Intertemporal Cost-efficient Consumption

Abstract.

We aim to provide an intertemporal, cost-efficient consumption model that extends the consumption optimization inspired by the Distribution Builder, a tool developed by Sharpe, Johnson, and Goldstein. The Distribution Builder enables the recovery of investors’ risk preferences by allowing them to select a desired distribution of terminal wealth within their budget constraints.

This approach differs from the classical portfolio optimization, which considers the agent’s risk aversion modeled by utility functions that are challenging to measure in practice. Our intertemporal model captures the dependent structure between consumption periods using copulas. This strategy is demonstrated using both the Black-Scholes and CEV models.

Mauricio Elizalde, Departamento de Matemáticas, Universidad Autónoma de Madrid. Calle Francisco Tomás y Valiente, 7, 28049, Madrid, Spain. (e-mail mauricio.elizalde@estudiante.uam.es)

Stephan Sturm, Department of Mathematical Sciences, Worcester Polytechnic Institute, 100 Institute Road, Worcester, MA 06109, USA. (e-mail: ssturm@wpi.edu)

Keywords: Cost-efficiency, distribution builder, copula, Girsanov theorem, Malliavin derivative, CEV model, Black-Scholes model, Laplace transform.

Mathematics Subject Classification (2010): 60H05, 60H07, 60H10, 60H35, 91G10.

JEL classification: C02, G11, G11.

1. Introduction

In this work, we address the problem of intertemporal optimal consumption, a model to consume an investment aiming to attain desired distributions while minimizing costs. We develop our model in the same spirit of the Distribution Builder, a tool developed by Sharpe et al. (refer to [GJS08] and [Sha06]), which is designed to recover the investor’s risk preferences by allowing them to arrange blocks in a screen that represent units of probability to shape their own consumption distribution attained to an initial capital.

Our methodology stands in contrast to classical portfolio optimization, which relies on modeling the risk aversion of the agent through utility functions. However, utility functions can be challenging to measure in practice and under certain circumstances they violate most assumptions ([Tve75]). As a result, our intertemporal approach provides an alternative that avoids the complexities associated with utility functions and offers a more flexible and practical solution for achieving optimal consumption distributions.

In their works [GJS08] and [Sha06], the authors focused on a single-period model and utilized the Distribution Builder with a finite equiprobable probability space , where , and . In this context, the wealth distribution can be represented as follows

where represents the outcome of a random variable in the states respectively. We associate each of the random variable with one of the states of the market.

The expression of the minimum-cost problem in the equiprobable space is given by the following formula:

where is the state price process or price kernel. Consequently, each claim is priced as .

Dybvig ([Dyb88a], [Dyb88b]) showed that the anticomonotonic property is a sufficient condition for cost-efficiency. Two random variables and on a probability space are considered comonotone if there exists with such that for any . and are anticomonotone if and are comonotone. Thus, in the pursuit of finding the random variable that achieves the optimal consumption, we aim for it to be anticomonotonic with the price kernel. This involves assigning the largest consumption outcome to the state with the cheapest price, the second largest consumption outcome to the state with the second cheapest price, and so on.

We preserve the spirit of the distribution builder but in a multiperiod model. A naive approach to propose an extension of the cost-efficient consumption in an intertemporary way for periods is letting the investor specify a desired distribution of every consumption period and iterate the terminal market approach, arranging every distribution to be antimonotonic with the price kernel :

But this is economically not sensible as this approach does not capture comonotonicity between consumption flows.

We introduce a method that is both sophisticated and uncomplicated for introducing a connection between variables using copulas. Copulas are mathematical functions that describe the relationships between multiple variables, featuring uniform distributions on the range [0, 1]. They are particularly useful for indicating interdependencies between random variables. This approach streamlines the agent’s choices by breaking them down into two main components: the selection of individual distributions and the adoption of a copula to express their interrelation.

The exploration of cost-efficient consumption remains a current and evolving subject, with recent research including [JZ08], where the authors described the optimal portfolio choice of an investor optimizing a Cumulative Prospect Theory objective function in a complete discrete market with a equiprobable probability space, [BBV14], a work that provides an explicit representation of the lowest cost strategy to achieve a given payoff distribution in the Black-Scholes market, and [BS22], where the authors extend the problem to incomplete markets. They found that the main results from the theory of complete markets still hold in adapted form, and reveals that the optimal portfolio selection for preferences characterized by law-invariance and non-decreasing tendencies toward diversification must be perfect cost-efficient.

This, paper is organized as follows. In Section 2, we establish the existence of cost-efficiency. Specifically, we prove the existence of the portfolio that attains the minimum cost. This is achieved by considering the given consumption distributions that represent the preferences of the agent. Section 3 outlines the manner in which we establish a dependency structure between consumption flows, focusing on the application of the Clayton copula. In Section 4, we introduce an algorithm designed to determine the optimal consumption random vector. This algorithm incorporates a dependency structure through the utilization of copulas. It consists of three essential steps: simulating the state-price process, generating values for the consumption distribution, and ultimately computing the solution. We would like to express our gratitude to Carole Bernard of Grenoble Ecole de Management for her ideas to develop this algorithm. Section 5 provides concrete examples that demonstrate the application of the strategy under both the Black-Scholes model and the Constant Elasticity of Variance (CEV) model. We employ Clayton copulas in both cases. In the context of the CEV model, computing the state price process is not a straightforward task. As a solution, we derive its moment generation function using the Laplace transform and subsequently estimate it through simulations of the stock price. This approach capitalizes on the equivalence of the CEV model to a square root diffusion.

2. Existence of the Cost-efficient Consumption

In pursuit of the objective to determine a cost-efficient consumption aligned with the agent’s preferences, we consider the sum of random variables that represent the consumption at each time instance. As previously mentioned, the distribution of this sum has to be anticomonotonic with the distribution of the state price process. In this section, we provide a proof to establish that the set of random variables which meets the agent preferences is not empty. Particularly, the following theorem proves that given the consumption distributions, it is possible to find a random vector that satisfies these distributions.

Theorem 2.1.

Let be a random vector on the atomless standard probability space with joint cumulative distribution function . The marginal distributions of the vector and represent the agent preferences. We define . Let be a random variable defined on that has the same distribution as . Then, there exists a random vector , which represents the agent consumption at time respectively, with joint cumulative distribution function , such that and is distributed as for . It is in general not unique.

Proof.

For the case , consider the joint distribution function of the given random variables including the sum, i.e.,

Then the goal is to construct a vector with distribution which satisfies . This can be done by combining a one-dimensional distribution transform with a multidimensional quantile transform (see [Rüs09]). Specifically, define as the distributional transform of , i.e., by setting

for some independent of . Then is a standard uniform random variable, and for the generalized inverse (quantile function) of we have . Note that the existence of such an independent random variable follows from the atomlessness of the probability space (cf. [FS11, Proposition A.27]).

Now consider the conditional distribution of given the sum . We have

We note that the conditional regular probabilities exist as our probability space is standard. Therefore we can define the vector by generating a standard uniform independent of and (and thus independent of ) and setting

since the third quantile function is trivial as . Thus we have to provide a construction of a random vector that has indeed the distribution by construction as well as .

We finish by noting that the construction is unique if and only if is independent of the choice of the uniforms and . This is the case only if the random variable has no atom (i.e., the c.d.f. is continuous) and and are monotone functions of the same random variable, i.e., either comonotonic or anticomonotonic.

For the case , we retake the previous procedure renaming as and as . Then we have

where has the same distribution as .

We apply the case of for the triple and results

We apply the procedure times to have

where is a standard uniform random variable independent of , . ∎

Once we have proven the existence of such a random vector, we are ready to present how we model the dependence structure and the algorithm to find an optimal random vector that leads us to a cost-efficient strategy.

3. Dependency structure

We propose a sophisticated and simple way to add a dependency structure of consumption flow via copulas, which are multivariate cumulative distribution functions with uniform marginal distributions on the interval [0,1] and are practical to describe the inter-correlation between random variables. In this work, we choose the Clayton copula due to its easiness to model it with one parameter. Clayton copulas are Archimedean copulas useful to model dependent structure as they have only one parameter in its expression

which we denote just by for short when there is no confusion.

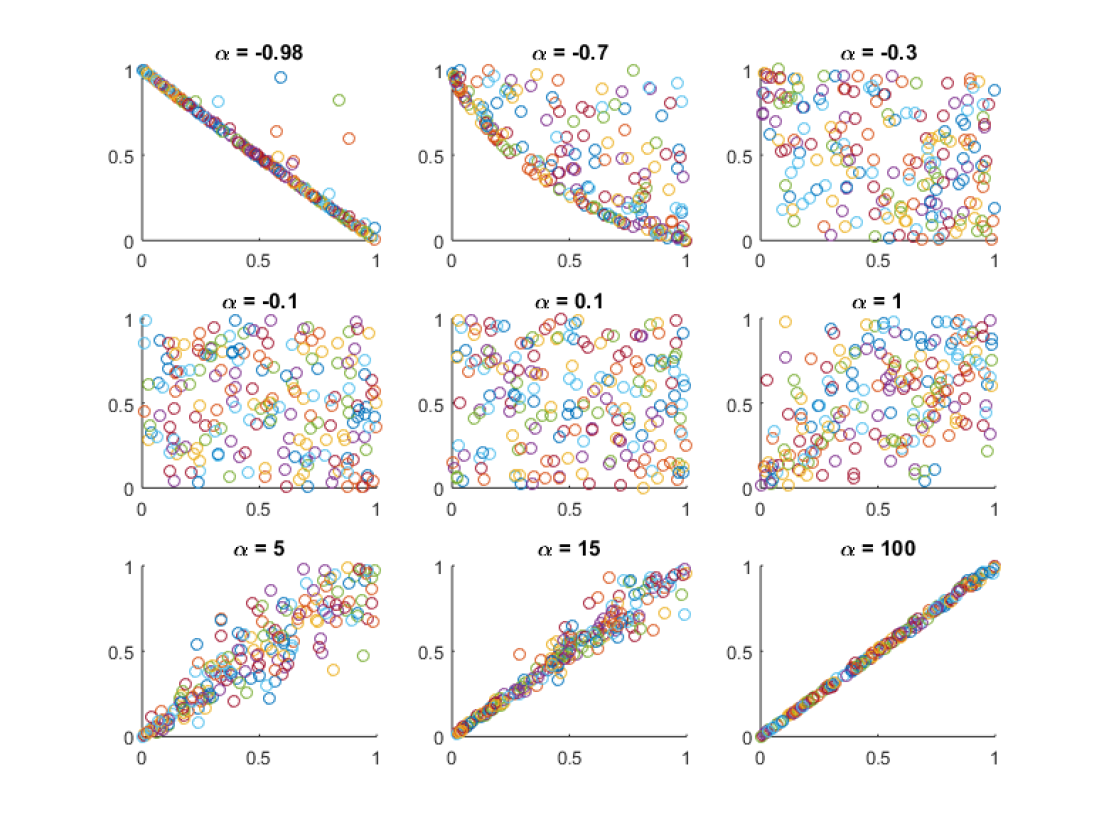

The interpretation of is easy and related to the correlation between the random variables: if is closer to , we have an anticorrelated structure; if it is close to zero, we have an independent structure; and while it grows to , we have a highly correlated structure, as we show in figure 3.1 with for random variables.

The generator function of a Clayton copula with parameter is

| (1) |

Its inverse function is

| (2) |

and its k-th derivative is

| (3) |

We use expressions (1), (2) and (3) to generate a tuple vector from a Clayton copula with parameter through the following procedure described in [WVS07].

-

1.

We generate independent random values, and denote them by .

-

2.

We set for .

- 3.

-

4.

We set , for , and .

-

5.

The desired values are , where we fixed , .

4. Optimal consumption algorithm

We present an algorithm to find the optimal consumption process. To do this, we consider a grid of states of the market at each time-tick , denoting the state space as .

We assume that the financial market is free of arbitrage and that there exists a price kernel at each time , such that is priced as , where is the risk neutral measure. Without loss of generality, we can consider , .

The process of optimal consumption until horizon time-tick satisfies the following equation:

| (4) |

where for fixed desired distributions . We represent with the copula that describes the relation between the random variables .

We describe the algorithm in three steps:

-

(1)

Simulate the state-price process:

We generate simulated values of the state-price process , , at time .

-

(2)

Simulate the values of the consumption distribution:

We generate simulated values of correlated vectors of the chosen copula.

From these vectors, we compute , which are correlated vectors with distributions respectively, and set .

Then we have the following arrangement

(5) -

(3)

Solution:

We construct from the elements of ordered to be antimonotonic with the state price vector. It means that we arrange the observations increasingly to be antimonotonic with the last column.

(6) Let be the permutation function such that for every , for some in . Therefore, the vector , , that improves the original one is

(7) The variables have the same joint distribution and a lower or equal cost with respect to the original ones, and we achieve

(8)

5. Examples of implementation

We show an implementation of the intertemporal optimal consumption. Our first example is under the Black-Scholes model, where we can explicitly compute the state price process. The second one is under the Constant Elasticity of Variance (CEV) model, where we obtain the distribution of the price kernel via the inverse Laplace transform and reproduce its values through a simulation. In both examples, the number of periods is .

For both models, we assume the investor chooses a consumption lognormal distribution with parameters and (which are kept the same for every period for ease of computation). We model the dependency between them using a Clayton copula.

5.1. Black-Scholes model

Under the Black-Scholes model, the dynamics of are

| (9) |

where , is a Brownian motion on a probability space , where is the natural filtration for this Brownian motion.

Therefore, the dynamics of the discounted price process are

| (10) |

To find the state price process or price kernel under the Black-Scholes model, we require to find the risk-neutral measure in virtue of Girsanov theorem, such that the discounted price process is a -martingale.

We let , be an -adapted process such that is a martingale with dynamics where

To find explicitly, we rewrite the dynamics of as

set , and find that , where , the Sharpe ratio of the stock.

Note that satisfies the Novikov’s condition since it is constant, and therefore, the stochastic exponential

is a martingale under the probability measure , given by

and the process , is a -Brownian motion.

In consequence, the measures and are related by the Radon-Nikodym derivative

| (11) |

and we have that the state price process under the Black-Scholes model is

| (12) |

We rewrite the state price process at time in terms of

| (13) |

where

Under the Black-Scholes model, the unique state-price process at time , is given in (13). Assuming that the stock expected return is bigger than the risk-free rate, i.e., , we see from the previous expression that is anticomonotonic with since is equal to , where is a positive constant, and we use as a grid of the state space.

Having obtained the expression for the price kernel, we proceed with the first step of the algorithm outlined in Section 4—that is, simulating the state-price process. Subsequently, we move on to step two, where we simulate the values of the consumption distribution while incorporating a dependency structure defined by a copula. Finally, in step three, we compute the cost of the strategy.

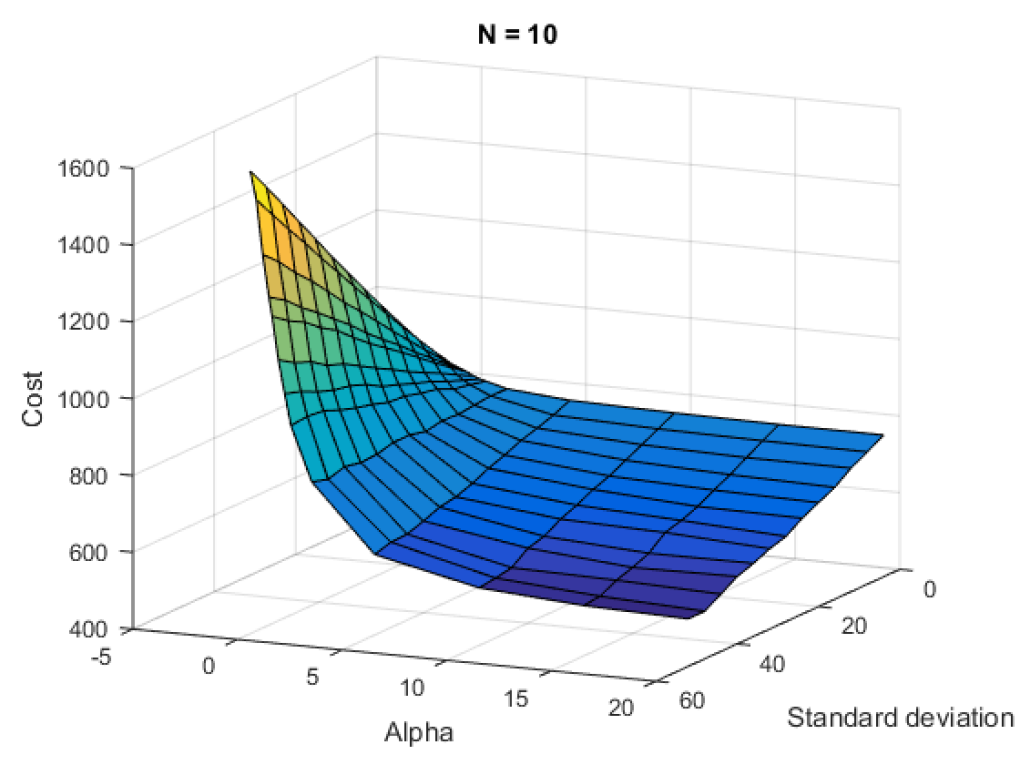

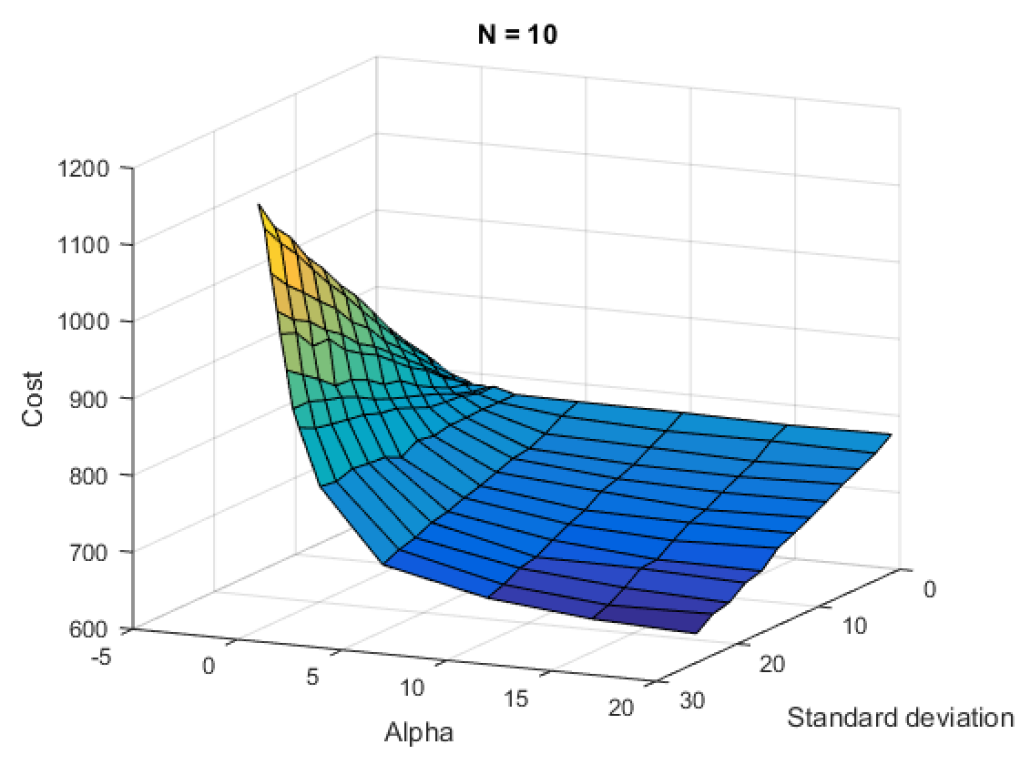

We carry out these steps within a Black-Scholes model and 10 periods of consumption, employing the following market parameters: an expected rate of return of the stock (), a stock volatility (), a risk-free rate (), and we consider a lognormal distribution with parameters and a standard deviation of as our target distribution. Additionally, we employ a Clayton copula to establish the dependency structure, utilizing different values of .

We show in Figure 5.1 the resulting relationship between the strategy cost, the parameter alpha of the Clayton copula, and the standard deviation of the lognormal distribution, which is different from the parameter . We fixed the parameter .

We notice that for negative values of alpha, the standard deviation of the chosen lognormal distribution is inversely proportional to the cost, and for positive values, the relationship is proportional. Then, the best choice to get a cost-efficient consumption is a positive alpha (e.g., or ).

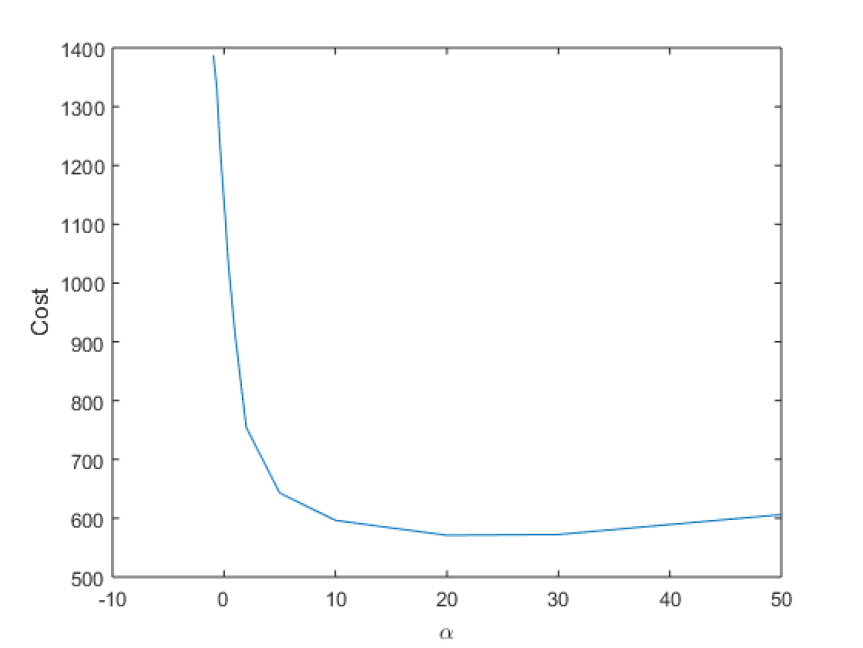

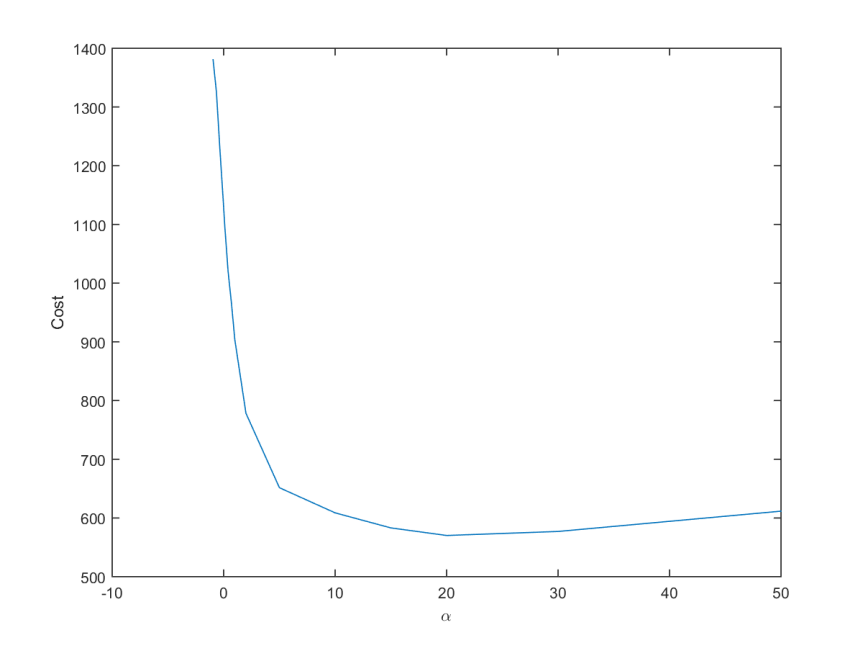

Fixing the standard deviation to , we see that the value of alpha that achieves the minimum cost is , as we show in Figure 5.2.

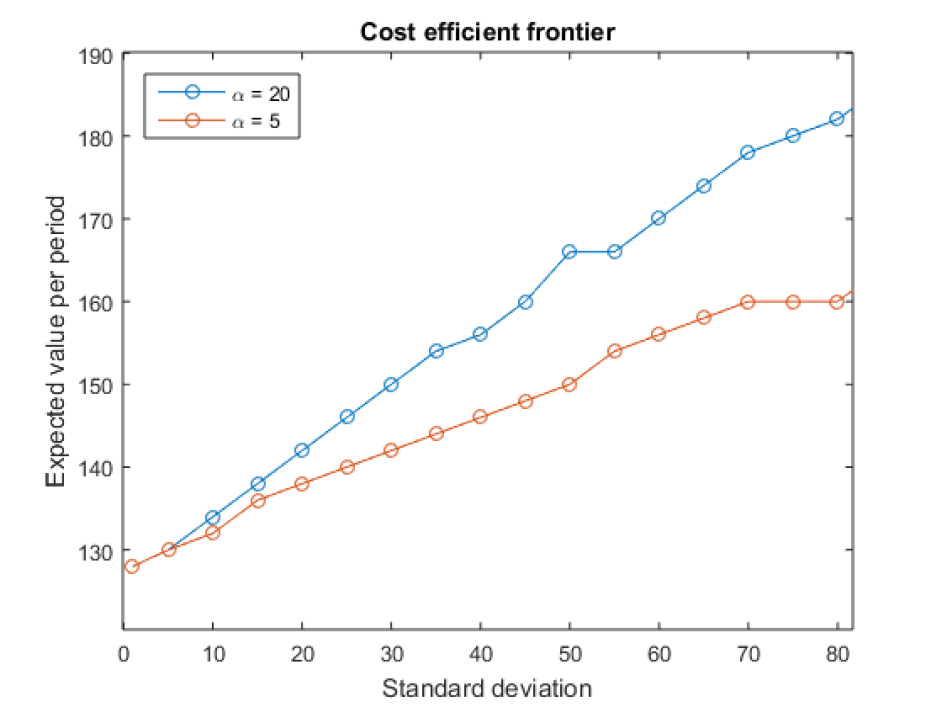

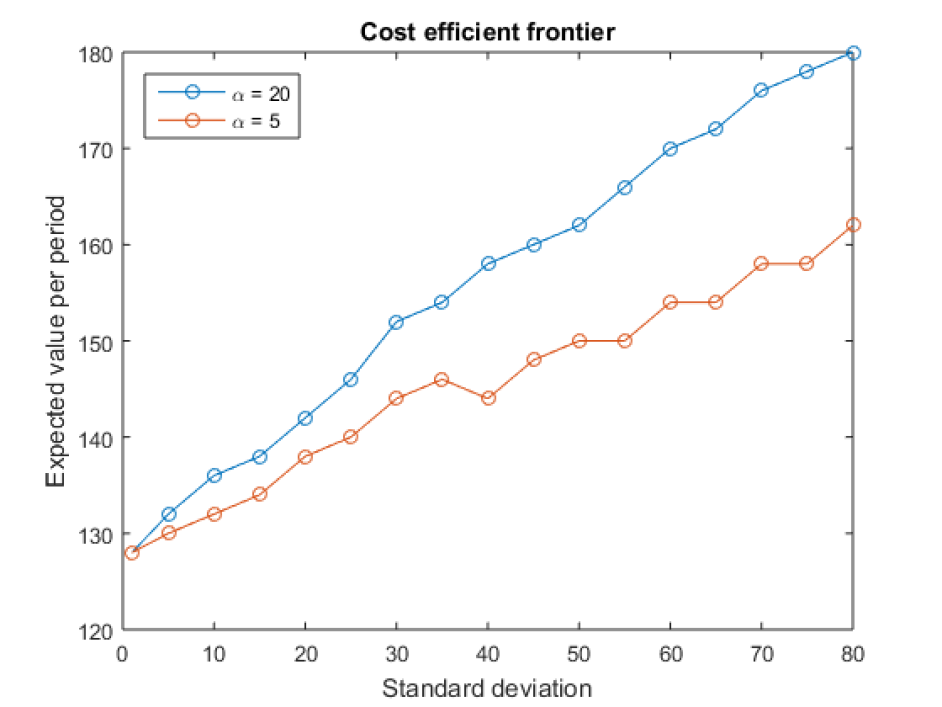

Figure 5.3 displays what we refer to as the Cost-Efficient Frontier for and . The horizontal axis represents the standard deviation, acting as the input, while the vertical axis showcases the expected value of the lognormal distribution, which is the expected consumption per period. We have set periods and a fixed budget of .

We see that we have bigger expected values for than . The curve of the second case grows less fast. For bigger values of standard deviation, both curves show the classical concave shape of risk aversion behavior.

The cost-efficient frontier tells us that given the market conditions described above, if we assume a risk of for example, we can expect to win an average of over periods with a budget of using a consumption correlation structure given by .

Hedging strategy

Within this section, we construct the hedging strategy to replicate the cost-efficient consumption process in a Black-Scholes market.

On the basis of the fact that is anticomonotonic with and that it is the cheapest way to achieve the distribution , we have that

| (14) |

Under the Black-Scholes model, the state price process is anticomonotonic with when , or equivalently, . Assuming this, we have

| (15) |

To find the hedging strategy for consisting on holding units of the stock and units of the bond, we let denote the value of at time under the measure , i.e.,

where is the standard bond process, and we assume that is Malliavin differentiable and admits the Clark-Ocone representation formula:

| (16) |

where . We use the following expression of under

and substitute it in (16) to find that

| (17) |

Equation (17) is the integral form of the SDE

| (18) |

where represents the units of the stock we need to hold. The units of the bond we need are given by

and the value of the position at time , is .

Lognormal example

To illustrate the application of these results with closed-form expressions, we show an example when is a lognormal distribution with parameters and . Then , where is the c.d.f. of the standard normal distribution.

In this case, we find that

where . Hence, we obtain,

where and .

Since , then , and finally, we have that the hedging positions are

| (19) |

5.2. CEV model

We consider the case follows a Constant Elasticity of Variance (CEV) process, with dynamics

where . Then the discounted price process has the following dynamics

Observe that if and , the CEV model reduces to the Black-Sholes model and the Bachelier model, respectively.

According to [MU12], we can use the density process

| (20) |

to change the measure to the risk neutral measure . Then is a martingale under . In particular, is a CEV process that satisfies the driftless equation . Moreover, if , is a uniformly integrable martingale, and if , is a martingale that is not uniformly integrable (see [MU12]).

To find the distribution of , we take the logarithmic version of and write

where , and consider the moment generating function of

We define the measure such that

Observe that . Under this measure, the stochastic exponential

is a martingale for in virtue of the theorem 4.1 in [KL14]. Here, the authors develop an extension of Beneš method.

Under , the discounted price process has the dynamics

and quadratic variation

Subsequently, we can rewrite

| (21) |

where is the quadratic variation of , where is a CEV process with parameter and any drift. Let us take, for convenience, with no drift.

We let be the instantaneous variance rate of , defined by . We express as a quadratic drift 3/2 process

| (22) |

where , and to apply the Theorem 3 of [CS07] to (21), and find that the Laplace transform of is given by

| (23) |

where

and denotes the Pochhammer’s symbol: .

Our objective is to calculate the cumulative distribution function of the state price process to facilitate the consumption optimization process. To achieve this, one can either compute the inverse Laplace transform of the aforementioned expression or opt for Monte Carlo simulations of the paths of . We have chosen to work with the latter approach due to its ease of programming.

We set with and apply Itô’s formula to find that satisfies the SDE of the following square-root diffusion

| (24) |

where , and .

We simulate for using the following algorithm presented in [Gla03] which simulates the square root diffusion on time grid :

Finally, we invert the transformation from to to obtain . Utilizing the expression (20), we compute , and subsequently, we implement the algorithm described in Section 4 with a dependence structure defined by a Clayton copula.

We present an example using the market parameters , , with periods cf consumption. We fixed the parameter . In Figure 5.4, we depict the resulting relationship between the strategy cost, the parameter alpha of the Clayton copula, and the standard deviation of the lognormal distribution, which is different from the parameter .

It is noteworthy that for negative values of alpha, the standard deviation of the chosen lognormal distribution is inversely proportional to the cost, whereas for positive values, the relationship is proportional, as in the Black-Scholes model. When comparing it with the Black-Scholes model, we observe that under the CEV model with , the range of the cost is smaller, but the overall shape of the plot remains the same.

We choose a standard deviation equal to as in Black-Scholes model to see that the value of alpha that achieves the minimum cost is , as we see in Figure 5.5.

In Figure 5.6, we show the Cost-efficient frontier for and under the CEV model. We plot the standard deviation as an input and the expected value of the lognormal distribution as an output, which is the expected consumption per period. We have set periods and a fixed budget of 1000.

We observe that the expected value is higher for compared to . This is related with the fact that the curve in the second case exhibits a slower growth rate.

What the cost-efficient frontier tells us is that, for example, if we assume a risk of , we can expect to win an average of over periods with a budget of using a consumption correlation structure given by .

6. Conclusions

In this paper, we have explored intertemporal cost-efficient consumption, which represents an extension of the Distribution Builder approach to portfolio selection. We have addressed the problem of achieving desired consumption distributions while minimizing costs across multiple time periods.

The incorporation of a dependency structures using copulas is central to our method, these provide an elegant means of representing relationships between multiple variables. In our work, we opt for the Clayton copula due to its simplicity and ability to be modeled with a single parameter.

We have developed an algorithm designed to determine the cost-efficient consumption and offer the methodology to attain the optimal strategy within the Black-Scholes market and the Constant Elasticity of Variance (CEV) market.

Our findings reveal that in both markets, positive correlated consumption random variables lead to cost-efficient strategies. We have also introduced a cost-efficient frontier for both cases, offering the expected return of each period according to the risk the agent is willing to face.

Acknowledgements

This project has received funding from the European Union’s Horizon

2020 research and innovation programme under the Marie

Skłodowska-Curie grant agreement No. 777822.

References

- [BBV14] Carole Bernard, Phelim P. Boyle, and Steven Vanduffel. Explicit representation of cost-efficient strategies. Finance, 35(2):5–55, 2014.

- [BS22] Carole Bernard and Stephan Sturm. Cost-efficiency in incomplete markets. Social Science Research Network, 2022.

- [CS07] Peter Carr and Jian Sun. A new approach for option pricing under stochastic volatility. Review of Derivatives Research, 10(2):87–150, 2007.

- [Dyb88a] Phil Dybvig. Distributional analysis of portfolio choice. Journal of Business, 61(3):369–393, 1988.

- [Dyb88b] Phil Dybvig. Inefficient dynamic portfolio strategies or how to throw away a million dollars in the stock market. Review of Financial Studies, 1(1):67–88, 1988.

- [FS11] Hans Föllmer and Alexander Schied. Stochastic finance. Walter de Gruyter & Co., Berlin, extended edition, 2011. An introduction in discrete time.

- [GJS08] Daniel G. Goldstein, Eric J. Johnson, and William F. Sharpe. Choosing outcomes versus choosing products: Consumer-focused retirement investment advice. Journal of Consumer Research, 35(3):440–456, 2008.

- [Gla03] Paul Glasserman. Monte Carlo methods in financial engineering, volume 53. Springer, 2003.

- [GR01] Christian Genest and Louis-Paul Rivest. On the multivariate probability integral transformation. Statistics & probability letters, 53(4):391–399, 2001.

- [JZ08] Hanqing Jin and Xun Yu Zhou. Behavioral Portfolio Selection in Continous Time. Mathematical Finance, 18(3):385–426, 2008.

- [KL14] Fima Klebaner and Robert Liptser. When a stochastic exponential is a true martingale. extension of the benes method. Theory of Probability & Its Applications, 58(1):38–62, 2014.

- [MU12] Aleksandar Mijatović and Mikhail Urusov. On the martingale property of certain local martingales. Probability Theory and Related Fields, 152(1-2):1–30, 2012.

- [Rüs09] Ludger Rüschendorf. On the distributional transform, Sklar’s theorem, and the empirical copula process. J. Statist. Plann. Inference, 139(11):3921–3927, 2009.

- [Sha06] William F Sharpe. Investors and Markets: Portfolio Choices, Asset Prices, and Investment Advice. Princeton University Press, 2006.

- [Tve75] Amos Tversky. A critique of expected utility theory: Descriptive and normative considerations. Erkenntnis, pages 163–173, 1975.

- [WVS07] Florence Wu, Emiliano Valdez, and Michael Sherris. Simulating from exchangeable archimedean copulas. Communications in Statistics, Simulation and Computation, 36(5):1019–1034, 2007.