Adaptive Optimal Market Making Strategies with Inventory Liquidation Cost111A preprint of this paper was distributed under the title of “Market Making with Stochastic Liquidity Demand: Simultaneous Order Arrival and Price Change Forecasts”. The present paper extends the results in the referred preprint, which will remain as an unpublished manuscript.

Jonathan Chávez-Casillas, José E. Figueroa-López, Chuyi Yu, and Yi Zhang

Department of Mathematics and Applied Mathematical Sciences, University of Rhode Island, USA (jchavezc@uri.edu).Department of Statistics and Data Science, Washington University in St. Louis, St. Louis, MO 63130, USA (figueroa-lopez@wustl.edu). Research supported in part by the NSF Grants: DMS-2015323, DMS-1613016.Department of Mathematics, Washington University in St. Louis, St. Louis, MO 63130, USA (chuyi@wustl.edu).Department of Statistics, UIUC, IL, USA (yiz19@illinois.edu).

Abstract

A novel high-frequency market-making approach in discrete time is proposed that admits closed-form solutions. By taking advantage of demand functions that are linear in the quoted bid and ask spreads with random coefficients, we model the variability of the partial filling of limit orders posted in a limit order book (LOB). As a result, we uncover new patterns as to how the demand’s randomness affects the optimal placement strategy. We also allow the price process to follow general dynamics without any Brownian or martingale assumption as is commonly adopted in the literature. The most important feature of our optimal placement strategy is that it can react or adapt to the behavior of market orders online. Using LOB data, we train our model and reproduce the anticipated final profit and loss of the optimal strategy on a given testing date using the actual flow of orders in the LOB. Our adaptive optimal strategies outperform the non-adaptive strategy and those that quote limit orders at a fixed distance from the midprice.

1 Introduction

1.1 Overview

In a financial market, a market maker (MM) provides liquidity to the market by repeatedly placing bid and ask orders into the market and profiting from the bid-ask spread of her orders. The literature of market making is extensive (see, e.g., the monographs of Cartea et al. (2015) and Guéant (2016) for references in the subject). In Subsection 1.2 below, we mention a few important works in addition to those more closely related to our model, which are reviewed through this part.

In the context of a Limit Order Book based market, we consider an intraday high-frequency MM who quotes both bid and ask limit orders (LO) at some prespecified discrete times and liquidates her inventory at the end of the trading period. As is often assumed in the literature, the terminal liquidation cost or price impact, originated from the use of a market order, is modeled as , with and respectively denoting the final fundamental stock price and the MM’s inventory. Here, is a constant ‘penalization’ parameter. We aim to maximize the final Profit and Loss (PnL), , at the end of the trading period , where is the MM’s final wealth. Her wealth and inventory trajectory are determined by the prices of her quotes and the number of shares that are filled or lifted from her orders at these prices.

Modeling the number of lifted shares between consecutive actions is a key element of our framework. In continuous-time control problems, a common approach is to model the probability with which an incoming market order (MO) can lift one share of the MM’s LO in the book (known as ‘lifting probability’). This approach, rooted in the seminal work of Ho & Stoll (1981), was popularized by the work of Avellaneda & Stoikov (2008) and later on by other important works including Guéant et al. (2013), Cartea et al. (2014), among others.

For instance, in the seminal work of Cartea & Jaimungal (2015), it is assumed that MOs arrive according to a Poisson process and the lifting probability is modeled as the exponential of the negative distance of the MM’s quote from the fundamental price times a constant.

An alternative approach

is to directly model the number of lifted shares between actions via a liquidity demand function. For instance, in their work on price pressures, Hendershott & Menkveld (2014) assume that the liquidity demand is normally distributed with a mean parameter that is linear in the bid and ask quoted prices and constant variance. Adrian et al. (2020) propose a demand function that decreases linearly with the distance of the quotes from a reference price, though their demand function is further restricted to be deterministic. We refer the reader to Remark 4 below for some further discussion about possible connections between the lifting probabilities- and the demand function-based approaches.

Our work extends existing models of high-frequency market-making in several ways. As in Adrian et al. (2020),

we assume the demand to be linear in the spreads when modeling the number of filled shares from the MM’s limit orders. However, in our case, the demand is not deterministic but stochastic. This means that the actual number of shares bought or sold varies over time, even if the distances of quotes from the reference stock price stay the same. The resulting optimal placement strategy does not boil down to simply replacing the constant demand slope and reservation price in the optimal strategy obtained in Adrian et al. (2020) with their respective average values, but also depends on their ‘second-order’ information and their mutual correlation. The proposed randomization not only allows for greater flexibility and better fit to empirically observed order flows, but also uncovers novel properties of the resulting optimal placement strategies. For instance, it is known from Adrian et al. (2020) that, under a constant demand slope, the required inventory adjustment in the optimal placement at any given time decreases with the size of the slope. We show that the variance of the slope further reduces the strength of this adjustment. This implies that assets with more volatile demand profiles require less strict inventory adjustments. We also find that the optimal placement spreads (i.e., the distances between the optimal bid and ask prices and the fundamental price) increase with the correlation between the demand slope and investors’ reservation price.

Another distinguishing feature of our study is that we allow a general reference stock price process without assuming that its dynamics follow that of a martingale or some kind of parametric specification (e.g., a Brownian Itô semimartingale). We obtain a parsimonious formula that describes how the investor should adjust online her LO placements based on her ongoing forecasts of future asset prices. Intuitively, if the MM expects future price changes to be negative, she will reduce the ask spread and increase the bid spread, proportionally to the expected price change. The proportionality constant depends on the model parameters in a non-trivial way, which we characterize precisely. This feature could also enable the investor to take advantage of sophisticated time series or machine learning-based forecast procedures for asset prices and incorporate them into the intraday market-making process.

One of the key factors that affects the performance of any placement strategy is the arrival intensity of MOs on either side of the book. A successful placement strategy should incorporate, in an online manner, current information about the intensity level of MOs or about imbalances in the likelihood of buying and selling MOs. In other words, it is desirable that the placement strategy adapts to the local behavior of MOs. In many works, the intensity of MOs is fixed a priori as a deterministic function of time.

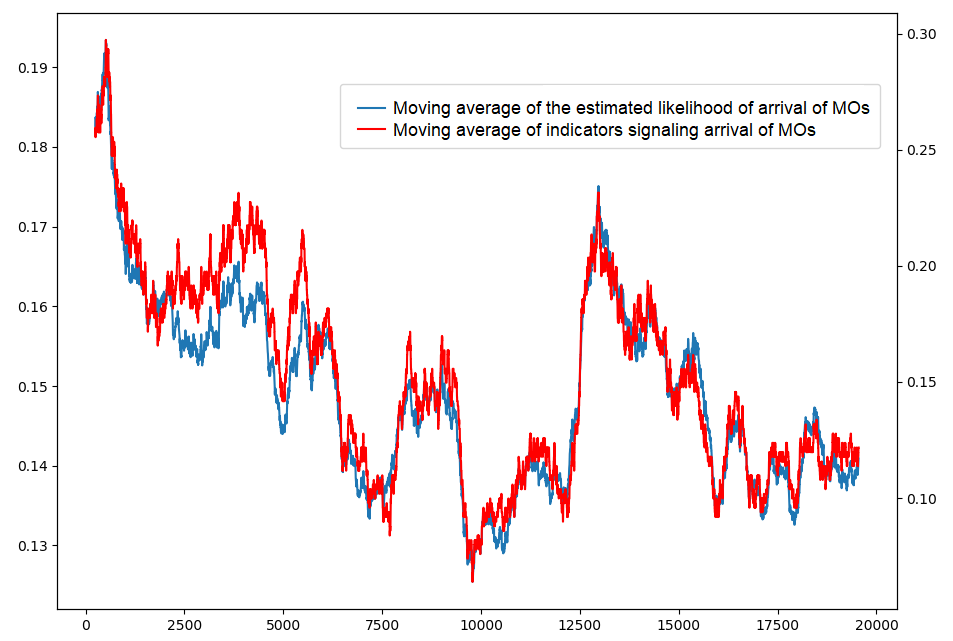

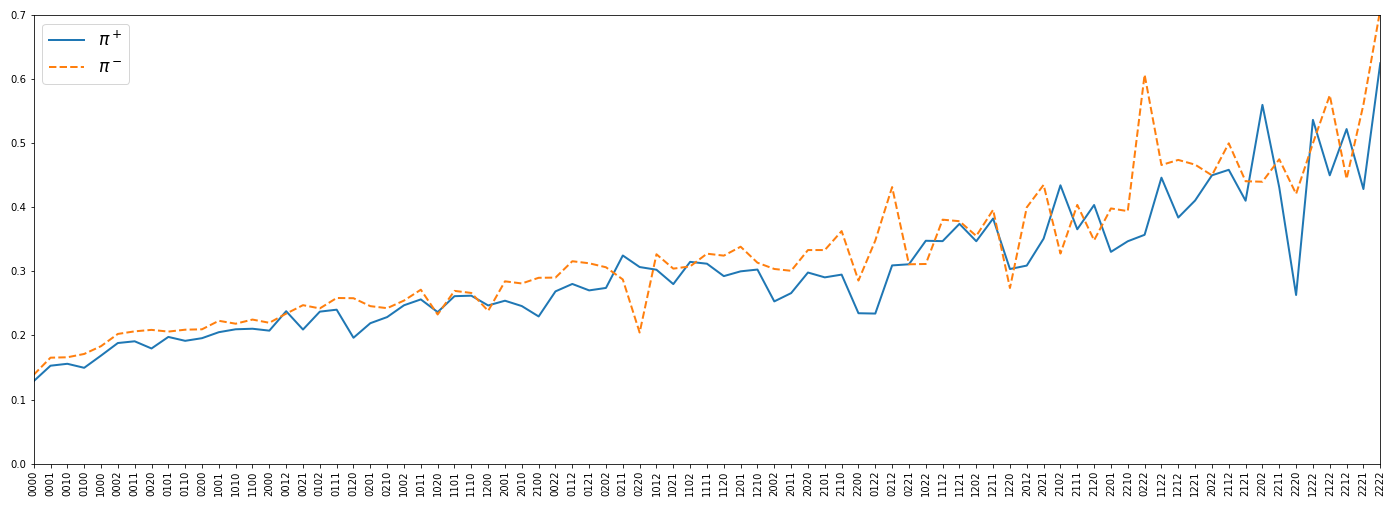

In reality, the intensity of MO is highly random and ‘rough’ as indicated by Fig. 1 below, where the averages of the indicators signaling the arrivals of buy MOs in a rolling window are plotted. However, as shown by the same figure, the intensity’s level can be tracked or predicted quite well in an adaptive or online manner (see Subsection 3.1.1 for details as to how to perform this prediction) and it would be desirable that the optimal strategy incorporates this information online.

Figure 1: Moving average of adaptive arrival probabilities of buy MO and the moving average of the indicators signaling arrival of MOs in consecutive intervals of 1 second based on LOB MSFT data on July 11th, 2019. The window size of the rolling moving average is 500. Note that the scale for the blue (red) curve is shown on the left (right) side of the figure.

By construction, it would seem that adaptive placement strategies are not feasible since the dynamic programming problem to find them is solved in a backward manner in time, which contradicts the direction of a natural learning process that proceeds forward in time. However, in this work, we offer a natural approach to resolve this riddle. Essentially, we propose to create a ‘catalog’ of optimal strategies depending not only on the current asset price and inventory level as well as future price forecasts but also on the recent history of MOs arrivals. In some figurative sense, we create parallel ‘universes’, one for each possible combination or scenario of past MOs events, and solve the optimal placement in each of those universes. We do this by making the conditional probabilities of arrivals of MOs dependent on the recent history of MOs. When implementing the placements strategy, the MM observes the recent history or combinations of MOs to determine in which ‘universe’ or scenario she is in, and places her LOs accordingly using the catalog of optimal strategies.

To put our proposed approach to the test, we implement our optimal placement strategy using actual LOB data. Specifically, for a given testing day, we start calibrating the model parameters using LOB data of the past few days and then compute, backward in time, the optimal placement strategy for each possible scenario of consecutive MOs. Next, we roll forward our optimal placement strategy using the actual LOB events of the testing day to determine in an online manner the scenario we are at and choose the optimal placements accordingly. We then compute the MM’s cash flows and inventory changes using the actual flow of MOs and the LOB state. At the end of the trading period, the MM submits a MO to liquidate its final inventory and determine the actual cost taking into account the state of the LOB. We repeat this procedure for each day of a 1-year time span. We find that our optimal placement yields, on average, larger revenue compared to those where the intensity of MO is assumed to be deterministic (time-dependent). Our empirical analysis also lends strong support to demand stochasticity: the slope coefficient has a standard deviation that is about 200% larger than the average demand level, and a correlation of about 20% with the investors’ reservation price. Moreover, using real LOB data we estimate the optimal placement strategy based on a simple one-step ahead price process forecast and compare it to the one that presumes a martingale price evolution.

1.2 Other relevant works

Optimal market making problems have a long history. In this part we mention a few important works that have not previously been discussed. Early contributions include those of Bradfield (1979), who analyze the increasing price variability induced by strategies that target a flat end-of-day inventory level, and O’Hara & Oldfield (1986), who consider a repeated optimal market making problem, in which each day consists of several trading periods, and the market maker maximizes utility over an infinite number of trading days while facing end-of-day inventory costs. More recently, Guilbaud & Phan (2013) studied the performance of a MM submitting buy/sell LOs at the best two bid and ask levels, while Guilbaud & Phan (2015) also considered agents that can submit market orders. Both of these works assume a constant spread of one tick (the so-called large-tick stocks) and price dynamics that move 1 tick at a time. Other works in the same vein include Fodra & Phan (2015) and Fodra & Phan (2015). In all these works, there is no partial filling and the MM’s LOs are filled in its totality when they are lifted.

Stochastic demand functions of different type have been considered in other works. As mentioned above, both Cartea & Jaimungal (2015) and Cartea et al. (2014) modeled the demand during a given time interval via filling probabilities, which depend on the distance between the quotes and the fundamental price. While in the first of those two works, the features of these probabilities are assumed to be deterministic, in the second work, those are assumed to be stochastic. As explained in Remark 4 below, there is a possible connection between the linear demand assumption adopted in this work and the fill probabilities approach, but, in general, the two models are not equivalent. It is worth mentioning that liquidity models with stochastic features have also been considered in other problems of algorithmic trading. For instance, Barger & Lorig (2018) and Becherer et al. (2018) both assume stochastic price impact of trades in optimal liquidation problems.

More recent works in the area have also incorporated other model features such as price impact (Cartea et al. (2014), Barger & Lorig (2018)), model ambiguity (Cartea & Jaimungal (2015), Nyström et al. (2014)), and latency (Cartea et al. (2021), Gao & Wang (2020)). More recently, Bergault & Guéant (2021) introduce a different modeling approach to incorporate different transaction sizes and the possibility for the MM to respond to requests with different sizes using marked point processes.

1.3 Outline of the paper

The rest of the paper is organized as follows. In Section 2, we present the model setup and our assumptions together with the Bellman equation for our problem and its explicit solutions. In Section 3, we assess the performance of our market-making strategy against real LOB data. We finish with a conclusion section. We defer the proofs to an appendix section.

2 A Finite-Horizon Optimal Control Problem for a Market Maker

In this section,

we introduce the model along with the relevant notation and its assumptions. Then, by using the Dynamic Programming Principle (DPP), we propose an adaptive trading strategy and by using the verification theorem, it is shown that, indeed, the solution is optimal. Finally, its admissibility is investigated. All the proofs of this section will be deferred to Appendix A.

2.1 The Model and its Assumptions

We assume that a high-frequency (HF) Market Maker (MM) places simultaneously buy and sell LOs at some preset discrete times , where and hereafter represents the terminal time of the trading. All the random variables used in the model are defined on the same probability space equipped with an information filtration , where . For , let () be Bernoulli random variables indicating whether at least one buy (sell) MO arrived during the time period , i.e.,

(1)

Let be a fixed positive integer and define the lag- recent history of MOs at time as

(2)

We often use the shorthand notation .

Above, we are assuming that is the beginning of the MM’s trading and that there is a sufficiently large “burn-out” period prior to it. In particular, the indicators (1) are also defined for by setting some times before the beginning of the trading at time . Thus, for instance, is if at least one MO arrived during the time period and represents the indicators of MOs in the time periods previous to .

For future reference, let us introduce some notation. For any adapted process , we set

(3)

which can be considered some sort of one-step ahead forecasts of . Note that all these processes are adapted to the information process .

As mentioned before, at each time , the MM will place simultaneously a buy and a sell LO. Her sell LO will be submitted with an execution price of , while her buy LO will have an execution price of . The volume of these orders is typically set to be the average volume of submitted LO in the stock of interest. Both and are the MM’s ‘controls’. It will be important to reparameterize the controls relative to a reference price associated with the stock such as the midprice or other related proxy.

The MM’s buy (sell) LOs submitted at time () will be matched against the sell (buy) MOs submitted during the period as follows. Let us first consider the ask side. If denotes the reference or fundamental price of the stock at time and the MM’s ask LO is placed above (i.e., ), then the total number of shares from the MM that are sold during is denoted by and is given by

(4)

where are nonnegative random variables. Broadly (but not literally) is related to the maximum depth that buy MOs walk into the LOB during and is such that indicates the executed volume of a sell LO if this were placed at the same level as the reference price (that is, if ). We can also interpret as the buyers’ reservation price in the market; i.e., the highest price that ‘buyers’ in the market are willing to pay for the stock. These interpretations should not be taken literally as explained in points 2-4 of Remark 1 below.

We analogously define the corresponding quantities for the bid side of the book. That is, provided that at least one sell MO arrives during the time interval , will be the executed volume of the MM’s buy LO placed at time at the price level . Similarly to , we reparameterize in terms of the distance below the reference price so that . Similarly to (4), is modeled as

(5)

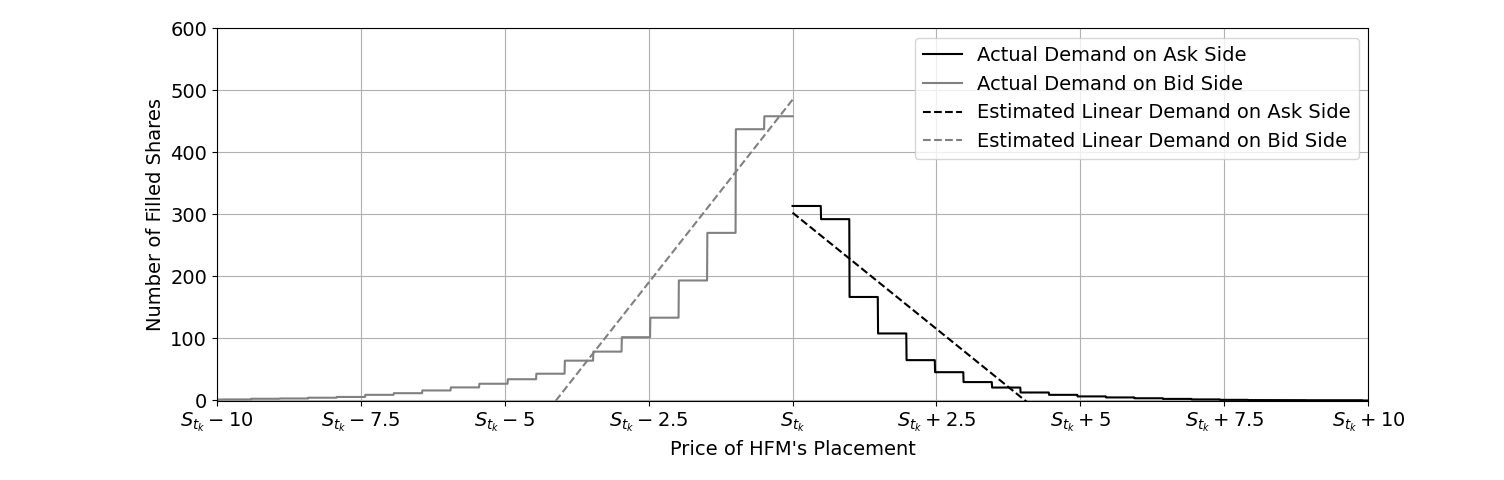

where and has analogous interpretations as and . Above, both and are the MM ‘controls’, while the reference price is exogenously determined by market conditions independently from the MM actions. The form of the function of is illustrated in Figure 2.

Remark 1.

Some comments are in order to clarify our model assumptions (4)-(5) and contrast to earlier work:

1.

As mentioned in the introduction, in a continuous-time setting, Adrian et al. (2020) considered demand functions similar to (4)-(5), but with and being known deterministic constants. Then, the actual numbers of shares bought or sold over depend only on the spreads . Introducing randomness is more realistic since the actual demand during , not only depend on the spreads of the quotes, but also on the initial state of the book, which is hard to summarize and incorporate given its high-dimensionality and variability, and on the flow of orders during the interval, which is extremely unpredictable at time . One may argue that for the purposes of market making all what matters in the average demand during the given trading period . That is, all what we need is to take the deterministic demand functions or , where , , are the average values of , , and over , respectively. As explained in the items 1 and 4 of page 18 and 19 (see formulas (24) and (26) therein), the randomness of and the correlation between and play key roles in the optimal MM strategy. This is further verified in our numerical/empirical Section 3 (see Tables 6-7 therein).

2.

As mentioned above, the actual demand during corresponding to placements would depend on the shape of the book at time as well as the volume and timing of MMs and the arrival of other LOs and cancellations during that interval. Figure 3 shows the approximate demand during a prototypical time interval where at least one MM order arrived (see Subsection 3.1.2 for details about how to estimate such a demand). Then, in a nutshell, and are chosen so that the resulting linear model is close to the ‘actual’ demand. In other words, (4)-(5) are viewed as the ‘best’ linear fit for the actual demand during a given time period.

3.

One of the obvious drawbacks of (4)-(5) is that, in principle, we are assuming the possibility of negative demands (negative number of units sold or bough), which is obviously not realistic. But, this would happen only if the LO quotes were large compare to . This assumption would then be an issue if the resulting optimal placements were, at times, far away from the reference price, since, in that case, the optimal strategy may be favoring or looking for negative demands, which in reality are not feasible. In the context of Figure 3, this would be the case if the optimal placements were more than about 6 ticks away from that is when the linear demand functions start to produce negative values. However, our empirical implementation in Section 3 shows us that the resulting optimal placements are almost never far away from the reference price (almost always less than or equal to 4 ticks away) and, thus, the linear demand assumption is not an issue in practice.

4.

Above it was mentioned that is connected to the maximum depth that the buy MOs walk into the LOB during . This is because, under this interpretation, we obviously have that if , then the corresponding demand should be . However, as mentioned above, it is more accurate to see as the value for which provides a good fit for the demand when is small.

Figure 2: is the lowest price that a sell market order can attain, and is the highest price that a buy market order can attain during the time interval . The number of filled shares increase as the market maker places limit orders closer to the fundamental price .Figure 3: Prototypical Plot of the Actual Demand vs. Estimated Linear Demand over Time Interval .

Next we introduce the main assumptions on the distribution of the random variables , and .

Assumption 1.

For , let . Then,

(i)

and are conditionally independent given .

(ii)

The conditional distribution of given is a measurable function depending solely on , and it does not depend on .

(iii)

The conditional distribution of given is a measurable function depending solely of that does not depend on .

(iv)

Let be the fixed number defined in Eq. (2) and define . Then, for some , we assume the existence of functions and such that for all ,

(6)

By virtue of conditions (ii) and (iii) above, for each , there exist functions and such that

(7)

for any . The optimal placement strategy will depend on the following nonrandom quantities:

(8)

When or are , we simply write and , and omit the exponents if and/or are . Note also that

(9)

and, thus, they all satisfy representations similar to (6) and, in particular, can be written as functions of .

Remark 2.

It is important to stress the relevance of the assumption given by Eq. (6). In Adrian et al. (2020) and our earlier preprint Capponi et al. (2021), it is assumed that the probabilities and are deterministic smooth functions of time, fixed throughout the trading day. In that case, for implementation purposes, these functions have to be estimated at the beginning of the trading day from, for instance, historical data or other type of preliminary market analysis, but once they are chosen, they cannot be changed through the trading day. In the present work these probabilities are allowed to ‘react’ to the ‘recent’ history of buy/sell market orders , through a chosen function . The purpose of the function is two-fold: it summarizes the information contained in and it allows us to alleviate the computational burden by reducing the dimension of past information. This novelty enables the MM to adapt or adjust her trading strategy to the recently observed “trades” in the market, which as shown empirically in Section 3.1, can provide a good forecast for the likelihood of a MO arriving on a given interval in either side of the book. In our framework, the hyperparameter functions and in Eq, (6) will then have to be calibrated at the beginning of the trading day based on historical data. We can think of each value of as a possible ‘scenario’ of the recent MOs history. At the beginning of the trading day, we calibrate the probabilities and for each possible scenario. This will allow us to choose the best possible placement strategy for each possible scenario. We give further details in Subsection 3.1.

Remark 3.

Under our conditions stated in Assumption 1, the average number of lifted shares from the MM will depend on the constants and and the probabilities (6). In particular, these will be adapted to the recent history of MOs, , at each time . For instance, if the MM placed her sell LO at the the same level as the reference price at time (), she would expect that shares of her order would be sold. In general, if ticks away from the reference price , she would expect shares of her LO to be lifted during . Indeed, from the formula (4) and notations (6)-(8),

Remark 4.

There is a possible connection between the approach based on exponential lifting probabilities (cf. Cartea & Jaimungal (2015)) and that based on linear demand functions. Specifically, if is the arrival intensity of MO’s and the lifting probability is set to be , where is the distance between the LO quote and the fundamental price, then, during a time span of , we expect that times a MO will lift a LO placed at distance . Since in this stream of literature, it is typically assumed that only ‘one’ share of the order is lifted at a time, when is small (as it is commonly the case), the expected number of shares filled during a time span is approximately equal to , which is precisely linear in . Since we are allowing actions to take place only at discrete times, we believe that the modeling based on stochastic linear demand functions provides greater flexibility.

As in Cartea et al. (2015), Adrian et al. (2020), and others, for the performance criterion of our placement strategy, we use , where and respectively represent the MM’s cash holding and stock inventory at time , and is a constant penalization term. Note that at time , the last two terms can be rewritten as, , which may be interpreted as the MM’s end-of-the-day cash flow incurred when liquidating her inventory using a MO. Overall, the latter interpretation seems to be a good approximation of reality as shown by our empirical analysis of Section 3.2 (compare Tables 2 and 3)222Related to this, some recent works have proposed equilibrium models to deduce the price impact of a market order (see, e.g., Cetin & Waelbroeck (2023)). See also Bhattacharya & Saar (2021) for further insights about the relation between price impact and the depth of the book or the arrival frequencies of trades.. The optimal control problem then consists of finding the adapted placement positions that maximize

(10)

For future reference, note that, in light of Eqs. (4) and (5), we have, for ,

(11)

(12)

2.2 Optimal Placement Strategy for a Martingale Midprice Process

For ease of exposition and to establish the main ideas, in this subsection we first present the solution of the optimal placement problem under the assumption that the reference price process is a martingale. The case of a general price process

is presented in the following subsection. The results herein will enable us to give a more tractable presentation of the general case. All the proofs in this subsection are deferred to Appendix A.1.

In order to proceed, we need to make an additional assumption on the distribution of the increments of the price process.

Assumption 2.

(i) For any , the price increments and the random vector are conditionally independent given , and (ii) is a martingale, i.e., , for any .

We now specify when a strategy will be admissible. We specify two types of admissibility.

Definition 1.

For any , a strategy running from time to time is said to be admissible if, for every , . If, in addition, we have , for all , we say that the strategy is strictly admissible. The set of all (strictly) admissible strategies running from time to time is denoted by () .

Note that the strict admissibility condition is equivalent to , i.e., the selling price of the MM is higher than her buying price at all future times. We don’t require that and are nonnegative because is not necessarily seen as the midprice , but rather as the ‘fundamental’ price of the stock. In practice, the placement will always be set at the tick right above (below) the midprice if () is found to be below (above) .

In accordance to performance criterion (10), we can then write the value function at time as

(13)

To solve the optimal control problem, we first assume that follows the ansatz

(14)

where are some

-adapted real-valued random variables to be determined from the dynamical programming principle (see Theorem 1 below). The ansatz is motivated by the specific form of the performance criterion in (10) and the dynamic principle given in Eq. (15) below.

The Dynamic Programming Principle (see, e.g., Hernández-Lerma & Lasserre (1996) and Bäuerle & Rieder (2011)) associated with (13) can then be written as

(15)

where we set and consists of all . Using the ansatz (14), we can rewritten (15) as

(16)

By plugging the recursions (11)-(12) in (16), we will be able to find a candidate for the optimal placement strategy (Theorem 1 and Corollary 3 below).

It is until Theorem 4 when we shall verify that our candidate is indeed the solutions to our original optimal control problem (13). In Section 2.4, we study the strict admissibility of the optimal strategy.

To write explicit formulas for the optimal placement strategy, we introduce the following terminology:

(17)

where above and are defined using the notation (3). We will prove below that the optimal spreads for the ask and bid side can be written as and with the coefficients:

(18)

where we again used (3) to define . We first show that the maximization problem in (16) is indeed well-posed.

Theorem 1.

Under the Assumptions 1 and 2, the following statements hold:

(i)

There exist coefficients , , and that solve (16) for with dynamics (11)-(12) and terminal conditions and .

(ii)

For , the coefficients , , and in (i) are -measurable random variables, where recall from Assumption 1 that .

(iii)

For , the coefficients of (i) can be computed recursively by the equations:

Before finding the optimal controls of (15), we state an important preliminary result that will also be needed to show the verification theorem and the strict admissibility of the optimal controls. This result is deceivable simple, though its proof is rather intricate.

Lemma 2.

The random variables defined in Eqs. (19) are such that

We are now ready to find the optimal controls of (15) under the ansatz (14). Most of its proof is embedded into the proof of Theorem 1 but due to its importance it is stated separately.

Corollary 3.

The optimal placements that maximize the right-hand side of the Eq. (15) under the ansatz (14) are given by

(22)

where the coefficients above are given as in (18).

In light of the previous result, the optimal placement strategy takes the form:

(23)

In the preprint Capponi et al. (2021), an extensive analysis of the properties of the optimal strategy was carried out in the case that the arrival intensity of MOs is deterministic rather than adaptive as in our setting (see Remark 2). One of the main conclusions therein is that the randomness of and are not just a mathematical ‘artifact’ for the sake of generalization, but play an important role in the behavior of the optimal placement strategy. Many of the conclusions therein transfer to our setting, but, for the sake of space, we just highlight some of the most important here:

1.

The second term in (23) is fundamental as it can be interpreted as the inventory adjustment to the optimal strategy. In the case of (which is met to a good degree when trading frequency is high enough), the coefficient simplifies as follows:

(24)

Due to Lemma 2, the coefficient above is negative, which means that when the inventory is positive (negative), the ask and bid levels decrease (increase) to stimulate selling (buying) of stock and, hence, bring inventory closer to . The larger the level of the slope , the smaller the effect of inventory in the optimal placement strategy. However, with the same average value of , stocks with more variable require smaller inventory adjustment.

2.

In the case of , we still have that .

Indeed, recalling (17)-(18) and , and applying (A-12), the numerator of satisfies:

Since the denominator (cf. (A-13)), we conclude that .

3.

Again, assuming that , we can further write:

(25)

Computationally, it can be shown that and are close to for most of the time interval and it is only for close to , that their values are significantly different from (especially, ). Then, we have the approximations:

(26)

The correlation between and now plays a key role in the optimal placements. When and are uncorrelated (such as when or are deterministic), the optimal placements are near the midpoint between and the average reservation price for most of the time. However, when the correlation between and is positive,

instead of placing LOs around , the HFM will tend to go deeper into the book. Roughly, a larger realization of also implies a large value of , resulting in a larger demand function and, hence, greater opportunity for the MM to obtain better prices for her filled LOs.

4.

Under the condition and certain market symmetry and independence conditions, we can strengthen the conclusions of the previous item. Specifically, if we assume that , , , and , when , and (see Lemma 8 and the proof of Corollary 7 for sufficient conditions for the latter to hold), then we have that and (25) uncovers the existence of a critical inventory level that dictates the relation of the optimal placements relative to the nominal values and . Specifically, let .

Then, we have:

•

When (), the optimal ask (bid) quote is at the level

();

•

When the inventory level (), the optimal ask (bid) quote is deeper in the LOB relative to the levels ();

•

When the inventory level (), the optimal strategy is to place the ask (bid) quote closer to than to (), and the bid (ask) quote farther from than from () into the LOB.

We next prove a verification theorem for the optimal placements given in Eq. (23). Its proof is given in Appendix A.1.

Theorem 4.

The optimal value function of the control problem (13) is given by

where, for ,

with , and given as in Theorem 1.

Furthermore, the optimal controls are given by as defined in (22).

2.3 Optimal Placement Strategy for a General Midprice Process

The objective of this subsection is to extend our previous results to the case when the midprice process is a general stochastic process without relying on a martingale assumption. As we will see below, in that case, the optimal placement strategy will also depend on the forecasts of future price changes:

(27)

We can see as the MM’s forecast of the price change during the time interval , , as seen at time . We first need to modify our Assumption 2 as follows:

Assumption 3.

For any , and are conditionally independent given .

To solve the optimization problem (15), we use an ansatz for the value function similar to that in the previous subsection:

(28)

where , , and are -adapted real-valued random variables to be determined from the dynamical programming principle (15). As one may suspect from the notation above, will turn out to be the same as before: an -measurable random variable determined by the recursive relation (19). However, will be different (in fact, not necessarily -measurable).

The following theorem summarizes the analogous results of Theorem 1 and Corollary 3 under a general price dynamics. Its proof is provided in Appendix A.2.

Theorem 5.

Under Assumptions 1 and 3,

the optimal strategy that solves the Bellman equation (15) with the ansatz (28) and terminal conditions and is given, for , by

(29)

where is defined as in Corollary 3, , , and are defined as in (17), and the quantity is given as:

(30)

Remark 5.

Formula (29) gives us some interesting insights, even in the simplest case where only one-step-ahead forecast is implemented, while assuming that afterward (). In that case, the third summands of and vanish, yielding the following parsimonious formulas for the optimal placement strategy:

(31)

The last term above allows the MM to adjust ‘online’ her strategy depending on her views or forecast of the next price change at each time instant . This feature in turn provides a more data driven placement strategy in addition to the method described in Remark 2 above. Using the facts that , , and (A-10)-(A-11), it is possible to show that

Since , we conclude that if

(32)

In those cases, since (cf. (A-13)), the coefficients of in (31) are positive. This sign makes sense since, if, for example, , the MM will try to post her LOs at higher price levels (on both sides of the book) to anticipate the expected higher price in the subsequent interval. The first condition in (32) is satisfied to a good extend when the trading frequency is high enough, while the second condition therein is supported empirically by our analysis in Section 3.1.

2.4 Admissibility of the Optimal Strategy

In this section, we will give sufficient conditions to guarantee that the optimal strategy of Theorem 5 is strictly admissible. All the proof of this subsection are deferred to Appendix A.3.

Recall from Definition 1 that a strategy is strictly admissible if for all , , and , implying that the execution price of the ask LO is always larger than the execution price of the bid LO. Proposition 6 below provides sufficient conditions under which the optimal strategy introduced in Theorem 5 enjoys this property.

Proposition 6.

Under Assumptions 1 and 3 and regardless of the dynamics of the midprice process, the optimal strategy of Theorem 5 yields positive spreads at all times i.e., , for all , provided that the following four conditions hold:

(1)

The first and second conditional moments of , as defined in Equation (8), satisfy

(33)

(2)

At every time ,

(34)

(3)

For every , the conditional expectations of and , as defined in Eq. (8), satisfy

(35)

(4)

For every , the -measurable random variables and , defined by Eqs. (19) and (20), depend on and only through .

Conditions (33) and (34) are some type of symmetry conditions between the bid and ask sides of the market. Condition

(35) postulates that the demand and supply slopes and the corresponding reservation prices are uncorrelated. These assumptions are empirically supported by our empirical analysis in Section 3 (see Figure 4 and Table 1).

The following result shows that the conditions (2) and (3) of Proposition 6 can be relaxed in the case that there is no possibility of simultaneous arrivals of sell and buy market orders in the same subinterval. The latter condition is expected to be met reasonably well when the frequency of trades is high enough (i.e., ).

Corollary 7.

Suppose that, for every , the conditional probability is . Then, regardless of the dynamics of the midprice process, the optimal strategy is admissible if Conditions (1) and (4) of Proposition 6 are satisfied.

The most technical condition in the results above is (4), which can also be interpreted as another symmetry assumption.

This condition could be difficult to verify due to the intrinsic complexity of the recursive formulas (19) and (20).

In the Lemma 8 below, we show that it suffices to pick the function introduced in Eq. (6) such that it depends on and through .

Lemma 8.

If the function in Eq. (6) is of the form for some , then and will depend on and only thorugh . In particular, they depend on and only through and the condition (4) in Proposition 6 is satisfied.

2.5 Inventory Analysis of the optimal strategy

In this section we analyze the behavior of the inventory under the optimal strategy found in Section 2.2, when and some symmetry conditions are satisfied.

As explained above, the first condition is reasonable

when the trading frequency is high enough.

The following result shows that when the initial inventory is , then the expected inventory stays at at all future times. The proofs of this part are deferred to the Appendix A.4.

Proposition 9.

Suppose that the Assumptions of Theorem 1, the conditions (1)-(2) of Proposition 6, and the condition of Lemma 8 are satisfied. We also assume that and and .

Then, under the optimal placement strategy of Corollary 3, for any , we have

Note that (36)-(ii) does not follow directly from (36)-(i) as in the nonadaptive case of Capponi et al. (2021) because is random here and correlated to . The derivation of (36)-(ii) requires an explicit representation of and heavily depends on the symmetry condition of Lemma 8.

Recalling from Lemma 2 that and since ,

we have . Thus, by Equation (36)-(i), it follows that

(37)

In particular, if (), then (), hence the inventory is mean-reverting toward .

2.6 Optimal MM strategy under running inventory penalization

In continuous-time settings, Guilbaud & Phan (2013), Cartea et al. (2014), and others have advocated for a running inventory penalty to further control the inventory risk. Under this control, the performance criterion is . In discrete-time, the analogous value function at time naturally takes the form:

(38)

where as usual . The dynamic programming principle corresponding to (38) can then be written, for , as

(39)

starting with . The heuristics behind (39) is classical:

The following result, whose proof is deferred to Appendix A.5, formalizes the heuristics above. Specifically, this shows that, under (38), most of the results considered in this paper follow with minor modifications.

Theorem 10.

Suppose that the setting and assumptions of Theorem 1 and Corollary 3 hold true. Then, the following statements hold:

1.

The conclusions of Theorem 1 and Corollary 3 follow with (39) replacing (15) and an ansatz of the form

(40)

The optimal controls , are then given by

(41)

with the coefficients , , and taking the same form as (18), but with and replaced with and . Here, , , and follow the same formulas as (19)-(21), but with , , , , , and replaced with , , , , , and , respectively, on the right-hand side of all the formulas.

2.

The conclusion of Lemma 2 also follows under the new running inventory penalty; i.e.,

3.

The verification Theorem 4 holds true with the value function (13) replaced with (38).

2.7 Implementing the Optimal Strategy

As indicated in Remark 2, the function introduced in (6) has two main purposes. First, it summarizes the information contained in the recent history of MOs, , and, more importantly, it alleviates the computational burden by reducing the dimension of the different scenarios one needs to consider. However, in order for to work as intended, we must impose one additional condition:

Assumption 4.

For , is a function of ; i.e., if we denote the image of as , then there exists a function such that

(42)

Obviously, if we picked to be the identity function () so that there is no dimension reduction, then (42) is trivially satisfied by taking to be the mapping that drops the last two coordinates of the vector . A more interesting example is when (which satisfies the conditions for admissibility stated in Lemma 8). In that case, denoting the mapping that drops the last two entries in a vector as , we have:

Working backward by induction, it is not hard to check that, under Assumption 4, the coefficients , , and for the optimal placement strategy (22) depend only on .

Indeed, the probabilities have this property since these can be expressed in terms of and (see (9)), which enjoy the stated property per Assumption 1-(iv). So, it only remains to show that , , and (and the corresponding quantities for ) have this property. Indeed, by the induction step, we can assume that , for some function , and, by Assumption 4, . Then, similar to (A-6),

(43)

which is clearly a function of . We can similarly deal with , , , , and .

To carry out the optimal placement strategy, we think of each value , the image of , as a possible scenario of the immediate history of MOs. Before the beginning of trading, the MM first computes, backward in time using Eqs. (17)-(19), the coefficients , , and of the optimal placement strategy (22) for each time and each possible scenario . This results in a type of “dictionary” or “catalog”. Once the catalog is computed, she can then start her trading moving forward in time. At each time , she observes the recent history of MOs . Based on the , the inventory value , the asset price , and her forecasts of future price changes, she places her bid and ask LOs using the catalog. For instance, if she assumes , for all , she will place her orders at

(44)

where above we are also assuming that the coefficients of are computed at the beginning of the trading for each time and each scenario .

3 Calibration and Testing the Optimal Strategy on LOB Data

In this section, we give further details about the implementation of the optimal placement strategy of Section 2.3, including model calibration. We then illustrate our approach with real LOB data from Microsoft Corporation (stock symbol MSFT) during the year of 2019333We have tried a few other stocks but the results are not shown here for the sake of space.. Our data set is obtained from Nasdaq TotalView-ITCH 5.0, which is a direct data feed product offered by The Nasdaq Stock Market, LLC444http://www.nasdaqtrader.com/Trader.aspx?id=Totalview2. TotalView-ITCH uses a series of event messages to track any change in the LOB. For each message, we observe the timestamp, type, direction, volume, and price. We reconstruct the dynamics of the top 20 levels of the LOB directly from the event message data. We treat each day as an independent sample.

In the first subsection

we detail the model training or parameter estimation procedure. The training will be based on the historical LOB data of the 20 days prior to each testing day555We tried different windows. The performance is good provided that the window size is not too small (say, 2 or 5 days)..

In the second subsection, we present the performance of the optimal placement policy using the real flow of orders for MSFT in a given testing day and compare it with “fix-placement” strategies that place LOs at fixed ask (bid) price levels. More specifically, in each test day, we assume the MM places her LOs every second from 10:00 am to 3:30 pm, placing a total of 19800 LOs at each side of the book.

3.1 Parameter Estimation

3.1.1 Estimation of

We first need to specify the function in Assumption 1-(iv). We consider the following three functions:

(45)

The first function does not satisfy the conditions for admissibility of Lemma 8. However, in practice, for each of the functions above, it is very rare that or that () is below (above) the midprice . When any of these events happen, we simply set and/or at the tick right above and below the midprice depending on what is appropriate.

Once we have selected the function , we use the historical LOB data of the 20 days prior to each testing day to estimate the functions , , and in Assumption 1-(iv). To this end, we simply leverage the interpretations of those functions as conditional probabilities.

Specifically, setting , for every , we estimate and as

(46)

(47)

where indicates the cardinality of a set and the times ’s range over all the seconds from 10:00 am to 3:30 pm in the 20 days prior to the testing day.

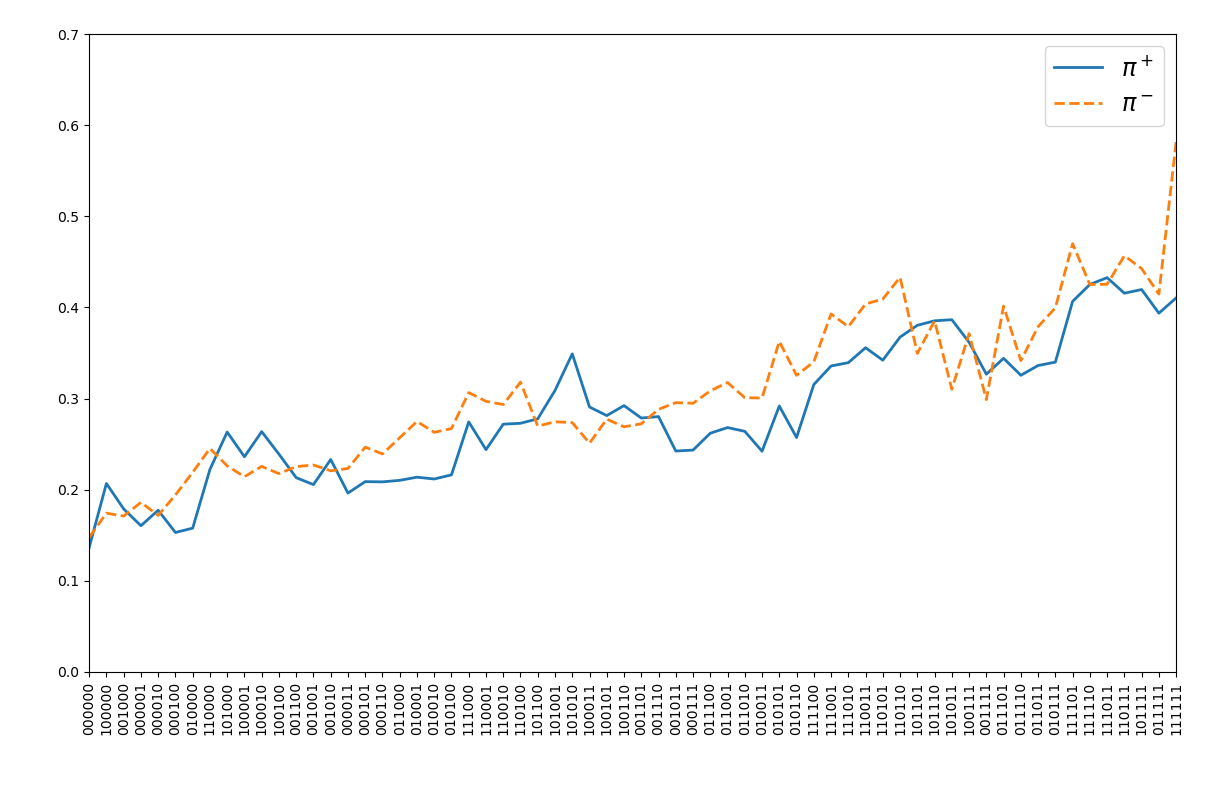

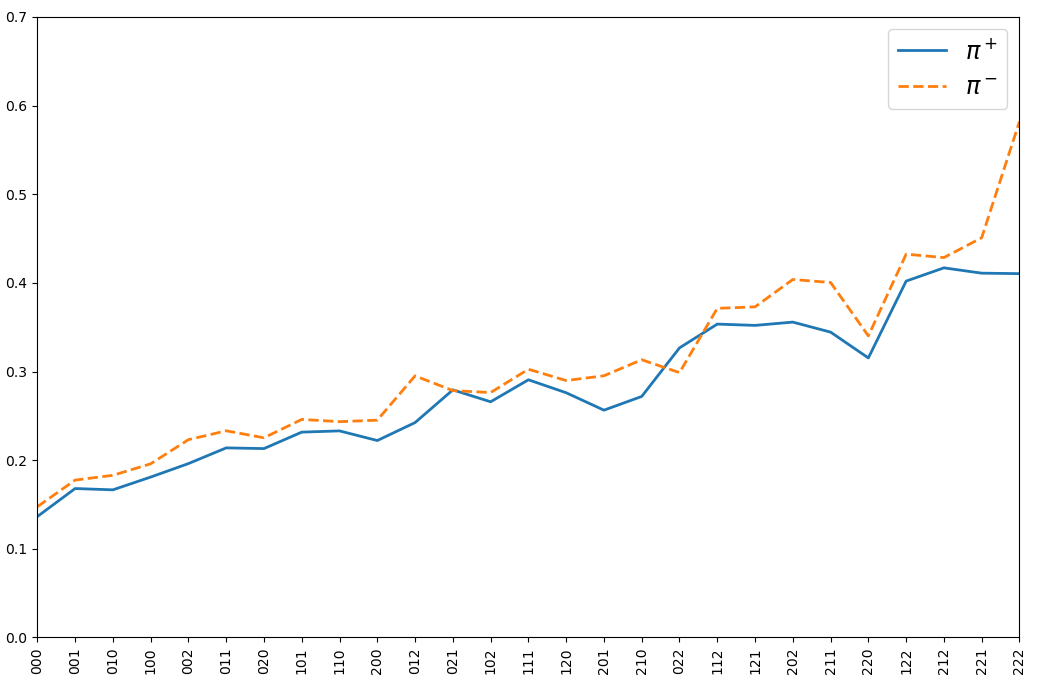

The results of the estimation procedure for and can be found in Figure 4 below. The overall behavior is what one will expect: when takes a value corresponding to more ones in , the probabilities take larger values. These figures also indicate that our symmetry assumption required for admissibility (see Proposition 6) is reasonable.

(a) as functions of .

(b) as functions of .

(c) as functions of .

Figure 4: Estimation of under the different choices of the function given in (3.1.1). The -axis displays the equivalence classes where the function assumes different values, whereas the -axis represents the value of .

Remark 6.

One of the key principles behind our approach is the presumption that we could forecast to a good degree the intensity of MOs through the day using the estimated functions (46) and (47) and the history of previous MOs, . To assess the validity of this principle, we compare the average of the sets

where .

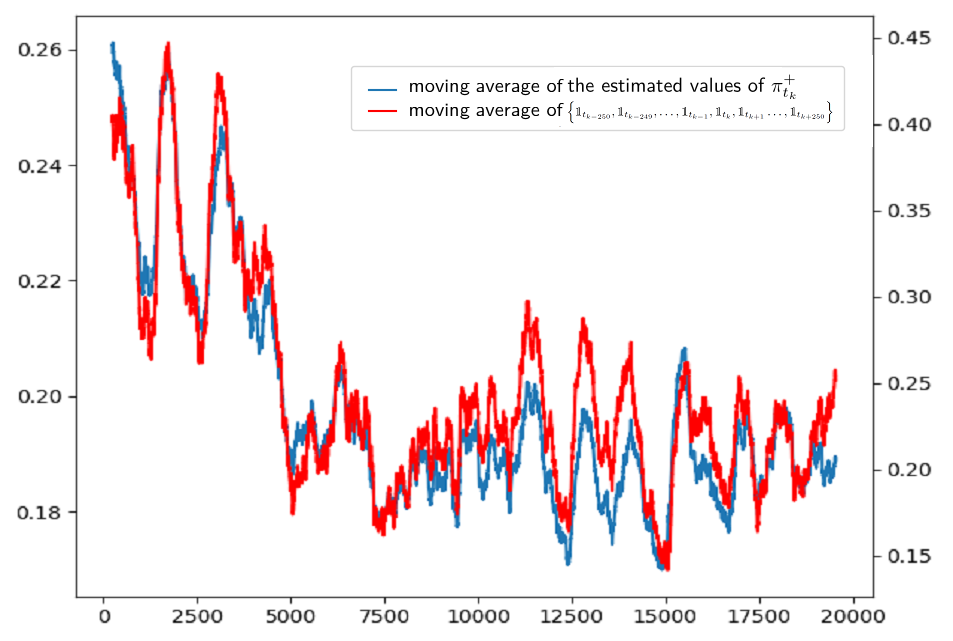

Figure 5 below shows the result for all the seconds in a prototypical day. This shows that our approach is surprisingly accurate in tracking the intensity of MO’s throughout the day using historical data from previous days and past information of MOs.

Figure 5: Moving average of the estimated values of (using the function ) and the moving average of on August 7th, 2019.

3.1.2 Estimation of the Demand Functions.

To estimate the constants of Eq. (8), upon which our strategy depends on, we use the sample averages within the previous 20 trading days. For instance, the estimate of is

(48)

where ranges over all the seconds of the previous 20 days from 10:00 am to 3:30 pm and is the total number of those. To estimate for one of those previous 1-second time intervals , we apply the following procedure. Assume that the MM places an ask LO at price level at time with volume , and that the volume of existing ask LOs with prices lower than is . If a buy MO with volume arrives during , then the number of shares of the MM’s LO to be filled equals to 666Here, for computational simplicity, we are assuming the MM’s LO at level is ahead of the queue (hence, her shares are the first to be filled at that level), which is a common simplification in the literature.. We then compute this quantity for all buy MOs arriving during the interval so that will quantify the actual demand at price level during that interval. Once those demands have been computed for all price level above the midprice, we performed a weighted linear regression to estimate , with the actual demand being the response variable and the price level being the predictor, placing higher weights on price levels closer to the midprice . Following Eq. (4), we can estimate and as the slope and as the quotient intercept/slope of the regression line, respectively. In the preprint (Capponi et al., 2021, p. 28), it is shown that time series are reasonably stationary, implying that our method to estimate the constants as (48) is justifiable.

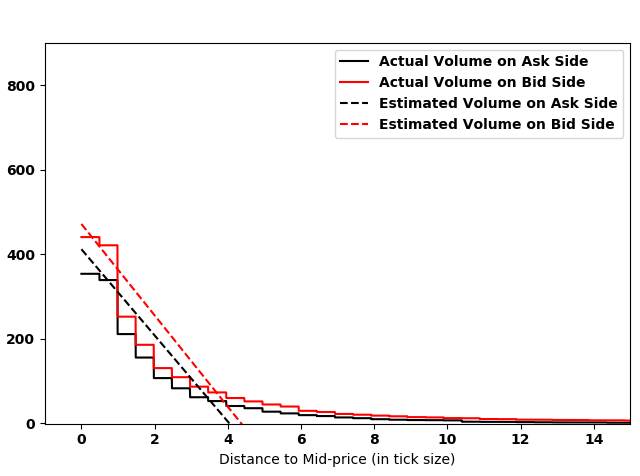

In Figure 6 below, we plot the average demand curve and the regression line whose slope and value is set to the averages of the ’s of all 1-second time intervals during that date. This graph shows that the linear model in Eqs. (4)-(5) is a reasonably good approximation of the actual volume of shares executed, especially as they are closer to the midprice where most MOs are executed.

Figure 6: Plot of the actual demand on October 3rd vs. the estimated linear demand function over a 1-second trading interval

To give an idea of the values of , we estimate those constants for each day of the 252 days of our sample (using an estimator like that in (48) but with the ’s ranging over all the seconds of each day) and then we take the averages of the resulting 252 estimates . Table 1 shows the results. The table also shows some other related quantities to assess the validity of Eqs. (33) and (35) in Proposition 6. As shown therein, these assumptions are reasonably met in our sample data.

=

=

=

=

=

=

=

=

=

=

=

=

=

=

Table 1: Average values of and over 252 trading days in 2019. Entries with the same color should be of a similar magnitude to have our model assumptions validated.

3.1.3 Estimation of the Drift for the Midprice Process.

For simplicity, we set the fundamental price to be the midprice process. For our implementation, we assume that

because in practice, one could expect to quickly decrease to as is farther away from (otherwise, statistical arbitrage opportunities are likely appear) and also because the estimation error of the forecasts increases quickly as is farther away from . To estimate the one-step ahead forecast , we simply take the average over the last 5 increments:

(49)

3.2 Numerical Results

In this subsection we illustrate the performance of the optimal trading strategy using as function each of the functions in (3.1.1). For each of these choices we compute the terminal value of the performance criterion under the martingale assumption. We also compute the terminal value when applying the placement strategy (31) with estimated as (49) and using the function . As mentioned above, our optimal placement strategy was tested based on the LOB data of MSFT observed in the year 2019. As suggested in the preprint (Capponi et al., 2021, Section 5.2), we set , which gives a good estimate of the average liquidity cost for our sample data. The cash holding and the stock inventory were computed as

where and were the price of selling (buying) LOs placed at time and () was the executed volume of selling (buying) LOs calculated by using the actual flow of MOs in the market in each one-second interval of each testing day777Here, we are again assuming for simplicity that the MM’s LO is ahead of the queue.. Since all the parameters of the model, namely the filling probabilities and the constants , are calibrated using the past 20 days to each testing day, the first testing day is set to be January , which was the trading day of 2019.

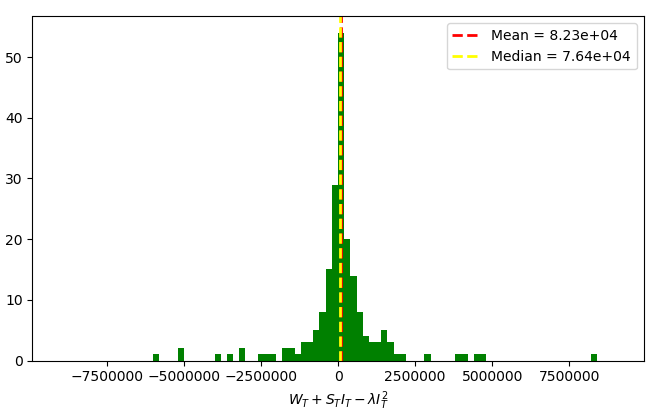

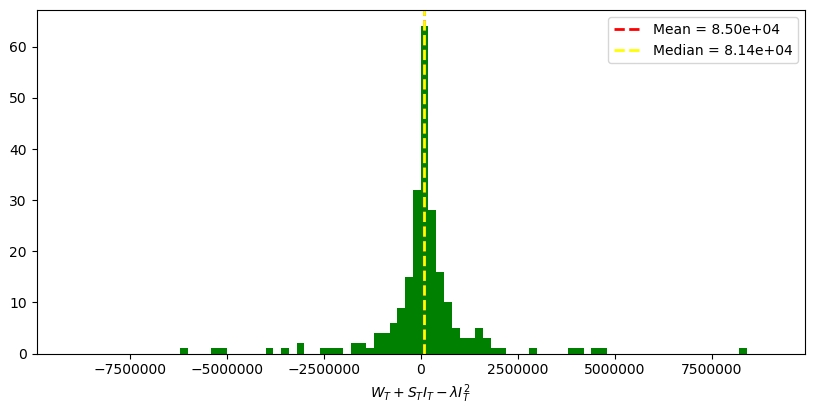

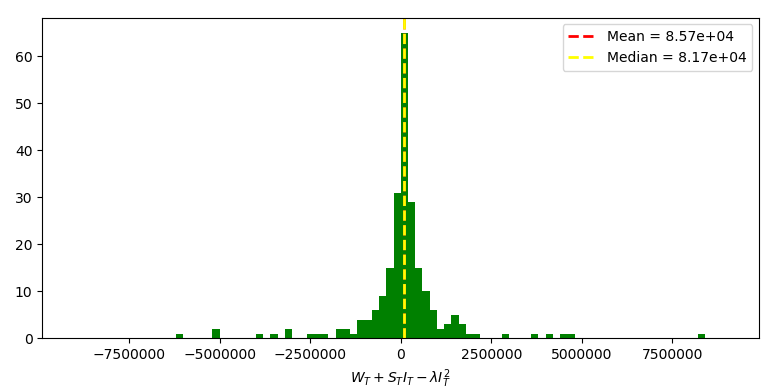

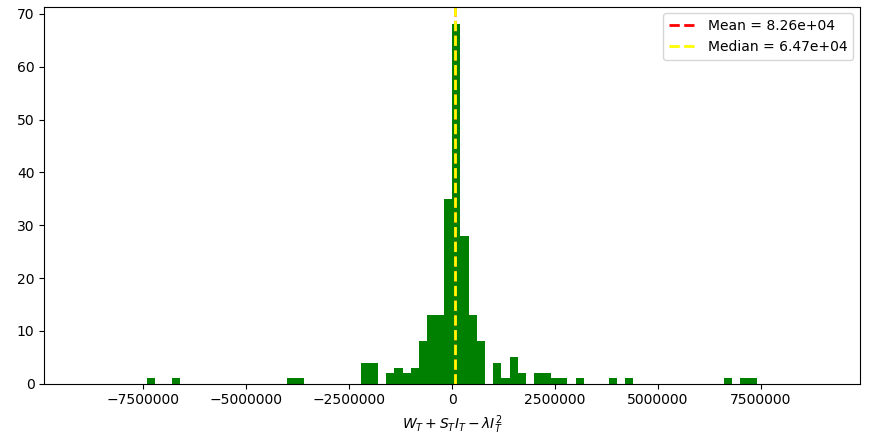

3.2.1 Performance Criterion Distribution.

The sample means and standard deviations of the end of the day performance criterion for the 232 testing days under the four different implementations of our optimal placement strategy are shown in Table 2. For comparison, we also computed the corresponding values when using 6 deterministic strategies labeled ‘Level 1’- ‘Level 6’, where the strategy ‘Level ’ is the one where the MM always posts her orders -ticks deep in the order book at both sides. To complement Table 2, we also present Figure 7 below, where we display the histogram of performance criterion for the 232 testing days. Table 3 presents the means and standard deviations of the terminal values , computed using the actual average price per share that the HFM would get when liquidating her inventory with a MO based on the state of the book at time . We refer to as the liquidation proceeds. We do not observe significant differences with the results presented in Table 2, which validates our assumption of modeling the liquidation cost as and the chosen penalization value of .

Optimal Strategy

with Martingale Midprice

Conditioning on

Optimal Strategy

with Martingale Midprice

Conditioning on

Optimal Strategy

with Martingale Midprice

Conditioning on

Optimal Strategy

with General Midprice

Conditioning on

Mean

Std.

Level 1

Level 2

Level 3

Level 4

Level 5

Level 6

Mean

Std.

Table 2: Sample Mean and Std. Dev. of the performance criterion over 232 days for the different strategies considered (optimal and fixed-placement) based on LOB MSFT Data in 2019.

Optimal Strategy

with Martingale Midprice

Conditioning on

Optimal Strategy

with Martingale Midprice

Conditioning on

Optimal Strategy

with Martingale Midprice

Conditioning on

Optimal Strategy

with General Midprice

Conditioning on

Mean

Std.

Level 1

Level 2

Level 3

Level 4

Level 5

Level 6

Mean

Std.

Table 3: Sample Mean and Std. Dev. of the Terminal PnL, (Terminal Cash Holdings plus the Actual Liquidation Proceeds based on the LOB state at expiration), over 232 trading days based on LOB MSFT data in 2019.

(a)Optimal strategy by using the function under the assumption of a martingale price dynamics.

(b)Optimal strategy by using the function under the assumption of a martingale price dynamics.

(c)Optimal strategy by using the function under the assumption of a martingale price dynamics.

(d)Optimal strategy by using the function under the assumption of a general price dynamics.

Figure 7: Histogram of the performance criterion obtained from the optimal strategies under different scenarios for 232 trading days of MSFT in 2019.

Based on the results observed in Tables 2 - 3 and Figure 7, we can conclude that our optimal strategy under any scenario significantly outperforms the fixed-level placement strategies. From Tables 2 - 3, we can observe that the mean and standard deviation for all three policies under the martingale assumption are close to each other but the policy obtained by choosing the function as has the highest mean and lowest standard deviation. In contrast, when using a one-step forecast (49) and choosing the function as , the average of the performance of the optimal strategy is slightly lower than that under martingale assumption, but the standard deviation is also lower. Furthermore, as shown in Figure 7, the values of the performance criterion for the optimal strategy under all 4 scenarios concentrate around zero, but exhibit some “outliers”, which indicate heavy tails.

For comparison, in Tables 4 - 5, we report the analogous results using the optimal placement strategies from the preprint Capponi et al. (2021), in which the probabilities and are deterministic quadratic functions of time calibrated using historical data. While the sample standard deviations of our adaptive placement strategy are slightly larger than those in Capponi et al. (2021), the sample means of the performance criteria are significantly better.

We can further wonder how important adopting random demand is to achieve good PnL. In Table 6-7 below, we compute the sample means and standard deviations of and based on the 232 day, still assuming adaptive probabilities , but now taking and at each test day constant to their sample averages of the previous 20 trading days. As shown therein, though the average PnL are all positive, they are significantly smaller than those in Tables 2-3 and even those using nonadaptive ’s but stochastic demand as illustrated in Tables 4-5.

Optimal Strategy

with Non-Martingale Fundamental Price

and

Optimal Strategy

with Martingale Fundamental Price

and

Optimal Strategy

with Non-Martingale Fundamental Price

and

Mean

Std.

Table 4: Sample Mean and Std. of the Terminal Objective Values over 232 Days. We fix . We control cash holdings and inventory processes assuming stochastic demand functions but deterministic intensity of MO arrivals as Capponi et al. (2021).

Optimal Strategy

with Non-Martingale Price

and

Optimal Strategy

with Martingale Price

and

Optimal Strategy

with Non-Martingale Price

and

Mean

Std.

Table 5: Sample Mean and Std. of the Terminal Values (Terminal Cash Holdings plus the Actual Liquidation Proceeds based on the LOB state at expiration) over 232 Days. We control cash holdings and inventory processes assuming stochastic demands functions but deterministic intensity of MO arrivals as Capponi et al. (2021).

Optimal Strategy

with Martingale Midprice

Conditioning on

Optimal Strategy

with Martingale Midprice

Conditioning on

Optimal Strategy

with Martingale Midprice

Conditioning on

Optimal Strategy

with General Midprice

Conditioning on

Mean

Std.

Table 6: Sample Mean and Std. Dev. of the performance criterion over 232 days for the different adaptive strategies, but with deterministic demand functions (i.e., and are constant to its average values in the 20 days previous to each testing day.

Optimal Strategy

with Martingale Midprice

Conditioning on

Optimal Strategy

with Martingale Midprice

Conditioning on

Optimal Strategy

with Martingale Midprice

Conditioning on

Optimal Strategy

with General Midprice

Conditioning on

Mean

Std.

Table 7: Sample Mean and Std. Dev. of the Terminal PnL, (Terminal Cash Holdings plus the Actual Liquidation Proceeds based on the LOB state at expiration), over 232 days for the different adaptive strategies, but with deterministic demand functions (i.e., and are constant to its average values in the 20 days previous to each testing day.

3.2.2 Inventory and price evolution.

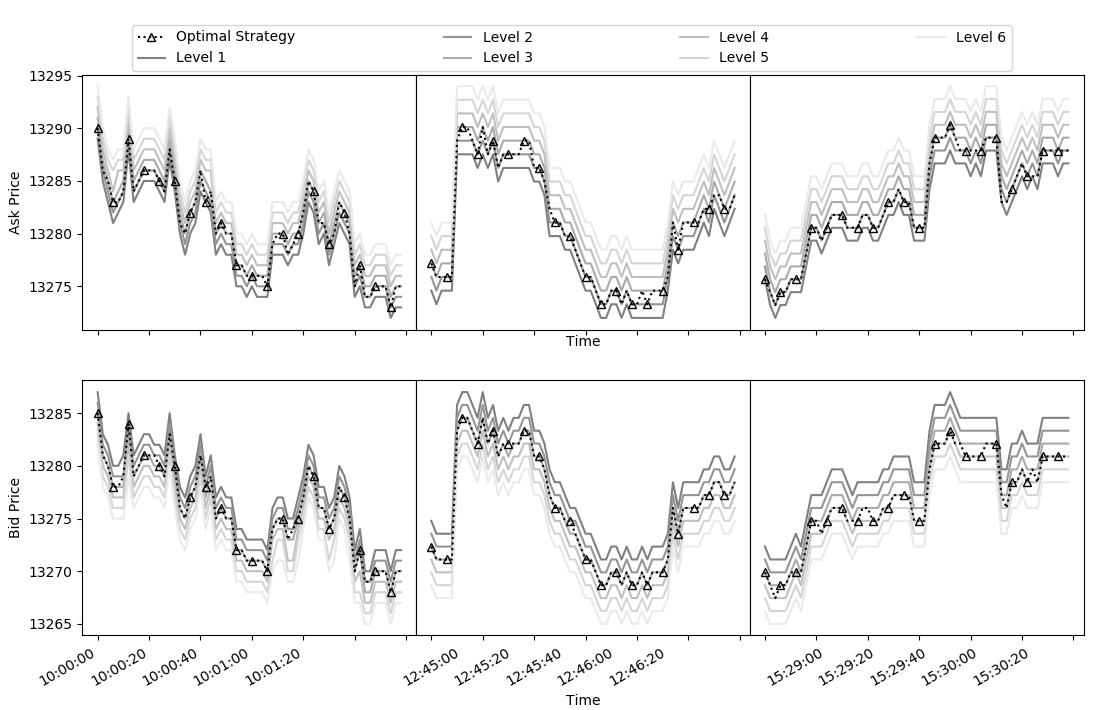

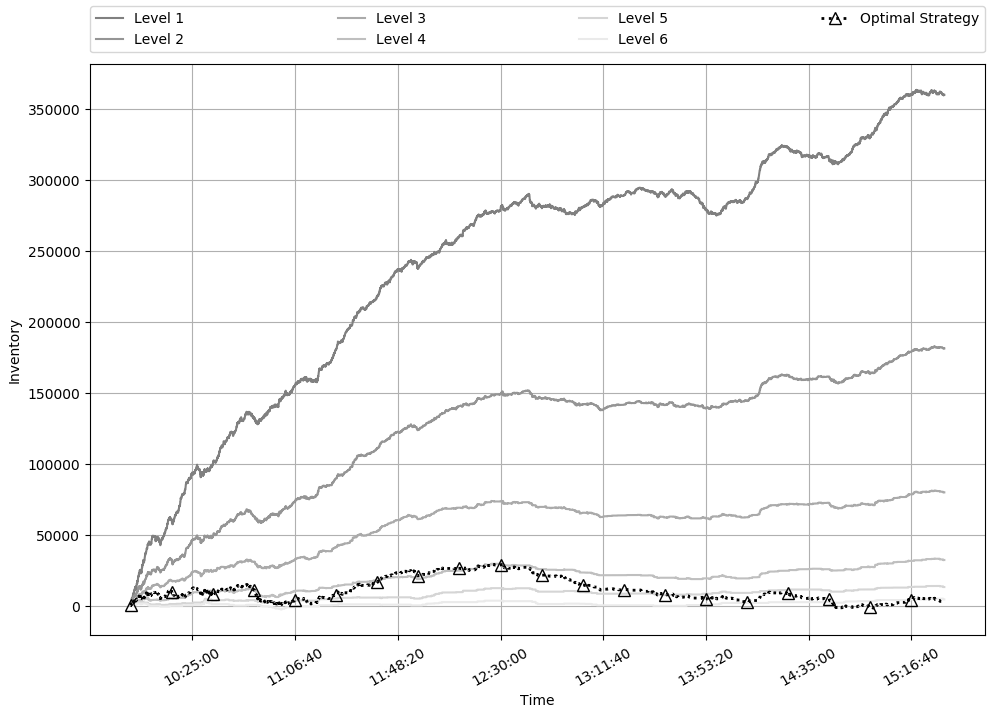

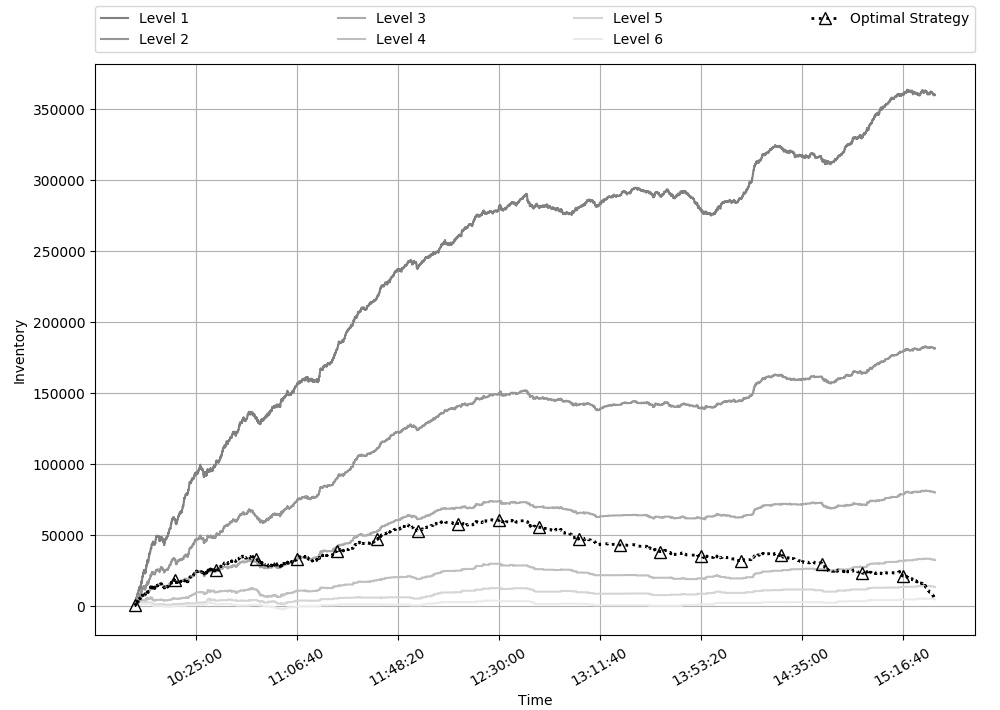

To analyze whether the penalization term in the performance criterion is indeed able to push the MM to lower her inventory towards the end of the trading day, we display in Figures 8 and 9 two prototypical sample inventory paths throughout the trading day of August 7th when computing the optimal strategy with the choice , under both the martingale (Figure 8(a)) and the non-martingale (Figure 9(a)) price dynamics. To compare, we also display the inventory process under the fixed-placement strategies ‘Level 1’-‘Level 6’.

Under the general price dynamics assumption, the inventory path can reach a higher level in the middle of the day, though it is able to bring the inventory down at the end of the day.

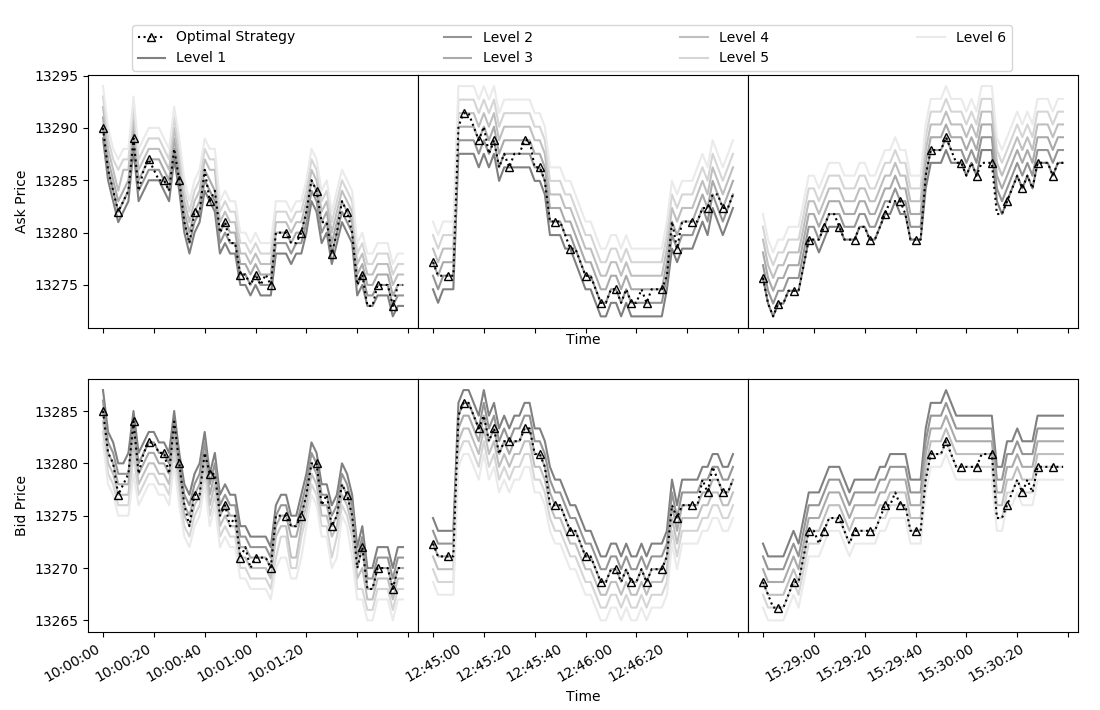

As we can see from Figure 8(b) and Figure 9(b), the optimal prices for both strategies swings between prices for level 1 and level 6. At the end of the trading day, the optimal ask prices under the general midprice assumption is closer to the level 1 price than under the martingale assumption, and the optimal bid prices are close to the level 6 price under both assumptions, which leads to a faster decrease in the inventory.

For the two optimal strategies, the end-of-day inventory is lower than the ‘Level 1’-‘Level 6’ policies. This shows the effectiveness of the liquidation penalty in controlling inventory and avoiding large end of the day costs.

Finally, in Figures 8(a) and 9(a) we present the intraday optimal ask and bid placement prices and for August 7th when choosing the function as under, both, the martingale and the general midprice assumptions. We also compare them with the ‘Level 1’- ‘Level 6’ benchmark policies. The price paths are for three 1-minute time intervals at the beginning of the trading day 10:0010:01, in the middle of the trading day 12:45 12:46, and at the end of the trading day 15:2915:30, respectively. These graphs illustrate how the optimal placement strategies compare to the the fixed level strategies at different times of the day. In particular, the bid and ask prices behave as one should expect at the end of the day to control the inventory.

4 Conclusions

In this manuscript, we focus on end-of-day inventory control in a market making problem. We assume the demand to be linear with random slope and intercept, which allows for greater flexibility and uncovers novel features of the resulting optimal control policy. We account for simultaneous arrivals of buy and sell MOs between consecutive market making actions, which also lead to novel patterns of the optimal policy. We allow the market maker to incorporate forecasts of the fundamental price in her placement strategy. Finally, we enable the investor to integrate the information on the arrival of market orders throughout the trading.

The performance of the proposed optimal policy is assessed using historical exchange transaction data throughout an entire year. The optimal strategy derived with the novel model specifications mentioned above yields greater flexibility and better results in our empirical study.

There are some key areas for future research based on our results:

•

It is natural to consider the possibility that the features of the demand functions also depend on the history of market orders rather than being assumed constants as in the current framework.

•

It would be important to drop the assumption of independent between the price changes and the vector .

•

It is natural to consider the continuous limit of the model considered here. Such an extension could help us to consider general inventory penalties.

(a)The Intraday Prices Paths.

(b)The Intraday Inventory Paths.

Figure 8: A comparison of the intraday price and inventory paths of the optimal strategy under martingale price dynamics assumption when choosing the function as and the ones of the benchmark policies on August 7th.

(a)The Intraday Prices Paths.

(b)The Intraday Inventory Paths.

Figure 9: A comparison of the intraday price and inventory paths of the optimal strategy under the general price dynamics assumption when choosing the function as and the ones of the benchmark policies on August 7th.

Appendix A Proofs Of Main Results

In this Appendix we provide all the proofs pertaining to Section 2.

A.1 Proofs of Section 2.2: Optimal Strategy for a Martingale Midprice

The proof is done by backwards induction. First, note that for , i.e., at the terminal time , the statement (ii) is immediate due to the terminal conditions and . So, it suffices to show the following two assertions:

(a)

If the statement (ii) is true for , then the statements (i) and (iii) are true for ;

(b)

If the statement (ii) is true for and the statements (i) and (iii) are true for , then the statement (ii) is true for .

Let us start to prove the first assertion (a) above.

To proceed, we consider Equation (16) for . Replacing and on the right-hand-side of (16) by their corresponding recursive formulas (11)-(12), we obtain

(A-1)

Expanding the squares inside the expectation and rearranging terms, we can write:

(A-2)

We need to compute the conditional expectation of each term above. Recall from Assumption 1 that and that, by our backwards induction hypothesis, . The idea is to apply the law of iterated expectations, . We can then pull out all the -measurable factors (e.g., , , , , , , , etc.) from the inside expectation . We also use the fact that and are conditionally independent given (see Assumption 1), in addition to Eq. (8).

As an example, we will explicitly show the computations of two terms in (A-2). The remaining terms follow similar arguments. Consider :

.

Now, since , we have

(A-3)

for some function . Using the well-know property

(A-4)

for a discrete r.v. and a -measurable variable , we can write:

where we used the definition and that

Similarly, consider , for . Then, by Assumption 2 and the martingale condition :

We then proceed as before:

After computing the conditional expectations therein and

substituting in the LHS of (A-2), we get the equation:

(A-5)

The expression inside the outer brackets on the right-hand side of the above equation is a quadratic function in . Simple partial differentiation and some simplifications (see (A-28) below) show that the unique stationary points of the quadratic functional are given by

where , , and satisfy the relations given in (18) with the auxiliary quantities , , and satisfying the relations given in (17).

It remains to show that and are in fact the global maxima points of the quadratic function inside the outer brackets on the right-hand side of (A-5). This is deferred to Corollary 3.

Substituting the values of above into Equation (A-5) and equating the coefficients of , , and the remaining terms that do not depend on or , on both sides of the Equation A-5,

we obtain Equations (19)-(21), which proves parts (i) and (iii) of the theorem for .

We now prove the assertion (b) stated at the beginning of the proof; i.e., we show that if statement (ii) is true for and statements (i) and (iii) are true for , then statement (ii) is true for (that is,

). We show the details for (we can similarly prove ).

First, notice that by Assumption 1-(iv), . Furthermore, by Assumption 1-(iv) again and the representation (A-3), which follows from our backward induction assumption , we can compute the variables , , and , defined as in (3), as follows:888Note that Assumption 1-(iv) actually implies that for all and not only for .

(A-6)

Therefore, it is now clear that

.

Using an identical argument, we can conclude that .

Then, since are constants, we can easily see that and are -measurable. From Eq. (19), we conclude that is -measurable random variables. Finally, we conclude the validity of the statement (ii) of the theorem for .

∎

Substituting the value of , defined in Eq. (18), into the recursive Eq. (19), we get that

(A-7)

with

(A-8)

Note that for , we have that and thus ,

as is a positive constant.

By backwards induction, to prove the lemma it suffices to show that , whenever . The remaining proof is then divided into three smaller subparts: proving that, for , (i) , (ii) , and that (iii) .

We shall prove that , which will imply that and, finally, that due to Equation ((iii)). Finally, by using the previous equation together with (A-21) we get that

and will conclude the proof.

It remains to show that . Taking the derivative with respect to ,

(A-24)

where

(A-25)

Due to (A-18), the first term of ((iii)) is nonegative. It is also easy to see that the quadratic function attaining its minimum value over any interval at the endpoints since . On the other hand, observe that . Then, by taking conditional expectation with respect to and using (A-12), we obtain the bounds

(A-26)

Therefore, to show that ((iii)) is nonnegative, it suffices to check that

To show (1), we consider the cases (a) or (b) . To show (2) above, we consider the cases (c) ; or (d) .

The only case left is when (d) . Together with (A-18), we will have

(A-27)

and, by rearranging terms,

where

is a quadratic function, opening downward due to (A-18). Furthermore, at the lower and upper bounds of (A-27), we have .

Therefore, , for all . Finally, we conclude that in the case (iv) as desired.

Refer to the proof of Theorem 1. Denote the right hand side of Equation (A-5) as . It is easy to observe that is a quadratic function of and . Setting the partial derivatives with respect to and equal to , we have that

(A-28)

Solving for and , we get that the unique stationary points and are given by

(A-29)

as pointed out in Eq. (22). To prove that the stationary point is the maximum of , we apply the second derivative test. Indeed,

because, due to Lemma 2, we have and, thus, .

It remains to show that

(A-30)

However, above is just , with defined as in (A-8), and it was shown in the proof of Lemma 2 that (see ((A-13)). The proof is now complete.

∎

Throughout, , for , are the cash holding and inventory processes resulting from adopting an admissible placement strategy , . Similarly, for , are the resulting cash holding and inventory processes, starting from time at the initial states , when setting .

First note that, for an arbitrary admissible placement strategy ,

is a supermartingale since

(A-31)

where above and are the time- cash holding and inventory for an arbitrary admissible placement strategy when and .

The equation in (A-31) follows from (16) and Corollary 3. That is,

are picked in order for (A-31) to hold true.

From the supermartingale condition, we then have that

(A-32)

The first equality in Eq. (A-32) holds because by the terminal conditions .

Next we prove that . To this end, recall from (16) and Corollary 3 that are chosen so that

for all . Hence, recalling that we set and , by induction,

It also trivially follows that

We then conclude that , which combined with (A-32) implies that

.

∎

A.2 Proofs of Section 2.3: Optimal Strategy for a General Midprice

For simplicity, we write and . For future reference, define , , and using the notation (3).

Let us start by writing the optimization problem (15) in terms of the ansatz (28):

(A-33)

We will prove the result by backwards induction. Consider the following statements:

(i)

For , we have:

(A-34)

(A-35)

(ii)

The optimal controls that solve (A-33) under dynamics (11) with terminal conditions and are given by

The random variables satisfy the following iterative equation,

(A-38)

while

(A-39)

(iv)

Equation (29) holds true (at time ) and the random variables and , as defined in Equations (17), are measurable while the random variables given by Eq. (30) are measurable.

To start, note that the statement (i) is immediate for due to the terminal condition on . The strategy that we will employ to finish the proof is the following: we will show that if statement (i) holds true for , then statements (ii), (iii), and (iv) will hold true for . In the final step, we prove that the statement (i) holds true for if (i)-(iv) holds for .

Let us start with the first step described in the previous paragraph.

Assume that statement (i) is true for . By substituting the values of and given by Equation (11)-(12) into the optimization problem (A-33) with we get,

(A-40)

Computing the conditional expectations on the right-hand side using statement (i) and the techniques used in the proof of Theorem 1, we get that

(A-41)

Then, since the function of the right-hand side is a quadratic function of the controls , it can be shown, as in the proof Theorem 1, that the optimal controls are the ones given in statement (ii) with . Furthermore, after plugging in the optimal controls; equating the coefficients of on both sides; and the independent terms on both sides, we obtain statement (iii).

To obtain statement (iv), notice that by plugging the expression for , given by Equation (18), into the Equation (20), we can rewrite as:

(A-42)

where is a collection of measurable random variables. In the same fashion, by plugging the quantities defined in Equation (A-37) into Equation (A-38), we can rewrite as:

(A-43)

Next, by substituting the value of in Equation (A-43) into the term , as defined in Equation (A-37), and then plugging this equivalent formula along with , as given by Equation (A-37) into Equation (A-36), we obtain Equation (29). To verify the measurability of and , notice that by definition (see Equations (8)-(6)), the random variables and are -measurable. Also, by definition, (see Equation (3)) the random variables and are also -measurable. All of this implies that and are measurable. However, due to the presence of the random variables , the random variables cannot be -measurable but they are certainly measurable.

Finally, all what is left is to prove that if statements (i)-(iv) hold true for , then statement (i) holds true for . Indeed, since Equations (A-34) and (A-35) hold for , then Equation (A-43) holds for . That is,

Multiplying both sides by and taking the conditional expectation with respect to , we have that

where we used that is an -measurable random variable. Thus, we have that Equation (A-34) holds for . Similarly we can prove Equation (A-35) holds for , which concludes the proof.

∎

A.3 Proofs of Section 2.4: Admissibility of the Optimal Strategy

Proof of Proposition 6. Let us define the numerators of and in (18) as and , respectively. First, we will prove the result when the price process is a martingale. In this case, all we need to show is that

First we prove that, under the Condition (2) (Equation (34)) and Condition (4) of Proposition 6, . Indeed, by Eqs. (A-10) and (A-11),

Now, recall that is -measurable (see Theorem 1), and, by assumption, depends on and only through . This means that for some function . It follows that

Since , we then conclude that .

By doing the same computations as in the set of Equations A-9, we can obtain the analogous relations to Equations (A-10) and (A-11) for and these can be used to show that in the same way as above.

Let and .

Since , it follows that

implying that and .

Thus, it suffice to show that . By assumption (4) of Proposition 6, and and, thus, we can write as

where

Recall from (A-13) that and, thus, it remains to show that the numerator is also negative. Since is a linear function of , and, by Lemma 2, , we have that

From here, it follows that for every , .

Similarly,

implying that . Note

By Equation (A-12),

,

implying that the term (I) above is negative. Further, by Lemma 2, we know that and, thus, the term (II) above is also negative.

Finally, by using our assumption (33) and Eq. (A-12), we can conclude that

the term (III) above also negative. It follows that

. Similarly, we can show that and conclude that .

For the general midprice dynamics, we need to recall Eqs. (17).

Then, under our conditions (1)-(4),

we have trivially that and .

It then follows from Eq. (29) that

, as we have already shown. This concludes the general dynamics of the midprice process.

∎

Proof of Corollary 7.

The proof follows along the same lines as the one of Proposition 6.

As before, since depends on and only through ,

and, thus, recalling (A-10)-(A-11),

it follows that when . Similarly, and we can denote and .

Since , and , it also follows that and ,

implying that and .

We are only left to prove that , but as the denominator is negative, we only need to prove that its numerator, denoted by , is also negative. However, under our conditions, we have that

which is negative because (since ), and each of the terms inside the brackets above are positive.

For the general midprice dynamics notice that our conditions and the definitions (17) readily imply that

and ,

and the proof follows as in the proof of Proposition 6.

∎

Proof of Lemma 8.

The proof will done by backwards induction. We only give the details for (the proof for is very similar).

To start, note that at time , and, hence, it trivially satisfies the condition. For the inductive step, assume that the lemma holds for . We will now proceed to prove that depends on only thorugh .

By Equation (A-7),