Random Utility Models with Skewed Random Components:

the Smallest versus Largest Extreme Value Distribution

Abstract

At the core of most random utility models (RUMs) involving multinomial choice behavior is an individual agent with a random utility component following a largest extreme value Type I (LEVI) distribution. What if, instead, the random component follows its mirror image — the smallest extreme value Type I (SEVI) distribution? Differences between these specifications, closely tied to the random component’s skewness, can be quite profound. For the same preference parameters, the two RUMs, equivalent with only two choice alternatives, diverge progressively as the number of alternatives increases, resulting in substantially different estimates and predictions for key measures, such as elasticities and market shares.

The LEVI model imposes the well-known independence-of-irrelevant-alternatives property, while SEVI does not. Instead, the SEVI choice probability for a particular option involves enumerating all subsets that contain this option. The SEVI model, though more complex to estimate, is shown to have computationally tractable closed-form choice probabilities. Much of the paper delves into explicating the properties of the SEVI model and exploring implications of the random component’s skewness, including offering new insights into multinomial probit models. SEVI-based counterparts exist for most LEVI-based generalizations of the conditional logit model such as mixed logit, and the LEVI versus SEVI issue is largely orthogonal to the issues these models are intended to address.

Conceptually, the difference between the LEVI and SEVI models centers on whether information, known only to the agent, is more likely to increase or decrease the systematic utility parameterized using observed attributes. LEVI does the former; SEVI the latter. An immediate implication is that if choice is characterized by SEVI random components, then the observed choice is more likely to correspond to the systematic-utility-maximizing choice than if characterized by LEVI. Examining standard empirical examples from different applied areas, we find that the SEVI model outperforms the LEVI model, suggesting the relevance of its inclusion in applied researchers’ toolkits.

Keywords: Conditional Logit, Gumbel Distribution, Independence of Irrelevant Alternatives, Multinomial Logit, Reverse Gumbel Distribution, Largest Extreme Value Type I Distribution, Smallest Extreme Value Type I Distribution.

JEL codes: C10, C18, C25

1 Introduction

Random utility models (RUM) are a cornerstone of applied microeconomics and other fields such as marketing, health policy, and transportation research. Since the seminal work of McFadden, (1973), the vast majority of RUMs have been formulated as conditional or multinomial logit models, or their generalizations (Hensher et al., (2015) and Train, (2009)).111Conditional logit typically refers to choices between alternatives with different observable attributes. In contrast, multinomial logit focuses on choices where the decision-makers themselves differ in characteristics. These two models can be combined by interacting alternative attributes with agent characteristics. Here, we primarily use the conditional logit representation for simplicity. These models posit that the total utility of an alternative comprises two components: a systematic component parameterized by observable attributes, and an idiosyncratic component known only to the agent (Manski, (1977)). The latter is often referred to as the random component, since it is unknown to the econometrician, who generally assumes it follows a specific distribution. The agent chooses the alternative with the highest total utility, making choice behavior appear random from the econometrician’s perspective, even though it may be regarded as deterministic from the agent’s viewpoint.

The conditional logit model and its standard generalizations assume that the random component follows the Largest Extreme Value Type I (LEVI) distribution, also known as the Gumbel or double exponential distribution (Gumbel, (1958)). This distribution is continuous, has a single mode, is asymmetric and skewed with a long right tail. Mirroring the LEVI distribution is the Smallest Extreme Value Type I (SEVI) distribution, also known as the Reverse Gumbel. It is also asymmetric but with a long left tail. This paper presents a systematic study of RUMs based on the SEVI distribution, highlighting their differences from conventional logit models and practical implications.

The natural question at this point for a choice modeler is: does the choice between LEVI and SEVI random components matter empirically? Two important bits of information suggest it should not. First, the difference between two (standard) LEVI random variables or two (standard) SEVI random variables is the same (standard) logistic distribution, and thus, RUMs based on LEVI and SEVI random components are equivalent when there are only two alternatives. Second, there is a long standing belief (Hausman and Wise, (1977); Horowitz, (1982)) that a multinomial probit (MNP) model produces essentially the same results as the conditional/multinomial logit model.222As succinctly summarized in the popular graduate econometric text by Greene, (2018): “An MNP model that replaces a normal distribution with [zero covariance between the random components] will yield virtually identical results (probabilities and elasticities) compared to the multinomial logit model.” This belief has been taken to suggest that it is the iid assumption imposed on the random components that drives the well-known independence of irrelevant alternatives (IIA) substitution pattern. However, insights from the case with only two alternatives do not extend to the case with more than two alternatives. In this paper, we show that as the number of alternatives increases, the choice probabilities from a LEVI-based conditional logit and a SEVI-based conditional logit model increasingly diverge from each other. We also show that the IIA property does not follow from the iid assumption. Even though the random components are still iid, a SEVI-based conditional logit model with more than two alternatives exhibits a distinctly non-IIA substitution pattern.

Let’s consider a simple stylized example. An agent (individual ) enters a store with the intention of purchasing a pair of running shoes, and there are five different alternatives and to choose from. Before trying them on, the individual rates each of the five pairs based on observable features like brand and price. These ratings capture the systematic components, , of a random utility model. For illustrative purposes, assume that the ’s are known to be and so there is no need to specify the shoe attributes and the associated preference parameters.333The vector of systematic utilities can vary among different individuals. Here, for simplicity, we assume that ’s are the same across all individuals. Next, the individual tries on each of the five pairs of shoes, making an idiosyncratic judgement on comfort and fit. This provides the random component, , to add to the systematic component, , to get the total utility level, for each pair of shoes. The chosen pair for purchase is the one with the highest .

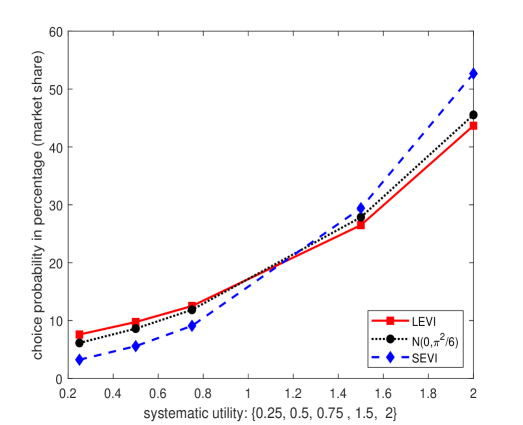

Now let the store’s customers comprise of a large number of individuals (), with identical and known systematic components , but different random components They try on the shoes, therefore observing their individual random components, then make their decision on which of the five pairs of shoes to purchase. The question we posed can now be framed solely in terms of: what are the choice probabilities cast in percentage terms (or equivalently, market shares) for each of the five pairs of shoes, if the are drawn from the following distributions: (a) the standard LEVI distribution, (b) the standard SEVI distribution, (c) N (hereafter referred to as NORM, a normal distribution normalized to have the same variance as the standard LEVI and SEVI distributions)?

The answer to this question is displayed in Figure 1. The results are quite striking, particularly for the alternatives with the smallest and largest systematic utilities. With a LEVI error component, the alternative with the smallest systematic utility has a market share 137% higher than its SEVI counterpart and 25% higher than its independent normal counterpart. This pattern continues for the alternatives with the second smallest and third smallest systematic utilities, with LEVI giving rise to market shares 73% and 37% higher than SEVI, respectively. However, this pattern of a higher LEVI market share reverses around a 20% market share (i.e., or equal share for all alternatives), where the SEVI distribution leads to a higher market share than the LEVI distribution. For the alternative with the second-largest systematic utility, the SEVI market share is 11% higher than its LEVI counterpart and 5% higher than that under the NORM distribution. The pattern of a higher market share under SEVI intensifies for the alternative with the largest systematic utility. Here, SEVI leads to a market share 21% higher than LEVI and 16% higher than NORM.

The magnitude of all of these differences is likely to be important in empirical applications. For instance, if Alternative 1 were a new product, use of a LEVI-based prediction when the true error component was SEVI would have led to an overestimation of demand by more than double (7.6% vs. 3.2% market shares). The potential for the random component to be SEVI rather than LEVI provides one possible explanation for why most new products perform much worse than predicted by marketing researchers. On the other hand, a LEVI-based prediction for the market leader, when the true error component is SEVI, could substantially underestimate its market share (43.7% vs. 52.7%). It is easy to see how either of these faulty predictions could be disastrous from both production and profit perspectives. Antitrust implications are also obvious.

Why do these differences in choice probabilities arise, despite these three simple models sharing the same (known) systematic components and random components from iid draws from simple, single-peaked distributions with the same finite variance? The answer lies in the skewness of the random components. From the econometrician’s viewpoint, the fundamental question in our stylized example is: for a randomly chosen agent, is the overall utility from a randomly chosen pair of shoes (a) more likely to move up, (b) stay the same, or (c) move down? Surprisingly, this fundamental property of the random component of a RUM seems to have never been raised in the voluminous literature on multinomial choice models and serves as the driving force behind the present paper.

If the total utility of an arbitrarily chosen agent for an arbitrarily chosen alternative is more likely to move upward relative to the systematic utility after receiving the private signal representing the random component, then the random component is right-skewed. The classic exemplar in this scenario is the LEVI distribution, and the canonical model is the conditional logit. If the total utility for this agent is just as likely to move up as move down, then the random component is symmetric. The normal distribution is the exemplar, and the multinomial probit is the canonical model. If this agent’s total utility is more likely to move down, then the random component is left-skewed. There is not a similar exemplar distribution or canonical model for this left-skewed case. We propose employing the SEVI distribution and its corresponding model for the left-skewed scenario, serving as the natural counterpart to the standard LEVI formulation.

Once the potential importance of the skewness of the random component is acknowledged, an entirely new line of inquiry is opened up. Are there conditions (e.g., in-store vs. online purchases) or deep personality traits (e.g., risk averse vs. risk loving) that influence the random component’s skewness? We don’t provide answers to this question but hope that we provide tools that can help researchers explore these issues.

Fitting an RUM based on LEVI random components to data generated with SEVI random components results in substantially biased estimates of the preference parameters and vice versa. For the same preference parameters in the RUM’s systematic components, SEVI-based random components result in substantively different (compared to LEVI-based random components) estimates for quantities such as elasticities and average partial derivatives routinely relied upon in decision making.444We identify one specific scenario: a ratio estimator, such as those used in many willingness-to-pay calculations, where the LEVI-based estimator remains consistent even if the true error component is SEVI, provided that an important set of restrictions on the attribute matrix is met. Standard generalizations of the multinomial/conditional logit do not address issues that arise when a LEVI random component is assumed, incorrectly, when SEVI is appropriate. Instead, SEVI-based analogues of those models exist to deal with the specific deviations from the standard multinomial/conditional logit that those models are intended to address.

While we make no claim that the SEVI assumption is always or even generally preferable to that of LEVI, the empirical relevance of the SEVI model is easily demonstrated. When examining a set of six datasets taken from standard econometric textbooks and well-known papers, we find that the SEVI distributional assumption is consistently preferred over LEVI and is favored over the normal distribution in five out of the six datasets. For any particular application, the skewness of the random component is obviously an empirical question, and a priori, nothing rules out mixtures of random component skewness types, an issue we examine near the end of this paper (see Section 6.1).

The bulk of the paper is devoted to studying the theoretical properties of a SEVI model and delving into aspects of the estimation, inference, and prediction within the SEVI framework. Here, we offer a preview of some intriguing properties of the SEVI model.

First, both the choice probabilities and the surplus function in a SEVI model have intuitive and closed-form representations, allowing us to explore new avenues of discrete choice analysis. Using the strict convexity of the social surplus function, we show that a SEVI model is identified under the same conditions that ensure the identification of a LEVI model.

Second, the structure of the choice probability for any given alternative in a SEVI model is considerably richer than in the LEVI model, where its dependence on other alternatives is solely through the sum of the exponentiated systematic components for each alternative. In the SEVI model, the choice probability for a given alternative can be seen as an aggregation involving all choice subsets in which the alternative occurs and the overall choice set. This dependence of the choice probability on all subsets of alternatives is a distinctive feature of the SEVI model that differentiates it from the LEVI model. As a consequence of such dependence, IIA does not hold in the SEVI model.

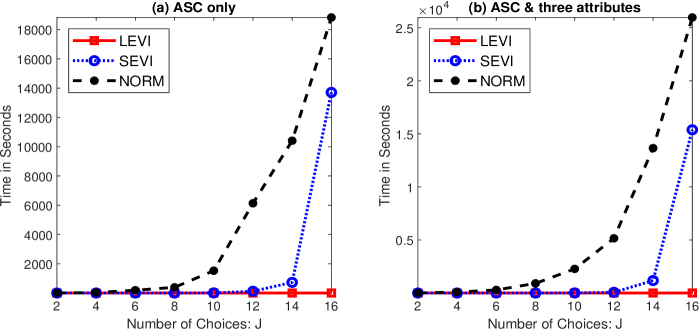

Third, on its surface, the all-subsets representation of SEVI might seem computationally challenging when the number of alternatives is of any appreciable size. We overcome this issue by employing Gosper’s hack (Knuth, (2011)) from the computer science literature to efficiently enumerate all possible subsets containing a target alternative. For a moderately large with typical sample sizes and attribute numbers in economic analysis, the computation time for a SEVI model is somewhat higher than its standard logit LEVI counterpart but much lower than that of the MNP with iid normal errors. In the case of the computation time for a SEVI model can be less than 2% of that of the corresponding independent MNP model.555It is an open issue how SEVI’s enumeration of subsets of alternatives interacts with the computational intensity inherent in the generalizations of the conditional logit model, where long run times are often the norm.

Fourth, we explore the regions where the SEVI model is likely to produce results similar to the LEVI model and where the results are most likely to diverge. We develop a Vuong-type test, showing its effectiveness in distinguishing between the SEVI and LEVI models (Vuong, (1989)). We also show that AIC/BIC can be employed to help guide appropriate model choice.

Fifth, we explore the implications of the skewness of the random component as the number of alternatives increases, going beyond the case with only two alternatives. One immediate implication is that in an RUM with SEVI random components, the observed choice and the choice that maximizes the systematic utility are more likely to correspond than in the case of LEVI. This is because SEVI error components have less of an impact on determining the selected alternative compared to LEVI ones. In contrast, SEVI random components play a larger role than their LEVI counterparts in determining what is not chosen.666One way to conceptualize the role of the random components, consistent with this observation, is that an agent with SEVI random components seeks idiosyncratic reasons to reject alternatives, whereas under LEVI, the agent aims to find a high-quality idiosyncratic match component to accept an alternative.

The rest of the paper is organized as follows. Section 2 provides a literature overview, largely from a historical perspective, that hints at why the importance of the skewness of the random component was overlooked. Section 3 studies the structure of the choice probabilities in a SEVI model, contrasting its properties with those of the conventional LEVI model. This section shows that while Luce’s choice axiom holds for the SEVI model when , this restriction does not hold when . This section also provides a closed-form expression for the surplus function and shows how it can be used to compute the compensating variation and establish the identification of the SEVI model. Section 4 considers estimating the SEVI model by MLE and QMLE, studies the consistency of the QMLE up to a scale normalization, and describes the use of AIC/BIC and the Vuong test for selecting between the SEVI and LEVI models. Section 5 presents a variety of simulation results, exploring different aspects of the SEVI model. Section 6 introduces a mixed model that accommodates individuals of either LEVI or SEVI type in a population. It also contains a straightforward extension to discrete choice problems where agents aim to minimize, rather than maximize, an objective function, such as cost and regret. Section 7 contains a set of empirical applications drawn from textbooks and well-known papers, allowing us to compare the goodness of fit using LEVI, SEVI, and independent MNP with the same error variance. The final section offers concluding remarks and outlines some future research directions based on generalizing the SEVI model. Proofs are provided in the appendix, and an online supplementary appendix contains additional materials and figures.

2 Literature Review: a Historical Perspective

Early empirical research on individual-level choices was hindered by the lack of data and appropriate statistical models. Operationally, the study of choice requires a conceptualization involving a systematic component and a random component. The psychologist Thurstone, (1927) is generally credited with pioneering this concept and proposing a variant of the now-familiar binary probit model. The binary logit model soon emerged from biology. Statistical advancements related to the random component, whether logistic or normal, largely took place in the realm of biometrics (Cox, (1969)).

The transition from the binary choice case to the multinomial choice proved not to be easy. While significant advancements occurred within biometrics (e.g., Cox, (1969)), the pendulum swung back to psychology and, in particular, to the seminal work of Luce, (1959). This effort quickly spilled over into economics (e.g., Block and Marschak, (1960)). Formal requirements for choice models to meet the rationality requirements of utility maximization were explored, and patterns of choice behavior, such as the IIA property in the multinomial logit model, were examined. The multinomial logit model and its statistically equivalent flipped version, known as the conditional logit model, came together in its current form with the tour-de-force synthesis of McFadden, (1973). The work of McFadden and those following in his footsteps spawned a truly massive empirical enterprise in economics and other social sciences (see McFadden, (2001)). This involves the construction and application of various random utility models, almost all based on the LEVI kernel of the conditional logit.

There are many reasons why the LEVI distribution was originally chosen for RUMs and has become popular in applied research.

First, utility is inherently unobservable and hence is typically represented as a latent variable. The assumption of continuity makes economic theory and applied work much more tractable. This ruled out discrete distributions.

Second, in the case of a binary response, there had been a long-running debate over tacking on an error term, first from a normal and later from a logistic distribution, in bioassay experiments. In these experiments, the error component was perceived as coming from an unobserved tolerance distribution. When response data were plotted, bell-shaped tolerance distributions seemed more appropriate than either a uniform or bimodal distribution. Eventually, the binary logit model prevailed over its probit counterpart because of its computational advantages and the early literature’s observation of largely indistinguishable empirical results across the two models with sample sizes available at the time (Chambers and Cox, (1967)). This outcome also influenced the adoption of the binary logit model in the social sciences; see Chapter 9 of Cramer, (2003) for a historical account.

Third, there was a long-standing belief that the multinomial logit and the multinomial probit with iid normal unobserved utilities were very close approximations to each other.777Hausman and Wise, (1977) state: “We might expect the independent probit and the logit models to have similar properties [including inducing the IIA red bus/blue bus property via the iid random component assumption] and, in fact, they lead to almost identical empirical results.” Horowitz, (1982) proposes a Lagrange multiplier test of the unrestricted MNP model, assuming that the MNL estimates adequately approximate the restricted MNP results. The belief may have led to the misconception that there is no need to go beyond the multinomial logit if the random utility components are iid. However, this belief turns out not to be generally true. The misconception likely stems from limitations in computational techniques and resources, restricting early literature to examine only cases with a small number of alternatives. When the number of alternatives, is small, particularly when and , the estimates from an independent multinomial probit with a common variance normalization tend to be very close to those from a LEVI multinomial logit. Nevertheless, as shown in Figure 1, the multinomial logit and probit models can exhibit significant differences for even a moderate such as

These, however, are not reasons for not exploring the implications of other distributions, as Manski, (1977) had urged. This is particularly relevant in light of the increased computational power and insights from behavioral economics, which suggest frequent violations of the IIA property.

The “non-IIA” property of a SEVI model bears some resemblance to that of the mother/universal logit (McFadden et al., (1978)) and the random regret minimization model (e.g., Mai et al., (2017)). However, the mechanisms of removing the IIA property are fundamentally different. By definition, a SEVI model considered here is a utility maximization model, and hence the resulting choice probability function can be rationalized by a probability distribution over linear preference orderings (Block and Marschak, (1960)). The absence of the IIA property is due solely to the distribution of the error component. In contrast, most implementations of the mother/universal logit and the random regret minimization models are inconsistent with random utility maximization, and the lack of the IIA property in these models is a result of the specification that the difference in the systematic (not random) component of utility between any two alternatives depends on the presence or absence of another alternative.

A significant portion of the history of this field revolves around building models utilizing the LEVI kernel to relax the IIA constraint. This is achieved by permitting agents to have different preferences or scale parameters or by allowing subsets of alternatives to be correlated in some fashion, while still maintaining computational feasibility (Hensher et al., (2015); Train, (2009); Greene, (2018)). Among these models, random-parameter (mixed) logit, latent-class multinomial logit, scale-heterogeneity logit, generalized multinomial logit, and nested logit stand out as the most prominent examples. All these more general specifications can be constructed using a SEVI rather than a LEVI random component. Conceptually, specifying the random component’s skewness should precede relaxing restrictive assumptions of the conditional logit model, such as the independence of random components and the homogeneity of preferences across individuals.

Our discovery of the LEVI vs. SEVI distinction came about through an inadvertent sign flip while generating draws from a standard LEVI distribution. In doing so, a SEVI random component was generated instead. This would likely have gone unnoticed if our objective had not been to study whether the behavior of agents facing choice sets of varying sizes differed. In a baseline simulation, we observed sizeable differences in the conditional logit model estimates of preference parameters and other statistics, as the number of alternatives increased. These unexpected results led us to realize that we had fit a LEVI-based logit model to data generated by a SEVI logit. A search of general and specialized econometrics texts revealed no discussion of LEVI vs. SEVI or the broader issue of the role of the skewness of the random component in choice behavior.

We eventually found one short and largely ignored paper in the literature (Hu, (2005)) which points out that the likelihood functions of SEVI and LEVI-based choice models are different. However, that paper does not delve into any of the other results presented here. It asserts that the SEVI model does not appear to have a closed-form solution and hence has to be estimated using a simulation approach. In Theorem 1, we show this not to be the case. SEVI has a mathematically elegant and intuitive closed-form solution that facilitates direct comparisons between the properties of LEVI vs. SEVI choice models. In an empirical marketing application with three alternatives involving types of bread, Hu, (2005) shows that the SEVI model fits marginally better than the LEVI model, but the difference is smaller than the variation due to different smoothing parameter values used in the simulation approach. To our knowledge, the SEVI model has not been used in subsequent empirical applications.

3 The Model: Choice Probability and Surplus Function

3.1 The SEVI-based RUM

We consider a probabilistic choice model based on utility maximization. We assume that the utility of individual from alternative is given by

| (1) |

where is the number of alternatives, is the observable utility that individual obtains from choosing alternative , captures the utility component unobservable to the econometrician, and is independent of . As is customary in the literature, we refer to as the systematic utility and as the random/stochastic utility. A common parametrization of the systematic utility is where is a vector of attributes of alternative as perceived by individual and is a vector of characteristics of individual .

Individuals choose the alternative that maximizes their total utility. Let denote the choice of individual then

| (2) |

One of our goals is to estimate the model parameter based on individual choice data.

For the stochastic utility, we assume that is iid over and follows the extreme value type I distribution based on the smallest extreme value. The CDF of the (standard) smallest extreme value type I (SEVI) distribution is

| (3) |

and the corresponding pdf is

| (4) |

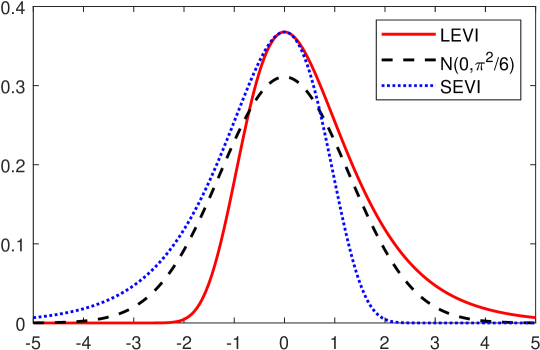

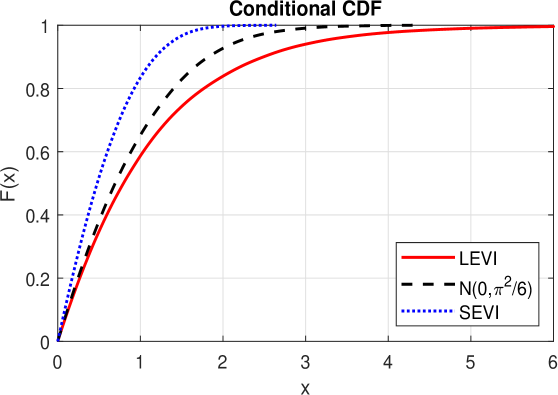

Our distributional assumption is in contrast with that in standard logit models, where the latent utility is given by , and the stochastic utility follows the (standard) extreme value Type I distribution based on the largest extreme value (i.e., the largest extreme value type I (LEVI) distribution). These two forms of extreme value distributions are related in that and have the same distribution, so they can be regarded as mirror images of each other. For easy reference, we call a stochastic utility following the SEVI distribution a SEVI error and the resulting RUM as the SEVI model. The same nomenclature applies to the LEVI case.888Throughout the paper, the SEVI is the standard SEVI with pdf given in (4) and variance A similar comment applies to the LEVI case.

Figure 2 illustrates the pdfs of the LEVI and SEVI distributions. The LEVI distribution exhibits a strong right-skewness with a heavier upper tail in contrast to its lower tail, while SEVI exhibits the opposite (mirror image) behavior. As a symmetric benchmark, the normal pdf with the same variance is also plotted. The SEVI distribution is appropriate when there is a prior belief that the random utility component is more likely to have a negative rather than a positive or neutral effect on the total utility. Such a belief is plausible, and we have been unable to find a strong a priori argument against using a SEVI random component or a mixture of SEVI and LEVI components, as we discuss in Section 6.1.

This notion of random component skewness has to be seen as conditional on what alternative attributes and agent characteristics are observed by the econometrician. To see this, note that in the case of a linear latent utility model, consists of for a scalar attribute known to individual but not observable to the econometrician. If has a negative skewness and , then will also have a negative skewness, implying that may exhibit left-skewness and follow the SEVI distribution. Thus, the inclusion or exclusion of a particular covariate may change the skewness of the stochastic utility component. More generally, the system utility may be misspecified, with the resulting specification error effectively becoming part of the stochastic utility. Given that specification errors can be manifest as left-skewed, symmetric, or right-skewed, the stochastic utility can display any of these forms of skewness as a consequence. This argument lends another support to the notion that the SEVI distribution of the stochastic utility is at least as plausible as the LEVI distribution.

A logical question at this point is whether the SEVI distribution belongs to the class of Generalized Extreme Value (GEV) distributions with the CDF given by for some parameter The SEVI distribution, however, does not align with a GEV distribution.999When the GEV distribution is not supported on the whole real line. When the GEV distribution is right-skewed. Nor does it correspond to the marginal distribution of a multivariate extreme value (MEV) distribution with CDF:

| (5) |

for some function . In both cases, the marginal distribution is right-skewed instead of being left-skewed like a SEVI distribution. See, for example, Chapter 4 of Train, (2009). In principle, exploring an extension of the GEV or MEV family by using the SEVI as the marginal distribution, potentially encompassing the SEVI as a special case within this broader framework, could be considered for future research.

3.2 Choice Probabilities in the SEVI-based RUM

In a SEVI-based RUM, similar to a LEVI-based RUM, the choice probabilities also have closed-form expressions, albeit a bit more complex. To simplify the notation, we suppress the dependence of and on , and we write and . We adopt the same convention for the realized values and of and in the theorem below.

Theorem 1

Assume that , where is independent of and the elements of follow independent and identical SEVI distributions. Then, under utility maximization, the probability of individual choosing alternative is

| (6) | ||||

where, for is the subset of alternatives leaving the -th alternative out.

Remark 1

In a standard LEVI conditional logit model, the choice probability is

| (7) |

We can compare the choice probabilities across the SEVI and LEVI models using a few examples. When there are only two alternatives so that we have, using Theorem 1,

The choice probability is exactly the same as what we obtain in a standard LEVI model. Therefore, in the presence of only two alternatives, it does not matter whether the stochastic utility follows the LEVI or SEVI distribution. This is because the difference between two independent LEVI or SEVI draws follows the same logistic distribution.101010By Lemma 5 of Yellott, (1977), the condition that the difference of two iid random components is logistic is necessary for the IIA to hold. Our results presented later can be seen as showing the existence of a simple distribution, SEVI, which meets this necessary condition, yet IIA does not hold.

When there are more than two alternatives so that the choice probabilities in a SEVI model are different from those in a LEVI model. Consider the case with It follows from Theorem 1 that

| (8) | ||||

This is clearly different from the LEVI choice probability, which is equal to

To understand the formula for we can examine which represents the probability that alternative 1 is not chosen. The latter event can be expressed as a union of two events , indicating that alternative 1 is dominated by either alternative 2 or alternative 3. But the probability of this union is

Each of the three probabilities above corresponds to a choice probability in a conventional LEVI model. Substituting the familiar LEVI formulas yields Equation (8), and Theorem 1 is a generalization of these arguments.

Remark 2

When Theorem 1 reveals that

which involves enumerating all choice subsets that contain the first alternative. In contrast, the corresponding choice probability in a LEVI model is

which involves only the largest choice set. As shown in Figure 1, and later, when becomes larger than 2, the choice probabilities in a SEVI model can be different from those in a LEVI model in an economically meaningful way. This has practical implications, underscoring the need for careful consideration when formulating distribution assumptions in discrete choice modeling.

Remark 3

When for all and we have

This result can also be obtained by using a symmetric argument. Since all alternatives have the same systematic utility, they are indistinguishable and hence have an equal chance of being chosen. The result is the same as that obtained under the LEVI assumption. On the other hand, when increases and dominates all other for approaches 1. The choice probability can, therefore, be regarded as a type of softmax function that maps into For example, it maps into which amounts to assigning almost all probability mass to the element with maximal systematic utility. This result is qualitatively similar to that obtained under the LEVI assumption.

Remark 4

The probability of choosing alternative in a SEVI model involves a summation over all subsets of resulting in an iteration over a total of subsets of alternatives. The choice probability in a LEVI model takes a simpler, more convenient form. While the choice probability in a SEVI model is considerably richer than that in a LEVI model, the SEVI model has a computational disadvantage when is large. To mitigate this, we employ Gosper’s hack, a technique rooted in bitwise operations, to streamline the iteration process efficiently. Additionally, by leveraging the arguments following Proposition 4.4 in Ross, (2013), it can be shown that for any :

| (9) |

where

This allows us to approximate by with a well-controlled approximation error. Note that takes the same form as but involves subsets of at most alternatives, and so it is computationally less intensive when is smaller than To achieve a desired level of precision, we can choose large enough and stop iterating over subsets of more than alternatives. Combining Gosper’s hack with an early stopping makes it computationally easy to estimate a SEVI model for as large as 14. Section 5.3 reports and compares the computation times for various models using simulated data with typical sample size and attribute numbers. Section 7 contains a comparison of computation times for real data applications.111111By leveraging multiple processors running in parallel to enumerate choice subsets, the feasible size of can be significantly increased. Unlike the sequential approach required for integration in the multinomial probit model, this can be accomplished simultaneously.

Remark 5

For the SEVI model with a linear parametrization of if is not present so that then the model is called a conditional SEVI (logit) model. As an extension of the basic model, we can allow the coefficient on to be alternative specific and so we may have On the other hand, if is not present so that then the model is called a multinomial SEVI (logit) model. These forms can be combined so that which provides the same flexibility as in a standard LEVI (logit) model. As in a standard multinomial LEVI (logit) model, not all of ’s are identified, and we need to normalize one of them, say to be zero.

To illustrate the difference between the SEVI and LEVI models, we simulate the choice probabilities when (there is no individual-specific characteristic or alternative-specific constant), and the stochastic utility is iid SEVI or LEVI. We set the number of covariates in to be (there are three attributes for each alternative) and let We consider two data generating processes (DGP) for the attributes . In the first DGP, for each and we let be iid over where

| (10) |

Here, is a just standardized version of the sequence (). In this case, each attribute becomes more dispersed when the alternative label is closer to or . As a result, the mean choice probabilities (i.e., ) are not all the same across the alternatives. In the second DGP, for each and we let be iid over In this case, the attributes have the same distribution across the alternatives, and the mean choice probabilities are the same across all alternatives. Under these two DGPs for the variances of the systematic utility are and respectively. These variances are comparable to the variance of the stochastic utility.

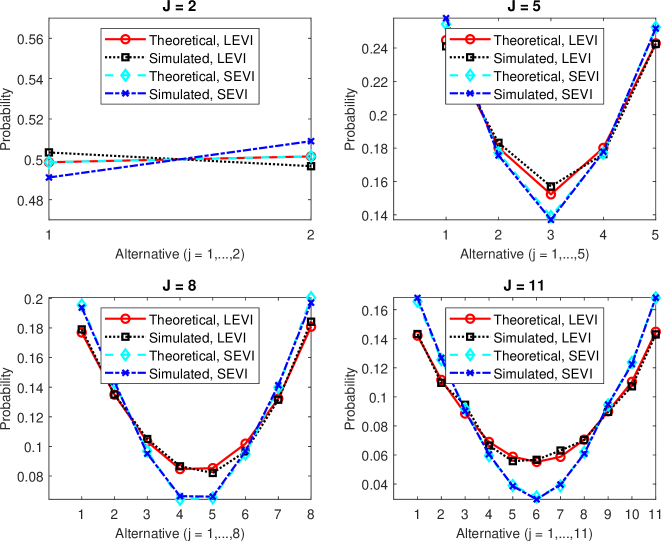

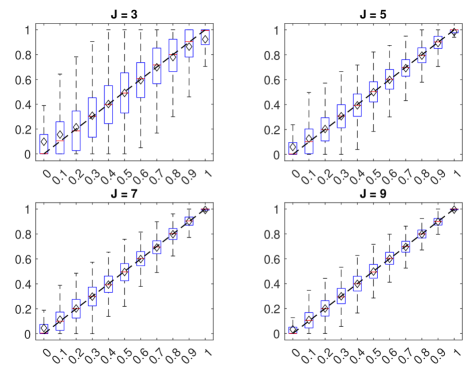

For each model, we compute the choice probabilities according to the theoretical formulae (i.e., (6) under the SEVI and (7) under the LEVI), and take the average of these choice probabilities over 10,000 individuals. We also simulate the decisions of 10,000 independent individuals and compute the proportion of individuals choosing each alternative. Figure 3 reports results for various values when iid Not surprisingly, since the sample size is large, the average theoretical choice probabilities match the simulated choice proportions well for both the SEVI and LEVI models. When the theoretical choice probabilities are the same across the two models. With only two alternatives, the simulated choice shares are very close across the two models, but not identical due to simulation errors. When for alternatives with relatively higher choice probabilities under the LEVI, the SEVI model assigns a higher choice probability than the LEVI model. On the other hand, when for alternatives with a relatively lower choice probability under the LEVI, the SEVI model assigns a lower choice probability than the LEVI model. The difference between the choice probabilities across the two models grows with The choice probability in a SEVI model is closer to the “arg max” function than that in a LEVI model. In this context, a SEVI model leans more towards embodying the concept of “the winner takes it all” than a LEVI model. More specifically, given the same set of systematic utilities, the probability of choosing the alternative with the maximum systematic utility in a SEVI model tends to be larger than that in a LEVI model.

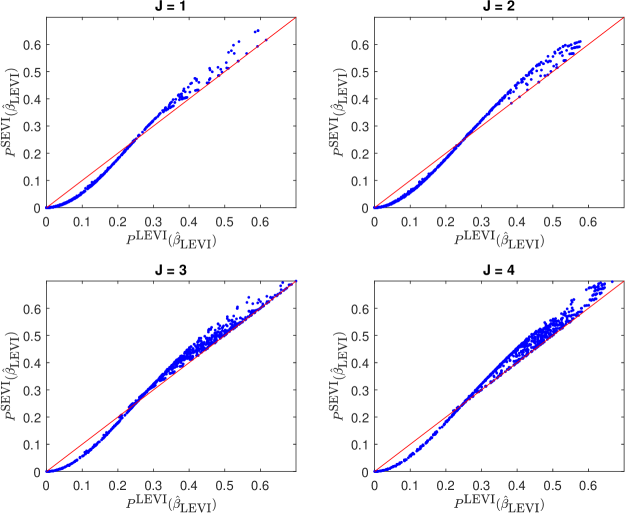

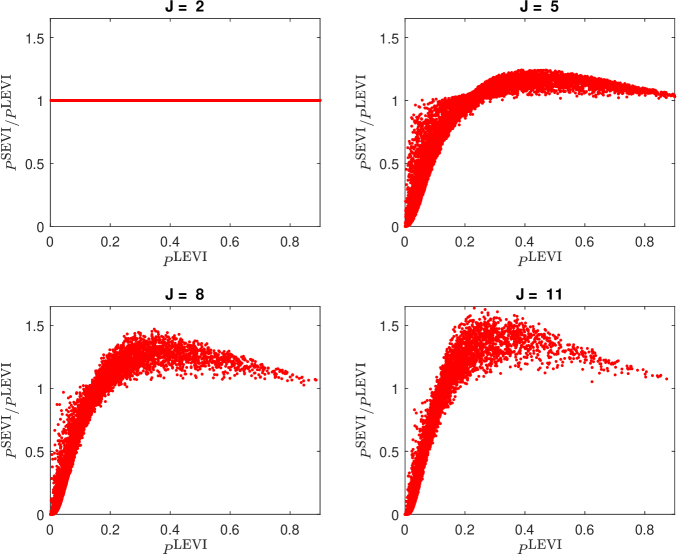

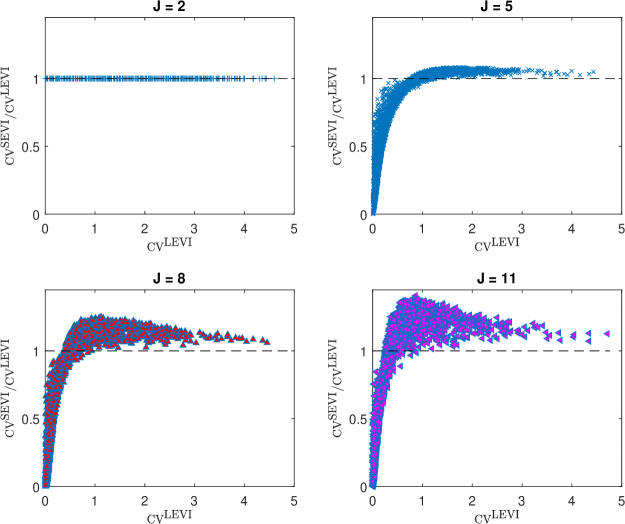

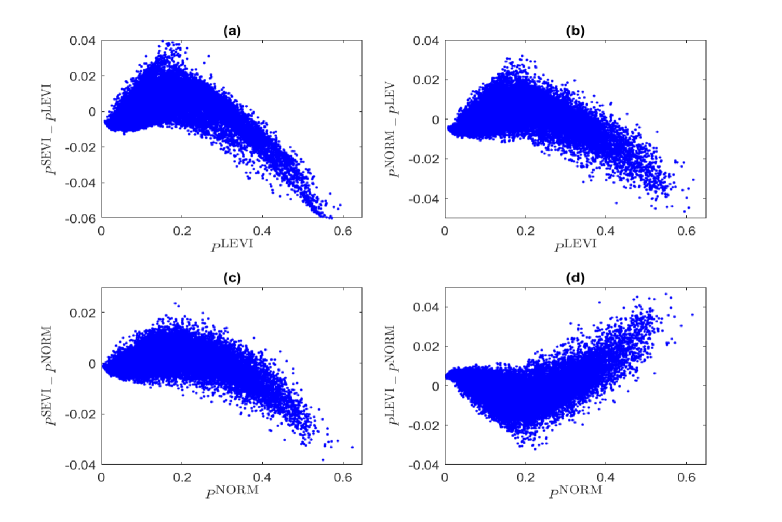

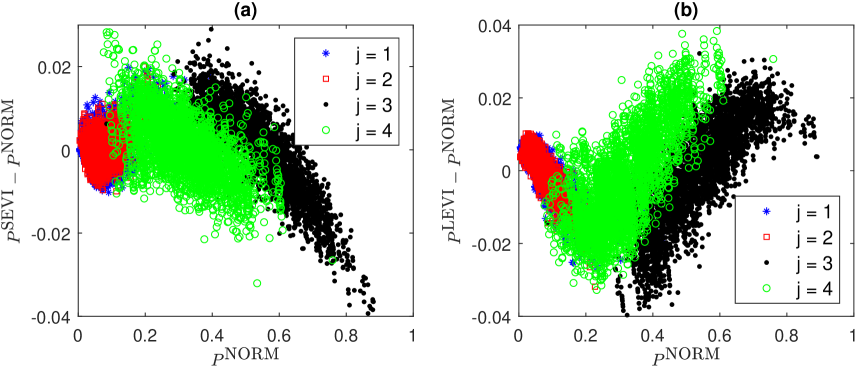

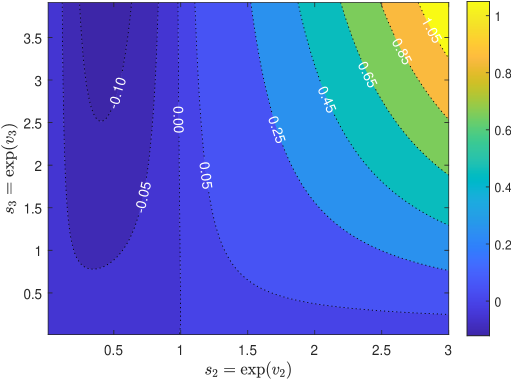

Next, we report the results when is iid , but we use a different type of plot. Figure 4 provides a scatter plot of the ratio of the choice probabilities in the SEVI and LEVI models (i.e., against . Instead of examining the average choice probabilities as done in Figure 3, we consider the choice probability of choosing a specific alternative (here, we use alternative 1 without loss of generality) for each realization of the systematic utilities. Figure 5 provides a supplementary illustration, offering a closer examination of certain details.

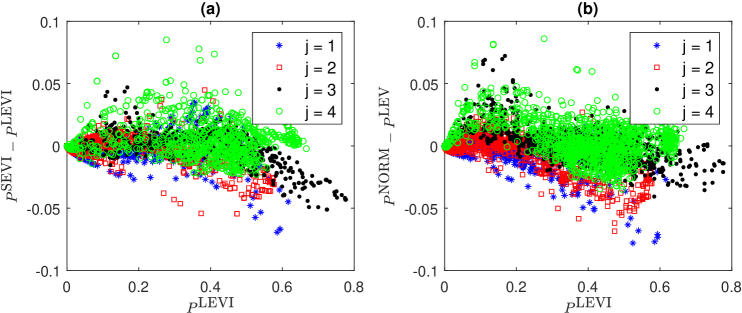

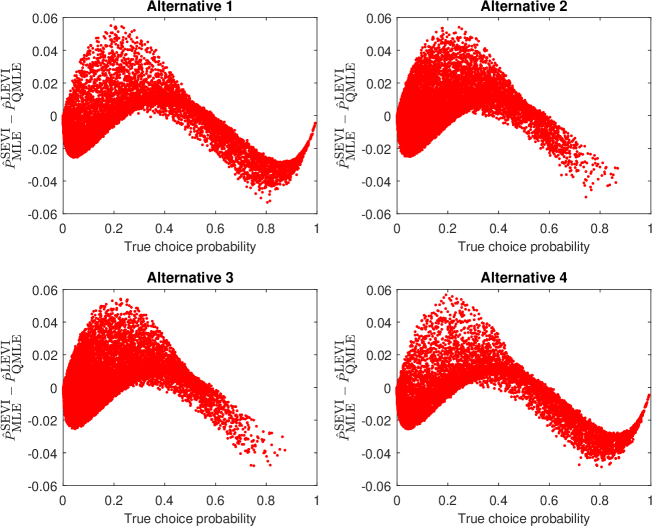

In both Figure 4 and Figure 5, the systematic utilities are held constant for each data point with either LEVI errors or SEVI errors. We note from these two figures that when and is low, can be more than 50 percent lower. For example, when there are five alternatives () and can be as low as . The LEVI probability can be roughly twice as large as the SEVI probability. Thus, from a practical point of view, a choice between the two models can have an enormous impact on predicting a lift for a minor brand with a market share between 5% and 10%. On the other hand, when and is high, tends to be higher. For example, when and can be 20 percent higher; when and can be 50 percent higher. The patterns we observe here are similar to those in Figure 1. The difference in the choice probabilities across the two models can be important in various contexts, ranging from antitrust actions to production planning.

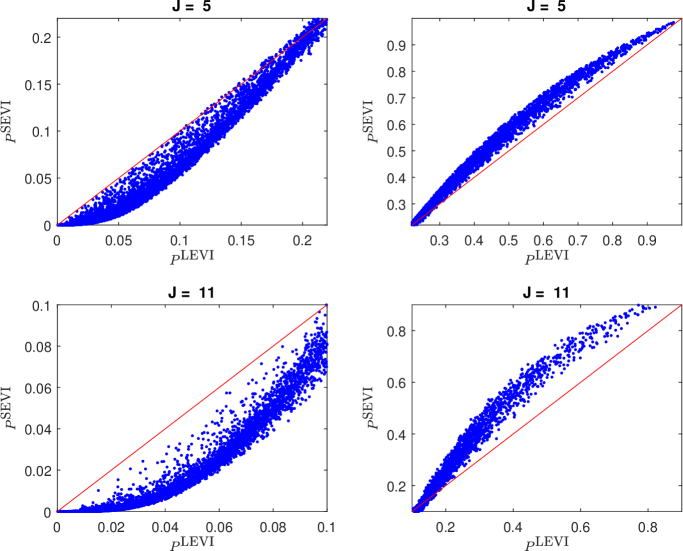

Figure 5 shows that when and the LEVI probability is below 0.20, the corresponding SEVI probability is lower. When the LEVI probability is above 0.20, the corresponding SEVI probability is higher. Similar patterns are found for other values of These qualitative patterns are consistent with what we find in Figure 3. The vector of choice probabilities in the SEVI model (i.e., ) is closer to the vertices of the probability simplex than that in the LEVI model. In other words, is closer to a - vector with the -th element equal to 1 if and only if is the maximum value of 121212For ease of discussion, we assume that there is a unique maximum among The 0-1 vector representation of is the so-called one-hot encoding of

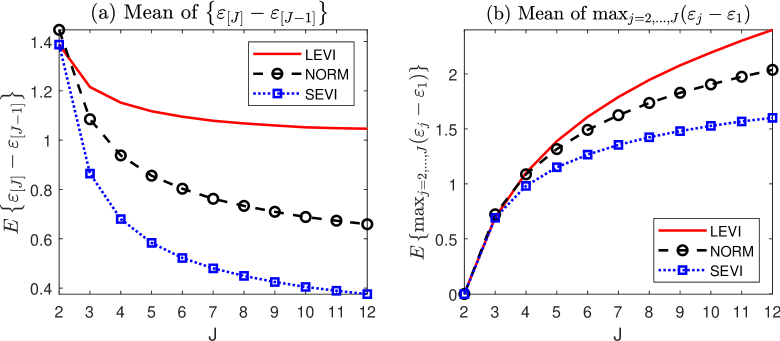

We now offer insights into why the probability vector is closer to the one-hot encoding of than When the top two values among independent draws from the stochastic utility distribution are more likely to be above or equal to the median of this distribution rather than below it. For a draw from the LEVI distribution, conditional on being above the median, the mean is 1.545 and the standard deviation is 1.079. In contrast, for the SEVI case, these values are 0.391 and 0.500, respectively. Hence, the absolute difference between any two above-the-median draws from the LEVI distribution is expected to be larger than that for the SEVI distribution. In fact, Monte Carlo simulations show that the former first-order stochastically dominates the latter (see Figure S.1). This implies that two above-the-median draws from the SEVI distribution are more likely to be closer to each other than those from the LEVI distribution. Therefore, with more than two alternatives, it is less probable for the stochastic utility components under the SEVI to make a difference in determining which alternative has the highest total utility. As a result, in the presence of more than two alternatives, the choice probabilities under the SEVI are better aligned with the systematic utilities than those under the LEVI. In other words, in a SEVI model with , the observed choice is more likely to correspond to the choice that maximizes the systematic utility than in a LEVI model. See Figure S.2 for an additional illustration.

3.3 Algebraic Relation between SEVI and LEVI Choice Probabilities

To relate the choice probabilities under SEVI and LEVI assumptions, we consider a general latent utility model where is iid across and may follow either SEVI or LEVI, is independent of . For any alternative and any subset of alternatives that does not include alternative we let

which are the probabilities of individual choosing alternative from the subset under SEVI and LEVI errors, respectively. It is important to point out that in the above definition, the probabilities depend on the choice subset under consideration.

Proposition 2

The choice probabilities under the SEVI and LEVI satisfy the following relations:

The proposition shows an intrinsic connection between the choice probabilities under the two assumptions of the stochastic utility. Note that the right-hand side of each relation involves the probabilities of choosing alternative over all subsets of alternatives that contain alternative but under a “reflected” model for ( on the left-hand side becomes on the right-hand side).

By taking the difference between the two equations in Proposition 2, we have

where

So, the difference in the SEVI and LEVI probabilities of choosing alternative from the entire choice set is an aggregation of the probability differences from choosing alternative from all subsets of alternatives that contain but with flipped systematic utilities. This is a recursive relationship, as each probability difference on the right-hand side can be represented in the same fashion as the left-hand side. An intriguing question emerges: can the difference in choice probabilities be fully captured by a simple index that measures the concentration of the systematic utilities? Given the intricate recursive relationship described above and the highly nonlinear dependence of the probability difference on systematic utilities, as shown in Figure S.3, it appears unlikely that commonly used measures like the Gini coefficient or the Herfindahl-Hirschman index would be sufficient for this task. However, in empirical practice, particularly for moderately sized , these measures are likely to prove useful in predicting differences in choice probabilities.

The second relation in Proposition 2 can be presented equivalently as follows:

| (11) |

Since is nonnegative, the sum in (11) is also nonnegative. This sum is a special Block-Marschak polynomial (Block and Marschak, (1960)). In the presence of a finite number of alternatives, it is well-known in the stochastic choice theory that the nonnegativity of Block-Marschak polynomials is both necessary and sufficient for a random choice rule to have an additive random utility representation. For a detailed discussion, see, for example, Chapters 1 and 2 of the recent book by Strzalecki, (2023). In the present setting, the choice probabilities under SEVI are derived from random utility maximization and as such, they trivially have an additive random utility representation. The significance of (11) is that it provides a simple characterization of a special Block-Marschak polynomial.

More generally, let be a target alternative of interest and

be a subset of alternatives that includes alternative Then, the (general) Block-Marschak polynomial for our probability choice rule under SEVI errors is defined to be

Note that when the first term in becomes and reduces to the special Block-Marschak polynomial in (11). We can show that is the probability that the -th alternative dominates all other alternatives in but is dominated by the alternatives that are not in See, for example, Barberá and Pattanaik, (1986). Hence, for all which is consistent with the nonnegativity of Block-Marschak polynomials for any additive RUM model.

The Block-Marschak polynomial is precisely the probability relevant for rank-ordered data. While using the SEVI model for rank-ordered data necessitates additional research, the formula for provides a good starting point.

3.4 Patterns of Substitution and the Lack of IIA

In this subsection, we compute , the effect of an infinitesimal change in alternative ’s systematic utility (as perceived by individual ) on the probability of individual choosing alternative This computation is essential for determining the effect of changing alternative ’s attributes on the probability of choosing alternative

For notational economy, we let We have, using Proposition 2 and some simple calculations,

| (12) |

where for

Furthermore, for

| (13) |

where for a subset of excluding and

In equation (13), the first term in the summation (i.e., when is understood to be

Equation (13) reveals that

| (14) |

for any and That is, the choice probabilities satisfy a symmetry property analogous to Slutsky symmetry in continuous choice models.

The expression of can be used to derive the score function, which is essential for finding the MLE and developing the asymptotic theory. It can also be employed to examine whether the IIA property holds in a SEVI model when . For the IIA to hold, the cross (semi)elasticity should be the same for all That is,

for all However, this condition is not met, as is clear from (13). Alternatively, for the IIA to hold, the probability ratio should not depend on the systematic utilities of alternatives other than alternatives and However, it is evident that the probability ratio does depend on the systematic utilities of all alternatives, indicating that the IIA does not hold.

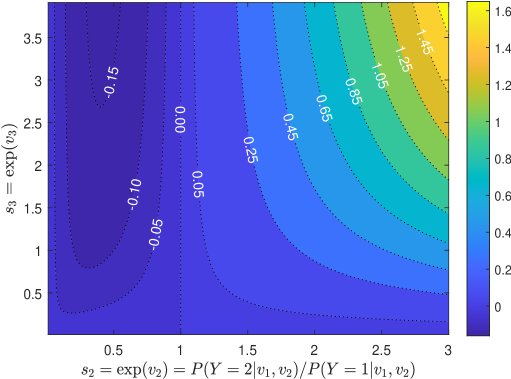

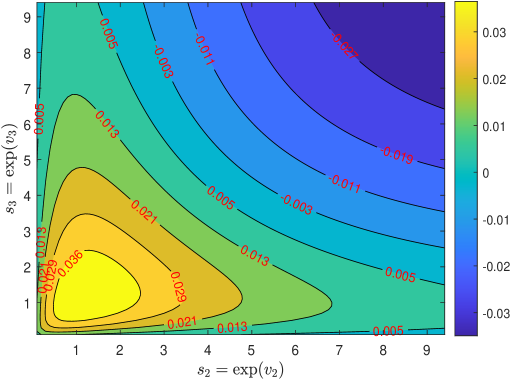

To illustrate the violation of the IIA in a SEVI model with , we start with a scenario featuring two initial alternatives: individuals must choose between alternative 1 and alternative 2. In this context, the choice between the SEVI or LEVI does not matter. For a fixed scale value (we set to so that ),131313Following Yellott, (1977)), we refer to the exponentiated systematic utility for alternative as the scale value () for this alternative. we examine a range of possible values for a grid of values from 0.01 to 3 with increment 0.01. Each combination of corresponds to a probability ratio:

Next, we introduce a third alternative with its scale value , the same grid for We investigate how the probability ratio of choosing alternative 2 versus alternative 1 changes. This ratio now depends on whether the stochastic utilities follow the SEVI or LEVI distribution.

The difference of the ratios under SEVI and LEVI models, denoted as is

Here we have used properties of the LEVI probabilities. By the third equality above, also gauges the extent of IIA violation. With set to 1, is a function of and , so we can write it as We present a contour plot of this function in Figure 6. To aid interpretation, we label the horizontal axis as representing the initial probability ratio with only two alternatives available.

It is clear from Figure 6 that is not a zero function. After the introduction of the third alternative, the market shares of alternatives 1 and 2 do not decrease proportionally in the SEVI model as what happens in the LEVI model, indicating a violation of the IIA.

Figure 6 also shows that there are two scenarios where equals zero or becomes approximately zero. First, equals zero when alternatives 1 and 2 have the same initial market share (i.e., . This is expected, as in this case, the first two alternatives are indistinguishable, and their market shares reduce proportionally in both the LEVI and SEVI models when the third alternative is introduced. Second, approaches zero when one of the alternatives becomes almost completely dominant in the market. This corresponds to a scenario where either is small and is very large, or is small and is very large. Hence, the difference between a SEVI model and a LEVI model may not be large when there is clearly a dominant player in the market who commands almost the entire market, and their disparities become more apparent when no alternative has nearly all market share.

In an additively separable RUM with as considered here, it is well known that the IIA property holds for any if and only if the stochastic utility follows the LEVI distribution (cf., Yellott, (1977)). Under certain conditions that permit an infinite it can be shown that in a random utility model with possibly nonseparable utility functions, the IIA holds for any only if the latent utility can be represented as for some strictly increasing function and LEVI-distributed This result is a corollary to Theorem 1 of Dagsvik, (2016); see also Lindberg and Smith, (2017) and the references therein.141414When is finite, the latent utility presentation of is not necessary for IIA to hold, but the counterexample given in Lindberg and Smith, (2017) is unlikely to be relevant to most empirical applications. The SEVI model does not have the required representation, and this provides another perspective on the absence of the IIA property in the SEVI model when

One consequence of the lack of IIA is that we cannot consistently estimate the preference parameters in a SEVI model using the random sampling approach. In this approach, for each decision maker, we sample a random subset of alternatives that contains the chosen alternative and treat this subset as if it were the choice set faced by this decision maker. In the simplest case with three total alternatives , the reason for the inconsistency is that

This contrasts with a LEVI-based logit, where such a random sampling procedure can be used to reduce the number of alternatives without inducing inconsistency. For a detailed discussion of the LEVI case, see page 64 of Train, (2009).

We note in passing that IIA also does not hold for standard multinomial probit models, i.e., the multinomial probit with iid normal random utility components. See Section S.D in the supplementary appendix for details.

3.5 The Surplus Function: Compensating Variation and Identification

A fundamental concept in the discrete choice analysis is the surplus function, defined as:

where the expectations are taken with respect to the distribution of In the above, the first term is the expected value of the maximum utility achieved, given the vector of the systematic utilities and the second term serves as a constant benchmark.151515If these terms are not well defined, can always be expressed as which is well defined. See, for example, McFadden, (1981). Among other uses, the surplus function can be used to obtain the choice probabilities. More specifically, the Williams-Daly-Zachary theorem161616It was termed the WDZ theorem in Section 5.8 of McFadden, (1981). McFadden refers to Daly and Zachery, (1978) and Williams, (1977) as forerunners of the result. says that

The specific form of the surplus function depends on the distribution of When LEVI, it is well-known that

taking the form of a “log-sum”. Here the superscript “” signifies that the surplus function is based on the assumption that LEVI.

The next proposition gives the form of the surplus function when SEVI.

Proposition 3

If across then the surplus function, denoted by is

| (15) |

where

Furthermore, is strictly convex.

Although the surplus function still contains “log-sum”, is more complex than . Nevertheless, Proposition 3 gives us a closed-form expression for and shows that it is strictly convex. The second representation given in (15) shows how is related to the log-sum over all subsets of choice alternatives but with the systematic utilities flipped.

As the first application of Proposition 3, consider a SEVI model of the form:

| (16) |

where for Here we have introduced an additional covariate as part of the systematic utility, where is the income of individual and is the cost/price of alternative The coefficient on this covariate represents the marginal utility of income. In this model, the systematic utility that individual obtains from alternative consists of two components: the utility derived from the expenditure on the numeraire and the utility derived from the characteristics of alternative . Such a formulation is common in applied welfare analysis using discrete choice models.171717In this formulation, income does not influence the choice probabilities. This assumption may be reasonable when costs associated with the alternatives are negligible compared to income or where measurement errors in income outweigh the costs. While it is possible to account for income effects, we do not explore this extension here.

Now suppose we change the cost/price for the -th alternative from to while keeping all else the same as before. For each individual the compensating variation is defined implicitly via the equation below:

where is the indicator function. That is, is the additional income that individual would need to maintain the same utility when the cost of alternative changes from to Solving for yields

Using Proposition 3, we can find that the expected value of conditional on and is

| (17) |

where is the unit vector with a value of 1 at the -th element and elsewhere. We can average over the distribution of to get the expected compensating variation over the population:

In empirical applications, we can estimate and using sample averages after plugging in parameter estimates.

As a second and closely related application, we can employ the surplus function to define the compensating variation when an alternative is removed from the choice set. Using the same model as in (16), we investigate the minimum compensation necessary for individual so that they would not be worse off if alternative were eliminated from their choice set. Denote this compensation as . Then, solves

By a similar argument used to derive (17), we find

where

By definition, represents compensation for an individual with systematic utility To emphasize the dependence of on and the distribution of random utilities, we denote it as hereafter.

We can define similarly under the LEVI model. For each value of the ratio quantifies the relative magnitude of the (conditional) compensating variations across the SEVI and LEVI models. Figure 7 plots this ratio against when follows the same data generating process as that in Figure 3, with one of the ’s regarded as the price/cost. Each point in the figure represents the ratio for a particular instance of and Qualitatively, the figure resembles Figure 4, where the general patterns are applicable to the DGP in Figure 3. Specifically, when the CV under the LEVI model is low, the CV under the SEVI model tends to be even lower, and conversely, when the CV under the LEVI model is high, the CV under the SEVI model tends to be higher. These results are intuitive: removing an alternative that is chosen more (or less) often should have a larger (or smaller) welfare implication.

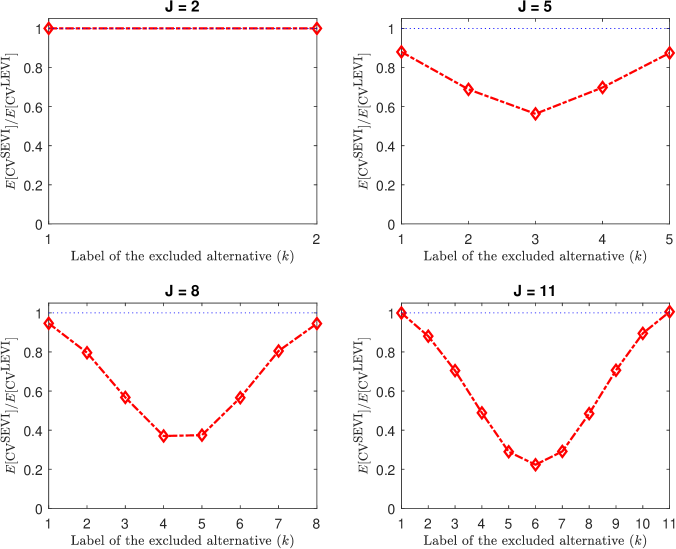

A drawback of Figure 7 is that each point in the figure does not clearly indicate which alternative is excluded from the choice set. To address this, we simulate the expected CVs, and for each alternative excluded, with respect to the distribution of . Figure S.6 in the supplementary appendix plots the ratio of these two expected CVs against the label of the excluded alternative (). From the figure, it can be observed that the expected CV under the LEVI appears to be larger than that under the SEVI, regardless of which alternative is excluded. In addition, the percentage difference between the two expected CVs appears to grow with the number of alternatives.

As a third application, we use Proposition 3 to establish the identification of a SEVI model. Note that the model under the vector of systematic utilities is equivalent to that under , as the choice problem depends only on utility differences. For the purpose of studying identification, we normalize the systematic utility of the last alternative to zero and maintain this normalization in the rest of this subsection. Each vector of systematic utilities maps into a vector of choice probabilities and The question remains whether we can deduce the systematic utilities from the choice probabilities.

Define the conjugate surplus function:

Since is known and given in Proposition 3, it follows by construction that all of and are known functions. Using Theorem 7 of Sørensen and Fosgerau, (2022), we have:181818This may be of independent interest in IO/marketing applications if the objective is to derive the systematic utilities from the observed market shares, but here we focus on identification.

for That is, we can plug the vector of choice probabilities into to recover the vector of systematic utilities.

Given that the vector of choice probabilities is identified, the vector of systematic utilities is also identified. The problem of identifying the model parameter in a SEVI model reduces to the problem of identifying from the (joint) distribution of Intuitively, if we have an infinite number of independent draws from the distribution of can we pin down Mathematically, if

| (18) |

then is identified. This identification condition requires that, for two different model parameters, there is a positive probability that the resulting vectors of (normalized) systematic utilities are different. For example, in the linear case where this requires that there is no perfect multicollinearity among the variables in for at least one

The identification condition in (18) does not involve the distribution of Therefore, it is applicable to any RUM model, provided that the unobserved random components is independent of the systematic utility and is absolutely continuous with full support See Corollary 1 of Sørensen and Fosgerau, (2022) for more discussions. In particular, this condition is applicable to a LEVI model. Hence, a SEVI model is identified if and only if the corresponding LEVI model is identified. No additional identification challenges arise in a SEVI model.

4 The MLE and QMLE of a SEVI Model

4.1 The Estimators

Consider the following conditional SEVI model

for where and All other models in Remark 5 can be reformulated to take the above form. For example, if we want to include alternative-specific constants, we can introduce a dummy variable for each alternative and include the dummies for alternatives as part of . This dummy-variable method can also be used to allow for alternative-specific coefficients for any covariate, including individual-specific characteristics.

Given a simple random sample from the above model, we consider estimating by MLE and QMLE. The MLE is the maximum likelihood estimator when the likelihood function is based on a correctly specified SEVI model, and the QMLE is the maximum likelihood estimator based on an incorrectly specified LEVI model.

The negative log-likelihood function of the model under the correct SEVI specification is

where and is defined as in (6) with replaced by By minimizing the above negative log-likelihood function we obtain the MLE:

where is a large enough compact set in

To compute the MLE, we can use a gradient-based algorithm. The gradient function is

where

In the above, the expression of the derivative is given in (12) or (13) after plugging in the parameter The closed-form expression for the gradient can be supplied to a gradient-based optimization algorithm.

Given the score and the estimator we can estimate the asymptotic variance of by

Following standard arguments, we can show that Details are omitted here, as the theory is standard; See, for example, Chapter 13 of Wooldridge, (2002).

If we want to test against for some matrix with row rank and vector we can form the Wald statistic and show that it is asymptotically chi-squared under the null:

In particular, we can use the square root of the diagonal elements of , denoted by as the standard errors for the elements of We can construct a 95% confidence interval as

If the stochastic utilities follow SEVI, but we employ the maximum likelihood method under the incorrect assumption that they follow LEVI, we obtain the quasi-MLE (QMLE):191919Here, we focus on the QMLE based on the LEVI likelihood. Other QMLEs may be considered. For instance, we might explore the QMLE derived from the specification that the random utility components follow an MEV distribution (see (5)). As long as the marginal distribution is incorrectly specified, such an alternative QMLE will generally be inconsistent for the preference parameters.

| (19) | ||||

The asymptotic properties of the QMLE are also standard results. In particular, we use the sandwich form for estimating the asymptotic variance of when we know that the LEVI model is not the correct model.

4.2 On the Estimation of Parameter Ratios

Under some standard regularity conditions, is consistent for but in general, is not. However, the ratio of the individual elements of , say may still be consistent for the true ratio, namely for a nonzero In this subsection, we provide sufficient conditions for the consistency of the ratio estimator, even though the distribution of the random utility component is misspecified.

We consider an RUM with and specify for some distribution This includes LEVI as an example but may be more general and incorrectly specified. Denote the choice probability derived under by . Let be the pseudo-true value defined by

which is also the probability limit of

We assume that is an interior point of the compact set so that satisfies the first order zero-derivative conditions. The derivative of the population objective function with respect to is

where

So, satisfies

Proposition 4

Assume that (i) , and is the unique solution to

(ii) , and there exists a nonzero scalar such that

(iii) for some scalars and and for

Then:

Proposition 4 shows that while the QMLE may not be consistent for , it converges to up to a multiplicative factor. In particular, if then

This says that the plug-in ratio estimator is consistent for the true ratio.

Assumption (iii) in Proposition 4 holds if are independent and each follows a multivariate normal or elliptical distribution. The latter assumption is sufficient but not necessary. There may exist other distributions of or specific ways to relax the independence assumption such that the proportionality result holds. In empirical applications, the ratio estimator could still be close to the true ratio even though Assumption (iii) does not hold.

Proposition 4 is proved along the lines of the proof of Theorem 1 in Ruud, (1986), which does not cover multinomial choice models. Some adjustments to the proof in Ruud, (1986) are needed to account for two main differences: there is no constant term in a multinomial choice model and the covariate in this model is a matrix rather than a vector.

4.3 The Choice between SEVI and LEVI

In empirical applications, it is often the case that neither the SEVI nor the LEVI is correctly specified. However, we still have to decide which model to use. To aid in this decision, we can employ the Akaike Information Criterion (AIC) or the Bayesian Information Criterion (BIC). Since both models have the same number of parameters, we can compare their empirical (quasi) log-likelihoods, which leads to the likelihood ratio statistic given by

Note that in the previous section, and were denoted as and respectively. However, in this section, both the SEVI model and the LEVI model can be misspecified and so both and can be quasi-maximum likelihood estimators.

In empirical applications, the choice between the SEVI model and the LEVI model can be based on the likelihood ratio. If , then the LEVI model is preferred.202020Note that and are the negative log-likelihood functions so when we may conclude that the LEVI model fits the data better. Conversely, if , then the SEVI model is preferred. This simple empirical rule of thumb is derived from the empirical goodness of fit and serves as a practical guide for selecting between the two models. It is worth pointing out again that this rule is also the model selection rule based on the AIC or BIC, as the two models have the same number of parameters.

Another method to determine which model to use is by employing Vuong’s test (Vuong, (1989)), which formally assesses the null hypothesis that the SEVI model and the LEVI model provide equally good fits to the data. Let and be the respective limits of and . In the present setting, the null hypothesis of Vuong’s test can be expressed as:

almost surely, where is the vector collecting the systematic utilities. Note that

where is the true choice probability. The right-hand side of the above equation is the cross entropy between and (), which quantifies the difference between these two distributions. By adding a constant to both sides, we have

where the right-hand side is the KL distance between the two distributions and () conditional on Similar calculations can be performed for Therefore, the null of Vuong’s test is that the SEVI and LEVI models are equidistant from the true data generating process, with the “distance” measured by either the cross-entropy or the KL distance.

Since the SEVI model and the LEVI model are nonnested, is asymptotically normal. We can standardize the LR statistic to obtain the statistic of Vuong, (1989):

Following the arguments in Vuong, (1989), we can show that under the null This serves as the basis for both one-sided tests and two-sided tests. For example, if then we may reject the null that the SEVI and LEVI models fit the data equally well at the 5% significance level. On the other hand, if we may reject the null that the SEVI model fits the data better at the 5% significance level. If we may reject the null that the LEVI model fits the data better at the 5% significance level.

5 Simulation Evidence

We generate the data from a conditional SEVI model. More specifically, we assume that

where SEVI over and or over and . The DGPs are the same as the SEVI DGPs in Figures 3–5. Given a simple random sample we use the MLE and QMLE in Section 4 to estimate To reiterate, the MLE is based on the correct specification that SEVI, and the QMLE is based on the incorrect specification that LEVI.

5.1 Simulation with a Large Sample Size

We first consider the case that the sample size is large, and there is only one simulation replication. The purpose of this exercise is to see how large the misspecification bias is. Table 1 reports the estimates when the sample size is When the MLE and QMLE give the same estimate of This is consistent with the result that the SEVI model and the LEVI model are the same when there are only two alternatives. When the MLE and QMLE are quite different. While the MLE is close to the true parameter vector for all values of considered, the QMLE grows with For example, when and the QMLE is , each element of which is higher than the corresponding true value by about 50%. The misspecification bias of the QMLE is substantial. In line with Proposition 4, the ratio of the estimates of any two elements of , say is close to the true ratio This is true regardless of whether the attributes have the same variance across the alternatives or not. Proposition 4 permits variance heterogeneity across the alternatives.

| True | |||||||||||||

| MLE | QMLE | MLE | QMLE | MLE | QMLE | MLE | QMLE | ||||||

| 1.00 | 1.01 | 1.01 | 1.00 | 1.37 | 0.98 | 1.48 | 1.02 | 1.64 | |||||

| 2.00 | 1.95 | 1.95 | 2.01 | 2.75 | 1.99 | 2.99 | 1.98 | 3.17 | |||||

| 1.00 | 0.99 | 0.99 | 1.00 | 1.37 | 1.01 | 1.49 | 0.98 | 1.57 | |||||

| 1.00 | 1.01 | 1.01 | 1.01 | 1.35 | 0.99 | 1.51 | 1.00 | 1.64 | |||||

| 2.00 | 2.03 | 2.03 | 2.05 | 2.80 | 1.98 | 3.09 | 1.98 | 3.37 | |||||

| 1.00 | 1.03 | 1.03 | 1.03 | 1.38 | 1.03 | 1.56 | 1.00 | 1.64 | |||||

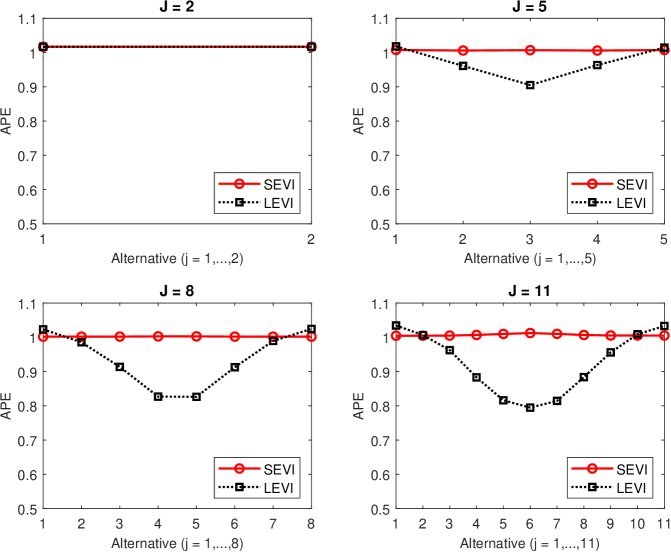

In a nonlinear model, instead of focusing on the parameter values, it can be more informative to examine the (empirical) average partial effects, defined by

In the above, and are the choice probabilities under the SEVI and LEVI specifications, respectively. and are the corresponding empirical APEs that measure the effect on the probability of choosing alternative when a marginal change is made to one of alternative ’s attributes. We focus on the first attribute and plot the ratios:

against the label of each alternative Figure 8 reports the results for the case that and makes it clear that the empirical APE is not close to the target APE (i.e., ) when the model is misspecified. This shows that the difference in the parameter estimates due to model misspecification has substantial effects on APE estimation.

To further illustrate the difference between the SEVI and LEVI specifications, we conduct an out-of-sample prediction exercise. Let and be the MLE and QMLE of , respectively, when there are alternatives. We use and to compute out-of-sample choice probabilities for a certain choice problem. More specifically, we assume that an out-of-sample individual chooses between the first two alternatives only, and the rest alternatives are not available. In this case, the out-of-sample choice probabilities are

where

and represents an out-of-sample individual whose observation was not used in constructing the MLE or QMLE, but is generated in the same way as any in-sample observation. Note that the number of “out-of-sample” individuals is the same as the number of “in-sample” individuals and both are equal to 10,000.

When there are only two alternatives in the out-of-sample prediction exercise, the formulae for the choice probabilities are the same under SEVI or LEVI. Hence, as given above, and are different only because they are based on different estimated parameters.

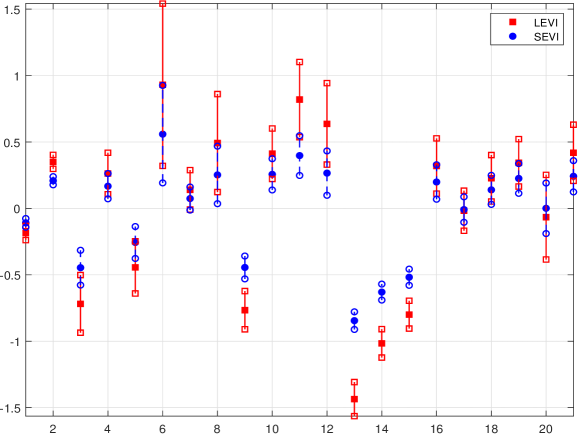

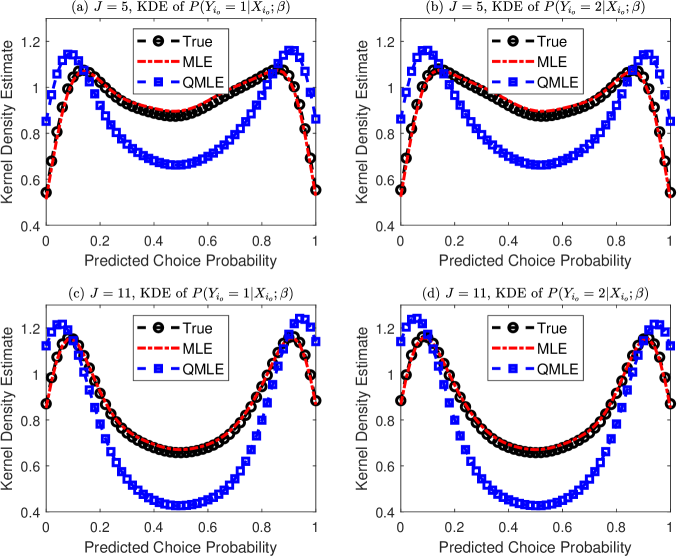

Figure 9(a&b) reports the kernel density estimators (KDE) of for and when and It is not surprising that the KDE under is very close to the target KDE, that is, the KDE under When the sample size is large, is very close to , as demonstrated in Table 1. As a result, is close to and therefore, the corresponding KDEs are close to each other. On the other hand, the KDE under is quite different from the target KDE. This demonstrates that the model misspecification introduces not only a significant bias in the parameter estimator but also a substantial discrepancy in the predicted choice probabilities.

The KDE figure for the case that and is qualitatively similar to Figure 9(a&b) and is thus omitted. The KDE figure for the case that and is reported in Figure 9(c&d). The difference between the KDE under and the target KDE appears to increase with

As final evidence that it matters whether the stochastic utility follows the SEVI or LEVI distribution, we compute the out-of-sample predicted choice probabilities when there are four alternatives for both the in-sample estimation and out-of-sample prediction. For the latter, we compute and where we have emphasized the dependence of the choice probability on the distributional assumption imposed on the stochastic utility. We plot the difference against the true choice probability as a scatter plot. We omit the figure here, but it is available as Figure S.7 in the supplementary appendix. The figure clearly shows that, relative to the true choice probability, the difference can be substantial.

5.2 Simulation with Smaller Sample Sizes

In this subsection, we study the performances of MLE and QMLE in finite samples. Using the same DGP as in the previous subsection, we consider the sample size , and the number of alternatives The number of simulation replications is 5000. For each estimator, we compute the bias, the empirical standard derivation, and the average of the standard errors across the simulation replications. Furthermore, we construct a 95% confidence interval for each element of following the standard procedure of adding and subtracting 1.96 times the standard error and report the empirical coverage of the CI (i.e., the proportion of times the so-constructed confidence interval contains the true parameter value).

Table 2 reports the results when and . The reported results are representative of other cases with a different DGP for or sample size. A few patterns emerge. First, the bias of the MLE is small and decreases with On the other hand, the bias of the QMLE is large and increases with This is consistent with our large sample result when and there is only one simulation replication. Here, the finite sample biases (with ) are averaged over 5000 simulation replications. Second, for both the MLE and QMLE, the empirical standard deviation decreases with A larger can be regarded as having more observations and, hence, smaller sampling noises. Third, for both estimators, the average of the standard errors across the simulation replications matches with the corresponding standard deviation very well. This indicates that the standard errors are reliable estimates of the standard deviation. Finally, for the MLE, the empirical coverage of the 95% confidence intervals is very close to 95%. This shows that the asymptotic normal approximation is reliable. On the other hand, for the QMLE, the empirical coverage of the 95% confidence intervals is much smaller than 95%. The only exception is the case when , where MLE and QMLE are identical. In this case, there is a small and nearly invisible difference in the empirical coverages, because the standard error for the MLE is based on the non-robust asymptotic variance estimator while the standard error for the QMLE is based on the robust sandwich asymptotic variance estimator. Both variance estimators are consistent when When the under-coverage of the CIs based on the QMLE is due to the bias in the QMLE. The larger the number of alternatives is, the larger the bias is, and the smaller the empirical coverage is.

| MLE | QMLE | ||||||||

| Empirical | Empirical | Average of | Empirical | Empirical | Empirical | Average of | Empirical | ||

| Bias | StD | SE’s | Coverage | Bias | StD | SE’s | Coverage | ||

| 0.009 | 0.211 | 0.210 | 0.951 | 0.009 | 0.211 | 0.209 | 0.948 | ||

| 0.023 | 0.240 | 0.241 | 0.950 | 0.023 | 0.240 | 0.239 | 0.950 | ||

| 0.010 | 0.209 | 0.210 | 0.950 | 0.010 | 0.209 | 0.209 | 0.950 | ||

| 0.003 | 0.105 | 0.107 | 0.957 | 0.366 | 0.141 | 0.142 | 0.261 | ||

| 0.010 | 0.136 | 0.137 | 0.950 | 0.738 | 0.175 | 0.173 | 0.004 | ||

| 0.004 | 0.106 | 0.107 | 0.958 | 0.367 | 0.142 | 0.142 | 0.266 | ||