An efficient Wasserstein-distance approach for reconstructing

jump-diffusion processes using parameterized neural networks

Mingtao Xia1111corresponding author, Xiangting Li2, Qijing Shen3, Tom Chou41 Courant Institute of Mathematical Sciences, New York University, New York, NY

10012, USA

2 Department of Computational Medicine, UCLA, Los Angeles, CA

90095, USA

3 Nuffield Department of Medicine,

University of Oxford, Oxford OX2 6HW, UK

4 Department of Mathematics, UCLA, Los Angeles, CA

90095, USAxiamingtao@nyu.edu, xiangting.li@ucla.edu,qijing.shen@ndm.ox.ac.uk, tomchou@ucla.edu

(July 6, 2024)

Abstract

We analyze the Wasserstein distance (-distance) between two

probability distributions associated with two multidimensional

jump-diffusion processes. Specifically, we analyze a temporally

decoupled squared -distance, which provides both upper and lower

bounds associated with the discrepancies in the drift, diffusion, and

jump amplitude functions between the two jump-diffusion processes.

Then, we propose a temporally decoupled squared -distance method

for efficiently reconstructing unknown jump-diffusion processes from

data using parameterized neural networks. We further show its

performance can be enhanced by utilizing prior information on the

drift function of the jump-diffusion process. The effectiveness of

our proposed reconstruction method is demonstrated across several

examples and applications.

Jump-diffusion processes are widely used across many disciplines such

as finance [1, 2, 3],

biology [4], epidemiology [5],

and so on. A -dimensional jump-diffusion process may be written in

the following form [6]:

(1)

Here, is a -dimensional jump-diffusion

process and is a standard

-dimensional white noise; is a compensated Poisson

process of intensity independent of :

(2)

where is a Poisson process with intensity

and is a measure defined on

, the measure space of the Poisson

process. and are independent if and . and

denote the -algebra associated with and ,

respectively. The drift, diffusion, and jump functions are defined by

(3)

respectively. Specifically, if , then

Eq. (1) becomes

(4)

for . Here, each is a compensated Poisson

process with intensity . and

are independent if . When

, Eq. (1) reduces to the pure

diffusion process.

In this paper, we study the problem of reconstructing a jump-diffusion

process Eq. (1) or Eq. (4)

from observed data at different time points by using a

different jump-diffusion process

(5)

to approximate Eq. (1). In

Eq. (5), is a

-dimensional standard Brownian motion that is independent of

and in Eq. (1); is a compensated Poisson process of intensity and independent of , in

Eq. (1) as well as . Specifically,

we are interested in reconstructing the jump-diffusion process

Eq. (1) with little or no prior information on the

drift, diffusion, and jump functions , and

. To reconstruct or approximate Eq. (1)

using Eq. (5), we wish to find small errors

in the drift, diffusion, and jump functions, i.e., to find

, and such that

, , and

are small.

Thus far, most studies related to jump-diffusion processes have

focused on the forward-type problem of efficient simulation of a

jump-diffusion process given coefficients [7, 8]. There are also several studies on the

statistical properties of jump-diffusion processes such as their first

passage times [9, 10]. While there has been

some research into the inverse problem of reconstructing a general

pure diffusion process, there has been little work on reconstructing

unknown jump-diffusion processes from sample trajectories although two

main strategies have been proposed. First, regression methods are

applied to determine unknown parameters if the forms of drift,

diffusion, and jump functions (, and

in Eq. (1)) are known. Unknown

parameters in these functions can then be determined from data

[11, 12]. Another strategy for

reconstructing a jump-diffusion process is to calculate the empirical

probability density function from observation data

and then reconstruct the integrodifferential equation

satisfied by [13]. Yet, this

method requires a large number of observations at different time

points to obtain a good empirical approximation of the density

function . Recently, a

Wasserstein-generative-adversarial-network(WGAN)-based method was

proposed to reconstruct the jump-diffusion process

Eq. (1) [4]. However, training a

WGAN can be intricate and computationally expensive.

Recent advancements in machine learning make it possible to use

parameterized neural networks (NNs) for representing , and in

Eq. (5) which approximate , and in Eq. (1). For

example, a recent torchsde package in Python

[14] models pure diffusion processes (SDEs with

Brownian noise) by using parameterized neural networks. These methods

have been used in the reconstruction of diffusion processes. For

example, in [15], a deep Gaussian latent model has

been applied for reconstructing a pure diffusion process;

[16] uses the neural SDE model to reconstruct a

stochastic differential equation with Brownian noise by minimizing a

KL-divergence-based loss function. In

[17, 18], generative adversarial

networks were used to reconstruct general stochastic differential

equations including a Brownian motion noise term without requiring

prior knowledge of the specific forms of the drift or diffusion

functions.

Another recent work analyzes the upper bound for a smooth Wasserstein

distance between two distributions associated with two 1D

jump-diffusion processes at a given time [19].

Since the -distance can effectively measure discrepancies between

probability measures over a metric space

[20, 21], an efficient

squared-Wasserstein-distance-based method for reconstructing pure

diffusion processes from data, without the need to specify forms for

the drift and diffusion, was recently proposed [22].

General jump-diffusion processes are distinct from pure diffusion

processes because the trajectories of jump-diffusion processes are

discontinuous. Thus, it remains unclear whether the Wasserstein

distance can also be employed to reconstruct an unknown jump-diffusion

process from data.

1.1 Contribution

In this paper, we analyze the -distance between two probability

distributions associated with two multidimensional jump-diffusion

processes Eqs. (1) and

(5). We then show that a temporally

decoupled squared Wasserstein distance can serve as effective

upper and lower error bounds on the errors in the drift,

diffusion, and jump functions ,

, and in

Eqs. (1) and (5),

respectively. This temporally decoupled squared Wasserstein distance

can be effectively evaluated using finite-sample observations at

discrete time points. Thus, we propose using this temporally decoupled

squared -distance to reconstruct general jump-diffusion processes

with the help of parameterized neural networks. Furthermore, we

explore how prior information on the drift function enhances the

performance of our temporally decoupled squared Wasserstein distance

method. Our results greatly extend the results in [22]

(reconstructing 1D pure diffusion processes) to allow for the

reconstruction of multidimensional jump-diffusion

processes. Specifically, we

1.

prove that the -distance is a lower bound for the errors

, and

. Thus, minimizing the -distance is

necessary for reconstructing the multidimensional jump-diffusion

process Eq. (1).

2.

analyze a temporally decoupled squared -distance defined

in [22] and show that it can be efficiently evaluated by

finite-sample empirical distributions. Thus, it is suitable to serve

as a loss function to minimize for reconstructing

Eq. (1) using parameterized neural networks.

3.

conduct numerical experiments to demonstrate the efficacy of

using the temporally decoupled squared Wasserstein distance to

reconstruct jump-diffusion processes. Our temporally decoupled

squared Wasserstein method performs better than some other benchmark

methods. Additionally, we propose incorporating prior information on

the drift function, which greatly improves the accuracy of

reconstructed diffusion and jump functions.

1.2 Organization

In Section 2, we analyze how the -distance between the

probability measures associated with solutions to two jump-diffusion

processes Eqs. (1) and (5)

can be a lower bound of the errors in the reconstructed drift,

diffusion, and jump functions ,

, and .

In Section 3, we analyze a temporally decoupled squared

-distance and show how it can be more effectively evaluated than

the squared distance. Specifically, the temporally decoupled

squared distance is smaller than the distance analyzed in

Section 2 while providing an upper bound of the errors in

the reconstructed drift, diffusion, and jump functions. Thus,

Sections 2 and 3 together show that our

temporally decoupled squared distance provides both upper and

lower error bounds. In Section 4, numerical experiments

are carried out to compare our proposed jump-diffusion process

reconstruction methods with other methods for reconstructing different

jump-diffusion processes. Additionally, we show how prior information

on the drift function of the ground truth jump-diffusion process

Eq. (1) improves the reconstruction of the

diffusion and jump functions in Eq. (1). In

Section 5, we summarize our proposed jump-diffusion

process reconstruction approach and suggest potential future

directions.

2 The -distance between the probability measures associated with

the jump-diffusion processes in Eqs. (1) and (5)

In this section, we shall show how the -distance between the

probability measures associated with the two jump-diffusion processes

Eqs. (1) and (5) can serve

as a lower bound for the errors ,

, and .

First, we specify the assumptions on the jump-diffusion processes in

Eqs. (1) and (5).

Assumption 2.1.

We assume that the jump-diffusion processes defined in

Eq. (1) satisfy the

following conditions:

1.

For each non-increasing sequence converging to

the empty set , .

2.

is a càdlàg martingale

for all , and .

3.

is an orthogonal

martingale measure with intensity ,

i.e., for any and

and any

(the measure on is ), we have

(6)

4.

Trajectories generated from both jump-diffusion processes,

Eqs. (1) and (5), reside

in the space .

5.

The drift, diffusion, and jump functions are all uniformly

Lipschtiz continuous, i.e., there exists three positive

constants

such that ,

(7)

Furthermore, we assume that conditions (i)-(iv) also hold for the

compensated Poisson process in

Eq. (5), and that condition (v) holds for the

drift, diffusion, and jump functions in

Eq. (5).

Now consider the -distance between the distributions associated

with solutions generated from the target jump-diffusion process

Eq. (1) and the approximate jump-diffusion process

Eq. (5), as defined below.

Definition 2.1.

For two -dimensional jump-diffusion processes

(8)

in the separable space with two associated probability distributions , respectively, the -distance for

is defined as

(9)

In Eq. (9), the norm is defined as

and iterates over all

coupled distributions of ,

defined by the condition

(10)

where denotes the

Borel -algebra associated with the space of -dimensional

functions in .

To prove that defined in Eq. (9) is a

lower bound for the errors in the drift, diffusion, and jump functions

, , and

, we first prove the following theorem.

Theorem 2.1.

Suppose and are two -dimensional

jump-diffusion processes that are determined by

Eq. (1) and Eq. (5). We

denote

(11)

and assume that

(12)

are martingales for all .

Then, the following inequality holds:

(13)

where denotes the -norm of a -dimensional vector,

is the initial condition, and is defined as

(14)

The proof to Theorem 2.1 is similar to the proof of the

stochastic Gronwall lemma (Theorem 2.2 in [6])

and is given in A. Theorem 2.1 greatly

generalizes the results of Theorem 1 in [22], which was

developed for analyzing the -distance between two one-dimensional

pure diffusion processes. Now, with Theorem 2.1, we can

analyze the -distance between two multi-dimensional jump-diffusion

processes.

The following corollary establishes the upper bound of the

-distance between and

, the two probability distributions associated with

jump-diffusion processes Eqs. (1) and

(5).

Corollary 2.1.

(Upper error bound for the -distance) The following bound holds

for , where and are the two

probability distributions associated with jump-diffusion processes

Eqs. (1) and (5)

The proof of Corollary 2.1 is a direct application of

Theorem 2.1. We denote to be the

distribution of defined in

Eq. (11). Since has the same

distribution as , we have, by the Hölder’s inequality

(16)

Using Eq. (13) and the fact that is non-decreasing

w.r.t. , we have

From Corollary 2.1, it is necessary to have a small

in Eq. (15) such that the errors in

the drift, diffusion, and jump functions ,

, and can

be small. Note that Corollary 2.1 analyzes the classic

-distance , which is different from the

smooth Wasserstein distance in [19] (the

classical Wasserstein distance is an upper bound for the smooth

Wasserstein distance used in [23]).

cannot be directly used as a loss

function to minimize as we cannot directly evaluate

in Eq. (9) since this term

requires evaluation of the integral .

However, when (), we shall show that we can

efficiently estimate by using finite-time-point

observations of the two jump-diffusion processes and

.

Let to be a mesh grid in the time interval

, and we define the following projection operator

(18)

The projected in Eq. (18) is piecewise

constant and is thus in the space . We denote the

distributions of and

in

Eq. 18 by and , respectively. We will

prove the following theorem for bounding the error .

Theorem 2.2.

(Finite-time-point approximation for distance) The following

triangular inequality for holds:

(19)

In Eq. (19), are the probability

distributions associated with and defined

in Eq. (18), respectively. Furthermore, we assume that

(20)

where and solve

Eqs. (1) and (5),

respectively.

Then, we have the following bound

(21)

where .

The proof to Theorem 2.2, given in B,

uses the Itô isometry as well as the orthogonal assumption of the

compensated Poisson process in Assumption 2.1.

Theorem 2.2 indicates that can be

approximated by the finite-time-point projections and

. Specifically, Theorem 2.2 is a

generalization to Theorem 2 in [22], developed for the pure

diffusion. Note that Eq. (21) holds for but Eq. (21) might

not hold for as we cannot directly apply the Itô isometry to the compensated

Poisson process for .

It has been shown in [22] that for reconstructing pure

diffusion processes, minimizing a temporally decoupled squared

distance can yield more accurate reconstructions of the drift and

diffusion functions than direct minimization of the squared

distance defined in

Eq. (9). Additionally, the squared distance is an upper bound of the temporally decoupled squared

distance that will be discussed in Section 3. Thus,

Corollary 2.1 also applies to the temporally decoupled

squared distance.

3 A temporally decoupled squared distance

In this section, we propose and analyze a temporally decoupled squared

distance, which could help effectively approximate the

jump-diffusion process Eq. (1) by the reconstructed

jump-diffusion process Eq. (5). Specifically,

we show why this temporally decoupled squared distance can be

more effectively evaluated using empirical distributions, making it a

more appealing choice than the squared distance discussed in Section 2. The

temporally decoupled squareddistance is

defined as

(22)

where are the distributions of -dimensional

random variables and at time ,

respectively:

(23)

where the joint distribution satisfies

(24)

The integration on the RHS of Eq. (22) is defined as

the limit

(25)

where is a grid mesh on the time interval and in the following. Here, we shall prove

that the temporally decoupled squared distance

is well defined and can be a more

effective loss function when seeking to reconstruct multidimensional

jump-diffusion processes than the original squared . Two features make this so: i) numerically evaluating

the temporally decoupled squared distance

Eq. (22) using finite-sample empirical distributions

can be more accurate than evaluating the original squared

distance when the number of training samples

becomes larger, and ii) the temporally decoupled squared

distance Eq. (22) provides upper error bounds for

, and when reconstructing jump-diffusion processes.

We denote and to be the distributions

for and , respectively. We can prove the following theorem that

shows the limit on the RHS of Eq. (25) exists and

thus the temporally decoupled squared in

Eq. (22) distance is well defined.

Theorem 3.1.

(The temporally decoupled squared distance is well-defined) We

assume the conditions in Theorem 2.2 hold. Furthermore, we

assume that for any , as , the following

conditions are satisfied

(26)

Additionally, we assume that there is a uniform upper bound

(27)

Suppose , then

(28)

Furthermore, the limit

(29)

is simply defined in

Eq. (22). Denoting to be the coupling

probability distribution of , whose

marginal distributions coincide with and ,

we have the following bound:

(30)

where

(31)

Theorem 3.1 generalizes Theorem 3 in [22] from

pure diffusion processes to jump-diffusion processes. The proof to

Theorem 3.1 is in C. Specifically, from

Eq. (30), if is of order , then the convergence rate of

to is . Specifically, we have

(32)

From Eq. (21), the error bound of is . Therefore,

the upper error bounds of using the finite-time distributions

to approximate both or

are both of order .

Next, we shall show that using the finite-sample empirical

distribution to estimate

(33)

where is the coupling distribution of such that its marginal distributions are

and , is more accurate than using the

finite-sample empirical distribution to estimate (where and are the distributions

of and defined in

Eq. (18)).

Theorem 3.2.

(Finite sample empirical distribution error bound) We assume that

(34)

where is the norm of a vector in . We

denote to be empirical distributions of

and , respectively; we denote

to be the empirical

distributions of and . Suppose is the number of observed trajectories

and the number of reconstructed trajectories

. We find the following error bound for

estimating using the empirical

distributions:

(35)

where is a constant and

(36)

We also have the empirical error bound for estimating

using the empirical distributions

:

(37)

where is a constant different from . Furthermore, there

exists a constant such that

(38)

The proof of Theorem 3.2 is given in D

and utilizes the upper bound of the -distance between the

ground truth distribution and the empirical distribution in

[24]. Specifically, if , then , and

(39)

Therefore, Theorem 3.2 indicates that as the number of

observed trajectories of the jump-diffusion process increases,

the upper bound of converges faster to 0 than the

upper bound of does when . Thus,

(40)

can be more accurately evaluated by the finite-sample empirical

distributions than the squared distance when is large.

For any coupled distribution such that

its marginal distributions are and , its marginal

distributions w.r.t and are

and , respectively. Thus,

(41)

Letting in Eq. (41), from

Theorems 2.2 and 3.1, we conclude that

(42)

Thus, Corollary 2.1 also provides an upper error bound

for the temporally decoupled . Next,

we show that there is a lower bound for and this lower bound depends on drift, diffusion, and jump

functions of the ground truth jump-diffusion process

Eq. (1) and the approximate jump-diffusion process

Eq. (5).

Theorem 3.3.

(Lower error bound for the temporally decoupled squared

-distance) We have the following lower bound:

(43)

where are two matrices in

with their elements defined by

(44)

The square roots and are the positive roots.

Proof.

First, we denote

(45)

and let and to be the probability

distributions of and , respectively.

From Theorem 1 in [25], we have

A lower bound for the temporally decoupled squared distance

between two jump-diffusion processes that depends on the expectation

of the summation of the error in the jump and the error in the

diffusion functions is worth further investigation. Such an intricate

analysis is beyond the scope of this paper but could imply that

minimizing the distance is necessary for a good reconstruction

of both the diffusion function and the jump function. Moreover, when

, it is not easy to make further simplifications to

Eq. (43). Analysis of the properties of the matrix

in

Eq. (43) can be quite difficult. Nonetheless, we

shall show in our numerical examples that our temporally decoupled

squared -distance method can

accurately reconstruct both the diffusion and the jump functions in

several examples of one-dimensional and multidimensional

jump-diffusion processes especially when the drift function can be

provided as prior information.

4 Numerical experiments

In this section, we implement our methods through numerical examples

and investigate the effectiveness of the temporally decoupled squared

-distance method for reconstructing the jump-diffusion process

Eq. (1). We also compare our results with those

derived from using other commonly used losses in uncertainty

quantification and methods for jump-diffusion process

reconstruction. Additionally, we explore how prior knowledge on the

ground truth jump-diffusion process Eq. (1) helps

in its reconstruction. All experiments are carried out using Python

3.11 on a desktop with a 32-core Intel® i9-13900KF CPU (when comparing

runtimes, we train each model on just one core).

In all experiments, we use three feed-forward neural networks to

parameterize the drift, diffusion, and jump functions in the

approximate jump-diffusion process Eq. (5),

i.e.,

(52)

are the parameter sets in the three

parameterized neural networks, respectively. We modified the

torchsde Python package in [14] to implement

the Euler-Maruyama scheme for generating trajectories of the two

jump-diffusion processes Eqs. (1) and

(5). Details of the training settings and

hyperparameters for all examples are given in

E. In Examples 4.1 and

4.2, the reconstruction errors are the relative

errors:

(53)

(54)

(55)

where is the number of time steps and is the number of

training trajectories.

Example 4.1.

For our first example, we reconstruct the following 1D jump-diffusion

process for describing the non-defaultable zero-coupon bond pricing

[2]:

(56)

where , are independently identically

distributed, and obeys the Poisson distribution with intensity

. We take so that Eq. (56) can be

rewritten as

(57)

with a 1D compensated Poisson process with intensity

. We define ground truth by in

Eq. (57) and take and initial condition

. We reconstruct Eq. (57) by minimizing

the temporally decoupled -distance Eq. (40).

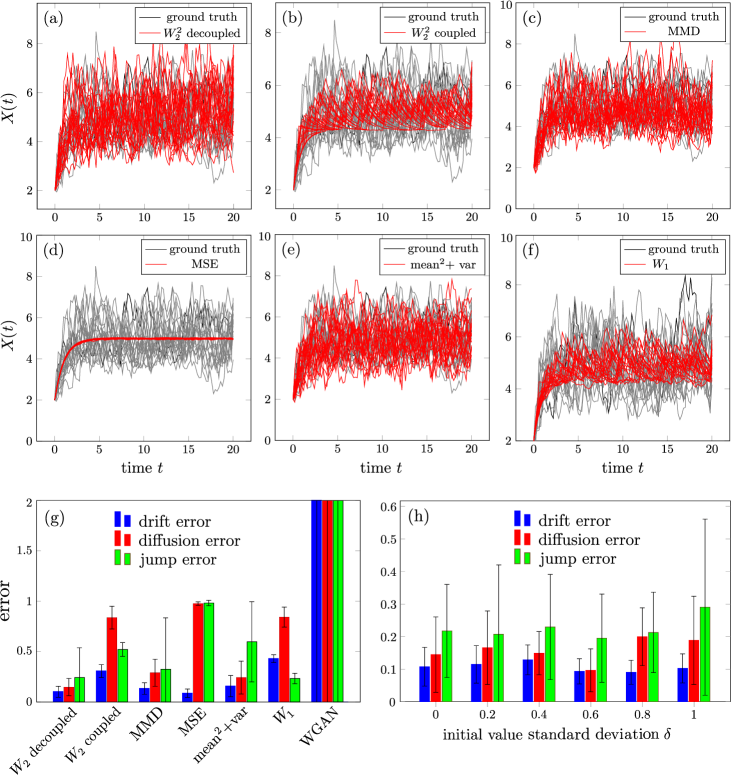

Figure 1: Reconstruction of trajectories and model functions. We

define ground truth as in

Eq. (57), with and initial

condition . (a-f) ground truth (black) and reconstructed

trajectories (red) generated from the learned jump-diffusion

process by minimizing different loss functions or using

different methods. (g) The reconstruction errors of the drift,

diffusion, and jump functions defined in

Eqs. (53), (54), and

(55). We compare errors from minimizing our

temporally decoupled squared -distance versus those from

minimizing the MSE, MMD, mean2+var, the -distance

, the squared -distance , and the error of results obtained using the WGAN

method. The mean and standard deviation of the error for

different methods are obtained by repeating the experiment 10

times. (h) The reconstruction errors in the drift, diffusion,

and jump functions defined in Eqs. (53),

(54), and (55) w.r.t. the

standard deviation of the initial condition

(Eq. (58)).

We compare our temporally decoupled squared distance loss

function with the WGAN method and other loss functions (MSE, MMD,

mean2+var, distance, and the squared distance

. The definitions of the other loss

functions are given in F). As shown in

Fig. 1(a-f), the trajectories we obtained by

minimizing our temporally decoupled squared -distance accurately

match the ground truth trajectories generated by

Eq. (57). When using ,

, and MSE loss functions, the reconstructed

trajectories deviate qualitatively from those of the ground truth.

The solutions of the reconstructed jump-diffusion process generated by

the WGAN method are also qualitatively incorrect and are thus not

shown here. From Fig. 1(g), minimizing our temporally

decoupled squared -distance gives the smallest reconstruction

errors , and . The

average errors in the reconstructed drift, diffusion, and jump are

kept below 0.25. Thus, minimizing our temporally decoupled squared

distance is found to be more accurate in reconstructing the

jump-diffusion process Eq. (57) than other

benchmark methods. We also list the average runtime per training

iteration as well as the memory usage of different methods in

Table 1. The runtime of the WGAN method is

significantly longer than that of other methods. Furthermore, the

computational cost of using our temporally decoupled squared is

similar to the cost of using other loss functions while our temporally

decoupled squared method can accurately reconstruct

Eq. (57).

Table 1: The runtime and memory usage of different methods

(loss functions) to reconstruct the jump-diffusion process

Eq. (57).

Method (loss)

temporally

decoupled

MMD

MSE

mean2+var

WGAN

Average time/iteration (s)

44.5

48.2

59.4

29.8

48.7

39.2

346.3

Average memory use (Gb)

2.61

3.52

2.59

5.00

2.61

2.60

3.34

We test the numerical performance of our temporally decoupled squared

method when reconstructing Eq. (57) under

different initial conditions. Instead of using the same initial

condition for all solutions, we sample the initial value from

(58)

where is the 1D normal distribution of mean

2 and variance . Using the same hyperparameters in the

neural networks and for training (in Table E) as

in Example 4.1, we varied the standard deviation and implemented the temporally decoupled

squared distance as a loss function. The results shown in

Fig. 1(h) indicate that the reconstruction of

Eq. (57) using the squared loss function

is rather insensitive to “noise”, i.e., the standard

deviation in the distribution of the initial condition.

Finally, we also use different values of the parameters and

in the diffusion and drift functions. The reconstructed drift

functions remain accurate when and are

varied. When are small, the corresponding diffusion

and jump functions can also be accurately reconstructed; however, when

are large, the reconstruction of the diffusion

function can be less accurate because the trajectories for training

are more sparsely distributed. Details of the results are given

in G.

It was shown in [22] that the accuracy of reconstructing a

pure-diffusion process ( in Eq. (1))

can deteriorate if trajectories for training are too sparsely

distributed (too few trajectories/too high noise). However, we find

that prior information on the drift function in

Eq. (1) enables efficient reconstruction even if

the number of training trajectories is limited, when the temporally

decoupled squared method for reconstructing jump-diffusion

processes without prior information would otherwise fail. In the next

example, we demonstrate enhanced reconstruction performance after

incorporating prior information on the drift function of

Eq. (1), greatly improving the accuracy of

reconstructed diffusion and jump functions.

Example 4.2.

Consider the following 1D jump-diffusion process

(59)

where is a 1D compensated Poisson process with intensity

. This model, if we set , can describe the

posited stock returns under a deterministic jump ratio

[1]. To test the efficiency of our temporally

decoupled squared -distance method, we set (i.e., the drift function to be a constant

risk-free interest rate [26]), the initial condition

, and and explore different forms of the diffusion

and jump functions and . We then input

the drift, diffusion, or the jump function , or

in Eq. (59) as prior information to test how

well our method can reconstruct the other terms.

Summarizing, i) we first give no prior information and reconstruct all

three functions , and ; ii) we specify the

risk-free interest rate and reconstruct ,

and ; iii) we provide the diffusion function and

reconstruct and ; iv) we provide the jump function

and reconstruct , and . In this example, “const”

refers to using a constant diffusion or jump function:

(60)

“linear” refers to using a linear diffusion or jump function

(61)

and “langevin” refers to using a diffusion or jump function of the

following form

(62)

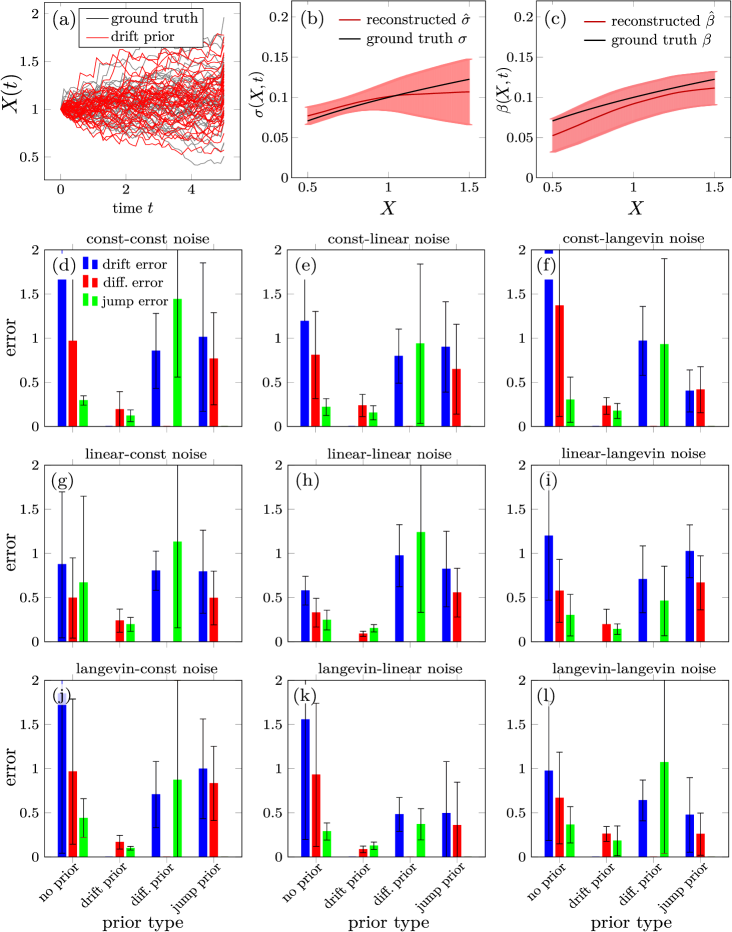

Figure 2: (a) The trajectories generated by the ground truth (black)

jump-diffusion process with and given drift function

in Eq. (59), plotted against reconstructed

trajectories (red) using the same drift function prior. (b-c) The

ground truth diffusion and jump functions

and ) shown against the reconstructed functions

and . (with drift function

given as prior). The red curves are the mean

and while the shaded bands show their standard

deviations, calculated over 5 independent experiments). (d-k) The

reconstruction errors of the drift, diffusion, and jump functions

without prior information on Eq. (59) or with one

of the drift, diffusion, and jump functions given. When the drift

function is given, errors in the reconstructed diffusion and jump

functions are the smallest in all cases (error bars under “drift

prior.”)

To illustrate the reconstruction, we set in

Eqs. (60), (61), and (62),

and plot in Fig. 2(a) the ground truth solutions

(black) generated from Eq. (59) with a given drift

function. Using the same drift function, trajectories of the

reconstructed jump-diffusion process are shown in red and exhibit a

distribution that matches well with that of the ground truth

solutions. Moreover, as shown in Fig. 2(b,c), the

differences between the learned diffusion and jump functions

and and the ground truth

diffusion and jump functions are small.

If no prior information on Eq. (59) is given, the

average errors for the reconstructed drift, diffusion, and jump

functions are 1.412, 0.790, and 0.347, respectively. This high error

might arise from training set trajectories that are too noisy or

sparsely distributed. However, if the drift function is given, the

diffusion and jump functions can be much more accurately

reconstructed, leading to relative errors below 0.2 for all three

forms of and used to define the

ground truth [see Fig. 2 (d-k)]. On the other hand,

providing the diffusion or jump function does not improve the accuracy

of the reconstruction of the other unknown functions in

Eq. (59). The average errors of the reconstructed

diffusion and jump functions, when different prior information is

given, are listed in Table 2.

In H, we carry out an additional numerical experiment by

varying the number of trajectories in the training set. The errors in

the reconstructed drift, diffusion, and jump function decrease when

the number of trajectories for training increases without any prior

information. This indicates that our temporally decoupled squared

method has the potential to accurately reconstruct

Eq. (59) even without prior information provided

there are a sufficient number of training trajectories. On the other

hand, if the drift function is given as prior information, the errors

of the reconstructed diffusion and jump functions are around 0.2 even

when only 100 trajectories are used. Therefore, information on the

drift function can significantly boost the performance of our

temporally decoupled squared method, allowing accurate

reconstruction of Eq. (59) even when the number of

observed trajectories is limited.

In real physical systems, the drift function can often be obtained by

measurements over a macroscopic ensemble of trajectories, such as

mass-action kinetics if the in Eq. (1) denotes

some physical quantity, e.g., the number density of molecules

[27, 28]. Thus, after

independently measuring the drift function and inputting it as a prior

knowledge, our temporally decoupled squared -distance method can

be used to reconstruct the diffusion and jump functions efficiently.

Table 2: Average errors in the reconstructed drift, diffusion, and

jump functions when using the temporally decoupled squared

distance to reconstruct Eq. (59). The error is

taken over 9 possible combinations of different forms of diffusion

and jump functions (constant, Langevin, and linear in

Eqs. (60), (62), and (61)) in

Fig. 2.

Prior info

error of reconstructed

Error

of reconstructed

Error of reconstructed

No prior

Given

0

Given

0

Given

0

We carry out an extra numerical experiment reconstructing

Eq. (59) by varying in

Eqs. (60), (61), and (62). With the

drift function provided, our temporally decoupled squared

-distance method can accurately reconstruct the diffusion and the

jump functions for different values of and in

Eqs. (60), (61), and (62). The

results are shown in I.

In our last example, we test whether our temporally decoupled

squared -distance can accurately reconstruct a 2D jump-diffusion

process with correlated Brownian-type and compensated-Poisson-type

noise across the two stochastic variables.

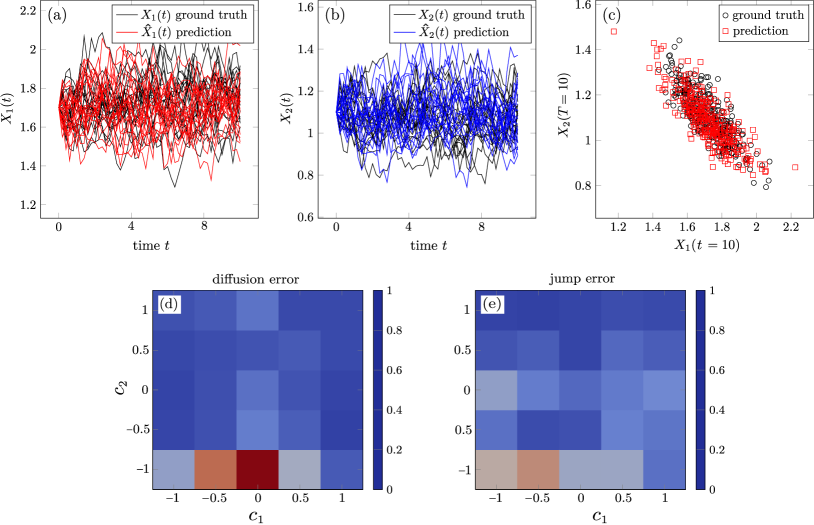

Example 4.3.

We reconstruct the following 2D jump-diffusion process, which is

obtained by superimposing a 2D compensated Poisson process

onto the

pure diffusion process that describes the dynamics of a synthetic data

set [4, 29]:

(63)

and are independent and both have

intensity . Here, ,

is the drift

function, and are the

diffusion and jump functions, respectively. The drift function

is given by

(64)

The parameters are set as . We set and an

initial condition .

We take the correlated diffusivity as

(65)

and the jump function of the compensated Poisson

process as

(66)

Here, and determine the correlations of Brownian noise

and compensated Poisson process across the two dimensions,

respectively. Specifically, when (or ), the Brownian

(or compensated Poisson) noise in each variable is independent of the

other; when (or ), the Brownian-type (or

compensated-Poisson-type) noise across the two dimensions are linearly

dependent; when (or ), the Brownian-type (or

compensated-Poisson-type) noise across the two dimensions are

perfectly negatively correlated.

From Example 4.2, imposing a prior on the drift function

can greatly improve the accuracy of the reconstructed diffusion and

jump functions. Thus, we input defined in

Eq. (64) as prior information. Since the jump-diffusion

process described by Eq. (63) is two-dimensional, we

use the following error metric to measure the errors in the

diffusion and jump functions:

(67)

(68)

Here, denotes the Frobenius norm of a matrix. We set

in Eqs. (65) and

(66). Different values of are used to tune the

correlations to explore how they affect the reconstruction of the

jump-diffusion process.

Figure 3: (a-b) Solutions generated by the reconstructed jump-diffusion

process using our temporally decoupled squared method versus

solutions generated by the ground truth

Eq. (63). (c) The reconstructed

versus the ground truth . In (a-c), .

(d) The error (Eq. (67)) between the ground truth

diffusion function and the reconstructed diffusion

function . (e) The error (Eq. (68))

between the ground truth jump function and the

reconstructed diffusion function . In (d-e), the

errors are averaged over 5 independent experiments.

Figs. 3(a-c) show that solutions generated by our

reconstructed jump-diffusion process with the temporally decoupled

squared loss function match well with solutions generated by the

2D jump-diffusion process Eq. (63) ( in

Eqs. (65) and (66)). Figs. (3)(d-e)

indicate that when the drift function is given,

our temporally decoupled squared method can accurately

reconstruct the diffusion and jump functions for most combinations of

The average errors in the diffusion and jump functions

averaged over all combinations of are 0.197 and 0.210,

respectively. Also, the final distribution of the reconstructed

aligns well with the ground truth .

In J, we implement our reconstruction method by

using different numbers of hidden layers and different numbers of

neurons in each layer for the neural-network-parameterized

approximation to the diffusion and jump functions and

. We find that with the drift function given as prior information,

increasing the number of neurons per layer can improve the accuracy of

the reconstructed diffusion and the jump function of the 2D

jump-diffusion process Eq. (63). Increasing the number

of hidden layers also leads to a more accurate reconstruction of the

diffusion and jump function when the number of hidden layers is

smaller than three; however, after three hidden layers, increasing

their number leads to less accuracy of the reconstructed

and . Setting the number of hidden layers to three and

the number of neurons per layer to about 400 leads to excellent

reconstruction of and . However, larger

numbers of hidden layers or neurons per hidden layer demand more

memory usage and lead to longer runtimes. The optimal network

architecture for reconstructing the diffusion and jump functions is

worth further investigation.

5 Summary & conclusions

In this paper, we proposed and analyzed Wasserstein-distance-based

loss functions for reconstructing jump-diffusion

processes. Specifically, we showed that a temporally decoupled squared

-distance defined in

Eq. (22) provides both upper and lower bounds for

errors in the drift, diffusion, and jump functions

, , and

when approximating a jump-diffusion

process Eq. (1) by another jump-diffusion process

5. Moreover, the temporally decoupled squared

-distance can be efficiently evaluated using finite-sample

finite-time-point observations, which yields an easy-to-calculate loss

function for reconstructing jump-diffusion processes.

Through several numerical experiments, we showed that minimizing our

proposed temporally decoupled squared -distance loss performs

much better than other commonly used loss functions and methods

for jump-diffusion process reconstruction using

parameterized neural networks. Furthermore, we showed that if we imposed

prior knowledge on the drift function of the jump-diffusion process,

then the diffusion and jump functions could be more accurately

reconstructed.

Although we analyzed a 2D stochastic jump-diffusion process,

investigating how our temporally decoupled squared method

performs in higher dimensional jump-diffusion processes with more general noise

correlation matrices should be further explored. Such analyses would

inform how our approach can be directly applied to real-world

multi-dimensional jump-diffusion models with applications in finance,

biology, physics, and other disciplines. Similarly, how the

Wasserstein distance can be adapted to reconstruct other stochastic

processes such as Lévy walks involving compound Poisson process

[30, 31] is a potentially fruitful

area of further investigation. Reconstructing such processes could

require inferring the intensity of the Poisson process, which is

nontrivial and would require consideration of differentiation

w.r.t. “discrete randomness” [32].

Data availability statement

No data was used during this study. All code will be published upon

acceptance of this manuscript.

Conflict of interest

The authors declare that they have no conflicts of interest to report

regarding the present study.

References

References

[1]

Robert C Merton.

Option pricing when underlying stock returns are discontinuous.

Journal of Financial Economics, 3(1-2):125–144, 1976.

[2]

Jiwook Jang.

Jump diffusion processes and their applications in insurance and

finance.

Insurance: Mathematics and Economics, 41(1):62–70, 2007.

[3]

Koichi Maekawa, Sangyeol Lee, Takayuki Morimoto, and Ken-ichi Kawai.

Jump diffusion model with application to the Japanese stock market.

Mathematics and Computers in Simulation, 78(2-3):223–236,

2008.

[4]

Jia-Xing Gao, Zhen-Yi Wang, Michael Q Zhang, Min-Ping Qian, and Da-Quan Jiang.

A data-driven method to learn a jump diffusion process from aggregate

biological gene expression data.

Journal of Theoretical Biology, 532:110923, 2022.

[5]

Almaz Tesfay, Tareq Saeed, Anwar Zeb, Daniel Tesfay, Anas Khalaf, and James

Brannan.

Dynamics of a stochastic COVID-19 epidemic model with

jump-diffusion.

Advances in Difference Equations, 2021(1):1–19, 2021.

[6]

Sima Mehri and Michael Scheutzow.

A stochastic Gronwall lemma and well-posedness of path-dependent

SDEs driven by martingale noise.

arXiv preprint arXiv:1908.10646, 2019.

[7]

Bruno Casella and Gareth O Roberts.

Exact simulation of jump-diffusion processes with Monte Carlo

applications.

Methodology and Computing in Applied Probability, 13:449–473,

2011.

[8]

Steve AK Metwally and Amir F Atiya.

Using Brownian bridge for fast simulation of jump-diffusion

processes and barrier options.

The Journal of Derivatives, 10(1):43–54, 2002.

[9]

Steven G Kou and Hui Wang.

First passage times of a jump diffusion process.

Advances in Applied Probability, 35(2):504–531, 2003.

[10]

Di Zhang and Roderick VN Melnik.

First passage time for multivariate jump-diffusion processes in

finance and other areas of applications.

Applied Stochastic Models in Business and Industry,

25(5):565–582, 2009.

[11]

Leonardo Rydin Gorjão, Jan Heysel, Klaus Lehnertz, and M Reza Rahimi Tabar.

Analysis and data-driven reconstruction of bivariate jump-diffusion

processes.

Physical Review E, 100(6):062127, 2019.

[12]

Cyrus A Ramezani and Yong Zeng.

Maximum likelihood estimation of asymmetric jump-diffusion processes:

application to security prices.

Available at SSRN 606361, 1998.

[13]

Leonardo Rydin Gorjão, Dirk Witthaut, and Pedro G Lind.

jumpdiff: A Python library for statistical inference of

jump-diffusion processes in observational or experimental data sets.

Journal of Statistical Software, 105:1–22, 2023.

[14]

Xuechen Li, Ting-Kam Leonard Wong, Ricky TQ Chen, and David Duvenaud.

Scalable gradients for stochastic differential equations.

In International Conference on Artificial Intelligence and

Statistics, pages 3870–3882. PMLR, 2020.

[15]

Belinda Tzen and Maxim Raginsky.

Neural stochastic differential equations: deep latent Gaussian

models in the diffusion limit.

arXiv preprint arXiv:1905.09883, 2019.

[16]

Anh Tong, Thanh Nguyen-Tang, Toan Tran, and Jaesik Choi.

Learning fractional white noises in neural stochastic differential

equations.

In Advances in Neural Information Processing Systems,

volume 35, pages 37660–37675, 2022.

[17]

Patrick Kidger, James Foster, Xuechen Li, and Terry J Lyons.

Neural SDEs as infinite-dimensional GANs.

In International Conference on Machine Learning, pages

5453–5463. PMLR, 2021.

[18]

Yuan Chen and Dongbin Xiu.

Learning stochastic dynamical system via flow map operator.

arXiv preprint arXiv:2305.03874, 2023.

[19]

Jean-Christophe Breton and Nicolas Privault.

Wasserstein distance estimates for jump-diffusion processes.

Stochastic Processes and their Applications, page 104334, 2024.

[20]

Cédric Villani et al.

Optimal transport: old and new, volume 338.

Springer, 2009.

[21]

Wenbo Zheng, Fei-Yue Wang, and Chao Gou.

Nonparametric different-feature selection using Wasserstein

distance.

In 2020 IEEE 32nd International Conference on Tools with

Artificial Intelligence (ICTAI), pages 982–988. IEEE, 2020.

[22]

Mingtao Xia, Xiangting Li, Qijing Shen, and Tom Chou.

Squared Wasserstein-2 distance for efficient reconstruction of

stochastic differential equations.

arXiv preprint arXiv:2401.11354, 2024.

[23]

Benjamin Arras and Christian Houdré.

On Stein’s method for infinitely divisible laws with finite

first moment.

Springer, 2019.

[24]

Nicolas Fournier and Arnaud Guillin.

On the rate of convergence in Wasserstein distance of the empirical

measure.

Probability Theory and Related Fields, 162(3-4):707–738, 2015.

[25]

DC Dowson and BV Landau.

The Fréchet distance between multivariate normal distributions.

Journal of Multivariate Analysis, 12(3):450–455, 1982.

[26]

John Hull.

Options, futures, and other derivative securities, volume 7.

Prentice Hall Englewood Cliffs, NJ, 1993.

[27]

Andrei B Koudriavtsev, Reginald F Jameson, and Wolfgang Linert.

The law of mass action.

Springer Science & Business Media, 2011.

[28]

Vijaysekhar Chellaboina, Sanjay P Bhat, Wassim M Haddad, and Dennis S

Bernstein.

Modeling and analysis of mass-action kinetics.

IEEE Control Systems Magazine, 29(4):60–78, 2009.

[29]

Shaojun Ma, Shu Liu, Hongyuan Zha, and Haomin Zhou.

Learning stochastic behaviour from aggregate data.

In International Conference on Machine Learning, pages

7258–7267. PMLR, 2021.

[30]

Jean Bertoin.

Lévy processes, volume 121.

Cambridge university press Cambridge, 1996.

[31]

Ole E Barndorff-Nielsen, Thomas Mikosch, and Sidney I Resnick.

Lévy processes: theory and applications.

Springer Science & Business Media, 2001.

[32]

Gaurav Arya, Moritz Schauer, Frank Schäfer, and Christopher Rackauckas.

Automatic differentiation of programs with discrete randomness.

Advances in Neural Information Processing Systems,

35:10435–10447, 2022.

[33]

Philippe Clement and Wolfgang Desch.

An elementary proof of the triangle inequality for the Wasserstein

metric.

Proceedings of the American Mathematical Society,

136(1):333–339, 2008.

[34]

Rémi Flamary, Nicolas Courty, Alexandre Gramfort, Mokhtar Z. Alaya,

Aurélie Boisbunon, Stanislas Chambon, Laetitia Chapel, Adrien Corenflos,

Kilian Fatras, Nemo Fournier, Léo Gautheron, Nathalie T.H. Gayraud,

Hicham Janati, Alain Rakotomamonjy, Ievgen Redko, Antoine Rolet, Antony

Schutz, Vivien Seguy, Danica J. Sutherland, Romain Tavenard, Alexander Tong,

and Titouan Vayer.

POT: Python optimal transport.

Journal of Machine Learning Research, 22(78):1–8, 2021.

[35]

Yujia Li, Kevin Swersky, and Rich Zemel.

Generative moment matching networks.

In International Conference on Machine Learning, pages

1718–1727. PMLR, 2015.

[36]

Xavier Glorot and Yoshua Bengio.

Understanding the difficulty of training deep feedforward neural

networks.

In Proceedings of the thirteenth international conference on

artificial intelligence and statistics, pages 249–256. JMLR Workshop and

Conference Proceedings, 2010.

[37]

Kaiming He, Xiangyu Zhang, Shaoqing Ren, and Jian Sun.

Deep residual learning for image recognition.

In Proceedings of the IEEE conference on computer vision and

pattern recognition, pages 770–778, 2016.

Here, we provide proof for Theorem 2.1. Our strategy is

similar to that used in the proof of the stochastic Gronwall lemma

(Theorem 2.2 in [6]). First, we apply the Ito’s

lemma to

(69)

Note that

(70)

Using the Lipschitz conditions on the drift, diffusion, and jump

functions , and in Assumption 2.1 as well as the Cauchy inequality, from Eq. (69)

and 70, we find

(71)

From Assumption 2.1 and the conditions in

Theorem 2.1, the second, third, and fourth terms on the RHS

of Eq. (71) are adapted and non-decreasing w.r.t. ; the

fifth and sixth terms on the RHS of Eq. (71) are

martingales. Thus, by taking the expectation of both sides of

Eq. (71), we find

(72)

where is defined in Eq. (14).

Applying Gronwall’s lemma to and noticing

that is non-decreasing w.r.t. , we conclude that

Here, we shall provide proof of Theorem 2.2, which

generalizes Theorem 2 in [22] for pure diffusion processes.

Denote

(74)

to be the space of piecewise functions. Clearly, it is a subspace of

. Also, the embedding map from

to preserves the norm, which

enables us to define the measures on induced by the measures . For

simplicity, we shall still denote those induced measures by .

Suppose are generated by two

jump-diffusion processes defined by Eq. (1) and

Eq. (5). The inequality Eq. (19) is

a direct result of the triangular inequality for the Wasserstein

distance [33] because .

Next, we prove Eq. (21). Because

(defined in Eq. (18)), we choose a specific

coupling measure, i.e. the coupled distribution, of that is essentially the “original” probability distribution.

To be more specific, for an abstract probability space associated with , and

can be characterized by the pushforward of via

and

respectively, i.e., , defined by , elements in the Borel

-algebra of ,

(75)

where is interpreted as a measurable map from

to , and is the preimage of

under . Then, the coupling is defined by

(76)

where are interpreted as a

measurable map from to . One can readily verify that the marginal

distributions of are and respectively.

Therefore, the squared can be bounded by

(77)

For each , by using the Itô’s isometry and the

orthogonality condition of the compensated Poisson process

(in Assumption 2.1), we have

(78)

where . Summing over ,

we have

(79)

where .

Similarly, we can show that

(80)

Plugging Eq. (79) and Eq. (80)

into Eq. (19), we have proved Eq. (21).

Here, we provide proof to Theorem 3.1. The proof builds

upon and generalizes the proof of Theorem 3 in [22] for

pure diffusion processes to jump-diffusion processes. First, notice

that

(81)

where are defined in

Eq. (20). By applying Theorem 2.2, for any , denoting , we have

(82)

where are the distributions for

and , respectively. Additionally, from

Eq. (30), we have

Now, suppose ;

to be two sets of grids on . We define a third set of grids such

that . Let . We denote and

to be the probability distribution of

and , , respectively.

We now prove that

(89)

as .

First, suppose in the interval , we have

,

then for , since

, we have

(90)

On the other hand, because we can take a specific coupling to be the

joint distribution of ,

(91)

Similarly, we have

(92)

Using the triangular inequality of the Wasserstein distance as well as the Cauchy inequality, we have

(93)

Substituting Eqs. (91), (92), (81), and

(93) into Eq. (90), we conclude that

(94)

Using Eq. (94) in Eq. (89), when the

conditions in Eq. (26) hold true, we have

Here, we provide definitions of loss functions used in our numerical

examples (the definitions of the MSE, mean2+var, and the MMD loss

functions are the same as Appendix E in [22]). Since we are

using a uniform mesh grid (), for simplicity, we shall omit in the

calculation of our loss functions:

1.

The squared Wasserstein-2 distance

where and

are the empirical distributions of the

vector and

, respectively. In

numerical examples, we use the following scaled squared

Wasserstein-2 distance:

(112)

where ot.emd2 is the function for solving the earth movers

distance problem in the ot package of Python

[34], is the number of ground truth and

predicted trajectories, is an -dimensional vector

whose elements are all 1, and is

a matrix with entries . is the 2-norm of a vector. is the vector of the values of the ground truth

trajectory at time points , and is the

vector of the values of the predicted trajectory at

time points .

2.

The temporally decoupled squared Wasserstein-2 distance

(Eq. (40)). In numerical examples, we use the

following scaled temporally decoupled squared Wasserstein-2

distance:

where is the time step and is the Wasserstein-2

distance between two empirical distributions of and , denoted by , respectively. These distributions are calculated by

the samples of the trajectories of at a given time

step , respectively. is calculated using the

ot.emd2 function, i.e.,

(113)

where is an -dimensional vector whose elements are

all 1, and is a matrix with

entries . is the vector of values of the ground truth

trajectory at time and is the vector of values of the

trajectory generated by the reconstructed jump-diffusion process at time .

3.

The Wasserstein-1 distance

where and

are the empirical distributions of the

vector and

, respectively. In

numerical examples, we use the following scaled distance:

(114)

where ot.emd2 is the function for solving the earth movers

distance problem in the ot package of Python, is the

number of ground truth and predicted trajectories, is

an -dimensional vector whose elements are all 1, and

is a matrix with entries

. is the vector of the

values of the ground truth trajectory at time points

, and is the vector of the values of

the predicted trajectory at time points

.

4.

Mean squared error (MSE) between the trajectories, where

is the total number of the ground truth and predicted

trajectories. and are the values of the

ground truth and prediction trajectories at time

, respectively:

5.

The summation of squared distance between mean trajectories and

absolute values of the discrepancies in variances of trajectories,

which is a common practice for estimating the parameters of an SDE.

We shall denote this loss function by

Here and and have the same meaning

as in the MSE definition. and

are the variances of the empirical

distributions of , respectively.

6.

MMD (maximum mean discrepancy) In our numerical examples, we use

the following MMD loss function [35]:

where is the standard radial basis function (or Gaussian kernel)

with multiplier and number of kernels . and

are the values of the ground truth and predicted trajectories at time

, respectively.

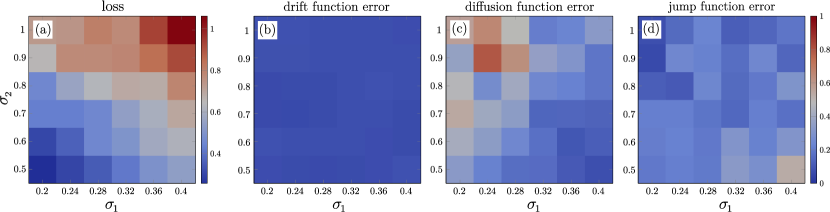

Appendix G Varying the coefficients that determine diffusion and jump functions

Here, we consider changing the two parameters in

Eq. (57) of Example 4.1. With larger

, the trajectories generated by

Eq. (57) will be subject to greater

fluctuations. We use the temporally squared distance as the loss

function. We vary to range from 0.2 to 0.4 and vary

from 0.5 to 1. We repeat our experiments 10 times, and we plot the

temporally squared distance as well as the errors of the

reconstructed .

Figure 4: (a) The temporally decoupled squared Wasserstein distance

. (b) the average relative

errors in the reconstructed drift function ; (c) the

average relative errors in the reconstructed diffusion function

; (d) the average relative errors in the

reconstructed jump functions .

From Fig. 4(a), larger

lead to larger . This could be

because larger lead to ground truth trajectories with

larger fluctuations, rendering the underlying dynamics harder to

reconstruct. Fig. 4(b) implies that

the drift function can be accurately reconstructed and is insensitive

to different . As seen in

Fig. 4(c), if is small, the

relative error in the reconstructed diffusion function can be well

controlled around ; when is larger, it is harder to

reconstruct the diffusion function and the relative error in the

reconstructed diffusion function will be

larger. Fig. 4(d) shows that the

reconstruction of the jump function is not very

sensitive to different values of and .

Appendix H Reconstructing Eq. (59)

in Example 4.2 with different numbers of trajectories in

the training set

Here, we carry out an additional numerical experiment of

reconstructing Eq. (59) by changing the number of

trajectories in the training set. We define the ground truth

jump-diffusion process by the drift function , and the diffusion function and jump functions . We consider four scenarios: i)

provide no prior information and reconstruct drift, diffusion, and

jump functions, ii) provide the drift function as

prior information and reconstruct the diffusion and jump functions,

iii) provide the diffusion function as prior

information and reconstruct the drift and jump functions, and iv)

provide the jump function as prior information and

reconstruct the drift and diffusion functions.

Figure 5: The reconstruction errors in the drift, diffusion, and

jump functions defined in Eqs. 54 and

55 as a function of the number of trajectories

when different prior information is provided. The results

are averaged over 5 independent experiments. Training

hyperparameters are the same as those used in

Example 4.2 listed in Table 3.

As seen in Figs. 5(b-c), providing the

drift function as prior information greatly boosts the efficiency of

our temporally decoupled squared method allowing it to

accurately reconstructing the unknown diffusion and jump functions

even with as few as 100 trajectories for training. Also, even with no

prior information, the errors in the reconstructed drift, diffusion,

or jump function decrease when the number of trajectories in the

training set increases (Figs. 5(a-c)). This

indicates that even without prior information, our temporally

decoupled squared method can accurately reconstruct

Eq. (59) when provided a sufficient number of training

trajectories.

When the diffusion or jump function is given as prior information, the

errors of the reconstructed unknown functions do not decrease much as

the number of trajectories for training increases. Even with the

correct diffusion or jump function, different realizations of the

Brownian motion or the compensated Poisson process yield very different

trajectories so that providing the diffusion or jump function may

provide little information in discriminating trajectories.

Appendix I Reconstructing Eq. (59)

in Example 4.2 with different parameters in the diffusion

and jump functions when providing the drift function

Here, given the drift function , we carry

out an additional numerical experiment of reconstructing

Eq. (59) by varying the parameters

that determine the strength of the Brownian-type and

compensated-Poisson-type noise in Eqs. (60),

(61), and (62).

Figure 6: The reconstruction errors in the diffusion, and jump

functions defined in Eqs. 54 and

55 w.r.t. the two parameters that determine the

strength of noise and in

Eqs. (60), (61), and

(62). Here, const-const indicates we are using

Eq. (60) for both the diffusion and jump functions;

linear-linear indicates we are using Eq. (61) for both

the diffusion and jump functions; langevin-langevin indicates we

are using Eq. (62) for both the diffusion and jump

functions. The results are averaged over 5 independent

experiments. Training hyperparameters are the same as

Example 4.2 in Table 3.

Fig. 6 shows our temporally decoupled

squared -distance loss function can be used to accurately

reconstruct the diffusion function and the jump function in Eq. (59), even when different

forms of in Eqs. (60),

(61), and (62) and different noise strengths

are given. The average errors (averaged over all

choices of ) in the reconstructed diffusion function

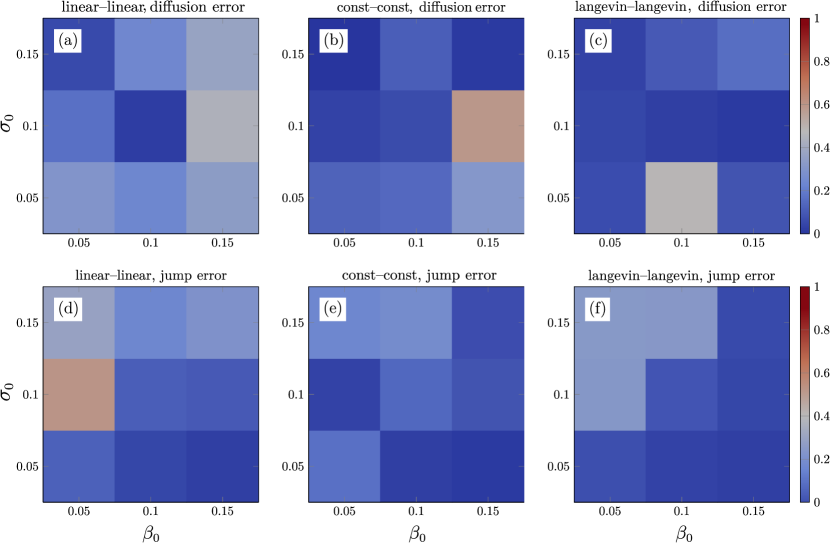

are 0.171 (const-const), 0.217 (linear-linear), and

0.176 (langevin-langevin). The average errors (averaged over all

choices of ) in the reconstructed jump function

are 0.173 (const-const), 0.188 (linear-linear), and

0.184 (langevin-langevin).

Appendix J Neural Network Architecture

Here, we investigate how the neural network architecture,

i.e., the number of hidden layers and the number of neurons

in each layer, influence the accuracy of reconstructing the 2D

jump-diffusion process (Eq. (63)). We vary only the

number of hidden layers and the number of neurons per layer for the

parameterized neural networks that we use to approximate the diffusion

and jump functions and in

Eq. (63). We set the parameters to be and in Eqs. (65)

and (66), and consider 200 trajectories.

Table 4: Reconstructing the jump-diffusion process

Eq. (63) when using neural networks with different

numbers of hidden layers and neurons per layer to parameterize

. Other training hyperparameters are the

same as those used in Table 3 of

Example 4.3.

Width

Layer

Relative Errors in

Relative

Errors in

25

3

5

50

3

5

100

3

5

200

3

5

400

3

5

200

1

5

200

2

5

200

4

5

From Table 4, we see that increasing the number of

hidden layers and increasing the number of neurons per hidden layer

can both increase the accuracy of the reconstructed

and . However, with a fixed

number of neurons per hidden layer (200), when the number of hidden

layers in the feed-forward neural network is greater than 3, the

errors in the reconstructed and

increase. This behavior may be due to vanishing gradients during

training of deep neural networks [36]; in

this case, the ResNet technique [37] can be considered if

deep neural networks are used. On the other hand, using a deeper or

wider network requires more memory usage and longer run times. For

reconstructing Eq. (63), we find an optimal neural

network architecture consisting of about three hidden layers

containing neurons each. How optimal architectures evolve

when reconstructing different multidimensional jump-diffusion

processes requires further exploration.