Condensation in scale-free geometric graphs

with excess edges

Abstract.

We identify the upper large deviation probability for the number of edges in scale-free geometric random graph models as the space volume goes to infinity. Our result covers the models of scale-free percolation, the Boolean model with heavy-tailed radius distribution, and the age-dependent random connection model. In all these cases the mechanism behind the large deviation is based on a condensation effect. Loosely speaking, the mechanism randomly selects a finite number of vertices and increases their power, so that they connect to a macroscopic number of vertices in the graph, while the other vertices retain a degree close to their expectation and thus make no more than the expected contribution to the large deviation event. We verify this intuition by means of limit theorems for the empirical distributions of degrees and edge-lengths under the conditioning. We observe that at large finite volumes, the edge-length distribution splits into a bulk and travelling wave part of asymptotically positive proportions.

1. Introduction and main results

1.1. Motivation

The physical phenomenon of condensation corresponds to the formation of drops of liquid when a gas is cooled down or put under high pressure. The mathematics behind this phenomenon however turns out not to be constrained to mathematical models of gases, it is ubiquitous throughout probability and the theory of stochastic processes, ranging from random walks [2], random trees [16], interacting particle systems [24] and Gaussian processes [25] to queueing networks [21] and extreme value statistics [9], to name just a few examples. In this paper we show how a condensation effect arises in the large deviation theory of scale-free geometric random graphs.

To compare the condensation effects we look at the simplest probabilistic model capturing a condensation effect, which is the balls-in-bins model, see [16, Sections 11 and 19]. In this model particles (or balls) are placed into labelled containers (or bins) and the probability of a configuration with particles in the th container (and hence ) is

where are the weights of a zeta distribution with and is a normalisation constant. As and for some particle density , it is shown in [16, Theorem 11.4] that the proportion of containers containing particles converges to a number with and

-

if ;

-

if .

As , we observe in the second case that particle mass is escaping. It turns out, see [16, Theorem 19.34], that the excess mass condenses in a single container, in other words, the container containing the largest number of particles contains asymptotically balls. The vastly increased particle density in this container is interpreted as a manifestation of the condensation phenomenon in a gas under high pressure.

In the balls-in-bins model, if are independent and zeta distributed, then

and the probability of a configuration is the conditional distribution of given the event . If this event has asymptotically decreasing probability and hence the condensation stems from conditioning on a rare event. In our main result a similar phenomenon arises in the context of large deviations for geometric random graphs. Here, loosely speaking, the bins correspond to vertices and the number of balls in a bin corresponds to the vertex degree. But other than in the balls-in-bins model, in the geometric random graphs we can have more than one vertex of macroscopic degree, depending on the number of excess edges generated in the large deviation event.

A further analogy arises in the context of Bose-Einstein condensation. Bose and Einstein predicted in 1925 that above a certain density a macroscopic fraction of particles in a Bose gas aggregate into a single quantum state. Based on Feynman’s representation of the Bose gas as a soup of interacting loops in a container, see for example [28], the phenomenon takes the form that as the particle number goes to infinity, loops of macroscopic length occur in the loop soup. This is studied rigorously under simplifying modelling assumptions, for example in [3, 1, 8], but a fully satisfactory mathematical result on a physical model is still missing. The results achieved so far show that in toy models, above a critical particle density, the empirical distribution of the loop lengths per particle in the limit as the volume of the container tends to infinity converges to a distribution of total mass strictly less than one. The missing mass escapes to infinity because a proportion of particles is associated with loops of a macroscopic length scale, see for example [23]. In our model of a random graph embedded in a -dimensional torus of volume , we look at the length of edges instead of loops and study the empirical distribution of the Euclidean length of all edges. Conditioning the random graph on having an edge density above the critical value we prove that a positive fraction of the mass of the empirical distribution converges to a limit distribution of mass strictly smaller than one, while the rest of the mass forms a travelling wave of macroscopic speed and width. In particular, asymptotically, a positive fraction of edge-lengths is of macroscopic order , loosely analogous to the behaviour of loop lengths in the models above.

Beyond the relation to condensation phenomena, our results are of interest from a purely random graph perspective, providing insight in the nature of the most important models of scale-free random geometric graphs by giving precise asymptotics for the probability that such a graph has a large number of edges. We also give limit theorems for the empirical edge-length distribution and the empirical degree distribution of the graph conditioned on having a large number of edges, which expose the condensation behaviour. Results of this nature have been found for non-geometric graph models like the Chung-Lu graphs [26], very simple geometric models [19], but also for Boolean models which are not scale-free, see the seminal paper of Chatterjee and Harel [4]. The behaviour of scale-free Boolean models, and more general scale-free random geometric graphs, is however fundamentally different from the latter and is explored in the present paper. Our results are set up in a general framework covering a wide range of scale-free geometric graphs.

Outline. We formulate our framework of scale-free geometric graphs and give several examples in Section 1.2, before presenting the main results in Section 1.3. In Section 2 we describe the proof strategies behind our theorems and reduce the proof to seven key propositions, which are proved in Sections 3 to 9.

Notation. We write , respectively , to denote that converges in probability, respectively, in distribution, to as . We write to denote the open ball of radius centred at in a given metric space. For real sequences and with being positive, we write if and if .

1.2. Geometric random graph models

In our general setup, the vertex set of the graph is contained in the -dimensional torus of volume , which we equip with the torus metric . The vertex set may be of two different types:

-

Lattice case: is an integer and the integer lattice on the torus,

-

Poisson case: is real and a Poisson point process of intensity one on .

Fix . To define the edge set , given the vertex set , we equip each vertex with a random weight such that the random variables are independent and identically distributed to some with density

| (1.1) |

We fix a profile function , which is nonincreasing and integrable, and a connection kernel , which is symmetric, continuous and nondecreasing in each argument. For every unordered pair , we define a function by if , and

| (1.2) |

Given the vertex set and the weights, we include the edge in with probability , independently for every unordered pair of distinct vertices in with weights . More precisely, let be conditionally independent Bernoulli-distributed random variables with success parameter . For notational simplicity write for . The edge set is given by

| (1.3) |

The degree of a vertex is the number of neighbours of in defined as

| (1.4) |

This model was introduced under the name weight-dependent random connection model in [12, 11] and under the name kernel-based spatial random graph in [18]. We now explain how our principal examples fit in this framework. In all our examples the empirical degree distributions of the graphs converge to a deterministic limit, which is a heavy-tailed distribution with the same tail index as the weight distribution.

(i) Scale-free percolation

(ii) Poisson Boolean model with heavy-tailed radii

Consider the Poisson case with profile function and connection kernel . Thinking of as the radius of a ball centred in , in this model two vertices are connected by an edge if and only if . Therefore this graph model shares the name with the union of the balls over all points , which is studied in stochastic geometry [27].

(iii) Age-based preferential attachment graphs

We define a dynamical graph model with vertices embedded in the torus of volume one as in [10]. Let , for some , and fix . We take a standard Poisson process of arrival times for the vertices. Given the graph , at the arrival time of a new vertex, we give this vertex a random location uniformly on the torus of volume one. Independently for every vertex of , we establish an edge to the new vertex with probability where is its location and its birth-time. As is the order of the expected degree of the vertex at time , the new vertex prefers to attach itself to existing vertices with large expected degree or, equivalently, old age.

For any fixed time , we rescale the graph to the torus by multiplying all locations with the factor . We denote the rescaled graph by and explain how it fits our framework. If is the birth time of a vertex at the new location , then we let its weight be . Then the new vertex locations are a standard Poisson point process on , the weights are independent Pareto-distributed with parameter , and the probability of two vertices at locations in being connected is

for . Hence results for the number of edges in as time goes to infinity can be transferred directly from results for the number of edges for the graph as the volume tends to infinity. The latter fits our framework with the given .

1.3. Main results

We now formulate the assumptions on the kernel and profile function in our framework for our main results to hold.

Assumption A. There exist constants such that

| (1.5) |

and the limit

| (1.6) |

exists. The profile function is continuous at and, for some ,

| (1.7) |

The graph of has no flat pieces except possibly at its essential supremum or infimum.

Observe that, in contrast to , the derived kernel is not symmetric, but linear in the first argument. Recall that denotes the total number of edges in . Then we have, as , by an application of a law of large numbers for geometric functionals,

| (1.8) |

for some . More details and an explicit formula for are given in Remark 1.7 below.

For and , let

| (1.9) |

and

| (1.10) |

Further, for set and

| (1.11) |

Our main result for the large deviations of the number of edges in the random graph models described in Section 1.2 is summarized in the following theorem.

Theorem 1.1 (Upper large deviations).

Let be the number of edges in the weight-dependent random connection model with kernel and profile satisfying Assumption A. Let be non-integer and the unique integer such that . Then, as ,

Remark 1.2 (Properties of ).

We always have . If , then and is a continuous function on all open intervals not containing an integer; see Lemma 2.4 for a proof. Therefore, under this assumption, Theorem 1.1 identifies the precise asymptotic behaviour of the large deviation probability. Otherwise, if , the graph can be identified with the graph with profile function after Bernoulli percolation with retention probability . Given the graph prior to percolation and denoting its edge set by , the number of edges in the percolated graph is binomial with parameters and . By Cramér’s theorem this random variable has the same upper large deviations as its conditional mean and so the upper large deviation result of Theorem 1.1 holds for verbatim and also identifies the precise asymptotic behaviour.

Remark 1.3 (Our assumptions).

Remark 1.4 (Non-integer restriction on ).

Observe that the exponent of in the power-law decay of the large deviation probability in Theorem 1.1 jumps at integer values of . At these values the asymptotic behaviour of depends on specific model details and a universal result covering a wide range of profiles and kernels in a single limit theorem with explicit limit as above does not hold. A deeper discussion of this fact is given in Section 2.4 below.

From now on we assume, without loss of generality, that and consider the behaviour of the graph conditioned on the large deviation event above.

Remark 1.5 (Conditional limit distribution of the number of edges).

It follows immediately from Theorem 1.1 that, conditionally on ,

| (1.12) |

where the random variable is supported on , and has tail distribution function

| (1.13) |

This follows as is continuous on . Observe that the distribution of has an atom at if and only if , which happens, for example, in the case of the Poisson Boolean model, Example (ii), in which is constant on the interval .

Next we describe the empirical distribution of the edge-lengths, which is the (random) measure on given by

| (1.14) |

where is the unit mass at . Now we introduce the objects appearing in the limit theorem below. For , define a measure on by

| (1.15) |

Consider the random measure where the law of is given by

| (1.16) | ||||

setting In terms of this notation, in (1.12)–(1.13) has distribution

| (1.17) |

For and , let

| (1.18) |

Let be continuous and define, for ,

| (1.19) |

Theorem 1.6 (Convergence of empirical edge-length distribution).

Let be the empirical edge-length distribution in (1.14) of

the weight-dependent random connection model with kernel

and profile satisfying Assumption

A.

Let be a non-integer and be the unique integer with .

For every that is continuous with compact support, conditionally on

,

-

(a)

-

(b)

Remark 1.7 (Law of large numbers for edge functionals).

The convergence in probability in (a) also holds when not conditioning on , in this case even for all bounded and continuous functions . A proof based on a local limit theorem, given for a slightly different vertex set, can be found in [14] and is easily adapted to our situation. Therefore the right-hand side in (a), with the choice , provides an explicit formula for the asymptotic edge density that appears in (1.8).

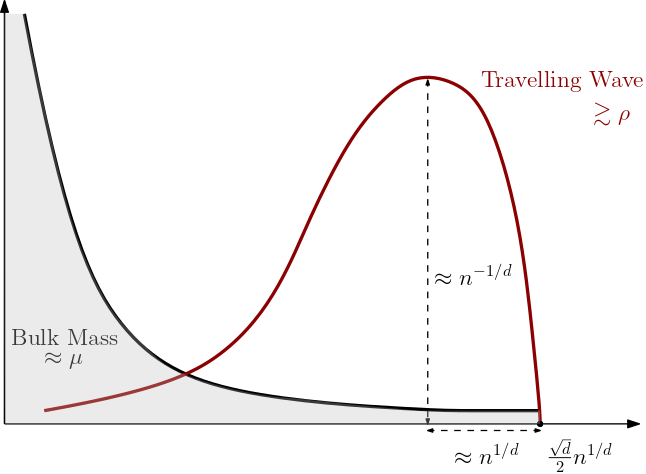

Theorem 1.6 shows that the empirical edge-length distribution splits into two parts, a bulk part of total mass which converges to the asymptotic edge-length distribution in the unconditional random graph, and a travelling wave part of mass at least and random shape, moving to infinity at speed , see Figure 1 for a schematic picture.

To state the next theorem, denote the order statistics of the weights of vertices in by

Let be the location of the vertex whose weight is , that is . For a vertex , define

| (1.20) |

We consider the joint empirical distribution of these two types of degrees. For and , define

| (1.21) |

In words, is the proportion of vertices that have exactly neighbours in the set , and neighbours in the set . Let be a sample from the law (1.16). We introduce the local limit of the graph , which is based on the same connection probabilities but with an infinite vertex set. For the lattice case, is obtained by considering as vertex set all the points of the lattice , for the Poisson case is constructed by taking as vertex set a Poisson point process of intensity one on , with an atom inserted at . In both cases, the infinite random graph, rooted at arises as the local (Benjamini-Schramm) limit in probability of , see [14, Theorem 1.11]. Denote the degree of the root in by and the degree of the root in conditioned on having weight by .

Our third main result describes the degree distribution of the graph conditioned on the event . We start with a version describing degree sequences of hubs and other vertices separately.

Theorem 1.8 (Degree sequences of hubs and normal vertices).

Consider the weight-dependent random connection model with kernel and profile satisfying Assumption A. Let be a non integer, and be the unique integer satisfying . Conditionally on the rare event , as ,

| (1.22) |

in distribution on sequence space with the product topology, while

| (1.23) |

where

| (1.24) |

and where the vector is chosen according to the law given by (1.16) and are i.i.d. uniformly distributed random variables on independent of . Moreover, the expectation is over which is uniformly distributed on , and an independent Pareto-distributed weight and, for and , over conditionally independent Bernoulli random variables with parameter

Combining the results in Theorem 1.8, we get convergence of the degree distribution.

Corollary 1.9 (Degree distribution).

Conditionally on the rare event , the empirical degree distribution

converges in distribution on the Polish space of probability measures with the weak topology to the random probability measure

Remark 1.10 (The condensate).

Theorem 1.8 identifies where the surplus edges, whose limit in distribution equals by Remark 1.5, are located. Indeed, using that the sum of the degrees equals , we see that the vertices of high-weight of order form the condensate attracting roughly incident edges. The other ends of the edges are at vertices whose weights have the unconditional weight distribution . Thus, the condensate consists of vertices, but other vertices can be incident to this condensate. This makes the condensation phenomenon different, and arguably richer, than the one described in Section 1.1.

2. Overview and proof strategies

2.1. Upper large deviations: Strategy and proof of Theorem 1.1

We call an edge high-weight if at least one of its endpoints has high weight, which we make precise below. Further, light-weight edges are edges where neither endpoints have high weight. We also divide edges into long and short edges, where long edges are those that connect vertices far away from each other. More precisely, let be some sequence tending to zero, let and split the edge set into the three disjoint sets

| (2.1) | ||||

| (2.2) | ||||

| (2.3) |

where denotes the maximum of and . These sets correspond to the sets containing short and light-weight edges, long and light-weight edges and lastly high-weight edges. Theorem 1.1 follows from three key steps estimating the number of edges in these sets.

Step 1. Short and light-weight edges form the bulk.

Consider short, light-weight edges. These constitute the ‘bulk’ edge count, i.e., a typical edge of the graph falls into this category. Proposition 2.1 shows that the number of these edges are well concentrated about the mean .

Proposition 2.1.

We prove Proposition 2.1 in Section 3. In the proof we first fix the vertex weights (and in the Poisson case both the vertex locations and weights) and apply a conditional version of McDiarmid’s concentration inequality, using that the edges are included independently. Then we use McDiarmid’s inequality again to show concentration of the resulting functionals of the independent weights (and in the Poisson case also the vertex locations).

Step 2. Long and light-weight edges are negligible.

Proposition 2.2 shows that this contribution is asymptotically negligible.

Proposition 2.2.

We prove Proposition 2.2 in Section 4 for which we use that the connection probability of a pair of vertices is increasing with respect to the weights of the vertices, and decreasing with respect to the spatial distance between the vertices. This implies that the total number of long and light-weight edges can be stochastically dominated by a suitable binomial random variable and we can use a standard binomial concentration argument.

Step 3. High-weight edges form the condensate.

Using the first two steps, it remains to understand the probability that the total number of high-weight edges is larger than . This is accomplished in Proposition 2.3.

We prove Proposition 2.3 in Section 5 for which we use that the number of high-weight edges is well approximated by the sum of the degrees of the high-weight vertices. The degree of a vertex given its weight has Poisson-like statistics with the mean being an increasing function (depending on ) of the weight, see for example [14, Proposition 1] for a proof of this fact when the locations of the vertices are uniform, as in the Poisson models. As a consequence, again using concentration arguments, when the weight of a vertex diverges, its degree behaves like this function evaluated at its weight. This observation allows us to approximate the total number of high-weight edges by an i.i.d. sum of a deterministic (but -dependent) function of the weights. To understand the probability that this sum is at least , we do a large deviation analysis similar to the one given in [19], and show that this event occurs precisely when there are vertices with weight of order . This shows that behaves as stated in Proposition 2.3.

We now prove continuity of , which is the last ingredient in the proof of Theorem 1.1, which then follows straightforwardly from the above propositions.

Lemma 2.4.

For all and ,

defines a continuous function .

Proof.

Finiteness for follows from . For , we note that . Choosing such that for all , and using that , we see that . To see positivity, we lower bound by

Note that and hence the set contains an interval unbounded to the right and hence has positive measure. Hence .

To see continuity, fix . Given , we need to find with

For this, we note that if is small enough, then implies that there exists with . Using that has no flat pieces except possibly at zero and one, we find such that if and . Hence one of the integrations with respect to is over an interval of length at most and choosing small we can upper bound the integral by . ∎

Proof of Theorem 1.1.

Take sufficiently small such that . Then fix and such that Propositions 2.1, 2.2 and 2.3 can be applied. Using the definitions of , and in (2.1)-(2.3), we can write

| (2.4) |

The upper bound of Theorem 1.1 follows by noting that

| (2.5) | |||

where the last equality holds by applying Propositions 2.1, 2.2 and 2.3. For the lower bound, remark that

| (2.6) | ||||

By Propositions 2.1 and 2.3, the last line equals . Combining the upper and lower bounds and, recalling from Lemma 2.4 that is continuous on , we complete the proof by letting tend to zero. ∎

2.2. Convergence of the empirical edge-lengths: Strategy and proof of Theorem 1.6

Throughout this section is the unique integer with . The key step in the proof of Theorem 1.6 (a) is the following law of large numbers.

Proposition 2.5.

Let be continuous with compact support and recall from (1.19). Then, for all ,

In the proof of Proposition 2.5, given in Section 6, we split the sum over all edges into the sum over the edges in , for which we can argue similarly as in Proposition 2.1, and the sum over the edges in and , which are negligible as most of these edges are too long to be in the support of .

For the proof of Theorem 1.6(b), we first approximate the empirical edge-length distribution at macroscopic scale by a deterministic function of the largest weights in the graph. Let be continuous with compact support and define

| (2.7) |

where we recall from (1.9). Our next result identifies the limiting distribution of long edges in terms of the largest weights.

Proposition 2.6.

Conditionally on ,

where are the largest weights in the graph ordered by decreasing size.

We prove Proposition 2.6 in Section 7 by using a concentration argument to approximate, for all vertices with weight exceeding , the term by its conditional expectation given . For (here meaning the ratio of the two sides going to ), the conditional expectation converges to . Together with the fact that the contribution of light-weight edges to the number of long edges is negligible, this allows us to approximate by a deterministic function of the largest weights.

We then show convergence in distribution of the largest weights in the graph.

Proposition 2.7.

We prove Proposition 2.7 in Section 8 by refining the analysis of the high-weight edges in Section 5. We show that the event is asymptotically equivalent to the event . The result follows because, given the vertex set , the random variables are independent Pareto distributed.

Remark 2.8 (A hub clique).

As a consequence of Proposition 2.7, conditionally on the event , there are vertices with weight at least , with probability at least , where as . We call these high-weight vertices hubs. As the length of any edge is at most , and the connection probability is , we use a union bound to see that the probability of the event that there is a pair of hubs which does not share an edge is at most . Hence if the hubs form a clique with high probability.

2.3. Convergence of degree distribution: Strategy and proof of Theorem 1.8

In this section, we reduce the proof of Theorem 1.8 to the following proposition. Recall denotes the degree of the root in the local limit of the graph conditioned on having weight .

Proposition 2.9.

Let and . Let

| (2.8) |

where are, conditionally on , independent Bernoulli random variables with parameter

Conditionally on and (in the lattice case projected to the nearest lattice point of ) for all ,

-

(i)

-

(ii)

-

(iii)

Proof of Theorem 1.8.

We present the technicalities in the language of the Poisson case, the lattice case is analogous. To prepare this proof, take an arbitrary, measurable function. Write for the point process of weights and for the corresponding point set. Then

Applying the multivariate Mecke formula [20, Theorem 4.4] and denoting the intensity measure of by , we get

Because and hence , we get

| (2.9) |

Now fix an integer and a bounded, continuous function . To simplify notation we write for and for , dropping the index range when there is no ambiguity. To prove (1.22), it suffices to show, as ,

| (2.10) |

Fix small enough so that . Abbreviate and

The left-hand side of (2.10) can be written as

| (2.11) | |||

| (2.12) | |||

| (2.13) |

We will show that (2.11) converges to the right-hand side of (2.10) while (2.12) and (2.13) tend to zero as .

Since is bounded, (2.13) can be bounded from above by a constant multiple of

| (2.14) |

By Proposition 2.7 and the Portmanteau theorem,

For the second summand of (2.3), observe that by Proposition 2.7,

Recall that is chosen such that and so cannot hold if there is with . Hence the law of given in (1.16) is such that for all , almost surely. It follows that (2.3), and hence (2.13) tend to zero.

Next, (2.12) can be bounded by a constant multiple of

By the above, the subtrahend goes to one. The minuend does the same as, by (2.9),

| (2.15) |

using the substitution and using that . Again by choice of if there is with then . Together with Theorem 1.1 this shows that (2.15) is asymptotically equivalent to .

It remains to show that (2.11) converges to the right-hand side of (2.10). Note that

Using (2.9) and the substitution again, this equals

By Theorem 1.1 the integrand (in the second line) is bounded, and by Proposition 2.9(i) and (ii), converges to

As the integrating measure (in the first line) is finite, dominated convergence implies convergence to

2.4. Discussion: Why we assume to be non-integer.

We now briefly discuss the nature of the problem when is an integer in Theorem 1.1. The proof can be reduced to studying the deviations of a truncated i.i.d. sum of the form for a suitable , where we can think of . It turns out that, for any , we have for some function , which converges to as . This leads us to study the large deviations of , with an i.i.d. sequence with law (1.1) and with as . We claim that these large deviations are not universal at the integers.

We discuss the probability of the event , where , for three illustrative examples of , which differ in the approach to in the large limit:

In case (a), we note that if , the corresponding summand contributes to the sum . Thus, we get if there are values of for which . The remaining contribution comes from the ‘small’ weights remaining tightly concentrated around . This strategy turns out to be optimal and has a probability of order , similar in flavour to Theorem 1.1.

In case (b), we can consider a strategy where there are exactly weights being at least for some large constant . The contribution coming from these large weights is at least . The contribution coming from the remaining small weights is again tightly concentrated around , so they contribute with good probability at least to the sum. This strategy has probability of order , which vanishes faster than , but is still much cheaper than having vertices with weight of order , and we believe it to be optimal.

In case (c), as before, we can always choose vertices of weight of order . However, another strategy similar to case (b) can be obtained by choosing weights to be at least for some appropriate , and arguing as before that the contribution from the small weights is highly concentrated. Depending on and , either of these strategies can be optimal, and we expect to see a phase transition depending on and in this case.

3. Concentration of the bulk: Proof of Proposition 2.1

In this section, we show that the short edges are essentially those in and the measure is asymptotically equivalent to the empirical measure of the edge lengths in the unconditioned model. We define to be the cube of volume in centred at zero.

3.1. Setup and main techniques

Recall the definition of given by (2.1),

where for some and such that . Our main goal is to prove that is well-concentrated around . The number of vertices in our graph, denoted by , is equal to in the lattice case, and a -distributed random variable in the Poisson case. In this case it is helpful to condition on the number of vertices. Let denote the probability of our graph models conditioned on the number of vertices and write for the associated expectation.

For , define the interval

| (3.1) |

Standard Chernoff concentration bounds [17, Remark 2.6] for Poisson random variables give us, for Poisson models,

| (3.2) |

for all . In particular, choosing sufficiently large, for example such that , we get that

| (3.3) |

for Poisson models. Once we condition on the number of vertices , the graph is completely determined by a vector of i.i.d. weights with law (1.1), the vector of conditionally i.i.d. uniform positions in in the Poisson case, resp. locations of all the lattice points in in the lattice case, and the edge indicators

We denote the degree of the th vertex by . This setup allows us to provide a single proof that covers both cases simultaneously. For notational simplicity we will abbreviate to for the rest of the paper.

In this section we actually prove a more general result than just for , which involves a continuous bounded function evaluated on the edge-lengths. The first step is to define a function that depends on the edge indicators as well as the positions and weights of vertices and the value of on the distances between the positions. We let

We define the function , which depends on as

| (3.4) |

The main result of this section is a concentration result for around the value .

Proposition 3.1.

Let be a random variable as in (1.1) and a continuous bounded function. Then, for any and , as ,

3.2. Proof of Proposition 3.1

The key tool behind proving the concentration result is two applications of McDiarmid’s inequality on . The first application conditions on the weights and positions, so that the edge indicators are independent Bernoulli random variables, and the second application is for the conditional expectation of given the weights and positions.

It turns out to be convenient to include the indicator of a good event in the function . For this, let for some , and define as the partition of of equally-sized cubes, each of side length . Note that contains at most many such cubes. For , consider the event

| (3.5) |

where we recall the interval from (3.1). In words, corresponds to the event that the number of points of contained in each cube in the partition lies in the given interval . Note that for a cube , and conditionally on , the number of points in is -distributed. Using standard Chernoff bounds, and a union bound for the number of cubes, it is easy to see that

| (3.6) |

for some constant . Hence, by taking an expectation over ,

Using (3.3) and the fact that , we can choose sufficiently large such that

| (3.7) |

Therefore it suffices to work conditionally on the event . Define the function

| (3.8) | ||||

The main technical result needed to prove Proposition 3.1 is the following concentration bound on .

Lemma 3.2.

Let . For both the lattice and Poisson case, there exist constants such that for sufficiently large , conditionally on the event ,

| (3.9) | ||||

Another technical lemma we need provides bounds on the conditional expectation of the degree of a vertex, given the number of vertices and the weight of the vertex.

Lemma 3.3.

For both the lattice and Poisson case, there exist positive constants such that, for any and ,

We postpone the proofs of both lemmas till the end of this section and proceed with the proof of Proposition 3.1 based on these technical results.

Proof of Proposition 3.1.

Throughout this proof we let denote the upper bound for the function . We start by splitting the difference between and the expectation into four parts as follows:

| (3.10) | |||

| (3.11) | |||

| (3.12) | |||

| (3.13) |

We aim to show that the probability of exceeding is for each of these four terms. Proposition 3.1 directly follows from this.

Bound on (3.10). For this term we have

Moreover, because is uniformly bounded by we get, using (3.2) and Markov’s inequality,

For Poisson models, picking sufficiently large gives us

| (3.14) | |||

As implies , the first term of (3.14) can further be bounded from above by a constant multiple of . Using that and (3.3), we conclude that (3.14) equals . The same conclusion holds for lattice models, as here .

Bound on (3.11). For this term we use Lemma 3.2 together with (3.3) to get, for sufficiently large ,

Observe that where , so that the first term is . Moreover, since by assumption , the same holds for the second term. Finally, when we pick large enough, while this also holds for the last term due to (3.7). We thus conclude that all four terms in the upper bound go to zero sufficiently fast.

Bound on (3.12). We will prove that, for all ,

| (3.15) |

Observe that Therefore,

| (3.16) | |||

The first term on the right-hand side can be bounded by , using that . For the second term on the right-hand side, we note that by (1.5) and (1.7), when and ,

where . It follows that

| (3.17) |

Finally, we have

By Lemma 3.3, it follows that and hence

Therefore,

| (3.18) |

Putting (3.17) and (3.18) back into the upper bound for (3.16) we get

Now recall that on the event , it holds that . Therefore, on this event, the right-hand side can be bounded from above by a constant multiple of . By selecting large enough, this is , using our assumptions that and and therefore . Hence, by picking a sufficiently large , we use (3.3) to conclude that

Bound on (3.13). For the final term, recall from (1.19) and from (1.18), for and . Let us write

Recalling that is the centred cube of volume , we observe

where in the lattice case we use that . Note that converges pointwise to as tends to infinity. Together with the fact that , the dominated convergence theorem implies that . It follows that for the Poisson case, on the event ,

since . The same equality holds for the lattice case. For Poisson models, this implies that for all and sufficiently large ,

Using (3.3) we can conclude that

by choosing sufficiently large. The bound above also holds for lattice models. This deals with the last term (3.13) and therefore finishes the proof of Proposition 3.1 subject to Lemmas 3.2 and 3.3. ∎

3.3. Proofs of technical lemmas

The rest of this section is dedicated to the proof of Lemmas 3.2 and 3.3. Since we condition on the number of vertices , the graph will be based on a vector of i.i.d. Pareto weights and of uniform positions in for the Poisson case and being just the locations of the lattice points of for the lattice case. The key tool in proving Lemma 3.2 lies in applying McDiarmid’s inequality [22] twice.

We begin by recalling the version of McDiarmid’s inequality we shall use, given in [5]. Consider a function , where each is a probability space. Moreover, let be in the domain of . We call this the good event and say that satisfies the bounded difference inequality on with non-negative constants if for every and for all with for ,

| (3.19) |

For such a function , for any independent random variables on the spaces and for all , it holds that

| (3.20) | ||||

For the proof we apply McDiarmid’s inequality to and also to , where we write for for notational simplicity. The first term considers the probability conditioned on the weights and edges. Under this conditioning the edge indicators are independent so that McDiarmid’s inequality can be applied without specifying a good event. The good event is however needed to apply McDiarmid’s inequality to the second term, where the good event will be .

Both these steps will yield an upper bound in terms of that is when , which holds for the lattice as well as the Poisson case with a probability that converges to , by (3.3) with an error of order .

Proof of Lemma 3.2.

Concentration bulk edges given the weights and positions.

We begin with a bound on the term (3.21). Choose and let be the canonical probability space for . Conditionally on the weights and the positions , we consider as a function on .

For the application of McDiarmid’s inequality we take the good event to be the entire space, i.e., so that in particular . Denote by the vector obtained from where we replace by and leave all other coordinates unchanged. Then, conditionally on and , the function satisfies, for all , the bounded difference inequality

The sum of the square of differences is given by

On the event , the number of points in every cube of side length is at most , and any ball of radius is covered by at most such cubes. This implies that, for any ,

| (3.23) |

Taking it follows that and hence McDiarmid’s inequality (3.20) implies that

| (3.24) | ||||

Concentration of bulk for weights and positions.

We next establish an upper bound for (3.22) by again an application of McDiarmid’s inequality. For the setup, let , for all , and take as the good event. We define the function , for and , as

| (3.25) | ||||

and observe that In addition, we note that

We claim that satisfies the bounded difference inequality on the event . To see this, for any two vectors and of weights and positions, denote by and the vectors where the entry is replaced by any value and , and all other coordinates are unchanged. Then,

We will show that there is a constant that does not depend on and such that

| (3.26) |

The other sum satisfies the same upper bound, which implies that satisfies a bounded difference inequality on the event with bounds and thus

We will first finish the application of McDiarmid’s inequality (3.20) using (3.26). For this, we note that on the event , it holds for sufficiently large that

which implies . Moreover, there exists a constant such that

Therefore, using that , we get

Noting that on the event we have it follows from (3.2) that for sufficiently large the last term is zero. Thus, by applying (3.20) to the first part we get

Combining this with (3.24), the main result (3.9) follows by picking and . It only remains to establish the bound (3.26). We first use (1.7) to get

Thus, the left-hand side of (3.26) can be bounded from above by a constant multiple of

| (3.27) | |||

| (3.28) |

We begin by studying (3.27). For any satisfying , (1.5) gives us that . Recall that we chose and to satisfy the conditions of Proposition 2.1, that is and . Thus, if , then for sufficiently large . Therefore, for large , (3.27) can be bounded from above by

Applying (3.23) with , the above can be bounded by . To conclude (3.26), it therefore remains to show that the second summand (3.28) is bounded from above by a constant multiple of .

For (3.28) observe that, since is translation invariant,

where for the canonical mapping of to with recalling that is the -dimensional cube of volume centred at the origin. In particular, there exist constants such that for sufficiently large

Plugging this back into the sum (3.28), and using 1.5, we get

Taking now yields (3.26). ∎

The proof of the last technical lemma rests on the following easy bound.

Lemma 3.4.

There exist constants such that

| (3.29) |

Proof.

Using (1.7), for , we bound

The integrals , and for , can both be bounded from above and below by constant multiples of , where the constants only depend on the dimension . Next, by (1.5),

where the last inequality follows from basic computations and holds for some constant . For the lower bound, by (1.5) and so

for some constant . Combining the above implies (3.29). ∎

Proof of Lemma 3.3.

We first consider the lattice models, where the number of vertices equals . For , by embedding the torus into the integer lattice and using the translation invariance of , we get

| (3.30) |

When conditioning on in the Poisson case, the positions of the vertices are sampled uniformly and independently on the torus. Thus, by embedding the torus into and using translation invariance of ,

Note that for the lattice case, the sum in (3.30) can be interpreted as a -dimensional Riemann sum. Hence, there exists constants such that

Lemma 3.3 for both lattice and Poisson cases follows from Lemma 3.4. ∎

4. Concentration of the long edges: Proof of Proposition 2.2

Recall that we denote the number of vertices in our graph by . Recall from (3.1) for . For both lattice and Poisson models we remark that, for all with , conditionally on and ,

where , using (1.5) and (1.7). Recall that we suppose that and satisfy the conditions of Proposition 2.1. More precisely, for some and . Define, for ,

where . We begin by proving the proposition for lattice models. Let be a -distributed random variable with mean since . Then is stochastically dominated by . Observe that since , there exists some such that

which goes to zero polynomially fast. Consequently, and the upper bound tends to zero stretched-exponentially fast again using a standard Chernoff bound [17, Theorem 2.1] for binomial random variables, and hence faster than for any . This concludes the proof of Proposition 2.2 for lattice models.

For Poisson models, conditionally on the number of vertices , let be a random variable, which is -distributed and note again that is stochastically dominated by . Further

| (4.1) |

The conditional mean of is , thus standard large deviation bounds for binomial random variables (see, e.g., [17, Theorem 2.1]) give

By taking expectations we can bound the first summand of the right-hand side of (4.1) from above by

By choosing sufficiently large, (3.3) gives us that the second summand above equals . The first summand of the above inequality can be bounded from above by

This can be further upper bounded by a constant multiple of for large . Since , the above equals . We are left to bound the second summand of (4.1). Note that, for the same as before,

using the fact that . Since is a Poi-distributed random variable, standard concentration bounds [17, Remark 2.6] imply is , which concludes the proof. ∎

5. Large deviations of the high-weight edges: Proof of Proposition 2.3

5.1. Overview of the proof of Proposition 2.3

In this section, we reduce the proof of Proposition 2.3 to a key technical result, which we state as Proposition 5.3. The proof of Proposition 5.3 is deferred to Section 5.3. We begin by noting that

| (5.1) |

where is the degree of defined in (1.4), and

Recall that for Poisson models, the vertex set is a Poisson point process of intensity one on . In this case, we need to state results for the Palm version obtained by adding the point with independent Pareto-distributed weight to . We denote by the probability and by the expectation with respect to this new vertex set.

For and define, for both lattice and Poisson models,

| (5.2) |

Observe that for , by the translation invariance of the torus , we therefore write for . Further, for , define the events

| (5.3) |

We now state a few results that are necessary to prove Proposition 2.3 and postpone some of their proofs to the end of the section:

Lemma 5.1 (Concentration of ).

For any , there is such that

For and , define

| (5.4) |

As before, for , we have and we therefore write for . The following lemma bounds and :

Lemma 5.2.

Let . There exist positive constants such that

for sufficiently large . Since , the above implies

The proof of Lemma 5.2 follows directly from Lemma 3.3 by noting that for lattice models , while for Poisson models .

The following proposition states a limit law for the sum .

Proposition 5.3.

Let be non-integer and . With as in (1.11)

| (5.5) |

The proof of Proposition 5.3 will be given in Section 5.3. We are now ready to prove Proposition 2.3 using Lemmas 5.1 and 2.4, and Proposition 5.3.

Proof of Proposition 2.3.

The idea of the proof is to approximate by the i.i.d. sum of Proposition 5.3, and argue that the errors we encounter in this approximation tend to zero faster than the right-hand side of Proposition 5.3. The proof holds for both lattice and Poisson models. To this end, we fix to be sufficiently large such that the probability of the event defined in (5.3), tends to zero faster than the right-hand side of (5.5). The existence of such is ensured by Lemma 5.1. Write

| (5.6) |

By choice of , the second term on the right-hand side tends to zero faster than . Using the definition of , the first summand of (5.6) can be bounded from below by

| (5.7) |

where as before, the term tends to zero faster than . An upper bound follows similarly, i.e.,

| (5.8) |

Fix such that . There exists such that is increasing on the interval . In particular, when for , we have for all sufficiently large, where the first inequality holds by monotonicity of , and the second inequality follows from the fact that diverges by Lemma 5.2. Using the monotonicity of the function on , we can then conclude that when for we have for all sufficiently large . This implies that, for sufficiently large and all ,

| (5.9) | ||||

| (5.10) |

Combining the above two inequalities together with (5.6), (5.7) and (5.8), it follows that for sufficiently large ,

| (5.11) |

Proposition 2.3 follows by multiplying this series of inequalities by , then letting , and finally , using (5.5) and the continuity of from Lemma 2.4.∎

5.2. Concentration of degrees: Proof of Lemma 5.1

We begin by introducing a lemma that states that the degree is a Poisson random variable for the Poisson case:

Lemma 5.4.

In the Poisson case, given a vertex and its weight , the locations and the weights of the vertices contributing to are distributed as a Poisson point process on with intensity

Consequently, given the weight , the degree is a Poisson random variable with parameter .

We omit the proof of this lemma, as it is a minor modification of [15, Lemma 2.1]. Next we state and prove a concentration result on given its weight, for any fixed .

Lemma 5.5.

For , any and ,

| (5.12) | ||||

Proof of Lemma 5.5.

We can write , where and given by (1.4). Recall that for , and define . For all ,

| (5.13) |

since we can write and . We begin by proving the statement concerning lattice models. Note that, conditionally on , both and are sums of independent Bernoulli random variables. Hence, standard concentration arguments (see e.g. [17, Theorem 2.8]) imply that, for all ,

| (5.14) | ||||

| (5.15) |

Now, we write

By (5.14) and (5.15) together with (5.13), and letting , this in turn is bounded from above by

| (5.16) |

which concludes the lemma for lattice models.

Proof of Lemma 5.1.

We begin by proving the lemma for lattice models. Note that a standard union bound gives us that

The upper bound (5.12) from Lemma 5.5 gives us that

Remark that by Lemma 5.2, inside the integral above can be bounded from below by , which is at least for all large . Together with the fact that the function is decreasing in we get that for large and . Hence, for large , the probability of can be bounded from above by

By Lemma 5.2, we conclude that for any we can choose a constant large enough such that the last term tends to zero faster than .

Next we prove the lemma for Poisson models. Similarly to the lattice case, and using a union bound, we observe that

where the second equality holds by Mecke’s formula [20, Theorem 4.1]. The remainder of the proof is identical to that of lattice models and is therefore omitted. ∎

5.3. The few-jumps phenomenon: Proof of Proposition 5.3

It remains to prove Proposition 5.3. We first state and prove a result that shows that it is unlikely to have many small macroscopic contributions.

Lemma 5.6.

Let be a positive integer. For all , there exists such that

| (5.17) |

Lemma 5.6 tells us that the sum cannot contribute significantly at a linear scale. Let us discuss the proof strategy. First, we use Lemma 5.2 to reduce the question to understanding the probability

for some fixed constant . The sum inside the last probability cannot contribute at least with good probability when we choose arbitrarily small. To show this, we use a Chernoff inequality to reduce the problem to understanding exponential moments of the form , where is the truncated random variable and where has density (1.1), and we take for a suitable . This we achieve by a second order Taylor expansion and choosing the scale appropriately.

Proof.

Let be an i.i.d. collection with law (1.1). For both lattice and Poisson models, we write

where the inequality holds by Lemma 5.2, and we use that the are independent of the location of . Recall that for lattice models, equals the number of points on the integer lattice of and for Poisson models, is a Poi()-distributed random variable. Recalling from (3.1) and using (3.3) we deduce that, for Poisson models,

From this it is clear that to prove the lemma for both lattice and Poisson models, it suffices to show that, for all ,

| (5.18) |

where is any deterministic sequence satisfying . To prove (5.18), define the truncated random variable . The Chernoff bound gives us that, for all ,

Let , for a constant to be chosen later. By the Taylor expansion of ,

| (5.19) |

where converges to zero as tends to infinity. We start by investigating the third term in (5.19). We choose constants such that for all . Thus, for sufficiently large ,

| (5.20) |

where the second inequality holds since

and . Note that is -bounded for . Thus we can choose such that and

where the last step holds since and converges to as increases, so . Next, note that

Plugging in , we get that, for some constant ,

For , we get and so, by (5.20),

| (5.21) |

as . From (5.21) it follows that

Putting everything together, it follows that

using that , and . Choosing and such that is satisfied, we obtain that which concludes the proof of (5.18). ∎

Next, we investigate the asymptotic behaviour of .

Lemma 5.7.

Proof.

We prove the lemma first for lattice models. Recall that is the cube of volume centred at . Embedding the torus around into the integer lattice and recalling the definition of , we write

| (5.22) |

By (1.6), for every ,

where the is uniform in . This term therefore converges to

The fact that together with the dominated convergence theorem implies that, for every ,

as . From this it also follows that the second summand in (5.3) converges to zero, concluding the proof for lattice models. The proof for Poisson models follows similarly and is therefore omitted. ∎

In the next lemma, we investigate the contribution of the macroscopic weights.

Lemma 5.8.

For all non-integers , with and for all ,

Proof.

For Poisson models, we observe that

| (5.23) |

recalling from (3.1) and using the bound (3.3). To prove the lemma for Poisson models it therefore suffices to show that for and sufficiently large ,

Note that, for , is independent of the location of for lattice and Poisson models. Therefore in order to prove Lemma 5.8 for both models, it suffices to show that

| (5.24) |

for an i.i.d. collection having law (1.1), where is any deterministic sequence satisfying . Thus for the rest of the proof, we work with such a sequence.

Let and define the events for as

| (5.25) |

We can write

Let . Then, using the fact that are i.i.d., we remark that

for sufficiently large , because deterministically and so . Next, we note that, by a union bound of the at least vertices with weight larger than ,

Since have law (1.1), this equals . Therefore,

| (5.26) |

It remains to study

Observe that since , using . By a change of variables , we can write the last expression as

since . By Lemma 5.7 and dominated convergence, the last expression is asymptotically equivalent to . ∎

Now we are ready to prove Proposition 5.3.

Proof of Proposition 5.3.

The following proof holds for both lattice and Poisson models. Recall the definition of given in Lemma 5.8 and recall that we write for . Let . Fix and such that , and such that

| (5.27) |

By Lemma 5.6 such choices are possible. A lower bound then easily follows using Lemma 5.8, by observing

| (5.28) | ||||

since . Thus,

The desired lower bound in Proposition 5.3 follows by letting and using monotone convergence. To establish an upper bound, we write

| (5.29) | |||

where the equality follows from (5.27) and Lemma 5.8 and the last inequality holds since . Therefore,

The desired upper bound follows by first letting , and then letting and using the continuity of on the interval .∎

6. Bulk in edge-length distribution: Proof of Proposition 2.5

Proof of Proposition 2.5.

We need to show that

Let be such that . Then

Since for sufficiently large, Proposition 3.1 implies that

Therefore it suffices to show that

We bound , and

so that we are left to show that

We first condition on the number of nodes and then consider the event , which indicates that the number of points in each each cube of length is inside the interval . Recall that for sufficiently large, (see (3.7)). Hence, it is enough to study the sum under the event . Recall that on this event,

see (3.23). Hence, we can bound

We now consider

Conditioned on , the sum is just a random variable. Now we condition on the event that , which happens with probability for large enough by (3.3). Then, on this event, for sufficiently large. Hence, an application of Hoeffding’s inequality yields that (writing )

Since the last term is bounded by on the event , we conclude that, for sufficiently large,

which is what we needed to show. ∎

7. Travelling wave in edge-length distribution: Proof of Proposition 2.6

Our proof strategy is to show that the edges of macroscopic length are those in and the form of the condensate emerges from the fact that originates from uniform vertices that all have weight of order . The total mass, that is at least , of these corresponds to edges with length of order . For the proof, we rely on the proofs of the previous sections.

To make the intuition outlined above precise, define the function by

| (7.1) |

Fix . Define the vertex set as the intersection of and the annulus centred at . Write for . Remark that for all , for the lattice case, we have that , while for the Poisson case, is Poisson distributed with mean . Recall that is the order statistic of the weights . For , recall that denotes the random vertex with the largest weight, i.e., . Define , to be the set of locations of the first largest weight vertices. Remark that to prove Proposition 2.6, it suffices to prove the statement for , for any satisfying . For , define as

| (7.2) |

where , defined in (1.9).

Recall that denotes the probability conditioned on having a point at .

Lemma 7.1.

Let and . For both lattice and Poisson models,

| (7.3) |

where the convergence is in probability with respect to conditionally on .

Proof of Lemma 7.1.

Fix throughout the proof. We begin by proving the lemma for the lattice case. Representing the neighbourhood of by with mapped to the origin, we get . Conditionally on , we note that are independent Bernoulli- distributed random variables. Using standard concentration arguments (see e.g. [17, Theorem 2.8.]), it suffices to show that as . We write

| (7.4) |

By a slight modification of Lemma 5.7, working with instead of , we get that

since . We can further conclude by the dominated convergence theorem that

The proof for the Poisson case is of a similar flavour. First note that given and the weight , the locations and the weights of the vertices contributing to are distributed as a Poisson point process on with intensity

| (7.5) |

This implies that given and the weight , the sum is a Poisson random variable with parameter

This is an analogue of Lemma 5.4 and we omit the proof as it is a simple adaptation of the proof of [15, Lemma 2.1]. Using Poisson concentration arguments [17, Remark 2.6], it suffices to prove that the mean of the Poisson random variable (7.5) converges to the right-hand side of (7.3). Just as in the lattice case, this follows from a modified version of Lemma 5.7, using that . We omit the details. ∎

Lemma 7.2.

Proof.

The following proof holds for both lattice and Poisson models. Let . A union bound gives that

| (7.6) |

We will show that, for any , the summand of the right-hand side above is . To be able to apply Lemma 7.1 requires still some work since the summand above conditions on the highest weights instead of on . Fix and recall . Using the triangle inequality we can upper bound the summand by

| (7.7) | |||

| (7.8) |

Note that the second summand equals zero for sufficiently large since we have the deterministic bound . Therefore it remains to show that the first summand (7.7) tends to zero as tends to infinity. The fact that the weights are independent and that the random variable only depends on the locations and weights , gives that, for ,

| (7.9) | |||

| (7.10) |

Similarly, we can lower bound (7.9) by

| (7.11) |

Thus, for sufficiently large , (7.7) can be bounded from above by

for some such that . Observing that the location of the vertex is just a uniformly chosen (lattice) point in , the above equals

| (7.12) |

Note that

and recall that for lattice models and is -distributed for Poisson models. Using the distribution of given by (1.1), we have for . We can conclude that (7.7) tends to zero by applying Lemma 7.1 to the first factor of (7.12). ∎

Corollary 7.3.

Proof.

By Theorem 1.1, it suffices to show that, for all

Let and recall from (5.25). We begin by noting that

By Lemma 7.2, the last line is . Using the density of and the fact that are i.i.d., we get that . Next, remark that

The last line equals by the bound (2.5) combined with Propositions 2.1, 2.2 and inequalities (5.11) and (5.26). ∎

Finally, we have all the tools to prove Proposition 2.6.

Proof of Proposition 2.6.

It is enough to prove the statement for , where . For this choice of , it holds that

By Corollary 7.3 it therefore suffices to prove that, conditionally on ,

| (7.13) |

Remark that

We can rewrite the double sum as

| (7.14) | |||

Further, bounding from above by one, we get that , which vanishes as increases. Putting everything together, in order to prove (7.13) we must show that, conditionally on ,

| (7.15) |

First, remark that , since for sufficiently large . Thus, Proposition 2.2 and Theorem 1.1 give that, for all ,

Further, by a slightly modified version of the upper bound (5.11) together with Lemma 5.6,

Lastly,

where the equality follows from the proof of Lemma 5.8. By (7), combining the above three bounds concludes the proof of (7.15). ∎

8. Limit for the weight order statistics: Proof of Proposition 2.7

Proof of Proposition 2.7.

Fix positive reals . Similar to the definition (5.25), define the event

| (8.1) |

To prove Proposition 2.7 for lattice and Poisson models, we will show that

| (8.2) |

By the proof of Theorem 1.1, it suffices to show that equals the right-hand side of (8.2) in order to conclude (8.2). Following the proof of (5.11) and using Lemma 5.1, we can deduce that, for small and sufficiently large ,

and

Combining (5.28) and (5.29) together with slight variants of Lemma 5.6 and the proof of Lemma 5.8, we can see that (8.2) follows if we can prove that equals the right-hand side of (8.2). We begin to prove this for lattice models. Note that

where is the falling factorial. By the change of variables for all , the above equals up to a factor,

since in the lattice case. Using Lemma 5.7, we conclude that

and so Proposition 2.7 follows. The proof for Poisson models follow by conditioning on the number of points and using that is a -distributed random variable. More precisely, recall given by (3.1) for , and note that for a given inverse power of , we can choose a sufficiently large such that tends to zero faster than this inverse power as . Thus,

The remainder of the proof follows straightforwardly and is omitted. ∎

9. The empirical degree distribution: Proof of Proposition 2.9

We begin the proof of Proposition 2.9(i) by following that of Proposition 2.6 in Section 7. For lattice and Poisson models, recall that Lemma 7.1 holds when we take the sum over all of , that is for and . This gives, for , and conditionally on , that

| (9.1) |

where the convergence is in probability with respect to . By adapting the proof of Lemma 7.2, starting from (7.6) and summing again over all of , we can show that, conditionally on the event for ,

| (9.2) |

Next, to show Proposition 2.9(ii), we use a second-moment method. Let be two independent uniformly chosen random vertices in . For we define

where, in the lattice case, we project to the nearest lattice point. Recall (1.20). We can write

| (9.3) |

We now first focus on the lattice case. For distinct points , we define

Then (9.3) can be written as

since on the event that and are not high-weight vertices, with high probability they do not share an edge. To see this, note that the weights of the vertices in are independent copies of a variable having the conditional law of the weights in (1.1) conditionally on , and their locations are distributed as the locations of with uniformly random vertices removed. In particular, the probability that and share an edge on the event that they are not in , equals up to an asymptotically negligible error, the probability that two random vertices share an edge in the graph where each vertex in now has an independent copy of the weight , instead of . The latter probability goes to zero using Assumption A and a straightforward calculation.

Next, for convenience, let us introduce the notation for and to denote the number of edges connecting the vertex to the set in the graph . Recall that stands for the set . Then

| (9.4) |

By conditioning on the weights and , and using the conditional independence of the events,

| (9.5) |

Recall that denotes the degree of the root of the local limit of the unconditional graph given that the weight of the root is . We claim that, for fixed and with

we have

| (9.6) |

To prove (9.6), as observed earlier, we recall that the weights of vertices in are independent copies of a variable having the conditional law of the weights in (1.1) conditionally on . We now show how to use this observation to couple the graph , conditionally on , with an unconditional geometric random graph where the weights are i.i.d. copies of . Sample independent copies of for every vertex in and, given the weights, edges between pairs of distinct vertices using the connection function . The graph is formed using these edges. For the conditional graph , we modify the weights of the vertices to be , for all , and resample (only) the edges adjacent to using these weights.

Note that the graph has the same local limit as the original unconditioned graph (with weights of law ) since as , and using the fact that the local limit is preserved under removal of a finite set of vertices. Therefore the degree of in , given , converges in distribution to . We also observe that with high probability the vertex has distance of order from the locations of the vertices in . Hence, with high probability, does not share an edge with the vertices at and the degree of in is the same as its degree in the subgraph of , induced by the vertices . Since in our coupling, these induced subgraphs of and match, we obtain that in fact . This proves (9.6).

Define We analyse the asymptotic behaviour of . In the conditioned graph , we can write where the random variables are independent and Bernoulli distributed with parameter . Using that is continuous almost everywhere, we get

| (9.7) |

where is uniformly distributed on . The random variables therefore converge in distribution to conditionally independent Bernoulli random variables with parameter given . Therefore,

Note that and converge in distribution to two independent copies and of the pair with a Pareto-distributed random variable and an independent uniform variable . As are continuous and bounded,

converges to

Combining the above with (9.3) and (9.5) gives

The above computations also imply that

Hence the variance of vanishes asymptotically and an application of Chebyshev’s inequality finishes the proof of Proposition 2.9(ii) for the lattice case. The Poisson case is analogous using that removing finitely many randomly chosen vertices from the Poisson point process leaves its law intact.

We next prove Proposition 2.9(iii), that is, for each . By the coupling of the conditional graph and the unconditional graph , for ,

Let be the maximum of i.i.d. random variables with law (1.1). Then, for there is such that . In we have and thus

where has law (1.1) and is a random uniform point in , and where the inequality holds since is increasing and decreasing.By Lemma 3.4 we can bound the above by a constant multiple of . This vanishes as tends to infinity, concluding the proof of Proposition 2.9(iii).

Concluding remarks on local limits.

Note that the proof of Proposition 2.9 shows that the subgraph of the conditional graph given induced by removing the vertices with the highest weights has a local limit which equals the unconditional local limit of . The local limit of the conditional graph given itself, however, does not exist. This is because with asymptotically positive probability a randomly sampled vertex connects to one of the high-weight vertices, and as these vertices have infinite degree in the limit, the two-neighbourhood of a randomly sampled vertex becomes infinite with positive probability. However, one can still give a local description of the conditional graph, which we now describe informally.

Sample a random vertex in the conditional graph. With high probability, it is not one of the high-weight vertices. Now start exploring the neighbourhood of this vertex in some order, e.g., the depth-first order. At every step of the exploration, when we discover an incidence to one of the high-weight vertices, we stop exploring from that vertex, and go back to the last visited vertex to restart exploring from there. In particular, this method of exploration avoids discovering the ‘forward’ neighbours of a high-weight vertex, of which there are linearly many, as we have seen. This ‘restricted’ exploration can be formalized easily, which we omit to keep the discussion informal. Now, say we explore the conditional graph in this fashion, and look at the set of explored vertices that are at graph distance from , and call this explored graph . Then, , rooted at , for any fixed , converges in the local (Benjamini-Schramm) topology (see [13, Chapter 2]) to the graph , whose construction we describe next.

We briefly describe the local limit of the unconditional graph . The vertex set of is the corresponding infinite vertex set - the infinite integer lattice in the lattice case and the Palm version of a standard Poisson process on in the Poisson case. Then the weight for each vertex is sampled as an independent random variable with density (1.1), and conditionally on the weights and locations, edges are placed independently between vertex pairs with probability (1.2). The graph is rooted at .

Now we describe the graph . Let be the graph neighbourhood of radius about in . Let the weights of the vertices in be . Note that the are not i.i.d., since the weights are tilted due to the fact that they are in the -neighbourhood of , and the precise law of is rather involved. The construction of the graph is as follows.

-

Append extra vertices, say , to and call the new vertex set .

-

The vertices have marks , where the first coordinates are i.i.d. uniform points of independent of , and the second coordinates have joint distribution (1.16).

-

Given the variables sampled above, we place an edge between each vertex of and each independently, with probability Denote the new edge set by .

-

The graph has vertex set and edge set .

This description gives a way to compute the typical distance (graph distance between two randomly sampled vertices) in the conditional graph : Independently sample two random vertices and in . Start exploring in the fashion described above from both and , and let (resp., ) be the distance from (resp., ) up to which one has to explore to see a high-weight vertex. Denote by the set of high-weight vertices exactly at graph distance from , for . Recalling from Remark 2.8 that the high-weight vertices form a clique, we note that the graph distance from to in the conditional graph is with high probability. This quantity as a sequence in is in fact a tight sequence of random variables - starting from a random vertex in the conditional graph, one finds a high-weight vertex within tight graph distance from it.

Acknowledgements

CK and PM are supported by DFG project 444092244 “Condensation in random geometric graphs” within the priority programme SPP 2265. The work of RvdH is supported in part by the Netherlands Organisation for Scientific Research (NWO) through Gravitation-grant NETWORKS-024.002.003.

References

- Adams and Dickson [2021] S. Adams and M. Dickson. An explicit large deviation analysis of the spatial cycle Huang–Yang–Luttinger model. Annales Henri Poincaré, 22(5):1535–1560, 2021.

- Berestycki and Yadin [2019] N. Berestycki and A. Yadin. Condensation of a self-attracting random walk. Ann. Inst. Henri Poincaré, Probab. Stat., 55(2):835 – 861, 2019.

- Betz and Ueltschi [2009] V. Betz and D. Ueltschi. Spatial random permutations and infinite cycles. Comm. Math. Phys., 285(2):469–501, 2009.

- Chatterjee and Harel [2020] S. Chatterjee and M. Harel. Localization in random geometric graphs with too many edges. Ann. Probab., 48(2):574 – 621, 2020.

- Combes [2015] R. Combes. An extension of McDiarmid’s inequality. Preprint arXiv:1511.05240, 2015.

- Deijfen et al. [2013] M. Deijfen, R. van der Hofstad, and G. Hooghiemstra. Scale-free percolation. Ann. Inst. Henri Poincaré, Probab. Stat., 49:817 – 838, 2013.

- Deprez and Wüthrich [2019] P. Deprez and M. V. Wüthrich. Scale-free percolation in continuum space. Communications in Mathematics and Statistics, 7(3):269–308, 2019.

- Dickson and Vogel [2021] M. Dickson and Q. Vogel. Formation of infinite loops for an interacting bosonic loop soup. arXiv preprint arXiv:2109.01409, 2021. doi: 10.48550/arXiv.2109.01409.

- Evans and Majumdar [2008] M. R. Evans and S. N. Majumdar. Condensation and extreme value statistics. J. Stat. Mech., 2008(05):P05004, 2008.

- Gracar et al. [2019] P. Gracar, A. Grauer, L. Lüchtrath, and P. Mörters. The age-dependent random connection model. Queueing Systems, 93(3):309–331, 2019.

- Gracar et al. [2021] P Gracar, L Lüchtrath, and P Mörters. Percolation phase transition in weight-dependent random connection models. Adv. Appl. Probab., 53(4):1090–1114, 2021.

- Gracar et al. [2022] P. Gracar, M. Heydenreich, C. Mönch, and P. Mörters. Recurrence versus transience for weight-dependent random connection models. Elect. J. Probab., 27:1–31, 2022.

- van der Hofstad [2024] R van der Hofstad. Random Graphs and Complex Networks, Volume 2. Cambridge University Press, 2024.

- van der Hofstad et al. [2023a] R van der Hofstad, P van der Hoorn, and N Maitra. Local limits of spatial inhomogeneous random graphs. Adv. Appl. Probab., page 1–48, 2023a.

- van der Hofstad et al. [2023b] R van der Hofstad, P van der Hoorn, and N Maitra. Scaling of the clustering function in spatial inhomogeneous random graphs. J. Stat. Phys., 190(6):110, 2023b.

- Janson [2012] S. Janson. Simply generated trees, conditioned Galton–Watson trees, random allocations and condensation. Probability Surveys, 9:103 – 252, 2012.

- Janson et al. [2000] S. Janson, T. Łuczak, and A. Rucinski. Random graphs. Wiley-Interscience Series in Discrete Mathematics and Optimization. Wiley-Interscience, New York, 2000.

- Jorritsma et al. [2023] J. Jorritsma, J. Komjáthy, and D. Mitsche. Cluster-size decay in supercritical kernel-based spatial random graphs, 2023.

- Kerriou and Mörters [2022] C. Kerriou and P. Mörters. The fewest-big-jumps principle and an application to random graphs. Preprint arXiv:2206.14627, 2022.

- Last and Penrose [2018] G. Last and M. Penrose. Lectures on the Poisson process. Cambridge University Press, 2018.

- Malyshev and Yakovlev [1996] V. A. Malyshev and A. V. Yakovlev. Condensation in large closed Jackson networks. Ann. Appl. Probab., 6(1):92 – 115, 1996.

- McDiarmid [1989] C. McDiarmid. On the method of bounded differences, page 148–188. London Mathematical Society Lecture Note Series. Cambridge University Press, 1989. doi: 10.1017/CBO9781107359949.008.

- Quitmann and Taggi [2023] A. Quitmann and L. Taggi. Macroscopic loops in the Bose gas, spin O(N) and related models. Comm. Math. Phys., 400(3):2081–2136, 2023.

- Rafferty et al. [2018] T. Rafferty, P. Chleboun, and S. Grosskinsky. Monotonicity and condensation in homogeneous stochastic particle systems. Ann. Inst. Henri Poincaré, Probab. Stat., 54(2):790–818, 2018.

- Smith and Majumdar [2022] N. R. Smith and S. N. Majumdar. Condensation transition in large deviations of self-similar gaussian processes with stochastic resetting. J. Stat. Mech., 2022(5):053212, 2022.

- Stegehuis and Zwart [2023] C. Stegehuis and B. Zwart. Scale-free graphs with many edges. Elect. Comm. Probab., 28:1 – 11, 2023. doi: 10.1214/23-ECP567. URL https://doi.org/10.1214/23-ECP567.

- Stoyan et al. [2013] D. Stoyan, W. Kendall, and J. Mecke. Stochastic Geometry and its Applications. Wiley, 2013.

- Ueltschi [2006] D. Ueltschi. Feynman cycles in the Bose gas. J. Math. Phys., 47(12):123303, 2006.