A Two-layer Stochastic Game Approach to Reinsurance Contracting and Competition

Abstract

We introduce a two-layer stochastic game model to study reinsurance contracting and competition in a market with one insurer and two competing reinsurers. The insurer negotiates with both reinsurers simultaneously for proportional reinsurance contracts that are priced using the variance premium principle; the reinsurance contracting between the insurer and each reinsurer is modeled as a Stackelberg game. The two reinsurers compete for business from the insurer and optimize the so-called relative performance, instead of their own surplus; the competition game between the two reinsurers is settled by a non-cooperative Nash game. We obtain a sufficient and necessary condition, related to the competition degrees of the two reinsurers, for the existence of an equilibrium. We show that the equilibrium, if exists, is unique, and the equilibrium strategy of each player is constant, fully characterized in semi-closed form. Additionally, we obtain interesting sensitivity results for the equilibrium strategies through both an analytical and numerical study.

Key words: Game theory; Stackelberg game; Non-cooperative Nash game; Optimal reinsurance; Relative performance

1 Introduction

Insurers play a critical role in maintaining the financial stability of households and businesses, but they also face significant claim risks that can threaten their solvency. To mitigate these risks, insurers can diversify their insurance portfolios through reinsurance. Of course, when reinsurers offer reinsurance coverage to insurers, their goal is not solely to help insurers maintain solvency but also to generate profit from such businesses. As the customers of reinsurance are relatively limited, especially when comparing to those of regular insurance policies, reinsurers naturally compete for those limited customers (insurers), and the competition in turn motivates reinsurers to take into account the competitors’ strategies in their own decision making. To capture the contract negotiation and business competition in the reinsurance market, we propose a two-layer stochastic game model with one insurer and two reinsurers, and aim to obtain an equilibrium for such a complex game. The topic of optimal reinsurance is well studied in the actuarial literature, and papers on dynamic reinsurance often differ in contract types, risk models, premium rules, optimization criteria (preferences), and additional controls (such as investment and dividend decisions). The two dominate reinsurance contracts are excess-of-loss reinsurance (see Asmussen et al., (2000)) and proportional reinsurance, also called quota-share reinsurance (see Schmidli, (2001)). Regarding the insurer’s risk exposure, a standard choice is the classical Cramér-Lundberg model (see Schmidli, (2002)), but its approximating diffusion model is equally popular (see Asmussen et al., (2000) and Schmidli, (2001)). When it comes to the premium principles, the expected value principle is arguably the most common option (see Schmidli, (2001)), and the variance principle is another popular choice (see Chi, (2012) and Liang and Yuen, (2016)). Further generalizations include the mean-CVaR premium principle (see Tan et al., (2020)) and extended distortion premium principles (see Jin et al., (2024)). Early works often adopt maximizing expected utility or minimizing ruin probability as their optimization criterion, but mean-variance preferences are also frequently used (see Li et al., (2015)). Several recent papers take into account ambiguity in modeling and apply different ambiguity preferences in the study (see Gu et al., (2018) for the worst-case approach and Zhang and Li, (2021) for the -maxmin preferences). Risk constraints, such as VaR and CVaR (CTE), can be incorporated so that the obtained optimal contracts help insurers meet the regulatory requirements in practice (see Tan et al., (2009) and Lu et al., (2016)). Last, we mention that some recent contributions to this topic include novel features in their models; for instance, Gu et al., (2018) allow the insurer to invest their surplus in a financial market to explore statistical arbitrages caused by mispricing of stocks, and Peng et al., (2021) consider an insurer who possesses inside information on the asset prices. We refer interested readers to Cai and Chi, (2020) for a review article and Albrecher et al., (2017) for a monograph on optimal reinsurance. Traditionally, research on optimal reinsurance takes the viewpoint of the insurer and seeks an optimal reinsurance contract that optimizes the insurer’s objective; see those reviewed above for evidence. However, both parties of a reinsurance contract come to an agreement through bargaining and negotiations. As such, to better describe the negotiation process, we should propose models that can capture the strategic interplay between the insurer and reinsurer of a contract. One obvious solution is to apply game theory and seek an equilibrium contract that takes into account the interests of both parties at the same time. Indeed, there has been a burgeoning interest to model reinsurance contracting as a game in recent years. Jiang et al., (2019) introduce a two-person cooperative game and solve it to obtain the equilibrium reinsurance contract. On the other hand, Chen and Shen, (2018, 2019) model the reinsurance contracting as a Stackelberg game, which is a type of noncooperative game. In this work, we adopt a game approach to study reinsurance contracting problems. In particular, we follow Chen and Shen, (2018) and model reinsurance contracting as a dynamic Stackelberg game. In such a game, the reinsurer is the leader and chooses the premium principle, while the insurer is the follower and chooses its reinsurance coverage. The hierarchical structure reflects the fact that reinsurers often have more advantages in negotiation; mathematically, this feature implies that the reinsurer knows the insurer’s optimal decision and uses such information in determining its own optimal strategy (premium). We note that the (dynamic) Stackelberg game framework has already received considerable attention since Chen and Shen, (2018, 2019), which are likely the first two papers proposing such a framework. For instance, Li and Young, (2022) generalize Chen and Shen, (2019) to a mean-variance premium principle and a random planning horizon; Cao et al., (2022) consider a general Lévy risk process and allow the insurer and reinsurer to have heterogeneous, ambiguous beliefs on the risk distribution. However, the Stackelberg game model for reinsurance discussed earlier (see Chen and Shen, (2018, 2019), Li and Young, (2022), and Cao et al., (2022)) only considers the simple case of one insurer and one reinsurer, and thus cannot capture the observed fact that insurers often seek reinsurance coverage from multiple reinsurers at the same time.111Reinsurers also compete with each other to win business from large insurers, as argued in Boonen et al., (2021) and Zhu et al., (2023). A minimum model that is consistent with this fact should consist of one insurer and two reinsurers; one of such models is proposed in Cao et al., 2023b . In that paper, the insurer faces two Stackelberg reinsurance games, and its optimal reinsurance strategies depends on the premium rules by both reinsurers in the market (one insurer applies the expected-value principle but the other uses the variance principle). As a result, although the two reinsurers in Cao et al., 2023b are not directly linked, each impacts the other’s decision through the common insurer. Cao et al., 2023b extend the -reinsurer model in Cao et al., 2023a to an -reinsurer model, in which all reinsurers apply the variance premium principle. Both Cao et al., 2023a ; Cao et al., 2023b adopt the ambiguity-averse and risk-neutral preferences from Cao et al., (2022) and obtain unique equilibrium strategies for all players. There are also recent works that propose a similar multi-player setup in their game model. Wang et al., (2020) study an asymmetric information linear-quadratic stochastic Stackelberg differential game with one leader and two followers; see also Kroell et al., (2023) for a model with multiple insurers (followers). Bo et al., (2024) consider an insurance market consisting of multiple competing insurers with a mean-field type interaction via the relative performance of their terminal wealth. With the motivations discussed above, we are now ready to present the game model in this paper, which is largely inspired by the one in Cao et al., 2023b . The reinsurance market is composed of one representative insurer and two competing reinsurers, who both apply the variance premium principle,222Chi, (2012) studies optimal reinsurance under variance related premium principles and argues that they form a crucial family of premium principles in actuarial science. We comment that the variance principle is indeed frequently used in the study of optimal reinsurance problems; see Zhou and Yuen, (2012), Chen et al., (2016), Liang and Yuen, (2016), Chen and Shen, (2019), and Cao et al., 2023a ; Cao et al., 2023b for a short list. but possibly with different loading factors, to price their reinsurance contracts. The insurer seeks proportional reinsurance contracts from both reinsurers simultaneously and thus faces two parallel Stackelberg reinsurance games. Given the variance loading factors , the insurer’s goal is to find its optimal reinsurance ceded proportions , in which is the optimal proportion ceded to Reinsurer , , and, as imagined, depends on the two reinsurers’ joint premium strategy . The two reinsurers in Cao et al., 2023b compete in an indirect way, but here they compete directly. To be precise, Reinsurer in our model does not optimize its own surplus, , at the terminal time , but compares its wealth to , the competitor, Reinsurer ’s wealth ( and ); by following Bensoussan et al., (2014), we define the so-called relative performance , in which , and assume that Reinsurer optimizes its relative performance as a way to model direct competition. Therefore, the two reinsurers in our model interact via two channels: the relative performance in their optimization criterion and the feedback response from the insurer; we note that Cao et al., 2023b only consider the latter channel. To settle the competition game, we resort to the notion of classical non-cooperative Nash game, in which the two reinsurers make decisions simultaneously. To summarize, we propose a novel two-layer stochastic game model to study reinsurance contracting and competition, with the former by two parallel Stackelberg games and the latter by a non-cooperative Nash game. All three players are utility maximizers, and we further assume that their preferences are given by an exponential, also called CARA (Constant Absolute Risk Aversion) utility function. Under the proposed game, the two reinsurers aim to find their equilibrium premium strategy , , and the insurer seeks an equilibrium reinsurance strategy . The key findings and contributions of this paper are discussed as follows. First, we propose a novel two-layer game model with multiple (two) reinsurers, which incorporates desirable features from at least three types of models: dynamic Stackelberg game models (see Chen and Shen, (2018)), models with multiple reinsurers (see Cao et al., 2023b ), and game models with relative performance (see Bensoussan et al., (2014)). Second, we obtain a sufficient and necessary condition for the existence of a game equilibrium, given explicitly by , in which is the competition degree parameter of Reinsurer in its relative performance, . Such a condition is precise and sharp because we show that if , the proposed game admits no equilibrium. In addition, when holds, the equilibrium is unique, and all equilibrium strategies are constant, even though random (stochastic) strategies are allowed in the mathematical formulation. We are able to fully characterize the equilibrium strategies for all players in semi-closed form, subject to finding a unique fixed point of a bivariate function (such a task is easy from the computational point of view). Third, for the reinsurers’ equilibrium premium strategies, we obtain analytical results on the impact of risk aversion and competition degree . We show that the increase of one player’s risk aversion will cause both reinsurers to charge a higher loading under equilibrium, but the competition drives them to lower the premium. We also conduct a numerical study to investigate how those model parameters affect the insurer’s reinsurance decisions. The key findings are that the insurer cedes more risk to reinsurers when its own risk aversion increases or when the reinsurers are less risk averse. The rest of the paper is organized as follows. We introduce the two-layer Stackelberg-Nash game model in Section 2. In Section 3, we solve the equilibrium strategies for all players in the Stackelberg game. We then analyze the equilibrium strategies mathematically and give the economic explanation in Section 4. Section 5 concludes this paper. Several technical proofs are placed in Appendix A.

2 Model

We consider a reinsurance market consisting of one insurer, labeled as Insurer (player) 0, and two competing reinsurers, labeled as Reinsurer (player) 1 and 2, over a finite horizon , with denoting the terminal time. To account for the competition between the two reinsurers, we assume that the market is formed under a tree structure as in Cao et al., 2023b ; Cao et al., 2023a ; see Figure 1 for graphic illustration. Under such a market formulation, the insurer negotiates reinsurance contracts with both reinsurers simultaneously, and the two reinsurers compete for business from the insurer. Note that our model includes two degenerate cases in which the insurer only purchases reinsurance from one reinsurer.

2.1 Strategies

We assume that the insurer receives income at a constant rate and is exposed to aggregate risks that follow a standard diffusion model (see, e.g., Schmidli, (2001)). To be precise, the dynamics of the risk exposure is governed by

in which are the drift and volatility parameters of the insurer’s risk process, respectively, and is a one-dimensional Brownian motion defined on a filtered, complete probability space . Here, is the augmentation of the natural filtration generated by and satisfies the usual conditions. Hereafter and denote the expectation and variance operators under , respectively. To mitigate the risk exposure, the insurer purchases proportional reinsurance from Reinsurers 1 and 2, with ceded proportions and , respectively. That is, at each time , is ceded to Reinsurer 1, is ceded to Reinsurer 2, while is retained by the insurer. To receive the reinsurance coverage, the insurer pays premiums that are computed by the variance premium principle (see, e.g., Chi, (2012) and Liang and Yuen, (2016)). Denoting the loading factor of Reinsurer , the premium for a reinsurance contract with ceded proportion satisfies

implying that

| (2.1) |

Let denote the insurer’s proportional reinsurance strategy and the pair of premium loadings, in which is Reinsurer ’s premium strategy, . Throughout the paper, we suppress the dependence of processes (e.g., and ) on strategy and/or . Given and , the insurer’s surplus process follows the dynamics

| (2.2) | ||||

| (2.3) |

with . Similarly, we obtain the dynamics of Reinsurer ’s surplus process by

| (2.4) |

with , for .

We proceed to define the insurer’s and reinsurers’ admissible strategies below.

Definition 2.1.

We call an admissible (reinsurance) strategy for the insurer if it satisfies the following conditions:

-

(i)

and are progressively measurable with respect to ;

-

(ii)

, , and almost surely (a.s.), for all .

We call an admissible (premium) strategy for Reinsurer , , if it satisfies the following conditions:

-

(i)

is progressively measurable with respect to ;

-

(ii)

is uniformly bounded and positive.

Let , , and denote the set of all admissible strategies for the insurer (Insurer ), Reinsurer , and Reinsurer , respectively,333With slight abuse of notation, we also use , , to denote the admissible set at each time . and denote the joint admissible set of all three players.

As stated in Section 1 (and will be described in detail shortly), we consider a game model with three players; as such, the surplus process of one player not only depends on its own strategy but also on the other two players’. For this reason, we will only consider strategies that are jointly admissible to all players, , in the subsequent analysis. Note that given a triplet , the insurer’s surplus equation (2.3) admits a unique solution for each , and the same is true for Reinsurer ’s surplus equation (2.4) under , . In Definition 2.1, both the proportional reinsurance strategy of the insurer and the premium strategies of the reinsurers are allowed to be rather general stochastic processes. But in practice, reinsurance contracts are signed and fixed over the life of specified periods, implying that both and are not random but constants. As such, it seems that we should impose such constraints upfront in defining admissible strategies. However, as shown in Theorem 3.3, all strategies under equilibrium are constants even when we consider random strategies as in Definition 2.1. Therefore, we decide not to impose the assumption of constant strategies in Definition 2.1 for the benefit of mathematical generality.

2.2 Games

To start, we assume that all three players, one insurer and two reinsurers, in the market are utility maximizers and further that the preferences of (Re)Insurer are characterized by an exponential function

| (2.5) |

in which is the (constant) absolute risk aversion parameter. Following Cao et al., 2023b ; Cao et al., 2023a , we model the reinsurance contracting between the insurer and each of the two reinsurers as a Stackelberg game and the competition between two reinsurers as a non-cooperative Nash game. In all games, the information is perfect and symmetric to both parties. In each Stackelberg game, the reinsurer is the leader and chooses its premium strategy , and the insurer is the follower and chooses its reinsurance strategy . However, different from these two papers, the competition here is modeled via the so-called relative performance; to be precise, Reinsurer in Cao et al., 2023b optimizes its own surplus (performance) , , but here it optimizes the relative performance , with , in which measures the competition degree of Reinsurer relative to its competitor Reinsurer . The limit case of reduces to the scenario investigated in Cao et al., 2023b ; Cao et al., 2023a and is considered in Section 3.4. As stated above, the insurer, as the follower in each Stackelberg contracting game, seeks an optimal reinsurance strategy in response to the reinsurers’ chosen premiums. This is formally defined below.

Definition 2.2 (Insurer’s Problem).

Let the reinsurers’ premium strategies be arbitrary but fixed, and . The insurer seeks an optimal reinsurance strategy that maximizes its dynamic objective defined by

| (2.6) |

in which may depend on the reinsurers’ strategies pair , and is given by (2.5) with . Denote the insurer’s value function by

| (2.7) |

In the Stackelberg contracting game between Reinsurer and the insurer, Reinsurer is the game leader and chooses its premium loading , . Given the hierarchical structure of Stackelberg game, the surplus dynamics of Reinsurer in (2.4) holds under the insurer’s optimal reinsurance strategy defined in (2.7); to account for such a fact, we introduce a more precise notation for Reinsurer ’s surplus process given . As each reinsurer compares its own surplus with the competitor’s, we define the relative performance of Reinsurer by

| (2.8) |

for and , in which measures the competition degree of Reinsurer to its competitor Reinsurer . Note that Reinsurer ’s relative performance, in (2.8), depends on not only its own premium strategy but also its competitor’s .

Definition 2.3 (Reinsurers’ Problem).

As is clear from Definition 2.3, Reinsurer ’s optimal strategy depends on its competitor’s strategy . The competition between them is settled by a non-cooperative Nash game, which leads to the following definition of the two-layer game equilibrium.

Definition 2.4 (Equilibrium).

Assume that there exists a fixed point, denoted by , to the mapping , and it is admissible (i.e., ). The equilibrium of the two-layer reinsurance contracting and competition game plotted in Figure 1 consists of the following controls:

-

•

and are the equilibrium premium strategies of Reinsurer 1 and Reinsurer 2, respectively, and forms the Nash equilibrium of the competition game between the two reinsurers;

-

•

is the insurer’s equilibrium reinsurance strategy in the Stackelberg games with Reinsurers 1 and 2.

3 Equilibrium

In this section, we first solve the insurer’s problem, for a given pair of admissible premiums , to obtain its optimal strategy in Section 3.1; next, assuming that the insurer follows , we solve each reinsurer’s problem in Section 3.2; finally, we combine the above results to obtain the equilibrium of the two-layer game model in Section 3.3.

3.1 Insurer’s Problem

Recall that the insurer’s problem is formally defined in Definition 2.2. To solve the insurer’s problem in (2.7), we apply the dynamic programming method (see Fleming and Soner, (2006) and Yong and Zhou, (2012)) and present the solution in the theorem below.

Theorem 3.1.

For every , the insurer’s optimal reinsurance strategy is given by

| (3.1) | ||||

| (3.2) |

and its value function , defined in (2.7), is given by

| (3.3) |

for every , in which is the insurer’s absolute risk aversion, and is

| (3.4) |

Proof.

From the dynamics equation of in (2.3), we define the infinitesimal generator , for every and every , by

| (3.5) | ||||

| (3.6) |

in which denotes the corresponding partial derivative of with respect to the subscript argument. Then, applying the dynamic programming principle, we obtain that the insurer’s value function , if , is a classical solution to the following Hamilton-Jacobi-Bellman (HJB) equation

| (3.7) |

To solve (3.7), we consider an ansatz in the form of (3.3), in which is yet to be determined. With the help of this particular ansatz, we reduce (3.7) into

| (3.8) |

A straightforward calculus shows that the minimization problem in (3.8) admits a unique minimizer given by

| (3.9) |

Solving the above system of equations immediately leads to the solutions in (3.1)-(3.2). Note that for in (3.1) and in (3.2), Condition in the definition of admissible reinsurance strategies is satisfied; as a result, given , we have .

3.2 Reinsurers’ Problem

This subsection aims to solve each reinsurer’s problem in the Stackelberg game, assuming that the premium strategy from the other reinsurer is fixed (see Definition 2.3). Recall that in each of the two Stackelberg contracting games, the insurer is the follower, and the reinsurer is the leader. As such, the definition of Reinsurer ’s relative performance (surplus) in (2.8) indicates that the insurer follows its optimal strategy obtained in Theorem 3.1; given , the dynamics of is governed by

| (3.10) |

for with . We present the key results below.

Theorem 3.2.

Proof.

This proof largely follows from that of Theorem 3.1, and for that reason, we only provide a sketch below to save space. To start, based on (3.10), we define an operator , for every and every , by

| (3.15) | ||||

| (3.16) |

for . It can be shown that the value function , assuming , satisfies the following HJB equation

| (3.17) |

By a length calculus (results are available upon request), we prove that the optimization problem in (3.17) admits a unique maximizer , and it is given by (3.11), which is positive and bounded for every . We then use in (3.11) to reduce (3.17) into an ODE of , to which there exists a unique solution given by (3.14). Finally, by a standard verification argument (see Theorem A.1 for a similar result), we confirm that in (3.11) is the optimal premium strategy for Reinsurer , and in (3.13) is the value function to Reinsurer ’s problem formulated in Definition 2.3. ∎

3.3 Equilibrium

In the last step, we combine the results from Theorems 3.1 and 3.2 to obtain the equilibrium of the two-layer game model plotted in Figure 1. Our findings are summarized in the next theorem.

Theorem 3.3.

If , the bivariate mapping , with and defined in (3.12), admits a unique constant fixed point in , denoted by , and the unique equilibrium consists of the following controls:

-

•

Reinsurer ’s equilibrium premium strategy is constant and equals (i.e., for all ), for .

- •

If , there does not exist an equilibrium.

Proof.

Based on the equilibrium definition (see Definition 2.4) and Reinsurer ’s optimal strategy in (3.11), the key is to find a fixed point for the bivariate mapping , which, if exists, forms the pair of equilibrium premium strategies for the two reinsurers.

We start with analyzing the individual functions and defined by (3.12). We compute their derivatives as follows:

| (3.18) | ||||

| (3.19) | ||||

| (3.20) | ||||

| (3.21) |

for with . We also have

| (3.22) |

Therefore, the inverse function of exists over ; let us denote it by hereafter. It is easy to see that, for ,

| (3.23) |

Using the above derivative results on and (3.12), we have the following limit results:

| (3.24) | ||||||

| (3.25) | ||||||

Assume for now that has a fixed point, and we denote it by . Then, by definition, is a solution to the following system of equations:

| (3.26) |

Given the properties of and , the system (3.26) either has no solution or admits a unique, positive solution. Furthermore, the sufficient and necessary condition for the existence of a unique solution is

| (3.27) |

which is equivalent to by recalling (3.24).

Recall that the quantity Reinsurer optimizes is not its own terminal performance (surplus) but rather the relative performance defined in (2.8). Although is allowed mathematically in the analysis, the term “relative” suggests that a more reasonable condition is that , under which a unique equilibrium exists and is characterized as in Theorem 3.3. As such, we assume holds onwards in the rest of the paper. Given such an assumption, Theorem 3.3 provides a complete characterization of the equilibrium in semi-closed form, subject to solving a nonlinear system (3.26) to obtain . As there does not exist a closed-form solution for , we focus on the sensitivity analysis of the equilibrium controls in the rest of this section.

Recall from the definition of in (3.12) that both and , and thus the equilibrium premium strategy , depend on two sets of model parameters: (1) risk aversions () and (2) competition degrees ( and ). We present an analytical result regarding the impact of all these parameters on the equilibrium premium strategy .

Proposition 3.4.

Let be the equilibrium premium strategy of Reinsurer , , as obtained in Theorem 3.3. We have the following sensitivity results for the equilibrium premium strategy:

| (3.28) |

for with . However, there does not exist any monotonicity result on the insurer’s equilibrium reinsurance strategy .

Proof.

See Appendix A for proof. ∎

The sensitivity results of in (3.28) are consistent with our intuition and will be explained in detail in the next section, in which we also study how these model parameters affect the insurer’s equilibrium reinsurance strategy , for which an analytical result is not available.

3.4 The Special Case of

The previous analysis assumes that for and shows that the game equilibrium exists if . In this subsection, we consider the special case of ; recall that the objective of the reinsurers in Cao et al., 2023b corresponds to the case of .

First, we consider the case with but , in which and . In this case, the function , originally defined in (3.12) for , changes to

| (3.29) |

We easily obtain the following limit results of :

and derive the first- and second-order derivatives of by

As such, has an inverse in the interval , which we denote by . Regarding this inverse, we have, for ,

| (3.30) |

and

| (3.31) |

Given the properties of and , the system (3.26) admits a unique, positive solution , in which .

Second, we consider the case with . In this case, we obtain

| (3.32) |

With the above and , we can solve the system (3.26) analytically and obtain the unique solution in closed form by

| (3.33) |

Therefore, the main result in Theorem 3.3 obtained for readily extends to the case when , as summarized below.

Theorem 3.5.

If , there exists a unique Nash equilibrium of premium strategies, , for the two competing reinsurers, and the insurer’s equilibrium reinsurance strategy is given by . In addition, the equilibrium premium pair is characterized by one of the following two cases:

- 1.

-

2.

If , then is given by (3.33).

4 Economic Study

We have solved the two-layer reinsurance contracting and competition game and obtained its equilibrium in Theorem 3.3. The characterization of all equilibrium controls is complete, subject to finding the fixed point, , of the mapping . However, finding such a can only be done by numerical methods in general. In this section, we conduct a thorough economic study focusing on the sensitivity analysis of the equilibrium controls, in particular, the insurer’s equilibrium reinsurance strategy .

In the subsequent analysis, the default model parameters are set as follows:

| 5 | 4 | 6 | 0.3 | 0.7 |

Note from Table 1 that Reinsurer exhibits higher risk aversion and stronger competition degree than Reinsurer does. Also, is satisfied, implying that there exists a unique equilibrium by Theorem 3.3. When we investigate the impact of one particular parameter, say , we will allow it to vary over a reasonable range but keep the rest parameters fixed as in Table 1.

4.1 Sensitivity Analysis for the Insurer

We first conduct a numerical study to investigate how model parameters affect the insurer’s equilibrium strategy , in which is the proportion ceded to Reinsurer , . Note that we were unable to derive any monotonicity results of in Proposition 3.4.

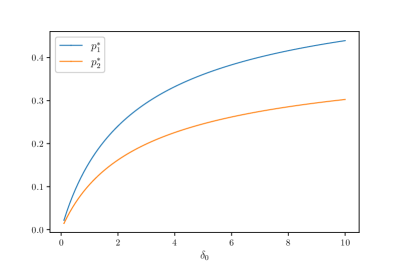

In Figure 2, we plot how the insurer’s equilibrium strategy changes with respect to its own risk aversion parameter . It is pleasing to see that a more risk averse insurer cedes a larger proportion of its risk to reinsurers under equilibrium because doing so reduces the uncertainty of its terminal wealth and yields a larger expected utility.444Such a result holds true under different Stackelberg game frameworks. For instance, when there is only one reinsurer, both Chen and Shen, (2018) and Chen and Shen, (2019) arrive at a similar result; that is, the increase of the insurer’s risk version leads to an increase of ceded risk to the reinsurer. Note that the reinsurer is a utility maximizer in Chen and Shen, (2018) but a mean-variance agent in Chen and Shen, (2019). This result can be further extended from risk aversion to ambiguity aversion, as shown in Cao et al., (2022). We observe from Figure 2 that ; recall from Table 1 that . This is because the reinsurance policy offered by a more risk averse reinsurer is more expensive than the one offered by a less risk averse reinsurer, and the insurer prefers a cheaper contract.

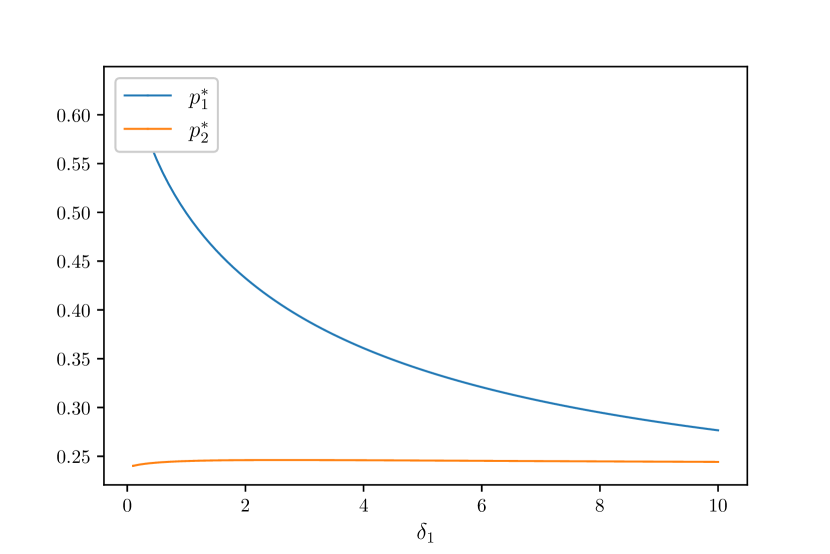

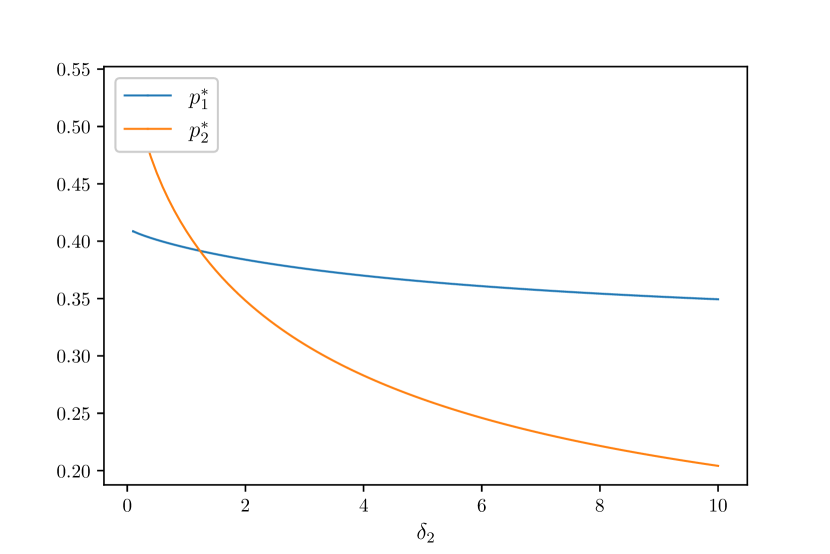

We next study how the risk aversion of the two reinsurers, and , affect the insurer’s decision and plot as a function of these parameters in Figures 4 and 4, respectively. We observe that, when the risk aversion coefficient of one reinsurer increases, the proportion of reinsurance ceded to this reinsurer will decrease significantly (see the blue curve in Figure 4 and the orange curve in Figure 4); however, the proportion of reinsurance ceded to the other reinsurer may stay almost unchanged (Figure 4) or decrease slightly (Figure 4). The first result can be easily understood as follows. When increases, the contract offered by Reinsurer becomes more expensive, and the insurer reacts by ceding less risk to Reinsurer , leading to a decrease of . However, the impact of on , , is more subtle because although Reinsurer will raise its premium , the increase may be at a much slower pace than Reinsurer .

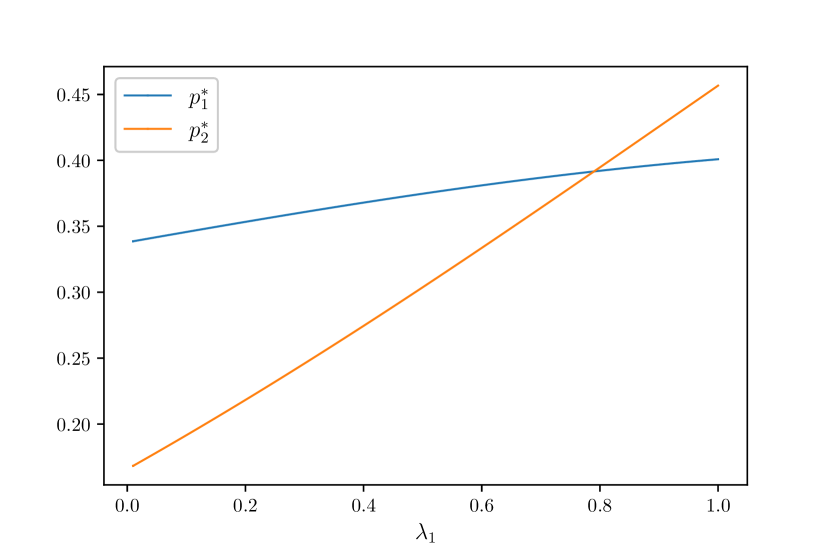

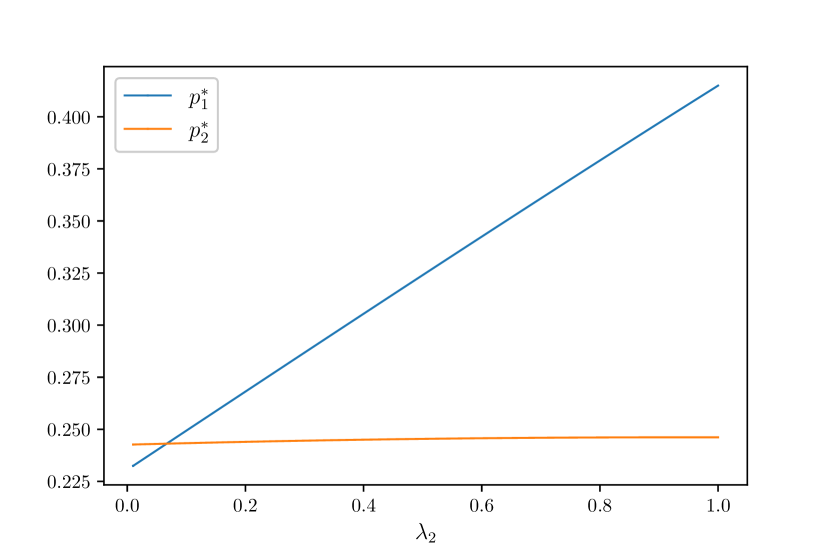

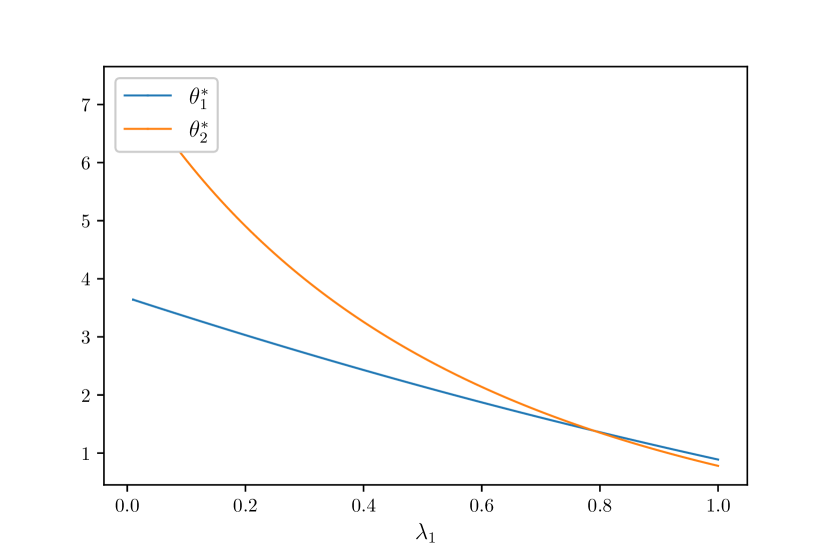

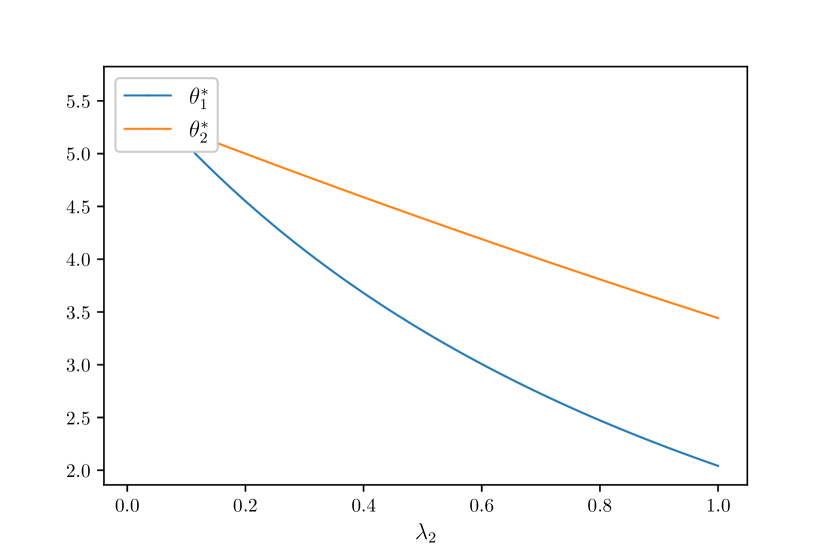

In the last step, we shift our attention to the impact of and on the insurer’s equilibrium strategies and . Recall that measures the competition degree of Reinsurer to its competitor Reinsurer in the relative performance (see (2.8)). Both Figures 6 and 6 show that an increase in the competition degree of one reinsurer pushes the insurer to purchase more coverage from both reinsurers, albeit at very different scales. This is because when increases, a more fierce competition drives both reinsurers to lower their premiums, which in turn incentives the insurer to cede more of its risk away to the reinsurers.

4.2 Sensitivity Analysis for the Reinsurers

We next turn our attention to the two reinsurers and investigate how model parameters affect their equilibrium strategies and . Keep in mind that we have already obtained analytical results on the sensitivity of and in Proposition 3.4.

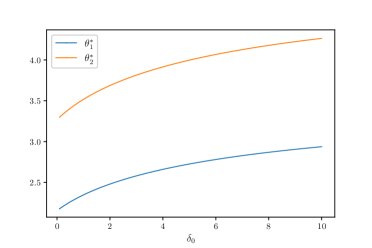

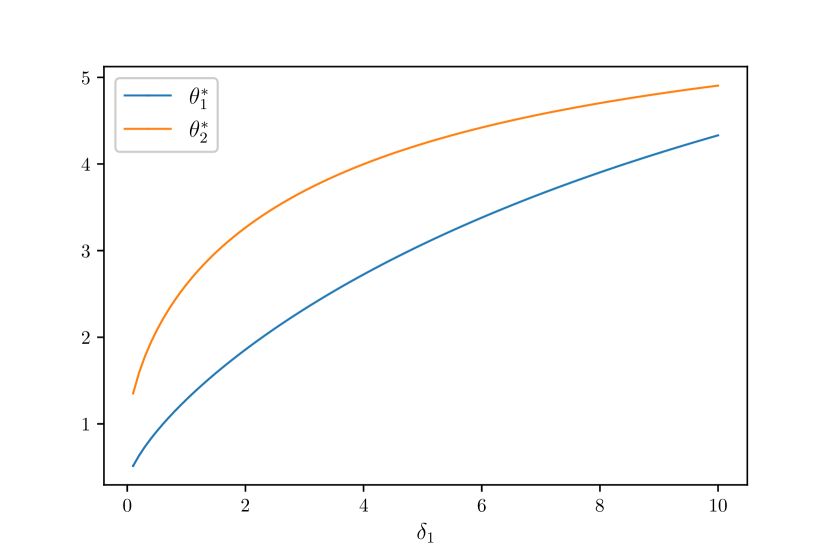

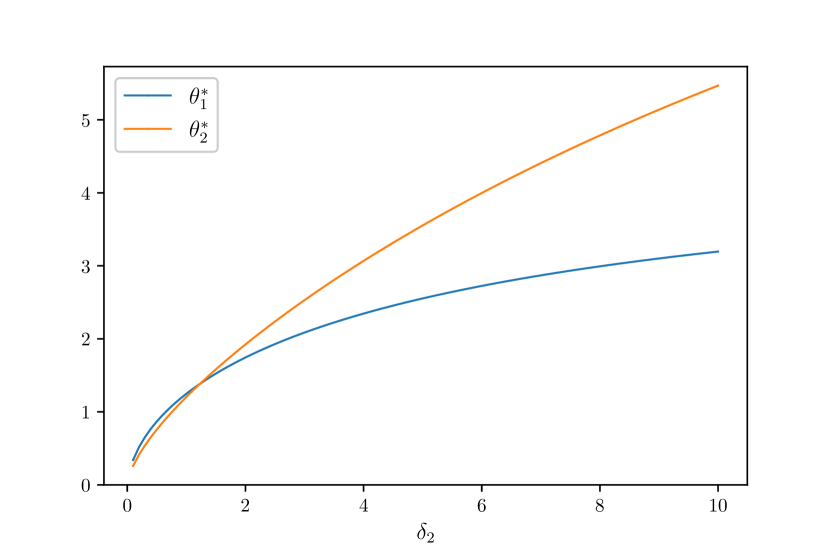

In Figures 7-9, we plot how each reinsurer’s equilibrium premium strategy , , reacts to the change of one player’s risk aversion (, , or ). The plots in all figures confirm the positive relation between and established in (3.28). A larger implies a higher demand from the insurer for reinsurance coverage; upon recognizing this, both reinsurers explore such an opportunity by increasing premiums to achieve a higher expected utility. When the risk aversion of Reinsurer increases, one naturally anticipates an increase in its own premium because this helps reduce the risk taking by Reinsurer from the insurer. Interestingly, we observe that the increase of pushes , the competitor’s equilibrium premium, up; such a result is likely due to the direct competition implied by the relative performance used in optimization. Last, we observe in most scenarios, except for very small in Figure 9. This observation can be explained by the fact that Reinsurer 2 exhibits a higher degree of risk aversion and places a greater emphasis on competition by choosing a larger .

Last, we study the competition degree on the reinsurers’ premium decision. Both Figures 11 and 11 show that when one reinsurer’s competition degree increases, both reinsurers lower their premium loadings. This is due to the “chain effect” of the competition game explained as follows. A larger means that Reinsurer has a stronger incentive to compete with Reinsurer , and to outperform its competitor Reinsurer , Reinsurer ’s natural move is to lower its price by choosing a smaller ; as Reinsurer also takes into account Reinsurer ’s performance in evaluating its utility, it will reduce its loading in order to stay competitive to Reinsurer .

5 Conclusion

In this paper, we introduce a two-layer stochastic game model to study reinsurance contracting and competition in a market with one insurer and two competing reinsurers. The reinsurance contracting problem between the insurer and each of the two reinsurers is captured by a Stackelberg game, in which the reinsurer is the leader and chooses the loading in its variance premium rule, and the insurer is the follower and chooses its proportional reinsurance strategy. Meanwhile, the competition between the two reinsurers is captured by the fact that each maximizes its expected utility of the relative performance at the terminal time. We solve such a complex game rigorously and completely; we show that a unique equilibrium exists and is fully characterized if , and no equilibrium exists if , in which is the competition degree of Reinsurer , . We also obtain several interesting qualitative results of the equilibrium strategies and conduct a numerical study to further study how insurer’s and reinsurers’ risk aversion coefficients, as well as competition parameters, influence the equilibrium strategies.

Acknowledgement. Zongxia Liang acknowledges the financial support from the National Natural Science Foundation of China (Nos.12271290, 12371477, 11871036). The authors also thank the members of the group of Actuarial Sciences and Mathematical Finance at the Department of Mathematical Sciences, Tsinghua University for their feedback.

Appendix A Technical Results

We first provide a formal verification for the solution to the insurer’s problem obtained in Theorem 3.1. For a similar result, please refer to Fleming and Soner, (2006)[Theorem III.8.1, p.135].

Theorem A.1 (Verification theorem for the insurer’s problem).

Proof.

(a) Let be a classical solution to the HJB equation (3.7). For every , applying Itô’s formula to , we get

Introduce short-handed notations and . Recall from Definition 2.1 that both and are uniformly bounded; as such, in (3.4), , and are also uniformly bounded. That is, there exists a positive constant, denoted by , such that

| (A.2) |

Then, by a standard localization technique and using (3.7), we obtain

| (A.3) |

and, by the terminal condition in (3.7) and the definition of in (2.6),

in which . Combining the above two results proves Assertion .

Assertion is self-evident because the inequality in (A.3) becomes equality when . ∎

Verification for Theorem 3.1.

Consider a function given by

in which is defined in (3.4). The proof of Theorem 3.1 shows that is a classical solution in the space of to the HJB equation (3.7), then Assertion in Theorem A.1 holds. In fact, for such a , the localization technique is not needed because we can directly show that the corresponding Itô process is a martingale. To see that, using (A.2) and setting , we obtain

which in turn implies that

Proof of Proposition 3.4.

By recalling in (3.12), also depends on the parameters . Although previously we have treated as a univariate function of in Section 3, we will treat as a multivariate function of these parameters in the subsequent sensitivity analysis. As such, is Section 3 translates to here.

First, we compute the partial derivatives of with respect to each parameter by

| (A.4) | ||||

| (A.5) | ||||

| (A.6) | ||||

| (A.7) | ||||

| (A.8) |

Because , we have

| (A.9) |

Solving the above equations, we get

| (A.10) |

in which we have used (3.23), (3.26) and (3.27) to derive the inequality

| (A.11) |

By following a similar argument, we show the sensitivity results of in (3.28) hold.

Next, we aim to analyze the sensitivity of with respect to those model parameters. To that end, recall that , in which and are given by (3.1) and (3.2), respectively. Similar to the above, we now treat each as a function of , , and model parameters, and compute the following derivatives:

| (A.12) | ||||

| (A.13) | ||||

| (A.14) |

Let us study the impact of on first and note

| (A.15) |

in which the first and third terms are positive, but the second term is negative. As such, a definite monotonicity result of with respect to is not available in general. By following the same argument, one can see that such a negative result applies to all partial derivatives of . ∎

References

- Albrecher et al., (2017) Albrecher, H., Beirlant, J., and Teugels, J. L. (2017). Reinsurance: Actuarial and Statistical Aspects. John Wiley & Sons.

- Asmussen et al., (2000) Asmussen, S., Højgaard, B., and Taksar, M. (2000). Optimal risk control and dividend distribution policies. Example of excess-of loss reinsurance for an insurance corporation. Finance and Stochastics, 4(3):299–324.

- Bensoussan et al., (2014) Bensoussan, A., Siu, C. C., Yam, S. C. P., and Yang, H. (2014). A class of non-zero-sum stochastic differential investment and reinsurance games. Automatica, 50(8):2025–2037.

- Bo et al., (2024) Bo, L., Wang, S., and Zhou, C. (2024). A mean field game approach to optimal investment and risk control for competitive insurers. Insurance: Mathematics and Economics, 116:202–217.

- Boonen et al., (2021) Boonen, T. J., Tan, K. S., and Zhuang, S. C. (2021). Optimal reinsurance with multiple reinsurers: Competitive pricing and coalition stability. Insurance: Mathematics and Economics, 101(B):302–319.

- Cai and Chi, (2020) Cai, J. and Chi, Y. (2020). Optimal reinsurance designs based on risk measures: A review. Statistical Theory and Related Fields, 4(1):1–13.

- Cao et al., (2022) Cao, J., Li, D., Young, V. R., and Zou, B. (2022). Stackelberg differential game for insurance under model ambiguity. Insurance: Mathematics and Economics, 106:128–145.

- (8) Cao, J., Li, D., Young, V. R., and Zou, B. (2023a). Reinsurance games with n variance-premium reinsurers: From tree to chain. ASTIN Bulletin, 53(3):706–728.

- (9) Cao, J., Li, D., Young, V. R., and Zou, B. (2023b). Reinsurance games with two reinsurers: Tree versus chain. European Journal of Operational Research, 310(2):928–941.

- Chen et al., (2016) Chen, L., Qian, L., Shen, Y., and Wang, W. (2016). Constrained investment–reinsurance optimization with regime switching under variance premium principle. Insurance: Mathematics and Economics, 71:253–267.

- Chen and Shen, (2018) Chen, L. and Shen, Y. (2018). On a new paradigm of optimal reinsurance: A stochastic stackelberg differential game between an insurer and a reinsurer. ASTIN Bulletin, 48(2):905–960.

- Chen and Shen, (2019) Chen, L. and Shen, Y. (2019). Stochastic Stackelberg differential reinsurance games under time-inconsistent mean–variance framework. Insurance: Mathematics and Economics, 88:120–137.

- Chi, (2012) Chi, Y. (2012). Optimal reinsurance under variance related premium principles. Insurance: Mathematics and Economics, 51(2):310–321.

- Fleming and Soner, (2006) Fleming, W. H. and Soner, H. M. (2006). Controlled Markov Processes and Viscosity Solutions. Springer Science & Business Media.

- Gu et al., (2018) Gu, A., Viens, F. G., and Yao, H. (2018). Optimal robust reinsurance-investment strategies for insurers with mean reversion and mispricing. Insurance: Mathematics and Economics, 80:93–109.

- Jiang et al., (2019) Jiang, W., Ren, J., Yang, C., and Hong, H. (2019). On optimal reinsurance treaties in cooperative game under heterogeneous beliefs. Insurance: Mathematics and Economics, 85:173–184.

- Jin et al., (2024) Jin, Z., Xu, Z. Q., and Zou, B. (2024). Optimal moral-hazard-free reinsurance under extended distortion premium principles. SIAM Journal on Control and Optimization, forthcoming.

- Kroell et al., (2023) Kroell, E., Jaimungal, S., and Pesenti, S. M. (2023). Optimal robust reinsurance with multiple insurers. arXiv preprint arXiv:2308.11828.

- Li et al., (2015) Li, D., Rong, X., and Zhao, H. (2015). Time-consistent reinsurance–investment strategy for a mean–variance insurer under stochastic interest rate model and inflation risk. Insurance: Mathematics and Economics, 64:28–44.

- Li and Young, (2022) Li, D. and Young, V. R. (2022). Stackelberg differential game for reinsurance: Mean-variance framework and random horizon. Insurance: Mathematics and Economics, 102:42–45.

- Liang and Yuen, (2016) Liang, Z. and Yuen, K. C. (2016). Optimal dynamic reinsurance with dependent risks: Variance premium principle. Scandinavian Actuarial Journal, 2016(1):18–36.

- Lu et al., (2016) Lu, Z., Meng, L., Wang, Y., and Shen, Q. (2016). Optimal reinsurance under VaR and TVaR risk measures in the presence of reinsurer’s risk limit. Insurance: Mathematics and Economics, 68:92–100.

- Peng et al., (2021) Peng, X., Chen, F., and Wang, W. (2021). Robust optimal investment and reinsurance for an insurer with inside information. Insurance: Mathematics and Economics, 96:15–30.

- Schmidli, (2001) Schmidli, H. (2001). Optimal proportional reinsurance policies in a dynamic setting. Scandinavian Actuarial Journal, 2001(1):55–68.

- Schmidli, (2002) Schmidli, H. (2002). On minimizing the ruin probability by investment and reinsurance. Annals of Applied Probability, 12(3):890–907.

- Tan et al., (2020) Tan, K. S., Wei, P., Wei, W., and Zhuang, S. C. (2020). Optimal dynamic reinsurance policies under a generalized Denneberg’s absolute deviation principle. European Journal of Operational Research, 282(1):345–362.

- Tan et al., (2009) Tan, K. S., Weng, C., and Zhang, Y. (2009). VaR and CTE criteria for optimal quota-share and stop-loss reinsurance. North American Actuarial Journal, 13(4):459–482.

- Wang et al., (2020) Wang, G., Wang, Y., and Zhang, S. (2020). An asymmetric information mean-field type linear-quadratic stochastic stackelberg differential game with one leader and two followers. Optimal Control Applications and Methods, 41(4):1001–1370.

- Yong and Zhou, (2012) Yong, J. and Zhou, X. Y. (2012). Stochastic Controls: Hamiltonian Systems and HJB Equations. Springer Science & Business Media.

- Zhang and Li, (2021) Zhang, L. and Li, B. (2021). Optimal reinsurance under the -maxmin mean-variance criterion. Insurance: Mathematics and Economics, 101:225–239.

- Zhou and Yuen, (2012) Zhou, M. and Yuen, K. C. (2012). Optimal reinsurance and dividend for a diffusion model with capital injection: Variance premium principle. Economic Modelling, 29(2):198–207.

- Zhu et al., (2023) Zhu, M. B., Ghossoub, M., and Boonen, T. J. (2023). Equilibria and efficiency in a reinsurance market. Insurance: Mathematics and Economics, 113:24–49.