorithms in practice.

4 Applications

In order to make the case for the efficiency of our proposed anomaly detection procedure TADA, we now present an assortment of both real-case and synthetic applications. The first application we call the Topological Wheels problem that is directly derived from Bourakna et al. (2022) to show the relevance of a topologically based anomaly detection procedure on complex synthetic data that is designed to mimic dependence patterns in brain signals. The second application is an up-to-date replication of a benchmark with the TimeEval library from Schmidl et al. (2022) on a large array of synthetic datasets to quantitatively demonstrate competitiveness of the proposed procedure with current state-of-the-art methods. The third application is a real-case dataset from Jacob et al. (2021-07) consisting in data traces from repeated executions of large-scale stream processing jobs on an Apach Spark cluster. Lastly we produce interpretability elements for the anomaly detection procedure TADA.

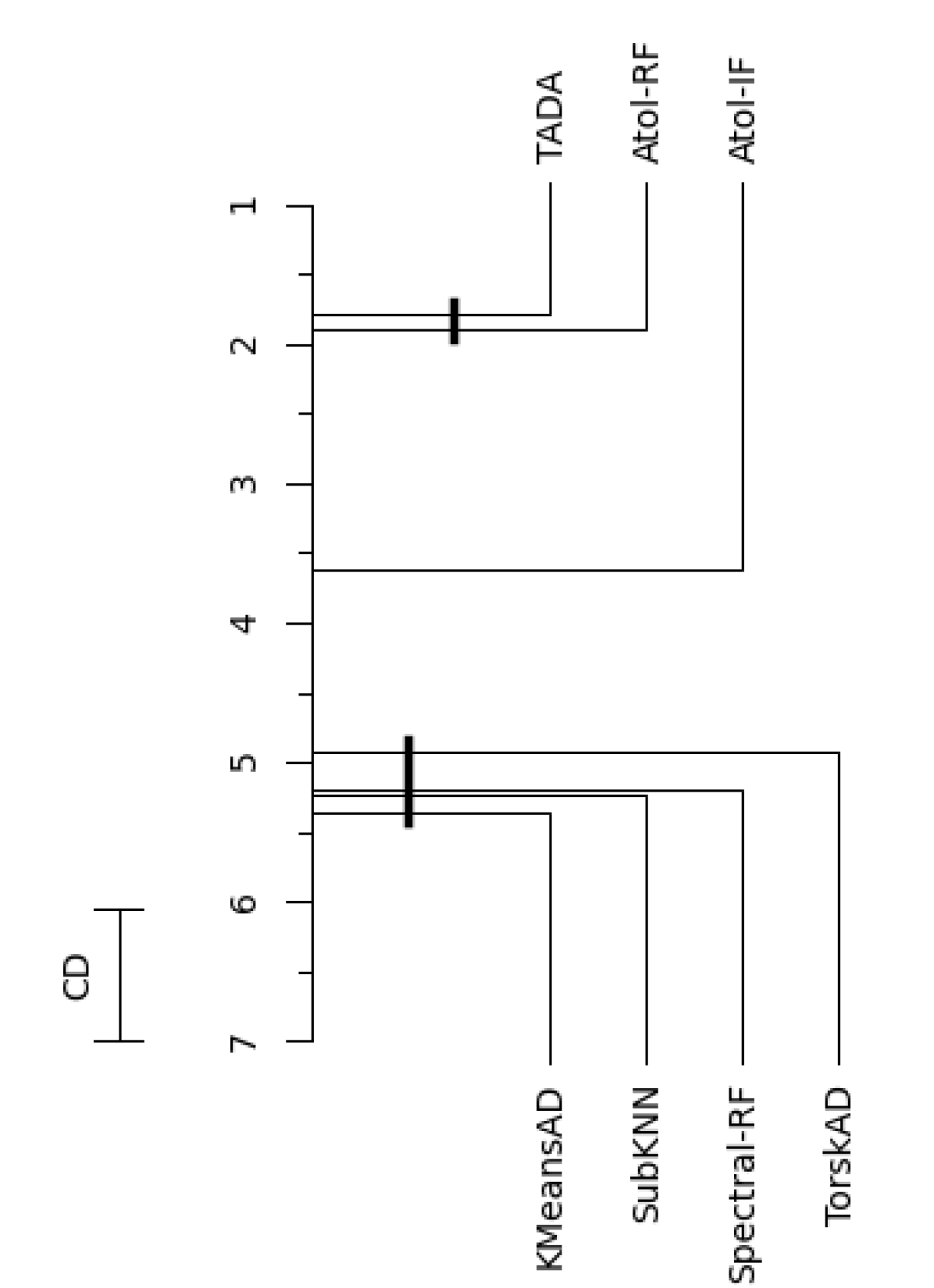

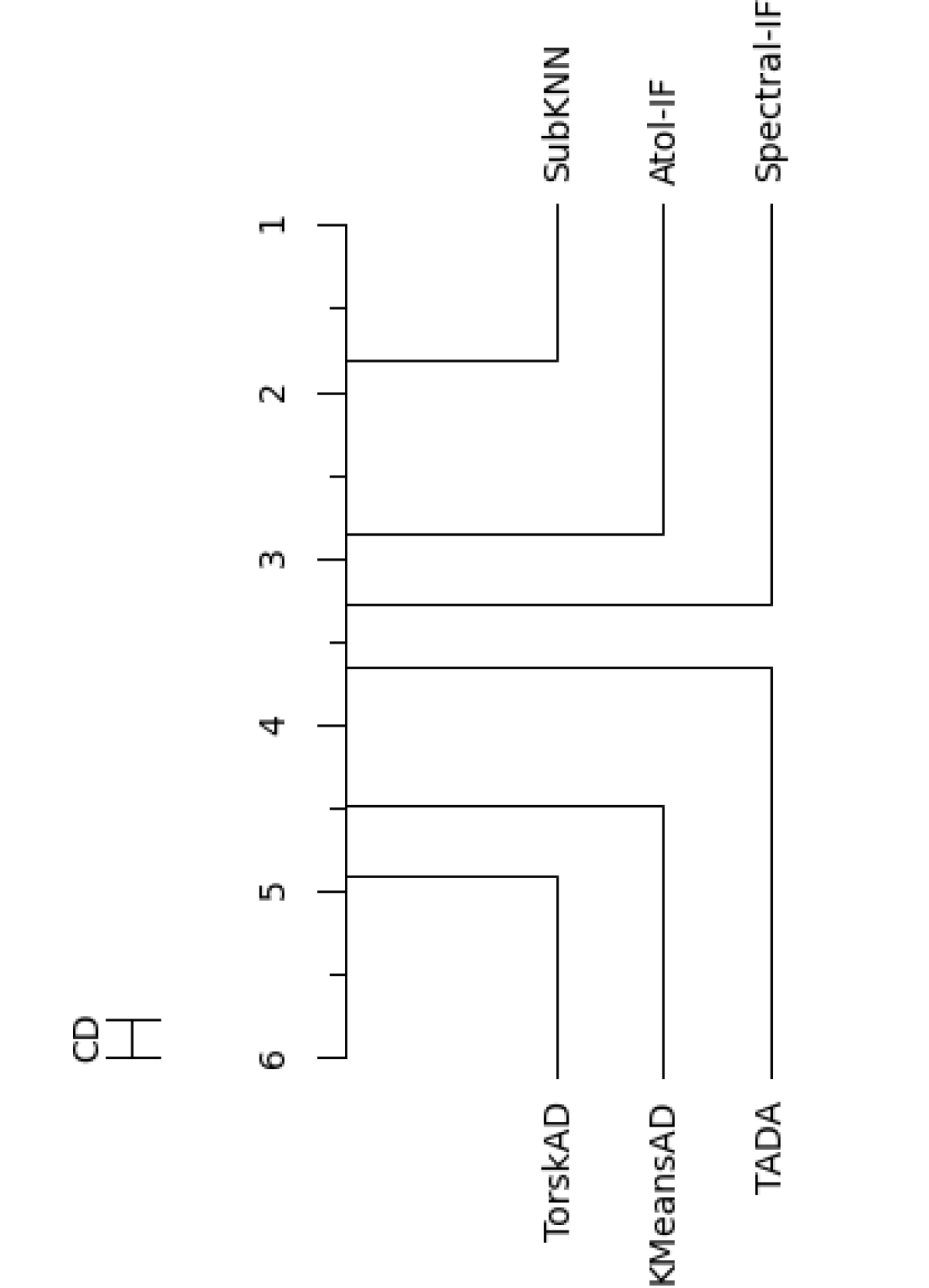

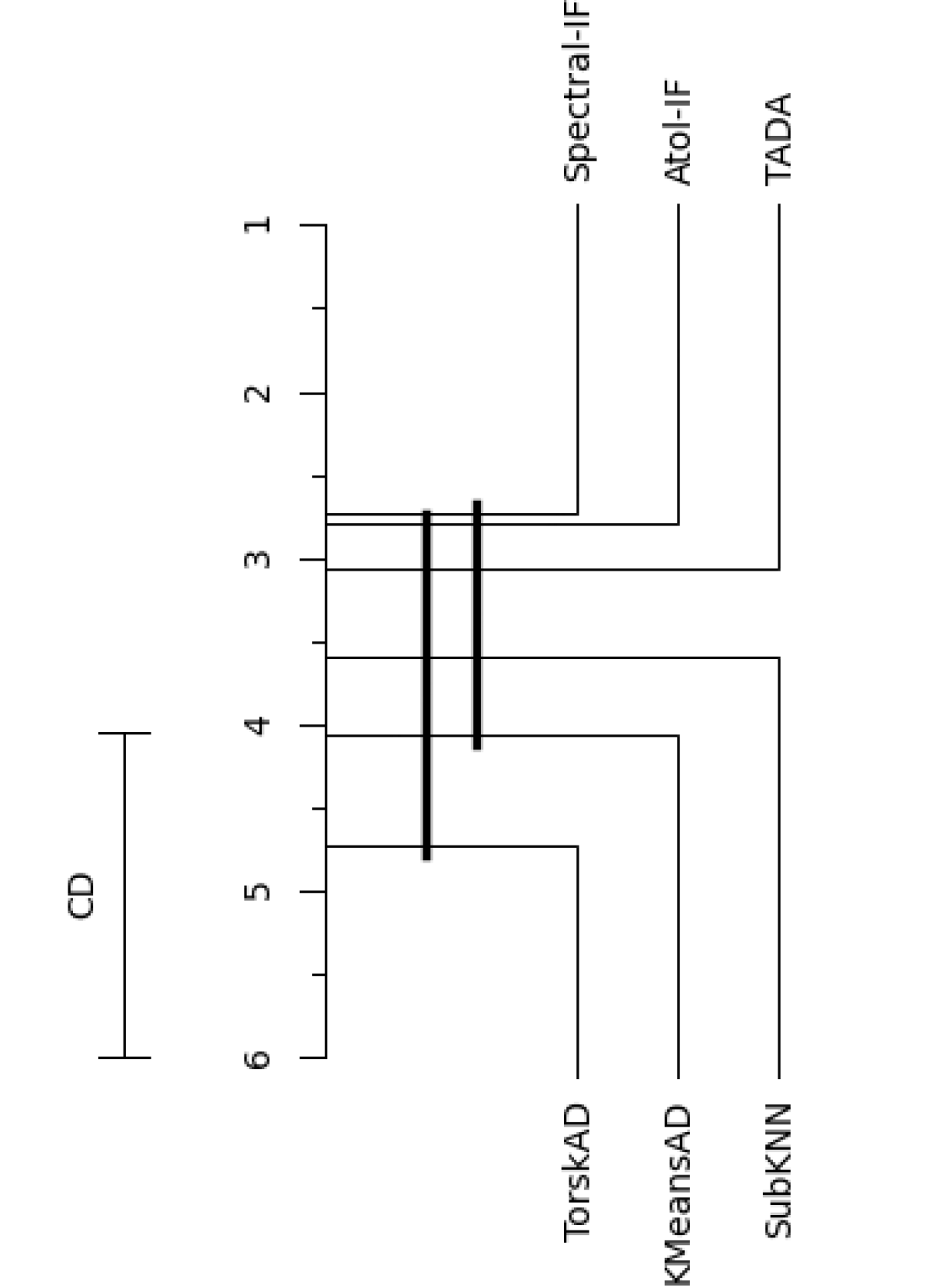

Evaluation of an anomaly detection procedure in the context of time series data has many pitfalls and can be hard to navigate, we refer to the survey of Sørbø and Ruocco (2023). Here we mainly evaluate anomaly scores with the robustified version of the Area Under the PR-Curve: the Range PR_AUC metric of Paparrizos et al. (2022a) (later just ”RANGE_PR_AUC”), where a metric of 1 indicates a perfect anomaly score, and a metric close to 0 indicates that the anomaly score simply does not point to the anomalies in the dataset. For the sake of comparison with the literature we also include the Area Under the ROC-Curve metric (later just ”ROC_AUC”) although as Sørbø and Ruocco (2023) demonstrated it is simply less accurate and powerful a metric in the unbalanced context of anomaly detection. Therefore each collection of anomaly detection problems will yield evaluation statistics. To summarize comparisons between algorithms we use a critical difference diagram, that is a statistical test between paired populations using the package Herbold (2020). We introduce two other statistical summary of interest:

-

•

the ”” metric, which we introduce for the number of anomaly detection problems an algorithm has a RANGE_PR_AUC over .9, which we roughly translates as ”finding” the anomalies in the dataset or ”solving” the problem,

-

•

the ”” metric, which we introduce for the number of problems where an algorithm reaches the best PR_AUC score over other algorithms. If a method reaches a not negligible number, this indicates that it makes sense to use the method for solving this kind of problem.

For the purpose of comparison with the state-of-the-art we draw from the recent benchmark of Schmidl et al. (2022). We take the three best performing methods from the unsupervised, multivariate category: the ”KMeansAD” anomaly detection based on k-means cluster centers distance using ideas from Yairi et al. (2001), the baseline density estimator k-nearest-neighbours algorithm on time series subsequences ”SubKNN”, and ”TorskAD” from Heim and Avery (2019), a modified echo state network for anomaly detection. In order to understand better the value of the introduced topological methodology, we also couple the topological features of Algorithm 4 to the isolation forest algorithm from Liu et al. (2008) for an unsupervised anomaly detection method denominated as ”Atol-IF” in reference to the Royer et al. (2021) paper. For an upper bound on what can be achieved on the first collection of problem we also couple those topological features to a random forest classifier Breiman (2001-10), resulting in a supervised anomaly detection method denominated as ”Atol-RF”. Lastly for discriminating effects of a spectral analysis respective to a topological analysis, we compute spectral features on the correlation graphs coupled to either an isolation forest or to a random forest classifier, in an unsupervised anomaly detection method denominated as ”Spectral-IF” and a supervised one named ”Spectral-RF”.

In practice all those methods involve a form of time-delay-embedding or subsequence analysis or context window analysis (we use these terms synonymously in this work), that requires to compute a prediction from a window size number of past observations. is a key value that acts as the equivalent of image resolution or scale in the domain of time series. In using a subsequence analysis, given a -uplet of timestamps , once an anomaly score is produced it is related to that particular -uplet but does not refer to a specific timestep. A window reversing step is needed to map the scores to the original timestamps. For fair comparison, we will provide all methods with the following (same) last-step window reversing procedure: for every timestep , one computes the sum of windows containing this timestep . Here we select not to use the more classical average , as this average produces undesirable border effects because the timestamps at the beginning and end of the signal are contained in less windows, which in turn makes them over-meaningful after averaging. Using the sum instead has no effect on anomaly scoring as the metrics are scale-invariant.

For the specific use of TADA in this section, the centroids computation part of Section 2.3 is made using and computed with the batch version described in Algorithm 2. Our implementation relies on The GUDHI Project (2015) for the topological data analysis part, but also makes use of the Pedregosa et al. (2011) Scikit-learn library for the anomaly detection part, minimum covariance determinant estimation and overall pipelining. The code is published as part of the ConfianceAI program https://catalog.confiance.ai/ and can be found in the catalog: https://catalog.confiance.ai/records/4fx8n-6t612. For now its access is restricted but it will become open-source in the following months. All computations are possible and were in effect made on a standard laptop (i5-7440HQ 2.80 GHz CPU).

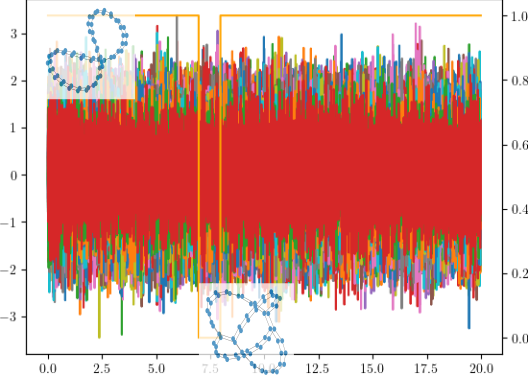

4.1 Introducing the Topological Wheels dataset.

In this first application section we introduce a hard, multiple time series unsupervised problem that emulates brain functions, and then solve the problem with our proposed method and compare solutions with state-of-the-art anomaly detection methods as well as supervised concurrent methods.

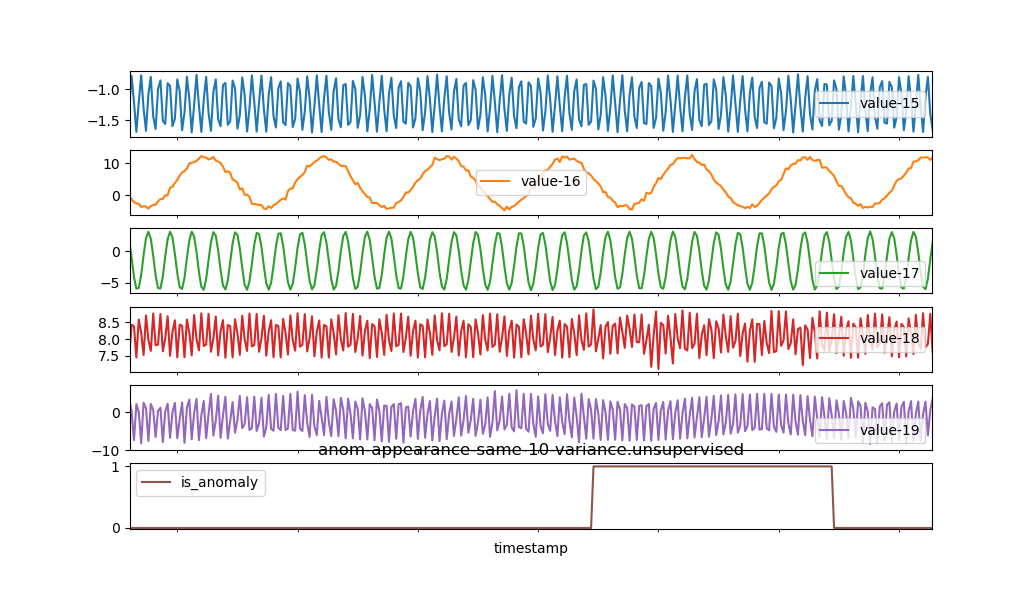

Bourakna et al. (2022) introduces ideas for evaluating methodologies relying on TDA such as ours. They allow to produce a multiple time series with a given node dependence structure from a mixture of latent autoregressive process of order two (AR2). One direct application for this type of data generation is to emulate the network structure of the brain, whose normal connectivity is affected by conditions such as ADHD or Alzheimer’s disease. Therefore in accordance with Bourakna et al. (2022) we design and introduce the Topological Wheels problem: a multiple time series datasets with a latent dependence structure ”type I” as a normal mode, and sometimes a ”type II” latent dependence structure as an abnormal mode. For the type I dependence structure we use a single wheel where every node are connected by pair, and every pair are connected to two others forming a wheel; then we connect a pair of pairs forming an 8 shape or double wheel, see Figure 7. And for the type II structure we start from a double wheel and add another connection between two pairs. The first mode of dependence is the prominent mode for the timeseries duration, and is replaced for a short period at a random time by the second mode of dependence. The total signal involves 64 timeseries sampled at 500 Hz for a duration of 20 seconds, see Figure 7. We produce ten such datasets and call them the Topological Wheels problem. It consists in being able to detect the change in underlying pattern without supervision. We note that by design the two modes are similar in their spectral profile, so overall detecting anomalies should be hard for methods that do not capture the overall topology of the dependency structure. The datasets are available through the public The GUDHI Project (2015) library at github.com/GUDHI/gudhi-data.

For learning this problem we use a cross-validation like procedure with a focus on evaluation: we perform ten experiments and for each experiment, every method is fitted on one dataset and evaluated on the other nine datasets. We then rotate the training dataset until all ten datasets have been used for training. We use this particular setup in order to be able to compare supervised and unsupervised methods on comparable grounds. As for method calibration we note the following: all methods are given (and use) the real length of the anomalous segment of consecutive timestamps, and since all of them use window subsequences we set the same stride for all to be . Lastly for all methods that use a fixed-size embedding (Atol-based methods and ”Spectral-RF”) we set the same size of the support to be .

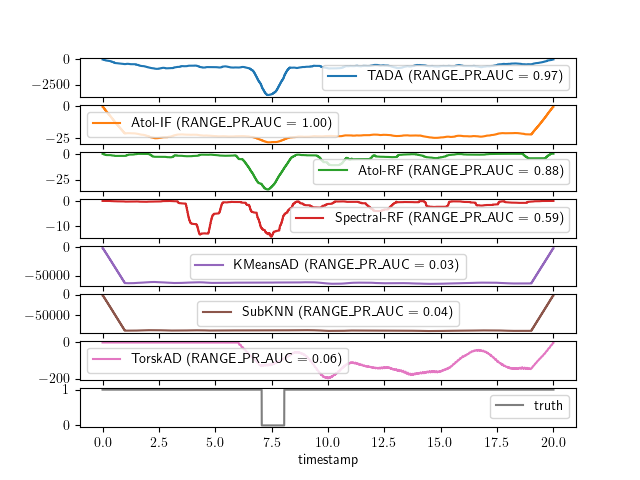

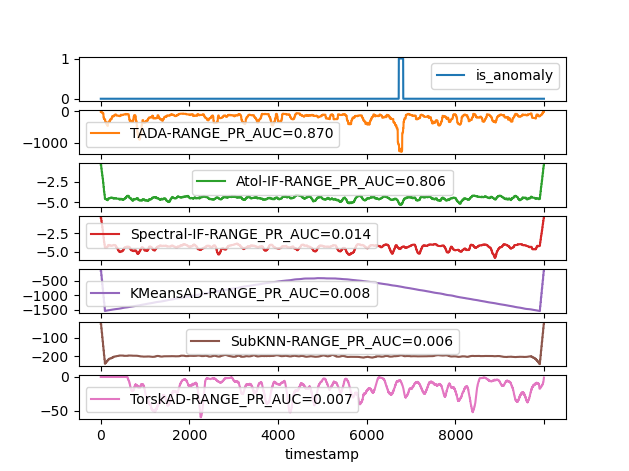

We first show in Figure 7 the results of one iteration of learning, that is when all methods are trained on a topological wheels dataset and evaluated on another. The last row of the figure with label ”truth” shows the underlying signal value of the evaluated dataset. The other rows are the computed anomaly score of each method along the time x-axis, with the convention that the lower the score, the more abnormal the signal. The corresponding RANGE_PR_AUC score of each method is written in the label. This first example confirms the intuition that methods that do not rely on topology, that is the spectral method, the k-nearest-neighbour method and the modified echo state network method all fail to capture the anomaly. This is particularly striking for the spectral method as it was trained with supervision. On the other hand all methods based on the topological features manage to capture some indication that there is anomaly in the signal. For the isolation forest method, even though it clearly separates the anomalous segment from the rest, it is not reliable as it seems to indicate other anomalies when there aren’t. The random forest supervised method perfectly discriminates the anomalous segment from the rest of the time series, and so does our method almost as reliably.

| algorithm | #xp | #.9 | #rank1 | med time | iqr time | |

|---|---|---|---|---|---|---|

| Atol-IF | (unsupervised) | 90 | 21 | 7 | 21.070 | 0.099 |

| Atol-RF | (supervised) | 90 | 45 | 38 | 21.104 | 0.104 |

| KMeansAD | (unsupervised) | 90 | 0 | 0 | 0.801 | 0.110 |

| Spectral-RF | (supervised) | 90 | 2 | 3 | 4.737 | 0.022 |

| SubKNN | (unsupervised) | 90 | 0 | 0 | 35.287 | 0.245 |

| TADA | (unsupervised) | 90 | 54 | 40 | 21.128 | 0.115 |

| TorskAD | (unsupervised) | 90 | 1 | 2 | 112.841 | 1.973 |

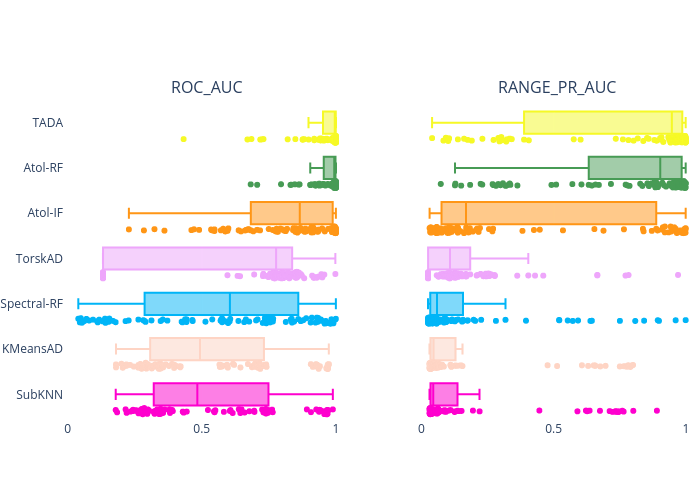

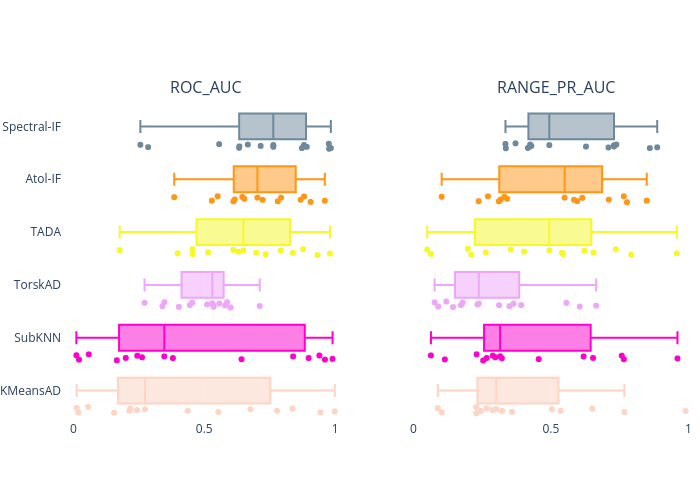

We now look at the aggregated results for the entire problem, see Figure 8 and times Table 1. We present both ROC_AUC and RANGE_PR_AUC averages with their standard deviations over experiments, as well as the computation times for the sake of completeness. Neither the spectral procedure nor the echo state network, subKNN or k-nearest-neighbour method are able to capture any information from the Topological Wheels problem. Using topological features with an isolation forest yields competitive results but it is simply inferior to our procedure. This demonstrates that the key information to this problem lies in the topological embedding which is not surprising, by design. Our procedure solves this problem almost perfectly, and although it is unsupervised it is as competitive as a comparable supervised method. This experiment demonstrates the impact of topology-based methods for anomaly detection, as the non-topology method fail to capture any of the signal in the datasets. Our proposed TADA method is clearly the best suited for learning anomalies in this setup.

4.2 A benchmark using the TimeEval library.

We now look at a broader and more general arrays of problems to evaluate the competitiveness of our method in comparison with state-of-the-art methods. For that purpose, we use the GutenTAG multivariate datasets, drawn from Wenig et al. (2022). We chose the GutenTAG datasets for the ability to generate a great (1084) number of varied anomaly detection problems; they are mostly formed from inserting anomalies of various lengths in frequency or variance or extremum values into a multivariate time series of 10000 timestamps. As the anomalies in these dataset seem to have an average size of 100, we set the window sizes of the anomaly detectors to be a fixed . Other than that, all other parameters from the previous section are left unchanged.

| algorithm | #xp | #.9 | #rank1 | med time | iqr time |

|---|---|---|---|---|---|

| Atol-IF | 1084 | 844 | 396 | 4.137 | 0.029 |

| KMeansAD | 1084 | 366 | 213 | 2.327 | 0.375 |

| Spectral-IF | 1084 | 751 | 281 | 1.502 | 0.014 |

| SubKNN | 1084 | 944 | 939 | 1.244 | 0.502 |

| TADA | 1084 | 521 | 255 | 4.525 | 0.062 |

| TorskAD | 1084 | 37 | 32 | 8.459 | 0.250 |

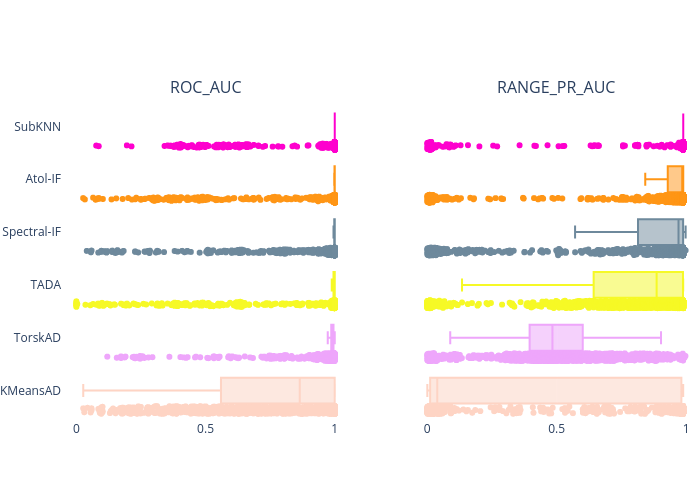

Statistical summaries and results on the synthetic datasets are shown Figure 9, and in Table 2. As a remainder, the SubKNN, KMeansAD and TorskAD methods were the top three performing methods from the largest anomaly detection benchmark to date (see Table 3 from Schmidl et al. (2022)). Our TADA procedure manages to solve roughly half the problems and is a top contender among competitors for about a quarter of them. Atol-IF performs better than TADA in this instance, which is not surprising as isolation forest retain much more information from training than TADA, which also implies heavier memory loads. Overall SubKNN is able to perform the best on those datasets, and TADA and Atol-IF show good performances, and in some instances only the topological methods manage to solve the problem, see for instance Figure 10. These results demonstrate competitiveness of our methodology in the unsupervised anomaly detection learning context.

4.3 Exathlon real datasets

Lastly we turn to a real collection of datasets: the 15 Exathlon datasets from Jacob et al. (2021-07) consisting in data traces from repeated executions of large-scale stream processing jobs on an Apach Spark cluster, and anomalies are intentional disturbances of those jobs.

| algorithm | #xp | #.9 | #rank1 | med time | iqr time |

|---|---|---|---|---|---|

| Atol-IF | 15 | 0 | 3 | 9.998 | 448.273 |

| KMeansAD | 15 | 1 | 1 | 3.336 | 2.568 |

| Spectral-IF | 15 | 0 | 4 | 6.212 | 1.503 |

| SubKNN | 15 | 1 | 2 | 8.604 | 13.357 |

| TADA | 15 | 1 | 5 | 11.516 | 450.723 |

| TorskAD | 15 | 0 | 0 | 34.282 | 37.395 |

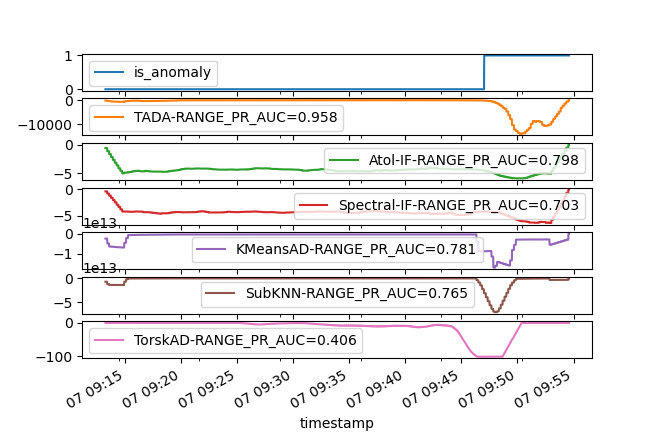

Using the same metrics, collection of anomaly detection methods and exact same calibration as in the previous TimeEval experiment, we produce the following results. The main statistical summaries are presented on Figure 11 and Table 3. Overall the topological methods are strong competitors for these datasets, with TADA coming off as the most often number one ranked method. Due to the real nature of the datasets it is not surprising that the studied methods do not ”solve” them in a way those methods were able to solve the GutenTAG datasets of the TopologicalWheels datasets. We show in Figure 12 the one instance where TADA is able to solve the problem completely, and highlight that is has happened without any calibration.

| dataset | TADA computing time (s) | n_sensors | n_timestamps |

|---|---|---|---|

| 10_2_1000000_67 | 1127.328406 | 165 | 10250 |

| 10_3_1000000_75 | 10.981673 | 8 | 46656 |

| 10_4_1000000_79 | 7.367096 | 3 | 43086 |

| 2_2_200000_69 | 121.436984 | 130 | 2874 |

| 3_2_1000000_71 | 457.991445 | 194 | 2474 |

| 3_2_500000_70 | 591.719635 | 208 | 2611 |

| 5_1_500000_62 | 14.912100 | 16 | 46660 |

| 5_2_1000000_72 | 460.615526 | 195 | 2481 |

| 6_1_500000_65 | 11.515798 | 12 | 46649 |

| 6_3_200000_76 | 9.138171 | 7 | 46654 |

| 8_3_200000_73 | 8.023327 | 4 | 46641 |

| 8_4_1000000_77 | 7.096984 | 2 | 43078 |

| 9_2_1000000_66 | 3046.870513 | 239 | 7481 |

| 9_3_500000_74 | 9.379143 | 7 | 46650 |

| 9_4_1000000_78 | 7.405223 | 3 | 43105 |

One drawback of the topological methods appearing here is the high variance in execution time, which originates from computing topological features on a great number of sensors, see Table 4 for a scaling intuition. As our implementation of Algorithm 5 is naive, we point that there are strategies for optimizing computation times: ripser, subsampling, clustering that makes sense, etc. Those strategies are outside the scope of this paper.

4.4 Score interpretability

The anomaly score we introduce is constructed from estimating the mean measure of persistence diagrams supported by centroids, and analysing the resulting embedding’s main distribution features. Once these centers are learnt it is possible to engineer anomaly scores respective to a particular center, or possibly to a set of centers e.g. centers associated with a particular homology dimension. Let us examine this first possibility, and introduce the center-targeted scores:

| (7) |

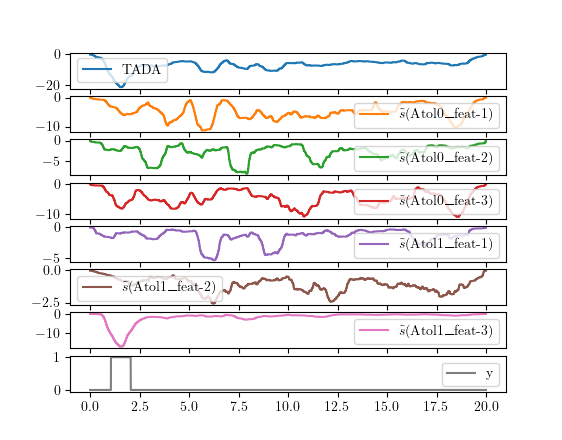

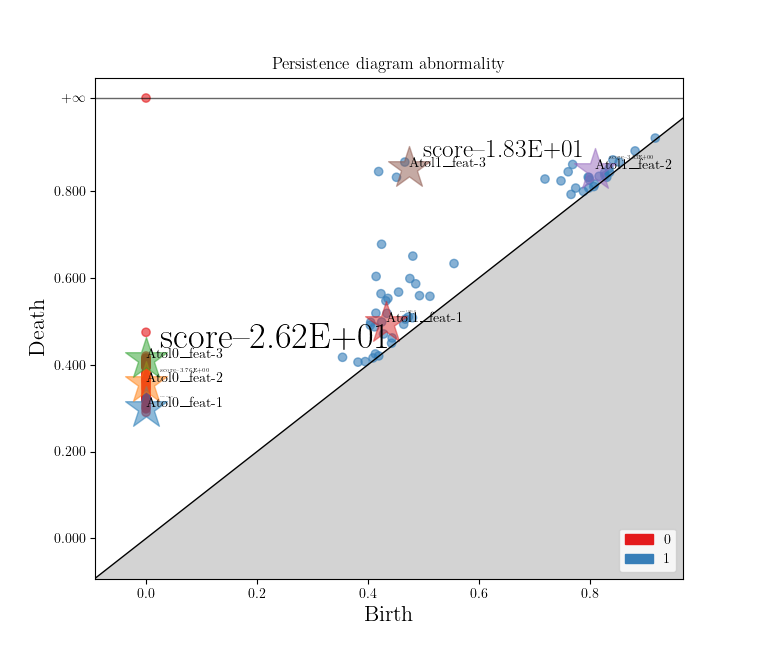

where are the estimated mean and covariance of the vectorization of Algorithm 4 (time indices are implied and ommited for this discussion). These scores can be interpreted as testing for anomalies with respect to a single embedding dimension as if the vectorization had independent components. These center-targeted scores allow to analyze an original anomaly by looking at the score deviations of each vector component. Because the vector components are integrated from a learnt centroid, the scores can be traced back to a specific region in , see for instance Figure 13.

This leads to valuable interpretation. For instance if an abnormal score of TADA were to be caused by a large deviation in a homology dimension 1 center-related component, it is likely that at that time an abnormal dependence cycle is created for a longer or shorter period of time than for the rest of the time series, therefore that the dependence pattern has globally changed in that period of time. See for instance an illustration on the Topological Wheels problem in Figure 13 where globally changing the dependence pattern between sensors is exactly how the abnormal data was produced. And in the case that the produced score is abnormal simply by virtue of a shift in several dimension 0 centers-related components, it signifies an anomaly in the connectivity dependence structure that does not affect the higher order homological features, therefore it could be attributed to a default (such as a breakdown) in one of the original sensors for instance.

5 Conclusion

It is common knowledge that no anomaly detection method can help with identifying all kinds of anomalies. The framework introduced in this paper is relevant for detecting abnormal topological changes in the dependence structure of data, and turns out to be competitive with respect to other state-of-the-art approaches on various benchmark data sets. Naturally, there are many different sorts of anomalies that the proposed method is not able to detect at all - for instance, as the topological embedding is invariant to graph isomorphism, any anomalies linked to node permutation (change of node labelling) cannot be caught. The same is true for homothetic jumps: when signals would simultaneously get identically multiplied, the correlation-based similarity matrix would remain unchanged, leading to unchanged topological embedding. While such invariances can be thought of as hindrances, they can also come as a welcome feature if those anomalies are in fact built-in the considered applied problem - for instance in the case of labeling uncertainties in sensors.

The topological anomaly detection finds anomalies that other methods do not seem to discover. It is generally understood that topological information is a form of global information that is complementary to the information gathered by more traditional approaches, e.g. spectral detectors. While confirming this, the above numerical experiment also suggest that topological information is commonly present in various real or synthetic datasets. Therefore for practical applied purposes it is probably best to use our method in combination with other dedicated methods, for instance one that focuses on ”local” data shifts such as the SubKNN method.

Focusing on the case of detection of anomalies in the dependence structure of multivariate time series, it appears that the only parameter that requires a careful tuning in our method is the window size (or temporal resolution) , as for most of existing procedures (see Section 4). Designing methods to empirically tune this window size, or to combine the outputs of our method at different resolutions would be a relevant addition to our work, that is left for future research.

Let us now emphasize the broader flexibility of the framework we introduce. First, it is not tied to detect changes in correlation structures: we may use Algorithm 1 with other dissimilarity measures between channels, and in fact we may build persistence diagrams from a time series of more general metric spaces - e.g. meshed shapes, images… - in the more general case (as done in Chazal et al. (2021) for graphs). Second, the vectorization we propose with Algorithm 2 and 4 does not necessarily take a sequence of persistence diagrams as input: any sequence of measures may be vectorized the same way. It may find applications in monitoring sequences of point processes realizations, as in evolution of distributions of species for instance - see, e.g., Renner et al. (2015). And finally, one may process the output of the vectorization procedure in other ways than building an anomaly score. For instance, using these vectorizations as inputs of any neural network, or change-points detection procedures such as KCP (Arlot et al. (2019)) could provide a dedicated method to retrieve change points of a global structure.

6 Acknowledgements

This work has been supported by the French government under the ”France 2030” program, as part of the SystemX Technological Research Institute within the Confiance.ai project. The authors also thank the ANR TopAI chair in Artificial Intelligence (ANR–19–CHIA–0001) for financial support.

The authors are grateful to Bernard Delyon for valuable comments and suggestions concerning convergence rates in -mixing cases.

7 Proofs

Most of the proposed results are adaptation of proofs in the independent case to the dependent one. A peculiar interest lies in concentration results in this framework, we list important ones in the following section.

7.1 Probabilistic tools for -mixing concentration

In the derivations to follow extensive use will be made of a consequence of Berbee’s Lemma.

Lemma 8

(Doukhan et al., 1995, Proposition 2) Let be a sequence of random variables taking their vales in a Polish space , and, for , denote by

Then there exists a sequence of independent random variables such that, for any , and have the same distribution and .

The above Lemma allows to translate standard concentration bounds from the i.i.d. framework to the dependent case, where dependency is seized in terms of -mixing coefficients.

Let us recall here the general definition of -mixing coefficients from Definition 4. For a sequence of random variables (not assumed stationary), the beta-mixing coefficient of order is

If the sequence is assumed to be stationary, may be written as

where denotes the total variation distance. We will make use of the following adaptation of Bernstein’s inequality to the dependent case.

Theorem 9

(Doukhan, 1994, Theorem 4) Let be a sequence of (real) variables with -mixing coefficients , that satisfies

-

1.

,

-

2.

,

-

3.

a.s..

Then, for every ,

To apply Theorem 9, a bound on the variance term is needed. Such bounds are available in the stationary case under slightly milder assumptions (see, e.g., Rio (1993)). For our purpose, a straightforward application of (Rio, 1993, Theorem 1.2, a)) will be sufficient, exposed below.

Lemma 10

Let denote a centered and stationary sequence of real variables with -mixing coefficients , such that a.s..

Then it holds

where .

7.2 Proofs for Section 3

7.2.1 Proof of Theorem 5

Proof [Proof of Theorem 5]

We begin by the proof of Theorem 5. It follows the proof of (Chazal et al., 2021, Theorem 9) in the i.i.d. case, with adaptations to cope with dependency using Lemma 8.

To apply Lemma 8, first note that the space , endowed with the Levy-Prokhorov metric, is a Polish space (see, e.g., (Prokhorov, 1956, Theorem 1.11)). Using Lemma 8 as in (Doukhan et al., 1995, Proof of Proposition 2) yields the existence of such that, denoting by (resp. ) the vector (resp. ), for , it holds:

-

•

For every has the same distribution as , and .

-

•

The random variables are independent, as well as the variables .

For any , we denote by (resp. ) the vector of centroids defined by, for all ,

where (resp. ) denotes (resp. ), adopting the convention when the corresponding cell weight is null.

The following lemma ensures that contracts toward , provided .

Lemma 11

With probability larger than , it holds, for every ,

where .

The proof of Lemma 11 is postponed to Section 7.2.3. Equipped with Lemma 11, we first prove recursively that, if , then w.h.p., for all . We let be defined as

Noting that , Markov inequality yields

Choosing in Lemma 11, for small enough yields, for large enough,

with probability larger than , provided . Denoting by the probability event onto which the above equation holds, a straightforward recursion entails that, if , then, for all , on .

Then, using Lemma 11 iteratively yields that, on , where , for all , provided ,

| (8) |

Theorem 5 now easily follows. For the first inequality, let , then, using Markov inequality again gives

Thus, the assumption entails that

with probability larger than that is larger than .

For the second inequality, denote by the random variable

and remark that (8) entails

We deduce that

which leads to

Noting that

and using

whenever leads to the result.

7.2.2 Proof of Theorem 6

Proof [Proof of Theorem 6] This proof follows the steps of (Chazal et al., 2021, Proof of Lemma 18).

As in the proof of Lemma 11, let be such that, denoting by (resp. ) the vector (resp. ), for , it holds:

-

•

For every has the same distribution as , and .

-

•

The random variables are independent, as well as the variables .

Let denote the event

A standard union bound yields that . On , the minibatches used by Algorithm 3 may be considered as independent, so that the main lines of (Chazal et al., 2021, Proof of Lemma 18) readily applies, replacing ’s by ’s. In what follows we let denote the output of the -th iteration of Algorithm 3 based on .

Assume that , and , for a large enough constant that only depends on , to be fixed later. For , let and denote the events

where . Then, according to Theorem 9 with and Lemma 10 to bound the corresponding , for , , for large enough.

Further, define

Then, provided that , where only depends on , we may prove recusively that

on whenever (first step of the proof of (Chazal et al., 2021, Lemma 18)).

Next, denoting by , we may write

with

recalling that . Proceeding as in (Chazal et al., 2021, Proof of Lemma 18), we may further bound

for some . Noticing that and yields that

Following (Chazal et al., 2021, Proof of Theorem 10), a standard recursion entails

for . At last, since , we conclude that

where and have been used.

7.2.3 Proof of Lemma 11

Proof [Proof of Lemma 11] Assume that , for some optimal . Then, for any , it holds

| (9) |

The first term of the right hand side may be controlled using a slight adaptation of (Chazal et al., 2021, Lemma 22).

Lemma 12

With probability larger than , for all and , it holds

where is an absolute constant. Moreover, with probability larger than , it holds

where is an absolute constant.

Proof [Proof of Lemma 12] We intend here to recover the standard i.i.d. bounds given in (Chazal et al., 2021, Lemma 22). To this aim, we let and be defined by

for , where is a measure in , with total number of support points bounded by , and remark that

Since , and the ’s are sums of independent measures evaluated on , we may readily apply (Chazal et al., 2021, Lemma 22) replacing by to each of them, leading to the deviation bounds on the ’s.

For the third inequality of Lemma 12, denoting by

for , it holds, for any ,

Since each of the ’s are i.i.d. sums of discrete measures (the ’s), (Chazal et al., 2021, Lemma 22) readily applies (with sample size ), giving the result.

We now proceed with the first term in (9) as in (Chazal et al., 2021, Proof of Lemma 17). Using the first two inequalities of Lemma 12 with yields a probability event onto which

Combining this with the inequality of Lemma 12 yields, for large enough and all , with probability larger than ,

| (10) |

The precise derivation of (10) may be found in (Chazal et al., 2021, Proof of Lemma 17, pp.34-35). Plugging (10) into (9) leads to, for a small enough ,

with probability larger than .

It remains to control the last term . To do so, note that, for every ,

| (11) |

and

On , it holds, for every ,

Squaring and taking the sum with respect to gives the result.

7.2.4 Proof of Proposition 7

Proof [Proof of Proposition 7] Let denote the sequence , that is a stationary -mixing sequence of real-valued random variables. For , we let

and , and be such that . In the i.i.d. case, we might bound using a standard inequality such as in (Boucheron et al., 2005, Section 5.1.2).

As for the proofs of Theorem 5 and 6, we compare with the i.i.d. case by introducing auxiliary variables.

We let be such that, denoting by (resp. ) the vector (resp. ), it holds

-

•

For every , and .

-

•

are independent, as well as .

Let denote . Then, for any , we have

If is the event , that has probability larger than (using Markov inequality as before), then on it readily holds

so that we may write, on the same event,

| (12) |

It remains to control the stochastic term . To do so, we denote by

for and . Note that, for any , ’s are i.i.d., take values in , and have expectation . Next, we define, for and ,

and we note that . Since the ’s are sums of i.i.d. random variables, the following concentration bound follows.

Lemma 13

For , and such that , it holds

7.2.5 Proof of Lemma 13

Proof [Proof of Lemma 13] The proof follows the one of (Chazal et al., 2021, Lemma 22) verbatim, at the exception of the capacity bound, that we discuss now. To lighten notation we assume that we have a sample of ’s, with , and we consider the set of functionals

Following (Chazal et al., 2021, Lemma 22), if denotes the cardinality of , we have to bound

where the ’s are i.i.d. copies of the ’s. Since, for every , recalling that , it holds

we deduce that

The remaining of the proof follows verbatim (Chazal et al., 2021, Lemma 22).

References

- Adams et al. (2017) H. Adams, T. Emerson, M. Kirby, R. Neville, C. Peterson, P. Shipman, S. Chepushtanova, E. Hanson, F. Motta, and L. Ziegelmeier. Persistence images: a stable vector representation of persistent homology. J. Mach. Learn. Res., 18:Paper No. 8, 35, 2017. ISSN 1532-4435.

- Agarwal and Duchi (2013) A. Agarwal and J. C. Duchi. The generalization ability of online algorithms for dependent data. IEEE Trans. Inform. Theory, 59(1):573–587, 2013. ISSN 0018-9448,1557-9654. doi: 10.1109/TIT.2012.2212414. URL https://doi.org/10.1109/TIT.2012.2212414.

- Arlot et al. (2019) S. Arlot, A. Celisse, and Z. Harchaoui. A kernel multiple change-point algorithm via model selection. J. Mach. Learn. Res., 20:Paper No. 162, 56, 2019. ISSN 1532-4435,1533-7928.

- Boissonnat et al. (2018) J.-D. Boissonnat, F. Chazal, and M. Yvinec. Geometric and Topological Inference, volume 57. Cambridge University Press, 2018.

- Boucheron et al. (2005) S. Boucheron, O. Bousquet, and G. Lugosi. Theory of classification: a survey of some recent advances. ESAIM Probab. Stat., 9:323–375, 2005. ISSN 1292-8100,1262-3318. doi: 10.1051/ps:2005018. URL https://doi.org/10.1051/ps:2005018.

- Bourakna et al. (2022) A. E. Y. Bourakna, M. K. Chung, and H. Ombao. Modeling and simulating dependence in networks using topological data analysis, 2022.

- Brécheteau et al. (2021) C. Brécheteau, A. Fischer, and C. Levrard. Robust Bregman clustering. The Annals of Statistics, 49(3):1679 – 1701, 2021. doi: 10.1214/20-AOS2018. URL https://doi.org/10.1214/20-AOS2018.

- Breiman (2001-10) L. Breiman. Random forests. 45:5–32, 2001-10. doi: 10.1023/A:1010950718922.

- Bruillard et al. (2016) P. Bruillard, K. Nowak, and E. Purvine. Anomaly detection using persistent homology. In 2016 Cybersecurity Symposium (CYBERSEC), pages 7–12, Los Alamitos, CA, USA, apr 2016. IEEE Computer Society. doi: 10.1109/CYBERSEC.2016.009. URL https://doi.ieeecomputersociety.org/10.1109/CYBERSEC.2016.009.

- Chazal and Divol (2018) F. Chazal and V. Divol. The density of expected persistence diagrams and its kernel based estimation. In 34th International Symposium on Computational Geometry, volume 99 of LIPIcs. Leibniz Int. Proc. Inform., pages Art. No. 26, 15. Schloss Dagstuhl. Leibniz-Zent. Inform., Wadern, 2018.

- Chazal and Michel (2021) F. Chazal and B. Michel. An introduction to topological data analysis: fundamental and practical aspects for data scientists. Frontiers in artificial intelligence, 4:108, 2021.

- Chazal et al. (2014) F. Chazal, V. de Silva, and S. Oudot. Persistence stability for geometric complexes. Geometriae Dedicata, 173(1):193–214, 2014.

- Chazal et al. (2016) F. Chazal, V. de Silva, M. Glisse, and S. Oudot. The structure and stability of persistence modules. Springer International Publishing, 2016.

- Chazal et al. (2021) F. Chazal, C. Levrard, and M. Royer. Clustering of measures via mean measure quantization. Electronic Journal of Statistics, 15(1):2060 – 2104, 2021. doi: 10.1214/21-EJS1834. URL https://doi.org/10.1214/21-EJS1834.

- Chrétien et al. (2024) S. Chrétien, B. Gao, A. Thebault-Guiochon, and R. Vaucher. Time topological analysis of eeg using signature theory, 2024.

- Dindin et al. (2019) M. Dindin, Y. Umeda, and F. Chazal. Topological data analysis for arrhythmia detection through modular neural networks, 2019.

- Doukhan (1994) P. Doukhan. Mixing, volume 85 of Lecture Notes in Statistics. Springer-Verlag, New York, 1994. ISBN 0-387-94214-9. doi: 10.1007/978-1-4612-2642-0. URL https://doi.org/10.1007/978-1-4612-2642-0. Properties and examples.

- Doukhan et al. (1995) P. Doukhan, P. Massart, and E. Rio. Invariance principles for absolutely regular empirical processes. Ann. Inst. H. Poincaré Probab. Statist., 31(2):393–427, 1995. ISSN 0246-0203. URL http://www.numdam.org/item?id=AIHPB_1995__31_2_393_0.

- Edelsbrunner and Harer (2010) H. Edelsbrunner and J. Harer. Computational topology: an introduction. American Mathematical Society, 2010.

- G. et al. (2014) P. G., E. P., T. F., C.-H. R., N. D., H. P.J., and V. F. Homological scaffolds of brain functional networks. Journal of the Royal Society Interface, 11(101), 2014. doi: 10.1098/rsif.2014.0873.

- Heim and Avery (2019) N. Heim and J. E. Avery. Adaptive anomaly detection in chaotic time series with a spatially aware echo state network. ArXiv, abs/1909.01709, 2019. URL https://api.semanticscholar.org/CorpusID:202541761.

- Herbold (2020) S. Herbold. Autorank: A python package for automated ranking of classifiers. Journal of Open Source Software, 5(48):2173, 2020. doi: 10.21105/joss.02173. URL https://doi.org/10.21105/joss.02173.

- Ho et al. (2023) T. K. K. Ho, A. Karami, and N. Armanfard. Graph-based time-series anomaly detection: A survey. arXiv preprint arXiv:2302.00058, 2023.

- Hubert et al. (2018) M. Hubert, M. Debruyne, and P. J. Rousseeuw. Minimum covariance determinant and extensions. Wiley Interdiscip. Rev. Comput. Stat., 10(3):e1421, 11, 2018. ISSN 1939-5108,1939-0068. doi: 10.1002/wics.1421. URL https://doi.org/10.1002/wics.1421.

- Jacob et al. (2021-07) V. Jacob, F. Song, A. Stiegler, B. Rad, Y. Diao, and N. Tatbul. Exathlon: a benchmark for explainable anomaly detection over time series. 14(11):2613–2626, 2021-07. ISSN 2150-8097. doi: 10.14778/3476249.3476307. URL https://doi.org/10.14778/3476249.3476307.

- Jana et al. (2024) S. Jana, J. Fan, and S. Kulkarni. A general theory for robust clustering via trimmed mean, 2024.

- Levrard (2015) C. Levrard. Nonasymptotic bounds for vector quantization in hilbert spaces. Ann. Statist., 43(2):592–619, 04 2015. doi: 10.1214/14-AOS1293. URL https://doi.org/10.1214/14-AOS1293.

- Levrard (2018) C. Levrard. Quantization/clustering: when and why does k-means work. Journal de la Société Française de Statistiques, 159(1), 2018.

- Li et al. (2022) S. Li, W. Song, C. Zhao, Y. Zhang, W. Shen, J. Hai, J. Lu, and Y. Xie. An anomaly detection method for multiple time series based on similarity measurement and louvain algorithm. Procedia Computer Science, 200:1857–1866, 2022.

- Liu et al. (2008) F. T. Liu, K. M. Ting, and Z.-H. Zhou. Isolation forest. In 2008 Eighth IEEE International Conference on Data Mining, pages 413–422, 2008. doi: 10.1109/ICDM.2008.17.

- McDonald et al. (2015) D. J. McDonald, C. R. Shalizi, and M. Schervish. Estimating beta-mixing coefficients via histograms. Electron. J. Stat., 9(2):2855–2883, 2015. ISSN 1935-7524. doi: 10.1214/15-EJS1094. URL https://doi.org/10.1214/15-EJS1094.

- Mohammed et al. (2023) A. H. Mohammed, M. Cabrerizo, A. Pinzon, I. Yaylali, P. Jayakar, and M. Adjouadi. Graph neural networks in eeg spike detection. Artificial Intelligence in Medicine, 145:102663, 2023. ISSN 0933-3657. doi: https://doi.org/10.1016/j.artmed.2023.102663. URL https://www.sciencedirect.com/science/article/pii/S093336572300177X.

- Mohri and Rostamizadeh (2010) M. Mohri and A. Rostamizadeh. Stability bounds for stationary -mixing and -mixing processes. J. Mach. Learn. Res., 11:789–814, 2010. ISSN 1532-4435,1533-7928.

- Ombao and Pinto (2021) H. Ombao and M. Pinto. Spectral dependence, 2021.

- Paparrizos et al. (2022a) J. Paparrizos, P. Boniol, T. Palpanas, R. S. Tsay, A. Elmore, and M. J. Franklin. Volume under the surface: a new accuracy evaluation measure for time-series anomaly detection. Proc. VLDB Endow., 15(11):2774–2787, jul 2022a. ISSN 2150-8097. doi: 10.14778/3551793.3551830. URL https://doi.org/10.14778/3551793.3551830.

- Paparrizos et al. (2022b) J. Paparrizos, Y. Kang, P. Boniol, R. S. Tsay, T. Palpanas, and M. J. Franklin. Tsb-uad: an end-to-end benchmark suite for univariate time-series anomaly detection. Proc. VLDB Endow., 15(8):1697–1711, apr 2022b. ISSN 2150-8097. doi: 10.14778/3529337.3529354. URL https://doi.org/10.14778/3529337.3529354.

- Pedregosa et al. (2011) F. Pedregosa, G. Varoquaux, A. Gramfort, V. Michel, B. Thirion, O. Grisel, M. Blondel, P. Prettenhofer, R. Weiss, V. Dubourg, J. Vanderplas, A. Passos, D. Cournapeau, M. Brucher, M. Perrot, and E. Duchesnay. Scikit-learn: Machine learning in Python. Journal of Machine Learning Research, 12:2825–2830, 2011.

- Pham and Tran (1985) T. D. Pham and L. T. Tran. Some mixing properties of time series models. Stochastic Process. Appl., 19(2):297–303, 1985. ISSN 0304-4149,1879-209X. doi: 10.1016/0304-4149(85)90031-6. URL https://doi.org/10.1016/0304-4149(85)90031-6.

- Prokhorov (1956) Y. V. Prokhorov. Convergence of random processes and limit theorems in probability theory. Teor. Veroyatnost. i Primenen., 1:177–238, 1956. ISSN 0040-361X.

- Ravishanker and Chen (2019) N. Ravishanker and R. Chen. Topological data analysis (tda) for time series, 2019.

- Renner et al. (2015) I. W. Renner, J. Elith, A. Baddeley, W. Fithian, T. Hastie, S. J. Phillips, G. Popovic, and D. I. Warton. Point process models for presence-only analysis. Methods in Ecology and Evolution, 6(4):366–379, 2015. doi: 10.1111/2041-210X.12352. URL https://besjournals.onlinelibrary.wiley.com/doi/abs/10.1111/2041-210X.12352.

- Rio (1993) E. Rio. Covariance inequalities for strongly mixing processes. Ann. Inst. H. Poincaré Probab. Statist., 29(4):587–597, 1993. ISSN 0246-0203. URL http://www.numdam.org/item?id=AIHPB_1993__29_4_587_0.

- Rousseeuw and Driessen (1999) P. J. Rousseeuw and K. V. Driessen. A fast algorithm for the minimum covariance determinant estimator. Technometrics, 41(3):212–223, 1999. doi: 10.1080/00401706.1999.10485670. URL https://www.tandfonline.com/doi/abs/10.1080/00401706.1999.10485670.

- Royer et al. (2021) M. Royer, F. Chazal, C. Levrard, Y. Umeda, and Y. Ike. Atol: Measure vectorization for automatic topologically-oriented learning. In A. Banerjee and K. Fukumizu, editors, Proceedings of The 24th International Conference on Artificial Intelligence and Statistics, volume 130 of Proceedings of Machine Learning Research, pages 1000–1008. PMLR, 13–15 Apr 2021. URL https://proceedings.mlr.press/v130/royer21a.html.

- Schmidl et al. (2022) S. Schmidl, P. Wenig, and T. Papenbrock. Anomaly detection in time series: A comprehensive evaluation. Proceedings of the VLDB Endowment (PVLDB), 15(9):1779–1797, 2022. doi: 10.14778/3538598.3538602.

- Sørbø and Ruocco (2023) S. Sørbø and M. Ruocco. Navigating the metric maze: a taxonomy of evaluation metrics for anomaly detection in time series. Data Mining and Knowledge Discovery, pages 1–42, 11 2023. doi: 10.1007/s10618-023-00988-8.

- Tang and Monteleoni (2016) C. Tang and C. Monteleoni. On lloyd’s algorithm: New theoretical insights for clustering in practice. In A. Gretton and C. C. Robert, editors, Proceedings of the 19th International Conference on Artificial Intelligence and Statistics, volume 51 of Proceedings of Machine Learning Research, pages 1280–1289, Cadiz, Spain, 09–11 May 2016. PMLR. URL http://proceedings.mlr.press/v51/tang16b.html.

- The GUDHI Project (2015) The GUDHI Project. GUDHI User and Reference Manual. GUDHI Editorial Board, 2015. URL http://gudhi.gforge.inria.fr/doc/latest/.

- Umeda et al. (2019) Y. Umeda, J. Kaneko, H. Kikuchi, and D. Kikuchi. Topological data analysis and its application to time-series data analysis. 2019. URL https://api.semanticscholar.org/CorpusID:225065707.

- Wenig et al. (2022) P. Wenig, S. Schmidl, and T. Papenbrock. Timeeval: A benchmarking toolkit for time series anomaly detection algorithms. Proceedings of the VLDB Endowment (PVLDB), 15(12):3678–3681, 2022. doi: 10.14778/3554821.3554873.

- Yairi et al. (2001) T. Yairi, Y. Kato, and K. Hori. Fault detection by mining association rules from house-keeping data. 2001.

- Zheng et al. (2023) Y. Zheng, H. Y. Koh, M. Jin, L. Chi, K. T. Phan, S. Pan, Y.-P. P. Chen, and W. Xiang. Correlation-aware spatial–temporal graph learning for multivariate time-series anomaly detection. IEEE Transactions on Neural Networks and Learning Systems, 2023.