Conditional uncorrelation equals independence

Abstract

It is well known that the independent random variables and are uncorrelated in the sense and that the implication may be reversed in very specific cases only. This paper proves that under general assumptions the conditional uncorrelation of random variables, where the conditioning takes place over the suitable class of test sets, is equivalent to the independence. It is also shown that the mutual independence of is equivalent to the fact that any conditional correlation matrix equals to the identity matrix.

keywords:

correlation, independence, linear dependence, conditional moments1 Introduction

It is well known that if and are two independent integrable real-valued random variables then they are uncorrelated in the sense and that this implication cannot be reversed unless very specific assumptions on and are satisfied, David (2009). More, even the uncorrelation of all the higher moments of and is not enough to force the independence, De Paula (2008). This paper proves that under general assumptions the conditional uncorrelation of random variables, where the conditioning takes place over the class or , is equivalent to the independence. This solves Problem 6327 from Chernoff, Móri et al. (1981) which, according to my knowledge, is solved only in the case where the vector has a joint probability density , see Jaworski, Jelito, Pitera (2024) which applies copula functions to the problem (under some additional technical assumptions on ). Theorem 1 from the next section shows that the independence of and is equivalent to the conditional uncorrelation for all types of random variables and and any dependencies between them. The direct conclusion is that if and are not independent then there is some rectangle conditioning on which we have the nonzero Pearson correlation coefficient. The motivation for such study comes from the developing field of conditional statistics which have proved to provide useful applications and nontrivial theoretical problems, see for instance Hebda-Sobkowicz et al.(2020), Jaworski-Pitera (2016), Jaworski-Pitera (2020), Jelito-Pitera (2021), Jaworski et al. (2024), Pitera et al. (2022), Navarro et al. (1998). For the previous papers on the conditional correlations one can see, for instance, Akeman et al. (1984), Baba et al. (2004), Lawrance (1976). The general methodology we will present here is, roughly speaking, about using the properties of the Radon-Nikodym derivative to reduce the problem of conditional uncorrelation to the one- dimensional conditioning which is well understood, Navarro et al. (1998). The presented approach allows to prove other general statements about the independence and Theorem 2 shows that the mutual independence of the marginals of the random vector is equivalent to the fact that any conditional correlation matrix of equals to the identity matrix. Section 2 introduces the basic definitions and presents the main results. Section 3 presents the necessary theory and proves Theorems 1 and 2.

2 Conditional uncorrelation and the main results

Let be a probability space. The space is naturally equipped with the sigma-algebra of Borel sets and is a random vector iff for any . The probability distribution of the random vector is denoted by and given by , . For any with the will denote the conditional probability measure:

Let be a random variable and let denote the characteristic function of , i.e. for and for . If the expectation exists, the conditional expectation is defined by and satisfies If , where is a Borel set with , then

If and are non-constant random variables with and then both the covariance and the (Pearson’s) correlation are well defined:

where denotes the standard deviation of .

If are Borel sets with then one can consider the corresponding conditional covariance and the conditional correlation, i.e. for one may calculate those coefficients with respect to the conditional probability . The conditional covariance is thus given by

assuming that the above expectations exists, and the conditional correlation satisfies

where is the standard deviation with respect to the conditional probability . Those conditional statistics are easy to estimate in practice: given the sample of pairs of observations , one just calculates the standard covariance and correlation coefficients on the subsample of determined by

The mathematical justification of this procedure follows directly from the properties of the conditional probability: if the random vectors , , are i.i.d. and then for

the random variables are independent and have probability distribution equal to the conditional distribution , i.e.

If the and are not square - integrable (in practice, for instance, the data may exhibit heavy tails), the tests based on the classical covariance fail to work properly. At the same time, the conditional covariance is well defined for any bounded rectangle and one may consider the conditional covariance instead of the classical one, see Jaworski et al. (2024) for other applications.

If and are independent in the sense , , then and for any admissible test set . The theorem below states that this implication may be reversed.

Theorem 1.

Assume that . For any random variables and , the following conditions are equivalent:

-

1)

and are independent,

-

2)

for any with ,

Under additional assumption: and , we may replace the bounded intervals with the family ( or with ).

In conclusion, the square-integrable random variables and are independent iff they are uncorrelated conditioning on the tails and , i.e. for any with the following function

| (1) |

is constant and equal to zero.

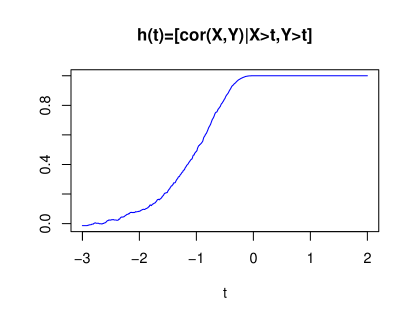

Below, just for illustration, we consider the textbook example of with dependent but uncorrelated normal-distributed marginals, Broffitt (1986).

Example 1.

Let and be independent and such that and . Define . It is easy to see that , and are not independent and at the same time they are uncorrelated: We will take a look on the behaviour of the function

This function may be calculated analytically but instead we draw the sample of size and calculate the conditional correlations numerically, see Figure 1 below. The conditional correlation coefficient increases until it reaches value 1 at as the condition implies full linear dependence .

The proof of Theorem 1 may be found in the next section. It is based on the properties of the Radon-Nikodym derivative and the conditional moments from Navarro et al. (1998). The same technique will allow us to prove Theorem 2 which characterizes the mutual independence of by the conditional correlation matrix given by

where satisfies and , , and the correlation is calculated with respect to the conditional probability . If for some and with we have then we shortly define

which avoids unnecessary techniqualities.

Theorem 2.

Let be random variables and . The following conditions are equivalent:

-

1.

random variables are mutually independent,

-

2.

for any with and the conditional correlation matrix equals to the identity matrix

(in case let ).

If the second moments are finite , , the bounded intervals may be replaced with (or with ).

We end this section with the following example.

Example 2.

Consider the following linear model

3 Conditional uncorrelation equals independence

Before we start proving theorems 1 and 2 we will need to introduce two lemmas and one observation. Let us start with the following lemma which follows directly from the results of Navarro et al. (1998).

Lemma 3.

-

1.

For any random variable , the function

(2) uniquely determines the probability distribution (the domain of the function is the set of pairs with ).

-

2.

For any random variable with , the function

(3) uniquely determines the probability distribution (the domain of the function is the set of with .)

Let denote the set of Borel probability measures on . In the whole paper we assume that

although other types of intervals could be considered as well. For any let

Paper Navarro et al. (1998) shows how the function

(uniquely) determines the distribution function (in case it is assumed that has a first moment: ). Observation 4 is a consequence of Lemma 3.

Observation 4.

If and are two probability measures (with finite first moments in case ) and , then conditioning

| (4) |

forces and, by Lemma 3, for any .

Proof.

Let us assume that and are random variables with , , so we may use the convenient notation , .

1. Consider the case which does not assume the existence of the first moments. Assume for a contradiction that for some we have

We have and without loss of generality we assume that . Let

| (5) |

For any we have and, by (4),

From the assumptions , and thus . Hence

As , we have . This forces and

It remains to show that contradicts . By definition of given by (5), and by , we have for any small . We thus may write (recall that ) :

Hence, by (4),

| (6) |

Let

We have, by , by and next by ,

a contradiction.

2. The proof of the case (with , ) is not very different than the above proof: first we show that for

the conditioning (4) (and the equality ) force , and next it remains to show that the situation and would lead to a contradiction.

∎

Now we will introduce some notation and definitions from measure theory, see Dudley (2018) or Rudin (1986) for more. Let denote the set of probability measures on the measurable space and let denote the set of Borel probability measures on . We will say that is a nonnegative measure on if is of the form , where and . We will say that is a signed measure if it is of the form , where and . We will say that a signed measure is absolutely continuous with respect to , denoted by , if for any with we have . For example, if is a random variable with then given by

is a signed measure on the measurable space with . A Borel measurable function is Radon-Nikodym derivative of a signed measure with respect to a nonnegative measure , denoted by , if we have

By Radon-Nikodym theorem, for any signed measure and a nonnegative measure , the Radon-Nikodym derivative exists if and only if . A useful property is that and , and , , then

| (7) |

Now we are ready to prove the following lemma. As in the previous section, all the random variables are defined on the probability space .

Lemma 5.

Let and be random variables with , and . Define the nonnegative measure and the signed measure , both on , by:

We have

Proof.

On the measurable space , where , we define two measures and by

By the definitions of and , and , and next by the definition of the conditional expectation

and

which implies

| (8) |

Above, from the formal perspective, is treated as a probability measure on the space which is smaller then . From (8), by (7), we have:

Hence, by the definition of the Radon-Nikodym derivative and by standard change of variables,

which implies . ∎

Now we are ready to prove the main results. We start with Theorem 1: Assume that contains the family . For any random variables and , the following conditions are equivalent:

-

1)

and are independent,

-

2)

for any with ,

Under additional assumption: and , we may replace the bounded intervals with the family ( or with ).

Proof.

We will prove the theorem under the assumption or .

1. We will start with the direct implication . The independence:

implies

and, by the definition of the conditional expectation, for any with ,

Now we will prove the second implication .

2. Assume that and .

2a. We will now consider the case . Fix with which implies that . More, for any we have

From condition 2) of the theorem, for any with we have

and thus

| (9) |

Note that

are nonnegative Borel measures with the same class of null sets . We now normalize those measures to obtain the corresponding probability measures:

and

We want to reformulate equation (9) in a way which will allow us to use Lemma 5. In this purpose define the following signed measures

so, for any with , equation (9) takes the form

| (10) |

Now, we apply Lemma 5 to the pair and (with ) which provides the Radon Nikodym-derivative . In case Equation forces (see the differentiation of measures from Mattila (1995)) but in case we need to use Lemma 5 again: the pair and , by Lemma 5 with , satisfies . Hence, the equation (10) takes the form

By Observation 4 (see also Navarro et al. (1998) for the details on how to reconstruct the probability distribution from the conditional first moments ), we have , . As with was fixed arbitrarily, by definitions of and , we have obtained that for all and with , we have

Thus, for with we have ended up with the following

| (11) |

As the conditioning does not depend on , it is easy to believe that and are independent. As Lemma 5 and Observation 4 and are still warm, we will use them again: Equation (11) may be rewritten as:

which, for any with , by Lemma 5, takes the form

By Observation 4, we have , where is arbitrary with . This implies that and are independent (note that if then the event is independent of for any .

2b. Now consider the case , where . By the assumption, and are conditionally uncorrelated in sense for any admissible ,. We will show that and are conditionally uncorrelated too. Note that for any we have , where . Furthermore, the covariance is translation-invariant and the class is translation invariant in sense Thus, for any with , we have:

Now, as we see that and are conditionally uncorrelated, by point 2a. and are independent. Hence, and are independent.

2c. Now we do not assume that is bounded from below. The random variables and are independent if and only if for any with the and are independent with respect to the conditional probability , i.e.

For any small enough let denote the covariance calculated on the probability space . Note that for any admissible we have and

By 2b., the and are independent with respect to the conditional probability measure . As may be arbitrarily small, and are independent.

3. It remains to consider the case without assuming the existence of the first moments of and . To prove that and are independent it is sufficient to prove that they are independent with respect to the conditional probability

for any large enough to have . On the probability space the and are integrable and conditionally uncorrelated by the assumptions (note that if and then ), which by point 2. implies that and are - independent for any large . ∎

In the above proof, points 2c. and 3. have been done separately because the reasoning from point 3. does not apply to the class . The second theorem may be proved by mathematical induction with use of the same techniques.

Theorem 2:

Assume that are random variables and . For any with and , denotes the conditional corelation matrix, i.e. (if let ) . The following conditions are equivalent:

-

1.

random variables are mutually independent,

-

2.

the conditional correlation matrix equals to the identity matrix, i.e.

for any with .

The bounded intervals may be replaced with under assumption that have finite second moments.

Proof.

The implication is straightforward and we will focus on The proof is based on the induction. The case is a straightforward conclusion from Theorem 1. Assume that Theorem 2 holds true for some natural and assume that we are given the random vector which satisfies condition 2., i.e. for any admissible . We may apply Theorem to any -dimensional vector of the form which implies the mutual independence of . Thus, to show the induction step it is enough to show that some marginal variable is independent of the -dimensional vector . The general induction step from to is the same as in the case from to but the notation is more complex. We will thus focus on the implication from to . Assume that We will show that is independent of the vector . The proof is similar the reasoning from the proof of Theorem 1 and we will be a little more concise.

1. Assume that are square-integrable.

1a) Assume that . If satisfy , then for , by the assumptions, we have

which may be rewritten as

| (12) |

We fix with and we normalize the nonnegative measures and to obtain the following two probability Borel measures

Now we rewrite (12) with use of and and next, as in the proof of Theorem 1, we use the Lemmas 3 and 5 to obtain , i.e.

| (13) |

for any and with . If then we rewrite (13) to obtain

| (14) |

Now fix and with and normalize the nonnegative measures and from the denominators of , and again use Lemmas 5 and 3 to obtain:

for any and with . In other words, for such , and any we have

| (15) |

By the assumptions, and are conditionally uncorrelated and thus, as Theorem 2 holds true for , and are independent. To sum up: for any and any with , by (15) and by the independence of and ,

which implies that is independent of the vector .This finishes the proof (recall that the marginals and are independent by Theorem 2 applied to the -dimensional vector ).

1b) If there is such that then note that the random variables satisfy the assumptions of Theorem 2 and thus they are mutually independent by point 1a). This forces the independence of .

1c) In general case , for any small with we consider the probability space on which, as we may note, the random vector satisfy for any admissible . By 1b), the marginals are mutually independent with respect to for any small enough wich implies that they are independent with respect to .

2. At the end note that in case we do not need the assumption that have finite moments as the conditional standard deviations are finite. Also, note that are bounded and conditionally uncorrelated on the probability space , where is large enough to have the following conditional probability well defined

By point 1., are mutually independent with respect to for any large which implies that are mutually independent with respect to . ∎

Funding. This research did not receive any specific grant from funding agencies in the public, commercial, or not-for-profit sectors.

Data availability statement. No datasets were generated or analysed during the current study.

Conflict of interest. The author has no conflicts of interest to declare that are relevant to the content of this article

References

- [1] Akemann, C. A., Bruckner, A. M., Robertson, J. B., Simons, S., and Weiss, M. L. (1984). Asymptotic conditional correlation coefficients for truncated data. Journal of mathematical analysis and applications, 99(2), 350-434.

- [2] Baba, K., Shibata, R., and Sibuya, M. (2004). Partial correlation and conditional correlation as measures of conditional independence. Australian and New Zealand Journal of Statistics, 46(4), 657-664.

- [3] Broffitt, J. D. (1986). Zero correlation, independence, and normality. The American Statistician, 40(4), 276-277.

- [4] Chernoff, P. R., Móri, T. F., Szanto, S., Erugin, N. P. and Evans, R. J. (1981). Advanced Problems: 6326-6329. The American Mathematical Monthly 88, 68–69.

- [5] David, H. A. (2009). A historical note on zero correlation and independence. The American Statistician, 63(2), 185-186.

- [6] De Paula, A. (2008). Conditional moments and independence. The American Statistician, 62(3), 219-221.

- [7] Dudley, R. M. (2018). Real analysis and probability. Chapman and Hall/CRC.

- [8] Hebda-Sobkowicz, J., Zimroz, R., Pitera, M., and Wyłomańska, A. (2020). Informative frequency band selection in the presence of non-Gaussian noise–a novel approach based on the conditional variance statistic with application to bearing fault diagnosis. Mechanical Systems and Signal Processing, 145, 106971.

- [9] Jaworski P., Pitera M., (2016), The 20-60-20 Rule, Discrete and Continuous Dynamical Systems - Series B vol. 21, Issue 4 (2016), 1149-1166

- [10] Jaworski, P., Jelito, D., and Pitera, M. (2024). A note on the equivalence between the conditional uncorrelation and the independence of random variables. Electronic Journal of Statistics, 18(1), 653-673.

- [11] Jaworski, P., Pitera, M. (2020). A note on conditional variance and characterization of probability distributions. Statistics and Probability Letters, 163, 108800.

- [12] Jelito, D. and Pitera, M. (2021). New fat-tail normality test based on conditional second moments with applications to finance. Statistical Papers 62 2083–2108.

- [13] Lawrance, A. J. (1976). On conditional and partial correlation. The American Statistician, 30(3), 146-149.

- [14] Mattila P., "Geometry of sets and measures in euclidean spaces". Cambridge Studies in Advanced Mathematics, 44. Cambridge University Press, Cambridge, 1995. MR1333890 Zbl 0911.28005

- [15] Navarro, J., Ruiz, J., and Zoroa, N. (1998). A unified approach to characterization problems using conditional expectations. Journal of statistical planning and inference, 69(2), 193-207.

- [16] Pitera, M., Chechkin, A., and Wyłomańska, A. (2022). Goodness-of-fit test for -stable distribution based on the quantile conditional variance statistics. Statistical Methods and Applications, 31(2), 387-424.

- [17] Rudin, W. (1986). Real and complex analysis. MGH, 1986, ISBN: 9780071002769,0071002766