Nonparametric estimation of FBSDEs with random terminal time

Shaolin Ji Chenyao Yu Linlin Zhu

Email: jsl@sdu.edu.cn Email: yucy@mail.sdu.edu.cn Corresponding author. Email: 201611343@mail.sdu.edu.cn

Institute for Financial Studies,

Shandong University, Jinan, Shandong 250100, PR China

Abstract. This paper investigates the nonparametric estimation of the functional coefficients of the FBSDEs with random terminal time, including the local constant and local linear estimators. We provide complete two-dimensional asymptotics in both the time span and the sampling interval, allowing for the precise characterization of their distribution. Moreover, the empirical likelihood (EL) method to construct the data-driven confidence intervals for these estimators is provided.

Some numerical simulations investigate the finite-sample properties of the estimators and compare the performance of the EL method and the conventional method in constructing confidence intervals based on asymptotic normality.

Nonlinear BSDEs were introduced by

Pardoux and Peng [10]. It was shown in [12] that coupled with a forward SDE, such BSDEs give a probabilistic interpretation for systems of quasilinear parabolic and elliptic partial differential equations (PDEs), which generalized the classical Feynman-Kac formula for linear parabolic and elliptic PDEs. Later, many researchers developed the theory of FBSDEs and their applications. In mathematical finance, FBSDEs can be used in the theory of stochastic differential utility and the theory of contingent claim evaluation for a large investor. The existence and uniqueness of the solutions to some kinds of FBSDEs are closely linked to optimal stochastic control problems. In many applications, there is a lack of prior information about the structure of the model. Therefore, it becomes important to identify and estimate the parameters and functionals of the process with discretely observed data. In the past few decades, there has been a thorough study on the nonparametric estimation of the (jump-) diffusion processes and stochastic volatility models (see [1], [2], [3], [4], [6], [7], [8], [13], [14], [16], [17]). However, as one of the important tools used to describe the stochastic process in many fields, research on the statistical inference of BSDEs is rarely performed.

In this paper, we consider the nonparametric estimation of the forward-backward stochastic differential equations (FBSDEs) with random terminal time.

Consider the following FBSDE,

(1.1)

where is a -dimensional standard Brownian motion defined on a complete filtered probability space . is the natural filtration of this Brownian motion such that contains all -null elements of . is an -stopping time with values in .

take values in , respectively.

Assume the specific form of the functional coefficients , , and is unknown, but only the process and are observed at discrete times. Based on these observations, we are interested in establishing the point-wise estimators of the functional coefficients and the term .

There are only a few studies on the statistical inference of BSDEs.

Su and Lin [15] proposed the local constant estimator of and the least square estimator of the unknown parameter in the generator for a linear FBSDE with fixed terminal time. Chen and Lin [5] considered a coupled Markovian FBSDE with fixed terminal time. They constructed the local linear estimators of the functional coefficients and and obtained the asymptotic properties of these estimators.

In these articles, some assumptions are strict, such as some stationary assumptions. Moreover, their estimators are based on the relationship between FBSDEs with deterministic terminal time and quasi-linear parabolic PDEs, in which the solutions and the functional coefficients of the FBSDEs are all deterministic functions of and . However, there is insufficient information to estimate the bivariate functions with only one observed trajectory.

It is well known that BSDEs with random terminal time are connected with quasi-linear elliptic PDEs. The solutions to these BSDEs are deterministic functions of , i.e., they depend on the current state of , not on time. Applying this property, we construct the local constant estimators and local linear estimators of the functional coefficients and for FBSDEs with random terminal time.

The asymptotic properties of the estimators are obtained under mild conditions (the process and need not be stationary).

The local polynomial estimator, the double-smoothing estimator, can be easily generalized.

Given these estimators, the common confidence intervals can be obtained based on their asymptotic normality, provided consistent estimators of the asymptotic variances are available. However, this type of confidence interval is always symmetric, and the estimated variances usually have large biases. We apply the empirical likelihood in conjunction with the local constant estimators to construct the data-driven confidence intervals that can account for possible skewness of the estimators and avoid imprecise variance estimation. We focus on local constant smoothing, and the extensions to the local linear or local polynomial estimators are straightforward.

This paper is organized as follows. The models and some preliminaries are introduced in Section . The estimators and their asymptotic properties are presented in Section .

Section introduces the EL method to construct the point-wise confidence interval. The proofs are given in Section .

Some numerical examples are shown in Section .

2 Model setup and preliminaries

Denote

, where , the space of -valued progressively measurable processes such that

and ;

Further, define

Let denote the solution of the following forward SDE:

(2.1)

where , , are globally Lipschitz and twice continuously differentiable.

2.1 BSDEs with infinite horizon

Consider the infinite horizon BSDE which is defined as follows,

(2.2)

where is a continuous function, the process is defined as .

Assumption 2.1

There exists some constants such that

Moreover, for some , and all ,

According to Theorem in [11],

under Assumption 2.1, the BSDE has a unique solution which belongs to .

Consider a semilinear elliptic PDE in which is of the form

(2.3)

where

is the infinitesimal generator of the Markov process .

Let Assumption 2.1 hold.

If is a classical solution of such that

Then for each , is the unique solution of the BSDE

.

2.2 BSDEs with finite random terminal time

Let be an open bounded subset of with boundary of class . For each , define

the stopping time

.

Assume that , and for all , the set is closed.

Consider the following BSDE

(2.4)

where , is continuous and satisfies Assumption 2.1. Assume that for some , .

Then, the BSDE has a unique solution in .

Consider the PDE with Dirichlet boundary condition which is of the form

(2.7)

Lemma 2.3

Let Assumption 2.1 hold.

If has a classical solution ,

then is the unique solution of the BSDE .

Remark 2.4

The conditions to guarantee a unique solution of the elliptic equation can be referred to Theorem 4.1 in [12].

3 Nonparametric estimation of the coefficients

In this section, we will construct the nonparametric estimators of and in the models and . We consider the one-dimensional case for simplicity, and similar results can be generalized in multi-dimensional cases under a more complex proof.

Assume is the range of the process and in the two models, where .

In the following, assume that and both have a unique solution and Assumption 2.1 holds.

Then, the solutions of the above BSDEs could be represented as deterministic functions of . With this conclusion, we denote and as and , respectively.

Note that for the diffusion process satisfying and a smooth function , the conditional expected increment can be expressed as

(3.1)

Setting and in , we have

(3.2)

and

(3.3)

respectively for both and .

Assume the processes and in and are observed at in the time interval with and , and the observations are equispaced. Then,

, are the observations, where .

Based on the infinitesimal conditional moment restriction (3.2) and (3.3), the common nonparametric regression methods, such as local constant regression, local polynomial regression can be exploited to estimate and at every spatial point .

3.1 Nonparametric kernel estimation of the generator

3.1.1 Locally constant estimator

The locally constant estimator of for and is defined as follows,

(3.4)

where , .

Let

where

with

To give the asymptotic property of the estimator, we make the following assumptions.

Assumption 3.1

The kernel function is a bounded, twice continuously differentiable, symmetric function with a compact support and for which

, .

Define , .

These conditions can be satisfied by many kernel functions, including the Epanechnikov kernel , the Quartic kernel , where is the indicator function.

Assumption 3.2

The process is recurrent, i.e., the scale function of

where is a generic fixed number belonging to , satisfies

Intuitively, recurrence ensures that the Markov process could visit every spatial point infinite times with probability one when . The recurrence-related concepts and their applications for statistical inference of stochastic processes can be found in [1], [2]. This condition does not imply the existence of a time-invariant distribution for , therefore, nonstationary is allowed.

To illustrate the asymptotic properties of the estimators, we apply the local time of the Markov process defined in [1]. It measures the amount of calendar time spent by the process in the neighborhood of . For a recurrent diffusion process, diverges as at every spatial point .

In this paper, of the Markov process in and need to satisfy the following Assumption.

Assumption 3.3

There exits such that , where .

for some nonrandom sequence .

Assumption 3.4

Given and such that

(i) . .

, where .

(ii) , where .

Note that and converge only if

. As we all know, for a recurrent process, we have as at each , does not diverge for the transient process. Therefore, if the process is recurrent, the local estimator of the generator for the infinite horizon BSDE is consistent. This does not apply to the BSDE .

3.2 Nonparametric kernel estimation of

3.2.1 Locally constant estimator

The locally constant estimator for is given by

(3.6)

where

Write

where

with

Assumption 3.8

Given and such that

(i) . .

, where .

(ii) , where .

(iii) .

To ensure the consistency of and , we only need and , we do not need or . i.e., and could be consistent as long as tends to sufficiently fastly relative to , and the process need not be recurrent. So these estimators can be applied to both the infinite horizon BSDE and the BSDE .

This section investigates the empirical likelihood method in constructing the data-driven point-wise confidence intervals of and for the two types of FBSDEs.

4.1 Confidence interval for

Denote

where is the candidate value of the target quantity .

Define

(4.1)

and

(4.2)

The following theorem describes the asymptotic properties of which helps to construct the confidence interval of .

as , where is fixed and is the chi-squared distribution with degree of freedom and non-central parameter .

Then the EL confidence interval for is defined as

where is the inverse cumulative distribution function for the

distribution evaluated at .

Remark 4.2

(i) Here we focus on local constant smoothing, although the extensions to the local linear (polynomial) are entirely straightforward.

(ii) can be calculated easily.

Using Lagrange multipliers, the constrained optimization problem is solved by

(4.3)

where satisfies

(4.4)

Then, given , we can solve numerically, and then compute

.

4.2 Confidence interval for

The point-wise EL confidence interval for can be constructed in a similar way.

Denote

and,

(4.5)

(4.6)

The following theorem describes the asymptotic properties of which helps to construct the confidence interval of .

Proof of Theorem 3.9.

Applying Lemma 5.2 and 5.5, we have,

uniformly in as and .

Then, can be obtained. For the second part , we analyse the numerator (denoted as ) first, define a continuous martingale such that

In this section, we investigate the finite-sample performance of the estimators for two models by the following measures:

where is the estimated function. represents the -th Monte Carlo replication, . are chosen uniformly to cover the

range of sample path of .

We use the Epanechnikov kernel and the bandwidth is chosen applying the cross-validation rule.

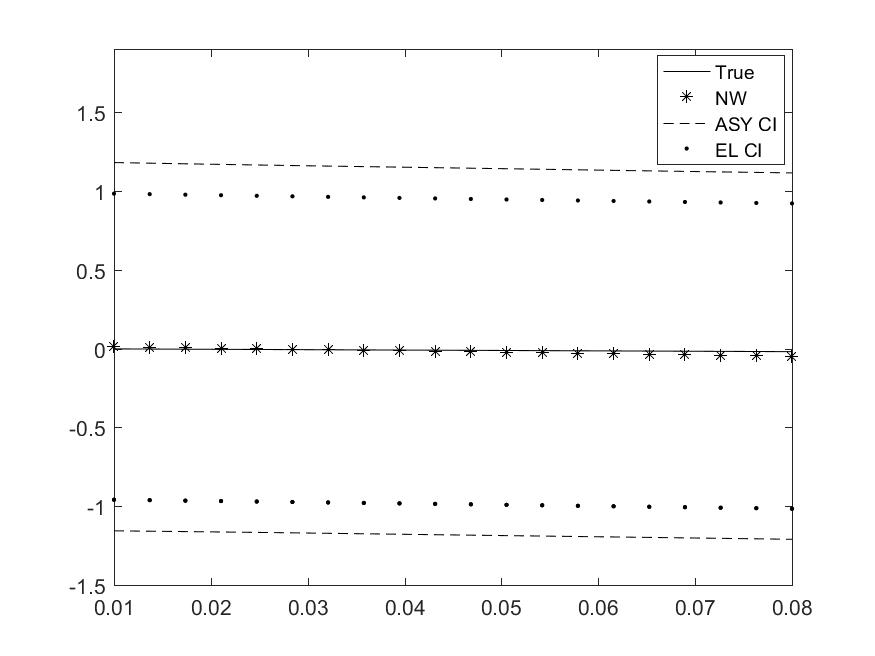

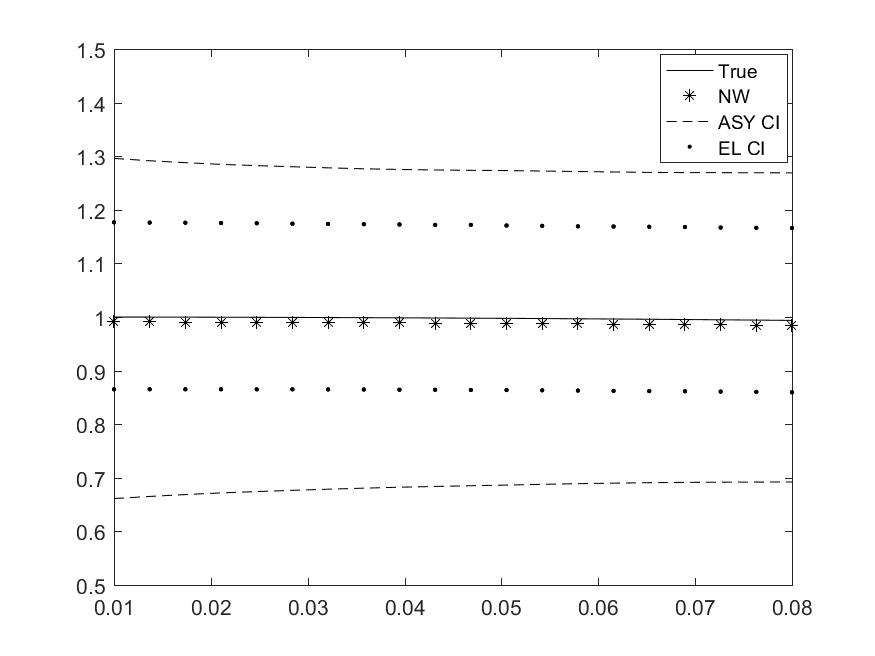

Example 6.1 ( is recurrent)

Consider an infinite horizon FBSDE,

(6.3)

The solution to is , . The true estimated functions are and .

The parameters we take are , .

Tables - report the MAE and MSE of the local constant and linear estimators for and given the estimated points with different observation time and . Figures and report the 95% confidence

intervals for these estimators, based on the common method using the asymptotic normality of the estimators and the empirical likelihood method.

Table 1: MAE and MSE of the estimators for

MAE

NW

0.129

0.134

0.123

LL

0.192

0.293

0.192

MSE

NW

2.466

2.450

2.171

LL

5.420

12.498

5.476

Table 2: MAE and MSE of the estimators for

MAE

NW

0.200

0.085

0.094

LL

0.037

0.081

0.031

MSE

NW

4.026

0.723

0.885

LL

0.140

0.653

0.100

(a) Confidence interval of

(b) Confidence interval of

Figure 1: The solid lines represent the true values, the ’*’ lines represent the local constant estimators, the ’–’ dotted lines represent the confidence intervals based on the common method using the asymptotic normality of the estimator, the ’’ dotted lines represent the confidence intervals applying the empirical likelihood method.

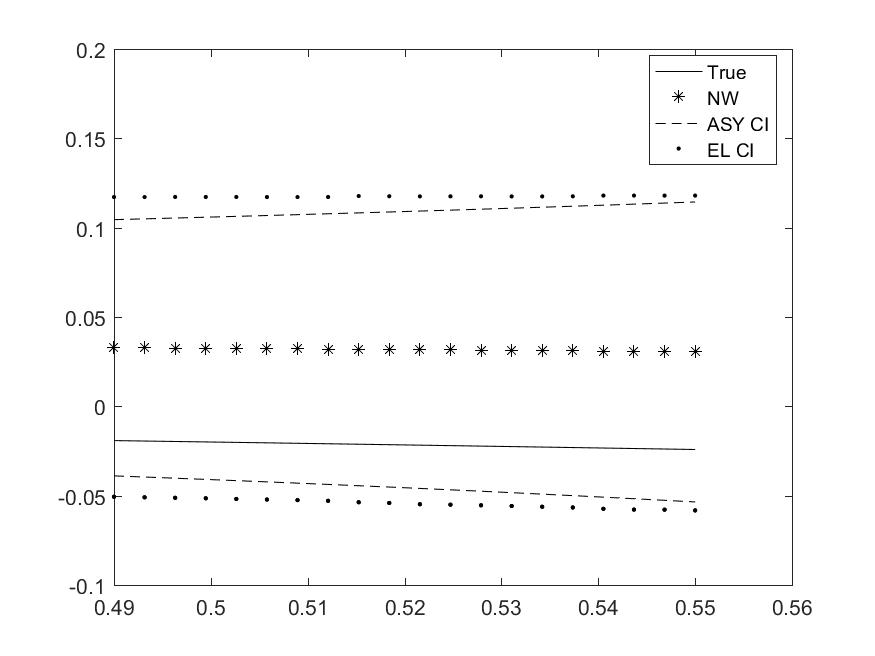

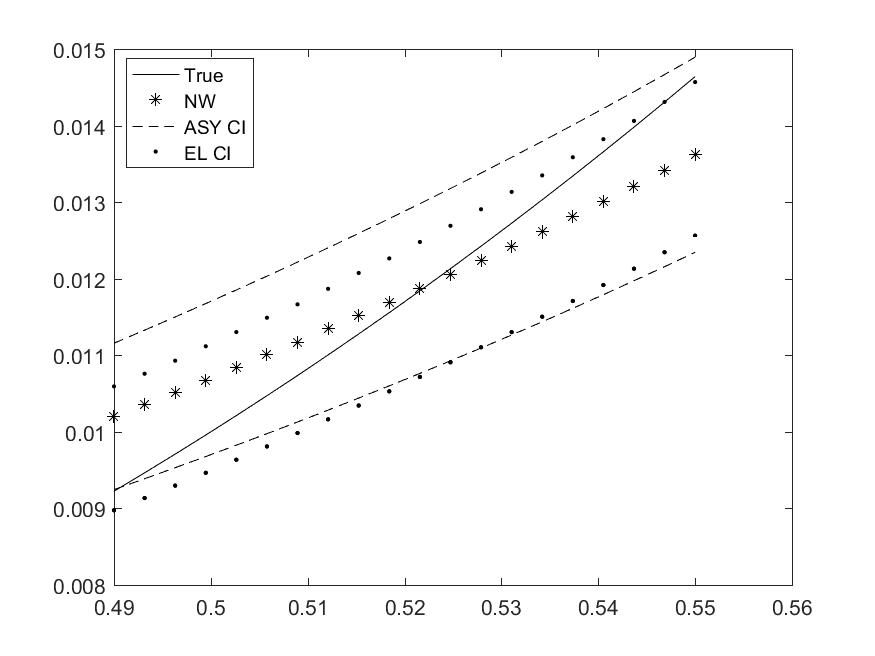

Example 6.2

Consider an infinite horizon FBSDE,

(6.6)

The solution to is , . We aim to estimate and .

.

Tables - report the MAE and MSE of the local constant and linear estimators for and given the estimated points with different observation time interval and . Figures reports the 95% confidence intervals based on the two methods.

Table 3: MAE and MSE of the estimators for

MAE

NW

0.533

0.482

0.533

LL

0.386

0.306

0.279

MSE

NW

0.028

0.023

0.028

LL

0.016

0.011

0.010

Table 4: MAE and MSE of the estimators for

MAE

NW

0.532

0.630

0.529

LL

0.201

0.182

0.139

MSE

NW

3.776

5.370

3.716

LL

0.533

0.342

0.246

(a) Confidence interval of

(b) Confidence interval of

Figure 2: The solid lines represent the true values, the ’*’ lines represent the local constant estimators, the ’–’ dotted lines represent the confidence intervals based on the common method using the asymptotic normality of the estimator, the ’’ dotted lines represent the confidence intervals applying the empirical likelihood method.

The above simulations show that the estimators behave better as the time span increases and the observation interval decreases. The local linear estimators have a better performance because their biases do not depend on the first derivative of the corresponding function. Moreover, the empirical likelihood method works well at most cases.

References

[1]Aït-Sahalia, Y., & Park, J. Y. (2016). Bandwidth selection and asymptotic properties of local nonparametric estimators in possibly nonstationary continuous-time models. Journal of Econometrics, 192(1), 119-138.

[2]Bandi, F. M., & Phillips, P. C. (2003). Fully nonparametric estimation of scalar diffusion models. Econometrica, 71(1), 241-283.

[3]Bandi, F. M., & Moloche, G. (2018). On the functional estimation of multivariate diffusion processes. Econometric Theory, 34(4), 896-946.

[4]Bandi, F. M., & Ren, R. (2018). Nonparametric stochastic volatility. Econometric Theory, 34(6), 1207-1255.

[5]Chen, X., & Lin, L. (2010). Nonparametric estimation for FBSDEs models with applications in finance. Communications in Statistics-Theory and Methods, 39(14), 2492-2514.

[6]Fan, J., & Zhang, C. (2003). A reexamination of diffusion estimators with applications to financial model validation. Journal of the American Statistical Association, 98(461), 118-134.

[7]Florens-Zmirou, D. (1993). On estimating the diffusion coefficient from discrete observations. Journal of applied probability, 30(4), 790-804.

[8]Jacod, J. (2000). Non-parametric Kernel Estimation of the Coefficient of a Diffusion. Scandinavian Journal of Statistics, 27(1), 83-96.

[9]Kim, J., & Park, J. Y. (2017). Asymptotics for recurrent diffusions with application to high frequency regression. Journal of Econometrics, 196(1), 37-54.

[10]Pardoux, E., & Peng, S. (1990). Adapted solution of a backward stochastic differential equation. Systems & Control Letters, 14(1), 55-61.

[11]Pardoux, E. (1998). Backward stochastic differential equations and viscosity solutions of systems of semilinear parabolic and elliptic PDEs of second order. In Stochastic Analysis and Related Topics VI (pp. 79-127). Birkhuser, Boston, MA.

[12]Peng, S. (1991). Probabilistic interpretation for systems of quasilinear parabolic partial differential equations. Stochastics and stochastics reports (Print), 37(1-2), 61-74.

[13]Stanton, R. (1997). A nonparametric model of term structure dynamics and the market price of interest rate risk. The Journal of Finance, 52(5), 1973-2002.

[14]Song, Y., & Wang, H. (2018). Central limit theorems of local polynomial threshold estimator for diffusion processes with jumps. Scandinavian Journal of Statistics, 45(3), 644-681.

[15]Su, Y., & Lin, L. (2009). Semi-parametric estimation for forward-backward stochastic differential equations. Communications in Statistics-Theory and Methods, 38(11), 1759-1775.

[16]Xu, K. L.(2009). Empirical likelihood-based inference for nonparametric recurrent diffusions. Journal of Econometrics, 153(1), 65-82.

[17]Xu, K. L. (2010). Reweighted functional estimation of diffusion models. Econometric Theory, 541-563.