Generalized extremiles and risk measures of distorted random variables

Abstract

Quantiles, expectiles and extremiles can be seen as concepts defined via an optimization problem, where this optimization problem is driven by two important ingredients: the loss function as well as a distributional weight function. This leads to the formulation of a general class of functionals that contains next to the above concepts many interesting quantities, including also a subclass of distortion risks. The focus of the paper is on developing estimators for such functionals and to establish asymptotic consistency and asymptotic normality of these estimators. The advantage of the general framework is that it allows application to a very broad range of concepts, providing as such estimation tools and tools for statistical inference (for example for construction of confidence intervals) for all involved concepts. After developing the theory for the general functional we apply it to various settings, illustrating the broad applicability. In a real data example the developed tools are used in an analysis of natural disasters.

Keywords: Distortion risk measure, expected loss minimization, extremile, nonparametric estimation, risk measure, statistical functional.

1 Introduction

There is a vast literature on quantiles and expectiles, and their applications in a variety of settings, in particular as risk measures. See Artzner et al. (1999), Taylor (2008), Bellini and Di Bernardina (2017), among others. For a random variable , its th quantile (with ) can be defined as

| (1) |

see for example Ferguson (1967) and Koenker and Bassett (1978). Herein denotes the indicator function on a set , i.e., , if holds, and zero otherwise. Expectiles, introduced and first studied by Aigner et al. (1967) and Newey and Powell (1987), are defined as follows: the th expectile (with ) of is given by

| (2) |

Quantiles can also be viewed via an alternative optimization problem, namely the th quantile (with ) of (with cumulative distribution function ) is obtained via

| (3) |

and

| (4) |

with . This alternative formulation of quantiles can be found in Newey and Powell (1987). Consequently (1) and (3) (taking in the latter ) provides two approaches to obtain the th quantile of a random variable . Recently Daouia et al. (2019) studied the class of extremiles, where the th extremile of is obtained via

| (5) |

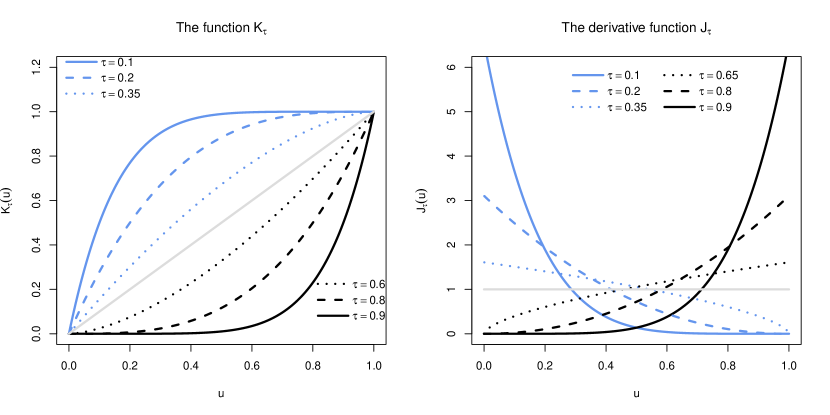

Of interest is further to note that the function is in fact the derivative of a function , which is a specific cumulative distribution function defined on the interval (see expression (9) and Figure 1).

The above observations inspire to look at a more general form of an optimization problem, and to study functionals defined via

where is the density associated to a cumulative distribution function , such that and . As shown in Section 2, this minimization problem can also be looked upon as , where denotes the random variable which has as cumulative distribution function the transformed function , and the expectation is taken with respect to this distributional distorted (shortly distorted) random variable . Moreover, with , i.e. square loss, this leads to and subsequently .

In the special case of square loss, the functional thus relates to the mean of the transformed random variable . This is linked to the probability distortions studied by Liu et al. (2021), as a particular setting of distributional transforms. The paper investigates probabilistic properties of these distributional transforms, and discusses (new) risk measures generated from such distributional transforms. In Section 5 we rely on some results of Liu et al. (2021) to study risk measures of the distorted random variable . Distortion risk measures have found widespread application in the literature, for example, in finance, economics, insurance; see Wang (1996), Wang et al. (1997), Föllmer and Schied (2002), and Cherny and Madan (2017), among others. Our general functional involves a loss function . There are numerous examples of loss functions appearing in the literature. Tables 1 and 2, as well as Section 2.4 review some of these.

As our main contribution we introduce and study a general class of functionals, which cover and generalize these in (1), (2), (3), and (5), as special cases. This generalization allows an interesting link to distortion risks as well as to risks of non-distortion type. We call this general class of functionals generalized extremiles. The main contribution of this paper consists of developing estimators for generalized extremiles, and establish consistency and asymptotic normality of these estimators, with explicit expression for the asymptotic variance. This general theory can then be applied to a variety of population target quantities. The asymptotic normality result allows to construct asymptotic confidence intervals of estimators in the general framework.

Specific optimization problems capture a number of situations studied in actuarial science, financial mathematics or statistics which are a special case of our framework. For example, our framework applies if a functional can be defined as the expected loss minimizer

| (6) |

for a suitable loss function (where we surpressed the index ), and a random variable . In this case can be the mean, quantile or expectile of the distorted random variable . Equally, one could for example consider functionals defined as the expected loss minimum

| (7) |

in which case can for example be the variance or expected shortfall of the distorted random variable . See Embrechts et al. (2021) for details and a discussion connecting risk measures of the form in (6) and (7).

While we present some general theory for risk functionals applied to distorted random variables in Section 5, our study mainly focusses on the specific case of expected loss minimizers as in (6), due to their ubiquitous nature in the literature.

The paper is organized as follows. In Section 2 we introduce the generalized extremile functionals, establish some basic properties, and explain the link with distortion risks. Section 3 deals with estimation of the broad class of generalized extremiles, and proves consistency and asymptotic normality results. These are then applied to various settings, revealing the breath of the studied functionals. Numerical studies and real data analysis are given in Sections 4 and 6. The proofs of the main theoretical results are provided in the Appendices. Some further discussions are given in a final section. Some additional information and explanations are in the Supplementary Material.

2 Generalized extremiles and their properties

In this section we introduce the concept of generalized extremile, study its basic probabilistic properties, highlight some issues toward solving the associated optimization problem, and review and discuss some loss functions. In a final subsection we discuss how generalized extremiles link up to distortion risk measures. In Section 3 we then turn to statistical estimation of generalized extremiles.

2.1 Generalized extremiles and distorted random variables

The class of functionals that we study is based on a pair of key ingredients, denoted by , consisting of a distribution function and a loss function . Their formal definitions are provided below.

Definition 2.1.

Consider a set . For every we denote by the loss function

Where appropriate we use to denote the partial derivative of with respect to .

Definition 2.2.

Let be some subset of where is some positive integer. For each denote by an absolutely continuous cumulative distribution function supported on , with density . We denote by for the set of all such .

Definition 2.3 (Generalized extremile).

Consider a cumulative distribution function , and a loss function . For a random variable we define the generalized extremile of index , denoted , as

| (8) |

Taking , with , equal to

| (9) |

with , in minimization problem (8), leads on the one hand to the concept of th quantiles when taking as loss function (see (3)), and on the other hand to the concept of th extremile with squared loss (see (5)). We refer to the class of functionals in Definition 2.3 as generalized extremiles, since it steps away from the specific choice of the pair in quantiles and extremiles, but having its inspiration strongly influenced by these two concepts.

Note that the choice of the distribution function in (9) already reveals why we allow this distribution function to depend on a parameter (vector) . From the viewpoint on quantiles expressed in (1) it is also clear why we allow the loss function to depend on a parameter . Figure 1 depicts the function and its derivative for various values of .

| loss function | sign symmetric | shift invariant | positive homogeneous | |

|---|---|---|---|---|

| of degree | ||||

| 1 | ||||

| absolute value loss | yes | yes | yes, of degree 1 | |

| 2 | with | |||

| power absolute loss | yes | yes | yes, of degree | |

| 3 | ||||

| quantile loss | no | yes | yes, of degree 1 | |

| 4 | ||||

| expectile loss | no | yes | yes, of degree 2 | |

| 5 | yes | yes | no | |

| Huber loss function | ||||

| 6 | no | no | no | |

| Esscher loss (see Van Heerwaarden et al. (1989)) |

| loss function | sign symmetric | shift invariant | positive homogeneous | |

|---|---|---|---|---|

| of degree | ||||

| G1 | no | no | no | |

| G2 | , | |||

| (see e.g. Hürlimann (2006)) | ||||

| with | no | no | no | |

| G3 | no | no | no | |

| G4 | yes | no | yes, of degree 2 | |

| (see Dickson (2005)) |

Note that in Definition 2.1 we allow a loss function to take values in . Several commonly used loss functions are restricted to take values in . Table 1 lists some of these. Table 2 provides some examples of real-valued loss functions. Throughout the paper we allow for a general loss function, and state explicitly when we restrict it to be nonnegative.

When defining generalized extremiles in Definition 2.3 we require the distribution function to be absolutely continuous admitting a density function . The latter can be relaxed, as we illustrate next.

Recall that denotes the random variable with cumulative distribution function , i.e., .

Proposition 2.1.

Consider . We then have

where the expectation on the right-hand side is taken with respect to the random variable .

Proof.

The proof is straightforward by noting that

∎

An alternative would be to define generalized extremiles as stipulated in Proposition 2.1, via

as such not requiring the existing of the density . Although this would be a slightly broader definition, it would make it more tedious to establish (asymptotic) properties when dealing with statistical inference for the studied functionals. The latter is the main goal of the paper.

In Tables 4 and 5 (see later) we indicate for each of the loss functions in Tables 1 and 2 this alternative view, with focus on the loss function applied to the random variable . Table 3 lists a selection of distribution (distortion) functions (with their associated densities).

| distrib. function or distortion function | density | bounded density | |

| or | |||

| and | |||

| 1 | yes | ||

| uniform distr. | |||

| 2 | as in (9) | as in (4) | yes |

| 3 | possibly unbounded | ||

| in 0 and/or 1 | |||

| Beta distr. | bounded if | ||

| 4 | possibly unbounded | ||

| Kumaraswamy distr. | in 0 and/or 1 | ||

| bounded if | |||

| 5 | yes, for | ||

| or | |||

| or shortly | |||

| expected shortfall | |||

| 6 | for on | ||

| unbounded in 1 for | |||

| Wang Transform risk measure | unbounded in 0 for | ||

| 7 | |||

| Proportional Hazard transform | unbounded in 1 | ||

| 8 | , with | bounded | |

| minvar (see Cherny and Madan (2017)) | |||

| 9 | , with | unbounded in 1, | |

| maxvar (see Cherny and Madan (2017)) | unless | ||

| (but then ) | |||

| 10 | , with | unbounded in 1 | |

| minmaxvar (see Cherny and Madan (2017)) | |||

| 11 | , with | unbounded in 1 | |

| maxminvar (see Cherny and Madan (2017)) | |||

| 12 | yes, on | ||

| cumul. distr. function, with log-concave | possibly unbounded | ||

| Junike’s distortion function (see Junike (2019)) | in 0 or 1, depending on | ||

| 13 | yes | ||

| bivariate copula | |||

| (see Yin and Zhu (2018)) |

2.2 Generalized extremiles: properties

Before stating some probabilistic properties of generalized extremiles, we first define some properties of loss functions, as well as the notion of a dual of a cumulative distribution function .

Definition 2.4.

Consider a loss function . It is called

-

1.

sign symmetric if ;

-

2.

shift invariant if for all ;

-

3.

positive homogeneous of degree if for all and .

In Tables 1 and 2 we indicate for each of the listed loss functions whether they possess the property of sign symmetry, shift invariance and positive homogeneity.

For a given cumulative distribution function in the set it is of interest to consider its dual.

Definition 2.5.

Given we define its dual as .

It is clear that the dual function is again part of the set . Furthermore, the dual of is equal to .

The proofs of all propositions in this section can be found in Appendix A. Proposition 2.2 provides sufficient conditions under which the expectation in Definition 2.3 is finite. The proof is straightforward and omitted.

Proposition 2.2.

If the cumulative distribution function is differentiable with bounded density and for all then

for all .

Remark 2.1.

The condition on the loss function (and ) in Proposition 2.2 is very mild, and fulfilled for several commonly used loss functions. In case of the absolute value loss the reverse triangle inequality yields and hence for all random variables . In case of the square loss we have and hence for all random variables with .

From Remark 2.1 it also becomes clear why the term is included in (8), whereas it does not depend on the argument . Due to the inclusion of that term we have, for example, that quantiles obtained by taking and , exist for all random variables. Similarly, expectiles of only require the finiteness of the first absolute moment of .

Propositions 2.3, 2.4 and 2.5 establish the behaviour of generalized extremiles when the underlying random variable is transformated either by taking the negative of it (Proposition 2.3), or by an affine transformation (Proposition 2.4), or by applying a strictly monotone function to it (Proposition 2.5). From these propositions we can conclude that generalized extremiles have similar properties as quantiles and expectiles, among others.

Proposition 2.3 (Sign symmetry).

Denote by a sign symmetric loss function. If the distribution function of is continuous then we have

Proposition 2.4.

Consider scalars and , and a random variable such that . If the loss function is shift invariant, positive homogeneous of degree and if

| (10) |

then

If in addition the loss function is sign symmetric, is continuous and (10) holds for and then

Proposition 2.5 (Monotone transformations).

Suppose is a strictly increasing function and hence measurable function, then

where . If is strictly decreasing and is a random variable with continuous then

When a random variable is symmetric and has finite expectation it is possible to express this mean in terms of differences or sums of generalized extremiles, as stated in Proposition 2.6.

Proposition 2.6 (Mean symmetry).

Denote by a shift invariant loss function. If is finite and is symmetric, i.e., , then

If in addition is a sign symmetric loss function and the distribution function of is continuous then

For two random variables and , it is interesting to know how the generalized extremile of their sum, i.e., , relates to the sum of the generalized extremiles of each of the random variables. Proposition 2.7 below provides some answer to this question, establishing the property of comonotonic additivity for the absolute value and square loss functions.

Proposition 2.7 (Comonotonic additivity).

Denote by and two random variables that have a comonotonic dependence structure, i.e., . If is either the absolute value loss or the square loss we have (assuming the considered generalized extremiles are finite) that

A final result states the equivalence of an injective transformation of a generalized extremile and a generalized extremile of the same random variable with a transformed loss function. It is similar to results in (Gneiting, 2011, see Theorem 4) and in (Osband, 1985, see p. 9) known as revelation principle.

Proposition 2.8 (Revelation principle).

Let be an injective function. Define , then

2.3 Towards solving the minimization problem

When it comes to finding a generalized extremile, defined in (8), Proposition 2.1 is a good starting point, showing that we need to find a minimizer of with respect to . Proposition 2.9 below provides a way to find such a minimizer, and states sufficient conditions on the pair .

Proposition 2.9.

Let be a function such that is (strictly) convex for every and . Additionally, assume that both and are differentiable functions. Under these conditions, the function is (strictly) convex, and the generalized extremile is equal to any value for which

| (11) |

provided the derivative exists. When the mapping is strictly convex, there exists at most one value fulfilling (11). The existence of such a value is ensured when is convex and is coercive.

Proof.

To solve the minimization problem we want to find the value that minimizes

By Boyd and Vandenberghe (2004), p. 79, we know that is convex in if is convex for every .

It is clear that strict convexity of implies that is also strict convex and hence the minimum is unique (see Theorem 3.4.4 on p. 114 in Niculescu and Persson (2006)).

The existence of a value follows by Theorem 4.4 on p. 638 in Herrmann et al. (2018).

∎

In Proposition 2.9 uniqueness of solving (11) is guaranteed when is a coercive function. Some sufficient conditions for this to hold are discussed in the following remark.

Remark 2.2.

Consider a random variable (with associated probability measure ) such that is finite. Additional to convexity, assume that is (i) coercive for almost all , i.e., , and (ii) bounded from below, i.e., , such that -a.s. Then also is coercive. To see this consider a sequence such that and define to have -a.s. and due to the coercivity of . A slight modification of the monotone convergence theorem, see Feinstein (2007), then implies , showing that is coercive. The result is now applicable in the context of Proposition 2.9 if the necessary conditions apply for the choice of .

As is clear from the above result, convexity of the function will be an important requirement when it comes to calculating generalized extremiles. In addition it also makes it transparant that interchanging integral and differentiation operators will be helpful. For any random variable (not necessarily absolutely continuous) and any distribution function (not necessarily admitting a density) the next theorem (stating a type of Leibniz rule) is helpful.

Theorem 2.1 (see Klenke (2013), Theorem 6.28, p. 142).

Denote the measure induced by . Suppose that a loss function satisfies the following properties.

-

•

For every , the map is integrable (with respect to the measure );

-

•

For -almost all , the map is differentiable with derivative ;

-

•

There is an integrable function (with respect to the measure ) such that for all and -almost all .

Then for all we have

For absolutely continuous with density function , and admitting a density , the adaptation of this theorem is as follows.

Theorem 2.2.

Consider an absolutely continuous random variable , and a cumulative distribution function with density . Suppose that a loss function satisfies the following properties.

-

•

For every , the map is integrable;

-

•

For almost all , the map is differentiable with derivative ;

-

•

There is an integrable function (with respect to the measure ) such that

for all and almost all .

Then for all we have

In Tables 4 and 5 we return to the loss functions listed in respectively Tables 1 and 2, and now focus on the properties of convexity and differentiability of these loss functions.

| loss function | alternative view | convex | differentiability | derivative | |

| from | in | in | with respect to | ||

| 1 | yes | yes, for | |||

| absolute value loss | |||||

| 2 | with | for | yes, | depends on the | |

| power absolute loss | if | value of | |||

| 3 | th quantile of | yes | yes, for | ||

| quantile loss | |||||

| 4 | th expectile of | yes | yes, | ||

| expectile loss | |||||

| 5 | (⋆1) | yes | yes, for | ||

| such that | |||||

| Huber loss function | |||||

| 6 | yes | yes, | |||

| Esscher loss |

(⋆1): Value c for which ).

| loss function | alternative view | convex | differentiability | derivative | |

|---|---|---|---|---|---|

| from | in | in | with respect to | ||

| G1 | yes | yes, for all | |||

| G2 | , | yes | yes, | ||

| with | |||||

| G3 | value for which | yes | yes, for all | ||

| G4 | yes | yes, | |||

| expected value | |||||

| premium principle |

2.4 Examples

Complementary to the loss functions listed in Tables 1 and 2 we review here some loss functions that have been proposed in recent literature, illustrating as such the broad framework we consider. Some more loss functions are given in Section S1 in the Supplementary Material (non exhaustive list).

2.4.1 Nonnegative valued loss functions

Adaptive quantile loss function for censoring

In the context of quantile estimation under right random censoring,

De Backer et al. (2019) established an approach based on considering a loss function that adapts to the cumulative distribution function of the censoring variable :

| (12) |

Note that the mapping is in general not convex, nor is it monotone. In case of no censoring, i.e. when , the adapted loss function reduces to the usual quantile loss function.

M-quantile loss

For a function , consider the loss function

This is the M-quantile loss function. Taking leads to the power absolute loss function, also called quantiles as defined in Chen (1996). See also Jiang et al. (2021). Obviously, the qualitative properties of depend on the qualitative properties of the function .

Generalized quantile loss

An extension of the M-quantiles are obtained by involving two different functions and . Namely consider , convex and strictly increasing functions satisfying

The generalized quantile loss function is then

leading to the th generalized quantile of a random variable. See Bellini et al. (2014). The qualitative properties of the generalized quantile loss depend on these of the functions and .

In Mao and Cai (2018), the authors further generalized this class by using rank-dependent expected utility (RDEU) theory. This corresponding class of generalized quantiles based on RDEU theory is given by

| (13) |

The functions are two distortion functions on , which means they are right-continuous and increasing with and for , with no jumps at and . Furthermore, and are nondegenerate increasing convex functions on . When we can describe (part of) this class using the generalized extremile framework. Indeed, to do so, we have to take

Here we used the notations: and .

Generalized shortfall loss

In Mao and Cai (2018) and Mao et al. (2023), the authors study generalized shortfall risk measures. These are obtained by replacing with their derivatives in (13). Just as before, part of these generalized shortfall risk measures can be described in our generalized extremile framework when .

Loss function for trimmed mean

The Hampel family of functions (see Hampel et al. (1986)) is defined as

where the function depends on parameters and , with . This is a non-convex function.

A limiting case of this family is obtained by letting and taking the limiting value , leading to the loss function (see p. 79 in Huber (1964))

appearing in the context of trimmed means.

Note that the function

is quadratic in around , but attributes always the same constant value () when is such that . Consequently the function is not convex.

2.4.2 Real-valued loss functions

Various functionals involving moments

Let be an interval. Consider and measurable functions. Let be a strictly convex function with subgradient . Let be a random variable supported on such that , , , and exist and are finite.

Consider the loss function

The corresponding generalized extremile equals

We refer to Gneiting (see e.g. Theorem 8 on p. 754 in Gneiting (2011)) for an in-depth discussion.

Taking , and leads to the special case of

In this special case the loss function is (see also p. 83 in Heilmann (1989)). This is a convex function in for , and the derivative of exists for every and is given by

.

Consider ; and take and . The interpretation of the resulting generalized extremile

for different weighting functions is discussed in Furman and Zitikis (2009).

2.5 Square loss and distortion risk measures

A special subclass of functionals of generalized extremiles is obtained when focussing on the square loss . Indeed, as already pointed out in Section 1, we know that where is distributed with cumulative distribution function . This implies that

| (14) |

where . An expression as in (14), with , a non-decreasing function and and , is termed a distortion risk of . For this distortion risk to be a coherent risk measure (see for example Wang (1996) and Artzner et al. (1999)) one needs to require in addition that is a concave function. See, for example, Wang et al. (1997) and CaiWangMao2017. Note that generalized extremiles, in case of square loss function, can be seen as a distortion risk measure with distortion function . This implies that

Note that concavity of is equivalent with convexity of . Therefore not every coherent distortion risk measure is necessarily part of our class. If the function is differentiable then . In summary, the class of generalized extremiles contains part of the distortion risk measures, but it also contains non-distortion risk measures, for example, expectiles. Table 3 lists several distortion risk measures that can be seen as part of our general class of functionals.

3 Estimation

Based on an i.i.d. sample from , with unknown distribution function , the aim is to estimate the generalized extremile defined in Definition 2.3, and this for a general pair . We firstly focus on the setting of a square loss function, but with general ; and secondly treat the setting of a general pair . The reason is that in the former setting estimation of the generalized extremile is simpler, and subsequently establishing (asymptotic) properties for it is somewhat less involved.

3.1 Square loss and general distribution function

As discussed in Section 2.5 in case of square loss the generalized extremile reduces to

| (15) |

An estimator of (and hence of the corresponding distortion risk) can be easily derived from (15). Denote by the th order statistic in the random sample of size . Let be the empirical cumulative distribution function (with factor instead of ), and denote by the corresponding empirical quantile function, i.e. for , , where is chosen such that . A plug-in type of estimator for is then

where it is thus readily seen that is proportional (with factor ) to an -statistic with weights .

A second estimator, denoted , relies on the fact that in case of square loss we have

leading to the estimator

A third estimator is obtained by solving the empirical minimization problem. That is by solving

Differentiating the objective function with respect to and equating this to zero gives

We thus obtain a new M-type estimator

Note that, since we work with the empirical cumulative distribution function rescaled with the factor , which takes values between and , when evaluated in the observations , we avoid evaluation of the density in the endpoints 0 and 1.

All the above three estimators are consistent and have the same (first order) asymptotic distribution. The proofs of the results stated in this section are given in Appendix B.1.

Theorem 3.1.

Given is a fixed index . Assume that is differentiable with density . Let be any of the two estimators or .

-

(i)

[Consistency] Assume for some . Let be continuous almost everywhere. If for some

for some , then as .

If in addition is Lipschitz continuous or bounded (uniformly) on then as -

(ii)

[Asymptotic normality result] Assume for some . Suppose exists and is continuous on . Furthermore, suppose there exists some such that

and

Then as where

(16) If in addition is Lipschitz continuous or bounded (uniformly) then as .

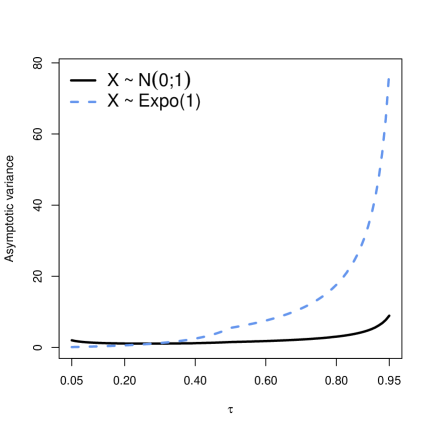

When is bounded, we obtain the almost sure convergence for any random variable with a finite absolute th moment (for some ). In particular, when , that is the case of extremiles, we obtain the same result as in Theorem 1(i) on p. 1370 of Daouia et al. (2019). In the case of extremiles, also the function is bounded. Hence, also the asymptotic normality result in Theorem 1(ii) on p. 1370 of Daouia et al. (2019) is included as a special case of Theorem 3.1 in our more general framework.

3.2 General loss functions and distribution functions

We now turn to the general setting of any pair . From now on we assume that is an absolutely continuous random variable, i.e., has an associated density function . We only consider loss functions for which By Proposition 2.9 we know that solving the minimization problem is equivalent to finding a value for which

Since is an absolutely continuous random variable, Theorem 2.2 then ensures the right-hand side equals

We are now in the setting of an -functional problem: finding a value such that

Given a random sample from , the -estimator is defined as the solution to

However, the appearance of leads to an extra complication. Since is unknown we replace it by a consistent estimator for it, for example, by its empirical version . The estimator is then defined as the value for which

If there is no such value , then we define as the value minimizing . If, in practice, there are multiple values of for which , we take the smallest of them.

In what follows we establish the consistency and the asymptotic normality of the estimator . Before stating the results, we introduce some assumptions, needed in various parts of the theoretical results.

-

(A1)

-

1.

is an absolutely continuous random variable;

-

2.

is finite for every and has a unique root ;

-

3.

is convex for every ;

-

4.

is measurable for every .

-

1.

-

(A2)

.

-

(A3)

There exist functions with non-decreasing and left continuous for such that for every and .

-

(A4)

There exists an , such that for with from (A3).

-

(A5)

There exist constants such that with from (A4).

-

(A6)

has a continuous derivative on . Furthermore, with from (A4) there exist such that and .

-

(A7)

is continuous except at possibly a finite number of points.

-

(A8)

-

1.

is bounded on ;

-

2.

is locally uniformly continuous except at a finite number of points.

-

1.

-

(A9)

is differentiable at with derivative .

-

(A10)

For any sequence as

Throughout this section we assume the existence (i.e. finiteness), as well as uniqueness, of the target quantity of interest (also shortly denoted as ).

Appendix B.2 contains the proofs of the results stated in the various lemmas in this section. Lemma 3.1 expresses the consistency of when using a general estimator of , satisfying some condition. Note that this lemma requires the Lipschitz continuity of which might be a quite restrictive condition. For this reason, we also prove the consistency of , when using as an estimator for the empirical distribution function. This then allows to show consistency under weaker conditions on . See Lemma 3.2.

Lemma 3.1.

Suppose Assumption (A1) and Assumption (A2) hold. Furthermore, assume that is Lipschitz continuous. Then for any estimator of for which as , we have that as .

Remark 3.1.

(i)

Suppose in addition to the assumptions of Lemma 3.1 that is continuous in in a neighborhood of , for every . Then has a root and this root is equal to .

(ii) The requirement on the nonparametric estimator for is satisfied by the usual empirical distribution function (or its rescaled version ). Indeed, this is expressed by the Glivenko-Cantelli theorem (see p. 62 in Serfling (1980)).

In Lemma 3.2, and in all subsequent results, we work with the estimator . This allows us to weaken the assumption on the density .

Lemma 3.2.

Suppose Assumptions (A1), (A3), (A4), (A5) and (A7) hold, then as .

We next turn to establishing an asymptotic normality result for the estimator . We therefore first prove the asymptotic normality of . In Lemma 3.3 this is done under, among others, the assumption that the density has a continuous derivative. In Lemma 3.4 this assumption is relaxed. To ease calculations in practice, we provide two equivalent expressions for the asymptotic variance in Lemma 3.3 (and subsequently Lemma 3.4).

Lemma 3.3.

Suppose Assumptions (A1), (A3), (A4) and (A6) are satisfied. Then as , where

| (17) | ||||

| (18) |

As Lemma 3.3 does not allow for a discontinuous density , it does not cover the case for corresponding to expected shortfall (entry number 5 in Table 3). The following result covers this specific case.

Lemma 3.4.

Suppose Assumptions (A1), (A3), (A4) with and (A8) are satisfied. Then as .

We can now state (and prove) the asymptotic normality result for .

Theorem 3.2.

Proof.

Remark 3.2.

(i)

Assumption (A10) is a kind of equicontinuity assumption.

In Section S2 of the Supplementary Material it is shown that this assumption is satisfied for several loss functions, among which the square loss, the Esscher loss (entry number 6 in Table 1), and the loss function with entry G2 in Table 2.

(ii) In Section 3.1 we established an asymptotic normality result for the considered estimators, in the specific setting of square loss (). See Theorem 3.1. Theorem 3.2

on the other hand is for general loss functions.

It is easily seen that in case of square loss the expression for the asymptotic variance in (18) reduces to that in (16). Indeed, note that for the square loss function: and . A simple substitution into (18) leads to (16). A setting with square loss was also considered in Jones and Zitikis (2003).

Although the authors consider another estimator, the asymptotic variances coincide. Since Jones and Zitikis (2003) (see pp. 49–50) also discuss a consistent estimator for the asymptotic variance, this estimator can also be used in our context.

3.3 Applications of the asymptotic normality result

The asymptotic normality results established in Theorem 3.1(ii) and Theorem 3.2 allow, for example, to create asymptotic (pointwise) confidence intervals for the generalized extremile .

In this section, we apply Theorem 3.2 for various loss functions, establishing as such results on the corresponding estimator for the generalized extremile under study. In each of the illustrative examples, we focus on the asymptotic normality result and in particular the expression for the asymptotic variance.

We start by looking into the two loss functions encountered when estimating quantiles. Recall from Section 1 that quantiles of can be obtained using at least two different pairs .

| (19) | |||||

| (20) |

where in approach 2, one takes to obtain the th quantile of .

In Corollary 3.1 we consider an absolute value loss function, whereas in Corollary 3.2 we apply Theorem 3.2 with the loss function . Before stating the first corollary we make an important remark.

Remark 3.3.

Consider the absolute value loss The derivative with respect to of this function is not defined in the point . In order for to be left continuous (see Assumption (A3)), we will choose to be the right-hand side derivative. In the specific case of the absolute value loss, this means . This choice for the right-hand side derivative is justified since we are integrating with respect to . Meaning that the integrand is uniquely defined almost everywhere.

Corollary 3.1.

Consider the absolute value loss function Consider a random variable and a cumulative distribution function such that the assumptions of Theorem 3.2 are satisfied. Then the asymptotic variance reduces to

| (21) |

where denotes the median of a random variable with cumulative distribution function .

Proof.

We have , with thus non-increasing. This means we can take and for Assumption (A3). When integrating a function, say , with respect to this measure, we get

This implies . Further, we have that

from which it follows that , and also .

Furthermore . In conclusion, leads to expression (21). ∎

Remark 3.4.

When taking , expression (21) leads to the asymptotic variance for the quantile estimator, obtained via approach 2 (see (20)). It is easily seen from (9) that and the th order quantile of . Hence for the setting of approach 2 in (20), expression (21) reduces to

| (22) |

which is the well-known asymptotic variance for the empirical quantile estimator (see p. 77 in Serfling (1980)).

Corollary 3.2.

Consider the quantile loss function (with ). Consider a random variable and a cumulative distribution function such that the assumptions of Theorem 3.2 are satisfied. Then the asymptotic variance reduces to

| (23) |

Proof.

We have (see also Table 4), with non-increasing. This means we can take and for Assumption (A3). If we integrate with respect to this measure then

For this reason . Furthermore,

leading to , the th quantile of the random variable . Moreover, . This concludes the proof. ∎

Remark 3.5.

The asymptotic variance stated in Corollary 3.2 can be estimated by

| (24) |

where is the empirical cumulative distribution and a kernel density estimator.

Corollary 3.3 results from applying Theorem 3.2 with the loss function , i.e. the expectile loss function (entry number 4 in Table 1).

Corollary 3.3.

Consider the loss function (with ), corresponding to expectiles. Consider a random variable and a cumulative distribution function such that the assumptions of Theorem 3.2 are satisfied. Then the asymptotic variance reduces to , where

Proof.

We have , for which is non-increasing. This means we can take and for Assumption (A3). If we integrate with respect to this measure, then we obtain

This explains the factors in the numerator. By expanding the factors we obtain the second expression for the numerator . Here we take into account that by changing the order of integration

This explains the term with factor . ∎

Remark 3.6.

When using the expectile loss function, the corresponding generalized extremile equals the th expectile of . Hence, if we consider the uniform cumulative distribution function, we can use our estimator to estimate the th expectile of . Doing so, our estimator coincides with the estimator studied in Holzmann and Klar (2016). The latter authors also established the asymptotic normality of their estimator (see p. 2359 in Holzmann and Klar (2016)), with asymptotic variance given by

| (25) |

where

In Section S3 of the Supplementary Material we prove that the asymptotic variance as stated in Corollary 3.3, equals that in (25), for the specific case that . Hence the asymptotic normality result for expectiles is obtained as special case of our Theorem 3.2 and Corollary 3.3.

Applying Theorem 3.2 to the loss function establishes the asymptotic normality results for the proposed estimator for .

Corollary 3.4.

Consider the loss function , for . This corresponds to . Consider a random variable and a cumulative distribution function such that the assumptions of Theorem 3.2 are satisfied. Then the asymptotic variance equals

where

and

Proof.

We calculate using (18), where we use with

non-decreasing and left-continuous in . First, we find an expression for . This is done by observing that , consequently for . For the result follows by noting that

Similarly, we obtain the stated expression for . Furthermore, it is clear that , and application of Theorem 3.2 concludes the proof. ∎

4 Simulation study

4.1 Aims of the simulation study, and simulation models

In this section we investigate the finite-sample behaviour of the estimator of the generalized extremile . We conduct five small simulation studies considering different pairs for , and hence looking into estimating different quantities. Tables 6 and 7 summarize the settings for the various parts (simulation studies (St) 1–5). The various scenarios have the following aims: investigating

-

St1

the performance of for different choices of ;

-

St2

the performance of for different choices of parameters ;

-

St3

estimation of quantiles via two different pairs ;

-

St4

the asymptotic normality result for quantile estimation under censoring;

-

St5

the asymptotic normality result when using as loss function (see Corollary 3.4).

In each simulation study we draw 500 samples of size from the simulation model. We adapt various ways to present the results. We evaluate the finite-sample performance of by reporting on the bias, variance and Mean Squared Error (MSE) across the Monte Carlo runs. For illustration of the sampling distribution of we present a kernel density estimate based on the 500 values for .

| Simulation study (St) | |||||

|---|---|---|---|---|---|

| St1 | St2 | St3 | St5 | ||

| expectile | expectile | absolute value | quantile | ||

| loss | loss | loss | loss | loss | |

| same as in St1 | |||||

| in (9) | in (9) | same as in St2 | |||

| same as in St1 | |||||

| or | |||||

| same as in St1 | same as in St1 | ||||

| adapted quantile | |||||

|---|---|---|---|---|---|

| loss; see (12) | |||||

4.2 Simulation results

Simulation study 1

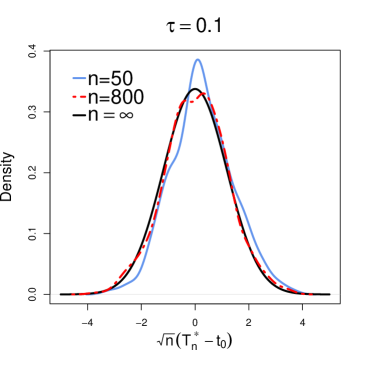

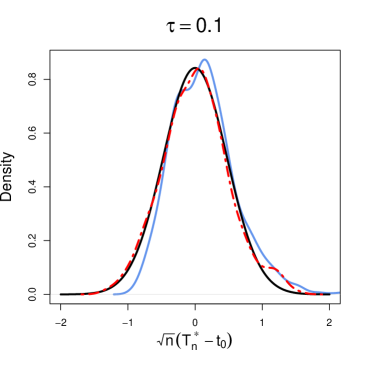

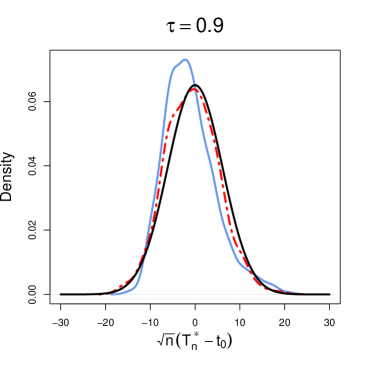

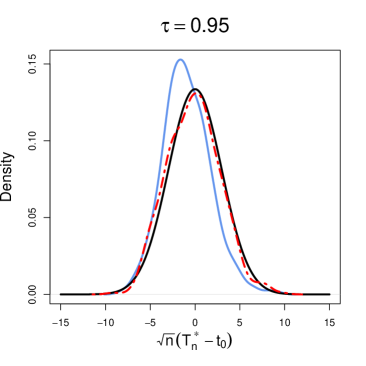

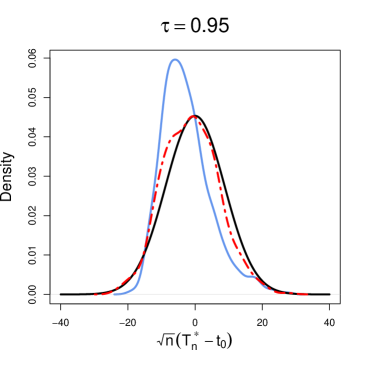

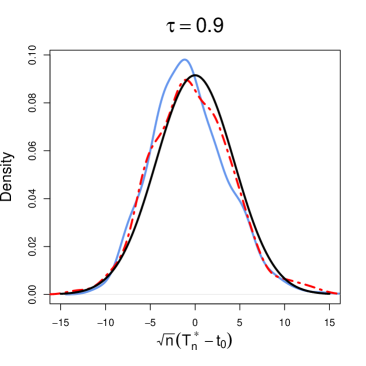

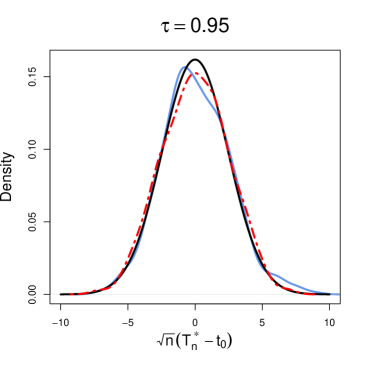

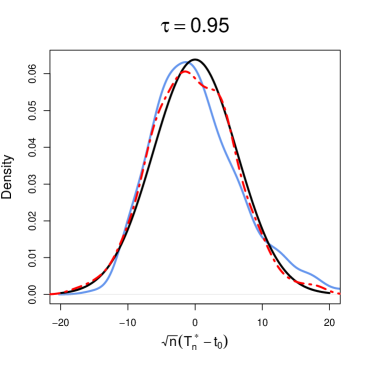

Figure 2 shows a kernel density estimate of for . The left (respectively right) panels are for samples drawn from (respectively ). Presented are the results for sample size (blue lines) and (red lines), together with the normal density with variance equal to the asymptotic variance of Theorem 3.2. Note that with increasing the kernel density estimates approach the asymptotically normal density. To be noted is also that for values of closer to 1, the variance of the sampling distribution of as well as the asymptotic variance is largest (see the scale of the horizontale axis). Table S1 in the Supplementary Material provides the estimated bias, variance and MSE of the estimator .

Simulation study 2

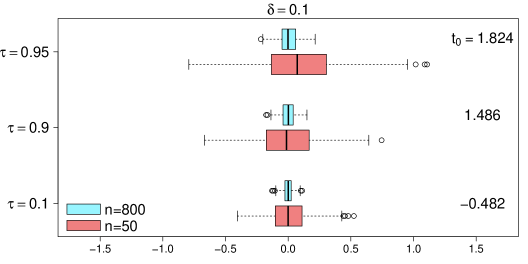

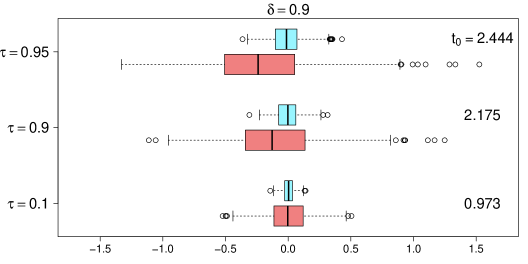

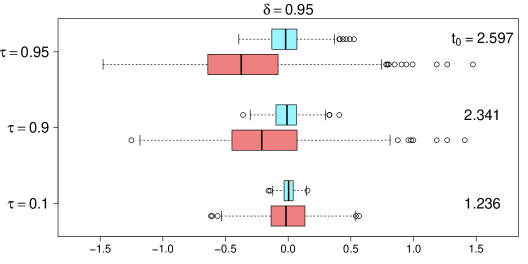

In this part, the function corresponds to the distortion function of expected shortfall (see entry 5 in Table 3). Several values of the parameters of respectively the distribution and the loss function are considered. The simulation results are summarized in Figure 3 as boxplots of (with the true generalized extremile) over all Monte Carlo runs. The value of is indicated on the right-hand side of each plot. Note that when passing from sample size to all boxplots become narrower, and more positioned around zero. For , the median is close to zero for the cases where and/or . In all cases the boxplots are relatively symmetric. As already seen from Figure 2, for fixed , our estimates are more variable for larger values of . Similarly, for fixed , the estimates are more variable for larger .

Simulation study 3

As already mentioned at the start of Section 3.3 quantiles can be estimated from two viewpoints, i.e. using two different pairs . We present simulation results of the two resulting estimators:

-

Estimator 1: based on using and the quantile loss function ;

-

Estimator 2: based on using and absolute value loss function .

By Corollaries 3.1 and 3.2, and Remarks 3.4 and 3.5 we know that both estimators are asymptotically equivalent to the empirical quantile estimator.

Table 8 lists the mean squared error (MSE) for the two estimators, together with their Monte Carlo approximated variance (between brackets). The results for both estimators for sample size are identical, except for quantile level . When the sample size increases to , the estimators are indistinguishable when only considering the mean squared error. The difference between the two estimators for quantile level is due to a larger bias of estimator 1.

| Estimator 2 | ||

| 1.26 | ||

| Estimator 1 | ||

| 0.01 | ||

| Other | Identical to results for Estimator 2 | |

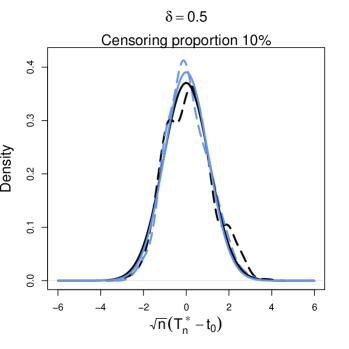

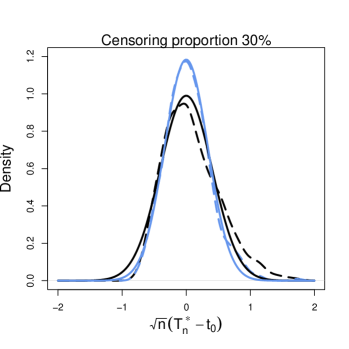

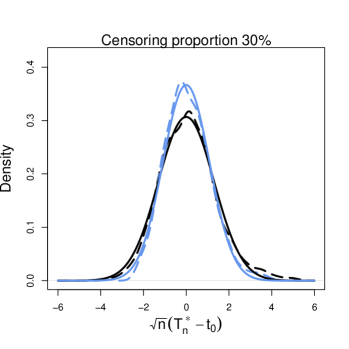

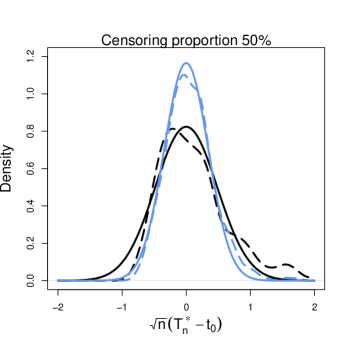

Simulation study 4

The adaptive loss function for quantile estimation in case of censoring was briefly discussed in Section 2.4. This loss function is not convex, and hence does not satisfy the conditions stated in Theorem 3.2. Since these are however sufficient conditions, we might wonder whether the finite-sample distribution can nevertheless be well approximated with the asymptotic normal distribution as stated in the theorem.

In the right-random censoring setting, the variable of interest is possibly censored by a variable . We are interested in a th quantile of , but only have data of the form , where and . Given a sample from , we can use our estimator to estimate such a th quantile of . Table 7 summarizes the various elements of the simulation model.

When calculating the estimator we have to deal with the non-convexity of and . Globally minimizing is not feasible, and instead we implemented the following procedure. Based on a sample from , we construct a sequence of values ranging from to . More precisely we take a equispaced grid of points, with an increment of 0.01, i.e. for , with , we have . We then search for the smallest value in this sequence, say , which satisfies the following inequalities

This requires difference quotients (discrete slopes) to be strictly positive in an interval past a given point. In this manner, we search for a (local) minimum. By considering multiple subsequent difference quotients, we avoid selecting a value due to a small spike in the function .

Recall that denote respectively the density and the cumulative distribution function of . Similarly, we use the notations for these quantities for the censoring variable . The asymptotic variance stated in Theorem 3.2 equals in this case

| (26) |

When there is no censoring (meaning that for all ), this expression reduces to the asymptotic variance of the empirical quantile estimator.

Sander (1975) estimated a quantile for censored data relying on the Kaplan-Meier estimator for a distribution function. We refer to this quantile estimator as the Kaplan Meier-based (KM-based) estimator. The author established asymptotic normality for the estimator (see Corollary 1 on p. 5 in Sander (1975)). The asymptotic variance of this estimator equals

| (27) |

Again, in case of no censoring, this asymptotic variance reduces to the one of the empirical quantile estimator.

| MSE Loss-based estimator | MSE KM-based estimator | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| () | () | () | () | ||||||

| () | () | () | () | ||||||

| () | () | () | () | ||||||

| () | () | () | () | ||||||

| () | () | () | () | ||||||

| () | () | () | () | ||||||

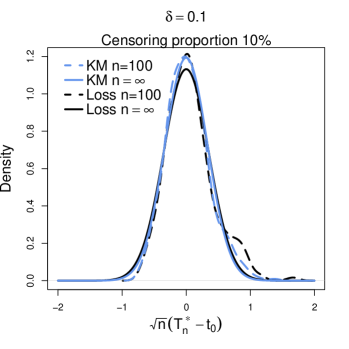

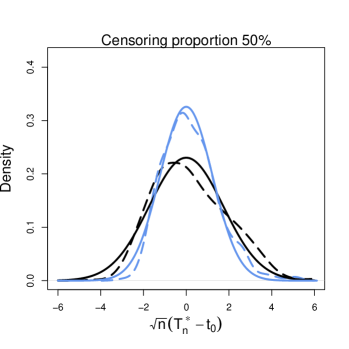

Figure S2 in the Supplementary Material depicts the density estimates of the loss-based estimator , as well of the KM-based estimator. The figure also superimposes the asymptotic normal distributions with asymptotic variances as in (26) and (27) respectively. These results confirm the appropriateness of the asymptotic variance (26), and seem to indicate that the asymptotic normality result of Theorem 3.2 holds, even in this case where the loss function does not satisfy the stipulated conditions.

Some findings from the simulation results are as follows.

-

The KM-based estimator shows a smaller (finite-sample) variance compared to the loss-based estimator.

-

For the different censoring proportions, the asymptotic variance of both estimators is larger when is .

-

The finite-sample variances of both estimators increase with increasing censoring proportion.

Table 9 provides a summary of bias, variance and MSE for both estimators, and confirms the visual findings from Figure S2.

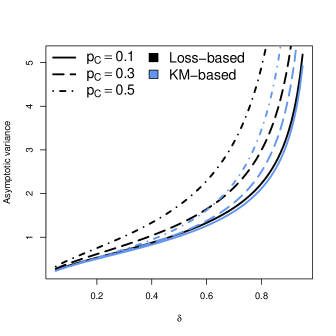

Figure 4 presents the asymptotic variances in (26) and (27) for different quantile levels and different censoring proportions . As to be expected the (asymptotic) variances of both estimators increase as the censoring proportion increases. For small censoring proportion the asymptotic variances are almost identical. As the censoring proportion increases, so does the difference between the two asymptotic variances. For larger censoring proportions it becomes more advantageous to use the KM-based estimator. We end this simulation regarding censored quantiles by noting that in De Backer et al. (2019), the authors established, in a linear regression setting, asymptotic normality of an estimator using the adapted quantile loss. They coped with non-convexity by using a majorize-minimize (MM) algorithm.

Simulation study 5

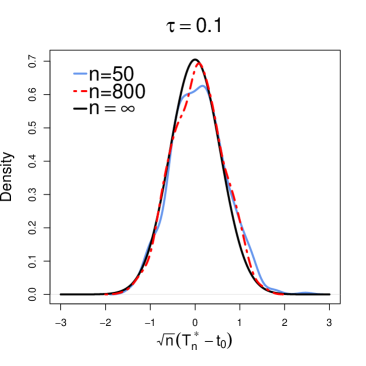

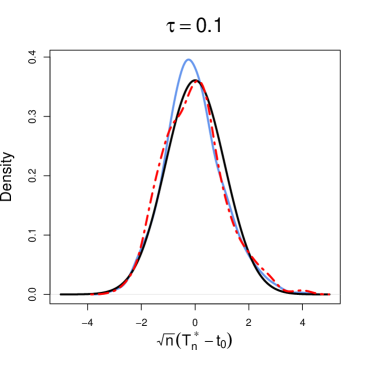

With this simulation we aim to illustrate the result in Corollary 3.4. Figure 5 shows density estimates (based on 500 values) of for . The left panels are for samples drawn from . The right panels are for samples drawn from . The normal density with variance equal to the asymptotic variance is presented as the black lines.

Note that even for small sample size , there is a good correspondence between the finite-sample distribution and the asymptotic disribution. Recall from Section S2.2 that the equicontinuity assumption of Theorem 3.2 is satisfied under the sufficient condition that is Lipschitz continuous. Despite the fact that this not holds for in this simulation model, the asymptotic normality result still seems to hold.

5 General considerations for risks of distorted random variables

In this section we establish some general properties about risk measures . In the real data example in Section 6 we refer to these results. For notational simplicity we simply write instead of in this section. Consider a random variable defined on the probability space , with the sigma-algebra, and the probability measure. Denote by the linear space of random variables defined on , and for a given consider a risk measure

Before stating the main result of this section, we recall some basic properties of a risk measure .

-

A risk measure is called monotone if: .

-

A risk measure is called translation invariant if: , .

-

A risk measure is called positive homogeneous if: , , such that .

-

A risk measure is called subadditive if: it holds that .

A risk measure is coherent when it is monotone, translation invariant, positive homogeneous and subadditive.

Theorem 5.1 investigates risk measures for the distorted random variable . In establishing some of these statements, we can rely on results of Liu et al. (2021).

The proof of the theorem is provided in Appendix C.

Theorem 5.1.

Denote by a distortion function and by a risk measure defined on , the linear vector space of random variables. For two random variables and in the domain of we then have:

-

(i)

If is positive homogeneous, then also for .

-

(ii)

If is translation invariant, then also for .

-

(iii)

If is monotone and then .

-

(iv)

Suppose is coherent. If is convex, then the composition (distortion) risk measure is also coherent (and thus in particular subadditive), i.e. for all and , we have .

-

(v)

Denote by and two distortion functions such that for all . If is monotone, then . Specifically for we have .

-

(vi)

Suppose that the risk measure depends on a parameter , and denote the risk measure by . If is monotone increasing in , then so is the composition risk measure .

Risk measures defined as the minimizer of an expected loss minimization procedure as in (6) avoid unjustified risk-loading under general conditions. If is such that for all then we have for an almost surely constant random variable , i.e., for some , that . This property also carries over to the distorted version , where we have due to and . As such we have and hence also .

6 Real data example: US disaster data 1980-2023

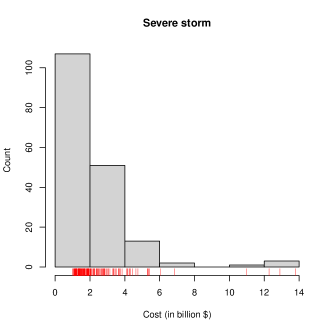

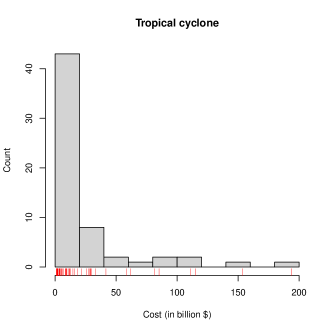

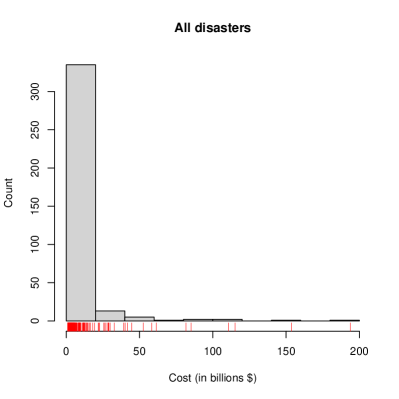

As an illustration we include some analysis of a dataset from NOAA National Centers for Environmental Information (2023) (NCEI). The data concern measurements on weather and climate disasters in the U.S. since 1980, restricted to disasters that led to an overall damage/costs of more than or equal to $1 billion (Consumer Price Index (CPI) adjusted to 2023). There are 360 such disasters amounting to a total cost of $2575,7 billion. Each disaster event has been classified into one of seven classes. Some summary statistics regarding the different (disaster) events are in Table 10. Our analysis mainly focusses on the three disaster types with the largest number of observations: severe storms, tropical cyclones and flooding. Per disaster type, we treat the entries as outcomes of i.i.d. nonnegative random variables . The left panels of Figure 6 display histograms and scatter plots of the data.

| Disaster Type | Events | Events/Year | Total Costs∗ | Cost/Event∗ | Cost/Year∗ | Variance/Event∗ |

|---|---|---|---|---|---|---|

| Drought | 30 | 0.7 | $334,8 | $11,2 | $7,6 | 12,2 |

| Flooding | 41 | 0.9 | $190,2 | $4,6 | $4,3 | 7,2 |

| Freeze | 9 | 0.2 | $36,0 | $4,0 | $0,8 | 2,2 |

| Severe Storm | 177 | 4.0 | $423,1 | $2,4 | $9,6 | 1,9 |

| Tropical Cyclone | 60 | 1.4 | $1359,0 | $22,7 | $30,9 | 38,5 |

| Wildfire | 21 | 0.5 | $135,5 | $6,5 | $3,1 | 7,7 |

| Winter Storm | 22 | 0.5 | $97,1 | $4,4 | $2,2 | 5,6 |

| All Disasters | 360 | 8.2 | $2575,7 | $7,2 | $58,5 | 17,9 |

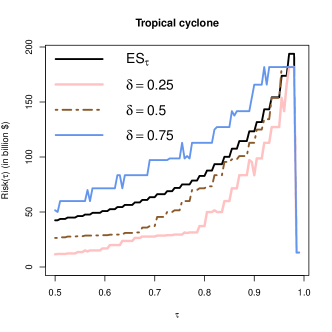

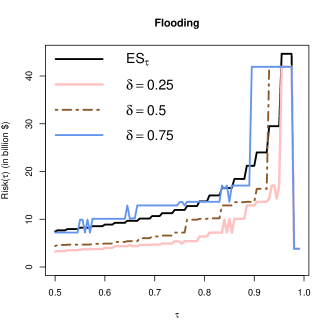

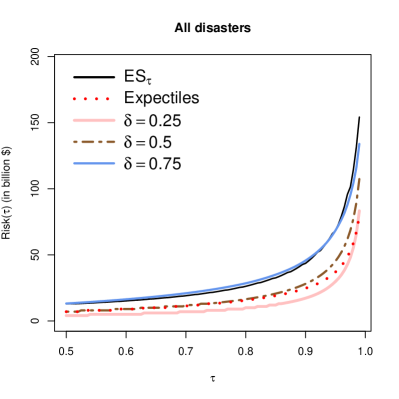

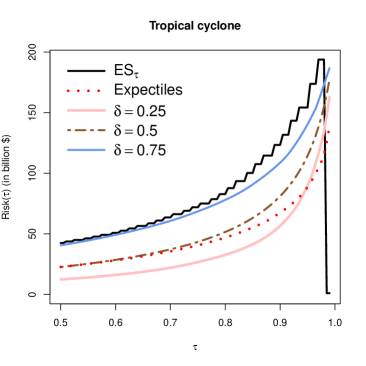

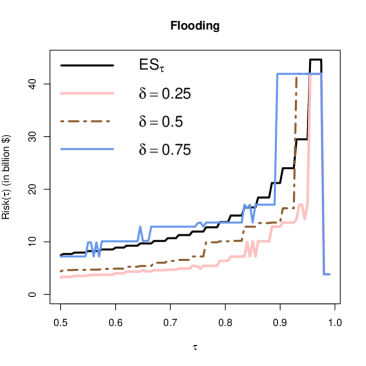

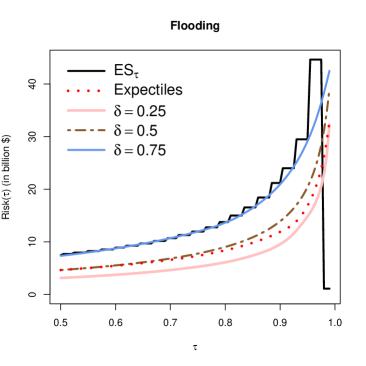

We firstly consider the distorted random variable using , the Expected Shortfall distortion function (see entry 5 in Table 3). We evaluate the risks attributed to , using (i) the mean risk (denoted by in the figures)–using square loss; and (ii) the risk associated to the th quantile –using quantile loss. The right panels of Figure 6 display estimates of these risks, as a function of . Note that the estimates break down, i.e., become zero, at . This is to be expected from the fact that is the cumulative distribution function corresponding to , and the lack of ranked data beyond . For the three different disaster types the estimates of lie below the estimates of (denoted on the plots) when . This means that the distribution of is right-skewed. For the cases of floodings and severe storms, the estimates of the quantiles are close to the estimates of , although floodings are roughly two and a half times as risky/costly.

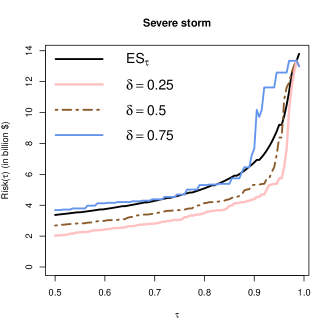

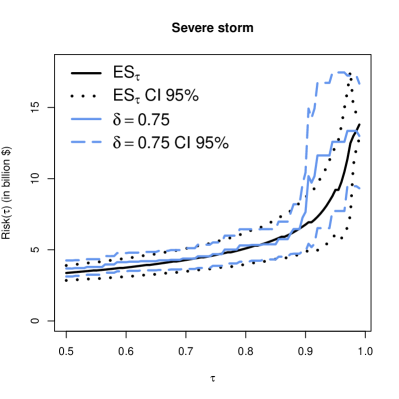

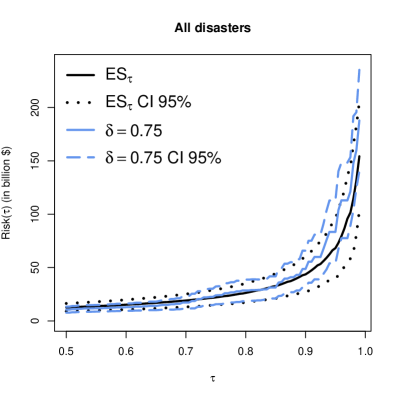

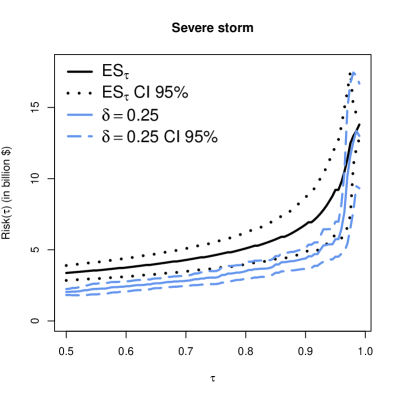

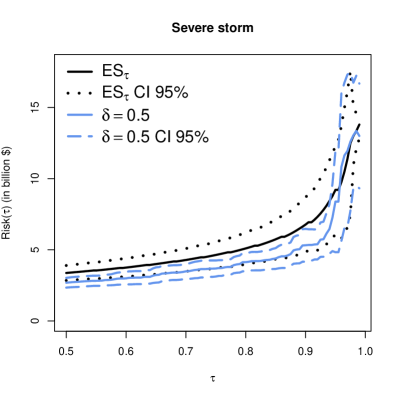

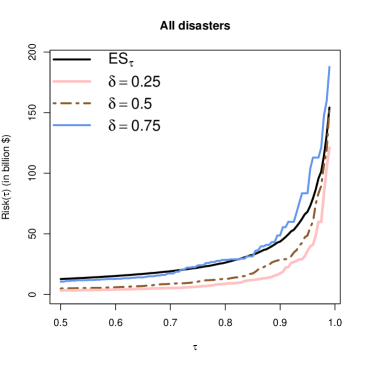

To illustrate the uncertainty that comes with the estimates, we calculated also approximate 95% pointwise confidence intervals for the severe storm category, relying on the asymptotic results established in Sections 3.2 and 3.3. In Figure 7 (left panel) we depict these approximate pointwise 95% confidence intervals, for both and the 0.75th quantile. The construction of these approximate confidence intervals relies on estimators for the asymptotic variance. For the estimate of , we obtain the approximate variance by substituting the empirical cumulative distribution function into expression (16). For the asymptotic variance of the estimated th quantile, we use expression (24). In our implementation we apply the kernel density estimator from the R package stats in combination with the Sheather & Jones bandwidth selection method. More specifically, we use the command density with bandwidth selector bw.SJ. To prevent division by zero in expression (24), we need to ensure that . To achieve this, we increase the Sheather & Jones bandwidth at each point where we estimate the density, ensuring that the neighbourhood determined by the bandwidth contains at least a fixed proportion of observations. We set the threshold at 10% of the total number of observations. For the severe storm category, this corresponds to a minimum of 18 observations. Similar plots for the other two values of (quantile curves) are to be found in Figure S3 in Section S5 of the Supplementary Material. In the right panel of Figure 7 we display the estimated and 0.75th quantile curves together with the approximate pointwise 95% confidence intervals, but now for all disasters together. A histogram and scatter plot for data on all disasters (all seven categories) is depicted in the left panel of Figure 9. The discrepancy between the estimated curve and the quantile curve, in Figure 7, is less pronounced when considering all disasters together.

It is also interesting to evaluate the estimated risk curves keeping in mind the theoretical results established in Theorem 5.1. Note that since is decreasing in , the risk is expected to be an increasing function in , according to Theorem 5.1(v). As can be seen from Figure 6 (right panels) there is no guarantee that the estimated curves are increasing (although the overall increasing trend is clear). Furthermore, since the quantile risk is monotone increasing in , Theorem 5.1(vi) ensures that this is also the case for the risk applied to the distorted random variable . From visual inspection of the estimated curves in Figure 6 it seems that there is no issue of crossing quantile curves in this example (at least not before the occurence of the breakdown point). Developing estimation procedures that would guarantee that estimators also present the associated theoretical properties is an open research question.

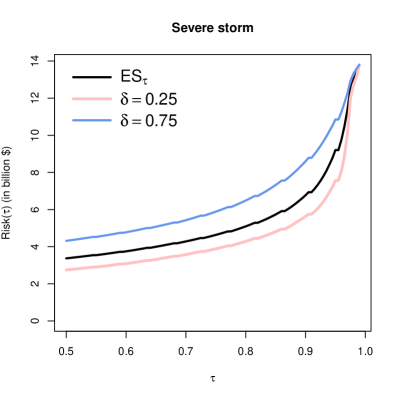

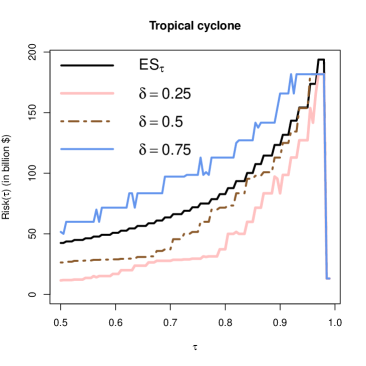

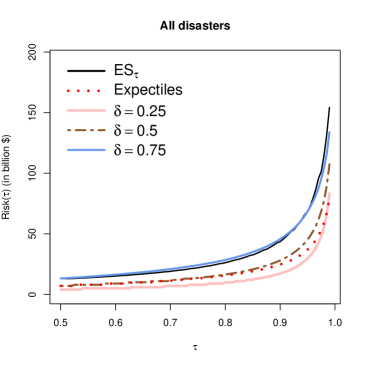

Secondly, we estimate expectile risk measures associated to , meaning that we take the expectile loss function. In the left panel of Figure 8, we display estimates of various expectiles () of . In this figure and in Figure 9, we display the black curve corresponding to the estimate as a reference curve. This in fact corresponds to the estimated risk curve for the th expectile risk. Within each disaster type the curves exhibit a high degree of similarity. The parameter allows us to obtain more (or less) conservative risk estimates. As in our previous risk analysis, there is a similar behaviour for the disasters of floodings and severe storms. We only present the plots for the disaster severe storms here. Similar plots for tropical cyclone and flooding disaster categories are displayed in Section S5 of the Supplementary Material. By Theorem 5.1(v), we know that the population risk is an increasing function in , for each expectile level . The estimated risk curves also clearly exhibit this increasing behaviour. Theorem 5.1(vi) also states that there should be no crossings of the population risk curves for different -values. Also the estimated risk curves do not show crossings (before the breakdown point).

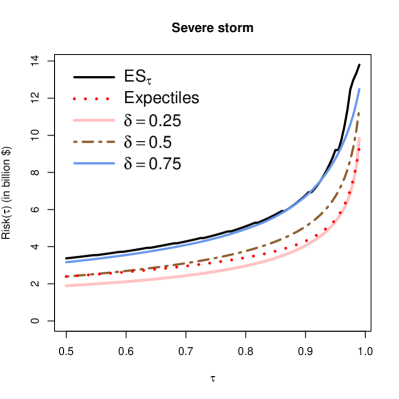

Thirdly, we look into extremiles as risk measures. Therefore we take , and consider expectile risks of the distorted random variable . The right panel of Figure 8 displays estimates of different expectile risk curves () of with , which gives estimated extremile risk curves for . We only present the estimates for the disaster category severe storms. In black, we also display estimates of the usual expectile curve (as function of ). In contrast to all previous estimated curves in this example, we now observe smooth estimated curves. In addition, there is no breakdown point. We note that the th expectile of coincides with the usual extremile. Note again that the estimated curves exhibit a high shape similarity. For low -values the estimates of the usual expectiles (in black) and the usual extremiles almost coincide. For larger -values, expectiles are more conservative than extremiles. The cumulative distribution function is decreasing in . Hence, again by Theorem 5.1(v), we know that the population risk is an increasing function in . The estimated risk curves also show this monotone behaviour. Also the non-crossingness property stated in Theorem 5.1(vi) seems to hold for the estimated curves. Figure S4 in the Supplementary Material presents the estimated expectile and extremile curves for floodings, tropical storms as well as for all disasters together.

| pair | Severe | Tropical | Flooding | All | Severe | Tropical | Flooding | All |

|---|---|---|---|---|---|---|---|---|

| storm | cyclone | disasters | storm | cyclone | disasters | |||

| Squared loss | 5.73 | 100.20 | 16.53 | 32.61 | 9.21 | 154.23 | 29.49 | 68.23 |

| Quantile loss | 3.97 | 59.91 | 10.10 | 11.88 | 5.74 | 127.20 | 17.06 | 35.99 |

| Quantile loss | 4.38 | 95.48 | 12.89 | 17.30 | 8.38 | 153.75 | 41.92 | 48.63 |

| Quantile loss | 5.39 | 127.20 | 13.66 | 31.39 | 12.59 | 181.75 | 41.92 | 83.43 |

| Expectile loss | 4.81 | 81.65 | 12.80 | 22.12 | 7.56 | 138.60 | 21.92 | 51.64 |

| Expectile loss | 7.32 | 122.84 | 23.56 | 49.81 | 10.85 | 170.06 | 37.07 | 91.34 |

| Expectile loss | 3.39 | 41.36 | 7.39 | 12.40 | 5.36 | 89.60 | 14.82 | 29.83 |

| Expectile loss | 4.28 | 63.08 | 10.86 | 20.72 | 6.71 | 114.35 | 20.41 | 45.24 |

| Expectile loss | 5.63 | 90.73 | 16.43 | 35.04 | 8.74 | 140.32 | 29.13 | 68.45 |

| Expectile loss | 5.46 | 88.48 | 16.84 | 37.02 | 5.46 | 88.48 | 16.84 | 37.02 |

In a final analysis, we again combine the data of all seven classes of disasters. In Figure 9, and Figure S4 (bottom panel) in the Supplementary Material, we display similar estimated risk curves, now based on all 360 observations. Table 10 shows that over half of the total cost is due to tropical cyclones. Nevertheless, the shape of the estimated risk curves of all disasters together appear to be somewhat similar to the estimated risk curves for floodings and severe storms. To compare various risks estimates, we present in Table 11 the values of the estimated risks for each of the separate disaster categories, as well as the estimated risks for all disasters together. We quantify the various risks for two specific values of , namely , and . Note that, for all risk estimates (i.e., looking row by row), the risks are systematically highest for tropical cyclones, and lowest for severe storms. The estimated risks for flooding are about a factor 3 larger than these for severe storms, and a factor 6 to 7 smaller than these for tropical cyclones. Our framework not only allows to estimate the various risks, it also provides approximate confidence intervals for the risks. In Table 12 we provide this information for some of the risk measures for severe storms. As expected the approximate CIs are wider for larger values of . For a given , the CIs are wider for higher-level risk measures (i.e. higher values of ).

| pair | risk | risk | ||||

|---|---|---|---|---|---|---|

| estimate | CI | length CI | estimate | CI | length CI | |

| Squared loss | 5.73 | 2.77 | 9.21 | 6.33 | ||

| Quantile loss | 3.97 | 1.16 | 5.74 | 2.46 | ||

| Quantile loss | 4.38 | 1.46 | 8.38 | 7.11 | ||

| Quantile loss | 5.39 | 2.22 | 12.59 | 9.73 | ||

7 Concluding remarks and further discussion

This paper studies general functionals, called generalized extremiles, that are solutions to an optimization problem involving as crucial ingredient a pair with a cumulative distribution function with support , and with a loss function. The main contribution in the paper consists of providing estimators for the generalized extremile, and proving their consistency and asymptotic normality. By allowing for a general pair several functionals studied in the literature fall under this framework, and hence we also provide statistical inference for all these. Cases for which estimators and asymptotic normality results for them are available in the literature are limited, and for these cases we showed that our general theorem includes these results as special cases.

Several interesting research questions can be raised. A first question is that one can wonder under which conditions the pair would lead to a coherent risk measure itself. Some partial answers are to be found in Section 2.2. Furthermore, in Section 5 we derive properties such as e.g. monotonicity or coherence of distorted risk measures based on properties of the base risk measure and the utilized distortion function. We provide an expression for the asymptotic variance for the estimator of the generalized extremile. Such a result allows to construct approximate confidence intervals for it. This however requires an estimator for the asymptotic variance. Although plug-in estimators are straightforward, it still remains to be established which are sufficient conditions for such a plug-in estimator to be consistent. Another interesting aspect is the behaviour of the asymptotic variance as a function of the parameters and . For certain functionals it would be interesting to look into such behaviour. Lastly regarding the asymptotic normality result, this has been established under a set of sufficient conditions. From the simulation study however we know that the result continues to hold in cases even when some of these conditions are violated. It would be interesting to look for a minimal set of conditions. A final issue concerns the qualitative properties to be expected from a generalized extremile, such as monotonicity as a function of , or non-crossingness for various values of . See Section 6 and the discussion therein. An interesting open research question involves estimation of the generalized extremile which would guarantee these properties to hold for the estimators.

Acknowledgement This work was initiated while the third author was visiting the KU Leuven. The first and second author gratefully acknowledge support from the Research Fund KU Leuven [C16/20/002 project]. The third author acknowledges support from NSERC through Discovery Grant RGPIN-2020-05784.

References

- Aigner et al. (1967) D.J. Aigner, T. Amemiya, and D.J. Poirier. On the estimation of production frontiers: maximum likelihood estimation of the parameters of a discontinuous density function. International Economic Review, 17(2):377–396, 1967.

- Artzner et al. (1999) P. Artzner, F. Delbaen, J. M. Eber, and D. Heath. Coherent measures of risk. Mathematical Finance, 9(3):203–228, 1999.

- Bellini and Di Bernardina (2017) F. Bellini and E. Di Bernardina. Risk management with expectiles. The European Journal of Finance, 23(6):487–506, 2017. doi: 10.1080/1351847X.2015.1052150.

- Bellini et al. (2014) F. Bellini, B. Klar, A. Müller, and E. R. Gianin. Generalized quantiles as risk measures. Insurance: Mathematics and Economics, 54:41–48, 2014.

- Boyd and Vandenberghe (2004) S. Boyd and L. Vandenberghe. Convex Optimization. Cambridge University Press, 2004. doi: 10.1017/CBO9780511804441.

- Cai and Wang (2019) J. Cai and Y. Wang. Reinsurance premium principles based on weighted loss functions. Scandinavian Actuarial Journal, 2019(10):903–923, 2019. doi: 10.1080/03461238.2019.1628101.

- Chen (1996) Z. Chen. Conditional -quantiles and their application to the testing of symmetry in non-parametric regression. Statistics & Probability Letters, 29(2):107–115, 1996. ISSN 0167-7152. doi: 10.1016/0167-7152(95)00163-8.

- Cherny and Madan (2017) A. Cherny and D. Madan. New measures for performance evaluation. The Review of Financial Studies, 22(7):2571–2606, 2017. URL https://doi.org/10.1093/rfs/hhn081.

- Daouia et al. (2019) A. Daouia, I. Gijbels, and G. Stupfler. Extremiles: A new perspective on asymmetric least squares. Journal of the American Statistical Association, 114(527):1366–1381, 2019. doi: 10.1080/01621459.2018.1498348.

- De Backer et al. (2019) M. De Backer, A. El Ghouch, and I. Van Keilegom. An adapted loss function for censored quantile regression. Journal of the American Statistical Association, 114(527):1126–1137, 2019.

- Dickson (2005) D. Dickson. Principles of premium calculation, page 38–51. International Series on Actuarial Science. Cambridge University Press, 2005. doi: 10.1017/CBO9780511624155.004.

- Embrechts et al. (2021) P. Embrechts, T. Mao, Q. Wang, and R. Wang. Bayes risk, elicitability, and the expected shortfall. Mathematical Finance, 31(4):1190–1217, 2021.

- Feinstein (2007) J. F. Feinstein. Convergence from below suffices. Bulletin of the Irish Mathematical Society, 59:65–70, 2007.

- Ferguson (1967) T.S. Ferguson. Mathematical Statistics: A Decision Theoretic Approach. Probability and Mathematical Statistics. Academic Press, 1967. ISBN 9780122537509.

- Föllmer and Schied (2002) H. Föllmer and A. Schied. Convex measures of risk and trading constraints. Finance and Stochastics, 6:429–447, 2002.

- Furman and Zitikis (2009) E. Furman and R. Zitikis. Weighted pricing functionals with applications to insurance. North American Actuarial Journal, 13(4):483–496, 2009. doi: 10.1080/10920277.2009.10597570.

- Gneiting (2011) T. Gneiting. Making and evaluating point forecasts. Journal of the American Statistical Association, 106(494):746–762, 2011. doi: 10.1198/jasa.2011.r10138.

- Hampel et al. (1986) F. Hampel, E. Ronchetti, P. Rousseeuw, and W. Stahel. Robust Statistics: The Approach Based on Influence Functions. Wiley, 1986.

- Heilmann (1989) W. R. Heilmann. Decision theoretic foundations of credibility theory. Insurance: Mathematics and Economics, 8(1):77–95, 1989. doi: 10.1016/0167-6687(89)90050-4.

- Herrmann et al. (2018) K. Herrmann, M. Hofert, and M. Mailhot. Multivariate geometric expectiles. Scandinavian Actuarial Journal, 2018(7):629–659, 2018. doi: 10.1080/03461238.2018.1426038.

- Herrmann et al. (2020) K. Herrmann, M. Hofert, and M. Mailhot. Multivariate geometric tail- and range-value-at-risk. ASTIN Bulletin: The Journal of the IAA, 50(1):265–292, 2020. doi: 10.1017/asb.2019.31.

- Holzmann and Klar (2016) H. Holzmann and B. Klar. Expectile asymptotics. Electronic Journal of Statistics, 10(2):2355 – 2371, 2016. doi: 10.1214/16-EJS1173.

- Hosseini (2009) M. Hosseini. Statistical models for agroclimate risk analysis. PhD thesis, University of British Columbia, 2009.

- Huber (1964) P. J. Huber. Robust estimation of a location parameter. The Annals of Mathematical Statistics, 35(1):73 – 101, 1964. doi: 10.1214/aoms/1177703732.

- Hürlimann (2006) W. Hürlimann. A note on generalized distortion risk measures. Finance Research Letters, 3(4):267–272, 2006. doi: 10.1016/j.frl.2006.07.001.

- Jiang et al. (2021) Y. Jiang, F. Lin, and Y. Zhou. The kth power expectile regression. Annals of the institute of statistical mathematics, 73(1):83–113, 2021. doi: 10.1007/s10463-019-00738-y.

- Jones and Zitikis (2003) B. L. Jones and R. Zitikis. Empirical estimation of risk measures and related quantities. North American Actuarial Journal, 7(4):44–54, 2003. doi: 10.1080/10920277.2003.10596117.

- Junike (2019) G. Junike. Representation of concave distortions and applications. Scandinavian Actuarial Journal, 2019(9):768–783, 2019. doi: 10.1080/03461238.2019.1615543.

- Klenke (2013) A. Klenke. Probability Theory: A Comprehensive Course. Springer Science & Business Media, 2013.

- Koenker and Bassett (1978) R. Koenker and G. Bassett. Regression quantiles. Econometrica, 46(1):33–50, 1978. doi: 10.2307/1913643.

- Liu et al. (2021) P. Liu, A. Schied, and R. Wang. Distributional transforms, probability distortions, and their applications. Mathematics of Operations Research, 46(4):1490–1512, 2021.

- Mao and Cai (2018) T. Mao and J. Cai. Risk measures based on behavioural economics theory. Finance and Stochastics, 22:367–393, 2018. doi: 10.1007/s00780-018-0358-6.

- Mao et al. (2023) T. Mao, G. Stupfler, and F. Yang. Asymptotic properties of generalized shortfall risk measures for heavy-tailed risks. Insurance: Mathematics and Economics, 111:173–192, 2023. ISSN 0167-6687. doi: 10.1016/j.insmatheco.2023.05.001.

- Newey and McFadden (1986) W. K. Newey and D. McFadden. Large sample estimation and hypothesis testing. In R. F. Engle and D. McFadden, editors, Handbook of Econometrics, volume 4, chapter 36, pages 2111–2245. Elsevier, 1 edition, 1986.

- Newey and Powell (1987) W. K. Newey and J. L. Powell. Asymmetric least squares estimation and testing. Econometrica, 55(4):819–847, 1987. doi: 10.2307/1911031.

- Niculescu and Persson (2006) C. Niculescu and L.-E. Persson. Convex Functions and Their Applications, volume 23. Springer, 2006.

- NOAA National Centers for Environmental Information (2023) (NCEI) NOAA National Centers for Environmental Information (NCEI). U.S. Billion-Dollar Weather and Climate Disasters. https://www.ncei.noaa.gov/access/billions/, 2023.

- Osband (1985) K. H. Osband. Providing Incentives for Better Cost Forecasting. PhD thesis, University of California at Berkeley, December 1985.

- Pakes and Pollard (1989) A. Pakes and D. Pollard. Simulation and the asymptotics of optimization estimators. Econometrica, 57(5):1027–1057, 1989. doi: 10.2307/1913622.

- Sander (1975) J.M. Sander. The weak convergence of quantiles of the product-limit estimator. Technical Report 5, Division of Biostatistics, Stanford University, 1975.

- Serfling (1980) R. J. Serfling. Approximation Theorems of Mathematical Statistics. Wiley series in probability and mathematical statistics. Wiley, 1980. ISBN 978-0471024033.

- Shorack and Wellner (2009) G. R. Shorack and J. A. Wellner. Empirical Processes with Applications to Statistics. Society for Industrial and Applied Mathematics, 2009. doi: 10.1137/1.9780898719017.

- Taylor (2008) J. W. Taylor. Estimating value at risk and expected shortfall using expectiles. Journal of Financial Econometrics, 6:231–252, 2008.

- Van Heerwaarden et al. (1989) A.E. Van Heerwaarden, R. Kaas, and M.J. Goovaerts. Properties of the esscher premium calculation principle. Insurance: Mathematics and Economics, 8(4):261–267, 1989. doi: 10.1016/0167-6687(89)90001-2.

- Wang (1996) S. Wang. Premium calculation by transforming the layer premium density. Astin Bulletin, 26(1):71–92, 1996.

- Wang et al. (1997) S.S. Wang, V. R. Young, and H. H. Panjer. Axiomatic characterisation of insurence prices. Insurance: Mathematics and Economics, 21(2):173–183, 1997.

- Wellner (1977) J.A. Wellner. A Glivenko-Cantelli theorem and strong laws of large numbers for functions of order statistics. The Annals of Statistics, 5(3):473–480, 1977. doi: 10.2307/2958898.

- Wozabal (2009) N. Wozabal. Uniform limit theorems for functions of order statistics. Statistics & Probability Letters, 79(12):1450–1455, 2009. doi: 10.1016/j.spl.2009.03.007.

- Yin and Zhu (2018) C. C. Yin and D. Zhu. New class of distortion risk measures and their tail asymptotics with emphasis on VaR. Journal of Financial Risk Management, 7(1):12–38, 2018. doi: 10.4236/jfrm.2018.71002.

- Ziemer and Torres (2017) W. P. Ziemer and M. Torres. Modern Real Analysis, volume 278. Springer, 2017.

Appendices

A Proofs of propositions in Section 2.2

Proof of Proposition 2.3

We have and by continuity of also for all . Defining

and setting we have

The minimizer of is therefore the negative of which minimizes . ∎

Proof of Proposition 2.4

Setting , with , we have and hence . Defining we then get, based on the assumed properties of , that

Based on our assumptions the last equation (and hence ) is finite and by definition minimized for . Hence,

the minimal value of is . This value is attained for This shows

For set . Applying the first part of the proposition then yields Under the additional assumption we use Proposition 2.3 to find , which gives . ∎

Proof of Proposition 2.5

Consider a strictly increasing function. The quantity is the minimizer of

We used here that . Note that the latter expected value is by definition minimized by which proves the first statement.

For the second statement, when considering being strictly decreasing, we note that

For the first equality we used that since is strictly decreasing and is continuous, it follows that . The first expected value is minimized when . The latter expected value is minimized by . ∎

Proof of Proposition 2.6

Mean symmetry is a standard property for minimizers of expected loss, see, for example, Proposition 2.1 in Herrmann et al. (2020) where the arguments only need to be adapted slightly to cover more general shift invariant loss functions. This leads directly to

Under the additional assumptions on and we use Proposition 2.3 to obtain the second statement. ∎

Proof of Proposition 2.7

In case of the absolute value loss, the generalized extremile is a fixed quantile of , where we have for comonotonic random variables . In case of the squared loss we can use the fact that

Indeed, this gives

∎

Proof of Proposition 2.8

Applying Proposition 2.1 we know that

is minimal in . Hence,

is minimal for satisfying . Or thus is minimal for . Observe further that

The right-hand side is well defined and is by definition minimized by , concluding the proof. ∎

B Proofs of results in Section 3

B.1 Proof of Theorem 3.1

Preliminary results