Factor Augmented Matrix Regression

Abstract

We introduce Factor-Augmented Matrix Regression (FAMAR) to address the growing applications of matrix-variate data and their associated challenges, particularly with high-dimensionality and covariate correlations. FAMAR encompasses two key algorithms. The first is a novel non-iterative approach that efficiently estimates the factors and loadings of the matrix factor model, utilizing techniques of pre-training, diverse projection, and block-wise averaging. The second algorithm offers an accelerated solution for penalized matrix factor regression. Both algorithms are supported by established statistical and numerical convergence properties. Empirical evaluations, conducted on synthetic and real economics datasets, demonstrate FAMAR’s superiority in terms of accuracy, interpretability, and computational speed. Our application to economic data showcases how matrix factors can be incorporated to predict the GDPs of the countries of interest, and the influence of these factors on the GDPs.

Keywords: Matrix factor models; Matrix regression; Factor-augmented regression; Diversified projections; High-dimensionality.

1 Introduction

Matrix-variate data are commonly encountered in diverse domains nowadays, such as finance, economics, spatio-temporal data, healthcare, images, and social networks (Chen et al., 2020, 2023). In many problems, especially in high-dimensional regimes, it is common that matrix covariates assume low-rank structure or can be well approximated by low-rank matrices as exemplified by factor models (Wainwright, 2019; Chen & Fan, 2021). The outcomes of interest are directly influenced by latent low-rank matrix factors, not by the observable matrix covariates themselves. For instance, autism diagnosis relies on identifying specific patterns within brain connectivity networks, underscoring a direct link to reduced-dimensionality factors (Nogay & Adeli, 2020); regional GDP is shaped by the condensed economic indicators found within spatial-temporal housing data (Kopoin et al., 2013); and the GDP growth of countries is determined by underlying economic factors, demonstrating a direct relationship with these distilled elements (Banerjee et al., 2005).

To incorporate the matrix factor structure in matrix regressions, we introduce the Factor Augmented Matrix Regression (FAMAR) for observed random variables , in which is a scalar response of interest and is a covariate matrix, defined as

| (1) |

where is the latent factor matrix of lower dimensions for , is the unobserved idiosyncratic matrix, and of dimension and of dimension are the loading matrices of the Matrix Factor Model (MFM) (Chen & Fan, 2021). The impact of covariate matrix on outcome is through the latent factors and unobserved idiosyncratic matrix with matrices of dimension and of dimension as the regression coefficient matrices of the Matrix Factor Regression (MFR). As the first component in MFR is the low-dimensional factor effect, the coefficient can be estimated without any structures. We consider both sparse and low-rank structure for the regression coefficient matrix since it is high-dimensional.

As practitioners harness the power of various data, model (1) has wide applications in economics and finance. For example, represents the monthly GDP of a country of interest, and consists of the economic variables collected from different countries. Model (1) is able to separate economic common factor and idiosyncratic shocks and provide economists with their respective impacts on the GDP of one country of interest. A salient feature of model (1) is that the association between the response and the covariate matrix is established directly through the factor and idiosyncratic matrix . This structure makes covariate inputs much weakly correlated and relates to various traditional models, as illustrated below.

Example 1 (Matrix regression with MFM covariates).

While we directly observe , using the matrix regression model (2) might seem straightforward. The influence of the latent factor in model (2) is represented as . However, the general FAMAR model introduces , which quantifies the additional impact of the latent factor in model (1) that is not accounted for by the observed predictor in model (2).

Example 2 (Reduce-rank matrix regression).

Low-rank matrix regression corresponds to a special case of (1) with low-rank coefficient matrix , matrix factor and when does not admit a factor structure, and when it does.

Example 3 (Sparse matrix regression).

Sparse matrix regression is a special case of model (1) with sparse coefficient matrix , and has not low-rank component, i.e., and .

There are several advantages of considering the more general model (1). First, in reality, especially when the columns and rows of are highly correlated, the leading factors are likely to make additional contributions to the outcome, beyond a fixed portion represented by in model (2). To this end, model (1) involves incorporating the primary factors into a low-rank regression that extends the linear space defined by in useful ways by noting that using and as covariates are the same as the usage of and . In addition, even when model (2) is correctly specified, model (1) is helpful in dealing with the colinearity of due to the factor structure (Fan, Ke & Wang, 2020). This is also confirmed in our empirical analysis. When covariates are highly correlated, direct low-rank regression on ’s often overestimates the rank due to their dependency structure, reducing the effectiveness of regularization and the interpretability of estimation. FAMAR enhances performance by utilizing the space spanned by , which is the same as that span by , with augmented feature , capitalizing further on underlying information. Additionally, its factor model approach decorrelates the covariance matrix, leading to coefficient estimators that are both more interpretable and stable.

Factor augmentations in the vector contexts have been studied under various settings and shown to be powerful (Fan, Ke & Wang, 2020; Zhou et al., 2021; Fan & Gu, 2022; Fan et al., 2023). In contrast, little work has been done on the matrix-variate problems. Matrix-variate settings are intrinsically different because of their multidimensional structure, where low rankness comes into play. Linear and generalized matrix regression have been studied in Zhou & Li (2014); Wang et al. (2017); Fan et al. (2019). However, model (1) in the present paper is different in that the association between and is not direct as those in the literature but rather through the latent variables and . We present in the real data analysis that such an association provides better prediction and interpretation of the effect of common economic factors and idiosyncratic variables. In addition, existing estimation methods solving model (1) MFM entail spectral or iterative optimization methods (Chen et al., 2019; Chen & Fan, 2021; Liu & Chen, 2022; Yu et al., 2022). We propose a new non-iterative method, consisting of simple procedures of “Pre-Trained Projection” and “Block-Average-an-OLS”, to obtain good estimators of and from the MFM, which are of independent interest.

The rest of this paper is organized as follows. Section 2 develops the FAMAR method in details, including a new method for estimating the MFM parameters in model (1) in Section 2.1 and an efficient algorithm for solving MFR parameters in model (1) in Section 2.2. Section 3 establishes their theoretical properties. Sections 4 and 5 present empirical results on synthetic and real datasets. Section 6 concludes and discusses future works. All proofs are relegated to the supplementary material.

2 Factor-Augmented Matrix Regression

When the factors and the residuals are directly observable, unknown coefficients in model (1) can be obtained by a general matrix regression (Wainwright, 2019). In the more challenging setting where and are not directly observed, we need first to estimate from the observed matrix variate . Section 2.1 introduces a novel non-iterative estimation approach to obtain estimated and in model (1) that achieve optimal convergence rates. With these, to facilitate the estimation of under the high-dimensional setting, we could impose either low-rank or sparse structure on .

FAMAR with Low-Rank .

The low-rank structure on can be achieved by solving nuclear norm regularized matrix regression with an accelerated algorithm introduced in Section 2.2:

| (3) |

where denotes the nuclear norm of the matrix coefficient.

FAMAR with Sparse .

The overall sparsity structure on can be induced by using the norm on vectorized , akin to factor augmented regression in vector form (Fan, Ke & Wang, 2020; Fan et al., 2023). Specifically, the overall sparsity on can be achieved by solving the following optimization problem

| (4) |

We also note that FAMAR provides a broader range of sparsity options compared to its vector-based counterpart, thanks to the multi-dimensional nature of the coefficient matrix . This allows for the imposition of row-wise or column-wise sparsity in , an option not available in vector-based models. We establish theoretical guarantees for the overall sparsity structure with LASSO in Section 3.3.2. Theoretical analysis on FAMAR with row-wise or column-wise sparsity in can be carried out by applying, e.g., Yuan & Lin (2006); Obozinski et al. (2011); Hastie et al. (2015) in the theoretical frameworks presented therein and are left for future research.

2.1 Pre-Trained Projection and Block-Wise Averaging

We present an innovative non-iterative estimation approach that utilizes pre-training and exploits the unique structure inherent in Kronecker products. It consists of two major steps, namely “Pre-Trained Projection”, where we estimate the latent factor matrix by a one-time projection, and “Block-Averaging-an-OLS”, where we exploit the unique Kronecker structure and estimate by simple averaging in a block-wise fashion.

Estimating matrix factors by “Pre-Trained Projection”. The idea of pre-trained projection is inspired by the diversified projection proposed by Fan & Liao (2022) for the vector factor models. Here for the matrix factor model, we introduce “row and column diversified projection matrices” and in Definition 4. Accordingly, we can obtain a crude estimator of the matrix factor

| (5) |

Following from the matrix factor structure of , we have

| (6) |

where and are transformation matrices. A rotated version of (i.e. ) can be estimated by as long as the second idiosyncratic term in (6) is averaged away and the first signal term dominates the average of the noise in the second term. Formally, we characterize the desirable projection matrices as follows.

Definition 4 (Diversified projection matrices).

Let , be universal positive constants. Matrices and are said to be diversified projection matrices for MFM in (1) if they satisfy

-

(a)

and , where is the element-wise -norm.

-

(b)

The matrices and satisfy and , respectively.

-

(c)

are independent of .

Diversified projection matrices can be achieved in various ways (Fan & Liao, 2022; Fan & Gu, 2022), such as those based on observed characteristics, initial transformation, and the Hadamard projection. We consider the idea of “pre-trainning”, which is a data-driven method of constructing and by -PCA (Chen & Fan, 2021) through data splitting. Specifically, with a separate independent set of samples , we obtain and as the estimations of and utilizing the method of -PCA. As condition 4(b) does not require a consistent estimation, the pre-trained sample size can be a negligible fraction of sample size , as to be formally demonstrated. Then, with the sample of interest , we obtain an estimator of the matrix factor , using equation (5) with and as the diversified projection matrices.

Estimating the loading matrix by “Block-Averaging-an-OLS”. To estimate and , our proposed method averages over blocks of an OLS estimator of the vectorized MFM (1). The details and rationales are explained as follows. The vectorized model of MFM (1) with all samples stacked in rows can be written as , or equivalently,

| (7) |

where and are the transformation matrices defined in Definition 4, is an matrix whose -th row is the vectorized , and are matrices defined similarly, is the true loading matrix satisfying ,

| (8) |

are the rotated truth that our pre-trained projected estimators are targeting at.

Now with the vectorized estimator from the “pre-trained projection” that well approximates , the rotated loading matrix can be well-approximated by an OLS:

| (9) |

Our estimation target naturally admits a Kronecker product structure with

| (10) |

which are the rotated truth. To take advantage of such a structure, we use block averaging to improve the quality of estimation. Specifically, can be divided into blocks of matrices and the -th block is matrix , where is the -th element of . Denote as the matrix consisting of blocks of , we have that

and

where is the shuffle matrix defined by taking slices of the :

MATLAB colon notation is used here to indicate submatrices, where creates a regularly-spaced vector using as the increment between elements. This Kronecker structure enables us to refine by block-wise averaging. We define the averaging estimator

| (11) |

Therefore, two constants and can be estimated by and , respectively, where (resp. ) is the -th element of (resp. ). Accordingly, the estimator of the idiosyncratic matrix is given by

| (12) |

where is obtained by “pre-trained projection” and and are estimated by “block-averaging-an-OLS”. Note that , , and estimate the affine transformed version of , , and , while directly estimates .

2.2 Accelerated Algorithm for Solving Matrix Factor Regression

Using and estimated through pre-trained projection and block-averaging-an-OLS, we estimate the model coefficients and for the MFR (1) by applying Nesterov’s accelerated iterative algorithm (Nesterov, 2013; Ji & Ye, 2009) to solve the optimization program (3). We explore both low-rank and sparse settings for in our subsequent analysis.

Accelerated algorithm for low-rank coefficient matrix .

The process is detailed in Algorithm 1 as follows. We define the objective function from (3) as:

where

We now drop the in and and use and instead for clear presentation. The accelerated algorithm keeps two sequences and and updated them iteratively. At the beginning of the -th step, is the approximate solution from the last step, and is the search point for the current step. The accelerated algorithm performs the gradient descent update at the search point . Specifically, we define the update equations as

where is an appropriate step size, is an operator defined as on a matrix with SVD and is diagonal with the soft thresholding . The solution for the -the step is updated as

At last, the search point for the next step, , is constructed as a linear combination of the latest two approximate solutions at step and . Specifically,

| (13) |

where we set and update it iteratively by . To choose an appropriate step size , we start from an initial estimate and increase this estimate with a multiplicative factor repeatedly until the convergence condition

| (14) | ||||

is satisfied for . The and are defined, respectively, as

| (15) | ||||

Lemma 18 in the supplementary shows that Algorithm 1 converges under condition (14).

An alternative numerical method involves initially estimating using linear regression on the vectorized form of MFM (1), followed by estimating as a general low-rank matrix regression problem using the residuals from the first step, leveraging the fact that ’s and ’s are uncorrelated. For the low-rank setting, we maintain the joint update of both parameter matrices in our description to align with the convergence proof provided. In contrast, for the sparse setting, we adopt this two-step method, enabling the direct application of existing accelerated algorithms for sparse vector regression.

Accelerated algorithm for sparse coefficient matrix .

Define as the projection matrix, and let represent the residuals of the response vector after projection onto the column space of , which contains vectorized factors. Given that results in , the solution to (4) can be straightforwardly determined as:

| (16) |

Nesterov’s accelerated gradient algorithms (Simon et al., 2013; Yang & Zou, 2015; Yu et al., 2015) can be effectively utilized to solve convex problem (16). For a comprehensive review of additional computational methods for sparsity, refer to Chapter 3.5 in Fan, Li, Zhang & Zou (2020).

3 Theoretical Results

3.1 Analysis of the Pre-Trained Projection

We start with some assumptions that are necessary for our theoretical development.

Assumption 5.

Without loss of generality, we assume that , are mean zero, and thus and are mean zero. Throughout this paper, we assume that are observed, and latent are i.i.d. copies of .

Additionally, we adhere to Assumptions 19 and 20 outlined in the appendix. These are standard assumptions in factor models, as discussed in Chen & Fan (2021). They are presented in the appendix due to constraints on page length.

Identification issue is inherent with latent factor models: for any invertible matrices and , the triples and are equivalent under the MFM model (1). The following assumptions are commonly used to separate and and identify one targeting value of .

Assumption 6.

-

(a)

There exist universal constants , , , and such that

-

(b)

, and .

The following proposition shows that the pre-trained projection matrices and proposed in Section 2.1 satisfies Definition 4 as diversified projection matrices.

Proposition 7.

Proposition 7 indicates that when and , the conditions of diversified projection matrices in Definition 4 are satisfied by the pre-trained projection matrices we proposed in Section 2.1 with , for . In particular, by taking , this condition holds with probability at least . With that, the convergence rate of pre-trained estimator to the true up to transformation matrices is given below.

Proposition 8.

Remark 1.

The optimality of the rate presented in Proposition 8 can be understood by considering an oracle scenario where and are known. This scenario reduces the problem to estimating in a linear regression framework by vectorizing the matrix factor model:

Here, , with dimension , acts as the unknown “parameter” vector to be estimated. Standard OLS analysis indicates that the convergence rate of this estimator is , aligning with the rate achieved in Proposition 8.

3.2 Properties of the Block-Wise Averaged Estimators

Proposition 26 in Section D.2 of the appendix establishes the asymptotic normality of obtained by least squares in (9). Next we establish the asymptotic normality of the block-wise averaged estimator (11) of the loading matrices and element-wise convergence rate of the estimator (12) of the idiosyncratic component. All proofs are relegated to Section D in the appendix.

Theorem 9.

Remark 2.

The optimality of the rate for presented in Theorem 9 can be interpreted by considering an oracle scenario where and are known. This scenario reduces the problem to estimating using a linear regression model by stacking the matrix factor model along the second axis:

In this model, of dimension , is treated as the unknown “parameter” vector. According to standard OLS analysis, the element-wise convergence rate of this estimator is , which is consistent with the rate determined in Theorem 9.

Theorem 10.

Under the same condition of Theorem 9, we have, for each , , and , that

| (19) |

where and are the -th element of and , respectively.

Remark 3.

The three components that shows up in the convergence rate in Theorem 10 comes from the errors in estimating , , and , respectively.

3.3 Statistical Convergence of FAMAR Coefficients

We focus our theoretical analysis on latent FAMAR (1) where are not directly observable. Theoretical results for observable FAMAR are provided in Section E for low-rank and in Section G for overall sparse in the supplemental material.

3.3.1 FAMAR with Low-Rank

To study the property of and obtained by solving (3), we introduce the adjusted-restricted strong convexity condition (adjusted-RSC), which is a modification of the strong convexity condition (RSC) (Negahban & Wainwright, 2011).

Definition 11 (Adjusted-restricted strong convexity).

We let denote the projection operator onto the matrix subspace where and are the left and right singular space of respectively. Any can be decomposed as

| (20) |

Define a set in as

| (21) |

We say that the operator satisfies adjusted-RSC over the set if there exists some scalar-valued such that

Theorem 12.

Suppose that the projection matrices and are generated by the pre-trained projection in Section 2.1 with , . Then, under the same condition of Proposition 26, the solutions to the optimization problem (3) satisfy

| (22) |

where is the Frobenious norm of the true coefficient matrix. In addition, suppose that there exists a positive constant such that , and satisfies adjusted-RSC with constant over the set , where for some constant . Then we have

| (23) |

when the tuning parameter is chosen such that , where and .

Remark 4.

In FAMAR model (1), the signal strength from the factors should be comparable to the signal strength from the idiosyncratic component . Since the predictors and both have bounded entries, but differ in dimensions, it is reasonable to expect in the low-rank setting when . This aligns with the matrix regression model (2) in Example 2, where the size of each element in inherently has order , given the dimensions of , , and . Consequently, the convergence rate of in (22) is interpreted for the relative error

This contrasts sharply with factor-augmented sparse vector or matrix regression models where is sparsely supported on a set , , and .

The convergence rate of described in Theorem 12 can be further clarified when FAMAR reduces to matrix regression with MFM covariates (2), or equivalently , and is a sub-Gaussian random vector. This scenario is elaborated in the subsequent proposition.

Proposition 13.

Remark 5.

The two primary components contributing to the error bound rate for are: (i) the interaction between regression noise and the true covariates ’s and ’s, quantified as , and (ii) the interaction of regression noise with the estimation errors of ’s, quantified as .

3.3.2 FAMAR with Sparse

When the true exhibits certain sparse structures, such as global, row- or column-wise sparsity, the methodologies and theoretical frameworks developed for high-dimensional vector regression with sparse or group sparse structures can be effectively adapted to the FAMAR model with sparse . We have established theoretical results for overall sparsity using LASSO. Analogous results could be developed for overall sparsity employing non-concave penalties like SCAD and MCP, or for group sparsity, leveraging the relevant literature, e.g. Yuan & Lin (2006); Obozinski et al. (2011); Hastie et al. (2015). We leave these developments for future research to maintain focus and adhere to page limits.

To study the property of and obtained by solving (4), we consider the vectorized version with the restricted strong convexity condition (RSC) in Assumption 14 and adapt the proofs in Fan, Ke & Wang (2020). The analysis on is exactly the same as Theorem 12 based on the fact that , we include it in the following theorem for completeness. The consistency of is established in Theorem 15.

Assumption 14.

We denote , and and denote , , and . Let represent the true covariate matrix, we assume that

-

(a)

(Restricted strong convexity) There exist such that and , where is the matrix of columns of supported on ;

-

(b)

(Irrepresentable condition) for some .

Theorem 15.

The proof is presented in Section H in the appendix. By taking , we have

The convergence rate of described from Theorem 15 can be further clarified when FAMAR reduces to matrix regression with MFM covariates (2), that is , and is a sub-Gaussian random vector. This scenario is elaborated in the subsequent corollary.

Corollary 16.

Suppose the conditions for Theorem 15 hold. In addition, we assume that the true matrix regression model is , i.e. , and that and is -sub-Gaussian. Then

| (24) |

Remark 6.

When is a balanced matrix, that is, , error bound (24) can be further reduce to

which is optimal for vector sparse regression for vectorized .

4 Simulations

We study the finite-sample performance of the proposed FAMAR through simulations.

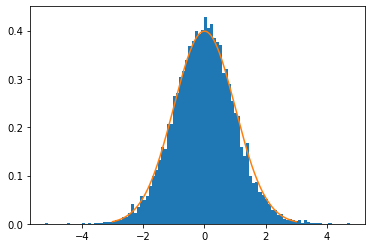

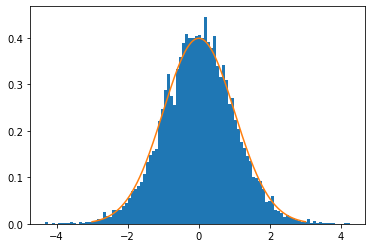

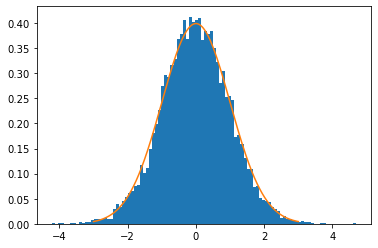

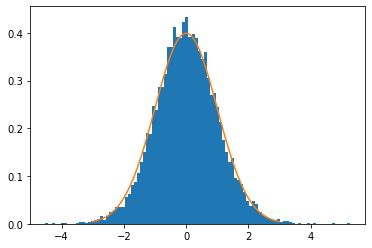

FAMAR Matrix Loading’s Asymptotically Normality. We test the asymptotic normality for the estimated loading matrices and according to Theorem 9. To that end, we conduct experiments as follows: . The true loadings and are generated such that their elements are i.i.d. from . The true factors and residuals have their elements i.i.d. from and , respectively. The experiments are repeated 10,000 times, and in each repetition, we compute and . For each elements , , (resp. , , ), we get 10,000 realizations of (resp. ). Let (resp. ) be the sample standard deviation of the sequence. According to Theorem 9, and should distribute closely to standard Gaussian. This result is validated empirically by histograms for all the elements of the matrices in Appendix I.2. Figure 1 showcases histograms of four randomly picked elements.

Next, we investigate the accuracy of the estimated factors, idiosyncratic variable, and FAMAR model coefficients. All experiments are repeated 100 times to reduce the effect of randomness. The simulations are carried out under two settings of parameters:

-

Setting I.

Fix and change in .

-

Setting II.

Fix and change in .

More settings of simulation exploration are available in Appendix I. For all cases, the true loading matrices and are generated element-wise from . The true factors and residuals are generated such that each element is drawn from and , respectively. Thereafter, the are generated by the matrix factor model . For , we first generate a matrix, with its individual elements sampled from , and then we take its best low-rank () approximation by SVD. The true response variables are defined by , where and are drawn from . By setting the variance of loading matrices much higher than that of the residual, we generate with highly correlated rows and columns. The experiments are repeated 100 times to reduce the impact of randomness. The tuning parameter for the nuclear norm penalty is chosen by cross-validation.

FAMAR Matrix Factor and Idiosyncratic Estimation.

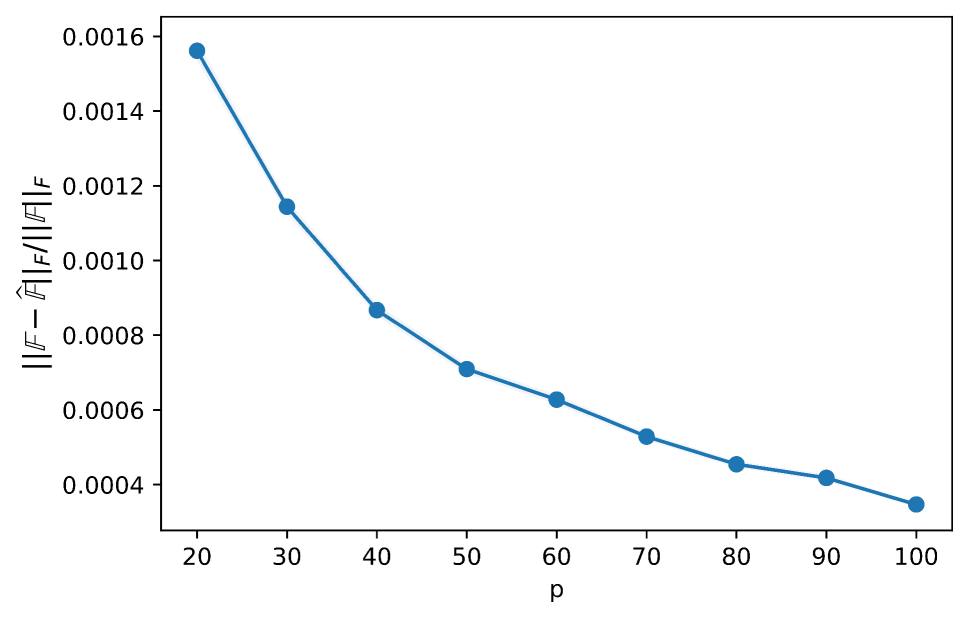

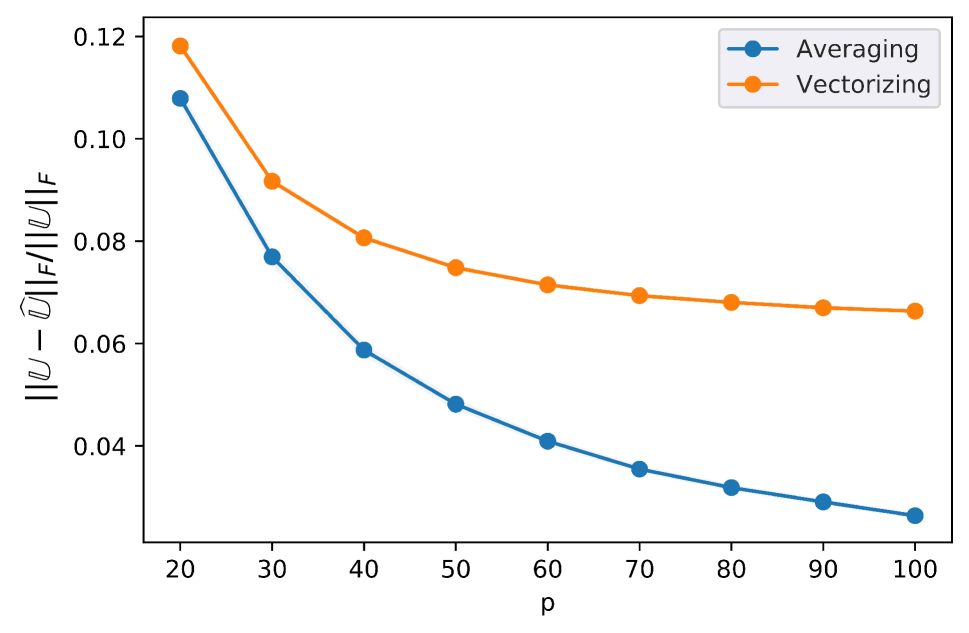

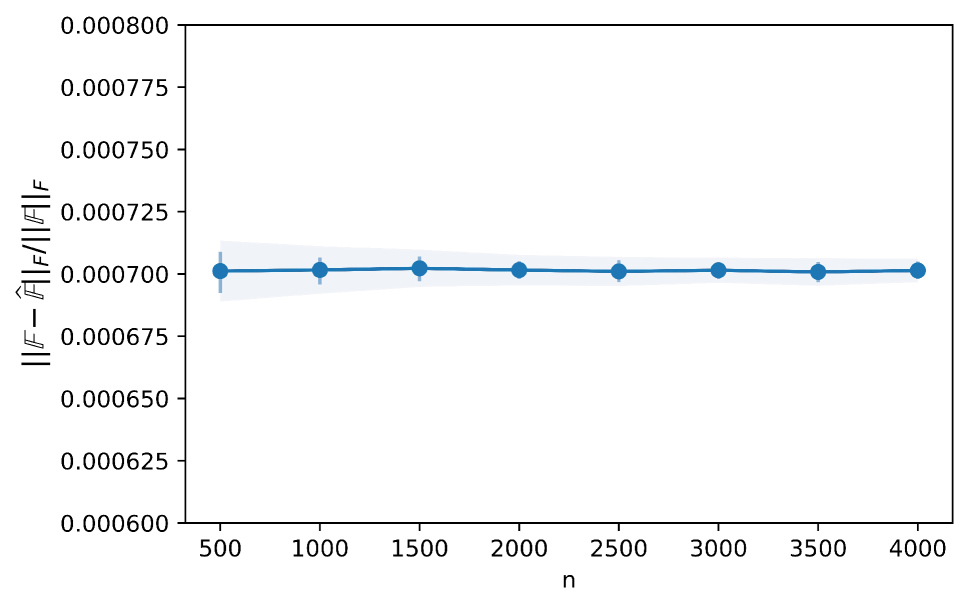

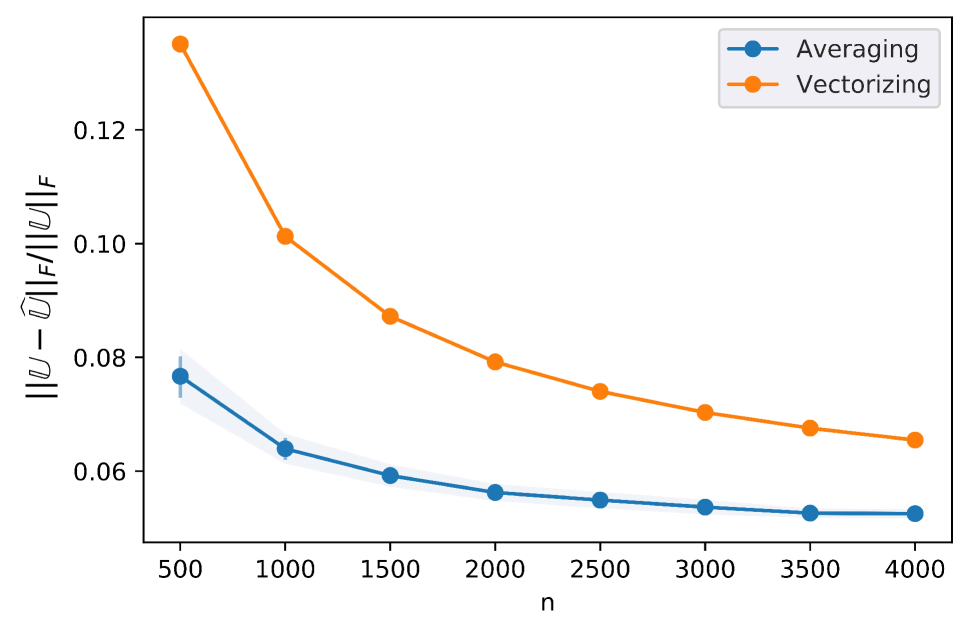

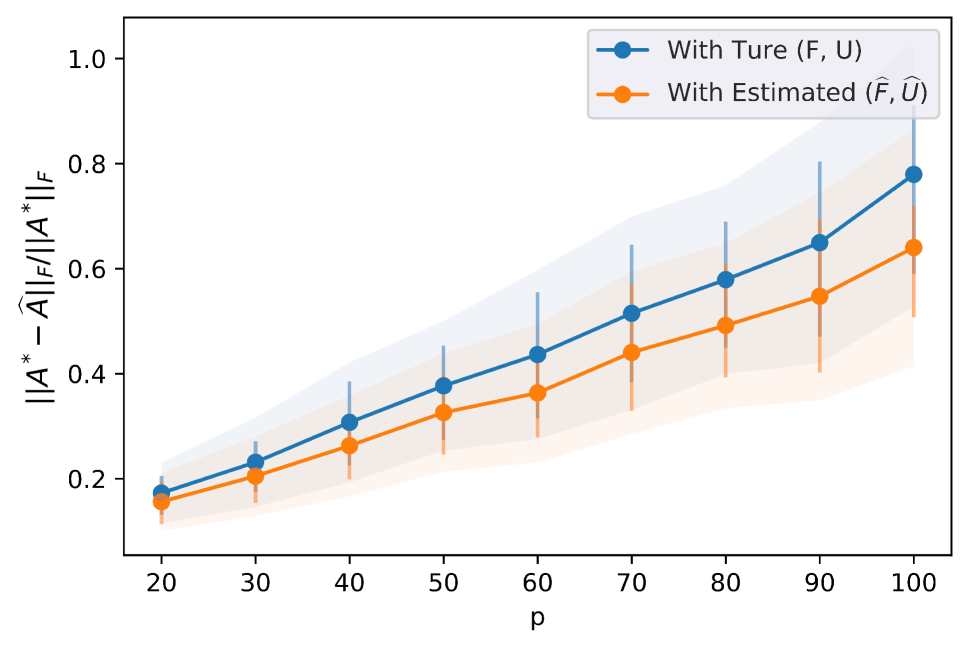

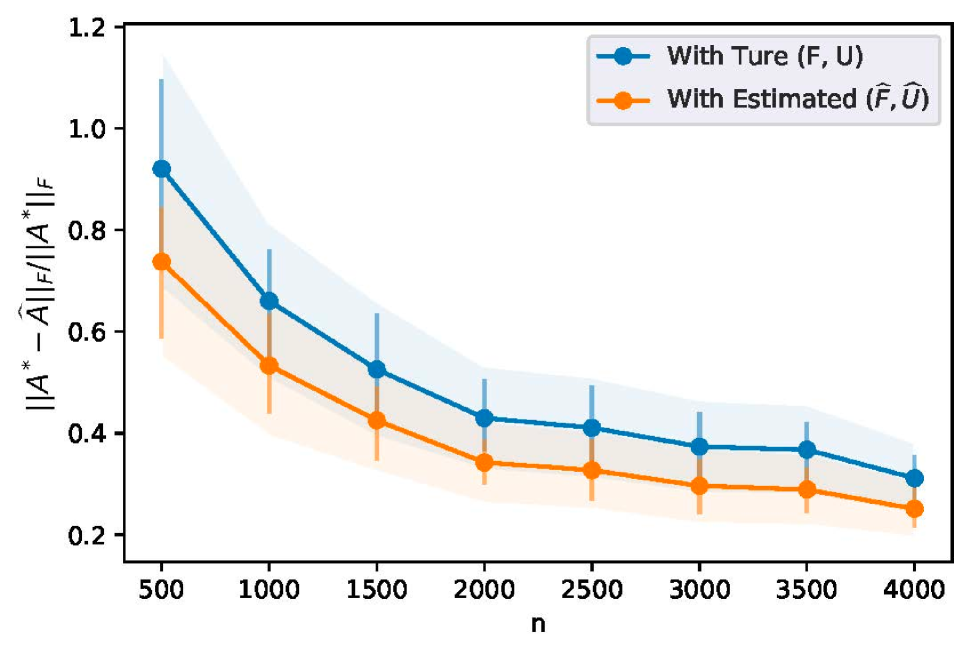

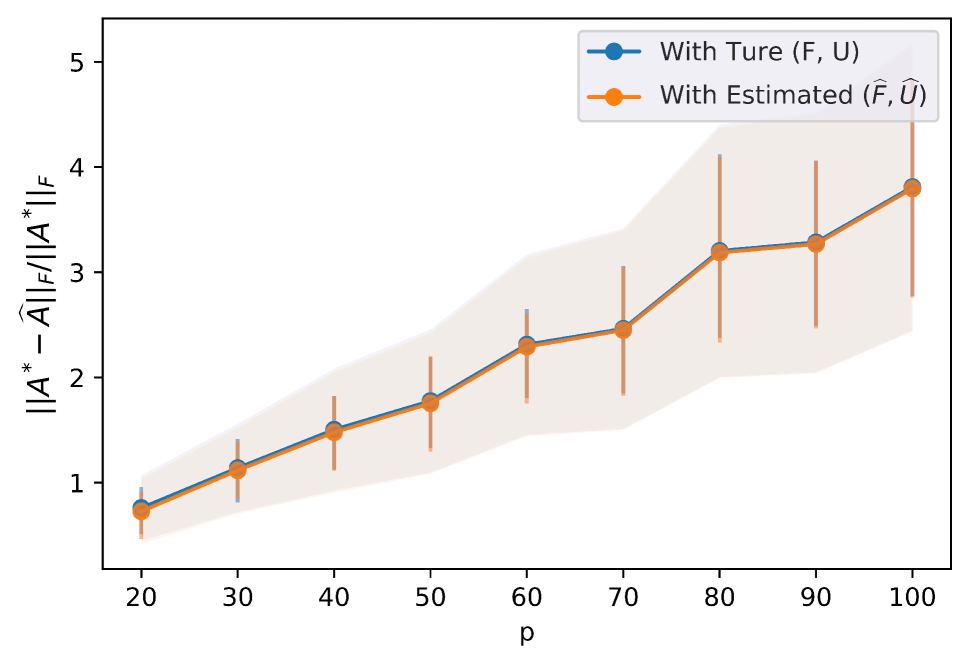

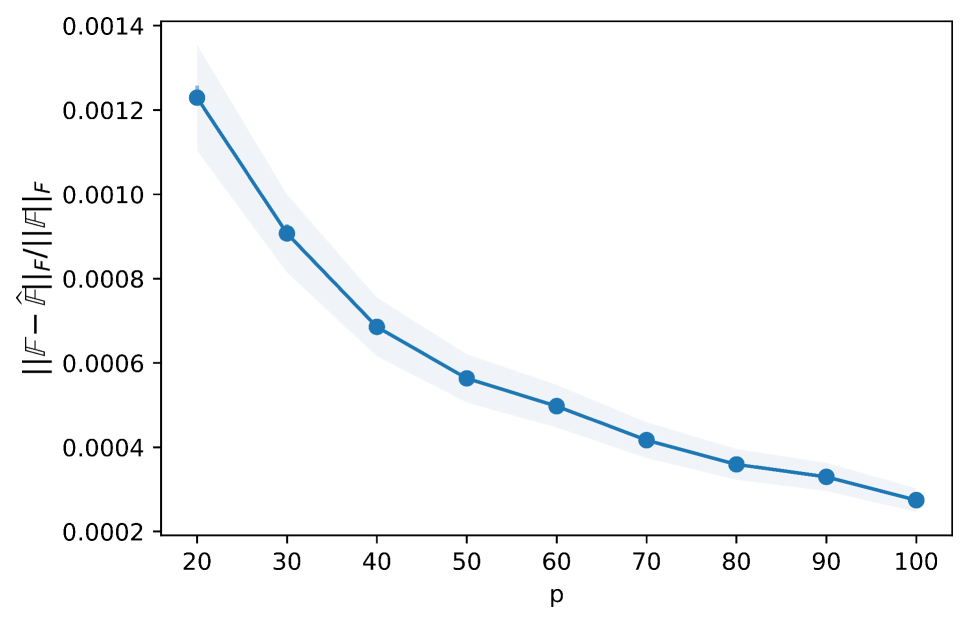

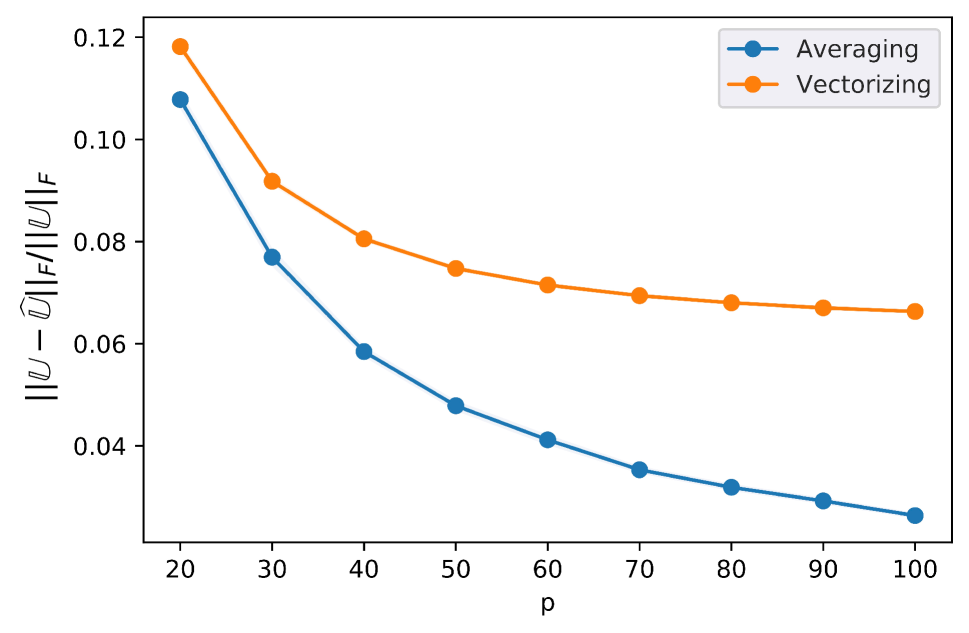

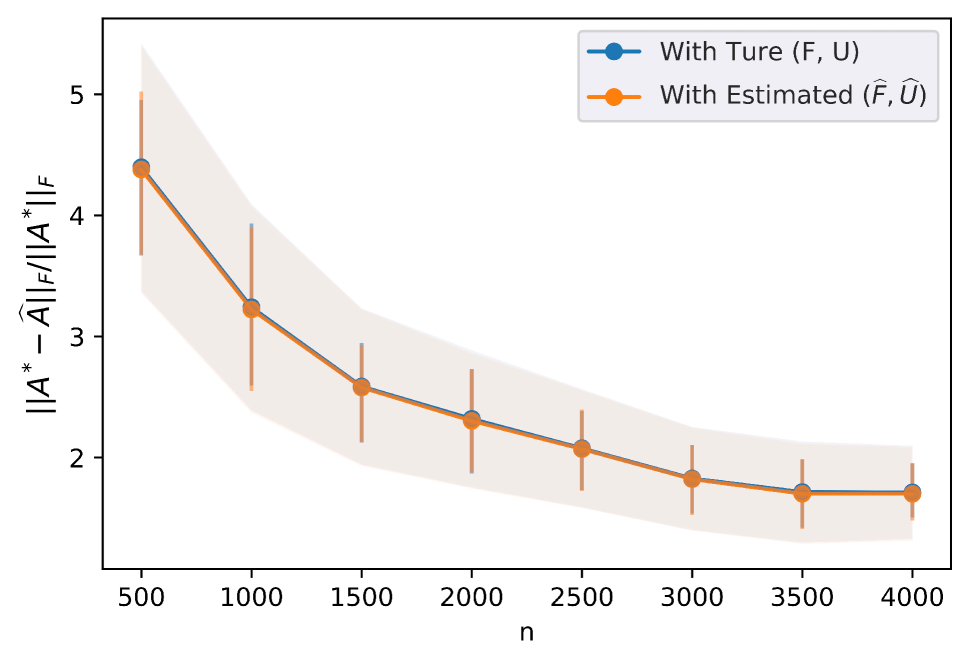

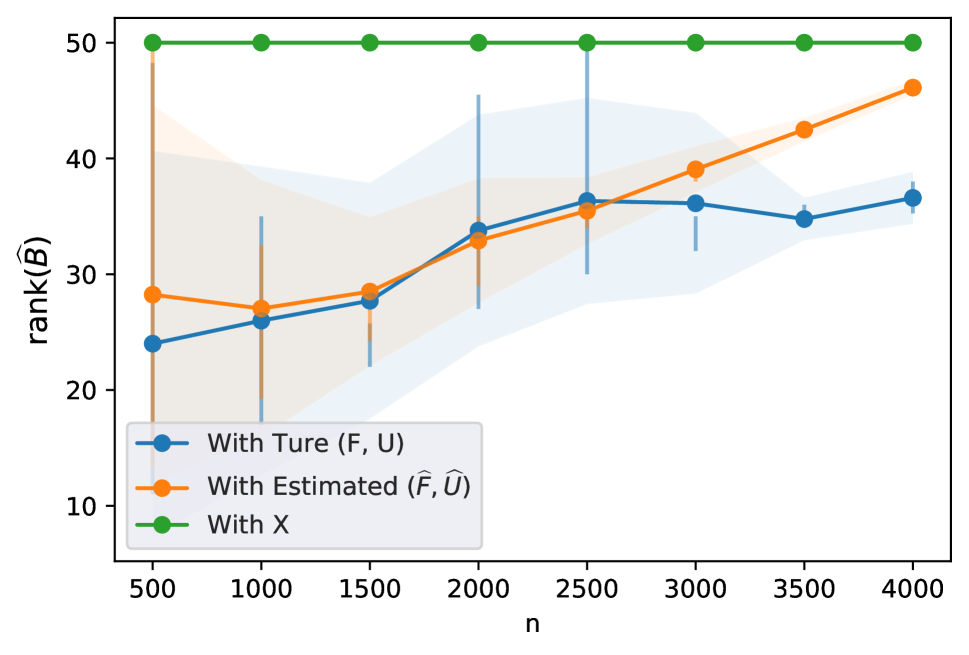

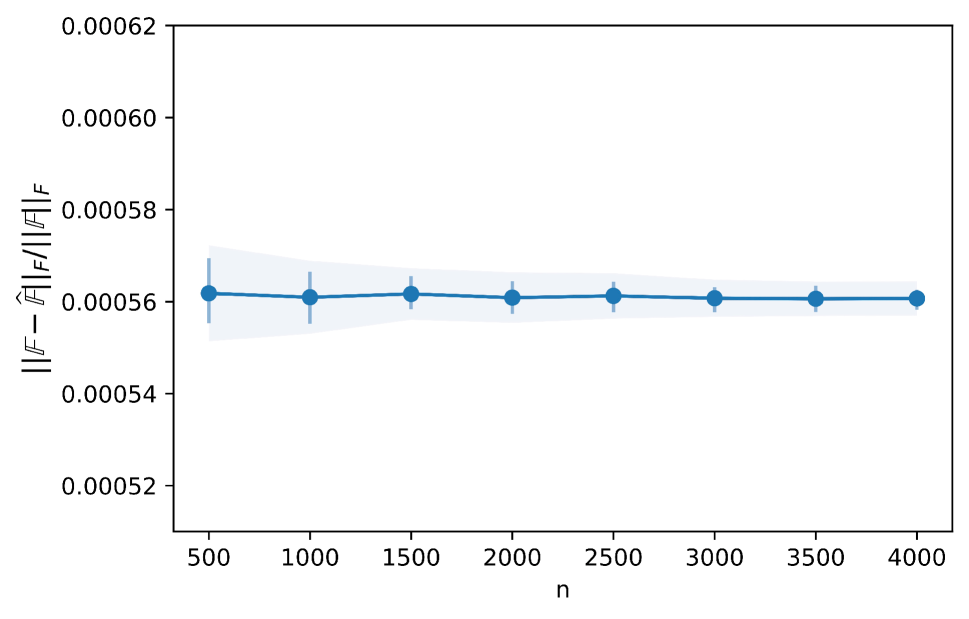

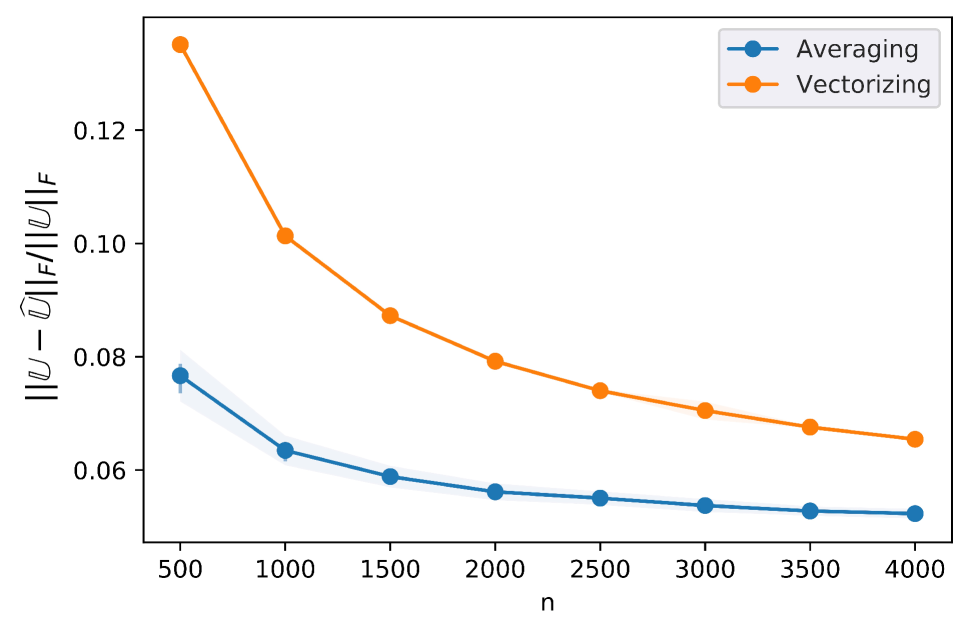

Figures 2 and 3 plot the performance of the proposed algorithm in estimating and under Setting I. and Setting II., respectively. The estimation errors are all very small and decrease as either or , increase, except that the error for is not affected by increasing number of as it uses pre-training sample size. Those observations are consistent with our theoretical results. The comparison of the estimation on with and without the block-averaging method showcases the privilege of the averaging algorithm.

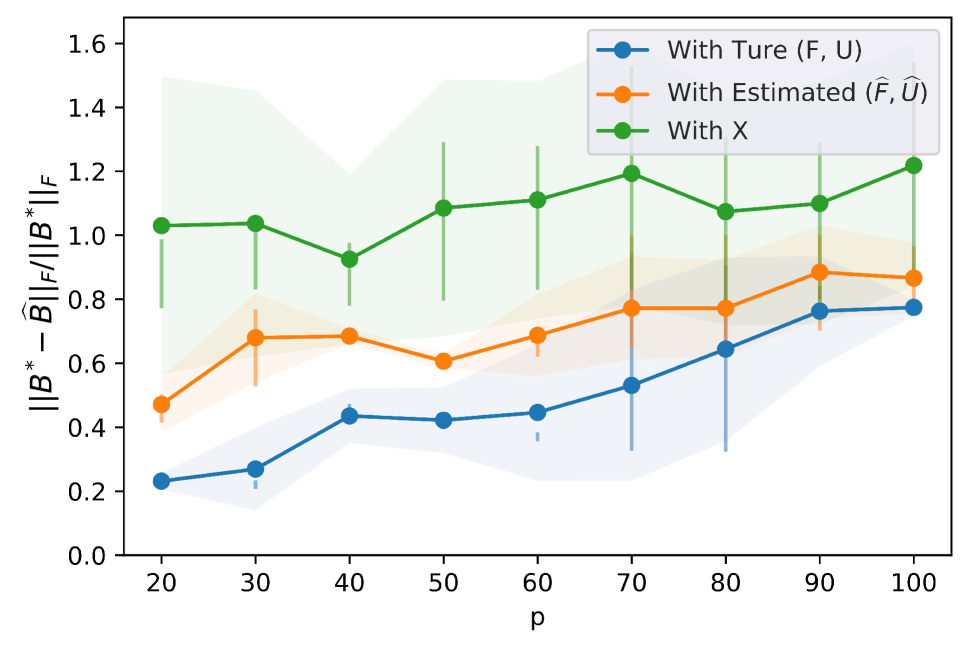

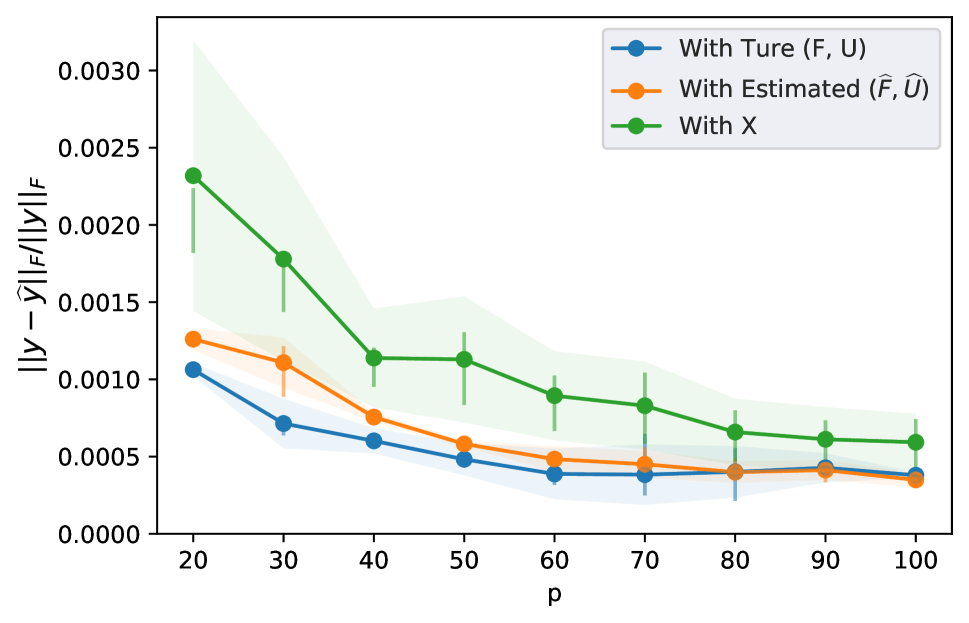

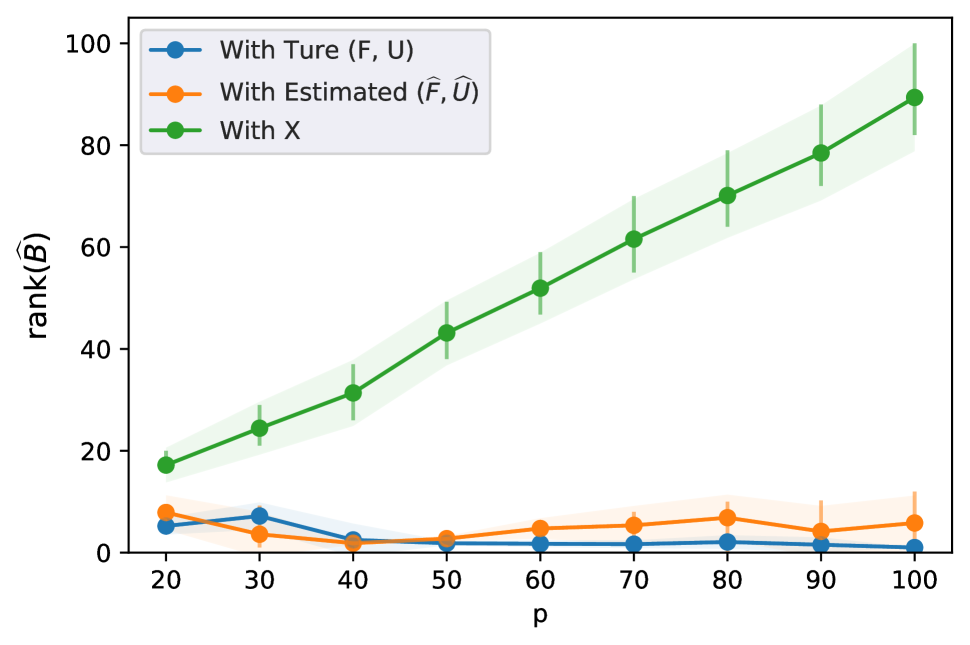

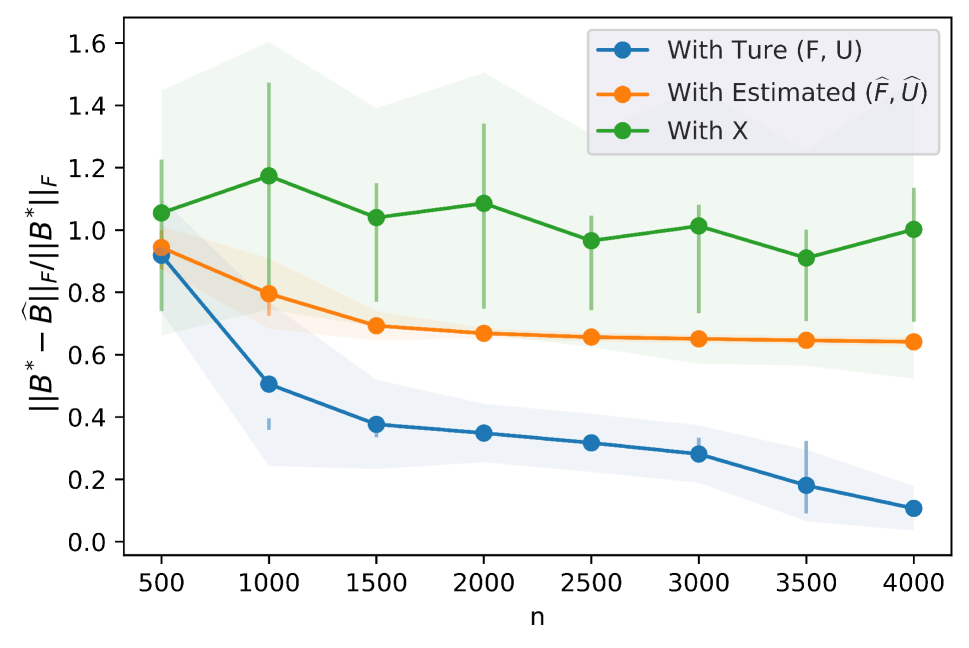

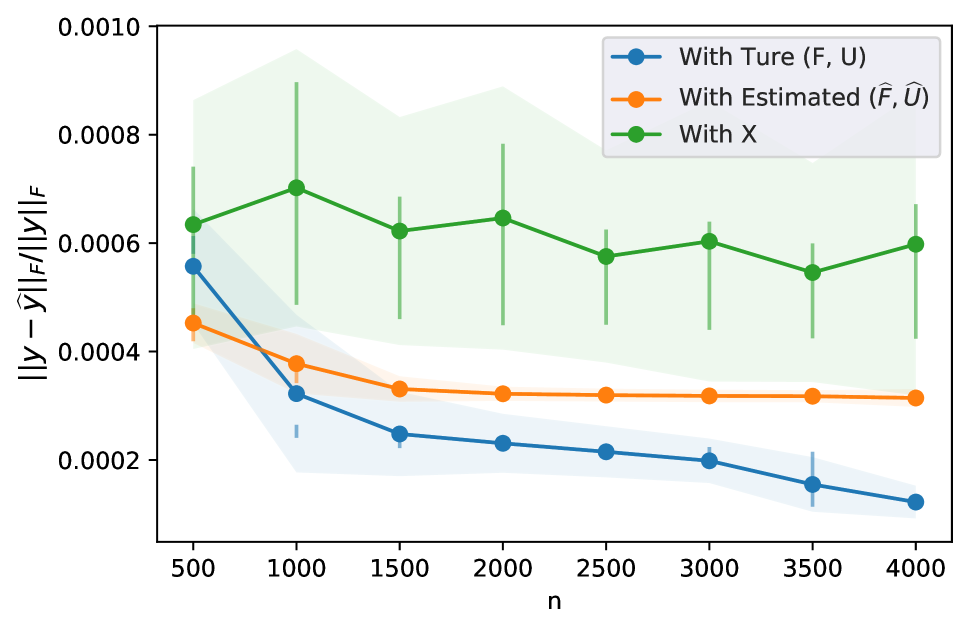

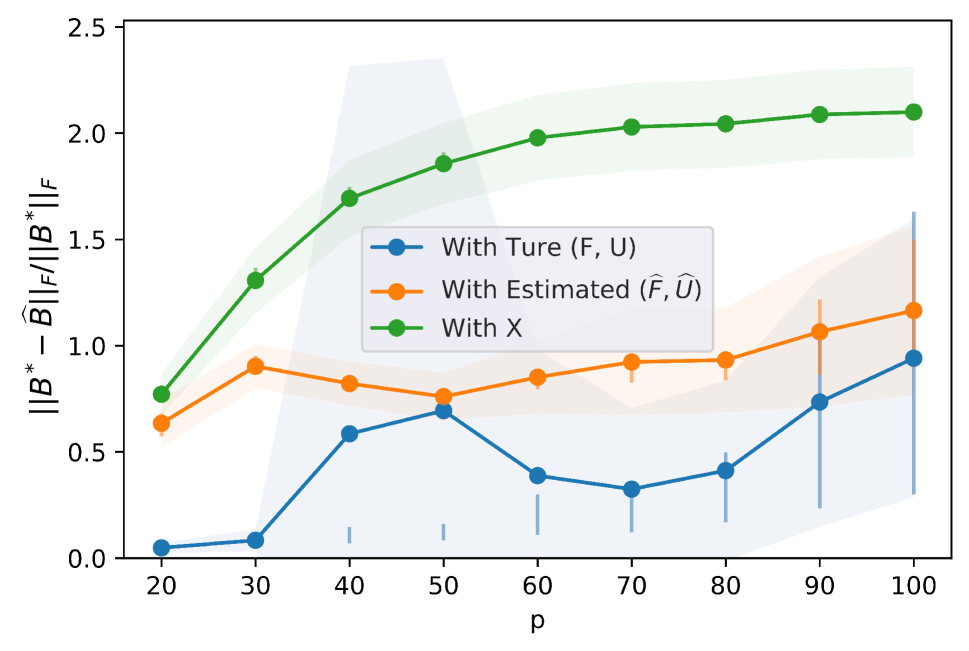

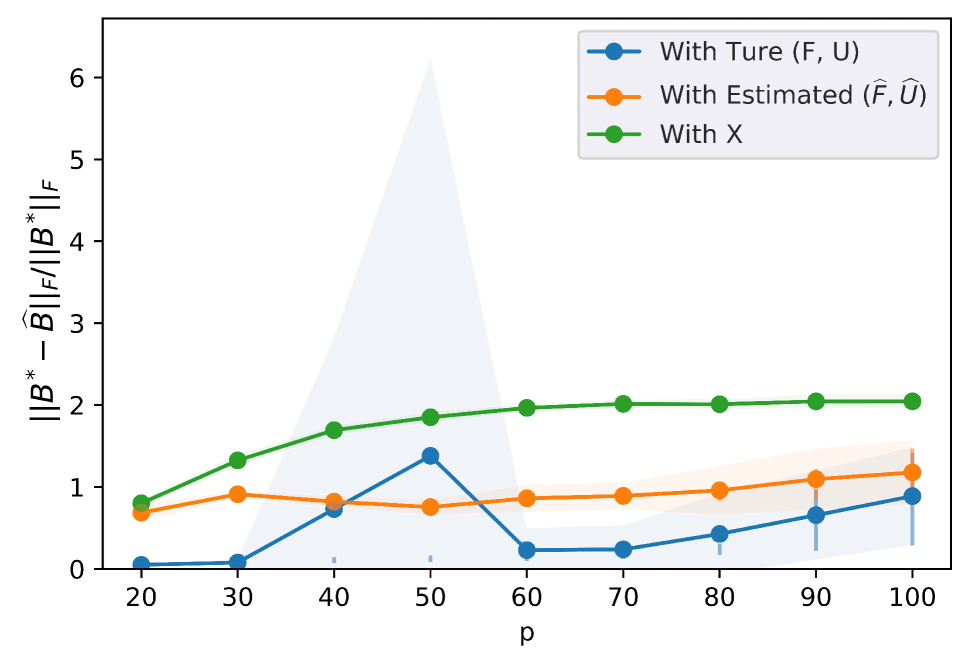

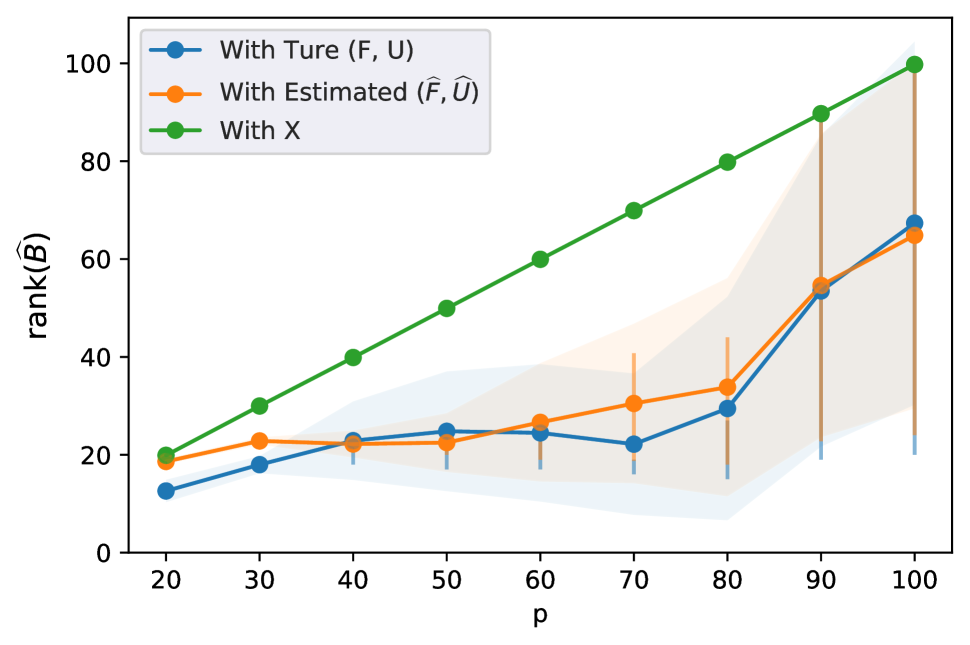

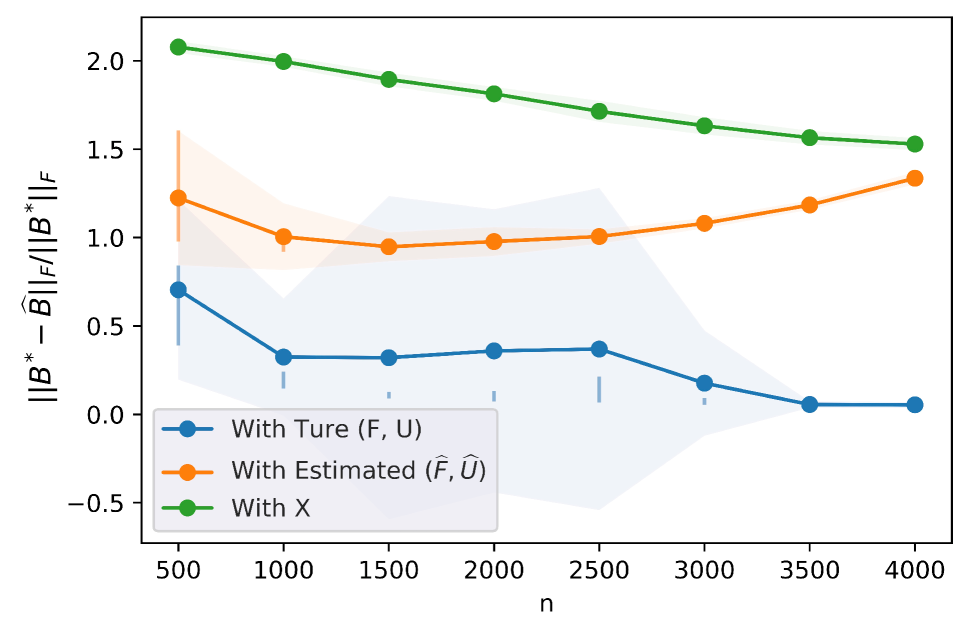

FAMAR Coefficient Estimation and Prediction. Figures 4 and 5 compare our proposed FAMAR with two current benchmarks, namely, the vanilla matrix regression model (2) with nuclear penalty on , and the oracle factor augmented regression model (1) with observed and , under Setting I. and Setting II., respectively. We could clearly see that our proposed FAMAR estimation tracks the performances of the oracle factor augmented regression closely in almost all tasks. Our proposed method outperforms the existing matrix regression with nuclear norm penalty in both estimation of coefficient and prediction of new response . Additionally, by generating a low-rank , as illustrated in the lower-right plots of Figures 4 and 5, FAMAR offers improved interpretability and stability compared to direct regression on ’s. When the covariates are highly correlated, applying low-rank regression directly to ’s tends to overestimate the rank due to their dependency structure, which hampers the effectiveness of regularization and the interpretability of the model.

The superior performance of FAMAR stems from two key advantages. Firstly, since the space spanned by is identical to that spanned by , FAMAR facilitates feature augmentation with , effectively leveraging latent information. Secondly, the factor model decorrelates the covariance matrix, resulting in more stable and interpretable coefficient estimators.

5 Real Data Analysis

We demonstrate the advantages of FAMAR with an real application to the multinational macroeconomic indices collected from OECD (Chen et al., 2019). The dataset contains 10 quarterly macroeconomic indexes of 14 countries from 1990.Q4 to 2016.Q4 for 105 quarters. By implementing the proposed FAMAR, we accomplish various empirical objectives, including the prediction of economic indicators, extraction of economic factors, and estimation of factor impacts. Subsequent sections showcase the results.

Economic prediction. Here we showcase one-step ahead prediction of individual countries GDP using all the economic indicators from all countries in the last period. The covariate is the (index) (country) matrix in one quarter and the response is the GDP of a country of interest in the next quarter. We take the estimated factor dimension as according to the analysis in Chen & Fan (2021).

We use a rolling window to do a one-step ahead prediction on the GDP of the United States (USA), United Kingdom (GBR), France (FRA), and Germany (DEU). We set the window width as 68, the first samples of which are set to pre-train the projection matrices and , while the following samples are used to estimate the loading matrices , and the regression coefficient matrix . In each window, the covariate matrices are normalized by subtracting the mean and dividing the standard deviation of the training set. The response variable is also demeaned by subtracting the sample mean of each training set.

The out-of-sample of GDP prediction on some representative countries are reported in Table 1. It is clear that FAMAR outperforms the vanilla matrix regression with a nuclear-norm penalty with much higher out-of-sample . Besides the comparison with the baseline, we also present predictions based only on the estimated factors or the estimated idiosyncratic components , respectively, to showcase their individual contributions to the process. As expected, it appears that factors play a predominant role in prediction, whereas the idiosyncratic components capture comparatively less valuable information in the context. This aligns with our expectation, for factors should capture most of the main and common features, and the residuals are regarded as idiosyncratic components corresponding to each feature, which are less representative and may vary a lot across time.

| FAMAR | ||||

|---|---|---|---|---|

| USA | 0.1540 | 0.1751 | -0.0512 | -0.1066 |

| GBR | 0.2057 | 0.1727 | 0.0287 | -0.0403 |

| FRA | 0.1961 | 0.1540 | 0.0789 | -0.0411 |

| DEU | 0.1814 | 0.1460 | 0.1197 | 0.0050 |

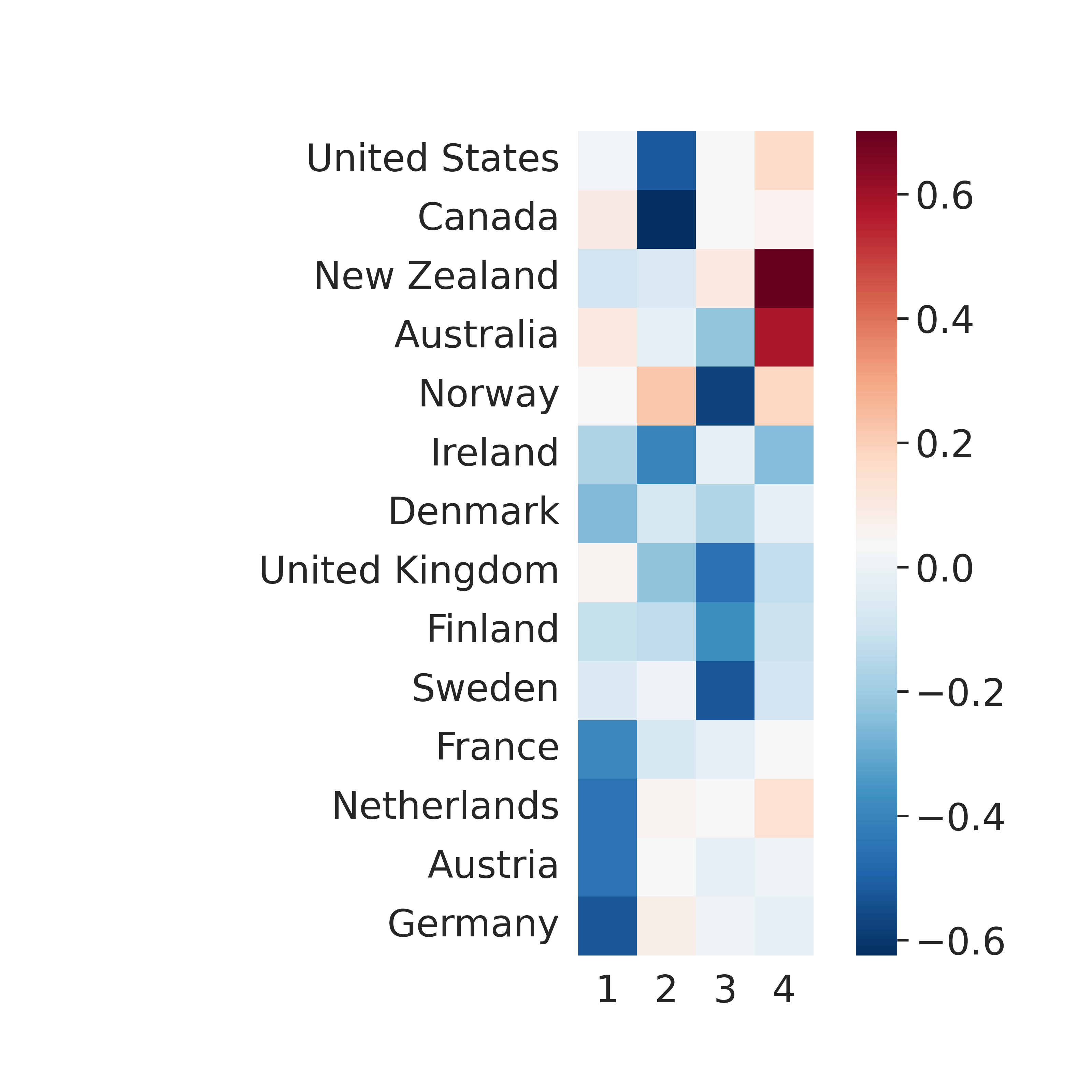

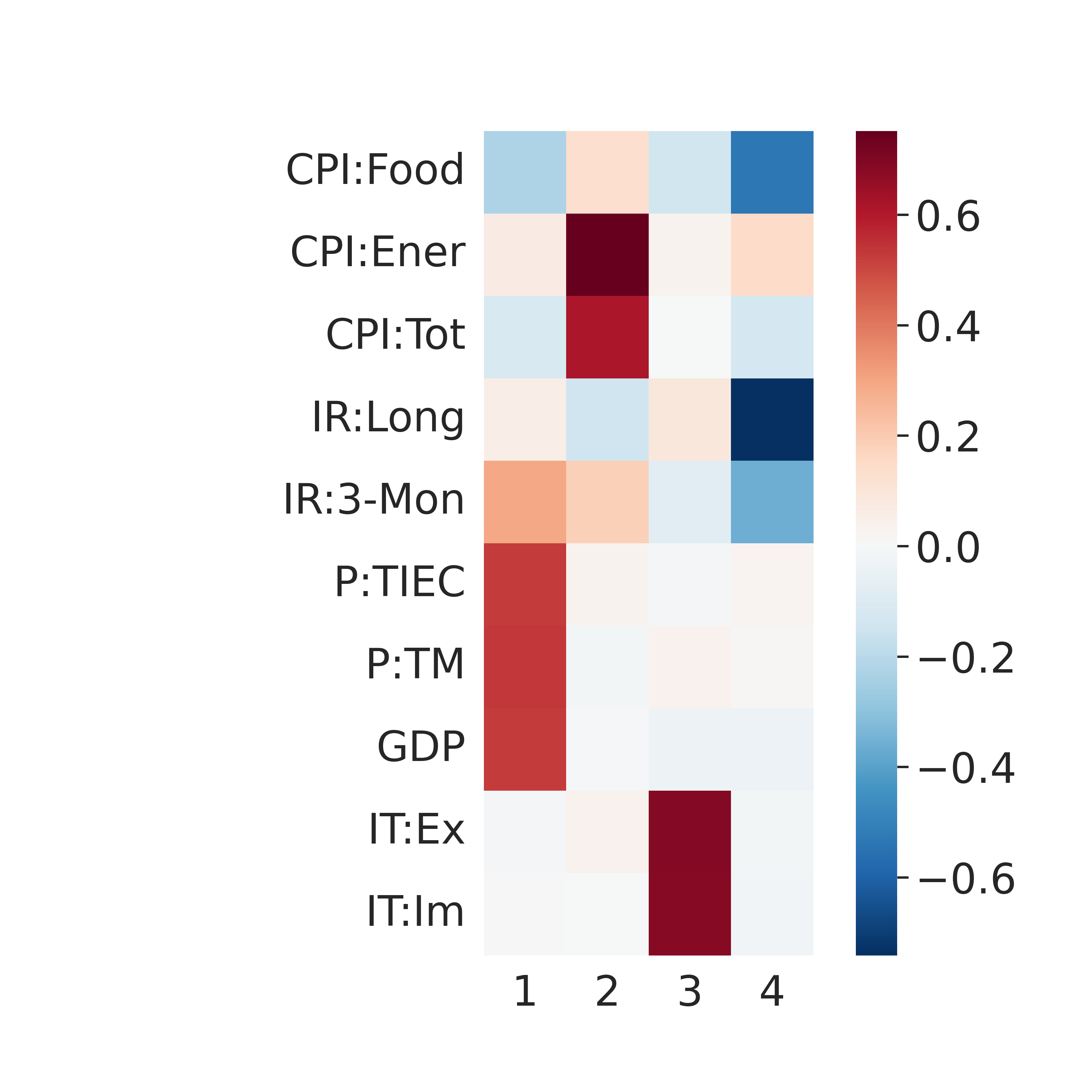

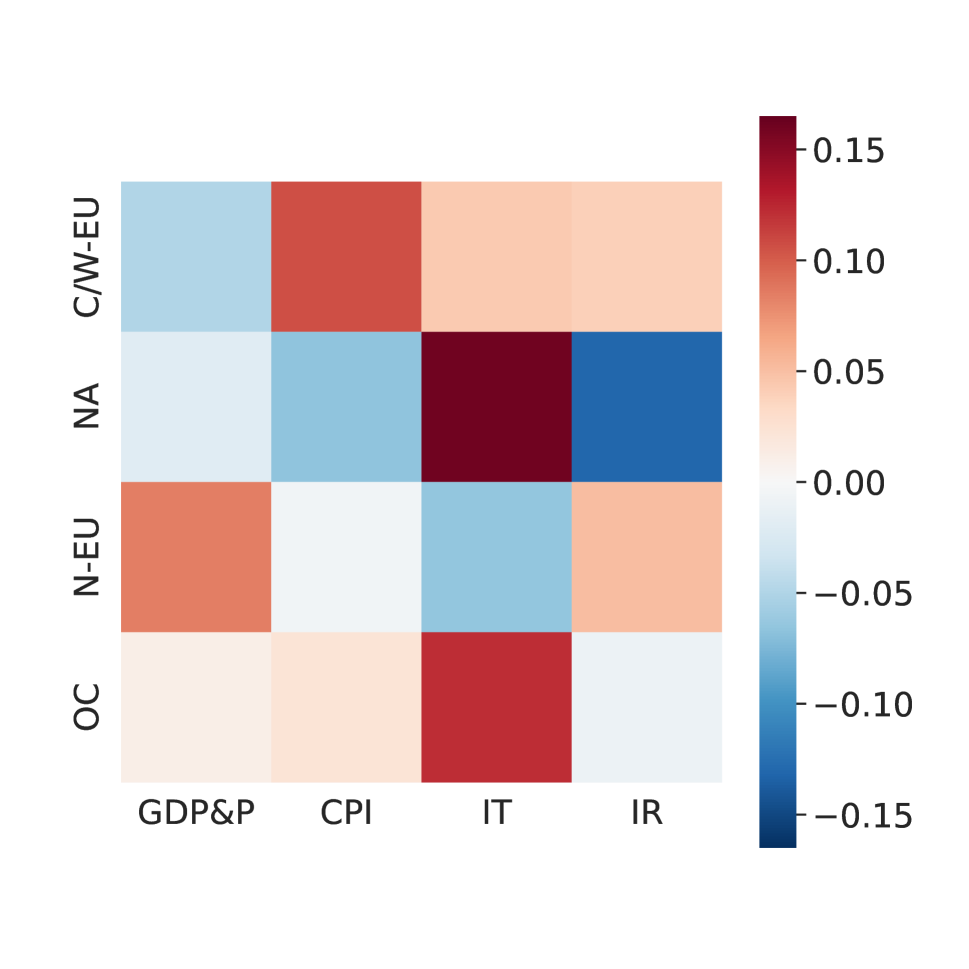

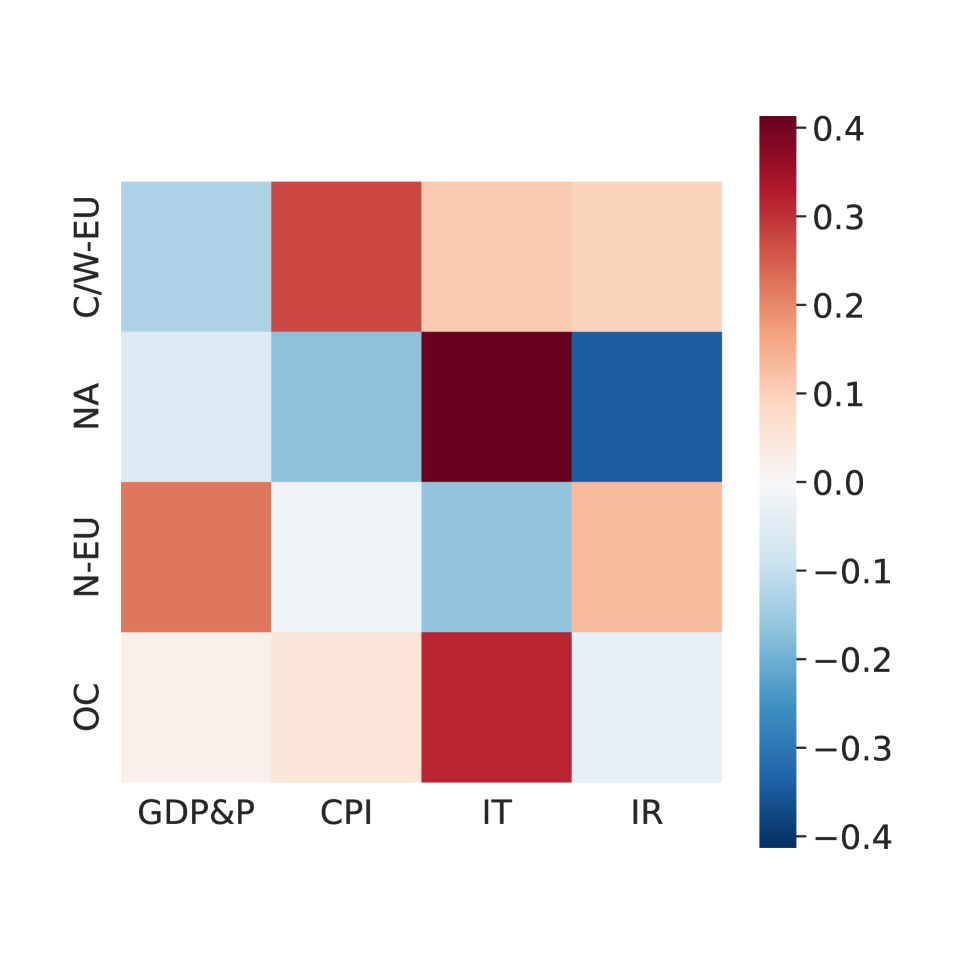

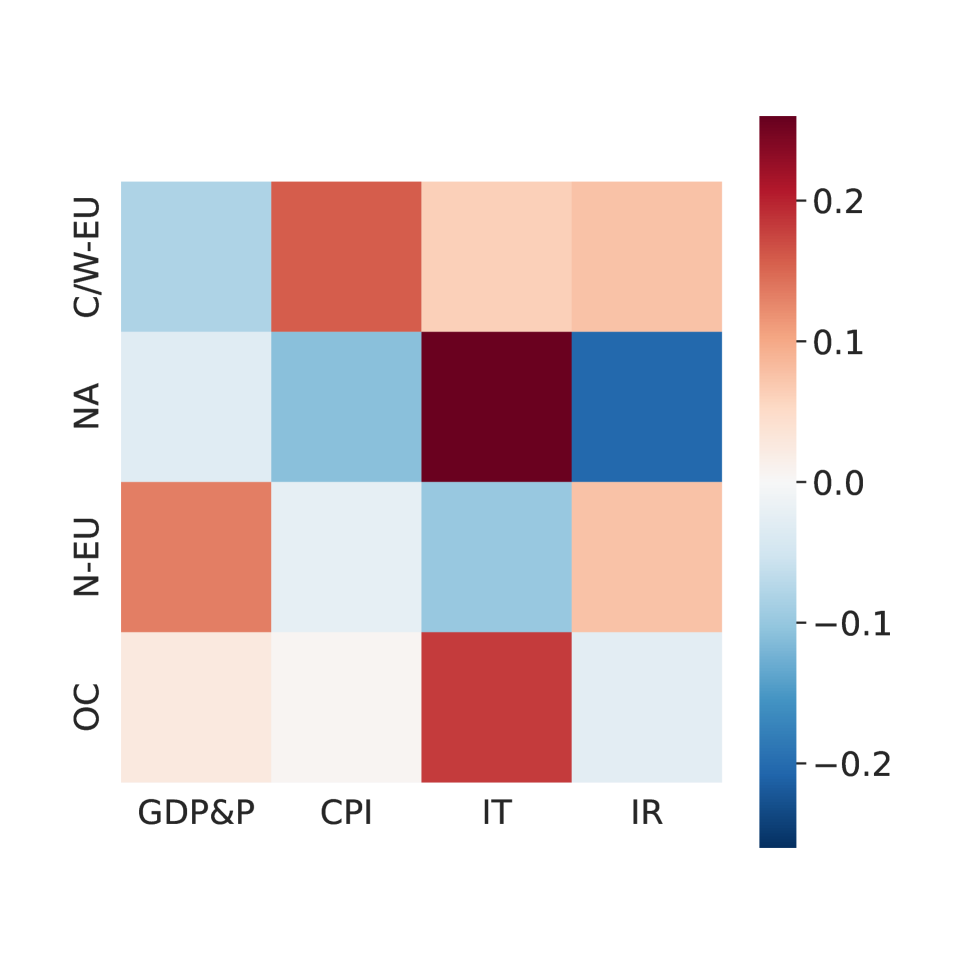

Economic and Country Factors and Loadings. Figure 6 shows the heatmaps for estimates of the row and column loading matrices for the factor model. The loading matrices are normalized so that the norm of each column is one. They are also varimax-rotated to reveal a clear structure. From Figure 6(a) of the row factor loading matrix , we observed clearly that the rotated row factor 1-4 loaded heavily on central/western European, north American, Northern European, and Oceania countries, respectively. Accordingly, the four rotated row factors can be interpreted as the Central/Western European (C/W-EU), North American (NA), Northern European (N-EU), and Oceanian (OC) factors, mostly following geographical partitions. In a similar fashion, the four rotated column factors are (i) Economic output and industrial production (GDP&P); (ii) Consumer Price Index (CPI); (iii) International Trade (IT); (iv) Interest Rates (IR). Again, the factors agree with common economic knowledge.

Factors Impacts. To explore the impact of latent factors on the GDP of different countries, Figure 7 presents the heat map of over the period. The heatmaps of exhibit notable similarities across the four examined countries. A discernible pattern reveals several coordinates characterized by substantial magnitudes. Specifically, the four most significant coefficients, in terms of magnitude, correspond to the pairs: (IT, NA), (IR, NA), (IT, OC), and (CPI, C/W-EU). This implies that international trade and interest rates in North America, international trade in Oceania, and the CPI of Central and Western Europe play pivotal roles in forecasting the GDP of the countries.

6 Conclusion

We introduce Factor-Augmented Matrix Regression (FAMAR) as a powerful framework to tackle the growing complexity of matrix-variate data and its inherent high-dimensionality challenges. FAMAR comprises two pivotal algorithms, each designed to address distinct aspects of the problem. The first algorithm presents an innovative, non-iterative approach that efficiently estimates the factors and loadings within the matrix factor model. Leveraging advanced techniques such as pre-training, diverse projection, and block-wise averaging, it streamlines the estimation process. The second algorithm, equally crucial, offers an accelerated solution for nuclear-norm penalized matrix factor regression. Both algorithms are underpinned by robust statistical and numerical convergence guarantees, ensuring their reliability in practical applications.

Empirical assessments across a range of synthetic and real datasets substantiate the efficacy of FAMAR. Notably, it outperforms existing methods in terms of prediction accuracy, factor interpretability, and computational efficiency. FAMAR’s versatility and superior performance make it a valuable addition to the toolkit of researchers and practitioners working with matrix-variate data. Its potential applications extend across diverse domains, from economics and finance to machine learning and data mining, where handling high-dimensional matrix data efficiently and effectively is paramount. As we move forward in the era of big data, FAMAR stands as a testament to the ongoing innovation in statistical modeling and data analysis, promising new avenues for extracting valuable insights from complex datasets.

References

- (1)

- Banerjee et al. (2005) Banerjee, A., Marcellino, M. & Masten, I. (2005), ‘Leading indicators for euro-area inflation and gdp growth’, Oxford Bulletin of Economics and Statistics 67, 785–813.

- Bertsekas et al. (1999) Bertsekas, D. P., Hager, W. & Mangasarian, O. (1999), ‘Nonlinear programming. athena scientific belmont’, Massachusets, USA .

- Cai et al. (2010) Cai, J.-F., Candès, E. J. & Shen, Z. (2010), ‘A singular value thresholding algorithm for matrix completion’, SIAM Journal on optimization 20(4), 1956–1982.

- Chen & Fan (2021) Chen, E. Y. & Fan, J. (2021), ‘Statistical inference for high-dimensional matrix-variate factor models’, Journal of the American Statistical Association pp. 1–18.

- Chen et al. (2023) Chen, E. Y., Fan, J. & Zhu, X. (2023), ‘Community network auto-regression for high-dimensional time series’, Journal of Econometrics 235(2), 1239–1256.

- Chen et al. (2019) Chen, E. Y., Tsay, R. S. & Chen, R. (2019), ‘Constrained factor models for high-dimensional matrix-variate time series’, Journal of the American Statistical Association .

- Chen et al. (2020) Chen, E. Y., Xia, D., Cai, C. & Fan, J. (2020), ‘Semiparametric tensor factor analysis by iteratively projected svd’, arXiv preprint arXiv:2007.02404 .

- Fan et al. (2019) Fan, J., Gong, W. & Zhu, Z. (2019), ‘Generalized high-dimensional trace regression via nuclear norm regularization’, Journal of econometrics 212(1), 177–202.

- Fan & Gu (2022) Fan, J. & Gu, Y. (2022), ‘Factor augmented sparse throughput deep relu neural networks for high dimensional regression’, arXiv preprint arXiv:2210.02002 .

- Fan, Ke & Wang (2020) Fan, J., Ke, Y. & Wang, K. (2020), ‘Factor-adjusted regularized model selection’, Journal of econometrics 216(1), 71–85.

- Fan, Li, Zhang & Zou (2020) Fan, J., Li, R., Zhang, C.-H. & Zou, H. (2020), Statistical foundations of data science, Chapman and Hall/CRC.

- Fan & Liao (2022) Fan, J. & Liao, Y. (2022), ‘Learning latent factors from diversified projections and its applications to over-estimated and weak factors’, Journal of the American Statistical Association 117(538), 909–924.

- Fan et al. (2013) Fan, J., Liao, Y. & Mincheva, M. (2013), ‘Large covariance estimation by thresholding principal orthogonal complements’, Journal of the Royal Statistical Society Series B: Statistical Methodology 75(4), 603–680.

- Fan et al. (2023) Fan, J., Lou, Z. & Yu, M. (2023), ‘Are latent factor regression and sparse regression adequate?’, Journal of the American Statistical Association (just-accepted), 1–77.

- Hastie et al. (2015) Hastie, T., Tibshirani, R. & Wainwright, M. (2015), ‘Statistical learning with sparsity’, Monographs on statistics and applied probability 143(143), 8.

- Ji & Ye (2009) Ji, S. & Ye, J. (2009), An accelerated gradient method for trace norm minimization, in ‘Proceedings of the 26th annual international conference on machine learning’, pp. 457–464.

- Kopoin et al. (2013) Kopoin, A., Moran, K. & Paré, J.-P. (2013), ‘Forecasting regional gdp with factor models: How useful are national and international data?’, Economics Letters 121(2), 267–270.

- Liu & Chen (2022) Liu, X. & Chen, E. Y. (2022), ‘Identification and estimation of threshold matrix-variate factor models’, Scandinavian Journal of Statistics 49(3), 1383–1417.

- Negahban & Wainwright (2011) Negahban, S. & Wainwright, M. J. (2011), ‘Estimation of (near) low-rank matrices with noise and high-dimensional scaling’.

- Nesterov (2013) Nesterov, Y. (2013), ‘Gradient methods for minimizing composite functions’, Mathematical programming 140(1), 125–161.

- Nogay & Adeli (2020) Nogay, H. S. & Adeli, H. (2020), ‘Machine learning (ml) for the diagnosis of autism spectrum disorder (asd) using brain imaging’, Reviews in the Neurosciences 31(8), 825–841.

- Obozinski et al. (2011) Obozinski, G., Wainwright, M. J. & Jordan, M. I. (2011), ‘Support union recovery in high-dimensional multivariate regression’.

- Recht et al. (2010) Recht, B., Fazel, M. & Parrilo, P. A. (2010), ‘Guaranteed minimum-rank solutions of linear matrix equations via nuclear norm minimization’, SIAM review 52(3), 471–501.

- Simon et al. (2013) Simon, N., Friedman, J., Hastie, T. & Tibshirani, R. (2013), ‘A sparse-group lasso’, Journal of computational and graphical statistics 22(2), 231–245.

- Wainwright (2019) Wainwright, M. J. (2019), High-dimensional statistics: A non-asymptotic viewpoint, Vol. 48, Cambridge University Press.

- Wang et al. (2017) Wang, X., Zhu, H. & Initiative, A. D. N. (2017), ‘Generalized scalar-on-image regression models via total variation’, Journal of the American Statistical Association 112(519), 1156–1168.

- Yang & Zou (2015) Yang, Y. & Zou, H. (2015), ‘A fast unified algorithm for solving group-lasso penalize learning problems’, Statistics and Computing 25, 1129–1141.

- Yu et al. (2015) Yu, D., Won, J.-H., Lee, T., Lim, J. & Yoon, S. (2015), ‘High-dimensional fused lasso regression using majorization–minimization and parallel processing’, Journal of Computational and Graphical Statistics 24(1), 121–153.

- Yu et al. (2022) Yu, L., He, Y., Kong, X. & Zhang, X. (2022), ‘Projected estimation for large-dimensional matrix factor models’, Journal of Econometrics 229(1), 201–217.

- Yuan & Lin (2006) Yuan, M. & Lin, Y. (2006), ‘Model selection and estimation in regression with grouped variables’, Journal of the Royal Statistical Society Series B: Statistical Methodology 68(1), 49–67.

- Zhou & Li (2014) Zhou, H. & Li, L. (2014), ‘Regularized matrix regression’, Journal of the Royal Statistical Society: Series B (Statistical Methodology) 76(2), 463–483.

- Zhou et al. (2021) Zhou, Y., Xue, L., Shi, Z., Wu, L. & Fan, J. (2021), ‘Measuring housing activeness from multi-source big data and machine learning’, Available at SSRN 3940180 .

SUPPLEMENTARY MATERIAL of

“Factor Augmented Matrix Regression”

Elynn Y. Chen♭ Jianqing Fan♮ Xiaonan Zhu♮

♭New York University ♮ Princeton University

Appendix A Notations

We use the notation to refer to the positive integer set for . For any matrix , we use , , and to refer to its -th row, -th column, and -th entry, respectively. All vectors are column vectors and row vectors are written as for any vector . For any two scalers , , we denote and .

We use as the vectorization of and use to denote a matrix whose rows are specifically vectorized matrices. That is, the -th row of is . For two matrices and , is the Kronecker product. Note that . We denote as the block-diagonal matrix with and being its diagonal blocks.

For any vector , we let be the -norm, and let be the -norm. Besides, we use the following matrix norms: -norm ; -norm ; Frobenius norm ; nuclear norm . When is a square matrix, we denote by , , and the trace, maximum and minimum singular value of , respectively. For two matrices of the same dimension, define the inner product .

Appendix B Computation

B.1 Explanation of the Accelerated Algorithm

To elucidate the accelerated algorithm, we first consider the vanilla gradient algorithm with the gradient step performed at the approximate solution , which consists of a singular value thresholding (SVT) on the gradient step of estimating and a regular update of . The partial gradient of with respect to is

Both and are -Lipschitz with given . Given a prescribed precision level and some initialization and , we can estimate and alternatively. Given , and the step size , can be updated by:

| (25) |

which admits an analytic solution

| (26) |

where is an operator defined as on a matrix with SVD and is diagonal with the soft thresholding . Since is of low dimension, it can be updated directly by gradient descent:

| (27) |

The accelerated algorithm performs the gradient step at the search point . So and are calculated according to equation (26) and (27) with replaced by the search point .

B.2 Numerical Convergence

Lemma 17.

Given , and the step size , can be updated by:

| (28) |

or, equivalently,

| (29) |

where is an operator defined as on a matrix with SVD and is diagonal with .

Lemma 18.

Let

where

| (30) | ||||

| (31) |

Assume the following inequality holds:

| (32) | ||||

Then for any and , we have

| (33) | ||||

Further, let be the sequences generated by Algorithm 1. Then for any , we have

| (34) |

Proof.

The and defined in Lemma 18 is equivalent to that defined in Section 2.2, which can be shown using Lemma 17 and Bertsekas et al. (1999), see also equation (5)-(7) in Ji & Ye (2009). The global convergence rate of Algorithm 1 is established by Lemma 18, whose proves are direct extensions of Theorem 4.1 in Ji & Ye (2009) and are therefore omitted. ∎

Appendix C Technical Assumptions

The following assumptions are needed for technical purposes. Assumption 19 and 20 imposes conditions on factors and idiosyncratic components, still allowing weak correlations. Assumption 21 is already satisfied by the data-driven method we have studied by its construction and by Proposition 7. Nevertheless, since some other reasonable projection matrices can also be used, we impose Assumption 21 for genreality. Assumption 22 is needed for asymptotic normality.

Assumption 19.

For MFM (1), there exists universal constants and such that

-

(a)

The elements of are mean zero, sub-Gaussian, and weakly correlated in the sense that: , where has independent mean zero sub-Gaussian entries, and for , , assume that for .

-

(b)

The elements of are mean zero, sub-Gaussian, and weakly correlated in the same sense as above. Furthermore, assume that

Assumption 20.

There exist universal constants , and such that

-

(a)

-

(b)

, and for some positive definite matrix , where and .

Assumption 21.

There exist universal constants , , and such that

-

(a)

, for .

-

(b)

, for .

Assumption 22.

-

(a)

There exists a constant such that the matrix satisfies

where is the -th column of , is the -th row of , and is the -th element of .

-

(b)

There exists a full-rank matrix such that

This also implies , for .

-

(c)

There exists an matrix such that

-

(d)

Assume that there exist a matrix and a matrix such that

where , is divided into blocks, denoted as , for , and that for all .

-

(e)

There exists such that for all , and , , .

Appendix D Theoretical Analysis of “Pre-trained Projection” and “Block-wise Averaging”

D.1 Proof of Proposition 7

We denote , , , and . We first present a technical lemma that bounds the norm between (resp. ) and (resp. ). Its proof is provided at the end of this section.

Lemma 23.

Proof of Proposition 7.

Since the proof for and are the same, we only provide that for as follows. The argument below is deterministic, conditioned on the event in Lemma 23.

Let be the matrix consists of the top top eigenvectors of . Then . Since is symmetric, it has the eigen decomposition , where is a diagonal matrix, and satisfies . Hence, . The upper bound is derived from

for some universal positive constant , where the second inequality is because of Assumption 6.

As for the lower bound, we have

| (35) |

where the last inequality follows from Assumption 6. Let be the eigenvalues of in the non-decreasing order, and let be the eigenvalues of in the non-decreasing order. Then by Assumption 6 and that , we have

| (36) |

Let . By Weyl’s Theorem and Lemma 23, there exists a universal constant such that

| (37) |

with probability at least .

To prove Lemma 23, we first show the following Lemma.

Lemma 24.

Under Assumption 19 (a), there exists a universal constant , such that

Proof of Lemma 24.

We can find an -net of the sphere and of the sphere with cardinalities:

Then the spectral norm of can be bounded using these nets as follows:

| (38) |

Fix . By the decomposition of in Assumption 19 (a) , we have

Denote and , we have

where . That leads to the tail bound:

By -net argument, we have

and setting , we bound the probability above by

Choose . If is chosen sufficiently large, such that , we have

Finally, combining the above inequality with (38) and by the assumption that and are bounded, we conclude that

∎

Proof of Lemma 23.

We provide in details the proof for as follows. The proof for is similar and thus omitted here. By definition, we can decompose by

| (39) | ||||

where . Now we establish the upper bounds of the operator norm of each terms above.

For , by Lemma 24, there exist a constant such that

with probability at lease . In what follows, we analyze under this event. We have,

for some universal constant . Accordingly, for some universal constant . This indicates that satisfies Bernstein condition with parameter . Together with Assumption 19 (a) and by Bernstein inequality (Theorem 6.17 in Wainwright (2019)), we have

where we use that fact that

Then we have

with probability at lease , and thus

with probability at lease .

For , similarly to Lemma 24, there exist a constant such that with probability at least . Similar to the above part for , we have by Bernstein inequality,

with probability at least .

Moreover, can be decomposed to

and the first term can be bounded by by Assumption 5. The second term is bounded using the same technique as above. First, we have

with probability at least . Hence satisfies Bernstein condition with parameter with probability at least . Therefore, by Bernstein inequality, we have

with probability at least . Thus, with probability at least .

All in all, substituting all the above results into (39) completes the proof.

∎

A straightforward corollary of Proposition 8 is stated as follows.

Corollary 25.

Under the same conditions as Proposition 8, we have

D.2 Analysis of OLS after pre-trained diversification

Proposition 26 (OLS after pre-trained diversification).

Before providing the proof of Proposition 26, we first present two lemmas whose proofs will be given shortly after.

Lemma 27.

Lemma 28.

Suppose the same condition of Lemma 27 holds, we have

Proof of Proposition 26.

Proof of Lemma 27.

D.3 Proof of Theorem 9

Proof.

By Proposition 26, we have that

where . Then

| (42) |

and by the proof of Proposition 26,

By linear transformation of matrix Gaussian distribution, we have

Since as goes to infinity, by Assumption 22 (d), we have

Bring back to equation (42), we have

With some linear shuffle transformation, we can similarly get that

∎

D.4 Proof of Theorem 10

Proof.

For clear presentation of the proof, we assume that and let . The proof is similar under the general setting without this assumption but more tedious. By Theorem 9, we obtain that

which implies that , where and are columns of the -th row of and , respectively. Also, it indicates that element-wise, we have

where are some constants. Thus, . Besides, Theorem 9 implies that . Hence, we have

Now we can bound as follows.

∎

Appendix E FAMAR-LowRank with Observed

We first establish the results of the general optimization problem (3) with and known. We start with introducing some notations. Let be the block-diagonal matrix of observations for . Let be the block-diagonal matrix of matrix parameters. Then, the operator is defined via . Similarly, define mapping via and mapping via . With these notations, the MFR model (1) can be re-written as

where , , and is the true parameter matrix. In addition, define the operator by . Moreover, considering the nuclear norm regularization on , the following notations are needed. For any true , let . Matrix has a singular value decomposition of the form , where and are orthonormal matrices. Let and be matrices of singular vectors associated with the top singular values of . Two sub-spaces of are defined by

and

where row and are the row space and column space, respectively, of the matrix . The shorthand notations and are used when are already clear from the context.

With that, we are able to introduce an important technical condition called adjusted-restricted strong convexity condition (adjusted-RSC), which is a modification of the strong convexity condition (RSC) proposed by Negahban & Wainwright (2011). Letting denote the restricted set, we say that the operator satisfies adjusted-RSC over the set if there exists some such that

To specify the set of interest, let denote the projection operator onto the subspace , and let

| (43) |

The set of low-rank matrices is defined by:

The following theorem presents the Frobenius norm error bound for the FARMA estimator.

Theorem 29.

Suppose that the operator satisfies adjusted-RSC with constant over the set , and that the tuning parameter is chosen such that . Then any solution to (3) satisfies

Remark 7.

By taking , Theorem 29 indicates that

with . The following proposition provides the convergence rate under this case with sub-Gaussian assumptions.

Assumption 30.

For , assume that

-

(i)

;

-

(ii)

is -sub-Gaussian, and there exists a constant such that .

Proposition 31.

Suppose that the operator satisfies adjusted-RSC with constant over the set , and that the tuning parameter is chosen such that . In addition, suppose Assumption 30 holds and . Then we have

E.1 Proof of Theorem 29

We start with providing a Lemma on the estimation error.

Lemma 32.

Let , and be matrices consisting of the top left and right (respectively) singular vectors of . Then there exists of the error such that:

-

(a)

;

-

(b)

if , then the nuclear norm of is bounded as

The proof of the Lemma will be provided shortly after, and with that, we are ready to prove Theorem 29.

Proof of Theorem 29.

Denote and . Then . By optimality, we have

Letting , , and , we have

| (44) | ||||

where the first identity is by definition, and the second inequality is by Hölder’s inequality. Lemma 32 (b) shows that . Thus, by adjusted-RSC, we have

| (45) |

Combining inequality (44) and (45) gives

where the third inequality is by the condition that and the triangular inequality. By triangular inequality and Lemma 32, we have

which leads to

The proof is completed by the fact that for any matrix , , which leads to

∎

Proof of Lemma 32.

Part (a) of the Lemma was proved in Recht et al. (2010) and Negahban & Wainwright (2011). The proof is provided here for completeness. Recall that the SVD of is , (resp. ) is the matrix of singular vectors associated with the top left (resp. right) singular values of . Let , and write it in block form as

Let ), and . Note that

For part (b), we have derived in (44) that

| (46) |

By construction of and , we know , and

Hence

Thus

Substituting that to (46), we have

Since , that leads to

i.e.

∎

E.2 Proof of Proposition 31

Proof.

Let , where . Then , and by the assumptions, is sub-Gaussian with parameter , where is some universal constant. Hence, by Matrix Hoeffding’s inequality, we have

| (47) |

for large enough. The conclusion follows directly from Theorem 29. ∎

Appendix F FAMAR-LowRank with Estimated

Let denote the residuals of the response vector after projecting onto the column space of , where is the corresponding projection matrix. Then . Thus, , and it is straightforward to verify that the solution of (3) is equivalent to

F.1 Consistency of

Proof of Theorem 12 Part I.

Let , . Vectorizing them gives

Recall that the true MFR (1) is

Thus, we have

By the definition of and MFM (1), it can be equivalently rewritten as

where . We are now ready to calculate the error of by

where the last identity uses the equality . Applying the -norm, we have

The first part, by Lemma 28, under Assumption 6 (b), 20 (b), and 22 (a) - (c), can be bounded by . The second part, by the definition of operator norm and Proposition 26, can be bounded by

As for the last term, we have shown that under the condition of Lemma 27, . Together with the fact that , we have

Combining the above results together, we get

Moreover, by the assumption that and is bounded (so ), we complete the proof of the first part of the theorem by

∎

F.2 Consistency of

Proof of Theorem 12 Part II.

Replacing the true in MFM (1) by the estimated , we have

where and . Consider the optimization problem (3). Let

| (48) |

Let , and recall that and the operator is defined such that . Letting , , we have . Optimality of gives

By elementary algebra, we get

| (49) |

Based on the proof of Theorem 29 and Lemma 32, to upper bound the error of , we only need to show that all the regularization conditions in Theorem 29 hold for optimization problem (48) with respect to the error and the residual .

There are two parts to be verified. The first is to show that the error , where the set is defined following Definition 11, with the projections of defined based on the SVD of , the lower-right part of . This is straightforward from Lemma 32 and the condition that , where , as a reminder, is defined as .

What left is to show that the adjust-RSC holds for with some constant for all matrices in based on the assumption that satisfied adjusted-RSC with constant over the set . That is, to show for all ,

By triangular inequality,

By the definition of and Cauchy-Schwartz inequality, we have

| (50) | ||||

By proof of Theorem 10, we have

Moreover, by the Assumption 19, we know that for any and , are independent sub-Gaussian random variables, where is the -th element of . Therefore, is sub-Exponential. By Maximal tail inequality, we have

Thus, . With the assumption and , by Cauchy-Schwartz inequality, we obtain the following bound.

Together with inequality (50) and Proposition 8, we have

for some constant . Together with the assumption and that , we have

F.3 Proof of Proposition 13

In cases where FAMAR simplifies to matrix regression with MFM covariates (2), specifically when , it becomes possible to eliminate and directly utilize the true error in determining the tuning parameter .

Corollary 33.

Suppose the assumptions inTheorem 12 hold. When , when , the result for still holds.

Proof of Corollary 33.

Consider the same optimization problem as (3):

| (51) |

Let . Different from the proof of Theorem 12, we define

Recall that , and the operator is defined that . By the decomposition , we have

Letting , , we have . Optimality of gives

By elementary algebra, we get

| (52) |

Similar to Theorem 12, to upper bound the error of , we only need to show that all the regularization conditions in Theorem 29 hold for optimization problem (48) with respect to the error and the residual .

Lemma 32 and the condition that shows that , where the set is defined following Definition 11, with the projections of defined based on the SVD of , the lower-right part of . It is straightforward to show that = , where is defined based on while is defined based on , for both and have the structure . Thus, we have .

The rest of the proof is exactly the same as that for Theorem 12 by replacing with .

∎

Proof of Proposition 13.

By taking , Corollary 33 indicates that

when all other quantities are finite. By triangular inequality,

| (53) |

Appendix G FAMAR-Sparse with Observed

When the true is sparse, the results from Fan, Ke & Wang (2020) can be similarly applied by vectorizing the matrices and applying sparse regularization. Here, we take Lasso as example. Let , and . Denote , , and . Further, let , , and , Let , , and . By adding the subscript , we only take the -th column for all . Define the loss function

We solve

After vectorization, this equals to

where .

We make the following assumptions.

Assumption 34.

All elements of are sub-Gaussian.

Proposition 35.

-

(i)

Error bounds : Under Assumptions 14, if then and

-

(ii)

Sign consistency : In addition, if the following condition

holds for some , then by taking , the estimator achieves the sign consistency .

Proof of Proposition 35.

Corollary 36.

Appendix H FAMAR-Sparse with Estimated

Recall that we defined , , and , where . The estimators solves the following optimization problem:

The analysis on is similar to that of Theorem 12 based on the fact that , which leads to

The consistency of is established in Theorem 15. Before proving Theorem 15, we first introduce a technical lemma and proposition.

Lemma 37.

Suppose and and , where is an induced norm. Then .

Proposition 38.

For the element-wise error of ’s, we have the following results.

-

(a)

-

(b)

;

-

(c)

.

Proof of Proposition 38.

To start with, By Definition 4 (a), we have

Moreover, similar to Fan et al. (2013), we have

Thus, by Proposition 26, we have

Similarly, we have . Therefore, by triangle inequality, we have

Similarly, by Cauchy-Schwartz inequality, we have

Furthermore, replacing the average over in the above inequality with maximum over and with , we can can also derive

∎

H.1 Proof of Theorem 15

Proof of Theorem 15.

Replacing the true in MFM (1) by the estimated , we have

where . Consider the optimization problem

We have for any norm .

To apply Proposition 35, we need to show that the conditions on needed to hold for Proposition 35 also hold for . We start with checking the restricted strong convexity. By Proposition 7, 8, and 38 (c), we have

Moreover, by Assumption 34 and maximal tail inequality, we have

Also, by Assumption 34 and maximal tail inequality, we have . Therefore, for ,

| (57) | ||||

Let . With the assumption and bound (57), we have

| (58) | ||||

with high probability for some constant when are large enough. Hence, by Lemma 37, we have

Together with Assumption 14 and triangle inequality, we have

Meanwhile, for matrix 2-norm, let . Then

By Lemma 37, we have

when are large enough. Together with Assumption 14 and triangle inequality, we have

Therefore, the restricted strong convexity holds for .

We also need to show that the irrepresentable condition holds for .

By (57) and Assumption 14 (a), we have

with high probability. By Lemma 37 and Assumption 14 (b), we have

with high probability, where the third inequality is by (57).

Combining these two bounds, we have

with high probability when are large enough. Therefore, by triangle inequality and Assumption 14 (b), we have

To sum up, we have verified that the conditions needed for Proposition 35 also holds for , and thus, by Proposition 35, we have

| (59) | ||||

Notice that

Thus

In addition, . We conclude the proof by substituting the above bounds to (59).

∎

H.2 Proof of Theorem 16

Appendix I Extra Experiment Results

I.1 FAMAR Coefficient Estimation and Prediction

As an extension of the simulations in Section 4, we present three more settings with a different way of generating true . Recall that previously in Section 4, is generated as . As mentioned in Section 1, we can also deal with cases where is not related with at all. To show this in simulations, Figure 9 to 10 present the result for matrix factor and idiosyncratic component estimation, FAMAR coefficient estimation, and dependent variable prediction. The detailed settings for each group of simulations are as follows.

- •

- •

- •

The results are mostly similar to that in Section 4, showing the efficiency of FAMAR. Notice that the trend of relative errors on is different from what we see in Figure 4 as and increases. Since the dimension of factors is fixed as (2,2) and does not change with and , the contribution of decreases as the dimension increases. To verify that, we make the elements in to have mean and std grow with problem dimensions with order . The results are shown in Figure 9, where the errors on present similar patterns as that in Figure 4 .

I.2 FAMAR Matrix Loading Asymptotically Normality.

We present the full graph of the asymptotic normality check of the estimated loadings and according to Theorem 9 in Figure 11.