A Weighted Multilevel Monte Carlo Method

Abstract

The Multilevel Monte Carlo (MLMC) method has been applied successfully in a wide range of settings since its first introduction by Giles [12]. When using only two levels, the method can be viewed as a kind of control-variate approach to reduce variance, as earlier proposed by Kebaier [18]. We introduce a generalization of the MLMC formulation by extending this control variate approach to any number of levels and deriving a recursive formula for computing the weights associated with the control variates and the optimal numbers of samples at the various levels.

We also show how the generalisation can also be applied to the multi-index MLMC method [16], at the cost of solving a -dimensional minimisation problem at each node when index dimensions are used.

The comparative performance of the weighted MLMC method is illustrated in a range of numerical settings. While the addition of weights does not change the asymptotic complexity of the method, the results show that significant efficiency improvements over the standard MLMC formulation are possible, particularly when the coarse level approximations are poorly correlated.

Keywords Monte Carlo Multilevel Monte Carlo Control Variates Stochastic Differential Equations

1 Introduction

The Multilevel Monte Carlo method targets a situation where the goal is to compute an expectation via Monte Carlo estimation, but where is either impossible or prohibitively expensive to sample directly. Instead, one has a sequence of approximations that may be sampled with a computational cost that increases with the index , with converging to as increases.

With single-level Monte Carlo estimate, the total error is controlled by choosing the level to ensure an acceptable bias, and increasing the number of samples to reduce the variance of the estimate. A typical scenario leads to a computational cost of in order to achieve an overall error of . The MLMC method offers a way to improve on this by combining the estimate at the finest level with differences of estimates at coarser levels, generating more samples at the coarser, cheaper, levels, and fewer at finer, more expensive levels. The result is a method with the bias of the finest level, but potentially much lower variance for a given computation effort, and an computational cost that can be as low as , matching the best-possible accuracy for Monte Carlo estimation (see, for instance, Theorem 2.1 of [13]).

The potential of the MLMC approach has lead to hundreds of papers dealing with refinements and generalisations of the original approach, along with a host of application areas. Giles [13] provided a comprehensive overview of the development of MLMC methods in the first few years following its first appearance in [12]. Generalisations included randomised MLMC [27] (for truly unbiased estimates), Multilevel quasi-Monte Carlo (qMLMC) [15], combinations of MLMC with Richardson extrapolation [21], and Multi-index MLMC [16] (for situations where there is more than one ‘scale’ that can be adjusted in the approximate samples, such as might arise in simulations of stochastic partial differential equations [25, 5, 26, 20, 24, 7]).

Other applications of MLMC and qMLMC include their use for estimation, uncertainty quantification, optimal control in the context of PDEs with random coefficients [8, 6, 1, 28, 19, 2, 23, 29]. They have also been applied in settings involving nested expectations[14], including Picard iterations for solving semilinar parabolic PDEs [33]. In recent years there have been some applications of MLMC method to Machine Learning and Deep Learning techniques, for instance [17] on uncertainty quantification, [30] for intractable distributions and [10] for variational inference frameworks.

In order to fix ideas here, we will focus on the applications of MLMC described in Giles’ original papers [12, 11], i.e. to option valuation for assets governed by one-dimensional stochastic differential equations (SDEs). To that end, suppose that an asset price is governed by a one-dimensional Itô diffusion

| (1) |

where is a standard Brownian motion under the pricing measure, and are given functions satisfying certain conditions, and the initial value is assumed to be given. We may wish to compute the value of a European (possibly path-dependent option with payoff , where denotes the path followed by over the interval , given a realisation of the Brownian motion on that interval. For example, a call option with strike price will have , while for an Asian put option we would have . The option value will be given by a discounted expected payoff (we assume a constant interest rate ), so that in this setting .

Approximate samples () for might arise from simple Euler-Maruyama discretisations of (1), with using steps and a constant time step (other discretisations, such as the Milstein discretisation, c.f. [11], can also be used). We define and, given the initial value , define the values of the discrete path via

| (2) |

where . For such a sequence, we can define a discrete payoff function that should correspond in an appropriate way to . (In the case of a call option, .) Then, if we have a sequence of grids with steps, , we can define .

A single-level Monte Carlo estimate for , using independent sample paths, will be formed as the average of the values of resulting from those paths, and we denote such an average .

Then , and the variance of is

The mean square error (MSE) associated with our approximation is then

| (3) |

It is well established (c.f. [4], for instance) that, provided , and the payoff function satisfy certain conditions, the Euler-Maruyama discretisation of (1) will have a weak order of convergence of 1, so that . Given that , the MSE will be . The total computational cost will be proportional to , and it is straightforward to show that, to achieve an MSE of while minimising the computational effort, we should have proportional to and proportional to , giving a total computational cost proportional to .

Some early steps toward reducing this computational complexity involved the use of approximations at two levels, with the coarser level approximation serving as a control variate. This was the approach taken by Kebaier [18], who proved that the the total cost can be reduced to through an appropriate combination of two estimators with time steps and . His work was an application of a more generally-applicable approach of quasi-control variates analysed by Emsermann and Simon [9]. Giles’ Multilevel Monte Carlo approach can in some cases reduce this cost to .

1.1 Multilevel Monte Carlo

The multilevel approach proposed by Giles [12] involves forming a geometric sequence of grids using time steps, for some integer (typically or ), and for . These grids are then used to construct basic estimators , and, for , , where is an estimate constructed on a grid with timestep , but using the same random samples as were used to compute . This can be done, for instance, by summing successive samples, so that, if , we can set , for and use these to compute a discrete path with timestep , which can then be used to compute .

In this way, we find that , for , and this means that a telescoping sum of Monte Carlo samples of the basic estimators, using samples for , i.e.

| (4) |

satisfies .

If we denote the computational effort needed to compute a single sample of by , and the standard deviation of by , then the computational effort required to compute is

and the variance of is given by

The minimal (square root) cost needed to achieve a variance of is

| (5) |

and this is achieved by setting

| (6) |

(This can be readily derived using a Lagrange multiplier approach.)

1.1.1 Complexity Theorem

The potential savings of the approach, and the circumstances under which they may be realised, are shown in the following theorem (c.f. Theorem 2.1 of [13]).

Theorem 1.1.

The conditions of the theorem constrain the rate of decay of the bias of and the standard deviation of the basic estimators and the rate of growth in the cost of sampling the estimators. In the ‘ideal’ case, where , we see that, for a given ,

Thus the cost is proportional to for any . We can thus set111Note that it is possible to optimise over the proportion of that is split between the error sources. and choose so that to satisfy the conditions of the theorem and verify its conclusions in this case.

1.1.2 Performance at the coarsest levels

While the asymptotic complexity of the MLMC method is an improvement over that of single-level Monte Carlo (in almost all cases), in practice, it may be optimal to reduce the number of coarsest levels used. In particular, unless the correlation between and is sufficiently high, it will be better to set level to be the coarsest level.

If we denote the correlation between and by , and the standard deviation of by , then we have, with the coarsest level,

If is the coarsest level, then . The total effort for an MLMC estimate starting from level will be lower than that for an estimate starting from unless

Moving the term to the right hand side, and squaring, we find that the condition becomes

where we have assumed a) that the cost of computing a sample of is similar to the cost of computing , and b) that .

As an example, if and , then the correlation needs to be above roughly in order for the level samples to add any benefit. Moreover, if in fact a sample of is more expensive to compute than a sample of , this lower bound will be higher.

2 Weighted Multilevel Monte Carlo (WMLMC)

Here we propose a generalisation of the standard MLMC method that involves rewriting the MLMC estimators as nested control variate estimators, and (in that spirit) adding weights. The impact of this is to enable more efficient use to be made of the coarsest level samples, especially when the correlation between the levels is relatively low, with potentially significant cost savings (although with no impact on the asymptotic order of complexity).

Recent work by Amri et al. [3] also takes a multilevel control variate point of view, although their approach differs from the method proposed here by using extrinsic surrogate estimators as control variates.

A weighted version of MLMC was also proposed in [21], where the possibility of adding weights in order to better control the bias was introduced. There a design matrix was used to define a general multilevel estimator. Several templates for were discussed (c.f. Section 3.32 and Section 5.1). However, a defining property of these design matrices was that their columns (apart from the first) should all sum to zero. The weighting scheme we propose here breaks that property; its goal is to improve the variance, rather than the bias.

2.1 A recursive formulation of MLMC

We start by showing that the MLMC estimators can be written recursively, which is possible because the ratio between successive numbers of samples is independent of the finest level . We define, for , (c.f. (5)), and set

| (7) |

(Note that , so that .) Then we can recursively define the multilevel estimators

| (8) | ||||

The fact that we use the same notation for these multilevel estimators as for the MLMC estimators defined in (4)–(6) is justified by the following lemma.

Lemma 2.1.

Proof.

2.1.1 MLMC and control variates

The final step of the recursion (8) can be expanded to give

| (12) |

The term in brackets has mean zero and can be seen to act as a control variate, correlated with the finest level single-level estimator . This can be continued at each level, so that the MLMC estimator can be seen as a nested sequence of control variates, each employed to reduce the variance of the finer level estimator.

At this point, we are naturally lead to consider adding weights to improve the efficiency of these control variates.

2.2 Adding weights

Given a set of weights , with , we define the estimators for our weighted multilevel Monte Carlo method (WMLMC) recursively.

| (13) | ||||

so that, here for , and the values of and , along with those of , will be determined so as to minimise the cost (for a given variance of ) of computing each .

We see that we can write

| (14) |

with, as before , and

| (15) |

If we try to optimise the values of and directly, we find that they satisfy a coupled system of nonlinear equations. It is possible ([31]) to solve these equations using a sweeping approach reminiscent of the Thomas algorithm for tridiagonal systems. However, it is more natural to use the recursive equations (13), and the resulting optimal values are provided in the Proposition 2.2 below.

We denote the cost of generating a sample of by , and the standard deviation of by , so that

| (16) | ||||

| (17) |

We will seek to determine optimal weights that minimise the cost of computing , for a given variance. We denote the resulting estimators by and , and the corresponding values of and by and , respectively.

Proposition 2.2.

The values for the weights and the effort parameters and that generate estimators with variance for the minimal cost satisfy the following equations, which may be solved recursively:

and, for , if ,

| (18) | ||||

| (19) | ||||

| (20) | ||||

| (21) |

and otherwise

| (22) |

Proof.

We start by supposing that we have an optimised estimator at level with variance and computational cost . From (13), for any given value of we have

The cost of computing is given by (16), and the variance of is given by

Minimising subject to (by means of a Lagrange multiplier, for example) gives us provisional versions of (20) and (21):

| (23) |

It remains to determine the value that minimises in (23). If , we can differentiate the expression for in (23), using (17), to obtain

We note that . If this is negative, and we will find a minimum of for some . Similarly, . If this is positive, and we will find a minimum of for some . Otherwise, the minimum of will occur when . In this case, we effectively make level our new coarsest level.

We summarize the resulting WMLMC estimator in the following corollary to Proposition 2.2, which is proven straightforwardly by induction.

Corollary 2.3.

To help us explore the implications of Proposition 2.2, we introduce notation for the normalised cost

| (29) |

which can be seen to be the ratio between and the (square root) single-level cost (again assuming222This assumption can be relaxed, adding a constant (say) that is the ratio of the cost of generating a sample of and the cost of generating a single-level sample . This complicates things a little but does not fundamentally change any of the results presented here. that the cost of generating a sample of is the same as the cost of generating a single-level sample , even when ).

Corollary 2.4.

We see immediately from (30) that the cost of the WMLMC estimator is bounded from above by the single level cost, so that , and that it is strictly lower than that cost whenever . Moreover, since each MLMC estimator is a particular case of the weighted estimator with each , the cost of the optimally weighted estimator will be no greater than the cost of the MLMC estimator. This implies that we can inherit the results of the MLMC Complexity Theorem (Theorem 1.1). Nevertheless, we now give a direct statement of the corresponding result for the optimally weighted MLMC method.

2.3 Complexity theorem

Lemma 2.5.

Proof.

From (30), we see immediately that

Then, since , and given that , we can deduce by induction that

The result follows. ∎

2.4 Comparison with MLMC

If we also define , then the MLMC analogue to (30) is

| (32) |

Given that the MLMC estimator is a special case of the weighted MLMC estimator (with ), it is necessarily true that . This can be verified to be the case directly using (30) and (32). Indeed, it is possible to show from these equations that, if , , with equality when only if

Note that, as , we expect that , and , so that we do not anticipate that adding (the optimal) weights will improve the asymptotic complexity of the method.

However, signficant gains are still possible in some settings, mainly because of the potential to make more efficient use of the low cost–high bias–low correlation samples at the coarser levels. To gain some insight into this, we consider the simplified situation where the single-level samples all have the same standard deviation , and we are working on a geometric grid with , i.e. . We suppose too that we are at the coarsest level, so that . Then, if ,

| (33) |

This highlights the comparison with the weighted version derived from (30). Again there are two terms, but the weighted version has an additional factor of multiplying the first term, and an additional factor of multiplying the second term, and can be applied for a wider range of values of .

The comparative costs can be seen in Figure 1, which shows and (from (33)) as functions of the correlation between and , for . The maximum ratio between these costs is , which occurs when . At this point, , and for lower values of the correlation, the single-level MC estimate (with a normalised cost of ) is more efficient than the two-level MLMC estimate.

In Figure 2 we show the three-level comparison in the form of the ratio between and , as a function of the two correlations and , between and and between and , respectively. Note that the potential efficiency savings are compounded, and are maximised when the correlations are close to .

3 Weighted Multi Index Multilevel Monte Carlo

In this section we show that a weighted version of the multi-index multilevel Monte Carlo (MIMC) formulation introduced by [16] can also be formulated. In order to do so, we review the MIMC method and show that it can be written in a recursive form, and weights added.

Our goal is to estimate a quantity via a set of approximate estimators indexed by multi-indices333For a d-dimensional multi-index , we define . For two multi-indices and , we say that if , , and if and . We also define to be the multi-index with th entry , and we define similarly. We also define subsets and . . These have means , with as .

A single-level estimator for will be denoted by . Whenever a sample of is computed, we also compute , a collection of estimators for the lower index quantities , but computed from the same underlying random variable(s). These are collected into basic estimators

where . We denote the computational effort needed to compute one sample of by , and by the variance of .

A multilevel estimator at level is then constructed from the basic estimators in the form

| (34) |

where denotes the average of independent samples of . It is straightforward444We note that and that the term in brackets is zero unless , in which case the sum inside the bracket is empty and we are left with . to verify that , and that, since the are computed independently of one another, . The total computational effort required to compute is .

We set a target variance for of , and seek to find the least computationally expensive way of achieving that. Minimising , subject to , results in

| (35) |

3.1 A recursive formulation

As we saw in the single-index case, the first step to formulating a weighted version of the method is to write it in recursive form. To wit, we have the following proposition.

Proposition 3.1.

Proof.

Adding weights

As in the single-index case, we define weighted versions of the multilevel estimators. We start with local weights for , which we take to be given (for the moment), and we define

| (37) |

and

| (38) |

where the effort parameters and are to be chosen to minimise the effort required to compute subject to .

We are going to look to expand (38) as a collection of basic estimators . Doing this will generate sums of products of the weights . We denote these by for , which we define recursively:

| (39) |

Intuitively, is the sum of products of the weights along all possible paths from to . The definition above can be used to recursively define these sums of products, starting from .

We can now expand (38), as follows.

Proposition 3.2.

Suppose that the estimates satisfy the recurrence relation (38) for . Then we may write

| (40) |

Proof.

Note that the estimators on the right hand side of (38) are combined in such a way as to ensure that the number of samples of to be computed is consistently defined. Thus at each node , can be computed, independently of the values at other nodes, using samples555In practice, of course, the number of samples is rounded to the nearest positive integer. of .

The work required to compute is

| (41) |

and, from (40),

| (42) |

When , we can minimise subject to by setting . For , we assume that and have been determined for all , and we choose and so as to minimise subject to . This results in

| (43) |

Note here that the original MIMC method of [16] corresponds in this context to taking .

It remains to determine the optimal weights . We have, by definition, . We suppose, inductively, that the values of have been determined for all . We may then expand, from (42) and using (39),

| (44) |

We can write this more succinctly in vector form. We introduce the vectors , , allowing us to write

| (45) |

We can also express

| (46) |

where , , and .

We can now define the optimal to be the value that minimises

| (47) |

It is not, in general, going to be possible to express the optimal value explicitly, and hence we have no explicit expressions for the corresponding optimal values , , , etc. Given estimates for the covariance matrices , they are, however, readily computable by means of the following sequence of steps, which is continued until , and have been found for all , where is the highest index at which an estimate is required (c.f. (34)).

-

•

Initialise the computation by setting , , .

- •

4 Numerical experiments

In this section we illustrate the performance of the (optimally) weighted (single-index) MLMC method in comparison to MLMC. The implementation of the weighted MIMC method, as well as its performance in a range of settings, will be explored in a subsequent paper (see also [22]).

For the results shown in Figures 3–7, the covariances, means, optimal weights, etc. were calculated using samples at each level. When using the methods in practice, the number of samples used would be smaller, and an algorithm along the lines of Algorithm 1 of [13] would be used. In Figure 8 we illustrate numerical results from using such an algorithm, with an initial samples used at each level to estimate the covariances.

The experiments in this section are based on European option valuation, with three stochastic models (c.f. (1)) with and as shown in Table 1. We employ two discrete approximations: Euler-Maruyama (2) and Milstein (48):

| (48) |

We also consider three payoff functions, listed in Table 2, where we show the discrete forms. In the experiments shown here, we form each of our samples using antithetic variates, so that each SDE path is recomputed using Brownian increments with the opposite sign, the payoffs are computed and the results averaged. We note that, for the Asian payoff, we employ an interpolation-based formula for the intermediate values for , as described in Section 5 of [13]. In Figure 7 we show the results for a digital payoff, and note that here we use the naive implementation (without the payoff smoothing technique described in [13]). Our purpose here is to illustrate the relative gains possible when adding weights for situations where such smoothing may not be available.

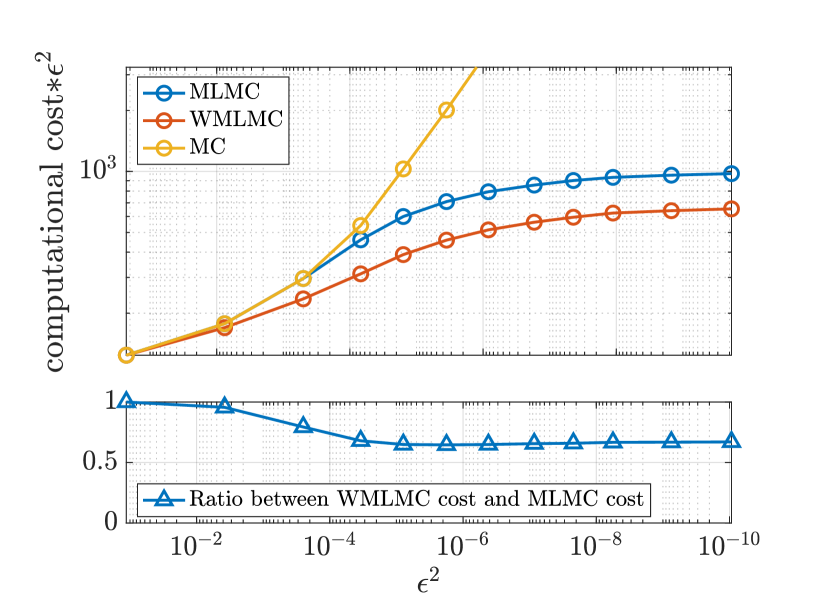

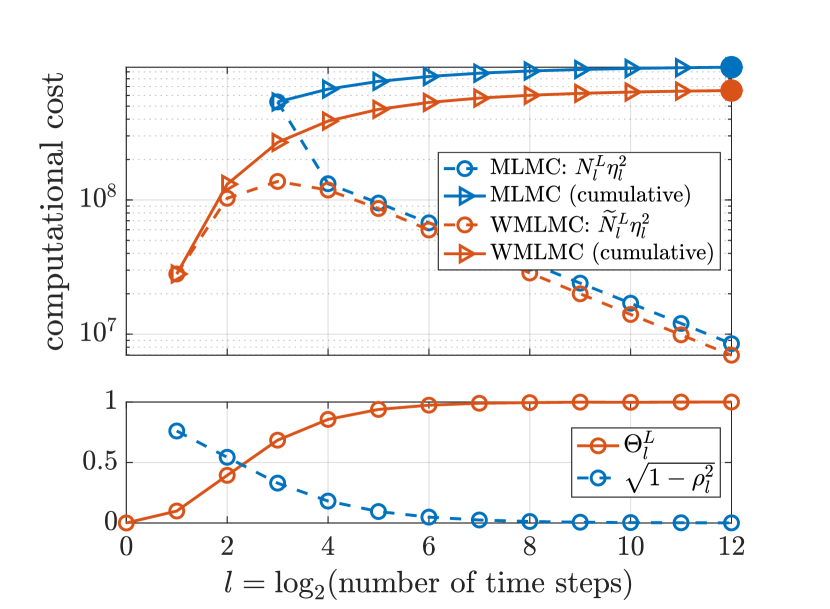

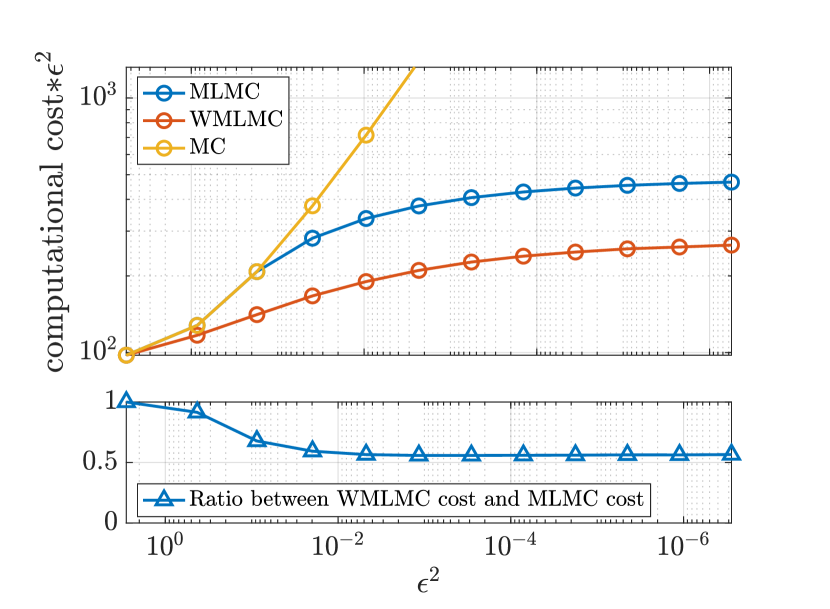

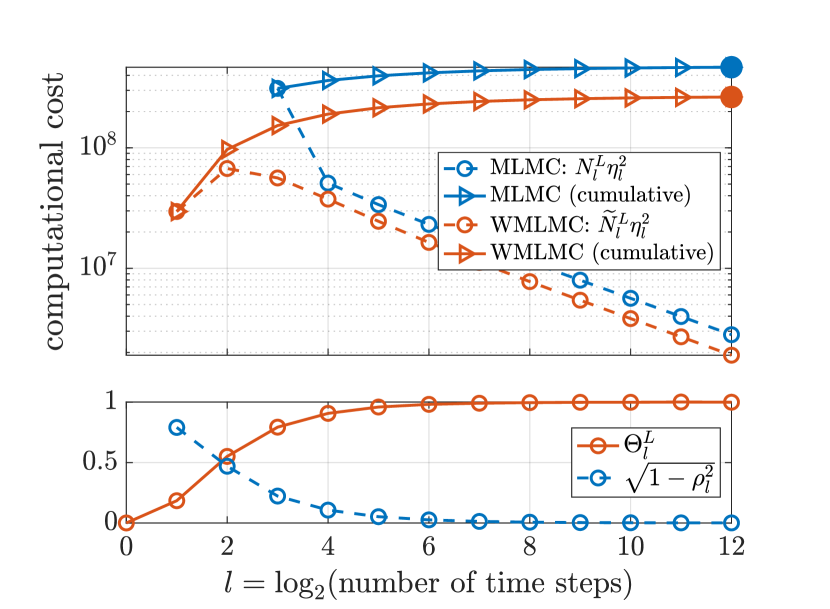

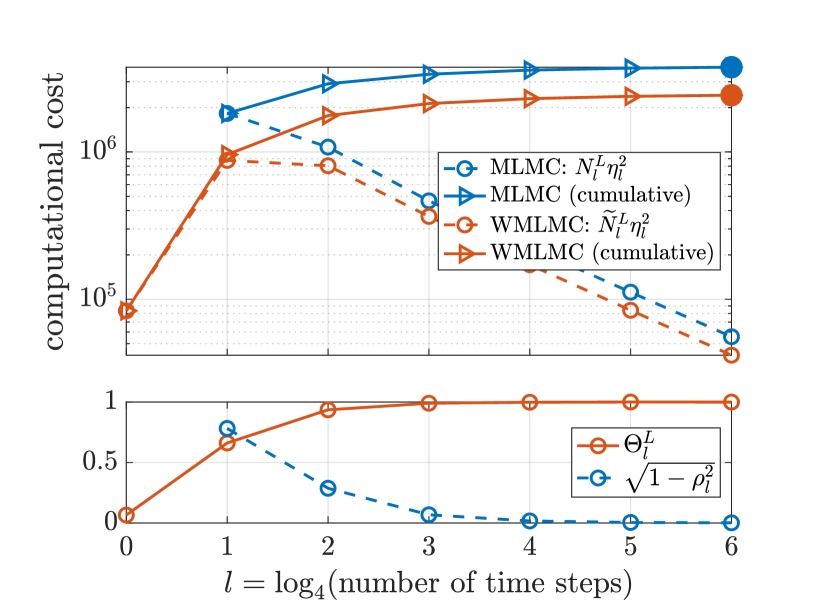

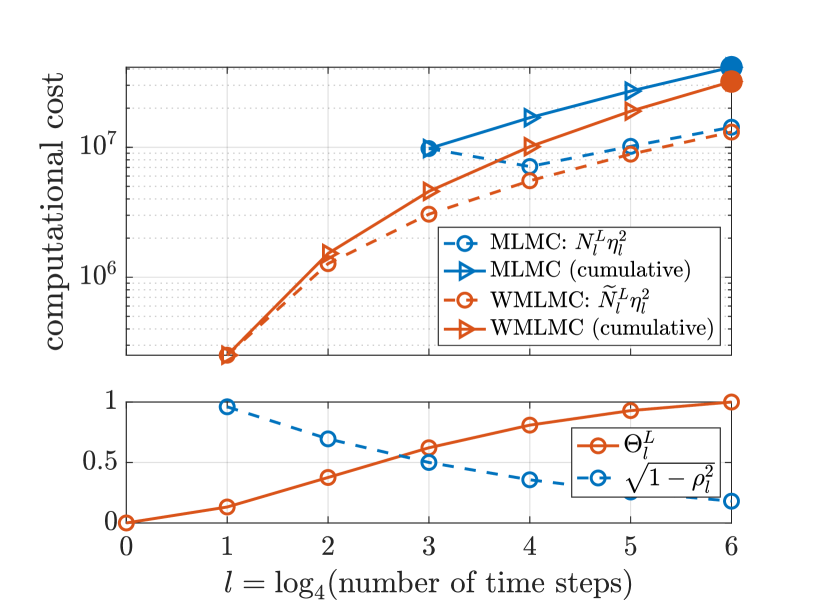

In each of Figures 3–7 we show four graphs. On the left hand side of each figure we show the computational cost (calculated as multiples of the cost of a single sample at level ) multiplied by the MSE, as a function of the MSE. The costs for MLMC, WMLMC and single-level MC estimates are shown in the upper figure, while the lower figure shows the ratio between the WMLMC cost and the MLMC cost. On the right hand side of each figure we show the contributions from levels to the total cost of MLMC and WMLMC estimates at level , with the total variance being . The cumulative sums of these costs are also shown, marked by triangles, leading to the total costs indicated by solid circles. The bottom right hand graphs show the correlations666Strictly speaking, the values of are shown, rather than the correlations themselves. between and , and also the values of used for WMLMC.

SDE Drift and volatility GBM , IGBM , CIR ,

Payoff Discrete form Call: Asian: Digital:

(a)

(a)

(b)

(b)

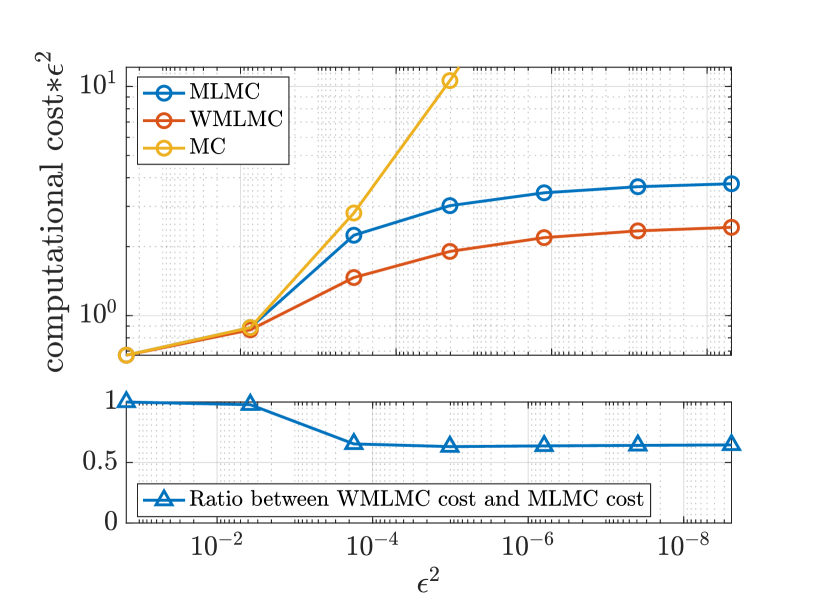

The first results we show in Figure 3 serves to show that the WMLMC method does not always offer a measurable improvement over MLMC. In this case, we are evaluating a European call option under GBM with a Euler-Maruyama discretisation, with . Note here that the ratio between the MLMC and WMLMC costs shown in the bottom left hand graph is almost exactly 1.

(a)

(a)

(b)

(b)

In Figure 4 we show results for the evaluation of an Asian call option under GBM, with the Milstein discretisation. Again . This time, however, the correlations between the levels take a while to approach 1. This means, in particular, that for MLMC, it is optimal to take to be the coarsest level (forcing MLMC to use all the levels would result in higher overall cost). In contrast, WMLMC is able to take advantage of coarser-level estimates, with being the optimal choice of coarsest level. The effect of this can be seen in the left-hand graphs, which show that, by the time MLMC starts to differ from MC (at level , with a MSE of just below ), WMLMC has already started to make some efficiency gains. These then persist as the MSE decreases, leading to an eventual WMLMC cost of about 2/3 the MLMC cost.

(a)

(a)

(b)

(b)

Figure 5 shows results for a call option under IGBM, with a Milstein discretisation, and again . Here the complexity is for both MLMC and WMLMC. However, as in the previous example, WMLMC is able to make efficient use of coarser estimates than is possible for MLMC, resulting in the cost of WMLMC being less than of the MLMC cost.

(a)

(a)

(b)

(b)

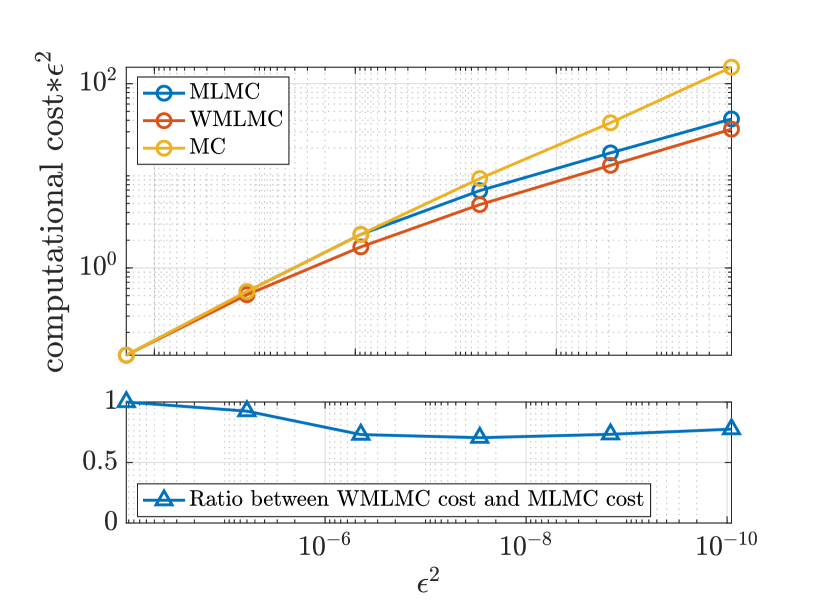

The next experiment involves the CIR process with a Milstein discretisation, and the results are shown in Figure 6. The payoff is a European call, and we take . In this case, and and so the asymtotic complexity is . As in the previous experiments where this is the case, it shows up in the exponential decrease in level-wise costs in the top right figure, and in the levelling-off of the MLMC and WMLMC costs in the top left figure. Here both MLMC and WMLMC start to make gains over single-level MC estimates at . However, the correlation is still relatively far away from 1 at this point, and the choice of optimal weights in WMLMC generates much more significant gains, so that the overall cost ends up being just under of the MLMC cost.

(a)

(a)

(b)

(b)

In Figure 7, we illustrate a situation where the gains from MLMC (and WMLMC) are relatively small. This can be seen to occur with a naive implementation of a digital option payoff (as a result of the discontinuity in the payoff). We show results for an Euler Maruyama discretisation of GBM, with . Here again WMLMC is able to take some advantage of coarse estimates with low correlations, and the cost is around of the MLMC cost.

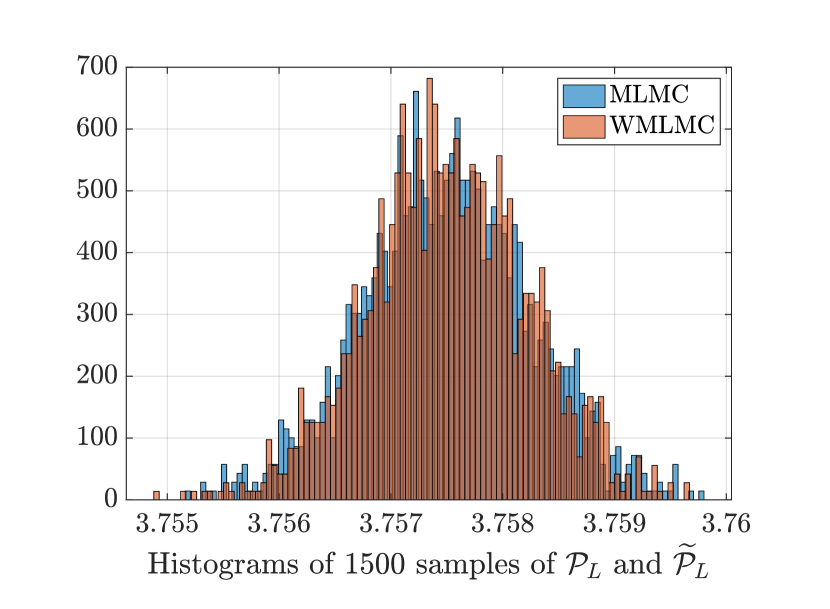

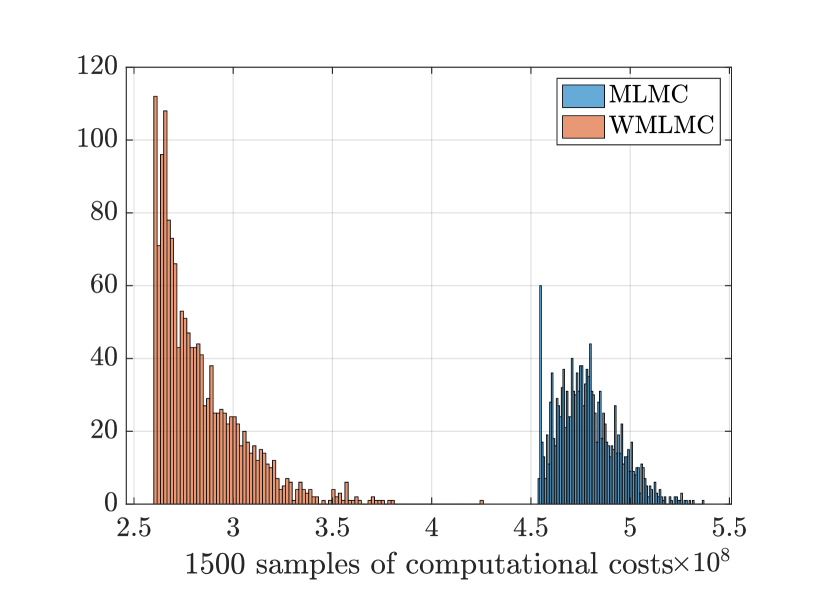

In order to illustrate the potential performance of the MLML and WMLMC methods, the experiements so far have been run under ‘ideal’ conditions, using samples at each level, so that we have been able to compute the variances, correlations and associated values of and , etc. with very little uncertainty. As mentioned at the beginning of this section, in practice an algorithm along the lines of Algorithm 1 of [13]. For our final experiment, we implemented such an algorithm 1000 times on the IGBM call option valuation with Milstein discretisation and antithetic variates, using an initial 20 samples at each level (to generate initial estimates of the bias, covariance and correlation). The target MSE was , and we aimed to split the error evenly between the contributions from the bias and from the variance. In Figure 8 we show histograms of the resulting MLMC and WMLMC estimates (left) along with histograms of the computational effort required (i.e. ; the value of determined by the algorithm was either or , depending on the run). The average costs were for MLMC, and for WMLMC, a ratio of about 1.69 (only slightly less than the value of 1.77 obtained under idealised conditions, as shown in Figure 5). The MSE values, estimated from (3) using a value for computed using WMLMC with a target MSE of , were for MLMC and for WMLMC.

(a)

(a)

(b)

(b)

5 Discussion

The addition of weights to the standard MLMC (or MIMC) approach is based on viewing the multilevel estimator as a nested sequence, with each estimator in the sequence using a lower-level multilevel estimator as a control variate. The computation of the optimal weights creates some additional overhead cost, but this is marginal, and so the efficiency savings essentially come ‘for free’.

As mentioned in the introduction to Section 4, a weighted MLMC approach was proposed in [21]. The weights there are used to improve the bias, rather than the variance, and can be seen as complementary to the weights used here. Indeed, the two approaches can be combined, and the potential gains from this combination are explored in [22].

The extension to the multi-index case has been outlined here in the case where the set of indices is in tensor product form. Initial experiments in this setting [32] indicate that the potential gains in efficiency are even higher than in the single-index case. Future work will explore this more fully (see also [22]), along with extensions to a weighted version of the non tensor-product MIMC implementation.

Acknowledgments

We acknowledge the support of the Natural Sciences and Engineering Research Council of Canada (NSERC).

Nous remercions le Conseil de recherches en sciences naturelles et en génie du Canada (CRSNG) de son soutien.

References

- [1] A. Abdulle, A. Barth, and C. Schwab. Multilevel Monte Carlo methods for stochastic elliptic multiscale PDEs. Multiscale Modeling & Simulation, 11(4):1033–1070, 2013.

- [2] A. A. Ali, E. Ullmann, and M. Hinze. Multilevel Monte Carlo analysis for optimal control of elliptic PDEs with random coefficients. SIAM/ASA Journal on Uncertainty Quantification, 5(1):466–492, 2017.

- [3] M. R. E. Amri, P. Mycek, S. Ricci, and M. De Lozzo. Multilevel surrogate-based control variates. arXiv preprint arXiv:2306.10800, 2023.

- [4] V. Bally and D. Talay. The Euler scheme for stochastic differential equations: error analysis with Malliavin calculus. Mathematics and Computers in Simulation, 38(1-3):35–41, 1995.

- [5] A. Barth and A. Lang. Multilevel Monte Carlo method with applications to stochastic partial differential equations. International Journal of Computer Mathematics, 89(18):2479–2498, 2012.

- [6] A. Barth, C. Schwab, and N. Zollinger. Multi-level Monte Carlo finite element method for elliptic PDEs with stochastic coefficients. Numerische Mathematik, 119:123–161, 2011.

- [7] N. K. Chada, H. Hoel, A. Jasra, and G. E. Zouraris. Improved efficiency of multilevel Monte Carlo for stochastic PDE through strong pairwise coupling. Journal of Scientific Computing, 93(3):62, 2022.

- [8] K. A. Cliffe, M. B. Giles, R. Scheichl, and A. L. Teckentrup. Multilevel Monte Carlo methods and applications to elliptic PDEs with random coefficients. Computing and Visualization in Science, 14:3–15, 2011.

- [9] M. Emsermann and B. Simon. Improving simulation efficiency with quasi control variates. Stochastic Models, 18(3):425–448, 2002.

- [10] M. Fujisawa and I. Sato. Multilevel Monte Carlo variational inference. The Journal of Machine Learning Research, 22(1):12741–12784, 2021.

- [11] M. B. Giles. Improved multilevel Monte Carlo convergence using the Milstein scheme. In Monte Carlo and Quasi-Monte Carlo Methods 2006, pages 343–358. Springer-Verlag, 2008.

- [12] M. B. Giles. Multilevel Monte Carlo path simulation. Operations Research-Baltimore, 56(3):607–617, 2008.

- [13] M. B. Giles. Multilevel Monte Carlo methods. Acta Numerica, 24:259–328, 2015.

- [14] M. B. Giles. MLMC for nested expectations. Contemporary computational mathematics-A celebration of the 80th birthday of Ian Sloan, pages 425–442, 2018.

- [15] M. B. Giles and B. J. Waterhouse. Multilevel quasi-Monte Carlo path simulation. Advanced Financial Modelling, Radon Series on Computational and Applied Mathematics, 8:165–181, 2009.

- [16] A. L. Haji-Ali, F. Nobile, and R. Tempone. Multi-index Monte Carlo: when sparsity meets sampling. Numerische Mathematik, 4(132):767–806, 2015.

- [17] N. K. Jabarullah Khan and A. H. Elsheikh. A machine learning based hybrid multi-fidelity multi-level Monte Carlo method for uncertainty quantification. Frontiers in Environmental Science, 7:105, 2019.

- [18] A. Kebaier. Statistical Romberg extrapolation: a new variance reduction method and applications to option pricing. The Annals of Applied Probability, 15(4):2681–2705, 2005.

- [19] F. Y. Kuo, C. Schwab, and I. H. Sloan. Multi-level quasi-Monte Carlo finite element methods for a class of elliptic PDEs with random coefficients. Foundations of Computational Mathematics, 15:411–449, 2015.

- [20] A. Lang and A. Petersson. Monte Carlo versus multilevel Monte Carlo in weak error simulations of SPDE approximations. Mathematics and Computers in Simulation, 143:99–113, 2018.

- [21] V. Lemaire and G. Pagès. Multilevel Richardson-Romberg extrapolation. Bernoulli, 23(4A):2643–2692, 2017.

- [22] Y. Li. A weighted multilevel Monte Carlo method. PhD thesis, University of Calgary, in preparation.

- [23] Y. Luo and Z. Wang. A multilevel Monte Carlo ensemble scheme for random parabolic pdes. SIAM Journal on Scientific Computing, 41(1):A622–A642, 2019.

- [24] A. Petersson. Rapid covariance-based sampling of linear SPDE approximations in the multilevel Monte Carlo method. In Monte Carlo and Quasi-Monte Carlo Methods: MCQMC 2018, Rennes, France, July 1–6, pages 423–443. Springer, 2020.

- [25] C. Reisinger and M. Giles. Stochastic finite differences and multilevel Monte Carlo for a class of SPDEs in finance. SIAM Journal on Financial Mathematics, 3(1):572–592, 2012.

- [26] C. Reisinger and Z. Wang. Analysis of Multi-Index Monte Carlo estimators for a Zakai SPDE. Journal of Computational Mathematics, 36(2):202–236, 2018.

- [27] C.-h. Rhee and P. W. Glynn. A new approach to unbiased estimation for SDEs. In Proceedings of the 2012 Winter Simulation Conference (WSC), pages 1–7. IEEE, 2012.

- [28] A. L. Teckentrup, R. Scheichl, M. B. Giles, and E. Ullmann. Further analysis of multilevel Monte Carlo methods for elliptic PDEs with random coefficients. Numerische Mathematik, 125:569–600, 2013.

- [29] A. Van Barel and S. Vandewalle. Robust optimization of PDEs with random coefficients using a multilevel monte carlo method. SIAM/ASA Journal on Uncertainty Quantification, 7(1):174–202, 2019.

- [30] T. Wang and G. Wang. Unbiased Multilevel Monte Carlo methods for intractable distributions: MLMC meets MCMC. Journal of Machine Learning Research, 24(249):1–40, 2023.

- [31] A. Ware and Y. Li. A generalised multilevel Monte Carlo method. Presented at the 2021 CAIMS Annual Meeting, June 2021.

- [32] A. Ware and Y. Li. Weighted multilevel Monte Carlo. Presented at the International Conference on Computational Finance, April 2024.

- [33] E. Weinan, M. Hutzenthaler, A. Jentzen, and T. Kruse. Multilevel Picard iterations for solving smooth semilinear parabolic heat equations. Partial Differential Equations and Applications, 2(6):80, 2021.