Variance-Reducing Couplings for Random Features: Perspectives from Optimal Transport

Abstract

Random features (RFs) are a popular technique to scale up kernel methods in machine learning, replacing exact kernel evaluations with stochastic Monte Carlo estimates. They underpin models as diverse as efficient transformers (by approximating attention) to sparse spectrum Gaussian processes (by approximating the covariance function). Efficiency can be further improved by speeding up the convergence of these estimates: a variance reduction problem. We tackle this through the unifying framework of optimal transport, using theoretical insights and numerical algorithms to develop novel, high-performing RF couplings for kernels defined on Euclidean and discrete input spaces. They enjoy concrete theoretical performance guarantees and sometimes provide strong empirical downstream gains, including for scalable approximate inference on graphs. We reach surprising conclusions about the benefits and limitations of variance reduction as a paradigm.

1 Introduction

Kernel methods are ubiquitous in machine learning (Canu and Smola, 2006; Smola and Schölkopf, 2002; Kontorovich et al., 2008; Campbell, 2002). Through the kernel trick, they provide a mathematically principled and elegant way to perform nonlinear inference using linear learning algorithms. The eponymous positive definite kernel function measures the ‘similarity’ between two datapoints. The input domain may be continuous, e.g. the set of vectors in or discrete, e.g. the set of graph nodes or entire graphs.

Random features for kernel approximation. Though very effective on small datasets, kernel methods suffer from poor scalability. The need to materialise and invert the Gram matrix leads to a time complexity cubic in the size of the dataset . Substantial research has been dedicated to improving scalability by approximating this matrix, a prominent example being random features (RFs) (Rahimi and Recht, 2007, 2008; Avron et al., 2017b; Liu et al., 2022). These randomised mappings construct low-dimensional or sparse feature vectors that satisfy

| (1) |

The features are typically constructed using ensembles of random frequencies drawn from some known distribution . The choice of and manner in which they are combined to construct depends on the particular input space and kernel function being approximated. The set of RFs can then be used to construct a low-rank or sparse approximation of the Gram matrix, providing substantial space and time complexity savings. RFs exist for a variety of kernels, including for continuous and discrete input spaces (Dasgupta et al., 2010; Johnson, 1984; Choromanski et al., 2020; Goemans and Williamson, 2001; Rahimi and Recht, 2007; Choromanski, 2023).

Variance reduction for RFs. Eq. 1 can be understood as a Monte Carlo (MC) estimate of . In practical applications, it is often found that this estimate converges slowly. This can be addressed by taking many features , but this undermines the efficiency gains of RFs. Therefore, substantial effort has been dedicated to reducing the variance of the kernel estimates. Variance reduction methods include quasi-Monte Carlo (QMC) (Dick et al., 2013; Yang et al., 2014a), common random numbers (CRNs) (Glasserman and Yao, 1992), antithetic variates (Hammersley and Morton, 1956) and structured Monte Carlo (SMC) (Yu et al., 2016), all of which are well-studied in computational statistics. These techniques all ultimately work by replacing i.i.d. frequencies by a dependent ensemble, with the dependencies between samples designed to improve RF convergence.

Limitations of previous techniques. The best choice of dependencies between is an active research area. Though straightforward to apply, standard QMC techniques are suboptimal. They are based on fixed ‘low-discrepancy sequences’ so typically do not incorporate information about the particular kernel function being approximated. Empirical performance may be poor and theoretical guarantees lacking in the low-sample, high-dimensional regime (Rowland et al., 2018; Morokoff and Caflisch, 1995) – which is precisely where RFs are most important. On the other hand, hand-crafted SMC dependencies – which impose strict geometrical conditions like orthogonality between frequencies – tend to fare better (Yu et al., 2016). But they are still difficult to design, theoretical guarantees are hard-won and optimality is not guaranteed. RFs for estimating kernels defined on discrete spaces like the nodes of a graph have only recently been developed (Choromanski, 2023; Tripp et al., 2024), so here very few effective variance reduction techniques have even been proposed.

Optimal transport. To address these shortcomings, we propose to frame variance reduction as optimal transport: an active research area of applied mathematics that studies how to move (probability) mass between distributions as efficiently as possible (Villani et al., 2009). This fruitful perspective equips us with proof techniques and numerical tools to identify the best possible dependencies between samples, giving lower kernel estimator variance compared to previous approaches. We use these insights to develop better couplings for RFs in Euclidean and discrete spaces.

Our contributions. We summarise our key contributions below.

-

1.

We frame the problem of variance reduction of RFs as optimal transport (OT) (Sec. 2), and use this perspective to improve the convergence of three popular classes of RFs: random Fourier features, random Laplace features and graph random features.

-

2.

For random Fourier features (RFFs) and random Laplace features (RLFs), we exactly solve the OT problem for the norms of orthogonal frequencies, finding a novel coupling with the lowest possible variance (Sec. 3). We use a copula as a numerical OT solver to consider arbitrary .

-

3.

For graph random features (GRFs), we couple the lengths of random walks by solving an OT bipartite matching, outcompeting previous algorithms for estimating graph node kernels (Sec. 4).

-

4.

We test our algorithms on UCI datasets and real-world graphs, verifying that OT couplings substantially reduce kernel estimator variance (Secs 3 and 4). We show that this sometimes translates to much better performance in downstream tasks (in particular, approximate inference with scalable graph-based Gaussian processes), but also reach surprising conclusions about the limitations of variance reduction for RFs in machine learning.

All proofs are saved for the Appendices, but are also sketched in the main body where space allows. We will make source code available if accepted.

2 Background

From kernel estimation to optimal transport (OT). Considering the expression in Eq. 1, define the kernel estimator . Recall that is computed using random frequencies , with the space in which they live, distribution from which they are drawn, and manner in which they are combined dependent on the particular kernel being approximated. The estimator is unbiased provided each frequency obeys some known, fixed marginal distribution . Importantly, independence of is not a requirement: any joint distribution with marginals gives an unbiased estimator. We refer to the set of such joint distributions as couplings.

The choice of coupling between the frequencies determines the variance of the estimator. It is straightforward to see that finding the coupling that minimises this variance is equivalent to solving

| (2) |

where we defined the cost function

| (3) |

denotes the set of couplings over random variables with marginal measures . This is precisely the Kantorovich formulation of a multi-marginal optimal transport problem, with cost function (see e.g. Eq. 4 of the seminal OT text of Villani (2021)). The relationship between variance reduction and optimal transport was also noted by Rowland et al. (2018), but in the different setting of estimating the expected value of functions drawn from Gaussian processes.

(Approximately) solving the OT problem. For many popular RF constructions, the OT problem in Eq. 2 is intractable. The cost function and corresponding optimal coupling will in general depend on the choice of RF map and data distribution. A further practical consideration is that, to be useful, must be easy to sample from; even if it guarantees lower variance, an expensive sampling mechanism will obviate any efficiency gains from a coupling. However, we will see that for certain RFs under particular assumptions we can solve the OT problem exactly, obtaining computationally lightweight couplings that provide the smallest possible kernel estimator variance. Even if the OT problem is intractable, we can often leverage numerical methods to approximately solve Eq. 2. The formulation of these methods will depend on the input domain of the RF being considered.

3 Random Fourier features and random Laplace features

RFFs and RLFs. To begin, we consider the task of approximating the popular Gaussian kernel with data . This can be achieved using Rahimi and Recht’s celebrated random Fourier features (RFFs) (Rahimi and Recht, 2007),

| (4) |

where denotes concatenation. These provide an unbiased estimate if the frequencies are marginally Gaussian, . They are widely used for scaling kernel methods such as Gaussian processes (GPs; Williams and Rasmussen, 2006) and support vector machines (SVMs; Scholkopf and Smola, 2018). The time complexity of computing the exact posterior of a GP is where is the number of datapoints. Using RFFs, one can approximate the posterior with features, reducing this cost to . Beyond RFFs, can also be approximated using random Laplace features (RLFs) (Yang et al., 2014b),

| (5) |

where again Unlike RFFs, RLFs give strictly positive kernel estimates. This makes them better suited to estimating attention in linear-attention transformers (Choromanski et al., 2020), where negative estimates can cause training instabilities. Using RLFs to write a low-rank decomposition of the attention matrix with -dimensional tokens, one can reduce the computational cost of transformers from down to with low performance loss.

Orthogonal random features. A common variance reduction technique for both RFFs and RLFs is the orthogonality trick (Yu et al., 2016; Rowland et al., 2018; Reid et al., 2023; Choromanski et al., 2018). Exploiting the isotropy of , it is possible to constrain the frequency vectors to be exactly orthogonal whilst preserving their marginal distributions. This is found to reduce the kernel estimator variance and improve performance in downstream tasks. Whilst this technique couples the directions of the random frequencies , their norms (with ) are left independent so the coupling is suboptimal. We will now use tools from OT to find a coupling between frequency vector norms that provides strictly lower kernel estimator variance.

3.1 Solving the OT problem for maximal variance reduction

Consider an ensemble of orthogonal random frequency directions , jointly randomly rotated so they are marginally isotropic. Recall that our task is to couple their norms to suppress the RFF and RLF kernel estimator variance. The marginal distribution of each must be (a Chi distribution with degrees of freedom) to ensure that each is marginally Gaussian. It is simple to extend recently-derived results (Reid et al., 2023) to compute the OT cost functions.

Lemma 3.1 (OT formulation for RFFs and RLFs).

When estimating with orthogonal RFFs and RLFs, the OT formulation of the variance reduction problem is:

| (6) |

| (7) |

with and .

This is a challenging multi-marginal OT problem. However, remarkably, we can solve it exactly, under mild asymptotic assumptions for RFFs, when . The following result is novel.

Theorem 3.2 (Solution to OT problem when ).

Denote by the cumulative distribution function (CDF) of . Considering orthogonal frequencies with norms , the OT problem in Eq. 6 is solved by the negative monotone coupling

| (8) |

when for RFFs and in full generality for RLFs.

Proof sketch. We defer a full proof of this important result to App. A.2, but provide a sketch for the interested reader. It is well known that optimal transport plans satisfy a property called ‘-monotonicity’, which specifies how the support of the optimal coupling depends on the cost function. For and , we can show that this is commensurate with negative monotonicity (Eq. 8), though only asymptotically for the former. ∎

Given orthogonal frequencies, it is possible to partition the ensemble into orthogonal pairs, with one remaining frequency if is odd. For every such pair, we can impose negative monotone coupling (Eq. 8). We refer to such dependent ensembles as pairwise norm-coupled (PNC).

To reduce the variance further, one can of course take multiple independent PNC ensembles. A corollary of Thm. 3.2 is as follows.

Corollary 3.4 (Supriority of pairwise norm-coupled RFs).

The kernel estimator variance with pairwise norm-coupled RFs is strictly lower than orthogonal RFs with independent norms, provided for RFFs and in full generality for RLFs.

Negative monotone coupling differs from OT plans usually seen in machine learning; it is a space-filling coupling that seeks long transport plans that give diverse samples. However, it is a popular heuristic technique for variance reduction via common random numbers (CRNs) in computational statistics (Glasserman and Yao, 1992). This is (to our knowledge) the first result applying it to improving the convergence of orthogonal RFs, and the first corresponding guarantees for variance reduction. We make one further theoretical contribution regarding coupled RLFs.

Theorem 3.5 (Recovering antithetic sampling with RLFs).

For RLFs with frequencies whose respective orientations are unconstrained, the variance reduction OT problem is solved by conditioning that almost surely (that is, opposite directions and equal norms).

This coupling is popularly known as antithetic sampling (Hammersley and Morton, 1956). Thm. 3.5 shows that, given a PNC ensemble , we can obtain further variance reduction by augmenting it to . Antithetic sampling is also a common (though often heuristically motivated) variance reduction strategy used e.g. when estimating attention in Performers (Choromanski et al., 2020). We can reinterpret its effectiveness through the lens of OT. Note that Thm. 3.5 does not hold for RFFs.

3.2 Pushing further with numerical OT solvers

Multi-marginal OT. The insights of Sec. 3.1 have equipped us with pairwise norm-coupled RFs: a computationally efficient coupling that guarantees strictly lower kernel estimator variance. We obtained it by solving the variance reduction OT problem exactly in , then combining independent copies of such pairs to get the ensemble. A natural question is whether we can do better by inducing dependencies between the all the frequencies’ norms. Solving this multi-marginal optimal transport problem analytically is a challenging open problem.

Copulas as numerical OT solvers. Whilst a full analytic solution to the multi-marginal OT variance-reduction problem is (for now) out of reach, we can make progress using a numerical OT solver. Our basic strategy is to restrict , the full set of joint distributions over random variables with marginals, to a tractable subset amongst which we can efficiently optimise and sample. One such subset is provided by Gaussian copulas (Nelsen, 2006; Haugh, 2016): joint distributions obtained by taking a multivariate Gaussian and pushing each of its coordinates forward first with the Gaussian CDF , and then the inverse CDF . If the diagonal terms of the underlying Gaussian covariance matrix are equal to (i.e. it is a correlation matrix), this has the prescribed marginals so unbiasedness is baked in. Meanwhile, correlations between the random variables are controlled by the off-diagonal entries of . This family parameterises a very broad (though not universal) set of couplings, including pairwise norm-coupled RFs (Def. 3.3).

In App. A.5 we show that it is possible to use gradient descent with the reparameterisation trick to learn the optimal copula covariance matrix , approximately solving the multi-marginal OT problem (Chi et al., 2019). We do this by minimising the kernel approximation error on training data, exploiting the fact that all operations to construct the features are differentiable. Remarkably, optimising the copula recovers our pairwise norm-coupling scheme (or other equally well-performing variants). This suggests that PNC may in fact exactly solve the multi-marginal OT problem in Eq. 6, a tantalising possibility which we aim to explore in future work.

3.3 Experiments for norm-coupled RFs

| Fourier Features | Concrete | Abalone | CPU | Power | Airfoil | Boston |

|---|---|---|---|---|---|---|

| i.i.d. | ||||||

| Halton | ||||||

| Orthogonal | ||||||

| + PNC | ||||||

| Laplace Features | Concrete | Abalone | CPU | Power | Airfoil | Boston |

| i.i.d. | ||||||

| Halton | ||||||

| Orthogonal | ||||||

| + PNC + antithetic |

To verify the efficacy of pairwise norm-coupled RFs (Def. 3.3), we now compute kernel estimates with RFFs and RLFs for real-world UCI datasets. We choose the kernel lengthscale parameters (equivalently, the data normalisation) based on a training set, either by training a GP (RFFs) or selecting reasonable values for downstream Performer applications (RLFs) (Choromanski et al., 2020). We then compute the kernel approximation RMSE on a test set. Full details are in App. B.1.

Results. Table 1 shows the results. For RFFs, we take orthogonal frequencies. For RLFs, we also include their antiparallel directions, giving frequencies. For each dataset, the RMSEs are normalised by the result with i.i.d. features. As a further baseline, we include RFs constructed using Halton sequences (Dick et al., 2013; Yang et al., 2014a), a fixed, off-the-shelf QMC scheme that sometimes provides gains but is clearly suboptimal. The third row shows orthogonal frequencies with independent norms (Yu et al., 2016). When we also couple the frequencies’ norms using our OT-driven PNC scheme (plus antithetic sampling for RLFs, due to Thm 3.5), we access even lower estimator variance at no extra computational cost. Note that the condition for RFFs is found to be nonrestrictive, and coincides with the limit where standard QMC may fail.

4 Graph random features

We now shift our attention from to the discrete domain. Consider an undirected graph where is the set of nodes and is the set of edges, with if and only if there exists an edge between and in . Graph node kernels are positive definite, symmetric functions defined on pairs of nodes of , reflecting some notion of their ‘closeness’ via the graph edges and weights. captures the structure of , letting practitioners repurpose popular kernelised learning algorithms – including their theoretical guarantees and empirical success – to the discrete domain (Smola and Kondor, 2003b, a). Examples include the diffusion, regularised Laplacian, cosine and random walk kernels, all of which are typically considered as functions of the graph Laplacian matrix (Kondor and Lafferty, 2002). We give a short introduction in App. C.1.

Graph random features. As in the Euclidean setting, graph-based kernel methods scale notoriously poorly on account of the time complexity of inverting the Gram matrix . In fact, even computing often incurs a cubic cost since it involves multiplying large adjacency matrices. This has motivated research dedicated to improving efficiency by approximating , including the recently-introduced class of graph random features (GRFs) (Choromanski, 2023; Reid et al., 2024b). These are finite-dimensional, explicitly manifested vectors whose Euclidean dot product is equal to the graph kernel evaluation in expectation,

| (9) |

GRFs enable practitioners to compute a sparse, unbiased estimate of the graph kernel (or its inverse) in subquadratic time. They can be constructed for arbitrary functions of a weighted adjacency matrix.

Coupled random walks. Whereas RFFs and RLFs sample random vectors in , GRFs sample simple random walks. These are sequences of graph nodes where consecutive nodes are connected by an edge, . At every timestep, the walker chooses one of its neighbours uniformly and at random. The length of the walk may itself be a random variable. For GRFs, it is drawn from a geometric distribution , which corresponds to the walker terminating with probability at every timestep.

Random walks are usually taken to be independent, but this can lead to slow mixing times, poor efficiency and high kernel estimator variance (Alon et al., 2007; Zhou et al., 2015). A natural question is: can we use insights from OT to couple graph random walks to improve the convergence of GRFs?

The simplest approach to induce dependencies between random walks is to couple their lengths.111Walker directions can also be coupled for additional variance reduction (Reid et al., 2024a), but our work will not consider (and can be easily combined with) this complementary approach. For GRFs, the constraint for unbiasedness is that the marginal distribution of each random variable must remain geometric. Reid et al. (2024c) recently proposed a simple, heuristically-motivated algorithm to achieve this called antithetic termination, which directly anticorrelates the termination events between walkers at every timestep (see App. C.2). They provide asymptotic theoretical guarantees, but only for particular choices of graph kernel. In the following section, we will see that an OT-based approach that optimises a coupling using real data performs substantially better.

4.1 Approximating and solving the OT problem for GRFs

Here, we present our approach for formulating and approximately solving the variance reduction OT problem with GRFs. It works by mapping to a corresponding bipartite matching problem which we can solve efficiently.

Constructing GRFs from random walks. GRFs are constructed differently to RFFs and RLFs. To obtain (where ), we sample random walks out of node and compute the arithmetic mean of their corresponding ‘projections’,

| (10) |

Here, the projection function maps from the set of graph random walks to a sparse -dimensional feature vector satisfying . depends on the particular kernel being approximated. We refer the reader to the works of Choromanski (2023) and Reid et al. (2024b) for an introduction to GRFs, but also provide background in App. C.1 for completeness. For our purposes, it will be sufficient to note that is a complicated function; it is difficult to reason about analytically but straightforward to compute for a particular walk. Moreover, its input walks are discrete random variables so is not differentiable with respect to their lengths (where and is the walker’s start node) – a property that will preclude optimisation using copulas (Sec. 3.2).

A pair of walkers. Let us initially consider just walkers. The kernel estimator is

| (11) |

which is unbiased provided (i) the marginal distribution of each is a simple random walk with geometrically distributed length (hereafter denoted ) and (ii) walks from node are independent from walks from node . The variance of the estimator depends on the quantity

| (12) |

where the expectation is taken over both the directions and lengths of the random walks. Suppose the directions remain independent, but the lengths and (and likewise and ) are to be coupled for variance reduction. The OT problem can then be written

| (13) |

where denotes the expectation over the walkers’ directions, i.e. which neighbour they choose at each timestep.

OT, permutation densities and bipartite matchings. The OT problem in Eq. 13 is analytically intractable. To make progress, we must make some approximations. We report them in full in App. C.3; Fig. 6 provides a visual overview. We limit the main text to the most important points.

Our first problem is intractability of the cost function in Eq. 13. We can mitigate this by moving , the expectation over walker directions, inside the square brackets. This clearly modifies the objective, ignoring higher-order correlations between features induced by walker directions (but not lengths). However, it yields a cost function we can estimate efficiently, if not compute exactly.

The second challenge is optimising over the class of couplings , joint distributions over two discrete random variables with geometrically distributed marginals. As in Sec. 3.2, a sensible numerical approach is to optimise amongst a tractable subclass of . Copulas are unsuitable because in this discrete setting we cannot compute gradients to optimise the covariance matrix. Instead, we consider the family of measures on described by the permutation densities

| (14) |

with a permutation of order (that is, a bijection ). The unit square is split into a grid where each row and column has a single ‘tile’ of probability density and is otherwise.

Note that both marginal distributions of are manifestly uniform on . Moreover, the marginals can be transformed to an arbitrary probability distribution by pushing forward with the inverse CDF, . Transforming both coordinates in this way yields a joint measure which will give an unbiased estimator. We will refer to these as -couplings, and remark that such couplings exist for a given permutation order .

The permutations can be interpreted as matchings between the quantiles of the geometric distributions over the lengths of a pair of walkers. With the right choice of , they can ensure that e.g. if one of the walk lengths is short then the other tends to be long, diversifying the ensemble. In App. C.1 we formalise this by writing the optimisation of as a bipartite matching problem, with a cost matrix estimated by sampling walks. Unfortunately, the matching problem has quadratic weights (albeit with some extra symmetric structure). It is challenging; we discuss progress towards a fast, exact algorithm in App. C.3.1. More pragmatically, with another simplification we can obtain a related linear-weights bipartite matching problem. This can be solved efficiently in time using linear programming techniques, e.g. the Hungarian algorithm (Kuhn, 1955), thereby optimising the coupling . Taking the optimal permutation , we define -coupled GRFs as follows.

Besides being easy to optimise and sample from, there are also more rigorous OT motivations for the choice of -couplings . They relate to the asymptotic behaviour of as the permutation order and the stability of OT plans (Villani, 2021). We defer this technical point to App. D.

As in Sec. 3.2, an interesting question is whether one could couple the lengths of walkers. This is challenging and has received little attention in the literature. One possibility would be to combine permutations, finding a minimum-weights -partite matching with all subgraphs constrained to be complete . Another approach would be to approximately solve this multi-marginal OT problem using the Sinkhorn-Knopp algorithm (Sinkhorn and Knopp, 1967; Cuturi, 2013).

Broader applicability. As a final remark, the utility of our OT-approach to coupling walker lengths extends to graph-based estimators beyond GRFs. For example, it can be used to improve estimates of the PageRank vector, a popular measure of the relative importance of the nodes of a graph proposed by Page et al. (1998) to rank websites in search engine results. We discuss this in App. E.

4.2 Experiments with -coupled GRFs

In this section, we empirically evaluate -coupled GRFs for variance reduction of graph node kernel estimates. We begin by testing our method on a variety of real-world graphs, then show that lower variance unlocks better approximate inference with scalable graph-based Gaussian processes (GPs).

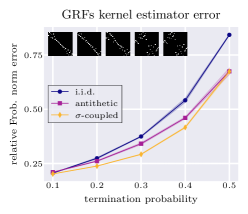

Gram matrix approximation. GRFs take the termination probability as a hyperparameter, determining the rate of decay of the geometric distribution over walk length. A smaller value of samples longer walks and gives more accurate kernel estimates, but takes longer to run. The optimal coupling changes depending on . We will consider the values , finding the optimal permutation in each case.

To find the optimal , we solve the matching problem (App. C.3) for a random Erdős-Rényi graph with nodes, taking a permutation order and choosing the -regularised Laplacian kernel as our target. We then use the Hungarian algorithm, averaging the cost matrix over every possible node pair to find a coupling that reduces the variance of all entries of the Gram matrix.

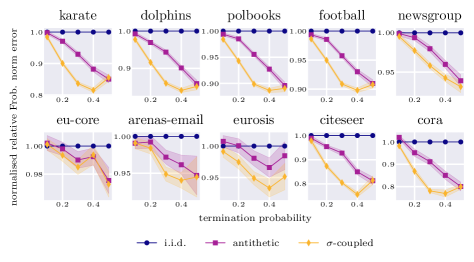

Having computed couplings for each value of , we then test the corresponding -coupled GRFs on a variety of real-world graphs. Fig. 1 shows the results for cora (), with the rest left to App. F.1. We plot the relative Frobenius norm error of the Gram matrix approximation with walkers that are i.i.d., antithetic (Reid et al., 2024c) or -coupled. For every value of , -coupled GRFs give equally good or smaller kernel estimator errors. Our general-purpose OT approach often substantially outperforms antithetic termination: a bespoke algorithm designed specifically to improve GRFs. We include visualisations of the optimal permutations for different values of in the inset, verifying that the -coupling adapts to different GRF hyperparamaters.

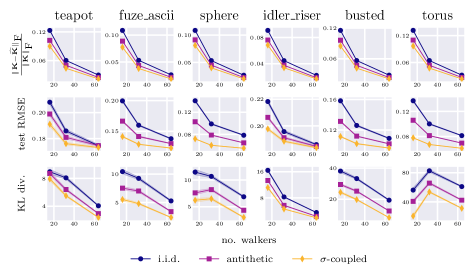

Novel application: -coupled GRFs for scalable graph-based GPs. We conclude this section by applying -coupled GRFs to scalable graph-based Gaussian processes (GPs), where we find that the improved estimation of the covariance function permits better approximate inference. Scalable GPs are a novel application of GRFs that may be of independent interest; we provide discussion in App. F.

Let us consider the task of probabilistic graph interpolation. This aims to predict unknown values corresponding to particular graph nodes from a set of observed values, along with principled uncertainty estimates (Pfaff et al., 2020). We consider mesh graphs where every node is associated with a normal vector (Dawson-Haggerty, 2023). The objective is to predict the -components of a masked set, with . To predict the missing normal vectors, we use a graph-based GP with a heat kernel covariance function. We compute a sparse, unbiased approximation of this kernel using GRFs with walkers that are i.i.d., antithetic (Reid et al., 2024c) or -coupled. Details of GP hyperparameter optimisation are given in App. F.2.

Fig. 2 shows the results. For mesh graphs of different sizes (the largest as big as nodes), we plot the relative Frobenius norm error of the Gram matrix approximation, the test root mean square error (RMSE), and the KL divergence to the true posterior. We see that the improvement in covariance function estimation unlocks better predictive accuracy and better uncertainty quantification.

Probabilistic interpolation of traffic data. To further demonstrate, we train a scalable graph-based GP on a traffic flow dataset of the highways of San Jose, California, curated by Borovitskiy et al. (2021) using data from Chen et al. (2001) and OpenStreetMap. The graph has nodes, with the traffic speed available at . With this sparse, noisy dataset, -coupled GRFs again give more accurate predictions and better uncertainty estimates. Full results are reported in App. F.3.

5 Discussion and outlook

OT provides a powerful paradigm for variance reduction with random features. It offers proof techniques and numerical algorithms for finding novel RF couplings on continuous and discrete input domains. Whilst the presence of variance reduction is unambiguous, the downstream benefits it provides are less clear. With GRFs for scalable GPs, variance reduction permits much better approximate inference (Sec. 4.2). With RFFs and RLFs, this is not the case (App. B.2). This surprising finding suggests that, though popular, variance reduction is not always the right goal.

Right framing, wrong cost function. The reason for this counterintuitive behaviour is that, even if a coupling guarantees lower variance pointwise kernel estimates , functions like the predictive mean and KL-divergence are highly nonlinear in these estimates. For example, they may involve inverting a Gram matrix. It is hard to predict how the bias and variance of these downstream quantities will depend on the distribution of the pointwise estimates; they are not guaranteed to improve. Couplings that reduce the variance of and often also modify their covariance, which may effect downstream estimators that combine them. This includes seemingly innocuous quantities like the KL divergence from the true to the approximate prior (App. B.2).

We posit that OT provides the right framing for the problem of coupling RFs, but sometimes pointwise kernel variance is the wrong cost function. This naive choice may not fully capture how the joint distribution over kernel estimates determines downstream performance. Coupling to optimise e.g. the spectral properties of may prove better (Choromanski et al., 2018; Avron et al., 2017a). Fortunately, OT provides a suite of theoretical and numerical tools achieve this; one simply modifies the cost function in Eq. 2. We hope this research will spur further work in this exciting direction.

6 Contributions and acknowledgements

Relative contributions. IR conceptualised the project, proposed the coupling mechanisms in Defs 3.3 and 4.1, proved the major theoretical contributions, ran the GRF experiments and wrote the manuscript. SM designed and ran the RFF and RLF GP experiments (Sec. 3.3), helped shape the project’s direction and made core contributions to the text. KC acted as the senior lead, providing technical guidance and developing the algorithms for the matching problem in App. C.3.1. RET met frequently throughout the project, giving important advice and support. AW provided helpful discussion, supervision and feedback on the manuscript.

Acknowledgements and funding. IR acknowledges support from a Trinity College External Studentship. SM acknowledges funding from the Vice Chancellor’s and the George and Marie Vergottis scholarship of the Cambridge Trust, and the Qualcomm Innovation Fellowship. RET is supported by Google, Amazon, ARM, Improbable and an EPSRC grant EP/T005386/1. AW acknowledges support from a Turing AI fellowship under grant EP/V025279/1 and the Leverhulme Trust via CFI.

We thank Bruno Mlodozeniec for his suggestion to use copulas in Sec. 3.2 and Mark Rowland for insightful discussions about multi-marginal optimal transport and the limitations of pointwise variance reduction. Viacheslav Borovitskiy helped guide our discussion of scalable graph-based GPs and, together with Iskander Azangulov, kindly provided updated code for loading the traffic data graph in Sec. 4.2 and App. F.3. We thank Matt Ashman and Arijit Sehanobish for their thoughtful feedback on the text, and Jihao Andreas Lin for interesting suggestions about possible GP applications.

References

- Alon et al. (2007) Noga Alon, Itai Benjamini, Eyal Lubetzky, and Sasha Sodin. Non-backtracking random walks mix faster. Communications in Contemporary Mathematics, 9(04):585–603, 2007. URL https://doi.org/10.1142/S021919970700255.

- Avron et al. (2017a) Haim Avron, Michael Kapralov, Cameron Musco, Christopher Musco, Ameya Velingker, and Amir Zandieh. Random fourier features for kernel ridge regression: Approximation bounds and statistical guarantees. In International conference on machine learning, pages 253–262. PMLR, 2017a. URL https://doi.org/10.48550/arXiv.1804.09893.

- Avron et al. (2017b) Haim Avron, Michael Kapralov, Cameron Musco, Christopher Musco, Ameya Velingker, and Amir Zandieh. Random fourier features for kernel ridge regression: Approximation bounds and statistical guarantees. In Proceedings of the 34th International Conference on Machine Learning, ICML 2017, Sydney, NSW, Australia, 6-11 August 2017, volume 70 of Proceedings of Machine Learning Research, pages 253–262. PMLR, 2017b. URL http://proceedings.mlr.press/v70/avron17a.html.

- Bhat and Mondal (2021) Chandra R Bhat and Aupal Mondal. On the almost exact-equivalence of the radial and spherical unconstrained choleskybased parameterization methods for correlation matrices. Technical report, Department of Civil, Architectural and Environmental Engineering, The University of Texas at Austin, 2021. URL https://repositories.lib.utexas.edu/server/api/core/bitstreams/69c04b9a-2175-4392-b7b0-a8f5445ad405/content.

- Billingsley (2013) Patrick Billingsley. Convergence of probability measures. John Wiley & Sons, 2013.

- Bojarski et al. (2017) Mariusz Bojarski, Anna Choromanska, Krzysztof Choromanski, Francois Fagan, Cedric Gouy-Pailler, Anne Morvan, Nouri Sakr, Tamas Sarlos, and Jamal Atif. Structured adaptive and random spinners for fast machine learning computations. In Artificial intelligence and statistics, pages 1020–1029. PMLR, 2017. URL https://doi.org/10.48550/arXiv.1610.06209.

- Borovitskiy et al. (2021) Viacheslav Borovitskiy, Iskander Azangulov, Alexander Terenin, Peter Mostowsky, Marc Deisenroth, and Nicolas Durrande. Matérn gaussian processes on graphs. In International Conference on Artificial Intelligence and Statistics, pages 2593–2601. PMLR, 2021. URL https://doi.org/10.48550/arXiv.2010.15538.

- Campbell (2002) Colin Campbell. Kernel methods: a survey of current techniques. Neurocomputing, 48(1-4):63–84, 2002. URL https://doi.org/10.1016/S0925-2312(01)00643-9.

- Canu and Smola (2006) Stéphane Canu and Alex Smola. Kernel methods and the exponential family. Neurocomputing, 69(7-9):714–720, 2006. URL https://doi.org/10.1016/j.neucom.2005.12.009.

- Chapelle et al. (2002) Olivier Chapelle, Jason Weston, and Bernhard Schölkopf. Cluster kernels for semi-supervised learning. Advances in neural information processing systems, 15, 2002. URL https://dl.acm.org/doi/10.5555/2968618.2968693.

- Chen et al. (2001) Chao Chen, Karl Petty, Alexander Skabardonis, Pravin Varaiya, and Zhanfeng Jia. Freeway performance measurement system: mining loop detector data. Transportation research record, 1748(1):96–102, 2001. URL https://api.semanticscholar.org/CorpusID:108891582.

- Chi et al. (2019) Jinjin Chi, Jihong Ouyang, Ximing Li, Yang Wang, and Meng Wang. Approximate optimal transport for continuous densities with copulas. In IJCAI, pages 2165–2171, 2019. URL https://www.ijcai.org/proceedings/2019/0300.pdf.

- Choromanski et al. (2018) Krzysztof Choromanski, Mark Rowland, Tamás Sarlós, Vikas Sindhwani, Richard Turner, and Adrian Weller. The geometry of random features. In International Conference on Artificial Intelligence and Statistics, pages 1–9. PMLR, 2018. URL http://proceedings.mlr.press/v84/choromanski18a/choromanski18a.pdf.

- Choromanski et al. (2020) Krzysztof Choromanski, Valerii Likhosherstov, David Dohan, Xingyou Song, Andreea Gane, Tamas Sarlos, Peter Hawkins, Jared Davis, Afroz Mohiuddin, Lukasz Kaiser, et al. Rethinking attention with performers. arXiv preprint arXiv:2009.14794, 2020. URL https://doi.org/10.48550/arXiv.2009.14794.

- Choromanski et al. (2017) Krzysztof M Choromanski, Mark Rowland, and Adrian Weller. The unreasonable effectiveness of structured random orthogonal embeddings. Advances in neural information processing systems, 30, 2017. URL https://doi.org/10.48550/arXiv.1703.00864.

- Choromanski (2023) Krzysztof Marcin Choromanski. Taming graph kernels with random features. In International Conference on Machine Learning, pages 5964–5977. PMLR, 2023. URL https://doi.org/10.48550/arXiv.2305.00156.

- Chung (1997) Fan RK Chung. Spectral graph theory, volume 92. American Mathematical Soc., 1997.

- Cuturi (2013) Marco Cuturi. Sinkhorn distances: Lightspeed computation of optimal transport. Advances in neural information processing systems, 26, 2013. URL https://papers.nips.cc/paper_files/paper/2013/file/af21d0c97db2e27e13572cbf59eb343d-Paper.pdf.

- Dao et al. (2017) Tri Dao, Christopher M De Sa, and Christopher Ré. Gaussian quadrature for kernel features. Advances in neural information processing systems, 30, 2017. URL https://doi.org/10.48550/arXiv.1709.02605.

- Dasgupta et al. (2010) Anirban Dasgupta, Ravi Kumar, and Tamás Sarlós. A sparse johnson: Lindenstrauss transform. In Proceedings of the forty-second ACM symposium on Theory of computing, pages 341–350, 2010. URL https://doi.org/10.1145/1806689.1806737.

- Dasgupta and Gupta (2003) Sanjoy Dasgupta and Anupam Gupta. An elementary proof of a theorem of johnson and lindenstrauss. Random Struct. Algorithms, 22(1):60–65, 2003. doi: 10.1002/RSA.10073. URL https://doi.org/10.1002/rsa.10073.

- Dawson-Haggerty (2023) Michael Dawson-Haggerty. Trimesh repository, 2023. URL https://github.com/mikedh/trimesh.

- Dick et al. (2013) Josef Dick, Frances Y Kuo, and Ian H Sloan. High-dimensional integration: the quasi-monte carlo way. Acta Numerica, 22:133–288, 2013. URL https://doi.org/10.1017/S0962492913000044.

- Fogaras et al. (2005) Dániel Fogaras, Balázs Rácz, Károly Csalogány, and Tamás Sarlós. Towards scaling fully personalized pagerank: Algorithms, lower bounds, and experiments. Internet Mathematics, 2(3):333–358, 2005. URL https://doi.org/10.1007/978-3-540-30216-2_9.

- Glasserman and Yao (1992) Paul Glasserman and David D Yao. Some guidelines and guarantees for common random numbers. Management Science, 38(6):884–908, 1992. URL https://doi.org/10.1287/mnsc.38.6.884.

- Goemans and Williamson (2001) Michel X Goemans and David Williamson. Approximation algorithms for max-3-cut and other problems via complex semidefinite programming. In Proceedings of the thirty-third annual ACM symposium on Theory of computing, pages 443–452, 2001. URL https://doi.org/10.1016/j.jcss.2003.07.012.

- Halton (1960) John H Halton. On the efficiency of certain quasi-random sequences of points in evaluating multi-dimensional integrals. Numerische Mathematik, 2:84–90, 1960. URL https://doi.org/10.1007/BF01386213.

- Hammersley and Morton (1956) JM Hammersley and KW Morton. A new monte carlo technique: antithetic variates. In Mathematical proceedings of the Cambridge philosophical society, volume 52, pages 449–475. Cambridge University Press, 1956. URL https://doi.org/10.1017/S0305004100031455.

- Haugh (2016) Martin Haugh. An introduction to copulas. quantitative risk management. Lecture Notes. New York: Columbia University, 2016. URL http://www.columbia.edu/~mh2078/QRM/Copulas.pdf.

- Ivashkin (2023) Vladimir Ivashkin. Community graphs repository, 2023. URL https://github.com/vlivashkin/community-graphs.

- Johnson (1984) William B Johnson. Extensions of lipschitz mappings into a hilbert space. Contemp. Math., 26:189–206, 1984. URL http://stanford.edu/class/cs114/readings/JL-Johnson.pdf.

- Kingma and Ba (2014) Diederik P Kingma and Jimmy Ba. Adam: A method for stochastic optimization. arXiv preprint arXiv:1412.6980, 2014. URL https://doi.org/10.48550/arXiv.1412.6980.

- Kondor and Lafferty (2002) Risi Imre Kondor and John Lafferty. Diffusion kernels on graphs and other discrete structures. In Proceedings of the 19th international conference on machine learning, volume 2002, pages 315–322, 2002. URL https://www.ml.cmu.edu/research/dap-papers/kondor-diffusion-kernels.pdf.

- Kontorovich et al. (2008) Leonid Kontorovich, Corinna Cortes, and Mehryar Mohri. Kernel methods for learning languages. Theor. Comput. Sci., 405(3):223–236, 2008. doi: 10.1016/j.tcs.2008.06.037. URL https://doi.org/10.1016/j.tcs.2008.06.037.

- Kuhn (1955) Harold W Kuhn. The hungarian method for the assignment problem. Naval research logistics quarterly, 2(1-2):83–97, 1955. URL https://doi.org/10.1002/nav.3800020109.

- Lázaro-Gredilla et al. (2010) Miguel Lázaro-Gredilla, Joaquin Quinonero-Candela, Carl Edward Rasmussen, and Aníbal R Figueiras-Vidal. Sparse spectrum gaussian process regression. The Journal of Machine Learning Research, 11:1865–1881, 2010. URL https://jmlr.csail.mit.edu/papers/volume11/lazaro-gredilla10a/lazaro-gredilla10a.pdf.

- Le et al. (2013) Quoc Le, Tamás Sarlós, Alex Smola, et al. Fastfood-approximating kernel expansions in loglinear time. In Proceedings of the international conference on machine learning, volume 85, 2013. URL https://doi.org/10.48550/arXiv.1408.3060.

- Likhosherstov et al. (2022) Valerii Likhosherstov, Krzysztof M Choromanski, Kumar Avinava Dubey, Frederick Liu, Tamas Sarlos, and Adrian Weller. Chefs’ random tables: Non-trigonometric random features. Advances in Neural Information Processing Systems, 35:34559–34573, 2022. URL https://doi.org/10.48550/arXiv.2205.15317.

- Liu et al. (2022) Fanghui Liu, Xiaolin Huang, Yudong Chen, and Johan A. K. Suykens. Random features for kernel approximation: A survey on algorithms, theory, and beyond. IEEE Trans. Pattern Anal. Mach. Intell., 44(10):7128–7148, 2022. doi: 10.1109/TPAMI.2021.3097011. URL https://doi.org/10.1109/TPAMI.2021.3097011.

- Luo (2019) Siqiang Luo. Distributed pagerank computation: An improved theoretical study. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 33, pages 4496–4503, 2019. URL https://doi.org/10.1609/aaai.v33i01.33014496.

- Lyu (2017) Yueming Lyu. Spherical structured feature maps for kernel approximation. In International Conference on Machine Learning, pages 2256–2264. PMLR, 2017. URL http://proceedings.mlr.press/v70/lyu17a/lyu17a.pdf.

- Morokoff and Caflisch (1995) William J Morokoff and Russel E Caflisch. Quasi-monte carlo integration. Journal of computational physics, 122(2):218–230, 1995. URL https://doi.org/10.1006/jcph.1995.1209.

- Munkhoeva et al. (2018) Marina Munkhoeva, Yermek Kapushev, Evgeny Burnaev, and Ivan Oseledets. Quadrature-based features for kernel approximation. Advances in neural information processing systems, 31, 2018. URL https://doi.org/10.48550/arXiv.1802.03832.

- Nelsen (2006) Roger B Nelsen. An introduction to copulas. Springer, 2006.

- Page et al. (1998) Lawrence Page, Sergey Brin, Rajeev Motwani, and Terry Winograd. The pagerank citation ranking: Bring order to the web. Technical report, Technical report, stanford University, 1998. URL https://www.cis.upenn.edu/~mkearns/teaching/NetworkedLife/pagerank.pdf.

- Panaretos and Zemel (2020) Victor M Panaretos and Yoav Zemel. An invitation to statistics in Wasserstein space. Springer Nature, 2020.

- Pfaff et al. (2020) Tobias Pfaff, Meire Fortunato, Alvaro Sanchez-Gonzalez, and Peter W Battaglia. Learning mesh-based simulation with graph networks. arXiv preprint arXiv:2010.03409, 2020. URL https://doi.org/10.48550/arXiv.2010.03409.

- Rahimi and Recht (2007) Ali Rahimi and Benjamin Recht. Random features for large-scale kernel machines. Advances in neural information processing systems, 20, 2007. URL https://people.eecs.berkeley.edu/~brecht/papers/07.rah.rec.nips.pdf.

- Rahimi and Recht (2008) Ali Rahimi and Benjamin Recht. Weighted sums of random kitchen sinks: Replacing minimization with randomization in learning. In Advances in Neural Information Processing Systems 21, Proceedings of the Twenty-Second Annual Conference on Neural Information Processing Systems, Vancouver, British Columbia, Canada, December 8-11, 2008, pages 1313–1320, 2008. URL https://papers.nips.cc/paper_files/paper/2008/file/0efe32849d230d7f53049ddc4a4b0c60-Paper.pdf.

- Reid et al. (2023) Isaac Reid, Krzysztof Marcin Choromanski, Valerii Likhosherstov, and Adrian Weller. Simplex random features. In International Conference on Machine Learning, pages 28864–28888. PMLR, 2023. URL https://doi.org/10.48550/arXiv.2301.13856.

- Reid et al. (2024a) Isaac Reid, Eli Berger, Krzysztof Choromanski, and Adrian Weller. Repelling random walks. In International Conference on Learning Representations, 2024a. URL https://doi.org/10.48550/arXiv.2310.04854.

- Reid et al. (2024b) Isaac Reid, Krzysztof Choromanski, Eli Berger, and Adrian Weller. General graph random features. In International Conference on Learning Representations, 2024b. URL https://doi.org/10.48550/arXiv.2310.04859.

- Reid et al. (2024c) Isaac Reid, Adrian Weller, and Krzysztof M Choromanski. Quasi-monte carlo graph random features. Advances in Neural Information Processing Systems, 36, 2024c. URL https://doi.org/10.48550/arXiv.2305.12470.

- Rowland et al. (2018) Mark Rowland, Krzysztof M Choromanski, François Chalus, Aldo Pacchiano, Tamas Sarlos, Richard E Turner, and Adrian Weller. Geometrically coupled monte carlo sampling. Advances in Neural Information Processing Systems, 31, 2018. URL https://mlg.eng.cam.ac.uk/adrian/NeurIPS18-gcmc.pdf.

- Scholkopf and Smola (2018) Bernhard Scholkopf and Alexander J Smola. Learning with kernels: support vector machines, regularization, optimization, and beyond. MIT press, 2018.

- Shen et al. (2017) Weiwei Shen, Zhihui Yang, and Jun Wang. Random features for shift-invariant kernels with moment matching. In Proceedings of the AAAI conference on artificial intelligence, volume 31, 2017. URL https://doi.org/10.1609/aaai.v31i1.10825.

- Sinkhorn and Knopp (1967) Richard Sinkhorn and Paul Knopp. Concerning nonnegative matrices and doubly stochastic matrices. Pacific Journal of Mathematics, 21(2):343–348, 1967. URL https://msp.org/pjm/1967/21-2/pjm-v21-n2-p14-s.pdf.

- Sklar (1959) M Sklar. Fonctions de répartition à n dimensions et leurs marges. In Annales de l’ISUP, volume 8, pages 229–231, 1959. URL https://hal.science/hal-04094463/document.

- Smola and Kondor (2003a) Alexander J. Smola and Risi Kondor. Kernels and regularization on graphs. In Computational Learning Theory and Kernel Machines, 16th Annual Conference on Computational Learning Theory and 7th Kernel Workshop, COLT/Kernel 2003, Washington, DC, USA, August 24-27, 2003, Proceedings, volume 2777 of Lecture Notes in Computer Science, pages 144–158. Springer, 2003a. URL https://doi.org/10.1007/978-3-540-45167-9_12.

- Smola and Kondor (2003b) Alexander J Smola and Risi Kondor. Kernels and regularization on graphs. In Learning Theory and Kernel Machines: 16th Annual Conference on Learning Theory and 7th Kernel Workshop, COLT/Kernel 2003, Washington, DC, USA, August 24-27, 2003. Proceedings, pages 144–158. Springer, 2003b. URL https://people.cs.uchicago.edu/~risi/papers/SmolaKondor.pdf.

- Smola and Schölkopf (2002) Alexander J. Smola and Bernhard Schölkopf. Bayesian kernel methods. In Advanced Lectures on Machine Learning, Machine Learning Summer School 2002, Canberra, Australia, February 11-22, 2002, Revised Lectures, volume 2600 of Lecture Notes in Computer Science, pages 65–117. Springer, 2002. URL https://doi.org/10.1007/3-540-36434-X_3.

- Thorpe (2019) Matthew Thorpe. Introduction to optimal transport. Lecture Notes, 3, 2019. URL https://www.damtp.cam.ac.uk/research/cia/files/teaching/Optimal_Transport_Notes.pdf.

- Tripp et al. (2024) Austin Tripp, Sergio Bacallado, Sukriti Singh, and José Miguel Hernández-Lobato. Tanimoto random features for scalable molecular machine learning. Advances in Neural Information Processing Systems, 36, 2024. URL https://doi.org/10.48550/arXiv.2306.14809.

- Villani (2021) Cédric Villani. Topics in optimal transportation, volume 58. American Mathematical Soc., 2021.

- Villani et al. (2009) Cédric Villani et al. Optimal transport: old and new, volume 338. Springer, 2009.

- Williams and Rasmussen (2006) Christopher KI Williams and Carl Edward Rasmussen. Gaussian processes for machine learning, volume 2. MIT press Cambridge, MA, 2006.

- Yang et al. (2014a) Jiyan Yang, Vikas Sindhwani, Haim Avron, and Michael W. Mahoney. Quasi-monte carlo feature maps for shift-invariant kernels. In Proceedings of the 31th International Conference on Machine Learning, ICML 2014, Beijing, China, 21-26 June 2014, volume 32 of JMLR Workshop and Conference Proceedings, 2014a. URL http://proceedings.mlr.press/v32/yangb14.html.

- Yang et al. (2014b) Jiyan Yang, Vikas Sindhwani, Quanfu Fan, Haim Avron, and Michael W Mahoney. Random laplace feature maps for semigroup kernels on histograms. In Proceedings of the IEEE Conference on Computer Vision and Pattern Recognition, pages 971–978, 2014b. URL https://vikas.sindhwani.org/RandomLaplace.pdf.

- Yu et al. (2016) Felix Xinnan X Yu, Ananda Theertha Suresh, Krzysztof M Choromanski, Daniel N Holtmann-Rice, and Sanjiv Kumar. Orthogonal random features. Advances in neural information processing systems, 29, 2016. URL https://doi.org/10.48550/arXiv.1610.09072.

- Zhi et al. (2023) Yin-Cong Zhi, Yin Cheng Ng, and Xiaowen Dong. Gaussian processes on graphs via spectral kernel learning. IEEE Transactions on Signal and Information Processing over Networks, 2023. URL https://doi.org/10.48550/arXiv.2006.07361.

- Zhou et al. (2015) Zhuojie Zhou, Nan Zhang, and Gautam Das. Leveraging history for faster sampling of online social networks. arXiv preprint arXiv:1505.00079, 2015. URL https://doi.org/10.48550/arXiv.1505.00079.

Appendix A Solving the OT problem for RFFs and RLFs

In this appendix, we provide proofs for the theoretical results in Sec. 3.1 and supplement the discussion of copula-based numerical OT solvers in Sec. 3.2.

A.1 Proof of Lemma 3.1

We begin by proving Lemma 3.1, which formulates variance reduction for RFFs and RLFs as an optimal transport problem. We will first reason about the simpler case of RLFs, then consider RFFs.

Lemma A.1 (Kernel estimator MSE for RLFs [Reid et al., 2023]).

When estimating the Gaussian kernel for datapoints using random Laplace features (synonymously, positive random features), the mean square error of the kernel estimate is given by:

| (15) |

where is the number of sampled random frequencies, is a data-dependent scalar and is the RF-conformity,

| (16) |

Here, is the norm of the resultant of a pair of distinct frequencies and is the Gamma function.

Proof. Reid et al. [2023]. ∎

The simple derivation, reported in full by Reid et al. [2023], is based on rewriting the angular integral as a Hankel transform, yielding a Bessel function of the first kind with a known Taylor expansion.

Supposing that , we have that , where denotes the -norm of the frequency . Note that, for to be marginally Gaussian, we require that the marginal distribution over its norm is , a Chi distribution with degrees of freedom. Substituting this into Eq. 15 and dropping terms unmodified by the coupling and irrelevant multiplicative factors, it is straightforward to arrive at the expression for the cost function in Eq. 7.

Finding the cost function for RFFs is only slightly more difficult. We begin by citing another recent result by Reid et al. [2023].

Lemma A.2 (Kernel estimator MSE for RFFs [Reid et al., 2023]).

When estimating the Gaussian kernel for datapoints using random Fourier features, the mean square error of the kernel estimate is given by:

| (17) |

where is the number of samples, and is defined by

| (18) |

Proof. Reid et al. [2023]. ∎

Note the close resemblance to Eq. 16. The only term that depends on couplings between the random frequencies is , which we seek to suppress with carefully engineered correlations. From elementary trigonometry, , and for any coupling scheme is isotropic. Defining the random variables and and integrating out the angular part,

| (19) |

where is a Bessel function of the first kind, order . If , so their distributions are identical. It follows that we can write

| (20) |

Again dropping multiplicative factors and terms unmodified by the coupling, we arrive at the RFF OT cost function specified in Eq. 7. This completes the derivation. ∎

A.2 Proof of Thm. 3.2

We now solve the OT problem formulated in Lemma 3.1 exactly in the special case that (with mild asymptotic assumptions for RFFs). For the reader’s convenience, we copy it from the main text below.

Theorem A.3 (Solution to OT problem when ).

Denote by the cumulative distribution function of . Considering orthogonal frequencies with norms , the OT problem in Eq. 6 is solved by the negative monotone coupling

| (21) |

when for RFFs and in full generality for RLFs.

The proof of Thm. 3.2 uses ideas from optimal transport theory. In particular, it modifies arguments made for a related problem by (among others) Thorpe [2019], to which we direct the interested reader for further context and discussion. Before giving the proof, we establish some basic definitions and results.

Definition A.4 (-monotone sets).

Given a cost function , we refer to a set as -monotone if for all pairs we have that

| (22) |

It is intuitive that -monotonicity should be a property of the support of Kantorovich optimal transport plan: if we could have accessed lower cost by sending and instead of and , the plan would have done this instead. This is formalised as follows.

Lemma A.5 (Support of optimal transport plan is -monotone [Thorpe, 2019]).

Consider , and assume that is the Kantorovich optimal transport plan for a continuous cost function . Then for all we have that

| (23) |

Proof. Thorpe [2019]. ∎

We are now ready to provide our proof of Thm. 3.2.

Proof of Thm. 3.2. Inspecting the cost functions in Eq. 7, it is clear that in the special case we have that

| (24) |

with and as usual.

First consider . We claim that for any satisfying Eq. 23 for this , implies . This is seen by observing that

| (25) |

Supposing that , Eq. 23 is satisfied if and only if , verifying the statement.

Denote by the support of the optimal transport plan for the cost function , and consider some point . An immediate implication of the statement above is that

| (26) |

Let , , and . Note that so since the measure is normalised. The subsets are also disjoint apart from , a singleton of zero measure.222e.g. since and since the marginal measure is nonatomic. Eq. 26 implies that , whereupon . Now and the set is zero measure. Therefore, . Likewise, . Relabelling by , Eq. 21 immediately follows. This completes the proof that negative monotone coupling minimises the kernel estimator variance for orthogonal RLFs.

Let us now turn to the case of RFFs. The optimal transport plan will instead be -monotone. Unfortunately, Eq. 25 does not hold in general for , so we cannot immediately use the same arguments to conclude that the OT plan is negative monotone. However, Eq. 25 does hold if we just consider the first nontrivial term in the Taylor expansion in or . In particular, dropping terms that are not modified by a coupling (i.e. depend only on or ),

| (27) |

It is straightforward to show that, if we take the limit so we can neglect higher-order terms, indeed satisfies Eq. 25 and we can make the same arguments about as with . In this limit, the optimal transport plan is again negative monotone. The proof is then complete. ∎

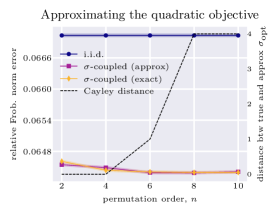

Comments on the limit for RFFs. We have seen that for RFFs it is only possible to solve the OT problem in Eq. 6 exactly in the asymptotic limit. Here, we comment on why this result is nonetheless interesting and useful. Firstly, note that in practice pairwise norm coupling still substantially suppresses kernel estimator variance, even at data lengthscales chosen by training an exact GP independent of the RF construction (Table 1). Even if at bigger the method no longer provides the smallest possible estimator variance, it can still substantially reduce it compared to an i.i.d. coupling. Second, from a more theoretical perspective, the , small sample regime is exactly where standard QMC methods often fail. It is interesting that OT-driven methods can still provide theoretical guarantees in this low-sample, high-dimensionality setting. Last, we note that, for RFF variance reduction schemes, it is very common to only guarantee gains in the asymptotic limit. This is also the case e.g. for orthogonality [Reid et al., 2023, Yu et al., 2016]: a well-established and widely-used algorithm.

A.3 Proof of Corollary 3.4

We now prove that pairwise norm-coupled RFs (Def. 3.3) provide strictly lower kernel estimator variance than i.i.d. RFs.

Proof of Corollary 3.4. Supposing that we have frequencies, the sum has terms in total. Of these, correspond are negative monotone norm couplings, and the remainder are independent. The independent terms are the same in the pairwise norm-coupled and fully i.i.d. configurations, so can be ignored. By Thm. 3.2, we have seen that negative monotone coupling exactly solves the variance reduction OT problem (under mild asymptotic assumptions for RFFs), so these variance contributions will be strictly smaller in the norm-coupled case. It immediately follows that pairwise norm-coupled RFs give strictly lower kernel estimator variance than orthogonal independent-norm RFs, so the result follows. ∎

A.4 Proof of Thm. 3.5

We now drop the restriction that and consider the variance reduction problem for frequencies whose respective direction is unconstrained. We will prove Thm. 3.5, which asserts that in this case the best possible coupling is antithetic, .

Proof of Thm. 3.5. Recalling the expression for RLF variance in Lemma A.1, the more general OT problem under consideration is

| (28) |

The term in square parentheses is an expectation of an infinite sum, every term of which is greater than or equal to . The sum is manifestly minimised if , which sets every term (apart from the first) to . This is achieved if and only if : a valid coupling called ‘antithetic sampling’. Any other joint distribution assigns nonzero probability to the event , so this optimal coupling is unique. ∎

A.5 Copulas as numerical OT solvers

copula_schematic

In the main text, we noted that finding an analytic solution to the multi-marginal OT problem for RFFs and RLFs (Eq. 6) is an open problem. In Sec. 3.2, we briefly presented an alternative numerical approach using copulas. Here, we discuss this in greater detail. Fig. 3 gives a visual overview.

Copulas. A copula is a multivariate cumulative distribution function (CDF) whose marginals are uniformly distributed on . By Sklar’s theorem [Sklar, 1959], its joint distribution can be arbitrary. Given a copula, we can easily enforce the constraint that its marginals are by pushing each coordinate forward with the inverse CDF , whilst retaining necessary flexibility in the joint to reduce estimator variance. Copulas can be used to model dependencies between random variables and are popular tools in quantitative finance [Haugh, 2016].

Gaussian copulas. The general family of copulas is still intractable to optimise and sample from so we constrain ourselves to Gaussian copulas. These are distributions with uniform marginals whose joint distributions are determined by multivariate Gaussians, defined below.

Definition A.6 (Gaussian copula).

Let where is a correlation matrix, i.e. a positive definite matrix with unit diagonals, and let be the CDF of the standard univariate Gaussian. We say is distributed according to a Gaussian copula with covariance and use the notation to denote this.

Parameterising correlation matrices. Gaussian copulas are easy to sample from since they involve sampling a multivariate Gaussian and applying the univariate Gaussian CDF. We are therefore left with the task of finding an appropriate correlation matrix for which we turn to numerical optimisation. The family of correlation matrices can be parameterised by a vector In fact, there exist tractable bijections between unconstrained vectors of real numbers and lower triangular Cholesky factors such that is a valid correlation matrix [Bhat and Mondal, 2021]. In particular, suppose that for each and we have where Then the parameterisation we use is

| (29) |

where Note that, since we are directly parameterising the Cholesky factor, we can sample from the associated Gaussian copula with an computational cost.

Optimising correlation matrices. In order to pick an appropriate correlation matrix we optimise it directly to minimise the root mean squared error (RMSE) loss

| (30) |

where Note that here depends on though we have suppressed this dependence for notational simplicity. Assuming that is differentiable with respect to which is the case in RFFs and RLFs, we can optimise the copula parameters by estimating the loss in Eq. 30, computing its gradients with respect to and updating its values accordingly.

Training curves. Fig. 4 shows an example of training curves for RFFs and RLFs using a numerically optimised Gaussian copula to learn an appropriate norm-coupling, here on the Boston dataset. We observe that the numerically optimised copula recovers the performance of the pairwise norm coupling scheme we proposed. This suggests that the proposed scheme may in fact be (close to) optimal. Rigorous analytical investigation is an important avenue for future work.

Appendix B RFF and RLF experimental details

In this appendix, we supplement the discussion in Sec. 3.3, providing more details of our experimental setup for Gram matrix estimation. We also apply norm-coupled RFs to sparse spectrum Gaussian processes [Lázaro-Gredilla et al., 2010], explaining the surprising closing remarks of Sec. 3 that in this case variance reduction does not help downstream performance.

B.1 Details for RFF and RLF experiments

Overview. In both our RFF and RLF experiments, we compare different coupling schemes for approximating the Gaussian kernel. The Gaussian kernel, including a lengthscale parameter an output scale variable and a noise scale parameter , takes the form

Our baselines include standard methods for sampling random frequency vectors for use within RFFs and RLFs: i.i.d. sampling and Halton sequences [Halton, 1960]. In addition, for both settings, we consider ensembles of frequency vectors that are coupled to have orthogonal directions but i.i.d. lengths. For a dataset of dimension for RFFs we use ensembles of orthogonal vectors. For RLFs we use ensembles of vectors, including orthogonal basis vectors and their antiparallel vectors.

Selecting kernel hyperparameters. We want to compare our coupling schemes using realistic kernel hyperparameter values, which we determine as follows. A realistic application setting for RFFs is within GPs for probabilistic regression. Therefore, we first fit a GP on a tractable subset of the data, specifically a maximum of 256 randomly chosen datapoints, to select appropriate parameters and We optimise the exact GP marginal likelihood with respect to these hyperparameters, and subsequently fix them. On the other hand, it is well-documented that RLFs suffer from poor estimator concentration when the data norm becomes large because of the exponential function in the feature map (Eq. 5); see e.g. Thm. 4 and App. F6 of Choromanski et al. [2020] or Thm. 4.3 of Likhosherstov et al. [2022], where the authors bound the -norm of queries and keys. This is anecdotally responsible for the deterioration in performance of Performers when networks become very deep. To reflect this fact and choose a data regime where vanilla RLFs can perform reasonably well (so we can assess any gains from our coupling), we set the lengthscale to two twice the average summed norm of the data, namely

| (31) |

over the training set. We train the rest of the kernel parameters ( and ) to maximise the marginal likelihood of the data under the exact GP.

Splitting procedure. To obtain mean evaluation metrics and standard errors, we evaluate the methods on multiple random splits as follows. For each dataset, we conduct cross validation with 20 splits, splitting each dataset into a training and a test set. Because we train an exact GP to determine kernel hyperparameters and evaluate its predictive NLL, we need to limit the number of datapoints used in both the training and the test set. We set them to a maximum of 256 points each by sub-sampling at random without replacement. After training the GP, we evaluate the metrics on the test set, and repeat this procedure for all 20 splits.

Optimisation details. We train the exact GP using the Adam optimiser [Kingma and Ba, 2014], using a learning rate of The exact GP optimisation stage converges around steps, and we run it up to steps.

B.2 Do better kernel approximations give better predictions?

Kernel and posterior approximations. Suppose that we have drawn an ensemble of frequency vectors from which we construct random features . Group these in a large design matrix ,

| (32) |

where of course depends on the ensemble frequencies (suppressed for notational compactness). For RFFs whereas for RLFs . We estimate the Gram matrix by .

As noted by Lázaro-Gredilla et al. [2010], this RF kernel approximation is exactly equivalent to a linear model, namely

| (33) |

where and The prior covariance of this linear model is which is, by construction, equal in expectation to the exact covariance produced by the kernel, namely . The predictive means of the approximate linear model and corresponding exact model are

| (34) | ||||

| (35) |

whereas the predictive covariances are

| (36) | ||||

| (37) |

Here, and are the design matrices corresponding to the training inputs and prediction outputs respectively, is the covariance matrix corresponding the training inputs, is the covariance matrix corresponding to the prediction inputs and and are the cross-covariance matrices between the training and prediction datapoints. These models become exactly equivalent in the limit of an infinite number of features since the kernel approximation becomes exact.

We have seen that pairwise norm coupling improves the approximation of the Gram matrices . In particular, we are able to suppress the variance of each pointwise kernel estimate (Thm. 3.2 and Corr. 3.4), and therefore the relative Frobenius norm error between the true and approximate Gram matrices (Table 1). In light of the discussion above, it would be natural to assume that this would result in more accurate approximations of the predictive mean and covariance. However, in the following section we will see that surprisingly this is not the case.

Evaluating posterior approximation quality. Table 2 takes the RFs from Sec. 3.3, where we found that our coupling can substantially improve the quality of kernel estimation. It then reports the KL divergence between the exact predictive posterior and the approximate predictive posteriors computed with RFFs and RLFs, respectively. To be clear, Eqs 34 and 36 can be rewritten

| (38) |

where , , and It is then straightforward to compute the KL divergence between Gaussian distributions with means , and covariances , .

| Fourier Features | Concrete | Abalone | CPU | Power | Airfoil | Boston |

|---|---|---|---|---|---|---|

| i.i.d. | ||||||

| Halton | ||||||

| Orthogonal | ||||||

| + PNC | ||||||

| Laplace Features | Concrete | Abalone | CPU | Power | Airfoil | Boston |

| i.i.d. | ||||||

| Halton | ||||||

| Orthogonal | ||||||

| + PNC + antithetic |

Surprisingly, we find that, even though our couplings improve the accuracy of kernel approximation, the approximate mean and covariance and hence the KL divergence to the true posterior do not necessarily improve. In Table 1 we routinely see variance reductions of -%, but even with very many trials this is not reflected in the data splits used for Table 2.

The reason for this experimental finding is that, as is clear in Eq. 38, the posterior is highly nonlinear in . This is on account of the presence of matrix multiplications and inversions. These nonlinear operations on the Gram matrix entries mean that, despite our pointwise estimates being unbiased, and are in fact biased. We have achieved our objective of variance reduction of – with pairwise norm coupling, it is both theoretically mandated and empirically observed. But clearly this does not necessitate variance (or bias) reduction for and . The relationship between the distribution of and the distribution of the approximate posterior is more complex.

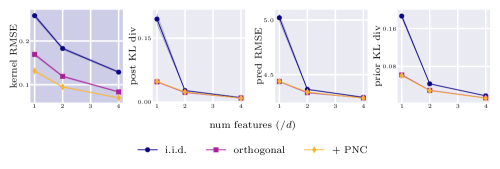

Variance reduction does not always help predictive performance. To sharpen this point, we now take a single data split of the power dataset and plot the the kernel approximation RMSE (i.e. kernel estimator variance), as well as various quantities of predictive interest, against the number of features . We exclude the Halton coupling (which is consistently worse than ‘orthogonal’) for clarity of presentation. Fig. 5 shows the results.

The left hand panel confirms that we have achieved our stated objective of variance reduction. Moreover, for all couplings the quality of approximation improves as we introduce more ensembles of size . Reading left to right, the other three panels show: (i) the KL divergence between the exact and approximate GP predictive posteriors (as in Table 2), (ii) the predictive RMSE on a held out test set, and (iii) the KL divergence between the exact and approximate GP priors. In every instance, orthogonality provides a substantial gain but, despite the encouraging results for kernel RMSE, there is no additional benefit from PNC. However, it would be wrong to draw the simplistic conclusion that PNC does not give large enough variance savings to see downstream gains: comparable reductions from orthogonality yield substantial improvements. The problem is more fundamental, relating to how the joint distribution of kernel estimates – beyond just the second moment of its pointwise entries – interacts with nonlinear operations like matrix multiplication and inversion.

A non-exhaustive list of publications with a substantial focus on reducing the variance of RF kernel estimates is given by: Yu et al. [2016], Rowland et al. [2018], Reid et al. [2023], Likhosherstov et al. [2022], Yang et al. [2014a], Le et al. [2013], Bojarski et al. [2017], Choromanski et al. [2017], Lyu [2017], Shen et al. [2017], Dao et al. [2017], Munkhoeva et al. [2018]. This can sometimes be a very effective approach for improving downstream performance; e.g. observe the benefits from -coupled GRFs in Sec. 4. But our findings suggest that the true reasons for any boost in performance are more complex than variance reduction alone. There has been some recognition that other properties of the kernel approximation are important e.g. for kernel ridge regression – in particular, the spectral properties of [Choromanski et al., 2018, Avron et al., 2017a] – but we believe this to be underappreciated in the literature. More work is needed to fully identify the right desiderata for RF couplings in machine learning, and more algorithms to optimise couplings to improve them. OT provides an excellent framework for achieving this.

Appendix C Graph random features

In this appendix, we provide a self-contained introduction to graph random features (GRFs) and previously-proposed techniques to reduce their variance. We also explain the motivations behind the series of approximations used in Sec. 4.1, and where possible provide empirical evidence that these approximations for tractability and efficiency do not substantially degrade the performance of the learned -coupling.

C.1 Constructing graph random features

For the reader’s convenience, we begin by providing a brief self-contained introduction to GRFs.

Graph node kernels. Recall that graph node kernels are positive definite, symmetric functions defined on pairs of nodes of . Note that one can also define kernels that take pairs of graphs as inputs, but these are not the object of our study.

Many of the most popular graph node kernels in the literature are functions of weighted adjacency matrices [Smola and Kondor, 2003b, Chapelle et al., 2002]. In particular, they are often functions of the graph Laplacian matrix,

| (39) |

where is a (weighted) adjacency matrix and is a diagonal degree matrix (satisfying ). It is also common to consider its normalised variant,

| (40) |

whose spectrum is contained in [Chung, 1997]. We provide examples in Table 3.

| Name | Form |

|---|---|

| -regularised Laplacian | |

| -step random walk | |

| Diffusion | |

| Inverse Cosine |

Formula for graph random features. Computing graph node kernels exactly is computationally expensive because of the cost of e.g. matrix inversion or exponentiation. Inspired by the success of random Fourier features in the Euclidean domain [Rahimi and Recht, 2007], the recently-introduced class of graph random features (GRFs) permits unbiased approximation of in subquadratic time [Choromanski, 2023, Reid et al., 2024b]. Intuitively, GRFs interpret the powers of weighted adjacency matrices in the Taylor expansions of the expressions in Table 3 as weighted sums over walks on a graph. Instead of computing this infinite sum of walks exactly, we can sample finite walks (using importance sampling) to construct an unbiased estimate of .

Concretely, GRFs compute a set of estimators such that by taking:333Strictly, for unbiased estimation of diagonal kernel entries we should construct two independent sets of features, but this is found to make little practical difference [Reid et al., 2024b] so we omit further discussion in this manuscript.

| (41) |

where is the th walk (out of a total of ) simulated out of the starting node . We remind the reader that by a ‘walk’ we mean a sequence of neighbouring graph nodes. The projection function maps from then set of graph random walks to a sparse -dimensional feature vector. It is computed as follows:

| (42) |

In this expression,

-

•

is the th component of the feature projection of the random walk (itself a sequence of neighbouring graph nodes beginning with ).

-

•

is the set of all graph walks between nodes and , of which each is a member.

-

•

is the indicator function that evaluates to if its argument is true and otherwise.

-

•

is the condition that , a particular walk between nodes and , is a prefix subwalk of , the random walk we actually sample.444Meaning that the walk from node initially follows , then optionally continues to visit further nodes. Note the subtle difference in usage of the symbol compared to in the expression , where it means ‘a member of the set of walks’ rather than ‘a prefix subwalk’.

-

•

is the modulation function, which controls the particular graph node kernel we choose to approximate.

-

•

is the length of graph walk .

-

•

is the marginal probability of sampling a random walk , which is known from the sampling strategy.

-

•

is a function that returns the products of weights of the edges traversed by .