Learned harmonic mean estimation of the Bayesian evidence

with normalizing flows

Abstract

We present the learned harmonic mean estimator with normalizing flows – a robust, scalable and flexible estimator of the Bayesian evidence for model comparison. Since the estimator is agnostic to sampling strategy and simply requires posterior samples, it can be applied to compute the evidence using any Markov chain Monte Carlo (MCMC) sampling technique, including saved down MCMC chains, or any variational inference approach. The learned harmonic mean estimator was recently introduced, where machine learning techniques were developed to learn a suitable internal importance sampling target distribution to solve the issue of exploding variance of the original harmonic mean estimator. In this article we present the use of normalizing flows as the internal machine learning technique within the learned harmonic mean estimator. Normalizing flows can be elegantly coupled with the learned harmonic mean to provide an approach that is more robust, flexible and scalable than the machine learning models considered previously. We perform a series of numerical experiments, applying our method to benchmark problems and to a cosmological example in up to dimensions. We find the learned harmonic mean estimator is in agreement with ground truth values and nested sampling estimates. The open-source harmonic Python package implementing the learned harmonic mean, now with normalizing flows included, is publicly available. \faGithub

1 Introduction

Model selection plays a crucial role in understanding the complexities of the Universe. It involves the task of identifying the underlying model that best describes observations, for instance of astrophysical phenomena. The field of Bayesian statistics provides a framework for statistical inference and decision-making that incorporates prior knowledge to update probabilities based on observed data. This approach is well-suited for cosmology, for example, as experiments in the field tend to consist of single observations of events, as opposed to repeatable experiments which are at the core of the frequentist framework. As a consequence, Bayesian inference and model comparison are widespread in the field (Trotta, 2008). In the Bayesian formalism, an essential tool in this process is the estimation of the Bayesian evidence, also called the marginal likelihood, which quantifies the probability of observed data given a model. The Bayesian evidence allows us to evaluate the relative plausibility of models and assess which hypotheses are best supported by the available data, which is of course not only useful in cosmology but in many other fields.

As a topical illustration of the importance of model selection in cosmology, recent baryon acoustic oscillations measurements from the Dark Energy Spectroscopic Instrument (DESI Collaboration et al., 2016), combined with observations of the cosmic microwave background (Aghanim et al., 2020; Carron et al., 2022; Madhavacheril et al., 2024) and with supernovae Ia measurements from PantheonPlus (Brout et al., 2022), Union3 (Rubin et al., 2023) or DESY5 (DES Collaboration et al., 2024), provide a tantalizing suggestion of the existence of a time-varying dark energy equation-of-state. Whether dark energy can be described by Einstein’s cosmological constant or whether an equation-of-state with is required is a fundamental question of modern cosmology that we hope to answer definitively in the near future through the application of Bayesian model selection techniques to upcoming observational data. We showcase the application of the methodology presented in this article to precisely this question through a simulated Dark Energy Survey (DES) galaxy clustering and weak lensing analysis (cf. Abbott et al., 2018b).

In practice, the computation of Bayesian evidence is very challenging as it involves evaluating a multi-dimensional integral over a potentially highly varied function. The most widespread method for estimating the Bayesian evidence, particularly in astrophysics, is nested sampling (Skilling, 2006; Ashton et al., 2022; Buchner, 2021). While nested sampling has been highly successful and many effective nested sampling algorithms and codes have been developed (Feroz & Hobson, 2008; Feroz et al., 2009a, b; Brewer et al., 2011; Handley et al., 2015a, b; Feroz et al., 2019; Speagle, 2020; Buchner, 2021; Williams et al., 2021; Cai et al., 2022), it imposes constraints on the method used to sample. By sampling in a nested manner it is possible to reparameterize the likelihood in terms of the enclosed prior volume such that the evidence can be computed by a one-dimensional integral. The computational challenge then shifts to how to effectively sample in a nested manner, i.e. how to sample from the prior subject to likelihood level-sets or isocontours. The need to sample in this nested manner severely reduces flexibility (hence the need to design custom nested sampling algorithms), typically restricting application to relatively low dimensional settings.111A notable exception that is applicable to high-dimensional settings is proximal nested sampling (Cai et al., 2022), although it is only applicable for log-convex likelihoods.

The harmonic mean estimator of the Bayesian evidence, introduced by Newton & Raftery (1994), provides much greater flexibility since it only requires samples from the posterior, available from any Markov chain Monte Carlo (MCMC) method, for example. However, it was immediately realized by Neal (1994) that the method can easily fail catastrophically due to the estimator’s variance becoming very large. To solve this issue the learned harmonic mean estimator was recently proposed by McEwen et al. (2021), where machine learning techniques were developed to learn a suitable internal importance sampling target distribution. Since the estimator requires only samples from the posterior and so is agnostic to the method used to generate samples, in contrast to nested sampling, it can be easily applied with any MCMC sampling technique, including saved down MCMC chains, or any variational inference approach. This property also allows the estimator to be adapted to address Bayesian model selection for simulation-based inference (SBI) (Spurio Mancini et al., 2023), where an explicit likelihood is unavailable or infeasible.

In this article we present the use of normalizing flows as the internal machine learning technique within the learned harmonic mean estimator. Normalizing flows can be elegantly coupled with the learned harmonic mean to provide an approach that is more robust, flexible and scalable than the machine learning models considered previously. In Polanska et al. (2023) we presented preliminary work introducing normalizing flow as the machine learning technique within the learned harmonic mean. We fully develop the methodology in the current article, introduce the use of additional, more expressive flows, and perform more extensive numerical experiments validating and showcasing the method. The harmonic222https://github.com/astro-informatics/harmonic Python package implementing the learned harmonic mean estimator, including with normalizing flows, is publicly available.

While normalizing flows can learn a normalized posterior density by definition, the normalization constant itself, i.e. the Bayesian evidence, is not directly accessible. Nevertheless, the Bayesian evidence can be computed by backing out the normalization constant, as discussed in Spurio Mancini et al. (2023), by taking the ratio of the unnormalized posterior (given by the product of the likelihood and prior) with the normalizing flow representing a surrogate for the posterior. This approach, which we call the naïve normalizing flow estimator in Spurio Mancini et al. (2023), is highly dependent on the accuracy of the approximating normalizing flow and suffers a large variance, as discussed in Spurio Mancini et al. (2023). For comparison, we compute this naïve estimator in the current article and demonstrate its large variance. Very recently, Srinivasan et al. (2024) adopt this naïve estimator and attempt to reduce its variance by introducing an additional term in the loss that penalizes variability when training the flow. While this reduces the variability of the estimator, the estimator nevertheless remains highly dependent on the accuracy of the approximating flow and there is no guarantee that resulting evidence estimates are unbiased. Training flows using the forward Kullback-Leibler (KL) divergence when given samples from the target distribution is known to suffer from mode seeking behaviour, where the learned flow has narrower tails than the target (e.g. Murphy, 2022). While the approach presented in Srinivasan et al. (2024) suffers from this problem as it directly impacts the accuracy of estimated evidence values, our learned harmonic mean estimator does not. Firstly, in the learned harmonic mean approach the internal importance sampling target distribution that is learned should in any case have narrower tails than the posterior. Secondly, the distribution that is learned in our approach is not used as a surrogate for the posterior so it need not be an accurate approximation. For further details see Section 2.3 or McEwen et al., 2021.

The remainder of this article is structured as follows. In Section 2 we briefly review Bayesian model comparison, the original harmonic mean estimator, elucidating its catastrophic failure arising from its large variance, and the learned harmonic mean estimator, which solves this large variance problem. In Section 3 we describe normalizing flows and how they can be integrated elegantly into the learned harmonic mean framework to provide a more robust, flexible and scalable approach than the simple machine learning models considered previously. In Section 4 we present numerical experiments that validate the effectiveness of our method. This includes low-dimensional benchmark examples where the ground truth value is accessible and a higher-dimensional practical cosmological example on DES-like simulations, as discussed above, where we validate against the evidence value computed by nested sampling. Finally, in Section 5 we present concluding remarks.

2 The harmonic mean estimator

In this section we briefly review Bayesian model comparison, the original harmonic mean estimator, and the learned harmonic mean estimator. We discuss the exploding variance problem of the original harmonic mean and describe how the learned harmonic mean solves this problem.

2.1 Bayesian model comparison

Using empirical data to test theoretical models lies at the heart of the scientific method, the foundation of research progress and innovation. Bayesian model comparison is a powerful approach for evaluating the relative plausibility of competing models in the light of data. In the Bayesian framework probability distributions provide a quantification of uncertainty.

Bayes’ theorem is a fundamental principle in Bayesian statistics that allows us to update our beliefs about models in light of observed data. Consider observed data described through a model parametrised by . Bayes’ theorem gives us the posterior , the probability density of a model’s parameter given observed data and model . It is expressed in terms of the prior probability density of the model, the likelihood of the data under that model, and the Bayesian evidence for the data:

| (1) |

The likelihood expresses how probable the observed data is for different values of the parameter . The prior quantifies pre-existing knowledge or assumptions about . The Bayesian evidence, also called the marginal likelihood, is a normalizing factor for the posterior distribution.

The Bayesian evidence is often omitted when estimating parameters, for instance using MCMC methods, as only the relative values of the posterior probability are of interest. However, it is a crucial quantity in Bayesian model comparison. It quantifies the probability of observing the data under a particular model, integrating over the model’s parameter space:

| (2) |

The Bayesian evidence can be used to compute Bayes’ factors to provide a direct measure of the relative support for one model over another. The Bayes’ factor between two models , is defined as

| (3) |

Given prior model probabilities, Bayes’ factors offer a straightforward way to compare models and help make informed decisions about model selection.

In practice, the Bayesian evidence can be very challenging to calculate as is often high-dimensional. As a result, computing involves evaluating a multi-dimensional integral over a potentially highly varied function. In principle, this could be done through a standard MCMC integration of the posterior, but this approach is not accurate in practice, even in relative low dimensions. Many alternative methods have been proposed; for reviews see Friel & Wyse (2012); Clyde et al. (2007). The most popular method for computing the evidence, particularly in the astrophysics community, is nested sampling Skilling (2006). As discussed already, many highly effective nested sampling algorithms have been developed. However, nested sampling imposes strong constraints on the method used to generate samples, significantly reducing its flexibility. Consequently, custom nested sampling algorithms must be designed and are typically restricted to relatively low dimensional settings.

2.2 The original harmonic mean estimator

The original harmonic mean estimator of the Bayesian evidence was introduced by Newton & Raftery (1994), providing an expression for the reciprocal Bayesian evidence given by

| (4) |

This motivates the harmonic mean estimator of the reciprocal Bayesian evidence, which can be written as an expectation of the reciprocal of the likelihood under the posterior,

| (5) |

The Bayesian evidence can then be straightforwardly obtained as the inverse (although a more accurate estimator of the evidence from its reciprocal can also be considered; McEwen et al. 2021). In principle, this estimator provides a simple and flexible method of evaluating the Bayesian evidence.

However, it was quickly realised that the harmonic mean estimator can be highly inaccurate due to its variance growing very large (Neal, 1994; Clyde et al., 2007; Friel & Wyse, 2012). The reason for this can be seen when interpreting the harmonic mean estimator through the lens of importance sampling (e.g. McEwen et al., 2021). Equation (4) can be rewritten as

| (6) |

It is clear that this expectation is equivalent to importance sampling, where the target density is the prior and the sampling density is the posterior . This is in contrast to the typical importance sampling use case, where the posterior is the target distribution. For importance sampling to be effective, the sampling density must have fatter tails than the target in order for the target parameter space to be explored efficiently. If this condition is not fulfilled, the variance of the expectation becomes large. In the case of the harmonic mean estimator, the target density (prior) will normally have fatter tails than the sampling density (posterior). This is because the posterior gets updated with new information about the model encoded in the data, and as a result becomes narrower. Thus, the original harmonic mean estimator suffers from an exploding variance issue and is often inaccurate.

2.3 Learned harmonic mean estimator

One strategy to remedy the exploding variance problem of the harmonic mean estimator was proposed by Gelfand & Dey (1994), where an arbitrary normalized density is introduced to rewrite the expectation in Equation (4) as

| (7) |

which naturally results in the estimator

| (8) |

The density now takes the role of the importance sampling target. This estimator can therefore remedy the exploding variance problem provided that the target density is selected so that it is contained within the posterior. However, this condition is not trivial to enforce, especially in high dimensions since there is a trade-off between accuracy and efficiency. The contribution to the estimator from each posterior sample is weighted by the target density . Low weights reduce the contribution of the posterior sample to the estimator, reducing its effective sample size and thus efficiency. However, the alternative of avoiding low weights can result in a target that is not contained within the posterior, giving rise to the exploding variance problem. In prior work, a multivariate Gaussian has been considered Gelfand & Dey (1994), although this often fails to contain within the posterior (Chib, 1995; Clyde et al., 2007). Indicator functions have also been considered (Robert & Wraith, 2009; van Haasteren, 2014), although typically result in low efficiency. Other solutions to this problem have been proposed but they can be inaccurate, inefficient or limited in their use cases (Chib, 1995; Lenk, 2009; Raftery et al., 2006).

The learned harmonic mean estimator was proposed recently by some of the authors of the current article (McEwen et al., 2021), where machine learning methods are used to solve the exploding variance problem of the original harmonic mean. It was realized by McEwen et al. (2021) that the optimal target density is the normalized posterior, i.e.

| (9) |

By definition of the problem, however, the normalized posterior is not accessible as the normalization factor is the Bayesian evidence itself. However, the target does not need to be a close approximation of the posterior for the estimate to be correct. It is more important for the target’s probability mass to be contained within the posterior to avoid the variance becoming large. McEwen et al. (2021) develop a bespoke optimization approach that learns the posterior density from its samples while ensuring that the resulting model satisfies this condition. They also derive an unbiased estimator of the variance of the estimator and the variance of the variance, which are empirically shown to be accurate. The estimate of the Bayesian evidence computed with the learned harmonic mean thus comes with an error estimate, which can give an indication of how confident one should be in the result, and a number of additional sanity checks (McEwen et al., 2021).

The learned harmonic mean results in an accurate estimator of the Bayesian evidence that is agnostic to the sampling strategy, just like the original harmonic mean. This property ensures flexibility of the method, meaning it can be used in conjunction with efficient MCMC sampling techniques and variational inference approaches. The learned harmonic mean has been shown to be highly accurate on numerous example problems, including several cases where the original harmonic mean had been shown to fail catastrophically (Clyde et al., 2007; Friel & Wyse, 2012). However, the bespoke training approach requires an appropriate model to be chosen carefully and the hyperparameters to be fine-tuned through cross validation. Moreover, the simple machine learning models considered previously do not scale well to high-dimensional settings.

3 Learned harmonic mean estimator with normalizing flows

In this section we describe the learned harmonic mean with normalizing flow for estimation of the Bayesian evidence. Normalizing flows can be elegantly coupled with the learned harmonic mean to provide an approach that is more robust, flexible and scalable than the machine learning models considered previously.

3.1 Normalizing flows

Normalizing flows meet the core requirements of the learned target distribution of the learned harmonic mean estimator: namely, they provide a normalized probability distribution for which one can evaluate probability densities. Flows are a class of machine learning model, where an underlying probability distribution is learned, e.g., from training data. The learned distribution can then be sampled from, generating new data instances similar to those in the training set. The learned approximation of the probability density is also accessible, and it is normalized, which is crucial for our use.

Normalizing flow models work by transforming a simple base distribution into a more complex distribution through a series of bijections (invertible transformations). For a comprehensive review of normalizing flows we refer the reader to Papamakarios et al. (2021). The base distribution is chosen so that it is easy to sample from and to evaluate its probability density, typically a Gaussian with unit variance. A vector of an unknown distribution , can be expressed through a transformation of a latent vector sampled from the base distribution :

| (10) |

must be invertible and and its inverse must be differentiable. When these conditions are satisfied, we can simply calculate the density of the distribution of through the change of variables formula by

| (11) |

where is the Jacobian corresponding to . Such transformations are composable: can be transformed again, and the resulting normalized density can be obtained analogously. In practice consists of a series of transformations. These are often defined in such a way that the determinant of can be computed efficiently. This is where the power of normalizing flows lies – a simple base distribution, when taken through a series of simple transformations can become much more expressive and is able to approximate complex targets. In reality, the resulting distribution is an imperfect approximation of that we call , where denotes the trainable parameters of the transformations.

A multitude of flow architectures with different strengths have been proposed. In this work (and in the harmonic code), we use real-valued non-volume preserving (Dinh et al., 2017) and rational quadratic spline flows (Durkan et al., 2019). However, any flow model can be integrated into the method, offering greater computational scalability.

3.1.1 Real non-volume preserving flows

Real-valued non-volume preserving (real NVP) flows were introduced by Dinh et al. (2017). Their architecture is relatively simple, consisting of a series of affine coupling layers. Consider the dimensional input , split into elements up to and following , respectively, and , for . Given input , the output of an affine couple layer is calculated by

| (12) | ||||

| (13) |

where denotes Hadamard (elementwise) multiplication, and the scale and translation are neural networks with trainable parameters. The Jacobian of such a transformation is a lower-triangular matrix, making its determinant efficient to calculate.

3.1.2 Rational quadratic spline flows

A more complex and expressive class of flows are rational quadratic spline flows introduced by Durkan et al. (2019). The architecture is similar to real NVP flows, but the layers include monotonic splines. These are piecewise functions consisting of multiple segments of monotonic rational quadratics with learned parameters. Given input , the output of a rational quadratic coupling layer has the form:

| (14) | ||||

| (15) | ||||

| (16) |

where is a neural network and is a spline parametrised by , with each bin defined by a monotonically-increasing rational-quadratic function. Such layers are combined with alternating affine transformations to create the normalizing flow. Thanks to their more expressive and sophisticated architecture, rational quadratic spline flows are well-suited to higher dimensional and more complex problems than real NVP flows (Durkan et al., 2019).

3.2 The learned harmonic mean estimator with normalizing flows

In this work we address the limitations of the simple machine learning methods considered in the learned harmonic mean framework previously. Recall, the aim is to learn an approximation of the posterior from samples but with the critical constraint that the tails of the learned distribution are contained within the posterior. To learn appropriate models a bespoke optimization algorithm was considered in McEwen et al. (2021). Normalizing flows afford an elegant alternative solution for keeping the learned target density contained within the posterior, rendering the bespoke training approach unnecessary. The importance sampling target density is first learned using a normalizing flow model and then concentrated by reducing the variance of the base distribution, i.e. reducing its “temperature”. The resulting method provides an improved estimator of the Bayesian evidence that retains the flexibility and accuracy of its predecessor, while improving its robustness and scalability.

3.2.1 Training the flow

Before we estimate the evidence we need to train a normalizing flow on samples from the posterior. When training normalizing flows, the forward KL divergence is well-suited as the loss function when we have samples of the target distribution. Consider an unknown posterior distribution of interest and its approximating flow , where are the trainable flow parameters. The KL divergence can be interpreted as a measure of the dissimilarity between and and is therefore a natural quantity to minimize when training a normalizing flow. The forward KL divergence between the two distributions can be expressed as

| (17) |

Given samples from the posterior, where , the expectation in Equation (3.2.1) can be approximated by Monte Carlo as

| (18) |

Minimizing this approximation is equivalent to fitting the normalizing flow to the samples by maximum likelihood (Papamakarios et al., 2021). We take this approach to trainining our flow, and minimize the loss given by Equation (18) using the Adam optimizer (Kingma & Ba, 2017; Dozat, 2016). We use a portion of the samples for training the flow and reserve the rest to be used for inference, to be substituted when estimating the evidence.

It is worth stressing that this is the standard training approach for normalizing flows. By replacing the simple machine learning methods considered in McEwen et al. (2021) with flows, we render their bespoke training approach unnecessary, making the method more robust and flexible.

As discussed in Section 1, training a flow by forward KL divergence, or equivalently maximum likelihood, can suffer from mode seeking behaviour, where the learned flow has narrower tails than the target (e.g. Murphy, 2022). Nevertheless, this is not a problem for use of the flow in the learned harmonic estimator since we seek a learned distribution that has narrower tails than the posterior. Moreover, the learned distribution is not used as a surrogate for the posterior but rather as the importance sampling target. The learned distribution need not be a highly accurate approximation of the posterior but it critically must be concentrated within the posterior. Consequently, the mode seeking behaviour of training normalizing flows by forward KL divergence does not compromise the learned harmonic mean estimator.

3.2.2 Concentrating the probability density

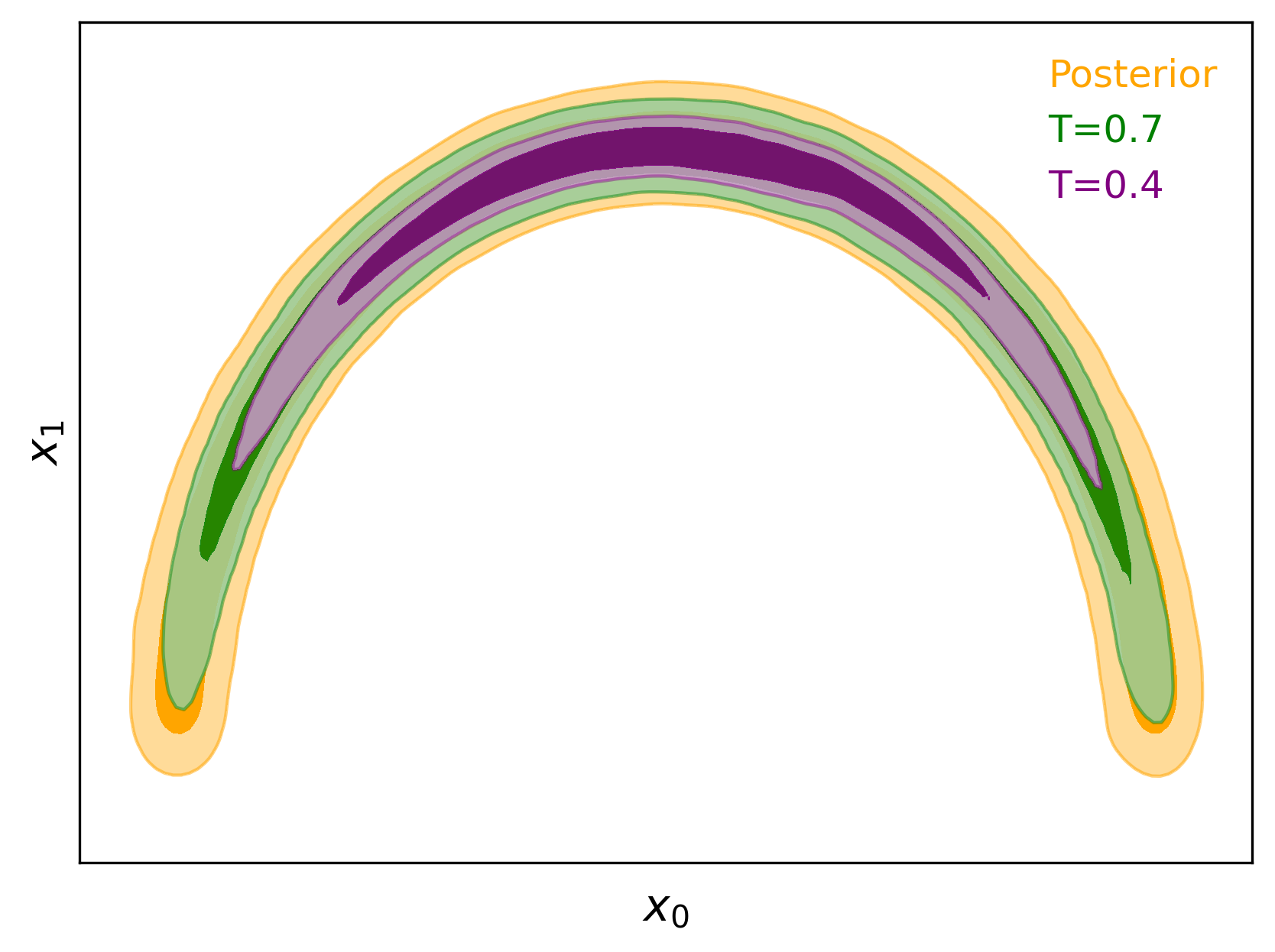

Once the flow is trained on samples from the posterior, we concentrate its probability density by reducing what we call the flow temperature parameter . This is a factor by which the variance of the base Gaussian distribution is multiplied. Reducing the base distribution’s variance has the effect of concentrating its probability density in parameter space, or reducing its “temperature” in a statistical mechanics interpretation. This has the effect of also concentrating the probability density of the transformed distribution due to the continuity and differentiability of the flow, as illustrated in Figure 1. Hence, the concentrated flow is the perfect candidate for the importance sampling target in the harmonic mean estimator, as it is normalized and close to the posterior but contained within it. After a flow is trained, it can be used in the learned harmonic mean estimator with different temperature values without the need to retrain for each .

3.2.3 Standardization

We standardize the training and inference data. We calculate the mean and variance of the input training data represented in a matrix and remove that before fitting the model. This means that each entry of the data matrix is transformed as

| (19) |

where is the mean and is the standard deviation of the training data parameter column (calculated over the data points). This training data consists of samples from the parameter space so , where is the dimension of . We then apply this same transformation, with and vectors kept the same, to the data points for which we are predicting the probability density, namely the inference data. For the density to still be normalized, we need to then also multiply the flow density by the Jacobian of this transformation, so the predicted density for a standardized model is

| (20) |

3.2.4 Evidence error estimate

In addition to an estimate of the evidence itself, we also require an estimate of its error. In McEwen et al. (2021) approaches are proposed to estimate the variance of the learned harmonic mean estimator and also its variance. Specifically, the Bayesian evidence estimate and its error are considered . While quoting these terms is sufficient for many toy problems, to ensure numerical stability for practical problems in higher dimensions it is necessary to always work in log space to avoid numerical overflow. Converting the error estimate to log space is non-trivial as in general. To remain in log space we are interested in the log-space error defined by

| (21) |

The log-space error estimate can be computed by

| (22) |

where

| (23) |

This way we can avoid computing directly. We only compute , which we expect to be much smaller and less susceptible to overflow. When quoting the result with log-space errors we use the notation . The log evidence errors can be straightforwardly obtained by swapping the negative and positive errors of the reciprocal log evidence.

3.2.5 Code

The learned harmonic mean estimator with normalizing flows is implemented in the harmonic package333https://github.com/astro-informatics/harmonic, from version 1.2.0 onwards. The methodology described in this section, with real NVP and rational quadratic spline flows, has been implemented in JAX and is available in recent releases of harmonic on PyPi and GitHub. Furthermore, other parts of the harmonic code have been updated to run on JAX, which is a Python package offering acceleration, just-in-time compilation and automatic differentiation functionality (Bradbury et al., 2018). Consequently, harmonic can now be run on hardware accelerators such as GPUs, potentially reducing computation times and allowing the user to tackle more complex, computationally demanding problems. Additionally, the automatic differentiation functionality opens up the possibility of optimizing based on evidence (e.g. for experimental design), as gradients are now accessible all the way down to evidence level, which provides an intriguing avenue for further research. The normalizing flow portion of the code is implemented using the flax (Heek et al., 2023), TensorFlow Probability (Dillon et al., 2017), optax and distrax (DeepMind et al., 2020) packages.

3.2.6 Naïve Bayesian evidence estimation using normalizing flows

As discussed in Section 1, and first described in Spurio Mancini et al. (2023), since flows are normalized it is possible to back out their normalizing constant to provide an estimate of the Bayesian evidence. We recall this approach here for reference.

Given samples an estimate of the evidence can be computed for each sample by

| (24) |

While posterior samples are typically available and hence used, in principle the samples do not necessarily need to be drawn from the posterior. An overall estimate of the evidence and its spread can then simply be computed from the mean of these evidence estimates and their standard deviation. However, the resulting evidence estimator is likely to be biased and will have a large variance. This is because it is highly dependent on the accuracy of the learned normalizing flow, which is used as a surrogate for the posterior, as discussed in Section 1. The learned harmonic mean does not suffer from these issues.

4 Numerical experiments

To validate the effectiveness of the method presented in this paper, we perform a series of numerical experiments. Firstly, in Section 4.2 we repeat a series of low-dimensional benchmark problems performed by McEwen et al. (2021) but using normalizing flows to learn the importance sampling target. The underlying examples are described in more detail by McEwen et al. (2021). The original harmonic mean estimator has been shown to fail catastrophically for many of these examples (Friel & Wyse, 2012), while our learned harmonic mean remains accurate. In Section 4.3 we study the impact of varying the temperature parameter on the evidence estimate, showing the robustness of our method. Then in Section 4.4 we present a practical application of our method in a cosmological context for the DES (Dark Energy Survey). We perform a joint lensing-clustering analysis (“3x2pt”) on a DES Y1-like configuration. We compare our results with the values obtained through the conventional method of nested sampling.

4.1 Architectures, sampling and training

In the experiments where a real NVP flow is used, translation networks of the affine coupling layers are given by two-layer dense neural networks with a leaky ReLU activation function in between. For the scaling layers this is scaled by another dense layer with a softplus activation. We permute the inputs between coupling layers to ensure the flow transforms all elements. In the low dimensional benchmark experiments we consider a real NVP flow, unless otherwise stated, with six coupling layers, where typically only the first two include scaling. When we use a rational quadratic spline flow, it has a range to (outside of this range it defaults to a linear transformation). The conditioner for the spline hyperparameters is a multi-layer perceptron with a tanh activation. We use a Gaussian base distribution with zero mean and an identity covariance matrix for all flows.

For the low-dimensional benchmark examples, we generate samples from the posterior using MCMC methods implemented in the emcee package (Foreman-Mackey et al., 2013). In the practical cosmological example, we use the Metropolis-Hastings sampling approach (Metropolis et al., 1953; Hastings, 1970) implemented in the cobaya package (Torrado & Lewis, 2019). We then train the flow on half of the samples by maximum likelihood and use the remaining samples for inference.

4.2 Benchmark examples

4.2.1 Rosenbrock

The Rosenbrock problem is a common benchmark example considered when estimating the Bayesian evidence. The Rosenbrock distribution’s narrow curving degeneracy presents a challenge in sufficiently exploring the resulting posterior distribution to accurately evaluate the Bayesian evidence. The Rosenbrock function is given by

| (25) |

where denotes the number of dimensions. In our example we consider a 2-dimensional problem with the log-likelihood given by and a uniform prior and .

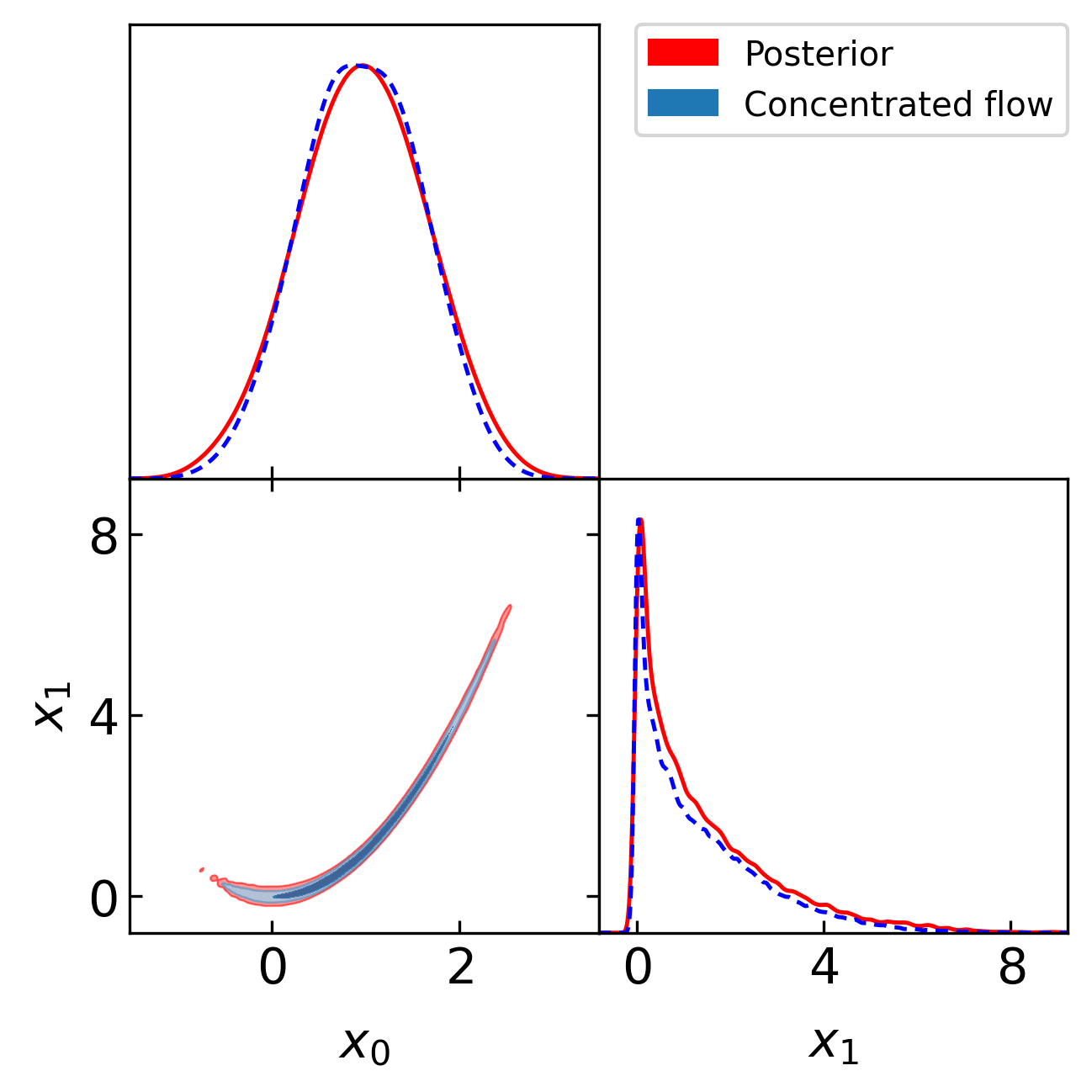

We draw samples for chains, with burn-in of samples, yielding posterior samples per chain. Figure 2 shows the corner plot of samples from the posterior (solid red line) and a real NVP flow with scaled and unscaled layers at temperature (dashed blue line). It can be seen that the flow approximates the posterior quite well while remaining contained within it. This is exactly what we want in a target distribution for the harmonic mean estimator.

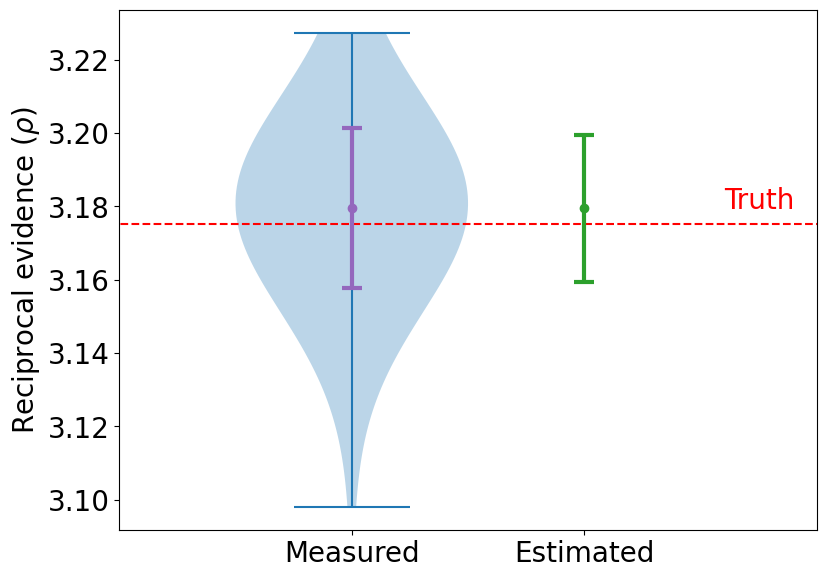

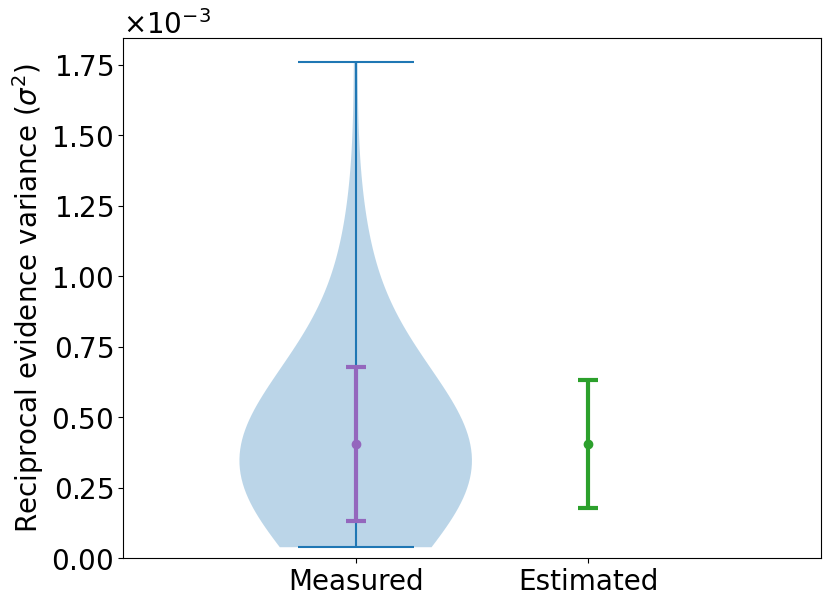

Figure 3a shows a violin plot of the results of this experiment repeated times with posterior samples generated from different seeds. The ground truth obtained through numerical integration is shown in red. It can be seen that the evidence values estimated using our method are accurate, agreeing with the ground truth value. It can also be seen that the estimator of the population variance agrees with the variance measured across the repeats. Figure 3b shows a violin plot of the variance estimator across runs alongside the standard deviation calculated from the variance-of-variance estimator. It can be seen they are also in agreement. The Bayesian evidence estimates obtained using the learned harmonic mean and their error estimates are highly accurate.

4.2.2 Normal-Gamma

We also consider the Normal-Gamma model (Bernardo & Smith, 1994) where data are distributed normally

| (26) |

for , with mean and precision . A normal prior is assumed for and a Gamma prior for :

| (27) | ||||

| (28) |

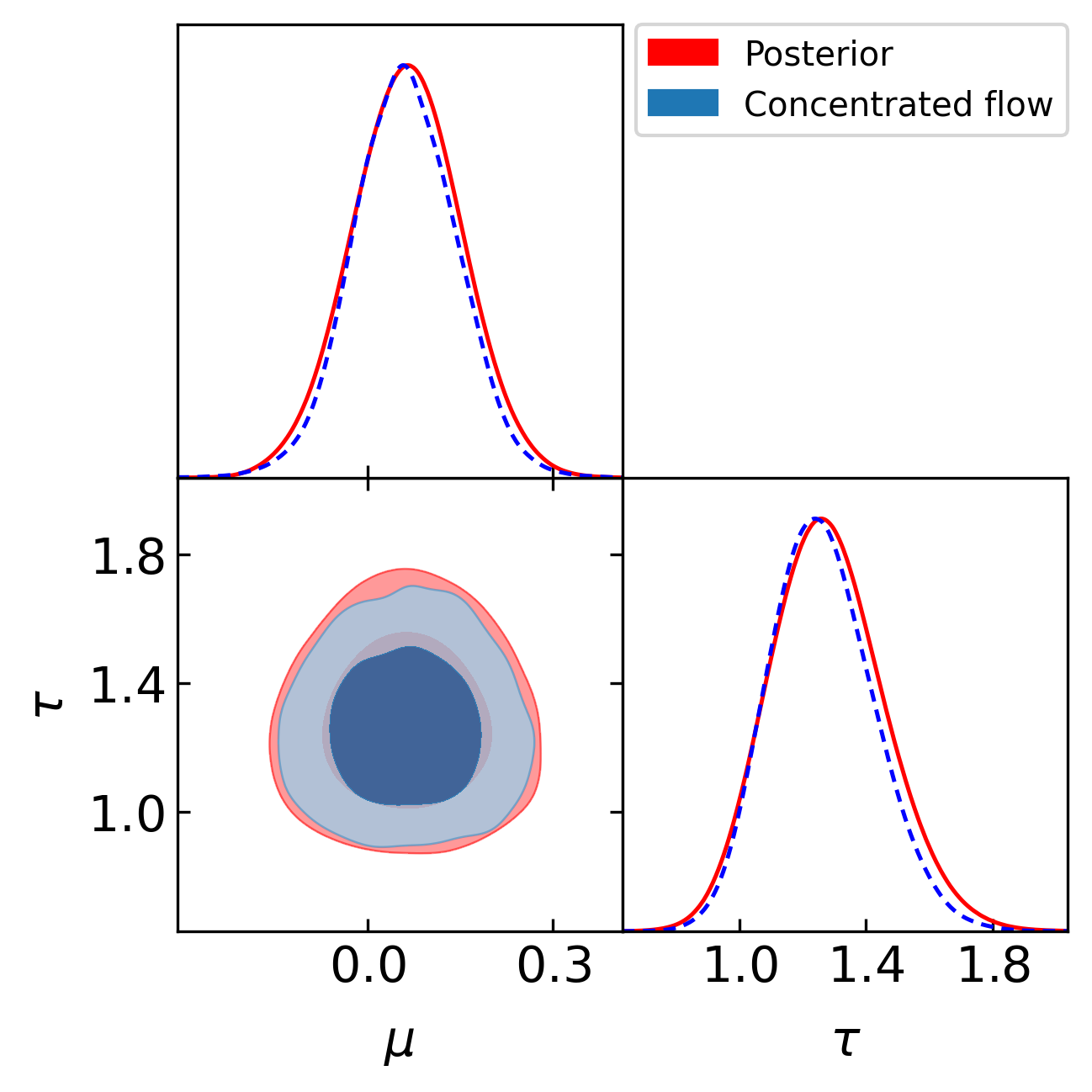

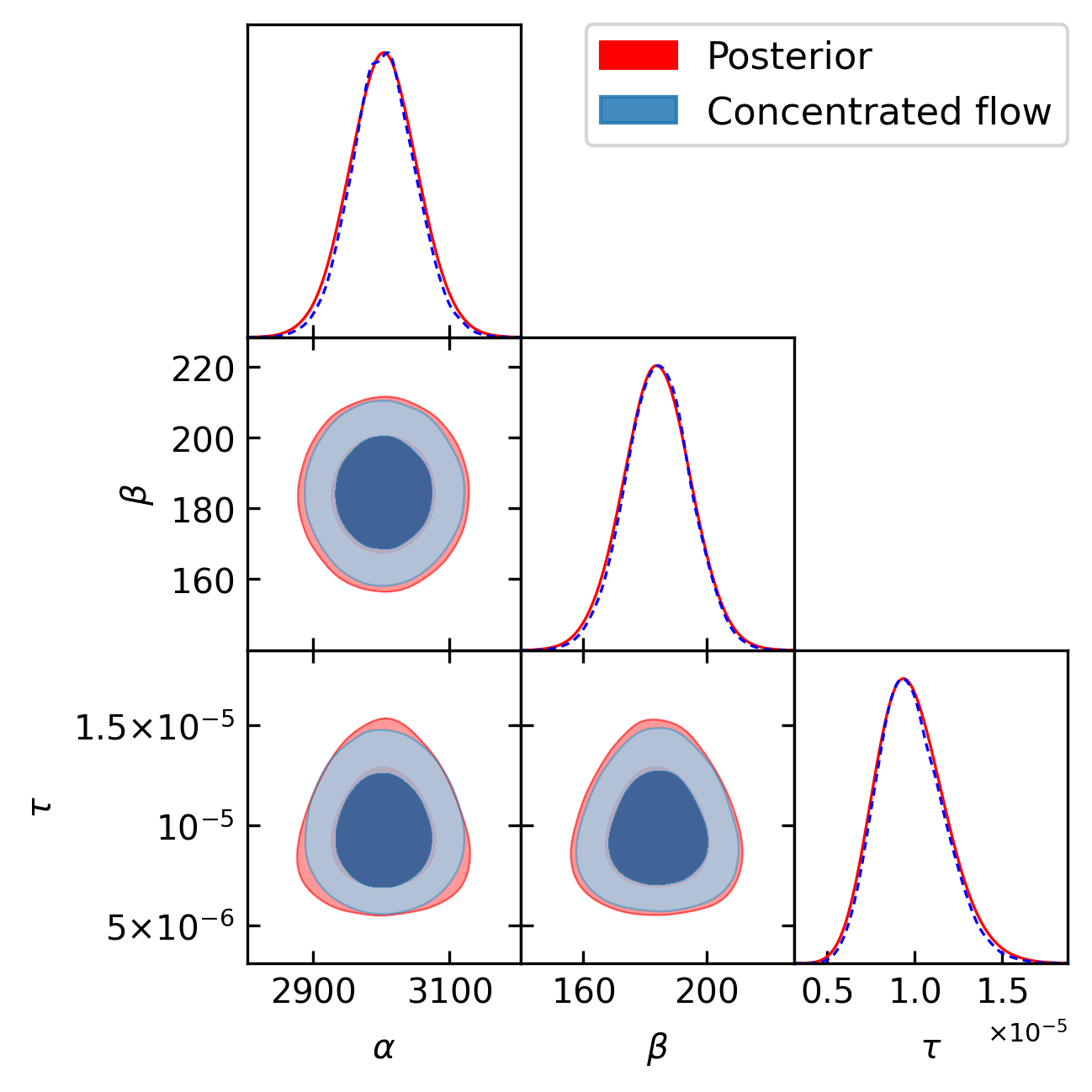

with mean , shape and rate . The precision scale factor controls how diffuse the prior is. Friel & Wyse (2012) apply the original harmonic mean for this example and show that the evidence estimate does not vary with , unlike the analytic ground truth value. We repeat this experiment, drawing samples for chains, with burn in of samples, yielding posterior samples per chain. We use a real NVP flow with scaled and unscaled layers at temperatures and to estimate the evidence.

Figure 4a shows an example corner plot of the training samples from the posterior for (red) and from the normalizing flow (blue) at temperature . Again, it can be seen that the concentrated learned target is close to the posterior but with thinner tails, as is required.

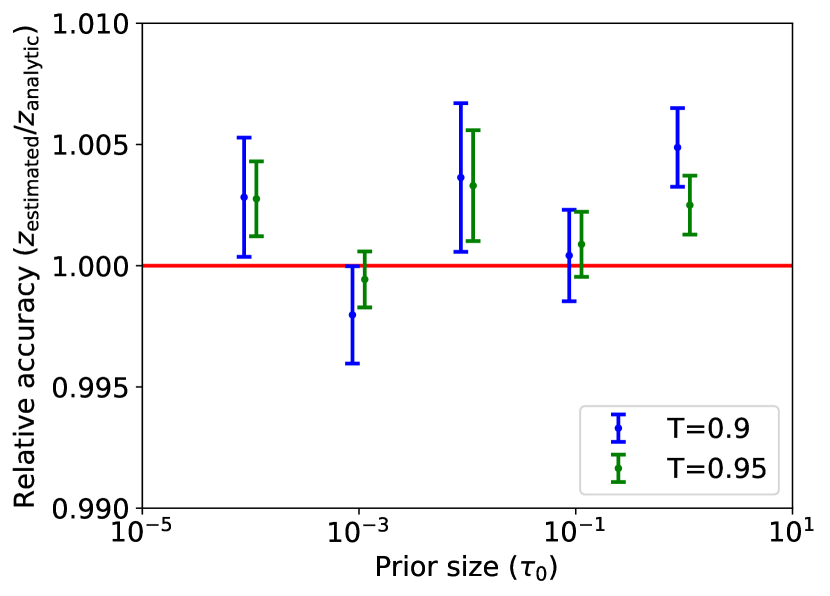

Figure 4b shows the relative accuracy of the evidence estimate computed using our method for a range of prior sizes. It can be seen that, unlike the original harmonic mean estimator, our method is accurate for a range of . Results are computed with the trained flow at temperature (blue) and (green). They are accurate in both cases, showing that the temperature parameter does not require fine-tuning.

4.2.3 Logistic regression models: Pima Indian example

We consider an example involving the comparison of two logistic regression models used to describe the Pima Indians data (Smith et al., 1988), originally from the National Institute of Diabetes and Digestive and Kidney Diseases.

This analysis was originally performed to study indicators of diabetes in Pima Indian women. The predictors of diabetes considered included the number of prior pregnancies (NP), plasma glucose concentration (PGC), body mass index (BMI), diabetes pedigree function (DP) and age (AGE). The probability of diabetes for person is modelled by the logistic function

| (29) |

with covariates and parameters , where is the total number of covariates considered. The likelihood is given by

| (30) |

where is the diabetes incidence with equal to one if patient has diabetes and zero otherwise. The prior distribution on is a Gaussian with precision .

Two such logistic regression models are considered:

| covariates = {NP, PGC, BMI, DP}; | |||

| covariates = {NP, PGC, BMI, DP, AGE}, |

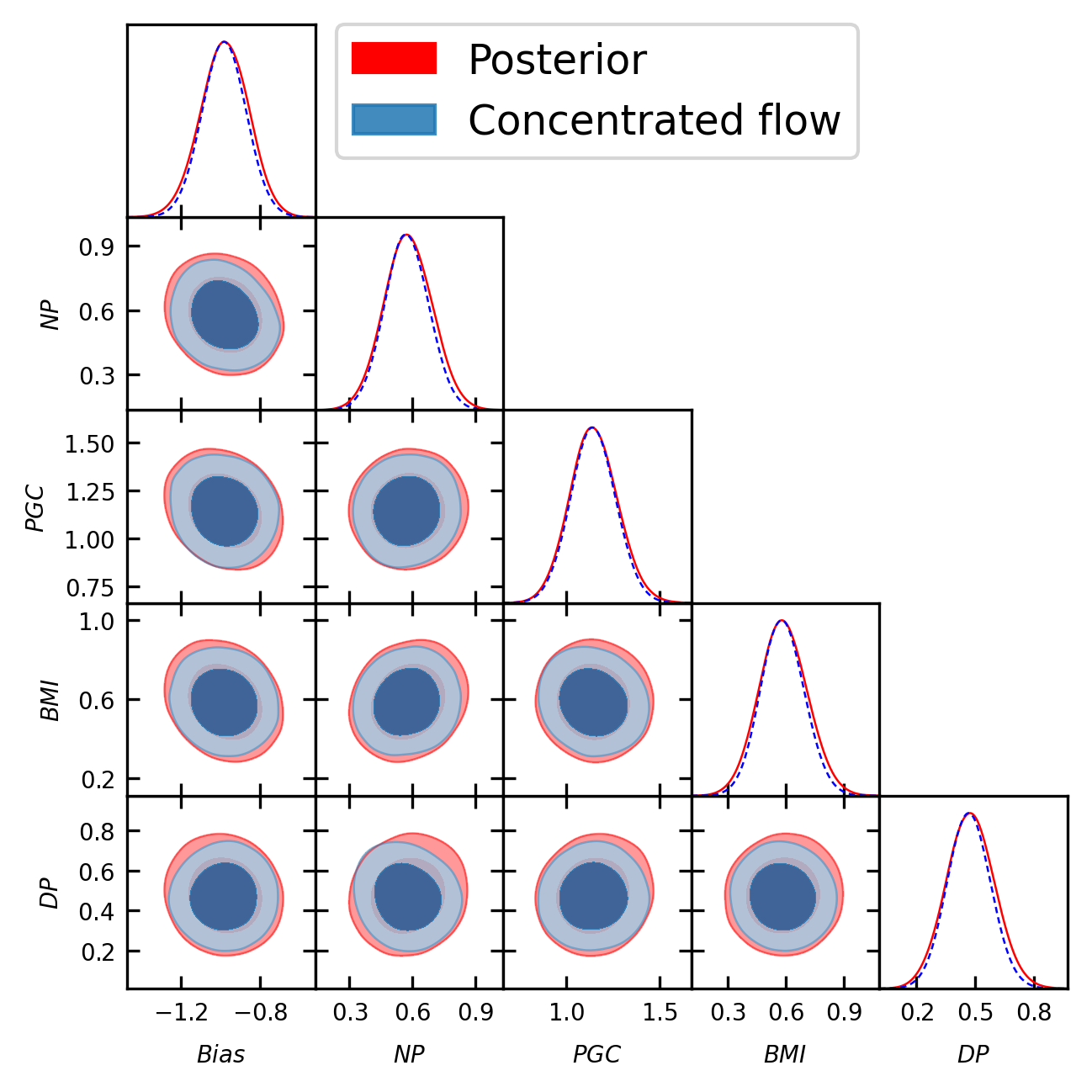

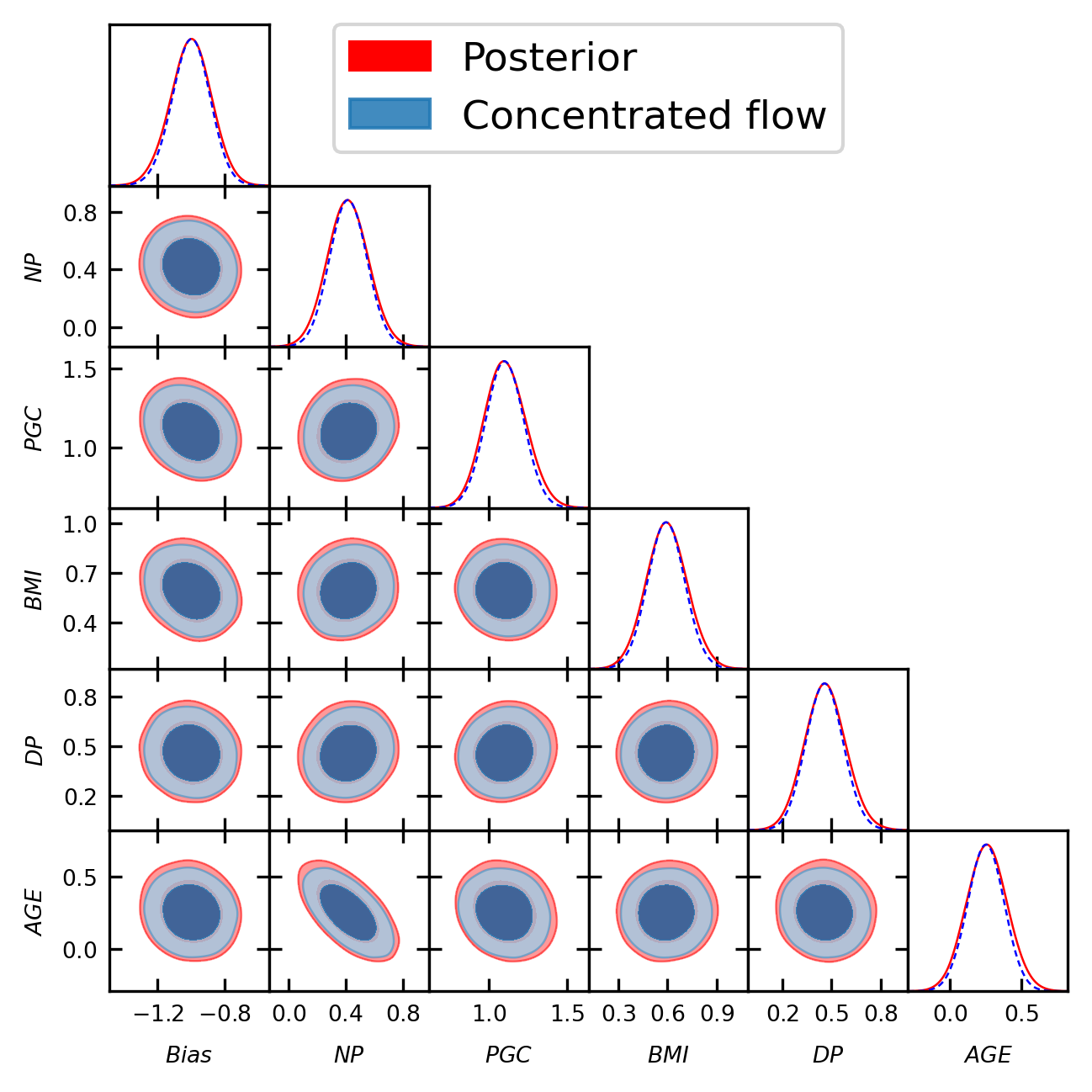

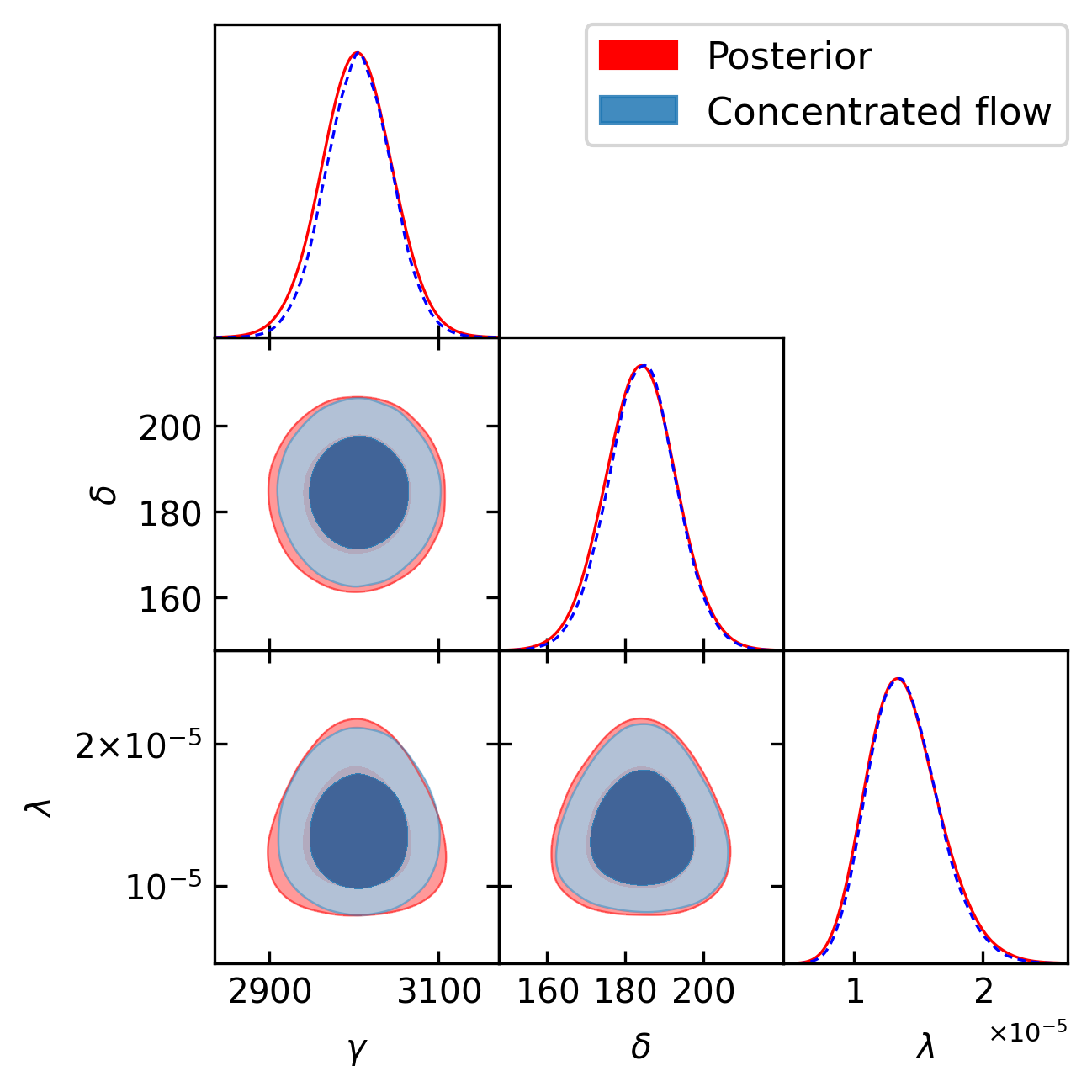

where both additionally include a bias. We estimate the Bayes factor of these models with our method and compare it to a benchmark value computed by Friel & Wyse (2012) using a reversible jump algorithm (Green, 1995). They obtain a value of (), which we treat as ground truth. We draw samples for chains, with burn in of 0 samples, yielding posterior samples per chain. We use a real NVP flow with scaled and unscaled layers at temperature , applying standardization.

Figure 5 shows the corner plots for this example for both models. The training samples from the posterior are shown in red and from the normalizing flow at temperature in blue. Once again, we see that the concentrated flow is contained within the posterior as expected. The log evidence found for Model 1 and 2 is and respectively, resulting in the estimate , indicating a slight preference for Model 1. The Bayes factor value is in close agreement with the benchmark, whereas the original harmonic mean estimator was not accurate (Friel & Wyse, 2012).

4.2.4 Non-nested linear regression models: Radiata pine example

In the last benchmark example we compare two non-nested linear regression models describing the Radiata pine data (Williams, 1959). The dataset consists of measurements of the maximum compression strength parallel to the grain , density and resin-adjusted density , for specimen . Two Gaussian linear models are compared, one with density and one with resin-adjusted density as variables:

| (31) | ||||||||

| (32) |

where , denote the mean values of and respectively, and and denote the precision of the noise for the respective models. For both models, Gaussian priors with means and , and precision scales and are chosen. A gamma prior is assumed for the noise precision with shape and rate .

The evidence can be computed analytically for this example (McEwen et al., 2021).

Using emcee, we draw samples for chains, with burn in of samples, yielding posterior samples per chain. We train a rational quadratic flow consisting of layers, with spline bins. Standardization is applied to the data as detailed in Section 3.2, which is necessary due to the vast difference in scale of the parameter dimensions.

Figure 6 shows a corner plot of the training samples from the posterior (red) and from the normalizing flow (blue) at temperature for both models. Again, it can be seen that the concentrated learned target is contained within the posterior. The log evidence found for Model 1 and 2 is and respectively, resulting in the estimate . The analytic values of the log evidence are and for Models 1 and 2 respectively, resulting in the estimate . The value obtained using our estimator is in close agreement with the ground truth. The learned harmonic mean gives an accurate estimate of the evidence, whereas the original harmonic mean estimator fails catastrophically for this example (Friel & Wyse, 2012).

4.3 Robustness of the temperature parameter

| Method | Computation time (64 CPU cores) | |||

|---|---|---|---|---|

| Learned harmonic mean | 16 hours (sampling) 16 minutes (evidence) | |||

| Nested sampling | 94 hours (sampling and evidence) | |||

| Naïve flow estimator | Similar to learned harmonic mean |

Many methods of estimating the evidence require careful fine-tuning of hyperparameters. As explained in Section 2.3, this was also the case for the learned harmonic mean estimator when using the classical machine learning models as considered previously. The target distribution was learned using simple machine learning models and a bespoke optimization approach designed to ensure the target distribution is contained within the posterior. The models had to be carefully chosen and their hyperparameters had to be fine-tuned for the estimator to be accurate and validated by cross-validation. In this work, through the introduction of a more sophisticated machine learning model, normalizing flows, we are able to avoid this drawback and create a more robust estimator.

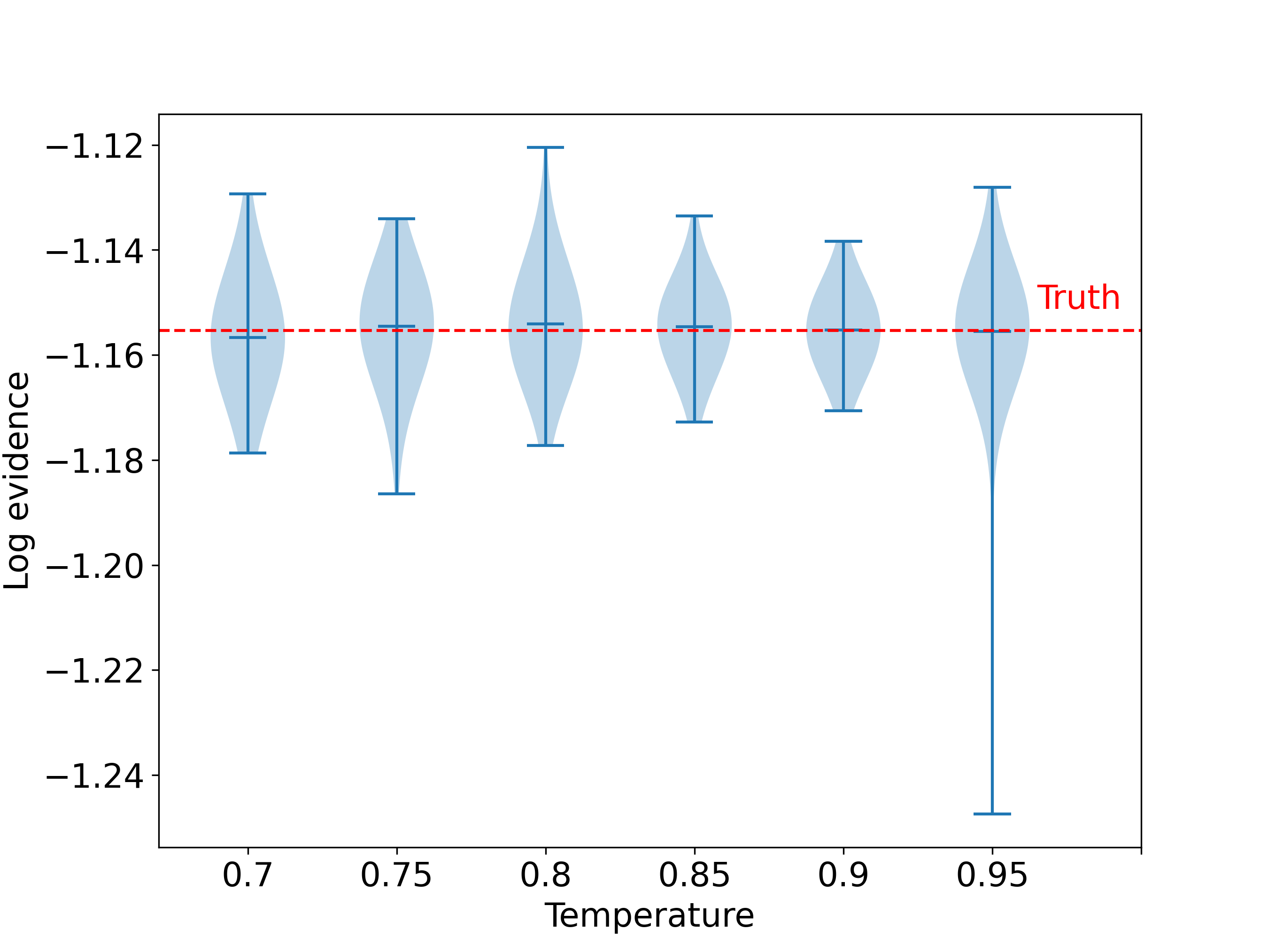

Our learned harmonic mean estimator with normalizing flows contains essentially just a single hyperparameter: the temperature of the concentrated flow. We perform numerical experiments to study the influence of the temperature parameter on the evidence estimate. The Rosenbrock benchmark problem is considered again, as described in Section 4.2.1. The experimental process is performed for a range of temperatures , repeating it times for each value. For each repeat, a new seed is used to generate a new dataset of posterior samples, and to initialize the optimizer.

Figure 7 shows violin plots of the log evidence estimates obtained in this experiment plotted for each temperature value. The ground truth, obtained through direct numerical integration is shown in red. It can be seen that the evidence estimates remain accurate and unbiased for the range of temperature values considered. This illustrates the robustness of our method – the temperature parameter does not need to be fine-tuned.

One must nevertheless ensure that the flow is indeed contained within the posterior as required for the learned harmonic mean to be accurate. The temperature parameter needs to be sufficiently small for this to be the case. If the flow was a perfect approximation of the posterior, any value would do. In practice this is not the case, and if the temperature is chosen to be too close to unity, the flow might not be contained within the posterior in some regions of the parameter space, causing the estimator’s variance to grow. This effect can partially be seen when looking at the violin plot for in Figure 7. Most of the evidence estimates remain accurate but it can be seen that there exists an outlier. The smallest evidence estimate computed is many standard deviations away from the ground truth. To avoid this, one should always ensure that the flow at the chosen temperature does not have fatter tails than the posterior. If the flow for were a perfect approximation of the posterior, one would expect the variance of the estimator to increase as is reduced below unity due to the resulting smaller effective sample size. However, when dealing with a finite number of samples from the posterior and imperfect approximations, a temperature value closer to unity is not always best. When is large, the possibility of the flow not being contained within the posterior increases. It is better to choose a lower, more conservative value of when dealing with a more complicated or high-dimensional posterior. In practice, we find works well for most problems. A lower value should be used if the posterior is particularly complex or high-dimensional. This value can then be adjusted based on the error estimate or other diagnostics computed by the harmonic code (McEwen et al., 2021).

4.4 Practical cosmological example: DES Y1 analysis

In Section 4.2 we showed that the learned harmonic mean estimator with normalizing flows works very well on a range of simple benchmark examples, where the ground truth Bayesian evidence is available. In this section we show it also performs well in a practical context, by applying it to a Dark Energy Survey Year 1 (DES Y1) example. DES is an on-going cosmological survey designed to gain insight into the nature of dark energy. We perform a 3x2pt analysis (Abbott et al., 2018a; Joachimi & Bridle, 2010), i.e. a joint analysis of galaxy clustering and weak lensing considering shear, clustering and their cross correlation, on a DES Y1-like configuration.

We follow the reference approach described by Campagne et al. (2023), who extract and compress a subset of the DES Year 1 lensing and clustering data and set up a forward model following the DES Y1 Pipeline (Abbott et al., 2018a). We use the DES Y1 redshift distributions444http://desdr-server.ncsa.illinois.edu/despublic/y1a1_files/chains/2pt_NG_mcal_1110.fits and simulate a 3x2pt data vector for a fixed cosmology. We use this as our mock data vector and run an inference pipeline to obtain posterior contours and evidence estimates. We refer the reader to Campagne et al. (2023) for the priors and all other details. To sample from the posterior we use the Cobaya package (Torrado & Lewis, 2019) with the Metropolis-Hastings algorithm. We then apply harmonic to these samples to evaluate the Bayesian evidence. For comparison, we also sample using the PolyChord nested sampler (Handley et al., 2015a, b) in Cobaya, which provides a benchmark Bayesian evidence estimate. We perform the analysis twice, assuming either a CDM or CDM cosmological model, with the dark energy equation of state parameter fixed to or free to vary, respectively.

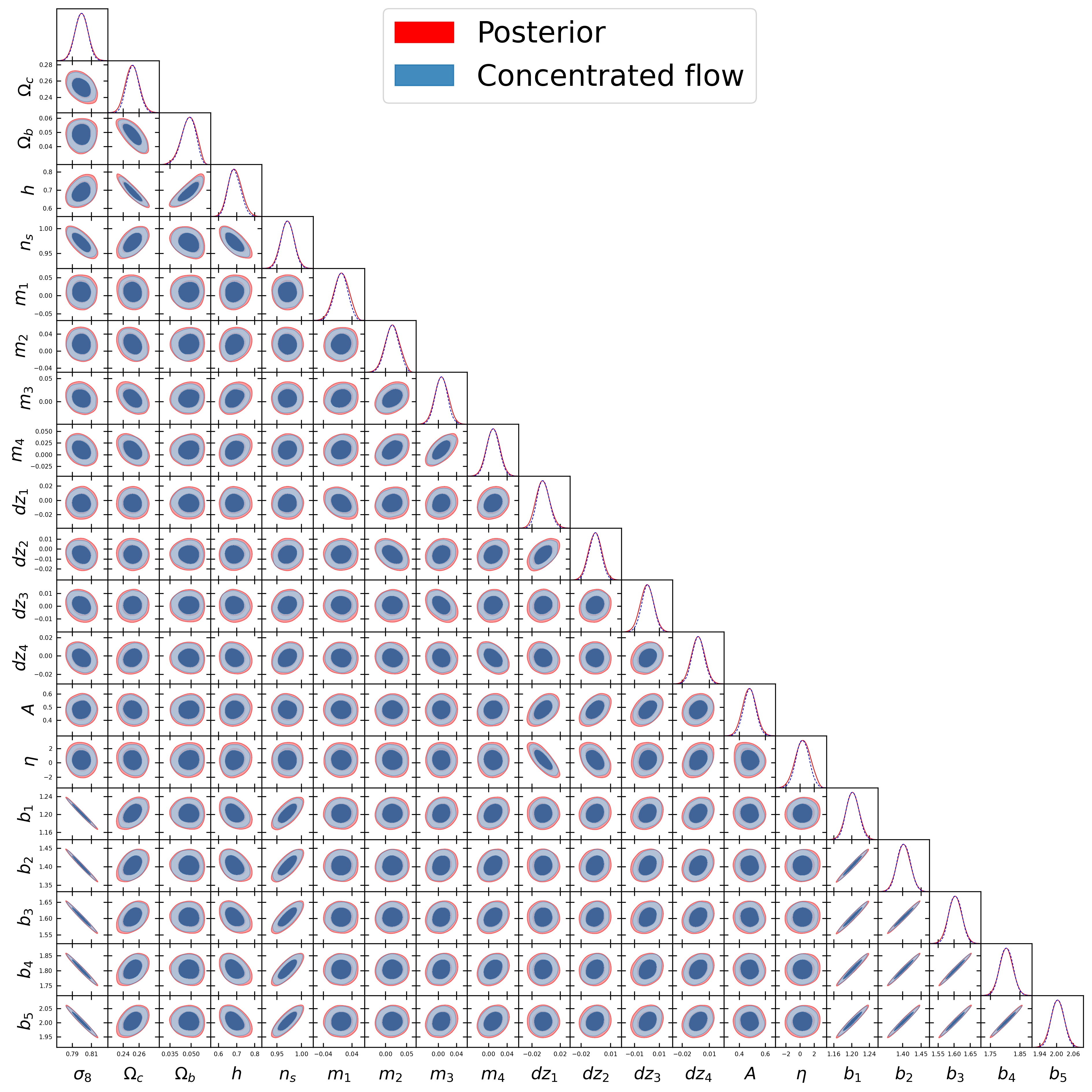

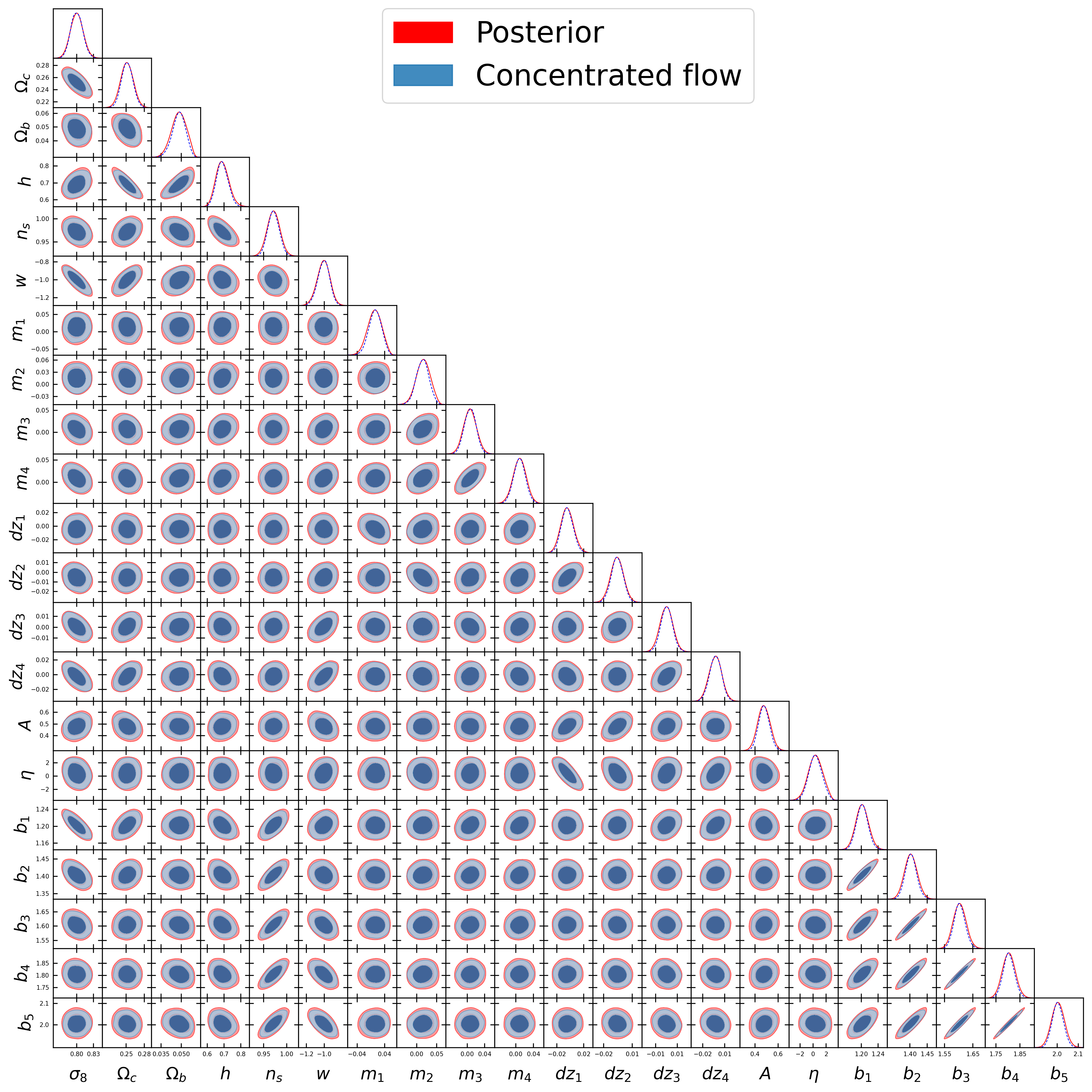

The CDM and CDM models have and parameters respectively. With the Metropolis-Hastings sampler, we run chains per model, obtaining an average of approximately and samples per chain for CDM and CDM respectively. We discard samples for burn-in in both cases. We train a rational quadratic flow consisting of layers, with spline bins, applying standardization, on half of the chains, and use the other half for inference.

Figure 8 shows the corner plots of the training samples alongside the flow at . It can be seen the flow also behaves as expected in this higher-dimensional practical setting, capturing the posterior distribution while being contained within it. Log evidence values, Bayes factors and computation time are reported in Table 1 for the learned harmonic mean estimator, nested sampling with PolyChord and by the naïve flow estimate introduced in Spurio Mancini et al. (2023) and described in Section 3.2.6.

Note that the values computed by the learned harmonic mean and nested sampling are in close agreement, showing a slight preference for CDM, matching the configuration of our simulated setup. The values computed by the naïve estimator are in approximate agreement but exhibit an error two orders or magnitude larger than the error of the learned harmonic mean (in higher dimensional examples to be reported in an ongoing work we observe the naïve estimator failing much more catastrophically).

In terms of computational speed (summarized in Table 1 but reported in great detail here), sampling with Cobaya using the Metropolis-Hastings algorithm takes approximately hours for CDM and CDM each on CPU cores. The compute time added by harmonic is around minutes on GPU for training and minutes on CPU cores to estimate the evidence for each model. Using PolyChord takes approximately hours for CDM and CDM each, on the same CPU cores used for the Metropolis-Hastings sampling. The Metropolis-Hastings algorithm in this case is much quicker due to the use of a proposal covariance matrix based on a Planck cosmology (Campagne et al., 2023). Thanks to the flexibility of the learned harmonic estimator, we can leverage this advantage and choose Metropolis-Hastings over nested sampling, while still being able to estimate the Bayesian evidence and perform model comparison. Even in this higher dimensional setting, the learned harmonic mean only adds a few minutes of compute time on top of the sampler. This demonstrates the potential scalability of the method and its potential for computing the evidence from existing saved down MCMC chains.

5 Conclusions

In this work we outlined the learned harmonic mean estimator with normalizing flows, a robust, flexible and scalable estimator of the Bayesian evidence. Normalizing flows meet the core requirements of the learned importance target distribution of the learned harmonic mean estimator: namely, they provide a normalized probability distribution for which one can evaluate probability densities. We use them to introduce an elegant way to ensure the probability mass of the learned distribution is contained within the posterior, a critical requirement of the learned harmonic mean. This avoids the need for a bespoke training approach, resulting in a more robust and flexible estimator. Furthermore, flows offer the potential of greater scalability than the classical machine learning models considered previously.

To validate its accuracy, we applied the learned harmonic mean to several benchmark problems. Our method produced accurate results, even in cases where the original harmonic mean had been shown to fail. We also applied the learned harmonic mean to a practical cosmological example, the Dark Energy Survey Year 1 (DES Y1) data 3x2pt analysis. Even in this higher dimensional context for up to parameters our method computed an estimate that was in excellent agreement with the conventional approach using nested sampling. This shows the potential for scalability of our method. Many existing methods of estimating the Bayesian evidence, including previous work on the learned harmonic mean, require careful parameter fine-tuning. Beyond the flow architecture, we only introduced one hyperparameter – the concentrated flow temperature , which does not require any fine-tuning. We showed this empirically by considering a selected benchmark problem for a range of values. The estimate remained accurate, demonstrating the robustness of our method.

Since the learned harmonic mean estimator is decoupled from the sampling method, it can be used in a wide variety of settings. This includes approaches such as simulation-based inference, variational inference and various MCMC methods where the evidence could not otherwise be computed accurately, such as the No U-Turn Sampler (NUTS) (Hoffman & Gelman, 2011). When using MCMC methods for parameter estimation, the Bayesian evidence can be obtained essentially “for free” or even post-hoc from saved down MCMC chains. Since the estimator is agnostic to the sampling strategy, it is highly flexible. The best suited sampling strategy may be used for the problem at hand, as we demonstrated in the DES Y1 example, where Metropolis-Hastings accurately sampled the posterior much faster than nested sampling. In ongoing work we leverage the flexibility of the learned harmonic mean to demonstrate its use with NUTS and the CosmoPower-JAX emulator (Spurio Mancini et al., 2022; Piras & Spurio Mancini, 2023) to scale evidence calculation to dimensions. Overall, the learned harmonic mean estimator with normalizing flows is a robust, flexible and scalable tool for Bayesian model comparison that can be used in a variety of contexts.

Acknowledgements

We thank Kaze Wong for insightful discussions regarding normalizing flows. A.P. is supported by the UCL Centre for Doctoral Training in Data Intensive Science (STFC grant number ST/W00674X/1). M.A.P. and J.D.M. are supported by EPSRC (grant number EP/W007673/1). D.P. was supported by a Swiss National Science Foundation (SNSF) Professorship grant (No. 202671), and by the SNF Sinergia grant CRSII5-193826 “AstroSignals: A New Window on the Universe, with the New Generation of Large Radio-Astronomy Facilities”. A.S.M. acknowledges support from the MSSL STFC Consolidated Grant ST/W001136/1.

References

- Abbott et al. (2018a) Abbott T., et al., 2018a, Physical Review D, 98

- Abbott et al. (2018b) Abbott T. M., et al., 2018b, Physical Review D, 98, 043526

- Aghanim et al. (2020) Aghanim N., et al., 2020, Astronomy & Astrophysics, 641, A6

- Ashton et al. (2022) Ashton G., et al., 2022, Nature Reviews Methods Primers, 2, 39

- Bernardo & Smith (1994) Bernardo J., Smith A., 1994, Wiley Online Library

- Bradbury et al. (2018) Bradbury J., et al., 2018, JAX: composable transformations of Python+NumPy programs, http://github.com/google/jax

- Brewer et al. (2011) Brewer B. J., Pártay L. B., Csányi G., 2011, Statistics and Computing, 21, 649

- Brout et al. (2022) Brout D., et al., 2022, The Astrophysical Journal, 938, 110

- Buchner (2021) Buchner J., 2021, Journal of Open Source Software, 6, 3001

- Cai et al. (2022) Cai X., McEwen J. D., Pereyra M., 2022, Statistics and Computing, 32

- Campagne et al. (2023) Campagne J.-E., et al., 2023, The Open Journal of Astrophysics, 6

- Carron et al. (2022) Carron J., Mirmelstein M., Lewis A., 2022, Journal of Cosmology and Astroparticle Physics, 2022, 039

- Chib (1995) Chib S., 1995, Journal of the American Statistical Association, 90, 1313

- Clyde et al. (2007) Clyde M., Berger J., Bullard F., Ford E., Jefferys W., Luo R., Paulo R., Loredo T., 2007, in Statistical challenges in modern astronomy IV. p. 224

- DES Collaboration et al. (2024) DES Collaboration et al., 2024, The Dark Energy Survey: Cosmology Results With 1500 New High-redshift Type Ia Supernovae Using The Full 5-year Dataset (arXiv:2401.02929)

- DESI Collaboration et al. (2016) DESI Collaboration et al., 2016, The DESI Experiment Part I: Science,Targeting, and Survey Design (arXiv:1611.00036)

- DeepMind et al. (2020) DeepMind et al., 2020, The DeepMind JAX Ecosystem, http://github.com/deepmind

- Dillon et al. (2017) Dillon J. V., et al., 2017, TensorFlow Distributions (arXiv:1711.10604)

- Dinh et al. (2017) Dinh L., Sohl-Dickstein J., Bengio S., 2017, in International Conference on Learning Representations. https://openreview.net/forum?id=HkpbnH9lx

- Dozat (2016) Dozat T., 2016, in Proceedings of the 4th International Conference on Learning Representations. pp 1–4

- Durkan et al. (2019) Durkan C., Bekasov A., Murray I., Papamakarios G., 2019, Advances in neural information processing systems, 32

- Feroz & Hobson (2008) Feroz F., Hobson M. P., 2008, Monthly Notices of the Royal Astronomical Society, 384, 449–463

- Feroz et al. (2009a) Feroz F., Hobson M. P., Bridges M., 2009a, MNRAS, 398, 1601

- Feroz et al. (2009b) Feroz F., Hobson M. P., Bridges M., 2009b, Monthly Notices of the Royal Astronomical Society, 398, 1601–1614

- Feroz et al. (2019) Feroz F., Hobson M. P., Cameron E., Pettitt A. N., 2019, The Open Journal of Astrophysics, 2

- Foreman-Mackey et al. (2013) Foreman-Mackey D., Hogg D. W., Lang D., Goodman J., 2013, PASP, 125, 306

- Friel & Wyse (2012) Friel N., Wyse J., 2012, Statistica Neerlandica, 66, 288

- Gelfand & Dey (1994) Gelfand A. E., Dey D. K., 1994, Journal of the Royal Statistical Society: Series B (Methodological), 56, 501

- Green (1995) Green P. J., 1995, Biometrika, 82, 711

- Handley et al. (2015a) Handley W. J., Hobson M. P., Lasenby A. N., 2015a, Monthly Notices of the Royal Astronomical Society: Letters, 450, L61–L65

- Handley et al. (2015b) Handley W. J., Hobson M. P., Lasenby A. N., 2015b, Monthly Notices of the Royal Astronomical Society, 453, 4385–4399

- Hastings (1970) Hastings W. K., 1970, Biometrika, 57, 97

- Heek et al. (2023) Heek J., Levskaya A., Oliver A., Ritter M., Rondepierre B., Steiner A., van Zee M., 2023, Flax: A neural network library and ecosystem for JAX, http://github.com/google/flax

- Hoffman & Gelman (2011) Hoffman M. D., Gelman A., 2011, The No-U-Turn Sampler: Adaptively Setting Path Lengths in Hamiltonian Monte Carlo (arXiv:1111.4246)

- Joachimi & Bridle (2010) Joachimi B., Bridle S. L., 2010, A&A, 523, A1

- Kingma & Ba (2017) Kingma D. P., Ba J., 2017, Adam: A Method for Stochastic Optimization (arXiv:1412.6980)

- Lenk (2009) Lenk P., 2009, Journal of Computational and Graphical Statistics, 18, 941

- Madhavacheril et al. (2024) Madhavacheril M. S., et al., 2024, The Astrophysical Journal, 962, 113

- McEwen et al. (2021) McEwen J. D., Wallis C. G. R., Price M. A., Mancini A. S., 2021, Machine learning assisted Bayesian model comparison: learnt harmonic mean estimator (arXiv:2111.12720)

- Metropolis et al. (1953) Metropolis N., Rosenbluth A. W., Rosenbluth M. N., Teller A. H., Teller E., 1953, J. Chemical Physics, 21, 1087

- Murphy (2022) Murphy K. P., 2022, Probabilistic Machine Learning: An introduction. MIT Press, probml.ai

- Neal (1994) Neal R. M., 1994, JR Stat Soc Ser A (Methodological), 56, 41

- Newton & Raftery (1994) Newton M. A., Raftery A. E., 1994, Journal of the Royal Statistical Society: Series B (Methodological), 56, 3

- Papamakarios et al. (2021) Papamakarios G., Nalisnick E., Rezende D. J., Mohamed S., Lakshminarayanan B., 2021, The Journal of Machine Learning Research, 22, 2617

- Piras & Spurio Mancini (2023) Piras D., Spurio Mancini A., 2023, The Open Journal of Astrophysics, 6

- Polanska et al. (2023) Polanska A., Price M. A., Spurio Mancini A., McEwen J. D., 2023, Physical Sciences Forum, 9

- Raftery et al. (2006) Raftery A. E., Newton M. A., Satagopan J. M., Krivitsky P. N., 2006, Preprint

- Robert & Wraith (2009) Robert C. P., Wraith D., 2009, in Aip conference proceedings. pp 251–262

- Rubin et al. (2023) Rubin D., et al., 2023, Union Through UNITY: Cosmology with 2,000 SNe Using a Unified Bayesian Framework (arXiv:2311.12098)

- Skilling (2006) Skilling J., 2006, Bayesian Analysis, 1, 833

- Smith et al. (1988) Smith J. W., Everhart J. E., Dickson W., Knowler W. C., Johannes R. S., 1988, in Proceedings of the annual symposium on computer application in medical care. p. 261

- Speagle (2020) Speagle J. S., 2020, MNRAS, 493, 3132

- Spurio Mancini et al. (2022) Spurio Mancini A., Piras D., Alsing J., Joachimi B., Hobson M. P., 2022, Monthly Notices of the Royal Astronomical Society, 511, 1771

- Spurio Mancini et al. (2023) Spurio Mancini A., Docherty M. M., Price M. A., McEwen J. D., 2023, RAS Techniques and Instruments, 2, 710–722

- Srinivasan et al. (2024) Srinivasan R., Crisostomi M., Trotta R., Barausse E., Breschi M., 2024, floZ: Evidence estimation from posterior samples with normalizing flows (arXiv:2404.12294)

- Torrado & Lewis (2019) Torrado J., Lewis A., 2019, Astrophysics Source Code Library, pp ascl–1910

- Trotta (2008) Trotta R., 2008, Contemporary Physics, 49, 71

- Williams (1959) Williams E. J., 1959, Regression analysis. Wiley, New York

- Williams et al. (2021) Williams M. J., Veitch J., Messenger C., 2021, Physical Review D, 103

- van Haasteren (2014) van Haasteren R., 2014, in , Gravitational Wave Detection and Data Analysis for Pulsar Timing Arrays. Springer, pp 99–120