A Geometric Unification

of Distributionally Robust Covariance Estimators:

Shrinking the Spectrum by Inflating the Ambiguity Set

Abstract.

The state-of-the-art methods for estimating high-dimensional covariance matrices all shrink the eigenvalues of the sample covariance matrix towards a data-insensitive shrinkage target. The underlying shrinkage transformation is either chosen heuristically—without compelling theoretical justification—or optimally in view of restrictive distributional assumptions. In this paper, we propose a principled approach to construct covariance estimators without imposing restrictive assumptions. That is, we study distributionally robust covariance estimation problems that minimize the worst-case Frobenius error with respect to all data distributions close to a nominal distribution, where the proximity of distributions is measured via a divergence on the space of covariance matrices. We identify mild conditions on this divergence under which the resulting minimizers represent shrinkage estimators. We show that the corresponding shrinkage transformations are intimately related to the geometrical properties of the underlying divergence. We also prove that our robust estimators are efficiently computable and asymptotically consistent and that they enjoy finite-sample performance guarantees. We exemplify our general methodology by synthesizing explicit estimators induced by the Kullback-Leibler, Fisher-Rao, and Wasserstein divergences. Numerical experiments based on synthetic and real data show that our robust estimators are competitive with state-of-the-art estimators.

1. Introduction

The covariance matrix of a random vector is a fundamental summary statistic that captures the dispersion of . Together with the mean vector , it characterizes a unique member of the family of Gaussian distributions, which occupies the central stage in statistics and probability theory. Hence, any probabilistic model involving Gaussian distributions requires an estimate of as an input. For example, Gaussian distributions are ubiquitous in finance (e.g., in portfolio theory [41]), in statistical learning (e.g., in linear and quadratic discriminant analysis [20, § 4.3]) or control and signal processing (e.g., in Kalman filtering [25]). In addition, is intimately related to the correlation matrix, including the Pearson correlation coefficients [48], and it permeates medical statistics [60] and correlation network analysis [13, 40] etc.

If the distribution of is known, then the mean vector and the covariance matrix can be obtained by evaluating the relevant integrals with respect to —either analytically or via numerical integration quadratures. If is unknown, however, one typically has to estimate and from independent samples . Arguably the simplest estimators for and are the sample mean and the sample covariance matrix , respectively. An elementary calculation shows that is unbiased. Up to scaling, further coincides with the maximum likelihood estimator for provided that constitutes a normal distribution. In 1975, much to the surprise of statisticians, Charles Stein showed that one can strictly reduce the mean squared error of by shrinking it towards a constant matrix independent of the data [23, 57]. Even though it improves the mean squared error, Stein’s shrinkage transformation suffers from two major shortcomings, that is, it may alter the order of the estimator’s eigenvalues and may even render some eigenvalues negative [51]. Nonetheless, since Stein’s surprising discovery, the study of shrinkage estimators embodies an important research area in statistics.

Note also that is ill-conditioned if and even singular if [63]. Indeed, as is unbiased and as the maximum eigenvalue function is convex on the space of symmetric matrices, Jensen’s inequality ensures that the largest eigenvalue of exceeds, in expectation, the largest eigenvalue of . Similarly, the smallest eigenvalue of undershoots, in expectation, the smallest eigenvalue of . Hence, the condition number of , defined as the ratio of its largest to its smallest eigenvalue, tends to exceed the condition number of . This effect is most pronounced if is (approximately) proportional to the identity matrix and is exacerbated with increasing dimension . A simple and effective method to improve the condition number is to construct a linear shrinkage estimator by forming a convex combination of and a data-insensitive shrinkage target such as [32]. Other popular shrinkage targets include the constant correlation model [31], that is, a modified sample covariance matrix under which all pairwise correlations are equalized, the single index model [30], that is, the sum of a rank-one and a diagonal matrix representing systematic and idiosyncratic risk factors as in Sharpe’s single index model [56], and the diagonal matrix model [61], that is, the diagonal matrix that contains all sample eigenvalues on its main diagonal. The shrinkage weight of is usually tuned to minimize the Frobenius risk, that is, the expected squared Frobenius norm distance between the estimator and . Linear shrinkage estimators can be computed highly efficiently, improve the condition number of the sample covariance matrix, and are guaranteed to have full rank even if .

In the remainder of the paper, we focus on covariance estimators that depend on the samples only indirectly through the sample covariance matrix. This assumption is unrestrictive. Indeed, it is satisfied by all commonly used covariance estimators. Moreover, it comes at no loss of generality if is a normal distribution, in which case constitutes a sufficient statistic for . Without prior information about the eigenvectors of , it is natural to restrict attention to rotation equivariant estimators. Rotation equivariance means that evaluating the estimator on the rotated dataset is equivalent to evaluating the rotated estimator on the the original dataset for any rotation matrix . One can show that any rotation equivariant estimator commutes with the sample covariance matrix , that is, and share the same eigenvectors, and the spectrum of can be viewed as a transformation of the spectrum of [49, Lemma 5.3]. Such spectral transformations are referred to as a shrinkage transformations. Note that the linear shrinkage estimators discussed above are rotation equivariant only if the shrinkage target commutes with .

If is governed by a spiked covariance model, that is, if is Gaussian, and tend to infinity at an asymptotically constant ratio and constitutes a fixed-rank perturbation of the identity matrix, then one can use results from random matrix theory to construct the best rotation equivariant estimators in closed form for a broad range of different loss functions [12]. Nonlinear shrinkage estimators that are asymptotically optimal with respect to the Frobenius loss can also be constructed in the absence of any normality assumptions, and they can significantly improve on linear shrinkage estimators if the eigenvalue spectrum of is dispersed [33, 35]. Similarly, one can construct optimal shrinkage estimators for the inverse covariance matrix , which is usually termed the precision matrix; see [8, 36]. However, the available statistical guarantees for all shrinkage estimators described above are asymptotic and depend on assumptions about the structure of and/or the convergence properties of the spectral distribution of , which may be difficult to check in practice.

In this paper, we propose a flexible and principled approach to estimate the covariance matrix by using ideas from distributionally robust optimization (DRO). Specifically, our approach generates a rich family of covariance matrix estimators corresponding to different ambiguity sets that can encode prior distributional information. All emerging estimators are rotation equivariant and thus represent nonlinear shrinkage estimators. In addition, they all improve the condition number of the sample covariance matrix, are invertible, and preserve the order of the sample eigenvalues. They also offer finite sample guarantees on the prediction loss and are asymptotically consistent. These appealing properties are not enforced ad hoc but emerge naturally from the solution of a principled distributionally robust estimation model. We emphasize that our results do not rely on any restrictive assumptions such as the requirement that is Gaussian or that the spectral distribution of converges to a well-defined limit as and tend to infinity at a constant ratio.

To develop the distributionally robust estimation model to be studied in this paper, we first express the unknown true covariance matrix as the minimizer of a stochastic optimization problem involving the unknown probability distribution . Specifically, adopting the standard assumption that [32, 33, 34, 36] and noting that the squared Frobenius norm is strictly convex, we obtain

If we could solve the stochastic optimization problem on the right-hand side of the above expression, we could precisely recover the ideal estimator . This is impossible, however, because the distribution needed to evaluate the stochastic optimization problem’s objective function is unknown. Nevertheless, replacing with a nominal distribution constructed from the training samples yields the nominal estimation model

| (1) |

which requires no unavailable inputs. An elementary calculation shows that (1) is uniquely solved by , which is the covariance matrix of under the nominal distribution , provided that . Of course, characterizing as a minimizer of (1) has no conceptual or computational benefits because we have to compute the integral already to evaluate the objective function of (1). Nevertheless, the nominal estimation problem (1) is useful because it allows us to construct a broad range of nonlinear shrinkage estimators in a principled and systematic manner by robustifying the prediction loss.

Any nominal distribution constructed from a finite dataset must invariably differ from the true data-generating distribution . Estimation errors in are conveniently captured by an ambiguity set of the form

| (2) |

where indicates that has mean and covariance matrix under , and represents a divergence on the space of positive semidefinite matrices. Divergences are general distance-like functions that are non-negative and satisfy the identity of indiscernibles (that is, they satisfy if and only if ). However, divergences may fail to be symmetric and may violate the triangle inequality. Intuitively, can be viewed as a divergence ball of radius around in the space of probability distributions. Robustifying the nominal estimation problem (1) against all distributions in yields the following DRO problem.

| (3) |

Problem (3) seeks an estimator that minimizes the worst-case expected prediction loss across all distributions in . Note that if , then the DRO problem (3) collapses to the nominal estimation problem (1) because the divergence satisfies the identity of indiscernibles, which ensures that . Hence, (3) embeds (1) into a family of estimation models parametrized by and . Moreover, DRO models naturally bridge optimization and statistics in that they offer an intuitive way to derive generalization bounds. Indeed, if is tuned to ensure that contains the data-generating distribution with high confidence , then the optimal value of the DRO problem (3) provides a -upper confidence bound on the prediction loss of its unique minimizer under [42]. Stronger generalization bounds that do not require to belong to are provided in [7, 15]. Even if the ambiguity set does not contain , DRO models tend to yield high-quality solutions because there is a deep connection between robustification and regularization [16, 53, 54]. This connection may also explain the empirical success of DRO in statistical estimation [6, 27, 59].

The flexibility to choose the divergence underlying the ambiguity set is both a blessing and a curse. On the one hand, can encode prior distributional information and thus lead to better estimators. On the other hand, the family of divergences is vast. Hence, the choice of a suitable instance could overwhelm the modeler. Given the statistical estimation task at hand, it makes sense to restrict attention to divergences that admit a statistical interpretation. Many popular divergences on the space of covariance matrices are obtained by restricting a divergence on the space of probability distributions to the family of normal distributions. For example, the Kullback-Leibler divergence, the 2-Wasserstein distance, or the Fisher-Rao distance between zero-mean normal distributions all admit closed-form formulas in terms of the distributions’ covariance matrices. These ‘Gaussian’ divergences are popular because they are conducive to tractable DRO models in risk management [17, 44], ethical machine learning [10, 66], likelihood evaluation [46, 47], Kalman filtering [71, 55] and control [58] etc. In addition, the shrinkage estimator for the inverse covariance matrix proposed in [43] also leverages a ‘Gaussian’ divergence. Nonetheless, the approach proposed in this paper does not rely on the assumption that is Gaussian.

The main contributions of this paper can be summarized as follows.

-

•

We propose a rich family of distributionally robust covariance matrix estimators. Each estimator is defined as a solution of (3) for a particular ambiguity set of the form (2). Here, the nominal covariance matrix characterizes the center, the divergence determines the geometry, and the radius determines the size of the ambiguity set. We demonstrate that all such estimators are well-defined, unique and efficiently computable under natural structural assumptions on and mild regularity conditions on and .

-

•

We prove that our distributionally robust covariance matrix estimators constitute nonlinear shrinkage estimators, that is, they have the same eigenbasis as , and their eigenvalues are obtained by shrinking the spectrum of towards by using a nonlinear shrinkage transformation depending on and a shrinkage intensity depending on . We further prove that these estimators improve the condition number of .

-

•

We identify various divergences commonly used in statistics, machine learning and information theory that satisfy the requisite regularity conditions. To this end, we generalize Sion’s classic minimax theorem from Euclidean spaces to Riemannian manifolds, which could be of independent interest. We also exemplify our framework by deriving explicit analytical formulas for the distributionally robust covariance estimators induced by the Kullback-Leibler divergence, the 2-Wasserstein distance and the Fisher-Rao distance.

-

•

We prove that, if scales with the sample size as , then the proposed estimators are strongly consistent and enjoy finite-sample performance guarantees at a fixed confidence level. Numerical experiments based on synthetic as well as real data for portfolio optimization and binary classification tasks suggest that our robust estimators are competitive with state-of-the-art estimators from the literature.

The first robustness interpretation of a shrinkage estimator was discovered in the context of inverse covariance matrix estimation [43]. Specifically, it was shown that a particular nonlinear shrinkage estimator can be obtained by robustifying the maximum likelihood estimator for across all Gaussian distributions of the training samples within a prescribed Wasserstein ball. This result critically relies on the restrictive assumption that the unknown data-generating distribution, the nominal distribution as well as all other distributions in the Wasserstein ball are Gaussian. In addition, this result has not been extended to more general ambiguity sets based on other divergences beyond the 2-Wasserstein distance, thus limiting the modeler’s flexibility.

In this paper we show that a broad spectrum of shrinkage estimators for can be obtained from a versatile DRO model that does not rely on restrictive normality assumptions. That is, we seek the most general conditions on the DRO model under which a shrinkage effect emerges. In addition, we uncover a deep connection between the geometry of the ambiguity set, which is determined by the choice of the divergence , and the nonlinear shrinkage transformation of the corresponding distributionally robust estimator.

Notation. We use as a shorthand for the extended real line. The space of -dimensional real vectors and its subsets of (entry-wise) non-negative and positive vectors are denoted by , , and , respectively. Similarly, the space of symmetric matrices in , as well as its subsets of positive semidefinite and positive definite matrices, are denoted by , , and , respectively. The group of orthogonal matrices in is denoted by , and stands for the identity matrix in . For any , we use and to denote the vectors obtained by rearranging the entries of in non-increasing and non-decreasing order, respectively. The trace of a matrix is defined as . Finally, and stand for the spectral norm and the Frobenius norm of , respectively.

2. Overview of Main Results

The distributionally robust estimation problem (3) perturbs—and thereby hopefully improves—the nominal estimator in view of the divergence . We now derive a simple reformulation of (3) as a standard minimization problem, and we informally outline the main properties of the corresponding optimal solution, which will be established rigorously in the remainder of the paper. From now on, the nominal covariance matrix can be viewed as any naïve initial estimator for the covariance matrix . The construction of from the samples is immaterial for most of our discussion. As the loss function underlying problem (3) is quadratic in and as , its expected value depends on only indirectly through the covariance matrix . Thus, the DRO problem (3) is equivalent to the robust covariance estimation problem

| (4) |

with uncertainty set

| (5) |

We stress that the divergence function may fail to be symmetric, that is, may differ from . It is therefore important to remember the convention that is the second argument of in the definition of . Note also that grows with the size parameter and collapses to the singleton for . The robust estimation problem (4) constitutes a zero-sum game between the statistician, who moves first and chooses the estimator , and nature, who moves second and chooses the covariance matrix . The following dual estimation problem is obtained by interchanging the order of minimization and maximization in (4).

| (6) |

From now on, we denote by and the optimal solutions of the primal and dual estimation problems (4) and (6), respectively. In Section 3.1 below, we will identify mild conditions on and under which and are indeed guaranteed to exist and to be unique. If the uncertainty set is convex and compact, then strong duality prevails (that is, (4) and (6) share the same optimal value) by Sion’s classic minimax theorem. As several popular divergence functions are non-convex in their first argument and thus induce a non-convex uncertainty set ; however, we will develop a generalized minimax theorem that guarantees strong duality under significantly more general conditions. Whenever strong duality holds, constitutes a Nash equilibrium of the zero-sum game between the statistician and nature [52, Lemma 36.2].

A cursory glance at its first-order optimality condition reveals that the inner minimization problem in (6) is solved by . Hence, the inner minimum evaluates to . Eliminating the factor further shows that solves the maximization problem (6) if and only if it solves the minimization problem

| (P) |

Thus, nature’s Nash strategy can be computed by solving (P) instead of (6). By the defining properties of Nash strategies, the statistician’s Nash strategy must be a best response to , that is, must solve the inner minimization problem in (6) for . However, the unique optimal solution of this minimization problem is . In summary, this reasoning implies that if strong duality holds, then the Nash strategies and of the statistician and nature coincide and are both given by the unique minimizer of problem (P).

Problem (P) is reminiscent of a ridge regression problem [21, 64], which seeks an estimator that minimizes a weighted sum of a least squares fidelity term and a Frobenius norm regularization term. Indeed, problem (P) seeks a covariance matrix with minimum Frobenius norm and a fidelity error of at most , where the fidelity of with respect to the nominal covariance estimator is measured by the divergence .

| Divergence function | Domain | |

|---|---|---|

| Kullback-Leibler / Stein [28] | ||

| Wasserstein [18] | ||

| Fisher-Rao [3] | ||

| Inverse Stein [28] | ||

| Symmetrized Stein / Jeffreys divergence [24] | ||

| Quadratic / Squared Frobenius | ||

| Weighted quadratic |

We now informally state our key result, which applies, among others, to all divergence functions of Table 1.

Theorem 1 (Distributionally robust estimator (informal)).

If is any divergence functions from Table 1, the nominal covariance matrix satisfies a regularity condition, and is not too large, then the distributionally robust estimator exists, is unique, and can be computed efficiently via the following procedure.

-

(1)

Compute the eigenvalues and the eigenvectors of the nominal covariance matrix .

-

(2)

Construct the inverse shrinkage intensity by solving a univariate nonlinear equation that depends only on the spectrum of .

-

(3)

Shrink the eigenvalues of by applying a nonlinear transformation that depends only on .

-

(4)

Construct by combining the eigenvectors found in step (1) with the eigenvalues found in step (3).

The estimator constructed in this manner preserves the eigenvectors of , shrinks the eigenvalues of , and reduces the condition number of . Thus, it represents a nonlinear shrinkage estimator.

Theorem 1 reveals that a wide range of nonlinear shrinkage estimators admit a robustness interpretation in the sense that they correspond to solutions of the distributionally robust estimation problem (3) for different divergence functions. This insight is of interest from a statistical point of view because it relates nonlinear shrinkage estimators to distributional ambiguity sets, which can be used to derive new generalization bounds. Theorem 1 also implies that the distributionally robust estimation problem (3) can be solved efficiently by diagonalizing and solving a univariate nonlinear equation, both of which are computationally cheap.

3. Distributionally Robust Covariance Shrinkage Estimators

This section formally introduces our distributionally robust estimation framework. Specifically, Section 3.1 details all technical assumptions needed throughout the paper, Section 3.2 formally states the main result, and Section 3.3 describes several desirable properties of the emerging distributionally robust estimators.

3.1. Assumptions

The uncertainty set is non-convex for some choices of the divergence function . In these cases, we cannot use Sion’s minimax theorem to establish strong duality between the primal and dual estimation problems (4) and (6), respectively. Instead, we will have to develop a more nuanced minimax theorem. For now, we assume that such a minimax theorem is readily available.

Assumption 1 (Minimax property).

We will later see that Assumption 1 is satisfied for all divergence functions listed in Table 1. In addition, we require to constitute a spectral divergence in the sense of the following assumption.

Assumption 2 (Spectral divergence).

The divergence function is non-negative, and satisfies the identity of indiscernibles, that is, for any we have if and only if . In addition, satisfies the following structural conditions.

-

(a)

(Orthogonal equivariance) For any and we have .

-

(b)

(Spectrality) There exists a function such that

and is continuous111By convention, a continuous extended real-valued function must tend to when approaching the boundary of its domain. in for every . In the following, we refer to as the generator of .

-

(c)

(Rearrangement property) For any and we have

If its left side is finite, this inequality becomes an equality if and only if .

Assumptions 2(a) and 2(b) imply that if and are simultaneously diagonalizable, then the divergence of with respect to depends only on the spectra of and and the generator . Specifically, we have

| (7) |

where the entries of the vectors and represent the eigenvalues and where the columns of the orthonormal matrix represent the (common) eigenvectors of and , respectively. Note that the last two equalities in (7) readily follow from 2(a) and 2(b). Assumption 2(b) further implies that if is a spectral divergence on , then its generator is a spectral divergence on . Indeed, restricting and to multiples of the vector of all ones reveals via Assumption 2(b) that and that inherits continuity, non-negativity and the identity of indiscernibles from . Orthogonal equivariance, spectrality, and the rearrangement inequality are trivially satisfied in the one-dimensional case. Finally, we point out that Assumption 2(c) is reminiscent of the Hardy-Littlewood-Polyak rearrangement inequality [19], which asserts that for any vectors .

Our results also require the following assumptions about the eigenvalues of the nominal covariance matrix as well as about the radius of the uncertainty set .

Assumption 3 (Regularity of input parameters).

The following hold.

-

(a)

For any we have .

-

(b)

The radius of the uncertainty set satisfies , where .

Together with Assumptions 2(a) and 2(b), Assumption 3(a) ensures that the nominal covariance matrix is feasible in problem (P). Indeed, inserting into (7) implies that . This implies that and, more importantly, that the feasible region of problem (P) is non-empty. This assumption is not entirely innocent because some divergence functions from Table 1 have domain . In all these cases, Assumption 3(a) requires that has full rank and, if is the sample covariance matrix, that the sample size is at least as large as the dimension . Assumption 3(b) ensures that the radius is small enough for the feasible region of the reformulated dual estimation problem (P) not to contain . Otherwise, problem (P) would trivially be solved by the nonsensical estimator .

Assumption 4 (Smoothness and convexity of the generator ).

For any , the function is twice continuously differentiable throughout and convex on the interval .

Assumption 4 implies that the domain of contains for every . Hence, can evaluate to only at , which means that the domain of is either or . We emphasize that the convexity of on the interval does not imply that problem (P) is convex. However, we will see below that this restricted convexity assumption helps us to reduce problem (P) to a convex program.

3.2. Construction of the Distributionally Robust Estimator

We need the following notation to restate Theorem 1 rigorously. We denote the -th smallest eigenvalue of a symmetric matrix by , and we use as a shorthand for the spectrum of . We also reserve the symbols and for the non-negative eigenvalues and the corresponding orthonormal eigenvectors of the nominal covariance matrix . In addition, we use and to denote the nominal spectrum and the orthogonal matrix of the nominal eigenvectors, respectively. The nominal covariance matrix thus admits the spectral decomposition . We also define the auxiliary function corresponding to a divergence function with generator via

| (8) |

In the remainder of the paper, we refer to as the eigenvalue map. We will see below that it is well-defined under Assumption 4, which implies that the nonlinear equation in (8) has a unique solution whenever . We will also prove that for every , which means that it can be viewed as a shrinkage transformation that maps any input eigenvalue to a smaller output eigenvalue for every fixed . Given these conventions, we are now ready to restate Theorem 1 formally.

Theorem 1 (Distributionally robust estimator (formal)).

Theorem 1 provides a quasi-closed form expression for the optimal covariance estimator that solves the robust estimation problem (4) as well as its dual reformulation (P). In particular, it shows that has the same eigenvectors as and that all positive eigenvalues of can be computed by solving a nonlinear equation parametrized by . Remarkably, this nonlinear equation admits a closed-form solution for all divergences listed in Table 1. In addition, we will see that can be computed efficiently by bisection. All of this implies that the complexity of computing is largely determined by the complexity of diagonalizing . In addition, we will see that decreases with . Thus, and are naturally interpreted as a nonlinear shrinkage estimator and inverse shrinkage intensity, respectively.

We now outline the high-level structure of the proof of Theorem 1; see Figure 1 for a visualization. The proof is divided into three steps that give rise to three propositions. Proposition 1 below first shows that there is a one-to-one relationship between the minimizers of the robust estimation problem (4) and problem (P).

Proposition 1 (Dual characterization of ).

The proof of Proposition 1 follows immediately from the discussion in Section 2 and is thus omitted. Next, we show that problem (P), which optimizes over all matrices in the positive semidefinite cone , is equivalent to problem (P) below, which optimizes over all vectors in the non-negative orthant :

| (P) |

We henceforth use to denote the unique minimizer of problem (P) if it exists.

In the third and last step, we solve problem (P) in quasi-analytical form. To this end, we denote the Lagrange multiplier associated with the divergence constraint by . The following proposition characterizes the unique solution of problem (P) through an explicit function of and shows that (P) can be computed by solving a single nonlinear equation.

Proposition 3 (Solution of (P)).

In summary, Proposition 3 provides a simple characterization of and shows how one can use to construct a unique solution for problem (P). Proposition 2 reveals how can be used to construct a unique solution for problem (P), and Proposition 1 guarantees that is uniquely optimal in the robust estimation problem (4). Taken together, Propositions 1, 2 and 3 therefore prove Theorem 1.

3.3. Properties of the Distributionally Robust Estimator

We now highlight several desirable characteristics of the distributionally robust covariance estimator .

3.3.1. Efficient Computation

We have seen that can be constructed from , which can be constructed from . In addition, we have seen that the Lagrange multiplier is the unique positive root of the equation , where the function is defined through . The following proposition suggests that this root-finding problem can be solved highly efficiently by bisection or Newton’s method.

Proposition 4 (Structural properties of ).

Suppose now that we have access to an a priori upper bound on the Lagrange multiplier . Note that is guaranteed to exist under the assumptions of the proposition. Section 4 shows that can be constructed explicitly for several popular divergence functions. The structural properties of established in Proposition 4 allow us to estimate the number of function evaluations needed to compute . For example, can be computed via bisection to within an absolute error of using function evaluations. Under additional mild conditions, can also be computed via Newton’s method to within an absolute error of using merely function and derivative evaluations [11, Theorem 2.4.3].

3.3.2. Shrinkage Properties

Proposition 3 asserts that if Assumptions 2, 3 and 4 hold, then the optimal solution of problem (P) is unique and can thus be seen as a function of the radius of the uncertainty set, where is defined as in Assumption 3(b). In fact, can naturally be extended to a function on . As satisfies the identity of indiscernibles, we can define as the unique solution of problem (P) for . In addition, we may define . One can then show that each component of monotonically decreases to on . By Theorem 1, the distributionally robust estimator inherits the eigenbasis from the nominal covariance matrix . Hence, and commute, and is rotation equivariant. In summary, these insights imply that essentially shrinks the eigenvalues of towards zero.

Proposition 5 (Shrinkage estimator).

Proposition 5 asserts that the eigenvalues of are bounded above by the corresponding nominal eigenvalues. This shrinkage property persists across a remarkably broad class of estimators. The shrinkage effects of robustification were first discovered in a distributionally robust inverse covariance estimation problem with a Wasserstein ambiguity set [43]. The results presented here are significantly more general. Indeed, they reveal that a broad class of divergence functions gives rise to diverse shrinkage estimators.

3.3.3. Improvement of the Condition Number

The condition number of a positive definite matrix is defined as the ratio of its largest to its smallest eigenvalue. It is well known that unless , the sample covariance matrix tends to be ill-conditioned, that is, [63]. Therefore, most shrinkage estimators are designed to improve the condition number of an ill-conditioned baseline estimator . Below we will show that the distributionally robust estimator is also guaranteed to improve the condition number of whenever the generator of the divergence satisfies a second-order differential inequality.

Assumption 5 (Differential inequality).

The generator of the divergence function is twice continuously differentiable on and satisfies the following differential inequality for all with .

Assumption 5 may be difficult to check. In Theorem 2 below, we will show, however, that it is satisfied by all divergence functions of Table 1. We can now prove that robustification improves the condition number.

The proof of Proposition 6 exploits a generalized monotonicity property of the eigenvalue map .

Lemma 1 (Generalized monotonicity property of the eigenvalue map ).

3.3.4. Statistical Guarantees

We finally show that the distributionally robust estimator is consistent and enjoys a finite-sample performance guarantee. To this end, we make the dependence on explicit, that is, we let be the unique solution of (4), where the nominal estimator is any covariance estimator constructed from i.i.d. training samples, and where the radius is set to a non-negative number that may depend on . We say a covariance estimator is strongly consistent if it converges almost surely to as tends to infinity.

Proposition 7 (Consistency).

Proposition 7 is intuitive because the uncertainty set is assumed to shrink with , and the nominal covariance matrix at its center is assumed to be consistent. As the uncertainty set is defined as a generic divergence ball, however, the proof is perhaps surprisingly tedious. The standard example of a consistent nominal covariance estimator is the sample covariance matrix. Next, we establish finite-sample performance guarantees, that is, we show that the uncertainty set of radius around the sample covariance matrix constitutes a confidence region for . In the following we say that the probability distribution is sub-Gaussian if there exists with for every . As both sides of this inequality are differentiable and coincide at , one can show that any sub-Gaussian distribution must have mean .

Proposition 8 (Finite-sample performance guarantee).

Suppose that is sub-Gaussian with covariance matrix , and let be the sample covariance matrix corresponding to i.i.d. samples from . For any divergence function from Table 1 there exist and that may depend on such that for every and .

Proposition 8 implies that if and , then the optimal value of the robust covariance estimation problem (4) provides a -upper confidence bound on the actual estimation error with respect to the true covariance matrix . We emphasize that the dependence of and on the sample size and significance level is sometimes substantially better than the worst-case dependence reported in Proposition 8. Explicit formulas for and tailored to different divergence functions can be found in the proof of Proposition 8 in the appendix.

4. A Zoo of New Covariance Shrinkage Estimators

In this section, we first show that the assumptions of Theorem 1 are satisfied by a broad spectrum of divergence functions commonly used in statistics, information theory, and machine learning. Next, we explicitly construct the shrinkage estimators corresponding to three popular divergence functions.

Theorem 2 (Validation of assumptions).

We emphasize that the uncertainty sets corresponding to the Fisher-Rao and inverse Stein divergences fail to be convex, in which case one cannot use standard minimax results to prove Assumption 1. However, perhaps surprisingly, in Appendix C.2, we show that the uncertainty sets corresponding to these divergences are geodesically convex with respect to a particular Riemannian geometry on the space of positive definite matrices. Moreover, we prove a Riemannian minimax theorem, which requires geodesic convexity instead of ordinary convexity and, therefore, significantly generalizes the classic Euclidean minimax results; see Theorem 3 in Appendix C.3. This new theorem enables us to prove the desired minimax property even for robust estimation problems based on the Fisher-Rao and inverse Stein divergences.

To showcase the richness of our framework, we now focus on three popular divergence functions and analyze the corresponding robust covariance estimators. Specifically, we will derive the optimal solutions of problem (P) in quasi-closed form for the Kullback-Leibler, Wasserstein, and Fisher-Rao divergences. In doing so, we develop a general recipe for the other divergence functions listed in Table 1.

4.1. The Kullback-Leibler Covariance Shrinkage Estimator

Table 1 defines the Kullback-Leibler (KL) divergence between two matrices as

This KL divergence between matrices is intimately related to the KL divergence between distributions.

Definition 1 (KL divergence).

If and are two probability distributions on , and is absolutely continuous with respect to , then the KL divergence from to is .

The following lemma shows that the KL divergence between two non-degenerate zero-mean Gaussian distributions coincides with the KL divergence between their positive definite covariance matrices.

Lemma 2 (KL divergence between Gaussian distributions [28]).

The KL divergence from to with is given by .

Lemma 2 justifies our terminology of referring to as the KL divergence and suggests that inherits many properties of the KL divergence between distributions. For example, it is easy to verify that satisfies the identity of indiscernibles but fails to be symmetric. Indeed, for any we have , whereas . An elementary calculation further reveals that the generator corresponding to the KL divergence can be expressed as

The following corollary of Theorem 1 characterizes the eigenvalue map and the inverse shrinkage intensity corresponding to the KL divergence, which determines the KL covariance shrinkage estimator.

Corollary 1 (KL covariance shrinkage estimator).

If is the KL divergence, and , then problem (4) is uniquely solved by the KL covariance shrinkage estimator with shrunk eigenvalues , . The underlying eigenvalue map is given by

| (9a) | |||

| and the inverse shrinkage intensity is the unique positive solution of the nonlinear equation | |||

| (9b) | |||

| where | |||

4.2. The Wasserstein Covariance Shrinkage Estimator

Table 1 defines the Wasserstein divergence between two matrices as

In the following, we will show that the Wasserstein distance between matrices is closely related to the squared 2-Wasserstein distance between distributions, where the transportation cost is defined via the 2-norm.

Definition 2 (Wasserstein distance).

The 2-Wasserstein distance between two probability distributions and on with finite second moments is defined as

where denotes the set of probability distributions on with marginals and , respectively.

One can show that Wasserstein distance is a metric on the space of probability distributions with finite second moments [65, § 6]. However, the squared Wasserstein distance is only a divergence as it fails to satisfy the triangle inequality. The following lemma shows that the squared 2-Wasserstein distance between two zero-mean Gaussian distributions matches the Wasserstein divergence between their covariance matrices.

Lemma 3 (Squared Wasserstein distance between Gaussian distributions [18]).

The squared 2-Wasserstein distance between and evaluates to .

Lemma 3 justifies our terminology of referring to as the Wasserstein divergence and suggests that inherits many properties from the Wasserstein distance between distributions. Note that remains well-defined even if or are rank-deficient. The generator of the Wasserstein divergence is given by

The following corollary of Theorem 1 characterizes the eigenvalue map and inverse shrinkage intensity corresponding to the Wasserstein divergence, which determines the Wasserstein covariance shrinkage estimator.

Corollary 2 (Wasserstein covariance shrinkage estimator).

If is the Wasserstein divergence, and , then problem (4) is uniquely solved by the Wasserstein covariance shrinkage estimator with eigenvalues , . The underlying eigenvalue map is given by

| (10a) | |||

| and the inverse shrinkage intensity is the unique positive solution of the nonlinear equation | |||

| (10b) | |||

where .

The requirement that be strictly smaller than is equivalent to Assumption 3(b). It is needed to prevent problem (P) from admitting the trivial solution . To see this, note that the condition is equivalent to , which in turn implies that is feasible and even optimal in (P). In this case, the trivial (and essentially nonsensical) estimator would be optimal in problem (4).

4.3. The Fisher-Rao Covariance Shrinkage Estimator

Table 1 defines the Fisher-Rao divergence between two matrices as

The Fisher-Rao divergence can be interpreted as the Fisher-Rao distance on a particular statistical manifold.

Definition 3 (Fisher-Rao distance).

Consider a family of probability density functions whose parameter ranges over a Riemannian manifold with metric . The geodesic distance on induced by this metric is referred to as the Fisher-Rao distance.

Note that represents the Fisher information matrix corresponding to the parameter . Next, we show that the squared Fisher-Rao distance between two non-degenerate zero-mean Gaussian probability density functions is proportional to the Fisher-Rao divergence between their positive definite covariance matrices.

Lemma 4 (Fisher-Rao distance between positive definite covariance matrices [3]).

Let be the family of all non-degenerate zero-mean Gaussian probability density functions encoded by their covariance matrices , which range over the Riemannian manifold equipped with the Fisher-Rao distance. If and belong to , then .

Lemma 4 justifies our terminology of referring to as the Fisher-Rao divergence. As is proportional to the squared Fisher-Rao distance , it fails to satisfy the triangle inequality and is indeed only a divergence. Moreover, Example 1 in Appendix C.1 reveals that is neither convex nor quasi-convex. However, it is geodesically convex. The generator corresponding to can be expressed as

The following corollary of Theorem 1 characterizes the eigenvalue map and inverse shrinkage intensity corresponding to the Fisher-Rao divergence, which characterizes the Fisher-Rao covariance estimator.

Corollary 3 (Fisher-Rao covariance shrinkage estimator).

If is the Fisher-Rao divergence, and , then problem (4) is uniquely solved by the Fisher-Rao covariance shrinkage estimator with eigenvalues , . The underlying eigenvalue map is given by

| (11a) | |||

| and denotes the principal branch of the Lambert-W function. In addition, the inverse shrinkage intensity with is the unique positive solution of the nonlinear equation | |||

| (11b) | |||

4.4. Other Covariance Shrinkage Estimators

Theorem 2 ensures that all divergence functions from Table 1 satisfy Assumptions 1, 2, 4 and 5 and thus induce via Theorem 1 a distributionally robust covariance shrinkage estimator. The generators and eigenvalue maps corresponding to all these divergences can be derived by using similar techniques as in Corollaries 1, 2, and 3. Details are omitted for brevity. All generators and eigenvalue maps are provided in Table 2.

| Divergence | for | ||

|---|---|---|---|

| Kullback-Leibler/Stein | |||

| Wasserstein | |||

| Fisher-Rao | |||

| Inverse Stein | |||

| Weighted quadratic |

5. Numerical Experiments

We now compare our distributionally robust covariance estimators against the linear shrinkage estimator with shrinkage target [32] as well as a state-of-the-art nonlinear shrinkage estimator proposed by Ledoit and Wolf [35], henceforth referred to as the NLLW estimator. The performance of the linear shrinkage estimator depends on the choice of the mixing parameter , which we calibrate via cross-validation.

We first study the dependence of our estimators on the radius of the uncertainty set. Using synthetic data, we assess their Frobenius risk as a function of the sample size. Using real data, we further test the performance of minimum variance portfolios constructed from our estimators. In addition, we illustrate the use of covariance estimators in the context of linear and quadratic discriminant analysis. The code for all experiments as well as an implementation of our methods can be found on GitHub.222https://github.com/yvesrychener/covariance_DRO

5.1. Dependence on the Radius of the Uncertainty Set

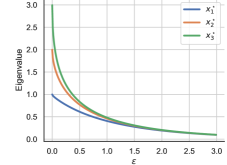

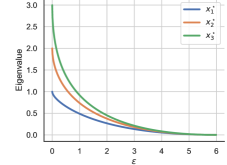

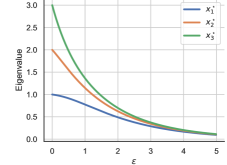

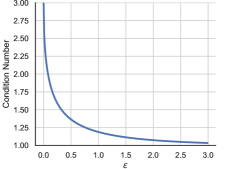

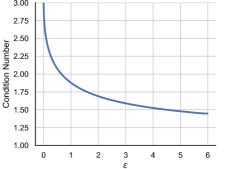

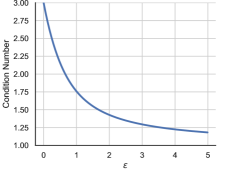

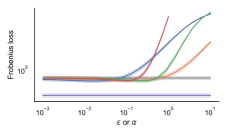

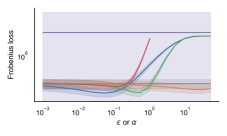

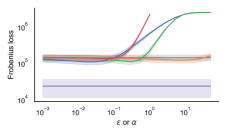

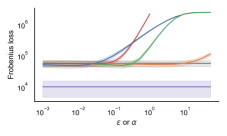

We first study the decay of the eigenvalues and the condition number of the Kullback-Leibler, Wasserstein, and Fisher-Rao covariance shrinkage estimators with the radius of the uncertainty set. To this end, we set and consider a nominal covariance matrix with eigenvalue spectrum . Figure 2 visualizes the eigenvalues of as a function of . In agreement with Proposition 5, we observe that shrinks the eigenvalues of the underlying nominal estimator towards as grows. Recall from Assumption 3(b) and the subsequent discussion that whenever . As the generator of the Wasserstein divergence satisfies , the eigenvalues of the Wasserstein covariance shrinkage estimator thus vanish for any . In contrast, the eigenvalues of the Kullback-Leibler and Fisher-Rao covariance shrinkage estimators remain strictly positive for all . We further observe that, for small values of , the Wasserstein and Fisher-Rao covariance shrinkage estimators primarily shrink the large eigenvalues of and keep the small ones constant. Figure 3 visualizes the condition number as a function of . As predicted by Proposition 6, is at most as large as . Note also that is undefined for . Figure 3 indicates that the condition number of decreases monotonically as tends to .

5.2. Frobenius Error

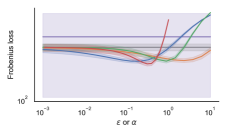

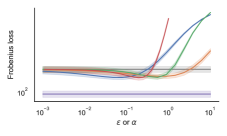

In the first experiment, we use synthetic data to analyze the Frobenius risk of different covariance estimators. Specifically, we construct a diagonal covariance matrix with eigenvalues equal to and ‘spiking’ eigenvalues equal to . Thus, we have . Next, we let be the sample covariance matrix constructed from independent samples from . This experimental setup captures the small to medium sample size regime with , in which we expect to provide a poor approximation for . We thus compare against the Kullback-Leibler, Wasserstein, and Fisher-Rao covariance shrinkage estimators as well as against the linear shrinkage estimator with shrinkage target and against the NLLW estimator. Figure 4 visualizes the Frobenius loss of all estimators as a function of the underlying hyperparameters, that is, the radius of the uncertainty set for the distributionally robust estimators and the mixing weight for the linear shrinkage estimator. The NNLW estimator and the sample covariance matrix involve no hyperparameters and are thus visualized as horizontal lines. Figure 4 shows both the means (solid lines) as well as the areas within one standard deviation of the means (shaded areas) of the Frobenius loss based on independent training sets for all possible combinations of and . As tends to , all distributionally robust estimators approach the sample covariance matrix. Thus, they overfit the data and display a high variance. As tends to , on the other hand, all distributionally robust estimators collapse to and thus display a high bias. We thus face a classic bias-variance trade-off. Figure 4 reveals that the Frobenius loss of the distributionally robust estimators is minimal at intermediate values of . We observe that the linear shrinkage estimator is competitive with the distributionally robust estimators for well-conditioned covariance matrices (small , top row). As the covariance matrix becomes more ill-conditioned (large , middle and bottom rows), the linear shrinkage estimator is dominated by the distributionally robust estimators, which attain a significantly smaller Frobenius loss. The advantage of the distributionally robust estimators relative to the nominal sample covariance matrix diminishes with increasing sample size . The NLLW estimator is designed to be asymptotically optimal and, therefore, dominates the other estimators for large sample sizes. However, it is suboptimal if training samples are scarce.

The insights of this synthetic experiment can be summarized as follows. Linear shrinkage estimators are suitable for well-conditioned covariance matrices and small sample sizes, while the NLLW estimator is preferable for large sample sizes, irrespective of the condition number. The distributionally robust estimators perform better when the covariance matrix is ill-conditioned and training samples are scarce.

5.3. Minimum Variance Portfolio Selection

We consider the problem of constructing the minimum variance portfolio of risky assets by solving the convex program [22], where denotes the -dimensional vector of ones, and stands for the covariance matrix of the asset returns over the investment horizon. The unique optimal solution of this problem is given by . In practice, however, the distribution of the asset returns is unknown, and thus the covariance matrix needs to be estimated from historical data. If the chosen covariance estimator is invertible, then it is natural to use as an estimator for the minimum variance portfolio. This approach seems reasonable, provided that the asset return distribution is stationary over the (past) estimation window and the (future) investment horizon.

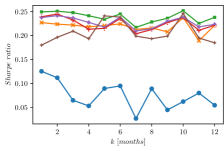

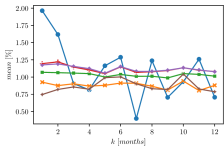

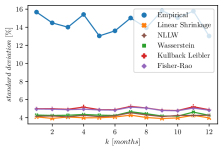

In the next experiment, we assess the minimum variance portfolios induced by several covariance estimators on the “48 Industry Portfolios” dataset from the Fama-French online library,333https://mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library.html which contains monthly returns of 48 portfolios grouped by industry. Specifically, we adopt the following rolling horizon procedure from January 1974 to December 2022. First, we estimate from the historical asset returns within a rolling estimation window of months and construct the corresponding minimum variance portfolio. We then compute the returns of this portfolio over the months immediately after the estimation window. Finally, the covariance estimators are recalibrated based on a new estimation window shifted ahead by months, and the procedure starts afresh. Some covariance estimators involve a hyperparameter, which we calibrate via leave-one-out cross-validation on the return samples in each estimation window. To this end, we assume that the mixing weight of the linear shrinkage estimator with shrinkage target ranges from to , whereas the radius of the uncertainty set ranges from to for the Kullback-Leibler and Fisher-Rao covariance shrinkage estimators and from to for the Wasserstein covariance shrinkage estimator. We discretize these parameter ranges into logarithmically spaced candidate values and select the one that induces the smallest portfolio variance. Given the selected hyperparameter, the covariance estimator corresponding to the current estimation window is computed using all data points. In the following, we measure the quality of a given covariance estimator by Sharpe ratio and the mean and the standard deviation of the portfolio returns generated by the above rolling horizon procedure over the backtesting period.

Figure 5 displays the Sharpe ratios, means, and standard deviations corresponding to different covariance estimators as a function of the length of an updating period. All shrinkage estimators produce lower standard deviations and higher Sharpe ratios than the sample covariance matrix. Even though the mean portfolio returns of the sample covariance matrix are—on average—similar to those of the shrinkage estimators, they change rapidly with , which is troubling for investors who need to select before seeing the results of the backtest. The distributionally robust estimators proposed in this paper outperform the other shrinkage estimators in terms of mean returns and Sharpe ratios for most choices of , and the Wasserstein covariance shrinkage estimator results in the globally highest Sharpe ratio. However, the Kullback-Leibler and Fisher-Rao covariance shrinkage estimators result in slightly higher means and standard deviations.

5.4. Linear and Quadratic Discriminant Analysis

Quadratic discriminant analysis (QDA) seeks to predict a label from a feature vector under the assumption that for every . If the mean , the covariance matrix as well as the marginal class probability are known for all , then the Bayes-optimal classifier predicts as a solution of . Linear discriminant analysis (LDA) operates under the additional assumption that . The decision boundaries of the resulting LDA and QDA classifiers are thus given by linear hyperplanes and quadratic hypersurfaces, respectively [20].

In the last experiment, we use LDA and QDA to address the breast cancer detection [68] and banknote authentication [39] problems from the UCI Machine Learning Repository. As the distribution governing and is unobservable, we replace the unknown class probabilities and class means by the empirical frequencies and sample average estimators, respectively, and we use different shrinkage estimators for the unknown covariance matrices . All tested shrinkage estimators use the debiased empirical covariance matrix as the nominal estimator. QDA constructs a separate covariance estimator for each class that only uses class- samples, whereas LDA pools all samples to construct a single joint covariance estimator.

We use 50% of each dataset for training and the rest for testing. The hyperparameters (for the distributionally robust shrinkage estimators) and (for the linear shrinkage estimator) are selected by the holdout method with a validation set comprising 20% of the training data. The quality of a covariance estimator is then measured by the accuracy (i.e., the proportion of correct predictions) of the resulting LDA and QDA classifiers. Table 3 reports the means and standard errors of the accuracy achieved by different covariance estimators. We observe that shrinking the empirical covariance estimator can improve the performance of LDA and QDA, and that nonlinear shrinkage methods outperform the linear shrinkage method across all experiments. The Kullback-Leibler covariance shrinkage estimator consistently performs well. QDA based on the NLLW estimator attains the highest accuracy on the banknote authentication dataset but performs poorly on the breast cancer dataset. On the other hand, the distributionally robust covariance estimators are consistently on par with or better than the empirical and the linear shrinkage estimator. Note that the best-performing distributionally robust shrinkage estimator changes with the dataset. This highlights the usefulness of our approach, which results in a zoo of complementary covariance shrinkage estimators.

| Dataset | Empirical | Linear | NLLW | Wasserstein | Kullback-Leibler | Fisher-Rao | |

|---|---|---|---|---|---|---|---|

| LDA | Banknote | 0.9751(0.0005) | 0.9754(0.0005) | 0.9510(0.0011) | 0.9761(0.0005) | 0.9763(0.0005) | 0.9759(0.0005) |

| Cancer | 0.9520(0.0011) | 0.9365(0.0015) | 0.8902(0.0015) | 0.9520(0.0011) | 0.8874(0.0043) | 0.9515(0.0013) | |

| QDA | Banknote | 0.9854(0.0005) | 0.9839(0.0005) | 0.9877(0.0004) | 0.9854(0.0005) | 0.9853(0.0005) | 0.9854(0.0005) |

| Cancer | 0.9418(0.0012) | 0.8945(0.0027) | 0.6320(0.0052) | 0.9418(0.0012) | 0.9451(0.0013) | 0.9414(0.0016) |

Acknowledgments. This research was supported by the Hong Kong Research Grants Council under the GRF project 15304422, by the Swiss National Science Foundation under the NCCR Automation, grant agreement 51NF40_180545, and by CUHK through the ‘Improvement on Competitiveness in Hiring New Faculties Funding Scheme’ and the CUHK Direct Grant with project number 4055191.

Appendix

The appendix is organized as follows. In Appendix A, we prove Theorem 1 and derive basic properties of and , which will be used in Appendix B to establish the computational, structural and statistical properties of the distributionally robust estimators. Appendices C and D verify Assumptions 1 and 2 for all divergences in Table 1, respectively. As a byproduct, we derive a Riemannian generalization of Sion’s minimax theorem. The insights of Appendices C and D are used in Appendix E to prove the results of Section 4.

Appendix A Proof of Theorem 1

A.1. Proof of Proposition 2

We first reduce problem (P), which optimizes over matrices, to an equivalent problem of the form

| (P) |

which merely optimizes over vectors. Here, denotes as usual the vector whose -th entry is the -th smallest eigenvalue of the nominal covariance matrix . We therefore have . To simplify the subsequent discussions, for any minimization problem designated by “P,” say, we use “,” “” and “” to denote its minimum/infimum, the set of its optimal solutions and its feasible region, respectively.

Proposition 9 (Reduction of (P) to (P)).

If is a spectral divergence in the sense of Assumption 2, then the following assertions hold.

Proof of Proposition 9.

Select any , and use to denote its eigenvalue decomposition. By our notational conventions, we have . We then obtain

| (12) |

where the first equality follows from Assumption 2(b), the first inequality follows from Assumption 2(c), and the second equality follows from Assumption 2(a). This implies that .

Next, select any such that . By Assumptions 2(a) and (b), we thus have

| (13) |

where the three equalities follow from the eigenvalue decomposition of , Assumption 2(a) and Assumption 2(b), respectively. This implies that . In summary, we have thus shown that problem (P) is feasible if and only if problem (P) is feasible. This establishes assertion (i).

The first part of the proof of assertion (i) actually implies that . Conversely, the second part of the proof of assertion (i) implies that . To see this, recall that any feasible in (P) satisfies . As is feasible in (P), we may indeed conclude that . As the eigenvalue map is continuous [4, Corollary VI.1.6], is compact if and only if is compact. This observation establishes assertion (ii).

As for assertion (iii), assume that for otherwise the claim is trivial. Choose then any , and note that by virtue of (13). It remains to be shown that . Suppose, for the sake of contradiction, that there is with

and let be the eigenvalue decomposition of for some . By (12), we then have , which contradicts the optimality of in problem (P) because

Therefore, . This proves assertion (iii).

As for assertion (iv), assume that for otherwise the claim is trivial. Choose then any , and note that by virtue of (12). It remains to be shown that . Suppose, for the sake of contradiction, that there is with

By (13), we then have , which contradicts the optimality of in (P) because

Therefore, . This proves assertion (iv).

Proposition 9(iii) and the discussion after Assumption 1 imply that if , then the matrix is optimal in (4). We can thus compute robust covariance estimators by solving problem (P).

Although problem (P) optimizes over a significantly lower-dimensional search space than (P), it still involves ordering constraints . This is undesirable because each of these ordering constraints necessitates a separate dual variable. We now show that problem (P) is in fact equivalent to problem (P), which suppresses all ordering constraints, and which is repeated below for convenience.

| (P) |

More precisely, we will show that relaxing the ordering constraints preserves the optimal value and even the minimizers of problem (P)—up to simple rearrangements. Our proof will critically rely on Assumption 2 and on the following lemma, which shows that if feasible is in (P), then is feasible in (P).

Lemma 5.

If Assumption 2 holds, then we have

If the right-hand side is finite, then the above inequality collapses to an equality if and only if .

Proof of Lemma 5.

Proof.

We only show that . This readily implies that the optimal values match.

To prove the inclusion , select any . Hence, . Suppose now for the sake of argument that there exists with . By Lemma 5, which applies because , we may thus conclude that . However, this contradicts the optimality of in problem (P) because . Therefore, .

To prove the reverse inclusion , select any . We claim that . Suppose for the sake of contradiction that . This readily guarantees that not all components of are equal. Since and , Lemma 5 then implies that

that is, satisfies the constraint in (P) strictly. In the following we use to denote the -th standard basis vector in . As is not constant, there is with . This readily implies that . As is continuous by virtue of Assumption 2(b) and as strictly satisfies the explicit constraint in (P), the perturbed vector remains feasible in (P) for all sufficiently small . In addition, for all sufficiently small . This contradicts the optimality of . Hence, we may conclude that . Therefore, is feasible in (P). Since (P) is a relaxation of problem (P) (with the same objective function), we may thus conclude that . ∎

With these results in place, the proof of Proposition 2 is now immediate.

A.2. Proof of Proposition 3

The next lemma shows that any solution of problem (P) shrinks towards the origin. This will imply that our proposed distributionally robust estimators constitute shrinkage estimators.

Lemma 6 (Eigenvalue shrinkage).

Proof of Lemma 6.

Select any . As , it is clear that for all . Next, suppose that for some , and define through

Recall now that if Assumption 2(b) holds, then constitutes a spectral divergence on . Assumption 3(a) further implies that . Hence, , which ensures that . However, from the construction of it is evident that , which contradicts the optimality of in (P). Thus, we have for all . This observation completes the proof. ∎

Lemma 6 allows us to prove the existence and uniqueness of the proposed robust covariance estimators.

Proposition 11 (Existence and uniqueness of optimal solutions).

Proof of Proposition 11.

Suppose first that only Assumptions 2, 3 and 4 hold. Lemma 6 then implies that problem (P) has the same set of optimal solutions as the following variant of (P) with box constraints

| (P) |

Note that problem (P) is feasible due to Assumption 3(a), which posits that for all . Next, we show that the feasible region of (P) is compact. To this end, note that is continuous in on the interval for every . Indeed, continuity trivially holds if , in which case collapses to a point. Otherwise, if , then continuity follows from Assumption 2(b). This readily implies that the feasible region of (P) is closed and—thanks to the box constraints—also compact. The solvability of problem (P) thus follows from Weierstrass’ maximum theorem, which applies because the objective function is continuous. Assumption 4 further implies that is convex in on for all , which implies that the feasible region of (P) is convex. The uniqueness of the optimal solution thus follows from the strong convexity of the objective function. This shows that problem (P) has a unique optimal solution. The other claims immediately follow from Propositions 1, 9 and 10. ∎

From now on we use as a notational shorthand for the function for any fixed .

Proposition 12 (Solution of problem (P)).

The following lemma shows that is strictly decreasing on , which will be used to prove Proposition 12.

Proof of Lemma 7.

Select any . As is finite and convex on thanks to Assumption 4, we have

The desired inequality then follows from an elementary rearrangement. ∎

Proof of Proposition 12.

Lemma 6 allows us to rewrite problem (P) equivalently as

| (P) |

where with for each . Note that the objective and the constraint function adopt finite values on . By Proposition 11, problem (P) has a unique minimizer , and by Lemma 6 we have for all with . For such indices , by Assumption 3(a). By removing the corresponding decision variables from (P) and focusing on the optimization problem in the remaining variables, we can therefore assume without loss of generality that for all . Hence, problem (P) can be viewed as an ordinary convex program in the sense of [52, Section 28].

Following [52, Section 28], we define the Lagrangian of problem (P) through

By [52, Corollary 28.2.1 and Theorem 28.3], problem (P) is thus equivalent to the minimax problem

Specifically, the dual maximization problem on the right-hand side is solvable, and every maximizer gives rise to a saddle point of the minimax problem. Next, we prove that . Suppose for the sake of contradiction that . Note first that for otherwise problem (P) would be infeasible, thus contradicting the feasibility of . Hence, we find . If for some , then

where the second inequality holds because is a saddle point. However, the discussion after Assumption 4 implies that either equals or for every . Hence, we have , that is, contains points that are arbitrarily close to . This leads to the contradiction

We may thus conclude that if , then for all , that is, . However, this contradicts Assumption 3(b), which implies that . In summary, this shows that .

Next, we note that for any dual optimal solution , the minimization problem

| (15) |

admits a unique optimal solution, and by [52, Corollary 28.1.1] this minimizer must coincide with the unique optimal solution of problem (P). Given , we can thus solve (15) instead of (P). This is attractive from a computational point of view because is rectangular, whereby problem (15) can be simplified to

Therefore, it suffices to solve the following simple univariate minimization problem for each .

| (16) |

If , then by Assumption 3(a), and hence . In this case, is the only feasible—and thus unique optimal—solution of (16). Assume next that . In this case we need to prove that falls within the open interval and satisfies (14). We will first show that . From the discussion after Assumption 4 we know that can evaluate to only at . If , then we trivially have . Assume next that . By Assumption 2(b), is continuous and . There exists a threshold such that for all sufficiently small . In addition, as the function is convex and differentiable in by virtue of Assumption 4, we have

for all sufficiently small . Here, the second inequality follows from Lemma 7, and the third inequality holds because for all sufficiently small . This reasoning implies that

| (17) |

for all sufficiently small . Thus, small are strictly preferable to , that is, .

Next, we prove that . As the differentiable function is non-negative and attains its minimum at , we may conclude that its derivative converges to as tends to . For any sufficiently close to we thus have . As is convex in on , this ensures that

Hence, any sufficiently close to is strictly preferable to . Setting , we thus find .

Finally, note that since , the constraints of problem (16) are not binding at optimality. Thus, the minimizer of (16) is uniquely determined by the problem’s first-order optimality condition (14).

It remains to be shown that is unique. As thanks to Assumption 3(b), there exists at least one with , and hence . Since is differentiable on , equation (14) implies

Hence, is unique because is unique. Note also that is the Lagrange multiplier associated with the constraint in problem (P). As strong duality holds and , we have

by complementary slackness. Using the definition (8) of the eigenvalue map , we then obtain

This observation completes the proof. ∎

A.2.1. Properties of and

We first provide a detailed analysis of the nonlinear equation that defines the eigenvalue map .

Lemma 8 (Properties of ).

Recall that, for and fixed , the function shrinks the input in the sense that . Lemma 8 further shows that, for any fixed , strictly increases from to as grows. Therefore, we can interpret as an inverse shrinkage intensity.

Proof of Lemma 8.

Next, we prove assertion (ii). Recall from Assumption 4 that is twice continuously differentiable on . Thus, the function is continuously differentiable on . Assumption 4 further stipulates that is convex on . Hence, is strictly increasing in in the sense that

As by assertion (i), the implicit function theorem ensures that is differentiable (and in particular continuous) at any . It remains to be shown that is continuous at . Given any and as by definition, we thus need to show that there is such that for all . As for all , we may assume without loss of generality that . By Lemma 7, we have , which guarantees that is positive. For any , we thus obtain

where the equality follows from the definition of in (8), and the inequality follows from the definition of . This confirms that . Suppose to the contrary that . Then the above inequality implies . As is non-decreasing by virtue of the convexity of , this in turn leads to the contradiction . Thus, for all . We conclude that is indeed continuous at .

To show that is strictly increasing on , recall that is differentiable on . We may thus differentiate both sides of the equation with respect to to obtain

Rearranging terms then yields

| (18) |

which is strictly positive because thanks to Lemma 7 and thanks to the convexity of on . Hence, is strictly increasing on . This completes the proof of assertion (ii).

It remains to prove assertion (iii). The continuity of at has already been established in assertion (ii). As is strictly increasing in , it is clear that, as tends to infinity, has a well-defined limit not larger than . By the definition of in (8), we further have

Driving to infinity and recalling that for all thus shows that

where the second equality follows from the continuity of on . Note that exists and falls within the interval because is a strictly increasing function mapping to . These arguments imply that the limit must be a root of within . Lemma 7 implies that has no root in the open interval . We may thus conclude that must coincide with . As a sanity check, one readily verifies that because attains its minimum of at . Thus, assertion (iii) follows. ∎

We now prove that the function has one and only one root. By the proof of Proposition 12, this root must coincide with the unique optimal solution of the problem dual to (P).

Proof of Lemma 9.

Recall that by the definition of in (8). Recall also that if , then by virtue of Assumptions 2 and 3(a). Therefore, vanishing components of do not contribute to the function . In addition, Assumption 3(b) ensures that there exists at least one with and hence also with . For these reasons, we henceforth assume without loss of generality that for all . By Lemma 8(ii), constitutes a continuous real-valued function of . Similarly, by Assumption 2(b), constitutes a continuous extended real-valued function of . Therefore, the extended real-valued function is continuous on . Assumption 3(b) implies that . Recall now from Lemma 8(iii) that converges to as tends to infinity. By the continuity of in we thus have

All of this implies that the equation has at least one positive root. In the remainder we prove that this root is unique. As , Lemma 8 implies that strictly increases from (at ) to (as tends to infinity). Lemma 7 further implies that is strictly decreasing on . Thus, the composite function is strictly decreasing in for every . This readily shows that is strictly decreasing in throughout , thus implying that the equation has only one root. ∎

We are now ready to prove Proposition 3.

Appendix B Proofs of Section 3.3

Proof of Proposition 4.

In view of the proof of Lemma 9, it only remains to be shown that is differentiable at any . Towards that end, recall that vanishing components of do not contribute to such that

For any fixed , is differentiable with respect to by Lemma 8(ii), and is differentiable with respect to by Assumption 4. Therefore, is differentiable at any . ∎

From the proof of Proposition 12 we know that the problem dual to (P) has a unique optimal solution . Thus, can be viewed as a function of the radius of the divergence ball (2).

Proof of Lemma 10.

The proof of Proposition 12 implies that is the unique maximizer of the problem dual to (P). By inverting its objective function, this problem can be recast as the minimization problem

| (19) |

where the function is defined through

Note also that the non-negativity constraint on in (19) is strict because cannot be optimal, or, dually, because the constraint in (P) must be binding at optimality for . By construction, constitutes a pointwise maximum of multiple linear functions and is, therefore, convex. Next, select with , and introduce the notational shorthands and . By the optimality of and in problem (19) at and , there exist subgradients and satisfying the first-order optimality conditions and , respectively. Since is convex, its subdifferential is monotone, whereby . Together with the first-order optimality conditions, this implies that . As , we may thus conclude that . Hence, the claim follows. ∎

Proof of Proposition 5.

Note that for every thanks to Proposition 3, and recall that by definition. We aim to show that is non-increasing on and that . To this end, note first that both claims are trivially satisfied if , in which case for all thanks to Proposition 3 and our conventions that and . Assume next that . Recall that is non-increasing on thanks to Lemma 10, while is strictly increasing on thanks to Lemma 8(ii), which applies because . Therefore, is non-increasing on . We also have for all thanks to Proposition 3, and we have and by definition. All of this readily implies that is non-increasing on . In order to prove that , note first that must exist because is non-negative as well as non-increasing in . Next, recall from Lemma 7 that the function is strictly decreasing on . In fact, this monotonicity property extends to because is continuous thanks to Assumption 2(b). We then choose an arbitrary tolerance and assume without loss of generality that is smaller than the smallest non-vanishing component of . Next, consider a vector defined through if and if , , and set . By construction, we have

where the strict inequality holds because has at least one strictly positive component and because whenever thanks to the monotonicity properties of established above. Hence, is feasible in P, and is consistent with Assumption 3(b). In addition, one readily verifies that the objective function value of satisfies . By the optimality of in P, we thus find

Thus, for any sufficiently small there exists with . As is non-increasing on , this implies indeed that . It remains to be shown that constitutes a shrinkage estimator. This is now evident, however, because . ∎

Proof of Lemma 1.

Throughout this proof we fix any . We first aim to show that the function

is non-decreasing on . To this end, note that is twice continuously differentiable on by Assumption 5. Using the implicit function theorem as in Lemma 8, one can thus show that is differentiable with respect to and that for every . Recall also that by the definition of in (8). Differentiating both sides of this equation with respect to then yields

| (20) |

This in turn implies that

| (21) |

which is well-defined because and is convex by Assumption 4. We then find

The second term on the right hand side of the above expression satisfies

where the first and the second equalities follow from (20) and (21), respectively, and the third equality follows from the defining equation of in (8). Combining the last two equations finally yields

Recall now that for every thanks to Lemma 7 and that thanks to Lemma 8. This implies that the derivative of is non-negative if and only if

| (22) |

Assumption 5 guarantees that (22) holds indeed for all . Hence, is a non-decreasing function.

We now prove the desired inequality. By the defining equation of in (8) we have

for any , where and inequality follows from the monotonicity of established above. This implies that for all with . Hence, the claim follows. ∎

Proof of Proposition 7.

Throughout the proof we use the shorthands and for all and . By the strong consistency assumption, converges almost surely to . Fix now temporarily a particular realization of the uncertainties, for which converges deterministically to . In this case, converges to because the eigenvalue map is continuous [4, Corollary VI.1.6], and the sequence is bounded by Lemma 6. Thus, any convergent subsequence satisfies

In addition, we have

where the first equality holds because of Assumptions 2(a) and 2(b) and because and share the same eigenvectors. The second inequality follows from Proposition 1(ii), which ensures that is feasible in problem (P). As converges to and as is continuous on , the above implies that