High Rank Path Development: an approach of learning the filtration of stochastic processes

Abstract

Since the weak convergence for stochastic processes does not account for the growth of information over time which is represented by the underlying filtration, a slightly erroneous stochastic model in weak topology may cause huge loss in multi-periods decision making problems. To address such discontinuities Aldous introduced the extended weak convergence, which can fully characterise all essential properties, including the filtration, of stochastic processes; however was considered to be hard to find efficient numerical implementations. In this paper, we introduce a novel metric called High Rank PCF Distance (HRPCFD) for extended weak convergence based on the high rank path development method from rough path theory, which also defines the characteristic function for measure-valued processes. We then show that such HRPCFD admits many favourable analytic properties which allows us to design an efficient algorithm for training HRPCFD from data and construct the HRPCF-GAN by using HRPCFD as the discriminator for conditional time series generation. Our numerical experiments on both hypothesis testing and generative modelling validate the out-performance of our approach compared with several state-of-the-art methods, highlighting its potential in broad applications of synthetic time series generation and in addressing classic financial and economic challenges, such as optimal stopping or utility maximisation problems.

1 Introduction

A popular criterion for measuring the differences between two stochastic processes is the weak convergence. In this framework, one views stochastic processes as path-valued random variables and then defines the convergence for their laws, which are distributions on path space. However, this viewpoint ignores the filtration of stochastic processes, which models the evolution of information, and therefore such loss may have negative implications in multi-period optimisation problems. For example, for the American option pricing task, even if the two underlying processes are stochastic processes with very similar laws, the corresponding price of American options can be completely different, see a toy example A.1 in Appendix A.1. To address this shortcoming of weak convergence, D. Aldous [1] introduced the notion of extended weak convergence. The central object in this methodology is the so-called prediction process, which consists of conditional distributions of the underlying process based on available information at different time beings, and therefore reflects how the associated information flow (i.e., filtration) affects the prediction of the future evolution of the underlying process as time varies. Instead of considering the laws of processes (i.e., distributions on path space) in weak convergence, one compares the laws of prediction processes, which are distributions on the measure-valued path space, in extended weak convergence. Since the knowledge of filtration is captured through taking conditional distributions, it was shown in [3] the topology induced by extended weak convergence, which belongs to the so-called adapted weak topologies111In general, any topology on the space of stochastic processes which can reflect the differences of associated filtrations can be called an adapted weak topology., fully characterise essential properties of stochastic processes and endow multi-period optimisation problems with continuity, provided filtration is generated by the process itself.

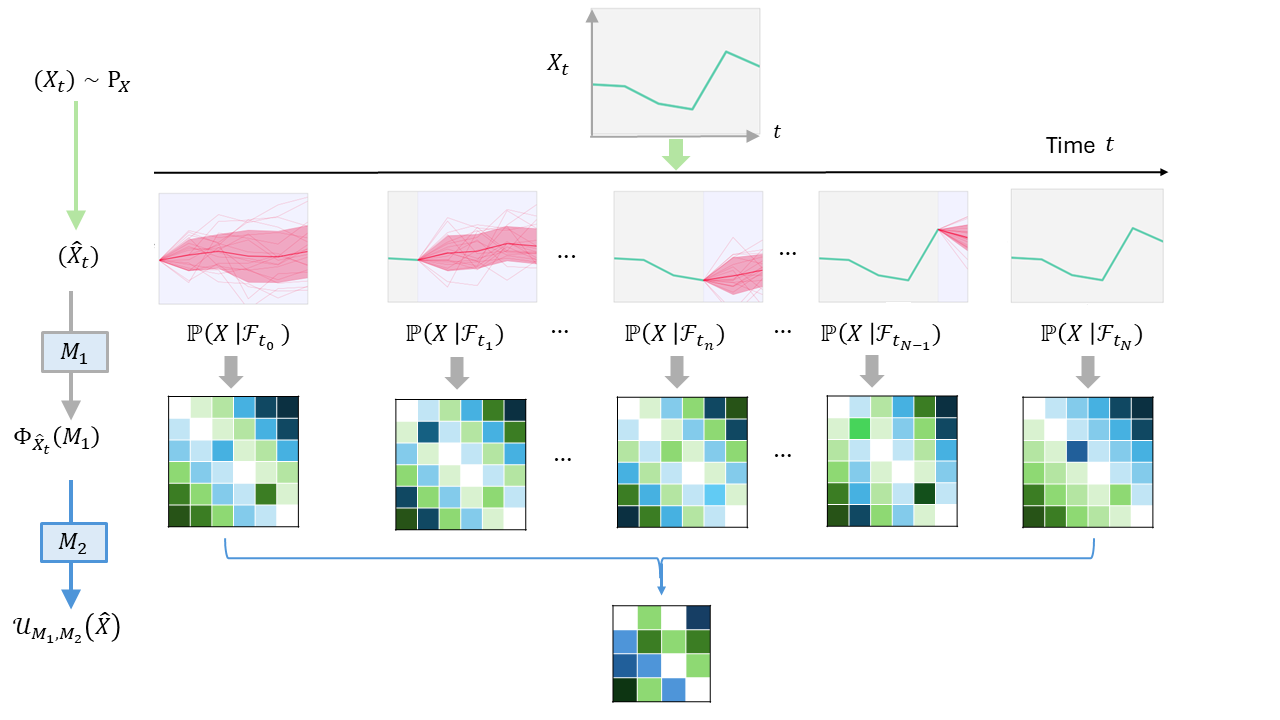

While the theoretical contributions to adapted weak topologies flourish in recent years (e.g., [3], [2], [4]), the related work on numerics is still very sparse because of the very complex nature of these topologies. In this paper, we propose a novel metric called High Rank Path Characteristic Function (HRPCFD) which can metrise the extended weak convergence, and, more importantly, admits an efficient algorithm. The core idea of this approach is built on top of the unitary feature of -valued paths ([17], [6]), which exploits the non-commutativity and the group structure of the unitary developments to encode information on order of paths. Based on the same consideration, Lou et al. [18] introduced the Path Characteristic Function (PCF) for stochastic processes, which induces a computable distance (namely, PCFD) to metrise the weak convergence. As extended weak convergence is defined in terms of laws of prediction processes which are measure-valued stochastic processes, the scheme of PCF remains valid in adapted weak topologies as long as one can construct a PCF of measure-valued paths. One of the main contributions of the present work is to give such a suitable notion via the so-called high rank path development (see Figure 1 for illustration); moreover, we can show that the induced distance (called HRPCFD) does not only characterise the more complicated extended weak convergence, but also inherits almost all favourable analytic properties of classical PCFD mentioned in [18]. Since the measure-valued paths take values in an infinite dimensional nonlinear space, such a generalisation of the results in [18] from -valued paths to measure-valued paths is much technically involved and therefore significantly nontrivial.

On the numerical side, we design an efficient algorithm to train HRPCFD from data and construct the HRPCF-GAN model with HRPCFD as the discriminator for time series generation. A key computational challenge in applying distances based on extended weak topology is the accurate and efficient estimation of the conditional probability measure. To address this issue, we have implemented a sequence-to-sequence regression module that effectively resolves this bottleneck. Our work is the first of its kind to apply the adapted weak topology for generative models on time series generation. Moreover, to validate the effectiveness of our approach, we conduct experiments in (1) hypothesis testing to classify different stochastic processes, and (2) conditional time series generation to predict the future time series given the past time series. Our HRPCF-GAN can be viewed as a natural generalisation of PCF-GAN [18] to the setting of extended weak convergence, so that the data generated by HRPCF-GAN possesses not only a similar law but also a similar filtration with the target model. The numerical experiments validate the out-performance of this new approach based on HRPCFD compared with several state-of-the-art GAN models for time series generation in terms of various test metrics.

Related work. So far most of existing statistical and numerical methods for handling stochastic processes (e.g., [8, 15, 18]) are based on weak convergence, and the results on numerical implementation of adapted weak topologies are rather limited. The most relevant work is [20], whose theoretical foundation roots in [5]. The present paper shares a similar philosophy with [20] in the sense that both methods for defining metrics for extended weak convergence rely on the construction of a feature of the measure-valued path by transforming it into a linear space-valued path. In contrast to [20], where a measure-valued path is lifted to an infinite-dimensional Hilbert space, we reduce measure-valued paths into matrix-valued paths through unitary development which allows us to apply the techniques from [18] to design the algorithm. Another remarkable point is that in [20] one has to solve a large family of PDEs to compute the distance, which can be avoided in the numerical estimation of the HRPCFD proposed here. On the other hand, as Wasserstein distances can metrise weak convergence, the so-called causal Wasserstein distances can be used to measure adapted weak topologies. One related work is [21] which can be seen as an improved variant of the Sinkhorn divergence tailored to sequential data. Note that the discriminator (i.e., causal Wasserstein metric) used in [21] is slightly weaker than the HRPCFD, as the latter is actually equivalent to the bi-causal Wasserstein distance.

2 Preliminaries

2.1 Prediction Processes and Extended Weak Convergence

Let and be an –valued stochastic process defined on a filtered stochastic basis such that is adapted to the filtration , i.e., is measurable with respect to for all . We call the five–tuple a filtered process, and denote it by . Throughout this paper, we will use FP to denote the space of all (–valued) filtered processes on the discrete time interval , and assume that is the natural filtration in the sense that for every , .

Since each discrete time path can be uniquely extended to a piecewise linear path on by linear interpolation, we will not distinguish the product space and the subspace of (the space of all continuous functions in with bounded variation)222This means that is equipped with the topology induced by the total variation norm.. Clearly each stochastic process can be seen as -valued random variable, and therefore the law of , denoted by , belongs to , the space of probability measures on the path space . Recall that a sequence of filtered processes converges to a limit weakly or in the weak topology (in notation: ) if the laws converges to in weakly, i.e., for all continuous and bounded functions , it holds that .

For each , we denote as the (regular) conditional distribution of given , which is a random measure taking values in . We call this measure-valued process the prediction process of the filtered process . By definition it is clear that the state space of is and, again, by a routine linear interpolation333For and , define ., we can embed into . Thus the law of , denoted by , belongs to (the space of probability measures on the measure-valued path space ), where is endowed with the product topology and is equipped with the corresponding weak topology.

Definition 2.1.

-

•

Two filtered processes and are called synonymous if their prediction processes and have the same law in , i.e., .

-

•

A sequence of filtered processes , converges to another filtered process in the extended weak convergence if the law of their prediction processes converges to the law of in weakly, i.e., for all continuous and bounded functions , . In notation: .

If and are the trivial -algebra, then and are laws of and respectively, so that certainly implies that . This implies that extended weak convergence is stronger than weak convergence. Moreover, the extended weak convergence induces the correct topology in multi-period decision making problems, as the next theorem (see [1, 3]) shows.

Theorem 2.2.

The extended weak convergence provides continuity for the value functions in multi-period optimisation problems (e.g., optimal stopping problem, utility maximisation problem), as long as the reward function is continuous and bounded.

Admittedly, the above notions related to extended weak convergence (e.g., the spaces and , the weak convergence in etc.) are rather abstract. Therefore, we provide some simple examples in Appendix A.1 to explain these notions in a more transparent way. We refer readers to [1] and [3] for more details on extended weak convergence.

2.2 Path Development and Path Characteristic Function (PCF)

In this subsection, we review some important notions and properties of -valued path development and characteristic function (PCF) for -valued stochastic processes, which will be used later to construct characteristic functions for measure-valued stochastic processes. We refer readers to [18] and [17] for a more detailed discussion on this topic.

For , let be the space of complex matrices, denote the identity matrix in , and be conjugate transpose. Write and for the Lie group of unitary matrices and its Lie algebra, resp.:

Let denote the space of linear mappings from to .

Definition 2.3.

Let be a continuous path with bounded variation and be a linear map. The unitary feature of under is the solution to the following equation:

| (1) |

where denotes the usual matrix product. We write , i.e., the endpoint of the solution path, and by an abuse of notation, also call it the unitary feature of (under ).

The unitary feature is a special case of the path development, for which one may consider paths taking values in any Lie group . It is easy to see that for piecewise linear path , it holds for and denotes the matrix exponential. We now use the unitary feature to define the Path Characteristic Function (PCF) for -valued stochastic processes:

Definition 2.4.

Let be a filtered process and be its law. The Path Characteristic Function (PCF) of is the map given by

To distinguish from the so-called high rank PCF which will be defined in the next subsection, we also call the rank PCF. The next theorem (see [18, Theorem 3.2]) justifies why defined in Definition 2.4 is called PCF for path-valued random variables.

Theorem 2.5 (Characteristicity of laws).

For and two filtered processes, they have the same law (i.e., ) if and only if .

The characteristicity of PCF allows us to define a novel distance on FP which metrises the weak convergence (locally). This metric is called the PCF-based distance (PCFD), see [18, Definition 3.3]. Moreover, such PCFD possesses many nice analytic properties including boundedness ([18, Lemma 3.5]), Maximum Mean Discrepancy (MMD, [18, Proposition B.10]) among others, see [18, Section 3.2], which ensures the feasibility of using PCFD in numerical aspect.

Remark 2.6.

Rigorously speaking, we need to add an additional time component to every -valued process (i.e., consider ) to guarantee Theorem 2.5 holds true. We will always implicitly use such time-augmentation throughout the whole paper and still write instead of for simplicity of notations.

3 High Rank Path Development Embedding

We now want to construct a characteristic function for prediction processes and use it to metrise the extended weak convergence just like PCFD metrises the weak convergence. Since prediction processes are -valued random variables, we first need to find a suitable notion of unitary feature/development for measure-valued paths.

3.1 High Rank Development of Prediction Processes

Given a filtered process , remember that its prediction process satisfies for . Now, for a linear operators for , we take the conditional expectation of against to obtain a –valued stochastic process Then, for any with some , the unitary feature of –valued path is well defined and takes values in the unitary group . We call each pair for an admissible pair of unitary representations, and the set of all admissible pairs of unitary representations is denoted by .

Definition 3.1.

For with , and a filtered process with its prediction process , we call

| (2) |

the high rank development of the prediction process under .

See Figure 1 for the schematic overview of the high rank development. From above we can see that the construction of involves with taking finite dimensional path development in Section 2.2 twice: first use the PCF under to transform each conditional distribution into a matrix , and then apply the unitary feature to the resulting matrix-valued path for .

3.2 High Rank Path Characteristic Function

With the above notion of unitary feature of measure-valued paths, following Definition 2.4, we define the high rank Path Characteristic Function (HRPCF) for filtered processes.

Definition 3.2.

For a filtered process , the function

| (3) |

is called the High Rank Path Characteristic Function of (Abbreviation: HRPCF)444We use the superscript “” in to emphasise that is induced by taking usual path development twice..

is said to be a HRPCF for as it satisfies the following characteristicity of synonym for filtered processes (see Definition 2.1). For a detailed proof please check the Appendix A.

Theorem 3.3 (Characteristicity of synonym).

Two filtered processes and are synonymous if and only if they have the same high rank PCF, that is,

3.3 A New Distance induced by High Rank PCF

In this subsection, we will use the second rank PCF to define a distance on FP, which can (locally) characterize the extended weak convergence, as the classical PCFD introduced in subsection 2.2 can metrise the weak topology on FP.

Definition 3.4.

For two filtered processes and , let be a random admissible pair in with for some , and for some . The High Rank Path Characteristic Function-based distance, for short HRPCFD, between and with respect to and is defined by

where denotes the Hilbert-Schmidt distance555For , . on .

As previously mentioned in the introduction, the so-defined HRPCFD shares the same analytic properties as the classical PCF, e.g., the separation of points, boundedness and the MMD property, whose proof can be found in Appendix A. Moreover, it metrises a much stronger topology (the extended weak convergence). as shown in the next theorem.

Theorem 3.5.

Suppose and are filtered processes whose laws and are supported in a compact subset of . Then iff , where

where the sequence satisfies that for any there is a such that and and , have full supports for all .

We provide a concrete example in the last paragraph of Appendix A.1 to verify the fact that HRPCFD really reflects the differences of filtrations via an explicit computation.

4 Methodology

In this section, let and be two filtered processes with the law , let and be sample paths.

4.1 Estimating conditional probability measure and HRPCF

A fundamental question is to estimate the conditional probability measure from the finitely many data , in particular the random variable for any . We solve this problem by conducting a regression. Fix we learn a sequence-to-sequence model , where the input and output pairs are . More specifically, we optimize the model parameters of by minimizing the loss function:

| (4) |

It is worth noting that the choice of must be autoregressive models to prevent information leakage. A detailed pseudocode is shown in Algorithm 1. Then, we approximate using the trained regression model following the Algorithm 2. We denote by the estimation of .

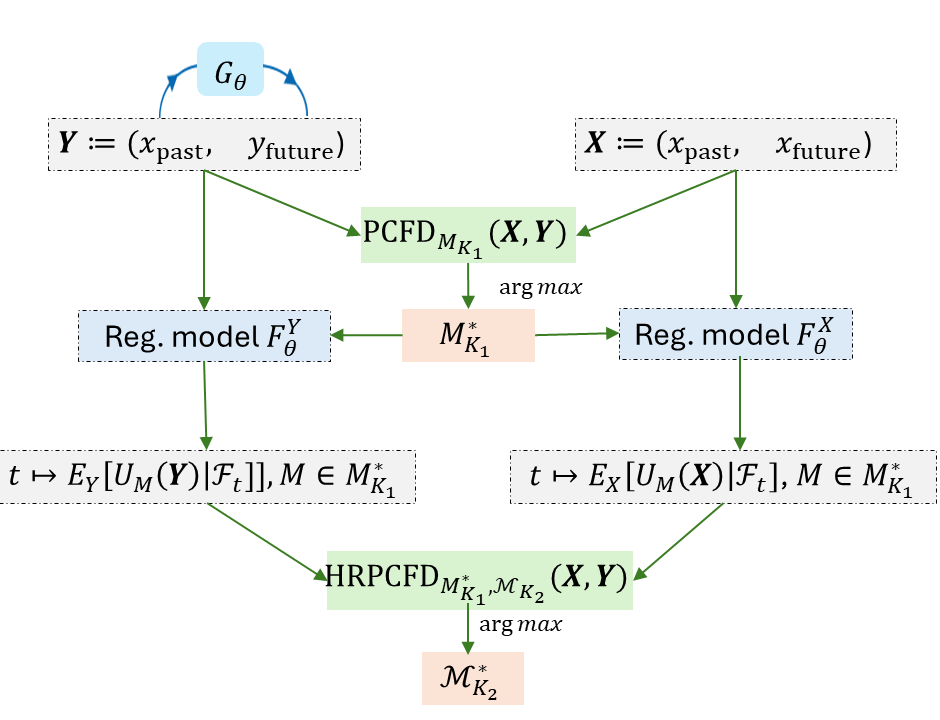

4.2 Optimizing HRPCFD

In most empirical applications as we will show in Section 5, we employ HRPCFD as a discriminator under the GAN setting. That is, we optimize the loss function . We would approximate the pair of random variables by discrete random variables parametrized by and , and optimize so-called Empirical HRPCFD

| (5) |

In practice, the joint training on both and is computationally expensive and prone to overfitting. We alleviate this problem by splitting the optimization procedure in the following three steps: 1) Optimize to maximize ()[18, Section 3.3] , denote by the optimized linear maps. 2) Train regression modules for each using data sampled from and respectively. 3) Optimize to maximize .

The reason behind it is natural: the optimal set captures the most relevant information that discriminates the distribution from . This difference is reflected in the design of higher rank expected path developments through regression models specifically trained for this purpose. Finally, the HRPCFD based on tends to be more significant among other choices of , making it a stronger discriminator.

4.3 HRPCF-GAN for conditional time series generation

Following [15, 12], we consider the task of conditional time series generation to simulate the law of the future path given the past path from samples of X. To this end, we propose the so-called HRPCF-GAN by leveraging the autoregressive generator and the trainable HRPCFD as the discriminator. See Figure 2 for the flowchart illustration.

Conditional autoregressive generator To simulate future time series of length , we construct a generator based on the step-1 conditional generator following [15]. This generator, , aims to produce a random variable approximating . By applying inductively, we can simulate future paths of arbitrary length. To address the limitation of AR-RNN generator proposed in [15], where depends solely on -lagged values of , we incorporate an embedding module. This module efficiently extracts past path information into a low-dimensional latent space. The output of this embedding module, along with the noise vector, serves as the input for to generate subsequent steps in the fake time series. Further details of our proposed generator are provided in Section B.2.

High Rank development discriminator To capture the conditional law, we use the HRPCFD as the discriminator of joint law of under true and fake measures. Here the empirical measures of and are model parameters of the discriminator, which are optimized by the following maximization:

In principle, one can generate the fake data by the generator via Monte Carlo and apply the training procedure outlined in Section 4.2 for training the generative model. However, it would be computationally infeasible due to the need for recalibration of the regression module per generator update. To enhance the training efficiency for the regression module under the fake measure, we use the gradient descent method with efficient initialization obtained by the trained regression model under real data. For each generator, the corresponding regression model parameters are then updated to minimize the RLoss (Equation 4) on a batch of newly generated samples by . The detailed algorithm is described in Algorithm 3.

5 Numerical results

5.1 Hypothesis testing

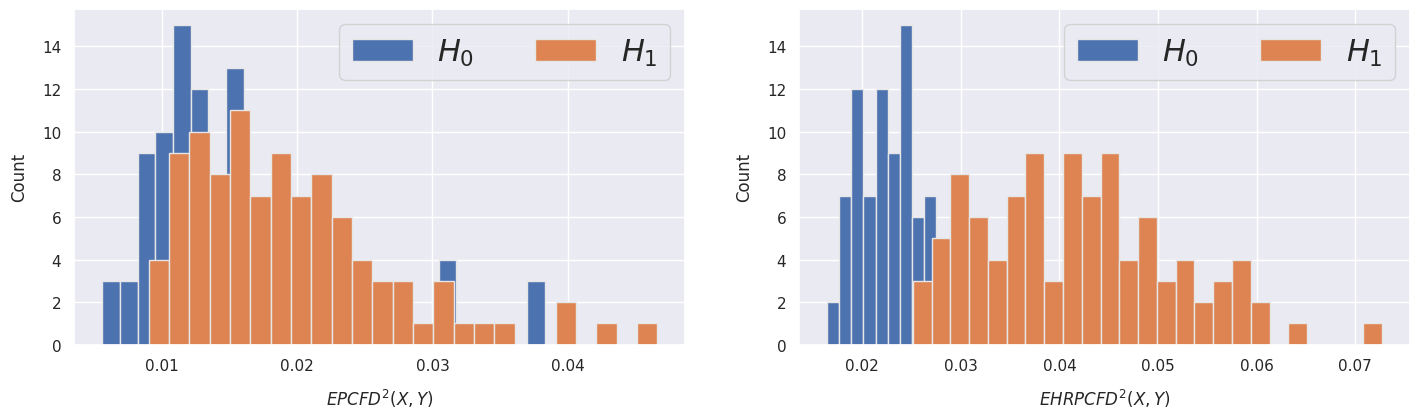

To showcase the power of EHRPCFD in discriminating laws of stochastic processes, we use it as the test statistic in the permutation test. Similar experiments have been done in [20, 14]. By regarding the permutation test as a decision rule, we assess its performance via computing its power (probability of correctly rejecting the null hypothesis) and type-I error (probability of falsely rejecting the null hypothesis). Similar to [14], we compare the law of -dimensional Brownian motion with the set of laws of -dimensional fractional Brownian motion with Hurst parameter ranging from . Details of the methodology and implementation can be found in Section C.1.

Baselines We compare the performance of HRPCFD with other test metrics including 1) the linear and RBF signature MMDs [7, 19] and its high-rank derivative, namely High Rank signature MMDs [20]; 2) Classical vector MMDs; 3) PCFD [14, 18].

As shown in Table 1 of the test power, HRPCFD consistently outperforms other models, especially when is close to . We do see an improvement from the vanilla PCFD by considering a stronger topology. Furthermore, comparing HRPCFD and High Rank signature MMD, we observe a distinct advantage for HRPCFD. This may be due to the challenge of capturing the conditional probability measure, as High Rank signature MMD relies on linear regression for estimation, whereas we obtained a better estimation using a non-linear approach. Additional test metrics such type-I error and computational cost can be found in Section C.1.

| Developments | Signature MMDs | Classical MMDs | |||||||

|---|---|---|---|---|---|---|---|---|---|

| High Rank PCFD | PCFD | Linear | RBF | High Rank | Linear | RBF | |||

| 0.4 | |||||||||

| 0.425 | |||||||||

| 0.45 | |||||||||

| 0.475 | |||||||||

| 0.525 | |||||||||

| 0.55 | |||||||||

| 0.575 | |||||||||

| 0.6 | |||||||||

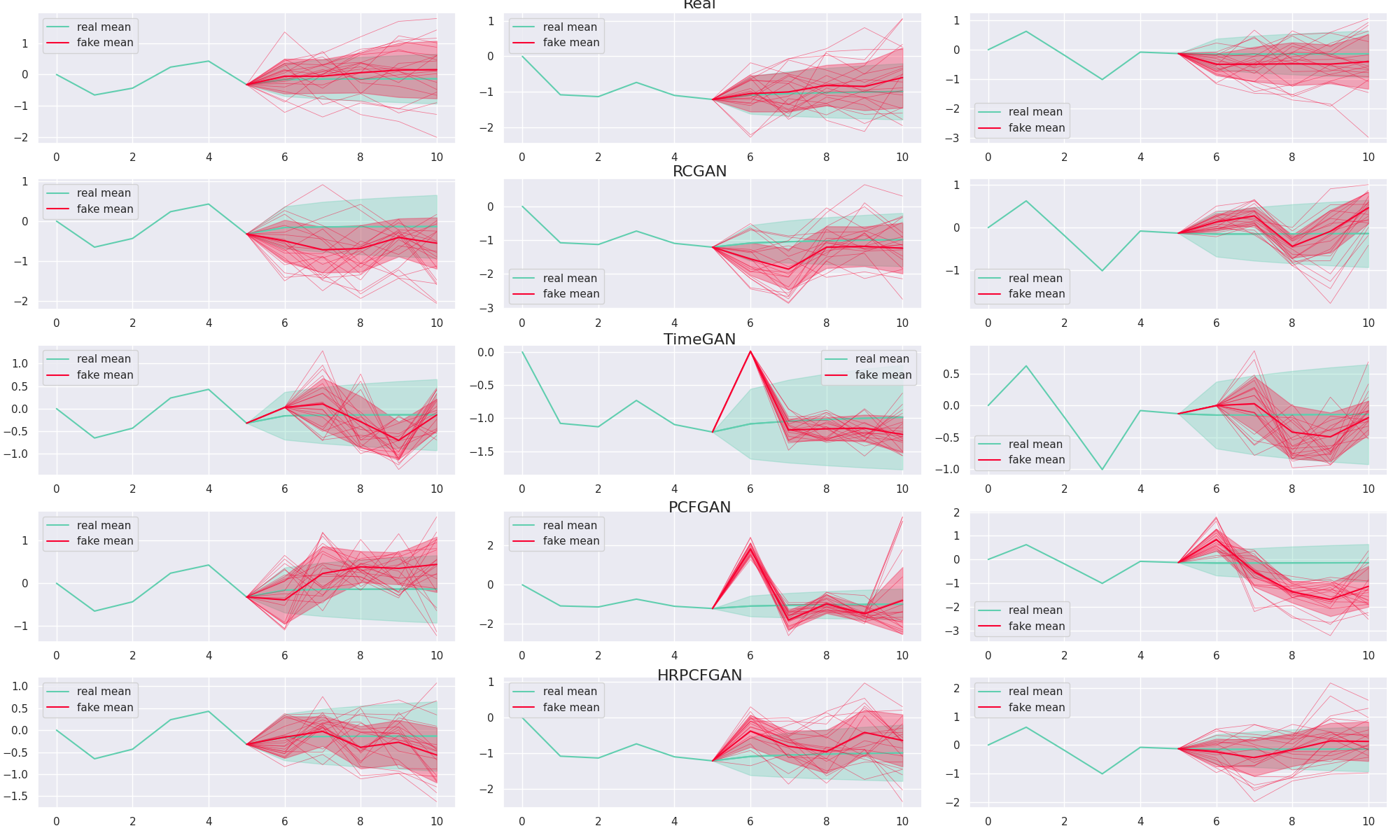

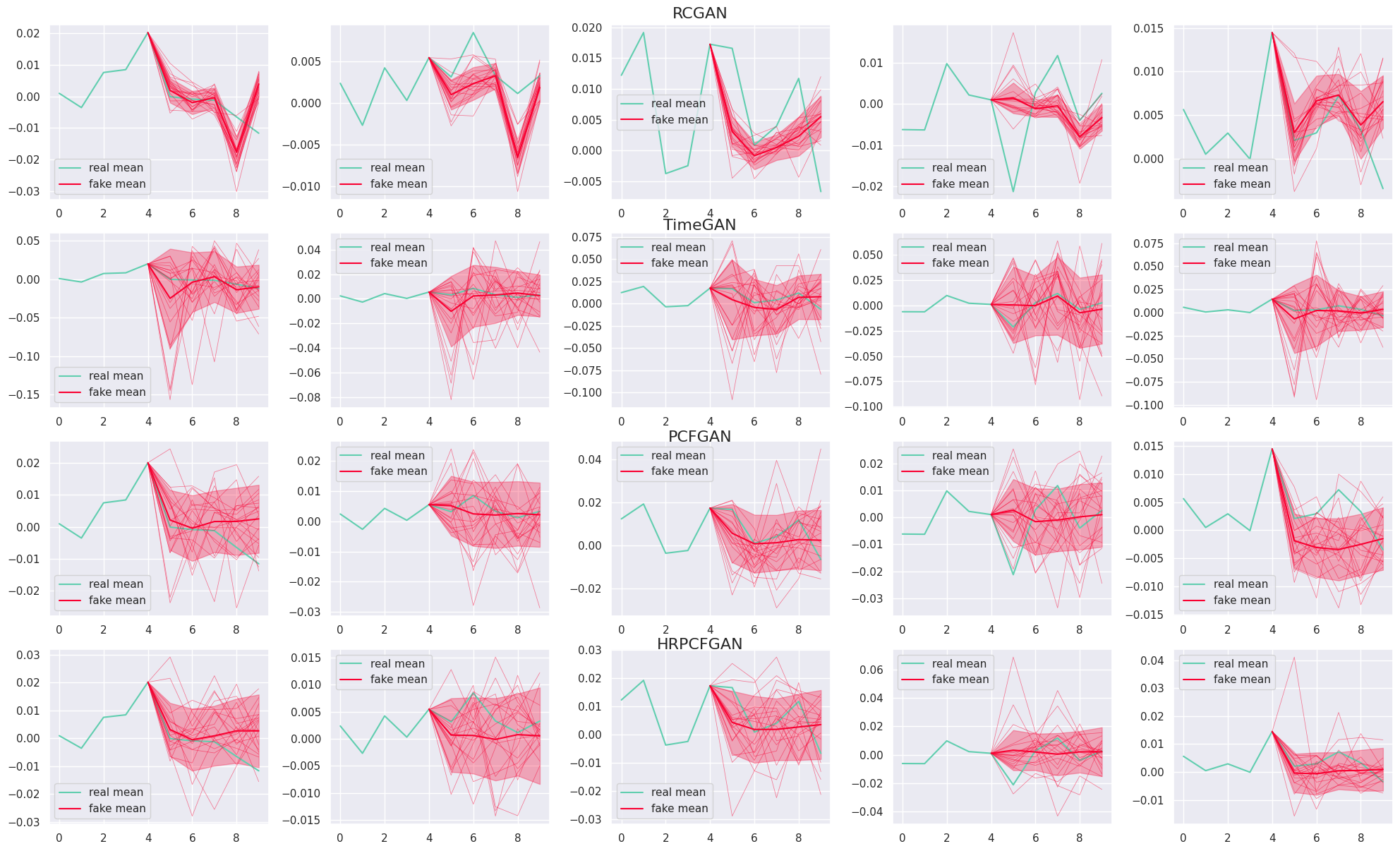

5.2 Generative modeling

To validate the effectiveness of our proposed HRPCF-GAN, we consider the task of learning the law of future time series conditional on its past time series.

Dataset We benchmark our model on both synthetic and empirical datasets. 1) multivariate fractional Brownian Motion (fBM) with Hurst parameter : this dataset exhibits non-Markovian properties and high oscillation. 2) Stock dataset: We collected the daily log return of 5 representative stocks in the U.S. market from 2010 to 2020, sourced from Yahoo Finance.

Baseline We compare the performance of HRPCF-GAN with well-known models for time-series generation such as RCGAN [9] and TimeGAN [22]. Furthermore, we use PCFGAN [18] as a benchmarking model to showcase the significant improvement by considering the higher rank development as the discriminator. For fairness, we use the same generator structure (LSTM-based) for all these models.

Test metrics To assess the fidelity, usefulness, and diversity of synthetic time series, we consider 7 test metrics, including Auto-Correlation, Cross-Correlation, Discriminative Score, Sig- Distance, and Conditional Expectation. For the stock dataset, we also consider a test metric based on American option pricing. A detailed definition of these test metrics can be found in Section C.2.

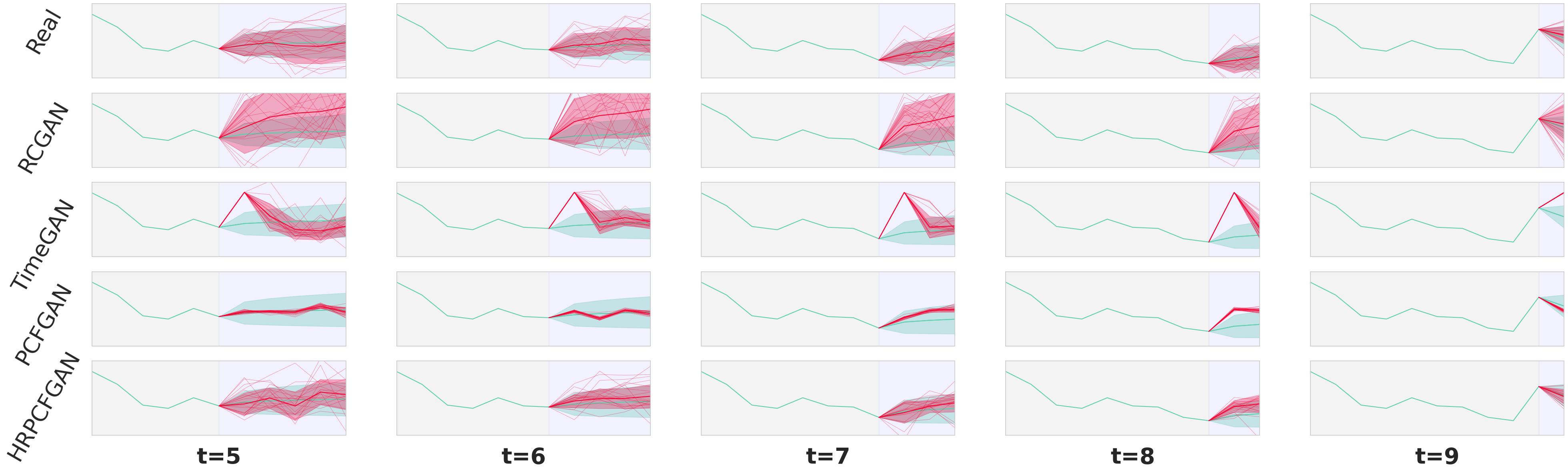

We summarize in Table 2 the performance comparison between HRPCF-GAN and benchmarking models. For both datasets, HRPCF-GAN consistently outperforms the other models. Focusing on the fBM dataset, HRPCF-GAN achieves the lowest Auto-Correlation () and Cross-Correlation (), which is approximately / lower than the second-best model, indicating better performance in fitting the dynamics of the underlying process across time and feature dimensions. We also observe strong evidence in capturing the conditional probability measure as HRPCFGAN achieves the lowest Conditional Expectation score ( on fBM and on Stock). Furthermore, we observe on average an improvement of of HRPCF-GAN with respect to PCFGAN on fBM/Stock datasets respectively. The strong empirical results demonstrate the effectiveness of considering high rank path development to capture the filtration of stochastic processes. Finally, HRPCF-GAN attained the best estimation of an at-the-money American put option, which demonstrates its potential usage for optimal stopping problems in finance. Sample plots from all models conditioned on the same path are also shown in Figures 3, 7 and 6 for a qualitative analysis of generative quality. For additional test metrics, we refer readers to Table 5.

| Dataset | Test Metrics | RCGAN | TimeGAN | PCFGAN | HRPCF-GAN |

| Auto-C. | .105.001 | .459.003 | .125.003 | .082.002 | |

| Cross-C. | .051.001 | .092.001 | .047.001 | .013.001 | |

| fBM | Discriminative | .207.008 | .480.002 | .265.006 | .151.006 |

| Sig- | .512.006 | .341.011 | .199.004 | .169.009 | |

| Cond. Exp. | 1.822.023 | 2.265.029 | 2.278.033 | 1.693.021 | |

| Auto-C. | .239.016 | .228.010 | .198.003 | .189.010 | |

| Cross-C. | .067.011 | .056.002 | .055.004 | .053.005 | |

| Stock | Discriminative | .134.058 | .020.021 | .028.017 | .016.005 |

| Sig- | .013.002 | .008.001 | .005.001 | .004.002 | |

| Cond. Exp. | .078.003 | .079.001 | .060.001 | .056.002 | |

| Amer. Put | .546.318 | .243.411 | .202.020 | .179.006 |

6 Conclusion and Future work

Conclusion: In this paper, we apply the unitary feature from rough path theory to define the CF for measure-valued paths, which further induces a distance (HRPCFD) for metrising the extended weak convergence. Theoretically, we prove the key properties of HRPCFD, such as characteristicity, uniform boundedness, etc. Additionally, the numerical experiments validate the out-performance of the approach based on HRPCFD compared with several state-of-the-art GAN models for tasks such as hypothesis testing and synthetic time series generation.

Limitation and Future work: The suitable choice of network architecture for generating data is crucial in the proposed HRPCF-GAN, which merits further investigation; in particular, it will be interesting to understand how the network architecture impacts the filtration structure of the generated stochastic process. Furthermore, there is room for further improvement on the estimation method of conditional expectation in terms of accuracy and training stability. Possible routes include exploring the interplay between the regression module and the generator, which merits future investigation.

Broader impacts: Our approach based on the extended weak convergence has the potential in many important financial and economic applications, such as optimal stopping, utility maximisation and stochastic programming. Unlike classical methods built on top of parametric stochastic differential equations, our non-parametric and data-driven method alleviates the risk of the model mis-specification, providing better solution to complex, real-world multi-period decision making problems. However, like other synthetic data generation models, it also poses risks of misuse, e.g., misrepresenting the synthetic data as real data.

References

- [1] David Aldous. Weak convergence and the general theory of processes. Unpublished Monograph, 1981.

- [2] Julio Backhoff-Veraguas, Daniel Bartl, Mathias Beiglboeck, and Manu Eder. Adapted Wasserstein distances and stability in mathematical finance. Finance and Stochastics, 24, 2020.

- [3] Julio Backhoff-Veraguas, Daniel Bartl, Mathias Beiglboeck, and Manu Eder. All adapted topologies are equal. Probability Theory and Related Fields, 178(3), 2020.

- [4] Daniel Bartl, Mathias Beiglboeck, and Gudmund Pammer. The Wasserstein spaces of stochastic processes. arXiv:2104.14245, 2021.

- [5] Patric Bonnier, Chong Liu, and Harald Oberhauser. Adapted topologies and higher rank signatures. The Annals of Applied Probability, 33(3), 2023.

- [6] Ilya Chevyrev and Terry Lyons. Characteristic functions of measures on geometric rough paths. Annals of Probability, 44(6), 2016.

- [7] Ilya Chevyrev and Harald Oberhauser. Signature moments to characterize laws of stochastic processes. Journal of Machine Learning Research, 2022.

- [8] Rama Cont, Mihai Cucuringu, Renyuan Xu, and Chao Zhang. TailGAN: Nonparametric scenario generation for tail risk estimation. arXiv:2203.01664, 2022.

- [9] Cristóbal Esteban, Stephanie L. Hyland, and Gunnar Rätsch. Real-valued (medical) time series generation with recurrent conditional GANs, 2017.

- [10] Peter Friz and Nicolas Victoir. Multidimensional Stochastic Processes as Rough Paths. Cambridge University Press, 2010.

- [11] Diederik P. Kingma and Jimmy Ba. Adam: A method for stochastic optimization, 2017.

- [12] Daniel Levin, Terry Lyons, and Hao Ni. Learning from the past, predicting the statistics for the future, learning an evolving system. arXiv preprint arXiv:1309.0260, 2013.

- [13] Mark Leznik, Arne Lochner, Stefan Wesner, and Jörg Domaschka. [sok] the great gan bake off, an extensive systematic evaluation of generative adversarial network architectures for time series synthesis. Journal of Systems Research, 2(1), 2022.

- [14] Siran Li, Zijiu Lyu, Hao Ni, and Jiajie Tao. On the determination of path signature from its unitary development, 2024.

- [15] Shujian Liao, Hao Ni, Marc Sabate-Vidales, Lukasz Szpruch, Magnus Wiese, and Baoren Xiao. Sig-Wasserstein GANs for conditional time series generation. Mathematical Finance, 34(2), 2024.

- [16] Francis A. Longstaff and Eduardo S. Schwartz. Valuing american options by simulation: A simple least-squares approach. The Review of Financial Studies, 14(1):113–147, 2001.

- [17] Hang Lou, Siran Li, and Hao Ni. Path development network with finite-dimensional Lie group representation. arXiv:2204.00740, 2022.

- [18] Hang Lou, Siran Li, and Hao Ni. PCF-GAN: generating sequential data via the characteristic function of measures on the path space. Advances in Neural Information Processing Systems, 36, 2023.

- [19] Cristopher Salvi, Thomas Cass, James Foster, Terry Lyons, and Weixin Yang. The signature kernel is the solution of a goursat pde. SIAM Journal on Mathematics of Data Science, 3(3):873–899, January 2021.

- [20] Cristopher Salvi, Maud Lemercier, Chong Liu, Blanka Hovarth, Theodoros Damoulas, and Terry Lyons. Higher order kernel mean embeddings to capture filtrations of stochastic processes. Advances in Neural Information Processing Systems, 34:16635–16647, 2021.

- [21] T. Xu, L. K. Wenliang, M. Munn, and B. Acciaio. Cot-gan: Generating sequential data via causal optimal transport. Advances in Neural Information Processing Systems, 33:8798–8809, 2020.

- [22] Jinsung Yoon, Daniel Jarrett, and Mihaela Van der Schaar. Time-series generative adversarial networks. Advances in neural information processing systems, 32, 2019.

Appendix A Examples and Proofs

A.1 Examples related to extended weak convergence

Prediction processes

First let us give an explicit example for prediction processes of some simple filtered processes. Consider the two processes and , where

-

•

, and ;

-

•

for and is the coordinate process on ;

-

•

;

-

•

is the natural filtration generated by : and is the power set of ,

and

-

•

, and ;

-

•

for and is the coordinate process on ;

-

•

;

-

•

is the natural filtration generated by : and is the power set of .

We plot the sample paths of and in Fig. 4.

From the above, it is straightforward to check that the prediction process of is

where is the law of under ;

where () denotes the Dirac measure at ; and

Consequently, it holds that the law of satisfies

Similarly, the prediction process of is

where is the law of under ;

and

so that the law of reads

Test functions for extended weak convergence

For and filtered process on , the typical test functions for defining the extended weak convergence have the following form:

where are continuous bounded functions on the path space and . For instance, for the filtered processes and in the above example, we have , and by choosing , , and , in view of the facts that are the power set of (see the last paragraph), we obtain that for each ,

and therefore . On the other side, since are trivial -algebra, for the prediction process of we have

as ; and therefore

Clearly, as , we have , which shows that cannot converge to in the extended weak convergence according to Definition 2.1, although it is easy to see that the laws of converges to the law of in the weak topology.

Some important multi-periods optimisation problems

The following multi-periods optimisation problems are very important in financial and economic applications, whose value functions are, in general, discontinuous with respect to the weak convergence, but continuous in the extended weak topology.

Example A.1 (Optimal Stopping Problem).

Let be a continuous and bounded non-anticipative (i.e., for any and , the value of only depends on ) function. For each filtered process we set be the collection of all stopping times with respect to the filtration and similarly define ST for . Then the value function in the Optimal Stopping Problem (OSP) with the reward (in the context of mathematical finance, it is also called the price of American option) is defined by

If , then , whilst this continuity fails in the weak convergence: for the processes and considered as above (see Fig. 4) and the reward function , one has but

Indeed, since is a martingale with initial value , it is obvious that for any stopping time it always holds that which in turn implies that ; on the other hand, since the filtration of satisfies that (i.e., the agent already knows everything at day ), it is easy to check that is the optimal -stopping time for and consequently converges to .

Example A.2 (Utility Maximisation Problem).

Let be a continuous, bounded and concave utility function. For each filtered process we set be the collection of all predictable strategies (i.e., is -measurable for all ) with respect to the filtration and similarly define for . Then the value function in the utility maximisation Problem with the utility function is defined by

where is the stochastic integral. If , then , whilst this continuity fails in the weak convergence.

An example of HRPCF

We still consider the example mentioned before (see the paragraph Prediction processes and Fig. 4). In the previous discussions we have known that in the weak convergence (i.e., the laws converges to the law ), but cannot converge to in the extended weak convergence. Now we show that there exists an admissible pair such that

by an explicit calculation, which confirms that the HRPCFD does metrise the extended weak convergence and therefore reflect the differences of filtrations of stochastic processes.

Now we pick a linear operator 666 Recall that in the unitary representation of a path we actually always consider the time-augmented version , so here the domain of for real valued path is . which is given by , where denotes the imaginary unit in . Since the prediction process of is

where is the law of under ;

and

we can check that

and

which shows that the -valued process satisfies that

| (6) |

and

| (7) |

On the other hand, for every , we have

and

which provides that

and

Therefore, the -valued process satisfies that

| (8) |

and

| (9) |

By viewing as and only consider the imaginary part of the above two processes in (6), (7) and in (8), (9), we may without loss of generality assume that

and

Now, adding the additional time component to the above real valued paths, and choosing via

we can easily verify that

and

where denotes the matrix exponential on . From the above calculation, we can further derive that

because the matrix multiplication is non-commutative. Therefore,

which coincides with our observation that cannot converge to for the extended weak convergence.

A.2 Proof of Theorem 3.3

In this section we prove Theorem 3.3 in a more general setting.

Definition A.3.

For with , and a measure-valued path, we call

the high rank development of under .

Definition A.4.

For a probability measure on the measure-valued path space , the function

is called the high rank path characteristic function of (Abbreviation: HRPCF).

The next lemma is straightforward, but will be helpful for us to construct the characteristicity for laws of measure-valued stochastic processes.

Lemma A.5.

Let for some , Then, there exists an for , such that for any measure–valued path and for any , one has

Proof.

Given an , we define for via

| (10) |

which is obviously a linear mapping due to the linearity of .

For any –valued path , we know that its unitary feature is the unique solution (evaluated at time ) to the linear differential equation

On the other hand, let be a curve in defined by

where , is the unique solution to the linear differential equation

It is clear that satisfies that

Hence, by the uniqueness of the solution to the differential equation , and invoking that for all , we must have

Now it follows immediately that

∎

Theorem 3.3 follows immediately from the next lemma by inserting and for prediction processes and of filtered processes and , respectively.

Lemma A.6.

Let and be two probability measures on measure–valued path space (that is, ). Then if and only if for every admissible pair of unitary representations , it holds that

Proof.

Obviously we only need to show the “if” part.

Step 1: By hypothesis, for any admissible pair of unitary representations with and we have

which means that , where the pushforward measures and are probability measures on the –valued path space.

In fact, if we fix an arbitrary and an arbitrary , and let vary over all , we actually have the above equality for all , . Therefore, by applying the characteristicity of PCF of measures on finite dimensional vector space valued path spaces, see Theorem 2.5, we obtain that for any and any .

Step 2: Fix an and a sequence of operators . Let . By Lemma A.5 above, there exists an such that for any , one has

Now we take an arbitrary partition of the time interval . Since we have shown in Step 1 that , that is, the law of –valued stochastic process , under coincides with its law under , we indeed have that the distributions of their marginals at are same, that is,

Now, for each and , we pick arbitrary linear functions and continuous and bounded functions , and use them to define a function for such that for any matrix (recall that ) written in the form

it holds that

Obviously each function is continuous and bounded.

Let be the continuous and bounded function such that for every sequence . From the equality it follows that

which can be reformulated as

| (11) | ||||

where .

Step 3: It is a well known fact (see e.g. [6]) that the vector space generated by all real-valued linear functionals of unitary representations on the path space , namely

is a subalgebra in the space of continuous and bounded (real-valued) functions on which separates the points. Moreover, by picking to be the trivial representation (i.e., for all ) we see that for any path , . Therefore, by the Giles’ Theorem ([7, Theorem 9]) it follows that the set is dense in related to the so called strict topology777For the definition of the strict topology, see e.g. [7, Definition 8]..

Now, fix arbitrary continuous and bounded functions , . From the density of in

one can find a sequence of unitary representations , together with a sequence of

linear operators , with each such that for every it holds that

| (12) |

where the convergence happens in the strict topology. Furthermore, since every probability measure () belongs to the topological dual of equipped with the strict topology by the Giles’ theorem, invoking the relation (12) we actually obtain that for every ,

Then, as a consequence of the result (11) obtained in Step 2, we can apply the bounded convergence theorem to get that

| (13) |

On the other hand, by the Urysohn’s lemma, for any , any positive number , the indicator function can be pointwise approximated by a sequence of –valued continuous functions . Hence, by replacing the functions by in (A.2) and then letting , using the bounded convergence theorem we can derive that

or, equivalently,

| (14) |

where denotes the evaluation map of against the measure .

Step 4: By the very definition of weak topology on , its Borel –algebra is generated by the sets of the form that for and . Consequently, the Borel –algebra on the product space is generated by the measurable rectangles of the form that for and . From Eq. (14) we know that

for all such measurable rectangles. Since the above equation holds for any partition of and the laws of (continuous) stochastic processes are uniquely determined by their marginals on finitely many time points, we can conclude that in by a routine application of the monotone class theorem. ∎

Now, for filtered processes and , we note that the associated prediction processes and are stochastic processes taking values in which can be viewed as -valued random variable, which in turn implies that their laws and are elements in . Hence, inserting and into the above Lemma A.6 we can easily deduce Theorem 3.3.

A.3 Properties of HRPCFD

In this section we will mainly prove the properties recorded in section 3.3.

First let us prove the property of HRPCFD on the separation of laws of prediction processes. To achieve this we need the following useful continuity lemma.

Lemma A.7.

For any fixed , any fixed and , the mapping

is continuous for the operator norm topology on and the Hilbert–Schmidt norm topology on .

Proof.

For admissible pairs and from , by the definition of HRPCF we have

| (15) |

Let us first estimate the first integrand on the right hand side of (A.3). By [18, Proposition B.6] we know that for each measure–valued path , one has

where and are –valued paths. Since is piecewise linear, these –valued paths and are also piecewise linear, say, they are linear on time subintervals for . Then we indeed have

whence the estimates

| (16) |

Now we note that for each , we have

Recalling that for each –valued path , one has and , where and are the unique solutions to the linear ODEs

and

respectively, by the continuity of the flow of ODE (see e.g. [10, Theorem 3.15]), we obtain that for any ,

In particular, if , then for all we have . Then because and are unitary representations taking values in the compact group , by the dominated convergence theorem we have as for any . As a result, in view of (16) we obtain that

for all . Then, as is a unitary representation taking values in the compact group , by the dominated convergence theorem again we have

| (17) |

Next we turn to bound the second integrand in (A.3), namely Again, invoking that and are the unique solutions (evaluated at ) to the linear ODEs

and

respectively, by the continuity of the flow of ODE, we obtain that for each ,

Since takes values in the compact group , it is easy to see that for piecewise linear path it holds that , which implies that for any and for any ,

Again, since and are unitary features with values in compact group , by the dominated convergence theorem we must have

| (18) |

as long as . Now, combining (18), (17) and (A.3) we can conclude that

as long as , which is the desired continuity claim.

∎

Now we are able to prove the first property of HRPCFD.

Theorem A.8 (Separation of points).

Let be two distributions on measure–valued path space such that . Then there exists a pair of integers such that for any with full support and any with full support, one has

In particular, for filtered processes and , if they are not synonymous, then with and there exists a pair of integers such that for any with full support and any with full support, one has

Proof.

Thanks to Lemma A.6, if , then there must exist an admissible pair of unitary representations with and such that

Then, by the continuity result proved in Lemma A.7, there exists a such that for all and all with and , it holds that

Let and denote the ball centered at and with radius (with respect to the operator norms) respectively. Then if and have full supports, we have and which implies that

as claimed. ∎

The boundedness of HRPCFD is easy to show by using the same arguments as in the proof of [18, Lemma 3.5] for PCFD.

Lemma A.9.

Let be two distributions on measure–valued path space. Then for any given integers , for any and any , one has

Proof.

By the triangle inequality, we have

Since and takes values in such that , we indeed have

Similarly, it holds that . Combining all above together we can deduce that ∎

Just like the classical PCFD (cf. [18, Proposition B.10]) we can also show that the HRPCFD is a specific Maximum Mean Discrepancy (MMD). For the definition of MMD, we refer readers to [18, Definition B.9].

Proposition A.10.

For any , any and any , the HRPCFD with respect to and is an MMD with the kernel function given by

where denotes the concatenation operator on paths and denotes the reverse of the path .

Proof.

For , it is easy to deduce that

Moreover, note that

where we used the Fubini’s theorem in the last equality. Therefore we actually obtain that for the kernel

it holds that

which implies that is a MMD with the kernel function .

The last claim is obvious: for any , one has, due to the fact that every satisfies , that

where we used the multiplicative property of the unitary features for –valued paths and , see also [18, Lemma A.5]. ∎

Now we will construct a metric from HRPCFD which can characterise the extended weak convergence on precompact subset of FP.

Lemma A.11.

Suppose that is a double sequence of distributions with full supports. After a re-numeration we label them as a sequence such that each is a random admissibe pair in . Then the following defines a metric on :

Proof.

The symmetry and the triangle inequality are easy to check. We only need to show that if and only . The “if” part is trivial. Now suppose that holds but . Then by Theorem A.8 we know that there exists a pair of integers such that for any and any with full supports, it holds that . So, let us pick some such that , we must have , which implies that , a contradiction. Hence we obtain that the so–defined is really a metric. ∎

Theorem A.12.

Fix a sequence of random admissible pairs such that for every there exists a with and and their distributions and are fully supported. Let be the metric defined as in Lemma A.11 via this sequence .

-

1.

Let be a compact subset in the space FP of filtered processes equipped with the topology induced by extended weak convergence. Then, for every sequence of filtered processes and , we have

as .

-

2.

Let be a compact subset. Let be the space of all filtered processes taking values in . Then, for every sequence of filtered processes and , we have

as .

Proof.

-

1.

First suppose that for a sequence and . Clearly, for any sequence of piecewise linear measure-valued paths , and (which are linear on each subinterval , ) we have with respect to the product topology on implies that for each fixed unitary representation , the –valued paths converges to with respect to the total variation norm as . Then, for every fixed unitary representation , by the continuity of unitary feature map relative to the total variation norm (see e.g. [18, Proposition B.6]), we have in (relative to the Hilbert–Schmidt norm) as . Hence, we actually have shown that the function is continuous and bounded for the product topology on . Now, as means that weakly in as , we indeed have for all ,

that is, . This observation together with the boundedness of the HRPCFD (see Lemma A.9), allows us to apply the dominated convergence theorem to derive that for every one has

as . Consequently, we can conclude that as .

Conversely, suppose that is a sequence of filtered processes in and such that . Since is compact, there is a subsequence of (without loss of generality, assume this subsequence is the sequence itself) converging to a limit in the extended weak topology. From the previous argument we know that . Therefore, we actually obtain that . In view of Theorem A.8, the equality means that , i.e., and are synonymous. The above reasoning reveals that any accumulation point of the sequence in the extended weak convergence coincides with . As a consequence, we have in the extended weak topology as . -

2.

By [4, Theorem 1.7] the subspace is precompact in FP for the extended weak topology, if is compact. Hence the claim follows immediately from the result contained in the statement 1 with (the closure of with respect to the extended weak convergence).

∎

Appendix B Methodology and algorithm

B.1 Estimating the conditional probability measure

Input: - real data; - batch size; - learning rate for the regression module; - path feature dimension; - lie degree; ; - path length; - learning rate.

Input: - regression module; - data sampled from distribution ; - learning rate for the regression module; - path feature dimension; - Lie degrees; ; - path length.

B.2 HRPCF-GAN

In this section, we provide the mathematical formulation of HRPCF-GAN for conditional time series generation. Let denote a -valued time series of length with its distribution . Suppose that we have i.i.d. samples from . We are interested in generating synthetic future paths to approximate the conditional distribution of the future path given the past path . For ease of notations, let and denote the space of the past path and future path, respectively.

Conditional generator

One step generator , which maps to samples of the next time step via the following formula:

is the sequence-to-sequence embedding module to extract the key information of the path up to time and exhibits the autoregressive generator architecture. We denote by where the generator’s parameter.

We then apply one step generator in a rolling window basis to generate future time series of length . More specifically, , where we first set and for every ,

In the following, we summarise the training algorithm for HRPCF-GAN in Algorithm 3.

Input: - past path length; - total path length; - path feature dimension; - real data; - lie degree for EPCFD; - number of linear maps; ; - lie degree for EHRPCFD; - number of linear maps for EHRPCFD; ; - generator; - batch size; - noise dimension; frequency of regression module fine-tuning; , - generator and discriminator learning rates.

B.3 Hypothesis testing for stochastic processes

We provide the following two algorithms for training ERHPCFD for the permutation test and computing the test power/Type 1 error of the permutation test, respectively.

Input: - samples from distribution ; - samples from distribution ; - sample size of ; - sample size of ; - lie degree for EPCFD; - number of linear maps; ; - lie degree for EHRPCFD; - number of linear maps for EHRPCFD; ; - batch size; - learning rate; - number of iterations.

Input: - significance level; - # of experiments; - # of permutations; - samples from distribution ; - samples from distribution ; - sample size of ; - sample size of ; - test statistic function; - whether the null hypothesis is true or false ( if ; otherwise )

Appendix C Numerical results

Code

The code is written in Python 3.10.8 and Pytorch 1.11.0. We have attached the code for reproduction in supplementary files. The experiments were performed on a computational system running Ubuntu 22.04.2 LTS, comprising five Quadro RTX 8000 GPUs with 48GB of memory each. The experiments are run on single GPU and the training time ranges from 30 minutes to 4 hours.

C.1 Hypothesis testing

Description

The permutation test is a statistical method used to decide whether two measures are the same. The null hypothesis states whereas the alternative hypothesis . Given a test metric and sample data , from and respectively. We construct the following distribution

where and is the permutation group of elements. Given the significance level , we reject the null hypothesis if quantile of .

Methodology

For each , we sample the training dataset and optimize the set to maximize between the pair of measures, a detailed procedure can be found in Algorithm 4. Then, we sample two independent sets , and calculate the power and type-I error accordingly. We refer to Algorithm 5 for the computation of test metrics.

Implementation details

We provide the full details of the implementation of the numerical experiment in Section 5.1. Adopting the notation in Algorithm 4, we fix , , and , these values are chosen via hyper-parameter fine-tuning. The regression model consists of a 2-layer LSTM module. The model’s parameter is optimized using Adam optimizer with learning rates (for regression) and (for EHRPCFD).

Additional numerical results

We provide comprehensive tables for summarising the Type-I error and the computational time involved in Section 5.1.

| Developments | Signature MMDs | Classical MMDs | |||||||

|---|---|---|---|---|---|---|---|---|---|

| High Rank PCFD | PCFD | Linear | RBF | High Rank | Linear | RBF | |||

| 0.4 | |||||||||

| 0.425 | |||||||||

| 0.45 | |||||||||

| 0.475 | |||||||||

| 0.525 | |||||||||

| 0.55 | |||||||||

| 0.575 | |||||||||

| 0.6 | |||||||||

| Developments | Signature MMDs | Classical MMDs | |||||||

| High Rank PCFD | PCFD | Linear | RBF | High Rank | Linear | RBF | |||

| Inference time (seconds) | |||||||||

| Mini-batch size | Training time (seconds over 500 iterations) | ||||||||

| 1024 | |||||||||

C.2 Generative modeling

Datasets construction

(1) -dimensional fractional Brownian motion: we simulate samples using the publicly available Python package fbm. The total length of each sample is (counting a fixed initial point). The training and test data consists of two independent sampled sets of size . (2) Stock: we select 5 representative stocks in the U.S. market, namely, Apple, Lockheed Martin, J.P. Morgan, Amazon, and P& G, and collect the daily return data from 2010 to 2020. The data collection is done using the Python package yfinance. We then construct the dataset using a rolling-window basis with length (two weeks in real time) and stride . Finally, we split the dataset into training and test sets with a ratio of .

Baseline

We compare the performance of HRPCF-GAN with well-known models for time-series generation such as RCGAN [9] and TimeGAN [22]. Furthermore, we use PCFGAN [18] as a benchmarking model to showcase the significant improvement by considering the higher rank development as the discriminator. For fairness, we use the same generator structure (LSTM-based) for all these models.

Conditional Generator

The generator design is described in Section B.2. In particular, we choose and to be two independent 2-layer LSTM modules. The first module takes the past path and encodes the necessary information to the latent space. The final hidden and cell state will be used as the input for the second LSTM module and the latent noise vector to produce the output distribution of the next time step. Also, we use the auto-regressive to simulate the future path recursively.

Implementation details

The training procedure is described in Algorithm 3, we adopt the same notation in this section. For both datasets, we set and . We use the development layers on the unitary matrix [17] to calculate the PCFD distance, in particular, we fix , , , for the discriminator design, these are obtained via hyper-parameter tuning. The regression model consists of a 2-layer LSTM module. Finally, we use the ADAM optimizer [11], to train both the generator and discriminator with learning rates and respectively. We fine-tune the regression every 500 generator optimization iterations. To improve the training stability of GAN, we employed three techniques. Firstly, we applied a constant exponential decay rate of to the learning rate for every 500 generator training iterations. Secondly, we clipped the norm of gradients in both generator and discriminator to .

All benchmarking models are trained with 15000 training iterations. For HRPCF-GAN, we trained the vanilla PCF-GAN with 10000 iterations then we switched to HRPCF discriminator and trained the model for a further 5000 iterations.

Evaluation metrics

We list here the test metrics we used for generative model assessment.

-

•

Marginal score [15]: the average of Wasserstein distance of the marginal distribution between real and fake data across each dimension.

-

•

Auto-correlation score [15]: the norm of the difference in the ACF between real and fake data

where is the empirical auto-correlation estimator of and .

-

•

Cross-correlation score [15]: the norm of the difference in the correlation between real and fake data across each feature dimension.

where is the empirical correlation estimator.

-

•

Discriminative score [22]: we train a post-hoc classifier to distinguish real data from fake data. Lower the score (absolute difference between classification accuracy and 0.5), meaning inability to classify, indicate better performance of the generative model.

-

•

Predictive score [22]: we train a sequence-to-sequence model to predict the latter part of a time series given the first part, using generated data and real data, resp. The trained models are then tested on the real data resp. The lower loss (|TSTR-TRTR|) means the better resemblance of synthetic data to real data for the predictive task.

-

•

Sig score [15]: by embedding the time series to the signature space, we can approximate the distance by the norm of the signature of the real and fake data.

where Sig denotes the signature transform of a path.

-

•

Conditional expectation score: we estimate the conditional expectation of the future path on the fake measure via Monte Carlo and compute the averaged pairwise norm between real data.

-

•

Outgoing Nearest Neighbour Distance score [13]: the ONND calculates for each example of real data the distance between the nearest generated data. This score tests the model’s capability to capture the diversity of the target distribution.

-

•

American put option score: we use Least-Square Monte Carlo method [16] to price an at-the-money American put option using both real and generated data. We set the strike date days and risk-free rate . The score is computed as the average of differences of the estimated price across each stock.

For each test metric, a lower value indicates better model performance. We provide the results on the additional metrics in Table 5.

| Dataset | Test Metrics | RCGAN | TimeGAN | PCFGAN | HRPCF-GAN |

|---|---|---|---|---|---|

| Marginal | .010.000 | .041.000 | .007.000 | .005.000 | |

| fBM | Predictive | .456.004 | .686.013 | .474.003 | .446.002 |

| ONND | .622.002 | .632.002 | .654.002 | .622.002 | |

| Marginal (1+) | 1.181.144 | .626.137 | .476.146 | .272.122 | |

| Stock | Predictive | .010.000 | .009.000 | .009.000 | .009.000 |

| ONND | .017.001 | .017.000 | .016.000 | .016.000 |