Reinforcement Learning with Lookahead Information

Abstract

We study reinforcement learning (RL) problems in which agents observe the reward or transition realizations at their current state before deciding which action to take. Such observations are available in many applications, including transactions, navigation and more. When the environment is known, previous work shows that this lookahead information can drastically increase the collected reward. However, outside of specific applications, existing approaches for interacting with unknown environments are not well-adapted to these observations. In this work, we close this gap and design provably-efficient learning algorithms able to incorporate lookahead information. To achieve this, we perform planning using the empirical distribution of the reward and transition observations, in contrast to vanilla approaches that only rely on estimated expectations. We prove that our algorithms achieve tight regret versus a baseline that also has access to lookahead information – linearly increasing the amount of collected reward compared to agents that cannot handle lookahead information.

1 Introduction

In reinforcement learning (RL), agents sequentially interact with a changing environment, aiming to collect as much reward as possible. While performing actions that yield immediate rewards is enticing, agents must also bear in mind that actions influence the state of the environment, affecting the potential reward that could be collected in future steps. When the environment is unknown, agents also need to balance reward maximization based on previous data and exploration – gathering of data that might improve future reward collection.

In the standard interaction model, at each timestep, agents first choose an action and only then observe its outcome on the rewards and state dynamics. As such, agents can only maximize the expected rewards, collected through the expected dynamics. Yet, in many applications, some information on the immediate outcome of actions is known before actions are performed. For example, when agents interact through transactions, prices and traded goods are usually agreed upon before performing any exchange. Alternatively, in navigation problems, nearby traffic information is known to the agent before choosing which path to go through.

In a recent work, Merlis et al. (2024) shows that even for agents with full statistical knowledge of the environment, such ‘lookahead’ information can drastically increase the reward collected by agents – by a factor of up to when immediate rewards are revealed in advance and when observing the immediate future transitions.111 is the size of the action space and is the interaction length. Intuitively, agents do not only gain from instantaneously using this information – they can also adapt their planning to account for lookahead information being revealed in subsequent states, significantly increasing their future values. However, the work of Merlis et al. (2024) only tackles planning settings in which the model is known and does not provide algorithms or guarantees when interacting with unknown environments.

In this work, we aim to design provably-efficient agents that learn how to interact when given immediate (‘one-step lookahead’) reward or transition information before choosing an action, under the episodic tabular Markov Decision Process model. While such information can always be embedded into the state of the environment, the state space becomes exponential at best, and continuous at worst, rendering most theoretically-guaranteed approaches both computationally and statistically intractable. To alleviate this, we start by deriving dynamic programming (‘Bellman’) equations in the original state space that characterize the optimal lookahead policies. Inspired by these update rules, we present two variants to the MVP algorithm (Zhang et al., 2021b) that allow incorporating either reward or transition lookahead. In particular, we suggest a planning procedure that uses the empirical distribution of the reward/transition observations (instead of the estimated expectations), which might also be applied to other complex settings. We prove that these algorithms achieve tight regret bounds of and after episodes (for reward and transition lookahead, respectively), compared to a stronger baseline that also has access to lookahead information. As such, they can collect significantly more rewards than vanilla RL algorithms.

Outline. We formally define RL problems with reward/transition lookahead in Section 2. Then, we present our results in two complementary sections: Section 3 analyzes reward lookahead while Section 4 analyzes transition lookahead. We end with conclusions and future directions in Section 5.

1.1 Related Work

Problems with varying lookahead information have been extensively studied in control, with model predictive control (MPC, Camacho et al., 2007) as the most notable example. Conceptually, when interacting with an environment that might be too complex or hard to model, it is oftentimes convenient to use a simpler model that allows accurately predicting its behavior just in the near future. MPC uses such models to repeatedly update its policy using short-term planning. In some cases, the utilized future predictions consist of additive perturbations to the dynamics (Yu et al., 2020), while other cases involve more general future predictions on the model behavior (Li et al., 2019; Zhang et al., 2021a; Lin et al., 2021, 2022). To the best of our knowledge, these studies focus on comparing the performance of the controller to one with full future information (and thus, linear regret is inevitable), sometimes also considering prediction errors. They do not, however, attempt to learn the predictions. In contrast, we estimate the reward/transition distributions and leverage them to better plan, thus increasing the value gained by the agent. In addition, these works focus on continuous (mostly linear) control problems, whereas we study tabular settings; results from any one of these settings cannot be directly applied to the other.

In the context of RL, lookahead is mostly used as a planning tool; namely, agents test the possible outcomes after performing multiple steps to decide which actions to take or to better estimate the value (Tamar et al., 2017; Efroni et al., 2019a, 2020; Moerland et al., 2020; Rosenberg et al., 2023; El Shar and Jiang, 2020). However, when agents actually interact with the environment, no additional lookahead information is observed. One notable exception is (Merlis et al., 2024), which analyzes the potential value increase due to multi-step reward lookahead information (with some mentions to transition lookahead). However, they only tackle planning settings where the model is known and do not study learning. In this work, we continue a long line of literature on regret analysis for tabular RL (Jaksch et al., 2010; Jin et al., 2018; Dann et al., 2019; Zanette and Brunskill, 2019; Efroni et al., 2019b, 2021; Simchowitz and Jamieson, 2019; Zhang et al., 2021b, 2023). Yet, we are not aware of any work that performs regret minimization with reward or transition lookahead information.

Finally, various applications that involve one-step lookahead information have been previously studied. The most notable ones are prophet problems (Correa et al., 2019), where one-step reward lookahead is obtained, and the Canadian traveler problem with resampling (Nikolova and Karger, 2008), which can be formulated through one-step transition lookahead. We discuss the relation to these problems and the relevant existing results when analyzing each type of feedback, and also discuss the relation between transition lookahead and stochastic action sets (Boutilier et al., 2018).

2 Setting and Notations

We study episodic tabular Markov Decision Processes (MDPs), defined by the tuple , where is the state space (of size ), is the action space (of size ) and is the interaction horizon. At each timestep of an episode , an agent, located in state , chooses an action and obtains a reward . We assume that the rewards are supported by and of expectations . Afterward, the environment transitions to a state and the interaction continues until the end of the episode. We use the notation (or ) to denote reward (next-state) samples for all actions simultaneously at step and state and assume independence between different timesteps.222This assumption is not used by our algorithms: it is only to ensure that the optimal policy is Markovian. On the other hand, samples from different actions at a specific state/timestep are not necessarily independent.

Reward Lookahead.

With one-step reward lookahead at timestep and state , agents first observe the rewards for all actions and only then choose an action to perform. Formally, we define the set of reward lookahead policies as , where is the probability simplex, and denote . The value of a reward lookahead agent is the cumulative rewards gathered by it starting at timestep and state , denoted by

We also define the optimal reward lookahead value to be . When interacting with an unknown environment for episodes, agents sequentially choose reward lookahead policies based on all historical information and are measured by their regret,

We allow the initial state of each episode to be arbitrarily chosen.

Transition Lookahead.

Denoting , the future state when playing action at step and state , one-step transition lookahead agents observe before acting. The set of transition lookahead agents is denoted by with values

The optimal value is , and we similarly define the regret versus optimal transition lookahead agents as

When the type of lookahead is clear from the context, we sometimes denote values by and .

Other Notations.

For any and , we define . Also, given a transition kernel and a vector , we let and similarly define it for value or transition kernel differences. We denote by , the number of times the pair was visited at timestep up to episode (inclusive) and similarly denote . We also let and be the empirical expected rewards and transition kernel at using data up to episode and assume they are initialized to be zero. Finally, we denote by , the empirical reward distribution across all actions, and use to denote the empirical joint next-state distribution for all actions. In particular, we assume that a previous timestep where was visited at step is sampled uniformly at random and the rewards/next-states for all actions are taken from this timestep.

When we want to indicate the distribution used to calculate an expectation, we sometimes state it in a subscript, e.g., write to indicate that or use to emphasize that all distributions are according to an environment . In this paper, -notation only hides absolute constants while hides factors of . We also use the notation .

3 Planning and Learning with One-Step Reward Lookahead

In this section, we analyze RL settings with one-step reward lookahead, in which immediate rewards are observed before choosing an action. One well-known example of this situation is the prophet problem (Correa et al., 2019), where an agent sequentially observes values from known distributions. Upon observing a value, the agent decides whether to take it as a reward and stop the interaction, or discard it and continue to observe more values. This problem has numerous applications and extensions concerning auctions and posted-price mechanisms (Correa et al., 2017). As shown in (Merlis et al., 2024), it is critical to observe the distribution values before taking a decision; otherwise, the agent’s revenue can decrease by a factor of .

prophet-like problem

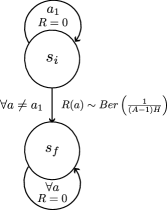

To further illustrate this, consider a simple 2-state prophet-like example, depicted in Figure 1. Starting at , agents can either stay there by playing , earning no reward, or play any other action and move to the absorbing , obtaining a Bernoulli reward . Actions in the terminal state yield no reward. Without observing the rewards, agents will arbitrarily move from to , obtaining a reward in expectation. On the other hand, when agents observe the rewards before acting, they should move from to only if a reward was realized for some action (and otherwise, stay in by playing ). Such agents will have opportunities to observe a unit reward across all timesteps and actions, collecting in expectation . In other words, just by observing the rewards before acting, the agent’s value multiplicatively increases by almost .

The most natural way to tackle this setting is to extend (augment) the state space to contain the observed rewards; this way, we transition from a state and reward observations to a new state with new reward observations and return to the vanilla MDP formulation. However, this comes at a great cost – even for Bernoulli rewards, there are possible reward combinations at any given state, so the state space increases exponentially. Even worse, for continuous rewards, the augmented state space becomes continuous, and any performance guarantees that depend on the size of the state space immediately become vacuous. Hence, algorithms that naïvely use this reduction are expected to be both computationally and statistically intractable.

We take a different approach and derive Bellman equations for this setting in the original state space.

Proposition 1.

The optimal value of one-step reward lookahead agents satisfies

Also, given reward observations at state and step , the optimal policy is

We prove 1 in Section B.2, where we present an equivalent environment with extended state space in which one could apply the standard Bellman equations (Puterman, 2014) to calculate the value with reward lookahead. In contrast to the previously discussed augmentation approach, we find it more convenient to divide the augmentation into two steps – at odd steps , the augmented environment would be in a state , while at even steps , the state is . Doing so creates an overlap between the values of the original and augmented environments at odd steps, simplifying the proofs. We also use this augmentation to prove a variant of the law of total variance (LTV, e.g. Azar et al., 2017) and a value-difference lemma (e.g. Efroni et al., 2019b).

We remark that calculating the exact value is not always tractable – even for (bandit problems) and Gaussian rewards, 1 requires calculating the expectation of the maximum of Gaussian random variables, which does not admit any simple closed-form solution. On the other hand, these equations allow approximating the value by using reward samples – in the following, we show that it can be used to achieve tight regret bounds when the environment is unknown.

3.1 Regret-Minimization with Reward Lookahead

We now present a tractable algorithm that achieves tight regret bounds with one-step reward lookahead. Specifically, we modify the Monotonic Value Propagation (MVP) algorithm (Zhang et al., 2021b) to perform planning using the empirical reward distributions – instead of using the empirical reward expectations. To compensate for transition uncertainty, we add a transition bonus that uses the variance of the optimistic next-state values (w.r.t. the empirical transition kernel), designed to be monotone in the future value. Such construction permits using the variance of optimistic values for the bonus calculation while being able to later replace it with the variance of the optimal value (see discussion in Zhang et al. 2021b). A reward bonus is used for the value calculation, but does not affect the action choice in the current state. Intuitively, this is because we get the same amount of information for all the actions of a state, so they have the same level of uncertainty – there is no need for bonuses to encourage reward exploration at the action level.

A high-level description of the algorithm is presented in Algorithm 1, while the full algorithm and its bonuses are stated in Section B.3. Notice that the planning requires calculating the expected maximum using the empirical distribution, whose support always contains at most elements, so both the memory and computations are polynomial. The algorithm ensures the following guarantees:

Theorem 1.

When running MVP-RL, with probability at least uniformly for all , it holds that .

See proof in Section B.7. Remarkably, our upper bound matches the standard lower bound for episodic RL of (Domingues et al., 2021) up to log-factors; this lower bound is proved for known deterministic rewards, so in particular, it also holds for problems with reward lookahead.

To our knowledge, the only comparable bounds in settings with reward lookahead were proven to prophet problems; as agents observe (up to) distributions at a fixed order, it can be formulated as a deterministic chain-like MDP, with , and . Agents start at the head of the chain and can either advance without collecting a reward or collect the observed reward and move to a terminal non-rewarding state (for more details, see Merlis et al. 2024). For this problem, (Gatmiry et al., 2024) proved a regret bound of (albeit requiring a weaker form of feedback), and (Agarwal et al., 2023) proved a bound of – slightly better than ours, but heavily relies on the ability to control which distributions to observe, which is a specific instance of deterministic transitions. We are unaware of any previous results that cover general Markovian dynamics.

3.2 Proof Concepts

When analyzing the regret of RL algorithms, a key step usually involves bounding the difference between the value of a policy in two different environments (‘value-difference lemma’). In particular, for a given policy , many algorithms maintain a confidence interval on the value , calculated based on optimistic and pessimistic MDPs that use the empirical model with bonuses/penalties (Dann et al., 2019; Zanette and Brunskill, 2019; Efroni et al., 2021). Then, the instantaneous regret (without lookahead) is bounded using the optimistic values by

while the pessimistic values are used either as part of the bonuses or while bounding them. However, when trying to perform a similar decomposition with reward lookahead, we do not have the difference of expected rewards, but rather terms of the form

(see, e.g., the last term of Lemma 4 in the appendix). As the action can be an arbitrary function of the reward realization, this term is extremely challenging to bound. For example, one could couple both distributions while trying to relate this error term to a Wasserstein distance between the empirical and real reward distribution; however, such distances exhibit much slower error rates than standard mean estimation (Fournier and Guillin, 2015). Instead, we follow a different approach and show that uniformly for all possible expected next-state values (as a function of the action at a given state), it holds w.h.p. that

| (1) |

Throughout the proof, whenever we face an expectation w.r.t. the empirical rewards, we reformulate the expression to fit the form of Equation 1 and use it as a ‘change of measure’ tool. We remark that while this confidence interval admits an extra -factor compared to standard bounds, the counts only depend on the visits to the state (and not to the state-action), which compensates for this factor.

The choice of MVP for the bonus is similarly motivated – unlike some other bonuses (e.g., Zanette and Brunskill 2019), MVP does not require pessimistic values – either in the bonus itself or in its analysis. In contrast to the optimistic ones, the pessimistic values are not calculated via value iteration, but rather by following the policy in the pessimistic environment. As such, they cannot be easily manipulated to fit the form in Equation 1.

The analysis of the transitions adapts the techniques in (Efroni et al., 2021), while requiring extra care in handling the dependence of actions in the rewards.

4 Reinforcement Learning with One-Step Transition Lookahead

We now move to analyzing problems with one-step transition lookahead, where the resulting next state due to playing any of the actions is revealed before deciding which action to play. For example, consider the stochastic Canadian traveler problem with resampling (Nikolova and Karger, 2008; Boutilier et al., 2018). In this problem, an agent wants to navigate on a graph as fast as possible from a source to a target, but observes which edges at a node are available only upon reaching this node. When edge availability is stochastic and resampled every time a node is visited, this is a clear case of one-step transition lookahead, as the information on the availability of edges is given before trying to traverse them.

To illustrate the potential gain from transition lookahead, consider a chain of states. In each state, one action deterministically keeps the agent in its current state, while all other actions move the agent one state forward w.p. , but reset it to the head of the chain otherwise. If the reward is located at the end of the chain, any standard RL agent can collect it only at an exponentially low probability. On the other hand, transition lookahead agents could move forward only if there is an action that allows it while staying at their current state otherwise; such agents will collect a reward with constant probability, leading to an exponential improvement.

As with reward lookahead, the future states for all actions can be embedded into the state, but doing so increases the size of the state space by a factor of , again making this approach intractable. We once more show that this is not necessary; the transition-lookahead optimal values can be calculated using the following Bellman equations:

Proposition 2.

The optimal value of one-step transition lookahead agents satisfies

Also, given next-state observations at state and step , the optimal policy is

The proof can be found at Section C.2 and again relies on augmenting the state space to incorporate the transitions; this time, we divide the episode into odd steps whose extended state is (for an arbitrary fixed ) and even steps with the state . Beyond planning, this again allows proving a variant of the LTV and of a value-difference lemma.

One important insight is that the policy admits the form of a list. Namely, consider the values and assume some ordering of next-state-action pairs such that . Then, an optimal policy would look at all realized pairs and play the action with the highest location in this list. We refer the readers to Section C.4 for an additional discussion on list representations in transition lookahead.

Similar results could be achieved through a reduction to RL problems with stochastic action sets (Boutilier et al., 2018). There, at every round, a subset of base actions is sampled, and only these actions are available to the agent. In particular, one could sample actions of the form and impose a deterministic transition to given this extended action. However, since every original action must be sampled exactly once, this sampling procedure creates a dependence between pairs even when next-states at different actions are independent, adding unnecessary complications. We show that when transitions are independent between states, the expectation in 2 can be efficiently calculated (see Section C.4.1 for details), and otherwise, it can be approximated through sampling, as we do in learning settings.

4.1 Regret-Minimization with Transition Lookahead

Relying on similar principals as with reward lookahead, we now present MVP-TL, an adaptation of MVP to settings with one-step transition lookahead (summarized in Algorithm 2; the full details can be found at Section C.3). This time, we estimate the empirical expected reward and add a standard Hoeffding-like reward bonus, while performing planning using samples from the empirical joint distribution of the next-state for all the actions simultaneously. A variance-based transition bonus is added to the values; though this time, the variance also incorporates the rewards, namely

The motivation for this modification is the technical challenges described in Section 3.2, in the context of reward lookahead. For reward lookahead, we analyzed a value term that included both the rewards and next-state values, and used concentration arguments to move from the empirical reward distribution to the real one. For transition lookahead, similar values are analyzed, but we require variance-based concentration to obtain tighter regret bounds (Azar et al., 2017), so this variance naturally arises. The bonus is again designed to be monotone, as in the original MVP algorithm, and does not affect the immediate action choice – only the optimistic lookahead value. As before, the planning relies on sampling the next-state observations at previous episodes, and so it is polynomial, even if the precise joint distribution is complex. The algorithm enjoys the following regret bounds:

Theorem 2.

When running MVP-TL, with probability at least uniformly for all , it holds that .

See proof in Section C.8. For transition lookahead, the regret bounds we provide exhibit two rates, both corresponding to a natural adaptation of known lower bounds to transition lookahead.

-

1.

‘Bandit rate’ : this is the rate due to reward stochasticity. Consider a problem where at odd timesteps and across all states, all actions have rewards of mean , except for one action of mean . Assuming that the state-distribution is uniform, each such timestep forms a hard instance of a contextual bandit problem with contexts, exhibiting a regret of (Auer et al., 2002; Bubeck et al., 2012). Since there are odd steps and we can design each step independently, the total regret would be . The even steps can be used to ‘remove’ the lookahead and create a uniform state distribution. To do so, we set that when taking an action at odd steps, we always transition to a fixed state . From this state, one action leads uniformly to all states, while the rest of the actions lead to an absorbing non-rewarding state – rendering them strictly suboptimal. Thus, no-regret agents will only play , regardless of the lookahead information, and the state distribution at odd timesteps will be uniform.

-

2.

‘Transition learning rate’ : recall that the vanilla RL lower bound designs a tree with leaves, to which agents need to navigate at the right timing (with options) and take the right action (out of ). While all leaves might transition agents to a rewarding state, one combination of state-action-timing has a slightly higher probability of doing so (Domingues et al., 2021). This roughly creates a bandit problem with arms, constructed such that the maximal reward is , yielding a total regret of . Now consider the following simple modification where in each leaf, only one action can lead to a reward (and the rest of the actions are ‘useless’ – never lead to rewards). Thus, the agent still needs to test all leaves at all timings, and so there are still ‘arms’ with a corresponding regret of . Moreover, to test a leaf at a certain timing, we must navigate to it, and since the agent is going to play the single useful action at the leaf, transition lookahead does not provide any additional information.

As discussed before, transition lookahead can be formulated as an RL instance with stochastic action sets. While Boutilier et al. (2018) prove that with stochastic action sets, Q-learning asymptotically converges, they provide no learning algorithm nor regret bounds. Therefore, to our knowledge, our result is the first to achieve sublinear regret with transition lookahead.

4.2 Proof Concepts

Transition lookahead causes similar issues as reward lookahead. Hence, it is natural to apply a similar analysis approach – first, formulate the value as the expectation w.r.t. the next-state observations of the maximum of action-observation dependent values; then use uniform concentration as a ‘change of measure’ tool between the empirical and real next-state distribution. In particular, if represents the value starting from state , performing and transitioning to , one can show that for all (see Lemma 19),

| (2) |

where the variance term stems from using a Bernstein-like concentration bound. However, in contrast to the reward lookahead, the -factor propagates to the dominant term of the regret, so pursuing this approach would lead to a worse regret bound of .

To avoid this, we pinpoint the two locations where this change of measure is needed – the proof that is optimistic and the regret decomposition – and make sure to perform this change of measure only on a single value , mitigating the need to cover all possible values and removing the additional -factor. However, doing so leaves us with a residual term. Defining and assuming a similar optimistic value , this term is of the form

While similar terms have been analyzed before (e.g., Zanette and Brunskill, 2019; Efroni et al., 2021), the analysis leads to a constant regret term that depends on the support of the distribution in question; in our case, it is the distribution over all possible next-states – of cardinality . Therefore, following the same derivation would lead to an exponential additive regret term.

We overcome it by utilizing the fact that both the optimistic policy and the optimal one decide which action to take according to a list of next-state-actions . In other words, instead of looking at the next-state (with possible values) to determine a value, we look at the highest-ranked realized pair in the list that corresponds to the policy that induces the value (with possible rankings). Since we have two values, we need to calculate the probability of being at a certain list location for both and , but the cardinality of this space is : polynomial and not exponential.

5 Conclusions and Future Work

In this work, we presented an RL setting in which immediate rewards or transitions are observed before actions are chosen. We showed how to design provably and computationally efficient algorithms for this setting that achieve tight regret bounds versus a strong baseline that also uses lookahead information. Our algorithms rely on estimating the distribution of the reward or transition observations, a concept that might be utilized in other settings. In particular, we believe that our techniques for transition lookahead could be extended to RL problems with stochastic action sets (Boutilier et al., 2018), but leave this for future work.

One natural extension to our work would be to consider multi-step lookahead information – observing the transition/rewards steps in advance. We conjecture that from a statistical point of view, a similar algorithmic approach that samples from the empirical observation distribution would be efficient. However, it is not clear how to perform efficient planning with such feedback.

Another possible direction would be to derive model-free algorithms (Jin et al., 2018), with the aim to improve the computation efficiency of the solutions; our model-based algorithms require at most computations per episode due to the planning stage, while model-free algorithms might potentially allow just computations per episode.

Finally, the notion of lookahead could be studied in various other decision-making settings (e.g., linear MDPs Jin et al. 2020) and can also be generalized to situations where lookahead information can be queried under some budget constraints (Efroni et al., 2021) or when agents only observe noisy lookahead predictions; we leave these problems for future research.

Acknowledgements

We thank Alon Cohen for the helpful discussions. This project has received funding from the European Union’s Horizon 2020 research and innovation programme under the Marie Skłodowska-Curie grant agreement No 101034255.

References

- Agarwal et al. [2023] Arpit Agarwal, Rohan Ghuge, and Viswanath Nagarajan. Semi-bandit learning for monotone stochastic optimization. arXiv preprint arXiv:2312.15427, 2023.

- Auer et al. [2002] Peter Auer, Nicolo Cesa-Bianchi, Yoav Freund, and Robert E Schapire. The nonstochastic multiarmed bandit problem. SIAM journal on computing, 32(1):48–77, 2002.

- Azar et al. [2017] Mohammad Gheshlaghi Azar, Ian Osband, and Rémi Munos. Minimax regret bounds for reinforcement learning. In International Conference on Machine Learning, pages 263–272. PMLR, 2017.

- Boutilier et al. [2018] Craig Boutilier, Alon Cohen, Avinatan Hassidim, Yishay Mansour, Ofer Meshi, Martin Mladenov, and Dale Schuurmans. Planning and learning with stochastic action sets. In Proceedings of the 27th International Joint Conference on Artificial Intelligence, pages 4674–4682, 2018.

- Bubeck et al. [2012] Sébastien Bubeck, Nicolo Cesa-Bianchi, et al. Regret analysis of stochastic and nonstochastic multi-armed bandit problems. Foundations and Trends® in Machine Learning, 5(1):1–122, 2012.

- Camacho et al. [2007] Eduardo F Camacho, Carlos Bordons, Eduardo F Camacho, and Carlos Bordons. Model predictive control. Springer, 2007.

- Correa et al. [2017] José Correa, Patricio Foncea, Ruben Hoeksma, Tim Oosterwijk, and Tjark Vredeveld. Posted price mechanisms for a random stream of customers. In Proceedings of the 2017 ACM Conference on Economics and Computation, pages 169–186, 2017.

- Correa et al. [2019] Jose Correa, Patricio Foncea, Ruben Hoeksma, Tim Oosterwijk, and Tjark Vredeveld. Recent developments in prophet inequalities. ACM SIGecom Exchanges, 17(1):61–70, 2019.

- Dann et al. [2019] Christoph Dann, Lihong Li, Wei Wei, and Emma Brunskill. Policy certificates: Towards accountable reinforcement learning. In International Conference on Machine Learning, pages 1507–1516, 2019.

- Domingues et al. [2021] Omar Darwiche Domingues, Pierre Ménard, Emilie Kaufmann, and Michal Valko. Episodic reinforcement learning in finite mdps: Minimax lower bounds revisited. In Algorithmic Learning Theory, pages 578–598. PMLR, 2021.

- Efroni et al. [2019a] Yonathan Efroni, Gal Dalal, Bruno Scherrer, and Shie Mannor. How to combine tree-search methods in reinforcement learning. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 33, pages 3494–3501, 2019a.

- Efroni et al. [2019b] Yonathan Efroni, Nadav Merlis, Mohammad Ghavamzadeh, and Shie Mannor. Tight regret bounds for model-based reinforcement learning with greedy policies. In Advances in Neural Information Processing Systems, pages 12224–12234, 2019b.

- Efroni et al. [2020] Yonathan Efroni, Mohammad Ghavamzadeh, and Shie Mannor. Online planning with lookahead policies. Advances in Neural Information Processing Systems, 33:14024–14033, 2020.

- Efroni et al. [2021] Yonathan Efroni, Nadav Merlis, Aadirupa Saha, and Shie Mannor. Confidence-budget matching for sequential budgeted learning. In International Conference on Machine Learning, pages 2937–2947. PMLR, 2021.

- El Shar and Jiang [2020] Ibrahim El Shar and Daniel Jiang. Lookahead-bounded q-learning. In International Conference on Machine Learning, pages 8665–8675. PMLR, 2020.

- Fournier and Guillin [2015] Nicolas Fournier and Arnaud Guillin. On the rate of convergence in wasserstein distance of the empirical measure. Probability theory and related fields, 162(3):707–738, 2015.

- Gatmiry et al. [2024] Khashayar Gatmiry, Thomas Kesselheim, Sahil Singla, and Yifan Wang. Bandit algorithms for prophet inequality and pandora’s box. In Proceedings of the 2024 Annual ACM-SIAM Symposium on Discrete Algorithms (SODA), pages 462–500. SIAM, 2024.

- Jaksch et al. [2010] Thomas Jaksch, Ronald Ortner, and Peter Auer. Near-optimal regret bounds for reinforcement learning. Journal of Machine Learning Research, 11(Apr):1563–1600, 2010.

- Jin et al. [2018] Chi Jin, Zeyuan Allen-Zhu, Sebastien Bubeck, and Michael I Jordan. Is q-learning provably efficient? Advances in neural information processing systems, 31, 2018.

- Jin et al. [2020] Chi Jin, Zhuoran Yang, Zhaoran Wang, and Michael I Jordan. Provably efficient reinforcement learning with linear function approximation. In Conference on learning theory, pages 2137–2143. PMLR, 2020.

- Li et al. [2019] Yingying Li, Xin Chen, and Na Li. Online optimal control with linear dynamics and predictions: Algorithms and regret analysis. Advances in Neural Information Processing Systems, 32, 2019.

- Lin et al. [2021] Yiheng Lin, Yang Hu, Guanya Shi, Haoyuan Sun, Guannan Qu, and Adam Wierman. Perturbation-based regret analysis of predictive control in linear time varying systems. Advances in Neural Information Processing Systems, 34:5174–5185, 2021.

- Lin et al. [2022] Yiheng Lin, Yang Hu, Guannan Qu, Tongxin Li, and Adam Wierman. Bounded-regret mpc via perturbation analysis: Prediction error, constraints, and nonlinearity. Advances in Neural Information Processing Systems, 35:36174–36187, 2022.

- Maurer and Pontil [2009] Andreas Maurer and Massimiliano Pontil. Empirical bernstein bounds and sample variance penalization. In Conference on learning theory, 2009.

- Merlis et al. [2024] Nadav Merlis, Dorian Baudry, and Vianney Perchet. The value of reward lookahead in reinforcement learning. arXiv preprint arXiv:2403.11637, 2024.

- Moerland et al. [2020] Thomas M Moerland, Anna Deichler, Simone Baldi, Joost Broekens, and Catholijn M Jonker. Think neither too fast nor too slow: The computational trade-off between planning and reinforcement learning. In Proceedings of the International Conference on Automated Planning and Scheduling (ICAPS), Nancy, France, pages 16–20, 2020.

- Nikolova and Karger [2008] Evdokia Nikolova and David R Karger. Route planning under uncertainty: The canadian traveller problem. In AAAI, pages 969–974, 2008.

- Puterman [2014] Martin L Puterman. Markov decision processes: discrete stochastic dynamic programming. John Wiley & Sons, 2014.

- Rosenberg et al. [2023] Aviv Rosenberg, Assaf Hallak, Shie Mannor, Gal Chechik, and Gal Dalal. Planning and learning with adaptive lookahead. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 37, pages 9606–9613, 2023.

- Simchowitz and Jamieson [2019] Max Simchowitz and Kevin G Jamieson. Non-asymptotic gap-dependent regret bounds for tabular mdps. In Advances in Neural Information Processing Systems, pages 1153–1162, 2019.

- Tamar et al. [2017] Aviv Tamar, Garrett Thomas, Tianhao Zhang, Sergey Levine, and Pieter Abbeel. Learning from the hindsight plan—episodic mpc improvement. In 2017 IEEE International Conference on Robotics and Automation (ICRA), pages 336–343. IEEE, 2017.

- Yu et al. [2020] Chenkai Yu, Guanya Shi, Soon-Jo Chung, Yisong Yue, and Adam Wierman. The power of predictions in online control. Advances in Neural Information Processing Systems, 33:1994–2004, 2020.

- Zanette and Brunskill [2019] Andrea Zanette and Emma Brunskill. Tighter problem-dependent regret bounds in reinforcement learning without domain knowledge using value function bounds. In International Conference on Machine Learning, pages 7304–7312. PMLR, 2019.

- Zhang et al. [2021a] Runyu Zhang, Yingying Li, and Na Li. On the regret analysis of online lqr control with predictions. In 2021 American Control Conference (ACC), pages 697–703. IEEE, 2021a.

- Zhang et al. [2021b] Zihan Zhang, Xiangyang Ji, and Simon Du. Is reinforcement learning more difficult than bandits? a near-optimal algorithm escaping the curse of horizon. In Conference on Learning Theory, pages 4528–4531. PMLR, 2021b.

- Zhang et al. [2023] Zihan Zhang, Yuxin Chen, Jason D Lee, and Simon S Du. Settling the sample complexity of online reinforcement learning. arXiv preprint arXiv:2307.13586, 2023.

Appendix A Structure of the Appendix

Both reward and transition lookahead appendices share the following structure. First, we describe our assumption on the data generation process and analyze general properties of reward and transition lookahead. This is done by looking at an extended MDP that incorporates the lookahead information into the state. Then, we present the full algorithm and describe the relevant probabilistic events that ensure the concentration of all the empirical quantities. For transition lookahead, we require some additional notions for the event definitions (including the list representation of values and policies), which are explained in a separate subsection.

Given the concentration-related good event, we can prove that the planning procedure in the algorithm is optimistic, which we do in the subsequent subsection. Then, we define an additional good event that allows adding and removing conditional expectations in a way that will be needed for the proof.

At this point, we provided all (almost all) the results required for the regret analysis, and the proof of the main theorems is stated. The proofs also require some additional analysis for the bonuses (and especially variance terms), which is located at the end of the regret analysis.

At the end of the appendix, we state and prove several lemmas that will be used throughout our analysis, while also stating several existing results that will be of use.

Appendix B Proofs for Reward Lookahead

B.1 Data Generation Process

To simplify the proofs, we assume the following ’tabular’ data-generation process: Before the game starts, a set of samples from the transition probabilities and rewards is generated for all . Once a state at step is visited for the time, the sample from the reward distribution is the reward realization for all action . When a state-action pair is visited for the time, the sample from the transition kernel determines the next-state realization. In particular, it implies that the reward samples from the first visits to a state are i.i.d., and the same for the next-states samples and state-action visitations. Throughout this appendix, we use the notation to denote the reward observation at episode and timestep for all the actions.

For the proof, we define the following three filtrations. Let

the filtrations that contains all information until episode and step , as well as the state at timestep , or all information of time , respectively. We make this distinction so that contains only , while also contains . We also define

which contains all information up to the end of the episode, as well as the initial state at episode .

B.2 Extended MDP for Reward Lookahead

In this appendix, we present an alternative formulation of the one-step reward lookahead that falls under the vanilla (no-lookahead) model and would be helpful for the analysis.

Throughout the section, we study the relations between MDPs with and without reward lookahead, and between different MDPs with lookahead. Therefore, for clarity, we state the concerning MDP in the value, e.g. . Specifically in this subsection, we distinguish between values without lookahead (denoted ) and values with lookahead (denoted ). In the following subsections, unless stated otherwise, we will only consider lookahead values; for brevity, and with some abuse of notations, we will then omit the in the value notation.

For any MDP , define an equivalent extended MDP of horizon that separates the state transition and reward generation as follows:

-

1.

Assume w.l.o.g. that starts at some initial state . The extended environment starts at a state , where is the zeros vector.

-

2.

For any , at timestep , the environment transitions from state to , where is a vector containing the rewards for all actions . This transition occurs regardless of the action that was played. At timestep , given an action the environment transitions from to , where .

-

3.

The reward at a state when playing an action is , namely, the reward is deterministic and only obtained on even timesteps.

We emphasize that throughout the section, we assume that and are coupled; that is, assume that under a policy in , the agent visits a state , observes , plays an action and transitions to . Then, in , the agent starts from , transitions to (regardless of the action it played), takes the action and finally transitions to .

Since the reward is embedded into the state, any state-dependent policy in is a one-step reward lookahead policy in the original MDP. Moreover, the policy at the odd steps of does not affect the value, and assuming that the policy at the even steps in is the same as the policy in , we trivially get the following relation between the values

| (3) |

While has a continuous state space, which generally makes algorithm design impractical, this representation permits applying classic results on MDPs to environments with one-step lookahead.

As a remark, rewards could be directly embedded into the state without separating the state and reward updates. However, this creates unnecessary complications when analyzing the relations between similar environments. This is because we are mainly interested in the value given the state – in expectation over the realized rewards. In particular, value-difference are analyzed assuming a shared initial state, but in our case, we do not want to assume the same reward realization, but rather also account for the distance between reward distributions, which the step separation enables. For similar reasons, this representation also simplifies the proof of the law of total variance [Azar et al., 2017].

See 1

Proof.

We prove the result in the extended MDP and remind the reader that in this formulation, the policy only uses state information, as in the standard RL formulation. In particular, it implies that there exists a Markovian optimal policy that uniformly maximizes the value (in the extended state space), and the optimal value is given through the dynamic-programming equations [Puterman, 2014]

| (4) |

By the equivalence between and for all policies, this is also the optimal value in . Specifically, combining both recursion equations and substituting the relation between the original and extended values of Section B.2, we get the desired value recursion for any and :

Similarly, for any , and , the optimal policy at the even stages of the extended MDP is

alongside arbitrary actions at odd steps. Playing this policy in the original MDP will lead to an optimal one-step reward lookahead policy, as it achieves the optimal value of the original MDP. This policy directly translates to the optimal policy in the statement, by the equivalence between the original and extended MDPs and the relation . ∎

Remark 1.

As in Section B.2, one could also write the dynamic programming equations for any policy , namely

In particular, following the notation of Section B.2, one can also write

We will use this notation in some of the proofs.

Another useful application of the extended MDP is a variation of the law of total variance (LTV), which will be useful in our analysis

Lemma 3.

For any deterministic one-step reward lookahead policy , it holds that

Proof.

We apply the law of total variance (Lemma 27) in the extended MDP; there, the rewards are deterministic and equal to either (at odd steps) or (at even steps), so the total expected rewards are .

Noting that concludes the proof. ∎

Finally, though not needed in our analysis, we use the extended MDP to prove the following value-difference lemma, which could be of further use in follow-up works. While we prove decomposition just using the next-step values, one could recursively apply the formula until the end of the episode to immediately get another formula that does not depend on the next value.

Lemma 4 (Value-Difference Lemma with Reward Lookahead).

Let and be two environments. For any deterministic one-step reward lookahead policy , any and , it holds that

where is the value at a state given the reward realization, defined in Section B.2 and given in Remark 1.

Proof.

We again work with the extended MDPs . Since under the extension, both the environments and the policy are Markovian, all values obey the following Bellman equations:

Using the relation between the value of the original and extended MDP (section B.2) and the Bellman equations of the extended MDP, for any , we have

| (5) |

We now focus on the first term. Denoting the action taken by the agent at environment , We have

Substituting this back into Section B.2, we have

∎

B.3 Full Algorithm Description for Reward Lookahead

We use a variant of the MVP algorithm [Zhang et al., 2021b] while adapting their proof and the one from [Efroni et al., 2021]. The algorithm is described in Algorithm 3 and uses the following bonuses:

where , and for brevity, we shorten to (omitting the state from the value).

For the optimistic value iteration, we use the notation to represent the episode where the state was visited at the timestep. Thus, line 9 of Algorithm 3 is the expectation w.r.t. the empirical reward distribution (when defining its realization to be zero when ). Since the bonuses are larger than when , one could write the update in more concisely as

We will often use this representation in our analysis.

B.4 The First Good Event – Concentration

We now define the first good event, which ensures that all empirical quantities are well-concentrated. For the transitions, we require each element to concentrate well, as well as both the inner product and the variance w.r.t. the optimal value function. For the reward, we make sure that the maximum of the rewards to concentrate well (with any possible bias, that will later correspond with the next-state values). Formally, for any fixed vector , denote

with the convention that if . We define the following good events:

where we again use . Then, we define the first good event as

for which, the following holds:

Lemma 5 (The First Good Event).

The good event holds w.p. .

Proof.

The proof of the first three events uses standard concentration arguments (see, e.g., Efroni et al. 2021) and is stated for completeness. For any fixed and number of visits , we utilize Lemma 16 w.r.t. the transition kernel , the value and probability ; notice that by the assumption that samples are generated i.i.d. before the game starts, given the number of visits, all samples are i.i.d., so standard concentration could be applied. By taking the union bound over all and slightly increasing the constants to ensure that trivially holds, we get that the events also hold for any number of visit , and taking another union bound over all ensures that each of the events and holds w.p. at least

We now focus on bounding the probability of the event . For any fixed , and , observe that the event trivially holds if , then the event trivially holds, since for all ,

where uses the boundedness of the rewards in . Next, recall that for any fixed , the rewards samples at state and step are i.i.d. vectors on . Therefore, by Lemma 18,

Taking a union bound on all possible values of , and , we get

By summing over all , the event holds with a probability of at least . Finally, taking the union bound with the other three events leads to the desired result of . ∎

B.5 Optimism of the Upper Confidence Value Functions

In this subsection, we prove that under the good event , the values that MVP-RL produces are optimistic.

Lemma 6 (Optimism).

Under the first good event , for all , and , it holds that .

Proof.

The proof follows by backward induction on ; see that the claim trivially holds for , where both values are defined to be zero.

Now assume by induction that for some and , the desired inequalities hold at timestep for all ; we will show that this implies that they also hold at timestep .

At this point, we also assume w.l.o.g. that , and in particular, the value is not truncated; otherwise, by the boundedness of the rewards, For similar reasons, we assume w.l.o.g. that , so that it is also not truncated.

By the optimism of the value at step due to the induction hypothesis and the monotonicity of the bonus (Lemma 23), under the good event, we have for all and that

| (Lemma 23) | |||

| (Under ) | |||

| (Under ) |

Thus, under the good event and the induction hypothesis, we have that

In particular, using 1, we get

where the last inequality holds under the event with . ∎

B.6 The Second Good Event – Martingale Concentration

In this subsection, we present four good events that will allow us to replace the expectation over the randomizations inside each episode with their realization.

Define the following bonus-like term that will later appear in the proof due to value concentration:

and let

The second good event is the intersection of the events defined as follows.

We define the good event .

Lemma 7.

The good event holds with a probability of at least .

Proof.

The proof follows similarly to Lemmas 15 and 21 of [Efroni et al., 2021].

First, define the random process and define , which is bounded in . Also observe that is measurable, since both values and policies are calculated based on data up to the episode , and in particular, it is measurable and is measurable. thus, by Lemma 25, for any and , we have w.p. at least that

Since is measurable, we can write the event as

and taking the union bound over all and , we get w.p. at least that the event

Importantly, by optimism (Lemma 6), under , it holds that for all , so we immediately get that .

Following the exact same proof just with the filtration and defining the equivalent , we get that this event also holds w.p. and is the desired event when holds.

Next, we prove that the other two events also hold w.p. at least .

By the assumptions of our setting, we know that , and so

In particular, applying Lemma 25 (w.r.t. the filtration ) with and any fixed , we get w.p. that

Taking the union bound on all possible values of proves that holds w.p. at least .

Similarly, by definition, we have that and is measurable. Thus, for any fixed and , using Lemma 25, we have w.p. that

applying the union bound on all , the event holds w.p. .

To summarize, we have that the event holds w.p. (Lemma 5), and we proved that the events hold each w.p. , so we also have that the event

holds w.p. at least . ∎

B.7 Regret Analysis

We finally analyze the regret of the algorithm See 1

Proof.

Assume that the good events holds, which by Lemma 7, happens with probability at least . Then, by optimism (Lemma 6), for any , and , it holds that . Moreover, we can lower bound the value of the policy as follows (see Remark 1):

| (6) |

Relation is by the definition of (see Algorithm 3), while holds under the good event with (due to the value and bonus truncation). Finally, is by the definition of , where the inequality also accounts for its possible truncation.

To further bound this, we need to bound

The first error term can be bounded under the good event, while the second using Lemma 24. More formally, under the good event , we have

and by Lemma 24 with (using and , , under ),

where the second inequality is since the value of cannot exceed the optimal value.

Since under the good event by Lemma 6, we have , we can trivially bound the error by and bound

Substituting back to Equation 6 while writing the linear operation as an expectation and letting the action be , we get under for all , and that

Next, taking , the action becomes , and summing on all , we can rewrite

where inequality holds when both and occur and inequality is by Lemma 8. In the last inequality, we also substituted the definition of the reward bonus. Recursively applying this inequality up to (where both values are zero), w.p. at least , we get

| (Lemma 6) | ||||

B.7.1 Lemmas for Bounding Bonus Terms

Lemma 8.

Conditioned on the good event , for any , it holds that

Proof.

We start by analyzing each of the terms separately. First, we apply Lemma 22 with , noting that under the good event (by Lemma 6), and using the event ; doing so yields

Using Lemma 24 with , under the good event and for any , we can further bound

| (Lemma 24) | |||

Thus, we get the overall bound

For the second bonus, we apply Lemma 21 w.r.t. and and get

where we again used the optimism. Combining both and summing over all , we get

Finally, under the good event , it holds that

Substituting this relation back concludes the proof. ∎

Lemma 9.

Under the event it holds that

Proof.

Following Lemma 24 of [Efroni et al., 2021], by Cauchy-Schwartz inequality, it holds that

The second term can be bounded by Lemma 20, namely,

We further focus on bounding the first term. Under , we have

| (Under ) | |||

| (By Lemma 3 ) | |||

where the last inequality is since both the values and cumulative rewards are bounded in . Combining both, we get

∎

Appendix C Proofs for Transition Lookahead

C.1 Data Generation Process

As for the reward transition, we also assume that all data was generated before the game starts for all state-action-timesteps, and it is given to the agent when the relevant is visited. Thus, the rewards and next-state from the first visits at a state (or a state-action pair) at a certain timestep are i.i.d.

Throughout this appendix, we use the notation to denote the next-state observations at episode and timestep for all the actions, and use the equivalent filtrations to the ones defined at Section B.1, namely

In particular, notice that since both and are measurable, then so does .

C.2 Extended MDP for Transition Lookahead

In this appendix, we present an equivalent extended MDP that embeds the lookahead into the state to fall under the vanilla MDP model, similarly to Section B.2. We use this equivalence to apply various existing results on MDPs without the need to reprove them. We follow the same conventions as Section B.2 while denoting transition lookahead values by (and again, the superscript will be omitted in subsequent subsections).

For any MDP , let be an MDP of horizon and state space that separates the state transition and next-state generation as follows:

-

1.

Assume w.l.o.g. that starts at some initial state . The extended environment starts at a state , where is a vector of copies of some arbitrary state .

-

2.

For any , at timestep , the environment transitions from state to , where is a vector containing the next state for all actions ; this transition happens regardless of the action that the agent played. At timestep , given an action , the environment transitions from to .

-

3.

The rewards at odd steps are zero, while the rewards at even steps are of expectation .

As before, since the next state is embedded into the extended state space, any state-dependent policy in is a one-step transition lookahead policy in the original MDP. Also, the policy at even timesteps does not affect either the rewards or transitions, so it does not affect the value in any way. We again couple the two environments to have the exact same randomness, so assuming that the policy at the even steps in is the same as the policy in , we trivially get the following relation between the values

| (7) |

While is finite, it is exponential in size, so applying any standard algorithm in this environment would lead to exponentially-bad performance bounds. Nonetheless, as with the extended-reward environment, we use this representation to prove useful results on one-step transition lookahead. See 2

Proof.

We prove the result in the extended MDP , in which (as with reward lookahead) the optimal value can be calculated using the Bellman equations as follows [Puterman, 2014]

| (8) |

By the equivalence between and for all policies, this is also the optimal value in . Combining both recursion equations and substituting Section C.2 leads to the stated value calculation for all and :

In addition, a given state and next-state observations , the optimal policy at the even stages of the extended MDP is

alongside arbitrary actions at odd steps. Playing this policy in the original MDP will lead to the optimal one-step transition lookahead policy, as it achieves the optimal value of the original MDP. By the value relations between the two environments (), this is equivalent to the stated policy. ∎

Remark 2.

As in Remark 1, one could write the dynamic programming equations for any policy , and not just to the optimal one, namely

In particular, following the notation of Section C.2, we can write

a notation that will be extensively used for transition lookahead.

We also prove a variation of the law of total variance (LTV) for transition lookahead:

Lemma 10.

For any one-step transition lookahead policy , it holds that

Proof.

We apply the law of total variance in the extended MDP; there, the expected rewards are either (at odd steps) or (at even steps), so the total expected rewards are . Hence, by Lemma 27,

Using again the identity leads to the desired result. ∎

Finally, prove a value-difference lemma also for transition lookahead

Lemma 11 (Value-Difference Lemma with Transition Lookahead).

Let and be two environments. For any deterministic one-step transition lookahead policy , any and , it holds that

where is the value at a state given the reward realization, defined in Section C.2 and given in Remark 2.

Proof.

We again work with the extended MDPs and use their Bellman equations, namely,

Using the relation between the value of the original and extended MDP (section C.2) and the Bellman equations of the extended MDP, for any , we have

| (9) |

Denoting the action taken by the agent at environment , We have

when taking the expectation w.r.t. , it holds that ; substituting this back into Section C.2, we get

∎

C.3 Full Algorithm Description for Transition Lookahead

As with reward lookahead, we again use a variant of the MVP algorithm [Zhang et al., 2021b], described in Algorithm 4. For the bonuses, we use the notation

and define the following bonuses:

where and

The notation again represents the episode where the state was visited at the timestep; in particular, line 9 of the algorithm is the expectation w.r.t. the empirical reward distribution . Since the transition bonus is larger than when , we can arbitrarily define the expectation w.r.t. when to be 0, and one could write the update in a more concise way as

C.4 Additional Notations and List Representation

In this subsection, we present additional notations for both values and transition distributions that will be helpful in the analysis. In particular, we show that instead of looking at the distribution over all combinations of next state , we can look at a ranking of all the next-state-actions and represent important quantities using the effective distribution on these ranks – this moves the problem from being -dimensional to a dimension of .

We start by defining the values starting from state , playing and transitioning to , denoted by

We similarly define (consistently with Remark 2)

List representation. We now move to defining lists of next-state-actions and distributions with respect to such lists. Let be a list that orders all next-state-action pairs from to and define the set of all possible lists to be (with ). Also, define , the list induced by a function such that , where ties are broken in any fixed arbitrary way. From this point forward, for brevity and when clear from the context, we omit the list from the indexing, e.g., write the list by .

We now define the probability of list elements. Denote by the event that the highest-ranked realized element in the list is element , namely

| (10) |

Then, for a probability measure on , define . Notably, when the list is induced by and element is the realized highest-ranked elements, we can write , so we have that (e.g. by Lemma 17 with )

We also denote by , the empirical probability for a list location to be the highest-realized ranking according to a list at state and step , based on samples up to episode ; We have by Lemma 17 that and

Similarly, we will require the distribution probability w.r.t. two lists – the probability that the top element w.r.t. list is and the top element w.r.t. list is ; we denote the real and empirical probability distributions by and , respectively. This allows, for example, using Lemma 17 to write for any ,

| (11) |

Finally, we say that a policy is induced by lists if it chooses an action such that its next-state is ranked higher in than all other realized next-state-action pairs. In particular, the policy and the optimal policy (defined in 2) are such policies w.r.t. the lists and – induced by and , respectively. As such, for any probability measure , function and a policy induced by a list , it holds that

| (12) |

C.4.1 Planning with Transition Lookahead

We have already seen the optimal policy is induced by a list , and in particular, we can write the dynamic programming equations of 2 as

Therefore, one way to perform the planning is to build a list of s.t. the values

are sorted in a non-increasing order and calculate the probability of any pair in the list to be the highest-realized pair:

In general, calculating this distribution is intractable, and one must resort to approximating it by sampling (as done in Algorithm 4. Nonetheless, if next states are generated independently between actions, this distribution could be efficiently calculated as follows:

Relation holds since if , it cannot get any previous value of the same action in the list, so these events can be removed. Relation is by the independence and directly calculates the probabilities.

C.5 The First Good Event – Concentration

Next, we define the events that ensure the concentration of all empirical measures. For rewards, an event handles the convergence of the empirical rewards to their mean. For the transitions, we want the Bellman operator, applied on the optimal value with the empirical model, to concentrate well, and we require the variance of values w.r.t. the empirical and real model to be close. Finally, the empirical measure must concentrate well around its mean for any list – this will allow the change-of-measure argument described in the proof sketch.

Formally, define the following good events:

where we again use . We define the first good event as

for which the following holds:

Lemma 12 (The First Good Event).

It holds that .

Proof.

We prove that each of the events holds w.p. at least . The result then directly follows by the union bound. We also remark that due to the domain of the variables and their estimators (e.g., for the rewards), all bounds trivially hold when the counts equal zero, so w.l.o.g., we only prove the results for cases in which states/state-actions were already previously visited.

Event . Fix and visits . Given all of these, the reward observations are i.i.d. random variables supported by . Denoting the empirical mean based on these samples by , by Hoeffding’s inequality, it holds w.p. that

Taking the union bound over all at timestep , we get that w.p.

and another union bound over all possible values of and implies that holds w.p. at least .

The event . For any fixed , a list and number of visits , we utilize Lemma 16 (event ) w.r.t. the distribution (whose support is of size ). When applying the lemma, notice that given the number of visits , the empirical distribution is the average of i.i.d samples, so that for all ,

w.p. . Choosing (such that since ), while taking the union bound on all , all and all lists implies that holds w.p. at least .

Events and . We repeat the arguments stated in Lemma 5. For any fixed and number of visits , we utilize Lemma 16 w.r.t. the next-state distribution for all actions , the value and probability ; we yet again remind that given the number of visits, samples are i.i.d.

As before, the events and hold w.p. at least through the union bound first on (to get the empirical quantities) and then on and . This proves that each of the events in holds w.p. at least , so holds w.p. at least . ∎

C.6 Optimism of the Upper Confidence Value Functions

We now prove that under the event , the values that MVP-TL outputs are optimistic.

Lemma 13 (Optimism).

Under the first good event , for all , , and , it holds that . Moreover, for all , and also .

Proof.

The proof of all claims follows by backward induction on ; the base case naturally holds for , where all values are defined to be zero.

Assume by induction that for some and , the inequality holds for all ; we will show that this implies that all stated inequalities also hold at timestep . At this point, we also assume w.l.o.g. that (namely, not truncated), since otherwise, by the boundedness of the rewards, In particular, under the good event , for all and , it holds that , so for all and , we have

where the inequality also uses the induction hypothesis. This proves the first part of the lemma. Moreover, it implies that

| (13) |

and proves the second part of the statement.

To prove the last claim of the lemma, we use the monotonicity of the bonus, relying on Lemma 23. This lemma can be used when applied to the empirical distribution of all possible next-states ; indeed, the non-truncated optimistic value can be written as

which is exactly the required form in Lemma 23, w.r.t. the distribution and the values (while noticing that due to the truncation of the values and bonuses, ). Thus, the lemma guarantees monotonicity in the value, so by Equation 13,

| (Under ) | ||||

| (Under ) | ||||

∎

C.7 The Second Good Event – Martingale Concentration

In this subsection, we present three good events that allow replacing the expectation over the randomizations inside each episode by their realization. Let

The second good event is the intersection of the events defined as follows.

We define the good event .

Lemma 14.

The good event holds with a probability of at least .

Proof.

The analysis of the first event follows exactly as the one of in Lemma 7: define (which happens a.s. under due to the optimism in Lemma 13 and truncation) and , which is bounded in and -measurable. The corresponding event w.r.t. this modified variables then holds w.p. by Lemma 25, and as in Lemma 7, we can use the fact that to conclude this part of the proof.

Moving to the second event, since , then . Therefore, by Lemma 25 (w.r.t. the filtration ) with and any fixed , we get w.p. that

Taking the union bound on all possible values of proves that holds w.p. at least .

Finally, by definition, we have that and is -measurable. Thus, for any fixed and , using Lemma 25, we have w.p. that

so that due to the union bound, holds w.p. .

To conclude, holds w.p. (Lemma 5) and the events each hold w.p. . As before, when accounting to the fact that and are identical under , the event holds w.p. at least . ∎

C.8 Regret Analysis

See 2

Proof.

Assume that the event holds, which by Lemma 14, happens with probability at least . In particular, throughout the proof, we use optimism (Lemma 13), which implies that (the upper bound is also by the truncation), as well as .

We first focus on lower-bounding the value of the policy : by Remark 2, we have

where is by the definition of and uses the reward concentration event. Thus, we can write

| (14) |

Bounding term : using the concentration event , we have

| (15) |

Relation uses Lemma 21 with the values with and is by optimism.

Bounding term : We first focus on the transition bonus; to bound it, we apply Lemma 22 w.r.t. , the values (by optimism), under the event and with :

Substituting back to term , we now have

The next step in the proof involves bounding the first term of . At this point, we remind that both values can be written as and , inducing the lists and , respectively; thus the expectations can be written as (see Section C.4 for further details on the list representation, and in particular, Equation 11):

Relations formulate the expectation using the list representations and backward, as done in Equation 11. For inequality we rely on Lemma 24 with under the event and the optimism, which ensures that the value difference is bounded in . We also remark that the support of the distributions is of size ; were we to use the same result on the distributions and , the support would be of size , which would lead to an exponential additive factor. And so, we finally have a bound of

| (16) |

Combining both terms. Substituting this and Equation 15 into Equation 14, we have

and further bounding (using the concentration event

we finally get the decomposition

At this point, we choose to take and sum over all ; specifically, for , the action becomes and . Formally, we can write the bound as

and, in particular, under the events and , it holds that

C.8.1 Lemmas for Bounding Bonus Terms

Lemma 15.

Under the event it holds that

Proof.

Similar to Lemma 9, we again rely on the lookahead version of the law of total variation to prove this bound. First, by Cauchy-Schwartz inequality, it holds that

We use Lemma 20 to bound the second term by

and focus on bounding the first term. Under , we have

| (Under ) | |||

| (By Lemma 10 ) | |||

where the last inequality is since both the values and cumulative rewards are bounded in . Combining both, we get

∎

Appendix D Auxiliary Lemmas

In this appendix, we prove various auxiliary lemma that will be used throughout our proofs.

D.1 Concentration results

We first present and reprove a set of well-known concentration results.

Lemma 16.

Let be a distribution over a discrete set of size and let be independent samples from this distribution. Also, let for some and define the empirical distribution . Then, for any , each of the following events hold w.p. at least :

where .

Proof.

All the results require standard probability arguments and are stated for completeness.

For the first event , notice that each of the components is the empirical mean of independent Bernoulli random variables of mean . Therefore, by Bernstein’s inequality, recalling that the variance of the variable is , we get w.p. at least that

Taking the union bound over all implies that holds w.p. at least .

For the second event , we apply Bernstein’s inequality on the variables . The empirical mean is given by and its average is . Similarly, the variance of the random variables is . Thus, by Bernstein’s inequality, w.p. at least ,

Stating the bounds in terms of leads to the second event.

For the last event, we follow the analysis of [Efroni et al., 2021, Lemma 19], which in turn, relies on [Maurer and Pontil, 2009, Theorem 10]. Define . This is a well-known unbiased variance estimator, namely, , and by [Maurer and Pontil, 2009, Theorem 10], for any it holds w.p. at least that

where we scaled the bound by to account for the values being in .

Next, we relate to the empirical variance. By elementary algebra, we have

The first two terms are exactly the variance w.r.t. the empirical distribution; therefore, using the inequality for positive numbers, we have

Combining both inequalities and recalling the trivial bound of on the difference, we get that w.p. at least ,

∎

Next, we present a short lemma that allows moving between different spaces of probabilities.

Lemma 17.

Let be a finite set and let . Also, let be a partition of the set , namely, for all , and . Finally, let such that for all and , it holds that , and define

Then, the following hold:

-

1.

and, in particular, .

-

2.

If is a distribution over and are i.i.d. samples from , then . It also holds that .

Proof.

For the first part, we have by definition that

In particular, it holds that

where is since is constant inside and is since partition .

For the second part of the statement, notice that since the samples are i.i.d., it holds that , and therefore,

Finally, as in the first part of the statement, it holds that

∎

Finally, we present two specialized concentration results that are needed for reward and transition lookahead, respectively.

Lemma 18.

Let be i.i.d. random vectors over and let be some constant. Then, for any , with probability at least ,

Proof.

Denote and and fix any . Since the variables are bounded in , their maximum is bounded almost surely in , namely, an interval of unit length. Therefore, by Hoeffding’s inequality, for any , w.p.

Now, for some , let be the closest vector to on a grid . Then, it clearly holds that

Taking the union bound over all possible choices for and fixing , we get w.p. for all that

Now, fixing and noting that for , we get

∎

Lemma 19.

Let be i.i.d. random vectors with components supported over the discrete set and let be some constant. Then, uniformly over all w.p. :

Proof.

We follow a similar path to Lemma 18 and use a covering argument. Denoting and , by Bernstein’s inequality, for any and fixed , it holds w.p. that

| (17) |

Now, for some , let be the closest matrix to on a grid and denote with samples . By the smoothness of the max function, it holds that

In particular, we also have that

so we have

Similarly, it holds that

Taking the union bound over all possible choices for and fixing , we get w.p. for all that

Now, fixing and noticing that , we get

∎

D.2 Count-Related Lemmas

Lemma 20.

The following bounds hold:

Proof.

Recall that every time a state (or state-action) is visited, its visitation-count is increased by , up to at the last episode. therefore, we can write

| (Jensen’s inequality ) | ||||

where we bounded the total number of visits by the number of steps . Similarly, we also have

We can likewise prove the inequalities for the state counts as follows:

| (Jensen’s inequality ) | ||||

and

∎

D.3 Analysis of Variance terms

Lemma 21.

Let be a distribution over a finite set and let . Also, let for some such that for all . Then, for any , it holds that

Proof.

By Lemma 26, we have