Quantum Computing for Option Portfolio Analysis

Abstract

In this paper, we introduce an efficient and end-to-end quantum algorithm tailored for computing the Value-at-Risk (VaR) and conditional Value-at-Risk (CVar) for a portfolio of European options. Our focus is on leveraging quantum computation to overcome the challenges posed by high dimensionality in VaR and CVaR estimation. While our innovative quantum algorithm is designed primarily for estimating portfolio VaR and CVaR for European options, we also investigate the feasibility of applying a similar quantum approach to price American options. Our analysis reveals a quantum ’no-go’ theorem within the current algorithm, highlighting its limitation in pricing American options. Our results indicate the necessity of investigating alternative strategies to resolve the complementarity challenge in pricing American options in future research.

I Introduction

Financial institutions such as banks and insurance companies often manage extensive portfolios of financial derivatives that require regular risk assessment. The Basel Accords have embraced a measure of market tail risk in global banking regulation, including using traditional Value-at-Risk (VaR) and Conditional Value-at-Risk (CVaR). For a given time horizon , where could be a day, a week or longer from now and before the expiry of any option in the portfolio, VaR is the maximum potential loss within a specified confidence level (e.g. 95%), and CVaR represents the expected value of losses that exceed the VaR threshold. Regularly calculating such risk values is crucial and often required by regulatory bodies and institutional risk management. As an example, an insurance company needs to compute VaR/CVaR of a large portfolio of hundreds of thousands of (potentially very complex) option contracts, as discussed in [1, 2, 3, 4]. Estimating the risk of a large portfolio of options is a computationally challenging task faced by financial institutions and insurance companies, because computing VaR and CVaR for a large portfolio of complex options is a computationally intensive task in classical computing.

The aforementioned challenge can be appreciated by considering the following. Computing VaR of a portfolio of financial options requires calculating the time value of each option for each possible underlying price realization at . Following classical no-arbitrage option pricing theory, the fair value of an option is derived from the value of the underlying asset and contract specification parameters, such as strikes and time to maturity. At any given future time , the fair value of the option is some nonlinear function of the underlying price and time . Since the underlying price follows a stochastic process, it exhibits a behavior characterized by random fluctuations over time. Consequently, the distribution of the value of a portfolio of options is determined by distributions of option values in the portfolio, which are given by distributions of underlying assets and corresponding option value functions. Calculating VaR/CVaR of a portfolio of options at a future time horizon requires the availability of joint distributions of all underlying assets and all option value functions. In general, VaR analysis consists of two significant components: (1) simulation of the time price joint distributions of all underlying assets of options in the portfolio and (2) computation of fair option values for all underlying asset price realizations at time .

For simplicity, in this paper, we assume that the underlying of an option is a single asset but underlying asset prices across different options can be correlated. In order to generate accurate option values, it is well known that a constant volatility Black-Scholes (BS) model is inadequate [5], as evidenced by the implied volatility smile [6, 7, 8, 9]. The local volatility function model is one of the simplest generalizations of the BS model, which has been widely studied in the literature, e.g., [9, 10, 11], in addition to being frequently adopted in industry practice. More sophisticated models used in option pricing include generalizations of the diffusion BS model augmented with stochastic jumps [12], stochastic volatility [13], and more recently, rough volatility [14]. The fair value of the option is generally characterized by the unique solution to a partial differential equation, which can suffer the curse of dimensionality and becomes computationally infeasible on a classical computer when when there are more than assets.

Recent advances in quantum computational processors have demonstrated significant quantum computational advantages in problems such as random quantum state sampling [15, 16, 17] and density matrix/quantum channel property learning [18, 19]. Given the significance of these outcomes, quantum computers are expected to be capable of accelerating finance models, such as option value modelling [20, 21, 22, 23], portfolio management [24, 25, 26, 27] and forecasting anomaly detection recommendations [28, 29, 30]. In the context of option value modelling, efficient quantum algorithms have been proposed for solving European options and Asian options [20, 21, 22], which approximately transform the differential equation into a system of linear equations on discretized grid points. Although under various assumptions on the conditioning of the linear systems and data-access model, the quantum linear system can be solved with an exponential reduction in the dependence on the dimension [31], a sampling cost needs to be paid to read out the solution from the quantum state, making this technique lose its original quantum advantage. As a result, a rigorous quantum advantage is still unclear for pricing risk modelling problems.

In this paper, we investigate the power of quantum computation in computing the VaR and CVaR for option portfolios. Specifically, when the fair option value function is determined by a PDE method for European options, we design an efficient quantum approach to estimate the VaR/CVaR value, where the involved fundamental steps are provided in Sec. III. The proposed quantum algorithm requires a -depth quantum circuit, where represents the additive error to VaR/CVaR estimation and represents the error induced by the discretization approach. Although the computation of VaR/CVaR value requires the joint distribution of all underlying assets and option value functions, the proposed quantum algorithm does not require expensive classical post-processing (large sampling cost to read out the solution) and thus maintains the potential quantum speed-up. The main goal of this paper is to present a quantum implementation for a hybrid PDE-MC approach to compute VaR/CVaR of a large portfolio of options, e.g., we are interested in computing, e.g., 5% VaR/CVaR at time .

II Theoretical Background

II.1 Black Scholes Model

To illustrate option pricing on a single underlying asset, we assume a generalized Black Scholes local volatility function model for an underlying asset price evolution,

| (1) |

where represents a standard Brownian motion, a drift, and a local volatility function. This stochastic differential equation (SDE) does not have a closed-form solution in general, and consequently there can be no analytic formula for the distribution function for at a given . In addition, prices of the underlying assets of the options in the portfolio are typically correlated, with a given correlation matrix (or its Cholesky factorization) for the corresponding Brownian motions. Without loss of generality, in this paper, we demonstrate here quantum VaR/CVaR calculation assuming the constant elasticity volatility model [32], , where is a positive constant.

II.2 PDE Approach to Compute Fair Option Value

Assume that is the risk-free interest rate. For an option with expiry , the fair option value function is the unique solution to the partial differential equation:

| (2) |

which is an expression of the no-arbitrage assumption and the existence of a hedged portfolio under continuous rebalancing. The expected rate of return of the underlying does not appear in BS PDE. Hence the no-arbitrage value of the option does not depend on . It can be shown that, for an European option with an expiry , under reasonable conditions, the fair value function has the form,

| (3) |

where is the conditional expectation, conditional on time and underlying price , i.e., assuming now satisfies

| (4) |

where is a standard Brownian motion, and is the risk free interest rate. Under a general model (1), this conditional expectation may not have an explicit formula but can be estimated using Monte-Carlo (MC) simulations. Note that the above BS PDE can be readily generalized to accommodate multi-assets.

The fair value of the American option is the solution to the following partial differential equation complementarity problem:

| (5) |

There are two main approaches for computing fair option values, either PDE or MC, with the PDE offering more accurate values in general. It is well known that the PDE approach can suffer the curse of dimensionality and becomes computationally infeasible on a classical computer as the dimensionality of the pricing problem becomes greater than . Monte Carlo simulation is an alternative approach for computing fair option value, where the underlying price is under the risk-neutral dynamics shown in Eq. (4). However, using the Monte Carlo pricing method, computing VaR of a portfolio of options requires nested Monte Carlo simulations, which is also computationally expensive on classical computers. In addition, accurately computing the option value using MC faces more challenges for American options in comparison to European options.

III Outline of the Quantum Approach

While an option can have multiple assets as the underlying and typically simulations of joint distribution of all underlying prices are required, to highlight quantum implementation of option pricing, VaR calculation, and Monte Carlo simulation, here we consider the underlying of each option to be a single asset, which is shared by all options in the portfolio.

For each option in the portfolio, option values on a finite grid can be computed by a finite difference PDE method. Recall that, for simplicity, here we have assumed that each option is written on a single asset. Assume a uniform discretization with timestep along the time axis and a non-uniform discretization along the asset axis is provided. Let denote option values on the grid, where and . Given a target time horizon , the proposed computation follows the following steps:

-

•

Step 1 (to be implemented in Section IV): Option values are computed on the discretization grid described above by a PDE approach. This step generates the quantum state

(6) where represents the fair option value on the point .

-

•

Step 2 (to be implemented in Section V): Stock price at time are computed by Monte Carlo simulations in quantum parallel. Each Monte Carlo trajectory is shaped by a distinct sequence of pseudo-random numbers. This step prepares the quantum state , where the register contains ancillary qubits such that with .

-

•

Step 3 (to be implemented in Section VI): A finite sample distribution of option values is obtained by the following mapping

where for some index , and the corresponding option value .

-

•

Step 4 (to be implemented in Section VII): A bisection search on option values provides the VaR of the portfolio at time . Based on the estimated VaR, a quantum amplitude estimation algorithm can be used to obtain the CVaR.

We provide the technical details of the above four steps in the following sections.

IV A Quantum Algorithm for European Option Values

IV.1 Discrete PDE for European Options

For each option in the portfolio, option values on a finite discretization grid can be computed by a finite different PDE method. Recall that, for simplicity, here we have assumed that each option is written on a single asset. For simplicity, assume that volatility function does not depend on time, for example set , and let

where is the risk-free interest rate. Let the vectors

| (7) |

and let be the tridiagonal matrix with entries

| (8) |

when . Let the first row and last row of correspond to boundary conditions. We can write the fully implicit time stepping as

| (9) |

Updating to requires a high-dimensional matrix transformation especially for multi-asset option pricing, posing significant challenges for classical computers.

IV.2 A Quantum algorithm for European Option PDE

Here, we demonstrate how to utilize a quantum computer to prepare the quantum state given in Eq. 6 where represents the target time. According to the update rule (Eq. 9), the vector at can be represented by

| (10) |

where the starting point . Note that the matrix is a -sparse tridiagonal matrix, whose entries are given in Eq. 8, and is thus generally non-Hermitian. Then we need to consider the singular value decomposition of , where represents the rank of , represent singular values of , and are singular vectors of . As a result, the vector can be further expressed in terms of the singular vectors and , that is

| (11) |

Since the function is classically efficiently computable, the initial quantum state

can be efficiently prepared by the Grover-Randolph algorithm [33]. In the following, we demonstrate how to utilize the Quantum Singular Value Transformation (QSVT) [34] to simulate the process on a quantum computer and finally yield the quantum state .

Let , where the norm , then the QSVT method provides a quantum circuit implementation to achieve , where the matrix function . Here, the fundamental idea within the QSVT method relies on two steps:

-

•

Encoding the non-unitary matrix into a higher-dimensional unitary matrix (Encoding Phase);

-

•

Constructing a -degree polynomial approximations to within -additive error. Furthermore, finding phase factors to modulate to achieve which approximates (Modulation Phase).

IV.2.1 Encoding Phase

We introduce the block-encoding technique, where the fundamental idea is to represent a sub-normalized matrix as the upper-left block of a unitary matrix

| (12) |

which is equivalent to .

Definition 1 (Block-Encoding).

Suppose that the matrix is an -qubit operator, and , then we say that the -qubit unitary is an -block-encoding of , if

| (13) |

In our case, is a tridiagonal matrix, and is thus a -sparse matrix. Camps et al. [35] provided an efficient method for constructing a Block-Encoding of sparsity matrices. Consider to be a function that gives the row index of the -th non-zero matrix elements in the -th column of . Suppose there exists a unitary such that , and a unitary such that

| (14) |

then represents a -block-encoding of . This statement can be verified easily. Starting from the quantum state , we have

| (15) |

Finally, we utilize to post-process the above quantum state, hence the inner product

which implies is a -block-encoding of .

IV.2.2 Modulation Phase

A polynomial approximation of is required.

Lemma 1.

Let , and function , then there exist a real polynomial function , such that and . The degree of is at most .

The proof is based on Corollaries 66 in Ref [34].

Lemma 2 (Ref [34]).

Let , and let and for all . Suppose that . Let , then there is an efficiently computable polynomial of degree such that .

Proof of Lemma 1.

Denote . For all , the generalized binomial theorem yields , where . Let and . Furthermore, we have and

| (16) |

As a result, the upper bound of is , and the polynomial approximation has degree . ∎

Fact 1 (QSVT).

Suppose the matrix is encoded by a -block-encoding unitary . Given the polynomial function described in Lemma 1, there exists a set of phase factors such that

| (17) |

and is a -block-encoding unitary of , where and the projector .

Noting that the phase factors can be efficiently calculated by using the QSPPACK. The above result directly yields

| (18) |

where the query complexity of is at most .

V A Quantum Circuit for Monte Carlo Stock Price Simulation in Quantum Parallel

Underlying price dynamics can be modelled according to a generalized Black-Scholes framework given by Eq.(1), which includes stochastic volatility using a local volatility function. This enhanced model demonstrates improved capability in matching traded option market prices, i.e. generating a volatility smile, which is widely recognized and documented in the equity options markets [6, 7, 8, 9]. The local volatility function allows volatility to vary with time and future random stock price realization, potentially leading to a more accurate depiction of price uncertainty. This enhanced model provides a sophisticated tool for analyzing and predicting stock price behaviour, recognizing the dynamic and variable nature of volatility in financial markets. Applying Euler’s method to (1), we have

| (19) |

where is the change in a standard Brownian motion, is a drift, is a local volatility function and the time variable which is different to the backward propagation shown in Sec. IV. Let , , represent the estimation of within additive error and the number of ancillary qubits . In the following, we demonstrate how to utilize a quantum computer to prepare in parallel.

The quantum algorithm starts from the initial state

| (20) |

where the first register contains qubits while the second register has qubits. Then can be efficiently prepared by -Hadamard gates and Pauli-X gates, since the composite system and are in a tensor product state. To simulate the random variable in the quantum circuit, we assign which naturally simulates the logistic chaos variable. Let the function and define the quantum gate

| (21) |

This enables us to achieve

| (22) |

Note that the inverse function of exists, that is , where and . This thus enables the map

| (23) |

Using quantum control gates - and - iteratively, the initial state may evolves to

| (24) |

after steps. The elaborate quantum circuit is shown in Fig. 2.

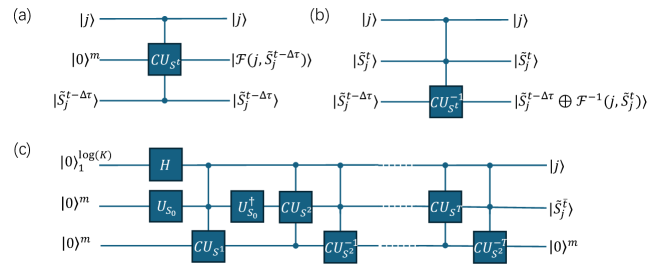

VI A Quantum Algorithm for Distribution of Value of Portfolio

Given several copies of the input quantum state , we demonstrate how to achieve the map

| (25) |

where represents the stock price at time .

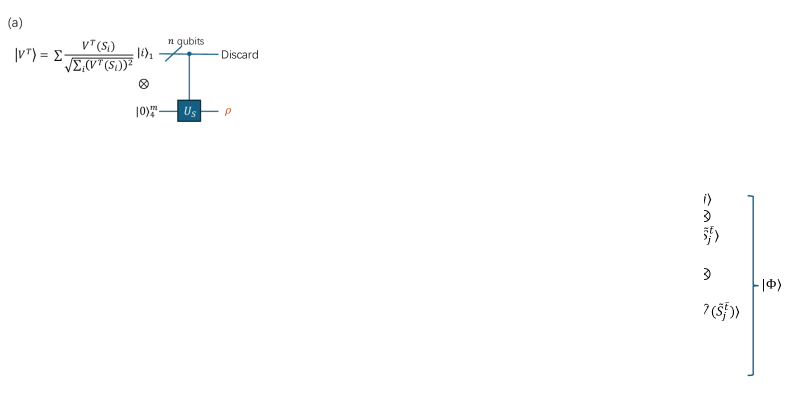

The fundamental idea is based on Quantum Principle Component Analysis (QPCA) [36, 37] and Quantum Phase Estimation (QPE) [38]. Suppose we have prepared the quantum state , then added ancillary qubits to store the grid information in the ancillary register

| (26) |

Discarding subsystem , the quantum system naturally becomes the density matrix

| (27) |

We can now utilize the QPCA method [36] to simulate and extract the spectrum information of by using the QPE algorithm [38]. To achieve the estimation , where the estimated value satisfies

we need the time parameter .

Starting from the quantum state , the QPCA algorithm can help us estimate the spectrum information of from the ancillary qubits. For any -qubit density matrix , we have , where represents the -qubit swap operator. As a result, we can perform the quantum operation

| (28) |

on systems , then perform the inverse Quantum Fourier Transformation and square-root function to prepare the quantum state

| (29) |

To provide an estimation of within an acceptable accuracy, we need the evolution time . The whole process is visualized as Fig. 3.

VII A Quantum Algorithm for VaR/CVaR estimation

VII.1 VaR Estimation

Here, we try to find the smallest value such that . To find on a quantum computer, we utilize the bisection search method over [24]. The bisection search approach depends on the unitary that achieves the map

where if , otherwise . Applying to the quantum state produces

| (30) |

The probability of measuring for the last qubit is . Therefore, with a bisection search over , we may efficiently find the smallest such that in at most steps, where represents the number of qubits in representing given in the second register. Using the quantum mean value estimation [39], we may estimate a -approximation to within queries to (as defined by Eq. 29).

VII.2 CVaR Estimation

Suppose we have estimated the VaR value such that . Then we can divide all given in Eq. 29 into two sets: and . As a result, CVaR could be estimated by

| (31) |

where represents the number of entries in .

The quantum algorithm in predicting CVaR can be summarized as follows.

-

•

After estimating the VaR of , we append ancillary qubits to (as defined by Eq. 29), and perform the unitary to achieve

(32) -

•

Undo the QFT and QPCA process (as demonstrated in Sec. VI), the quantum state becomes

(33) -

•

Now trace over the 2nd and 3rd registers, we have , where

(34) As a result, we can utilize the swap-test combined with quantum phase estimation to provide an -approximation to

(35) where the quantum state is given in Eq. 26, and . The above quantum state overlap can be efficiently estimated by utilizing a -depth quantum circuit, where represents the quantum circuit complexity in preparing and .

-

•

Recall that the selection of VaR enabling , as a result, CVaR can be predicted by

(36)

VIII Complexity Analysis

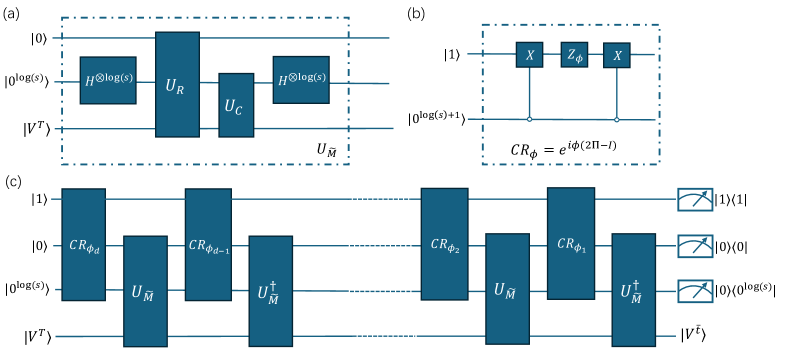

Here, we summarize all involved complexity in Steps 1-4 as demonstrated above. In step 1, the QSVT framework is used to prepare the quantum state . As shown in Fig. 1 (a), a constant-depth quantum circuit suffices to provide a -block-encoding of the -sparse matrix , given oracles and . Using and the QSVT technique, a -block-encoding to can be constructed, where the involved quantum circuit depth is upper bounded by . The error represents the upper bound on . Noting that we essentially utilize the discretisation method to approximate the exact option value function , as a result, -length time slice may introduce additive error. Then the corresponding quantum circuit depth can be approximated by .

In step 2, a quantum circuit implementation of “classical MC” is implemented, which is independent of the result given in step 1. Here, a -depth quantum circuit is designed to prepare the quantum state . Each layer utilizes quantum control gates to compute functions and , whose quantum gate complexity can be estimated by by using the Fourier-Transformation-based method [40], where represents the number of stock prices and represents the additive error in approximating functions and .

Step 3 utilized the QPCA and QPE methods to combine option values (given by ) with the stock prices state . To simulate , where the density matrix is provided by Eq. 27, we first divide the evolution time into time-slice , then utilize to approximate with additive error. Therefore, the total error in simulating can be approximated by , resulting in the sample complexity . Furthermore, to encode the spectrum information of into the quantum state , the QPE algorithm is required by utilizing the operator, as shown in Eq. 28. To provide an estimation within error, the evolution time (in Eq. 28) should satisfy . As a result, the sample complexity on in performing quantum phase estimation meanwhile generating is

| (37) |

The number of qubits is upper bounded by .

However, step 1 does not output the exact without any error. Actually, it outputs an -approximation to . Without loss of generality, we assume step 3 essentially performs QPCA on

| (38) |

where represents the error component. It is easy to verify that . Performing the gird computation gate (as shown in Eq. 26), the quantum system occupies

| (39) |

Let the error component , we have

| (40) |

where . This naturally results in

| (41) |

The demonstrated norm difference upper bound implies all eigenvalues of can be approximated by that of with at most additive error. Combining this error analysis with the sample complexity given in Eq. 37, let and , then repeat step 1 times. This suffices to prepare an -approximation to .

Finally, step 4 utilized the binary search program and mean value estimation algorithm, where each iteration step requires copies of to estimate VaR and CVaR. Combining all steps together, the quantum circuit depth can be approximated by

| (42) |

We summarize the required quantum computational resources for each step in Table 1.

| Alg. Steps | Assumption | Circuit Depth | Post-Selection | Sample Complexity |

| Step 1 | Efficient access to | |||

| Step 2 | — | — | ||

| Step 3 | — | — | -copies of (Eq. 6) | |

| Step 4 | — | — |

IX American Option Values

For American option pricing, finite difference approximation of the partial differential equation complementarity problem (5) leads to a linear complementarity problem. While more sophisticated iterative methods, e.g., penalty method [41] and Newton method [42] can be applied to compute the solution of this linear complementarity problem, here we attempt to implement a rudimentary method that explicitly handles the inequality payoff constraint, as described in Alg. 1. Note that, if explicit finite difference approximation is used, this simple scheme does solve the resulting linear complementarity finite difference approximation of Eq. 5.

As shown in Alg. 1, the option value is updated by two steps: (i) solving a linear system and (2) taking the higher value of and . Now encode the option values in the amplitudes in the same way as the European option values given in Eq. 6, and the representative quantum state is then . Given an efficient oracle to access entries within the matrix , there are several efficient quantum algorithms for preparing the quantum state . However, we argue that achieving the comparison between and is quantum hard.

Definition 2 (Amplitude Maximum (AM) Problem).

Given copies of valid quantum states and with qubits, where , prepare the quantum state

| (43) |

by using a quantum computer.

In what follows, we demonstrate the difficulty of solving the American option problem using the above proposed algorithm with quantum computers. In other words, the method described above would necessitate the same operations as classical computing, i.e. without any quantum advantage.

Theorem 1.

Given copies of valid quantum states and with qubits and real amplitudes , any quantum algorithm that generates (as shown in Eq. 43) will require samples.

Proof.

We first consider the sample complexity of a quantum state classification problem: how many samples suffice to distinguish quantum states and , where . It is known that quantum states and are distinguishable if [43]. Now suppose we have copies of and , then

| (44) |

may directly result in , equivalently .

Now suppose there exists a quantum algorithm that can solve the AM problem with copies of and , that is . Let the testing quantum state , and consider a classification program

| (45) |

This leads to

-

•

-

•

which imply and could be distinguished by a quantum algorithm with copies and constant number of computational basis measurements. This results in a contradiction. ∎

X Conclusion

In finance, even modest improvements in computational speed and model performance can have a substantial effect on the profitability of a business. For instance, fast and accurate evaluation of the risk metrics in derivatives trading is crucial in effectively hedging the risks especially under volatile market conditions.

This paper introduces an efficient end-to-end quantum algorithm for predicting the VaR/CVaR of a portfolio of European options. Specifically, given the backward propagation time target and accuracy , our quantum algorithm takes market sensitive parameters as inputs and generates a -approximate VaR/CVaR by running a quantum algorithm with time complexity, where represents the error induced by the discretization approach. The essential quantum speed-up relies on matching the stock price to its corresponding option value , where the option value function lives in a high-dimensional space induced by discretization. In general, classical approaches would require transverse all option values in the look-up table, however, QPCA and QPE provide an efficient approach to project all concerned option value functions to the concerned stock prices.

This work opens new avenues for further research. For instance, we have only considered the single stock option pricing in this paper to demonstrate potential quantum advantages of the proposed algorithm. Multi-stock scenarios naturally induce a high-dimensional fair option value PDE. The curse of dimensionality and the complex correlations between different stocks within this PDE pose formidable challenges to classical algorithms. Therefore, extending this quantum algorithm to multiple underlying stocks is an obvious next step. Furthermore, analyzing whether different discretization strategies for the American option PDE can bypass the established ’no-go’ theorem is a topic deserving further investigation.

References

- [1] M. Broadie, Y. Du, and CC Moallemi. Efficient risk estimation via nested sequential simulation. Management Science, 57(6):1172–1194, 2011.

- [2] Guojun Gan and X. Sheldon Lin. Valuation of large variable annuity portfolios under nested simulation: A functional data approach. Insurance: Mathematics and Economics, 62:138–150, 2015.

- [3] Guojun Gan and E. A. Valdez. Valuation of large variable annuity portfolios with rank order kriging. North American Acturial Journal, 24(1):100–117, 2020.

- [4] Lucio Fernandez-Arjona and Damir Filipović. A machine learning approach to portfolio pricing and risk management for high-dimensional problems. Mathematical Finance, 32(4):982–1019, 2022.

- [5] JC Hull. Options, futures, and other derivatives securities. eight ed, 2012.

- [6] B. Dupire. Pricing with a smile. Risk, 7(2):229–263, 1994.

- [7] E. Derman and I. Kani. Riding on a smile. Risk, 7(2):32–39, 1994.

- [8] B. Dumas, J. Fleming, and R. E. Whaley. Implied volatility functions: Empirical tests. Journal of Finance, 53(6):2059–2106, 1998.

- [9] Thomas F. Coleman, Yuying Li, and Arun Verma. Reconstructing the unknown local volatility function. The Journal of Computational Finance, 2(3):77–102, 1999.

- [10] L. Andersen and J. Andreasen. Jump-diffusion processes: Volatility smile fitting and numerical methods for option pricing. Review of Derivative Research, 4:231–262, 2000.

- [11] C. He, J.S. Kennedy, T.F. Coleman, P.A. Forsyth, Y. Li, and K.R. Vetzal. Calibration and hedging under jump diffusion. Review of Derivative Research, 9:1–35, 2006.

- [12] R. Merton. Option pricing when underlying stock returns are discontinuous. Journal of Financial Economics, 3:124–144, 1976.

- [13] S.L. Heston. A closed-form solution for options with stochastic volatility with applications to bond and currency options. Review of Financial Studies, 6:327–343, 1993.

- [14] J. Gatheral, T. Jaisson, and M. Rosenbaum. Volatility is rough. Quantitative Finance, 18:933–949, 2018.

- [15] Sergio Boixo, Sergei V Isakov, Vadim N Smelyanskiy, Ryan Babbush, Nan Ding, Zhang Jiang, Michael J Bremner, John M Martinis, and Hartmut Neven. Characterizing quantum supremacy in near-term devices. Nature Physics, 14(6):595–600, 2018.

- [16] Frank Arute, Kunal Arya, Ryan Babbush, Dave Bacon, Joseph C Bardin, Rami Barends, Rupak Biswas, Sergio Boixo, Fernando GSL Brandao, David A Buell, et al. Quantum supremacy using a programmable superconducting processor. Nature, 574(7779):505–510, 2019.

- [17] Han-Sen Zhong, Hui Wang, Yu-Hao Deng, Ming-Cheng Chen, Li-Chao Peng, Yi-Han Luo, Jian Qin, Dian Wu, Xing Ding, Yi Hu, et al. Quantum computational advantage using photons. Science, 370(6523):1460–1463, 2020.

- [18] Hsin-Yuan Huang, Michael Broughton, Jordan Cotler, Sitan Chen, Jerry Li, Masoud Mohseni, Hartmut Neven, Ryan Babbush, Richard Kueng, John Preskill, et al. Quantum advantage in learning from experiments. Science, 376(6598):1182–1186, 2022.

- [19] Yusen Wu, Bujiao Wu, Jingbo Wang, and Xiao Yuan. Quantum phase recognition via quantum kernel methods. Quantum, 7:981, 2023.

- [20] Koichi Miyamoto and Kenji Kubo. Pricing multi-asset derivatives by finite-difference method on a quantum computer. IEEE Transactions on Quantum Engineering, 3:1–25, 2021.

- [21] Patrick Rebentrost, Brajesh Gupt, and Thomas R Bromley. Quantum computational finance: Monte carlo pricing of financial derivatives. Physical Review A, 98(2):022321, 2018.

- [22] Javier Gonzalez-Conde, A Rodrĺguez-Rozas, Enrique Solano, and Mikel Sanz. Pricing financial derivatives with exponential quantum speedup. methods, 2:6, 2021.

- [23] Nikitas Stamatopoulos, Daniel J Egger, Yue Sun, Christa Zoufal, Raban Iten, Ning Shen, and Stefan Woerner. Option pricing using quantum computers. Quantum, 4:291, 2020.

- [24] Stefan Woerner and Daniel J Egger. Quantum risk analysis. npj Quantum Information, 5(1):15, 2019.

- [25] Iordanis Kerenidis and Anupam Prakash. A quantum interior point method for lps and sdps. ACM Transactions on Quantum Computing, 1(1):1–32, 2020.

- [26] Dengke Qu, Edric Matwiejew, Kunkun Wang, Jingbo B Wang, and Peng Xue. Experimental implementation of quantum-walk-based portfolio optimisation. Quantum Science and Technology, 2024.

- [27] Nicholas Slate, Edric Matwiejew, Samuel Marsh, and Jingbo B Wang. Quantum walk-based portfolio optimisation. Quantum, 5:513, 2021.

- [28] Guang Hao Low, Theodore J Yoder, and Isaac L Chuang. Quantum inference on bayesian networks. Physical Review A, 89(6):062315, 2014.

- [29] Sima E Borujeni, Saideep Nannapaneni, Nam H Nguyen, Elizabeth C Behrman, and James E Steck. Quantum circuit representation of bayesian networks. Expert Systems with Applications, 176:114768, 2021.

- [30] Catarina Moreira and Andreas Wichert. Quantum-like bayesian networks for modeling decision making. Frontiers in psychology, 7:163811, 2016.

- [31] Aram W Harrow, Avinatan Hassidim, and Seth Lloyd. Quantum algorithm for linear systems of equations. Physical review letters, 103(15):150502, 2009.

- [32] J. Cox. Notes on option pricing i: Constant elasticity of diffusion. Stanford University, page 023302, 1975.

- [33] Lov Grover and Terry Rudolph. Creating superpositions that correspond to efficiently integrable probability distributions. arXiv preprint quant-ph/0208112, 2002.

- [34] András Gilyén, Yuan Su, Guang Hao Low, and Nathan Wiebe. Quantum singular value transformation and beyond: exponential improvements for quantum matrix arithmetics. In Proceedings of the 51st Annual ACM SIGACT Symposium on Theory of Computing, pages 193–204, 2019.

- [35] Daan Camps, Lin Lin, Roel Van Beeumen, and Chao Yang. Explicit quantum circuits for block encodings of certain sparse matrices. arXiv preprint arXiv:2203.10236, 2022.

- [36] Seth Lloyd, Masoud Mohseni, and Patrick Rebentrost. Quantum principal component analysis. Nature Physics, 10(9):631–633, 2014.

- [37] Chao-Hua Yu, Fei Gao, Song Lin, and Jingbo Wang. Quantum data compression by principal component analysis. Quantum Information Processing, 18(8):249, 2019.

- [38] Michael A Nielsen and Isaac Chuang. Quantum computation and quantum information, 2002.

- [39] Ashley Montanaro. Quantum speedup of monte carlo methods. Proceedings of the Royal Society A: Mathematical, Physical and Engineering Sciences, 471(2181):20150301, 2015.

- [40] SS Zhou, Thomas Loke, Josh A Izaac, and JB Wang. Quantum fourier transform in computational basis. Quantum Information Processing, 16(3):82, 2017.

- [41] P. Forsyth and K. Vetzal. Quadratic convergence for a penalty method for American options. SIAM J. Sci. Comp., 23, 2002.

- [42] Thomas F. Coleman, Yuying Li, and Arun Verma. A Newton method for american option pricing. The Journal of Computational Finance, 5(3):51–78, 2002.

- [43] Jordan Cotler, Hsin-Yuan Huang, and Jarrod R McClean. Revisiting dequantization and quantum advantage in learning tasks. arXiv preprint arXiv:2112.00811, 2021.

Acknowledgements

The authors wish to express gratitude to Peter Forsyth, Song Wang, Robert Scriba, Tavis Bennett, Sisi Zhou, Des Hill for valuable discussions. Y. Wu is supported by the China Scholarship Council (Grant No. 202006470011) and UWA-CSC HDR Top-Up Scholarship (Grant No. 230808000954).