By Fair Means or Foul: Quantifying Collusion in a Market Simulation with Deep Reinforcement Learning

Abstract

In the rapidly evolving landscape of eCommerce, Artificial Intelligence (AI) based pricing algorithms, particularly those utilizing Reinforcement Learning (RL), are becoming increasingly prevalent. This rise has led to an inextricable pricing situation with the potential for market collusion. Our research employs an experimental oligopoly model of repeated price competition, systematically varying the environment to cover scenarios from basic economic theory to subjective consumer demand preferences. We also introduce a novel demand framework that enables the implementation of various demand models, allowing for a weighted blending of different models. In contrast to existing research in this domain, we aim to investigate the strategies and emerging pricing patterns developed by the agents, which may lead to a collusive outcome. Furthermore, we investigate a scenario where agents cannot observe their competitors’ prices. Finally, we provide a comprehensive legal analysis across all scenarios. Our findings indicate that RL-based AI agents converge to a collusive state characterized by the charging of supracompetitive prices, without necessarily requiring inter-agent communication. Implementing alternative RL algorithms, altering the number of agents or simulation settings, and restricting the scope of the agents’ observation space does not significantly impact the collusive market outcome behavior.

1 Introduction

The usage of pricing algorithm technologies has become ubiquitous within the realm of ECommerce platforms. In the last decade, these algorithms have shifted from static heuristics to AI-driven software that outperforms them in terms of average daily profits Kropp et al. (2019); Qiao et al. (2024). Studies have already shown that in certain markets it is unreasonable to conduct business at a profitable level lacking this technology, as algorithmic price setting frequencies create a significant competitive edge Assad et al. (2020).

Nevertheless, there is concern that these conditions harm competition and thus consumer welfare: The use of AI-based pricing algorithms often results in an inextricable pricing situation with a collusive market outcome. If the emergence of this collusive market outcome can be attributed to any form of concerted action, it gives rise to significant legal and ethical apprehensions.111For a more detailed introduction to Art. 101 Treaty on the Functioning of the European Union (”TFEU”), see Schlechtinger et al., Schlechtinger et al. (2021). There is a necessity to explore the factors that contribute to the collusive market outcome of RL agents and shed light on the vulnerabilities and potential risks associated with their deployment in pricing algorithms. In pursuit of this goal, we endeavor to elucidate their underlying mechanisms and enhance the transparency and comprehensibility of coordinative AI-pricing strategies.

If no such coordination can be identified, the collusive market outcome generally must be considered legally neutral. While collusion may harm consumers, it is considered undesirable for innovation and economic growth from a welfare economic standpoint. The challenge from a doctrinal perspective lies in the difficulty of attributing legal responsibility directly to a market outcome Commission (2011).

This evokes three major legal questions. First, does the agent’s behavior constitute a minimum degree of coordination and thus violate the cartel prohibition under existing German and European competition law? Second, do the existing rules readily fit an algorithmic conduct or do we face a regulatory gap within the cartel prohibition? Third, should we expand cartel law to encompass algorithmic collusion?

2 Related Work

Drawing from economic and AI literature presents tendencies of AI-based algorithms to reach seemingly collusive outcomes. As such, Calvano et al. Calvano et al. (2018) provide fundamentals for algorithmic pricing studies. While preceding research usually formulated a Cournot oligopoly model where two agents sell certain quantities of a good Waltman and Kaymak (2008); Kimbrough and Murphy (2009); Siallagan et al. (2013), they transitioned towards a simplified oligopoly model based on a Bertrand price setting scenario. The agents used q-learning to “consistently learn to charge supracompetitive prices, without communicating with one another”. The main contribution of this research is the illustration of a reward-punishment scheme among autonomous pricing agents. By manually precipitating exogenous price cuts for selected agents, the study shows that the algorithms are able to punish any behavior that deviates from a collusive state in order to gradually return back to it.

Other scholars investigated the issue by adding human participants Werner (2021), by specifically analyzing sizes of discrete action spaces Klein (2021), or by building custom, more elaborate scenarios Abada and Lambin (2023). Few researchers applied deep neural networks. The ones that did, were able to improve on Calvano et al. Calvano et al. (2018) by achieving a shorter learning time due to the usage of deep Q-Networks as well as reward averaging Hettich (2021). Others restricted algorithms to only memorize the periods when they do not exceed in terms of profits and ignored the ones when they outperform. Scholars, nevertheless, emphasize that “more efforts are needed in exploring other architectures of deep networks” Han (2021). Due to the characteristic learning behavior of RL-algorithms or AI, the quality of learning data significantly influences agents’ propensity for collusion. To test this hypothesis, some scholars employed a simple upper confidence bound bandit algorithm to set a discrete number of prices Hansen et al. (2020). Their outcome indicated that the prices are bound to the signal-to-noise ratio of their inputs, resulting in a supracompetitive state for less noisy input data and vice versa.

The current state of research is mainly simulation-based, with few scholars collecting empirical data. An investigation into Germany’s retail gas market, conducted using a catalog of potential characteristics, identified widespread adoption of pricing algorithms since 2016. Consequently, sellers achieved margins above competitive levels. As their data indicates no initial effects, followed by an eventual convergence to high prices and margins, they infer that the algorithms were able to learn tacitly collusive strategies over time Assad et al. (2020). Brown and MacKay Brown and MacKay (2021) tackle the issue from a different angle. The authors extract pricing data from five pharmacy firms with differing price changing frequencies Brown and MacKay (2021). Musolff Musolff (2022) employs a dataset acquired from Amazon’s buybox, an algorithmic pricing-heavy feature used by third-party sellers, to show that repricers have been able to avoid the competitive behavior by regular price raises.

In essence, the major shortcomings of current research are the substantial deviation from realistic market models, the over-representation of tabular q-learning, a comprehensive legal analysis of the experiments, as well as the low density of empirical studies. Our work aims to bridge the gap between real-world empirical analyses and purely theoretic models by providing a simplified, but scalable market simulation. Thus, we propose a novel demand framework that enables the implementation of various demand models and facilitates integration between them, allowing for a weighted blending of different models. Within the framework, we investigate the behavior of a scalable amount of agents that rely on state-of-the-art deep reinforcement learning technologies (i.e., PPO, DQN). By understanding the underlying causes of collusive outcomes using an interdisciplinary approach, we contribute to the ongoing efforts of building AI systems that align with societal values and objectives.

3 Experiment Design

We consider an oligopoly setting at the core of our experiments. This fundamental stage game comprises consumers and firms that simultaneously set the prices so that holds for all . Accordingly, we define a general selling or demand probability as follows:

| (1) |

The parameter represents the buyers’ background knowledge, allowing an implementation of a custom buying probability. For example, might entail domain data such as the demand function of a market, leading to new demand probabilities. Given and , we can then define a Bertrand selling probability via

| (2) |

thus exclusively depending on the prices . According to Bertrand Bertrand (1883), sellers will end up in a Nash equilibrium, represented by a price equal to the marginal costs (i.e., the competitive price) due to the buyers consistently purchasing the lowest-priced product. In a classic Bertrand oligopoly setting, the goods are characterized as perfect substitutes. However, this buying behavior is based on a theoretic construct as homogeneous goods may still be acquired from diverging sellers due to subjective consumer preferences in a realistic scenario. We aim to counteract this shortcoming from two sides. Legal research states that a relevant product market comprises all those products and services which are regarded as interchangeable or substitutable by the consumer, because of the products‘ characteristics, their prices, and their intended use 447/98 (1998). To combat this from an IT perspective, we used a selection strategy proposed by Zhong et al. (2005). While solely relying on prices, this approach allows us to create a simulation that counteracts the Bertrand model’s main limitation: Its extremely punishing nature, which might complicate the learning process or force the agents into a collusive state. Furthermore, with the roulette wheel, we can model switching barriers (i.e., expenses consumers feel they experience by switching from one alternative to another). Based on as the maximum price achievable in a market scenario, this modification results in the buying behavior

| (3) |

In order to bridge theory and empiricism, we introduce the factor . serves as a weight to gradually transition from one buying behavior to another. With this work, we combine the previously defined selection strategies in (2) and in (3) with by means of

|

|

(4) |

Due to this specific combination, acts as a bias.222We restrict to and in this work. However this approach can be analogously extended to buying behaviours via biases if . If it is set to 1, the products are perfect substitutes, if it is set to 0, the consumers’ buying behavior is regulated by the roulette selection (this means and ). With this in mind, we can switch from a theoretical Bertrand model to a more realistic setting, that involves subjective consumer preferences.

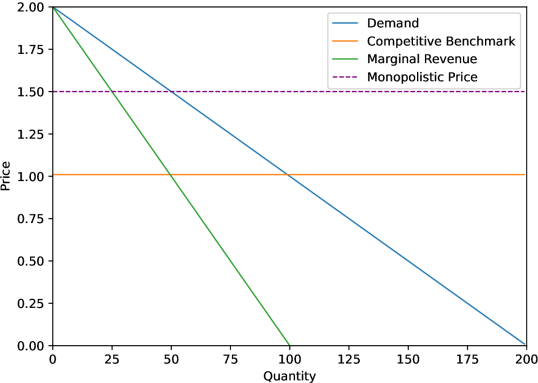

With the parameters set, a seller can achieve a monopolistic price (MP) (i.e., the price that relates to the maximum revenue a monopolist can achieve in the market) of 1.50 (with a cumulative quantity of 50) and a competitive benchmark (CB) (i.e., the price one unit above the marginal costs) of 1.01 (with a cumulative quantity of 99) (cf. Figure 1). To create comparable results, we restrict the number of consumers to and thus result in a maximum price . We chose these specific model settings based on the demand function. We need to choose arbitrary confinements in order to satisfy the presented economic rules. The agents can set prices above and below these confinements.

3.1 Deep Reinforcement Learning Algorithms

While the implementation and analysis of deep RL algorithms are more complex, we benefit from conditions that more likely resemble state-of-the-art pricing algorithms, as the number of possible states and variables of a real-world market environment most likely overstrain basic reinforcement learning tables. By including multiple, heterogeneous RL technologies we aim to scrutinize the robustness of our results further. However, our selection is confined to model-free methods as these are generally more popular, quicker to implement, and more extensively developed and tested than model-based methods Achiam (2018). Our selection includes Deep Q-Networks (DQN) Mnih et al. (2013) and Proximal Policy Optimization (PPO) Schulman et al. (2017) with the intention of featuring an algorithm for both sides of the model-free taxonomy (q-learning and policy optimization). The algorithms also support the use of discrete action spaces, reducing the number of possible error sources.

3.2 Markov Decision Process

When an agent tries to maximize its interests from the economic environment, it must consider both the reward it receives after each action and the feedback from the environment. This can be simplified as a Markov Decision Process (MDP) van Otterlo and Wiering (2012), more specifically, a Partially Observable Markov Process (POMDP) Hausknecht et al. (2015) due to the multi-agent environment hiding sensitive information from the competitors. We choose this method, as the main issue of this paper can only be solved by various agents conducting subjective observations, due to which future game states will depend on more than just a single agent’s current input. As MDPs are step-based and our previous illustrations were more general, we introduce time step to our established settings. We consider a sequential decision-making problem in which every agent (seller) interacts with a stochastic Multi-Agent Reinforcement Learning (MARL) environment. Each agent at time step observes a state where is the price set by agent at time , are the costs to purchase a good and is the global state space. For every time , an agent takes an action where is the valid, discrete action space, and executes it in the environment to receive a reward

| (5) |

where is the previously defined selling or demand probability at time . Given the state at time step t, the new state is to be reached after carrying out the actions with the probabilities . For a fixed timestamp , the goal of every agent is to determine a policy with and , that maximizes the long-term reward:

| (6) |

where is a discount factor for time period .

3.3 Preprocessing and Model Architecture

The RL agents are set up using a slight variation of the same baseline parametrization333cf. Raflin et al., Raffin et al. (2021) to see tested implementations and baseline parametrization for several RL algorithms. as we aim to keep our experiment as general as possible to ensure fungibility in different environments. In order to decrease the number of actions and thus simplify the action selection process, we decided to use a discrete action space. Compared to current literature444cf. Calvano et al., Calvano et al. (2018) and Hettich Hettich (2021) for other discrete (deep) q-learning action space implementations., however, actions are selected based on the price set in the last episode for an agent . In order to discretize the actions (i.e., the price) within the economic environment, we generate an evenly-spaced logarithmic distribution. The new price is calculated as follows:

| (7) |

For the sake of reducing complexity as well as computational cost we restrict the action space to a size of and the maximum adjustment of a price step to 2, resulting in the discrete action space 555We also test different action space sizes (i.e., 21, 51, and 71 actions). Please refer to the technical appendix at github.com/mschlechtinger/PriceOfAlgorithmicPricing.. Hence, they will be able to keep the same price or evoke an increase or decrease within 3 gradients (small/ moderate/ big adjustment). We choose a Softplus activation in order to restrict the agents from setting prices below 0 while facilitating a derivation of the function (as opposed to ReLU). In order to counteract potential price rises due to the Softplus activation and to improve the overall robustness of the learning process, we restrict the randomizer to initialize the prices randomly from the interval each at the beginning of every episode. Although we track the agents’ capital, they are able to accumulate debts without any consequences in the game, which yields more efficient learning.

4 Experiments

We investigate collusion in two scenarios. Our baseline scenario Scenario A depicts three agents that act based on decisions proposed by their given algorithm. In Scenario B we manipulate each agent’s state so that they are only able to observe their own prices as opposed to every price on the market. With this experimental setup, we can investigate whether the algorithms change their behavior when the experimental setup makes it more difficult to achieve collusion (i.e., in Scenario B). We apply Ray’s RLlIB to profit from an open-source, industry-standard RL-algorithm implementations.666To ensure full reproducibility, we attached the code to this work at github.com/mschlechtinger/PriceOfAlgorithmicPricing.

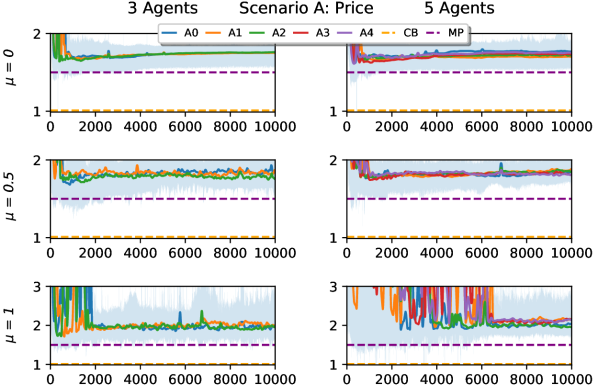

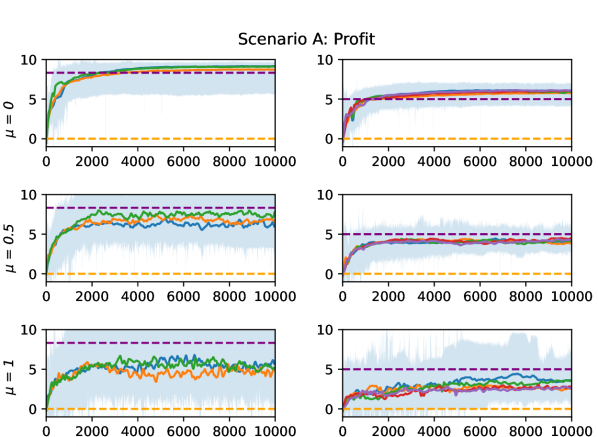

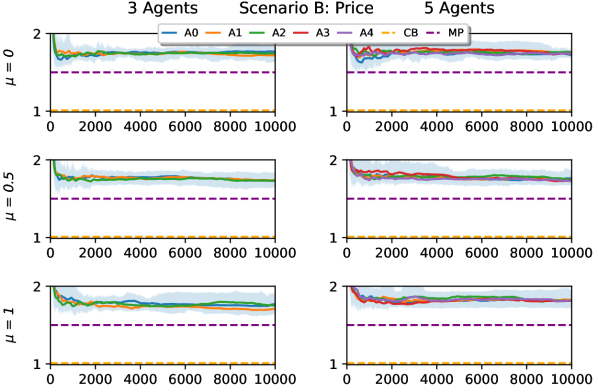

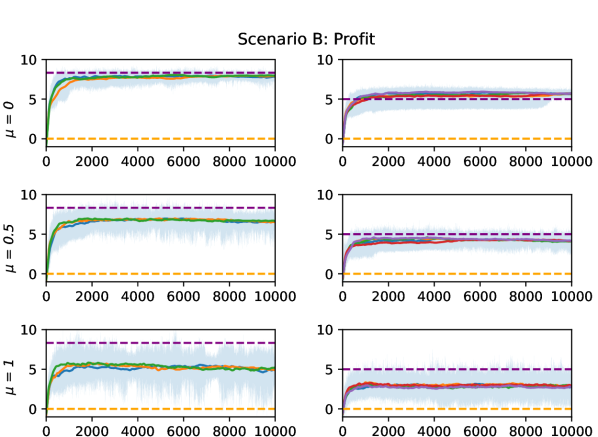

Each scenario is made up of several sub-scenarios, where we vary the number of agents (3, 5), the algorithm (PPO, DQN), and the biases . Every run is repeated 5 times to control for outliers, resulting in 90 runs overall (60 for Scenario A, 30 for Scenario B). A run comprises 10000 episodes with 365 steps each. We average the prices of every step to an episode price as well as a step profit (average profit of all steps in an episode) before averaging every run within the same setting. Finally, we apply locally-weighted scatterplot smoothing Royston (1992) to the averaged data. In addition to the agent data, the graphs incorporate the competitive benchmark (CB i.e., 1.01) as well as the monopolistic price (MP i.e., 1.50). On the other hand, the monopolistic profit (also abbreviated as MP) shown in the profit graphs is calculated by computing the profit a single seller would make by selling at the monopolistic price, divided by the number of sellers. If the agents converge to a price above the competitive benchmark (i.e., the Bertrand Equilibrium), economists classify this as a collusive market outcome. We assume that in practice, ECommerce companies would likely utilize similar pricing software due to the prevalence of a leading product. We thus focus on the interaction between similar agents. However, we challenge these settings by adjusting the neural network neurons, the algorithm’s learning rate, the number of agents as well as their time of entry, or the number of action gradients within the scope of an ablation study expounded upon in the technical appendix.

Due to our modified way of action space discretization, we define convergence in a slightly different way than previous literature Calvano et al. (2018). A run converges if the rolling standard deviation of the mean agents’ prices falls below a threshold of 0.01 for more than 100 episodes and this state lasts until the end of a run. If reaches a value above the threshold of 0.01, we restart the counter. If it lasts below the threshold, we define this as episodes until convergence . There is a legal implication in the chosen definition of convergence phases, as during cartel cases, jurists generally attempt to identify phases during a run in which the risk of collusive behavior is especially high. Unlike human collusive behavior, which can mostly be traced back to certain collusive acts, algorithmic collusion is not induced by one single action, but by specific episodic phases. Our definition of convergence is one possible attempt to narrow down critical phases that qualify as collusion.

To generate a factor for measuring a degree of collusion in an economic sense, we need a consistent measure across all simulations. In line with Calvano et al. Calvano et al. (2018), we calculate the average profit gain of all firms in a run , defined as

| (8) |

where represents the average profit upon convergence of all firms (i.e., after passing every ), is the profit in the Bertrand-Nash static equilibrium (i.e., the competitive benchmark), and constitutes the profit in a state of perfect collusion (i.e., the monopoly price). Thus, corresponds to the competitive outcome and to the perfectly collusive outcome. It is important to mention that collusion in an economic sense does not imperatively indicate collusion in a legal sense, however, it can be an indicator of the latter.

4.1 Scenario A: Competition

Scenario A represents the main competitive setting of this research. Every agent operates based on the decisions computed by its own algorithms and their neural networks. In various sub-scenarios, we employed three and five agents, averaging data generated by PPO and DQN algorithms.

Figure 2 presents the consolidated outcome of the runs through the price settings of three and five sellers on the left and right sides respectively. The pale blue area in each graph represents the variance of the runs. Although the competing agents exhibit distinct responses to the three bias weightings, each scenario leads to cooperative behavior that yields a supracompetitive price equilibrium in the long-term. These prices exceed the monopolistic price on average. However, the further we increase the price sensitivity () the higher the price-variance. We observe a similar, yet more extreme behavior when enhancing the number of sellers. The profit data (cf. Figure 2) asserts these observations; the increased variance also significantly reduces earnings.

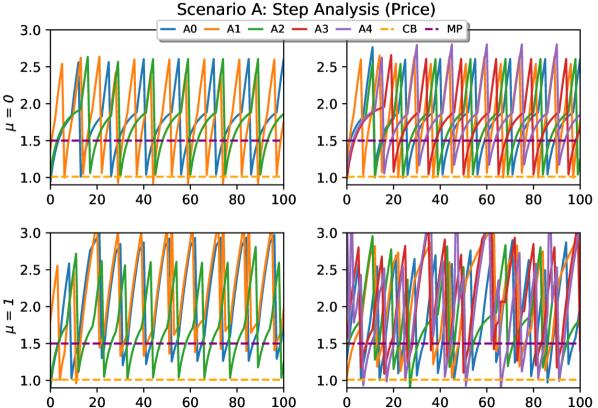

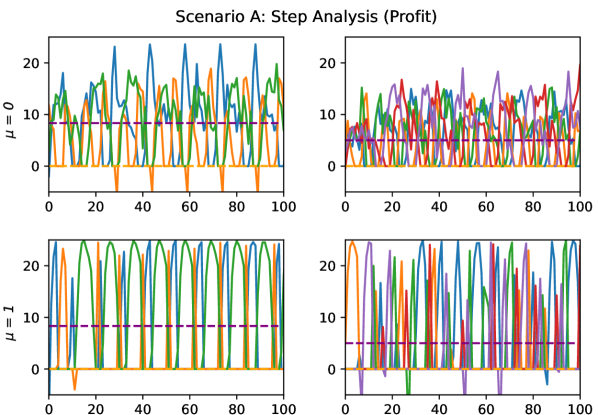

To further scrutinize these results, we extracted the prices set and profits accumulated during the first 100 steps of the last episode in Figure 3. Compared to the averaged episode overview, we can observe a price-setting behavior resembling an oscillation pattern, starting with a random price predefined by the environment. The agents occasionally slightly diverge from this cycle, however after a few steps, they usually get back in sync. These patterns explain why the prices exceed the monopolistic price on average; the agents find a strategy to collectively act as a monopolist on the market. To achieve this in a collaborative way, they traverse through three stages of pricing that are fundamentally the same but differ in execution in both and . Initially, prices are set in close proximity to the competitive benchmark. Subsequently, prices are gradually escalated until a certain threshold is reached, beyond which they surpass the point of consumer demand saturation. Then, they return below the MP. The presented strategy exploits the boundaries set by the simulation by always having one agent earning the maximum. When and they abuse the lowered price sensitivity to create an increased demand with a higher price, thus maximizing the joint profit and exceeding the profit a monopolist would be able to achieve (i.e., ). Similar patterns are discernible in instances where . Notably, due to heightened price sensitivity, agents are unable to effectively stimulate increased demand. As a result, the agents endeavor to establish a monopolistic pricing regime, whereby two agents adopt prices above the threshold of , while the third agent attempts to set a price near (i.e., ), with the objective of maximizing the joint profit. Although the oscillation patterns tend to remain consistent upon increasing the number of agents, identifying collaborative behaviors becomes more challenging when relying solely on visual inspection of the graphical representations.

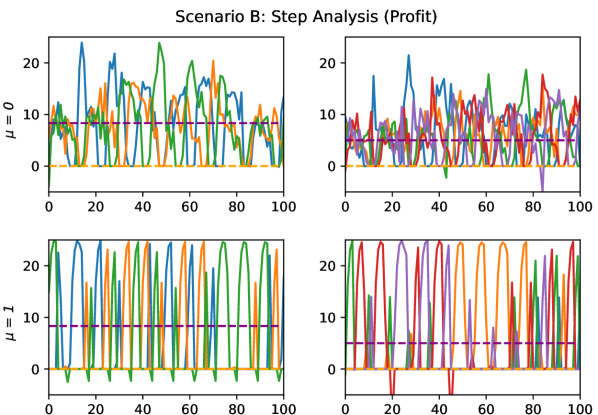

4.2 Scenario B: Constrained Observation Space

In an attempt to weaken the ability to set supracompetitive prices, we constrain the agents’ observation space in Scenario B to , thus removing the other competitors’ prices from each agent’s vision.

The modification yields results that are comparable to those of Scenario A, under both run settings (3 and 5 agents) (cf. Figure 4). In fact, contrary to our expectations, we observe less variance in the results. Analogously to Scenario A, we study a decrease in price with an increase of bias as well as an increase of variance when increasing the number of agents. The observations are reflected in the profit data.

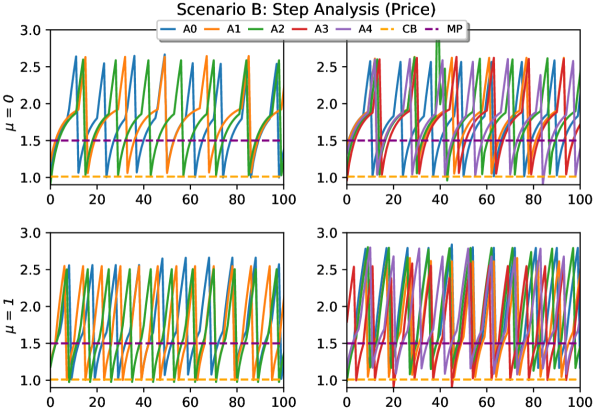

Upon investigating the step pricing (Figure 3), we observe similar patterns to those in Scenario A. In both cases, where and , the agents exhibit an oscillation pattern, resembling a slightly bent sawtooth shape. These observations are further confirmed by the step profit analysis, which depicts fluctuations between earning the minimum and earning above the monopolistic profit split.

5 Discussion

Our experiments have unveiled several noteworthy insights. First, our findings underscore the proficiency of DRL agents in establishing supracompetitive pricing strategies across a plethora of scenarios, without the need to disclose their competitors’ pricing information. Second, our observations revealed the emergence of oscillation patterns within the agents’ pricing behavior, which could be construed as an indicator of collaborative strategies. Third, the algorithms employed in our study yielded remarkable profitability, even more so when using PPO rather than DQN. This was exemplified by the agents achieving an average profit gain of , indicating an outcome akin to perfect collusion, surpassing even monopolistic profit benchmarks. Fourth, we observed an overarching market stagnation that was achieved within a short timeframe and characterized by a consistently elevated . Fifth, we underscore the robustness of our results in an ablation study (please refer to the supplementary material), revealing that modifications to fundamental simulation parameters fail to prevent a collusive outcome; conversely, they even enhance profit gains. These revelations collectively contribute to our understanding of the intricate dynamics of RL pricing agents in market scenarios and their inherent potential to attain collusive outcomes.

Although every run successfully implemented supracompetitive pricing strategies, subsequent analyses revealed that, within a theoretical Bertrand model, the agents encountered challenges in accumulating profits comparable to those observed in the unbiased runs. This can be attributed to multiple factors; the main reason for this weaker performance is the punishing nature of the theoretical scenario. Tying reward functions to the achieved profit immediately results in a punishment of exploration, which proves to be an important factor for collusive states (cf. Calvano et al. Calvano et al. (2018)). This finding is relevant to investigate how to prevent RL agents from colluding. Waltman and Kaymak Waltman and Kaymak (2008) expressed that a force towards the collusive state is stronger if the agents get to experiment; if we can constrain the agents’ ability to explore, we will thus experience less collusive behavior.

In line with Waltman Waltman and Kaymak (2008), we found that collusive states can be difficult to avoid in an oligopoly. This becomes particularly evident when examining the outcomes of the ablation study (please refer to the supplementary material). In contrast to the current literature, our outcome revealed that an increase in agents does not imply a decrease in prices. Aligning with the current research trend of employing base-parametrized RL algorithms, we assert that optimizing these algorithms through proper tuning will only enhance the effectiveness of price-setting mechanisms in real-world scenarios.

One of the most notable findings from the data is the agents’ capability to set prices above the competitive level without requiring access to their competitors’ pricing information. Hansen et al. Hansen et al. (2020) already argued that the signal-to-noise ratio heavily affects results. We can only partly confirm those findings. While the average profit gains in Scenario B are slightly lower, we find that the overall outcome shares a striking resemblance to the results of Scenario A despite this severe confinement. The resiliency stems from the ability to approximate the prices via the reward function, in which other agents’ prices embody unknown variables. This finding concurs well with Waltman Waltman and Kaymak (2008), who observed that agents without a memory were still able to collude.

In this context, it is important to mention that our step analysis experiments resemble the repricing patterns appearing in Amazon’s Buybox Musolff (2022) as well as the observations by Klein Klein (2021). We attribute two causes to the occurrence of these oscillating pricing patterns: First, the agents were able to increase short-term rewards with this strategy by increasing their profit above the monopolist’s profit. Second, the discretization of the action space implies that the exact Bertrand and monopoly prices may not be feasible at all times, so the agents created mixed-strategy equilibria (cf. Calvano et al. Calvano et al. (2018) and the results of our ablation study).

While the results of our experiments show a collusive outcome in an economic sense, they do not undoubtedly exhibit whether algorithmic pricing constitutes permissible parallel behavior or a prohibited concerted practice and thus violates the cartel prohibition. Yet, they show that the agents seem to develop a degree of certainty about their competitors’ anticipated next action to an extent that goes beyond mere observation of a single state and a logical adaption to it.

The cartel prohibition under Article 101 TFEU forbids any kind of joint conduct of independent market participants. According to the established case law of the European Court of Justice (ECJ), the characteristic of a concerted practice presupposes a minimum degree of coordination (concertation), a subsequent market conduct, and a causal link between the two.777cf. the cases ECJ (1999) para. 161; ECJ (2009) para. 38, 39; ECJ (2015) para. 125, 126. This concertation does not have to be as binding as a contract or a direct agreement. It is sufficient that the uncertainty about the competitors’ market behavior, which usually exists under competitive circumstances, is reduced.888cf. the cases ECJ (2009) para. 51; ECJ (2016) para. 39; ECJ (2015) para. 126. However, there has to be at least an indirect contact between them because the cartel prohibition does not deprive them of the right to adapt their behavior to the observed or expected behavior of their competitors ECJ (1998).

It is questionable whether these prerequisites, which follow human behavior’s basic assumptions and logic, can equally be applied to RL decision-making processes. Based on our results, it could be argued that RL algorithms do not require any further reciprocity to gain the extra amount of trust in their competitors’ expected next moves, which - in the case of human behavior - would be added through minimal contact. The insecurity about the competitors’ next move is already reduced by the significant number of processed results from previous rounds, which are even indistinguishable from other environmental information and therefore inherent to each decision Schlechtinger et al. (2021).

It could be considered that the requirement of a minimum degree of communication might be obsolete because every important piece of information is explicitly or implicitly received via the reward function (cf. Scenario B). This raises the possibility that the reward function might channel competitor information, facilitating a concerted practice. However, the reward function simply symbolizes the agents’ feedback on the profits achieved. Any market participant is allowed to know its own profit and draw conclusions about future pricing strategies from it. Given the aforementioned, the assumption that a collusive market outcome is inherently neutral if clear concertation is not detectable is debatable in the context of algorithmic pricing.

When conceptualizing simplified experiments, questions about the transferability of observations to reality and the validity of drawn conclusions quickly arise. We would like to emphasize that, while the present findings originate from a theoretical simulation, the overarching strategies hold the potential for broad applicability within real-world market contexts. As the economics of markets can be formulated as a (PO-)MDP, that - in theory - is solvable by RL algorithms, the agents will always strive for a policy that ultimately achieves the maximum reward. If this reward is tied to the profit, agents will realize that cooperation will help them achieve the best reward in the long run.

As with every study, the results are beset with limitations which opens the door for future research. Although our experiments systematically investigated multiple algorithms, the exploration of potential interactions among heterogeneous algorithms was not pursued. While we present diverse scenarios in the context of an ablation study, we believe that further diversification of simulations will broaden our understanding of pricing algorithms. Moreover, future research endeavors could delve into strategies for imposing constraints on algorithms, thereby discouraging the emergence of collusive states.

6 Conclusion

This paper utilizes an experimental approach to investigate algorithmic collusion. We find that deep RL agents using PPO and DQN are capable of charging supracompetitive prices without explicitly instructing them to do so. Furthermore, we have demonstrated that the algorithms will gravitate towards a collusive state, even when being restricted in their ability to conceive their competitors’ prices. The results have undergone rigorous validation with the help of an ablation study.

Acknowledgments

The work presented in this paper has been conducted in the KarekoKI project, funded by the Baden-Wurttemberg Stiftung in the Responsible Artificial Intelligence program.

References

- 447/98 [1998] Commission Regulation (EC) No 447/98. The Notifications, Time Limits and Hearings Provided for in Council Regulation (EEC), March 1998.

- Abada and Lambin [2023] Ibrahim Abada and Xavier Lambin. Artificial Intelligence: Can Seemingly Collusive Outcomes Be Avoided? Management Science, 69(9):5042–5065, September 2023.

- Achiam [2018] Joshua Achiam. Spinning Up in Deep Reinforcement Learning. https://spinningup.openai.com/, January 2018.

- Assad et al. [2020] Stephanie Assad, Robert Clark, Daniel Ershov, and Lei Xu. Algorithmic Pricing and Competition: Empirical Evidence from the German Retail Gasoline Market. CESifo Working Paper Series, 1(8521), January 2020.

- Bertrand [1883] Joseph Bertrand. Théorie des Richesses: Revue de Théories mathématiques de la richesse sociale par Léon Walras et Recherches sur les principes mathématiques de la théorie des richesses par Augustin Cournot. Journal des Savants, page 499, January 1883.

- Brown and MacKay [2021] Zach Brown and Alexander MacKay. Competition in Pricing Algorithms. National Bureau of Economic Research, January 2021.

- Calvano et al. [2018] Emilio Calvano, Giacomo Calzolari, Vincenzo Denicolo, and Sergio Pastorello. Artificial Intelligence, Algorithmic Pricing and Collusion. American Economic Review, 110(10):3267–97, January 2018.

- Commission [2011] European Commission. Guidelines on the Applicability of Article 101 of the Treaty on the Functioning of the European Union to Horizontal Co-operation Agreements, January 2011.

- ECJ [1998] ECJ. Case C-7-/95 - Deere/Kommission, January 1998.

- ECJ [1999] ECJ. Case C-199/92 - Hüls v Commission, January 1999.

- ECJ [2009] ECJ. Case C-8/08 - T-Mobile Netherlands v Raad van Bestuur van de Nederlandse Mededingingsautoriteit, January 2009.

- ECJ [2015] ECJ. Case C-286/13 - Dole Food and Dole Fresh Fruit Europe, January 2015.

- ECJ [2016] ECJ. Case -74/14 - Eturas UAB v Lietuvos Respublikos konkurencijos taryba, January 2016.

- Han [2021] Bingyan Han. Understanding algorithmic collusion with experience replay. https://arxiv.org/pdf/2102.09139, February 2021.

- Hansen et al. [2020] Karsten Hansen, Kanishka Misra, and Mallesh Pai. Algorithmic Collusion: Supra-competitive Prices via Independent Algorithms. CEPR Discussion Papers, 40(1)(14372), January 2020.

- Hausknecht et al. [2015] Matthew Hausknecht, Peter Stone, and arXiv:1507.06527. Deep Recurrent Q-Learning for Partially Observable MDPs. https://arxiv.org/pdf/1507.06527, July 2015.

- Hettich [2021] Matthias Hettich. Algorithmic Collusion: Insights from Deep Learning. SSRN Electronic Journal, January 2021.

- Kimbrough and Murphy [2009] Steven O. Kimbrough and Frederic H. Murphy. Learning to Collude Tacitly on Production Levels by Oligopolistic Agents. Computational Economics, 33(1):47–78, January 2009.

- Klein [2021] Timo Klein. Autonomous algorithmic collusion: Q-learning under sequential pricing. The RAND Journal of Economics, 52(3):538–558, January 2021.

- Kropp et al. [2019] Lennard Alexander Kropp, Jakob J. Korbel, M. Theilig, and R. Zarnekow. Dynamic Pricing of Product Clusters: A Multi-Agent Reinforcement Learning Approach. In Proceedings of the 27th European Conference on Information Systems (ECIS), volume 27, Stockholm & Uppsala, Sweden, January 2019. Association for Information Systems.

- Mnih et al. [2013] Volodymyr Mnih, Koray Kavukcuoglu, David Silver, Alex Graves, Ioannis Antonoglou, Daan Wierstra, Martin Riedmiller, and arXiv:1312.5602. Playing Atari with Deep Reinforcement Learning. In Proceedings of the 26th International Conference on Neural Information Processing Systems, volume 2. Curran Associates Inc., December 2013.

- Musolff [2022] Leon Musolff. Algorithmic Pricing Facilitates Tacit Collusion: Evidence from E-Commerce. In Proceedings of the 23rd ACM Conference on Economics and Computation, EC ’22, pages 32–33, New York, NY, USA, July 2022. Association for Computing Machinery.

- Qiao et al. [2024] Wenchuan Qiao, Min Huang, Zheming Gao, and Xingwei Wang. Distributed dynamic pricing of multiple perishable products using multi-agent reinforcement learning. Expert Systems with Applications, 237:121252, March 2024.

- Raffin et al. [2021] Antonin Raffin, Ashley Hill, Adam Gleave, Anssi Kanervisto, Maximilian Ernestus, and Noah Dormann. Stable-Baselines3: Reliable Reinforcement Learning Implementations. Journal of Machine Learning Research, 22(268):1–8, January 2021.

- Royston [1992] Patrick Royston. Lowess Smoothing. Stata Technical Bulletin, 1(3), January 1992.

- Schlechtinger et al. [2021] Michael Schlechtinger, Damaris Kosack, Heiko Paulheim, and Thomas Fetzer. Winning at Any Cost - Infringing the Cartel Prohibition With Reinforcement Learning. In Advances in Practical Applications of Agents, Multi-Agent Systems, and Social Good. The PAAMS Collection, Salamanca, Spain, January 2021. Springer Cham.

- Schulman et al. [2017] John Schulman, Filip Wolski, Prafulla Dhariwal, Alec Radford, Oleg Klimov, and arXiv:1707.06347. Proximal Policy Optimization Algorithms. https://arxiv.org/pdf/1707.06347, July 2017.

- Siallagan et al. [2013] Manahan Siallagan, Hiroshi Deguchi, and Manabu Ichikawa. Aspiration-Based Learning in a Cournot Duopoly Model. Evolutionary and Institutional Economics Review, 10(2):295–314, January 2013.

- van Otterlo and Wiering [2012] Martijn van Otterlo and Marco Wiering. Reinforcement Learning and Markov Decision Processes. In Marco Wiering and Martijn van Otterlo, editors, Reinforcement Learning: State-of-the-art, volume v. 12 of Adaptation, Learning, and Optimization, pages 3–42. Springer, Heidelberg; New York, January 2012.

- Waltman and Kaymak [2008] Ludo Waltman and Uzay Kaymak. Q-learning agents in a Cournot oligopoly model. Journal of Economic Dynamics and Control, 32(10):3275–3293, January 2008.

- Werner [2021] Tobias Werner. Algorithmic and Human Collusion. Heinrich Heine University Düsseldorf, January 2021.

- Zhong et al. [2005] Jinghui Zhong, Xiaomin Hu, Jun Zhang, and Min Gu. Comparison of Performance between Different Selection Strategies on Simple Genetic Algorithms. In International Conference on Computational Intelligence for Modelling, Control and Automation and International Conference on Intelligent Agents, Web Technologies and Internet Commerce (CIMCA/IAWTIC’06), pages 1115–1121, Vienna, Austria, 2005. IEEE.