Dynamic Contextual Pricing with

Doubly Non-Parametric Random Utility Models

Abstract

In the evolving landscape of digital commerce, adaptive dynamic pricing strategies are essential for gaining a competitive edge. This paper introduces novel doubly nonparametric random utility models that eschew traditional parametric assumptions used in estimating consumer demand’s mean utility function and noise distribution. Existing nonparametric methods like multi-scale Distributional Nearest Neighbors (DNN and TDNN), initially designed for offline regression, face challenges in dynamic online pricing due to design limitations, such as the indirect observability of utility-related variables and the absence of uniform convergence guarantees. We address these challenges with new population equations that facilitate nonparametric estimation within decision-making frameworks and establish the first analytical results on the uniform convergence rates of DNN and TDNN, enhancing their applicability in dynamic environments.

Our theoretical analysis confirms that the statistical learning rates for the mean utility function and noise distribution are minimax optimal. We also derive a regret bound that illustrates the critical interaction between model dimensionality and noise distribution smoothness, deepening our understanding of dynamic pricing under varied market conditions. These contributions offer substantial theoretical insights and practical tools for implementing effective, data-driven pricing strategies, advancing the theoretical framework of pricing models and providing robust methodologies for navigating the complexities of modern markets.

Keywords: Dynamic Contextual Pricing; Doubly Nonparametric Estimation; Distributional Nearest Neighbours; Random Utility Models; Regret Bound;

1 Introduction

Consumer demand is influenced not only by the price of a product but also by specific customer and product information, such as browsing history, zip codes, and product features. In digital sales environments, the economic model of random utility augmented with a wealth of sales data can offer crucial insights into consumer behavior, particularly consumers’ preferences and their reactions to different prices under varying contextual conditions. By implementing contextual pricing with random utility models, firms can not only gain deeper insights into the market, but also set dynamic prices tailored to individual customer profiles and product characteristics, potentially maximizing long-term revenue and gaining a competitive edge in the market.

Literature in dynamic contextual pricing often assumes a parametric form for either the mean utility, which represents the average preference of consumers, or the market noise, which captures the unobservable influences on demand. However, relying on parametric estimation poses significant disadvantages, primarily the risk of model misspecification. Parametric models make strong assumptions about the underlying data structure, and if these assumptions do not hold, the model’s predictions can be inaccurate, leading to suboptimal pricing strategies.

To address these challenges, our paper explores contextual pricing with doubly nonparametric random utility models. These models estimate both the mean utility function and the market noise’s distribution in a nonparametric manner, avoiding the pitfalls of model misspecification. The learning and decision process in these models is particularly challenging as the quantities of interest, including consumers’ true utility and the underlying market noise, are not directly observable. Sophisticated non-parametric estimation techniques designed for offline learning are not directly applicable, and they often lack the necessary theoretical guarantees for dynamic environments. We propose an innovative online approach to estimate and optimize under these models, overcoming the inherent challenges and offering a more robust framework for dynamic pricing.

1.1 Doubly Nonparametric Random Utility Models

The proposed doubly nonparametric random utility model are characterized by (1) and (2) without any parametric characterizations on or . It operates within a broad economic framework of random utility models. In such settings, products are sold individually, with each sale resulting in a binary outcome indicating success or failure. At each decision point , a -dimensional contextual covariate from is independently and identically drawn from a fixed, but a priori unknown, distribution. The expected market value of the product at time is determined by the observed contextual covariate . A general random utility model for the market value of the product is given by

| (1) |

where is the unknown function of the mean utility, and are i.i.d. noises following an unknown distribution with . We assume that the market value is within an interval with constants . Given a posted price of for the product at time , we observe that indicates whether the a sale occurs () or not (). The model is equivalent to the probabilistic model:

| (2) |

Given a posted price , the expected revenue at time conditioned on is

| (3) |

The doubly nonparametric contextual pricing works under a general economic framework of random utility models, the settings of which fundamentally differ from models that directly model the revenue function. For example, Chen and Gallego (2021) directly models the unknown expected revenue as with representing the personalized demand function. Bu et al. (2022) further assumes that separable in terms of and . In contrast, we work under the random utility model; the unknown expected revenue is given by (3) where it can be viewed as . This finer granularity in demand decomposition allows us to separately analyze the mean utility function and noise distribution, thus improving theoretical guarantees. Furthermore, our analysis highlights a crucial trade-off between the dimensionality and smoothness of and , offering practitioners a more nuanced control over pricing strategies.

The optimal price is the price that maximizes . For a policy that sets price for , its regret over the time horizon of is defined as

| (4) | ||||

The goal of this paper is to design a pricing policy that minimizes , or equivalently, maximizes the collected expected revenue .

1.2 Novelty and Contributions

This paper distincts from existing literature by adopting a fully nonparametric approach to model both the mean utility function, , and the noise distribution, , in the context of dynamic pricing with random utility. This approach eliminates the risk of model misspecification and enhances the flexibility and accuracy of our pricing strategy, which is particularly beneficial in complex and evolving market environments. We employ state-of-the-art nonparametric methods, notably the Distributional Nearest Neighbors (DNN) and the two-scale distributed nearest neighbor (TDNN) techniques, which are known for their simplicity in implementation and minimal assumptions. These estimators not only provide the flexibility needed in dynamic pricing but also achieve optimal convergence rates, improving as we scale up the model’s complexity and data fidelity.

However, existing DNN and TDNN methods, traditionally used for offline regression, are not directly applicable to the dynamic and online nature of pricing decisions due to their design limitations. Key challenges include the indirect observability of utility-related variables and the absence of robust convergence guarantees in such a dynamic context. To overcome these limitations, we employed two new population equations, (5) and (11), which enable the nonparametric estimation of both and using only binary response data . This innovative approach bypasses the need for direct measurements of variables like or , enhancing the robustness and accuracy of our estimations, and thereby substantially reducing the regret associated with pricing decisions.

Our theoretical developments include a new uniform convergence rate in Theorem 5 for the DNN and TDNN estimators. Employing the elegant U-Statistic representation of DNN and TDNN, Theorem 5 establishes that the DNN and TDNN estimators achieve the optimal rate of uniform convergence for nonparametric regression under the second-order smoothness condition and the fourth-order smoothness condition, respectively (Stone, 1982). Moreover, theoretical analyses uncover new insights into the interdependencies between the estimation accuracy for and , and how these relationships influence the performance of the overall pricing strategy in the doubly nonparametric setting. Specifically, we demonstrate that the regret bounds for our doubly nonparametric dynamic pricing model depend intricately on the trade-offs between the dimensionality of contextual variables () and the smoothness properties of the noise distribution (). To simply summarize, when , the regret is bounded by ; and when , the regret is bounded by , ignoring the logarithmic terms. Regret bounds under both settings improve upon existing nonparametric models (Chen and Gallego, 2021; Bu et al., 2022), offering finer control and better performance in practical settings.

1.3 Literature and Organization

We explore the extensive literature on contextual dynamic pricing, focusing on the underlying economic models and nonparametric techniques. Generally, this literature splits into two categories: contextual dynamic pricing under random choice models and direct modeling of demand or revenue functions. The latter is often treated as a special case of bandit problems where the reward function corresponds to the revenue function. Additionally, we review related work in dynamic pricing, including recent developments that incorporate inventory control, fairness, and privacy considerations. These areas could potentially integrate with our doubly nonparametric contextual pricing approach in future research directions.

Contextual dynamic pricing under random choice models. Recently, there has been a growing body of literature on context-based dynamic pricing, where product and customer features are taken into account when modeling the demand curve or market evaluation. We refer the reader to recent surveys (Den Boer, 2015; Ban and Keskin, 2021; Chen and Gallego, 2022; Chen et al., 2022; Chen and Hu, 2023) for a comprehensive review on this stream of literature. The most relevant literature to the present paper is those that model the demand by a binary random choice model characterized by (1) and (2). This group of literature can be categorized by the assumptions on the two unknown functions, namely the mean utility and the CDF of the noise . Assuming the CDF is a known priori, Javanmard and Nazerzadeh (2019); Cohen et al. (2020); Xu and Wang (2021) all impose a linear parametric model on the expected market value of the product at time , i.e. in (1), where is some unknown parameter, and aim to estimate the mean utility while optimizing the revenue. Alternatively, Shah et al. (2019); Fan et al. (2022); Luo et al. (2024) allow the noise distribution, i.e. the CDF in (2), to be unknown. (Fan et al., 2022; Luo et al., 2024) assume an underlying linear mean utility and estimate by kernel estimation and by the discretization method (Kleinberg and Leighton, 2003), respectively. While Shah et al. (2019) assume the market value , where has unknown distribution and propose the DEEP-C algorithm to optimize the regret. However, they all work under the settings where the mean utility is parametrically organized.

In contrast, we consider doubly nonparametric random utility models where neither or is imposed with parametric forms which is more flexible yet more challenging than considering only one non-parametric component.

Nonparametric contextual bandits and dynamic pricing as a special case. The literature on bandit problems is vast. We refer the reader to Lattimore and Szepesvári (2020); Slivkins et al. (2019) for comprehensive reviews. The most relevant literature in bandits to the present paper is nonparametric contextual bandit problems. The general contextual bandit problems consider estimating and optimizing over a random reward whose expectation is where is the contextual information and is the action taken. The -Multi-Arm contextual bandit considers discrete action and employs model for finite action space. While most bandit literature studies this problem with additional parametric models on , Perchet and Rigollet (2013); Hu et al. (2022) investigate the problem with nonparametric reward feedback under a general Hölder continuous assumption.

A stream of literature in contextual dynamic pricing models the demand function or the revenue function directly (Qiang and Bayati, 2016; Ban and Keskin, 2021; Chen and Gallego, 2021; Wang et al., 2021; Bu et al., 2022). This stream of work can be categorized into contextual bandits with a specialized reward function and continuous scalar action . Under the general bandit setting, Slivkins (2011) studies nonparametric bandits assuming that is Lipschitz and establishes the optimal regret being when is a scalar111Slivkins (2011) works with a general setting where an action can be a vector.. Mao et al. (2018) exploit a special structure where the demand function is modeled as a strictly binary feedback , where is Lipschitz, and develops the regret bound of . Guan and Jiang (2018) apply -Nearest Neighbour to nonparametric stochastic contextual bandits attaining a regret of . Under the dynamic pricing setting, Chen and Gallego (2021) estimate directly. However, they do not impose any functional structure that is specific to the dynamic pricing problem. Assuming that the revenue function is Lipschitz continuous and locally concave, the authors prove that the optimal regret is where is the dimension of . Nambiar et al. (2019) study the demand function motivated by model misspecification and propose a random price shock (RPS) algorithm to estimate price elasticity. They establish the optimal regret of order compared to a clairvoyant who knows the best linear approximation to . Bu et al. (2022) further explore the separable structure of the demand function in the sense that where both function and are unknown. This paper adopts the random utility model for demand characterization and is very different from these works in terms of aggregate demand modeling, algorithm development, and regret analysis.

Contextual dynamic pricing with related topics. There has been a wide range of literature studying contextual dynamic pricing with additional interesting topics including inventory constraints, fairness, privacy protection and more. We refer the readers to some recent works that could potentially incorporate our method in future research. In terms of joint pricing and inventory control problem, Chen et al. (2021) develop learning algorithm with censored demand and approximates nonparametrically, where represents inventory levels. Feng and Zhu (2023) further explore the impact of price protection guarantee, where the customers who purchased a product are endowed the right to receive a refund if the seller lowers the price during the price protection period. Li and Zheng (2023) take the inventory constraints into consideration where the inventory level B is given at the beginning and cannot be replenished. All those studies develop learning algorithms to estimate the underlying unknown demand functions, where our method could be seamlessly integrated. In terms of fairness, Maestre et al. (2018) consider the fairness in price, they introduce Jain’s index to measures the fairness in terms of the average price across groups, while Cohen et al. (2021) estimate unknown demand function under both price fairness and time fairness.

Additional constraints or addition conditions of related interest in dynamic pricing are explored in the following works. Chen et al. (2021) adopt the fundamental framework of differential privacy when implementing demand learning, and develop privacy-preserving dynamic pricing, which tries to maximize the retailer revenue while avoiding leakage of individual customer’s information. Keskin and Zeevi (2017) adopt a linear underlying demand model but assumes the unknown parameters can change over time. van den Boer and Keskin (2022) take reference-price effects into account and learn demand uncertainty by adding the reference-price updating mechanism with unknown parameters. Bastani et al. (2021) leverage a potentially shared structure of the demand function across multiple products and conduct a meta dynamic pricing algorithm to make pricing more efficiently.

2 Doubly Non-Parametric Learning and Decision

We propose an Algorithm 1 which outputs the empirical optimal policy for contextual dynamic pricing and balances the exploration-exploitation trade-off. The horizon of periods is divided into episodes with increasing length. Specifically, the th episode has length , where and is the minimal episode length. For each , the th episode is further divided into exploration and commit (or exploitation) phases, which are denoted by and , respectively. In the exploration phase , we collect sample through randomly setting price and then estimate both or nonparametrically using the collected sample . In the exploitation phase , we proceed to formulate a data-driven optimal policy leveraging the estimated mean utility and noise distribution learned in the exploration phase. The sizes of the exploration phase of uniform random pricing and the exploitation phase of greedy pricing based on estimation can be determined in theoretical analysis to minimize the total regret. The subsequent subsections introduce our proposed approach for the doubly non-parametric estimation of and .

2.1 Mean Utility Function Estimation

To address the challenge of not directly observing random utility , we observe the following property for both single-product dynamic pricing. Specifically, if a uniform random policy with being the upper bound for the market value is adopted, we can recover the mean utility function in an average sense. Denote by . It can be observed that given the contextual covariate , satisfies

| (5) | ||||

Therefore, if the seller randomly sets i.i.d. price for each period in the exploration phase , then the mean utility function can be estimated by regressing on based on observations .

Distributional Nearest Neighbors.

To non-parametrically estimate the mean utility function , we apply the method of Distributional Nearest Neighbors (DNN, Steele (2009); Biau et al. (2010)) which is flexible and applicable even with a limited amount of data. DNN is a variation of -Nearest Neighbours (-NN) and automatically assigns monotonic weights to the nearest neighbors in a distributional fashion on the entire sample. It incorporates the idea of bagging by averaging all 1-NN estimators, each constructed from randomly subsampling observations without replacement. Here is the subsampling scale diverging with the total sample size.

Suppose a sample of size is collected in the exploration phase of the th episode. Since satisfies (5), we build our estimator directly with . Considering a new contextual covariate observation , our goal is to fit a non-parametric mean function from the sample to estimate the underlying truth . We reorder the observations according to ’s Euclidean distance to and denote the reordered sample as such that

| (6) |

where denotes the Euclidean norm, and the ties are broken by assigning the smallest rank to the observation with the smallest natural index. is defined as the -NN estimator of based on the sample . For simpler notation, denote for . For , the DNN estimator with subsampling scale for estimating is formally defined as the average over all -NN estimators based on the -scale subsamples, that is,

| (7) |

where is the -NN estimator of based on the subsample . Specifically, with a abuse of notation, from the reordered sample of the subsample such that

| (8) |

The subsampling scale will be chosen to balance the trade-off between bias and variance. In addition, it is shown in Steele (2009) that the DNN estimator also admits an equivalent representation of a weighted nearest neighbor that

| (9) |

where is the overall ordered sample according to the ordered distance in (6).

A nice feature of the above DNN estimator is that the weights on the nearest neighbors are characterized exclusively by the total sample size and the subsampling scale . Therefore, the equivalent representation in (9) can be exploited for easy implementation, while the representation in (7) is crucial in theoretical analysis for the uniform convergence rate of the estimator.

Two-scale Distributional Nearest Neighbour.

When the mean utility function and density function of covariates have a higher degree of smoothness, two-scale DNN (TDNN, Demirkaya et al. (2022)) can be applied to eliminate the first-order bias of the DNN estimator by aggregating two DNN estimators with distinct subsampling scales and . Specifically, a TDNN estimator of the mean utility function is given by

| (10) |

where and satisfy and (this equation serves to remove the first-order bias). From these two equations, we derive the coefficients and .

In general, if the mean utility function and density function of covariates are ()-times differentiable for an integer , we can construct an -scale DNN estimator to eliminate the bias up to the -th order by constructing a linear combination of DNN estimators with distinct subsampling scales, utilizing a similar technique in (10).

2.2 Utility Noise Distribution Estimation

To non-parametrically estimate the cumulative distribution function of the random noise , the key observation is that it can be expresses through a conditional expectation:

| (11) | ||||

Thus, the Nadaraya-Watson kernel regression estimator can be applied to estimate . Given sample collected in the exploration phase and any estimated utility function , we define

| (12) | ||||

where is a chosen -th order kernel function and is the bandwidth that will be chosen appropriately later. Based on the sample and any estimated utility function , we apply the Nadaraya-Watson kernel estimator of defined by

| (13) |

In Section 2.1, we have introduced the DNN and TDNN estimators of the mean utility function. For instance, if the DNN estimator is applied for each period based on the collected sample , the estimator of the distribution in (13) can be written as

| (14) |

Analogously, the Nadaraya-Watson estimator of based on the TDNN estimator of the mean utility function is given by

| (15) |

2.3 Optimal Decision

In the -th episode, the estimators for the mean utility function and for the noise distribution , derived in the exploration phase, will be employed to inform data-driven optimal decision for dynamic pricing throughout the exploitation phase.

Oracle Optimal Decision.

Under the oracle setting where the true and are known, the optimal offered price can be determined according to

| (16) |

Under Assumption 4, the oracle optimal price is given by

| (17) |

Here is the composite function and is the first-order derivative of .

Feasible Optimal Decision.

In reality, we can only estimate and from collected data. In the -th episode of Algorithm 1, we obtain the estimated mean utility function using either the DNN or TDNN estimator and calculate the kernel estimator based on (14) or (15). Accordingly, the data-driven optimal offered price for in the exploitation phase is obtained by optimizing the estimated reward. That is, . As a result, it can be obtained that for any ,

| (18) |

where

| (19) |

Here represents the first-order derivative of and is defined by

| (20) |

where and are defined in (12) and their corresponding first derivatives are given by

3 Theoretical Guarantees

In this section, we establish the regret analysis of the proposed Algorithm 1 for doubly robust learning and decision in contextual dynamic pricing. For the theoretical analysis, we first introduce some notations and present necessary assumptions. For any candidate mean utility function , let be the density function of evaluated at and define . Therefore, the underlying true noise distribution according to (11). We next introduce the assumptions about the market noise , the distribution function , density function , and the kernel function .

Assumption 1 (Smoothness of and ).

The true distribution of the market noise is -Lipschitz. Let be the support of the market noise, it is assumed that, for any , . Moreover, it holds that for some constant .

Assumption 2 (Smoothness of ).

There exists an integer and a constant such that for all , the density function and is -Lipschitz continuous on . Moreover, there exist constants and such that for any , and . In addition, define and we assume is -Lipschitz on for all .

Assumption 3 (Condition for ).

The kernel function and are both -Lipschitz continuous with bounded support. In addition, is an order-m kernel, that is, , for , and .

Assumption 4 (Regularity condition).

There exist positive constants and such that for all with defined in (17).

Assumptions 1, 2, and 3 are standard assumptions for the smoothness of the relevant functions in nonparametric estimation and inference. The rate of convergence in Assumption 2 can be satisfied for the DNN estimator or TDNN estimator (with a further shrinked neighborhood size) with appropriately chosen subsampling sizes. Assumption 4 guarantees that is strictly increasing and, thus, the uniqueness of the optimal solution of (16). It is weaker than that in Javanmard and Nazerzadeh (2019) since is log-concave under the further restriction of .

The regret analysis unfolds in two steps. First, we will develop the uniform convergence rate of both the DNN and TDNN estimators in estimating the mean utility function , as well as the convergence rate of the Nadaraya-Watson kernel estimator for estimating the noise distribution . Second, building upon the uniform convergence rates established in the first step, we will derive an upper bound for the regret of Algorithm 1.

3.1 Statistical Convergence Rate of Learning

We will establish statistical uniform convergence of non-parametric estimators for both the mean utility function and the market noise distribution. The finite-sample uniform bound for the DNN and TDNN estimators of are presented below.

Theorem 5.

Suppose density function of and the mean utility function are twice continuously differentiable with bounded second derivatives on the compact support of . The density is bounded away from 0 and for . Then we have for the DNN estimator that with probability ,

| (21) |

Furthermore, assume density function of and the mean utility function are four times continuously differentiable with bounded second, third, and fourth-order derivatives on the compact support of . Then we have for TDNN estimator with that with probability ,

| (22) | ||||

Here is a constant depending on the underlying density function of , the mean utility function , the ratio of , and the dimensionality d, which may take difference values from line to line.

The proof of Theorem 5 can be found in Section C of the supplementary material. The uniform convergence rate results in theorem 5 and the proofs are new to the literature and hold independent interest. Regarding the the uniform convergence of DNN estimator, the first error term provides an upper bound for the bias, while the second error term corresponds to bound for the variance. In a similar manner, in the uniform bound for TDNN estimator, the first error term is related to the bias and the second error term is associated with the variance. We can observe from Theorem 5 that the TDNN estimator preserves the same order of variance as the DNN estimator but reduces the bias. This improvement is achieved by TDNN’s formulation of a linear combination of two DNN estimators, targeted at eliminating the first-order bias. For any general integer , one can employ an -scale DNN estimator, which is defined as a linear combination of DNN estimators, each with a distinct subsampling scale to remove the bias up to the -th order. This construction requires the mean utility function and density function of to have bounded derivatives up to the -th order.

Building upon the uniform convergence rate for DNN estimators, we obtain the following result on the accuracy of the kernel estimator defined in (14) for estimating the noise distribution .

Theorem 6.

Theorem 6 follows directly from applying Lemma 11 in Appendix A and Theorem 5. The first term in the upper bound comes from kernel approximation of the noise distribution, while the second term comes from the upstream estimation error of DNN estimator for mean utility . For existing work that assumes a parametric model of , the second error term is dominated by the first term (Fan et al. (2022)). However, Theorem 6 shows that the upstream estimation error of becomes non-negligible as the dimensionality grows under the more general non-parametric setting.

When TDNN estimator is applied to estimate the nonparametric mean regression function and then the same Nadaraya-Watson kernel estimator for the error distribution , we can obtain the following parallel result in Theorem 7 below for the kernel estimator when TDNN estimator is applied to estimate the mean utility function.

3.2 Regret Analysis of Decision Making

The following result establishes an upper bound for the cumulative regret of Algorithm 1 over a time horizon when DNN estimator is applied in the mean utility function estimation. The proofs of Theorem 8 and 9 are provided in Appendix A, respectively.

Theorem 8.

Remark 1.

Theorem 8 requires that the mean utility function is twice differentiable and the error distribution has -th order derivatives. The regret upper bound results from a synergistic learning of and . Specifically, learning a twice-differentiable incurs a regret bound of , while learning an -th differentiable incurs a regret bound of . Overall, the regret bound is dominated by as and is instead dominated by as .

If the mean utility function is further fourth differentiable, the more sophisticated TDNN estimator can be utilized to estimate in Algorithm 1, achieving a lower regret bound due to its debiasing capability. The corresponding regret bound of incorporating the TDNN estimator are detailed in Theorem 9 below.

Theorem 9.

Remark 2.

The overall regret of doubly-nonparametric learning and pricing is a trade-off between two components: the term of order corresponds to learning a fourth differentiable mean utility function , while the term of order corresponds to learning an -th differentiable distribution function .

When is comparatively more difficult to learn, i.e. less smooth such that , the overall regret is dominated by . When is comparatively more difficult to learn, i.e. higher-dimensional such that , the the overall regret is dominated by where the term corresponds to the setting of .

Remark 3.

Theorem 8 and 9 require only second- and fourth-order smoothness, respectively, of the true utility function . When the smoothness of reaches a general level for an even integer , it is possible to develop a -scale DNN estimator analogous to the TDNN framework that achieves better convergence rates.

Remark 4.

If we only consider the explore-and-exploit algorithms and the policy set with , where , , and are estimators for the mean utility function, noise distribution, and derivative of the noise distribution in the -th episode, respectively, then the optimality of the regret upper bound reduces to the optimality of these estimators. Based on Stone (1982), our nonparametric estimators DNN or TDNN , Nadaraya-Watson kernel estimator and its derivative , all achieve optimal rate of convergence. Therefore, the proposed algorithm using those estimators is minimax optimal when we only focus on the policy set .

Remark 5.

Our analysis can be generally extended to a broader range of nonparametric estimators for the mean utility function, such as kernel estimators, random forest, and neural network methods, provided that these estimators achieve a similar uniform convergence rate as presented in Theorem 5 for the DNN and TDNN estimators.

4 Empirical Analysis

4.1 Synthetic Data

In this subsection, we conduct large-scale simulations to illustrate the efficiency of our policy. Recall that the pricing model is characterized by (1) and (2). To elaborate, the mean utility function is set to be , where the contextual covariates are i.i.d. bounded random vectors of dimension , and each vector consists of independent entries uniformly distributed according to . The noise are i.i.d. with probability density where the smoothness order .

When implementing algorithm 1, we divide the time horizon into consecutive episodes by setting the length of the -th episode as with and . We further separate every episode into an exploration phase with length induced from Theorem 8, then the exploitation phase contains the rest of the time in that episode. In the exploration phase, we sample from , since is a valid upper bound of . In the exploitation phase, we set the kernels used in 12 as follows: . In episode , we set the bandwidth as with according to the assumptions in the theoretical analysis. In reality, one can also tune the bandwidth and the order of kernel by using cross-validation at the end of every exploration phase. Moreover, when calculating , we find as follows: First, we look for such that (We choose a large interval that contains the true support of [-0.5, 0.5], since in reality, we might only know a wider range of the true support). Then, we make a transformation of variable to and solve as the root of by using Newton’s method starting at . Finally, we set as and offer according to the algorithm.

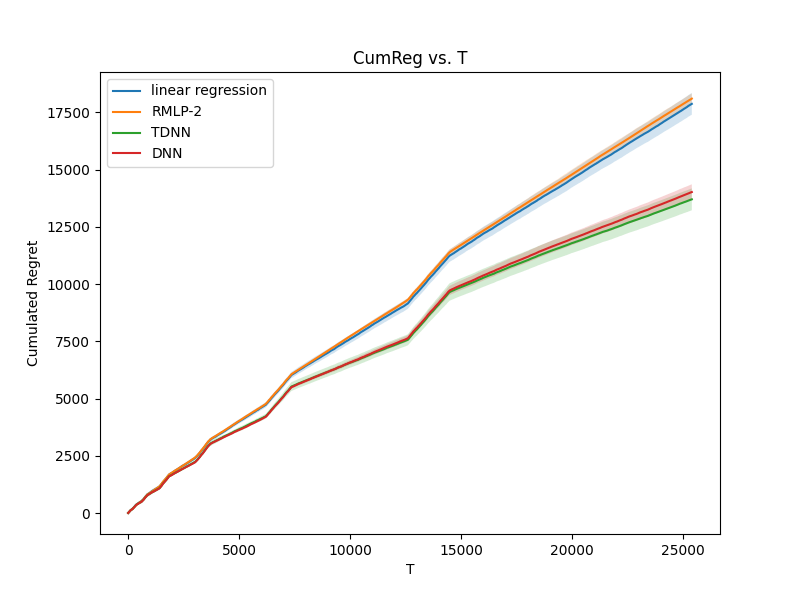

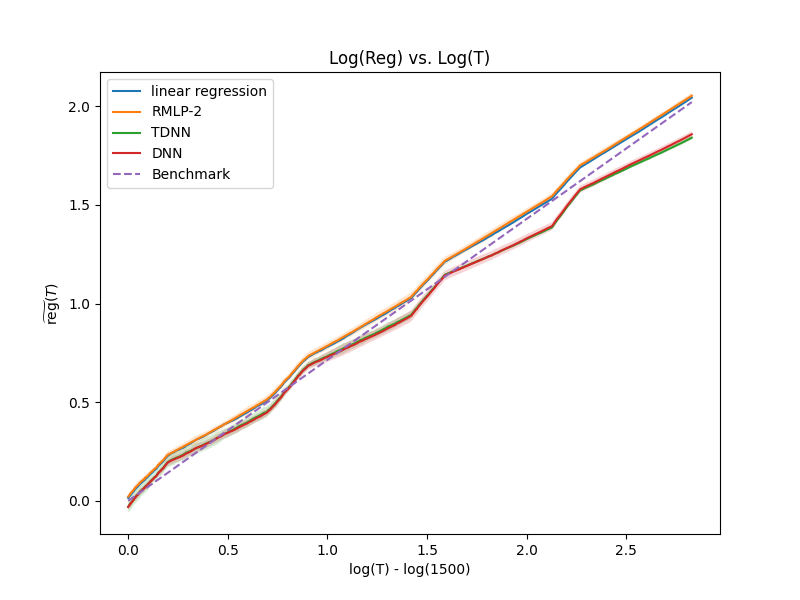

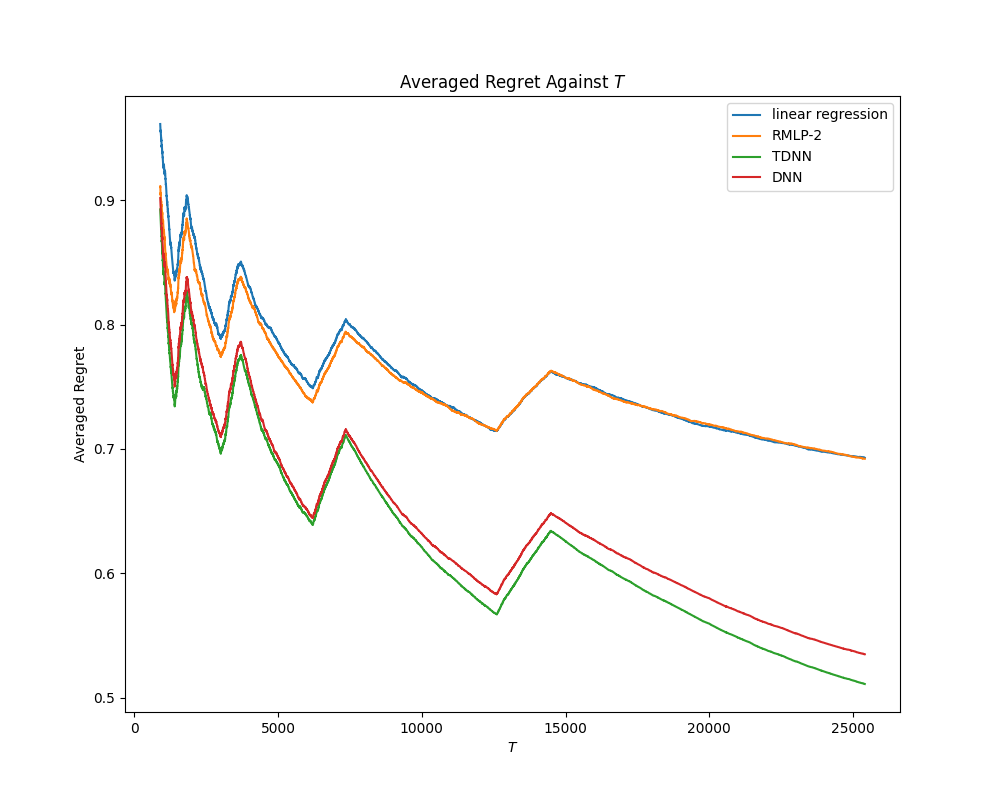

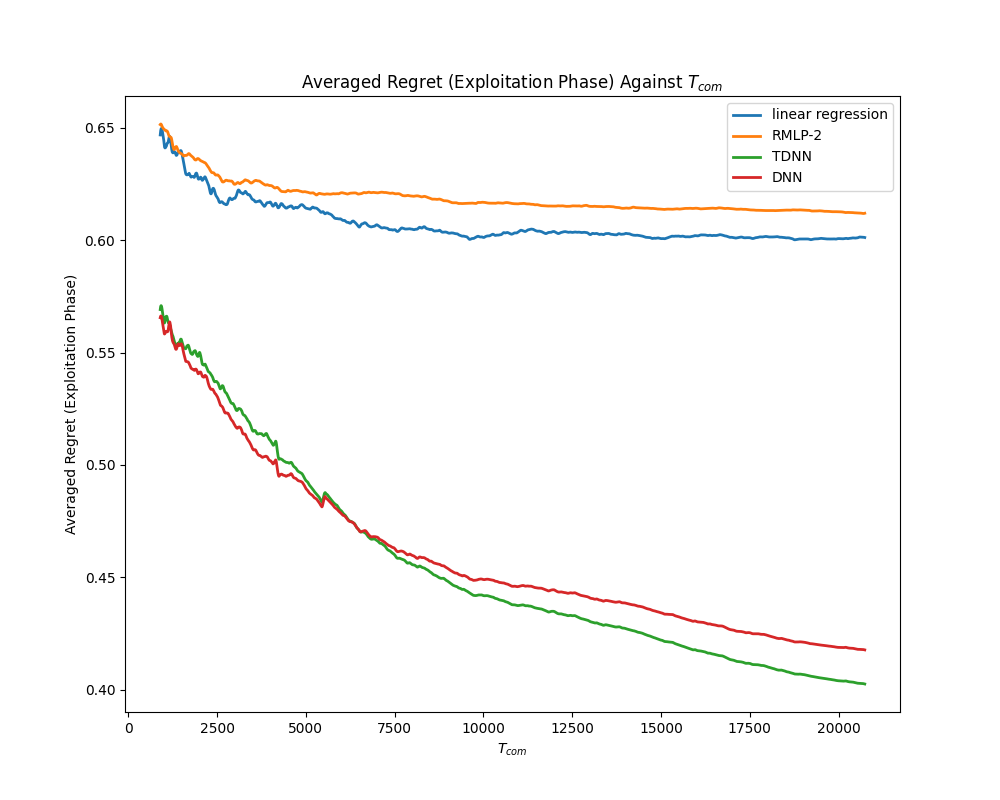

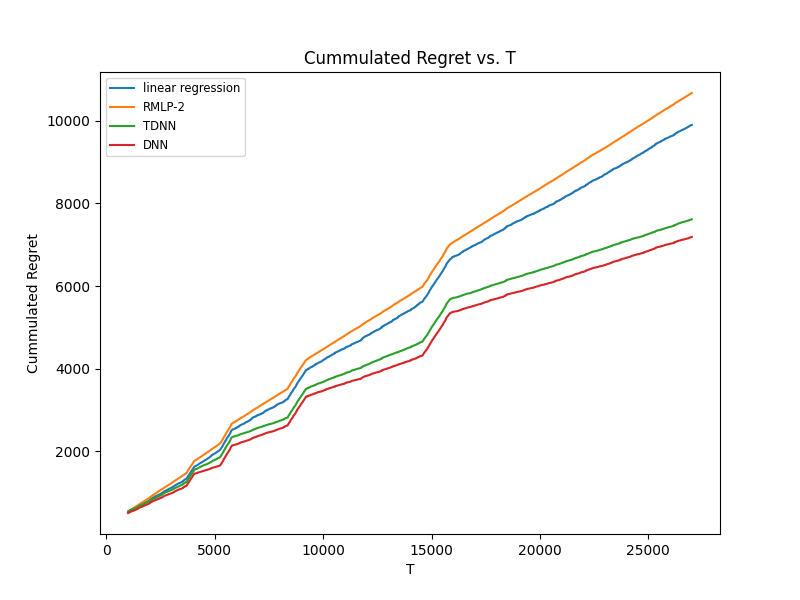

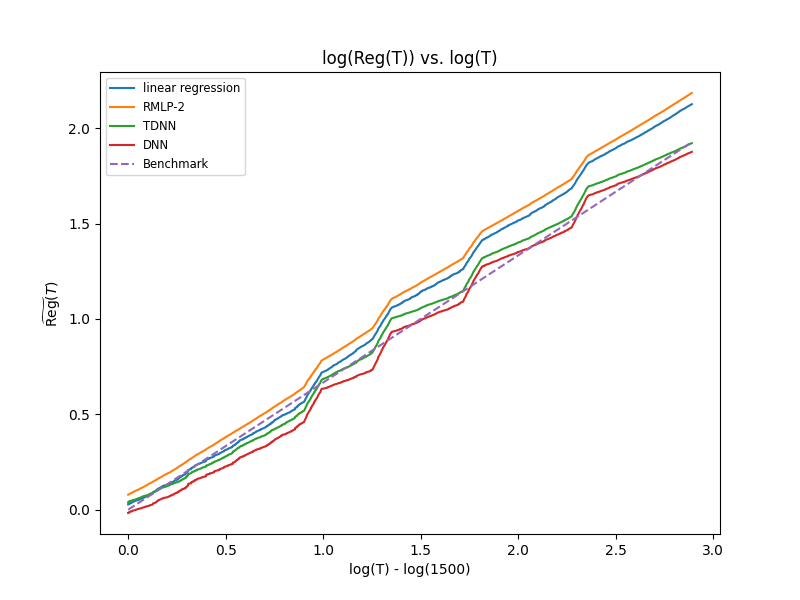

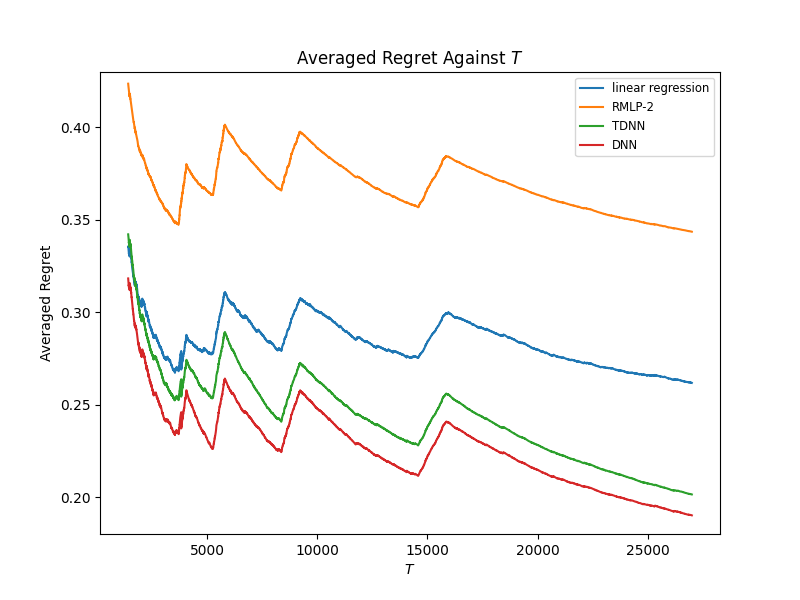

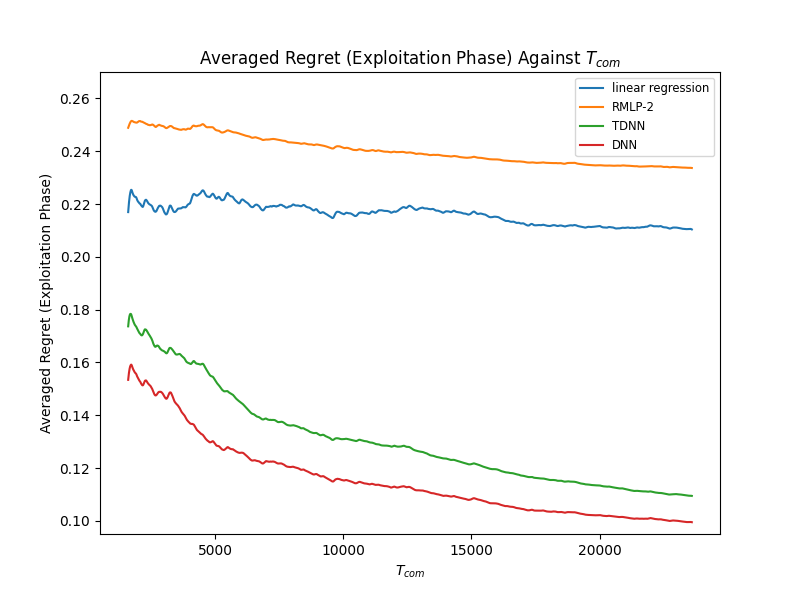

In the simulation, we also compare the efficiency of our methods with two closely related approaches: the ’RMLP-2’ proposed by (Javanmard and Nazerzadeh, 2019), and the linear model based policy introduced by (Fan et al., 2022). They both address the same problem but assume the underlying mean utility function to be the linear model and, hence, fit a linear regression during the exploration phase. Besides, the ’RMLP-2’ additionally assumes the noise distribution belongs to a parametric function class, while given the algorithm’s lack of access to the true noise distribution, we adopt a Gaussian distribution assumption for the noise. We conduct repeated trials of Algorithm 1, the linear model based policy and the ’RMLP-2’, respectively, from to , to document the cumulative regret with to . Consequently, the averaged regret is stored as And the illustration of the distinctions in performance is detailed in several figures. Specifically, we plot against in Figure 1(a), and the averaged regret against in Figure 2(a). Recall from Theorem 8 that the cummulative regret when . Hence, we plot against in Figure 1(b), where . In addition, we plot the averaged regret of the exploitation phase against in Figure 2(b), where the y-axis Averaged Regret (Exploitation Phase) is defined as: , and

From Figure 1, we conclude that under the specified setting, the rates of the empirical cumulative regrets produced by Algorithm 1 (as shown by the solid green and red lines) do not exceed their theoretical counterparts given in Theorems 8(as shown by the dashed lines). At majority of time points, the growth rates of the empirical regrets are very close to those of the theoretical line. This demonstrates the tightness of our theoretical results. We also see that the regrets we achieved are much smaller than those two approaches. As for the comparison with linear regression, TDNN and DNN estimations are robust to the mis-specification of the mean utility function, and in comparison with ’RMLP-2’, our method is robust to the mis-specification of the noise distribution since our algorithm can adapt to all noise distributions in the non-parametric class. From Figure 2, we conclude that under the same setting, Algorithm 1 incorporating TDNN estimation surpasses all other methods in performance, since as the episode length increases, the TDNN method achieves a lower regret during the exploitation phase with more accurate estimation of the underline mean utility function. In contrast, the averaged regret curves of exploitation phase for the two benchmark approaches exhibit minimal decay as the time horizon increases. Such phenomenon arises from model misspecification and the biased learning of the mean utility function by the two benchmark approaches.

4.2 Real Data Analysis

We utilize the real-life auto loan dataset from Columbia University’s Center for Pricing and Revenue Management, a dataset that has also been employed in several prior studies (Phillips et al., 2015; Ban and Keskin, 2021; Luo et al., 2024; Wang et al., 2023). This dataset encompasses 208,085 auto loan applications spanning from July 2002 to November 2004 and includes various features, such as loan amount and borrower information. For consistency, we perform feature selection in line with existing work (Ban and Keskin, 2021; Luo et al., 2024; Wang et al., 2023), focusing on the following four features: approved loan amount, FICO score, prime rate, and competitor’s rate. Regarding the price variable, we also computed it in the same way as the aforementioned literature, where . The rate is set as , which is an approximate average of the monthly London interbank rate for the studied time period. Moreover, this dataset also records the purchasing decisions of the borrowers, given the price set by the lender.

Note that one is not able to obtain online responses to any algorithms. Thus, we follow the calibration idea proposed in (Ban and Keskin, 2021; Luo et al., 2024; Wang et al., 2023) to first learn a binary choice model using the entire dataset and then leverage it as the ground truth to conduct numerical experiments. To make calibration model more stable, we process all covariates by standardization and take log of the price variable. One can also remove the extreme values that are outside the 0.01 and 0.99 percentiles to mitigate the influence of outliers. For learning the decision model, we typically fit a generalized logistic model with a quadratic form as the logits; meanwhile, instead of using a conventional logistic function, we adopt a specified sigmoid function with bounded support.

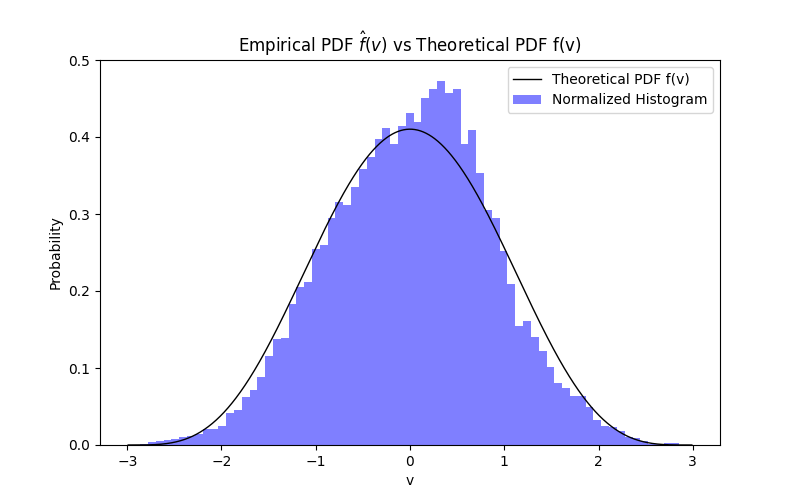

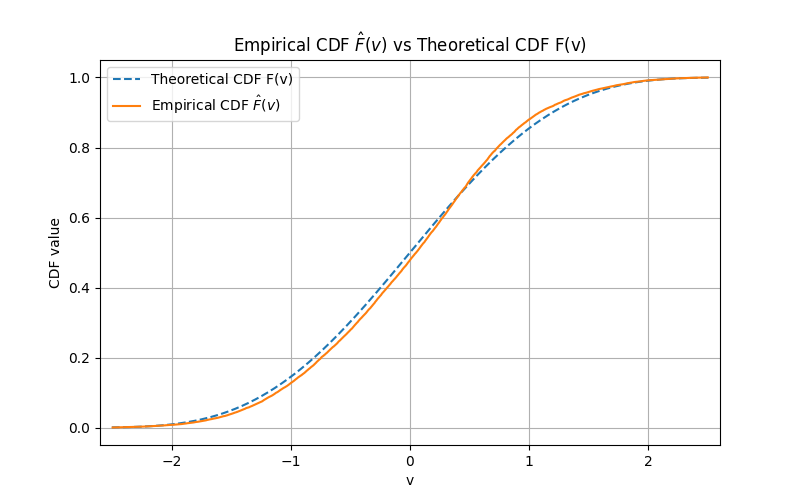

Specifically, denote the contextual covariate as and the quadratic form for the mean utility function. Then the noise are set to independently follow the distribution with probability density function Furthermore, with the belief that the coefficients of the mean utility function can be varied across the data while the noise shares the same distribution. We employ a two-stage approach learning calibration model. Initially, the covariates are divided into 20 clusters based on similarities, utilizing the K-means clustering technique. Here we denote if the covariate belongs to the -th cluster. Then, we apply generalized logistic regression to each data cluster, fitting the coefficients of the quadratic form for each group while maintaining the same noise distribution. Figure 3 demonstrates the alignment between observed data and the theoretical model over the noise , which means the calibration model is well specified.

Given these key components, the remaining experiments remain almost the same as discussed in the simulation part. Here the calibration model adopts the form , where is the learned coefficients when the contextual covariate belongs to the -th cluster. Since in reality we don’t know the true smoothness order of noise distribution, in each episode, we set the exploration phase with length . We set and conduct Algorithm 1. Recall from Theorem 8 that the regret Hence, we plot against in Figure 4(b), where .

5 Conclusion

This paper advances the field of dynamic pricing by introducing and exploring doubly nonparametric random utility models. By forgoing parametric assumptions for both the mean utility function and the noise distribution, our approach reduces the risk of model misspecification and increases the reliability of pricing strategies. Employing advanced nonparametric estimation techniques like Distributional Nearest Neighbors and Nadaraya-Watson kernel estimation, we enhance the accuracy of dynamic pricing decisions in complex market environments. Our theoretical contributions, which include new analytical results and insights into the interaction between model components, offer valuable guidance for both academic research and practical applications. This work not only deepens the understanding of nonparametric estimation in pricing models but also provides a robust framework for businesses to optimize pricing dynamically and effectively in data-driven markets.

References

- Ai et al. (2022) Ai, J., O. Kuželka, and Y. Wang (2022). Hoeffding and bernstein inequalities for u-statistics without replacement. Statistics & Probability Letters 187, 109528.

- Ban and Keskin (2021) Ban, G.-Y. and N. B. Keskin (2021). Personalized dynamic pricing with machine learning: High-dimensional features and heterogeneous elasticity. Management Science 67(9), 5549–5568.

- Bastani et al. (2021) Bastani, H., D. Simchi-Levi, and R. Zhu (2021). Meta dynamic pricing: Transfer learning across experiments. Management Science 68(3), 1865–1881.

- Biau et al. (2010) Biau, G., F. Cérou, and A. Guyader (2010). On the rate of convergence of the bagged nearest neighbor estimate. Journal of Machine Learning Research 11(2).

- Bu et al. (2022) Bu, J., D. Simchi-Levi, and C. Wang (2022). Context-based dynamic pricing with separable demand models. Available at SSRN.

- Chen et al. (2021) Chen, B., X. Chao, and C. Shi (2021). Nonparametric learning algorithms for joint pricing and inventory control with lost sales and censored demand. Mathematics of Operations Research 46(2), 726–756.

- Chen and Gallego (2021) Chen, N. and G. Gallego (2021). Nonparametric pricing analytics with customer covariates. Operations Research 69(3), 974–984.

- Chen and Gallego (2022) Chen, N. and G. Gallego (2022). A primal–dual learning algorithm for personalized dynamic pricing with an inventory constraint. Mathematics of Operations Research 47(4), 2585–2613.

- Chen and Hu (2023) Chen, N. and M. Hu (2023). Data-driven revenue management: The interplay of data, model, and decisions. Service Science.

- Chen et al. (2022) Chen, X., S. Jasin, and C. Shi (2022). The Elements of Joint Learning and Optimization in Operations Management, Volume 18. Springer Nature.

- Chen et al. (2021) Chen, X., D. Simchi-Levi, and Y. Wang (2021). Privacy-preserving dynamic personalized pricing with demand learning. Management Science 68(7), 4878–4898.

- Cohen et al. (2020) Cohen, M. C., I. Lobel, and R. Paes Leme (2020). Feature-based dynamic pricing. Management Science 66(11), 4921–4943.

- Cohen et al. (2021) Cohen, M. C., S. Miao, and Y. Wang (2021). Dynamic pricing with fairness constraints.

- Demirkaya et al. (2022) Demirkaya, E., Y. Fan, L. Gao, J. Lv, P. Vossler, and J. Wang (2022). Optimal nonparametric inference with two-scale distributional nearest neighbors. Journal of the American Statistical Association, 1–11.

- Den Boer (2015) Den Boer, A. V. (2015). Dynamic pricing and learning: historical origins, current research, and new directions. Surveys in operations research and management science 20(1), 1–18.

- Fan et al. (2022) Fan, J., Y. Guo, and M. Yu (2022). Policy optimization using semiparametric models for dynamic pricing. Journal of the American Statistical Association, 1–29.

- Feng and Zhu (2023) Feng, Q. and R. Zhu (2023, Jul). Principro: Data-driven algorithms for joint pricing and inventory control under price protection. Available at SSRN.

- Guan and Jiang (2018) Guan, M. and H. Jiang (2018). Nonparametric stochastic contextual bandits. In Proceedings of the AAAI Conference on Artificial Intelligence, Volume 32.

- Hu et al. (2022) Hu, Y., N. Kallus, and X. Mao (2022). Smooth contextual bandits: Bridging the parametric and nondifferentiable regret regimes. Operations Research 70(6), 3261–3281.

- Javanmard and Nazerzadeh (2019) Javanmard, A. and H. Nazerzadeh (2019). Dynamic pricing in high-dimensions. The Journal of Machine Learning Research 20(1), 315–363.

- Jiang (2019) Jiang, H. (2019). Non-asymptotic uniform rates of consistency for k-nn regression. In Proceedings of the AAAI Conference on Artificial Intelligence, Volume 33, pp. 3999–4006.

- Keskin and Zeevi (2017) Keskin, N. B. and A. Zeevi (2017). Chasing demand: Learning and earning in a changing environment. Mathematics of Operations Research 42(2), 277–307.

- Kleinberg and Leighton (2003) Kleinberg, R. and T. Leighton (2003). The value of knowing a demand curve: Bounds on regret for online posted-price auctions. In 44th Annual IEEE Symposium on Foundations of Computer Science, 2003. Proceedings., pp. 594–605. IEEE.

- Lattimore and Szepesvári (2020) Lattimore, T. and C. Szepesvári (2020). Bandit algorithms. Cambridge University Press.

- Li and Zheng (2023) Li, X. and Z. Zheng (2023). Dynamic pricing with external information and inventory constraint. Management Science 0(0).

- Luo et al. (2024) Luo, Y., W. W. Sun, and Y. Liu (2024). Distribution-free contextual dynamic pricing. Mathematics of Operations Research 49(1), 599–618.

- Maestre et al. (2018) Maestre, R., J. Duque, A. Rubio, and J. Arévalo (2018). Reinforcement learning for fair dynamic pricing. In Proceedings of SAI Intelligent Systems Conference, pp. 120–135. Springer.

- Mao et al. (2018) Mao, J., R. Leme, and J. Schneider (2018). Contextual pricing for lipschitz buyers. In Advances in Neural Information Processing Systems, Volume 31.

- Nambiar et al. (2019) Nambiar, M., D. Simchi-Levi, and H. Wang (2019). Dynamic learning and pricing with model misspecification. Management Science 65(11), 4980–5000.

- Perchet and Rigollet (2013) Perchet, V. and P. Rigollet (2013). The multi-armed bandit problem with covariates. The Annals of Statistics 41(2), 693–721.

- Phillips et al. (2015) Phillips, R., A. S. Şimşek, and G. van Ryzin (2015). The effectiveness of field price discretion: Empirical evidence from auto lending. Management Science 61(8), 1741–1759.

- Qiang and Bayati (2016) Qiang, S. and M. Bayati (2016). Dynamic pricing with demand covariates. arXiv preprint arXiv:1604.07463.

- Shah et al. (2019) Shah, V., R. Johari, and J. Blanchet (2019). Semi-parametric dynamic contextual pricing. In Advances in Neural Information Processing Systems, Volume 32.

- Slivkins (2011) Slivkins, A. (2011). Contextual bandits with similarity information. In Proceedings of the 24th annual Conference On Learning Theory, pp. 679–702. JMLR Workshop and Conference Proceedings.

- Slivkins et al. (2019) Slivkins, A. et al. (2019). Introduction to multi-armed bandits. Foundations and Trends® in Machine Learning 12(1-2), 1–286.

- Steele (2009) Steele, B. M. (2009). Exact bootstrap k-nearest neighbor learners. Machine Learning 74, 235–255.

- Stone (1982) Stone, C. J. (1982). Optimal global rates of convergence for nonparametric regression. Ann. Statist. 10(4), 1040–1053.

- van den Boer and Keskin (2022) van den Boer, A. V. and N. B. Keskin (2022). Dynamic pricing with demand learning and reference effects. Management Science 68(10), 7112–7130.

- Wang et al. (2023) Wang, C. H., Z. Wang, W. W. Sun, and G. Cheng (2023). Online regularization toward always-valid high-dimensional dynamic pricing. Journal of the American Statistical Association, 1–13.

- Wang et al. (2021) Wang, Y., X. Chen, X. Chang, and D. Ge (2021). Uncertainty quantification for demand prediction in contextual dynamic pricing. Production and Operations Management 30(6), 1703–1717.

- Xu and Wang (2021) Xu, J. and Y.-X. Wang (2021). Logarithmic regret in feature-based dynamic pricing. Advances in Neural Information Processing Systems 34, 13898–13910.

Supplementary Material of

“Dynamic Contextual Pricing with

Doubly Non-Parametric Random Utility Models”

Elynn Chen♭ Xi Chen♮ Lan Gao♯ Jiayu Li†

♭,♮,†Leonard N. Stern School of Business, New York University.

♯ Haslam College of Business, University of Tennessee Knoxville.

Appendix A Proof of Regret Bounds (Theorems 8 and 9)

The regret upper bound relies on the statistical convergence rate in estimating the mean utility function . To present our proof in a more general framework, Lemmas 11, 12, 13 and most proofs of Theorem 5 are build upon the following general assumption on the accuracy for an estimator of the . Specifically, when dealing with the DNN and TDNN estimators outlined in Section 2.1, we can deduce that the convergence rate by applying Theorem 5 with and .

Assumption 10.

Suppose an estimator is applied using i.i.d. observations , where is the exploration phase in the -th episode. Let be the number of observations in . Assume there exists a vanishing sequence such that

| (27) |

A.1 Proof of Theorem 8

The proof consists of two major steps. The first step is to establish the approximation accuracy of the kernel estimator for estimating the noise distribution , provided with the accuracy of the estimator for the non-parametric regression function . Therefore, we can obtain the approximation accuracy of the data-driven optimal price towards the optimal price . The second step is built on the accuracy derived for in the first step and establishes the overall regret bound. For simplicity, we denote by ignoring its dependence on the data points collected in the exploration phase. We define

| (28) |

and choose the bandwidth in the kernel estimators defined in (12).

Step 1. Establish the following three lemmas on the approximation accuracy of kernel estimator and its first-order derivative. In addition, we will also show the approximation accuracy of the estimator (defined in (19)) which plays a crucial role in determining the data-driven optimal price . Their proofs are presented in Sections B.1, B.2 and B.3, respectively.

Lemma 11 (Generalization of Theorem 6).

Lemma 12 (First derivative of noise c.d.f.).

Under the same condition as Lemma 11, it holds with probability at least that

| (30) |

where is a constant.

Lemma 13.

Assume the same condition as Lemma 11, and and , it holds with probability at least that

| (31) |

where is a constant.

We are now ready to bound the regret of our policy. For a policy that assigns a price at , its instant regret at time is defined as

| (32) |

where is the oracle optimal price given in (17). For the episode-based algorithm, we further define the accumulated regret in each episode :

| (33) |

Since the length of the episodes grows exponentially, the number of episodes by period is logarithmic in . Specifically, belongs to episode . Without loss of generality, we deal with the setting for some integer number . Hence, regret over the time horizon of can be expressed as

| (34) |

We bound the total regret over each episode by considering two separate cases where is relatively small or large.

Case I. When , we have . Those episodes are not long enough to accurately estimate and . We use the fact that to construct a naive upper bound. That is,

| (35) | ||||

Case II. When , we consider

| (36) |

where is the filtration generated by and the current feature . We write

| (37) | ||||

where is defined as the expected revenue under price . Note that and thus . It follows by Taylor expansion that

| (38) |

for some between and . Let , we claim that, for any between and ,

| (39) |

which is derived by the fact that

and . Combining (37), (38) and (39), we obtain

Let be the price given by Algorithm 1. Then it holds that

We can obtain by (36) as well as the definitions of and in (16) and (18) that

| (40) | ||||

| (41) |

We first analyze the first term on the right hand side of (41). It can be seen from Lemma 14 that for ,

Furthermore, applying Lemma 13 (let ), we have

| (42) | ||||

Next, for the second term in (41), in view of the fact that , we can obtain by Assumption 4 that

| (43) | ||||

In addition, under Assumption 10, it holds that

| (44) | ||||

Combining the inequalities (41) – (44) yields the following upper bound for the expected regret at any time during the commitment phase in episode :

Consequently, for , the total regret during the -th episode is

| (45) | ||||

Now we need to consider specific estimators with specific convergence rate in order to further choose an optimized exploration phase size and commitment phase size to minimize the regret . We consider DNN estimator in the sequel.

When DNN estimator is applied to estimate the mean utility function, we choose the involved subsampling scale , then it follows from Theorem 5 that Assumption 10 is satisfied for the DNN estimator with convergence rate . If , , otherwise if , . When , by setting and , we have for , and hence the condition is satisfied for Lemmas 11 – 13. Noting that , it follows from (45) that for ,

| (46) | ||||

where is a constant which can take different values from line to line. In view of (35) and (46), we obtain that the total regret over time horizon is bounded by

| (47) |

where we have used the definition that and the fact that .

A.2 Proof of Theorem 9

When TDNN estimator is applied in the mean utility function estimation with , it follows from Theorem 5 that the uniform convergence rate holds in the Assumption 10. If , it holds that , otherwise if , we have . When , by setting , we have for ,

In view of (35) and (46), we obtain that the total regret over time horizon is bounded by

| (49) |

where is a constant which can take different values from line to line.

When , by letting , we have for ,

Therefore, in view of (35) and (46), the total regret over time horizon is bounded by

| (50) |

where is a constant which can take different values from line to line. Combining the bound in (49) as and the bound in (50) as yields the desired result in (26). This completes the proof of Theorem 9.

Appendix B Proof of Lemmas

B.1 Proof of Lemma 11

Recall that and . The proof builds on the intuition that the kernel estimator converges to the population conditional expectation and further approaches as approaches . By the triangular inequality, we have

| (51) | ||||

In the sequel, we will bound each of the two terms on the right hand side of (51).

First, we concern ourselves with the accuracy of kernel estimator for a fixed . Applying the same technique of proving Lemma 4.2 in Fan et al. (2022), we can obtain that with probability at least ,

| (52) |

Next, regarding the second term on the right hand side of (51), recalling the definition of the neighborhood given in (28), we have for any ,

| (53) | ||||

and similarly,

| (54) | ||||

Therefore, by Assumption 1 that is -Lipschitz, we have

| (55) |

A combination of (51), (52) and (55) yields Lemma 11. This concludes the proof of Lemma 11.

B.2 Proof of Lemma 12

By the triangular inequality, we have

| (56) | ||||

Recall that is the density function of evaluated at , , and . We also define the following quantities:

Then it holds that

and , where

First, according to Assumption 1, the second term on the right hand side of (56) can be bounded by

| (57) |

Next we proceed to consider the first term in (56). Observe that

where we have omitted the dependence of the functions on and for notational simplicity. By Assumption 2 and Lemmas A.3 and A.4 in Fan et al. (2022), we obtain that with probability at least ,

| (58) |

Consequently, the desired result follows from a combination of (56), (57) and (58). This completes the proof of Lemma 12.

B.3 Proof of Lemma 13

Observe that the data-driven optimal price . We begin with presenting Lemma 14 that provides the range of for any and , which will be useful in our proof.

Lemma 14.

Under the conditions of Lemma 13, for any and , .

Proof of Lemma 13.

Recall the definitions of estimator in (19) and the population quantity in (17) that

| (59) |

and

| (60) |

Observe that

| (61) |

Thus it suffices to study the upper bound for .

Step. I. First, we derive a uniform upper bound for , which can be decomposed by

By Assumption 1, we have (noting that is an increasing function by Assumption 4)

and applying the continuity of yields that for some constant ,

| (62) |

Step. II. We bound through . The computation here involves obtaining the inverse of , which is not necessarily monotone. To deal with this challenge, we will show in the sequel that is very ‘close’ to in some main interval of interest, which contains and depends only on . Since , it holds that and similarly, . Therefore, we have . Moreover, by (B.3), we can deduce that as and ,

and

By continuity of and , it follows that

For , we define the inverse of as

| (63) |

B.4 Proof of Lemma 14

Proof of Lemma 14.

First, we show that for any ,

| (65) |

This can be validated as follows. Recall the definition that , where by assumption and . Since is independent of , to ensure , it must follow that .

Appendix C Proofs of Uniform Finite-Sample Bounds of DNN or TDNN

Recall that the DNN and TDNN estimators are constructed using the sample of size , where with being an Bernoulli random variable. To simplify the notation, we denote in this section when there is no ambiguity.

C.1 Proof of Theorem 5

We first prove the result (21) for the DNN estimator. The main idea of proof is to apply a bias-variance decomposition for the DNN estimator. The bias term can be bounded using existing result in Demirkaya et al. (2022) and the variance term can be addressed by applying the bound differences inequality in empirical theory and concentration inequality for U-statistic. Observe that the estimation error can be decomposed as

| (67) |

For the second term related to the bias, it follows from applying a similar technique of proving Theorem 1 in Demirkaya et al. (2022) that

| (68) |

where is a constant depending on the underlying density function of , the mean utility function and the dimensionality .

For the first term related to the variance in (67), observe that is a U-statistic of order . The main idea is to apply the concentration inequality for U-statistics and the fact that there are only finite number of distinct -NN sets over for any , given i.i.d samples. First, by Hoeffding inequality of U-statistic (Ai et al. (2022)), noting that , we have for any .

| (69) |

In addition, note that Lemma 3 in Jiang (2019) shows that there are at most distinct -NN sets over for any , given i.i.d. samples. Therefore, for fixed and , the DNN estimator can take at most distinct possible values in view of its L-statistic representation in (9). Consequently, applying union bound and (69) yields for any ,

| (70) |

Therefore, we have

| (71) |

which combining with (68) derives the desired uniform convergence rate for DNN estimator given in (21).

Next we deal with the TDNN estimator . Recall that the TDNN estimator is a linear combination of two DNN estimators with distinct subsampling scales and , that is,

where and . Similarly, we have the bias-variance decomposition

| (72) | ||||

By Corollary 1 in Demirkaya et al. (2022), it holds that

| (73) |

where is a constant depending on the underlying density function of , the mean utility function and the dimensionality .

Moreover, we have for the variance term that

Therefore, it follows from (71) that with probability ,

| (74) | ||||

where is a constant depending on the dimensionality and the ratio of . Substituting (73) and (74) into (72) yields the desired result (22) for TDNN estimator. The proof of Theorem 5 is completed.