Rachel \surCarrington*

Post-selection inference for quantifying uncertainty in changes in variance

Abstract

Quantifying uncertainty in detected changepoints is an important problem. However it is challenging as the naive approach would use the data twice, first to detect the changes, and then to test them. This will bias the test, and can lead to anti-conservative -values. One approach to avoid this is to use ideas from post-selection inference, which conditions on the information in the data used to choose which changes to test. As a result this produces valid -values; that is, -values that have a uniform distribution if there is no change. Currently such methods have been developed for detecting changes in mean only. This paper presents two approaches for constructing post-selection -values for detecting changes in variance. These vary depending on the method use to detect the changes, but are general in terms of being applicable for a range of change-detection methods and a range of hypotheses that we may wish to test.

keywords:

Changepoint detection; Breakpoint; Binary segmentation; Post-selection -value1 Introduction

The problem of detecting changes in time series has received a great deal of attention in recent years, with applications in finance [33], quality control [2], climate modelling [31, 32], genome sequencing [26, 5], neuroscience [1], and epidemic modelling [21], amongst many others. Various methods have been developed for detecting different types of change, for example changes in mean, variance, and slope. These are often developed based on developing a test for a single change of a specific type. To detect multiple changes, this test can be used recursively within algorithms such as binary segmentation [35] and its variants such as wild binary segmentation [14], seeded binary segmentation [22], and narrowest over threshold [3]. Alternatively one can write down a likelihood for the data as a function of the number and location of changes and aim to estimate the changes by minimising a penalised version of this likelihood – for many models this optimisation can be performed exactly, see [23, 28]. See [13] and [34] for recent reviews of changepoint methods.

Recently, increasing attention has been given to the problem of estimating the uncertainty associated with detected changepoints [12, 25, 7]. This is challenging due to the interplay of different elements of uncertainty, in terms of the number and location of the changepoints. Bayesian approaches [4, 11, 30, 8] give a natural way of quantifying this uncertainty, but require specifying prior information with the results sensitive to these choices. Alternatively one can use the properties of test statistics under the assumption of no changepoints. For example, [15] and [16] use a probabilistic bound on the maximum of the test statistic for the presence of a change over all possible intervals of data to find the narrowest set of intervals which each must contain at least one changepoint with a certain probability. Similar bounds are used within the MOSUM method [29] to produce asymptotic -values for detected changepoints [10].

In this paper we consider a related approach, of post-selection inference [24]. The idea is to construct a -value for each detected changepoint, with the these -values being valid in finite samples, albeit under strong distributional assumptions for the data. This is a challenging problem in general as, if we were to use the data to estimate changepoint locations, naively re-using the same data to estimate the uncertainty associated with each changepoint will lead to biased results. The idea of post-selection inference is, when testing for the presence of a changepoint at some detected location , we condition on the information in the data that led to detection at when calculating the -value. To date, almost all work in this area has focused on the univariate change in mean case, e.g. [18, 20, 9, 6], or the piecewise constant polynomial model [27]. As far as we know, there are no current approaches for quantifying the evidence for detected changes in variance. In this paper we fill this gap by extending the post-selection inference ideas to cover the change in variance setting.

The post-selection inference methods for the change in mean problem use the fact that the natural test statistic for a change at a given location will have a standard normal distribution under the null. To account for the fact that we have used the same data to detect changes and thus to decide which locations to test, we need to condition this distribution on the fact that the tested location is a detected changepoint. This leads to a conditional null distribution that is constrained to lie on an interval [18] or a union of intervals [20] of the real line – depending on precisely what information is conditioned on. Importantly it is straightforward to calculate this interval or intervals for methods for detecting a change in mean that use the popular CUSUM statistic within a binary segmentation algorithm or within a penalised likelihood approach. One of the advantages of this approach is that it is general: it applies to a wide range of methods for detecting changes, and also to most natural null hypotheses that one may wish to test.

In this paper, we consider the two most common ways of detecting a change in variance. The first uses the idea that a change in variance in some time series, say, will correspond to a change in mean in . Thus we can shift the data so it has mean zero, and apply a method for detecting a change in mean to the square of this shifted data. The second method is where we estimate changepoint locations by directly maximizing the likelihood of the piecewise constant variance model. In both cases we then use the same test statistic for testing whether a detected change is real. This test statistic is equivalent to the likelihood-ratio test statistic for a change in variance in Gaussian data, and is the proportion of the sum of squares of the data in the region prior to the putative change. If we had used separate information, or independent data, to choose which putative change location to test then the null distribution of this test statistic a Beta distribution with known parameters. For our setting we need to calculate the null distribution conditional on detecting the change, which leads to constraining the Beta distribution to a union of intervals of .

To calculate the post-selection -values requires us to calculate these intervals. For the first approach to detecting changes, this can be done analytically using the same ideas as for the change in mean setting. For the second approach, this is no longer possible so we show how Monte Carlo can be used to approximate the -values [see 36, for similar use of Monte Carlo in post-selection inference].

The rest of the paper is organized as follows. In Section 2 we define the model and set up the test we will use to detect changes in variance. Section 3 then describes the methods we will use to calculate -values. Section 4 details some extensions to different scenarios, such as different null hypotheses and changepoint detection methods. Section 5 presents results of our methods on simulated data, and in Section 6 we implement our method on a financial data set. Section 7 then concludes with some discussion of our results and suggestions for further research.

2 Testing for a change in variance

We consider the univariate Gaussian model with fixed mean and piecewise constant variance:

| (1) |

where is assumed known, , and except at changepoints .

Given the model in (1), suppose that we have a dataset and we have obtained a set of estimated changepoint locations , such that . For a particular changepoint , we want to test whether there is indeed a changepoint at, or close to, .

First, we need to define our null hypothesis and choose a test statistic. Since we are generally interested in whether there is a change close to , rather than exactly at , it makes sense to set the null hypothesis to be that there is no changepoint within a certain window of . There are various ways of choosing such a window, which will generally be informed by our particular application: for example, we can use a fixed window length, or allow the window to be determined by the locations of neighbouring changepoint estimates. For now we will assume that we have some fixed such that the window is , but note that the methods we describe are easily extended to other choices of ; we will discuss this in more detail in Section 4.1.

Hence, we have

| (2) |

with being that there is at least one inequality.

Let . A natural choice of test statistic is to consider what proportion of the total sum of squares within the region is accounted for by the data before the changepoint, i.e.

Under , , with . Under , we would expect to be closer to if the variance increases after , and closer to if is followed by a decrease in variance.

Our test statistic, , is equivalent to the F statistic, , a standard test statistic used to test for a change in variance, in the sense that each of and can be derived from the other ( and ). Hence using either will lead to the same result. The formulation we define above is more convenient, as it allows us to write as a linear function of (see below), which will simplify the calculations in the next section.

Let denote the observed value of . If corresponds to an increase in variance, the one-sided -value is ; if corresponds to a decrease in variance, then . To calculate the two-sided -value, we need to first calculate such that

Then, we let and , and the two-sided -value is

| (3) |

We will assume for the remainder of this paper that we are using the two-sided -value, i.e., we are not concerned about the direction of the change. However, our methods apply equally to the one-sided -value case.

2.1 Post-selection inference

The -value in (3) is valid if we use separate information, or independent data, to calculate the -value from that which we use to choose the location to test. However, if we use the same data to calculate the -value as we have used to estimate changepoint locations, this introduces bias into the -value. In order to get valid -values in this case, we need to calculate the probability of (3) and conditional on the information used to choose to test for a change at : here, this is the fact that is in the set of estimated changepoints. Letting denote the set of estimated changepoints which we obtain when we apply a particular changepoint algorithm to , we therefore want to calculate the -value in (3) conditional on the fact that :

Our null hypothesis (2) is that the variance is constant inside the region . This does not specify the value that takes for any outside this window, nor the value of the fixed variance within the window. Therefore, in order for the test to be well-defined, we must condition on sufficient statistics for these parameters: the values of outside of , and the sum of squares within the window: .

For now, we will also condition on the parameters within the window which are orthogonal to , following the approach of [20] for the change in mean case. This makes the -values more straightforward to compute, whilst still resulting in a valid test (i.e. uniform -values under ), although it may result in some loss of power [17, 20]. Later on, in Section 5.3, we consider relaxing this condition.

To make explicit the dependence of on , we consider a re-parameterization of . Let , the sum of the square of the data in the region being tested, and let

The following results shows how we can write the square of in terms of , , and and for , and that the latter set of variables are independent under the null hypothesis.

Lemma 1

We can write each , for , in terms of , , , and . More specifically, for , we can write

| (4) |

where for convenience we set .

Lemma 2

Under , are all independent.

Therefore, conditioning on the dimensions of the data which are orthogonal to is equivalent to conditioning on the values of , , and . We can see from (4) above that doing this while allowing only to change has the effect of multiplying by and multiplying by . (This transformation is illustrated in Figure 1.) Hence, let

| (5) |

We consider only the subset of possible data sets . Letting denote the set , the post-selection -value we want to calculate is

| (6) |

Since we know that, under , , the conditional distribution of is truncated to . Hence, calculating depends on calculating . Calculation of depends on the method used to estimate changepoints. In the following sections we describe how to do this for two classes of methods: in Section 3.1, we cover approaches based on finding changes in mean in using cumulative sums of squares, whilst in Section 3.2 we develop a more general approach, focusing on changepoint detection methods which attempt to maximize the likelihood ratio statistic.

3 Methods

3.1 CUSUM for change in variance

As a reminder, our model is

where , and we assume that is known. Suppose, without loss of generality, that (if this is not the case, we can just replace with ). Then a change in variance in will correspond to a change in mean in . Therefore, one approach to detecting a change in variance in is to look for a change in mean in , for example by maximizing the cumulative sum (CUSUM) statistic, which is defined on a interval as

Figure 2 illustrates this process for a single changepoint. We will focus on using the CUSUM statistic with binary segmentation [35]; our approach to calculating -values will also extend to variants of this such as wild binary segmentation, as well as to the iterated cumulative sums of squares method of [19], which uses a different statistic based on the cumulative sums of squares.

To detect whether there is a change in mean in an interval , where , we take

and determine that there is a changepoint at if is greater than some threshold. To detect multiple changepoints using binary segmentation, we start by maximizing across the whole dataset; we then split the data at and search for changepoints using calculated on each segment. This process is repeated until no more changepoints are detected.

Using this approach to detecting changes in variance is not always optimal, as the CUSUM statistic is derived under the assumption that the data follows a normal distribution with constant variance, which is not the case for our : when the variance of changes, the variance of will also change. This leads to a higher false discovery rate in regions of higher variance, and a tendency to miss changepoints in less variable regions. However, it can still work well when the changes in variance are not too large. It also gives us the advantage of being able to adapt existing post-selection inference methods for the change in mean model, as we shall see in the next section.

3.1.1 Calculating the post-selection -value

To calculate the -value in (6), we must compute – in other words, we need to find the set of values such that our changepoint algorithm detects a changepoint at . is therefore dependent on our choice of changepoint algorithm. We will focus initially on binary segmentation; the method generalizes straightforwardly to other related algorithms.

To calculate we can borrow ideas from methods used for the change in mean model. [18] showed that by conditioning on the set of changes , the order in which the changes are found, and the direction of each change (positive or negative), we can write down a set of inequalities which must be satisfied by the CUSUM statistic. For a given segment , in order to detect a change point at we must have , where is the changepoint detection threshold, and

where is the direction of the change. For no changepoint to be detected in the interval , we must have

Hence, we can write down a set of linear inequalities in the data for each iteration of binary segmentation, which must all be satisfied for the particular set of changepoints, with the order and directions of change, to be found. For the change in mean model, the test statistic is defined as , where

As for our model, we can then introduce perturbations of the data that correspond to changes in whilst fixing the information orthogonal to :

Since is a linear function of , and is a linear function of , the CUSUM statistic in terms of is also linear in . Hence, we can write the set of inequalities in as linear inequalities in , and they will therefore hold for an interval of values, which it is straightforward to calculate. [20] shows that we can increase power by extending this idea to avoid conditioning on the order and directions of the changes, by calculating the intervals associated with each possible combination of changes which yield . This gives us the set which is the union of all such intervals.

For the change in variance model, we can use the same approach, as the inequalities we write down in terms of are the same. As a reminder, the CUSUM statistic is

so

| (7) |

Using the definition of from (5), we can write each element of this as where

Hence, letting , we can write (7) as

This is linear in , so we can once again compute each possible interval by resolving a set of linear inequalities in . We can use the method of [20] to efficiently compute (and hence ).

3.2 Likelihood-ratio based detection of changes

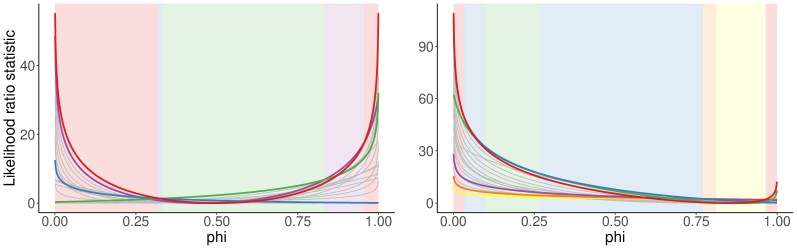

Whilst post-selection inference is relatively straightforward for the piecewise constant variance model when estimating changepoint locations using the CUSUM statistic, the use of the CUSUM statistic can lead to poor detection of changes. For example, Figure 3 shows an example of a simulated data set with 5 changepoints, where we apply binary segmentation and wild binary segmentation to detect changepoints. Both methods overestimate the number of changes in the region with highest variance, but fail to detect changes in other regions.

We can achieve more accurate changepoint detection by maximizing the likelihood ratio statistic, which on an interval is defined as

| (8) |

To estimate a single changepoint, we calculate for , and take . For multiple changepoints, we can either use an iterative method such as binary segmentation, or a penalized likelihood method such as PELT [23]. The approach we develop below will apply in both cases.

| CUSUM | LRS | |

|---|---|---|

| 0.755 | 0.915 | |

| 0.972 | 0.992 | |

| 0.012 | 0.914 |

Table 1 demonstrates how this leads to increased accuracy compared with using the CUSUM statistic. We simulated data from a model with and 3 changepoints at ; the variances on the four segments being , and for each simulated data set we used binary segmentation to estimate three changepoint locations, using both the CUSUM statistic and the likelihood ratio statistic to determine a change. The table records the proportion of runs in which a changepoint was detected within 10 of each true changepoint. We see that CUSUM does reasonably well at detecting the first two changes, but does very badly at locating the third, smaller change. Using the likelihood ratio statistic, however, all three changepoints are detected in over of cases.

3.2.1 Post-selection inference

As a reminder, the post-selection -value we want to calculate is

where . Previously, when detecting changes based on the CUSUM statistic, we were able to write down a set of linear inequalities in which defined the set . However, while we can write down inequalities in as we did for , is not a linear function of : we can show that

| (9) |

where and are constants depending on , , , and (see the Appendix for more details). In general, it is not possible to analytically solve these inequalities for as it was earlier.

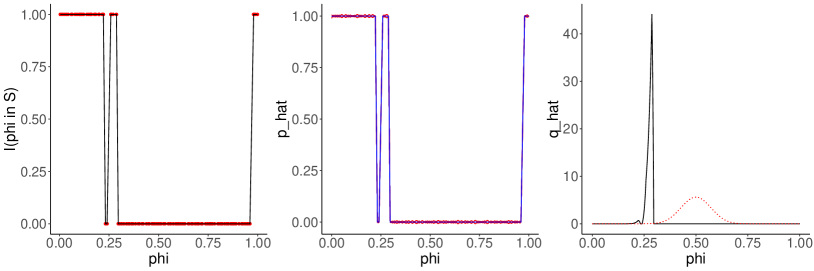

However still consists of a union of intervals as the inequalities are smooth functions of . To illustrate this, Figure 4 shows a plot of against for a simulated data set for different values of ; the red line corresponds to . The values of which are in are hence those for which the red line is higher than any of the other lines on the plot.

Although we cannot compute directly, we can find out whether a given is in by computing , as in (5), and re-running the changepoint algorithm to obtain the set of estimated changepoints . Hence, one way to approximate is by randomly sampling values and calculating whether each is in . We can then estimate by calculating what proportion of values which are in are also in the critical region :

| (10) |

However, sampling from its unconditional distribution often leads to very slow convergence of , as is typically small, so only a small proportion of samples will contribute to : the rest are discarded.

Since sampling in this way requires re-applying the changepoint algorithm for each , which may be computationally demanding (the length of time taken to apply the algorithm will scale with the number of data points and the number of detected changes), using a large number of samples to estimate the -value is undesirable. We therefore want to find ways to reduce the number of samples necessary to get a good -value estimate .

One way to reduce the variance of , without increasing the computation time, is to use stratified sampling. For , we sample . We then calculate to satisfy . (Section C.2 in the supplementary material shows how the variance of decreases using stratified, compared to random sampling.) Doing this ensures that our set of sampled values are spread evenly across the sample space, which can help to give more accurate estimates. However, it is not infrequently the case that is of the order of or smaller, in which case using stratified sampling is unlikely to significantly improve the estimate , as we will still have very few .

To overcome this we resort to using simulation to estimate the intervals that contribute to . These estimates can then be used to directly estimate the post-selection -value or to construct better proposal distributions for an importance sampling based Monte Carlo approach.

3.2.2 Estimating using Gaussian processes

If we can calculate then it is straightforward to calculate the -value. Whilst is intractable, as mentioned above, for any value of we can calculate . We can represent our beliefs about as a function of , through a probability distribution that gives a probability to for each . We can then model this function as a Gaussian process (GP) (see e.g. [37]). This means that we treat as a random function such that for any set of values, , follows a multivariate Gaussian distribution. We can then take as our estimate, , the mean of the Gaussian process. Given an observation or , the GP will force to take the value either 0 or 1. In between, the mean of the Gaussian process will smooth the function values between these observations.

To implement this, we first need to choose a kernel function, , which specifies the covariance between each pair of values. It is natural to choose an exponential kernel , as this is Markov. (This requires us to choose the value of : we investigate this in Section C.3 of the supplementary material, where we find that at long as is at least 1, the value we use does not have a noticeable effect on the results.) If we have evaluated at , and the Markov property means that our Gaussian approximation to will only depend on the values of and . Furthermore, for such a kernel the mean of the Gaussian process will be an average of these values and the prior mean – and thus will always lie within .

We first choose a stratified sample from , , and calculate for each . As before, we have to re-apply the changepoint algorithm to calculate each .

We calculate the estimate of at discrete locations , as

The most expensive step here computationally is calculating the inverse of , which is an matrix. However the Markov property of our kernel means that this scales linearly with .

From the output of the Gaussian process, we can estimate the distribution of given by

which is easy to evaluate numerically.

To estimate the -value, we have two options. The -value is

| (11) |

Since is an estimate of the density of , we can use this directly to estimate the -value, i.e.

Alternatively, we can use importance sampling with as the proposal distribution. This means that we sample ; then, denoting the true distribution of by , the -value estimate is

| (12) |

Since we have already calculated for the in our original sample (that we used to fit the Gaussian process), we can also include these points in our importance sampling estimator.

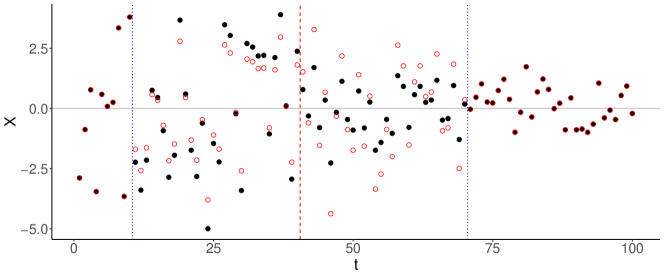

Figure 5 shows an outline of this process. First, we sample — we here sample from to ensure that we get good coverage of the range of values. For each , we calculate and apply the changepoint algorithm to evaluate . Panel (a) shows a plot of for our samples. Then we fit a Gaussian process: panel (b) shows the posterior mean . We then estimate as described above: this is shown by the black line in panel (c), with the dotted red line showing for comparison.

4 Extensions

In this section we discuss several extensions to the methods we have discussed so far: we consider (i) applying our method to different null hypotheses; (ii) different changepoint detection methods; (iii) reducing the amount of information we condition on using the method of [6].

4.1 Different null hypotheses

As mentioned in Section 2, we generally want to choose a null hypothesis that there are no changes close to the detected changepoint . A common way to do this is to use the approach we have used so far, to define to be the statement that there is no change within a fixed window . However, there are modifications or alternatives to this which could be used. For example, we could decide to truncate the region if we find another changepoint (other than ) within the region. Alternatively, if we denote our changepoint of interest , we can take the null hypothesis that there is no changepoint within (by convention setting and , where is the number of changepoints). (This approach is considered for the change in mean case, for example, in [20] and [6].)

In general, the methods we have described above will work in the same way for these different alternatives. However, in the case where the region of interest is determined by the locations of other estimated changepoints, it is necessary to redefine the conditioning set to take account of this. If the window is determined by the locations of neighbouring changepoints, then we also need to condition on the fact that these changepoint locations are included in the set of changepoints . This can be done, for example, by conditioning on the set of all estimated changepoints — i.e. — rather than just on the fact that . To do this, for the CUSUM method we construct the set of intervals in the same way, but only choose the ones for which this new condition holds to be in . For the more general case, it is straightforward to implement this.

4.2 Different changepoint detection methods

We have focused on two approaches to post-selection inference for the change in variance model. The CUSUM approach (Section 3.1) depends on being able to write down a set of linear inequalities in which can be resolved to obtain the set . We have focused on doing this for binary segmentation, as this is the most straightforward case; however, it is easy to show that we can do the same for variants such as wild binary segmentation, which also involve maximizing on a series of intervals. In this case, we condition also on the set of random intervals; provided we do this, we can construct linear inequalities in and calculate in the same way.

For our second, more general, approach (Section 3.2), we can use any method for changepoint estimation, since we just re-apply the algorithm for each sampled . This approach can also be used for the CUSUM case if we use a changepoint algorithm for which we cannot determine explicitly.

For some methods it is not necessary to re-run the algorithm from scratch each time. For example, to implement methods such as wild binary segmentation and narrowest over threshold we have to calculate the likelihood ratio statistic on a set of intervals . The set of intervals is the same each time we implement the algorithm on . Since is constant on intervals which do not overlap with the region of interest (i.e., or ), for these intervals we only have to calculate once. Therefore, at each sampling iteration we only have to re-calculate on intervals which overlap with the region of interest. This can help to speed up the process of estimating .

4.3 Increasing power by conditioning on less information

So far, we have calculated -values by conditioning on all aspects of the data except for the test statistic . However, whilst it is necessary to condition on sufficient statistics for the parameters which are not specified under , it is possible to define a -value which is not conditional on , i.e.

where here both and and allowed to vary.

This adds complication in calculating the conditional distribution of as the ’s are nuisance parameters: although, unconditionally, and are independent, when the distribution of is calculated truncated to the region of interest this is not the case, as the truncation region also depends on . Conditioning on the observed value of is one way of dealing with this. An alternative approach, as in [6] for the change in mean model, is to sample values of , calculate the truncation region for each, and then to calculate the -value as a weighted average of these individual -values, i.e.

Under , . As long as we include the observed value of as one of the samples, the -value estimates we obtain will be valid, in the sense that they will follow a uniform distribution under . We investigate applying this method on simulated data in Section 5.3.

5 Simulations

In this section we implement our methods on simulated data. All simulation results are based on 1000 replicates.

5.1 Detecting changes using CUSUM

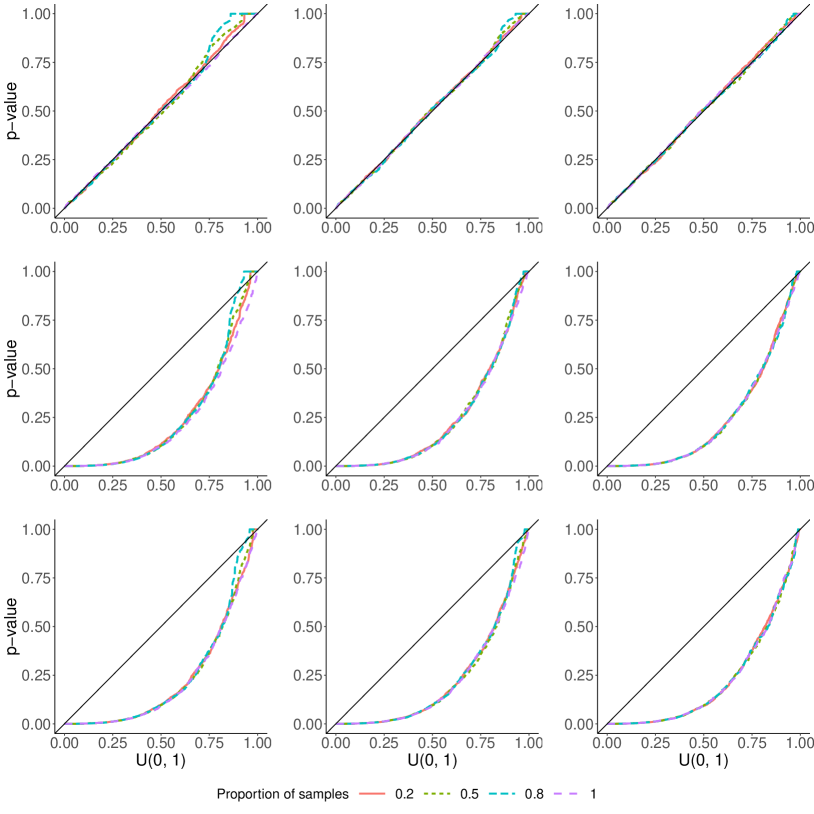

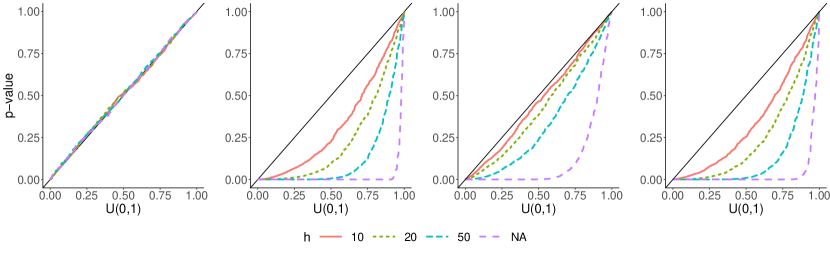

Figure 6 shows QQ plots of -values obtained by sampling from a model with . In (a) we sample from ; in (b)–(d) we sample from a model with a single change at , where in each case the variance before the changepoint is 1, and the variance after the changepoint is 0.5, 2, 4. We see that under , , and under the test has power to detect changes, which increases with the window size and the size of the change.

Figure 7 shows similar results where we simulate from a model with 4 changes, with . In panels (a) and (b) we simulated from a model with 4 equally spaced changes, . In (c) and (d), changepoints were chosen from a uniform distribution, with the constraint that the minimum distance between changepoints was . In each case we calculated the -value associated with the first changepoint.

5.2 Detecting changes using the likelihood-ratio test

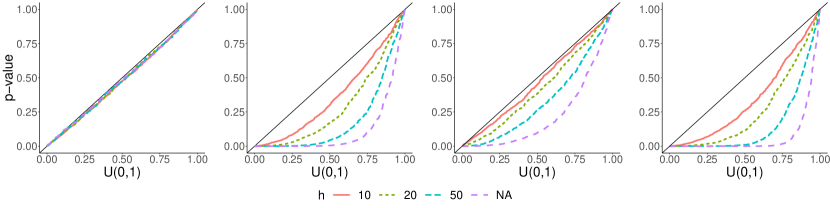

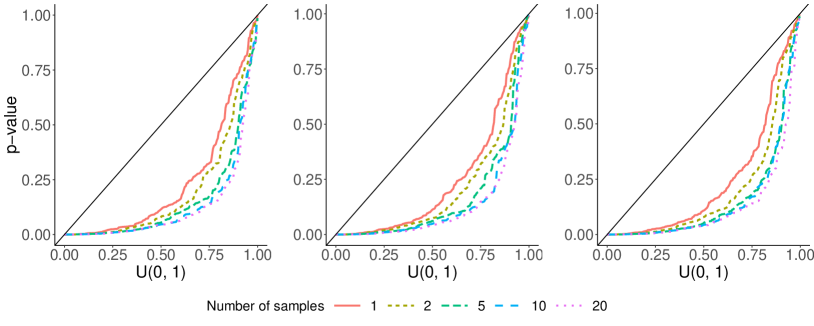

In Section 3.2.2, we discussed how we can estimate the -value using a Gaussian process. To implement this we must decide on the number of random samples , and also to decide whether we will estimate directly from the posterior of the Gaussian process, as in (11), or use importance sampling from the posterior distribution to estimate , as in (12). We here investigate difference choices of this for several different simulated scenarios. In particular, we are interested in knowing what happens when the number of samples is relatively small.

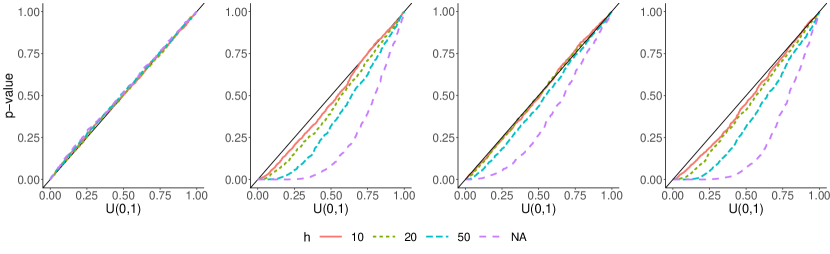

Figures 8 and 9 show QQ plots of estimated -values we obtain on simulated data for three different scenarios: (1) no change; (2) three changes at fixed equidistant locations, ; (3) three changes at random locations, sampled uniformly from and constrained to be at least apart. In each case we set and . For the cases with three changes, the variances on each segment were . For each simulated data set, we estimated changepoints using binary segmentation (Figure 8) or PELT (Figure 9) and calculated an estimate of the -value corresponding to the first detected changepoint using a Gaussian process (as outlined in Section 3.2.2), and using a Gaussian process followed by importance sampling from the posterior distribution, for .

Under , the -values obtained using just a Gaussian process (i.e. the proportion of GP samples is 1) lie along the straight line implying they follow the distribution , whilst if we use a GP followed by importance sampling the -values are slightly conservative for small , although still close to uniform. Similarly, when we sample data with changepoints, for small we get slightly greater power if we just use a GP. For there seems to be very little difference between these methods. Overall, it appears that using just a Gaussian process generally gives at least as good results as using a Gaussian process followed by importance sampling.

How do we know when we have enough samples? We see that seems to be sufficient in the above cases, as the estimated -values follow a uniform distribution under , and under increasing from 50 to 200 does not seem to lead to increased power. It is possible that we would need more samples if the number of data points or the number of changes was larger.

5.3 Increasing power

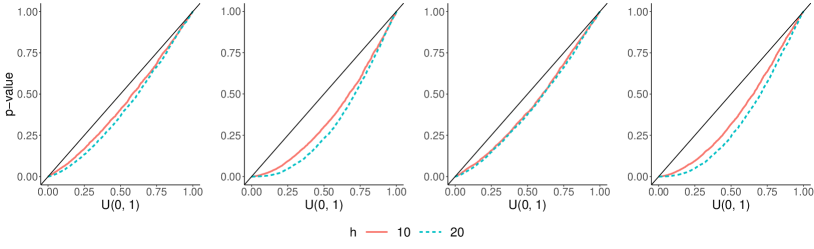

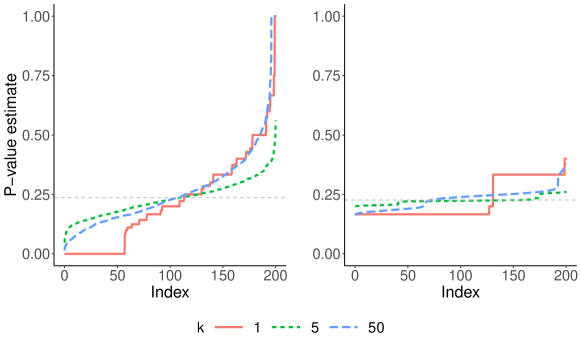

Figure 10 shows -values we obtained where we estimated a single changepoint using the CUSUM statistic and used the method described in Section 4.3 to calculate -values. We can see that under (left) we obtain valid -values for any value of the number of samples . When we sample from a model with a single change at (right), increasing from 1 to 5 gives greater power against , although increasing it beyond this does not seem to make much difference.

Figure 11 shows similar plots where we simulate from a model with a change at , and use the likelihood ratio to estimate changepoints, and a Gaussian process with samples to estimate -values. We see a similar pattern, where increasing the number of samples initially leads to greater power.

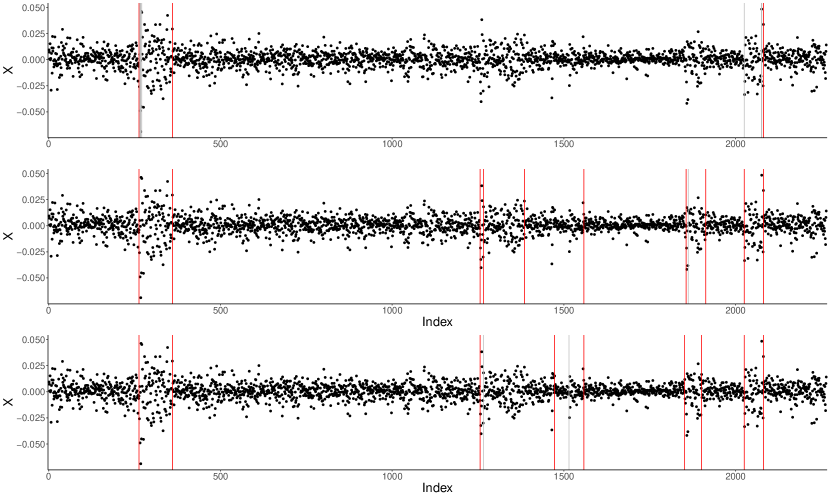

6 Application to financial data

To investigate how well our method works in a real-world setting, we applied our method to finanical data (Figure 12). The data is log returns from S&P500 stock market data for 2264 days from July 2010 to October 2019111The data was downloaded from https://www.kaggle.com/datasets/mathisjander/s-and-p500-volatility-prediction-time-series-data. We can see from Figure 12 that the data appears to have zero mean and several changes in variance. We estimated changepoints using three different methods: binary segmentation with the CUSUM statistic (top) and the likelihood ratio statistic (middle) and PELT (bottom), and calculated -values for each estimated changepoint. We set thresholds so that in each case we estimated 11 changepoints, and set . For the cases where we had to estimate -values, we used a Gaussian process with . On each plot estimated changepoints are shown by vertical lines, with red lines corresponding to estimated changepoint locations whose -values were smaller than (after controlling for multiple testing using the Holm-Bonferroni method) and grey lines corresponding to -values which were not significant. Using the likelihood ratio statistic generally seems to give better results than CUSUM, where there are more instances of multiple changepoints being estimated close together. However, these spurious changepoints generally have non-significant -values associated with them, showing that our method for post-selection inference is effective at distinguishing true from false changepoint estimates.

7 Discussion

In this paper we have proposed a test for the piecewise constant change in variance model. We have developed methods for post-selection inference, which allow us to quantify uncertainty by computing -values for estimated changes, and we have shown that our methods work on simulated and real data.

We have worked on the assumption that the data is i.i.d. Gaussian except for abrupt changes in variance. In practice, less restrictive models may be more appropriate in many cases, for example allowing the mean to change as well as the variance, or allowing autocorrelation between data points. Further work in this area could include extending or adapting our approach to apply to such models.

The strategies we have developed using Gaussian processes and importance sampling may be useful for other similar situations where we conduct post-selection inference but cannot characterise the selection event explicitly.

Acknowledgement

This work is supported by EPSRC grant number EP/V053590/1.

References

- \bibcommenthead

- Anastasiou et al. [2022] Anastasiou, A., Cribben, I., Fryzlewicz, P.: Cross-covariate isolate detect: A new change-point method for estimating dynamic functional connectivity. Medical Image Analysis 75, 102252 (2022)

- Amiri et al. [2015] Amiri, A., Niaki, S.T.A., Moghadam, A.T.: A probabilistic artificial neural network-based procedure for variance change point estimation. Soft Computing 19, 691–700 (2015)

- Baranowski et al. [2019] Baranowski, R., Chen, Y., Fryzlewicz, P.: Narrowest-over-threshold detection of multiple change points and change-point-like features. Journal of the Royal Statistical Society: Series B 81(3), 649–672 (2019)

- Barry and Hartigan [1993] Barry, D., Hartigan, J.A.: A Bayesian analysis for change point problems. Journal of the American Statistical Association 88(421), 309–319 (1993)

- Caron et al. [2012] Caron, F., Doucet, A., Gottardo, R.: On-line changepoint detection and parameter estimation with application to genomic data. Statistics and Computing 22, 579–595 (2012)

- Carrington and Fearnhead [2023] Carrington, R., Fearnhead, P.: Improving power by conditioning on less in post-selection inference for changepoints. arXiv preprint arXiv:2301.05636 (2023)

- Chen et al. [2023] Chen, Y.T., Jewell, S.W., Witten, D.M.: Quantifying uncertainty in spikes estimated from calcium imaging data. Biostatistics 24(2), 481–501 (2023)

- Cappello and Padilla [2023] Cappello, L., Padilla, O.H.M.: Bayesian variance change point detection with credible sets. arXiv preprint arXiv:2211.14097 (2023)

- Duy and Takeuchi [2022] Duy, V.N.L., Takeuchi, I.: More powerful conditional selective inference for generalized lasso by parametric programming. The Journal of Machine Learning Research 23(1), 13544–13580 (2022)

- Eichinger and Kirch [2018] Eichinger, B., Kirch, C.: A mosum procedure for the estimation of multiple random change points. Bernoulli 24, 526–564 (2018)

- Fearnhead [2006] Fearnhead, P.: Exact and efficient Bayesian inference for multiple changepoint problems. Statistics and Computing 16, 203–213 (2006)

- Frick et al. [2014] Frick, K., Munk, A., Sieling, H.: Multiscale change point inference. Journal of the Royal Statistical Society: Series B 76(3), 495–580 (2014)

- Fearnhead and Rigaill [2020] Fearnhead, P., Rigaill, G.: Relating and comparing methods for detecting changes in mean. Stat 9(1), 291 (2020)

- Fryzlewicz [2014] Fryzlewicz, P.: Wild binary segmentation for multiple change-point detection. The Annals of Statistics 42(6), 2243–2281 (2014)

- Fryzlewicz [2023] Fryzlewicz, P.: Narrowest significance pursuit: inference for multiple change-points in linear models. Journal of the American Statistical Association, 1–14 (2023)

- Fryzlewicz [2024] Fryzlewicz, P.: Robust narrowest significance pursuit: Inference for multiple change-points in the median. Journal of Business & Economic Statistics, 1–14 (2024)

- Fithian et al. [2014] Fithian, W., Sun, D., Taylor, J.: Optimal inference after model selection. arXiv:1410.2597 (2014)

- Hyun et al. [2021] Hyun, S., Lin, K.Z., G’Sell, M., Tibshirani, R.J.: Post-selection inference for changepoint detection algorithms with application to copy number variation data. Biometrics 77(3), 1037–1049 (2021)

- Inclan and Tiao [1994] Inclan, C., Tiao, G.C.: Use of cumulative sums of squares for retrospective detection of changes of variance. Journal of the American Statistical Association 89(427), 913–923 (1994)

- Jewell et al. [2022] Jewell, S., Fearnhead, P., Witten, D.: Testing for a change in mean after changepoint detection. Journal of the Royal Statistical Society: Series B 84(4), 1082–1104 (2022)

- Jiang et al. [2023] Jiang, F., Zhao, Z., Shao, X.: Time series analysis of covid-19 infection curve: A change-point perspective. Journal of econometrics 232(1), 1–17 (2023)

- Kovács et al. [2023] Kovács, S., Bühlmann, P., Li, H., Munk, A.: Seeded binary segmentation: a general methodology for fast and optimal changepoint detection. Biometrika 110(1), 249–256 (2023)

- Killick et al. [2012] Killick, R., Fearnhead, P., Eckley, I.A.: Optimal detection of changepoints with a linear computational cost. Journal of the American Statistical Association 107(500), 1590–1598 (2012)

- Kuchibhotla et al. [2022] Kuchibhotla, A.K., Kolassa, J.E., Kuffner, T.A.: Post-selection inference. Annual Review of Statistics and Its Application 9, 505–527 (2022)

- Li et al. [2016] Li, H., Munk, A., Sieling, H.: Fdr-control in multiscale change-point segmentation. Electronic Journal of Statistics 10, 918–959 (2016)

- Muggeo and Adelfio [2011] Muggeo, V.M., Adelfio, G.: Efficient change point detection for genomic sequences of continuous measurements. Bioinformatics 27(2), 161–166 (2011)

- Mehrizi and Chenouri [2021] Mehrizi, R.V., Chenouri, S.: Valid post-detection inference for change points identified using trend filtering. arXiv preprint arXiv:2104.12022 (2021)

- Maidstone et al. [2017] Maidstone, R., Hocking, T., Rigaill, G., Fearnhead, P.: On optimal multiple changepoint algorithms for large data. Statistics and Computing 27, 519–533 (2017)

- Meier et al. [2021] Meier, A., Kirch, C., Cho, H.: mosum: A package for moving sums in change point analysis. Journal of Statistical Software 97(8), 1–42 (2021)

- Nam et al. [2012] Nam, C.F., Aston, J.A., Johansen, A.M.: Quantifying the uncertainty in change points. Journal of Time Series Analysis 33(5), 807–823 (2012)

- Reeves et al. [2007] Reeves, J., Chen, J., Wang, X.L., Lund, R., Lu, Q.Q.: A review and comparison of changepoint detection techniques for climate data. Journal of Applied Meteorology and Climatology 46(6), 900–915 (2007)

- Shi et al. [2022] Shi, X., Beaulieu, C., Killick, R., Lund, R.: Changepoint detection: An analysis of the central England temperature series. Journal of Climate 35(19), 2729–2742 (2022)

- Schröder and Fryzlewicz [2013] Schröder, A.L., Fryzlewicz, P.: Adaptive trend estimation in financial time series via multiscale change-point-induced basis recovery. Statistics and Its Interface 6, 449–461 (2013)

- Shi et al. [2022] Shi, X., Gallagher, C., Lund, R., Killick, R.: A comparison of single and multiple changepoint techniques for time series data. Computational Statistics & Data Analysis 170, 107433 (2022)

- Scott and Knott [1974] Scott, A.J., Knott, M.: A cluster analysis method for grouping means in the analysis of variance. Biometrics 30, 507–512 (1974)

- Saha et al. [2022] Saha, A., Witten, D., Bien, J.: Inferring independent sets of Gaussian variables after thresholding correlations. arXiv:2211.01521 (2022)

- Williams and Rasmussen [2005] Williams, C.K., Rasmussen, C.E.: Gaussian Processes for Machine Learning. MIT press, Cambridge, MA (2005)

Supplementary Material for “Post-selection inference for quantifying uncertainty in changes in variance”

Rachel Carrington and Paul Fearnhead

Appendix A Details for (9)

and from (9) are given below.

Appendix B Proof of Lemma 2

We want to show that are independent. To do this we calculate the joint density of these variables and show that it can be factorized into functions of each variable.

Let ( denote the function such that , and let denote the Jacobian matrix of partial derivatives

Then the density function of is given by

We get

To calculate the determinant of , note that using elementary row operations, we can show that is equal to the determinant of the matrix

We can show that this matrix is upper triangular, which allows us to calculate the determinant as the product of its diagonal elements. Since

it follows that for , and clearly we also have for all . Similarly, we can show that for , and for all . In the bottom row, as , all the matrix entries except the last are 0.

We get

Hence,

Hence, we get

This can be factorized as . It is also verifiable that all these variables have domain (except for which is ) regardless of the values of the others. Hence these variables are all independent.

Appendix C Additional simulations

Here we include some additional simulations to those in Section 5, where we include different changepoint algorithms and parameter values.

C.1 Detecting changes using CUSUM

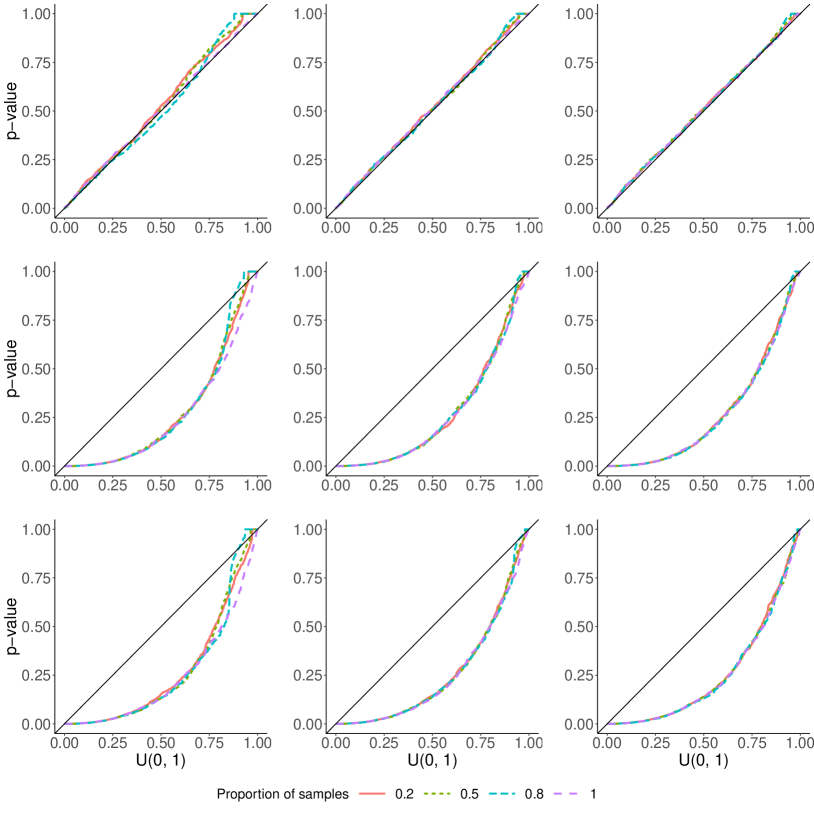

Figure 6 showed QQ plots of -values obtained for simulated data sets, where changepoints were estimated using binary segmentation with the CUSUM statistic. Here, we present similar results for two different scenarios: in Figure 13 we simulate data with data points (compared to in Figure 6) and once again estimate changepoints using binary segmentation; in Figure 14 we set and estimate changepoints using wild binary segmentation.

In each figure, panel (a) shows the results when data was simulated under ; panels (b)–(d) show -values obtained when we simulated from a model with a single changepoint at , with three different values of the post-change variance. In each case we see a similar pattern of results to Figure 6.

C.2 Sampling with and without stratification

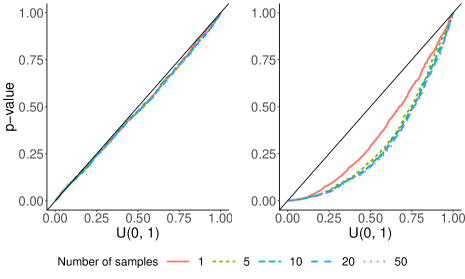

In Section 3.2.1, we discussed using stratified sampling to estimate the -value. Figure 15 shows plots of the -values we obtained for a given simulated data set, using importance sampling with and without stratification, with 200 samples in each case. (Values of are sampled from for ; the true distribution of is .) We can see that although the two methods have the same mean, using stratified sampling results in a much smaller variance in the -value estimate.

C.3 Extra simulations for Gaussian process approach

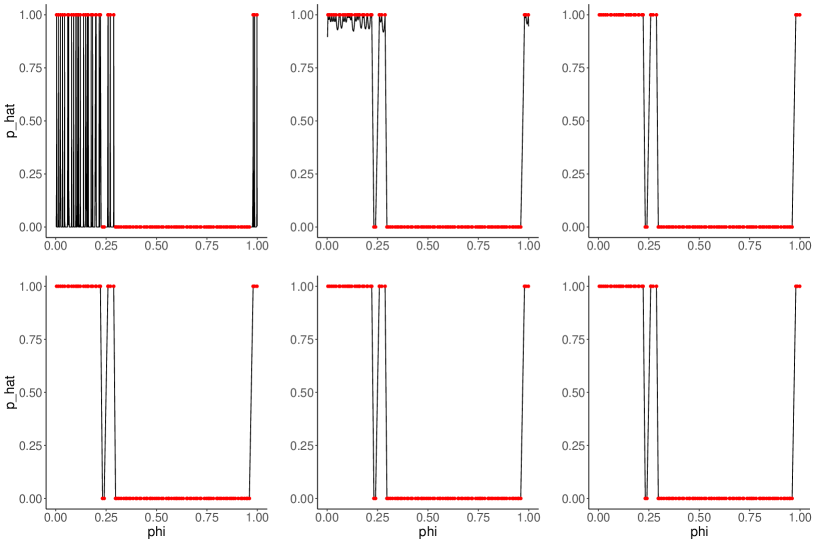

For the Gaussian process model, we use a kernel of the form

| (13) |

where are two possible values of . The value is a hyperparameter, which must be chosen before we fit the model. A larger will lead to a smoother function , as it will more strongly force and to take the same value when and are close together.

In Figure 16, we investigate the effect of using six different values of (), for a simulated data set. The figure displays , shown by a black line, with observed values shown as red points. For , the estimates we obtain of are very similar, and appropriately smooth: most values have in (or very close to one of these values), and we expect that will consist of a small number of intervals. Using or gives less good results. So, it seems like a value is likely to give good results. In the paper we set for all simulations and data analyses.