Rejection via Learning Density Ratios

Abstract

Classification with rejection emerges as a learning paradigm which allows models to abstain from making predictions. The predominant approach is to alter the supervised learning pipeline by augmenting typical loss functions, letting model rejection incur a lower loss than an incorrect prediction. Instead, we propose a different distributional perspective, where we seek to find an idealized data distribution which maximizes a pretrained model’s performance. This can be formalized via the optimization of a loss’s risk with a -divergence regularization term. Through this idealized distribution, a rejection decision can be made by utilizing the density ratio between this distribution and the data distribution. We focus on the setting where our -divergences are specified by the family of -divergence. Our framework is tested empirically over clean and noisy datasets.

1 Introduction

Forcing Machine Learning (ML) models to always make a prediction can lead to costly consequences. Indeed, in real-world domains such as automated driving, product inspection, and medical diagnosis, inaccurate prediction can cause significant real-world harm [16, 26, 44, 41]. To deal with such a dilemma, selective prediction and classification with rejection were proposed to modify the standard supervised learning setting [15, 17, 58]. The idea is to allow for a model to explicitly reject making a prediction whenever the underlying prediction would be either inaccurate and / or uncertain.

In classification, a confidence-based approach can be utilized, where a classifier is trained to output a “margin” which is used as a confidence score for rejection [7, 28, 57, 47, 44]. Given a threshold value, the model rejects whenever this confidence score is lower than the threshold value. A key component of these confidence-based approaches is that they rely on providing good class probability estimates [48], i.e., being calibrated [57, 44]. Some approaches avoid explicit estimation of probabilities, however, these are usually restricted to binary classification [7, 28, 38].

Another classification-rejection approach aim to simultaneously train a prediction and rejection model in tandem [16, 17, 44]. These approaches are theoretically driven by the construction of surrogate loss functions, but in the multiclass classification case many of these loss functions have been shown to not be suitable [44]. For the multiclass classification setting, one approach connects classification with rejection to cost-sensitive classification [14]. In practice, these classification-rejection approaches require models to be trained from scratch using their specific loss function and architecture — if there is an existing classifier for the dataset, it must be discarded. A recent approach proposes to learn a rejector on top of a pretrained classifier via surrogate loss functions [39].

In this work, to learn rejectors we shift from a loss function perspective to a distributional perspective. Given a model and a corresponding loss function, we find a distribution where the model and loss performs “best” and compare it against the data input distribution to make rejection decisions (see Fig. 1). As such, the set of rejectors that we propose creates a rejection decision by considering the density ratio [55] between a “best” case (idealized) distribution and the data distribution, which can be thresholded by different values to provide different accuracy vs rejection percentage trade-offs. To learn these density ratios for rejection, we consider a risk minimization problem which is regularized by -divergences [1, 19]. We study a particular type of -divergences as our regularizer: the family of -divergences which generalizes the KL-divergence. To this end, one of our core contributions in this work is providing various methods for constructing and approximating idealized distributions, in particular those constructed by -divergences. The idealized distributions that we consider are connected to adversarial distributions examined in Distributionally Robust Optimization (DRO) [51] and the distributions learned in Generalized Variational Inference (GVI) [34]; and, as such, the closed formed solutions found for our idealized distribution have utility outside of the rejection setting. Furthermore, when utilizing the KL-divergence and Bayes optimal models, we recover the well known optimal rejection policies, i.e., Chow’s rule [15, 58]. Our rejectors are then examined empirically by examining the classification learning setting with calibrated classifiers.

In summary, our contributions are the following:

-

•

We present a new framework for learning with rejection involving the density ratios of idealized distributions which mirrors the distributions learned in DRO and GVI;

-

•

We show that rejection policies learned in our framework can theoretically recover optimal rejection policies, i.e., Chow’s rule;

-

•

We derive optimal idealized distributions generated from -divergences;

-

•

We present a set of simplifying assumptions such that our framework can be utilized in practice and verify this empirically.

Notation

Let be a domain of inputs and be output targets. We primarily consider the case where is a finite set of labels , where . We will also consider output domains which is not necessarily the same as the output data , e.g., class probabilities estimates in the classification setting. We further denote the underlying (usually unknown) input distribution as . The marginals of a joint distribution are denoted by subscript, e.g., for the marginal on the label space. Similarly, we denote conditional distributions, e.g., . For marginals on , we make the subscripting of implicit with . The empirical distributions of are denoted by , with denoting the number of samples used to generate it. Furthermore, denote the Iverson bracket if the predicate is true and otherwise [35]. The maximum is shorthanded.

2 Preliminaries

Learning with Rejection

We first recall the standard risk minimization setting for learning. Suppose that we are given a (point-wise) loss function which measures the level of disagreement between predictions and data. Given a data distribution and a hypothesis set of models , we aim to minimize the expected risk w.r.t. ,

| (1) |

One way of viewing learning with rejection is to augment the risk minimization framework by learning an addition rejection function . This can be formally defined using a regularization term which controls the rate of rejection:

| (2) |

where denotes a hypothesis set of rejection functions.

Suppose that is complete (contains all possible rejectors). In such a case, one can see that setting reduces Eq. 2 to standard risk minimization setting given by Eq. 1. Furthermore, setting will result in always rejecting, i.e., the case where there is no rejection cost. Some values of can be redundant. If the loss is bounded above by , then any is equivalent to setting — the optimal will be to never reject. In classification, where is taken to be the zero-one-loss, is typically restricted to values in as otherwise low confidence prediction can be accepted [44] — our work only considers this case. Ramaswamy et al. [47] explores the scenario.

Once minimized, a combined model with rejection can be defined by,

| (3) |

where denotes a rejection token makes to abstain from making a prediction.

So far, the learning task has been left general. By considering Class Probability Estimation (CPE) [49], we recover familiar optimal rejection and classifier pairs.

Theorem 2.1 (Optimal CPE Rejection / Chow’s Rule).

The theorem can easily be generalized to non-binary cases. We note that Theorem 2.1 is a generalization of the well known Chow’s rule of classification with rejection [15, 14]. Indeed, taking to be the zero-one-loss function, we get . One can further clarify this by noticing that . In the general proper loss case, the optimal rejector is thresholding a generalized entropy function (known as the conditional Bayes risk [48]). This would also correspond to thresholding the class probabilities , but with different thresholding values per class (unless is a symmetric loss function).

Generalized Variational Inference

Generalized Variational Inference (GVI) [34] provides a framework for a generalized set of entropy regularized risk minimization problem. In particular, GVI generalizes Bayes’ rule by interpreting the Bayesian posterior as the solution to a minimization problem [59]. The Bayes’ rule minimization is given by,

| (4) |

where denotes a set of model parameters with likelihood function and denotes data. Here, denotes the prior and the optimal denotes the posterior in Bayes’ rule.

For GVI, we generalize a number of quantities. For instance, the ‘loss’ considered can be altered from the log-likelihood to an alternative loss function over samples . The divergence function can also be altered to change the notion of distributional distance. Furthermore, the set of distributions being minimized can also be altered to, e.g., reduce the computational cost of the minimization problem. One can thus alter Eq. 4 to give the following:

| (5) |

where and , , and denote the generalized loss, divergence, and set of distribution, respectively. Here seeks to act as a regularization constant which can be tuned.

In our work, we will consider a GVI problem which changes the loss function and divergence to define an entropy regularized risk minimization problem. Our loss function corresponds to the learning setting. For the change in divergence, we consider -divergence [1, 19], which are otherwise referred to as -divergences [50] or the Csiszár divergence [18].

Definition 2.2.

Let be a convex lower semi-continuous function with then the corresponding -divergence over non-negative measures for is defined as:

| (6) |

We note that for -divergences, the regularization constant in Eq. 5 can be absorbed into the -divergence generator, i.e., .

Distributionally Robust Optimization

A related piece of literature, is Distributionally Robust Optimization (DRO) [51], where the goal is to find a distribution that maximizes (or minimizes) the expectation of a function from a prescribed uncertainty set. Popular candidates for these uncertainty sets include all distributions that are a certain radius away from a fixed distribution by some divergence. -divergences have been used to define such uncertainty set [8, 22, 36]. Given radius , define . Given a point-wise loss function , DRO alters risk minimization, as per Eq. 1, to solve the following optimization problem:

| (7) |

The maximization over is typically over the target space . That is, and the maximization is adversarial over the marginal label distribution [60]. We note that by converting the -ball constraint into a Lagrange multiplier, the inner optimization over in Eq. 7 becomes a optimization problem which mirrors Eq. 5. The connection between GVI and adversarial robustness has been previously noted [31].

Typically in DRO and related learning settings, the construction of the adversarial distribution defined by the inner maximization problem is implicitly solved. For example, when is twice differentiable, it has been shown that the inner maximization can be reduced to a variance regularization expression [22, 21]; whereas other choices of divergences such as kernel Maximum Mean Discrepancy (MMD) yields kernel regularization [54] and Integral Probability Metrics (IPM) correspond to general regularizers [30]. Another popular choice is the Wasserstein distance which has shown strong connections to point-wise adversarial robustness [10, 11, 52].

The aforementioned work, however, seek only to find the value of the inner maximization in Eq. 7 without considering the form the optimal adversarial distribution takes.

3 Rejection via Idealized Distributions

We propose learning rejection functions by comparing data distributions to a learned idealized distribution (as per Fig. 1). An idealized distribution (w.r.t. model ) is a distribution which when taken as data results in low risk (per Eq. 1). are idealized rather than ‘ideal’ as they do not solely rely on a model’s performance, but are also regularized by their distance from the data distribution . Formally, we define our idealized distribution via a GVI minimization problem.

Definition 3.1.

Given a data distribution and a -divergence, an idealized distribution for a fixed model and loss is a distribution given by

| (8) |

where and .

Given the objective of Eq. 8, an idealized distribution will have high mass when is small and low mass when is large. The -divergence regularization term prevents the idealized distributions from collapsing to a point mass. Indeed, without regularization the distance from , idealized distributions would simply be Dirac deltas at values of which minimize .

With an idealized distribution , a rejection can be made via the density ratio [55] w.r.t. .

Definition 3.2.

Given a data distribution and an idealized distribution , the -ratio-rejector w.r.t. is given by , where .

Definition 3.2 aims to reject inputs where the idealized rejection distribution has lower mass than the original data distribution. Given Definition 3.1 for idealized distribution, small values of corresponds to regions of the input space where having lower data probability would decrease the expected risk of the model. Note that we do not reject on regions with high density ratio as would be necessarily small or the likelihood of occurrence would be relatively small. We restrict the value of to to ensure that rejection is focused regions where is high with high probability w.r.t. — further noting that always rejects.

Although Definitions 3.1 and 3.2 suggests that we should learn distributions (and ) separately to make our rejection decision, in practice, we can learn the density ratio directly. Indeed, through the definition of Definition 2.2, we have that equivalent minimization problem:

| (9) |

Such an equivalence has been utilized in DRO previously [23, Proof of Theorem 1]. Notice that the learning density ratio in Eq. 9 is analogous to the acceptor in Eq. 2. Indeed, ignoring the normalization constraint , by restricting , letting , and letting , the objective function of Eq. 9 can be reduced to:

| (10) |

Given the restriction of to binary outputs (and Definition 3.2), we have that . As such, Eq. 10 in this setting is equivalent to the minimization of in Eq. 2 (with as all possible functions ). Through the specific selection of and restriction of , we have shown that rejection via idealized distributions generalizes the typical learning with rejection objective Eq. 2.

By utilizing form of -divergences, we find the form of the idealized rejection distributions and their corresponding density ratio used for rejection.

Theorem 3.3.

Given Definition 3.1, the optimal density ratio function of Eq. 9 is of the form,

| (11) |

where are Lagrange multipliers to ensure non-negativity ; and is a Lagrange multiplier to ensure the constraint is satisfied. Furthermore, the optimal idealized rejection distribution is given by: .

Connections to GVI and DRO

The formulation and solutions to the optimization of idealized distributions has several connections to GVI and DRO. In contrast to the setting of GVI, Eqs. 4 and 5, the support of the idealized distributions being learned in Definition 3.1 is w.r.t. inputs instead of parameters. Furthermore, the inner maximization of the DRO optimization problem, Eq. 7, seeks to solve a similar form of optimization. For idealized distributions, the maximization is switched to minimization and we consider a distribution over inputs instead of targets . Indeed, notice that the explicit inner optimization of DRO (in Eq. 7) over can be expressed as the following via the Fan’s minimax Theorem [25, Theorem 2]:

| (12) |

Notably, the loss in Eq. 7 can be simply negated to make the optimization over in Eq. 12 equivalent to DRO Eq. 8 (noting the only requirement for Eq. 7 to Eq. 12 is that is a linear functional of ). This shows that switching the sign of the loss function changes idealized distributions of Definition 3.1 to DRO adversarial distributions. Indeed, through the connection between our idealized distributions and DRO adversarial distributions, the distributions will have the same form as the optimal rejection distributions implicitly learned in DRO.

Corollary 3.4.

Suppose denotes the optimal idealized distribution in Theorem 3.3 (switching to ) for a fixed . Further let . Then the optimal adversarial distribution in the inner minimization for DRO (Eq. 7) is .

As such, the various optimal idealized distributions (w.r.t. Definition 3.1) for rejection we will present in the sequel can be directly used to obtain the optimal adversarial distributions for DRO.

4 Learning Idealized Distributions

In the following section, we explore optimal closed-form density ratio rejectors. We first examine the easiest example — the KL-divergence — and then consider the more general -divergences.

KL Divergence

Let us first consider the KL-divergence [2] for constructing density ratio rejectors.

Corollary 4.1.

Let and . The optimal density ratio of Definition 3.1 is,

| (13) |

One will notice that corresponds to an exponential tilt [24] of to yield a Gibbs distribution . The KL density ratio rejectors are significant in a few ways. First, from a closed-form solution perspective, due to the properties of ‘’ and complementary slackness, . Secondly, due to the properties of , the normalization term has a closed form solution given by the typical log-normalizer term of exponential families.

Another notable property of utilizing a KL idealized distribution is that it recovers the previously mentioned optimal rejection policies for classical modelling with rejection via cost penalty.

Theorem 4.2 (Informal).

Given the CPE setting Theorem 2.1, if is optimal, then there exists a which is equivalent to the optimal rejectors in Theorem 2.1.

Theorem 4.2 states that the KL density rejectors (with correctly specified and ) with optimal predictors recovers the optimal rejectors of the typical rejection setting, i.e., Chow’s rule.

Until now, we have implicitly assumed that the true data distribution is accessible. In practice, we only have access empirical , defining subsequent rejectors . We show that for the KL rejector, is enough given the following generalization bound.

Theorem 4.3.

Assume we have bounded loss for , with h.p., and . Suppose , then with probability , we have that

where .

Looking at Theorem 4.3, essentially we pay a price in generalization for each element we are testing for rejection. For generalization, it is useful to consider how changes our rate in Theorem 4.3. If we assume that the test set is small in comparison to the samples used to generate empirical distribution , then the rate will dominate. A concrete example of this case is when is finite. A less advantaged scenario is when , yielding — the scenario where we test approximately the same number of data points as that used to learn the rejector. This rate will still decrease with , although with a price.

-Divergences

Although the general case of finding idealized rejection distributions for -divergences is difficult, we examine a specific generalization of the KL case, the -divergences [3].

Definition 4.4.

For , the -divergence is defined as the -divergence, where

We further define , where when and when .

Note that taking recover the KL-divergence. The -divergence covers a wide range of divergences including the Pearson divergence . For the density ratio, -divergences with (i.e. not KL) can be characterized as the following.

Theorem 4.5.

Let and . For , the optimal density ratio rejector is,

| (14) |

are Lagrange multipliers for positivity; and is a Lagrange multiplier for normalization.

One major downside of using general -divergences is that solving the Lagrange multipliers for the idealized rejection distribution is often difficult. Indeed, the “” and “” ensures non-negativity of the idealized distribution when the input data is in the interior of the simplex; and also provides a convenient normalization calculation. For -divergences, the non-negative Lagrange multipliers can be directly solved given certain conditions.

Corollary 4.6.

Suppose and , then Eq. 14 simplifies to,

| (15) |

where we take non-integer powers of negative values as 0.

On the other hand, for , whenever is on the boundary whenever is not on the boundary [3, Section 3.4.1]. As such, we can partially simplify Eq. 14 for .

Corollary 4.7.

Suppose , , and lies in the simplex interior, then in Eq. 14.

Both Corollaries 4.6 and 4.7 can provide a unique rejector policy than the KL-divergence variant. Corollary 4.7 can provide a similar effect when for all . Nevertheless, having to determine which inputs and solving these values are difficult in practice. As such, we focus on . If there are values of with high risk, the will flatten these inputs to in Corollary 4.6. However, if the original model performs well and is relatively small for all , then it is possible that the is not utilized. In such a case, the -divergence rejectors can end up being similar — this follows the fact that (as ) locally all -divergences will be similar to the / -divergence [46, Theorem 7.20]. This ultimately results in -divergences being similar to, e.g., Chow’s rule when in classification via Theorem 2.1.

Among the cases, we examine the -divergence () which results in closed form for bounded loss functions and sufficient large regularizing parameter .

Corollary 4.8.

Suppose that and . Then,

| (16) |

The condition on for Corollary 4.8 is equivalent to rescaling bounded loss functions . Indeed, by fixing , we can achieve a similar Theorem with suitable rescaling of . Nevertheless, Eq. 16 provides a convenient form to allow for generalization bounds to be established.

Theorem 4.9.

Assume we have bounded loss for , , with h.p., and . Suppose , then with probability , we have that

Notice that Theorem 4.9’s sample complexity is equivalent to Theorem 4.3 up to constant multiplication. Hence, the analysis of Theorem 4.3 regarding the scales of hold for Theorem 4.9.

A question pertaining to DRO is what would be the generalization capabilities of the corresponding adversarial distributions (through Corollary 3.4). On a finite domain, via Theorems 4.3 and 4.9 and a simple triangle inequality, one can immediately bound the total variation , see Appendix M for further details.

Practical Rejection

In the following, we consider practical concerns for utilizing rejector for the KL-or -divergence case, Eqs. 13 and 15. To do so, we need to estimate the loss and rejector normalizer or .

Loss: The former is tricky, we require an estimate to evaluate over any possible to allow us to make a rejection decision. Implicitly, this requires us to have a high quality estimate of . In a general learning setting, this can be difficult to obtain — in fact it is just the overall objective that we are trying to learning, i.e., predicting a target given an input . However, in the case of CPE (classification), it is not unreasonable to obtain an calibrated estimate of via the classifier [45]. In Section 5, we utilize temperature scaling to calibrate the neural networks we learn to provide such an estimate [29]. Hence, we set . For proper CPE loss functions, acts as a generalized entropy function. As such, the rejectors Eqs. 13 and 15 act as functions over said generalized entropy functions.

Normalization: For the latter, we utilize a sample based estimate (over the dataset used to train the rejector) of is utilized to solve the normalizers and . In the case of the KL-divergence rejector, this is all that is required due to the convenient function form of the Gibbs distribution, i.e., the normalizer can be simply estimated by a sample mean. However, for -divergences needs to be found to determine the normalization. Practically, we find through bisection search of

This practically works as the optimization is over a single dimension. Furthermore, we can have that . As an upper bound over the possible values of , we utilize a heuristic where we multiple the corresponding maximum of with a constant.

Cut-off : In addition to learning the density ratio, an additional consideration is how to tune in the rejection decision, Definition 3.2. Given a fixed density estimator , change amounts to changing the rate of rejection. We note that this problem is not limited to our density ratio rejectors, where approaches with rejectors via a (surrogate) minimization of Eq. 2 may be required multiple rounds of training with different rejection costs to find an accept rate of rejection. In our case, we have a fixed which allows easy tuning of given a validation dataset, similar to other confidence based rejection approaches, e.g., tuning a threshold for the margin of a classifier [7].

5 Experiments

In this section, we evaluate our distributional approach to rejection across a number of datasets. In particular, we consider the standard classification setting with an addition setting where uniform label noise is introduced [4, 27]. For our density ratio rejectors, we evaluate the KL-divergence based rejector (Corollary 4.1) and -based rejectors (Corollary 4.6) with 50 equidistant values. For our tests, we fix . Throughout our evaluation, we assume that a neural network (NN) model without rejection is accessible for all (applicable) approaches and this model is calibrated via temperature scaling [29]. As such, we use the practical considerations discussed in Section 4 for our density ratio rejectors. For our density ratio rejectors, we utilize the log-loss.

To evaluate our density ratio rejectors and baselines, we compare accuracy and acceptance coverage. Accuracy corresponds to the 0-1 loss in Eq. 1 and the acceptance coverage is the percentage of non-rejections in the test set. Ideally, a rejector smoothly trade-offs between accuracy and acceptance, i.e., a higher accuracy can be achieved by decreasing the acceptance coverage by rejecting more data. We study this trade-off by examining multiple cut-off values and rejection costs .

Dataset and Baselines

We consider 3 multiclass classification datasets.

For tabular datasets, we consider the gas drift dataset [56] and the human activity recognition (HAR) dataset [5].

Each of these datasets consists of 6 class labels to predict. Furthermore, we utilize a two hidden layer multilayer perceptron NN model for these datasets.

In addition we consider the MNIST image dataset [37], where we utilize a convolutional NN. These prediction models are trained utilizing the standard logistic / log-loss without rejection and then are calibrated.

For each of these datasets, we utilize a clean and noisy variant. For the noisy variant, we flip the class labels of the train set with a rate of 25%.

We note that the test set is clean in both cases.

All evaluation uses 5-fold cross validation. All implementation are done using PyTorch and are trained using a p3.2xlarge instance on AWS.

We consider 4 different baseline for comparison. Each baseline is trained with 50 equidistant costs . One baseline used in comparison is Mozannar and Sontag [40]’s cross-entropy surrogate approach (DEFER) which reduces the multi-class classification problem into a multi-class classification problem, treating the rejection option as a separate class. A generalization of DEFER is also considered [13] where we change the surrogate loss of cross-entropy to generalized cross-entropy [61] (GCE). We also consider a cost-sensitive classification reduction (CSS) of the classification with rejection problem [14] utilizing the sigmoid loss function. The aforementioned 3 baselines all learn a model with rejection simultaneously, i.e., a pretrained model cannot be utilized. We also consider a two stage predictor-rejector approach (PredRej) which learns a rejector from a pretrained classifier [39].

Results

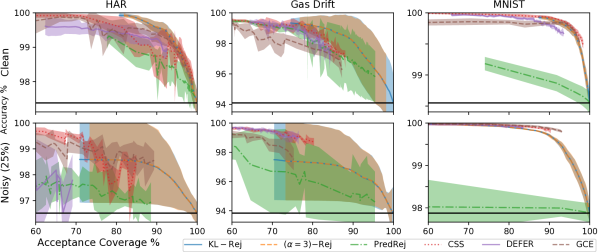

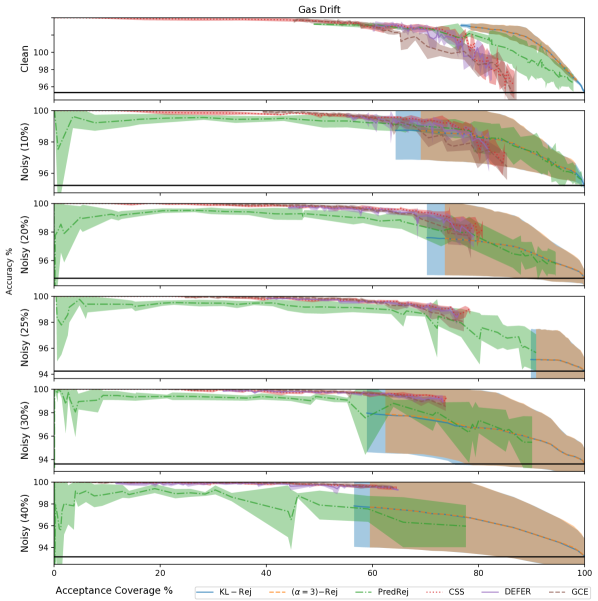

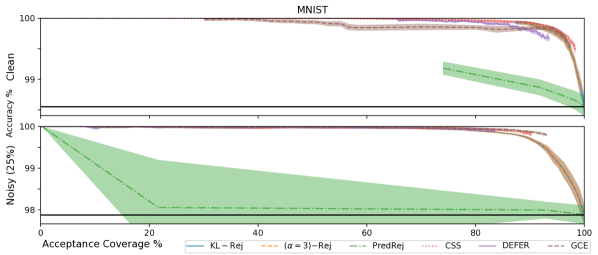

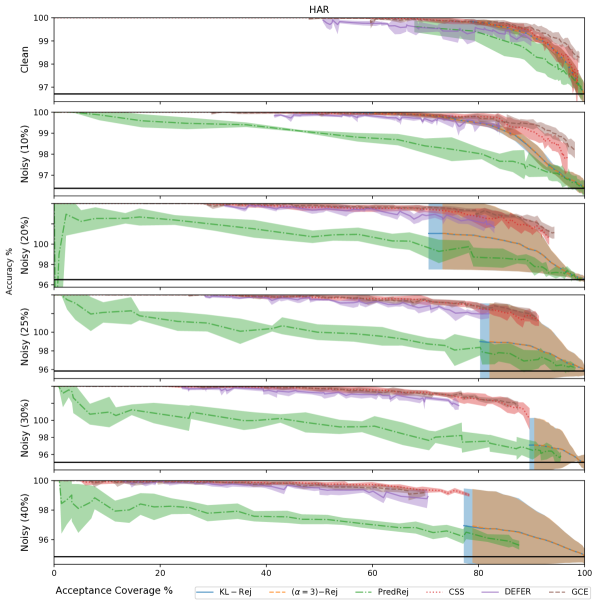

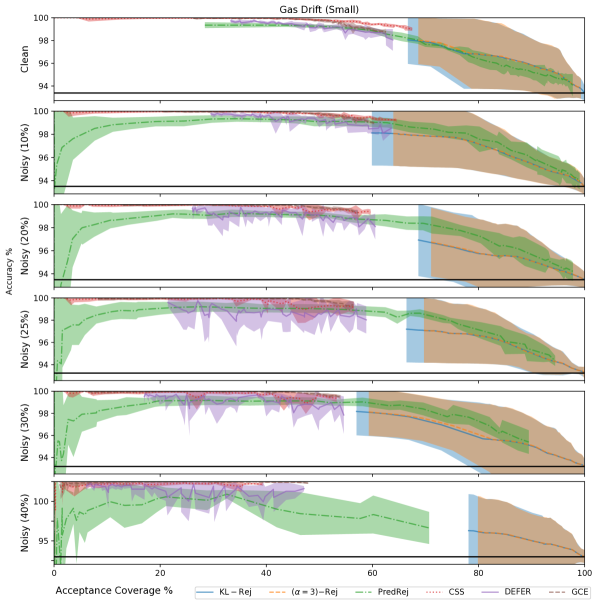

Fig. 2 presents a summary plot of the acceptance coverage versus model accuracy after rejection on the test set. The plot is focused around the 60% to 100% coverage region, with an extend plot presented in Appendix P. Over all folds for MNIST our density ratio rejectors take approximately hour to fit. A single baseline (fixed ) takes upwards of 2 hour for a single fold. Overall, given that the underlying model is calibrated, we find that our KL-divergence and -divergence density ratio rejector are either competitive or superior to the baselines. The baselines seem to become more competitive as noise increases, see Appendix P for further details. Furthermore, one might notice that the aforementioned baselines do not or provide poor trade-offs for coverage values . Indeed, to achieve rejection with high coverage (without architecture tuning), approaches which ‘wrap’ a base classifier seem preferable, i.e., PredRej and our density ratios rejectors. It should be noted that if large models are allowed to be used for the rejector — as per the MNIST case — CSS, DEFER, and GCE can provide superior accuracy vs acceptance coverage trade-offs (Noisy MNIST).

Among the approaches which ‘wrap’ the base classifier , we find that these approaches have higher variance ranges than the other approaches. In particular, the randomness of the base model potentially magnifies the randomness after rejection. The variance range of the base model tends to increase as the noise increases (additional ranges of noise for HAR and Gas Drift are presented in the Appendix). The influence on rejection is unsurprising as these ‘wrapping’ approaches predict via a composition of the original model (and hence inherits its randomness across folds). In general, our density ratio rejector outperforms PredRej. However, it should be noted that PredRej does not require a calibrated classifier. Among the density ratio rejectors, between KL and , the only variation is in coverage region that the threshold covers. This follows from the fact that for similar distributions, -divergences act similarly [46, Theorem 7.20]. We find this pattern holds for other values of .

6 Limitations and Conclusions

We propose a new framework for rejection by learning idealized density ratios. Our proposed rejection framework links typically explored classification with rejection to generalized variational inference and distributionally robust optimization. It should be noted that although we have focused on classification, could in theory be replaced by any other loss functions. In this sense, one could adapt this approach to other learning tasks such as regression, discussed in Appendix N. Furthermore, although we have focused on -divergences, there are many alternative ways idealized distribution can be constructed, e.g., integral probability metrics [42, 9]. One limitation of our distributional way of rejecting is the reliance on approximating with model . Alternatively, in future work, one may seek to approximate the density ratio by explicitly learning densities and or via gradient based methods (for the latter, see Appendix O).

References

- Ali and Silvey [1966] Syed Mumtaz Ali and Samuel D Silvey. A general class of coefficients of divergence of one distribution from another. Journal of the Royal Statistical Society: Series B (Methodological), 28(1):131–142, 1966.

- Amari and Nagaoka [2000] S.-I. Amari and H. Nagaoka. Methods of Information Geometry. Oxford University Press, 2000.

- Amari [2016] Shun-ichi Amari. Information geometry and its applications, volume 194. Springer, 2016.

- Angluin and Laird [1988] Dana Angluin and Philip Laird. Learning from noisy examples. Machine learning, 2:343–370, 1988.

- Anguita et al. [2013] Davide Anguita, Alessandro Ghio, Luca Oneto, Xavier Parra, Jorge Luis Reyes-Ortiz, et al. A public domain dataset for human activity recognition using smartphones. In Esann, volume 3, page 3, 2013.

- Asuncion and Newman [2007] Arthur Asuncion and David Newman. Uci machine learning repository, 2007.

- Bartlett and Wegkamp [2008] Peter L Bartlett and Marten H Wegkamp. Classification with a reject option using a hinge loss. Journal of Machine Learning Research, 9(8), 2008.

- Ben-Tal et al. [2013] Aharon Ben-Tal, Dick Den Hertog, Anja De Waegenaere, Bertrand Melenberg, and Gijs Rennen. Robust solutions of optimization problems affected by uncertain probabilities. Management Science, 59(2):341–357, 2013.

- Birrell et al. [2022] Jeremiah Birrell, Paul Dupuis, Markos A Katsoulakis, Yannis Pantazis, and Luc Rey-Bellet. -Divergences: interpolating between -divergences and integral probability metrics. The Journal of Machine Learning Research, 23(1):1816–1885, 2022.

- Blanchet and Murthy [2019] Jose Blanchet and Karthyek Murthy. Quantifying distributional model risk via optimal transport. Mathematics of Operations Research, 44(2):565–600, 2019.

- Blanchet et al. [2019] Jose Blanchet, Yang Kang, and Karthyek Murthy. Robust wasserstein profile inference and applications to machine learning. Journal of Applied Probability, 56(3):830–857, 2019.

- Boucheron et al. [2013] Stéphane Boucheron, Gábor Lugosi, and Pascal Massart. Concentration Inequalities: A Nonasymptotic Theory of Independence. Oxford University Press, 02 2013. ISBN 9780199535255. doi: 10.1093/acprof:oso/9780199535255.001.0001. URL https://doi.org/10.1093/acprof:oso/9780199535255.001.0001.

- Cao et al. [2022] Yuzhou Cao, Tianchi Cai, Lei Feng, Lihong Gu, Jinjie Gu, Bo An, Gang Niu, and Masashi Sugiyama. Generalizing consistent multi-class classification with rejection to be compatible with arbitrary losses. Advances in Neural Information Processing Systems, 35:521–534, 2022.

- Charoenphakdee et al. [2021] Nontawat Charoenphakdee, Zhenghang Cui, Yivan Zhang, and Masashi Sugiyama. Classification with rejection based on cost-sensitive classification. In International Conference on Machine Learning, pages 1507–1517. PMLR, 2021.

- Chow [1970] C Chow. On optimum recognition error and reject tradeoff. IEEE Transactions on information theory, 16(1):41–46, 1970.

- Cortes et al. [2016a] Corinna Cortes, Giulia DeSalvo, and Mehryar Mohri. Boosting with abstention. Advances in Neural Information Processing Systems, 29, 2016a.

- Cortes et al. [2016b] Corinna Cortes, Giulia DeSalvo, and Mehryar Mohri. Learning with rejection. In Algorithmic Learning Theory: 27th International Conference, ALT 2016, Bari, Italy, October 19-21, 2016, Proceedings 27, pages 67–82. Springer, 2016b.

- Csiszár [1964] Imre Csiszár. Eine informationstheoretische ungleichung und ihre anwendung auf beweis der ergodizitaet von markoffschen ketten. Magyer Tud. Akad. Mat. Kutato Int. Koezl., 8:85–108, 1964.

- Csiszár [1967] Imre Csiszár. Information-type measures of difference of probability distributions and indirect observation. studia scientiarum Mathematicarum Hungarica, 2:229–318, 1967.

- Csiszár et al. [2004] Imre Csiszár, Paul C Shields, et al. Information theory and statistics: A tutorial. Foundations and Trends® in Communications and Information Theory, 1(4):417–528, 2004.

- Duchi and Namkoong [2019] John Duchi and Hongseok Namkoong. Variance-based regularization with convex objectives. The Journal of Machine Learning Research, 20(1):2450–2504, 2019.

- Duchi et al. [2021] John C Duchi, Peter W Glynn, and Hongseok Namkoong. Statistics of robust optimization: A generalized empirical likelihood approach. Mathematics of Operations Research, 46(3):946–969, 2021.

- Dvijotham et al. [2019] Krishnamurthy Dj Dvijotham, Jamie Hayes, Borja Balle, Zico Kolter, Chongli Qin, Andras Gyorgy, Kai Xiao, Sven Gowal, and Pushmeet Kohli. A framework for robustness certification of smoothed classifiers using f-divergences. In International Conference on Learning Representations, 2019.

- Efron [2022] Bradley Efron. Exponential families in theory and practice. Cambridge University Press, 2022.

- Fan [1953] Ky Fan. Minimax theorems. Proceedings of the National Academy of Sciences of the United States of America, 39(1):42, 1953.

- Geifman and El-Yaniv [2017] Yonatan Geifman and Ran El-Yaniv. Selective classification for deep neural networks. Advances in neural information processing systems, 30, 2017.

- Ghosh et al. [2015] Aritra Ghosh, Naresh Manwani, and PS Sastry. Making risk minimization tolerant to label noise. Neurocomputing, 160:93–107, 2015.

- Grandvalet et al. [2008] Yves Grandvalet, Alain Rakotomamonjy, Joseph Keshet, and Stéphane Canu. Support vector machines with a reject option. Advances in neural information processing systems, 21, 2008.

- Guo et al. [2017] Chuan Guo, Geoff Pleiss, Yu Sun, and Kilian Q Weinberger. On calibration of modern neural networks. In International conference on machine learning, pages 1321–1330. PMLR, 2017.

- Husain [2020] Hisham Husain. Distributional robustness with ipms and links to regularization and gans. Advances in Neural Information Processing Systems, 33:11816–11827, 2020.

- Husain and Knoblauch [2022] Hisham Husain and Jeremias Knoblauch. Adversarial interpretation of bayesian inference. In International Conference on Algorithmic Learning Theory, pages 553–572. PMLR, 2022.

- Ioffe and Szegedy [2015] Sergey Ioffe and Christian Szegedy. Batch normalization: Accelerating deep network training by reducing internal covariate shift. In International conference on machine learning, pages 448–456. pmlr, 2015.

- Kingma and Welling [2013] Diederik P Kingma and Max Welling. Auto-encoding variational bayes. arXiv preprint arXiv:1312.6114, 2013.

- Knoblauch et al. [2022] Jeremias Knoblauch, Jack Jewson, and Theodoros Damoulas. An optimization-centric view on bayes’ rule: Reviewing and generalizing variational inference. The Journal of Machine Learning Research, 23(1):5789–5897, 2022.

- Knuth [1992] Donald E Knuth. Two notes on notation. The American Mathematical Monthly, 99(5):403–422, 1992.

- Lam [2016] Henry Lam. Robust sensitivity analysis for stochastic systems. Mathematics of Operations Research, 41(4):1248–1275, 2016.

- LeCun [1998] Yann LeCun. The mnist database of handwritten digits. http://yann. lecun. com/exdb/mnist/, 1998.

- Manwani et al. [2015] Naresh Manwani, Kalpit Desai, Sanand Sasidharan, and Ramasubramanian Sundararajan. Double ramp loss based reject option classifier. In Pacific-Asia Conference on Knowledge Discovery and Data Mining, pages 151–163. Springer, 2015.

- Mao et al. [2024] Anqi Mao, Mehryar Mohri, and Yutao Zhong. Predictor-rejector multi-class abstention: Theoretical analysis and algorithms. In International Conference on Algorithmic Learning Theory, pages 822–867. PMLR, 2024.

- Mozannar and Sontag [2020] Hussein Mozannar and David Sontag. Consistent estimators for learning to defer to an expert. In International Conference on Machine Learning, pages 7076–7087. PMLR, 2020.

- Mozannar et al. [2023] Hussein Mozannar, Hunter Lang, Dennis Wei, Prasanna Sattigeri, Subhro Das, and David Sontag. Who should predict? exact algorithms for learning to defer to humans. In International Conference on Artificial Intelligence and Statistics, pages 10520–10545. PMLR, 2023.

- Müller [1997] Alfred Müller. Integral probability metrics and their generating classes of functions. Advances in Applied Probability, 29(2):429–443, 1997.

- Narasimhan et al. [2022] Harikrishna Narasimhan, Wittawat Jitkrittum, Aditya K Menon, Ankit Rawat, and Sanjiv Kumar. Post-hoc estimators for learning to defer to an expert. Advances in Neural Information Processing Systems, 35:29292–29304, 2022.

- Ni et al. [2019] Chenri Ni, Nontawat Charoenphakdee, Junya Honda, and Masashi Sugiyama. On the calibration of multiclass classification with rejection. Advances in Neural Information Processing Systems, 32, 2019.

- Platt et al. [1999] John Platt et al. Probabilistic outputs for support vector machines and comparisons to regularized likelihood methods. Advances in large margin classifiers, 10(3):61–74, 1999.

- Polyanskiy and Wu [2022] Yury Polyanskiy and Yihong Wu. Information theory: From coding to learning. Book draft, 2022.

- Ramaswamy et al. [2018] H. G. Ramaswamy, Ambuj Tewari, and Shivani Agarwal. Consistent algorithms for multiclass classification with an abstain option. Electronic Journal of Statistics, 12:530–554, 2018. URL https://api.semanticscholar.org/CorpusID:126332033.

- Reid and Williamson [2010] Mark D Reid and Robert C Williamson. Composite binary losses. The Journal of Machine Learning Research, 11:2387–2422, 2010.

- Reid and Williamson [2011] Mark D Reid and Robert C Williamson. Information, divergence and risk for binary experiments. Journal of Machine Learning Research, 12:731–817, 2011.

- Sason and Verdú [2016] Igal Sason and Sergio Verdú. -divergence inequalities. IEEE Transactions on Information Theory, 62(11):5973–6006, 2016.

- Scarf [1957] Herbert E Scarf. A min-max solution of an inventory problem. Technical report, RAND CORP SANTA MONICA CALIF, 1957.

- Sinha et al. [2018] Aman Sinha, Hongseok Namkoong, and John Duchi. Certifiable distributional robustness with principled adversarial training. In International Conference on Learning Representations, 2018. URL https://openreview.net/forum?id=Hk6kPgZA-.

- Srivastava et al. [2014] Nitish Srivastava, Geoffrey Hinton, Alex Krizhevsky, Ilya Sutskever, and Ruslan Salakhutdinov. Dropout: a simple way to prevent neural networks from overfitting. The journal of machine learning research, 15(1):1929–1958, 2014.

- Staib and Jegelka [2019] Matthew Staib and Stefanie Jegelka. Distributionally robust optimization and generalization in kernel methods. In Advances in Neural Information Processing Systems, pages 9131–9141, 2019.

- Sugiyama et al. [2012] Masashi Sugiyama, Taiji Suzuki, and Takafumi Kanamori. Density ratio estimation in machine learning. Cambridge University Press, 2012.

- Vergara et al. [2012] Alexander Vergara, Shankar Vembu, Tuba Ayhan, Margaret A Ryan, Margie L Homer, and Ramón Huerta. Chemical gas sensor drift compensation using classifier ensembles. Sensors and Actuators B: Chemical, 166:320–329, 2012.

- Yuan and Wegkamp [2010] Ming Yuan and Marten Wegkamp. Classification methods with reject option based on convex risk minimization. Journal of Machine Learning Research, 11(1), 2010.

- Zaoui et al. [2020] Ahmed Zaoui, Christophe Denis, and Mohamed Hebiri. Regression with reject option and application to knn. Advances in Neural Information Processing Systems, 33:20073–20082, 2020.

- Zellner [1988] Arnold Zellner. Optimal information processing and bayes’s theorem. American Statistician, pages 278–280, 1988.

- Zhang et al. [2021] Jingzhao Zhang, Aditya Krishna Menon, Andreas Veit, Srinadh Bhojanapalli, Sanjiv Kumar, and Suvrit Sra. Coping with label shift via distributionally robust optimisation. In International Conference on Learning Representations, 2021. URL https://openreview.net/forum?id=BtZhsSGNRNi.

- Zhang and Sabuncu [2018] Zhilu Zhang and Mert Sabuncu. Generalized cross entropy loss for training deep neural networks with noisy labels. Advances in neural information processing systems, 31, 2018.

Supplementary Material

This is the Supplementary Material to Paper "Rejection via Learning Density Ratios". To differentiate with the numberings in the main file, the numbering of Theorems is letter-based (A, B, …).

Table of contents

Proof

Appendix A: Proof of Theorem 2.1 Pg A

Appendix B: Proof of Theorem 3.3 Pg B

Appendix C: Proof of Corollary 3.4 Pg C

Appendix D: Proof of Corollary 4.1 Pg D

Appendix E: Proof of Theorem 4.2 Pg E

Appendix F: Proof of Theorem 4.3 Pg F

Appendix G: Proof of Theorem 4.5 Pg G

Appendix H: Proof of Corollary 4.6 Pg H

Appendix I: Proof of Corollary 4.7 Pg I

Appendix J: Proof of Corollary 4.8 Pg J

Appendix K: Proof of Theorem 4.9 Pg K

Deferred Content

Appendix L: Broader Impact Pg L

Appendix M: Distribution Generalization Bounds Pg M

Appendix N: Rejection for Regression Pg N

Appendix O: Gradient of Density Ratio Objective Pg O

Appendix P: Additional Experimental Details Pg P

Appendix A Proof of Theorem 2.1

Proof.

We first rewrite the coverage probability as an expectation:

We note that point-wise, the proper loss is minimized by taking the Bayes optimal classifier . Thus taking the over all possible CPE classifiers, . We note that the point-wise risk taken by the Bayes optimal classifier is typical denoted as the Bayes point-wise risk [48, 49].

As such, we are left to minimize over,

Thus, we immediately get the optimal . ∎

Appendix B Proof of Theorem 3.3

Proof.

We use the theory of Lagrange multipliers to make different constraints explicit optimization problems.

Let us first consider the reduction from learing explicit distributions Eq. 8 to density ratios Eq. 9. First note that the objective Eq. 8 can be written as follows:

The reduction to Eq. 9 now follows from a reduction from minimizing over to , noting that is restricted to be on the simplex. As such, the simplex constraints are transfered to:

where the former is the non-negativity of simplex elements and the latter is the normalization requirement. Hence, taking completes the reduction. (we remove the subscript “” for the rest of the proof)

As such we have the optimization problem in Eq. 9, where we will convert the constraints into Lagrange multipliers, defining,

where .

We can obtain the first order optimality conditions by taking the functional derivative. Suppose that and is any function. The functional derivative is given by,

Thus, the first order condition is,

for all . As the condition must hold for all for an optimal , we have that for all ,

As required. ∎

Appendix C Proof of Corollary 3.4

Proof.

First notice that the inner maximization in the DRO optimization Eq. 7 can be simplified as follows:

where the last inequality follows from Fan’s minimax Theorem [25, Theorem 2] noting that is linear and the selected per Definition 2.2 makes a convex lower semi-continuous function.

Now notice that the inner minimization of this simplification is exactly our idealized rejection distribution objective Eq. 8 when we negate the loss. As such, noticing that solutions to Eq. 8 are exactly given by yields the result after optimizing for the ‘arguments’ in the above DRO objective for both and . ∎

Appendix D Proof of Corollary 4.1

We defer the proof of Corollary 4.1 to Appendix G, which covers any including KL ().

Appendix E Proof of Theorem 4.2

We breakdown Theorem 4.2 into two sub-theorems Theorem E.1 for each of the settings.

Theorem E.1.

Given the binary CPE setting presented in Theorem 2.1 and that we are given the optimal classifier , for any there exists a such that the rejector generated the optimal density ratio in Corollary 4.1 is equivalent to the optimal rejector in Theorem 2.1.

The proofs of each are similar. We first make the observation that the rejector function can be simplified as follows:

Now we note that given a fixed (which also fixes ), the RHS term has a one-to-one mapping from to . Thus all that is to verify is that thresholding is equivalent to the rejectors of Theorems 2.1 and N.1.

Proof.

For the CPE case, from assumptions, we have that as is optimal. Thus thresholding used in is equivalent to thresholding by keeping fixed and changine appropriately. ∎

Appendix F Proof of Theorem 4.3

To prove the theorem, we will be using the standard Hoeffding’s inequality [12].

Theorem F.1 (Hoeffding’s Inequality [12, Theorem 2.8]).

Let be independent random variables such that takes values in almost surely for all . Defining , then for every ,

Proof.

Let us denote to be the normalizer with the true expectation and to be the normalizer with the empirical expectation .

As is bounded, we take note of the following bounds,

This can be simply verified by taking the smallest and largest values of the .

Now we simply have

Notice that can be bounded via concentration inequality on (bounded) random variable .

Taking a union bound over , we have that

Thus taking , we have that with probability for , for any ,

As required.

∎

Appendix G Proof of Theorem 4.5

Before proving the theorems, we first state some basic properties of .

Lemma G.1.

For , and . Furthermore, these statements hold when is replaced with .

Lemma G.2.

| (17) |

The above statements follows directly from definition and simple calculation. The next statement directly connects to .

Lemma G.3.

For ,

| (18) |

Proof.

We prove this via cases.

:

:

∎

We now define the following constants depending on :

| (19) |

Lemma G.4.

For ,

| (20) |

Proof.

We prove this via cases.

:

Then,

:

Then,

∎

Lemma G.5.

For ,

| (21) |

Proof.

:

Then,

∎

Thus now via Lemmas G.4 and G.5, we can prove the Theorems.

Proof of Corollaries 4.1 and 4.5.

The proof follows from utilizing either Lemmas G.4 and G.5 in conjunction with Theorem 3.3.

: We have that,

As for is already positive by ‘’, by complementary slackness, the Lagrange multipliers . Hence, we can further simplify the above,

The normalizer then can be easily calculated, renaming , we simplify have that

which by normalization condition and setting ,

which completes the case (Corollary 4.1).

Appendix H Proof of Corollary 4.6

Proof.

First we simplify the density ratio rejector.

We suppose that it is possible for

for values of , , and . Otherwise, and we are done due to the above equation’s non-negativity.

Let be arbitrary. Suppose that . Then by complementary slackness, we have that

By contra-positive, we have that implies that . By prime feasibility, in this case we also have . We can solve either case by using the maximum as stated. ∎

Appendix I Proof of Corollary 4.7

Proof of Corollary 4.6.

The proof directly follows from a property of the -divergence when one of the measure have disjoint support. From [3] we have.

Theorem I.1 (Amari [3, Section 3.4.1 (4)]).

For -divergences, we have that

-

1.

For , when and for some .

This result immediately gives the result, as otherwise the objective function is . ∎

Appendix J Proof of Corollary 4.8

Proof.

Now, consider the following,

where the latter holds uniformly for all from assumptions on .

Thus setting , we simplify

As such, solves the required normalization. Substituting back into yields the Theorem. ∎

Appendix K Proof of Theorem 4.9

Proof.

First we note that for any meas , implies that (taking largest and smallest values of .

As such, for both have closed forms Corollary 4.8

Thus, the bound can be simply shown to have,

Thus by Hoeffding’s inequality Theorem F.1 and union bound (see for instance the proof of Theorem 4.3), setting , we have that with probability for all ,

As required. ∎

Appendix L Broader Impact

The paper presents work which reinterprets the classification with rejection problem in terms of learning distributions and density ratios. Beyond advancing Machine Learning in general, potential societal consequences include enhancing the understanding of the rejection paradigm and, consequentially, the human-in-the-loop paradigm. The general rejection setting aims to prevent models from making prediction when they are not confident, which can have societal significance when deployed in high stakes real life scenarios — allowing for human intervention.

Appendix M Distribution Generalization Bounds

In the following, we seek to provide generalization bounds on . That is, one seeks to know that as how and if . A natural measure of distance for probability measures is total variation [20],

Let us also define

One immediately gets a rate if we assume that is finite and we have a bound for .

Theorem M.1.

Suppose that is finite and bounded density ratio for . Then, if we have that with probability that ,

for some , then we have that

| (22) |

Proof.

Noting that the empirical distribution is a sum of Dirac deltas , we can establish a simple bound via a consequence of Hoeffding’s Theorem Theorem F.1 (also noting that ). We have that,

Thus,

Setting , we have with probability

We now consider the following:

Taking a union bound of the above inequality and our assumption, we have that, for some , with probability ,

Converting the bound to TV amounts to simply summing over , which gives , as required. ∎

Notably, with appropriate assumptions, Theorems 4.3 and 4.9 can be used with Theorem M.1 to get bounds for and .

Appendix N Rejection for Regression

In the main-text of the paper we have focused on classification. However, many of the idea discussed can be extended for the regression setting. For instance, similar to Chow’s Rule in Theorem 2.1 we can express the regression equivalent to the optimal solution of Eq. 2.

Theorem N.1 (Optimal Regression Rejection [58]).

Let us consider the regression setting, where and . Then w.r.t. Eq. 2, the optimal model is given by and the optimal rejector is given by , where is the conditional variance of given .

For regression, there is no clear analogous notion of output “confidence score” unless the model explicitly outputs probabilities. Indeed, rejection method for regression explicitly requires the estimation of the target variable’s conditional variance [58].

Similar to the CPE case, our KL density ratio rejector can provide a rejection policy equivalent to the typical case.

Theorem N.2.

Given the regression setting presented in Theorem N.1 and that we are given optimal regressor , for any there exists a such that the rejector generated the optimal density ratio in Corollary 4.1 is equivalent to the optimal rejector in Theorem N.1.

Proof.

The proof follows similarly to the proof of Theorem E.1. The regression case follows almost identically, by noticing that is the variance. This is similar to the proof of Theorem N.1 [58]. ∎

Despite the equivalence, there is a difficult in using the density ratio rejectors, as per the closed form equations of Section 4, for regression. Estimating is challenging. Unlike classification where learning calibrated classifiers has a variety of approaches, learning a regression model which explicitly outputs probabilities is quite difficult. As such, approximating with the model cannot be done.

Appendix O Gradient of Density Ratio Objective

As an alternative to the closed-form rejectors explored in the main-text, one may want to explore a method to learn iteratively. We consider the gradients of the optimization problem in Eq. 9. In practice, we found that we were unable to learn such rejectors via taking gradient updates and thus leave a concrete implementation of the idea for future work.

The idea comes from utilizing the “variational” aspect of the GVI formulation (which was not explored in the main-text). We suppose that the rejectors we are interested in come from a parameterized family. In particular, we consider the self-normalizing family , where normalizes the rejector such that . Having the normalizing term means that the constraint in Eq. 9 is satisfied for any . The only constraint that we must have for is non-negativity, i.e., is a neural network with exponential last activation functions from . By setting a parametric form of , we implicitly restrict the set of idealized distributions to . The gradients of such a parametric form can be calculated as follows.

Corollary O.1.

Let . Then the gradient of Eq. 9 w.r.t. is given by,

| (23) |

Proof.

The proof is immediate from differentiation of Eq. 9. ∎

An alternative form of Eq. 23 can be found by noticing that . This provides an expression in terms of the log density ratio.

One will notice that the gradient is in-fact the log-likelihood of the idealized distribution: noting free of , we have . As such, the gradient Eq. 23 is equivalent to the gradient of a weighted log-likelihood.

Despite the potential nice form of the gradient, we found that learning rejector through this was not possible. One limiting factor of computing such gradients is that we need to estimate at each gradient calculation, i.e., this must happen whenever changes. This can be particularly costly when is high-dimensional. Secondly, we suspect that the model capacity of was not sufficient: we only tested on simple neural networks and convolutions neural networks, mirroring the architecture of the base classifiers used in our experimental setting.

Appendix P Additional Experimental Details

P.I Training Settings

The neural network architecture used to train the base classifiers and baselines are almost identical. For the baseline approaches which have output dimension which is different than the output of the original neural network, we modify the last linear layer of the base classifier’s architecture to fit the baseline’s requirements, e.g., adding an additional output dimension for rejection in DEFER. Our architectures utilize batch normalization [32] and dropout [53] in a variety of places. Training settings are mostly identical, with some baselines requiring slight changes.

The base model’s architecture is as follows.

-

•

HAR (CC BY 4.0): We utilize a two hidden layer neural network with batch normalization. Both hidden layer is neurons and the activation function is the sigmoid function. We take a 64 batch size, 40 training epochs and a 0.0001 learning rate.

-

•

Gas Drift (CC BY 4.0): We utilize a two hidden layer neural network with batch normalization. Both hidden layers are neurons and the activation function is the sigmoid function. We take a 64 batch size, 40 training epochs and a 0.0001 learning rate.

-

•

MNIST (CC BY-SA 3.0): We utilize a convolutional neural network with two convolutional layers and two linear layers. The architecture follows directly from the MNIST example for PyTorch. We utilize the sigmoid function activation function. We take a 256 batch size, 40 training epochs and a 0.0001 learning rate.

For CSS, as noted in Ni et al. [44], batch normalization is needed at the final layer to stabilize training.

All training utilizes the Adam [33] optimizer.

All datasets we consider are in the public domain, e.g., UCI [6].

P.II Extended Plots

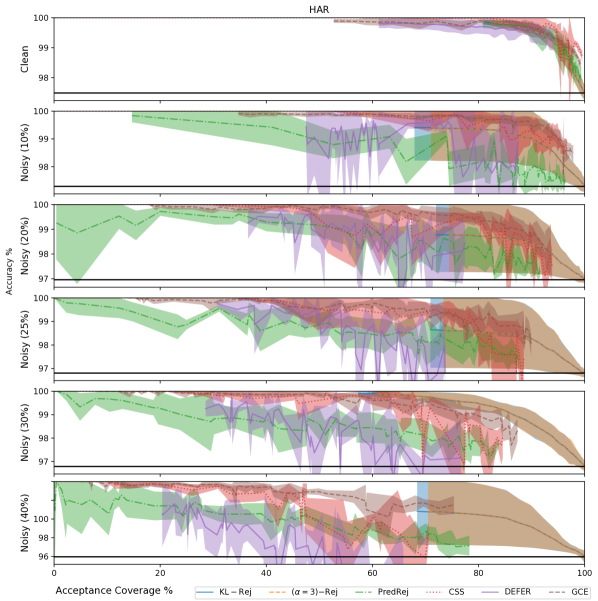

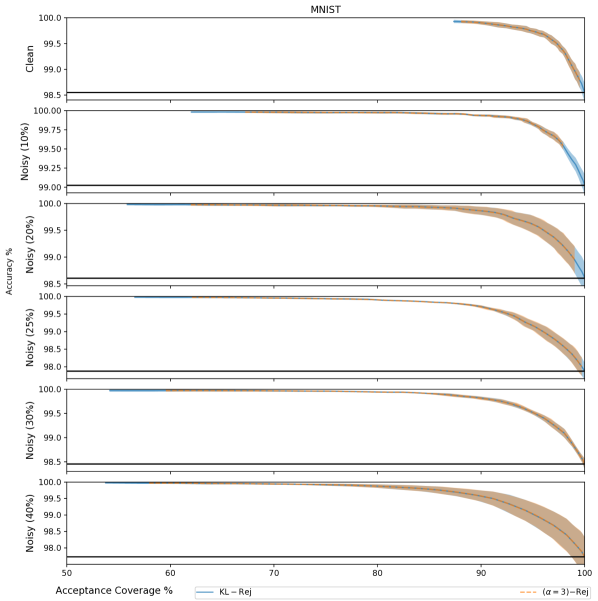

Plots Figs. I, II and III show Fig. 2 over and extend region of acceptable coverage percentages. In addition, we include a larger range of noise rates for HAR and Gas Drift. For MNIST, we explore a larger range of noise rates for MNIST in Fig. IV for our density ratio rejectors. We find that the findings in the main text are extended to these additional noise rates. In particular, we find that the our density ratio rejectors can be competitive with the various baseline approaches. We find that our density ratio approaches can have more fine-grained trade-offs at higher ranges of acceptance coverage. This is an important region where the budge for rejection may be low (and only a few examples, e.g. , can be rejected). Indeed, the baseline approaches which do not ‘wrap’ a base model require a lower maximum acceptance coverage as the noise rate increases (the approaches require a higher rejection % for any type of rejection). Nevertheless, we do see a downside of the density ratio approach: the quality of the density ratio rejectors is dependent on the initial model. As such, at higher levels of noise there can be higher variation in the quality of rejection, see Fig. II. Interestingly, for MNIST the base model the density ratio rejectors are more robust across noise rates than other models. This seems to be due to the default MNIST architecture being robust against higher noise rates (notice that the s.t.d. range is also quite small at 100% coverage).

P.III Smaller models case study

In the following, we consider the Gas Drift dataset when models are switched to a base model with only a single hidden layer. First we make note of the original setting explored in the main text. In Table I, we take note of the number of tunable parameters in all approaches and baselines. Notably, these default parameter / architecture sizes are similar to [14], with the HAR and Gas Drift setting including an additional hidden layer than previously utilized in the literature.

| Dataset | BaseClf | |||||

|---|---|---|---|---|---|---|

| HAR | 40,647 | 40,648 | 40,646 | 40,711 | 40,711 | 80,968 |

| Gas Drift | 12,935 | 12,936 | 12,934 | 12,999 | 12,999 | 25,544 |

| MNIST | 1,199,883 | 1,199,884 | 1,200,138 | 1,200,011 | 1,200,267 | 2,398,860 |

In Table II, we note the setting we consider in this subsection. The parameter sizes of the Gas Drift dataset is reduced to the originally explored model sizes in Charoenphakdee et al. [14]. Notice that both the base models and the baseline approaches have reduced parameter sizes. It should be noted that this smaller parameter size setting can be useful in the related learning with deferral setting [43], where having a small model to defer to a larger model is needed.

| Dataset | BaseClf | |||||

|---|---|---|---|---|---|---|

| HAR | 36,487 | 36,488 | 36,486 | 36,551 | 36,551 | 72,648 |

| Gas Drift | 8,775 | 8,776 | 8,774 | 8,839 | 8,839 | 17,224 |

The results are reported in Figs. V and VI. We can see that in this setting, PredRej and our density ratio approaches are more competitive. This might indicate that for simple base models, approaches which ‘wrap’ a base model for rejection can be quite effective (especially in higher coverage regimes). In general, it seems with this smaller architecture regime, the ‘non-wrapping’ baseline approaches only provide rejection options when the acceptance coverage is lower than .

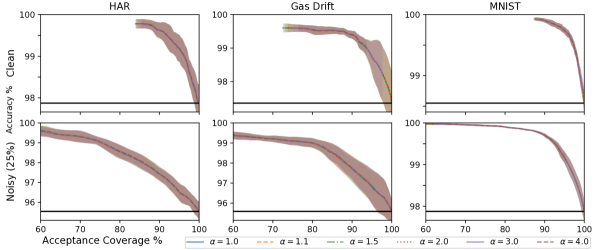

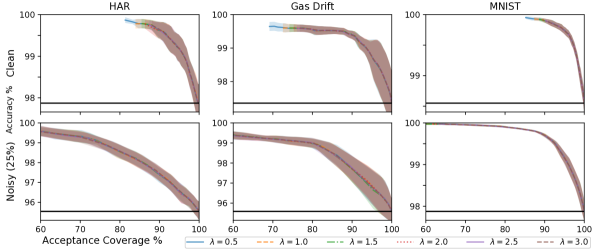

P.IV Parameter sweeps over and

The following shows parameter sweeps over and for our density ratio rejectors. These are given by Figs. VII and VIII respectively. We find that increasing compresses the trade-off curve from both sides. While decrease extends the trade-off curve on the left side.