Concentration Bounds for Optimized Certainty Equivalent Risk Estimation

Abstract

We consider the problem of estimating the Optimized Certainty Equivalent (OCE) risk from independent and identically distributed (i.i.d.) samples. For the classic sample average approximation (SAA) of OCE, we derive mean-squared error as well as concentration bounds (assuming sub-Gaussianity). Further, we analyze an efficient stochastic approximation-based OCE estimator, and derive finite sample bounds for the same. To show the applicability of our bounds, we consider a risk-aware bandit problem, with OCE as the risk. For this problem, we derive bound on the probability of mis-identification. Finally, we conduct numerical experiments to validate the theoretical findings.

1 Introduction

A major consideration in financial and clinical applications is the quantification of the risk associated with future random outcomes. In the pioneering framework of Markovitz, the variance of the underlying random variable is considered as a measure of risk, and the objective is to maximize the expected value subject to a constraint on the risk, or to maximize an affine function of the mean and variance [16]. Subsequently, another landmark paper [1] proposed an axiomatic approach to risk, by imposing four properties to be satisfied by the risk measure.

Specifically, for a r.v. and a real valued function , [1] imposes the properties of being positively homogeneous, sub-additive, translation invariant and monotone for a risk measure . A risk measure that satisfies all these properties is called a coherent risk measure. In [9], the authors relaxed the conditions of sub-additivity and positive homogeneity, and replaced them with a weaker property of convexity, i.e.,

| (1) |

and such a risk measure is said to be convex.

Optimized Certainty Equivalent (OCE) is a family of convex risk measures, introduced in [4] and explored further in [3]. Qualitatively, OCE is a class of risk measures which serves as an indicator of the investor’s risk appetite, particularly capturing the optimal allocation of resources/losses between the present and the future. Suppose the total loss that an investor could incur in the future is a random variable . The investor has the option to allocate a fraction of their uncertain losses, denoted by , to the present. Consequently the present value of losses under a disutility function then becomes . The optimal i.e. the infimum over all possible allocations then gives us the OCE risk of the investor. We shall denote this optimal by in this paper.

Under suitable choices of the disutility function , OCE risk encompasses a wide range of risk measures, one of which is the widely used risk measure Conditional Value at Risk (CVaR)[24]. Given a random variable and a level , define the VaR as . Then the CVaR . It can be shown that this is just a special case of OCE risk measure with the disutility function , and replaced with .

Our contributions.

In this paper, we consider the problem of estimating the OCE risk from independent and identically distributed (i.i.d.) samples of the loss distribution. First, we consider a straightforward Sample Average Estimator for the OCE risk, and bound its mean-squared error. Next, we derive a concentration bound for the SAA estimator when the underlying loss distribution is sub-Gaussian, and the disutility function is strongly convex and smooth. This OCE risk concentration bound enjoys a sub-exponential decay. We illustrate the applicability of our concentration bound in a multi-armed bandit setting with a ‘Best-OCE-arm’ identification problem.

Next, we consider a ‘streaming’ setting wherein the samples from the underlying loss distribution are available one-at-a-time. For this scenario, the sample average estimator is ineffective, because it requires recomputation for each sample. On the other hand, an iterative estimator that updates one step at a time upon receiving each fresh sample is better suited for such a streaming setting. We propose a stochastic approximation-based estimation procedure for OCE risk estimation. We then derive finite-sample bounds for the mean-squared error of the iterative OCE risk estimation procedure.

Related work.

In recent years, estimation of risk measures from i.i.d. samples has received a lot of research attention, cf. [13, 19, 25, 7, 5, 21, 20, 28, 6, 17, 15]. The majority of prior works consider CVaR estimation and derive concentration bounds usually under a sub-Gaussianity assumption.

For OCE risk estimation, bounds are available in [6, 14]. The former reference considers distributions with bounded support, while the latter includes sub-Gaussian and sub-exponential distributions. In [11], the authors study a stochastic approximation-based procedure for OCE risk estimation. In comparison to these closely related works, we remark the following: (i) Unlike [6], our OCE risk estimation bounds are for unbounded albeit sub-Gaussian distributions; (ii) In [14], the authors employ a Wasserstein distance based approach for deriving OCE risk concentration bounds for Lipschitz disutility functions. Our present work allows for smooth disutility functions, which cover mean-variance risk measure as an important special case. Moreover, our proof is direct, while they use a unified approach to handle several risk measures that satisfy a continuity criterion. The flip side with their approach is that the constants in the concentration bounds are conservative. Additionally, we derive a concentration bound for the OCE risk minimizer; (iii) In [11], the authors provide an asymptotic rate result for their OCE risk estimator, while we quantify the rate of convergence through bounds in expectation as well as high probability, in the non-asymptotic regime.

2 OCE Risk Measure

Definition 2.1.

For a random variable (r.v.) , the OCE risk with a disutility function is defined by

| (2) |

We denote the minimizer of OCE risk by .

As mentioned earlier, OCE risk accommodates a wide class of popular risk measures, for suitably chosen disutility fucntion Some common examples for the disutility function and their corresponding OCE risk expressions are given in Table 1.

| Risk measure | Disutility function | OCE risk minimizer | OCE risk |

|---|---|---|---|

| Expected loss | |||

| Entropic risk | |||

| Mean-variance | |||

| Conditional | |||

| Value-at-Risk |

Proposition 2.1.

It can be shown (See [3, Theorem 2.1]) that the OCE risk measure under the conditions of Proposition 2.1 satisfies the following properties, in addition to convexity: (a) Translation invariance: ; (b) Consistency: , for any constant ; and (c) Monotonicity: Let be any random variable such that . Then, .

3 OCE Risk Estimation and Concentration

OCE Risk Estimation.

Let denote i.i.d. samples from the distribution of . Using these samples, we estimate as follows:

| (3) |

We denote the minimizer of (3) by . For example, in the case of CVaR estimation as discussed in [22], is just , with being the order-statistics for .

For the -sample, the empirical distribution function (EDF) is defined by

| (4) |

The OCE risk estimator defined above can be seen as the OCE risk applied to a r.v., say , with distribution , i.e., .

Useful expressions for and .

We differentiate (2) and using the fact that is the OCE risk minimizer, we obtain

| (5) |

where the second equality follows from DCT (see [8, Theorem 4.6.3]) via Assumption A3.

Let be the infimum for . Then, by arguments similar to those leading to (5), we obtain

| (6) |

For deriving the OCE risk estimation bounds, we require assumptions on the tail of the underlying distribution. Two popular tail assumptions are sub-Gaussian and sub-exponential, which are formalized below.

Definition 3.1 (Sub-Gaussian distribution).

A r.v. with mean is sub-Gaussian if there is a positive parameter such that

Definition 3.2 (Sub-exponential distribution).

A r.v. with mean is sub-exponential if there are non negative parameters such that

Bounds for OCE risk estimation.

For deriving mean-squared error (MSE) and concentration bounds for OCE risk estimation, we make the following assumptions.

A1.

The function is -strongly convex.

A2.

The function is -smooth, i.e.,

A3.

The function is continuously differentiable, and the collection of random variables is uniformly integrable.

A4.

The r.v. is sub-Gaussian with parameter .

We now comment on the assumptions made above. Assumption A1 is required for providing MSE/concentration bounds for estimation of OCE risk minimizer . If the function is convex but not strongly convex, then it is difficult to bound , since the function could have a arbitrarily wide plateau around . For the special case of VaR, such an assumption has been made for obtaining concentration bounds in [21]. In this case Assumption A1 translates to a strictly increasing distribution, to ensure a VaR estimate can concentrate as the distribution is not flat around VaR.

In [14], the authors assume the disutility function is Lipschitz for deriving a concentration bound for OCE risk estimation. Such an assumption is restrictive since it disallows a mean-variance risk measure via OCE risk, as in some example above. In contrast, Assumption A2 imposes a smoothness condition on , in turn allowing a risk measure with mean-variance tradeoff.

Assumption A3 is a technical assumption that ensure certain integrals are finite, allowing an application of the dominated convergence theorem to interchange expectation and differentiation operators. For the case of r.v.s with unbounded support, such an assumption has been made earlier in the context of another risk measure, see [10].

An assumption on the tail of the underlying distribution is usually made for deriving concentration bounds, cf. [21] for CVaR. In Assumption A4, we impose a sub-Gaussianity requirement on the underlying distribution.

color=red!20!white,size=,,inline]P: Discuss how L-smoothness is the "breaking point" for sub-exponentiality and how anything beyond it will not hold and MGF integral will diverge.

Bounds for estimation of OCE risk minimizer .

The first result that we present is a mean-squared error bound on the estimator of the OCE risk minimizer .

Theorem 3.1.

Suppose Assumptions A1 to A3 hold. Further, assume has a finite second moment. Then, we have the following bound for , which is the minimizer of the empirical OCE risk defined in (3):

| (7) |

where is the smoothness parameter and is the strong-convexity parameter of the disutility function , and is the OCE risk minimizer.

Proof.

See Appendix A ∎

The mean-squared error bound in the result above is useful in bounding the error in OCE estimation owing to the following relation:

Under an additional sub-Gaussianity assumption, we present below a concentration bound for estimation of OCE risk minimizer .

Theorem 3.2.

Suppose Assumptions A1 to A4 hold. Then we have

| (8) |

where the quantities are as defined in Theorem 3.1, while is the sub-Gaussianity parameter of .

Proof.

See Appendix B. ∎

From the result above, it is apparent that the bound exhibits a Gaussian tail decay.

Bounds for OCE risk estimation.

For our first result which is a mean squared error bound for OCE risk, we require an additional assumption stated below.

A5.

is bounded for and is bounded for .

The moment bounds can be seen to be easily satisfied for a sub-Gaussian/sub-exponential . In the general case, such moment bounds are necessary owing to the fact that the mean-squared error derivation naturally leads to terms involving , and , where and .

The result below bounds the mean-squared error of the OCE risk estimator defined in (3).

Proof.

See Appendix C. ∎

Using Jensen’s inequality, we can infer that

where can be inferred from the result above.

For OCE risk estimates to concentrate, we require a bound on the tail probability . The lemma below establishes that is sub-exponential.

Lemma 3.4.

Suppose is -sub-Gaussian and is closed, convex, L-smooth, non-decreasing and satisfies and . Then the zero-mean r.v. is sub-exponential with parameters , where , and .

Proof.

See Appendix D. ∎

We can now use this result to provide a Bernstein-type concentration bound for the OCE risk estimate in (3).

Theorem 3.5.

Suppose Assumptions A1 to A4 hold. Let , , . Then, for any , we have

| (9) |

Proof.

See Appendix E. ∎

Remark 1.

We can see that the tail bound stated above exhibits an exponential tail decay. Since we assume that the function is strongly convex, a tighter sub-Gaussian decay does not hold. Intuitively, the r.v. underlying OCE risk concentration is bounded below by a quadratic function of , which precludes sub-Gaussian concentration for OCE risk.

Remark 2.

In [14], the authors assume is Lipschitz and employ a Wasserstein distance-based approach to arrive at a bound with a sub-Gaussian tail. In contrast, the bound in Theorem 3.5 exhibits sub-exponential tail decay for a -smooth . From Table 1, it is apparent that our bounds are applicable for the mean-variance risk measure, since the underlying function is smooth.

We can invert the bound in 3.5 to arrive at the following ‘high-confidence’ form:

Corollary 3.5.1.

Under conditions of Theorem 3.5, for any , with probability at least , we have

While the tail bound in (9) is useful for the bandit application under best arm identification framework in Section 5, the equivalent high-confidence form above cannot be employed for a upper confidence bound type algorithm to minimize regret, since require the knowledge of , which is not known in a typical bandit setting.

4 Stochastic approximation for OCE risk estimation

The estimators.

Recall that the OCE risk minimizer satisfies . Using stochastic approximation, we arrive at the following update iteration for obtaining an estimate of the OCE risk minimizer :

| (10) |

where are i.i.d. samples from the distribution and is a suitably chosen step size. Compared to the batch estimator in the previous section, the above update is more amenable to ‘streaming’ settings, where the samples arrive one at a time.

Inspired by [2], we derive bounds for the averaged iterate, and use this quantity to estimate OCE. These quantities, denoted by and are defined as follows:

| (11) |

Results.

For deriving a mean-squared error bound, we require the following assumption in addition to Assumptions A1 to A3 and A5:

A6.

The second derivative is -lipschitz. That is for all , , .

The main result that provides a mean-squared error bound for the averaged iterate after iterations of (10) is given below.

Theorem 4.1.

Suppose Assumptions A1 to A3, A5 and A6 hold. Suppose iterations of (10) are run with stepsize with . Then, the averaged iterate satisfies

| (12) |

where

and is a constant that depends only on and .

The mean-squared error bound from (12) is comparable to the corresponding result for the batch estimator (6) in Theorem 3.1, if we set , i.e., run (10) for -samples and compare it to .

Next, we use the bound in (12) to derive a bound on the mean-squared error for the OCE risk estimate in (11).

Theorem 4.2.

Proof.

See Appendix G. ∎

5 Application: Multi-Armed Bandits

We consider a a -armed stochastic bandit problem, which is characterized by the probability distributions of the arms, denoted as . We focus on identifying the arm exhibiting the lowest OCE risk value within a predetermined sampling budget. Here, a bandit algorithm engages with the environment over a fixed budget comprising rounds. At each round , the algorithm selects an arm and records a cost sample from the distribution . Upon completing the rounds, the bandit algorithm suggests an arm , and is evaluated based on the probability of mis-identifying the optimal arm, denoted as , where represents the arm with the lowest OCE risk value, i.e., .

Algorithm 1 outlines the pseudocode for our OCE-SR algorithm, tailored to identify the OCE-optimal arm under a fixed budget constraint. This algorithm presents a modification of the conventional successive rejects (SR) approach, with a distinction: while regular SR employs sample means to estimate the expected value of each arm, OCE-SR utilizes empirical OCE risk, as described in Equation 3, for estimating the OCE risk of each arm. The elimination strategy, involving phases and discarding the arm with the poorest OCE risk estimate at the conclusion of each phase, is borrowed from the regular SR framework.

The ensuing result delves into the performance analysis of the OCE-SR algorithm for sub-Gaussian distributions.

Theorem 5.1.

Consider a -armed stochastic bandit, where the arms follow a sub-Gaussian distribution. Let arm- to denote the arm with the lowest OCE risk value. Let represent the difference between the OCE risk values of and the optimal arm. For a given budget , the arm, say , returned by the OCE-SR algorithm satisfies:

where is a problem dependent constant that does not depend on the underlying OCE risk gaps and , and

Proof.

See Appendix H. ∎

6 Simulation experiments

In this section, we illustrate the effectiveness of our proposed OCE estimators in Equation 3 and Equation 11 on two different settings. In the first setting, we investigate the performance of our OCE estimators in a synthetic experimental setup. In the second setting, we apply our stochastic approximation-based OCE estimator Equation 11 to the credit risk model studied earlier in [7, 12].

Synthetic Setup.

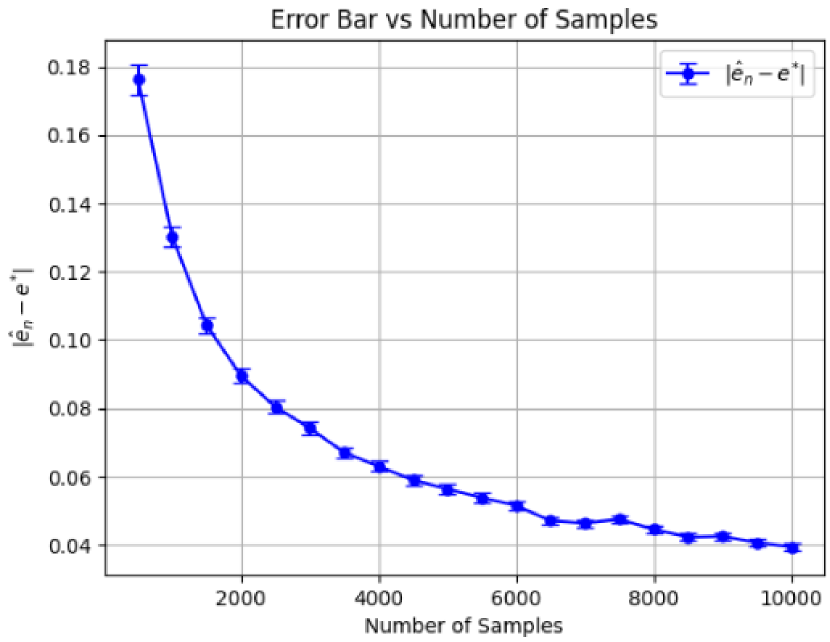

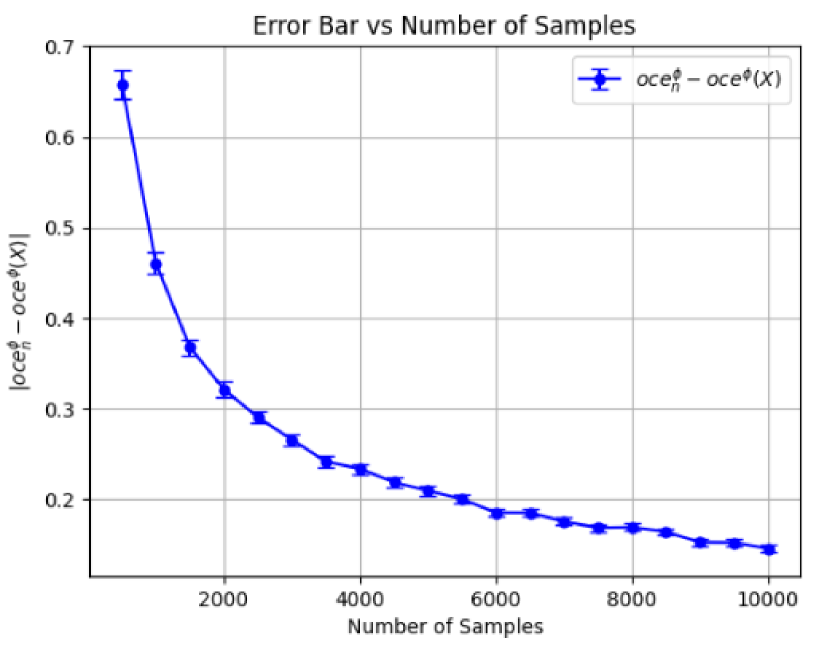

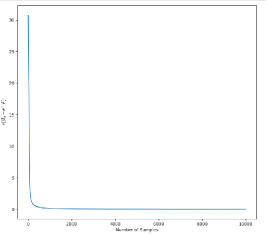

For this experiment, we consider a normal distribution with mean and variance . We set the disutility function , and this choice satisfies the smoothness assumption Assumption A2. From Table 1, we know and . Figure 1 presents the estimation errors and as a function of the number of samples (). The results are averages over independent replications. From Figure 1, it is apparent that the estimators Equation 6 and Equation 3 converge rapidly to the true values.

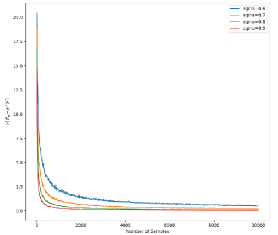

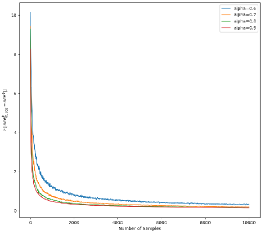

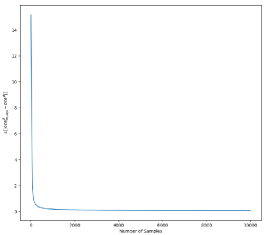

Next, we present results for the streaming estimator described in Section 4. We set the disutility function as . From Table 1, and . We carried out our stochastic approximation scheme Equation 10 for iterations and replicated the experiment times independently and took the averaged results for different step sizes. The plots for as a function of the number of samples () are in Figure 2(a) and Figure 2(b). Figure 2 demonstrates a clear and swift convergence of the estimators in 11 towards their true values.

Credit Risk Model.

In this experiment, we follow the credit risk model, which is described next. Suppose an investor ’s portfolio has positions, with each position subject to some risk of defaulting causing loss to the investor. The total loss is , with being an indicator variable which is if the position defaults and otherwise and is the fractional loss associated with the position. In order to quantify this, let where and are the threshold risk and marginal default probability of the position. Moreover, , the r.v. corresponding to the defaulting risk of the position is determined by the following factor model: For ,

Here, are the systematic risk variables and are the idiosyncratic risk variables and all of them are assumed to be distributed as . The parameters denote the cross-coupling coefficients. For testing our OCE estimator on this model, we decided to use the setup described in [7]: Let the number of positions , fractional losses . for all positions.The coupling parameters are given as , , , , , and otherwise. The distutility function we choose was . Under these values, it is easy to see that from Table 1, that , and .

Figure 3(a) and Figure 3(b) presents the plots of and (respectively) as a function of the number of samples (). The reported result represent the average of independent replications. From , we can see the rapid progress of our estimators in (11) to their true values under the credit risk model setup.

7 Conclusions and future work

We addressed the problem of OCE risk estimation from i.i.d. samples of the underlying loss distribution. We first considered an sample average OCE risk estimator, and derive a mean-squared error bound. We also derived a concentration bound for the sample average estimator when the underlying loss distribution is sub-Gaussian, and the disutility function is strongly convex and smooth. This concentration bound is useful in OCE risk-aware bandit applications. Finally, we also considered a stochastic root-finding based OCE risk estimator, and derived its finite sample guarantees.

For future work, OCE risk estimation with Markovian samples remains unaddressed. OCE risk optimization in a risk-sensitive reinforcement learning framework is another interesting future research direction.

References

- [1] P. Artzner, F. Delbaen, J. Eber, and D. Heath. Coherent measures of risk. Mathematical finance, 9(3):203–228, 1999.

- [2] Francis Bach and Eric Moulines. Non-asymptotic analysis of stochastic approximation algorithms for machine learning. In Neural Information Processing Systems (NIPS), pages –, Spain, 2011.

- [3] A. Ben-Tal and M. Teboulle. An old-new concept of convex risk measures: The optimized certainty equivalent. Mathematical Finance, 17:449–476, 02 2007.

- [4] Aharon Ben-Tal and Marc Teboulle. Expected utility, penalty functions, and duality in stochastic nonlinear programming. Management Science, 32(11):1445–1466, 1986.

- [5] Sanjay P Bhat and L. A. Prashanth. Concentration of risk measures: A Wasserstein distance approach. Advances in Neural Information Processing Systems, 32:11762–11771, 2019.

- [6] D. B. Brown. Large deviations bounds for estimating conditional value-at-risk. Operations Research Letters, 35(6):722–730, 2007.

- [7] J. Dunkel and S. Weber. Stochastic root finding and efficient estimation of convex risk measures. Operations Research, 58(5):1505–1521, 2010.

- [8] Rick Durrett. Probability: theory and examples, volume 49. Cambridge university press, 2019.

- [9] H. Föllmer and A. Schied. Convex measures of risk and trading constraints. Finance and stochastics, 6(4):429–447, 2002.

- [10] S. Gupte, Prashanth L.A., and Sanjay P Bhat. Optimization of utility-based shortfall risk: A non-asymptotic viewpoint. arXiv preprint arXiv:2310.18743, 2023.

- [11] A. Hamm, T. Salfeld, and S. Weber. Stochastic root finding for optimized certainty equivalents. In 2013 Winter Simulations Conference (WSC), pages 922–932, 2013.

- [12] V. Hegde, A. S. Menon, L. A. Prashanth, and K. Jagannathan. Online Estimation and Optimization of Utility-Based Shortfall Risk. Papers 2111.08805, arXiv.org, November 2021.

- [13] A. Kagrecha, J. Nair, and K. Jagannathan. Distribution oblivious, risk-aware algorithms for multi-armed bandits with unbounded rewards. In Advances in Neural Information Processing Systems, pages 11269–11278, 2019.

- [14] Prashanth L.A. and Sanjay P. Bhat. A wasserstein distance approach for concentration of empirical risk estimates. Journal of Machine Learning Research, 23(238):1–61, 2022.

- [15] J. Lee, S. Park, and J. Shin. Learning bounds for risk-sensitive learning. In Advances in Neural Information Processing Systems, volume 33, pages 13867–13879, 2020.

- [16] H. Markowitz. Portfolio selection. The Journal of Finance, 7(1):77–91, 1952.

- [17] Z. Mhammedi, B. Guedj, and R. C. Williamson. Pac-bayesian bound for the conditional value at risk. In H. Larochelle, M. Ranzato, R. Hadsell, M. F. Balcan, and H. Lin, editors, Advances in Neural Information Processing Systems, volume 33, pages 17919–17930. Curran Associates, Inc., 2020.

- [18] E. Moulines and F. Bach. Non-asymptotic analysis of stochastic approximation algorithms for machine learning. Advances in neural information processing systems, 24:451–459, 2011.

- [19] A. K. Pandey, L. A. Prashanth, and S. P. Bhat. Estimation of spectral risk measures. In AAAI Conference on Artificial Intelligence, 2021.

- [20] L. A. Prashanth, J. Cheng, M. C. Fu, S. I. Marcus, and C. Szepesvári. Cumulative prospect theory meets reinforcement learning: prediction and control. In International Conference on Machine Learning, pages 1406–1415, 2016.

- [21] L. A. Prashanth, K. Jagannathan, and R. K. Kolla. Concentration bounds for CVaR estimation: The cases of light-tailed and heavy-tailed distributions. In International Conference on Machine Learning, volume 119, pages 5577–5586, 2020.

- [22] L. A. Prashanth, N. Korda, and R. Munos. Concentration bounds for temporal difference learning with linear function approximation: the case of batch data and uniform sampling. Machine Learning, 110(3):559–618, 2021.

- [23] Philippe Rigollet and Jan-Christian Hütter. High-dimensional statistics, 2023.

- [24] R. T. Rockafellar and S. Uryasev. Optimization of conditional value-at-risk. Journal of risk, 2:21–42, 2000.

- [25] P. Thomas and E. Learned-Miller. Concentration inequalities for conditional value at risk. In International Conference on Machine Learning, pages 6225–6233, 2019.

- [26] R. Vershynin. High-dimensional probability: An introduction with applications in data science, volume 47. Cambridge university press, 2018.

- [27] M. J. Wainwright. High-dimensional statistics: A non-asymptotic viewpoint, volume 48. Cambridge university press, 2019.

- [28] Y. Wang and F. Gao. Deviation inequalities for an estimator of the conditional value-at-risk. Operations Research Letters, 38(3):236–239, 2010.

Appendix A Proof of Theorem 3.1

Proof.

| (14) |

We consider two cases for the analysis.

Case 1: ()

where we used the fact that is -strongly convex.

Case 2: ()

Thus,

| (15) |

Let . Note that . Squaring 15 and taking expectations, we obtain

| (16) |

Using and -Lipschitzness of , we have

Squaring on both sides above and taking expectations, we obtain

| (17) |

The main claim follows by substituting the bound above in (16). ∎

Appendix B Proof of Theorem 3.2

For establishing the bound in Theorem 3.2, we require the following result, which shows that a Lipschitz function of a sub-Gaussian r.v. is sub-Gaussian.

Lemma B.1.

Let be sub-Gaussian with parameter . Then if is -Lipschitz, is sub-Gaussian with parameter .

Proof.

By Lemma 54 of [14], if is a sub-Gaussian r.v. with parameter , then

| (18) |

Following a proof technique analogous to that of the proof of Proposition 2.5.2 in [26], we have

| (19) |

where the last step follows from the fact that .

Setting , we obtain

| (20) |

Employing the proof technique of https://mathoverflow.net/questions/442500/lipschitz-function-of-subgaussian-random-variable, we have

| (21) |

Setting , we obtain

| (22) |

We can now infer that is -sub-Gaussian by using Proposition 2.5.2 of [26]. ∎

Next, we prove Theorem 3.2 by using the result in the lemma above.

Proof.

(Theorem 3.2)

Recall from (15), we have

| (23) |

Appendix C Proof of Theorem 3.3

Using smoothness of , we derive two useful bounds in the lemmas below. These bounds would be used subsequently int he proof of Theorem 3.3.

Lemma C.1.

Under conditions of Theorem 3.3, we have

| (24) |

Proof.

By Lipschitzness of ,

| (25) |

| (26) |

| (27) |

Now take 2 cases: or vice-versa. According to the sign of take the relevant inequality, either case will yield:

| (28) |

∎

Lemma C.2.

Under conditions of Theorem 3.3, we have

| (29) |

Proof.

By L-smoothness of ,

| (30) | ||||

| (31) |

| (32) | ||||

| (33) |

And now just substitute the results obtained from Lemma 24.

∎

We now prove Theorem 3.3.

Proof.

Using the definition of , we have

| (34) |

Using the results of Lemma 24 and Lemma 29, we obtain

| (35) |

Using , we obtain

| (36) |

. Recall that from Equation 15, we have

| (37) |

Define and . Note that and . Using the fact that , we obtain

where and .

Notice that , , and . Each of these expectations are finite and the main claim follows. ∎

Appendix D Proof of Lemma 3.4

Proof.

Consider the r.v. . Using -smoothness of , we know

The bound above can be rewritten as follows:

| (38) |

where and . Notice that are non-negative constants.

Now we employ the proof technique adapted from the proof of [23, Lemma 1.12]. Using the dominated convergence theorem, we have

| (39) |

By part (II) of Theorem 2.2 in [27], we have that a r.v. is sub-exponential if there is a positive number such that for all .

We shall bound each of and to establish a exponential moment bound for the r.v. .

Since is a sub-Gaussian r.v. with parameter , we have

| (40) |

We now bound as follows:

We now bound as follows:

To bound the second term above, consider . . Then

We now bound as follows:

Combining the bounds obtained for and , we get

| (41) | ||||

| (42) | ||||

| (43) |

We have showed that the zero mean r.v. is sub-exponential r.v. whenever is -sub-Gaussian. We also showed the existence of a such that .

By the Chernoff Bound with , we have . Applying a similar argument to , we can conclude that with and . We can get an explicit bound for by setting in Equation 42 to get where . By a parallel argument one can arrive at so that .

By a parallel argument to the proof of Lemma 55 of [14], we obtain

which proves that satisfies Bernstein’s condition with parameters and .

We know from [p. 19, Chapter 2][27] that if satisfies Bernstein’s condition with parameters then it is also sub-exponential with parameters . Thus we have that is sub-exponential with parameters , completing the proof.

∎

Appendix E Proof of Theorem 3.5

Proof.

In Lemma 3.4 we showed that is sub-exponential with parameters .

Applying Bernstein’s inequality to , we obtain

| (44) |

with , and .

Using Equation 36 derived during the proof of Theorem 3.3, we know

| (45) |

The first term on the RHS of Equation 45 is bounded using Equation 44 as follows:

| (46) |

The second term on the RHS of Equation 45 can be bounded using the result derived in Theorem 3.2.

Combining the bounds on the aforementioned two terms, we obtain

| (47) |

Hence proved.∎

Appendix F Proof of Theorem 4.1

Proof.

We rewrite below the update iteration (10) in a form that is amenable to the application of a result from [2]

| (48) |

where are i.i.d r.v ’s sampled during iterations of SGD.

Define

Then Theorem 4.1 can be proved by applying [2, Thm. 3] which is subject to certain assumptions of [2]. For the sake of completeness, we include them here, restating them for the scalar case.

B1.

Let be an increasing family of -fields. is -measurable, and for each , the r.v. is square-integrable, -measurable, and for all , , , with probability .

B2.

For each , the function is almost surely convex, differentiable with Lipschitz-continuous gradient , with constant , that is:

B3.

The function is strongly convex, with convexity constant . That is, for all ,

B4.

There exists such that for all , , w.p.1.

B5.

For each , the function is almost surely twice differentiable with Lipschitz-continuous second derivative , the Lipschitz constant being . That is, for all and for all ,

(w.p 1).

B6.

There exists , such that for each ,

- B1:

-

Holds by definition of , and .

- B2:

-

Holds from the lipschitzness of .

- B3:

-

Consider . If this is strongly convex so is . By strong convexity of ,

- B4:

-

Holds trivially from A5.

- B5:

-

Follows from A6.

- B6:

-

This follows from A5, after noting that the samples are i.i.d. in our setting.

The proof of the theorem then follows by directly applying [Theorem 3][18] in its scalar version to the defined earlier.

Note that the first term in the bound from Theorem 3 of [2] is the dominant one. For our choice of , it can be shown that all the others terms in the aforementioned bound are asymptotically smaller than the first one, and so they can all be represented in the form of . Also, the first term in scalar form is . ∎

Appendix G Proof of Theorem 4.2

Proof.

Using the definitions of OCE risk and its estimator in (11), we have

| (49) | |||

| (50) |

The second term on the RHS of (50) can be bounded using -smoothness as follows:

Since the two-sided inequality above holds for any , we obtain

| (51) | ||||

| (52) | ||||

| (53) | ||||

Substituting (53) into (50), we obtain

Using the triangle inequality, we have

| (54) |

Using similar arguments, it can be shown that

As before, using the triangle inequality, we obtain

| (55) |

It is evident from (54) and (55) that

implying

| (56) |

The first term of Equation 56 is bounded above by from the result derived in Theorem 4.1. To bound the second term, we invoke the Cauchy-Schwarz inequality and simplify as follows:

Using Theorem 4.1, the first term on the RHS is bounded above . To bound the second term, notice that

since , and .

From the foregoing, we have

| (57) |

We now bound the third term of Equation 56 using Assumption A5 and Jensen’s inequality as follows:

Substituting the bounds on the three terms on the RHS of (56), we obtain

Hence proved. ∎

Appendix H Proof of Theorem 5.1

Proof.

The proof closely follows a similar claim for optimizing CVaR in a best arm identification framework, see Theorem 3.6 in [22].

Consider Equation 45. Since is sub-exponential via Lemma 3.4, invoking [Proposition 2.2][27], the first term can be bounded as,

The second term is bounded using the result derived in Theorem 3.2,

| (58) |

Combine both the bounds to get an upper bound on the OCE-estimate as:

| (59) |

Letting , the bound can be written in a simplified form as:

| (60) |

If the OCE-SR algorithm eliminates the optimal arm in phase , it means that at least one of the arms in the set of the last worst arms, denoted as , must not have been eliminated in phase . Therefore, we conclude that:

We now bound the above terms individually as follows.

| (61) | |||

| (62) | |||

| (63) | |||

| (64) |

where is due to Equation 59 and Equation 60 , and . Further, note that

where . By substituting the above in Equation 64, we obtain

| (65) |

Similarly, it can be shown that

| (66) |

The theorem follows by substituting Equation 65 and Equation 66 in Appendix H.

∎