Fourier-Laplace transforms in polynomial Ornstein-Uhlenbeck volatility models

Abstract

We consider the Fourier-Laplace transforms of a broad class of polynomial Ornstein-Uhlenbeck (OU) volatility models, including the well-known Stein-Stein, Schöbel-Zhu, one-factor Bergomi, and the recently introduced Quintic OU models motivated by the SPX-VIX joint calibration problem. We show the connection between the joint Fourier-Laplace functional of the log-price and the integrated variance, and the solution of an infinite dimensional Riccati equation. Next, under some non-vanishing conditions of the Fourier-Laplace transforms, we establish an existence result for such Riccati equation and we provide a discretized approximation of the joint characteristic functional that is exponentially entire. On the practical side, we develop a numerical scheme to solve the stiff infinite dimensional Riccati equations and demonstrate the efficiency and accuracy of the scheme for pricing SPX options and volatility swaps using Fourier and Laplace inversions, with specific examples of the Quintic OU and the one-factor Bergomi models and their calibration to real market data.

- JEL Classification:

-

G13, C63, G10.

- Keywords:

-

Stochastic volatility, Derivative pricing, Fourier methods, Riccati equations, SPX-VIX calibration

1 Introduction

Fourier inversion techniques hold a pivotal role in stochastic volatility modeling, particularly in the context of option pricing and hedging (Andersen and Andreasen [8], Carr and Madan [10], Eberlein, Glau, and Papapantoleon [16], Fang and Oosterlee [19], Lewis [26], Lipton [27]). They offer the dual advantage of significantly reducing computational time while maintaining a remarkable degree of accuracy, especially when compared to standard Monte Carlo methods. When it comes to model calibration, the applicability of Fourier methods is paramount, as thousands of derivatives across various maturities and strikes need to be evaluated simultaneously in real time.

Despite their numerical advantage, Fourier techniques have traditionally been confined to specific continuous stochastic volatility models where the characteristic function of the log-price is known in (semi)-closed form. These models usually exhibit Markovian affine structures in the sense of Duffie, Filipović, and Schachermayer [14] such as the renowned Heston [24], Stein-Stein [32] and Schöbel-Zhu [30] models, together with some of their non-Markovian Volterra counterparts (Abi Jaber [1, 2], Abi Jaber, Larsson, and Pulido [5], Cuchiero and Teichmann [11], El Euch and Rosenbaum [18], Gatheral and Keller-Ressel [22]). The key ingredient in all these models is to compute the characteristic function of the log-price by solving a specific system of deterministic Riccati equation.

More recently, Fourier techniques have also found applications in Signature volatility models in Abi Jaber and Gérard [3] and Cuchiero, Gazzani, Möller, and Svaluto-Ferro [12], where the volatility process is modeled as a linear functional of the path-signature of semi-martingales (e.g. a Brownian motion). In such models, certain characteristic functionals have been related to non-standard infinite dimensional system of Riccati ordinary differential equation (ODE). However, there exists no general theory regarding the existence of solutions for such equations, except for the specific result in Cuchiero, Svaluto-Ferro, and Teichmann [13, Proposition 6.2] which provides the existence of a solution to the infinite dimensional ODE for the case of the characteristic function of powers of a single Brownian motion modulo a non-vanishing condition of the characteristic function. The primary challenge comes from the intricate questions on analyticity of the logarithm of the characteristic function. Furthermore, numerically solving these equations poses challenges due to their stiffness and complexity. This forms our primary motivation: to establish theoretical results within a specific framework for a larger class of Riccati equations related to integrated quantities of power series of Ornstein-Uhlenbeck processes and to develop more suitable numerical schemes.

We demonstrate that Fourier techniques can be effectively extended to a broad class of flexible models previously considered infeasible as they fall beyond the conventional class of affine diffusions, including the celebrated one-factor Bergomi model (Bergomi [9], Dupire [15]) that has been shown to fit well to the SPX smiles and the recently introduced Quintic Ornstein-Uhlenbeck (OU) model of Abi Jaber, Illand, and Li [7], which has demonstrated remarkable capabilities in fitting jointly the SPX-VIX volatility surface for maturities between one week to three months supported by extensive empirical studies on more than 10 years of data in Abi Jaber and Li [4], Abi Jaber, Illand, and Li [6].

We refer to the class of models covered in this paper as the class of polynomial OU models, where the volatility of the log-price, denoted by , is defined as a power series of an Ornstein-Uhlenbeck process. Our three main theoretical results regarding the joint Fourier-Laplace functional of the log-price and integrated variance process are:

-

(i)

A verification result on the expression of the joint Fourier-Laplace functional in terms of a solution to an infinite dimensional system of Riccati ODE in Theorem 3.2,

-

(ii)

The existence of a solution to such a system of ODE modulo a non-vanishing condition of the joint characteristic functional in Theorem 3.5,

-

(iii)

An approximation procedure for the joint Fourier-Laplace functional in terms of exponentially entire expressions in Theorem 3.13.

On the practical side, we devise a numerical scheme to solve this system of infinite dimensional (stiff) Riccati equations making the application of Fourier pricing for models such as the one-factor Bergomi and the quintic OU models usable in practice. We demonstrate the efficiency and accuracy of the scheme for pricing SPX options and volatility swaps using Fourier and Laplace inversions. We also successfully calibrate using Fourier techniques the Quintic OU and the one-factor Bergomi models on real market data to highlight the stability and robustness of our numerical method across a wide range of realistic parameters values. We provide a Python notebook implementation here: https://colab.research.google.com/drive/1VCVyN1qQmLgOWjOy4fbWftyDqEQdm5n5?usp=sharing.

The paper is organised as follows: in Section 2, we introduce the class of polynomial OU volatility models. In Section 3, we present our three main theoretical results. In Section 4, we design a numerical scheme for solving the infinite dimensional Riccati ODE and test our scheme on pricing SPX vanilla options and volatility swaps for the one-factor Bergomi and quintic OU volatility models of various maturities and calibrate both models using real market data. Proofs of theorems discussed in Section 3 are collected in Section 5 onwards.

Notations. For a power series , we denote by the coefficients of , i.e. . We denote by the absolute power series of , i.e. . We remark that . It is well-known that if and have an infinite radius of convergence, then also has an infinite radius of convergence, with . Unless stated otherwise, we will assume that all power series in this paper have infinite radius of convergence. Moreover, we specify that the term continuity means joint continuity when applied to a function taking as variables. For example, a function is in if all its space derivatives in exist and are continuous in . We also adopt the following notations for the partial derivatives: when they exist. We say that a function is (real)-entire on , if it is equal to a power series (with infinite radius of convergence), that is for all , We say that it is (complex)-entire when is replaced by . Clearly, any real-entire function admits a complex-entire extension. When there is no-ambiguity, we will simply use the word entire. We say that a function does not vanish if it is non-zero at each point of its domain.

2 Polynomial Ornstein-Uhlenbeck volatility models

We consider the class of polynomial Ornstein-Uhlenbeck (OU) models for a stock price with the stochastic volatility process expressed as a power series of an OU process :

| (2.1) | ||||

with , , and . Here is a two-dimensional Brownian motion on a risk-neutral filtered probability space satisfying the usual conditions. The deterministic bounded input curve allows the model to match certain term structures of volatility, e.g. the forward variance curve since we have for :

| (2.2) |

The real-valued coefficients are such that the power series has infinite radius of convergence, i.e. for all and so that the stochastic integral is well-defined. This is the case for instance when is a finite polynomial or the exponential function. These two specifications already provide several interesting models used in practice:

- •

- •

-

•

Quintic OU model [7]: .

We will consider the following class of power series for which .

Definition 2.1.

A power series is said to be negligible to double factorial if the power series has an infinite radius of convergence, i.e.

with the convention .

By Definition 2.1, a power series negligible to double factorial also has infinite radius of convergence. This allows us to show that our class of polynomial Ornstein-Uhlenbeck volatility models (2.1) is well-posed in Proposition 2.3. For this we need a simple lemma about the absolute power series which will be useful later.

Lemma 2.2.

_

-

(i)

for all , and is monotonically increasing on ;

-

(ii)

for all ,

Proof.

is obvious; for , it suffices to notice that . ∎

Proposition 2.3.

Let be a measurable and bounded function. Let be a power series with infinite radius of convergence such that is negligible to double factorial. Then,

| (2.3) |

so that the stochastic integral , with , is well-defined and

| (2.4) |

is the unique strong solution to (2.1).

Proof.

Under (2.3), it is straightforward to obtain that the unique strong solution to (2.1) is given by (2.4). It suffices to prove (2.3). For this, we note that the explicit solution of is given by

| (2.5) |

We set , which is a deterministic continuous function of , and , which is a Gaussian random variable for . Applying Lemma 2.2 yields

| (2.6) | ||||

| (2.7) |

and since with bounded in , there exists a constant such that

| (2.8) |

By assumption, has an infinite radius of convergence, then so does , therefore

| (2.9) |

and thus we only need to prove

The random variable is Gaussian with bounded variance in , so there exists a constant such that for all , where is a standard normal variable. Given , hence

since is negligible to double factorial. This completes the proof. ∎

Remark 2.4.

Example 2.5.

Polynomials of finite degree (e.g. the Stein-Stein and the Quintic OU models) and the exponential function (e.g. the one-factor Bergomi model) are clearly negligible to double factorial. For the exponential function , it suffices to observe that . However, the function is not negligible to double factorial. Indeed, . In particular, if , then the expectation of does not exist for all .

3 The joint Fourier-Laplace transform

Our goal is to compute the joint Fourier-Laplace transform of the log-price and integrated variance

for some complex-valued functions .

Remark 3.1.

If are measurable functions , such that , and is negligible to double factorial, then the exponential above exists and with modulus of at most , so that the conditional expectation is well-defined.

It follows from the Markov property of that the above conditional expectation can be reduced to computing the deterministic measurable function given by

| (3.1) |

We will present three main results related to the computation of the characteristic functional in (3.1). The first result can be seen as a verification result and uncovers an affine structure in infinite dimension in terms of the powers by making a connection with infinite dimensional Riccati deterministic equations (Theorem 3.2 and Corollary 3.6). The second result is concerned with the existence of a solution to the infinite dimensional Riccati deterministic equation (Theorem 3.5). The last result provides an approximation procedure for obtaining the characteristic functional (Theorem 3.13).

3.1 A verification result

Our first main result uncovers an affine structure in infinite dimension expressed in powers and makes a connection with the following system of infinite dimensional deterministic Riccati equations:

| (3.2) | ||||

| (3.3) | ||||

| (3.4) | ||||

| (3.6) |

Theorem 3.2.

Let , be measurable and bounded functions. Let be a power series with infinite radius of convergence such that is negligible to double factorial. Assume that there exists a continuously differentiable solution to the system of infinite dimensional Riccati equations (3.6) such that the power series has an infinite radius of convergence. Define the process

| (3.7) |

Then the process is a local martingale. If in addition is a true martingale, then the following expression holds for the joint characteristic functional given in (3.1):

| (3.8) |

Proof.

The proof is given in Section 5. ∎

Remark 3.3.

Theorem 3.2 is in the spirit of [13, Theorem 5.5] which provides a similar verification result for the characteristic function of (real)-entire functions of solutions to stochastic differential equations with (real)-entire coefficients. Contrary to [13, Theorem 5.5], Theorem 3.2 deals with time-integrated quantities.

A possible strategy for obtaining the representation (3.8) would involve verifying the assumptions outlined in Theorem 3.2. These assumptions include ensuring the existence of a solution for the system of Riccati equations (3.4)-(3.6), such that the power series has infinite radius of convergence; together with proving that the local martingale is a true martingale. The latter can typically be achieved by arguing, for instance, that to obtain that is uniformly bounded by whenever are purely imaginary for instance.

In the specific case of the Stein-Stein model, i.e. when is an affine function, these assumptions are comparatively easier to confirm, as highlighted in the next example.

Example 3.4.

In the case of the classical Stein-Stein model [32], the volatility process process is defined as:

This is equivalent to (2.1) by setting and for . Notice the convolution term for and zero otherwise. In this case, the infinite dimensional Riccati equations (3.6)-(3.4) reduce to the following:

| (3.9) | ||||

| (3.10) | ||||

| (3.11) | ||||

| (3.12) | ||||

| (3.14) | ||||

| (3.15) |

which is a system of standard finite-dimensional Riccati equations whose existence is well-known whenever are such that

Hence the characteristic functional of the classical Stein-Stein model is affine in :

| (3.16) |

for which and can even be solved explicitly when and are constants, see [28].

Obtaining the representation (3.8) under the Stein-Stein model can be attributed to the finite number of terms, i.e. of the Riccati equations, involved in the sum. However, when dealing with an infinite sum, a notable challenge arises in proving that the log of the characteristic functional is entire in the variable on . In Section 3.2, we show how to generate a solution for the system of infinite-dimensional Riccati equations modulo a non-vanishing condition of . In Section 3.3, we provide an expression for the characteristic functional using approximation arguments where the approximations are entire functions thanks to the Gaussianity of the process .

3.2 Existence for the Riccati equations

Our second main result generates a solution to the infinite dimensional system of Riccati equations (3.4)-(3.6) by differentiating the logarithm of the characteristic functional :

This requires the logarithm of a complex-valued function, see Appendix B for its precise definition.

Theorem 3.5.

Fix , continuously differentiable such that and . Let be a power series negligible to double factorial. Then, in (3.1) is well-defined for any , and is continuous. If in addition does not vanish on , then can be defined as in Definition B.5. Furthermore, is in and in . In particular, the family of functions

| (3.17) |

Proof.

The proof is given in Section 6. ∎

Theorem 3.5 establishes the existence of a solution to the Riccati ODEs (3.4)-(3.6) when the coefficients are real as shown in the following corollary.

Corollary 3.6.

Proof.

Remark 3.7.

Theorem 3.5 is in the spirit of [13, Proposition 6.2], which provides the existence of a solution to the infinite dimensional ODE for the case of the characteristic function of powers of a single Brownian motion modulo similar assumptions. In contrast, Theorem 3.5 deals with more involved time-integrated quantities which requires a more delicate analysis.

Although Theorem 3.5 does not establish that is entire, its analyticity can be inferred from the properties of solutions to parabolic partial differential equations (PDEs).

Remark 3.8.

In order to prove Theorem 3.5, we establish the following PDE for in Theorem of 6.11:

where are continuous and are analytic functions. Following [17, Theorem 6.2 in Section II.2.], given that functions are continuous in , are bounded, Hölder continuous and analytic in variable within any open bounded set of , one would obtain that is analytic. Notice that is also analytic, then so is . Since analyticity is a local property, if does not vanish, then is also analytic. Therefore, we can deduce a local representation: for any , there exists such that

where the are defined by (3.17). In our case, both and are not only analytic but also entire. Extending the proof of analyticity using PDE techniques to establish that is entire might be possible, and that will lead to a global representation as in (3.8). However, this needs a more delicate analysis at the PDE level, diverging from our probabilistic approach that allowed us to obtain a global representation in terms of approximations by exponentially entire functions, see Theorem 3.13 below. Such a question holds independent interest for PDEs in its own right.

3.3 The Fourier-Laplace transform by approximation

Our third main result provides an approximation procedure for the characteristic functional . The main idea is to approximate the Riemann sum on the sample paths of the Ornstein-Uhlenbeck process to exploit an underlying Gaussian density in finite dimension.

For this, we need first to get rid of the stochastic integrals and express them in terms of functions of and Lebesgue’s integrals on . This is done by combining Itô’s Lemma and the Romano-Touzi conditioning trick [29] in the next Lemma.

Lemma 3.9.

For negligible to double factorial, , continuously differentiable with , there exists power series with infinite radius of convergence, and functions such that:

| (3.18) |

In addition, are continuous on , , such that are all negligible to double factorial.

Proof.

The proof and the precise expressions of are given in Appendix A. ∎

We now introduce the discretized version of .

Definition 3.10.

For , where is the Dirac mass at a point , we define the function

| (3.19) |

Definition 3.11.

Given an entire function on , we define the extension of to the complex plane by .

Remark 3.12.

Given an entire function on , the power series has infinite radius of convergence, so does , thus is well-defined in , and is entire on .

Theorem 3.13.

Suppose that is negligible to double factorial, , continuously differentiable such that , then as specified in Definition 3.10 is well-defined and entire in . If in addition, the extension of to the complex plane does not vanish for all and , then, is entire in such that

| (3.20) |

and

| (3.21) |

where for all , the family of functions is defined by

| (3.22) | ||||

| (3.23) |

where the family solves a (step-wise) ‘discretized’ system of Riccati ODEs:

Proof.

The proof is given in Section 7. ∎

Remark 3.14.

One of the features of Theorem 3.13 is to obtain that the functions are entire in with no additional assumptions. Unfortunately, inherits this property only when the extension of to the complex plane does not vanish, see Lemma B.3. The requirement of being non-vanishing on the real line is not enough, see Remark B.4. For this reason, we could not obtain a Corollary of Theorem 3.13 without the non-vanishing condition to deal with Laplace transforms as we did in Corollary 3.6.

4 Numerical illustration

4.1 Numerical scheme for high-dimensional Riccati equations

In this section, we show how to solve the infinite dimensional Riccati equations in (3.4)-(3.6) numerically for derivative pricing and hedging. The idea is to solve a truncated version of the ODE by assuming for some integer .

Even the truncated version of the infinite dimensional system of Riccati equations can be extremely difficult to solve. Standard techniques such as the Runge–Kutta methods usually fail to solve the ODE, especially when the parameters and in (2.1) are large. For example, see [13, Figures 2 and 3] for other attempts to a similar problem.

We present a customized algorithm that combines variation of constants and the implicit Euler scheme. For this section alone, all matrix and vector indices will start from 0. With some abuse of notation, we re-write the Riccati ODE (3.6) in the following matrix form:

| (4.1) |

with denoting the vector and the vector of element-wise derivative of . is a vector with it’s element being for . is a diagonal matrix with its diagonal . is an upper triangular matrix with , and zero elsewhere. The term denotes the discrete convolution of the vectors , with its element given by . Finally, is a matrix with where denotes the power series coefficient such that whenever , with collecting the term .

Variation of constants gives:

| (4.2) | ||||

with . By truncating the vector up to some level and assuming , we approximate the solution of in (4.2) by the following quasi-implicit scheme:

where is a diagonal matrix with and . Similarly, and are now matrices as defined above, with and both vectors of dimension .

For the quadratic term , we define

where is a matrix with . We can now solve iteratively by:

where . Detailed implementation of our algorithm can be found in a Python notebook here: https://colab.research.google.com/drive/1VCVyN1qQmLgOWjOy4fbWftyDqEQdm5n5?usp=sharing.

Lemma 4.1.

Assume that , the matrix is invertible.

Proof.

Since , the matrix is a upper triangular matrix, where the real part of the its diagonal is less than zero. Thus is also an upper triangular matrix with non-zero diagonal elements, thus completes the proof. ∎

Matrix contains very large coefficients resulting from the term when is large. This term introduces numerical instability so we capped to some level to ensure the scheme does not blown up.

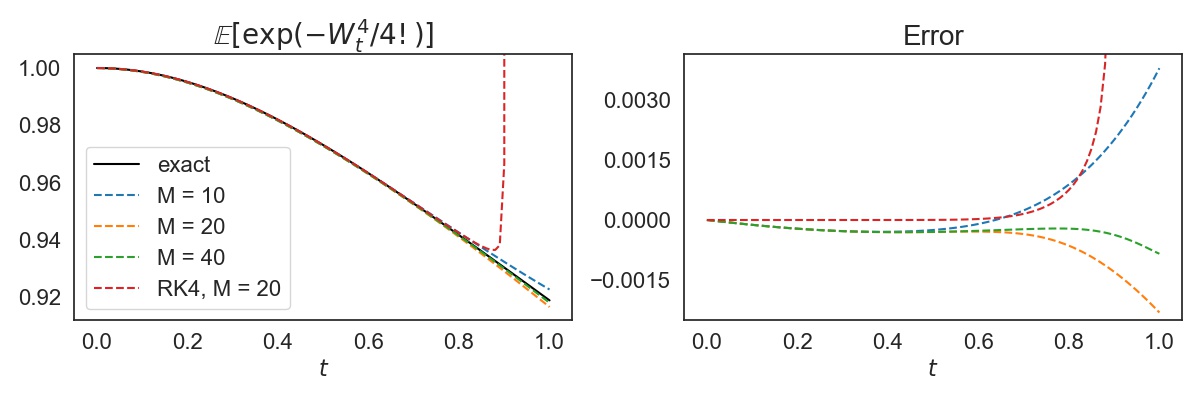

We first test our algorithm on the term considered in [13, Figures 2 and 3], which can be expressed by the solution of a particular case of the Riccati ODE in (3.4)-(3.6) with initial condition , and . The reference value can be computed via a numerical integration quadrature with respect to the Gaussian density, allowing us to evaluate our algorithm’s performance. Figure 1 illustrate numerical convergence in terms of , with step size and fixed. We clearly observe the instability of the Runge-Kutta scheme with increasing truncation , whereas the scheme we propose remains stable with the increase of .

4.2 Pricing SPX derivatives via Fourier

Our numerical scheme gives us direct access to the characteristic function of to price derivatives via Fourier inversion techniques, using the expression (3.8) with and , for . Specifically, we show how one can price European options via Fourier techniques for the Quintic Ornstein-Uhlenbeck Model [7] and the one-factor Bergomi model [9, 15]. This also serves as a numerical validation of the representation (3.8).

There are several Fourier inversion techniques available in the literature to price European-style Vanilla call and put options. Here we adapt the pricing formula suggested in [26] which involves only one integral to evaluate:

| (4.3) |

where denotes the European call option price with strike and maturity , is the log-moneyness and the Fourier-Laplace transform of by fixing and . We use the the representation of in (3.8) and compute the improper integral numerically via the Gauss-Laguerre quadrature, which has been demonstrated to be efficient, see [3, 25].

To speed up the computation of , we add a control variate to reduce the number of evaluation of for different :

| (4.4) |

where is the appropriate call price of the control variate and is the Fourier-Laplace transform of of the control variate.

In this section, we choose the Heston model as the control variate, which admits a closed form characteristic function that is also affine in its state variables, see [24]. The Heston model parameters can be efficiently selected via a standard optimization algorithm such that the difference between and is minimized. Of course, other control variates with explicit characteristic functions such as the Black & Scholes model can also be used.

4.2.1 Quintic Ornstein-Uhlenbeck volatility model

The volatility process under the Quintic OU Model takes the form of:

| (4.5) | ||||

with and . The non-negative coefficients ensure a negative leverage effect as well as the martingality of whenever , see [7] . The particular parametrization with means and from (2.1). This model has shown to produce remarkable joint fits to both SPX and VIX implied volatility surfaces [6, 7].

Since is an OU process which can be simulated exactly, one could be tempted to use Monte Carlo to estimate the SPX derivatives with appropriate control variates. However, the calibrated values of are usually very small and is negative, pushing the model effectively into a fast regime with large mean reversion of order and large vol of vol . It is known the standard Euler-scheme for pricing SPX derivatives can reproduce large estimation bias for longer maturities due to the highly erratic paths of , requiring finer step size or other asymptotic approximation techniques [20, 21]. Pricing via Fourier methods hence presents an attractive alternative given the increased efficiency and accuracy. To demonstrate, we choose the following parameters: , , , , which are typical values one can expect from calibrating the model to SPX and VIX smiles from [7]. Figure 2 shows the convergence of SPX implied volatility of different maturities as the truncation level increases:

4.2.2 One-factor Bergomi model

The one-factor Bergomi model [9, 15] assumes to be log-normal:

| (4.6) | ||||

with and . Similar to quintic OU model before, we have and . We now approximate the exponential as a truncated sum up to level :

| (4.7) |

where in converges to in (4.6) when sending . We now fix for the numerical experiment and set . Figure 3 shows that our numerical scheme quickly converges to Monte-Carlo estimates of the original one-factor Bergomi model:

4.3 Pricing -volatility swaps via Laplace inversion

The -volatility swap rate is defined by:

For the case of a standard volatility swap (i.e. ), one can price the swap rate via the following inverse Laplace transform [31]:

where from (3.1) by setting and using the presentation (3.8). Again, we can accelerate the computation via a control variate, for example the Black & Scholes control variate:

with where is an arbitrary level of volatility that can be fixed upfront.

Compared to the previous section, we are even more confident of our numerical scheme thanks to Corollary 3.6. For demonstration purposes, we use the same model parameters for the Quintic Ornstein-Uhlenbeck and the one-factor Bergomi model as per the previous section, and adopt a parametric forward variance curve in the form of with and .

Figure 4 shows the volatility swaps of the two models computed by inverse Laplace transform with truncation level vs. that computed by Monte-Carlo with 400,000 simulations and 10,000 steps:

4.4 Model calibration to market data via Fourier

The family of polynomial OU volatility models allows fast pricing of VIX futures and VIX options via numerical integration of the payoff with respect to the standard Gaussian density, see [7]. Together with fast Fourier pricing, this opens doors to joint calibration to SPX and VIX smiles. This section also serves the purpose of highlighting the stability of our numerical discretization scheme combined with Fourier inversion in a calibration procedure where a large number of evaluations of the characteristic function are needed for a wide range of realistic model parameters and Fourier variables.

In a nutshell, the calibration of a model involves minimizing the mean square error between prices coming from the model vs. that from market data. Without going too much into the details, we first demonstrate the capability of the quintic OU model (4.5) to jointly calibrate two slices of maturities of SPX smiles together with one slice of maturity of the VIX smile, with calibrated parameters and fixed : with coming directly from market data:

Next, we showcase the calibration results of the one-factor Bergomi model (4.6) on four slices of maturities of SPX smiles between around 1 week to 3 months, with calibrated parameters and fixed :

The market data of SPX and VIX volatility surface is purchased from the CBOE website https://datashop.cboe.com/. For more calibration examples under the quintic OU and the one-factor Bergomi models, please refer to the the Appendix C.

5 Proof of Theorem 3.2

We first introduce a lemma to justify the use of Itô’s formula to the series .

Lemma 5.1.

Under the condition of Theorem 3.2, is in and in , with , , .

Proof.

First, , and . So is well defined. In addition, if we restrict in a bounded set of , then is continuous and converges uniformly to when , so is continuous.

Notice that the domain of convergence for is , then so is . So are well-defined, continuous and have the expression as the statement for the same reason as for .

To treat , we should at first prove that has also an infinite radius of convergence.

Indeed, using the Riccati expression (3.4), we only have to check that we have an infinite radius of convergence for

| (5.1) |

where is among .

By assumption and Cauchy–Hadamard Theorem, we know that and thus we obtain that when , (5.1) has an infinite radius of convergence.

Also, for two power series and both with infinite radius of convergence, their product also has an infinite radius of convergence. And notice that are dominated by . Thus when is among , (5.1) has also an infinite radius of convergence. Therefore has an infinite radius of convergence, so that also has infinite radius of convergence and converges uniformly when is in a bounded subset of and also on . So is well-defined and also continuous.

Next, notice that and given the the uniform convergence of both series and , we deduce that

∎

Proof of Theorem 3.2.

We first notice that since the power series has an infinite radius of convergence, is well-defined for all .

With Lemma 5.1, we can now apply Itô’s formula on the semimartingale :

| (5.2) | ||||

| (5.3) | ||||

Applying the Cauchy product on the power series leads to

| (5.4) | ||||

is a local martingale if and only if it has zero drift (i.e. part is zero a.s.). This is true for all values of by assumption from (3.4), so that is a local martingale. Moreover, if is a true martingale, we have

| (5.5) | ||||

which follows from the martingality of and the assumption of the initial condition of from (3.6). This completes the proof. ∎

6 Proof of Theorem 3.5

To prove Theorem 3.5, we adopt the representation of as mentioned in Lemma 3.9:

where the functions are all negligible to double factorial and are continuous such that . Consider the following function defined by:

| (6.1) | ||||

| (6.2) |

for all and . We recall that is well-defined, since

Our proof is composed of five parts:

-

•

In Subsection 6.1, we start by deriving some properties of power series negligible to double factorial which will be used later.

- •

-

•

In Subsection 6.3, we prove that solves the associated PDE coming from Feynman-Kac formula. In particular, we prove that indeed exists.

-

•

In Subsection 6.4, we introduce a system of ODE and obtain a solution by comparing the derivatives of all orders of both sides of Feynman-Kac formula at .

- •

6.1 Properties of power series negligible to double factorial

We collect some properties of power series that are negligible to double factorial as defined per Definition 2.1.

Given a power series , we define the set as the -algebra generated by all higher-order derivatives of :

| (6.3) |

Notice that if , then by convention the product .

Remark 6.1.

This definition comes from the calculations of the successive partial derivatives For example, in the simple case when , by setting , we have by the Markov property of . Since we can write , where does not depend on , this means formally, , where and appears. Higher order derivatives like will also formally generate the elements in .

Now we prove some properties of power series which are negligible to double factorial. For the lemma below, we recall the convention . Notice that although the proof is a little cumbersome, the essential idea is the observation that behaves like and .

Lemma 6.2.

There exists a constant , such that for all , we have that

Proof.

For , we have . So we need only to prove that for a constant ,

| (6.4) |

Case 1: is an even number. If is an even number, . If is an odd number, . Therefore,

| (6.5) | ||||

| (6.6) |

Case 2: is an odd number, then

| (6.7) |

and since is even, as the Case 1, we have, for a constant :

| (6.8) |

Therefore there exists constant such that for all , . ∎

Lemma 6.3.

The following statements are true.

-

(i)

If is negligible to double factorial, then so is .

-

(ii)

The set of power series which are negligible to double factorial is closed under addition, differentiation, scalar multiplication, and multiplication. Thus if is negligible to double factorial, then for any , is also negligible to double factorial.

-

(iii)

If is negligible to double factorial, then so is , where is a constant.

-

(iv)

If is negligible to double factorial, then so is .

Proof.

-

(i)

Note that . It follows that

(6.9) (6.10) using that .

-

(ii)

Let be negligible to double factorial and note that . Then,

(6.11) then by ,

(6.12) By , , and for any constant .

Next, we will show that is again negligible to double factorial. For any , there exists , such that for all , we have that . Therefore there exists constant such that for all . Thus by Lemma 6.2,

(6.13) (6.14) thus . Since can be any arbitrary positive number, we obtain

Therefore, is also negligible to double factorial.

-

(iii)

Notice that

-

(iv)

It is obvious, since the modulus of has no impact on the .

∎

6.2 Regularity in space

In this subsection, we prove the regularity of in given by (6.2), i.e. is in such that the partial derivatives are bounded in a sense in preparation for the Feynman-Kac formula in Subsection 6.3.

Theorem 6.4.

The function given by (6.2) is in , i.e. the partial derivatives exist and are continuous in , for . Furthermore, for each , there exists a power series negligible to double factorial and a constant independent of , such that

| (6.15) |

Before proving Theorem 6.4, we first simplify the expression of in (6.2) to get rid of the conditioning. Thanks to the Markovianity of , we can write after a change of variable as:

| (6.16) |

with

| (6.17) | ||||

| (6.18) |

Notice when , with and . From now on, we will consider mainly the representation (6.16) for .

The main idea for proving Theorem 6.4 consists in taking successive derivatives in inside the expectation above and applying the dominated convergence theorem. To illustrate this, we first calculate formally . Notice that the derivative in for the terms inside the exponential of is:

| (6.19) | ||||

| (6.20) |

so that one expects

| (6.21) |

Notice that since the terms inside the exponential of have a non-positive real part as a result of Lemma 3.9. Therefore we only need to bound for and small enough . Notice that are continuous and thus bounded on , is also bounded in , are negligible to double factorial by the statement of Lemma 6.3. So we only need to bound the expressions of the following form

| (6.22) |

where is any power series negligible to double factorial.

First of all, we introduce a new definition and a lemma to help bound in a certain sense the quantities in (6.22). We also introduce the notation , which will be useful for applying Doob’s inequality.

Definition 6.5.

We say that a family of processes is estimable if there exists a power series negligible to double factorial such that for all fixed and ,

We will prove that the expressions in (6.22) are estimable in Proposition 6.7 below. For now, let us first prove that is integrable via the following lemma.

Lemma 6.6.

The set of estimable family of processes is closed under addition and multiplication. In addition, for all power series negligible to double factorial, . Therefore, if is estimable, then there exists a power series negligible to double factorial and a constant , such that for all and , .

Proof.

For the first part of this lemma, recall that by the statements and of Lemma 6.3, the property of being negligible to double factorial is closed under addition, multiplication, and taking absolute power series. So the set of estimable family of process is obviously closed under addition. For the multiplication, it suffices to use the basic inequality .

To show that , recall , where is a true martingale. There is a positive constant such that when . We use to denote and to denote its maximal process . By Doob’s maximal inequality for ,

For ,

Notice that is a centred normal distribution and that the constant can be taken large enough so that the variance of is smaller than . It follows that . By modifying a little the coefficients in the power series , which does not influence the conclusion, we obtain that satisfies the requirements and is finite, since is negligible to double factorial.∎

Proposition 6.7.

If is negligible to double factorial, then the expressions in (6.22) are estimable, and

where is negligible to double factorial and only depends on , and is a constant.

Proof.

Fix and . We first bound :

| (6.23) |

by Lemma 2.2. Since and are both bounded in , there exists a constant such that

| (6.24) | ||||

| (6.25) |

Setting , we get . By Lemma 6.3, is also negligible to double factorial, and is still negligible to double factorial. So is estimable. An application of Lemma 6.6 yields the bound for the expectation. Furthermore, the term is clearly bounded by . So we can update to to obtain the claimed bound and end the proof. ∎

We have now that since we can choose that , with coefficient of all positive. The dominating function is integrable. For the term , we can build a dominating function in a similar way.

Going back to (6.21), we now have all the ingredients to apply the dominated convergence theorem when on

where . Recall from (6.20), and that and are bounded, is bounded in , are negligible to double factorial. Therefore, (6.21) holds. Of course, we would like to prove by induction that

holds for all to show that is in , where

| (6.26) |

To achieve this, we need to prove first that are well-defined. Then, similarly to before, we will bound so that we can apply by induction the dominated convergence theorem to

| (6.27) | ||||

| (6.28) | ||||

| (6.29) |

For , we need to compute , recall that is just a sum of the Riemann integral of the continuously differentiable function and a differentiable function with respect to for a fixed outside a null-set. Therefore,

| (6.30) | ||||

| (6.31) |

Thus can be obtained explicitly, and similarly for . This procedure will differentiate many times the function , so it is useful to define:

| (6.32) | ||||

| (6.33) |

Definition 6.8.

We define the set :

| (6.34) |

as the -algebra generated by higher order derivatives of the function . We call generating elements of .

Notice that if , then by convention the product .

Lemma 6.9.

For every , the function in (6.26) is well-defined. In addition, is differentiable in , continuous in and estimable.

Proof.

First, note the following three facts:

-

(i)

is a generating element of ,

-

(ii)

,

-

(iii)

All generating elements of are differentiable in by applying the Leibniz’s rule, and . So if , then exists and .

By induction and noticing that is closed under linear sum and multiplication, are well-defined and in . For fixed outside a null-set, the generating elements are continuous in and differentiable in . This implies that is also continuous in and differentiable in .

We are now ready to prove Theorem 6.4.

Proof of Theorem 6.4.

Take as defined in (6.26) which are estimable by Lemma 6.9. By applying Lemma 6.6,the term is estimable with its expectation bounded by . Using induction, we first notice that for the case , which trivially satisfies the inequality in (6.15). Next, suppose that it is true for up to case , recall the definition of from (6.18) and that , where is defined in (6.20). Thus . Since both and are differentiable in as per 6.9, by the Mean value theorem:

where is . Strictly speaking, since is a complex-valued functions, we need to apply the Mean value on both the real part and imaginary part separately with different . However, this does not change the proof at all, so to simplify the notation and discussion, only is used.

By Lemma 2.2, Lemma 6.9 and the fact that , and is dominated by with bounded expectation by Lemma 6.6 if we choose that , where is negligible to double factorial. Applying dominated convergence theorem, for we have:

| (6.35) |

Therefore, for all , where negligible to double factorial and a constant , we have that (6.15) holds. Finally, for the continuity of , it suffices to notice that before taking the expectation, the random variable is continuous with respect to , Then fixing , again by Proposition 6.7, Lemma 6.9, its expectation is uniformly bounded with , and bounded. So again by the dominated convergence theorem and taking the limit at , the continuity holds.∎

6.3 Feynman-Kac

In this subsection, we derive the Feynman-Kac formula in Theorem 6.11. Since we do not have that exists a priori in our setting, we shall prove its existence and obtain the Feynman-Kac formula at the same time.

First, we introduce a lemma which will be useful later.

Lemma 6.10.

Let such that , then .

Proof.

We write , and . Then .

If , then . If , .

If , then . If , , . ∎

Theorem 6.11.

Proof.

By Theorem 6.4, is in . We will compute the infinitesimal generator

in two ways to obtain the PDE and the existence of at the same time. Here means the conditional expectation with .

First way: fix , we compute the quantity using the classical definition of generator. By Itô’s formula:

| (6.37) |

Note that are evaluated at here. By Theorem 6.4, statement of Lemma 6.3, are all bounded by , where is negligible to double factorial. Combining with Proposition 6.7, is bounded by for , where is negligible to double factorial. Thus is in and is a true martingale for . Similarly, the Riemann integral is estimable with finite expectation. In addition, we have

where the right hand side is still estimable and dominated by a random variable with finite expectation. By dominated convergence theorem,

| (6.38) | ||||

| (6.39) | ||||

| (6.40) |

Second way: compute the generator directly by applying the Markov property of . Define and , we apply Markov property of to the representation of in (6.2), i.e.

| (6.41) |

and by Markov property for ,

| (6.42) |

By the tower property of conditional expectation, we have

| (6.43) | ||||

| (6.44) | ||||

| (6.45) |

Therefore,

| (6.46) | ||||

| (6.47) | ||||

| (6.48) | ||||

| (6.49) | ||||

| (6.50) | ||||

| (6.51) |

Now we want to apply dominated convergence theorem when to the term

To dominate the term inside the expectation, notice that at first , thus . In addition,

| (6.52) | ||||

| (6.53) |

Since , therefore

and thus . Therefore we only need to dominate the term

Since , by Lemma 6.10 we just need to dominate the term

Notice are bounded, are negligible to double factorial so is dominated when conditioned by Proposition 6.7. Thus by the dominated convergence theorem :

| (6.54) | ||||

| (6.55) |

which is finite. Equating with (6.40), the term is thus well-defined. Of course, one can also replace by and perform similar computations as per the above two methods on the quantity

to obtain the existence of and also the PDE in (6.36). A subtle point to note is that for the first method, we do not apply Itô’s formula to for the variable , which requires the existence of the partial derivative a priori. Instead, we obtain the existence of by applying Itô’s formula to in and evaluate at :

| (6.56) | ||||

| (6.57) |

and taking the limit for as above. The continuity of is directly obtained from the continuity of the other terms in this equation, with boundary condition at comes from the continuity of and its definition. ∎

6.4 Infinite dimensional ODE

In this subsection, we obtain a solution of the system of ODE by comparing the derivatives of both sides of the PDE (6.36) when .

Since is continuous by Theorem 6.4, in addition if does not vanish, we can define such that and , see Lemma B.1. Note is also continuous in , and with .

Theorem 6.12.

If does not vanish, then

solves the system of ODE

| (6.58) | ||||

| (6.59) | ||||

| (6.60) | ||||

| (6.61) |

In order to prove the Theorem, we first link the PDE (6.36) to the system of ODE (6.61). Suppose does not vanish and set , then the following PDE holds:

| (6.62) |

To prove this theorem, we will need the following lemma.

Lemma 6.13.

If a function is in , and one of the partial derivatives and exists and is continuous, then they both exist and are equal.

Now we can prove Theorem 6.12.

Proof of Theorem 6.12.

Since does not vanish, we can define as per Definition B.5, i.e.

We can now define such that . By Theorem 6.11, is in and in , then since is continuous, by Lemma B.2, is also in and in . In addition, the PDE below can also be deduced:

The boundary condition comes from the fact , with the continuity of and the fact that .

Now substitute :

| (6.63) | |||

| (6.64) |

Since the right side of (6.63) is in , so is . Notice that by definition . We aim to take the partial derivative with respect to on both sides of (6.63) at to deduce the equation in (6.61). For the left side of (6.61), Lemma 6.13 allows the interchangeability of and the following equality can be proven by induction:

The right side of (6.61) can be deduced by noticing that for all . To obtain that

first notice that implies . The convolution follows naturally by applying the general Leibniz rule.

Lastly, the initial condition of (6.61) can be easily deduced from the fact that

∎

6.5 Putting everything together

Proof of Theorem 3.5.

Since is negligible to double factorial by assumption, and , are continuously differentiable such that , then in (3.1) is well-defined. We recall from Lemma 3.9 that

with are continuous in , , , and are negligible to double factorial. Notice that . Theorem 6.4 yields that is continuous.

If in addition, does not vanish, then so does . By Lemma B.1, we can define such that . By Theorems 6.4 and 6.11, is in and in , and so is . By Lemma B.2, are also in and in . Then, we can take the partial derivative with respect to for around . Then, the system of ODE (6.61) in Theorem 6.12 induces the system of ODE (3.6) by setting with defined in (6.61), with the coefficients of the ODE (3.6) coming from the precise definition of as defined in Appendix A. ∎

7 Proof of Theorem 3.13

Before proving Theorem 3.13, we introduce the following definition of the function :

Definition 7.1.

By the Markov property of , we can remove the conditioning and write equivalently as

| (7.3) | ||||

| (7.4) |

Notice that for , and .

The function is well-defined, since given the condition of and from Lemma 3.9.

The main advantage of considering functionals over is their entire property in shown in Theorem 7.3 below. As we shall see, the results of in Section 6 can be easily extended to to . We now layout the following steps to prove Theorem 3.13:

-

•

In Subsection 7.1, we prove that is entire in , without any additional conditions imposed on or .

- •

- •

Lemma 7.2.

, when , for all and .

Proof.

This follows from a direct application of the bounded convergence theorem: the Riemann sum converges to the Riemann integral, and the exponential has a module at most . ∎

7.1 Entire property

In this subsection, we do not need any additional condition imposed on or about their zeros.

Theorem 7.3.

For fixed , is entire in .

We first introduce a lemma that will be useful in proving Theorem 7.3. The idea of the proof is standard and comes from exploiting the fact that the Gaussian density is entire. A similar argument has been used for single marginals in [13, Lemma 6.1].

Lemma 7.4.

Suppose that is a centered Gaussian Process with independent increments such that has non-zero variance when . Let . Take a bounded measurable function from to , then is entire in .

Proof.

Denote the variance of as , we have

| (7.5) | ||||

| (7.6) |

Denote , we have

| (7.7) | ||||

| (7.8) | ||||

| (7.9) | ||||

| (7.10) |

where we applied Fubini in the last step since

This implies an infinite radius of convergence for

i.e. is equal to a power series with an infinite radius of convergence, so it is entire in .

∎

7.2 Discretized versions of the theorems in Section 6

In this subsection, we prove discretized versions of the results in Section 6, in the case when (or equivalently ) does not vanish on .

Remark 7.5.

Recalling Corollary 3.6, the conditions that and -valued with guarantee that and do not vanish on .

Theorem 7.6.

Proof.

Notice that all the lemmas and proofs used in Section 6 dealing with being in and the bound of can be easily adopted to by replacing the integral with a finite sum. ∎

Theorem 7.7.

(Discretized version of Theorem 6.11) For , the function

-

(i)

is continuous in the region . In addition, is in and in in the region , ,

-

(ii)

solves the following PDE

(7.13) (7.14) (7.15) with .

Proof.

The proof follows along the same lines as the proof of Theorem 6.11. By Theorem 7.6 and Lemma 6.3, and are bounded by , where is negligible to double factorial. Therefore by Proposition 6.7, the stochastic integral and is a true martingale. The Riemann integral is still dominated, allowing the interchange between limit and the expectation and thus computing the the infinitesimal generator as per the first way in Theorem 6.11.

The second way of computing the generator in Theorem 6.11 can also be adopted to compute thanks to the Markov property of . Indeed, define

we have

| (7.16) | ||||

| (7.17) | ||||

| (7.18) | ||||

| (7.19) | ||||

| (7.20) | ||||

| (7.21) |

Notice that, if , where is a finite set, then there exists such that for all , thus for ,

So similar the proof of Theorem 6.11, exists and . The boundary condition when can be deduced by applying the definition of .

∎

Remark 7.8.

Theorem 7.7 shows that for fixed , is left continuous for and is discontinuous at .

We now define in the following Lemma 7.9.

Lemma 7.9.

If does not vanish for , then there exists such that , and in the regions , is continuous in , and

| (7.22) | ||||

| (7.23) |

Proof.

We want to use Lemma B.1 to define from . However, Theorem 7.7 shows that is discontinuous when , with

we need to first define

where is continuous on and And since is non zero, so is . We can now apply Lemma B.1 to yield the existence of continuous on , such that , and to specify , we choose that . We can now define:

| (7.24) |

Since is continuous in the regions , for ,the definition of in (7.24) yields that

-

1.

-

2.

In the regions , , is continuous in

-

3.

Furhtermore, since , . Noticing that is continuous in , and , we deduce that . ∎

We now introduce the discretized version of Theorem 6.12.

Theorem 7.10.

Suppose that does not vanish on , then

solves the following system of ODE:

| (7.25) | ||||

| (7.26) | ||||

| (7.27) | ||||

| (7.28) |

Proof.

By Theorem 7.7, in the regions , for , is in and in . Since , thus by Lemma B.2, in 7.9 is in and in in these regions. Set , then satisfies the following PDE:

| (7.29) | |||

| (7.30) | |||

| (7.31) |

Next, we apply Lemma 6.13 as in the proof of Theorem 6.12, and then comparing the derivatives of both sides in yields the system of ODE. Lastly, the initial condition of (7.28) can be easily deduced from the fact that . ∎

7.3 Putting everything together

In this subsection, we will use the condition that the extension of in the the complex plane , defined in 3.11 does not vanish for as opposed to . This condition is both necessary and sufficient to guarantee that is entire in , see Lemma B.3 and Remark B.4.

Lemma 7.11.

If does not vanish on , then , where are defined as in Theorem 7.10.

Proof.

By Lemma B.3, is entire on , and notice that ∎

Appendix A Proof of Lemma 3.9

Lemma A.1.

Let be a power series with an infinite radius of convergence. Define the power series by

which again have an infinite radius of convergence. Then, for any continuously differentiable function , it holds that

Proof.

This follows from a straightforward application of Itô’s Lemma on the process between and . Recall the dynamics of in (2.1). ∎

Proof of Lemma 3.9.

Using , we have:

| (A.1) | ||||

| (A.2) |

Conditioning on ,the integral is Gaussian with conditional variance . Therefore,

| (A.3) | ||||

| (A.4) |

so that

| (A.5) | ||||

| (A.6) | ||||

| (A.7) |

By applying Lemma A.1 and choosing , we can rewrite the following:

Next, define . Since is negligible to double factorial, are continuously differentiable, and , we deduce that are continuous in , , , are negligible to double factorial by Lemma 6.3, and

∎

Appendix B A small remark on the complex logarithm

For complex-valued functions, such as in (3.1), the definition of is not trivial, especially if the range of is not simply connected. We use the lifting property in Algebraic Topology.

Lemma B.1.

If is a continuous function where is an interval of . Then, there exists a continuous function such that . And if the value of at one point is specified, then is entirely specified, i.e. there exists only one that satisfies these conditions in this case.

Proof.

Notice that is a covering projection from to , i.e. a local homeomorphism. And is path-connected, locally path-connected, and with a trivial fundamental group. Then by Proposition 1.33 of [23], the lifting criterion, as a continuous function from to , can be lifted to a continuous function from to , i.e. . And by Proposition of [23, 1.34], the unique lifting property, and the fact that is connected, if the value of at one point is given, then is specified. ∎

Lemma B.2.

Let be a continuous function, where is an interval of . Assume that is in the first variable and in the second variable . Then, the function as defined in Lemma B.1 is also in and in .

Proof.

Suppose that we define as in the Lemma B.1. We need only to prove that for all fixed point , is in , in in neighborhood of . Since , there exists a , for all such that , we have that . Therefore, for all such that , is contained in an open ball , with center and radius . Particularly, is simply connected and does not contain .

We define from to as , where is the line segment between and . We aim to prove that for all such that .

By the definition of , , thus , so is a constant on . What is more, . So , and thus for all such that . Thus . Notice again that , and by continuity, we have that for all such that . Notice that , so is holomorphic on . Therefore is on when regarding as a subset of . Then since is a composition of and , is also in , in . ∎

Lemma B.3.

Let be an entire function on and a continuous function such that . Then, is entire on if and only if the extension of to the complex plane, as defined in Definition 3.11, does not vanish on .

Proof.

Assume that does not vanish. Then, for , we can define , where is the line segment between and . It follows that , showing that is holomorphic on . What is more, consider the function , we know that , , thus , for all . Thus for all . Thus there exists a , such that . And notice that , we have that for . Particularly, is holomorphic on , so it is entire on and thus on , then so is .

Assume is entire on . Then, it can be written in the form , which is a power series with infinite radius of convergence. Then is entire on , and so is . Notice that and are both entire on , and for all . Since the zeros of an entire function are isolated, except for the zero function, we have that , and hence for all .

∎

Remark B.4.

We point out that for a real entire function that does not vanish on , there exists a continuous function such that , (choosing in Lemma B.1). However is not necessarily entire on . For instance the function , is entire on and does not vanish on . However, is no longer entire on . In fact, the Taylor series at for both and have a finite convergence radius of 1 (can easily be checked) and not .

Definition B.5.

If the joint characteristic functional is continuous on and , for all , we define by Lemma B.1, as the function such that and .

Remark B.6.

Notice that by the definition of in 3.1, , so the condition is satisfied.

Appendix C Another example of model calibration via Fourier

References

- Abi Jaber [2019] Eduardo Abi Jaber. Lifting the heston model. Quantitative finance, 19(12):1995–2013, 2019.

- Abi Jaber [2022] Eduardo Abi Jaber. The characteristic function of gaussian stochastic volatility models: an analytic expression. Finance and Stochastics, 26(4):733–769, 2022.

- Abi Jaber and Gérard [2024] Eduardo Abi Jaber and Louis-Amand Gérard. Signature volatility models: pricing and hedging with fourier. Available at SSRN 4714535, 2024.

- Abi Jaber and Li [2024] Eduardo Abi Jaber and Shaun Xiaoyuan Li. Volatility models in practice: Rough, path-dependent or markovian? Available at SSRN 4684016, 2024.

- Abi Jaber et al. [2019] Eduardo Abi Jaber, Martin Larsson, and Sergio Pulido. Affine volterra processes. The Annals of Applied Probability, 29(5):3155–3200, 2019.

- Abi Jaber et al. [2022] Eduardo Abi Jaber, Camille Illand, and Shaun Xiaoyuan Li. Joint SPX–VIX calibration with gaussian polynomial volatility models: deep pricing with quantization hints. Available at SSRN 4292544, 2022.

- Abi Jaber et al. [2023] Eduardo Abi Jaber, Camille Illand, and Shaun Xiaoyuan Li. The quintic ornstein-uhlenbeck volatility model that jointly calibrates SPX & VIX smiles. Risk Magazine, Cutting Edge Section, 2023.

- Andersen and Andreasen [2000] Leif Andersen and Jesper Andreasen. Jump-diffusion processes: Volatility smile fitting and numerical methods for option pricing. Review of derivatives research, 4:231–262, 2000.

- Bergomi [2005] L Bergomi. Smile dynamics II. Risk Magazine, 2005.

- Carr and Madan [1999] Peter Carr and Dilip Madan. Option valuation using the fast fourier transform. Journal of computational finance, 2(4):61–73, 1999.

- Cuchiero and Teichmann [2020] Christa Cuchiero and Josef Teichmann. Generalized feller processes and markovian lifts of stochastic volterra processes: the affine case. Journal of evolution equations, 20(4):1301–1348, 2020.

- Cuchiero et al. [2023a] Christa Cuchiero, Guido Gazzani, Janka Möller, and Sara Svaluto-Ferro. Joint calibration to spx and vix options with signature-based models. arXiv preprint arXiv:2301.13235, 2023a.

- Cuchiero et al. [2023b] Christa Cuchiero, Sara Svaluto-Ferro, and Josef Teichmann. Signature sdes from an affine and polynomial perspective. arXiv preprint arXiv:2302.01362, 2023b.

- Duffie et al. [2003] Darrell Duffie, Damir Filipović, and Walter Schachermayer. Affine processes and applications in finance. The Annals of Applied Probability, 13(3):984–1053, 2003.

- Dupire [1992] Bruno Dupire. Arbitrage pricing with stochastic volatility. Société Générale, 1992.

- Eberlein et al. [2010] Ernst Eberlein, Kathrin Glau, and Antonis Papapantoleon. Analysis of fourier transform valuation formulas and applications. Applied Mathematical Finance, 17(3):211–240, 2010.

- Eidelman [1969] S. D. Eidelman. Parabolic Systems. North-Holland Publishing Co., Amsterdam, 1969. Translated from the Russian by Scripta Technica, London.

- El Euch and Rosenbaum [2019] Omar El Euch and Mathieu Rosenbaum. The characteristic function of rough heston models. Mathematical Finance, 29(1):3–38, 2019.

- Fang and Oosterlee [2009] Fang Fang and Cornelis W Oosterlee. A novel pricing method for european options based on fourier-cosine series expansions. SIAM Journal on Scientific Computing, 31(2):826–848, 2009.

- Fouque et al. [2003] Jean-Pierre Fouque, George Papanicolaou, Ronnie Sircar, and Knut Solna. Multiscale stochastic volatility asymptotics. Multiscale Modeling & Simulation, 2(1):22–42, 2003.

- Fouque et al. [2016] Jean-Pierre Fouque, Matthew Lorig, and Ronnie Sircar. Second order multiscale stochastic volatility asymptotics: stochastic terminal layer analysis and calibration. Finance and Stochastics, 20(3):543–588, 2016.

- Gatheral and Keller-Ressel [2019] Jim Gatheral and Martin Keller-Ressel. Affine forward variance models. Finance and Stochastics, 23:501–533, 2019.

- Hatcher [2002] Allen Hatcher. Algebraic Topology. Cambridge University Press, 2002.

- Heston [1993] Steven L Heston. A closed-form solution for options with stochastic volatility with applications to bond and currency options. The review of financial studies, 6(2):327–343, 1993.

- Hurd and Zhou [2010] Thomas R Hurd and Zhuowei Zhou. A fourier transform method for spread option pricing. SIAM Journal on Financial Mathematics, 1(1):142–157, 2010.

- Lewis [2001] Alan L Lewis. A simple option formula for general jump-diffusion and other exponential lévy processes. Available at SSRN 282110, 2001.

- Lipton [2001] Alexander Lipton. Mathematical methods for foreign exchange: A financial engineer’s approach. World Scientific, 2001.

- Lord and Kahl [2006] Roger Lord and Christian Kahl. Why the rotation count algorithm works. Tinbergen Institute Discussion Paper, 2006.

- Romano and Touzi [1997] Marc Romano and Nizar Touzi. Contingent claims and market completeness in a stochastic volatility model. Mathematical Finance, 7(4):399–412, 1997.

- Schöbel and Zhu [1999] Rainer Schöbel and Jianwei Zhu. Stochastic volatility with an ornstein–uhlenbeck process: an extension. Review of Finance, 3(1):23–46, 1999.

- Schürger [2002] Klaus Schürger. Laplace transforms and suprema of stochastic processes. Advances in finance and stochastics: essays in honour of Dieter Sondermann, pages 285–294, 2002.

- Stein and Stein [1991] Elias M Stein and Jeremy C Stein. Stock price distributions with stochastic volatility: an analytic approach. The review of financial studies, 4(4):727–752, 1991.